Abstract

Using two studies of the same leading Israeli crowdfunding platform—‘Headstart’—various aspects of the fundraising method discussed in this article were explored. The first study identifies the factors that impact the amount of investment in crowdfunding projects. Using data from 517 backers who invested in ‘Headstart’ projects, direct correlations were established between the age of the backers, the minimum tangible reward levels, being friends or family of the entrepreneurs and the level of risk aversion with the investment amount. It is argued that these results are related to more extensive information being available to family and friends. Furthermore, the findings implicate that for different amounts of investment, different factors will have an impact. The second study seeks to identify the crowdfunding entrepreneurs’ unique characteristics that make some of them succeed in funding their projects more than others. According to the responses of 162 crowdfunding entrepreneurs to the ‘Big Five’ questionnaire, their agreeableness and extraversion have a positive impact on the success of campaign funding, but the impact is gender related. Neuroticism and conscientiousness are also factors. These studies contribute to the literature by using rare, first-hand information from entrepreneurs and backers to identify the internal and external factors that lead to success in crowdfunding.

Crowdfunding is a fundraising method based on the cooperation and trust between entrepreneurs and the crowd. The use of the term ‘crowdfunding’ was first recorded in 2006 1 and was preceded by ‘crowd-sourcing’, 2 which is a broader term for achieving the goal of an individual (or an organisation) by means of donations (not necessarily monetary) from many different sources. Of the several existing models of crowdfunding, the subject of this study is a reward-based platform, a form of crowdfunding in which the investment is made in exchange for non-monetary rewards of various kinds. In contrast to donation crowdfunding platforms, the purpose of this model is not philanthropic, but usually the promotion of a business, start-up or commercial enterprise.

Along with the rapid growth of the crowdfunding market, a new research area has developed within the academic literature (Le Pendeven et al., 2022). The literature on crowdfunding is vast, with many studies exploring the various categories of this fundraising method. Although many angles of crowdfunding have already been studied, mainly by analysing data from different crowdfunding platforms and drawing inferences from them, these studies not only contribute to the existing literature by expanding the known attributes of crowdfunding entrepreneurs and the crowd’s motivation for investment, but also fill a gap in crowdfunding research by providing a crucial approach to utilising real data from crowdfunding backers and entrepreneurs (Shneor & Vik, 2020). This work also takes a more holistic view of the phenomenon, by bringing both sides of crowdfunding.

First, the relevant literature is reviewed, for both the entrepreneurs’ and backers’ studies, followed by a description of the dataset, sample and method specification. Then, the results for each of the two studies are presented. Finally, contributions, practical implications, limitations and directions for future research are discussed.

Literature Review

The main subjects relevant to this work will be briefly reviewed from two points of view, the crowd (the investors/backers) and the entrepreneurs, as they represent the two sides of crowdfunding.

The Crowd

Several papers that deal with investors’ motives for participating in crowdfunding platforms claim that they are not only financial but also involve considerations such as pro-social motivations and expectations about recognition and validating a business idea (Bretschneider & Leimeister, 2017; Junge et al., 2022; Yuan & Wang, 2020). Lin et al. (2014) identified four distinct types of crowdfunders: active backers, trend followers, altruistic funders and the crowd. In contrast, Attuel-Mendes et al. (2021) argued that an investor’s motivation depends on the type of crowdfunding.

Studies have also explored the factors related to the success of crowdfunding projects. They indicate that social ties, especially through social networking, have a positive correlation to funding not only through traditional financing methods but also through crowdfunding platforms (Greenberg et al., 2013; Sauermann et al., 2019). A few studies have discussed gender-related effects, gender-based biases and gender homophily and their effect on crowdfunding outcomes (Greenberg & Mollick, 2017; Letwin et al., 2023). Other studies have suggested that geographic proximity also plays a role in the decision-making process of backers (Agrawal et al., 2015; Giudici et al., 2018).

Crowdfunding is considered an area in which information asymmetry between the parties is not only a given but is even more pronounced than in other methods of funding (Sannajust et al., 2014). Unlike the more traditional funding methods in which investors perform due diligence and rely on personal contacts and face-to-face encounters with entrepreneurs, such options are not possible in crowdfunding. The entrepreneurs reveal the information they deem necessary and, in return, ask for the investors’ trust (Agrawal et al., 2014). Perhaps the most well-known solution to the problem of asymmetric information is the theory of signals developed by Spence (1974).

Several studies have found evidence of the use of these signals to indicate the quality of the project to the crowd and its correlation to success in raising money through crowdfunding (Block et al., 2018; Kaminski & Hopp, 2020; Mollick, 2014; Shneor & Vik, 2020). According to Mollick (2014), crowdfunding investors decide whether to invest in projects in a manner similar to the decisions of venture capital funds and angels. They assess the quality of the project, the team of entrepreneurs and the chances of the project’s success based on various signals. For example, the following signals are considered positive signals and are correlated with campaign success: the use of linguistic styles that trigger excitement; attaching extra information such as a short video to a presentation about the project; frequent updates from the entrepreneurs during the funding; and mentioning of certificates, government grants and patents (this is just a partial list).

Until recently, the literature has generally paid little attention to the subject of the rewards offered by entrepreneurs on reward-based crowdfunding platforms. Given that the information about the rewards is actually presented on the same page as all of the other information about the project, 3 it can be assumed that investors consider it a factor in their decision-making process. A few studies have categorised the different types of rewards and related them to different aspects of the crowdfunding projects (Lin et al., 2016; Thurridl & Kamleitner, 2016). The incentive for backers/investors encompassed in offering rewards in crowdfunding was also further explained by the joint effects of different values (utilitarian, socioemotional and participatory) (Jiang et al., 2021; Kedas & Sarkar, 2023). Some studies determined that rewards are an important material incentive for investors, implying that it is better for entrepreneurs to offer tangible rewards (a copy of the book, album, display, etc.) rather than intangible rewards (such as thank-you e-mails) (Read, 2013; Verschoore & Araujo, 2020). This recommendation was also supported by later studies (James et al., 2021; van Teunenbroek et al., 2023).

