Abstract

ASEAN countries face significant environmental challenges contributing to climate change, biodiversity loss, deforestation, and soil degradation. Green banking can help redirect investments toward environmentally friendly activities and discourage deforestation by incentivizing sustainable financing and penalizing unsustainable practices. The article examines the potential benefits of green banking in promoting sustainable financing and discusses the challenges and opportunities for its implementation in ASEAN countries. This article was prepared using a simplified PRISMA method using selected literature and legal materials. The findings suggest that green banking can be vital in promoting sustainable financing and addressing deforestation in ASEAN countries. However, it requires a collaborative effort from stakeholders, including financial institutions, policymakers, and civil society. Importantly, there is a need for legal norms in several ASEAN to be carefully reformulated to support green banking performance.

Introduction

A shocking report on climate change and global financial companies released by the Rainforest Action Network in March 2020 urged hundreds of brands and banks worldwide to make public commitments to stop deforestation and development in peatlands and respond to human rights violations in their supply chains, investment, and financing portfolios over the past decade. The more than 400 companies that are members of the Consumer Goods Forum and several major European and US banks in the Banking Environment Initiative and the Soft Commodities Compact committed to achieving no “net deforestation” by 2020; unfortunately, this result was not achieved. Research by ForestAndFinance.org assessing this failure over the last five years shows that more than USD 48 billion have been provided to operations in forest-risk sectors through loans and guarantees to 100 companies directly linked to deforestation in Southeast Asia (‘Zero-deforestation Commodity Supply Chains by 2020: Are We on Track?’, n.d.).

An October 2019 report by the organization Indonesian Transformation for Justice (TUK Indonesia) examines 64 companies in 17 group structures so far suspected of receiving at least USD 19.2 billion in corporate loans and guarantee facilities since 2015. TUK Indonesia’s investigation shows that of the top ten banks financing corporate groups, Indonesian banks are responsible for the largest share of funding, with a value of USD 3.3 billion, followed by banks from China and Malaysia, which provided funding worth USD 2. 0 billion and US 1.9 billion, respectively (Indonesia, 2020). TUK Indonesia encourages financial service institutions, including banks, to take responsibility for the public funds they collect from customers affected by environmental damage.

These facts are in line with the worsening deforestation statistics. According to data exposure, the forests in which indigenous people live and on which they depend have been eroded or lost for various reasons and to meet a range of interests. Global Forest Watch (2020) reports that in 2010, Cambodia had 7.22 million hectares of natural forest, covering more than 42% of its land area; the country has since lost 140 thousand hectares of natural forest, with more than 57.5 Mt of CO₂ emissions in 2019. A press release by the Association of Southeast Asian Nations (ASEAN) shows that around 2000 square kilometers of forest are lost yearly to illegal logging in Cambodia (Thomas, 2019). Likewise, 37,000 ha of forest in Northern Thailand were destroyed between 2015 and 2020 (FAO, 2020). This tragedy has damaged Thailand’s efforts to convert 40% of its land into green forest, initiated in 1975 (IUCN Asia, 2019).

Other media outlets have reported that the recent landslides that killed hundreds in Vietnam can be directly attributed to deforestation. Much of the deforestation in Vietnam resulted from a hydropower development project; the country lost about 150 thousand hectares of natural forest in 2019. This differs from the situation in 2010, when Vietnam had 14.5 million hectares of natural forest, spanning more than 50% of its land area. Following a pattern similar to other Southeast Asian countries, Malaysia lost 193,000 ha of natural forest in 2019 and ranks sixth among the ten tropical countries that lost primary forest; the survey by Omran and Adile shows that oil palm plantations were the leading cause of deforestation. Malaysia is one of the largest exporters of palm oil, and its consequence requires a spacious area for cultivation. In the Philippines, records from the Ministry of Environment and Natural Resources show that around 47,000 ha of forest cover are lost annually due to a lack of security in wildlife reserve areas and rampant illegal logging. Satellite imagery shows that the Philippine rainforest covers about 90% of the country’s total land area. Over the last few decades, forest cover has been reduced by at least 10%, leaving only a tiny part of the old forest remaining.

Deforestation has also become a significant problem in Indonesia. In the last few decades, there has been severe deforestation of the area’s natural forests, including a decrease in the extent and quality of natural forest cover. According to an analysis by Forest Watch Indonesia, levels of deforestation were high between 2000 and 2017. For instance, between 2009 and 2013, Indonesia lost 1.4 million hectares of natural forest annually, though the rate of loss decreased to 1.1 million. Between 2013 and 2017, the rate of loss increased to 1.4 million hectares per year (Forest Watch Indonesia, 2020).

These findings increase the relevance of banks applying the concept of green banking to manage their financial business. According to Bai (2011), a bank is engaged in green banking when its operational activities are environmentally friendly, responsible, and have environmentally friendly outcomes. By contrast, Bihari Suresh & Pandey, 2015; Sharma & Choubey, 2021 argue that the concept refers to banks whose operations take into account aspects of environmental protection. The consideration of environmental factors in making business decisions is expected to reduce the negative impact of financial institution’s operating activities so that they can assist corporate social responsibility (CSR) efforts and achieve sustainability. Handajani et al. (2019) note that there are various ways to pursue green banking—these can take the form of online and mobile banking, green bank accounts, free loans, electronic banking outlets, and energy savings, all contributing to environmental sustainability programs. Masukujjaman and Aktar (2013) argue that green banking is when an environmentally friendly bank avoids environmental damage so that the Earth becomes a habitable place by providing innovative green banking products (green products) to support green bank initiatives. Understood in this way, banks, as high-visibility entities, tend to express issues of community interest. Their involvement in enhancing a positive social image in society and attracting consumers makes adopting green banking feasible in this context.

In addition to improving environmental banking standards, green banking also affects other business behaviors (Handajani, 2019). Ahmad et al. (2013) examine the issue in developing countries and conduct a factor analysis of private banks in Bangladesh. The authors show that economic factors, policy guidelines, loan requests, stakeholder pressure, environmental interests, and legal factors were the main reasons for banks engaging in green banking to guarantee a sustainable economy. Pariag-Maraye et al. (2017) examine customer perspective on green banking performance in Mauritius and show that customers were positive about the green banking policies practiced, primarily those related to banking products and funding. Mehedi et al. (2017) examines the conditions in developing countries and finds that in Bangladesh, regulatory and organizational pressures dominate green banking practices. Bryson et al. (2016) also demonstrate that commercial bank customers are motivated to use green banking services because of their integrity and concern for environmental insight and collectivism. Various studies have shown that green banking in developing countries such as Bangladesh still needs to be improved and is hindered by the common understanding of bank management, high costs of implementation, and low commitment of top management.

There needs to be greater consideration of corporate governance in the dominant regulatory studies regarding the reasons for adopting green banking and its outcomes in practice. Corporate governance becomes an essential factor in the financial sector when banks face the problem of return risk from shareholders. However, banks must address the social and environmental risks of sustainable business practices to create long-term value. According to Castelo Branco and Lima Rodrigues (2006), the banking industry has a lower environmental impact than other industries (such as manufacturing, energy, and automotive). However, in practice, banks are facilitators of industrial activities, which can lead to deforestation by funding these through credit loans (Castelo Branco & Lima Rodrigues, 2006). Banks face the risk of obtaining returns from shareholders because of the bank’s involvement in green banking activities (Bose et al., 2018). Banks will face pressure from various stakeholders, so corporate governance is needed to balance stakeholder interests. Gupta (2015) identifies various challenges to implementing environmentally sound bank practices. These are related to customer acceptance factors, technology adoption, data protection, human resource capabilities, and costs. Green banking is carried out in various ways by banks without any reporting guidelines but tends to be a process that occurs due to pressure from stakeholders (Gupta, 2015).

These various studies show that green banking goes beyond being a popular trend. In this study, green banking represents a fundamental shift in how financial institutions operate to ensure the long-term sustainability of our environment. A central challenge relates to how green banking addresses deforestation. This paper addresses this issue and presents three main answers. The first is from a legal perspective. This paper demonstrates that numerous countries have made international commitments to environmental preservation, for example, by adopting the Paris Agreement and the Convention on Biological Diversity. Green banking ensures that banks align their operations with these global commitments by refraining from financing projects that contribute to deforestation (‘The role of French banks in global forest destruction,’ n.d.).

