Abstract

This article investigates the relations between local housing policies and global corporate landlords in Berlin, Germany. While previous studies on the financialisation of housing markets have described the role of the state as facilitating and supporting the entry of institutional investors into the housing market, there is only limited understanding about the relationship between the local state and institutional investors after the latter have taken ground and established themselves in urban housing markets with a long-term perspective. Studying the local political arena in Berlin, we describe five distinct phases in which the relationship between financialised housing investors and the local state has undergone considerable twists and turns. We find that no stable partnerships between local authorities and financial investors have yet developed and identify a number of factors that explain the lack of engagement in building long-term collaborations on both sides. We argue that both local governments and financial investors are bound by complex and often contradictory logics that complicate their relations and create instability in partnership arrangements. A conflation of local ‘entrepreneurial’ policy, orientations and the interests of financial investors should therefore not be taken for granted. Rather, the Berlin case shows how achieving cooperation between these actors is unstable and challenging.

Keywords

Introduction

For almost three decades, Berlin has witnessed the sale of a significant portion of its housing stock to institutional investors. Consequently, the share of housing controlled by global corporate landlords is larger in Germany’s capital than almost anywhere else. 1 The financialisation of rental housing has a comparably long history. Against this background, this city, as a case, allows us to study the long-term implications of rental financialisation for housing policies.

In this article we argue that studying the case of Berlin can contribute to a better understanding of the role of the state in housing financialisation in general. Although the recent literature on housing financialisation broadly agrees that states have been supportive in enabling housing financialisation (see below), the political histories of financialisation still require further investigation. In particular, the relationships between local state institutions and institutional investors have only been examined in a piecemeal manner, typically with a focus on singular policies or events (e.g. deregulation or public stock sales). However, while the notion that states have been crucial in enabling, shaping and supporting financialisation is well established, the question of how this relationship develops in the long term remains to be studied.

In this article we aim to fill this gap by investigating the relationship between global corporate landlords and local policies in Berlin over a long-term period. While we are aware of the particularities of the German variant of housing financialisation (Aalbers et al., 2023; Wijburg et al., 2018), we argue that Berlin is where the relationship between local state institutions, politicians, social movements and financial investors can be observed most readily. Examining the political history of housing financialisation in Berlin, we find that local governments are not merely supportive of housing financialisation. Instead, states and institutional investors are involved in complicated and contradictory logics, leading to significant instability in their relationships.

The research methodology used for this article includes document analysis, media research and expert interviews. We have analysed the annual reports of the six largest institutional landlords in Berlin since 2012 as well as key public policy documents, such as parliamentary questions, expert statements and (selectively) minutes from commissions, hearings and parliamentary debates. Using media coverage in both local daily newspapers and specialist journals (e.g. Mietermagazin or Mieterecho), we have created a timeline of important local political events related to financial investors, which we used to create the periodisation discussed below. In addition, we have conducted five interviews with local politicians, housing lobbyists and housing market experts 2 and participated in numerous events (panel discussions, expert workshops and demonstrations) that were important for the field. Both authors have studied Berlin’s housing policies for nearly three decades now, so we can also build on substantial background knowledge.

The article proceeds as follows. First, we bring together and compare the central arguments of the recent housing financialisation literature with older contributions on urban governance in order to lay the foundation for a theoretically informed investigation of the case to be studied. This is followed by an introduction of the housing financialisation landscape in Berlin. Here, we focus on corporate landlords and describe their main business strategies. In the main section of the article, we reconstruct the development of the relationships between Berlin’s government and major corporate landlords over the subsequent two decades. In the remainder of this article, we derive conclusions and call for a more open-ended approach in research.

(Financialised) private capital and local politics

Recent studies have widely documented that institutional investors play an increasingly important role in rental housing markets (Aalbers, 2016; August and Walks, 2018; Beswick et al., 2016; Fields, 2017; Fields and Uffer, 2016; Nethercote, 2019). Much analysis has revealed ‘how the state has enabled, promoted and shaped housing financialization’ (Tulumello and Dagkouli-Kyriakoglou, 2023). This role of the state has been discussed in three ways.

First, representing the lion’s share of contributions, it has been shown that housing financialisation has been enabled and supported by a broad set of local and national policies, including new regulations on securitisation and financial vehicles (Aalbers, 2016; Aalbers et al., 2023; Beswick et al., 2016; Charles, 2019; Fields, 2017; Gotham, 2009), social housing privatisation and rent deregulation (August and Walks, 2018; Bernt et al., 2017; Fields and Uffer, 2016; Lima, 2020) as well as the financialisation of public and non-profit providers (Aalbers et al., 2017; Beswick and Penny, 2018). On this basis, manifold contributions take the notion that states have acted as facilitators of financialisation to be a matter of common sense.

Second, there is wide agreement that the ways in which states have engaged with institutional investors is geographically uneven, heterogeneous, hybrid and prone to diverse configurations across countries and housing systems (e.g. Aalbers et al., 2023; Aveline-Dubach, 2020; Fernandez and Aalbers, 2019; Tulumello and Dagkouli-Kyriakoglou, 2023). It has also been shown that financialisation operates based on the interplay between various levels of governments (Belotti and Arbaci, 2021; Holm et al., 2023) in such a way that multi-scalar analysis is necessary. In this vein, the literature has also clearly demonstrated that state policies towards institutional investors have not necessarily been coherent ideological projects or suites of policy measures; rather, they have operated through a multiplicity of piecemeal, ad hoc and pragmatic processes (Byrne and Norris, 2022; Oxenaar et al., 2024), which combine a wide set of actors, state departments and scales. Consequentially, it has been argued that financialisation must be understood as embedded within the ‘playing fields’ (Kadıoğlu and Listerborn, 2025) of local and national housing policies in which numerous structural or strategic selectivities are in place, leading to a broad variety of state–investor relationships (Alexandri and Hodkinson, 2025).

