Abstract

This study examines the factors influencing the sustainable reporting practices of commercial banks, focusing on green loan disclosures. Employing balanced panel data from 26 banks over 12 years (2012–2023), the binary logistic regression method is used to analyze sustainability disclosure practices, with validation provided by the system’s generalized method of moments estimation to address potential endogeneity. The findings reveal that a bank's asset size positively influences green lending disclosures, while the market value ratio and non-performing assets exert a negative impact. These results suggest that larger banks with lower market valuations and higher levels of bad loans are more inclined to disclose their green lending activities. The study enriches sustainability reporting literature by identifying key drivers of green lending disclosures in India, offering valuable insights for policymakers and stakeholders. It also provides a novel contribution to the under-explored area of green loan disclosures, particularly in the context of developing countries. By focusing on the Indian banking industry, the study fills a critical gap in the existing body of knowledge and sheds light on the disclosure practices related to green loans.

Introduction

Green loans, a concept that has evolved due to the increasing focus on environmental, social, and governance (ESG) principles and rising energy costs, are now used to finance businesses aiming to speed up their decarbonization efforts (Stefanie, 2023). Green loans as defined by the World Bank (2021), are loans that provide funding to environmentally impactful projects and substantially advance environmental objectives. Their increasing prevalence underscores the financial sector’s heightened acknowledgement of environmental sustainability. Introduced by Sainsbury’s in 2014, green loans adhere to the green loan principles (GLP) framework, established by the Loan Market Association and the Asia Pacific Loan Market Association in 2018. The GLP framework ensures the effective use of green loans for their intended environmental purposes including four key components: fund allocation to green projects, impact evaluation, benefit management, and transparent reporting (Reuters, 2024). However, despite the green loan market’s surge from $3 million in 2014 to $1.98 billion in 2023, the data for 2024 indicate a contraction to $498 million, suggesting potential market adjustments or changing investor priorities (Green Finance Portal, 2024). The Indian banking sector has played a pivotal role in driving the country’s economic development and is now embracing green lending practices, signaling a shift towards sustainable development (ET EnergyWorld, 2021). India’s sustainable future hinges on a financial shift towards green finance, which supports eco-friendly projects, fosters sustainable development, and shrinks the nation’s carbon footprint to reach net-zero goals (Aggarwal, 2023). Achieving these ambitious environmental goals depends on significant investments, and here’s where banks can be game-changers by enabling the flow of capital via green loans, paving the way for a more sustainable India.

Despite the significance of green finance, financial regulators of several countries (except China) do not have any policy intervention to mobilize funds for green projects unlike for other areas such as “priority sector lending.” Thus, green lending and its related disclosures are largely voluntary and depend upon the managerial discretion of the banks. Provided the significance of green lending to achieve the “net-zero” targets, it is paramount for various banks to report their green advancing practices for better evaluation and policy making for regulators. Besides, disclosures of non-financial performance data such as environmental impact augment the investors’ decision-making by diluting the information asymmetry among managers and investors (Chaudhry, 2022). Because of voluntary reporting, the research literature on green loan disclosures mostly remains constrained due to the unavailability of data and distinctive regulatory framework. Contrary to sustainability reporting research of non-financial companies, the number of studies focusing on green loan disclosures is scarce. A few studies have explored the green lending behavior of banks (Hoque et al., 2024; Zhou et al., 2020), however, these studies have primarily focused on the determinants of green lending performance instead of disclosures. Yet, as mentioned earlier, the disclosure of green lending is equally important for stakeholders and policymakers. It is important to note here that banks are gradually transitioning to disclose green lending data but the proportion is still very minimal (Hoque et al., 2024). To encourage bank-level green loan reporting, regulators must understand the present behavior of banks towards such disclosures to build and implement strategic interventions. The discussion poses a critical research question what factors shape the green loan reporting of the banking firms in the absence of any regulatory pressure? By answering this question, this study will provide crucial foundations for future policymaking. The past studies on the determinants of banks’ sustainability reporting have concentrated on the disclosures of direct actions such as emission reduction and clean energy adoption (Birindelli & Palea, 2023; Khan et al., 2021). However, there exists a significant research gap about the disclosures of banks’ contribution to sustainable development through an indirect channel by financing green projects. The current research enhances the extant sustainability literature by examining the factors of green lending disclosures within banking industry.

Considering dearth of conclusive research, this study contributes to the literature in several ways. First, the study investigates the financial as well as bank-based factors impacting the disclosure of green loans. Based on the review of past literature majority of these studies have ignored the sustainability disclosure behavior of finance companies and largely focused on non-financial organizations (Chen Tia et al., 2024; Cho et al., 2024; Devi & y, 2024; Zamil et al., 2023). Second, the current research is based on a sample of commercial banks in India, one of the largest emerging economies in the globe. India is the third largest emitter of CO2 (Niti Aayog, 2023) after China and the USA and therefore the regulators are actively striving to reduce the carbon footprint of the nation. To achieve carbon neutrality, the banking sector can play a pivotal role by channeling necessary financial resources in the appropriate direction. Therefore, it is imperative to understanding the present state of green lending for formulating a target-based regulatory framework and monitoring the green financing performance of banks. Third, as green lending disclosures are not compulsory in India, stakeholders have to rely upon voluntary reporting which creates information asymmetry and agency conflicts. Thus, by analyzing the determinants, the study provides a ground-breaking understanding of the bank characteristics that shape green lending disclosure to policymakers for building suitable disclosure regulations. Fourth, the current research builds upon the conceptual framework of stakeholder (Freeman, 1984) and legitimacy theory (Suchman, 1995) and empirically investigates the applicability of these theories in the context of banking companies operating in the emerging economy context. Therefore, the study widens the scope of stakeholder and legitimacy theory in describing the sustainability reporting behavior of banking firms. Finally, the study adopts a binary logistic regression approach as against the panel data method due to the dichotomous measurement of the dependent variable. Further, the study also controls for potential endogeneity issues using the system generalized method of moments (GMM) approach.