The main objective of Study 1 was to identify the factors that impact the investment amounts that the backers (the crowd) are willing to pay in reward-based crowdfunding. The second aim was to examine the issue of rewards and the crowd’s assumed preferences for tangible rewards as well as to investigate other characteristics of this funding method from the crowd perspective.

The Entrepreneurs

There are numerous studies about entrepreneurs’ personalities and specifically their connection with their success. In contrast, the literature addressing the same subject regarding crowdfunding entrepreneurs is lacking (Neuhaus et al., 2022). In Study 2, the impact of reward-based crowdfunding entrepreneurs’ personalities on their funding success is explored.

In this study, the ‘Big Five Personality Traits’ (McCrae & Costa, 1987) questionnaire, which has been used in many studies to identify human characteristics, is utilized. The five traits include: (a) extraversion, characterised by being talkative, assertive and energetic; (b) agreeableness, characterised as good-natured, trusting and cooperative; (c) conscientiousness, characterised as being responsible, orderly and dependable; (d) neuroticism, characterised as being easily upset and emotionally unstable and (e) openness, characterised as being intellectual, polished and independent minded (Barlett & Anderson, 2012; John & Srivastava, 1999).

The use of the Big Five questionnaire has been common since the mid-1980s and is considered an adequate and credible indicator for the measurement of the traits (Barrick & Mount, 1991; Hurtz & Donovan, 2000). The measurement of the Big Five traits was generally found to be robust across major regions of the world (Schmitt et al., 2007). McCrae and John’s (1992) version was translated into Hebrew and was used as the measurement tool in Study 2.

Many studies indicate that the Big Five are good predictors of performance and success. Examples include career success (Judge et al., 1999), academic success (Trapmann et al., 2007) and job performance (Barrick & Mount, 1991).

When applying the Big Five to entrepreneurship, studies indicate a connection between various dimensions of entrepreneurship success and performance and the Big Five. Nevertheless, inconsistent findings in the 1980s led some researchers to conclude that there is no relationship between entrepreneurs’ personalities and entrepreneurship (Gartner, 1988; Robinson et al., 1991). However, other studies have established such a relationship. A few examples include Ciavarella et al. (2004), who reported that entrepreneurs’ conscientiousness is positively related to the long-term survival of a new venture; Zhao and Seibert (2006), who claimed that entrepreneurs differ from managers in four of the five personality dimensions; and Zhao et al. (2010), who established an association between extraversion, conscientiousness, openness and neuroticism and both entrepreneurial intentions and entrepreneurial performance. In general, there is evidence that personality traits predict business (entrepreneurial) intentions and the creation and success of entrepreneurial ventures (Brandstatter, 2011).

As mentioned earlier, a few attempts have been made to connect personality traits with success in crowdfunding. Thies et al. (2016) used the Big Five questionnaire to examine how the signalling of a certain trait in a campaign’s video and description increases the likelihood of the campaign being shared on social media and becoming successful. Helmig and Rottler (2019) took a videometric approach and used the pitch video and observer raters to measure personality. Leonelli et al. (2020) found relationships between the crowdfunding entrepreneurs’ success and some of their dark traits (narcissism, psychopathy and Machiavellianism), as reflected in their campaigns. Gera and Kaur (2018) found a weak correlation between personality dimensions and success but concluded that the overall predictive value of traits is significant.

The main objective of Study 2 was to build on these attempts and try to expand the existing knowledge regarding the role of an entrepreneur’s personality in crowdfunding and thus to fill the literature gap in this field (Neuhaus et al., 2022).

The literature exploring gender differences in crowdfunding shows that the quality signalling of entrepreneurs to investors in crowdfunding might be gender related (Kleinert & Mochkabadi, 2021). Women’s choices of linguistic content in crowdfunding campaigns are different from men’s (Gorbatai & Nelson, 2015). Some nuances in the pitch of women were detected and were related to success in funding (McSweeney et al., 2022). It was also suggested that women should highlight their gender, talk about women’s perspective and avoid promotional language in order to succeed in crowdfunding (Wesemann & Wincent, 2021).

Study 2 addresses the impact of an entrepreneur’s gender on the success of campaigns.

In both Study 1 and Study 2, the case study of Headstart, 4 a pioneer of crowdfunding in Israel and one of the most prominent crowdfunding platforms in the country, was used. Headstart is a reward-based, AON (All or Nothing) platform. Crowdfunding in Israel has grown as part of and into a strong Israeli entrepreneurship ecosystem, which has consistently ranked at the top of several entrepreneurship indices of developed countries for the past three decades (Menipaz & Avrahami, 2019). Some previous Israeli studies explored aspects of the crowd’s and entrepreneurs’ characteristics using the Headstart platform (Efrat et al., 2020, 2021, 2023), although using different approaches and methods.

