Abstract

The state capitalism literature emphasizes the new roles played by states in global politics and domestic economies through heightened intervention and ownership of key resources and sectors. In Ireland, we instead find a reluctant state capitalism evinced by antipathy towards state ownership, the accommodation of private sector failures and embrace of hybrid governance. Rather than something new and unprecedented, the Irish state has been a long-standing feature of domestic market development and an important institution supporting private enterprise today as in the past. Urging a more academically robust conceptualization of state capitalism, this paper relinquishes innate assumptions of obvious boundaries dividing liberalized capitalism from state capitalism in favour of engaging the domestic state and sectoral developments on their own terms and within their proper historical context. We find reluctant state capitalism in Ireland's telecommunications sector through a continuum of state–market involvement in four phases: commercial, devolving, evolving and partnership state capitalism. By identifying temporal phases of state capitalism, we move beyond the here-and-now of more contemporary ‘new’ state capitalism analyses that suggest rupture with an idealized, liberalized past.

Keywords

The state is back!, or so says the new state capitalism literature. The reinvigoration of public ownership, reassertion of market intervention, development of more sophisticated circuits of public finance and promotion of national champions are often heralded as dramatic features of novel 21st-century global state capitalist competition. Positioned as an antithesis to neoliberal capitalism, renewed scholarly fascination with the state as an economic actor in capitalism often assumes such changes represent an abrogation of liberal values. Here we seek to better understand why and how the domestic state might enact state capitalist policies using Ireland and its telecommunications sector as our case study. We argue that a national scale assessment offers dual insights, both into the Irish case itself and as a mechanism for querying the analytical utility of the ‘state capitalism’ concept by engaging the domestic state, national developments on their own terms and within their proper historical context, and relinquishing innate assumptions of obvious boundaries dividing liberalized capitalism from state capitalism. We find that when pursuing some of the hallmark features of state capitalism, Ireland remains reticent to do so even when its hand is forced by market failure – thus charting a path of ‘reluctant state capitalism’.

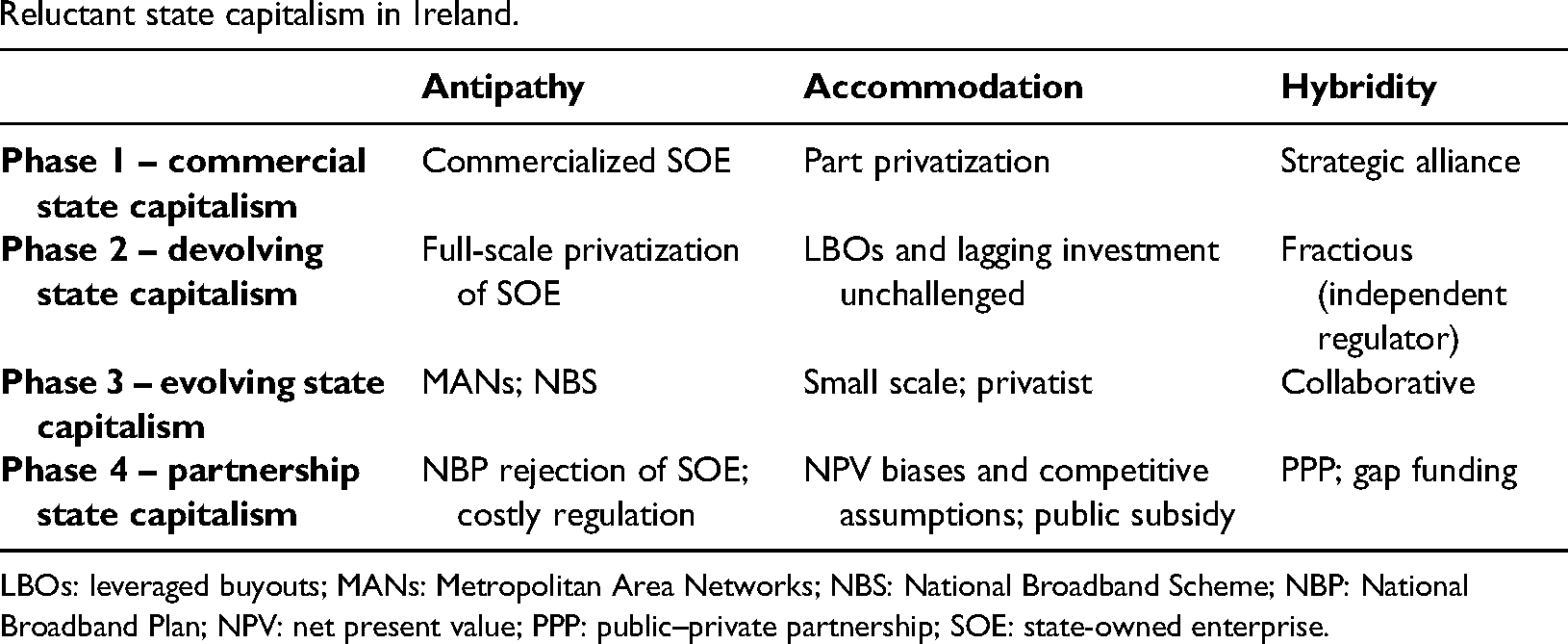

However, this is not a dichotomist tale of liberal endurance either. With pervasive hybridity comes trouble applying easy labels with clear timelines like ‘neoliberal’ versus ‘state capitalist’ or ‘developmental’, and so on. The Irish state as an economic actor has been a long-standing feature of its market development and remains an important institution supporting private enterprise today as in the past. Rather than an on–off switch – state capitalism or the lack thereof – we find in Ireland a reluctant state capitalism expressed through a continuum of state–market involvement in four phases. First with the establishment of a commercial state-owned enterprise (SOE) in the early 1980s (a corporatized SOE) and private sector delivery of retail services in the 1990s (sectoral liberalization), next with the private ownership of telecommunications infrastructure in 1999 (complete SOE privatization). Third, from 2001 onwards, a number of new state-led interventions to address market failure emerged when technological developments and the advent of the Internet age created a national need for investment in broadband infrastructure not met by the private sector, particularly in rural areas. The first major state interventions, the Metropolitan Area Networks (MANs) and the National Broadband Scheme (NBS), were small scale but in both cases, the government chose to rely on collaborative arrangements with private interests. More recently, the scale of collaboration with the private sector has expanded significantly through the fourth version of state capitalism. For the rollout of Ireland's National Broadband Plan (NBP), the government has chosen a public–private partnership (PPP) type model unmatched in the history of the state. By identifying temporal phases of state capitalism, we move beyond the here-and-now of more contemporary ‘new’ state capitalism analyses that suggest rupture with an idealized, liberalized past. We call these phases: commercial state capitalism, devolving state capitalism, evolving state capitalism and partnership state capitalism in Irish telecommunications.

Ian Bremmer, a leading critic of state capitalist practices, targets telecommunications as one of the main sectors that ‘a growing number of governments are no longer content with simply regulating’ (2009, 42). Our approach is instead sensitive to the specific characteristics (e.g. technological, regulatory and structural) of the complex and fast-changing telecommunications sector itself, and the particularities of the Irish domestic market. Sectoral contextualization equally illuminates how phases of state capitalism evolve through particular state orientations, namely antipathy towards state ownership and control, leading to new problems and collaborations. Initiatives in this area demonstrate a willful ignorance of the failures of privatization and the persistent overriding preference by governments and policy makers for a privatist paradigm – favouring private sector regulatory models even where state intervention is significant. This bias towards private ownership and the dismissal of SOEs are frequently forced to contend with various market failures and, at critical junctures, the state has stepped in to provide notable interventions. With successive governments avoiding state-owned approaches and choosing (or privileging) ‘lighter’ forms of state capitalism such as concessions and PPPs, Ireland presents a conundrum for the state capitalism literature in that the state plays a crucial but reluctant role in shepherding the sector.

To establish the phases of Irish state capitalism in telecommunications, and substantiate our argument that reluctance is expressed through antipathy, accommodation and hybridity, the paper develops its analysis through three sections. First, we provide a brief overview of the state capitalism literature. In short, state capitalism concerns itself with the activities of the state in capitalism, ranging from ownership dynamics to forms of market intervention, and the outward projection of national economic interests. Market intervention and ownership dynamics are the aspects of greatest concern in this paper. Second, we analyse public–private collaborations in Ireland's telecoms sector, identifying commercial, devolving, evolving and partnership forms of state capitalism across four phases of historical and contemporary development. Third, we discuss the implications of antipathy, accommodation and hybridity for Ireland. The paper concludes by reflecting on how the Irish case can inform the state capitalism literature more generally.

