Abstract

The purpose of this study is to present a systematic literature review of research articles on sustainable banking (SB). This study employed the SPAR-4 framework by integrating bibliometric analysis and qualitative content synthesis to review the literature in the domain. The review and analysis identified five thematic clusters: sustainable performance; environmental, social and governance integration in banks; green banking and ethical banking; corporate sustainability and financial stability brought by SB. The review further discovers the subthemes, which encompass influential researchers, top journals, their research findings and research agendas for future scholarly investigation. This study diverges from prior research that primarily relies on bibliometric mapping and insufficiently outlines future research agendas. This review combines bibliometric with a cluster-stratified comprehensive synthesis, progressing beyond the mere mapping of publication trends or the isolated evaluation of specific pillars of ESG to offer explanatory insights. Moreover, this study presents a conceptual framework specifying drivers, mechanisms, mediators and outcomes, and it further offers future research directions and policy-level insights that align SB with UN Sustainable Development Goals (SDGs).

Introduction

The global challenge of achieving sustainability, as incorporated by the United Nations Sustainable Development Goals (SDGs), has brought the financial sector into focus. Banks play a crucial role in the quest for sustainability, as they act as intermediaries in the flow of capital from suppliers to demanders. Sustainable banking (SB) is linked with multiple SDGs—economic inclusion (SDG 1, 8, 9, 10; Rahman, 2024; Úbeda et al., 2022), environmental accountability (SDG 7, 12, 13, 15; Feridun & Talay, 2023; Gafoor et al., 2023; Kashi & Shah, 2023; Weber, 2019) and governance and partnerships (SDG 16, 17; Aracil et al., 2021; Avrampou et al., 2019). This linkage highlights SB’s role as both a financial enabler and a strategic driver of the SDG agendas.

SB refers to aligning profitability with positive environmental, social and governance outcomes, guided by the UN Principles for Responsible Banking. The UNEP FI (United Nations Environment Programme Finance Initiative) principles for responsible banking surpassed 345 signatory banks in 2024, encompassing approximately 50% of global banking assets valued at approximately $98t (UNEP FI, 2019, 2024 signatories). Moreover, SB, in the parlance of banking institutions, refers to incorporating sustainability measures into their fundamental operations (Rajawat & Mahajan, 2024). SB comprises three components: environmental, social and governance (ESG), with green banking (GB) serving as a fundamental component (Sarma & Roy, 2020). In practice, this means integrating ESG criteria into banks’ operations and moving beyond profitability enhancement towards long-term stakeholder value. Banks, therefore, adopt GB practices, such as being mindful of environmental risk when lending loans and investing in projects that benefit both society and the environment. Notably, Gunawan et al. (2021) and Mir and Bhat (2022) highlighted that SB encompasses GB methods that integrate environmental issues, community engagement and ethical principles.

The SB: ESG Nexus

SB is defined in this study as an umbrella construct that integrates the ESG-based performance construct encompassing economic feasibility, environmental consciousness, social inclusion embedded within operations, strategy, disclosures, lending and investment, often linked to SDGs and principles of responsible banking. ESG constructs may suffer from opacity in scoring and benchmarking, and SB may exhibit boundary ambiguity unless the ESG components are explicitly and separately defined. GB is positioned as the environmental (E) pillar of SB, which refers to green lending, green investments made by banks and the consciousness about environmental issues and the strict screening of all loans to polluting entities. The socially responsible and inclusive (S) pillar includes responsible lending, financial inclusion, customer protection and loyalty by inducing trust and fair practices, obligations to society and employee well-being. The ethical banking pillar includes the governance (G) component, which values an integrity-driven orientation of banks anchored in stakeholder primacy and moral conduct.

Research Gaps in SB Domain

Recent review articles and bibliometric studies have examined the trends in SB research from multiple perspectives. Sarma and Roy (2020) conducted a scientometric analysis of GB and identified six broad aspects of GB: conceptual, legal, model, stakeholder, financial and green performance. Akomea-Frimpong et al. (2021) focused specifically on banks’ green finance, mapping the products and determinants of banks based on a content analysis. Furthermore, Galletta et al. (2024) studied greenwashing in banking by distinguishing finance-related themes—such as sustainable finance and banking practices, environmental regulations, and ethical banking principles and management themes—covering banks’ CSR efforts, transparency in environmental disclosures and their relatedness to greenwashing. Aslam and Jawaid (2023) employed a more systematic approach, using the PRISMA protocol, to investigate GB adoption.

These studies collectively highlight the expanding scope of SB research; however, they also reveal gaps, including excessive reliance on bibliometric mapping, and inadequately developed future research roadmaps. Moreover, the common limitations restrict the cumulative knowledge, including evidence that is primarily focused on investors and performance, while comparatively few outcomes related to customers, employees and society are synthesised. Additionally, a substantial portion of the underlying empirical research is cross-sectional and short-horizon, failing to adequately provide clues about whether the effects of SB/ESG are permanent or fluctuate with cycles and crises. Governance is often mentioned but rarely addressed with rigour, such as assurance, credible disclosure and the risks of greenwashing or ethical washing. To fill the gap, this study aims to conduct a systematic literature review of research articles on SB. The study further aims to integrate SDG linkages and greenwashing disclosure dimensions explicitly. This study integrates bibliometric clustering with a cluster-stratified comprehensive synthesis, advancing from mere mapping of publication trends or isolated investigation of specific pillars to providing explanatory insights. This study conceptualises SB as a broader concept and systematically deconstructs it into E/S/G pillars, enabling the identification of underlying mechanisms, boundary conditions and stakeholder outcomes. This integrated approach of review culminates in a theory-informed research agenda and a conceptual framework. This approach provides a more comprehensive synthesis of SB research, highlighting emerging themes, unresolved gaps and future research agendas by expanding SB coverage across regions and bank types. For policymakers and banks, this review article offers several implications, including how SB practices can be systematically aligned with SDGs and embedded into lending, investment and reporting transparency. The structured research agenda highlights critical pathways for scaling sustainable and climate finance, improving disclosure quality and mitigating greenwashing risks and supports the claim of novelty when contrasting old and new knowledge. Hence, this study proposes a replicable framework for multiple stakeholders—including regulators, banks and investors to benchmark their performance and activities against SDG-linked goals.

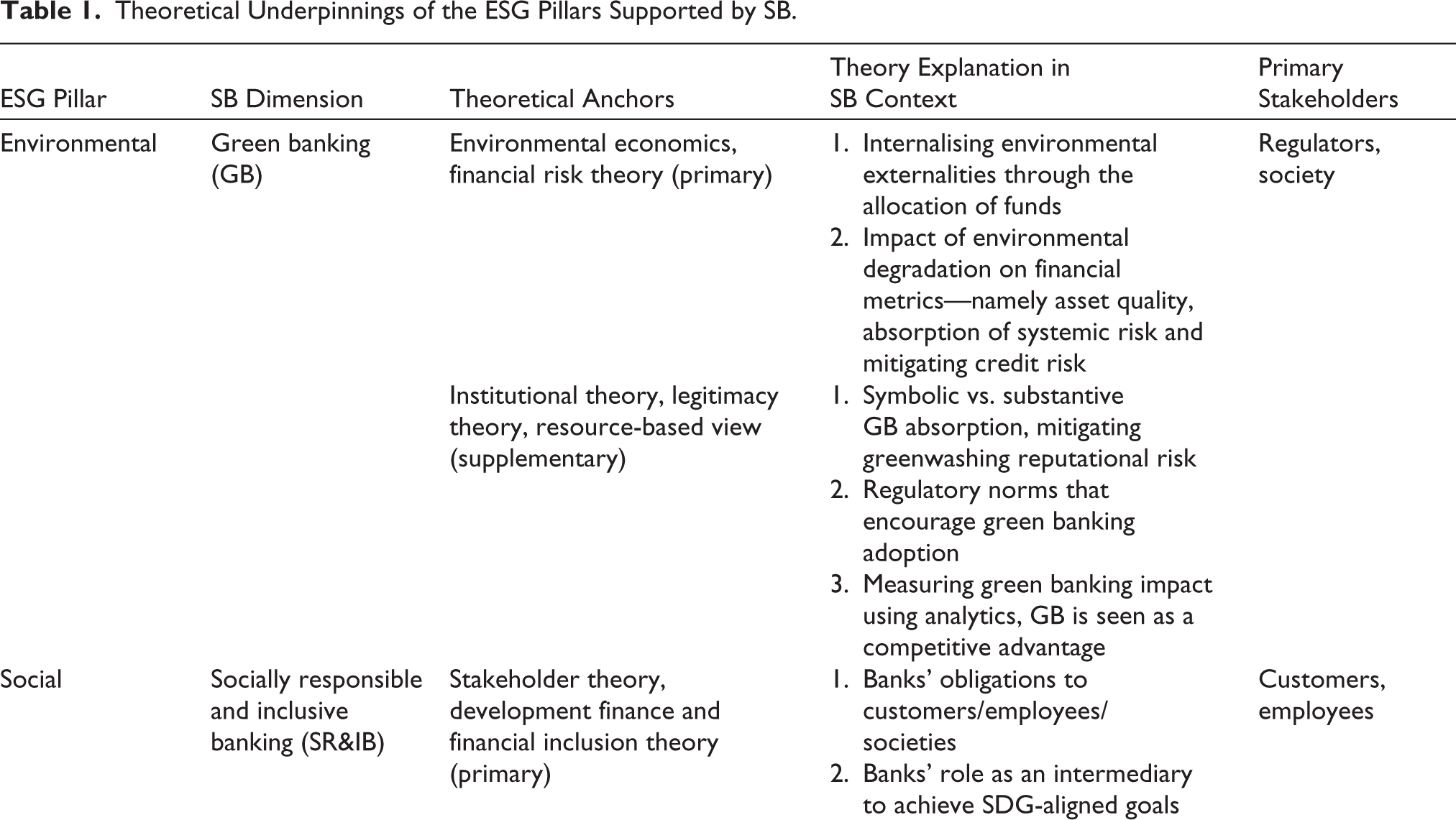

Theoretical Anchors of the ESG Pillars Supported by SB

This study anchors SB within a coherent theoretical framework aligned with environmental (E), social (S) and governance (G) dimensions of ESG. GB, the environmental dimension of SB, is primarily grounded in environmental economics, which conceptualises environmental degradation as a market failure arising from the inability of markets to account for price externalities (Pigou, 1920; Stern, 2007). Banks act as capital allocators, capable of internalising environmental costs by incorporating climate risk into their lending and investment decisions through green lending policies, environmental screening and financing of low-carbon projects. Complementing this foundation, the financial risk theory reframes the environmental degradation issues as financially material risks, namely credit risk, asset impairment and systemic risk vulnerability (Bolton & Kacperczyk, 2021; Merton, 1974). This perspective justifies GB practices with the aim of profit-maximising by increasing the integration of climate risk into credit appraisal and stress testing. Moreover, the resource-based view holds that banks with green practices have a competitive advantage (Barney, 1991) over other banks, but not for all. Advanced climate risk analytics and environmental expertise enhance the performance of banks when embedded in their core banking practices.