Study 1

Data and Method

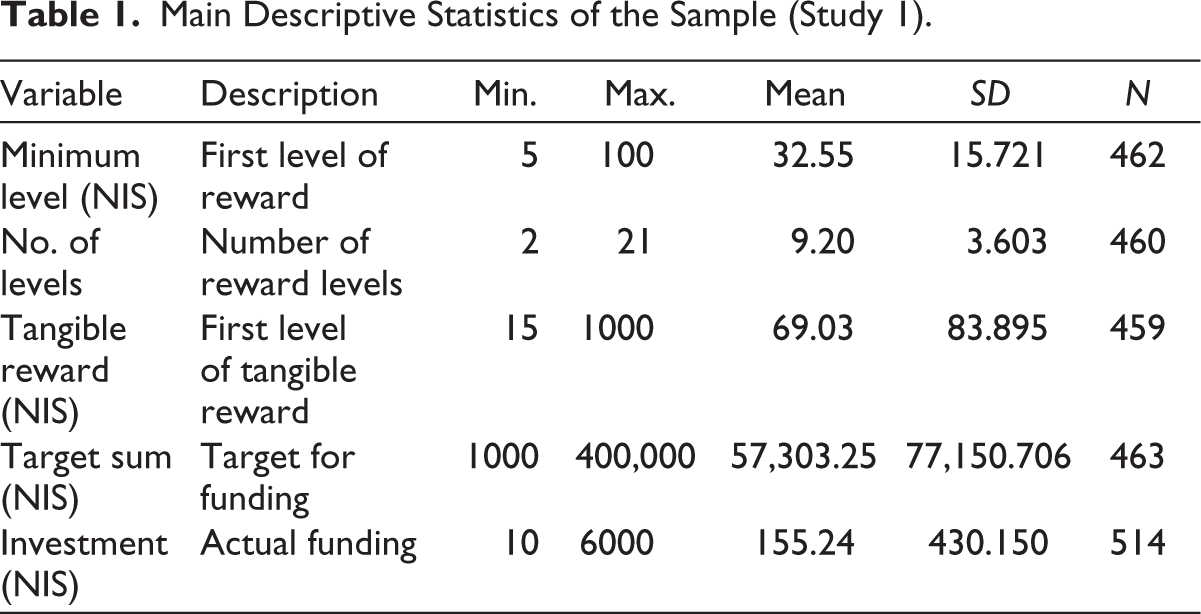

The sample population consisted of backers of Headstart projects, whose founders agreed to send an online questionnaire (using Google Forms) to an estimated number of 40,000 e-mails of backers listed on its database. 5 The backers were offered an incentive for participating: entry into a contest to win a mini iPad. A total of 520 respondents filled out the questionnaire. Three individuals who had not yet backed a project were omitted, resulting in a total of 517 participants. 6

In addition to the data collected from the questionnaires, for each project, information was gathered from the Headstart platform about the target sum, final number of backers, number of reward levels, the reward at each level and the number of backers at each level. The data were later combined and cross-referenced with the information from the questionnaires. 7

Results

Descriptive Statistics

Demographic characteristics: With regard to the demographics of the study, 56 per cent of the participants were men and 44 per cent were women. The average age of the participants was 38 years. With regard to income, 33 per cent of the participants reported an above-average income and 29 per cent had an average income. More than half of the participants

Main Descriptive Statistics of the Sample (Study 1).

Relationship to the entrepreneur: Approximately 21 per cent of the participants defined themselves as friends, family or close acquaintances of the entrepreneur.

Investors’ portfolio 8 : On a scale of 0 to 5, the participants invested on average 0.82 (out of 5 parts) of their investment portfolio in stocks (SD = 1.25).

