Abstract

While the drivers of preferences about tax progressivity and redistribution are well identified, the study of willingness to pay taxes remains underdeveloped. This article uses the 2016 ISSP on the Role of Government and the 2018 OECD Risks that Matter surveys to identify which groups of voters are more likely to be willing to pay taxes. It shows that ideology mediates the correlations between education or income and willingness to pay. Among the left, income and education tend to have a positive association with willingness to pay taxes, whereas both variables are negatively associated with willingness to pay among the right. Thus, the core constituencies of left-wing parties composed of socio-cultural professionals and of production and service workers have different tax policy preferences. Socio-cultural professionals, with their higher education and income, are significantly more willing to pay taxes than production and service workers, who share lower education and income.

Introduction

Governments wishing to significantly increase social spending face a conundrum: clear majorities of citizens want higher public social spending, but they seem unwilling to increase their own tax burden to pay for it. Indeed, while social expenditures are slowly rising, tax revenues are stagnating in advanced democracies (Karceski and Kiser, 2020). We know from public opinion research that the majority of citizens desire additional public spending but prefer to limit tax increases to high-income citizens (Barnes, 2015). Citizens’ preference for higher tax progressivity does not indicate a willingness to pay taxes: most citizens prefer to shift the tax burden towards high-income citizens, since few individuals consider themselves to be rich (Cansunar, 2021). As such, voters want to minimize their own tax burden and fund the public services they receive by taxing the rich.

The most generous welfare states, however, have traditionally been funded by broad-based taxes paid for by a very large proportion of the population, rather than by concentrating tax increases on relatively few richer citizens (Beramendi and Rueda, 2007; Martin, 2015). Tax competition, the relatively high elasticity of capital income to taxation, and the small number of high-income citizens, put some limits to the potential size of tax revenues to be extracted from a higher taxation of the rich (Lindert, 2004). While increasing taxes on higher income individuals remains possible, sustaining citizens’ willingness to pay is crucial to ensure the fiscal sustainability of the welfare state and to fund ambitious social policy expansion. Which voters are more likely to accept paying a higher tax burden? How does different constituencies’ degree of willingness to pay influence contemporary politics?

Analysing tax policy preferences provides an additional lens to study contemporary welfare state politics. Recent research in comparative political economy of the welfare state has been interested in how political parties try to build a winning coalition by proposing distinct kinds of social policies to attract different social classes, conceptualized in this article as occupational groups. This research agenda has been particularly attentive to left-wing parties’ core electorate: while socio-cultural professionals prefer social investment in education and childcare, service and production workers prefer social consumption policies geared towards income replacement (Beramendi et al., 2015; Häusermann et al., 2022; Busemeyer and Neimanns, 2017). Thomas Piketty (2019) deplored that centre-left parties became less interested in income redistribution as socio-cultural professionals gradually replaced the working class as their core constituency. The influence of this ‘Brahmin left’ would be one of the causes of the incapacity of governments to counter rising inequality with more redistributive social policy.

Yet, this research agenda has not studied the tax policy preferences of different constituencies and few political economists have developed theories about the preferences of different groups regarding the fiscal system (Ansell et al., 2021). Analysing the tax policy preferences of different social classes is one of the main contributions of this study. By classifying respondents with Oesch’s (2015) eight occupational groups scheme, this article contributes to comparative political economy by highlighting that willingness to pay differs between occupational groups, particularly among those composing centre-left coalitions (Gingrich and Häusermann, 2015).

Occupations have different tax policy preferences since they encompass specific combinations of income, of education and of ideology, three variables associated with willingness to pay. Education and income may reduce willingness to pay taxes as they make individuals more likely to be net contributors to the state (Benabou and Ok, 2001; Rehm, 2009). However, we argue that they can be positively associated with willingness to pay taxes. Indeed, a sufficient level of income is necessary to accept higher levels of taxes (Edlund and Johansson Sevä, 2013) and education is related to several factors that should increase willingness to pay, such as patience (Wang, 2017), trust (Hooghe et al., 2012) and the perception of the deservingness of welfare state beneficiaries (Attewell, 2022).