At the same time, many countries have domestic laws to safeguard their forests and native lands. By embracing green banking practices, banks can avoid unintentionally funding projects that violate these laws. This article argues that banks that provide funding for projects that lead to deforestation may face substantial legal liabilities (‘Banking on sustainable timber: What role do banks play?’, n.d.), particularly if these activities encroach upon protected areas or indigenous territories. These legal consequences may be accompanied by severe damage to the bank’s reputation. Implementing green banking principles is a form of due diligence, ensuring banks are not complicit in unlawful deforestation activities. In addition, regulatory bodies worldwide are increasingly emphasizing mandatory disclosure of environmental risks. Green banking positions banks favorably in relation to these emerging regulations and ensures their operations remain transparent and ethical (Mir & Bhat, 2022).

The second reason to pursue green banking to avoid deforestation involves scientific reasoning. Scientifically, forests are of paramount importance as carbon sinks, absorbing more carbon dioxide than they release (Brancalion et al., 2018). Reducing the extent of forests exacerbates the effects of greenhouse gases in the atmosphere. Green banking maintains the Earth’s delicate carbon balance by redirecting funds away from deforestation activities. Forests are incredibly diverse ecosystems, teeming with various plant and animal species. Scientific research consistently underscores the importance of biodiversity for the planet’s health and human survival. Within these ecosystems, many species (and their potential benefits, including medicinal applications) remain unexplored. As such, green banking can encourage projects that support and enhance forest biodiversity instead of destroying it. The field of ecology teaches us that Earth’s systems are interconnected. Deforestation can trigger alterations in rainfall patterns, river systems, and even local climates, with impacts that are felt regionally and globally (Lawrence et al., 2022). Through green banking, financial institutions can endorse projects that acknowledge and respect these intricate ecological feedback loops.

The final rationale is environmental. Beyond the immediate concern of trees being cut down, deforestation destroys habitats for numerous species, pushing many to extinction. Green banking can help ensure the survival of these species and preserve ecosystems by prioritizing environmentally conscious projects. Forests are essential to preserving soil health, preventing erosion, and facilitating nutrient recycling. The environmental consequences of deforestation include degradation that leaves land unsuitable for agriculture or any other productive use. Banks adhering to green principles can discourage such detrimental environmental outcomes by supporting sustainable land use projects. Forests are also crucial in the Earth’s water cycle, serving as watersheds and influencing precipitation patterns (Ellison et al., 2017). Deforestation can disrupt these patterns, leading to droughts, floods, and adverse effects on freshwater supplies. Green banking can facilitate projects that honor and harness rather than destabilize natural water systems.

This study explores these important green banking practices in developing countries in Southeast Asia and analyzes the influence of bank-governance regulatory determinants. This article uses Mousmouti’s design of effective legislative measures, considering regulatory purpose, content, and results to consider the regulations in selected ASEAN countries in an objective and precise way. The results here contribute to our understanding of why green banking practices are still needed to stop deforestation practices. This study also offers a standard framework and guideline for internalizing green banking to address deforestation in selected ASEAN countries.

Methods

This article analyzes the obstacles and challenges in implementing green banking to cope with deforestation in selected ASEAN countries. Using a simplified PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) method, various issues were identified based on the literature review above. The valuable examples of green banking implementation in various ASEAN countries are then considered, mainly through Mousmouti’s design of effective legislative measures (regulatory purpose, content, and result). The observations were sharpened through screening using the results of scientific publications, regulations, working papers, digital news, and authoritative reports from each selected ASEAN country, available on information portals and digital databases. The material collected was then systematized to produce several points of discussion results, which were expressed using deductive logical analysis. The multiple sources of information bolstered the analyses within this article. However, there were various constraints regarding limited data and information for several of the ASEAN countries studied––Lao People’s Democratic Republic, Cambodia, and Myanmar––that hindered the analysis of the success of green banking as a way to deal with deforestation.

Result

Green Banking and Deforestation: Facts and Overview in Selected ASEAN Countries

Indonesia

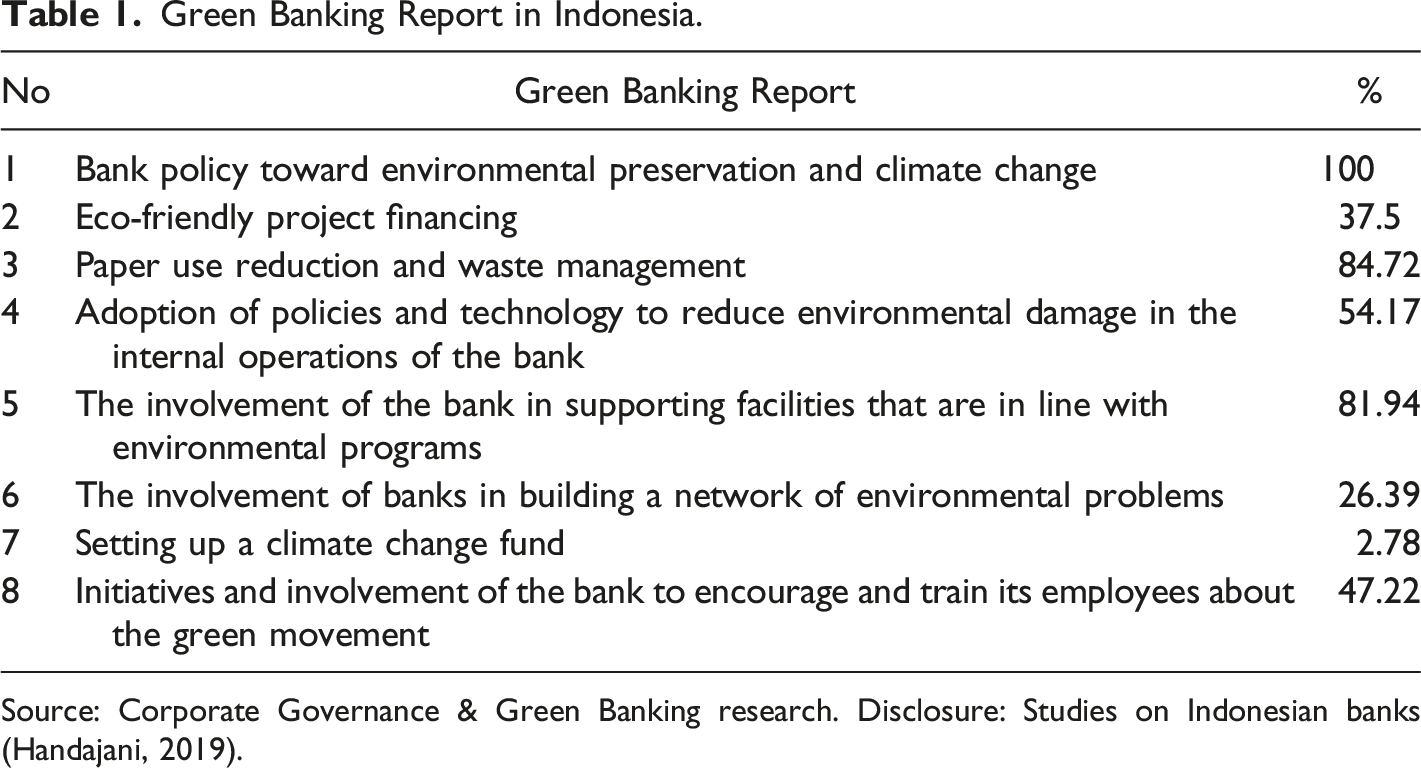

Green Banking Report in Indonesia.

Source: Corporate Governance & Green Banking research. Disclosure: Studies on Indonesian banks (Handajani, 2019).

Handajani (2019) reveals that green banking in Indonesia is focused on adopting policies and technology, paper use reduction and waste management, involvement of banks to support facilities that are in line with environmental programs, and the involvement of banks to encourage and train their employees regarding the green movement. Efforts related to deforestation prevention policies, such as financing environmentally friendly projects, account for only 37.5%, and those establishing a fund related to climate change, only 2.78%. These findings imply that the banking industry is still only attending to green operational activities by reducing the negative impact of environmental damage. Several Indonesian banks have begun to apply the green banking concept to reduce the impact of deforestation. Bank Mandiri, for example, has issued green bonds worth IDR 500 billion to support projects that contribute to reducing greenhouse gas emissions, including projects for sustainable forestry and forest governance (Bank Mandiri, 2022). Bank Negara Indonesia (BNI) has launched the BNI Go Green program, which aims to promote environmentally friendly and sustainable business practices, such as reducing paper use and developing environmentally friendly banking products (Bank Negara Indonesia, 2022).