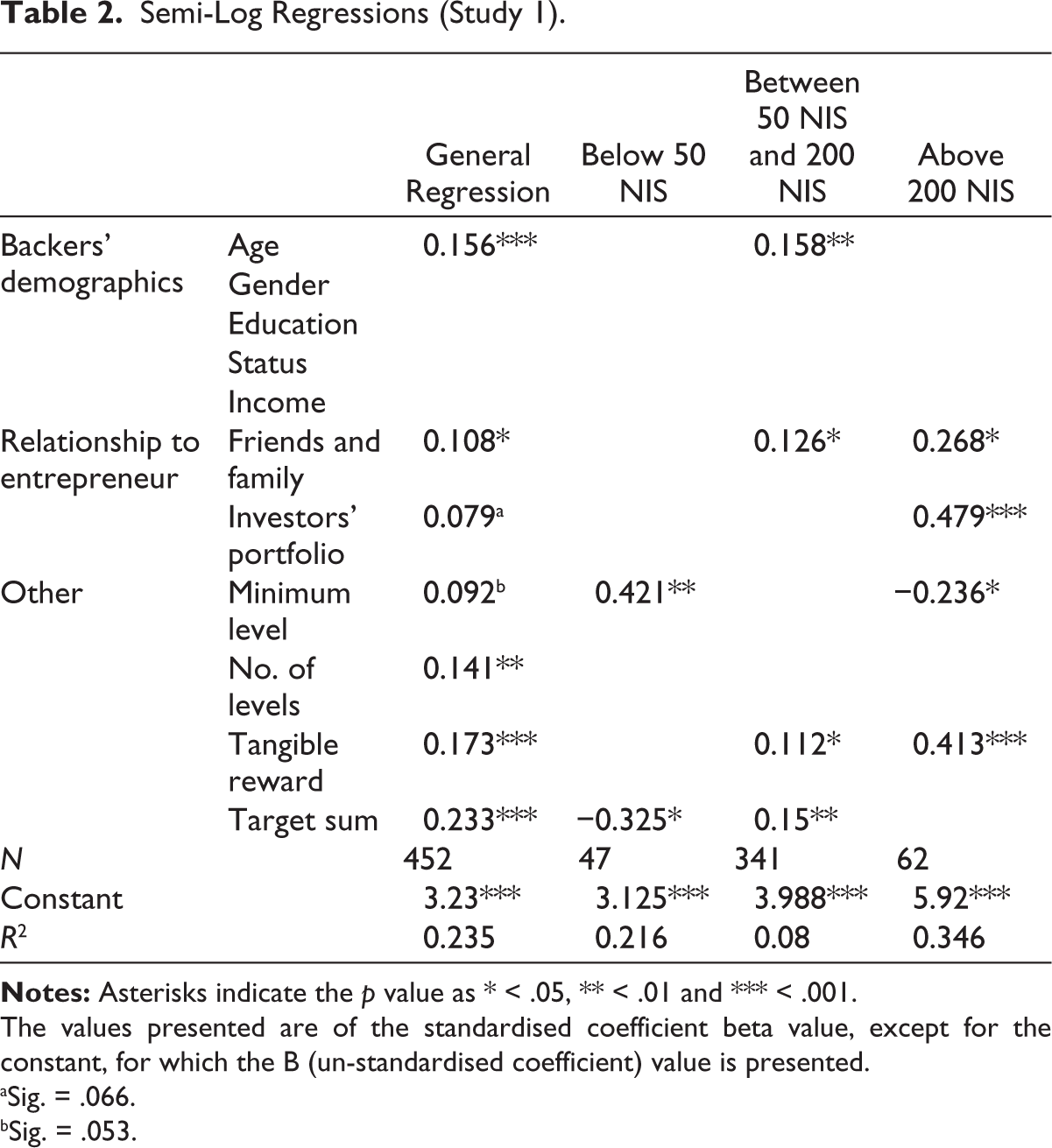

Semi-log Regressions

In order to analyse whether and to what extent the size of the investment (investment sum) could be explained by the independent variables, the variables were tested in a multivariate semi-log model with the investment sum as the dependent variable. Table 2 presents the results of these semi-log regressions.

The model was significant (N = 452, F = 19.531, p < .001). As expected, the findings in this model implied that friends and family, investment portfolio, tangible rewards, number of levels, target sum, age and minimum level are significant factors that impact the amount of money that the backers invest. All of the variables had a direct positive correlation with the investment sum, except target sum and minimum level, which were negatively correlated with the investment sum at specific ranges of investment.

Next, three different regression models were employed for each of the following ranges of investment amounts: below 50 NIS (lowest range), between 50 NIS and 200 NIS (medium range) and above 200 NIS (highest range). 9 The goal was to determine whether, in various ranges of investment amounts, different factors affect the dependent variable. All three regression models were significant (p < .001).

As the results presented in Table 2 imply, different factors affect the investment sum in the different ranges of the investment. For example, in the lowest range, the investment sum was most affected by the minimum level and target sum, so that the higher the minimum level for investing in the project, the larger the investment sum, whereas, in accordance with previous studies (Frydrych et al., 2014; Mollick & Kuppuswamy, 2014), a larger investment sum was correlated with a lower target sum. In the medium range of investment, age, friends and family, tangible rewards and target sums were significant factors that impact the investment amounts of the backers. All of these variables had a direct positive correlation with the investment sum. In other words, older backers invested more money, friends and family invested more than non-family and friends and the higher the minimum level of a tangible reward, the larger the investment. Contrary to expectations, the higher the target sum, the more money the backer will invest in this range. As for the highest range of investment, the individual’s portfolio, the minimum level, tangible rewards and family and friends are significant factors that impact the investment of the backers. These variables had a direct positive correlation with the investment sum. The results might suggest that the lower risk aversion of the participants (evident in their stock investments) might be related to higher investment amounts. Family and friends invest more than non-family and friends. Finally, the higher the level of tangible rewards, the more the money invested. The variable minimum level was negatively correlated with the investment sum, meaning that the lower the level, the more money the backer invests. This result is not only contrary to expectations but is also not relevant to this range of investment, because clearly none of the backers in this range chose the first level of investment.

Semi-Log Regressions (Study 1).

The values presented are of the standardised coefficient beta value, except for the constant, for which the B (un-standardised coefficient) value is presented.

aSig. = .066.

bSig. = .053.

Family and friends emerged as a significant and positive factor in all of the regression models except in under 50 NIS. As intuitively expected, and in accordance with previous literature (Chen, 2022), findings implicate that the familiarity between the investor and the entrepreneur reduces the information asymmetry that family and friends face compared to the other investors.

Study 2

Data and Method

The sample consisted of entrepreneurs of projects on the Headstart platform. A total of 162 entrepreneur respondents 10 filled out the questionnaire sent by an e-mail. 11

In addition to the data collected from the questionnaire, relevant information was gathered from the Headstart platform about each entrepreneur’s project: 12 number of backers, funding sum and target sum of funding. As in Study 1, the collected data was later combined and cross-referenced with information from the questionnaire.

The questionnaire consisted mostly of the 44 items on the Hebrew version (Etzion & Laski, 1998) of the Big Five Inventory questionnaire (Big Five Inventory versions 5a and 5b; John et al., 1991). The respondents provided their responses on a 7-point scale ranging from 1 (strongly disagree) to 7 (strongly agree). Scale reliabilities were adequate. The rest of the questions referred to demographics (gender, income, education, age and marital status). The respondents also revealed the name of the Headstart project they initiated.