Research Objectives

This study proposes the following research objectives (ROs) to understand the factors that affect the banks’ decision to disclose their green lending.

RO1: To understand the green loan disclosure practices among the banking firms operating in one of the largest emerging economies, that is, India

RO2: To analyze the universal financial factors (such as size, profitability, and valuation among others) determining the prospect of green loan disclosures by banks.

RO3: To analyze the bank-specific factors (such as capital adequacy and asset quality among others) influencing the likelihood of green loan disclosures by banks.

The composition of this article is as follows. The second section encompasses the theoretical and empirical literature review followed by the third section, which delineates the research methodology adopted. The fourth section offers an in-depth analysis of the data collected and a discussion of the results. Finally, the fifth section concludes the article by discussing the implications and limitations of the study.

Literature Review

Theoretical Literature Review

Stakeholders’ demands for transparency and accountability in the financial sector drive increased focus on non-financial disclosures, particularly within green loan products (Maama, 2020). This emphasis on environmental and social policies and their associated risk management strategies reflects a broader societal interest in responsible banking practices. By integrating such disclosures into their reporting, banks can enhance their legitimacy and reputation with investors and the public (Fadilah et al., 2022). This improved reputation can translate into positive market evaluations and potentially lower equity financing costs (Liu, 2020). In essence, robust non-financial disclosure practices within green loans are seen as a strategic tool for enhancing bank performance.

Aligning with stakeholder concerns and promoting transparency, the rise of integrated reporting offers a valuable tool for banks, particularly those issuing green loans (Buallay & Alhalwachi, 2022). This approach goes beyond traditional financial reporting by incorporating non-financial metrics, such as green loan volume, providing a more holistic view of a bank’s strategy and potential for future value creation. The integrated reporting approach is grounded in stakeholder theory, prioritizing transparency and accountability to diverse stakeholders, including investors, customers, and regulators. By disclosing green loan information, banks demonstrate their commitment to environmental sustainability, a key concern for stakeholders (Maama, 2020). Furthermore, such disclosures can be interpreted through the lens of Signaling Theory (Zhou et al., 2020), by making this information readily available, banks signal their dedication to environmental practices, reducing information asymmetry and potentially attracting stakeholders who prioritize sustainable investments. As stakeholders increasingly seek investments that align with their values, integrated reporting with a focus on green loans positions banks to capitalize on this growing market trend.

Transparency in green loan disclosure can address the principal–agent problem in banking, ensuring that management prioritizes sustainability practices and aligns with the interests of environmentally conscious owners (Girón et al., 2021). Disclosure serves a dual purpose: it fosters accountability to stakeholders and attracts capital from socially responsible investors (Buallay & Alhalwachi, 2022). Voluntary dissemination of non-financial information, such as green loans, enhances a bank’s legitimacy and demonstrates its commitment to sustainability principles, significantly shaping stakeholders’ perceptions (Suchman, 1995). Banks that disclose such information not only foster transparency but also fortify the sustainability narrative and bolster environmental stewardship within the banking sector (Elkington & Fennell, 1998), thereby promoting a more comprehensive and sustainable approach to corporate responsibility and stakeholder trust.

Review of Empirical Studies and Hypothesis Development

This section reviews empirical studies on the firm characteristics and their effect on sustainable reporting. In line with the study objectives, the section has been subdivided into common financial and banking sector-specific determinants. Due to limited research on green loan reporting, the study reviewed past research on the broad area of sustainability disclosures of financial and non-financial companies to understand the association between the dependent and explanatory variables. This study aims to analyze the bank-specific determinants of green lending disclosures. Consequently, the selected factors depict the cross-sectional differences among banks. Further, the research hypotheses are framed in line with the ROs and the direction (positive/negative) of the effect of the said factor has been explained through extant research. Finally, as this study measures green loan reporting using binary variables, each hypothesis proposes the association between the explanatory factor and the likelihood of green loan disclosures.

Firm Size

Firm size depicts the number of resources deployed by the firm and is suggested to exert a positive influence on corporate voluntary reporting level, as the increased size leads to increased public exposure and scrutiny, and concern for legitimacy due to society’s traditional expectations (Zamil et al., 2023). As reported by Fadilah et al. (2022) and Tauringana (2021), large firms postulate a higher probability of disclosing sustainability information to maintain stakeholder trust levels. Contrarily, Girón et al. (2021) observed a negative association between firm size and sustainability reporting disclosure, suggesting that as a company’s size increases, the sustainability reporting level decreases. This counterintuitive finding challenges the conventional wisdom that larger firms would be more diligent in their sustainability disclosures. Following the bidirectional influence of firm size and RO2, the following hypothesis is formulated.

H1: There is a significant impact of firm size on the probability of a bank’s voluntary green loan disclosure.

Market Value Ratio

As postulated by stakeholder theory (Freeman, 1984), shareholders integrate the ESG factors into their investment decisions. The market value of banks can impact their non-financial disclosure practices, as suggested by the findings of Al-Shatnawi and Al-Dalabih (2019), where commercial banks with higher market values were more likely to engage in transparent non-financial reporting (Cho et al., 2024). This finding aligns with the work of Veltri et al. (2020), who demonstrated that higher market value is associated with increased non-financial disclosure. This suggests that market confidence may act as a catalyst for greater transparency, as companies with higher valuations are more likely to engage in comprehensive disclosure practices. Conversely, Rehman et al. (2020) showed that a high market-to-book (M/B) ratio reduces the level of sustainability disclosure, arguing that firms with high market value may disclose less to avoid revealing proprietary information. After the contradictory outcomes and RO2, the study hypothesized as follows.

