Abstract

This article analyses the state’s contemporary role in capital accumulation in the development of public land. In the literature, it is argued that the state goes beyond a regulatory role and participates in the capital-accumulation process as the owner of land or financial assets derived from land-based revenue, thus transforming from an external to an internal actor. It is argued that, in this way, the state governs urban development and the distribution of the land rent. This article argues that in the privatisation of land before development, the state is involved as the regulator and landowner, as suggested in the literature; however, when the state participates in the development of public land through public-private partnerships led by entrepreneurial state agencies and state-owned companies, it is also involved in production, trade and finance. In the latter case, the state manipulates the distribution, and its revenue consists not only of land rent but also of profit. Based on Marx’s analysis of the total circuit of capital, which does not include the forms of state involvement, the article attempts to elucidate contemporary transformations in the state-capital relationship in the development of public land. It claims that the new government strategies aim to address problems of capital accumulation and state finance through land development. The article is based on an analysis of official data on the practices and revenue of three state agencies engaged in land privatisation and development in Turkey.

Keywords

Introduction

This article analyses the changing role of the state in the development of public land and its new relationships with capital. It approaches these transformations as current trends of entrepreneurial urban governance. This concept refers to new forms of urban governance generated by governments’ efforts to create favourable conditions for capital accumulation and to meet social demands in an environment of inter-urban competition intensified by global capital flows and economic and fiscal erosion (Hall and Hubbard, 1996; Harvey, 1989a; Jessop, 2002; Leitner, 1990; Molotch, 1976; Peck and Tickell, 2002; Swyngedouw et al., 2002). It is also claimed that, rather than a single logic of capital accumulation, entrepreneurial governance forms are shaped by struggles between different fractions of capital and alliances and conflicts between state managers and capitalists (Gotham, 2009; Kaika and Ruggiero, 2016; Yeşilbağ, 2022).

Current studies show that the state’s treatment of public land and its role in land development has changed (Beswick et al., 2016; Beswick and Penny, 2018; Byrne, 2016a, 2016b; Çelik, 2023; Christophers, 2017; Erol, 2019; Penny, 2022; Serin et al., 2020; Shatkin, 2017; Yeşilbağ, 2019, 2022). Evidence shows that governments treat public land as fictitious capital, commodify social uses, privatise public land or financial assets derived from land-based revenue and engage in land development through state-owned companies and public-private partnerships (PPP). In these studies, it is claimed that, the state goes beyond its role as a rule-maker and facilitator and assumes the role of landowner, hence transforming from an external actor that provides the necessary conditions for capital accumulation to an internal actor that participates in capital accumulation. It is argued that, in this way, the entrepreneurial state increases its capacity to drive urban development and the distribution of revenue generated in built environment production. The shortcoming of these analyses is that they do not identify the significant difference in the role of the state between the privatisation of land and of building units after development and that they focus only on state’s landownership and the land rent. In this article, it is argued that in the privatisation of land, the state is involved as a landowner and shapes the distribution of land rent, whereas in the development of public land, through PPPs managed by state agencies or state-owned companies, it is also involved in production, trade and finance and shapes the distribution of profits as well as land rent. The importance of revealing this difference is to accurately define the changing role of the entrepreneurial state in capital accumulation. It also helps to analyse the interest alliance between the state and capital formed by the participation of the state in various stages of the capital-accumulation process. Finally, it illustrates the impact of acute problems in capital accumulation and state finances on the transformation of state structures and public land policies (Adisson, 2018).

The reason for the poor knowledge on the new state-capital relationships in for-profit development of public land is the lack of clarification of the mechanism of revenue generation and distribution in built environment production. Starting from Marx’s (1991a, 1991b, 1991c) analysis of the total circuit of capital, which does not include the forms of state involvement, this article attempts to explain the way contemporary governments are involved in the development of public land and the source of government revenue. In different periods of capital accumulation, the ways of state involvement change. Contemporary transformations in neoliberal processes are subject to intense debate (Castree, 2006; Davies and Gane, 2021; Peck et al., 2009). The idea of enriching the concepts with empirical content motivated this study. The study is based on an analysis of the practices and revenue of three central government agencies engaged in land privatisation and development in Turkey using data compiled from their regulations and annual activity reports. The article first examines how the changing role of the state is discussed in the literature and presents the article’s arguments. Next, the development of public land policy in Turkey is presented to contextualise the data. The presentation of the research method is followed by the analysis of the data and conclusion.