The social aspect of SB is anchored primarily in the stakeholder theory, which posits that banks are responsible for balancing the interests of multiple stakeholders— customers, employees, communities, shareholders and suppliers (Freeman, 1984/2010). Financial inclusion, responsible lending and investing, protection of customer interests and employee well-being are not merely CSR activities, but integral components of social and responsible banking. This perspective is reinforced by the development finance theory, which positions access to capital as a catalyst for inclusive economic growth (Beck et al., 2007). Financial inclusion, including the underbanked population, MSMEs and disadvantaged regions, reflects a bank’s developmental role. At the micro-level, the relationship and trust theory explains how social and responsible banking initiatives influence customer loyalty induced by enhanced trust and reputational capital (Morgan & Hunt, 1994). Additionally, the human capital theory provides a rationale for internal social sustainability, highlighting how employee well-being, diversity, training and ethical practices contribute to organisational performance (Becker, 1964). The social norms adopted by SB can also be further anchored with institutional theory, with inclusion norms and mandates shaping the depth of socially responsible and inclusive banking with varied institutional settings (DiMaggio & Powell, 1983).

Ethical banking (EB) can be most appropriately explained through the lens of the agency theory. This theory emphasises the need for governance mechanisms to align the actions of managers with the interests of stakeholders (Jensen & Meckling, 1976). Board oversight, executive incentives, risk governance and internal controls transform ethical intent into enforceable practice, thereby reducing individual goals prioritisation with enhanced accountability. This can be further explained by the corporate governance theory, which focuses on good governance practices (Shleifer & Vishny, 1997), namely board independence, sustainability audit committees and foolproof disclosure systems, that promote transparency and control. Finally, the normative ethical theory underpins government-driven sustainability by articulating principles of fairness (Rawls, 2001), integrity and responsibility (Kant, 1785/1993). These theoretical underpinnings are presented in Table 1, positioning SB as a multidimensional construct which can be measured by ESG metrics, where environmental, social and governance initiatives operate through interrelated mechanisms. This integrated theoretical anchoring enables a more coherent synthesis of literature and provides a conceptual framework.

Theoretical Underpinnings of the ESG Pillars Supported by SB.

Methodology

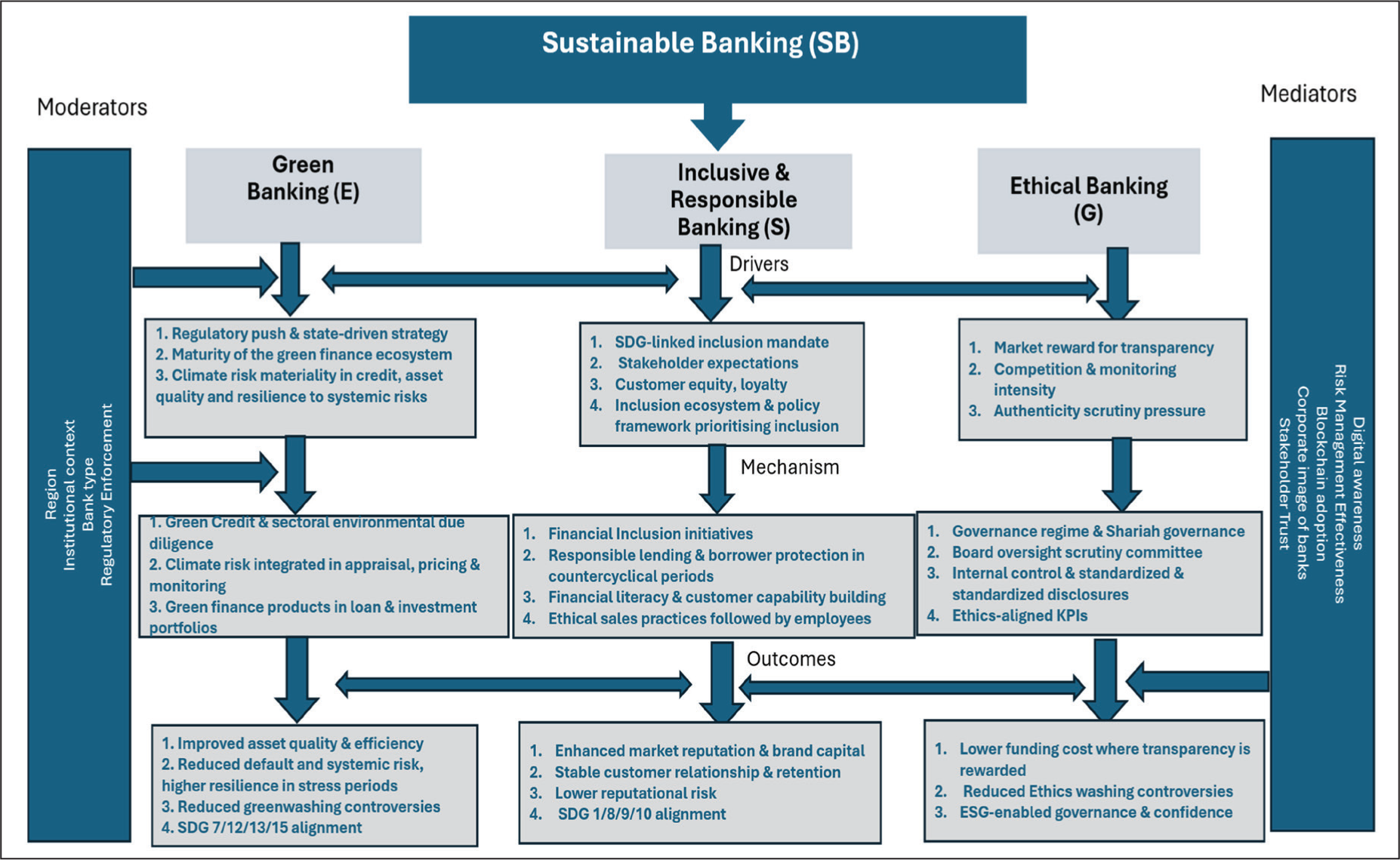

This study aims to conduct a systematic literature review using bibliometric methodology to explore and organise the existing literature in SB. The study used the SPAR-4-SLR protocol, which comprises three stages: assembling, arranging and assessing the literature for systematic review (Kumar et al., 2022; Paul et al., 2021). This protocol ensures a transparent and systematic approach that permits replication and reduces arbitrariness by providing detailed justifications for choices made during the review process (Ahiadu & Abidoye, 2023; Paul et al., 2021). The review methodology is summarised in Figure 2.

SB Deconstructed: Drivers, Mechanisms and Outcomes Across ESG with Boundary Conditions.

The first step, comprising the assembly stage, began with aligning the research objective using appropriate keywords. The study utilised publication data from the Scopus database, which offers extensive coverage of peer-reviewed journals and comprehensive bibliographic information and facilitates further content analysis (Bhaskar et al., 2022; Pandey et al., 2023). Specifically, Scopus coverage is reported to be 60% larger than that of Web of Science (WoS; Comerio & Strozzi, 2019; Garg et al., 2024; Rathi et al., 2022).

The preliminary search employed ‘sustainable* bank*’ and ‘bank* sustainable*’. Moreover, Boolean operators (OR) were used to retrieve articles pertinent to the study. Additionally, the ‘*’ symbol was used to identify relevant papers containing terms with identical roots but different endings (Agnusdei & Del Prete, 2022). The initial keyword search was conducted using these words to gather publications on bank sustainability or sustainable banks rather than research linked to domains outside the selected area of research. The initial search yielded 428 documents. In the second phase of compiling a corpus of literature, the study employed inclusion and exclusion criteria to refine the initial search results, such as publication span, document types and language utilised (Chebo & Dhliwayo, 2024). Moreover, subject classifications (Aparicio et al., 2019; Sardana & Singhania, 2022) were employed to identify pertinent publications related to the selected domain of the study and research objective. The publications from January 2009 to December 2024 were reviewed; documents prior to 2009 were excluded (18 documents). We selected this period because the search results showed the publications prior to 2009 were not continuous; for many years, there was only one or no publication. Similarly, publications in business, management, accounting, economics, econometrics, finance and the social sciences were included; the rest were excluded (71 documents). This study selected articles and journals as the document and source types for inclusion (excluded 76 documents) while excluding documents (5) published in languages other than English. Based on this protocol, a final corpus of 258 documents relevant to the study’s domain was selected.

In the assessment stage, the study employed analysis and review methods, utilising performance analysis and scientific mapping (Chebo & Dhliwayo, 2024). Performance analysis is commonly employed in reviews, as it is a standard procedure demonstrating the efficacy of various study components within the discipline (Donthu et al., 2021). The science mapping evaluates the connections between study elements and the intellectual framework of a discipline (Baker et al., 2021). Multiple criteria were employed to demonstrate publishing trends and the impact of authors’ research and documents within performance analysis. Similarly, keyword occurrence and thematic maps were used to explore science mapping. The bibliometric approach offers valuable insights and can be utilised to identify trends and research streams within the body of literature (Filho et al., 2024). This approach is commonly utilised across various domains to aid literature reviews (Mishra, 2023; Yadav & Dangi, 2022). The analysis utilised the ‘bibliometrics’ (Aria & Cuccurullo, 2017) package in ‘R Studio’ and ‘VOS viewer’ (Van Eck & Waltman, 2017) software applications for bibliometric analysis and data visualisation. For qualitative content analysis, the abstracts of 258 research articles were read and manually categorised into five subthemes. The authors further filtered the data (publications) that received more than eight citations (20 December 2024) and critically reviewed publications (50) to identify the key findings, gaps and the research agendas for future researchers.