Third, various literatures have studied how social movements are challenging financialisation (e.g. Berfelde and Heeg, 2024; Bond, 2024; Card, 2022; Kusiak, 2024; Vilenica et al., 2024; Vollmer and Gutiérrez, 2022; Wijburg and Waldron, 2024). State actions are a central focus in this literature, typically in relation to how greatly they are affected and challenged by social movements.

Against the background of these literatures, in summary, the role of the state vis-à-vis housing financialisation is a recurrent theme in geography and urban and housing studies. While the role of the state in enabling financialisation has received the most attention, most researchers would also agree with Aalbers’ (2023) warning that ‘both finance and the state are too complex, layered, ‘multi-actored’, scaled and variegated to reduce their interdependence to one type of relationship’ (Aalbers, 2023: 798). Nevertheless, there are few empirical studies analysing the complexities and contradictions involved in the relationship between institutional investors and politics on the ground. In our view, there are three problems at hand: (a) there is a tendency to focus on cases in which the role of the state has been to support financialisation; (b) most contributions focus on either local or national decisions, with very few examples of multi-scalar analysis (see Belotti and Arbaci, 2021, for a noticeable exception); and (c) there is a strong bias towards analysing one-time events or individual policies. In consequence of these limitations, we know very little about why, when and how state actors engage with financialisation and their motives, capacities and restrictions when doing so. Thus, although more and more scholars have voiced a clear interest in studying how financialisation can be ‘tamed’ (Norris and Lawson, 2022) or even how ‘de-financialisation’ can be (Wijburg, 2021) achieved, understanding state actions in relation to financialisation has remained cursory. This, we argue, is particularly worrying at the local level, where contestations of housing financialisation are most often articulated.

This state of the art is, in some respects, surprising, as ‘urban political economy’ and ‘governance’ approaches, which blossomed from the 1970s to the 1990s, have long conceptualised state–capital relations at the local level. In particular, the ‘growth machines’ argument (Molotch, 1976) has many parallels with the discussion outlined above, as it assumes that the main public and private actors will always tend to build tight-knit coalitions at the local level. In a similar vein, ‘Urban Regime Theories’ (Elkin, 1987; Stoker, 1995; Stone, 1989) and other ‘bargaining approaches’ (DiGaetano and Strom, 2003; Kantor and Savitch, 1993; Pierre, 1999) have hypothesised a mutual dependency on the part of politicians and businesspeople, which motivates them to form ‘regimes’ or ‘partnerships’. Finally, contributions from urban governance literatures (e.g. Le Galès, 2002; Pierre, 1999, 2005) have demonstrated that local governments have become increasingly involved in network building with the local business community. In summary, past urban studies literatures have developed quite a few advanced conceptualisations that enable an analytical understanding of the state–capital nexus at the local level. However, much of this literature dates to the times before housing financialisation took off, and its conceptualisations have been developed against a background of locally nested businesses. Thus, the degree to which these ideas, which were developed four decades ago, still hold for the globally active, financialised landlords discussed in this article remains to be seen.

In this study we use the above-mentioned ‘urban political economy’ literature as a point of reference. We argue that a theoretically informed viewpoint outside of current debates in financialisation studies can inform an up-to-date understanding of the relationships between financialised housing companies and local states and assist in formulating more theory-based and, therefore, testable and comparable findings. We do not aim to ‘copy and paste’ this literature. Instead, we engage the theoretical apparatus of past studies as a contrasting foil, which enables us to see the relationship between private financial capital and the local state more clearly. On this basis, we formulate three hypotheses that can be tested using empirical observations:

Both local governments and financial investors should share an interest in local growth, the former because their tax base is increased, new jobs are provided or public policy problems (e.g. a lack of affordable housing) can be addressed and the latter because local growth is a condition for profit-making (see Harvey, 1989; Molotch, 1976).

Both local governments and financial investors should only be able to reach their goals in tandem: investors require assets, regulations and a supportive business climate, whereas governments are interested in the taxes generated by business activities, jobs and housing and infrastructure provision (see DiGaetano and Strom, 2003; Elkin, 1987; Kantor and Savitch, 1993; Pierre, 1999; Stone, 1989).

Because of this mutual dependency, local states and private capital should engage in forms of local cooperation and build lasting networks, with the aim of increasing their capacities to make ‘governing decisions’ (Stone, 1989). These networks should go beyond an ‘issue-by-issue’ format. Rather, ‘. . . once formed, a cooperation (would) become(s) something of a value to be protected by all of the participants’ (Stone, 1989: 8–9).

In what follows we will examine the degree to which these hypotheses hold true for the relationships between institutional investors and local politicians in the case of Berlin.