The focus in the literature on the participation of the state as landowner and on the land rent

Studies examining the role of the state in privatising land and land-based financial assets argue that, under financial constraints and increased obligations to revitalise capital accumulation, the state goes beyond its external role as a regulator and facilitator and intervenes as an internal actor that owns land and financial assets. Christophers (2017) shows that the central government in the United Kingdom led the transfer of land owned by various government agencies to the private sector and argues that the role of the state changed when it sold public land to private companies that treated it as a financial asset. Beswick et al. (2016) and Byrne (2016a, 2016b) show that state asset-management companies took over assets, whose financial ties had become problematic after 2008, in exchange for government-guaranteed securities or recapitalisation, and transferred them to multinational financial institutions after restructuring. They argue that the role of the state changed when it bailed out national banks from troubled property and debt, made the real estate market profitable again and created more direct circuits between urban real estate and global capital flows through its companies. While these studies demonstrate the state’s role in opening up land and land-based financial assets to capital accumulation, the state’s contemporary role in land development is out of their scope.

The state’s involvement in for-profit land development has also been studied. Erol (2019), Yeşilbağ (2019) and Çelik (2023) analyse how the central government agency responsible for housing policy in Turkey manages low-cost housing production and participates in for-profit land development through a state-owned real estate investment trust. Serin et al. (2020) examine for-profit housing projects in Istanbul initiated by these agencies. Shatkin (2017) shows that in Chongqing, government agencies and state companies are involved in for-profit real estate development on public land in partnership with corporate entrepreneurs. Beswick and Penny (2018) analyse how London city councils produce mixed-ownership housing in the place of existing public housing through their off-balance-sheet companies. However, these studies’ conclusions about the role of the state do not differ effectively from those of aforementioned analyses of privatisation. They also focus on state’s landownership and the distribution of land rent. In Çelik’s (2023) conclusion about the state’s treatment of public land as a financial asset and Shatkin’s (2017) identification of the new government strategies as land monetisation and state’s revenue source as land rent, analysis of new relationships established by governments in the production, trade and finance phases of land development and sources of revenue other than land rent is lacking. This is also lacking in Shatkin and Yeşilbağ’s (2019) concept of land-based accumulation, which tends to dissociate capital accumulation from its foundation on value creation. In Beswick and Penny’s (2018) identification of land rent as the main source of revenue for municipal councils and the type of municipal entrepreneurialism as ‘speculative’, that is based on revenue types like rent or interest that change over time, or in Penny’s (2022) emphasis that the value of land rent for municipalities is higher than what can be produced on public land, profits obtained by state agencies in built environment production are not considered.

The participation of the state in production, trade and finance besides as landowner

In order to analyse the relationship between the state and capital in for-profit development on public land, it is necessary to clarify the mechanism of revenue generation and distribution in these projects. Based on Marx’s analysis of the total circuit of capital, the metamorphoses of capital in these projects can be stated as follows: Initial money capital–M (equity capital and credit) provided by the developer and financiers transforms into commodity capital–C (land, variable capital [labour], constant capital [material production inputs]) in the circulation process facilitated by commercial capital. C transforms into C’ (built units) in the production process–P (production of buildings and infrastructures) conducted by the developer and subcontractors, that is, productive capital. Finally C’ transforms into expanded money capital–M’ by the exchange of the built units (Beitel, 2016; Ercan, 2023; Marx, 1991b). The source of revenue generated in the production of buildings and infrastructures, as in the production of all commodities, is the value created by the labour employed in the production process (Marx, 1991a). The value is distributed in the form of wage (labour power), land rent (landowner) and profit (productive, commercial and money capital) (Marx, 1991c). Consideration of the different components and actors of the capital-accumulation process in built environment production and the revenue generated therein (Beitel, 2016; Ercan, 2023; Harvey, 1982; Kerr, 1996; Lipietz, 1985) shows that government engagement of public land makes sense to the extent that it activates the value-creation process by combining capital, land and labour (Ercan, 2023).

The government’s share is the tax on various types of revenue generated in the capital-accumulation process. However, state revenue in the development of public land is not limited to it. The phases at which government agencies are involved in the total capital circuit determine their capacity to manipulate the generation and distribution of revenue. The research presented in this article shows that when governments transfer ownership of the land at the beginning of the project, they are involved as public regulators and landowners. In this case, governments become a stakeholder in the distribution of land rent. When governments participate in one or more of the phases of production, trade and finance, through PPPs managed by enterpreneurial state agencies or state-owned companies, they become a stakeholder in the distribution of profits as well as land rent. The involvement of entrepreneurial state agencies in built environment production, with their regulatory power, land and companies, takes place in the face of acute problems of capital accumulation and state finances. One of the implications of this research is that, when accumulation possibilities are limited, governments revitalise and strengthen capital circuits by getting involved in them, especially by introducing land over which government has control, while simultaneously enlarging their own share from the increased capital accumulation (Ercan, 2023). This new strategy of governments addresses the problems of capital accumulation and state finance through land development.