Results

Descriptive Statistics

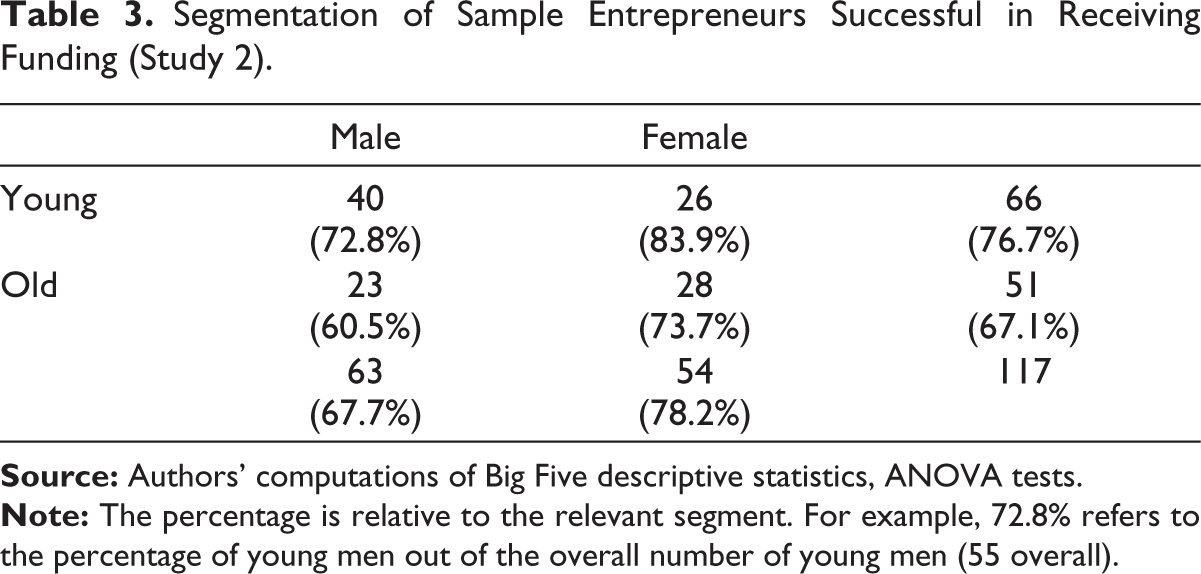

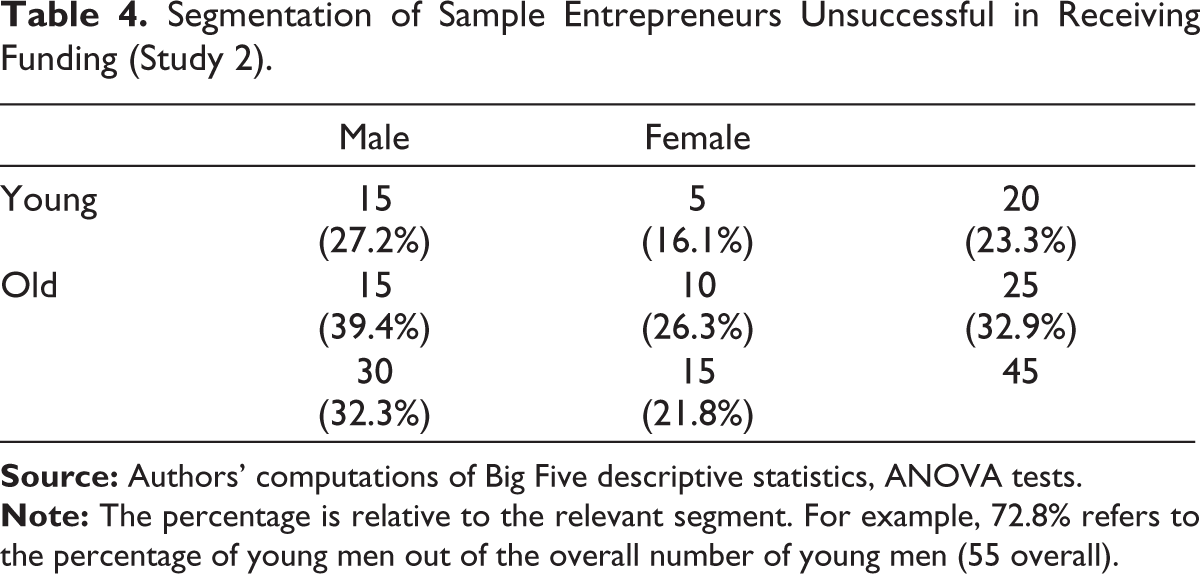

Forty-five of the 162 (27.8 per cent) respondents in the sample failed to receive funding for their Headstart crowdfunding campaign. The remaining 117 respondents succeeded in receiving funding. The average funding sum was 43,822.56 NIS (SD = 50,223.65). The average target sum was 38,943.97 NIS (SD = 45,270.33). The projects differed in the number of entrepreneurs. A majority (54.9 per cent) had only one entrepreneur, whereas 16 per cent had two entrepreneurs. The rest of the projects varied from three to eight entrepreneurs, but a few projects had even more entrepreneurs. 13

Demographic Characteristics

57.4 per cent of the respondents were men, and 42.6 per cent were women. The average age of the respondents was 37.91 years. 14 Their average monthly income was 11,356.55 NIS. 15 More than half of the participants (53.7 per cent) were married, and 38.3 per cent were single. The group was well-educated, with 64.2 per cent of the respondents having at least an undergraduate degree.

Tables 3 and 4 list the successful and unsuccessful entrepreneurs in the sample by age and gender. The definitions of ‘Old’ and ‘Young’ entrepreneurs are relative to the average ages of the sample (38 years) as presented in Figure 1.

Segmentation of Sample Entrepreneurs Successful in Receiving Funding (Study 2).

Segmentation of Sample Entrepreneurs Unsuccessful in Receiving Funding (Study 2).