Qualitative Synthesis and Integration with Bibliometric Clusters

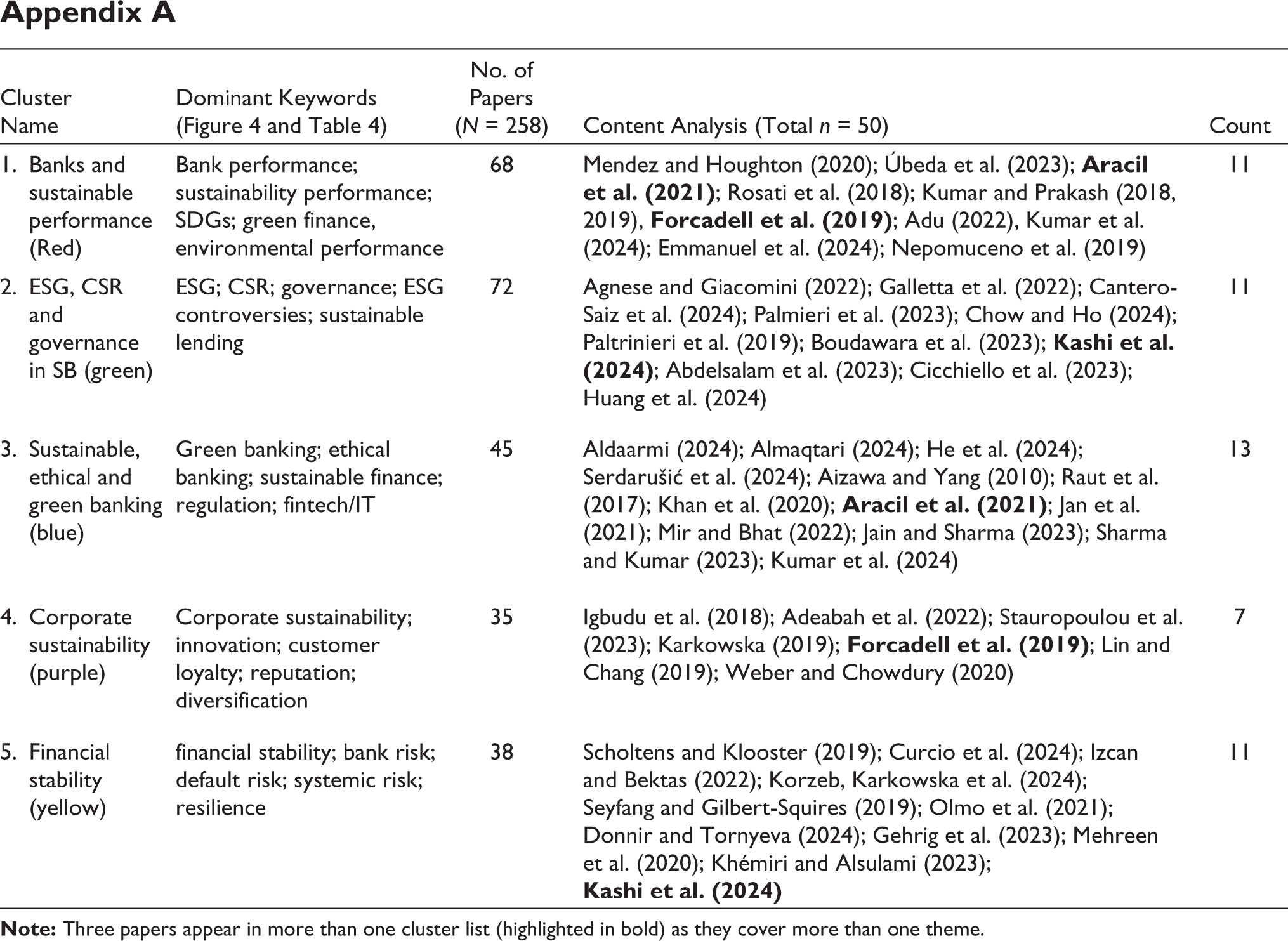

The screening of a corpus of documents based on titles and abstracts facilitated our understanding of broad topical focus. This step is followed by generating co-occurrence clusters by using five keywords in VOS viewer to organise structure and create five corresponding themes. From each theme, high-impact papers (≥8 Scopus citations as of 20 December 2024) were selected for in-depth narrative synthesis (n = 50), ensuring representation across all five clusters. This process positioned an interpretive synthesis anchored in bibliometric clustering rather than a formal code-based qualitative analysis. To strengthen transparency and traceability, Appendix A reports the cluster mapping (dominant keywords and paper counts per cluster). This cluster-stratified selection reduces the risk of over-representing a single theme and provides coverage of the full thematic space identified in the bibliometric mapping.

Results and Analysis

Trends in SB Research over the Years

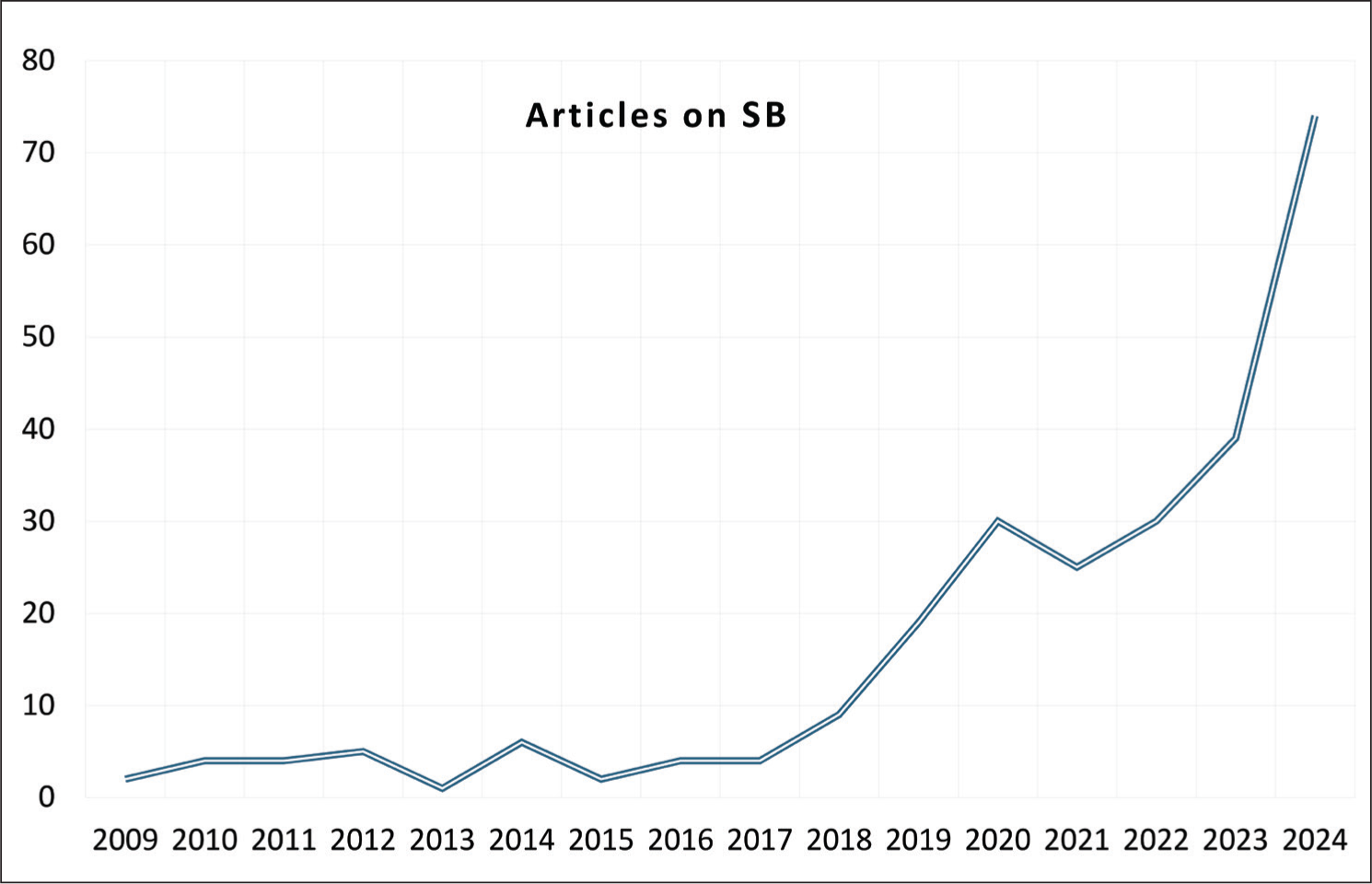

Figure 4 illustrates the publication trend in SB research over the 15 years from 2009 to 2024. It shows a consistent upward trend in publication rates from 2009. The research conducted by Yeoh (2009) explored two aspects of SB—financial and environmental—and was among the earlier studies during the selected period of review for this study. Subsequently, the field of SB research has drawn the attention of scholars. There has been a significant increase in literature since 2020, possibly because of the rise in ESG issues and ratings, concerns about climate and transition risks, and the COVID-19 pandemic. These factors possibly increased the focus on resilience, stakeholder welfare and responsible finance. Likewise, the bank’s focus on promoting sustainable finance, integrating ESG factors into investment decisions and the regulatory scrutiny of public institutions further contributed to the increased attention in literature during 2020 to 2021 (Galletta et al., 2024). Moreover, this attraction might be enhanced by the current prominence of sustainability in both industry and academia. The graph (Figure 4) reaches its peak in 2024, with 74 articles.