In his analysis of the secondary circuit of capital, Harvey (1982) argues that land has a different function in the production of built structures compared with that in the production of other goods. In the latter, goods and land are separated after production, whereas in the former, land remains an integral part of the good (Harvey, 1982). This links the value of buildings, with the land rent, which varies in space and changes over time. Urban land rent (the source of which is [surplus] value created in a particular production process or in all production processes in society) varies and changes due to locational features of and capital investments on land. Governments play the central role in the formation of urban land rent. It emerges when governments convert property into urban property by a zoning plan. Different types of rent arise when governments identify the functions, floor-area ratios and layout of buildings and make major infrastructure investments. Zoning and investments transform the status of parcels in the functional and investment surface of the city. In the sphere of production, differential features of land give way to surplus profits by shaping the magnitude and rate of capital and labour employed in built environment production (Beitel, 2016; Ercan, 2023; Harvey, 1985; Swyngedouw, 2012). In fact, conditions offered by zoning plans and government investments in for-profit development projects on public land generally give way to higher capital-labour ratios and magnitudes in building production as they inhere mix-use, high-rise developments mostly in the form of luxurious enclaves and smart spaces. In the sphere of circulation, that is, in the exchange of land or built units, another rent type that stems from the unique characteristics of sites for which buyers pay a monopoly rent/price is formed (Charnock et al., 2014; Harvey, 1989b; Lipietz, 1985). Changes in land rent over the course of the project and afterwards cause land to be exchanged for speculative prices (capitalised expected future rent) at the time of land acquisition and final project sale (Beitel, 2016).

Public land policy in Turkey

Public land policy took different forms in different periods of capitalist development and state structuring. After the Second World War, public land was provided to low-income farmers and urban dwellers by the transfer of use rights. 1 In the 1980s, it played an important role in compensating for the negative effects of the International Monetary Fund (IMF)-supported structural adjustment programme introduced in 1980, which aimed at closing the foreign trade deficit caused by import substitution (Keyder, 1987) and introduced trade liberalisation and export of labour-intensive industrial products through small- and medium-sized enterprises (Baysan, 1990). The deterioration in income distribution was alleviated with the regularisation of informal buildings and the transfer of ownership rights of public land 2 (Boratav, 1990).

In the 1990s, the policy of privatising land with the purpose of generating government revenue came up for the first time, when the competitiveness of labour-intensive production and the growth rate of exports decreased in the face of the intensification of global competition and the difficulty of reducing labour costs (Yeldan, 1995), and the foreign trade deficit continued to grow due to the dependence of domestic production on imported inputs (Ercan, 2004). Agricultural land owned by the Treasury was sold to farmers bestowed with use rights, de facto users or third parties, 3 when the depreciation of the Turkish currency in 1994 and Turkey’s entry into the EU Customs Union in 1995 increased the demand for government spending.

In 2001, a solution was sought to the sharp decline in the capital markets and the depreciation of the Turkish currency, with an IMF-supported stabilisation programme (Cizre and Yeldan, 2005). In order to compensate for the negative effects of the financial collapse and the stabilisation programme on wage-labour (Bozkurt-Güngen, 2018) and small- and medium-sized capital, the AKP governments, that took over at the end of 2002, resorted to generating financial resources by privatising public assets. Treasury-owned land was transferred to private parties by sale, lease or transfer of limited property rights. 4 State-owned companies and PPPs in the development of public land were also introduced. The objectives of public land policy in this period can be summarised in five points: (i) supporting accumulation by providing land for investments, in various sectors, (ii) and in the construction sector, (iii) providing disposable revenue to governments, (iv) creating popular consent by providing land for mega infrastructure projects, housing and public services (Ercan, 2023; Yeşilbağ, 2022) and (v) allocating land to capitalists who support the ruling party (Yeşilbağ, 2022). The second objective was a strategic choice of AKP governments (Doğru, 2021; Eraydın and Taşan-Kok, 2014; Ercan, 2023; Penpecioğlu, 2016; Tansel, 2019; Yeşilbağ, 2019, 2022), which did not initiate structural changes needed to solve the problems of competition and foreign trade deficit (Yeldan and Ünüvar, 2016), to delay the crisis dynamics (Ercan and Oğuz, 2020) and to control the tensions created by them (Bayırbağ and Penpecioğlu, 2017).

The 4.8% contraction in the economy in 2009 and increased government spending to compensate for this aggravated growth and public finance problems (T.C. Kalkınma Bakanlığı, 2013: 59). After that, AKP governments intensified their efforts to promote capital accumulation in built environment production and to increase the amount of public land under their control. An act 5 that required the compulsory renewal of buildings under disaster risk also established the legal grounds for the transfer of the land owned by various public agencies to the Treasury and the development of real estate projects on Treasury-owned land occupied by squatters. For-profit projects displacing the squatter settlements in the 2000s were met with strong resistance, and many of them could not be realised (Kuyucu and Ünsal, 2010; Türkün, 2014). Although the law triggered renewal in middle-income areas, it had little effect in low-income areas and in transferring land to the Treasury. However, thanks to the efforts to complete the country cadastre, the ratio of land owned by the Treasury in total surface area of the country increased from 15.2% in 2005 to 41.3% in 2021 (from 4.4% to 12.2% when forest category is excluded) (Milli Emlak Genel Müdürlüğü, 2023).