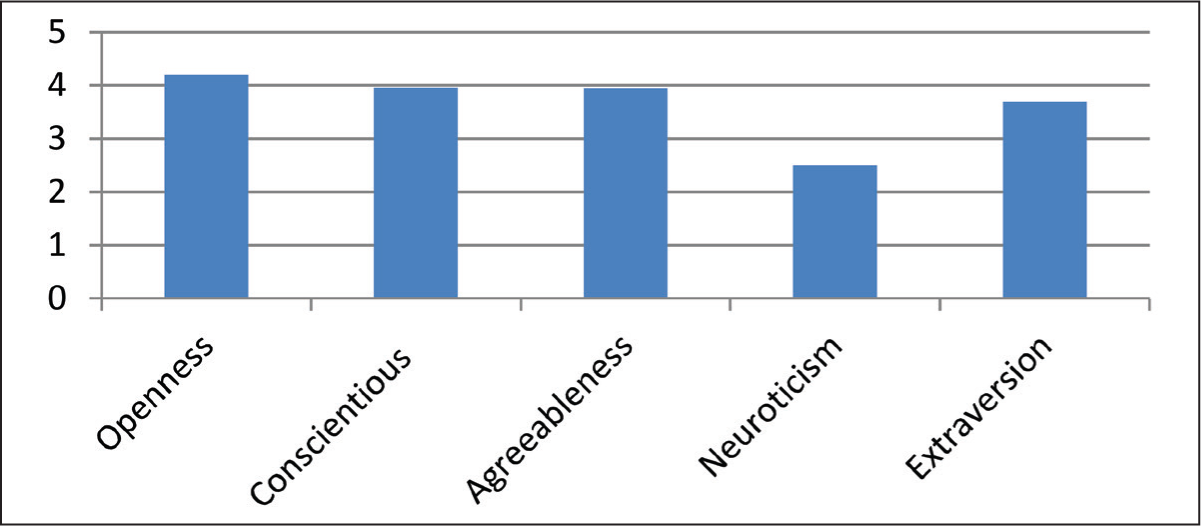

Averages of the Big Five Traits (Study 2).

The averages of the Big Five traits were calculated according to the detailed index in the Big Five questionnaire itself. The averages of the traits varied from 2.5 (SD = 0.748) for neuroticism to 4.2 (SD = 0.467) for openness. 16

A one-way ANOVA test did not reveal any significant differences in the traits of the entrepreneurs who failed to fund their project (N = 45) and those who succeeded (N = 117), except for extraversion (F = 3.309, p < .1). In light of the borderline significance of the result, the presence of a small sample bias was suspected. Therefore, several methods, such as bootstrapping, an established method for dealing with cases with small samples (Goodhue et al., 2012), were used to resolve this potential problem. The chi-square test also revealed a positive relationship between extraversion and successful funding (χ² = 35.426, p < .05). This trait was the only one of the Big Five that was significantly related to successful funding. This finding accords with previous literature documenting a relationship between extraversion and success in various occupational fields (Barrick & Mount, 1991; Lounsbury et al., 2009; Zhang et al., 2009).

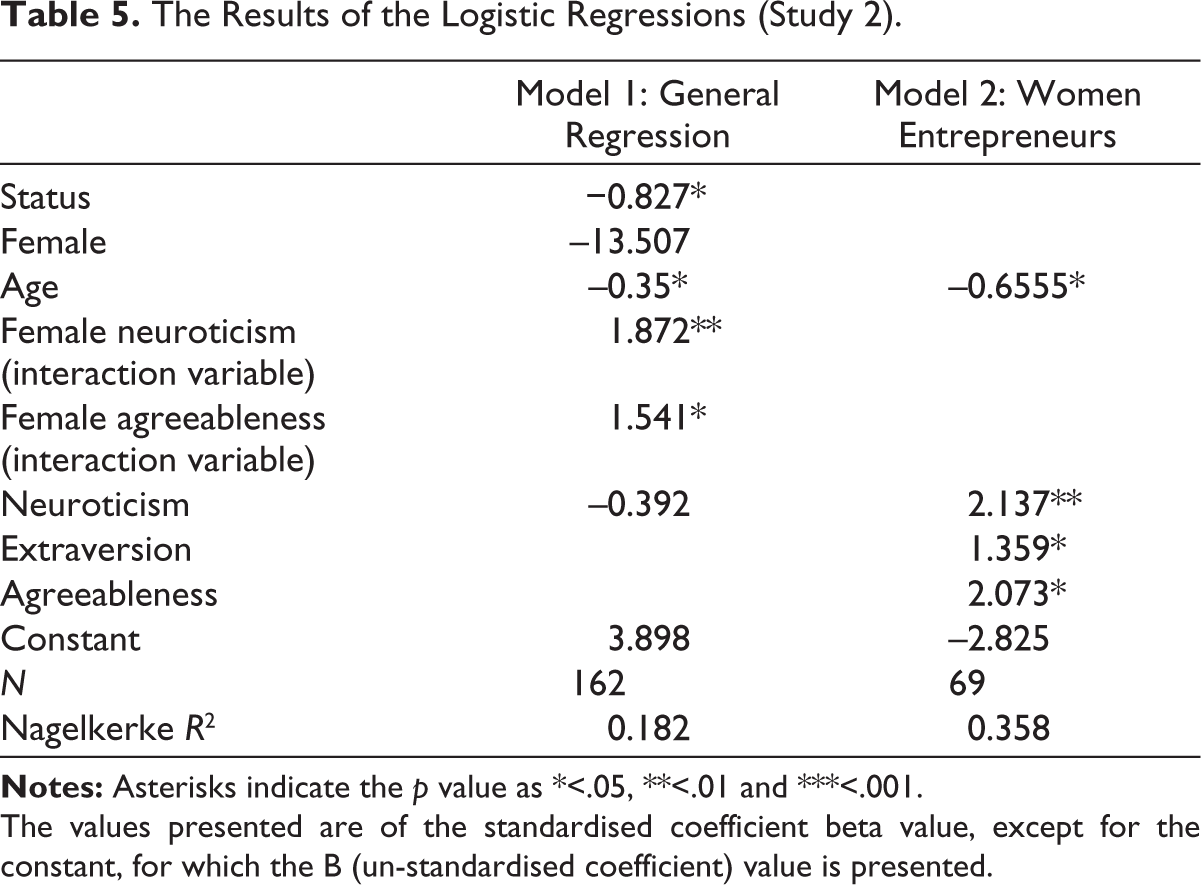

In order to analyse whether and to what extent the Big Five traits impact the success of funding, several other tests were conducted using logistic and linear models. Main results for the regressions are presented in Tables 5 and 6. In the logistic model, a dummy dependent variable for the success of the funding (success of funding = 1) was used, whereas in the linear model, the number of backers who invested in the campaign was used as the dependent variable. Both dependent variables represent different dimensions of the success of a crowdfunding campaign (Cumming et al., 2019). The independent variables in both regressions were the Big Five traits and demographic variables (age, gender, income, marital status and education). In light of previous literature indicating gender differences in personality attributes (Hachana et al., 2018; Lippa, 1991), interactions between the Big Five traits and gender were included. Another independent variable included in the regressions was the target funding sum of the campaign, which, according to previous studies, is an important factor that might impact the success of funding (Liu et al., 2020). Also see the results of Study 1. 17