Global corporate landlords in Berlin

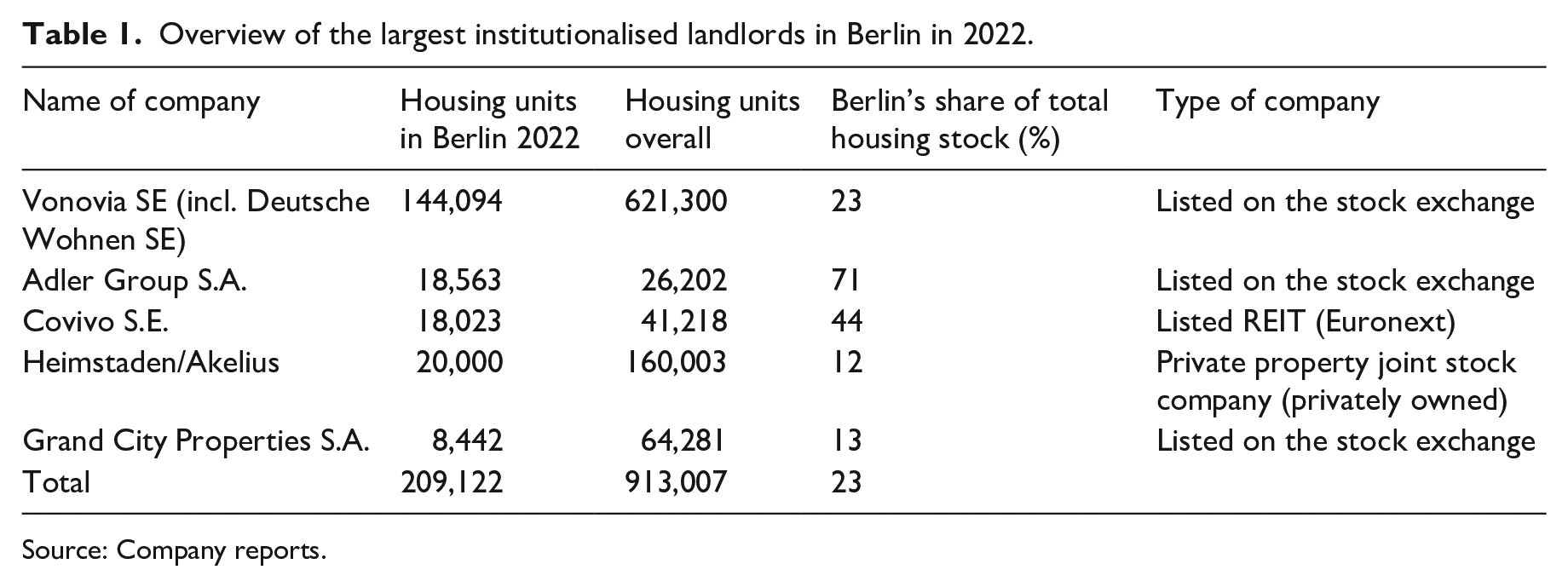

In Berlin, financialisation has primarily been enabled through the sale of more than 200,000 municipal rental flats (Uffer, 2013), both in the form of en bloc deals and through the sale of an entire company (Aalbers and Holm, 2008). Most purchasers were private equity companies, and the number of housing units held by global corporate landlords in Berlin is estimated at around 330,000 flats (Trautvetter, 2020: 9), which corresponds to a share of around 17 per cent of the total housing stock (20% of rental flats). After several rounds of resales, most of the privatised housing stock is now concentrated in the hands of five major companies, four of which are listed on the stock exchanges. Together, these companies hold around 210,000 housing units (see Table 1).

Overview of the largest institutionalised landlords in Berlin in 2022.

Source: Company reports.

The major institutional investors that are active in Berlin all have supra-regional portfolios. At the same time, the share of properties held in Berlin is subject to considerable variegation. For example, the Adler Group is largely concentrated in Berlin, whereas business in Berlin is less important for Grand City Properties. Consequently, changes in Berlin’s housing market and housing policies affect the investors to very different degrees.

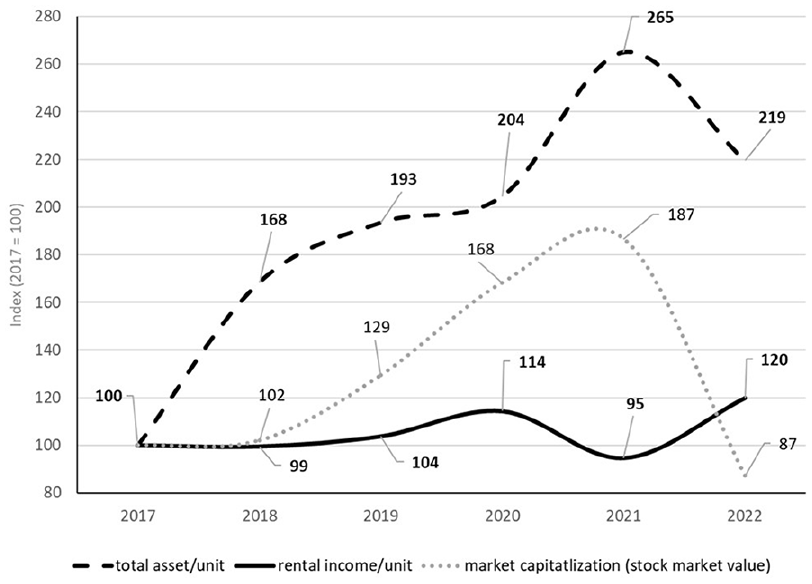

Except for Heimstaden, the corporate landlords that are active in Berlin are all listed on the stock exchanges. The consequences of this can hardly be overestimated, as the yields of these investors are, to a large degree, mediated via financial markets, rather than realised rental income. Figure 1 shows that rental incomes and stock market values have developed relatively independently of one another for the largest financial landlord in Berlin. This demonstrates the central role of stock valuations in financial markets, which sets the institutional investors in stark contrast to traditional property owners.

Comparison of key economic indicators for Vonovia SE (per index, 2017–2022).