State capitalism: Old and New

In a 2020 special issue of the Journal of World Business devoted to state capitalism, editors Wright et al., provide a thoughtful, if all-encompassing, account of the institutional variety involved with related phenomena. They define state capitalism as ‘an economic system in which the state uses various tools for proactive intervention in economic production and the functioning of markets’ (Wright et al., 2020, 3); adding that, ‘State interventions can occur within the home market and abroad, in the interest of domestic firms and for diplomatic reasons. States may intervene by owning a significant percentage of productive assets through various forms of statism such as government subsidies, investments, consumption, and various regulatory instruments, as well as through formal and informal coordinating mechanisms.’ With exclusions from ‘state capitalism’ reserved for command and control arrangements like when quotas trump prices (Wright et al., 2020), a circumstance very few, if any, political economists would classify as capitalist (Whiteside, 2020), one wonders what would not constitute ‘state capitalism’ given such a wide tent. Perhaps state capitalism might be better understood as capitalism, so as to not elide the fundamental, enduring role played by the capitalist state in supporting capital accumulation and economic development over the long haul (Whiteside, 2021). Indeed, an absent/incoherent theory of the state dogs the state capitalism literature generally (Alami and Dixon, 2019b).

One way of distinguishing state capitalism is to set it against liberal capitalism. Bremmer (2009, 41), a central proponent of this position, pits the national oil corporations, SOEs, privately owned national champions, and sovereign wealth funds of countries like Russia, China, Brazil, India and the Gulf states against the ostensibly free and unfettered activities of American capitalists in a realist international relations competition that has fundamentally altered previously established global dynamics: ‘… the free-market tide has now receded. In its place has come state capitalism, a system in which the state functions as the leading economic actor and uses markets primarily for political gain’. A hard-to-ignore wrinkle here is the well-established pattern of corporate support offered by countries firmly in the liberal heartland. Nevertheless, much of the literature proceeds in this dichotomous ‘states versus markets’ vein to include work more directly focused on China (e.g. Milhaupt and Zheng 2015) and rival (non-Western) ‘state forms’ (Fainshmidt et al., 2018; Witt and Redding, 2013).

The third body of literature, advanced by Musacchio and Lazzarini (2014, 2) and speaking to both managerial and comparative studies, defines state capitalism as ‘the widespread influence of the government in the economy, either by owning majority or minority equity positions in companies or by providing subsidized credit and/or other privileges to private companies’. In their widely cited account, there are three varieties of state capitalism: the traditional model (Leviathan as entrepreneur), and two new models (Leviathan as majority investor and minority investor). Leviathan as entrepreneur involved the management of SOEs within a public sector bureaucracy, largely for purposes of national economic development prior to the 1980s. In the wake of numerous privatization campaigns, two new categories of state capitalism emerged through the particularities of divestiture. As a majority investor, the state remains a controlling shareholder in SOEs though private owners are involved in particular ways; and as a minority investor, the state gives up decision-making control but maintains some degree of ownership in areas like sovereign wealth funds, pension funds and state-owned financial institutions. Musacchio et al. (2015, 122) list telecommunications-specific examples of Leviathan as majority investor (Singapore, Qatar, Norway and Malaysia) and minority investor (France, Germany and Sweden). Ngo and Tarko (2018) characterize Vietnamese telecommunications, a state-owned duopoly with limited private sector participation, as state capitalism. Additional management-oriented comparative literature on public–private telecommunications sectors includes Doh et al. (2004); Millward (2005); and Vaaler and Schrage (2009). Other similar publications can be found on the performance of SOEs, state ownership and sovereign wealth funds (e.g. Cuervo-Cazurra et al., 2014; Estrin and Pelletier 2018; Grosman et al., 2016; Lazzarini and Musacchio 2018; Tihanyi et al., 2019).

While Musacchio and Lazzarini (2014, 7) argue that their ‘intermediate types’ stand in opposition to Bremmer's idealized liberal market economy, their account is nevertheless predicated upon proto-liberal political philosophy located in the ‘Leviathan’ view of the state. 1 ‘New state capitalism’, animated through categories of Leviathan as majority and minority owner, ignores why SOEs and public sector market interventions were viewed as necessary or beneficial in the first place, an especially crucial line of inquiry for former colonies once without sovereignty, subject to the atrocities of imperial interventions by other Leviathans. For some state capitalisms, early 20th-century public ownership might have been urged on largely through the Keynesian economic desire to promote effective demand and overcome market failure; for others, public ownership might have been a more politically charged ambition to create an independent, autonomous state and foster domestic capitalism after centuries of colonial Leviathan incursions. Managerial studies and cost–benefit analyses of SOEs do not typically concern themselves with such philosophies and ugly histories. 2

The liberal philosophical commitments that commonly underpin the state capitalism literature make implicit and explicit assumptions about the (proper and actual) role of the state in capitalism. The activities of settler colonial and imperial states thus create problems for an easy application of state capitalism historically and today. The ‘developmental state’ also commonly featured direct state intervention in markets, including the protection of domestic industry and favouring of national champions. In an analysis of the state capitalism literature from its very origins to today, Sperber (2019, 100) finds that ‘In sharp contrast to 20th century theories of state capitalism, present-day scholarship on the topic tends to retreat from the integrated critique of political economy, shifting its problematics to state–market relations and meso- and micro-levels of analysis.’ A 2021 joint special issue published by New Political Economy and Review of International Political Economy, dubs the oversights, biases and omissions that often underpin scholarly analysis ‘blind spots’ (see Best et al., 2021). Enhancing a historically contextualized political economy understanding of state capitalism would require addressing lingering and latent liberal expectations about the state in capitalist society. Generally, ‘state capitalism’, as the label would suggest, gropes at bringing to light the overlap between public and private spheres in capitalism, even if the literature is frequently ill-prepared conceptually to identify longer run dynamics (due to its liberal biases and myopic focus on ‘new’ state capitalism or binary states vs. markets rather than partnerships, continuity, overlap and multiple forms of power). In what follows, this paper attempts to overcome some of these blind spots through its temporal and sectoral contemplation of the phases of Irish state capitalism that have come to be defined through reluctance and shaped by antipathy, accommodation and hybridity.

By addressing the ways in which history matters, the cross-cutting implications of phases of state capitalism, and the enduring processes of state-supported economic development, we move forward from Sperber's (2019, 119) lament that whereas earlier state capitalism literatures ‘grappled with system-wide attributes of state capitalism, in terms of state-owned capital and of public-private relations, … neglect of the past [in the literature today] induces a damaging tendency to ‘reinvent the wheel’, as writers [today] are tempted to label as ‘new’ phenomena that have not only long historical legacies but also have long been objects of study by others.’

Context: State–market relations and recent Irish economic development

Before embarking on our analysis of state capitalism and the Irish telecommunications sector it is necessary to consider perspectives on state–market relations and Irish economic development over the last 40 years. Since the 1980s, the Irish economy has moved from periods of economic stagnation (up to 1987) to rapid economic growth (especially 1994–2008, the so-called Celtic Tiger years), only to be upended once more through a turbulent time of calamitous crash, recession and austerity (2008–2013), followed by recovery the resumption of economic growth (2013–2020) until struck by the global COVID-19 pandemic. Throughout this period, Ireland pursued an uninterrupted economic strategy of increased integration into the global economy that often lent to the view that Ireland was a liberal small state that successfully adopted neoliberal policies such as free trade, market liberalization, privatization and a deep embeddedness in the global economy (Ó’Riain and O’Connell, 2000). This simple version of recent Irish economic history does not provide the full picture or a sufficient interpretation of the changes that have occurred over the last 40 years or so. In particular, it provides a misleading account of the balance between state and market in the Irish context. Whereas the state takes a back seat in neoliberal explanations of economic history, the long-standing reality in the Irish case has been that of an active state which played a critical role in positioning the Irish economy for successful adaptation to the changing circumstances of globalization.