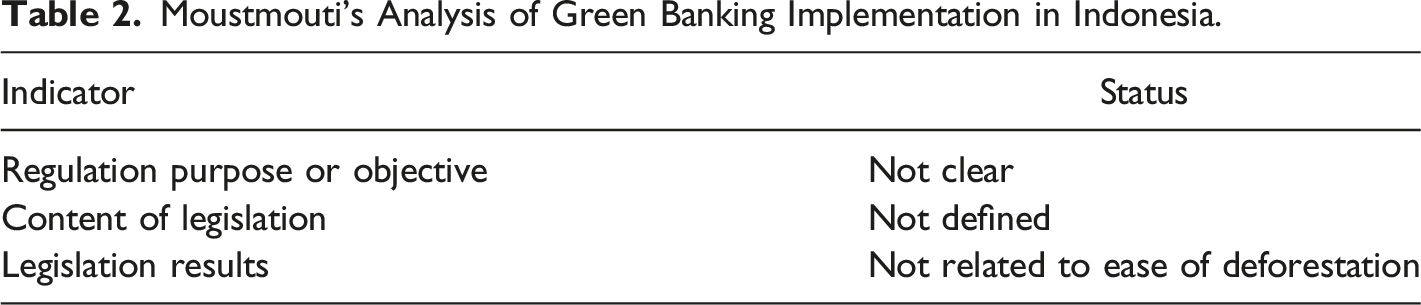

Moustmouti’s Analysis of Green Banking Implementation in Indonesia.

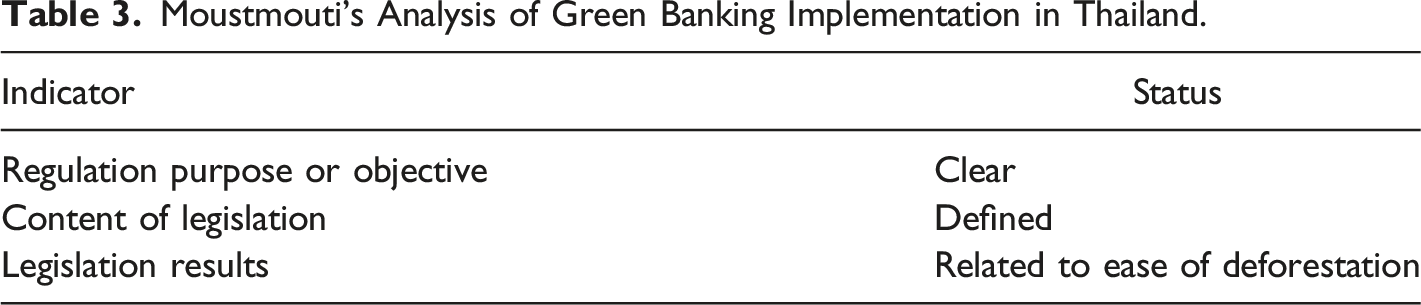

Moustmouti’s Analysis of Green Banking Implementation in Thailand.

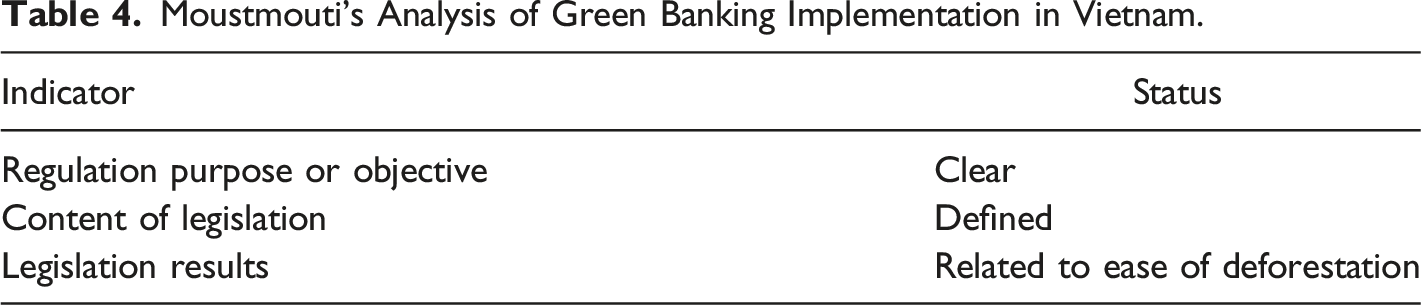

Moustmouti’s Analysis of Green Banking Implementation in Vietnam.

Analysis of the content of legislation shows that the choice of regulation content determines how behavior will be directed to the desired goal by law, what rights are granted or obligations imposed, how rules will be enforced, and what consequences or motives are attached (Mousmouti, 2019, p. 14). Because they do not contain objectives related to reducing deforestation significantly, Indonesia’s green banking regulations do not reflect behavior that leads to stopping deforestation. The obligations are limited to the implementation of sustainable finance and the preparation of sustainability reports. The rights established include the incentives that can be given to financial institutions, issuers, and public companies that implement sustainable finance effectively. Rules are enforced by imposing administrative sanctions as a warning or written caution.

As regards the assessment criteria of the regulatory result, this article argues that the anticipated result from this regulation is to put into full effect the procedure for preparing sustainability reports for financial institutions, issuers, and public companies. All three entity types apply sustainable finance in their operational systems following the distribution timeline specified in the regulation. The immediate results achieved are the compilation of sustainability reports by financial institutions, issuers, and public companies. The output is a sustainability report containing a sustainable financial action plan. No results are directly related to deforestation.

Thailand

The Bank of Thailand (BOT) issued the “Guidelines on Environmental and Social Risk Management for Financial Institutions” in 2018. These guidelines provide a framework for financial institutions to identify, assess, and manage environmental and social risks associated with their lending and investment activities. In response to a lack of government regulations regarding a sustainable financial system, the Thai Bankers Association (2019, p. 1), under the leadership of the BOT in 2019, released the “Sustainable Banking Guidelines for Responsible Lending” to improve the quality of sustainable banking practices in Thailand. This voluntary guideline formulates minimum standards for sustainable lending and includes sustainable business strategies and models. In preparing these guidelines, it also developed the BOT Strategic Plan, 2020–2022.

The BOT (2020) report “Central Bank in a Transformative World” examines three years of operations and underscores the significance of sustainability as a fundamental strategic challenge that necessitates efficient management. The BOT has consistently broadened its range of financial instruments, encompassing those that favorably impact the environment. The bank implemented the “Policy Directions on Green Bonds” in 2019, intending to facilitate the issuance of green bonds in Thailand. As mentioned previously, the policy incentivizes financial institutions to release green bonds to fund ecologically sustainable initiatives while furnishing a set of directives to which issuers must adhere. The Thai Government has also introduced tax incentives for the issue of green bonds by private and public entities (Asian Development Bank, 2022a). The incentives comprise tax exemptions to investors on interest income and tax deductions for expenses associated with the issuance of green bonds.

Thailand’s Securities and Exchange Commission (SEC) has also implemented guidelines for sustainable financing and green bonds (Asian Development Bank, 2022a, p. 2). The guidelines stipulate the standards and prerequisites to which issuers must adhere for their bonds to be classified as environmentally friendly. Additionally, issuers are obliged to furnish periodic updates on the allocation of funds and ecological ramifications. Numerous investigations have been conducted in Thailand to assess the participation of financial institutions in environmentally sustainable banking practices. Several studies reveal the growing trend among banks in Thailand to extend loans and other forms of financing to renewable energy projects. In addition, financial institutions in Thailand are implementing various eco-friendly banking measures, including advocating for sustainable farming and providing environmentally conscious credit card options. Although the evidence indicates an increase in green banking practices in Thailand, several banks have been hesitant to embrace such practices fully. Other studies reveal that despite the increasing recognition of the significance of sustainability among banks in Thailand, there remain considerable obstacles that impede the implementation of green banking. These barriers include inadequate awareness, limited financial resources, and insufficient regulatory support.

An analysis of the purpose of the legislation shows that Thailand’s efforts mainly focus on determining activities that reduce greenhouse gas emissions to achieve climate change mitigation objectives that align with Thailand’s climate policy and international obligations. The country’s efforts are classified according to six environmental objectives: (1) climate change mitigation; (2) climate change adoption; (3) sustainable use and protection of sea and water resources; (4) protection and restoration of biodiversity and ecosystems; (5) prevention and control of pollution; and (6) resilience of resources and circular economy transition. Deforestation-related goals are included under Goal 4. However, only Goal 1 is set for implementation in early 2023 in the taxonomy’s first draft, limiting the scope to the energy and transport sectors. The other goals will be implemented in the next phase, focusing on the industrial sector, agriculture, water and wastewater supply, treatment, and remediation. Thailand’s taxonomy precisely targets the preservation of forests by protecting biodiversity and ecosystems to minimize deforestation.