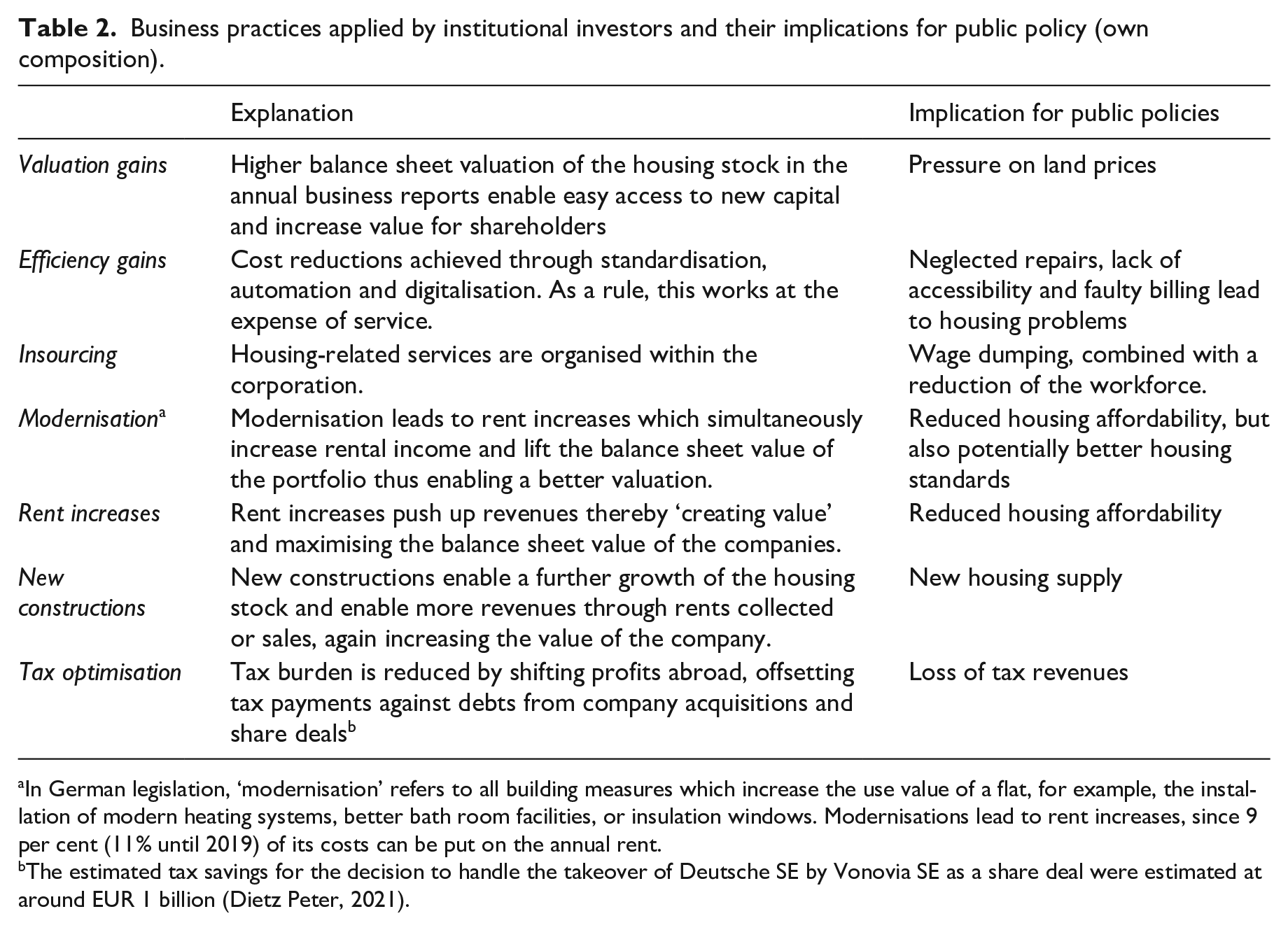

Their business strategies are intended to both increase the revenue generated from stocks acquired and maximise the stock value of the company. In reality, these strategies are implemented in the form of mixed, changeable, and sometimes contradictory ratios of practices, which are outlined in Table 2. All these practices have significant implications for public policy, which we highlight in the right column of the table.

Business practices applied by institutional investors and their implications for public policy (own composition).

In German legislation, ‘modernisation’ refers to all building measures which increase the use value of a flat, for example, the installation of modern heating systems, better bath room facilities, or insulation windows. Modernisations lead to rent increases, since 9 per cent (11% until 2019) of its costs can be put on the annual rent.

The estimated tax savings for the decision to handle the takeover of Deutsche SE by Vonovia SE as a share deal were estimated at around EUR 1 billion (Dietz Peter, 2021).

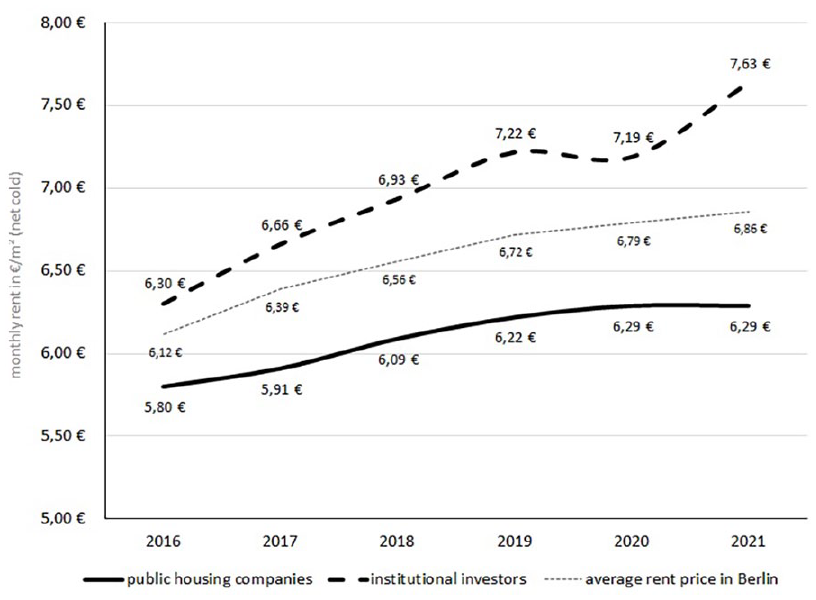

As this short table demonstrates, the impact of institutional housing investment on public policy is considerable. Already, in theory, land price increases, worsened housing affordability and maintenance issues, job losses and a reduction of tax revenue act as barriers to potential improvements in housing stock through modernisation and new supply. While it would require a separate paper to discuss institutional housing investors in Berlin in detail (see Holm and Bernt, 2023; Zimmermann, 2023), it is clear that the advantages that institutional investors have offered to the local state are fairly limited. Of the Big Five (i.e. the largest companies active in Berlin), only Covivio, Deutsche Wohnen and Vonovia are actively engaged in new construction. To date, however, they have completed only a total of 640 flats. If this is compared to the 21,409 flats that have been built by Berlin’s municipal housing companies between 2014 and 2021 (WVB, 2022: 21), it becomes clear that the investors’ contribution is rather negligible in this respect. At the same time, institutional investors have been responsible for significant rent increases, thus worsening affordable housing options. Compared both to public housing companies and the general market, the rents charged by institutional investors from 2016 to 2021 were not only significantly higher but also increased more quickly (Figure 2).