The role of the state in Ireland's economic and social development attracted much scholarly attention during the so-called Celtic Tiger period (1994–2008) of rapid economic growth. Authors including O’Malley (1989), Kirby (1997) and O’Hearn (1989; 1998; 2000) provided different accounts of how the state pursued active policies that resulted in improved growth performance while arguing that the thrust of state policy was characterized by significant weaknesses. For example, Kirby (1997) was critical of the ‘state's developmental direction, deferring too much to conservative forces rather than seeking a more robust project of national development’ (Kirby, 2009, 8). O’Hearn argued that a major weakness of the state's model of development was deference to multinational companies, which led to a form of dependent liberal industrialization.

Kirby (2009) describes how the debate about the Irish state was also examined in terms of two separate international literatures on the political economy of the state. Ó’Riain (2000a; 2000b; 2004) characterized the Irish state as a ‘flexible developmental state’, which was distinguishable from the bureaucratic and planned developmental states of South East Asia by virtue of its agility in responding to the demands and pressures of globalization.

The flexible developmental state thesis was in turn contested by O’Hearn (2000) and Kirby (2002; 2005) who argued that the concept of the ‘competition state’ (Cerny, 1995) provided a more persuasive framework for understanding Ireland's development path. This perspective stresses the importance of the state in terms of promoting competitiveness in response to the intensification of the forces of globalization. A key feature of the Irish competitive state was the subordination of social policy to the needs of the economy. Whereas the ‘developmental state’ perspective emphasizes the capacity of the state to foster economic development and achieve social outcomes, ‘competition state’ theorists stress the constraints imposed on states by the competitive pressures of globalization. In addition, they identify a logic in which the state prioritizes the promotion of enterprise and profits over welfare-oriented objectives.

Several authors have explored the strengths and weaknesses of the developmental and competition state characterizations of the Irish state (e.g. O’Donnell 2008 and Smith 2005), with some having suggested that we ‘may have to settle for the fact that it's a bit of both’ (Kirby, 2009, 12). Given the focus of this paper on SOE in general and telecommunications in particular, we find that both perspectives provide useful insights into the nature of state capitalism since the 1980s.

In historical terms, the key actors in the Irish developmental state included commercial SOEs in sectors such as electricity and natural resources that led to industrial development in the decades after independence. Other state agencies emerged as part of the response to the enormous economic and social crisis of the 1950s, which directed the economy towards fuller integration with the international economy. For example, the Industrial Development Authority (IDA), (originally established in 1956 to support indigenous industry) became the driving force behind an export-oriented industrial strategy that focused on the attraction of foreign direct investment (FDI). The state, therefore, became central to creating a ‘world class’ location for mobile investment and developing critical elements of locational advantage including ‘generous tax incentives and grants, a transnational-friendly environment, a young and co-operative labour force and (later) a world class telecommunications system’ (Ó’Riain and O’Connell, 2000, 315).

The reference to telecommunications in the quote above has obvious relevance to this paper. Although many commercial SOEs showed poor financial performance in the 1970s and 1980s, in several instances they made critical contributions to national economic development by channelling capital investment into strategically and socially important sectors such as telecommunications, energy (e.g. rural electrification), aviation (e.g. airports and the national airline – Aer Lingus) and natural resource-based industries including sugar and peat. Public enterprises were often required to invest in these sectors due to the absence of a strong private entrepreneurial tradition (O’Malley, 1989; Lee 1989).

The poor financial performance of several commercial SOEs became a matter of concern for governments in the 1980s as the economy entered recession, unemployment soared and public finances deteriorated. Governments and SOEs responded by taking measures aimed at improving the commercial focus of the sector and by the late 1980s most SOEs had shifted into a far more commercial mode and had become profitable (Sweeney, 1990). In this regard, SOE policy resonated with the characteristics of the competition state as it was necessary to ensure that public enterprises provided cost-efficient and quality services in strategically important infrastructure-based industries such as telecommunications which were critical for the attraction of inward investment.

A noteworthy feature of this period was that successive governments resisted the call to follow the increasing international trend of privatization pioneered in the UK. Ireland instead adopted an approach that emphasized commercialization of the SOE sector instead of privatization, thus changes to the Irish system of state capitalism were relatively modest in the 1980s and 1990s.

There is also the wider Irish institutional context shaping the formulation of economic and social policy between 1987 and 2008 to consider. A series of neo-corporatist social partnership institutions guided most major changes in economic policy (including SOE policy) during this period and ensured the state was deeply implicated in managing economic development (Ó’Riain and O’Connell, 2000). With respect to the question of privatization, Allen (2000) noted that the first social partnership agreement in 1987 contained a commitment not to sell off commercial SOEs. This institutional check on privatization policy was short-lived and in the 1990s, there was a degree of experimentation with privatization as shares were sold in four SOEs, three of which experienced financial difficulties in the 1980s (e.g. the Irish Sugar Company and Irish Steel) (Palcic and Reeves, 2011).

Notwithstanding an initial foray into the world of privatization, SOE policy continued to eschew explicit privatization measures especially in sectors where competition was limited and public enterprise was responsible for providing important social and economic services. The main thrust of SOE policy was to require companies to behave commercially and to liberalize the sectors in which they operated as required by various EU Directives. This pragmatic approach continued even during the period of austerity measures adopted after the global financial crisis when the economic policy was framed by the conditionality arising from the financial support programs provided by the Troika (European Commission, ECB, IMF) (Palcic and Reeves, 2013).

Telecommunications, however, represented an exception to the general thrust of SOE policy from the 1980s onwards. For several reasons including the liberalization agenda of the EU and the attraction of significant revenues for the Exchequer, the state adopted a largely pro-market approach to the regulation of the telecommunications sector that resulted in partial (1996) and then full (1999) privatization. Over the next 20 years, the state made several significant market interventions in this sector but we argue that a renewed appetite for ‘state capitalism’ alone cannot account for these interventions. It is our contention that state capitalist interventions co-exist with a preference for market-oriented approaches to regulation, and thus Irish state capitalism is reluctant in nature.

Phases of Irish state capitalism

With this backdrop in mind, we now explore the macro-political economy of national scale public–private collaboration in Irish telecommunications – the long run and varied involvement of the Irish state in its domestic telecoms sector. Almost 40 years ago, geographer Kellerman (1984) observed that: ‘In most OECD member countries, the operation of telecommunications services is a government monopoly’ (1984, 231). A decade later, with the advent of deregulation, Cooke (1992), identified the reassertion of uneven development once constrained by government concern for natural monopoly and public service. Indeed, there is a notable macrogeography to uneven development (Peck, 2016). 3 In Ireland, telecommunications planning and policy, orchestrated nationally by the central government (cf. Graham and Marvin 1999), greatly influence rural–urban disparities and economic development prospects. Privatized telecommunications provision creates contradictions for economic development, urging subsequent state interventions in a variety of state capitalist forms. Our description identifies four distinct phases or forms of state capitalism, with greatest detail provided for the current, most intricate, phase. Note that ‘phase’ is being used here in reference to forms of state capitalism, not wholly discrete timeframes as there is some chronological overlap between certain phases.

Phase 1 – commercial state capitalism (SOE)

With the foundation of the Irish Free State in 1922, the control and operation of the telegraph/telecommunications infrastructure were transferred to the Department of Posts and Telegraphs. After incurring increasing losses in the 1970s, mainly due to low levels of capital investment and a lack of commercial management, a review of the telecommunications service was conducted in 1979. The principal recommendation arising from the review was that responsibility for services be transferred to a state company run along commercial lines. In 1984 a new SOE, Telecom Éireann, was established and set about commercializing the telecommunications service and investing significantly to modernize the national network. The commercial focus of the new SOE was embodied in a 5-year corporate plan that aimed to reduce financial losses and debt levels. By the end of the 1980s, the company had made significant inroads in improving its performance mainly through a large reduction in staff numbers and strong business growth. The second 5-year plan aimed to build on these improvements but also emphasized a new imperative of coping with rapid technological advances and the move towards full market liberalization in 1998.