H2: There is a significant impact of the market-to-book value ratio on the probability of a bank’s voluntary green loan disclosure.

Sales Growth

Tran and Pham (2024) found that firms with strong sales performance tend to increase their ESG disclosures, especially during market turmoil. This suggests that high-performing companies invest in and report on ESG initiatives to maintain competitiveness in challenging market conditions. Similarly, Nyame-Asiamah and Ghulam (2019) highlight the significant impact of sales growth on environmental disclosure. These findings imply that increased consumer demand and positive financial outcomes can drive companies to adopt more transparent ESG practices. In addition to the previous findings, some studies have identified a affirmative influence of sales growth on ESG disclosure (Kaiser, 2019), while others have reported negative associations (Devi & y, 2024). This suggests that sales growth does not consistently or significantly influence ESG disclosure, indicating that the relationship may not always be straightforward or positive. Given the inconclusive results as well as RO2, it can be hypothesized that.

H3: There is a significant impact of sales growth on the prospect of the bank’s voluntary green loan disclosure.

Profitability

A spectrum of findings emerges in the academic discourse on the relationship between profitability and risk disclosure. On one hand, authors such as Alshirah et al. (2020) argue that there is a positive correlation, suggesting that profitable firms are more inclined to disclose risk information, possibly to demonstrate their financial health and effective risk management strategies. Conversely, ChenTia et al. (2023) present a counter-narrative, identifying a negative impact where profitable firms may disclose less risk information to avoid drawing attention to potential vulnerabilities. Consistent with prior findings, Al-Dubai and Abdelhalim (2021) demonstrated an inverse relationship between firm performance, when gauged by profitability metrics, and the extent of risk disclosure. This suggests that heightened profitability does not necessarily translate into enhanced transparency in risk reporting. Provided the discussion and RO2, the following hypothesis is formulated.

H4: There is a significant impact of profitability on the likelihood bank’s voluntary green loan disclosure.

Advances-to-Deposit Ratio

The advances-to-deposit ratio (ADR) reflects the balance between a bank’s lending activities and the deposits it receives from customers (Sari et al., 2023). Research by Citraningtyas et al. (2024), suggests that companies with strong liquidity, indicated by a high ADR, tend to be more forthcoming with disclosures. This aligns with stakeholder theory, which emphasizes responsible resource management by companies to meet stakeholder needs and ultimately enhance their reputation through sustainability reporting. Contrarily, Embuningtiyas et al. (2020) found that the ADR does not significantly affect the disclosure of sustainability reporting. Supporting the previous findings, Sari et al. (2023) also found no significant influence of liquidity on the disclosure of sustainable reports, implying that a higher ADR does not necessarily lead to increased sustainability reporting. Thus, following the RO3, the study formulates the following hypothesis:

H5: The ADR has a significant impact on the probability of a bank’s voluntary green loan disclosure.

Capital Adequacy Ratio

Capital adequacy ratio (CAR) and sustainability reporting have been subjects of extensive research. CAR reveals the appropriateness and sufficiency of a bank’s capital base in meeting its financial obligations (Ajili & Bouri, 2018). Banks with high CARs are more likely to engage in comprehensive sustainability reporting due to their financial stability, which encourages investment in sustainability initiatives, thereby reinforcing their capital position and sustainability (Citraningtyas et al., 2024). Conversely, if the CAR of banks decreases, they may prioritize core financial activities to maintain or improve their capital position, potentially reducing focus and resources for sustainability reporting and initiatives, as suggested by the findings of (Adegbie & Dada, 2019). Following RO3 and the previous discussion, this study proposes the following hypothesis.

H6: There is a significant impact of the CAR on the likelihood of a bank’s voluntary green loan disclosure.

Non-performing Assets

The extant literature has considered asset quality (measured by non-performing loans) as a significant determinant of banks’ sustainability disclosure. For instance, Fell et al. (2021), suggested that companies with lower (higher) asset quality (non-performing assets [NPAs]) may engage more in sustainability reporting as a means to improve their image and transparency. According to Gellidon and Soenarno (2022), banks burdened with higher NPAs should consider enhancing their sustainability reporting, as increased disclosure in this area has been shown to significantly influence non-performing loan ratios in some banking sectors. Conversely, other studies have indicated a negative relationship. Sari et al. (2023) supported this view, stating that financial distress reflected by high NPAs could reduce the resources available for comprehensive sustainability reporting. On the other hand, Embuningtiyas et al. (2020) found that NPAs do not significantly affect the disclosure of sustainability reporting. Therefore, with the increased NPA ratio, despite adopting sustainability practices, banks cannot enhance their long-term financial performance and threaten long-term survival (Fell et al., 2021). In line with the RO3, the study hypothesizes:

H7: The NPAs has a significant impact on the prospect of the bank’s voluntary green loans disclosure (GLN).

Research Methodology

Sampling and Data Collection

This study seeks to uncover the factors influencing the disclosure of GLN by Indian public and private sector banks, utilizing data extracted from their annual reports. Employing the content analysis method, which ensures accurate information retrieval from these reports, the research primarily gathered data from the annual reports of the banks. Relevant search keywords were used to ascertain if these banks extended loans to environmentally friendly sectors, such as renewable energy, residential solar power panels, energy-efficient initiatives, and financing for electric vehicle purchases. The study leveraged the CMIE PROWESS IQ database for the period spanning 2012 to 2023, which furnishes comprehensive financial data. Initially, the sample comprised 32 listed banks. However, to ensure data integrity and consistency, the study applied stringent criteria, including the availability of financial data and continuously being listed for the sample’s study period. From the initial pool, banks lacking complete data during the study period were omitted, leading to a final sample size of 26 Indian banks. The research utilizes a panel data framework covering twelve years (2012–2023), yielding a total of 312 firm-year observations.