Rent levels compared (Berlin, 2016–2021).

The taxes collected from institutional investors are also very low. Vonovia, the institutional landlord with the largest portfolio in Berlin, recorded total revenue of EUR 6.26 billion for 2022, while it only paid income taxes of EUR 188.2 million. This corresponds to a tax rate of only 3 per cent (Vonovia, 2023: 102; 146). A recent study by the NGO Finanzwende Recherche reported similar rates for other institutional landlords (Gerrard et al., 2023: 53–55).

To summarise, it is no exaggeration to say that institutional investors have done very little to solve existing housing problems in Berlin. It is not self-evident why politicians should have an interest in co-operation. At the same time, the analysis has shown that the profitability of financialised investments depends to on a broad variety of factors that are only partially influenced by local conditions.

Policymaking between regulation, expropriation and partnerships with institutional investors

What is the impact of this constellation on the relationship between institutional investors and Berlin’s government? When and how did Berlin’s public administrations and politicians engage with financial investors in housing, and why did they do so? The following section examines these dynamics over the subsequent two decades. For the sake of simplification, we identify five phases. 3

Phase 1: strange bedfellows (2000–2005)

The de facto relationship between the government of Berlin and institutional investors began in the early 2000s, when Berlin sold large portions of its municipal housing stock to institutional investors. 4 Most notable in this respect was the sale of an entire municipally owned housing company (Gemeinnützige Siedlungs- und Wohnungsbaugesellschaft Berlin mbH, GSW), with its 75,000 housing units, to a consortium composed of Whitehall (Goldman Sachs) and Cerberus in 2004.

Berlin faced enormous budgetary problems in the early 2000s. At the same time, the local population was stagnating in terms of numbers. Consequentially, many politicians saw no need for a large amount of municipally owned housing stock and welcomed the chance to generate additional income through its sale. This clearly resonates with an interview quote in which a former member of the governing coalition described the privatisation as primarily a ‘response to a public budget emergency’ (Interview 4). For the investors, the deal was also lucrative because large stocks could be acquired at discount prices. 5

With this deal, Berlin’s government and financial investors would, however, become bedfellows. Altogether, the share of municipally held stocks in relation to the total stock went down from more than 35 per cent (1991) to approximately 17 per cent of all housing units (2021; Holm et al., 2023: 23). A major consequence of the privatisations was a massive reduction in steering capacities regarding housing provision. At the same time, the investors buying stock in Berlin exposed themselves to a broad range of national and local regulations, as Germany’s rental market is highly regulated and rent regulations are subject to politicisation and frequent change (see Bernt, 2022: 77–97).

Phase 2: ignorance and growth (2005–2015)

In the early 2000s, these implications were scarcely noted. This only changed gradually over time. With housing affordability becoming a more serious issue from 2010 onwards, more and more reports of a lack of services and repairs, under-maintenance and drastic rent increases in the homes managed by institutional investors received attention. Mostly, this has been the outcome of press releases by tenant organisations and journalistic work, but the pressure applied by a growing number of tenant initiatives that oppose increasing rent burdens is important as well. The reaction of politicians was rather slow. The then-Mayor of Berlin, Klaus Wowereit, became famous in this respect when he declared that increasing rents were good because they were a sign of economic recovery.

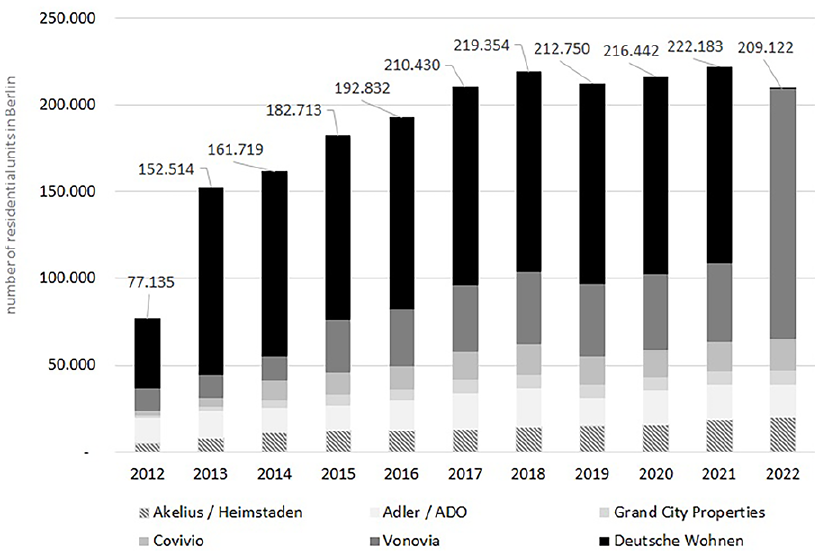

Our interviewees agreed that there was little contact between politicians and institutional investors during this period. It was only with the planned flotation of the formerly public GSW housing units that politicians were called upon to agree to the sale. A housing business lobbyist remembers that the Berlin Senate supported an acquisition by Deutsche Wohnen ‘because this is a company that will have its headquarters here in Berlin’ (Interview 5). Thus, the ideologies described by the ‘growth machine’ theory can be found in Berlin as well (Figure 3).

Number of housing units owned by large institutional investors in Berlin 2012–2022.

To sum up, from the point of view of the institutional landlords, their first decade in Berlin was a lucrative one. Their stock values grew by a factor of 4–5, and massive profit was made through rent increases and maintenance and service cuts. Public policies were inviting and supportive or, at least, passive at this time.