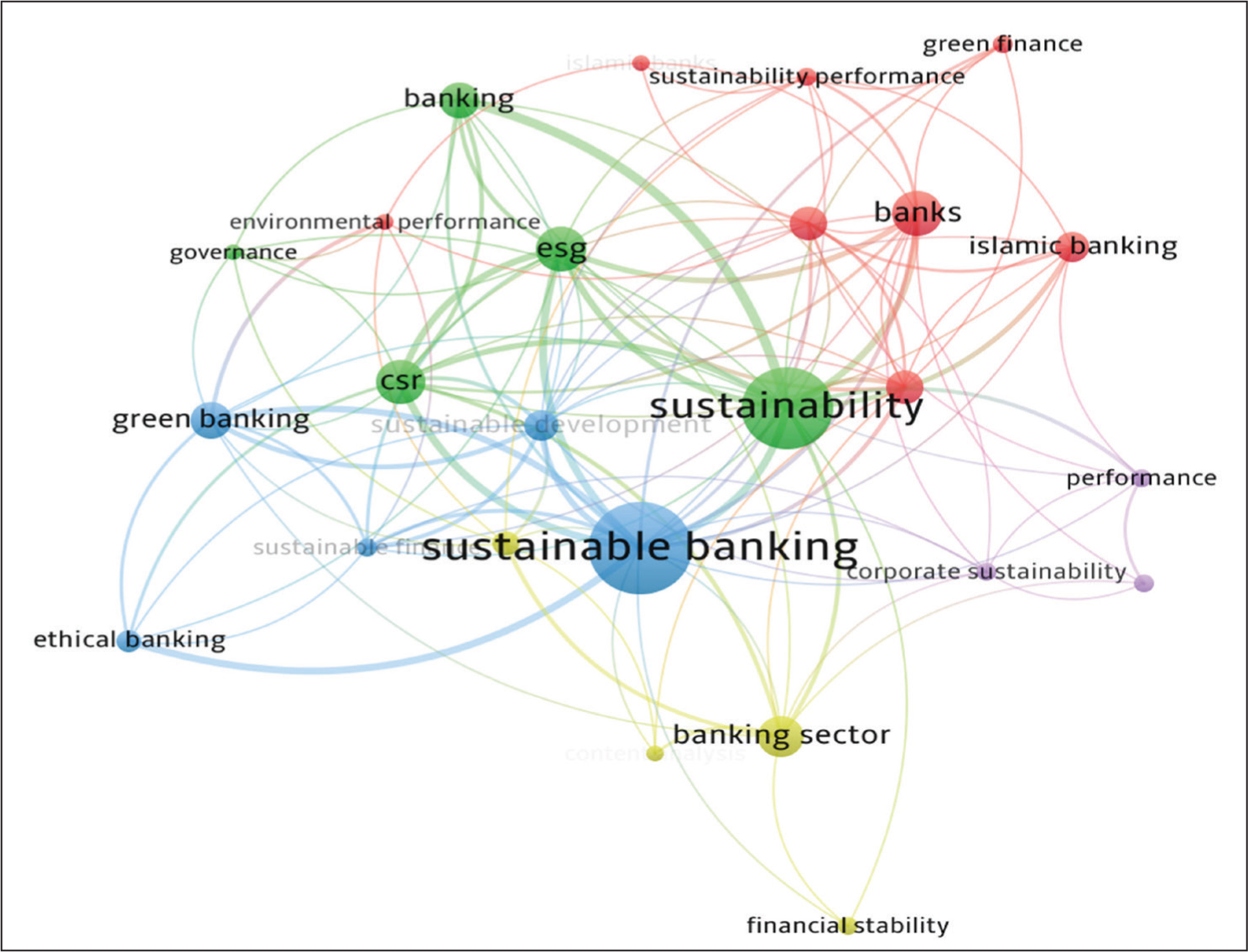

Keyword Co-occurrence Map Based on the Author’s Keywords.

Annual Publication Trends in the SB.

Influential Authors, Sources and Documents

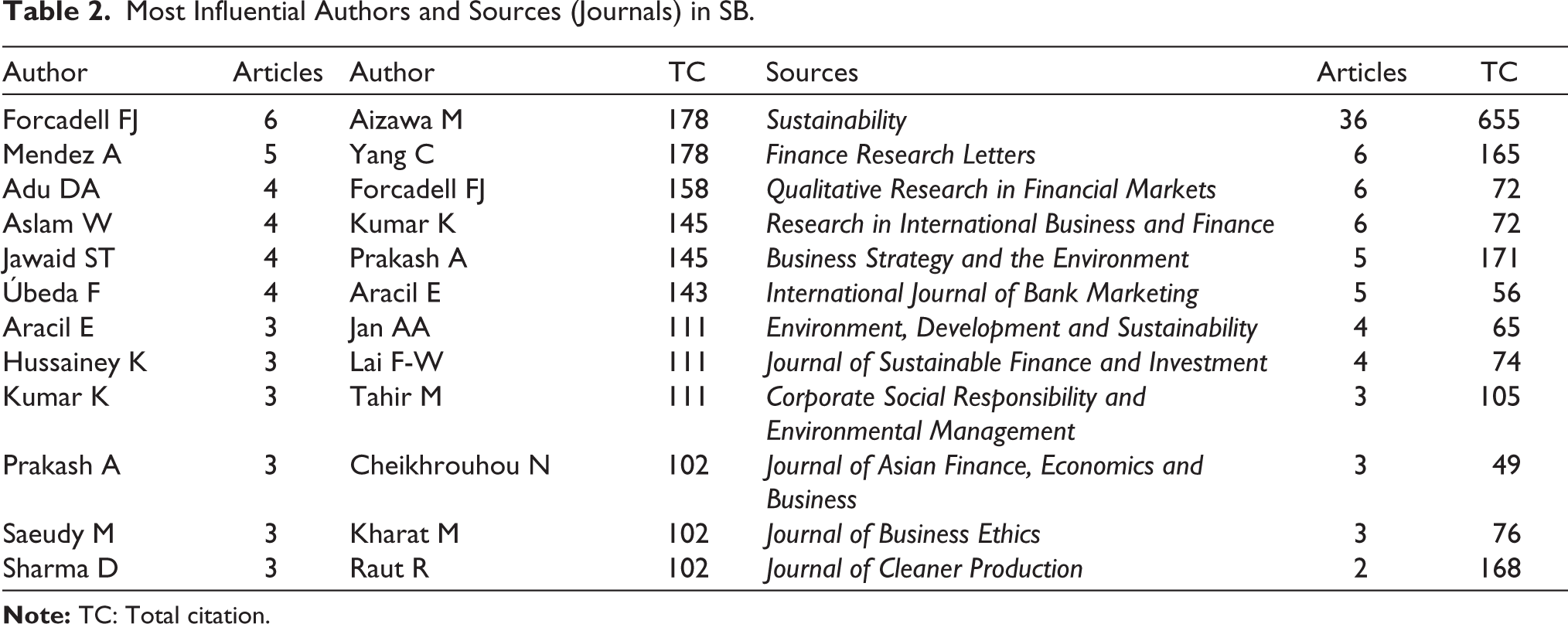

While analysing the most prominent sources in a field may indicate the most influential venues for disseminating research results, assessing top authors can elucidate key contributors to the discipline (Nobanee & Ullah, 2023). Table 2 outlines the most influential authors based on several publications and citation counts, as well as prolific sources. It lists authors who have published three or more articles in the field of SB, as well as the most prominent authors based on citations exceeding 100 for research articles in the selected domain. F. J. Forcadell leads with the highest number of publications (6), while M. Aizawa ranks first with the most citations (178) in the SB domain. The study’s analysis reveals that ‘sustainability’ has emerged as the most prolific journal, accounting for both the highest number of publications (about 14%) and citations (655). The highest publication counts are listed in the order of the most prolific sources. Notably, the Journal of Cleaner Production stands out with 168 citations, ranking at the top among these journals with two publications. The journal Finance Research Letters has garnered the second-highest number of research articles (6) on SB.

Most Influential Authors and Sources (Journals) in SB.