A persistent narrative that emerged in the early 1990s was that a small national monopoly supplier such as Telecom Éireann could ill afford to isolate itself given the pace of technological change and the challenges posed by the rapidly changing nature of the international telecommunications market. The company made it known that it was actively searching for a partner that could bring significant benefits to the company in the increasingly global telecommunications market. This culminated in the part privatization of the firm in 1996 when Telecom Éireann signed a strategic alliance with the Comsource consortium (consisting of the Dutch and Swedish national telecommunications operators) which saw the sale of 20% of Telecom Éireann's share capital. This entry into a hybrid form of governance marked a historical change for the company. Moreover, it pushed the company further along a continuum of commercialization, hybridity and liberalization that culminated in full privatization in 1999.

It is worth noting that in the decade preceding the full divestiture of Telecom Éireann, the company recorded significant improvements in performance and was shown to be amongst the most productive telecoms firms in Europe (Dassler et al., 2002; Pentzaropoulos and Giokas, 2002; Palcic and Reeves, 2010). Notwithstanding this impressive performance, there was broad support for the full privatization of the company. Prominent motivations for privatization included revenues for the Exchequer and the opportunity to sell shares to citizens. Furthermore, the narrative at the time reflected a widespread belief that privatization was necessary if the company was to thrive in its newly liberalized environment.

Phase 2 – devolving state capitalism (privatized and regulated)

The eagerness to privatize Ireland's state-owned telecommunications operator offers the only clear example of where SOE policy conformed to the neoliberal playbook. It arguably overshadowed any official recognition of the achievements under public ownership and paved the way for a new phase of state capitalism characterized by arm’s-length independent regulation. In comparative terms, the speed of the transition to full private ownership was a distinguishing feature of the Irish case. Unlike other European countries that privatized their telecommunications sectors in stages, the Irish government was unique in its decision to divest its entire remaining stake in the company at the initial public offering on the stock exchange in July 1999. Here Leviathan was to play neither a majority nor minority role.

This full divestiture of Telecom Éireann under the new name Eircom had an important bearing on developments in the post-privatization period. Relinquishing full control of the network left the government powerless to prevent a number of changes in the structure and ownership of the national operator that had severely negative consequences for the telecommunications sector and the Irish economy. The principal events that followed privatization were:

The demerger and sale of Eircom's mobile phone subsidiary, Eircell, to Vodafone in May 2001; The highly leveraged buyout (LBO) of the remaining fixed-line business in December 2001 by a private equity group; The reflotation of the company in 2004; The second highly LBO of the company in 2006 by another private equity group; The sale of the company to the state-owned Singapore Technologies Telemedia in 2010; The takeover of Eircom by creditors in 2012 after going into examinership.

Of the changes above, the takeovers in the form of highly LBOs by private equity groups and resultant ballooning of company debt had the biggest impact on the strategies and financial performance of Eircom after privatization. Moreover, as Eircom remained the dominant incumbent fixed-line operator in the Irish telecommunications sector, the LBOs had damaging consequences for the wider economy and society especially in relation to the slow development of broadband services in Ireland from 2001 onwards (see Palcic and Reeves 2013).

Evidenced through the economic geography literature reviewed briefly above, the availability and quality of broadband services are of significant strategic importance to any country. This is particularly the case for a peripheral small open economy such as Ireland, where it is critical for the attraction of FDI and balanced regional development. Quality broadband services also bring numerous societal benefits and can enhance the quality of life for citizens through economic, social and cultural development, as well as by enabling economic and social inclusion for rural communities. Unfortunately for Ireland, the post-privatization developments previously outlined had a seriously detrimental impact on the development of broadband services from 2001 onwards.

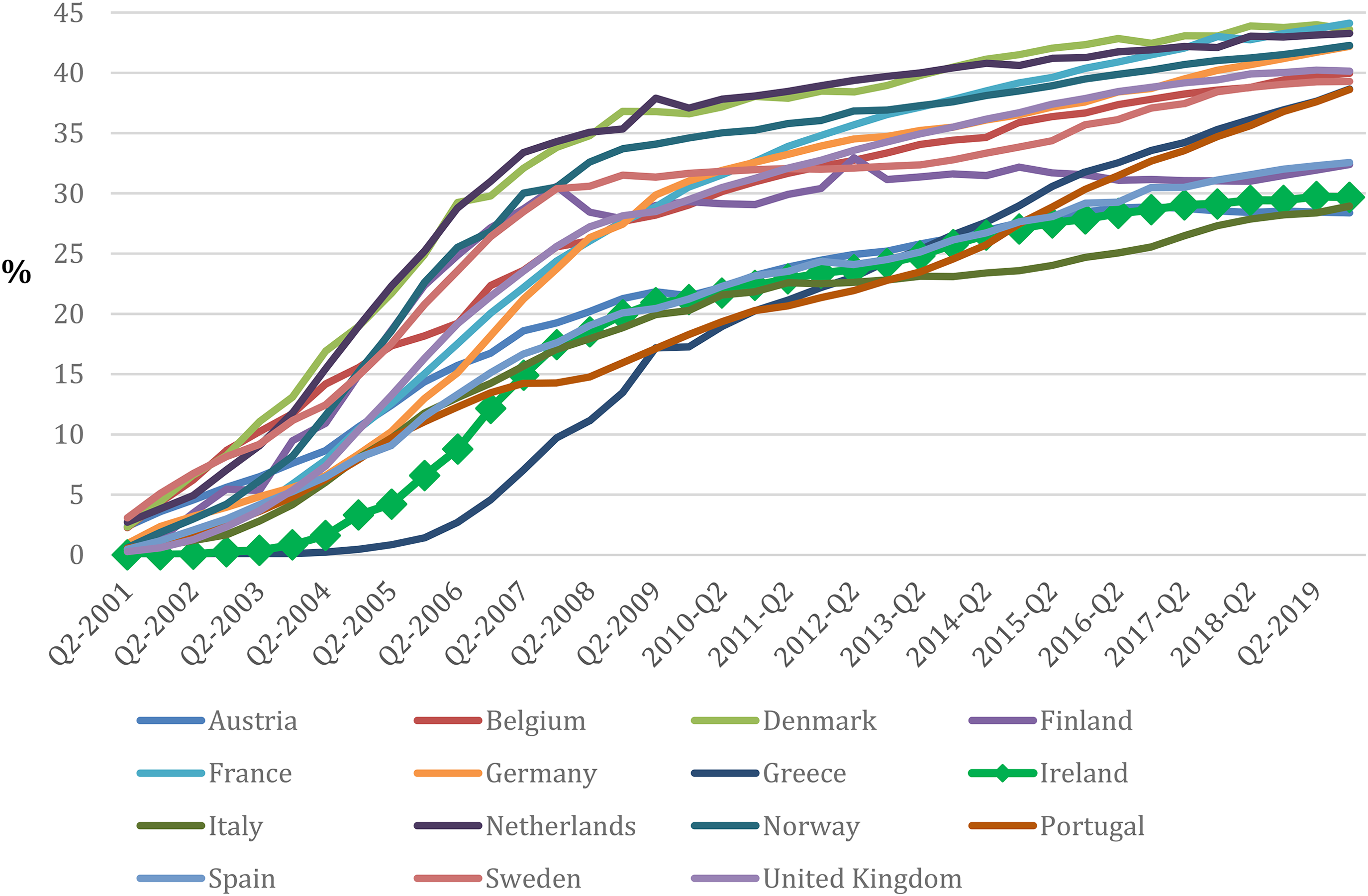

As shown in Figure 1, the initial rollout of broadband services in Ireland was a full 18–24 months behind its peers in Western Europe, with the country consistently ranked close to the bottom in terms of broadband penetration rates in the EU15 up until 2010. The principal reasons for Ireland's poor performance during this period were: (1) dramatic cuts to capital expenditure by the two different private equity owners of Eircom over the 2001–2010 period; (2) the stifling of competition in the fixed-line market by Eircom during the same period, which saw Ireland recording the lowest rate of local loop unbundling (LLU) as a percentage of DSL lines in the EU15 as well as one of the highest costs for LLU in the EU15; and (3) a lack of competition from competing broadband platforms (see Palcic and Reeves 2011). Developments during this period were not helped by a fractious relationship between Eircom and the independent telecommunications regulator (ComReg). Several rulings by ComReg were appealed by Eircom, leading to protracted High Court cases that hindered attempts by the regulator to increase the degree of competition in the market. 4

Fixed broadband penetration rates in Western Europe, 2001–2019. Source: OECD (n.d.).