In terms of the content of the legislation, the Thai taxonomy includes the criteria and steps for determining sustainability activities. First, the company’s operations are broken into different economic activities: those that generate value and those that have an environmental impact. The taxonomy categorizes activities as green (operating at or close to a net-zero trajectory), yellow (facilitating emission reductions), or red (not currently compatible with a net-zero trajectory). Second, the performance of activities is subjected to technical screening. Third, there must be compliance with the principles of doing no significant harm (DNSH) and having minimum social safeguards (MSS). The DNSH principle includes adaptation to climate change, protection of water and marine resources, waste reduction, recycling and transition to a circular economy, pollution prevention and control, and protection and restoration of biodiversity and ecosystems. The MSS principles reflected in the performance standards of the International Finance Corporation cover assessing and managing risks, social and environmental impacts, labor and working conditions, community health and safety, land acquisition and involuntary resettlement, indigenous peoples, and cultural heritage. The norms reflected in the taxonomy have relevance for stopping deforestation as indicated by the need for sustainability activities to conform to DNSH principles, namely, the protection and restoration of biodiversity and ecosystems.

Ultimately, in terms of the result criteria, the Thai taxonomy has the broad objective of accelerating the development of a sustainable financial market in Thailand because financial institutions are expected to have a clearer view of green economic activities to finance. The taxonomy allows a broader range of market players, from regulators to businesses, financial institutions to investors, and the public, to speak the “same language” when referring to green activities in Thailand. This puts in place a more robust check and balance mechanism, and companies may now find it more challenging to greenwash their activities (Ketsuriyonk et al., n.d.). Concerning deforestation, the taxonomy can guide the financing of green projects for protecting and restoring biodiversity and ecosystems. The guide facilitates verification and enhances the transparency of disclosures regarding green projects according to the criteria in the taxonomy.

In sum, it is not easy to provide a definitive answer on the success of green banking in Thailand in reducing deforestation without comprehensive data. However, it is essential to note that green banking initiatives in Thailand are still in their early stages and may take time to achieve their intended impact. This article assumes that Thai green banking initiatives have the potential to contribute to reducing deforestation through robust regulation, including promoting environmental risk management. For example, green loans and bonds can be used to finance renewable energy projects and other sustainable initiatives, reducing reliance on fossil fuels and promoting sustainable land use. Furthermore, environmental risk management practices adopted by Thai banks can help in the identification and mitigation of the environmental risks associated with their lending and investment activities.

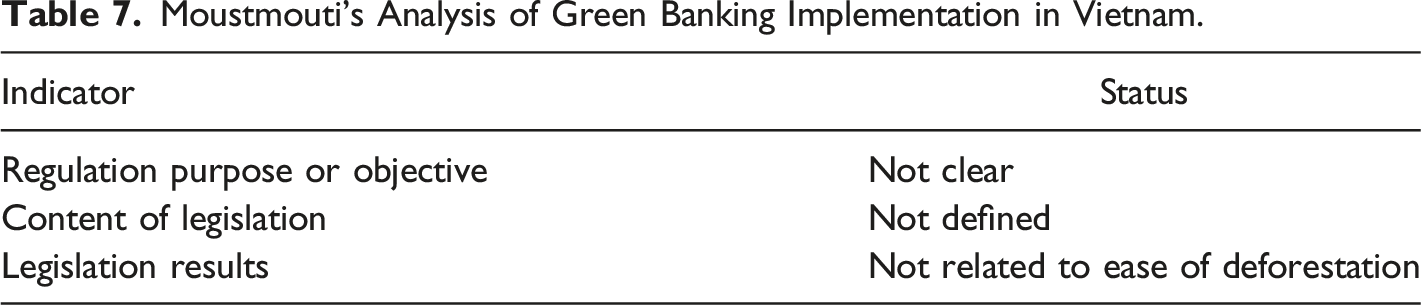

Vietnam

Vietnam’s policy related to the principle of sustainability is contained in the National Action Plan on Sustainable Consumption and Production (2021–2023). This aims to achieve economic development efficiency, protect the environment, reduce poverty, restructure the economy, promote a circular economy and sustainable development, and synchronously implement sustainable consumption and production. One of the policy’s proposed actions is promoting access to and support for green finance by offering additional green financial instruments, developing green finance guidelines, and establishing cooperation with national and international partners regarding green finance (Ministry of Industry and Trade, the Socialist Republic of Vietnam, 2021).

Over the past several years, green finance initiatives have emerged in Vietnam, initially promoted by foreign-owned commercial banks (Nguyen et al., 2022). A literature review in Vietnam shows that three large local banks and three commercial foreign-owned banks have actively introduced green finance as a financial product. The banks selected for the study have been involved in green finance for at least three years and have received national and international recognition and awards for their contributions to promoting green finance and sustainable development for businesses in Vietnam (Nguyen et al., 2022, p. 5).

Some Vietnamese banks have developed variations of green finance practices (Huang, 2022), including foreign and domestic partnerships/alliances to promote green finance and sustainable development, workshops and awareness-raising campaigns for stakeholders to direct funding for sustainability and climate change projects, and developing policies that support green finance and sustainable development. The increasingly widespread implementation of green finance requires legislative support from the government to avoid ambiguity in the standards for implementation. Unfortunately, the Vietnamese government has yet to accommodate this. Green finance in Vietnam is carried out voluntarily and is not mandated by law (2023). The Vietnamese government has yet to provide detailed guidelines and roadmaps for practicing green finance. The absence of such guidelines has left Vietnamese banks facing uncertainty in implementing regulations, understanding risks, and developing green finance strategies for their clients.

An analysis of the purpose of Vietnam’s National Action Plan on Sustainable Consumption and Production (2021–2030) shows it has two types of objectives. The general objectives are to promote efficient and sustainable management, exploitation, and use of natural resources, fuels, and materials; promote the development of environmentally friendly resources, fuels, materials, and products that are renewable, reusable, and recyclable; promote sustainable consumption and production based on innovation, creativity, practice, and development of sustainable consumption and production models; and promote the consumption and sustainable production of domestic products, create stable green jobs, enhance sustainable lifestyles and improve people’s quality of life toward a circular economy in Vietnam. The objectives are divided and attended to in two distinct periods: 2021–2025 and 2025–2030. In the 2021–2025 period, the focus is on developing legal policies for sustainable consumption and production and achieving targets for consumption and production in various sectors. The period ending in 2030 involves effectively improving and implementing legal policies on sustainable consumption and production and achieving higher targets for consumption and production in various sectors. The goal of promoting efficient and sustainable management, exploitation, and use of natural resources suggests that Vietnam is indirectly contributing to stopping deforestation.

An analysis of the content of the Vietnamese regulations shows clauses related to these objectives and regarding investment in natural resources to stop deforestation by promoting access to and supporting green finance by (1) developing and increasing the use of green financial instruments, policies to promote consumption models and continuous production and financial support for the production of eco-friendly and recyclable products; (2) developing manuals, handbooks, building green finance capacities aimed at promoting sustainable consumption and production; providing support to related companies and other organizations so that they can access green finance; and (3) developing a network of national and international partners in green finance to promote sustainable consumption and production, and a circular economy.

The regulation is enforced in two ways. First, ministries, ministerial-level institutions, and government agencies refer to the assigned tasks and ensure that sustainable consumption and production are studied and integrated into the strategies and development plans of relevant sectors and fields, thereby promoting sustainable consumption and production in relevant programs. Second, social and professional organizations, related associations and institutions, companies, communities, and individuals are able to proactively propose and coordinate with ministries and other sectors. This allows them to implement, support, and participate in communication and awareness-raising programs related to sustainable consumption and production in the fulfillment of their functions. Finally, there is only minimal information conveyed with respect to the legislation-result criteria. However, in general, the provisions only regulate the conversion of traditional consumption and production into more sustainable patterns in two periods, 2021–2025 and 2025–2030 period.