In 2018, the national administrative system was changed from a government formed by a prime minister appointed by a political party elected to the National Assembly to an elected president with party affiliation. Some legislative power was also given to the president through executive decrees. This system strengthened the centralisation tendencies in urban governance after 2009 (Kuyucu, 2017). The confrontation of the state and capital with crises in reproducing themselves led to strengthening of neoliberalism and autoritarian tendencies (Bruff, 2014; Ercan, 2023). The fact that one of the most important manoeuvring areas of these tendencies has been urban development models (Zunino, 2006) draws attention to public land policy in the analysis of contemporary restructuring of the entrepreneurial state.

Research method

The article’s argument is based on analyses that differentiate government practices in and revenue from ‘privatisation’ and ‘development’ of public land in Turkey. The agencies to be examined were selected according to the magnitude of the area and rent of the land they processed. The National Real Estate Department (NRED) manages land owned by the Treasury which holds the majority of public land. The Privatisation Administration (PRIVA) is responsible for the privatisation of state-owned enterprises and their real estate assets. The Mass Housing Administration (HOUSA) is responsible for supporting homeownership but has also been conducting for-profit real estate projects since 2003. HOUSA realises most of its for-profit projects through Emlak Konut Real Estate Investment Trust (E-REIT), of which it is a shareholder.