Variables of the Study

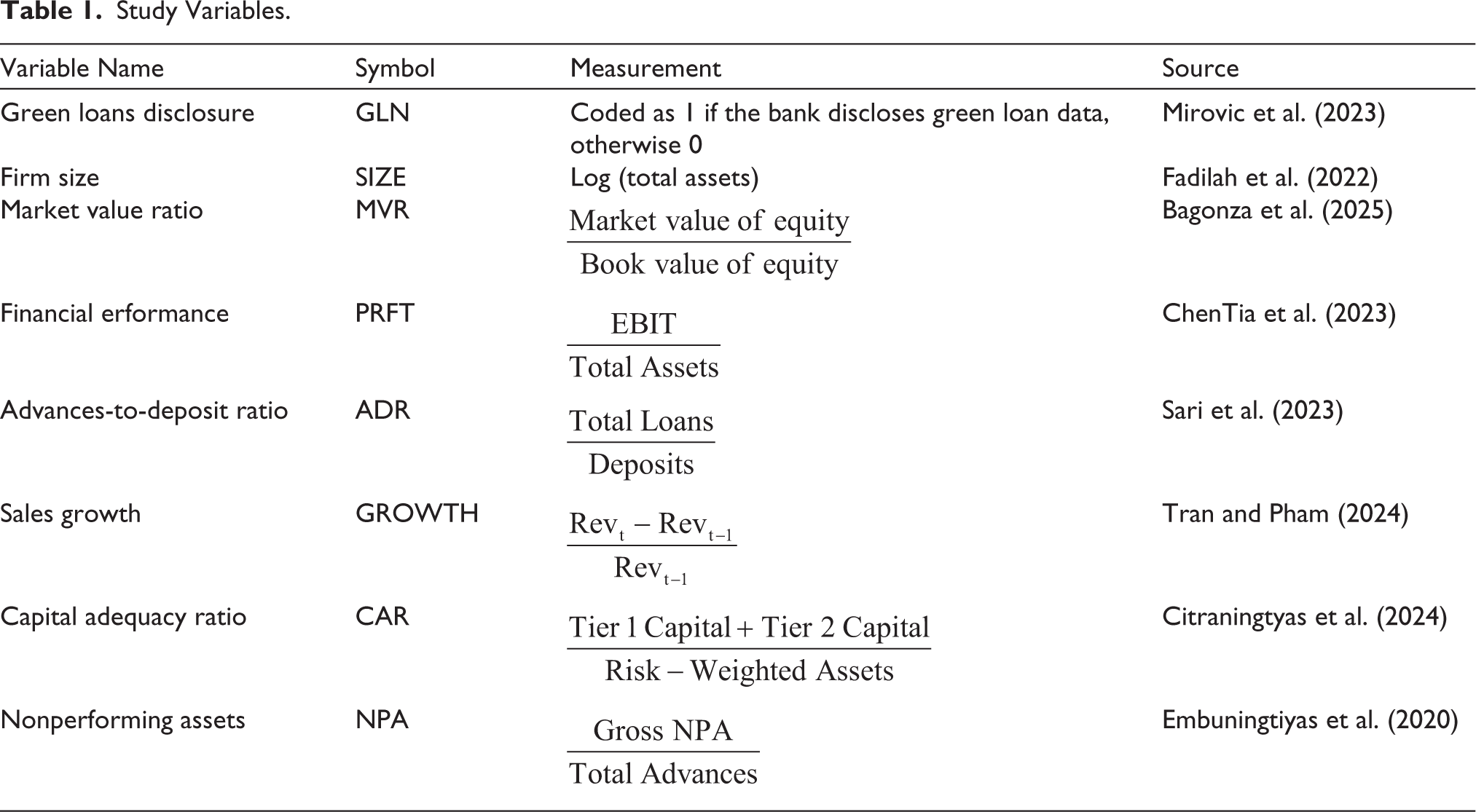

The primary dependent variable in this study is GLN, a metric recently defined by Mirovic et al. (2023). This variable is designed to capture the transparency of financial institutions regarding their environmentally sustainable lending practices. By adopting a binary coding scheme, where 1 indicates that the data on the amount of green loans is disclosed and 0 indicates non-disclosure, we aim to quantify the commitment of these institutions to green financing initiatives. This approach aligns with the growing body of literature that emphasizes the importance of transparency and disclosure in promoting sustainable finance (Flammer, 2021). The GLN variable serves as a proxy for the proactive stance of banks and other lending institutions in supporting projects that mitigate climate change and foster environmental stewardship. To understand what drives banks to disclose information on Green Loans, the study analyses seven independent bank financial variables which are SIZE (Zamil et al., 2023); MBVR (Veltri et al., 2020); GROWTH (Putri & Rahyuda, 2020); PRFT (Al-Dubai & Abdelhalim, 2021); ADR (Embuningtiyas et al., 2020); CAR (Adegbie & Dada, 2019) and NPA (Fell et al., 2021). Firm size can be stated in the total of assets and because of the varying amount of firm assets’ value, the logarithmic transformation has been used to control abnormality (Fadilah et al., 2022). Further, the M/B ratio is calculated by dividing the market price per share by the book value per share. According to Bagonza et al. (2025), MBVR helps gauge market sentiment and whether the firm is overvalued or undervalued. The annual sales growth has been computed as a percentage change in annual revenue (Yeni et al., 2024) which mainly portrays the future financial health and profitability (Putri & Rahyuda, 2020). Profitability, as a financial metric, is the measure of an entity’s ability to generate earnings relative to its revenue, assets, equity, or other financial interests. It is indicative of a company’s financial health and its efficiency in managing its resources (Chen Tia et al., 2024). CAR is computed as the ratio of the sum of Tier 1 and Tier 2 Capital to Risk-Weighted Assets (Citraningtyas et al., 2024). A more detailed breakdown of these variables and measures along with source references are provided in Table 1.