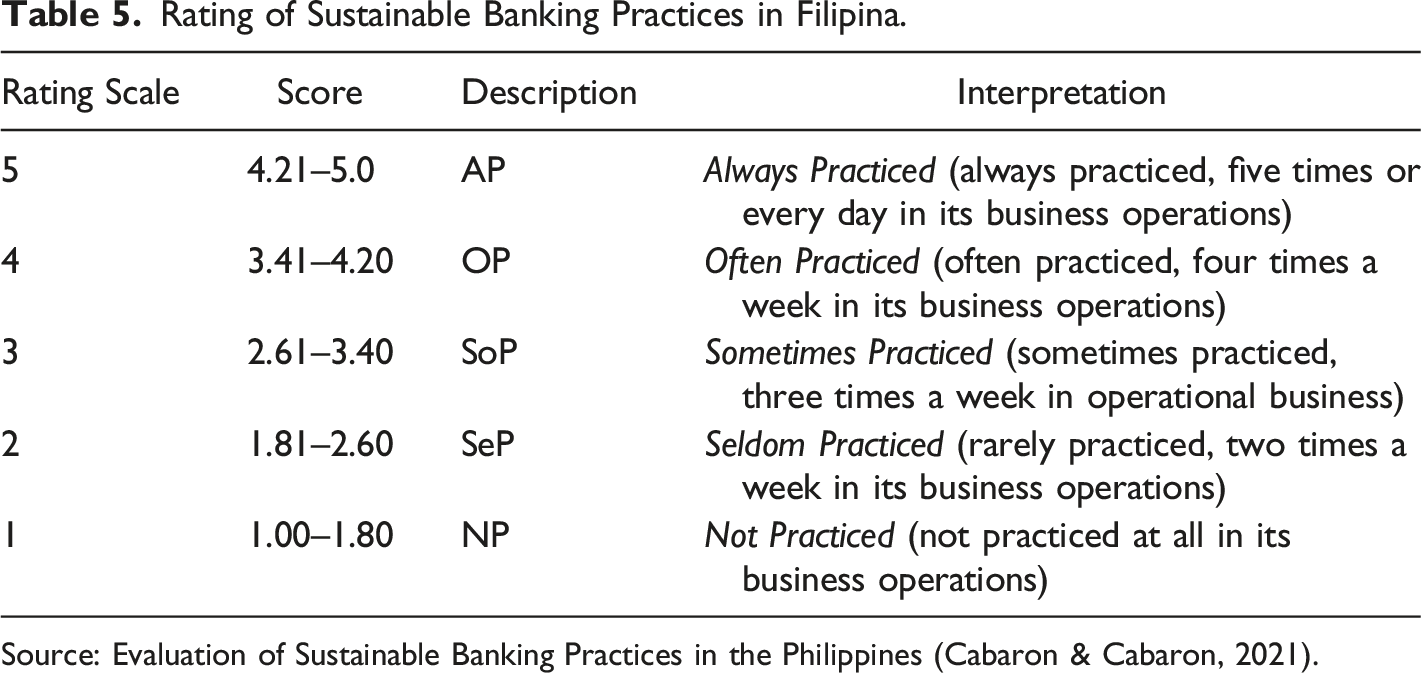

Filipina

In 2018, Bangko Sentral ng Pilipinas (BSP) launched a sustainable finance framework that requires banks to integrate sustainability principles and report on their sustainability framework by 2023 (2020a). Banks must disclose information in their annual reports on their sustainability strategy, environmental and social risks, risk exposure and risk management systems, sustainable financial products and services (including green, social, or sustainability obligations), and initiatives to promote compliance with internationally accepted sustainability standards. Furthermore, they are required to integrate sustainability principles into their governance and risk management systems, strategies, and operations (BSP 2020a, p. 4). The framework outlines the specific duties and responsibilities of banks’ boards of directors and senior management. All banks are required to have an environmental and social risk management system (BSP 2020a, p. 3).

Rating of Sustainable Banking Practices in Filipina.

Source: Evaluation of Sustainable Banking Practices in the Philippines (Cabaron & Cabaron, 2021).

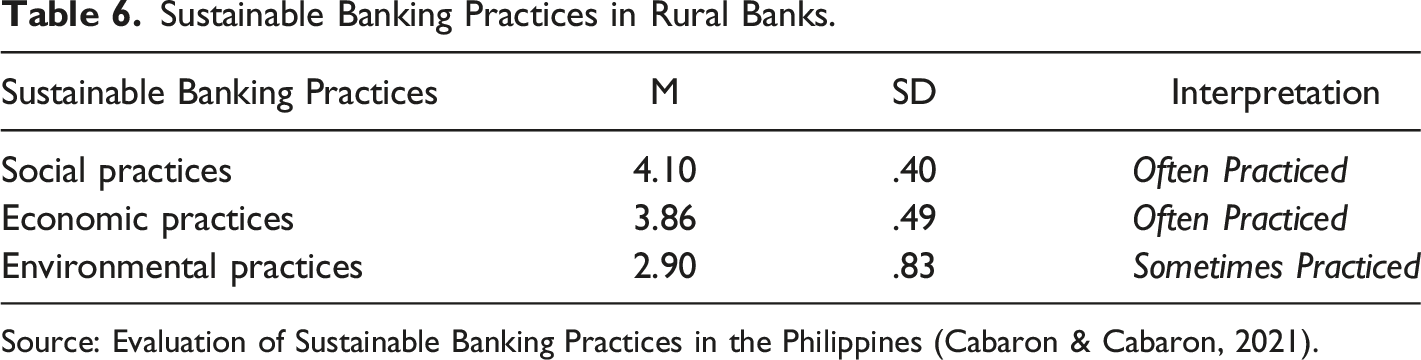

Sustainable Banking Practices in Rural Banks.

Source: Evaluation of Sustainable Banking Practices in the Philippines (Cabaron & Cabaron, 2021).

Moustmouti’s Analysis of Green Banking Implementation in Vietnam.

Moustmouti’s Analysis of Green Banking Implementation in Malaysia.

Role of Green Banking to Cope Deforestation Through Decisive Legal Framework.

There is an urgent need for government support for green banking practices for customers and the bank. The Philippines still needs legislation that comprehensively and in detail regulates the country’s green banking practices. In addition, there is a need for improvement in several priority areas related to sustainable finance, namely, the externality of prices into the economic and financial system, strong coordination in the financial system, climate-related financial risk management, the need to increase sustainability reporting requirements and capacity building programs to address knowledge gaps in the financial system, and participation in international initiatives on financial sustainability by sharing best practices and experiences (Ernst & Young, n.d.).

This study shows that deforestation in the Philippines is mainly driven by agricultural expansion, illegal logging, and mining activities, often linked to poverty and a lack of secure land tenure for rural communities. Addressing these drivers of deforestation through effective policies and strategies requires a comprehensive approach involving multiple stakeholders, including government agencies, civil society organizations, and the private sector. This article assumes that it is challenging to determine the extent to which green banking in the Philippines reduces deforestation; it is a complex and ongoing issue that involves multiple stakeholders and factors.

The purpose of the legislation, evident in the objectives of the Circular No. 1085 Series 2020 released by the Central Bank of the Philippines regarding a sustainable finance framework, is the integration of sustainability principles, including accounting for environmental and social risks, in corporate governance and risk management frameworks and in the bank’s strategic and operational goals. Like Indonesia, the Philippines’ green banking regulation does not have a direct goal of decreasing deforestation.

An analysis of the legislation’s content shows that its main objective is not related to deforestation. As such, the behavior of banks directed at integrating the principles of sustainability is not behavior that directly focuses on deforestation. The behavior is reflected in clauses requiring the boards and senior management of companies to take specific actions toward integration. The internal audit and compliance functions should include an assessment of compliance with policies related to managing environmental and social risks, an evaluation of the robustness and ongoing relevance of those policies, and a review of the bank’s compliance with international sustainability standards and principles and relevant laws and regulations. Banks must also provide an overview of the environmental and social risk management system in their annual report. There are no stipulations as to how the rules will be enforced and the consequences or motives attached.

The anticipated result of this regulation is a procedure for integrating sustainability principles––including those covering environmental and social risks––into the corporate governance and risk management framework and the bank’s strategic and operational goals. The immediate result in the banking industry is that banks must prepare an annual report that includes consideration of environmental and social risks. The output is the bank’s annual report, which considers environmental and social risks according to the criteria required by the regulation.

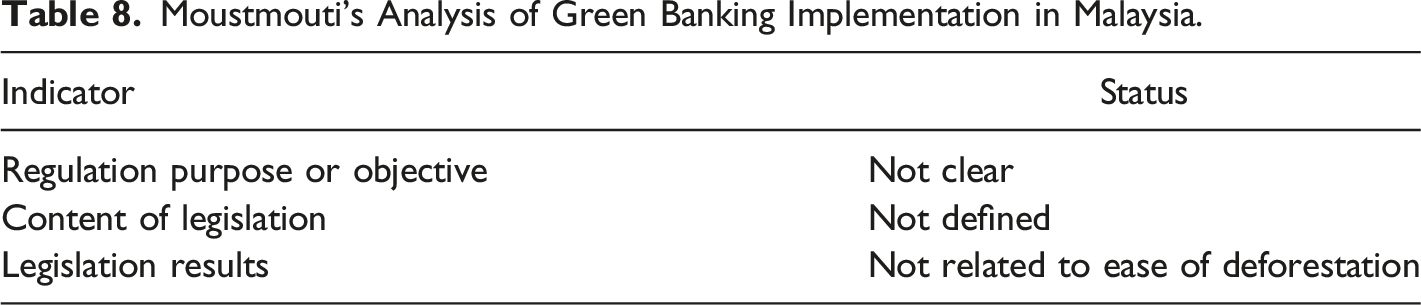

Malaysia

Malaysia is one of the largest issuers of sukuk, with a world market share of 41.5% by 2022 (2020b). As such, regulatory policies related to a sustainable financial system also focus heavily on sukuk and the capital market. This can be seen in several existing policies, such as the Sustainable and Responsible Investment (SRI) Sukuk Framework, the Sustainable and Responsible Investment (SRI) roadmap for the Malaysian capital market, Socially Responsible Investment (SRI) taxonomy, Bursa sustainability requirements, and Capital Market’s masterplan (2021).