Phase 3: recognition and re-regulation (2015–2020)

This situation was to change considerably in the second half of the 2010s. Due to city-wide rent increases, growing protests and widespread media coverage of the housing crisis, the housing issue became a central topic in local politics around 2015. The result was a change to a red-red-green state government after local elections in 2016. In this constellation, the Left Party gained control over the influential Urban Development Department and began to push for a series of tenant-friendly reforms (see Holm, 2021; Vollmer and Kadi, 2018). However, it quickly became clear that the leeway for new policies was severely limited by the national government. Thus, the introduction of a local rent cap (Mietendeckel) was stopped by the Federal Constitutional Court in 2021, and the right of first refusal regarding housing sales was abolished by the national government in 2022. In a climate of growing confrontation, this was seen as clear defeat by many observers, and the limits of local regulations were becoming evident.

At the same time, tenant movements grew stronger. In joint protests in 2018, activists and residents of a former social housing estate (Otto-Suhr-Siedlung) in Kreuzberg pushed through a formal agreement between the Friedrichshain-Kreuzberg district and Berlin’s then-largest landlord, Deutsche Wohnen, to limit rent increases after renovations of 3000 flats (Strobel, 2019). Local conflicts with Deutsche Wohnen became frequent and were resolved in less harmonious ways. In parallel to these local protests, a campaign entitled Expropriate Deutsche Wohnen & Co was founded in 2018. It was immediately supported by many Berlin tenant activists and organisations as well as by the Left Party, which was part of the governing coalition, and gained stunning support within a short time.

Interestingly, institutional investors did not seem greatly bothered by this development initially. On the contrary, they ignored or even attacked existing and potential regulations in an offensive way. For example, when the state parliament of Berlin invited the head of Deutsche Wohnen to a discussion of the rental practices and rent increases promoted by his company, he did not even attend. 6 Naturally, this was taken as an affront by many local politicians. To make matters worse, Deutsche Wohnen even went to the courts and appealed against the widely accepted rent index 7 (Mietspiegel) in 2019. Although Deutsche Wohnen lost this court case, the case made it clear that institutional investors did not accept long-established lines of consensus regarding German housing policies.

Thus, the third phase is marked by visible contradictions. On one hand, local politicians became more aware of the problematic business practices of financialised landlords, and social movements increased political pressure. The search for an appropriate strategy at the local level was, however, complicated by a lack of legislative powers, open attacks by the more conservative national government and substantial disagreement between the ruling parties in the red-red-green coalition governing Berlin. 8 On the other hand, it seems that the implications of growing political pressure were regarded as manageable by the corporate landlords. During the debate, it became increasingly clear that the stronger regulations aimed at by leftist politicians and tenant groups would, at best, be implemented with cutbacks and delays and would not become a problem in the short term. Even more importantly, stock values were still increasing, so potential losses from tougher rent regulations could be offset by valuation gains in the stock markets. In sum, the situation involved less favourable circumstances than in the previous decade but still seemed to be manageable.

Phase 4: between partnership and expropriation (2020–2023)

For the institutional investors, these contradictions became more challenging after the local elections in 2021. At that time, on one hand, the tenant movement gained an enormous victory with a successful referendum on the expropriation of private-investor-owned stock consisting of more than 3000 flats (for details on the campaign, see Kusiak, 2024; Vollmer and Gutiérrez, 2022). At the same time, the Social Democrats narrowly gained power by running a mayoral candidate who openly declared that expropriation would be a ‘red line’ for her government and argued for ‘cooperation instead of confrontation’. 9

Notwithstanding these clear statements, the successful referendum could not be ignored. The red-green-red state government thus ultimately agreed on a compromise, creating a commission of external experts to explore ‘possibilities and ways’ regarding the planned socialisation. The report was finally published in June 2023 (Expertenkommission Vergesellschaftung, 2023) and, to the surprise of many conservative observers, legal experts stated that the plans for expropriation were entirely compatible with the German constitution.

The local elections held in spring 2023 intensified this contradiction, as they brought a conservative coalition of Christian Democrats and Social Democrats to power. Leading politicians in the new government clearly announced their unwillingness to implement the referendum. In reaction, the Expropriate Deutsche Wohnen & Co initiative is preparing for a second referendum, which would implement an expropriation law instead of demanding it from the government as the first referendum did.

In stark contrast to the confrontational course of the initiative, the government led by the Social Democratic Party (SPD) proactively searched for partnership and formed an ‘Alliance for New Construction and Affordable Housing in Berlin’ with at least some institutional investors in mid-2022. Both Berlin’s largest tenants’ organisations and the companies Heimstaden, Grand City Properties and Covivio, which, together, own more than 50,000 flats, refrained from joining the initiative. The most important points agreed upon were a commitment by the participating companies to build at least 100,000 new residential units by the end of 2026, subsidies for up to 5000 social housing units per year by the state of Berlin, the commitment of 30 per cent of all lettings to low-income households, a cap on rent increases for low-income households and an expansion of the ‘protected housing segment’ for homeless people to 2500 flats (Senatsverwaltung Berlin, 2022).

How should this be interpreted? The reactions of local authorities and local politicians at this time are characterised by obvious contradictions. On one hand, the Left Party, which was part of the governing coalition, spoke out for expropriation and actively supported the referendum on the expropriation from major landlords. On the other hand, the Social Democrats and Christian Democrats cooperated with the same landlords and even built an official Alliance with them. Instead of clear support of business, as the growth machine and regime theories would have predicted, the local policy arena was thus marked by intensive contestations, even within the local government, and mutually exclusive strategic orientations. In this context, it is difficult to determine the motives of the political elites supporting a partnership with institutional investors. In fact, little explanation of why and how cooperating with the global corporate landlords could assist in solving the existing housing affordability crisis can be found in public statements. Instead, arguments brought forward targeted regulation in general, attacked ‘socialist expropriation fantasies from the day before yesterday’ (as the recent mayor of Berlin put it, see Süddeutsche Zeitung, 2021) or called for cooperation instead of confrontation. Interviews conducted with politicians indicated short-term political motivations, such as maximising votes by showing a clear profile and opening up new career opportunities for selected politicians. One attempt to explain the SPD’s positioning was made by a former coalition partner who suspected ‘[. . .] it was [based on] a belief in their propaganda and an inability to find their way back from election campaign mode’ (Interview 3).