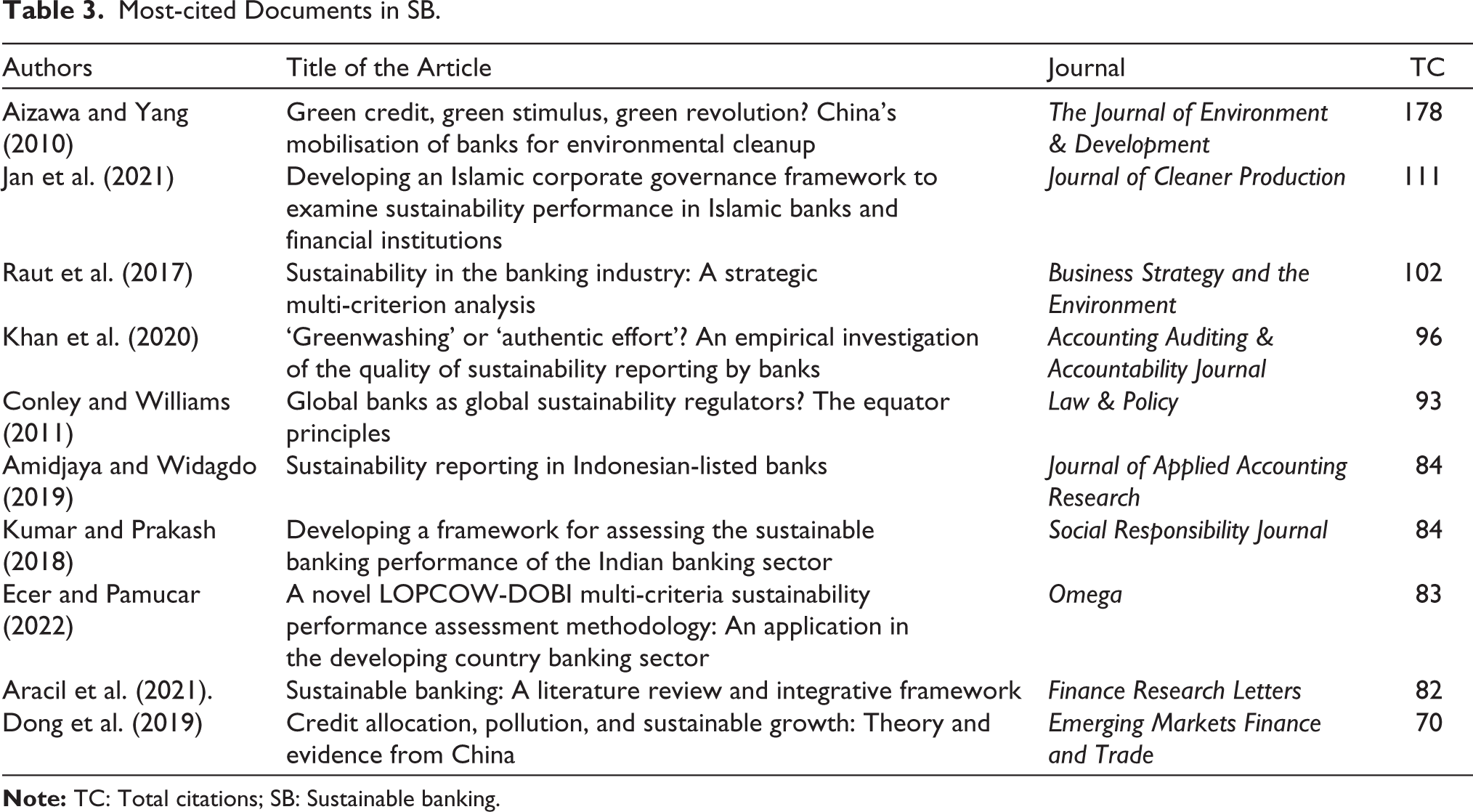

Reviewing the most influential documents (by the number of citations) provides insights into the current understanding of a field (Yumnam et al., 2024). Moreover, the citations of a research study have long been regarded as a primary metric for assessing the influence of scientific work over many years (Fareed et al., 2024). Table 3 presents the most influential documents in SB, ranked by total citation counts, along with their authors and journals. The study with the highest citation counts, by Aizawa and Yang (2010), highlighted the importance of banks in providing green credit for addressing environmental and social concerns. Financial institutions, such as banks, can enhance long-term profitability and societal welfare by promoting the integration of sustainable practices into business processes (Jan et al., 2021). The research conducted by Jan et al. (2021) has garnered 111 citations, making it the second highest in the selected study area. Similarly, Raut et al. (2017) explored sustainability practices in the banking industry, garnering over 100 citations and emerging as one of the most influential studies in the discipline. Moreover, banks began adopting SB practices through their services by aligning with the equator principles, which establish social and environmental standards (Conley & Williams, 2011). Credit allocation influences the environment through various industries and may contribute to sustainable growth (Dong et al., 2019). Notably, the environmental pillar of sustainability is the most researched topic, followed by the social and governance pillars. Aracil et al. (2021) reviewed the literature on SB using WoS data from 1995 to 2019. Another significant study in this domain, based on citation counts, includes studies of Amidjaya and Widagdo (2019) and Khan et al. (2020), which explored sustainability reporting in banks in Indonesia and Bangladesh, respectively. Kumar and Prakash (2018) examined SB practices in Indian banks and identified key sustainability concerns related to their operational frameworks, including financial inclusion, financial literacy and energy efficiency.

Most-cited Documents in SB.

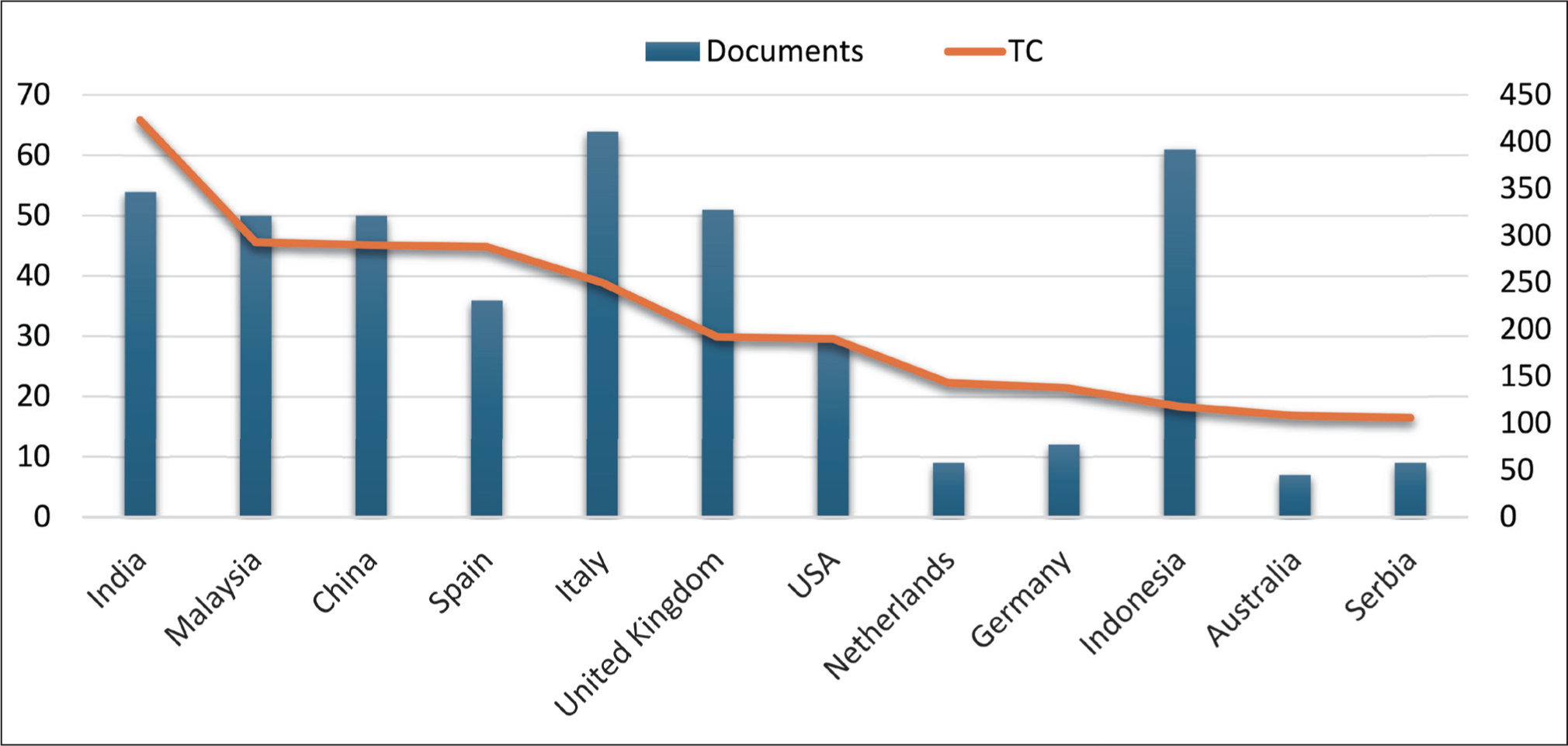

Country Citations and Productivity

The study employs a country-specific scientific production and citation analysis to comprehend the demographic composition of research articles within the SB literature. Figure 5 displays the country’s citations and publications in the body of literature. The analysis generated the figure by listing the top 12 countries with more than 100 citations, sorted by total citation counts. The analysis reveals that Italy has produced the most scientific articles (64), followed by Indonesia (61) and India (51) during the study period from 2009 to 2024. Moreover, India tops the list with 423 citations, followed by Malaysia (293) and China (290). The analysis also reveals that scholars from various geographic locations, including developing and developed countries, have been drawn to this domain. This attention is potentially driven by a combination of factors, including the increasing importance of ESG issues and ratings, growing concerns about climate and transition risks, and the effects of the COVID-19 pandemic, as demonstrated by the substantial increase in publications after 2020.

Country’s Scientific Production and Citations in SB Literature.

Keyword Co-occurrence Analysis

The study employs scientific mapping and keyword co-occurrence analysis to explore current themes and concepts in SB. This analysis enables the study to show emerging research clusters in the domain (Sanni & Verdolini, 2022). A co-occurrence map has been generated using the author's keyboard in VOSviewer, with a threshold set to a minimum of five occurrences and employing the full counting method. Figure 4 illustrates the network, which comprises 25 keywords organised into five distinct clusters.. The five most frequently occurring keywords are ‘sustainable banking’ (54), ‘sustainability’ (46), ‘bank’ (21), ‘ESG’ (21) and ‘CSR’ (20). Moreover, sustainable banking (SB) exhibits the strongest connection (link strength) among the keywords, suggesting its prominence in the discourse. Notably, themes such as ESG, CSR, GB, corporate governance, Islamic banking and sustainable finance have emerged as significant concepts within the literature.