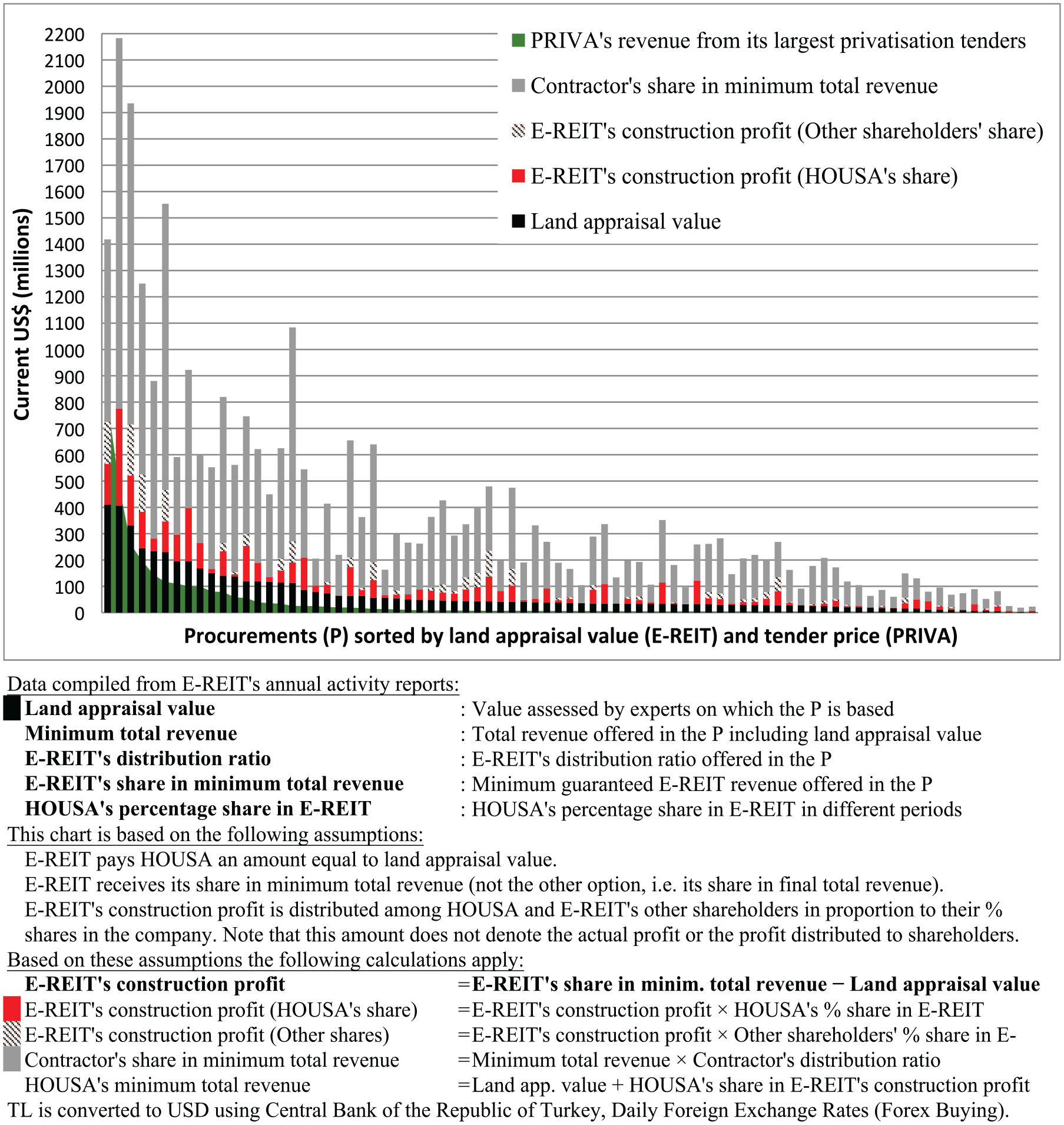

Three analyses were conducted. First, government strategies were assessed by examining the evolution of legislation and institutional structure regarding land privatisation and development. For this, the texts of the law, the regulations and annual reports of the agencies were studied. Second, the revenue sources of HOUSA that participates in land development were examined (Figure 2). By comparing land appraisal values with the minimum total revenue in E-REIT’s procurements, the profit accrued from construction was assessed. This analysis substantiated the article’s argument by showing that HOUSA earned revenue above the land appraisal values. In addition, HOUSA’s land appraisal values and PRIVA’s highest tender prices were compared to examine the governments’ strategies about the privatisation of high-rent land. Third, the annual revenue of PRIVA and NRED that privatise real estate by different methods (with and without changing the development rights) were compared (Figure 1). This analysis also identified periods in which real estate privatisation revenue increased, allowing to understand the relevance of this policy to economic and fiscal problems. PRIVA’s largest privatisation tender was examined in more detail.

The data for the second and third analyses were compiled from the annual reports of NRED (Milli Emlak Genel Müdürlüğü, 2022), PRIVA (Özelleştirme İdaresi Başkanlığı, 2022) and E-REIT (Emlak Konut GYO A.Ş., 2022). For NRED’s annual revenue, the ‘Total Property Sale Revenue’ entry was derived from NRED’s Monthly Distribution of National Real Estate Revenue Tables. For PRIVA’s annual revenue, the ‘Immovable Sale’ entry in the Application by Years ($) Table, and for the highest-priced auctions, the ‘Sales Transfer/Price (US Dollar)’ entry in the Immovable Sales-Transfer Table were used. Some types of data are not available for all years in E-REIT’s reports. Therefore, six data sets were used to compile data on land appraisal value, minimum total revenue, E-REIT’s share in minimum total revenue, E-REIT’s distribution ratio and procurement date: Capital and Ownership Structure, Completed Revenue Sharing Projects, Acquired/Ongoing Revenue Sharing Projects, Summary of Purchased Land, Business Models, Revenue Sharing Model Section, Quarterly Completed and Tendered Projects. Since information about all tenders of E-REIT could not be accessed, 81 tenders examined in this article do not cover all its tenders in 2003–2017. The tenders after 2017 could not be included, as crucial data were missing.