Although Ireland's broadband penetration rates had begun to converge towards the EU and OECD averages by 2010, the quality of the service available at that time was extremely poor. At the end of 2009, Ireland ranked last in the EU15 and 29 out of 30 OECD countries in terms of average advertised download speeds (Palcic and Reeves, 2011, 168). The evolution of broadband services in the post-privatization period also had significant spatial dimensions. While fixed-line (DSL) broadband coverage in urban and suburban areas was close to 100% from 2006 onwards, the expansion (and quality) of such services in rural Ireland significantly lagged the rest of the EU15. This was of particular concern given that almost 40% of the Irish population lived in rural areas at the time, one of the highest proportions in the EU; an indicator of dramatic uneven development.

Phase 3 – evolving state capitalism (collaborative, small scale)

The post-privatization period was therefore characterized by significant market failure in relation to the provision of broadband services. Underinvestment in the infrastructure necessary to provide access to high-speed broadband services had the strongest negative impact in rural areas and resulted in an urban-rural digital divide that was explicitly recognized in a number of policy documents. Nevertheless, the Irish state exhibited a reluctance to extensively intervene with a more state-led approach based on public ownership. The first government-led response to this market failure was the announcement of the MANs program in 2003. This relatively small-scale intervention marked a new phase of state involvement in the telecommunications sector whereby it chose to collaborate with private interests to resolve market failures that emerged following privatization. The MANs involved the construction of open-access ‘middle mile’ fibre networks providing a link between the local access network and national backbone network in 94 towns and cities across Ireland. Once constructed, the management and operation of these networks were transferred to a private sector company as part of a concession agreement.

While the MANs program targeted middle mile infrastructure in large towns across the country, the objective of the NBS launched in 2007 was to provide basic download speeds of at least 1Mbps to rural areas in Ireland where broadband was either unavailable or deemed to be inadequate. A commercial stimulus gap funding model was adopted to deliver the plan with mobile operator 3 Ireland appointed as the preferred bidder. Using predominantly 3G mobile technologies, basic broadband speeds were provided to rural areas covering approximately 10%–15% of the geographical area of the country between 2010 and 2014 when the scheme expired; however, the actual take-up of services was far lower than envisaged and by the time the scheme had been rolled out the technology was already obsolete. The MANs and NBS programs, therefore, embodied a policy of smaller scale interventions based on hybrid arrangements between the state and private sector players. The end result of this phase of reluctant state capitalism was that Ireland continued to lag its peers across most broadband scorecard indicators produced by the EU and OECD.

Phase 4 – partnership state capitalism (national planning, for-profit partnerships)

The Irish telecommunications sector reached a critical juncture in 2010 with the publication of the EU's Digital Agenda for Europe which set a target minimum download speed of 30 Mbps for all citizens in Europe by 2020, with over half of households subscribing to speeds of at least 100 Mbps by the same date.

In the same year, Fine Gael, one of the main political parties in Ireland which have been in government since 2011, published its NewERA plan as part of its pre-election manifesto in 2010. The plan proposed a radical restructuring of the SOE portfolio through a combination of mergers, divestments and the establishment of a number of new SOEs. One of the new proposed SOEs was Broadband 21, a company that would be formed through the amalgamation of the telecommunications assets of existing SOEs such as Bord Gáis (gas), the ESB (electricity), CIE (rail), the NRA (roads) and the MANs. The new SOE would then be tasked with building out a next-generation fibre broadband network with a total investment of €1.8 billion envisaged to connect 90% of households in the country to fibre broadband. However, once in government, the radical transformation envisaged by Fine Gael was never implemented.

Phase 4 coincided with a severe economic crisis in Ireland, culminating in financial support from the Troika and a series of austerity budgets that brought a collapse in public capital investment. Detailed in Whiteside et al. (2021), the Irish state played a dominant role in bailing out its financial industry through the National Asset Management Agency (NAMA) that acquired toxic assets using government bonds. Enormous bailout-related outlays pushed Ireland into a sovereign debt crisis: Hickey et al. (2017) calculate that the financial support measures to rescue private financial institutions between 2008 and 2016 added approximately €58 billion (21% of GDP in 2016) to the stock of gross government debt by the end of 2016, with the majority of this expenditure incurred in 2010 and 2011. The severe fiscal constraints imposed on successive Irish governments as a result of the economic downturn and cost of bailing out banks led to a series of austerity budgets from 2009 onwards, which saw public sector pay cuts, higher taxes on public sector pensions, reduced social welfare payments, and major cuts to public investment.

To compensate for draconian cuts in public capital expenditure, in mid-2012, the government announced a €2.25 billion economic stimulus plan which was essentially a program of non-Exchequer financed PPP projects in sectors including transport and education. PPP use may have been urged on by immediate circumstance but was already well established domestically. Amongst European countries, Ireland had one of the highest increases of PPP use as a percentage of GDP from 2005 to 2009 (Kappeler and Nemoz, 2010, 17), and by 2013, there were nearly 100 projects at various stages of procurement and delivery (Reeves, 2013).

An opportune moment for sweeping neoliberal-style reforms, the post-crash period in Ireland did not usher in the dramatic privatization one might expect in the wake of massive government debt run up and public sector austerity. However, notwithstanding certain token divestitures, PPP in telecommunications stands out for its broad and sweeping reforms with the well-established appetite for PPP extending to the telecommunications sector in unique ways. In July 2012, Ireland published its NBP setting out how it would achieve the EU's Digital Agenda for Europe targets. Although light on detail, the plan suggested that a hybrid approach involving the private sector would be adopted with the total cost projected amounting to €350 million, which would be co-funded on a 50:50 basis by the state and private sector. This heralded a major national infrastructure strategy that was often compared to the transformative campaign to roll out electricity infrastructure and services in the early years of the newly independent state (1922). Moreover, it created a number of major policy challenges and decisions for the government with respect to the scale and geography of the infrastructure rollout, the technologies to be deployed (e.g. fibre, fixed wireless, etc.) and the choice of regulatory model (e.g. SOE, PPP, concessions contracts, etc.).