The Government of Malaysia has made several vigorous attempts to implement green banking in the country, namely, by establishing the Malaysian Green Technology Corporation (MGTC) to oversee the operation of the National Green Technology Policy (Pek et al., 2019) The Green Technology Financing Scheme was created to prepare concessional loans to businesses eligible for green projects. These loans, worth MYR1.5 billion, were intended to drive green growth in their respective sectors under the 2010 Malaysian Budget (Pek et al., 2019). In support of the government’s efforts, Malaysia Debt Ventures Bhd (MDV) also launched a MYR 300 million financing program that assists various industries with green investment (Pek et al., 2019). The government also cooperates with and encourages commercial banks to offer green loans. Most commercial banks have responded positively to these cooperation efforts, especially in offering green loans. Domestic banks have given out green loans, and foreign banks operating in Malaysia are also pioneering green banking in the Malaysian domestic market by offering loans to qualified customers.

Regarding the issue of deforestation and the existence of green banking, this article reveals a reality that is similar to the countries considered above. The regulations governing the sustainable financial system in Malaysia are policies without binding legal force. It is vital for the Government of Malaysia to create legal certainty in its efforts to implement a sustainable financial system.

Discussion

Fundamental Barrier Implementing Green Banking in Selected ASEAN Countries

While green banking has recently gained traction, this article assumes that advancement is hampered by legal and policy barriers. Green banking initiatives can play a role in reducing deforestation, but on their own, they may not be sufficient. This investigation of the academic literature provides insights into how the objectives, content, and outcomes of green banking regulation and policy may impede efforts to reduce deforestation.

Lack of clear and consistent regulations and standardization

One of the significant legal barriers is the lack of clear and consistent regulations and standards for green banking practices. Different countries and regions each have their own definitions and criteria for what constitutes “green” or “sustainable” investments, which can lead to confusion and inconsistency in the market (Cheung & Hong, 2020). These ambiguities can also make it difficult for banks to identify and assess the environmental impact of their lending and investment activities. Another legal barrier is the lack of legal remedies or penalties for banks that fail to comply with green banking standards. Banks may have little incentive to invest in environmentally sustainable projects or reduce their carbon footprint without solid mechanisms for legal enforcement.

The lack of clear and consistent regulations and standards has the following impacts. a) Confusion and inconsistency Having a clear definition of green or sustainable investments is essential for several reasons. First, it can assist financial institutions in recognizing and evaluating the ecological consequences of their lending and investment undertakings. Despite its importance, establishing a clear definition for green or sustainable investments faces various obstacles. One of the challenges is the lack of agreement or consensus among the various stakeholders. Organizations employ diverse standards to assess the eco-friendliness or sustainability of an investment, and this may lead to confusion and inconsistency in the market. The complexity and interrelatedness of environmental and social concerns present a significant hindrance in identifying genuinely sustainable or environmentally friendly investments. If a renewable energy endeavor is produced using non-renewable resources, the ecological ramifications may not be as favorable as initially perceived. This article also reveals that insufficient data and a lack of transparency increase the difficulty of defining green or sustainable investments. Evaluating the environmental impact of an investment can pose challenges in the absence of comprehensive and accurate data. Financial institutions may also avoid detailed disclosures, posing a challenge for investors wishing to assess the ecological ramifications of their investments. The practice of greenwashing also makes it difficult to define green or sustainable investments in a meaningful way. Greenwashing, addressed below, refers to the act of making misleading or inaccurate claims about the environmental advantages of an investment. The practice can deceive investors and erode the legitimacy of the green investment market. b) Greenwashing The absence of well-defined criteria may facilitate greenwashing, with financial institutions overstating the ecological advantages of their offerings without substantially altering their operations. The absence of precisely delineated parameters for green products or services may allow financial institutions to employ equivocal or imprecise terminology to market their offerings as ecologically sound, notwithstanding the absence of particular environmental benchmarks to which they adhere. Greenwashing can occur when a financial institution purports to provide an environmentally friendly savings account or credit card yet neglects to reveal the precise ecological advantages or standards that qualify a product as green. The absence of transparency challenges consumers wishing to distinguish authentic environmentally friendly products from those merely marketed as such. This study posits that the establishment of unambiguous benchmarks and increased openness can effectively limit greenwashing within the financial sector. Financial institutions can enhance the reliability of information about their products’ environmental impact by establishing unambiguous standards for identifying green products or services. For example, financial institutions have adopted the Equator Principles or the Green Bond Principles, which contain distinct criteria for eco-friendly lending and investment. These standards furnish a set of criteria for appraising the ecological ramifications of lending and investment undertakings and guarantee that investments are congruent with environmental objectives. The environmental advantages of products and services can be verified through external certifications from independent third-party entities, such as the Leadership in Energy and Environmental Design (LEED) certification for buildings or the Forest Stewardship Council (FSC) certification for sustainable forestry (Taru Mustalahti, 2022, p. 44). c) Inefficiency and waste Without clear guidelines, banks may make inefficient investments in green projects or initiatives, leading to wasted resources and potential environmental harm (OECD, 2015, p. 17). They may even invest in projects that are harmful to the environment but are marketed as green, exacerbating the problem. The absence of guidelines for green investments can pose significant risks for banks and the environment (Luo, 2011). Banks may make inefficient investments in green projects or initiatives without specific criteria for evaluating the environmental impact of investment decisions, leading to wasted resources and potential environmental harm (GIZ, 2019, p. 62). This may include investment in renewable energy projects that are not economically viable, resulting in financial losses and a reduction in the capital available for other green investments (Cheng & Ma, 2018). Banks may also invest in projects that claim to be environmentally friendly but, in fact, cause environmental damage (Deschryver & de Mariz, 2020). This could occur in cases where a project does not meet clear environmental criteria, or the bank does not adequately assess the project’s environmental impact (Cheng, 2023). d) Risk to investors The lack of established criteria may impede investors’ ability to obtain reliable data on the ecological consequences of their investment decisions. This may lead to investment choices that rely on incomplete or erroneous information, elevating the likelihood of financial losses.

Lack of policy support and incentives

From a policy perspective, government support and incentives are crucial for advancing green banking. Environmentally friendly projects and initiatives may require a significant initial investment, and financial institutions may decline funding without government assurances or incentives. Moreover, policies that endorse the use of fossil fuels or other unsustainable practices can impede the expansion of eco-friendly banking. In some cases, the advantages of environmentally friendly investments may not be immediately apparent, making it difficult for financial establishments to rationalize the expense. Government and regulatory entities can tackle the issue through tax incentives or other supportive measures for eco-friendly investments and by enhancing consumer awareness and promoting the demand for sustainable goods and services.

Content: Limited scope

Green banking initiatives may be somewhat limited, primarily focusing on the funding of environmentally sustainable endeavors rather than tackling the underlying factors contributing to deforestation. For example, banks may finance reforestation projects, but these may not address the root causes of deforestation, such as agricultural expansion or infrastructure development. Moreover, green banking initiatives in several ASEAN countries can also promote sustainable financing practices that support the transition to a low-carbon and sustainable economy (Asian Development Bank, 2022b). This advance effort can include financing sustainable infrastructure projects, supporting the development of green bonds and other sustainable financial instruments, and integrating environmental and social considerations into investment decisions (Asian Development Bank, 2022b, p. 6).

While green banking initiatives can support these efforts, deforestation is a complex and multi-dimensional problem that requires a comprehensive approach involving collaboration between governments, civil society, the private sector, and local communities (n.d.). It is essential to address the root causes of deforestation, promote sustainable land use practices that prioritize the conservation and restoration of forests, and reduce the demand for products that contribute to deforestation. One of the concrete steps needed for green banking to overcome this problem might be CSR reforestation or third-party funding for reforestation (2007). Unfortunately, these projects may not effectively address the underlying drivers of deforestation, including large-scale agriculture, mining, logging, or infrastructure development (2007). Although reforestation is crucial in mitigating deforestation and encouraging sustainable land use practices, green banking initiatives in Indonesia must have a broader scope.