Study Variables.

Regression Model

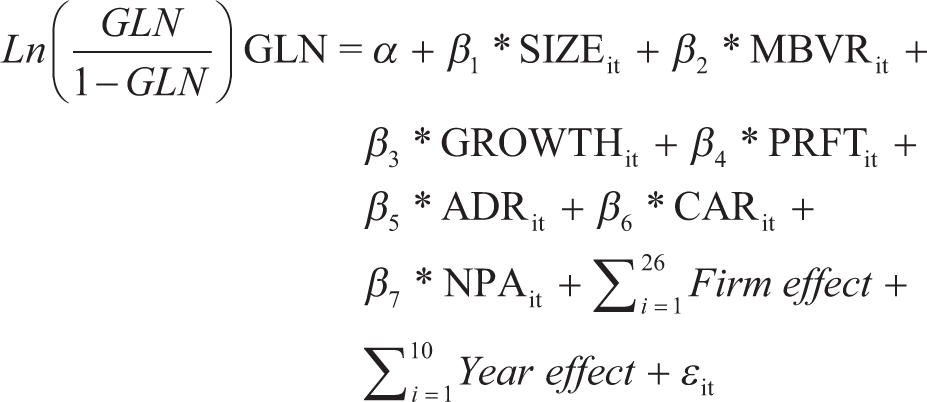

The study integrates a multiple linear regression approach for deriving influential statistics. Green loans are mainly indicated by quantitative values specifically, the amount of credit deployed in the ecological sectors. Thus, their disclosures can be measured through a binary variable as “disclosed” and “not-disclosed.” As the primary dependent variable, that is, green loan disclosure is measured as a binary indicator, the current research adopts a logistic regression model to estimate the results following Desai (2022) and Kumar and Firoz (2019). As against other estimation methods, the logistic regression approach is more suitable for evaluating categorical dependent variables (Saraf & Baser, 2024) due to the computation of the percentage accuracy in classification which depicts the success rate of predicting the likelihood of occurrence. To examine the impact of bank-specific characteristics on the probability of green loan disclosure, this study employed a regression model (Equation 1) using cross-sectional time series data. The model controlled for year and firm effects to account for potential sources of variation:

where GLN = disclosure of green lending; SIZE = asset size of bank; MVR = market value ratio; GROWTH = sales growth; PRFT = profit; NPA = non-performing assets; ADR = advances-to-deposit ratio; CAR = capital adequacy ratio; α = constant; β = parameters; i = cross-section units, and t = year.

Besides the binary logistic model, the study also adopts the system GMM, as noted by Li et al. (2021), to address endogeneity issues like unobserved heterogeneity, simultaneity, and dynamic endogeneity. To ensure result robustness, this study re-estimates Equation (1) using system GMM, mitigating potential endogeneity concerns and enhancing analysis reliability.

Data Analysis

Descriptive Statistics

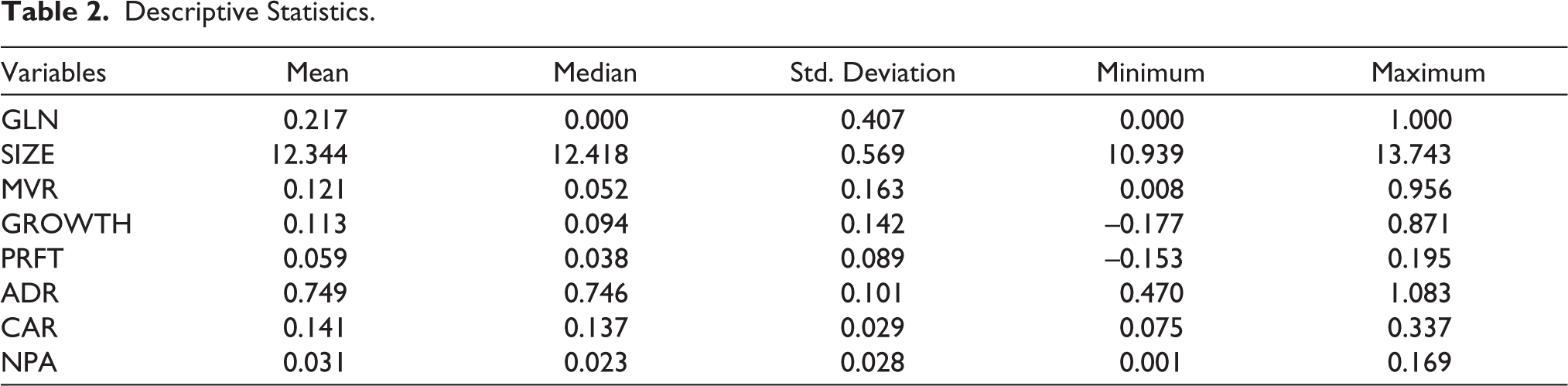

Descriptive statistics are delineated in Table 2 and reveal several key trends in the financial profile of the Indian banks. The banks are similar in terms of their scale of operations, with a mean firm size of approximately 12.34 and a median firm size of 12.41. The market valuation of these banks is significantly below their book value, with an average M/B ratio of 0.12, indicating that the market value is approximately 12% of the book value, suggesting potential undervaluation or financial distress. The data also suggests positive sales growth but a moderate profitability trend, with mean values of 11.30% and 5.90%, respectively, which signals operational resilience and potential recovery from any uncertain financial downturn. Additionally, the average ADR (74.90%) indicates the level of bank lending functions and the banks also maintain sufficient cash to meet the reserve requirements. An average CAR of 14.10% indicates that the banks adhere to regulatory requirements, ensuring they uphold adequate capital levels. The data also shows an average NPAs ratio of 3%, indicating that banks effectively manage loan risks by identifying and addressing potential defaults, thus minimizing losses. These statistics provide valuable insights into the risk profiles and overall performance, highlighting areas such as efficient credit risk management and potential liquidity risks.