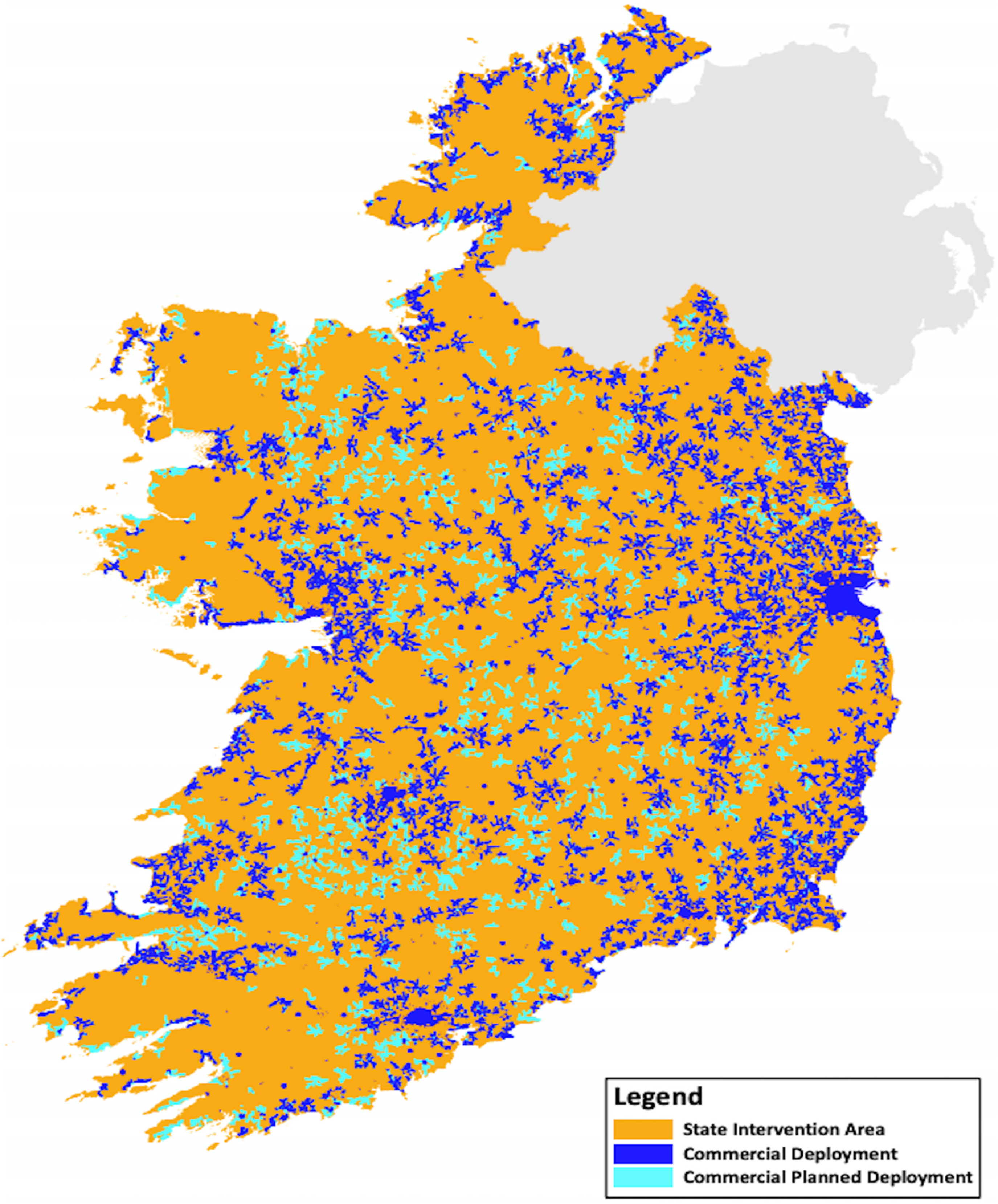

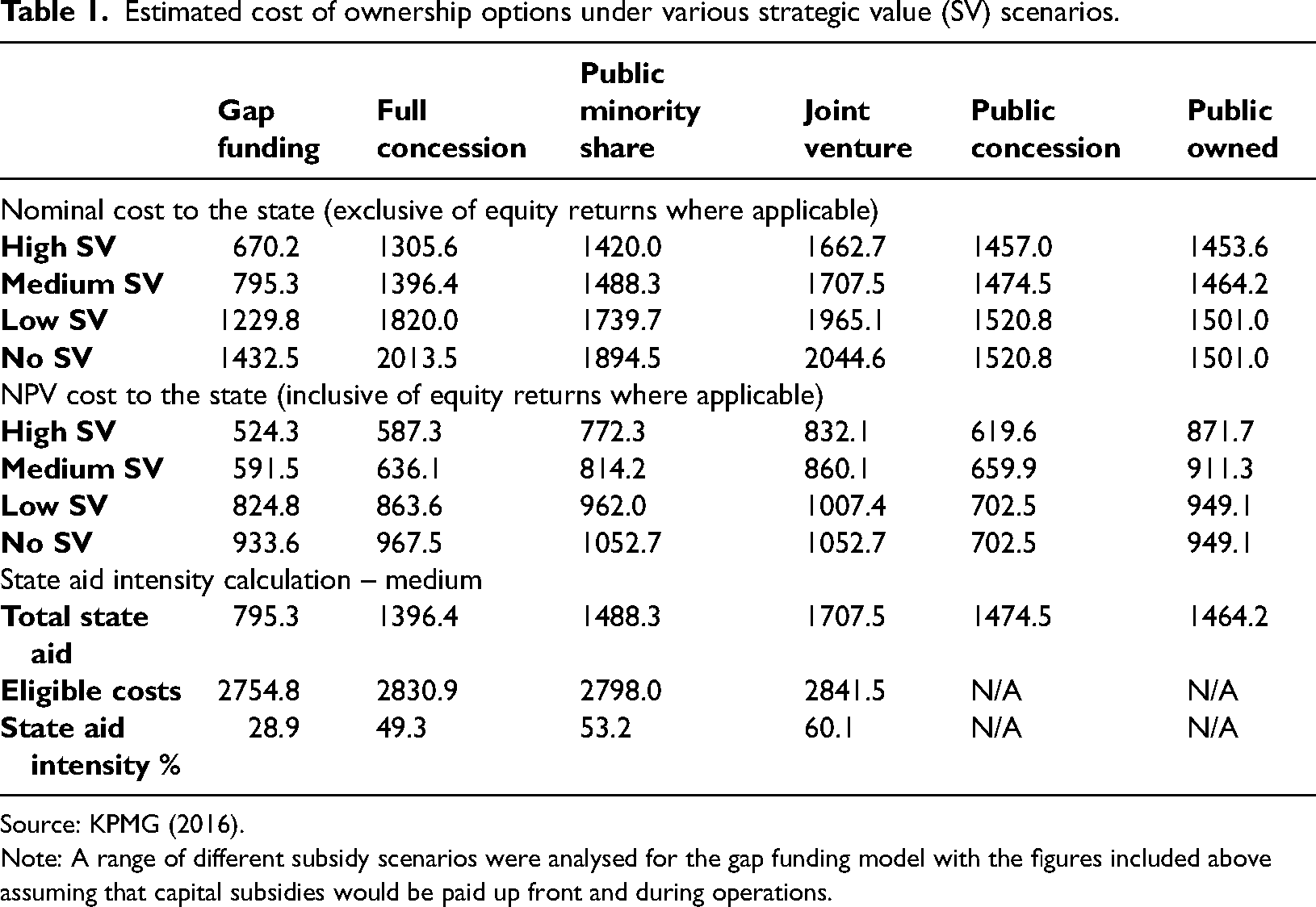

In December 2015, a more detailed broadband intervention strategy was published with the objective of connecting every premise in the country to high-speed broadband services. The intervention area for the NBP included areas where commercial operators had no current or future plans to invest within the next 2 years, and covered 757,000 premises across 96% of the landmass of Ireland (Figure 2). 5 Six separate ownership models were initially considered for the delivery of the plan ranging from the establishment of a new SOE to a variety of different public–private collaborative approaches. However, when the updated plan was published, only two options were formally put forward – a full concession (design, build, finance, operate, maintain: DBFOM) PPP model and a commercial stimulus ‘gap-funding’ PPP model. These were the only options considered after external consultants advised that they would involve the lowest cost of subsidy to the Exchequer. Table 1 sets out the assumed nominal and net present value (NPV) costs for each ownership option considered.

High-speed broadband Map, Q4 2018, Ireland. Source: DCCAE (2019).

Estimated cost of ownership options under various strategic value (SV) scenarios.

Source: KPMG (2016).

Note: A range of different subsidy scenarios were analysed for the gap funding model with the figures included above assuming that capital subsidies would be paid up front and during operations.

Reluctant state capitalism in Ireland.

LBOs: leveraged buyouts; MANs: Metropolitan Area Networks; NBS: National Broadband Scheme; NBP: National Broadband Plan; NPV: net present value; PPP: public–private partnership; SOE: state-owned enterprise.

In July 2016, the government chose to proceed with the gap funding approach on the basis that it would involve the lowest cost of subsidy to the Exchequer. However, a key assumption was that the contract would attract bids from established industry players with existing infrastructure and strong competition would drive up the strategic value (SV) bidders would attach to winning the contract, thereby lowering the cost of subsidy to the government. The figures in Table 1 highlight the importance of this assumption to the recommendation of the gap funding model. When no SV is assumed, the NPV cost estimates across all options were very close to each other. The main factor that led to the gap funding model being ranked as the least cost procurement option was the higher SV assumed.

The assumptions around SV and strong competition from existing network operators were questionable given that only two feasible bidders had existing infrastructure that they could leverage in the intervention area. The most important of these was the incumbent fixed-line telecoms operator, Eir (previously Eircom), given its legacy network and dominance in the area. The only other bidder with the existing infrastructure that could plausibly attach SV to winning the contract was Siro, a joint venture between Vodafone and the ESB, the incumbent electricity operator in Ireland. Both Eir and Siro submitted tenders for the contract and were shortlisted in July 2016 along with a third bidder made up of a consortium of different private companies, none of which had a substantial existing infrastructure in the intervention area that could be leveraged.