State-capital relationship in the privatisation of public land

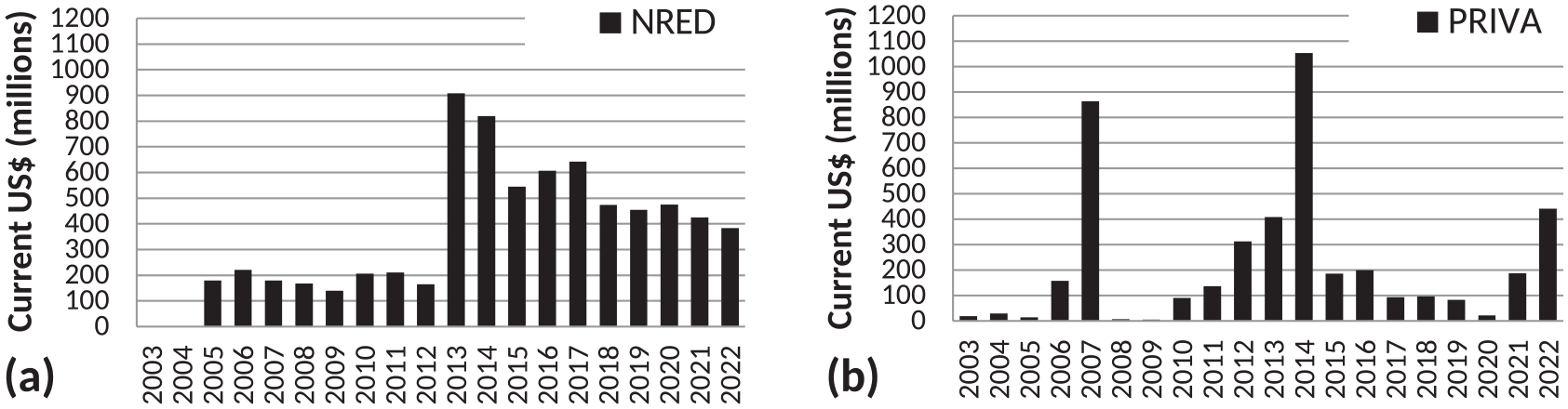

When governments transfer ownership of land to companies prior to development, they participate in the capital-accumulation process as public regulators and landowners. NRED and PRIVA, which directly privatise public real estate, manipulate the distribution of land rent, and the source of their revenue is land rent. NRED’s total nominal real estate sales revenue for 2005–2022 was approximately US$7.2 billion, and PRIVA’s was US$4.4 billion. PRIVA’s real estate privatisation revenue was 7% of its total nominal privatisation revenue (US$61.8 billion) in the same period (Özelleştirme İdaresi Başkanlığı, 2022). NRED’s revenue has fluctuated in line with problems of capital accumulation and government finances. Its annual revenue has increased significantly since 2012 (from average annual US$183 million in 2005–2012 to US$704 million in 2013–2017), when legislation on urban renewal and real estate privatisation was passed to offset the effects of the 2009 economic contraction with investments in the construction sector (Figure 1[a]). After 2018, when the macroeconomic balances deteriorated, it decreased again (to average annual US$442 million in 2018–2022). The fact that PRIVA’s real estate privatisation revenue was higher in 2010–2022 (average annual US$162 million excluding peak year) than that in 2003–2009 (average annual US$39 million excluding peak year) also reflects the impact of economic and fiscal crisis on government policy (Figure 1[b]). The peak in 2007 resulted from the sale of one plot for US$800 million, and in 2014, 10 plots were sold for a total of approximately US$970 million. The claim of the urban entrepreneurialism literature that real estate privatisation has become an important government strategy was manifested in an amendment to the privatisation law 6 in 2018, by which the two legal grounds of privatisation, namely ‘increasing efficiency in the economy’ and ‘reducing public expenditures’, were expanded by the addition of ‘providing public revenue by making use of real estate owned by the Treasury’.

NRED’s and PRIVA’s annual revenue from real estate sales.

Entrepreneurial policies could be implemented by state agencies with special authorities outside of the normative structure of public administration. In order to realise their strategies on public land, governments in Turkey have given PRIVA and HOUSA special authorities of land acquisition, urban planning, public procurement and revenue registration. PRIVA’s access to land was increased by transferring Treasury real estate allocated to the use of state-owned enterprises in the privatisation programme and the land under the control and possession of the state free of charge to PRIVA, 7 and the agency was given urban planning authority on its own land. The agency’s practices were exempted from the public procurement and accounting laws, and its revenue was deposited in privatisation accounts in public banks, which are not governed by the austerity restrictions. HOUSA’s land stock was increased when those of the Turkish Real Estate Bank (privatised in 2001) and the Land Office (closed in 2004) was transferred to HOUSA and the Treasury was authorised to transfer land free of charge to HOUSA. 8 The agency was given the authority to make and approve zoning plans, to respond to the objections to the plans and to execute the objection proceedings ex officio. 9 HOUSA’s procurements were excluded from the scope of the public procurement law, and the agency was authorised to sell land to E-REIT without tender. 10 In HOUSA’s projects, local governments were required to issue construction and residence permits without applying due procedures, and municipal fees were fixed at lowest rates. 11 HOUSA’s for-profit land development was made possible by transferring some company shares to HOUSA and authorising it to establish or participate in companies. 12

Entrepreneurial state agencies privatise land after increasing its development rights in order to increase the total yield of construction projects as well as their share in it. Christophers (2017) and Bryne (2016a) give examples of pre-privatisation urban planning from the United Kingdom and Ireland but interpret it as an action to ensure planning certainty, unlike the claim here. PRIVA, which privatised land after increasing the development rights, earned higher revenues in many tenders than NRED, which privatised without changing the development rights. For example, PRIVA’s revenue from its largest two real estate tenders (US$800 and US$482 million) in 2005–2021 is higher than NRED’s average annual revenue (US$401 million) in the same period. Note that this result was also influenced by the governments’ preference to privatise high-rent land through PRIVA.

Agencies with special authorities destabilise the normative hierarchy of public administration and cause structural problems in state’s social function. The authorities granted to PRIVA and HOUSA have taken away the urban planning authority of local governments. Objections were raised that these agencies violated the principle of impartiality in urban planning by granting their own property higher development rights than the zoning rules allowed. Associations of architects and urban planners took some of the zoning plan amendments made by these agencies to administrative courts on the grounds that they did not comply with the laws, zoning plans, urban planning principles and public interest. The courts cancelled some amendments, but they rejected the claims for others.