Descriptive Statistics.

Correlation Analysis

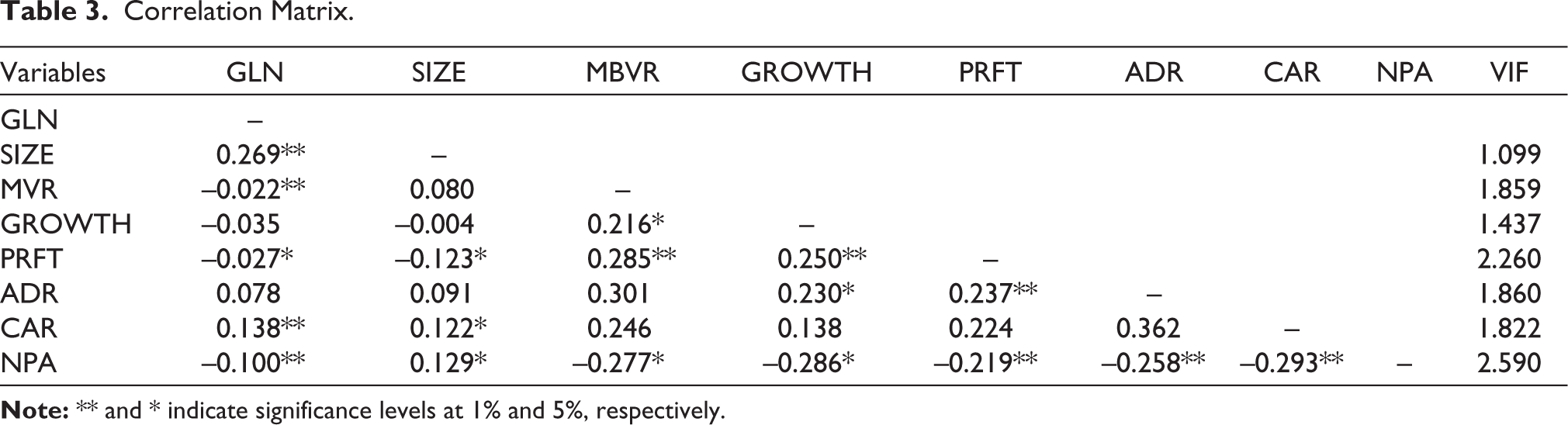

The study explores the correlation between various bank-specific variables and green loan disclosure and the results are summarized in Table 3. Among the selected variables, except sales growth and ADR, all variables are significantly correlated with the GLN practices of the Indian banks. Referring to the direction of relation, asset size (0.269, P < .01) and capital adequacy (0.138, P < .01) are positively related whereas MBVR (–0.022, P < .01), profitability (–0.027, P < .05), and NPA levels (–0.011, P < .01) are negatively associated with GLN. Another important implication of correlation analysis is the detection of multicollinearity. The present research computes the variance inflation factor (VIF) and the results are also included in Table 3. The highest VIF value is 2.590 which is not above the threshold of 10 (Desai, 2022), revealing multicollinearity not influencing the results.

Correlation Matrix.