The prospects of a competitive tendering process were dealt a hammer blow in April 2017 when the government was effectively obliged to enter a deal with Eir to remove 300,000 homes from the intervention area. Under EU state aid rules, if a commercial operator has plans to invest in an area, then state aid cannot be granted for competing investments in the same area. This strategic move by the former SOE to annex 300,000 premises from the intervention area led ‘to ballooning budget and significant controversy with accusations that Eir was taking all the premises with a greater chance of commercial viability thus increasing significantly the cost of providing connectivity to the remaining premises and reducing the attractiveness of the project to all other potential bidders’ (EC 2020, 387).

In September 2017, shortly after the commitment deal with Eir was signed, Siro announced it was withdrawing from the competition as the deal with Eir had a material impact on the technical design and resulting business case. In a subsequent surprise move in January 2018, Eir announced it was withdrawing from the competition citing concerns in relation to increasing uncertainty about regulatory and pricing issues. The remaining consortium bidding for the contract had limited existing infrastructure that could be utilized and was therefore left in a situation where it still had to traverse Eir's 300,000 premises area to connect the remaining 540,000 premises in the intervention area, utilizing Eir's infrastructure in both areas where necessary.

Despite the complete removal of the stated rationale for proceeding with the gap funding model (SV), the government decided to persevere with the procurement process. However, the degree of public scrutiny applied to the NBP intensified over the following months, especially after the Minister for Communications resigned when it was revealed he had attended a series of private dinners and meetings with the CEO of Granahan McCourt (lead of the remaining bidder consortium). The procurement was thrust further into the spotlight when, in late 2018, the Taoiseach (Prime Minister) suggested that the cost of NBP may be many multiples of original estimation and the cost of the subsidy could reach €3 billion (compared to the original 2015 estimate of €275 million). This apparent cost escalation sparked a wave of public interest in the project and widespread criticism of how the procurement was being managed. Throughout the first half of 2019 pressure mounted as further information was gradually placed in the public domain.

During this period, significant differences between the Department of Communications and Department of Public Expenditure and Reform (DPER) were made public. In April 2019, the publication of correspondence from the Secretary General of DPER (Watt, 2019) revealed information about the escalating cost of the project and related concerns. For example, this correspondence (and other sources) indicated that the level of private equity in the project was €220 million. When compared to the cost of public subsidy (estimated at between €2.2 and €2.9 billion), this level of private equity was extremely low and raised serious doubts about the level of financial risk assumed by the private bidder. The published correspondence also revealed that the remaining bidder would have recouped its initial investment by 2028, while the state would have spent well over €2 billion by that stage.

Despite the criticism and ensuing public debate that followed the publication of this correspondence, the government pressed ahead and the Granahan McCourt consortium was announced as the preferred bidder for the NBP in May 2019. This announcement proved immensely controversial as political opponents, media and other commentators sought fuller disclosure about the details of the project and procurement. Much of the controversy focused on the size of the public subsidy, the reasons for its escalation and whether the chosen ownership option was in the public interest (especially as ownership of the broadband infrastructure would remain in private hands at the end of the contract period). The NBP became the subject of a detailed investigation by Parliament. Following weeks of public hearings, the final report provided a damning critique of the whole process and made a number of recommendations including the launch of an external independent review of the procurement and alternative models for the delivery of the NBP that ensured all new broadband infrastructures would remain under public ownership. Flouting these recommendations, the government forged ahead and signed the final contract with Granahan McCourt in November 2019. A new company, National Broadband Ireland, was established to deliver the project which aims to complete the rollout of the NBP network by 2027.

Overall, the controversial procurement of the NBP outlined in this section exemplifies the latest stage in a continuum of state capitalism models in the Irish telecommunications sector that provides strong support for our ‘reluctant state capitalism’ thesis. Over a 20-year period, the prevailing variant has shifted from commercialized style state capitalism (with full public ownership) to a hybrid-based approach that demonstrates a stubborn rejection of public ownership for strategically important infrastructure and preference for a privatist model whereby the state has ended up bankrolling the majority of the capital investment required for the construction, provision and ultimate private ownership of public infrastructure. In addition, in its pursuit of this approach, the state has been forced to establish an extensive and costly regulatory framework to oversee the NBP contract, further adding to the state's level of involvement in the telecommunications sector. 6

Discussion

Why the ‘reinvention’ of state capitalism (to paraphrase the Musacchio and Lazzarini title Reinventing State Capitalism), or the need to parse a ‘new’ state capitalism? Whether rejigged or novel, the implicit/explicit suggestion in the literature is that state capitalism waxes and wanes in society; old forms are replaced by new ones. However, as the Irish case shows, linear, hierarchical or circular process descriptions do not entirely capture the political economy dynamics involved. There is no period in time when the state recedes from capitalist interventions. More specifically, partnerships are endemic, notwithstanding their evolution. Often state capitalist hybridity is a reaction to failure in/of private markets and public regulation rather than something intrinsic to state capitalism itself; although we do find support for the observation that ‘the organization of state capitalism … at the turn of the twenty-first century is the outcome of a long process of transformation’ (Musacchio and Lazzarini, 2014, 7).

Alami and Dixon (2019b) flag the need for a more detailed treatment of the state capitalism time horizon and its territorial considerations. In the previous section, we pushed beyond the immediate to provide a historically balanced sectoral investigation of the state–market continuum in Irish telecommunications over the past century. We found state capitalism oscillating from favouring fully public to fully private with multiple forms of partnership in between. In Irish telecommunications, partnerships are evident even within extreme phases of nationalization and privatization; and power and failure play out through uneven development (rural–urban and public–private).

Perhaps because the state capitalism literature is so often focused on instruments and institutions – sovereign wealth funds, SOEs, shareholding, public finance, statism, the outward projection of national economic power, etc. – it is frequently less attuned to the motivations for domestic capitalist economic development, particular sectoral dynamics, politics at home, the push–pull of domestic ambitions and failure, and regional or subnational (especially rural) state capitalism dynamics. Thus, our account of telecommunications (and state capitalism) in Ireland steps in to provide a historically informed political economy assessment: the expression of reluctant state capitalism through an orientation of antipathy towards state ownership, privatist (market failure) accommodation and determined efforts to encourage hybridity. Here, we consider how these three themes are interwoven over time and across phases.

Reluctant state capitalism in Ireland involves a degree of antipathy towards state ownership unpredicted by a literature focused on the eager competitiveness with which states take up national champions to protect key sectors, thwart international rivals and intrude on market actors. Instead, when examined from within the domestic and sectoral context and informed by a political economy understanding of public policy, we see an SOE thoroughly commercialized in its operations and service delivery capacities (Phase 1), majority or minority shareholder options shirked in favour of the complete privatization of the public telecommunications provider followed by a number of changes in ownership that proved severely detrimental to the development of the fixed-line telecoms sector (Phase 2), small scale and thoroughly collaborative state efforts to intervene when market actors failed to provide necessary investment (Phase 3) and promises of rejuvenated SOE quickly replaced by more costly PPP (Phase 4).

Fitting the phases together, and aiming not to duplicate what has already been discussed in the paper, it is worth highlighting that the gains in efficiency and performance achieved as a commercialized SOE through hybrid forms of the strategic alliance were such that Telecom Éireann was amongst the most efficient operators in Europe by 1999 (Dassler et al., 2002; Pentzaropoulos and Giokas, 2002). Thus, the decision to relinquish full control over the company and sell the government's entire stake at the IPO stage indicates antipathy towards public ownership and willful ignorance of the company's achievements during the previous decade. Further, the seemingly unbridled enthusiasm for privatization and liberalization underestimated the risks associated with full privatization of the national telecommunications network.

The post-privatization (1999) history of the telecommunications sector was soon dominated by the plunder of the sector by private equity groups (through LBOs) and coloured by a state willing to accommodate the resultant underinvestment and poor availability of services at the standard that was consistent with the aspirations of an export-oriented, open economy. The unwillingness of short-term-focused private equity groups to adequately invest in broadband infrastructure meant that the strategic, economic, and social needs of the country (especially outside urban centres) were not met during this phase of devolved state capitalism and lagging investment was largely unchallenged by the government (with the notable exception of a fractious relationship with the independent regulator). Although this period mirrors familiar trends of minimal state intervention through laissez-faire, the ‘neoliberal’ label is far too blunt to fully account for enduring public sector involvement in the telecommunications sector (especially with regard to rural/urban distinctions). Reluctant state capitalism remains present, even if devolving at this phase.