A brief history of PRIVA’s largest land privatisation exemplifies this agency’s practices and the difference with NRED. This was a high-rent plot in Istanbul, used by the Highways Department, located at the exit point of a bridge connecting Europe and Asia and adjacent to the central business district. Initially, NRED was set out to sell this plot; however, there was no bidder for the tender launched in 2004. The tender in 2006 was cancelled because the plot was included in the privatisation programme. Seven months later, it was transferred to a state-owned enterprise that was already in the privatisation programme (Özelleştirme İdaresi Başkanlığı, 2008: 34). PRIVA sold the land for US$800 million thanks to the superior development rights it granted to the land. In a lawsuit filed by the Chamber of City Planners, the Council of State Administrative Court ruled that the land uses, building densities and heights granted in PRIVA’s plan amendments were above the zoning limits recognised by law and cancelled them in 2009. However, this decision was overturned by the court of appeals. The company, which bought the land, developed a building complex including a shopping mall, an entertainment centre, a multinational hotel, offices and high-income residences.

In NRED’s and PRIVA’s practices, the government provides land and regulation and companies finance, produce and trade. While PRIVA supports the developers by offering scarce high-rent urban plots and granting high zoning rights, it is also a rival to them in the distribution of revenue, as it draws the land rent from the value created in production. The advantage of PRIVA’s practices over HOUSA for governments is that it generates revenue in the short run. However, PRIVA does not receive the additional income that HOUSA derives from production, trade and finance.

State-capital relationship in the development of public land

When governments participate in for-profit land development instead of transferring ownership of land to private companies, they are involved in the capital-accumulation process not only as landowners but also as company owners taking part in production, trade and finance. HOUSA takes part in production and trade of the built units through PPPs under its own or its company’s (E-REIT) management, besides participating as landowner and public regulator. After 2019, governments also took part in financing through the Turkish Real Estate Participation Bank owned by the Ministry of Finance and Treasury. This bank buys housing, mainly from E-REIT’s projects, and sells them to its customers. In E-REIT’s projects, HOUSA manipulates the distribution of the land rent and profit and generates revenue from both. The data compiled for this article show that, HOUSA earned more revenue than the land appraisal values in E-REIT’s projects due to its share in E-REIT’s profits. In E-REIT’s 81 procurements in 2003–2017, the ratio of HOUSA’s share in E-REIT’s construction profit (calculated in accordance with the assumptions listed in Figure 2) to land appraisal value is 0.79 on average (Figure 2). In other words, HOUSA has earned an additional revenue of 79% of the land appraisal value. This ratio was 0.84 before E-REIT’s initial equity offering in 2010, which reduced HOUSA’s percentage share in the company from approximately 100% to 75%, and 0.94 thereafter. It was 0.66 after the secondary offering in 2013, which reduced HOUSA’s share to 49%. In fact, HOUSA’s earnings beyond the land rent are confirmed on HOUSA’s website with the statement: The basic principle in these projects is to generate revenue by procuring the land intended for sale at a price above the appraisal and market values (Toplu Konut İdaresi Başkanlığı, 2022). The fact that governments have mostly privatised high-rent land through HOUSA can be considered as an indication that they see HOUSA as more efficient than PRIVA in terms of generating revenue. This becomes clear when the land appraisal values of 81 procurements made by E-REIT in 2003–2017 are compared with the prices of PRIVA’s largest tenders in the same number and period (Figure 2). HOUSA has privatised 18 and PRIVA 8 plots for over US$100 million.

E-REIT’s revenue-sharing construction procurements and PRIVA’s largest privatisation tenders between 2003 and 2017.

A description of E-REIT’s schemes explains Figure 2. HOUSA provides land using its land stock and capacity to access Treasury land. It makes the zoning plan and sells the land to E-REIT without a tender. E-REIT bids for construction, based on the appraisal value of the land, and the bidders make their offers about the ‘minimum total revenue’ and ‘E-REIT’s distribution ratio’. E-REIT selects the bidder who offers the highest amount as ‘E-REIT’s share in minimum total revenue’, which is guaranteed no matter how much revenue the project actually yields. After the completion of the project, the agency gets its share, according to the distribution ratio, either in the ‘minimum total revenue’ or in the ‘final total revenue’. The contractor covers all non-land costs and carries out project preparation, construction, marketing, pricing and sale while E-REIT approves all projects and contracts and supervises construction. E-REIT transfers ownership of the built units to final customers and releases the contractor’s revenue share.

E-REIT’s profit is basically the value created by the labour that performs the management and control work within the company. The company also earns speculative gains from land rent increments and from investing the money accumulated in the pool in financial instruments. However, with HOUSA backing it with regulative power, extensive land resources and a bank buying its products after 2019, E-REIT has more means than ordinary companies without a government share. The specific collaboration of HOUSA, E-REIT and contractors has implications for the distribution of revenue as well as the overall value created.