Phase 5: broken promises (since 2023)

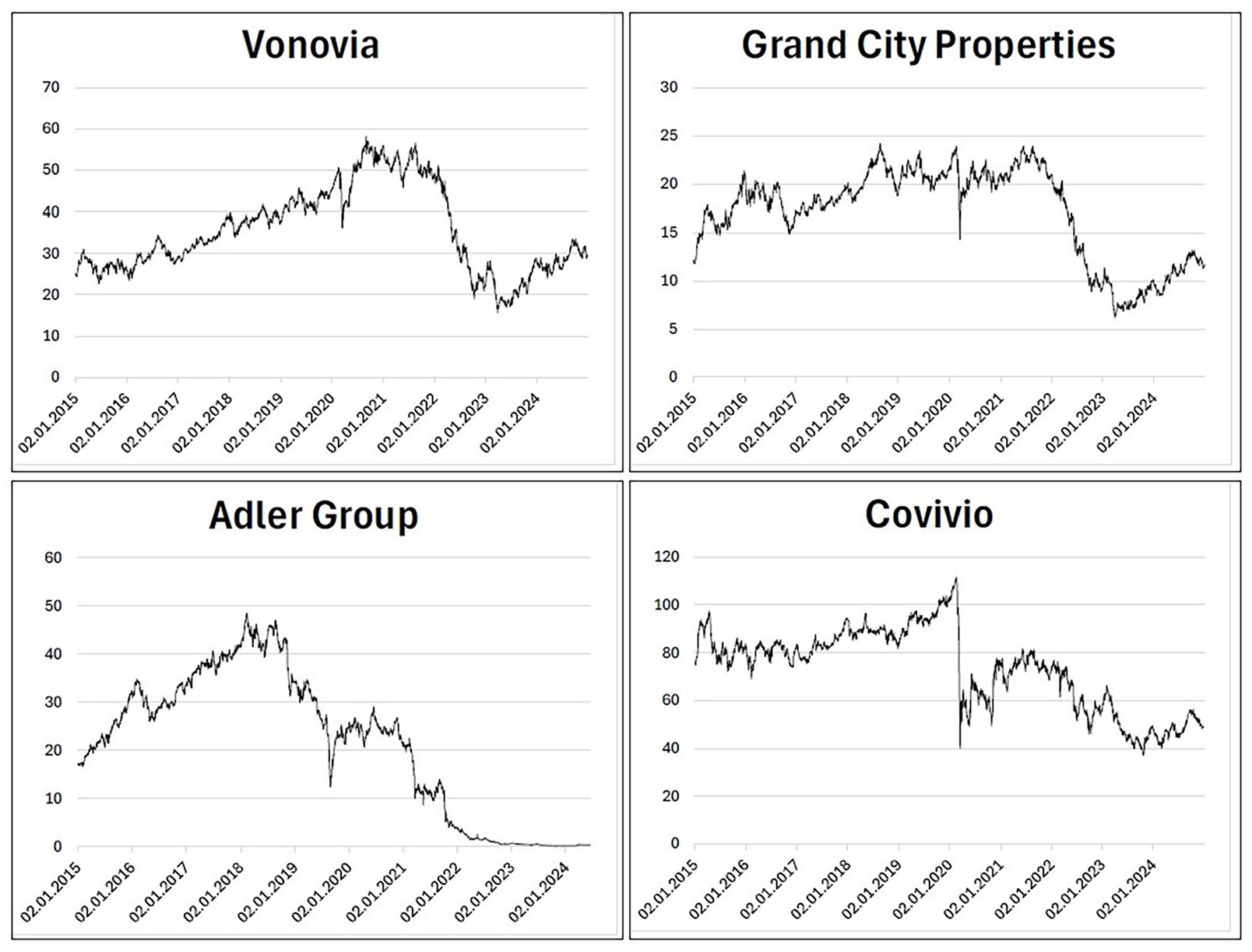

The new partnership proved to be short lived because of the unfavourable business climate resulting from a mixture of inflation, energy price increases and rising interest rates since 2022. In particular, the tighter fiscal policy of most central banks proved detrimental to the business of institutional investors. All companies have suffered brutal declines in share value, and one of the Big Five has even been charged with accounting manipulation (Financial Times, 2023a; 2023b). This altered environment was very aptly expressed by one fund manager when he described Vonovia, which is the biggest of the institutional investors in Berlin, as ‘. . . a skyscraper on shaky foundations rather than a DAX 10 -listed company’ (Handelsblatt, 2023).

Figure 4 illustrates this statement using the stock value charts of the major listed landlords in Berlin. It shows that the crisis of constantly rising valuations had already begun in 2019 (Adler), 2020 (Covivio) and 2021 (Vonovia, GCP). In 2022, this crisis accelerated, and all companies faced brutal stock value crashes.

Stock market values of Vonovia, Adler Group, Covivio and Grand City Properties.

This new business climate took a heavy toll on the agreements achieved in the Alliance for New Constructions and Affordable Housing in Berlin. In January 2023, Vonovia declared that it would freeze all new construction activities and not build 60,000 housing units as promised. In July 2023, it became public knowledge that Vonovia and Deutsche Wohnen had undermined the agreement to limit rent increases to no more than 2 per cent per year for WBS-eligible households by not informing their tenants regarding this cap when they sent out rent increase notices to 12,000 households. One year later, in July 2024, Vonovia announced, without prior consultation with politicians, that it would generally ignore the cap on rent increases and sent out rent increases of up to 15 per cent. Against this background, even representatives of the housing business lobby ‘(do) not see any added value of the alliance at the moment’ (Interview 5), as one described in an interview.