At critical junctures in the post-privatization period, when the state was required to step in to address market failures, a consistent pattern emerged whereby the state eschewed full public ownership and increasingly accommodated the private sector by establishing collaborations and partnership arrangements. As such, a phase of evolving state capitalism emerged in which hybridity was the manifestation of the overall approach. Initially, this occurred through relatively small-scale collaborations, namely the MANs and NBS, but as time elapsed, the importance of broadband infrastructure for Ireland's small open economy and the emergence of a significant digital divide between urban and rural areas made larger scale (state) intervention increasingly necessary.

Even with dramatic market interventions as of late, the state's response reflects reluctance for public ownership and preference for accommodating private delivery through methodological biases (skewed NPV calculations and untenable assumptions of a competitive procurement process). The NBP, the largest public infrastructure contract signed in the history of the state, involved the blithe rejection of a regulatory approach based on public ownership. This is consistent with more recent developments in other public infrastructure sectors where hybrid arrangements such as PPP have been used extensively to procure infrastructures such as motorways, water and waste and social infrastructure including schools and primary care centres (Reeves and Palcic, 2017). The details of the unfolding NBP procurement process provided further evidence of the state's willingness to persist with a hybrid approach despite intense political difficulties, the collapse of competition for the NBP contract and spiralling cost of subsidy to the government. 7

The end result of these events is that the scale of market failure in broadband has been such that the state is once again a major actor in the Irish telecoms sector 20 years after its ostensible exit – arguably state capitalism by default, and certainly through reluctance. Under the NBP, the state has committed to provide the vast majority of resources required to finance the capital investment thereby bearing some of the most important project risks; and yet the hybrid (gap funding) model means that ownership of vital national infrastructure will reside with the private sector. To accommodate this approach, the state is also investing, ab initio, in a new and costly regulatory structure, which will oversee the roll-out and operation of the NBP. Policies of accommodation such as these mean that the public sector absorbs the risks and costs of market failure.

But this is no simple story of neoliberalism triumphant; state capitalism, as in the past, is afoot. Even with an obvious preference for private options, contradictions have been apparent. For example, tensions were made especially acute when managing the political and economic fallout from the Global Financial Crisis. In 2011, a new state agency, the New Economy and Recovery Authority (NewEra) was created to develop and implement infrastructure investment proposals and initial plans were made for five SOEs in five key resource sectors (named Smart Grid, Gaslink, Broadband 21, Irish Water and Bio-energy and Forestry Ireland) with NewEra acting as holding company and shareholder. None of these concrete proposals have materialized to date. For broadband, the NBP gap funding model has effectively ruled out the creation of an SOE – although, in many respects, the scale of the NBP commitments are comparable to that which would exist under full state ownership. The state remains as present (albeit in new forms) as it ever was 20 years after full privatization. Even in the face of antipathy, willful ignorance, and political pressure for the private provision of public goods, plans such as those hatched in 2011 indicate ongoing debate in mainstream political circles, and the capacity for centre-right parties in a liberalized country to contemplate and promote state-led alternatives. As Peck (2019) argued, uneven development proceeds through complex hybridity in contradictory ways, and it is no less so with the political economy of public policy and state capitalism.

Concluding remarks: Understanding (reluctant) state capitalism

The state capitalism literature emphasizes a new role played by states in global politics and domestic economies – their heightened intervention and ownership of key resources and sectors. In Ireland, we instead find a reluctant state capitalism demonstrated through antipathy towards state ownership, the accommodation of private sector failures and hybrid governance forms. In terms of its synchronic features, we see collaboration, partnership and cautious interventions across the phases of public–private continuum. Unlike elsewhere in Europe, and in contrast to the minority/majority Leviathan model famous in the ‘new state capitalism’ literature, the full divestiture of telecommunications in 1999 was comparatively unique; rather than retaining public ownership shares, the Irish state gave up any stakes or veto decision-making, frustrating the government's own stated objective of encouraging information/communication infrastructure-driven economic development and setting the stage for protracted (ongoing) interventions of regulatory, collaborative and partnership forms. Despite resultant market failures and inevitable state-backed market support, the past two decades have featured accommodation rather than any state capitalist struggle to recover public control. Even when plans were drawn up for an expansion of state ownership in 2011, determined efforts were made to quash more bold expressions of state capitalism in favour of the PPP approach adopted for Ireland's NBP.

Alami and Dixon (2019b) caution against methodological nationalism given that state capitalist strategies cut across territory. While focused on a single state (Ireland), sectoral evolution in telecommunications clearly evokes geographical considerations like rural–urban development, spatially segregated risk transfer, multi-scalar European investment and post-colonial trajectories. Rather than something new and unprecedented, the Irish state has been a long-standing feature of domestic market development and an important institution supporting private enterprise today as in the past. Urging a more academically robust conceptualization of state capitalism than that typically afforded in the literature, this paper sought to relinquish innate assumptions of obvious boundaries dividing liberalized capitalism from state capitalism in favour of engaging the domestic state and sectoral developments on their own terms and within their proper historical context. We thus identified a reluctant state capitalism in Ireland's telecommunications sector as a continuum of state–market involvement in four phases: commercial, devolving, evolving and partnership state capitalism. By highlighting temporal phases of state capitalism, the paper provided an account beyond the here-and-now of more contemporary ‘new’ state capitalism analyses that suggest rupture with an idealized, liberalized past, thus helping to inform the literature more generally (beyond Ireland and telecommunications).

On diachronic dynamics, or phases of state capitalism in Irish telecommunications, periodization clarifies the similarities and differences across state capitalist forms with an appreciation for how past phases influence subsequent ones (largely through market failure amid privatist preferences) in an evolving rather than historically truncated story of the domestic political economy. Taking a critical approach to these phases, paraphrasing Best et al. (2021, 9), we have avoided fetishizing particular and widely accepted periodizations that privilege conventional analytic categories to the exclusion of others (like Keynesian vs. neoliberal). The phase dynamics in Irish state capitalism suggest overlap, with one phase informing the next, from a commercialized SOE, to private providers and public regulators, to small-scale collaborative initiatives, and expansive PPP. Within the Irish telecommunications sector, private markets and public sectors are intertwined through various identifiable phases, and thus a ‘new state capitalism’ variant is not atypical despite its unique features.

The involvement and endurance of the Irish state in domestic economic affairs set amid forms of partnership-oriented privatization support the argument of reluctant state capitalism. In contrast to other neoliberal states, the evolving Irish developmental state, with its neo-corporatist and social partnership forms of domestic relations, dampened the pursuit of privatization policies seen elsewhere (like the UK) in the 1980s and 1990s. Telecommunications is an outlier given the notable privatist approach in the sector. Accounting for these dynamics requires a more nuanced understanding than otherwise allowed for through a largely ahistoric ‘new state capitalist’ label, or simply resorting to familiar political economy timelines invoked through ‘developmental’ versus ‘neoliberal’ state forms – all of which fail to fully capture the timeline of telecommunication-specific state interventions in Ireland. Thus our label of ‘reluctant state capitalism’ attempts to reconcile dynamic temporal features by pointing to the hybrid relations forged through a privatist approach to enduring state involvement.

Returning to the wider literature once more, one might reasonably ask what value there is in using the ‘state capitalism’ label given the concept's heterogeneity and the long-standing presence of the state in capitalism. Here, the Irish case demonstrates that particular state capitalist dynamics are at play in the domestic telecommunications sector, but they are not always underpinned by enthusiasm – instead expression of state capitalism can be coloured by a reluctance to embrace fulsome state ownership in favour of more hybrid and market-amendable forms of collaboration and partnership. Alami and Dixon (2019a, 5) describe state capitalism as involving particular ‘imaginaries’ whereby public ownership and intervention are seen ‘as deviating from a Western norm of capitalist political organization.’ For Ireland, a state often located in the liberal heartland of comparative political economy categories, state capitalism is the norm but its forms/features change over time and privatism prevails. Much like how Osborne and Gaebler (1992) urged for Reinventing Government in the 1990s, Leviathan as majority/minority owner emerged as ‘a byproduct of the liberalization and privatization reforms that began in the 1980s’ (Musacchio et al., 2015, 115). Only the story does not end there. Full-scale privatization did not sever the state's role; Ireland continued to intervene in its telecommunications sector to address market failure and the need for development, albeit through state capitalist efforts both reluctant and circumspect.