In addition to providing financial support to reforestation programs, green banking initiatives in the ASEAN region could facilitate the adoption of sustainable forestry practices, including minimizing the use of hazardous chemicals in producing paper and pulp and ensuring that timber is sourced from managed sustainable forests. Implementing green banking practices can potentially advance sustainable energy sources and energy-efficient technologies. This scheme may, in turn, contribute to a decrease in the utilization of non-renewable resources and alleviate the consequences of climate change.

Lack of legal or policy enforcement

In some cases, green banking policies may not be adequately enforced, enabling banks to persist in their financing of unsustainable practices that are causative of deforestation. This could potentially be attributed to inadequate environmental regulations or a lack of effective enforcement mechanisms. The present study posits that inadequate environmental regulations and the absence of enforcement mechanisms can diminish the efficacy of green banking policies in mitigating deforestation. If environmental regulations are inadequate or are not executed with efficacy, financial institutions may continue to engage in unsustainable financial practices that allow ongoing deforestation (Luo, 2011, p. 57). Unsustainable financial practices may arise due to a lack of clarity and uniformity in environmental regulations, insufficient monitoring and reporting mechanisms, and corruption and political intervention in regulatory procedures. Achieving a substantial decrease in deforestation through green banking policies necessitates the establishment of unequivocal and consistent environmental regulations that are firmly based on empirical evidence.

The regulations can be enforced through monitoring and reporting mechanisms coupled with the imposition of sanctions for noncompliance. Furthermore, prioritizing the protection of forests and other natural resources is imperative (Dikau & Volz, 2018).

Promoting transparency and accountability in the banking industry can also help ensure that banks are held accountable for their environmental impact and incentivized to implement sustainable practices. This could include promoting the disclosure of environmental risks and impacts, engaging stakeholders in developing green banking policies, and supporting independent audits and environmental performance evaluations.

Conflicting interests

This study postulates a potential misalignment between the objectives of financial institutions and those of environmental preservation, which could result in a conflict of interests between banks and their clients. Banks may provide financial support to projects that lead to deforestation to maximize profits or cater to the escalating demand for commodities, such as palm oil or timber (Global Witness, 2021). The presence of divergent interests can present a formidable obstacle to the success of eco-friendly banking endeavors, potentially impeding progress in mitigating deforestation. Financial institutions may encounter demands from their stakeholders or investors to fund undertakings that result in deforestation, such as extensive farming, mining, or infrastructure construction. The activities mentioned above have the potential to yield short-term financial gains; however, they may have substantial adverse effects on the environment and local communities over an extended period.

It is imperative to endorse sustainable banking practices that prioritize environmental and social factors in conjunction with financial performance to tackle the conflict of interests. This requires the integration of environmental and social risk evaluations into lending determinations and the creation of sustainable finance commodities that encourage sustainable behaviors. Further, interactions with stakeholders, such as local communities and civil society groups, are required to guarantee that their perspectives are taken into account in decision-making.

Transparency and accountability within the banking industry can guarantee that financial institutions are held accountable for their ecological and societal effects and are motivated to implement sustainable measures. Sustainable practices may involve encouraging disclosure of environmental and social risks and impact, active engagement of stakeholders in the development of green banking policies, and provision of support for independent audits and assessments of environmental and social performance.

Limited outcome and impact

This article assumes that green banking initiatives may have a limited impact on deforestation due to the scale of the problem. Deforestation is often driven by large-scale agriculture, logging, and infrastructure projects, and addressing this problem may require significant changes to policy and investment practice. This article argues that green banking initiatives, the financing of reforestation projects, and the promotion of sustainable land use practices are essential to addressing deforestation. Nevertheless, these endeavors may prove inadequate in tackling the fundamental drivers of deforestation, which are frequently systemic and necessitate synchronized efforts across sectors and stakeholders. Effectively tackling the issue of deforestation requires all-encompassing approaches that target the fundamental causes of deforestation, including unsustainable land use methods, inadequate environmental regulations, and insufficient land tenure security for indigenous populations. Changing these may entail promoting sustainable agricultural practices, developing efficient environmental regulations and enforcement mechanisms, supporting community-based conservation initiatives, and allocating resources toward renewable energy and sustainable infrastructure projects that mitigate environmental harm.

Breaking the Impediment: Boosting the Role of Green Banking in Selected ASEAN Countries

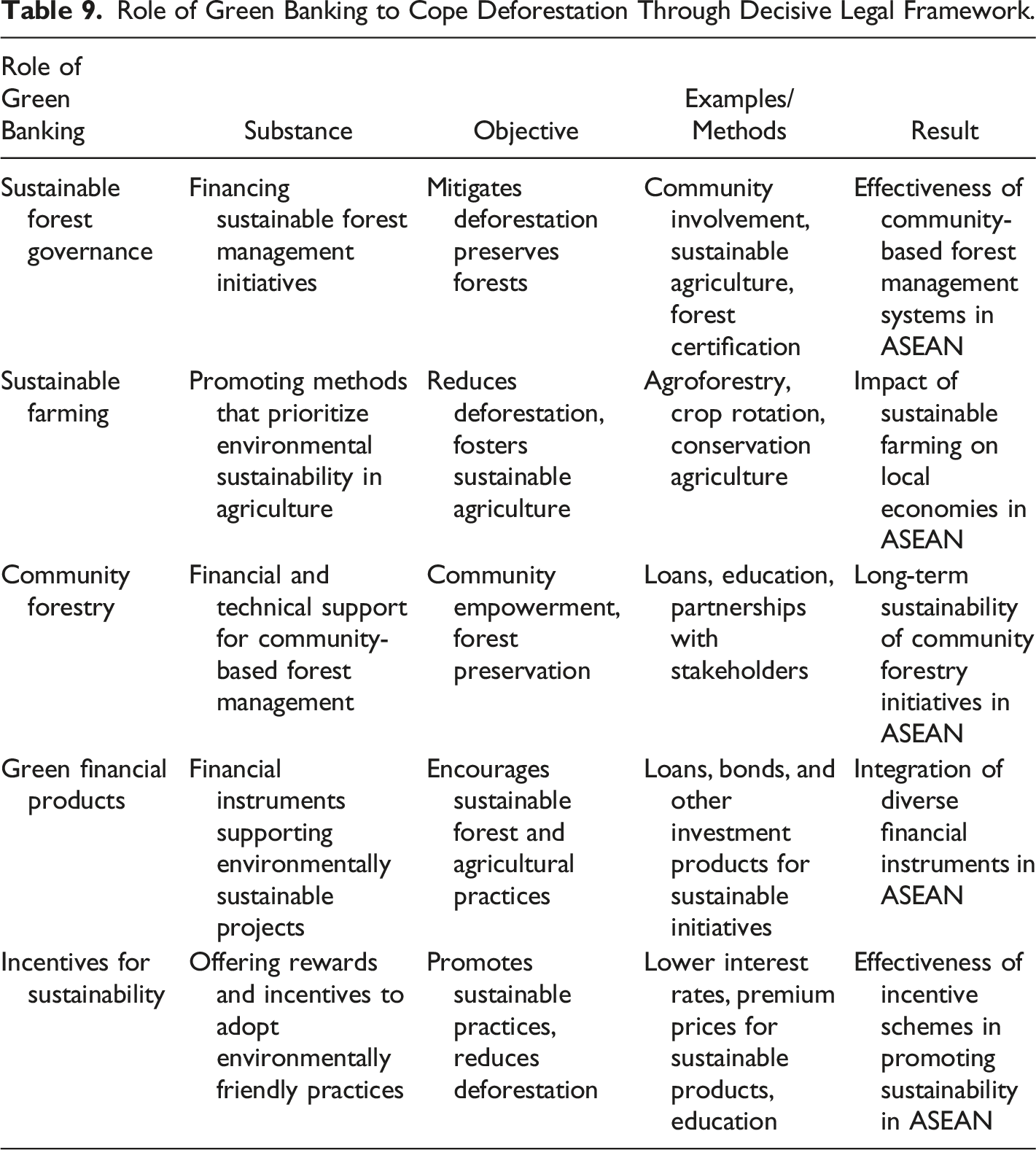

The increasing global concern for environmental conservation and sustainability has led to the adoption of several measures to reduce the negative impact of human activity on the environment. One of the measures that has gained significant attention in recent years is green banking. Green banking involves integrating environmental and social factors into the operational framework of the banking industry. In this article, the function of green banking in selected ASEAN countries is considered, and suggestions are offered for enhancing its efficacy. Implementing green banking practices can significantly impact the preservation and safeguarding of forests, which are fundamental to sustaining robust ecological systems and mitigating climate change. This article uses Mousmouti’s regulation effectiveness indicators to show that the processes and functions of green banking play a significant role in mitigating deforestation. This paper proposes several significant roles that the steps and functions of green banking play in mitigating deforestation through Mousmouti’s regulation effectiveness indicators in the following table.