Echoing this evaluation, the Adler Group left the Alliance in August 2023 to allow massive rent increases for their stocks. Covivio, which had only joined the Alliance after some delay, also announced massive rent increases, in September 2023, for several hundred households, which it partially withdrew after protests. Drastic rent increases have also been reported by Heimstaden and Grand City Properties, which did not join the coalition. In sum, all promises made have been broken in a very short time, and only 1 year after its formation, the newly formed Alliance between Berlin’s government and the institutional investors practically lies in ashes.

Discussion

What does this development reveal about the role of institutional investors in the local policy arena? Examining the hypotheses formulated at the beginning of this article, the following points can be made: First, regarding the corporate landlords, we can observe two orientations simultaneously. On one hand, stock market valuations are crucial. These are widely uncoupled from local rent revenues and, instead, reflect global interest rates, the business climate and financial market dynamics. On the other hand, asset managers have ‘an overriding interest in maximising their fees and thus their assets under management’ (Braun, 2022: 643). This can be achieved by either expanding the stock controlled or maximising returns so that asset owners are not motivated to move their money elsewhere. Both these strategies depend on local market conditions (e.g. property acquisition and rent revenues). This creates a double-bind for the companies. Their interest in maximising the assets controlled and the revenues achieved makes them vulnerable to changing regulatory conditions (i.e. rent laws, planning regulations and expropriations). At the same time, changes in the global financial markets can easily outweigh these local circumstances. In consequence, investors do as much as necessary to appease the local political arena and as much as possible to satisfy their stockholders. Depending on the geographical variation of their properties, companies are, however, differently affected, which explains why some companies were more likely to join the Alliance than others. The implications of these structural conditions were clearly reflected in the interviews. Thus, all interviewed partners reported intensive lobbying activities being performed by institutional investors at both the national and local levels. Interviewees describe ‘. . . a very intensive nurturing of the political arena’ (Interview 1); ‘telephone diplomacy’ (Interview 2), with a ‘direct line to the government mayor’ (Interview 5); engagement in ‘small communication business’ (Interview 5) and numerous ‘gives and takes’ (Interview 3) between local politicians and institutional investors. Notwithstanding these efforts, corporate landlords have nevertheless remained an unreliable partner for local politicians. After acquiring their stocks, they were not especially interested in cooperating with local politicians for a long period, and this only changed under pressure. When an Alliance was finally formed, it was broken in the blink of an eye when conditions in the financial markets changed.

For politicians, this relationship has been difficult. The mere weight of corporate landlords in Berlin’s housing market involves opportunities for deals that can be useful for political careers and election campaigns. Interviewees pointed to several instances of such ‘self-serving’ cooperation. Political support for a favourable business climate has also been in line with the ideological orientations of many politicians, especially those on the right of the political spectrum. At the same time, in the long term, institutional investors have offered very little. Their contribution to affordable housing provision is minimal, while their impact on increasing rents is substantial. Tax avoidance is a problematic issue, as are the jobs and wages provided. Moreover, for local politicians, institutional investors are not easy to operate with. Often, they control resources that are superior of those held by local administrations and can easily outmanoeuvre local politicians. With an eye on the large legal departments of the Big Five, one interviewee thus described ‘. . . an asymmetry with regard to resources available to influence opinion-forming’ (Interview 5). The situation was also vividly described by a lawyer interviewed by a local newspaper: ‘The Champions League is playing against the District League here, with professionals like Vonovia boss Rolf Buch at the helm, who can dribble out state politics as much as they like’ (Walther, 2024). In sum, while the investors have become too large to be ignored and cooperating with them can have benefits, these are outweighed by a lack of reliability and an imbalance of capacities, which works to the detriment of local politicians. In addition, due to their notorious role as rent sharks, corporate landlords have become very unpopular in Berlin, and this has made collaborations with institutional investors a potential liability in local elections. These factors are endangering long-term partnerships. In Berlin, we find short-lived collaborations but nothing that comes close to the regimes described in the urban governance literature.

Conclusion

In conclusion, this study provides insights into the long-term relations between institutional investors and local states. A key lesson from this research is that the assumption of a conflation of state interests and the interests of financial investors is being undermined. Over a long period, it appears that local governments receive too little and are, at the same time, placed under too much pressure (e.g. social movement contestation, multi-level government coordination and party competition implementation problems) to be merely supportive of housing financialisation. The same is true for investors who must manoeuvre the stormy waters of international financial markets and, simultaneously, engineer a supportive local business climate. For both sides, the stakes are too high to build stable, long-term partnerships. What we find, instead, are complicated and contradictory logics that lead to significant instability. The notion that states have been crucial in enabling, shaping and supporting financialisation, which is widespread in the literature, may therefore help in describing the conditions for the market entry of institutional investors. However, it appears to be too narrow to explain the relationship between these investors and the state in the long run.

While, empirically, the findings we have presented are only valid for the case we have studied, the insights of this study extend more broadly to the current literature on housing financialisation as they underline the heterogeneous, hybrid and contested nature of the relationships between institutional investors and local states. Examining the case of Berlin, in this study we have highlighted several factors driving the dynamics between local states and institutional investors. The degree to which these factors are only valid for the case of Berlin or have more general relevance remains to be examined by more comparative research designs in future studies. The ‘playing fields’ (Kadıoğlu and Listerborn, 2025) of housing policies are complex, and therefore, much remains to be done to explore the complexities, rationales, opportunities and restrictions faced by both policymakers and institutional investors when encountering financialisation at the local level.

Footnotes

Authors’ Note

Previous versions of this paper have been read and commented on by the participants in a workshop on financialisation and public policy in Brussels in November 2023 as well as Manuel Aalbers, Lisa Vollmer and two anonymous reviewers. We are grateful to all of them, as their reviews, critiques and comments helped to improve our original manuscript considerably.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was funded by SciencePo. Urban School in 2023.