Thematic Content Analysis and Research Agendas for Future

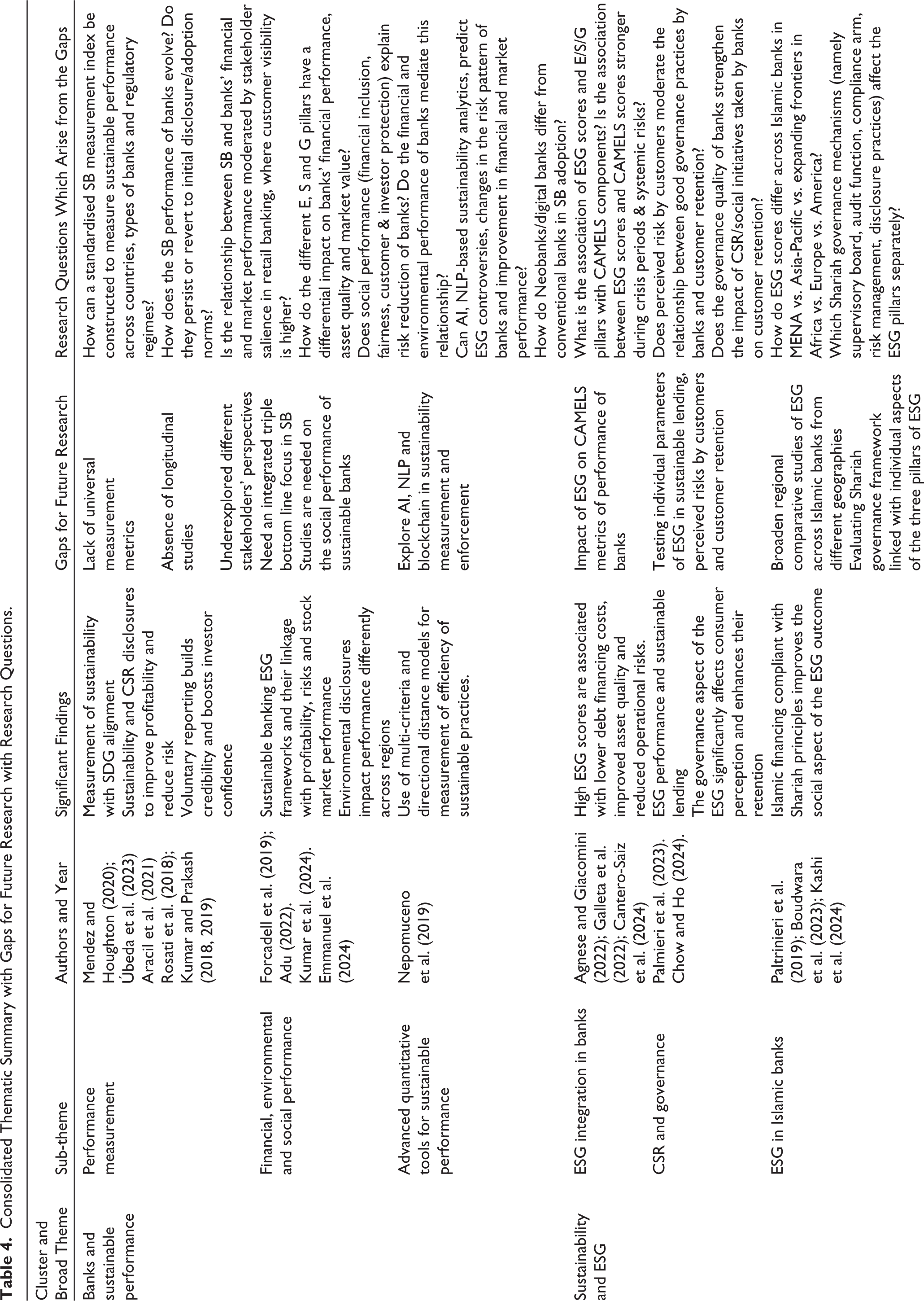

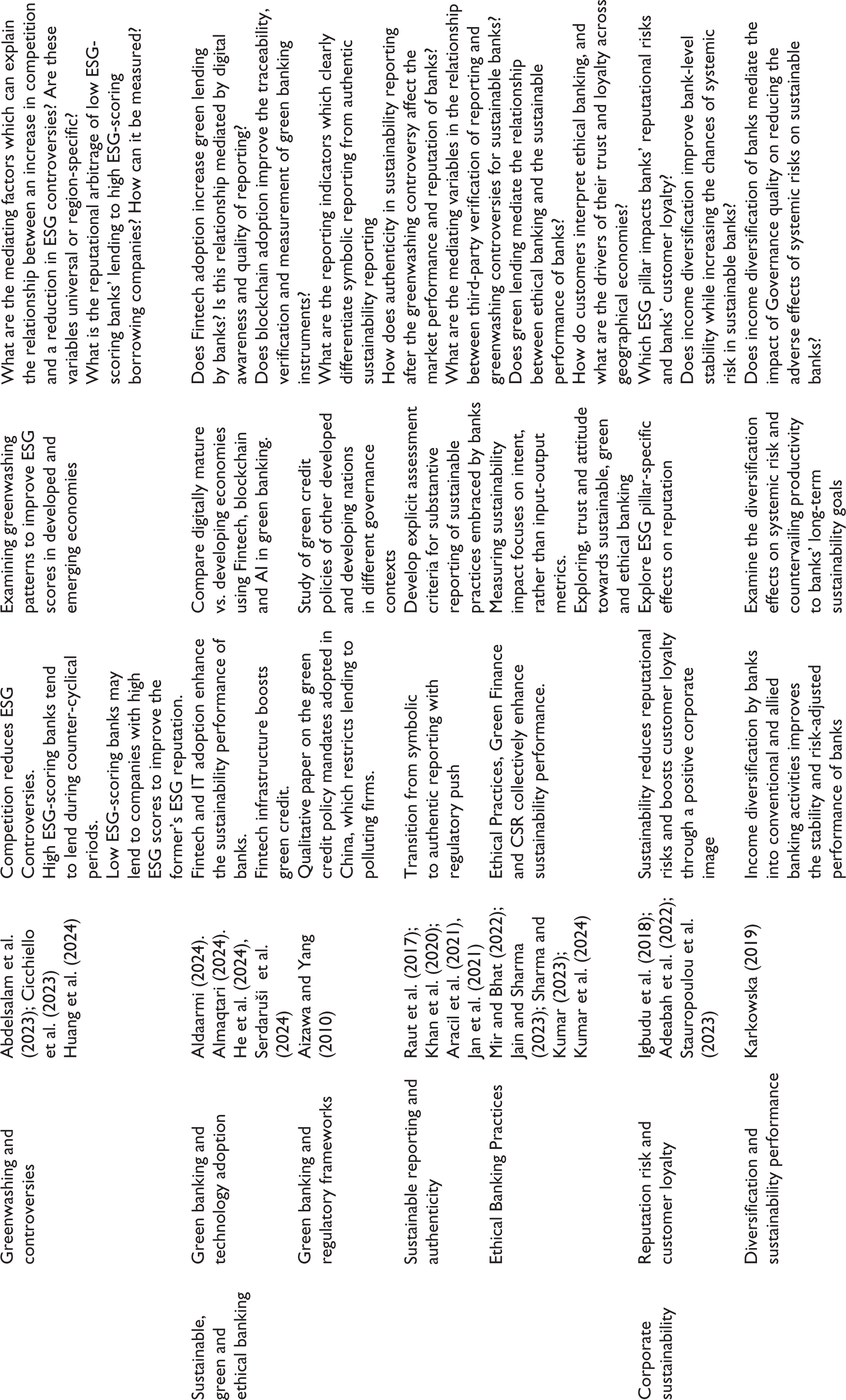

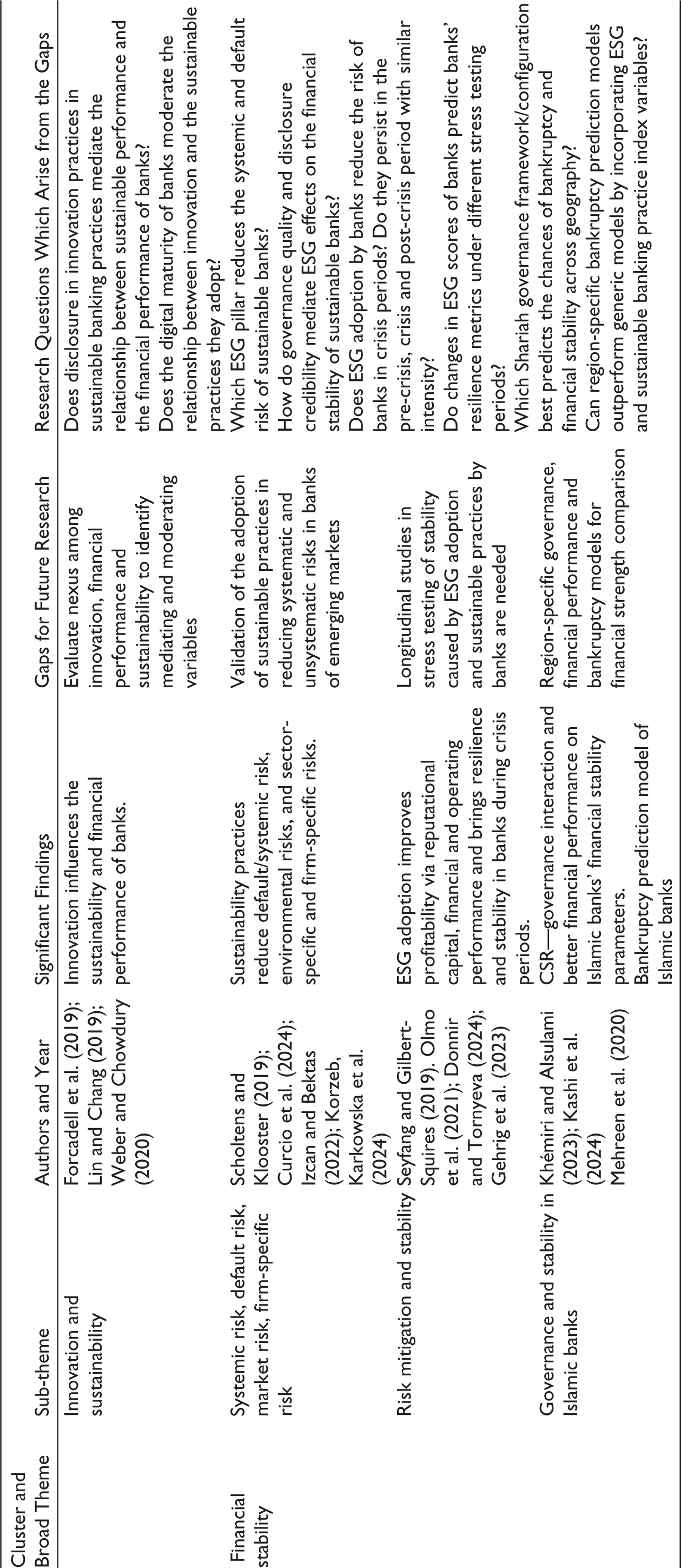

This section presents a qualitative content analysis of prominent research articles and highlights subthemes within each cluster. Within each bibliometric cluster, an interpretive synthesis has been conducted to extract recurring mechanisms, contexts, outcomes and research gaps and to develop a structured future research agenda (Table 4). Appendix A links these five clusters (Figure 3) to the corresponding themes, reports the number of papers per cluster (N = 258) and lists the papers (n = 50) used for content analysis within each cluster. While Table 4 displays a summary of prolific authors and their significant findings, future research gaps (agenda) and research questions, Figure 1 presents the proposed conceptual framework.

Consolidated Thematic Summary with Gaps for Future Research with Research Questions.

Banks and Sustainable Performance

Banks, Islamic banking, sustainability performance, environmental performance and green finance are prominent in the first cluster (red). The empirical studies focused on ESG–financial linkage (Adu, 2022; Forcadell et al., 2019; Kumar et al., 2024), risk analysis (Aracil et al., 2021; Úbeda et al., 2023), SDG alignment (Mendez & Houghton, 2020; Úbeda et al., 2023) and CSR impact, while qualitative studies (Kumar & Prakash, 2018, 2019; Rosati et al., 2018) explore disclosure frameworks, regulatory frameworks (Costa-Climent & Martinez-Climent, 2018), stakeholder trust, policy analysis and strategy.