Table 5 presents the results of the logistic regressions. The model was significant (N = 162, χ² = 21.857, p < .005). The main findings in this model imply that men and young entrepreneurs are more likely to have their crowdfunding campaigns funded. The findings regarding the relationship between the younger age 18 of entrepreneurs and this success accord with previous literature (Cumming et al., 2019). However, the findings regarding the apparent gender differences in the success of the funding are surprising. Previous studies have investigated gender differences and gender bias in the funding of entrepreneurial projects, revealing different results when considering offline and online funding. The findings do not accord with the few studies that indicate the relative success of women entrepreneurs compared with men entrepreneurs in funding their crowdfunding campaigns (Gorbatai & Nelson, 2015; Horvat & Papamarkou, 2017; Jennings & Brush, 2013; Malmstrom et al., 2017). More findings indicate significant interactions between gender and agreeableness and neuroticism. To explore these findings in depth, a second logistic regression was employed for only the women entrepreneurs in the sample. The results indicate a significant model (N = 69, χ² = 1 18.25, p < .005) with four main factors that impact the probability of successful funding: agreeableness, extraversion, neuroticism and age. Based on these findings, it is concluded that young female entrepreneurs who also scored higher on these traits would be more likely to have their crowdfunding campaign funded. In general, the findings are in accordance with previous literature indicating gender differences in the impact of personality on crowdfunding success (Hachana et al., 2018). 19 Other studies have also established that agreeableness and extraversion are important traits for entrepreneurs (Zhao & Seibert, 2006; Zhao et al., 2010), probably because these traits in particular represent the major inter-personal abilities that are crucial for entrepreneurs, especially when seeking funding. Extroverts are also more likely to use Facebook and other social media (Ryan & Xenos, 2011), which previous crowdfunding literature has associated with successful funding (Giudici et al., 2013; Greenberg et al., 2013; Mollick & Kuppuswamy, 2014).

The Results of the Logistic Regressions (Study 2).

The values presented are of the standardised coefficient beta value, except for the constant, for which the B (un-standardised coefficient) value is presented.

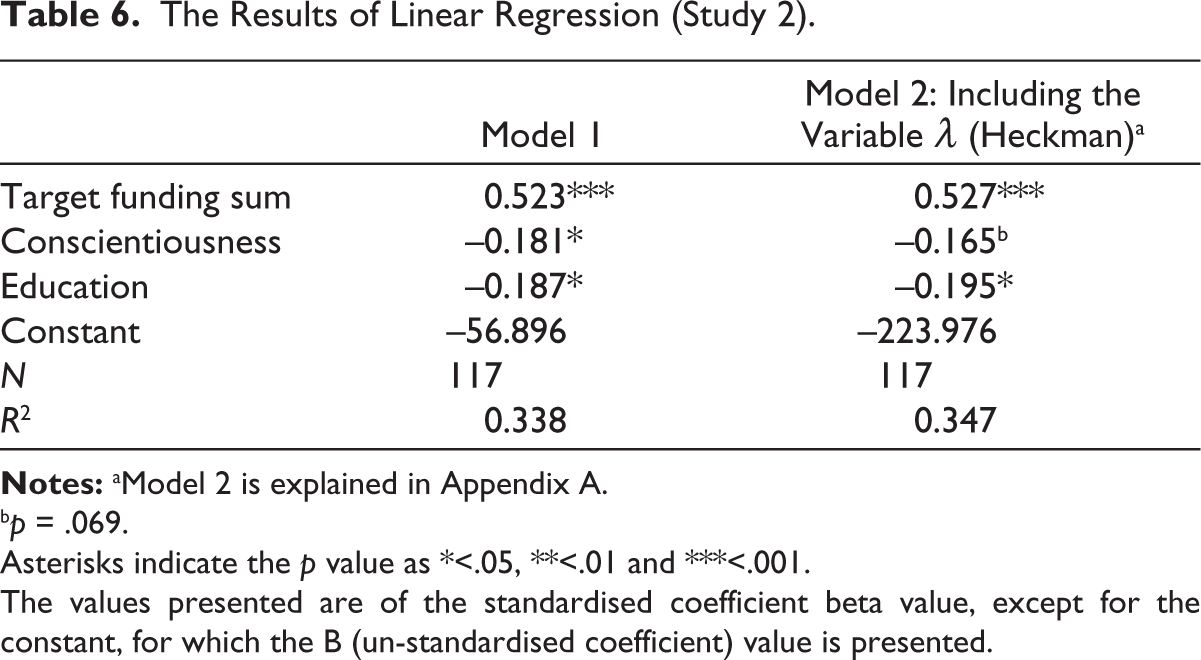

The Results of Linear Regression (Study 2).

bp = .069.

Asterisks indicate the p value as *<.05, **<.01 and ***<.001.

The values presented are of the standardised coefficient beta value, except for the constant, for which the B (un-standardised coefficient) value is presented.

Since many studies demonstrate the relatively small share of women in entrepreneurship (Cabrera & Mauricio, 2017), the findings expand the existing literature regarding women entrepreneurs and the personality factors that impact their success, especially in crowdfunding.