Entrepreneurial government agencies regulate the distribution of profit and risk with the contract models they use. The contract model called Revenue Sharing for Land Sales (Revenue Sharing), by which HOUSA and E-REIT manage their PPPs, guarantees the agencies not only a minimum revenue but also a ratio of the final revenue, which enables them to receive unpredictable gains which may accrue during the construction period. The feature of the contract that makes this possible is that, rather than the built units themselves, the revenue obtained from the sale of the built units are distributed between the parties. The contract regulates the trade-off between the landowner’s commitment to sell the built units to third parties and the revenue to be generated by construction. In addition to maximising the profit share of E-REIT, another result of this is that it combines the interests of E-REIT and the contractor throughout the project. E-REIT’s distribution ratio in 81 projects is 33% on average, varying between 16% and 55% (Figure 2). The difference between these ratios and the 50%–70% landlord share in land-scarce urban areas in Turkey, referred to by Serin et al. (2020), is due to the higher floor-area ratios in E-REIT’s projects, which give way to equivalent land prices per square metre with other plots in the vicinity.

The collaboration between the government and companies also enables them to increase the total value created in production by bringing together the strenghts of the state and capital and creating a synergy (Ercan, 2019; Yeşilbağ, 2019). HOUSA contributes to the collaborations by compiling land in high-rent areas and large-enough plots, increasing zoning rights, overcoming obstacles in legal procedures and synchronising them with the requirements of construction processes. In addition, as an influential agency affiliated to the office of the prime minister/president, it gives confidence to all parties including civil servants, financiers, suppliers, contractors and customers. While contractors often have little trust, HOUSA’s involvement creates customer trust, increasing demand for projects. As a private company with less than half government share (since 2013), E-REIT’s participation brings flexibility to procurements by exempting them from HOUSA’s procurement guide and Court of Accounts audit and the building inspection required in accordance with the zoning law. Contractors contribute by covering investment financing and implementing profit-maximising strategies, especially in the organisation of the work process and relations with the labour force (Gülhan, 2021).

In HOUSA’s practices, the government provides land and regulation and a state-owned company manages the PPPs in which companies produce, trade and finance. In these projects, the state, together with the contractors, is in an antagonistic relationship with the labour force, in the distribution of revenue between wages and profits, whereas the state and contractors are rivals in the distribution of profits and rent. Companies that are not included in the partnerships are at a great disadvantage in the competition against them.

Conclusion

I argued that governments’ new strategies on public land, put forward to solve the problems in capital accumulation and state finance, have transformed the relationship between the state and capital by making the state more embedded in the total capital circuit, that is, rendering it part of production, trade and finance besides participating as a landowner. The article contributes to the literature by clarifying the total circuit of capital in built environment production and the changing role of the contemporary state in it and by revealing the connection of the state with profit besides land rent. The importance of revealing these changes is to elucidate the transformations that occur in state structures and policies while implementing entrepreneurial policies to overcome the problems caused by economic and fiscal crisis.

Analysis of the central government agencies in Turkey has shown that, while on low-rent land, governments mobilise agencies that are part of the main body of the public administration, and on high-rent land, they create entrepreneurial agencies with special authorities to increase capital accumulation and government revenue. The collaborations between these agencies, state-owned companies and contractors increase the total value created in the projects by combining the strenghts of the government and companies and uniting their interests. However, analysis of the contracts used by government agencies in the projects has shown that these collaborations also contain contradiction in the distribution of revenue between the state and capital.

While the strategies on public land have benefitted the governments and companies involved in the projects as well as high-income groups gaining access to favourable urban locations, they have given way to dispossession and displacement. In these projects, public service and reserve areas, urban open spaces and low-income residential areas have been replaced with mixed-use luxury estates for high-income people. The high-rise and isolated character of these projects has reduced the quality of urban life and undermined social justice. These projects were met with strong resistance as in the lawsuits filed by the chambers of architects and urban planners and in the Gezi demonstrations in 2013 attended by millions of people.

The new role of the state in capital accumulation can be interpreted as the legitimacy dilemma of the liberal state. As the state becomes more embedded in the total capital circuit, the legitimacy of exercising public power becomes questionable. In cases where PRIVA and HOUSA broke the principle of impartiality in the use of public power by granting superior development rights to their own land, public authorities with capitalist motivations gave rise to structural problems regarding the function of the state. The new role of the state in capital accumulation can also be interpreted as a new stage of the transformations in the state-capital relationship that began in the 1970s. The evolution of the state from providing the necessary conditions for capital accumulation to being its more immanent part was the reaction of the state to the problems in the reproduction of the state and society. It seems plausible that the new state structures and policies created day by day while governments struggled with the accumulation and fiscal crisis will change state-capital relations on a permanent basis.

Footnotes

Acknowledgements

The author thanks the editor Tuna Taşan-Kok for providing important feedback, Fuat Ercan for providing constructive criticisms about the conceptual framework, Efza Evrengil and Şebnem Oğuz for providing helpful comments, and two anonymous peer-reviewers for their significant contribution to the improvement of the article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.