The key findings across studies (Adu, 2022; Forcadell et al., 2019; Kumar et al., 2024) in this cluster confirm that banks that adopt an ESG framework, sustainability disclosure and CSR strategies exhibit increased profitability, reduced risk and better stock market performance. Despite convergence among the subthemes of this cluster, three persistent gaps remain. First, the research theme that remains unexplored is that terms such as ‘green banking’, ‘ESG’ and ‘sustainability’ are inconsistently defined across studies, thereby weakening cumulative knowledge and cross-study comparability. Second, most empirical evidence is cross-sectional, covering a shorter time horizon, leaving the scope of rigorous investigation open on the causal direction of whether SB effects persist, amplify or decay over time. Third, past literature indicates that disclosures enhance legitimacy, and greenwashing dilutes the quality of reporting and undermines stakeholder trust (Aracil et al., 2021). The non-uniformity of environmental disclosures has an asymmetrical impact on the performance metrics (Emmanuel et al., 2024). This suggests testing SB under moderating variables, namely regulatory intensity, verification strictness and measurement parameters. Prior literature has evaluated SB from an investor’s lens. The impact of SB practices on customers, employees and society remains unexplored. Future research should prioritise (a) standardisation of SB measurement frameworks, including SDG-aligned indices that are comparable across countries, bank types and disclosure regimes; (b) longitudinal study designs to test persistence, reversals and post-controversy recovery of SB; and (c) stakeholder-inclusive SB assessment, where customer trust, social inclusion and ethical governance are not treated as peripheral.

ESG, CSR and Governance in SB

This cluster (green) extends the performance measurement of SB towards ESG, CSR and governance, particularly in recent work (post-2023). Empirical studies suggest that higher ESG scores are associated with lower debt financing costs in the primary market due to higher corporate governance standards and transparency in reporting, rather than environmental friendliness (Agnese & Giacomini, 2022). ESG is also linked to improved asset quality, though the benefits vary across regulatory contexts, particularly between EU and non-EU banks (Cantero-Saiz et al., 2024). A second mechanism emerges around competition: an increase in competition among banks is associated with lower ESG controversies, suggesting a reputational discipline effect (Cicchiello et al., 2023). Governance practices primarily influence customer perceptions and retention, while environmental and social initiatives also contribute, along with the governance dimensions (Chow & Ho, 2024). This cluster further links ESG to financial stability and vulnerability to environmental risks (Curcio et al., 2024; Korzeb, Karkowska, et al., 2024) and frames improvement in ESG scores as a response to competition and reputational risk (Wang, 2023).

Two salient tensions in SB arise in this cluster. First is the competition—controversy relationship, which remains theoretically ambiguous. Korzeb, Niedziółka, et al. (2024) found that with increased competition in banks, there may be more opportunities for banks to portray themselves as SB and engage in greenwashing and other ESG controversies. Such research becomes increasingly pertinent, especially in emerging and developing economies. Second, the counter-cyclical lending by high ESG-scoring banks (Abdelsalam et al., 2023) raises an important question during crisis regimes, as the relationship is not tested for COVID-19 and post-pandemic periods across geographies.

This cluster also discusses strategic ESG complications. ESG scores improved more by banks with lower profitability and leverage, enabling them to enhance their reputations and control risks, demonstrating that ESG performance is a strategic and reputational tool in competitive financial markets. Furthermore, industry-specific ESG applications underscore the complex risk mitigation measures required for sustainable lending (Palmieri et al., 2023). Islamic financing exhibits robust positive relationships with ESG performance, particularly in advancing the social aspects of sustainability (Boudawara et al., 2023; Kashi et al., 2024; Paltrinieri et al., 2019). In the context of greenwashing, Huang et al. (2024) empirically find that banks with low ESG performance lend to companies with better ESG performance, offering significantly lower loan spreads, longer loan maturities, fewer general covenants and fewer collateral requirements to improve the former’s ESG reputation. ESG disclosures reveal intricate, nonlinear effects on banks’ diversification strategies, necessitating context-specific ESG frameworks tailored to diverse economies (Saif-Alyousf et al., 2023).

Future research should decompose ESG into pillar-specific pathways and test moderators such as regulatory framework, bank type and market structure. They should test the association between banks’ ESG scores and the individual ESG pillars with the different components of the CAMELS rating system. The strength and direction of these relationships can further be examined during periods of crises and systemic risk.

Sustainable, Ethical and Green Banking

This cluster (blue) centres on SB’s environmental pillar (GB), its governance pillar (EB) and the authenticity of sustainability reporting. Aizawa and Yang’s (2010) paper on China’s state-driven strategy for GB exemplifies the green credit policy. Their study contrasts with the voluntary disclosures dominated by banks globally, highlighting how regulations can shape credit allocation. Reporting-focused studies show a transition from symbolic to authentic reporting when regulatory compliance and social performance are salient (Khan et al., 2020). Islamic banking research adds a governance-rooted authenticity framework. Jan et al. (2021) proposed a framework linking Islamic corporate governance and sustainability performance. The study emphasises that authenticity in sustainability reporting for Islamic banks and institutions is deeply rooted in the genuine implementation of Shariah governance, paired with transparent ownership structures. Advances in SB performance measurement tools, such as the multi-criteria model by Raut et al. (2017) and an integrative framework of SB literature mapping by Aracil et al. (2021), reinforce a shift from symbolic social responsibility and customer-centric corporate social responsibility to more authentic reporting of banks and the necessary regulatory frameworks.

The cluster exposes an intent–impact gap in SB, much of which is measured in disengagement rather than measurable outcomes. This leaves space for investigating situations where ethical washing and greenwashing may arise. Almaqtari (2024) and Serdarušić et al. (2024) confirm the role of technology in creating both an opportunity and a risk. Fintech and IT governance can improve sustainability performance, and fintech adoption can augment the scale of green credit (He et al., 2024). The future can examine the role of blockchain and AI in driving green fintech and developing risk management models for digital financial ecosystems, as well as the comparative studies between digitally mature and developing economies. Measuring the impact of banks’ sustainability adoption should move beyond mere input-output-based analyses to focus more on the intent and investigate the role of EB in advancing financial inclusion, particularly for the underbanked, as well as customers’ understanding, trust and attitudes towards adopting SB, GB and EB.

Corporate Sustainability

The studies in the fourth cluster (purple) treat sustainability as a broader corporate strategy intertwined with innovation (Forcadell et al., 2019) and risk-related fundamentals such as capital adequacy and non-performing loans in shaping sustainability more than growth proxies (Lin & Chang, 2019). Weber and Chowdury (2020) found that banks’ engagement in sustainable practices improves their financial performance; however, the benefits are greater for larger banks than for smaller banks. Furthermore, this cluster collectively analyses sustainability in banking from various perspectives, including customer loyalty, macro-financial performance, behavioural dynamics and alignment with the SDGs. Igbudu et al. (2018) examine the impact of sustainable practices on customer loyalty through corporate image in North Cyprus, employing structural equation modelling on survey data. Their findings align with those of Stauropoulou et al. (2023), who also connect SDG-aligned banking to loyalty in Greece, while distinguishing among social, economic and environmental impacts, noting that environmental factors are less influential.

A key point to consider is whether sustainability is a proactive measure or a reactive legitimacy response, particularly in weaker institutional frameworks. Another concern centres on diversification; while it may improve stability and risk-adjusted performance, overdiversification of the banking product and service portfolio can increase interconnectedness and may make banks more vulnerable to systemic risks (Karkowska, 2019). This may undermine long-run sustainability objectives, and evidence is geographically skewed towards Western countries, limiting generalisation. Future research should model sustainability as a capability—trade off with reputational risks, innovation, financial performance, testing mediation mechanisms (corporate image) and moderators (bank types, geographies, rigour of regulatory framework, digital maturity).

Financial Stability

This cluster (yellow) addresses systematic risks (including risks caused by a single event), as well as unsystematic risks, such as default risks and the resilience of sustainable banks. Scholtens and Klooster (2019) found that banks with higher sustainability scores exhibit a reduced risk of default. ESG performance markedly diminishes systemic and default risks, although effects differ among financial sectors; banks exhibit vulnerability to environmental risks (Curcio et al., 2024; Korzeb, Karkowska, et al., 2024). Firm-specific unique risks, especially at elevated risk levels, diminish with enhanced ESG scores, highlighting governance and environmental aspects (Izcan & Bektas, 2022). Seyfang and Gilbert-Squires (2018) identified systemic inertia, and Olmo et al. (2021) provide a quantification of financial benefits. Their findings demonstrate that sustainability offers distinct advantages, yet is limited by contextual factors, including customer awareness, institutional ecosystems and policy frameworks, all of which are influential elements. Significantly, ESG effects may operate through improved fundamentals, regulatory alignment, reputational capital or disclosure signalling. These channels may vary across crisis regimes. Islamic banking studies challenge the standard agency expectations, showcasing non-linearity in the relationship between CSR, financial stability and effects of board activity on sustainability performance (Kashi et al., 2024; Khémiri & Alsulami, 2023). Region-specific governance configuration and sustainability committees appear consequential, suggesting that the ‘one size fits all’ governance assumption may not hold (Mehreen et al., 2020).

Future researchers can investigate the macro-level validation of the adoption of sustainable practices by banks in reducing systematic and unsystematic risks in banks of emerging markets, which are more prone to systemic and default risks. Research can be undertaken to conduct a longitudinal stress test of ESG and sustainability practices adopted by banks, measuring the level of financial stability and resilience that these practices bring to banks. Future studies can also assess the effectiveness of governance in sustainable banks under stress scenarios and compare the effectiveness of ESG adoption between public and private banks.