The explicit provision of financial resources to promote sustainable forest governance

Sustainable forest governance entails the application of methods that preserve the forest’s ecological balance while catering to the surrounding community’s economic and social requirements. Implementing green banking practices can be pivotal in financing sustainable forest management initiatives, specifically those aimed at forest conservation and restoration (Erbaugh et al., 2020). This pivotal responsibility encompasses facilitating the advancement of forest management systems based on community involvement (Parhusip et al., 2019; Thammanu et al., 2020), allocating resources toward sustainable agriculture, and advocating for environmentally sustainable forest products.

In the present research, green banking is considered a viable strategy to mitigate deforestation by incentivizing corporations to adopt environmentally sustainable practices. Financial institutions have the potential to exert their influence in favor of sustainable supply chain practices, which may include the adoption of sustainably sourced materials or the promotion of more efficient and ecologically sound production techniques. In addition, green banking can support sustainable forest management techniques, including reduced-impact logging, forest certification, and reforestation initiatives. The provision of financial resources to support these endeavors by green banking institutions can potentially mitigate the need for illicit logging practices and lead to the preservation of forested areas.

Encouraging the implementation of farming methods that prioritize environmental sustainability

Smallholder farmers in the ASEAN region increasingly use slash-and-burn techniques to clear land for agricultural purposes, a practice identified as a significant contributor to deforestation in the area. The methodology may have negative consequences in the long-term, including soil health degradation, decreased biodiversity, and intensified climate change. The implementation of sustainable agricultural practices, including but not limited to agroforestry, crop rotation, and conservation agriculture, can potentially decrease the need for the practices that cause deforestation. Additionally, sustainable agricultural practices can offer financial advantages to farmers. Green banking, a financial service that prioritizes environmental sustainability, can significantly impact the progress of sustainable agriculture. Sustainable farming practices can be facilitated by providing financial resources for initiatives such as agroforestry and sustainable crop production. The sustainable approach involves allocating financial resources to farmers to aid their transition toward sustainable practices, providing education and training, and encouraging sustainable supply chains.

Green banking can also encourage corporations to engage in sustainable sourcing practices, including the acquisition of goods from farmers who employ sustainable agricultural practices or establishing sustainable sourcing rules and regulations. Financial can promote sustainable practices among companies, consequently mitigating the demand for unsustainable agricultural practices and the necessity for deforestation.

In summary, the incorporation of green banking practices can have a significant impact on advancing sustainable agricultural methods and reducing deforestation in the ASEAN region. This article argues that green banking practices can foster a sustainable and resilient food system, safeguarding the region’s forests and biodiversity. Furthermore, this can be achieved by providing financial support for sustainable agriculture and promoting sustainable sourcing practices.

Advocating for and promoting community forestry initiatives

Community forestry is a sustainable forest management system that confers authority on local communities to manage and utilize their forest resources, limiting deforestation and supporting sustainable forest governance. This article posits that green banking has the potential to support community forestry initiatives through various means. Initially, financial institutions can offer loans and other financial assistance to local communities to facilitate the establishment and upkeep of community forests. The present research strongly recommends that this endeavor include financial support for forest restoration, preserving biodiversity, and implementing sustainable forest management techniques.

Implementing green banking initiatives can also include technical guidance and educational opportunities for communities pursuing sustainable forestry methodologies, including agroforestry, carbon sequestration, and producing non-timber forest products. Implementing sustainable forestry practices can aid communities in formulating sustainable forest management plans that cater to their economic, social, and environmental requirements. Green banking practices can catalyze community forestry initiatives by fostering partnerships with relevant stakeholders and government entities to establish appropriate legal frameworks and policies.

This study offers a plausible strategy for operationalizing such a policy. This entails endorsing land tenure rights for indigenous communities, fostering community participation in forest management, and incentivizing sustainable forest management practices. Furthermore, implementing environmentally sustainable banking practices could significantly impact community forestry initiatives that aim to reduce deforestation. Adopting environmentally friendly banking practices can positively impact the preservation and sustainable administration of forest resources while simultaneously promoting economic and social progress. As mentioned above, these objectives can be attained by dispensing financial and technical aid alongside policies that empower indigenous communities.

There is a growing trend in the financial sector toward adopting financially sustainable products that exhibit environmentally friendly characteristics. These “green financial products” aim to promote sustainable economic growth while mitigating environmental risks. Green financial products refer to financial instruments that support environmentally sustainable projects and enterprises. According to existing research, an amalgamation of diverse financial instruments, such as loans, bonds, and other investment products, is recommended to finance initiatives to mitigate deforestation. Implementing environmentally conscious banking practices can facilitate financial instruments that incentivize sustainable forest management strategies, including forest conservation and reforestation initiatives. Utilizing these goods can provide economic support for sustainable forestry practices that assist in preserving and rehabilitating forest resources while fostering economic growth.

The adoption of sustainable agricultural practices can be facilitated through the implementation of green banking and financial instruments that support this objective. As an illustration, it has the potential to financially assist farmers who implement agroforestry techniques or distribute bonds that endorse sustainable agriculture supply chains. Utilizing these products can mitigate the strain on forests by supporting sustainable agricultural methodologies that curtail the need to deforest additional land. Moreover, implementing green banking practices can facilitate financial instruments that promote the advancement and integration of sustainable energy solutions. Green banking can reduce the demand for forest resources utilized in energy production by endorsing renewable energy sources like wind and solar power.

Offering rewards for adopting environmentally friendly behaviors

The notion of green banking pertains to the endeavors of financial institutions to advance sustainable and ecologically responsible practices in their lending activities and operational procedures (Sunio et al., 2021; Zhou et al., 2022). Green banking has the potential to mitigate deforestation by offering incentives for sustainable practices. Incentives, whether monetary or non-monetary, motivate individuals and organizations to embrace sustainable practices to mitigate deforestation. The present study posits that implementing green banking can motivate the adoption of sustainable practices through various means. For example, financial institutions can provide loans at lower interest rates or furnish other financial benefits to support sustainable forestry management and agriculture practices. This incentive has the potential to motivate individuals and businesses to embrace sustainable practices that effectively alleviate the burden on forests.

Furthermore, green banking can be implemented to offer technical support and education regarding sustainable methodologies, such as agroforestry or conservation agriculture. Financial institutions have the potential to facilitate the adoption of sustainable practices among individuals and businesses, thereby mitigating the necessity of clearing new areas for land-dwelling. Moreover, green banking can support collaboration with private entities and their supply chains to establish motivators for adopting sustainable sourcing practices. Implementing a sustainable incentive scheme offers potential economic benefits for sustainable products, including timber sourced from sustainably managed forests and agricultural products cultivated through sustainable practices offered at premium prices. In addition, green banking policy can encourage collaboration with legislative bodies and other relevant entities to establish favorable regulations and legal structures that promote environmentally responsible behaviors. This may involve devising tax incentives to encourage businesses to adopt sustainable practices, establishing certification programs for products sourced sustainably, or offering subsidies to support sustainable forest management.

In conclusion, providing incentives for sustainable practices is critical in employing green banking to mitigate deforestation. By offering financial and non-financial incentives, providing technical assistance, and promoting supportive policies, green banking can be used to encourage individuals and businesses to adopt sustainable practices that help conserve forests and promote sustainable economic development (Tedesco et al., 2022; Wu et al., 2011).

Conclusion

The emergence of green banking presents a promising sustainable financing strategy for a greener future in ASEAN. Several ASEAN countries face significant challenges related to the lack of clear and consistent regulations and standardization, limited policy support and incentives, limited scope, lack of enforcement, and conflicting interests. Nevertheless, there are several potential solutions. This article recommends ASEAN policymakers and societies develop robust green banking regulations with clear, objective, and precise content and definitive outcomes or impacts. They can do so by promoting finance sustainable forest management, encouraging sustainable agricultural practices, supporting community forestry initiatives, introducing green financial products, and providing incentives for sustainable practices. By addressing these challenges, green banking can help to reduce deforestation and promote sustainable economic development in the region. The evolution and adoption of green banking have the potential to drive positive change and contribute to a more sustainable and resilient ASEAN economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.