Results of Binary Logistic Regression Analysis

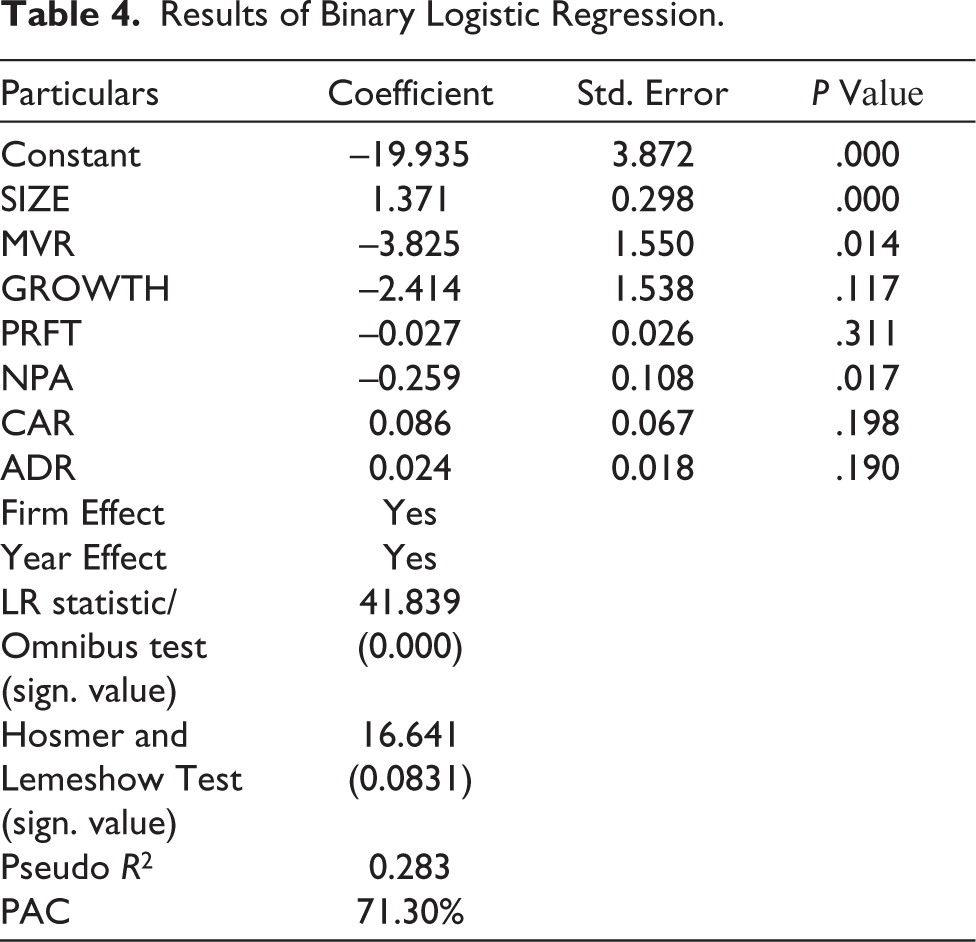

The output of the logistic regression model is reported in Table 4. To test model fit, the Omnibus test, and the Hosmer and Lemeshow, test have been performed and both have prescribed identical conclusions regarding the statistical significance (χ2 = 41.839, P < .01) of the model. Further, the pseudo-R2 value is 0.283 demonstrating that the selected variables can elucidate 28.30% changes in the firm’s probability of disclosing the green loan information. Besides, the percentage accuracy in classification (PAC) is 71.30% which describes the success rate of predicting the likelihood of firms’ disclosure. Among the selected variables, SIZE (β = 1.371; P < .01), MBVR (β = –3.825; P < .05), and NPA (β = –0.259; P < .05) are the significant determinants of disclosure of green lending. Besides, the results of this study contradict the findings of extant literature by negating the significant impact of sales growth, profitability, lending intensity, and capital adequacy on green loan disclosure practices.

Results of Binary Logistic Regression.

The research findings indicate that firm size is positively and significantly associated with the disclosure probability of green loans by selected banks, supporting H1. This aligns with legitimacy theory (Zamil et al., 2023), which suggests that larger firms are more likely to disclose green loans to maintain social legitimacy. The finding is supported by empirical studies as well (Fadilah et al., 2022; Tauringana, 2021), indicating that larger banks, due to their substantial influence on financial system stability and growth, tend to be more responsible, ethical, and transparent. Thus, they are more inclined to voluntarily disclose green loans and other sustainability practices to uphold social legitimacy and meet stakeholder expectations for greater accountability and transparency. Further, the results also indicate a significant negative association between MBVR and the banks’ likelihood to report green loans, leading to the acceptance of H2 in the negative direction. This suggests that banks with elevated market valuations tend to disclose little to no green lending information, contradicting the previous findings by Cho et al. (2024) and Veltri et al. (2020), which suggested that higher market valuations typically correspond to stronger ESG ratings and increased non-financial disclosure. However, the finding of MBVR reducing GLN aligns with the finding by (Rehman et al., 2020), who found high M/B ratio reduces the level of corporate social responsibility (CSR) disclosure, and argue that firms with high market valuations may limit their disclosures to prevent exposing confidential information. Lastly, NPA also has a significant negative association with the banks’ prospect to voluntarily report green loans supporting the H7 (negative). This finding aligns with the findings of Sari et al. (2023) who corroborated the perspective that poor asset quality can hinder comprehensive sustainability reporting. This is likely due to financial distress diverting resources away from sustainability initiatives, as banks prioritize addressing immediate financial concerns. Additionally, Embuningtiyas et al. (2020) found no significant impact of NPAs on sustainability reporting, indicating other factors may influence disclosure. This suggests that the relationship between NPAs and sustainability reporting may be more complex than initially thought, and could be mediated or moderated by other factors.

Furthermore, the analysis found that certain financial variables, specifically GROWTH, PRFT, ADR, and CAR, had no statistically significant impact on the level of green loan disclosures by Indian banks. This suggests that Indian banks’ decisions to disclose green loan information are not driven by these specific financial performance metrics, and instead may be influenced by other factors, such as regulatory pressures, stakeholder expectations, or CSR initiatives.