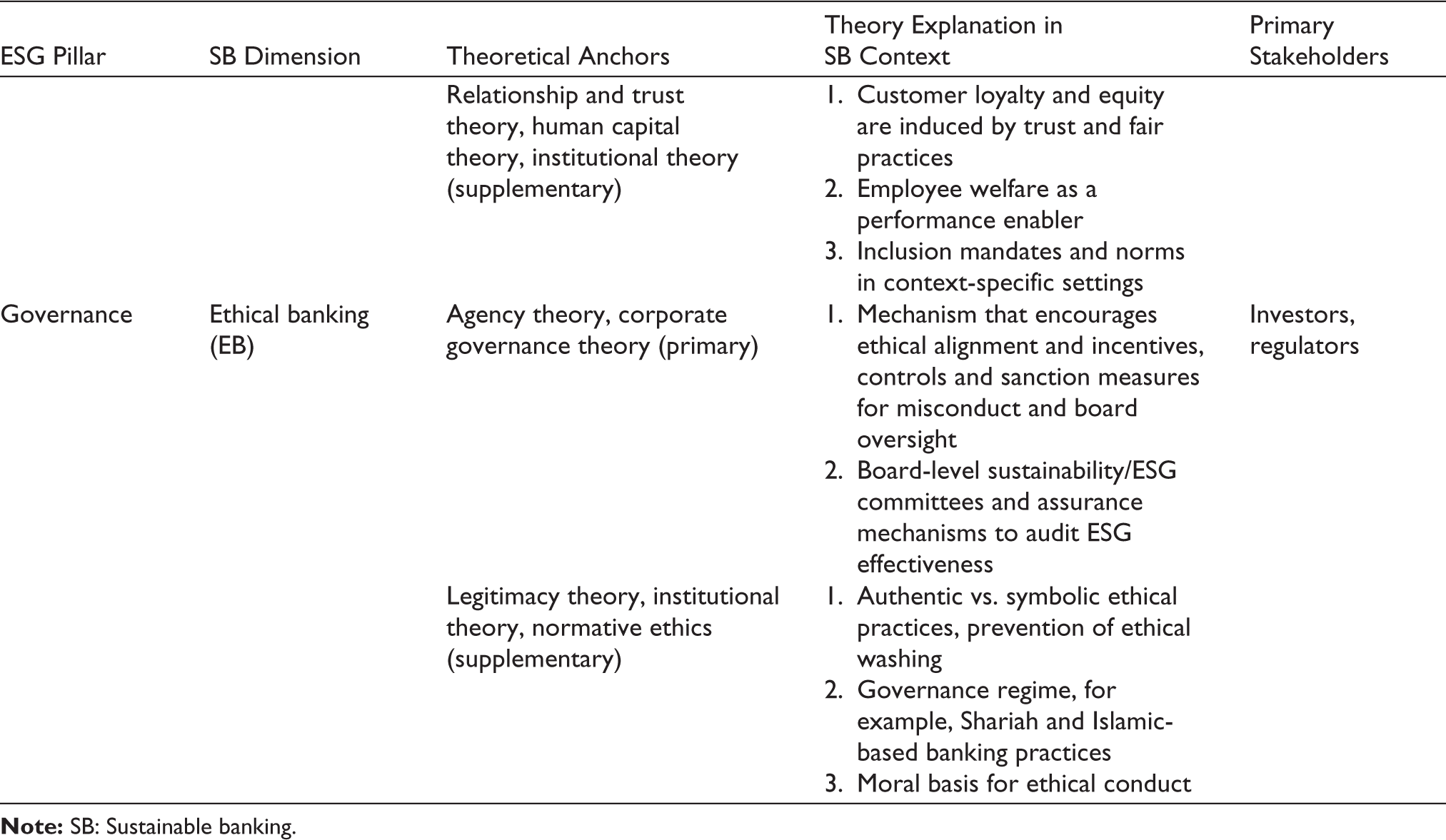

Proposed Conceptual Framework for SB Research

The framework displays that drivers are categorised by the ESG pillars, including GB (E), socially responsible and inclusive banking (S), and EB (G) to reduce definitional ambiguity and enable pillar-specific theorising and measurement. Figure 1 consolidates fragmented evidence on SB into a testable causal structure, specifying drivers → mechanisms → mediators → outcomes, with moderators that explain reported SB effects differ across contexts. The framework is anchored in the clustering (Figure 3) and interpretive synthesis (Table 4). This highlights recurring gaps in SB research regarding definitions, measurements, comparability across bank types and regulatory environments (Aracil et al., 2021; González-Ruiz et al., 2024; Rajawat & Mahajan, 2024). The framework’s drivers capture the institutional and market forces influencing banks’ adoption of SB practices, such as responsible banking principles and sustainability reporting expectations, competitive pressure, stakeholder scrutiny and crisis-linked risk salience. These drivers translate into SB only through mechanisms, that is, operational changes in (a) credit allocation and sustainable lending (green credit and environmental screening); (b) governance and controls (board oversight, ESG committees and assurance); and (c) measurement and disclosure systems. The mechanism logic is supported by evidence that policy instruments such as green credit directives can reshape lending behaviour (Aizawa & Yang, 2010), that the credibility of sustainability reporting hinges on whether practices are substantive rather than symbolic (Aracil et al., 2021; Khan et al., 2020) and that governance strength is central to how ESG translates into banking outcomes such as cost of funding and asset quality (Agnese & Giacomini, 2022; Cantero-Saiz et al., 2024).

The relationship between the drivers, mechanisms and outcomes is strengthened or weakened by the moderators (acting as boundary conditions), including regions (developed vs. emerging economies), bank types (conventional banks vs. digital banks), the institutional context, as well as the strength of the regulator’s enforcement. ESG-asset quality linkages differ across jurisdictions (Cantero-Saiz et al., 2024), and governance configurations (including Shariah governance) influence ESG performance and stability in Islamic banks (Boudawara et al., 2023; Kashi et al., 2024; Paltrinieri et al., 2019). Furthermore, through mediators such as transmission channels, SB mechanisms affect outcomes, including reputational capital and disclosure credibility (which determine whether sustainability signals are rewarded or discounted), customer trust and loyalty and risk-governance capability (which influences whether ESG integration reduces bank risk). These mediators are in line with prior findings that SB can improve customer loyalty through corporate image (Igbudu et al., 2018) and reduce operational risk via ESG-linked reputation effects (Galletta et al., 2022). Furthermore, the outcomes are multi-layered: (a) financial/market outcomes (profitability, funding costs); (b) risk/stability outcomes (default/systemic risk); and (c) ESG/SDG-linked societal outcomes. SB studies corroborate these outcome pathways, highlighting SB associations with risk mitigations (Curcio et al., 2024; Izcan & Bektas, 2022; Scholtens & Klooster, 2019) and SDG-aligned inclusion effects in institutional environments (Úbeda et al., 2022, 2023). The framework illustrates that successful SB implementation leads to multidimensional outcomes that benefit both the institution and the society at large. These activities ensure alignment with global SDGs, specifically addressing poverty, reduction in inequalities, climate action and responsible consumption and production.

Conclusion and Implications

This study is distinct and provides a comprehensive synthesis of the literature in the domain of SB using the SPAR-4 protocol by integrating bibliometric essentials, including annual publication trends, influential authors and journals, most-cited research papers, country citations and productivity, keyword co-occurrence analysis and content analysis. The analysis revealed scholar attraction in terms of the increasing trend of research output in the domain. The keyword co-occurrence analysis identified five key themes: banks and sustainable performance; sustainability and ESG; SB, GB and EB; corporate sustainability and financial stability. Empirical evidence consistently supports the benefits of ESG adoption for sustainable banks, including risk-adjusted returns, reduced operational losses and decreased systematic and unsystematic risks. SB has also strengthened customer loyalty and built reputational capital. However, persistent gaps remain in the literature, notably the absence of a universal measurement framework for sustainability, ambiguity in the definition of SB, GB and EB, and the limited availability of longitudinal and comparative studies between developed and emerging nations. There is an insufficient integration of technological innovations, such as AI, fintech and blockchain, into sustainability assessment and enforcement. The evolving frontiers should prioritise standardised ESG metrics, impact the assessment of separate contributions of the three ESG pillars in stakeholder studies, financial stability measurement and reputation building.

This review delivers several implications for the literature on SB. Policymakers should consider standardising SB measurement frameworks while enhancing the disclosure regime across banks and financial institutions. This may promote essential uniformity and thereby enhance the asymmetrical impact on performance metrics. While banks may use AI/NLP sustainability analytics with blockchain technology to enhance sustainability measurement and reporting, policymakers can use blockchain along with multi-criteria decision analysis and directional distance models (Nepomuceno et al., 2019) to identify anomalies and better enforce sustainability standards. To strengthen the transparency and resilience of digital financial ecosystems, the bank should consider integrating fintech and AI into its risk management systems. To enhance customer attitudes, establish trust and promote financial inclusion, they should shift their focus from input–output sustainability metrics to customer intent and ethical practices. To create a pathway that aligns innovation with social impact, industry practitioners should focus on a dual approach that integrates technological resilience with ethical intent. This approach has the potential to improve customer trust, strengthen the digital finance ecosystem, reduce reputational risks and increase positive views of EB, green banking and SB. Moreover, the proposed model provides managers with an organised way to identify areas where sustainability initiatives are ineffective, thereby ensuring their genuine implementation. Managers can also examine the drivers, mechanisms and results of sustainability initiatives. This can help an organisation look more trustworthy and ensure that its practices are in line with stakeholders’ expectations.

Despite its substantial contributions to the existing body of literature prior to its execution, this study may possess certain limitations, including the constraints of bibliometric methods, which encompass the selection of the research period, the extraction of data from a singular database and the potential exclusion of some publications from the analysis.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix A

| Cluster Name | Dominant Keywords (Figure 4 and Table 4) | No. of Papers (N = 258) | Content Analysis (Total n = 50) | Count |

| 1. Banks and sustainable performance (Red) | Bank performance; sustainability performance; SDGs; green finance, environmental performance | 68 | Mendez and Houghton (2020); Úbeda et al. (2023); |

11 |

| 2. ESG, CSR and governance in SB (green) | ESG; CSR; governance; ESG controversies; sustainable lending | 72 | Agnese and Giacomini (2022); Galletta et al. (2022); Cantero-Saiz et al. (2024); Palmieri et al. (2023); Chow and Ho (2024); Paltrinieri et al. (2019); Boudawara et al. (2023); |

11 |

| 3. Sustainable, ethical and green banking (blue) | Green banking; ethical banking; sustainable finance; regulation; fintech/IT | 45 | Aldaarmi (2024); Almaqtari (2024); He et al. (2024); Serdarušic´ et al. (2024); Aizawa and Yang (2010); Raut et al. (2017); Khan et al. (2020); |

13 |

| 4. Corporate sustainability (purple) | Corporate sustainability; innovation; customer loyalty; reputation; diversification | 35 | Igbudu et al. (2018); Adeabah et al. (2022); Stauropoulou et al. (2023); Karkowska (2019); |

7 |

| 5. Financial stability (yellow) | financial stability; bank risk; default risk; systemic risk; resilience | 38 | Scholtens and Klooster (2019); Curcio et al. (2024); Izcan and Bektas (2022); Korzeb, Karkowska et al. (2024); Seyfang and Gilbert-Squires (2019); Olmo et al. (2021); Donnir and Tornyeva (2024); Gehrig et al. (2023); Mehreen et al. (2020); Khémiri and Alsulami (2023); |

11 |