Table 6 presents the results of the linear regressions. The model was significant (N = 117, F = 7.901, p < .001). The findings in this model imply that three factors are key in influencing the number of backers of a crowdfunding campaign: the target funding sum (the higher the amount, the greater the need for more backers), conscientiousness (an inverse relationship between conscientiousness and the number of backers) and education (an inverse relationship between this variable and the number of backers). Conscientiousness has often represented the work ethic and diligence of the worker. Nevertheless, similar to this study, a few studies have already found an inverse relationship between this trait and success (Wilfling et al., 2011). One explanation for this result might be that an entrepreneur’s conscientiousness may also indicate a strong focus on details and lack of creativity, which may not necessarily be of use to the crowdfunding entrepreneurs’ success. The educational level of the entrepreneur also had an inverse relationship with the number of backers. One explanation for this result might be that, as the results of Study 1 indicated, highly educated entrepreneurs might receive more money from the crowd, reducing the need for a large number of backers to achieve the target funding sum. 20

Discussion and Conclusions (Studies 1 and 2)

A main contribution of both studies to the existing literature on crowdfunding is the use of first-hand data to search for answers. The advantage of the usage of primary data is obvious: it is most likely to provide trustworthiness and transparent information about the subject, whereas secondary data usually comes with a long list of caveats (Martins et al., 2018). Furthermore, primary information in crowdfunding is very hard to obtain since the backers’ and entrepreneurs’ details are not disclosed by the platforms. Therefore, these studies are a rare glimpse into crowdfunding through the eyes of the real participants.

The purpose of these studies was to describe both the crowd and the entrepreneurs in crowdfunding and to explore the factors that impact the behaviour of the parties in this funding method. By presenting both sides of crowdfunding, a better overall understanding of the complexity of factors behind the success (or failure) of a crowdfunding campaign is achieved. Combining studies 1 and 2 allows us to reveal that the attributes and motivations of both backers and entrepreneurs contribute to the success of funding, through the eyes of the actual participants in this unique funding method.

Findings show that both the crowd and the entrepreneurs were relatively young and highly educated and generally earned an average or above-average income. A direct approach to both backers (in Study 1) and entrepreneurs (in Study 2) was used, which was rare in previous crowdfunding studies.

The findings of Study 1 demonstrate, in accordance with those of previous literature, that, on one hand, the backers’ motives are not financial (van Teunenbroek et al., 2023). On the other hand, a clear preference for tangible rewards (Kuppuswamy & Bayus, 2018) is documented. Risk aversion is also revealed as a significant factor that impacts investment amounts (e.g., Kim et al., 2022; Zhou et al., 2022), particularly when larger amounts of money are involved. The latter finding accords better with investment funding methods than the previous one, which will better describe donations.

By employing three regressions for the different ranges of investment (lower, medium and higher amounts), it is also established that various factors affect the amount of the investment. Backers who invest small amounts of money seem to regard their investment more as a donation than as an investment. These backers tend to invest at the minimum level. The higher this level, the higher the investment. This seems logical, as most backers who invest small amounts of money choose the first possible level of investment. Therefore, their investment amount actually depends on the often arbitrary amount of this first level set by the entrepreneur. These results demonstrate that this determination is a key factor in this lower range of investment.

In contrast, those who invest larger amounts of money seem to regard it more as an investment. Among such backers, risk aversion is a significant factor. These backers often have larger investments in the stock market. In addition, they prefer tangible rewards. Furthermore, the higher the level at which such rewards are offered, the larger the investment. Clearly, such backers expect something in return for their money. Friends and family also feature often in this range of investment (in accordance with a number of studies which reveal that friends and family will often be an important source of funding for entrepreneurs in crowdfunding; Chen, 2022). The willingness to provide larger sums of money may be due to the simple desire to help someone they know or the fact that knowing the entrepreneur gives them more information about the entrepreneur and the project, reducing the risk involved in the investment. Definitive statements about those who invest in the medium range are more difficult to make. While they seem to regard their backing more as a donation than as an investment, any factors that indicate either way were not found.

Although the findings of both Studies 1 and 2 indicate that most of the factors that influence the amounts that the backers are willing to invest or the success of the funding of the campaign are out of the entrepreneurs’ control, one practical contribution of this work is that there are several factors that they can control to their advantage. First, they can offer more tangible rewards and set a higher level for receiving them. This is an important finding of Study 1: the higher the level at which the tangible reward is offered, the larger the investment (this finding is also supported by James et al., 2021). This direct correlation is a consistent result, evident in almost all ranges of investment amounts and in the general regression as well. Another result that entrepreneurs should heed is the importance of friends and family. According to the findings, on average, they will probably donate more than others to the project (also a consistent finding throughout almost all investment ranges).

Contrary to previous studies that found an inverse correlation between the success of the project and the target sum (Frydrych et al., 2014; Mollick & Kuppuswamy, 2014), the results are inconsistent and depend on the investment amounts. The target sum does seem to be a factor impacting the investment amount and the success of the funding (a result that repeated itself in both studies). However, it was not established that the number of levels of rewards has a positive influence on the investment amount. In previous studies, this finding was inconclusive, not significant or U-shaped (Du et al., 2019; Zhang & Chen, 2019). Furthermore, while the results pertaining to the minimum level were inconclusive, it was found that age has a significant direct impact on the investment sum. Given that no similar effect was evident with regard to income, it is only assumed that age in and of itself has aspects other than monetary ones that prompt backers to invest higher amounts. It is speculated that life experience and the desire of an older individual to help a younger, less experienced entrepreneur might play a role here.

The findings of Study 2 revealed the limited influence of the explored personality attributes and the character of the reward-based crowdfunding entrepreneurs on their ability to fund their project. The main findings suggest a gender difference in the traits that influence the success of the funding.

Further research is needed to conclude whether the male entrepreneurs’ personalities affect their success in crowdfunding. This study contributes to the few studies exploring the impact of personality in crowdfunding as well as to the lacking but growing literature on women entrepreneurs in crowdfunding.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.