System GMM Regression: Results

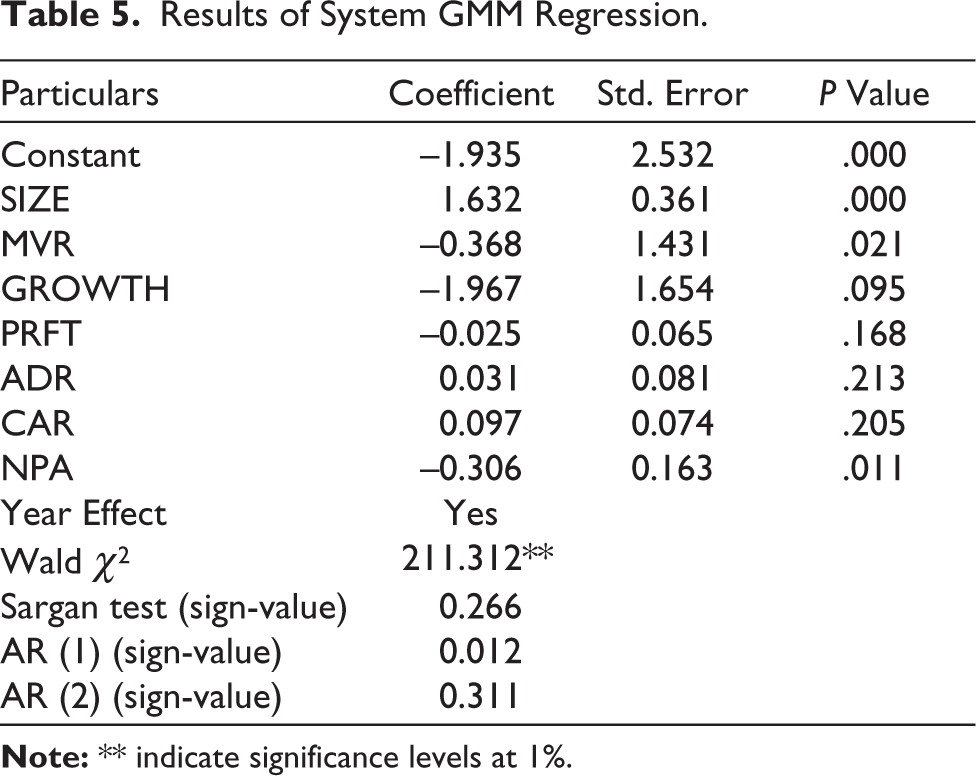

The GMM estimator has gained significant traction in contemporary research as a robust technique for addressing potential endogeneity concerns in panel data models. In the present context, the GLN of a bank also affects the key explanatory variables such as market value and profitability (Cho et al., 2024) which may pose the problem of endogeneity and to be specific, reverse causality. To counteract the bias introduced by endogeneity, this study implements the system GMM approach (Desai, 2022). Table 5 presents a summary of the regression output, utilizing the Wald-χ² statistic for evaluating overall model adequacy, alongside the Sargan test to check for over-identifying restrictions, and the Arellano–Bond test to detect serial correlation. The P value for the Wald χ² test is highly significant (<0.01), whereas the Sargan–Hansen test and AR (2) results are not statistically significant, indicating valid instruments and no serial autocorrelation. Further, analyzing the study variables, the GMM findings corroborate with the earlier results as bank size (β = 1.632; P < .01), market value (β = –0.368; P < .05), and NPA (β = –0.306; P < .05) significantly determine the probability of green loan disclosures. Overall, the results are robust with GMM estimation, and the interpretations remain consistent.

Results of System GMM Regression.

Conclusion and Limitations

Although sustainability disclosure research has received greater attention in general, sustainable lending by financial institutions (especially banks) has been underexplored. The present research addresses this research question through three-fold objectives. First, the current research proposed to understand the present green loan disclosure practices of the banking firms; second, as disclosures related to green lending are voluntary, financial factors and (third) banking industry-specific determinants influence disclosure practices. The findings of this study depicts that Indian banks are yet to adopt green loan disclosures completely as very few of them have reported green lending data. Further, concurrent with ROs, the study concludes that common financial factors such as asset size of bank and market value affect the prospect of the green loan disclosure of banks. Further, among the banking factors, the asset quality measured by the NPA greatly influences the probability of green loan reporting. Alternatively, the study concludes that larger banks with lower market value and lower NPAs demonstrate a greater possibility of disclosing their sustainable financing practices through green lending. Provided the nascent stage of green financing research, the findings of present research will continue to serve an important resource for scholars, especially those in developing nations, who are investigating green lending practices in their banking sectors, thereby further enhancing research in the field of green finance.

Limitations of the Study

Although the present research attempts to provide a comprehensive outlook of the GLN of banks, there are a few research areas that require further exploration. Initially, to improve the scope of future research, it is suggested to broaden the dataset by incorporating non-banking financial institutions. This would offer a more comprehensive view of the financial sector’s endeavors toward environmental sustainability. Second, this study considers the Indian context for research however; future studies may be conducted by integrating the perspective of cross-country analysis to enhance the generalizability. Third, besides financial factors, future research could explore the non-financial drivers such as ownership structure, regulatory pressures, CSR initiatives, and corporate governance to provide a more comprehensive understanding of the motivations behind green loan reporting.

Implications of Study

This study offers several implications for theory and practice. First, the extant literature on the determinants of sustainability reporting is largely focused on the disclosure of the environmental impact of firm activities such as carbon emissions (Desai, 2022; Girón et al., 2021; Tran & Pham, 2024). However, unlike non-financial companies, banks contribute to sustainability by financing ecological projects which call for a separate investigation. Present research fills this gap and enhances the understanding of sustainability reporting of banking companies. Second, as the results portray very low voluntary disclosure of green lending, problems like information asymmetry and agency conflicts get strengthened which may constrain stakeholders to correctly evaluate the bank’s performance. Thus, the regulatory authority must enact a compulsory green finance reporting framework for banks to alleviate the problem of information asymmetry and improve transparency in banking operations. Third, this study is based on binary indicators of GLN due to the absence of a standard measure of reporting framework. Besides mandatory reporting, policymakers must prescribe a format of GLN similar to financial statements to ensure standardized disclosures. Fourth, as this study advocates a significant impact on bank characteristics such as asset size, market value, and NPA, the regulatory disclosure framework should be linked with such characteristics instead of a generic one. The policymaker may start with escaping banks such as smaller ones with higher market value and larger NPAs to implement statutory disclosure of green loans. Finally, as market capitalization negatively affects GLN, investors should be cautious while analyzing the bank’s performance as high-value firms may refrain from sustainability reporting and cover the same through high market value. Besides, policymakers should also prioritize high-value banks to become more responsible and disclose green lending data in the greater interest of shareholders.

Footnotes

Authors’ Contribution

All authors have contributed equally to this article. Siddharth Patel has worked on the conceptualization, review of literature, and discussion. Dr. Rajesh Desai has conducted data analysis and interpretation of results along with implications

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.