We contend that ideology filters material conditions (Armingeon and Weisstanner, 2022) by determining the weight that individuals put on being a net contributor to the state to determine their preferences. As such, our second main contribution is to show that ideology determines which of the positive or the negative associations of income and education on tax preferences dominates. For left-wing individuals, higher education has a positive association with willingness to pay, while higher income is negatively associated with willingness to pay for right-wing individuals. We show, however, that education has a positive association with willingness to pay, even when controlling for income and ideology.

We argue that socio-cultural professionals are the group the most willing to pay taxes, as they tend to vote for the left, are highly educated and have decent levels of income. As such, they figure at the core of a coalition to expand the welfare state’s redistributive capacity and ensure its fiscal sustainability. In contrast, service and production workers, who are poorer and less educated, are significantly less willing to pay. Hence, not only do these groups differ regarding their spending preferences and their social values (Beramendi et al., 2015; Häusermann et al., 2022), but tax policy preferences also contribute to tensions within the typical social-democratic coalition composed of low-skilled service and production workers and of socio-cultural professionals (see also Kemmerling, 2014).

The next section discusses how socio-economic status and ideology interact to predict willingness to pay taxes and how occupational groups’ tax policy preferences differ. The empirical section uses the OECD 2018 Risks that Matter (RTM) survey and the ISSP 2016 survey on the Role of Government to identify which voters are willing to pay. The final section discusses the implication of this article for comparative political economy research.

Theory: Income, education, occupation, and willingness to pay

Most studies on tax preferences have focused on tax compliance or on tax progressivity. Studies on tax progressivity find significant support for higher taxes on the rich (Limberg, 2020; Boudreau and MacKenzie, 2018; Stiers et al., 2022). Research on tax compliance highlights the interplay of rational expectations such as the tax rate or the audit rate and individual attitudes such as trust or perceptions about the fairness of the tax system (Marandu et al., 2015). However, studies about tax compliance or tax progressivity are not identifying which voters are willing to pay additional taxes themselves to fund an expansion of the state, which is the focus of this article. In fact, Barnes (2015) and Sumino (2016) showed that support for tax progressivity and for levels of taxation are driven by different factors.

This article is innovative in that it develops a parsimonious theoretical model specifying how ideology determines the association of two core variables in comparative political economy, education and income, with willingness to pay taxes. While higher education is associated with more inclusive values and with post materialistic preferences (Gelepithis and Giani, 2022; Kitschelt and Rehm, 2019), it is also associated with less support for income redistribution (Attewell, 2022) as education cushions labour market risks (Rehm, 2009) and increases prospects of upward mobility (Bénabou and Ok, 2001). Hence, highly educated individuals are more likely to be net contributors to social insurance since they are less exposed to labour market risks.

Nonetheless, education is related to several factors favouring willingness to pay taxes. Higher education is associated with patience. Patient voters are socio-tropic voters; they vote for good managers of the economy because they think that it will benefit them in the future, while impatient voters are pocketbook voters who want lower taxes to improve their situation in the present (Wang, 2017). Patient citizens should be more likely to accept paying higher taxes today to improve the public services they will receive in the future. Hence, education should be positively related to willingness to pay taxes.

Since they have a better understanding of the constraints facing policymakers and have more coherent economic policy preferences (Elkjær, 2020), more educated citizens should have a better understanding of the necessity of paying taxes to sustain public services and appreciate the potential benefits of higher taxes. Education may also be related to a better knowledge of the tax system whereas misperceptions about its functioning lead to lower satisfaction with it (Eriksen and Fallan, 1996). Education should also be related to political sophistication. Stiers et al. (2022) find that among politically sophisticated respondents, higher income doesn’t reduce support for progressive taxes, possibly because these respondents understand that relatively high taxes can lead to positive social outcomes that they value more than a marginal improvement to their own material wellbeing.

Moreover, several studies have found that education increases institutional trust since individuals with higher social status, conferred by their educational credentials, are more trustful of the institutions that have granted them their social status (Hooghe et al., 2012). Previous studies have established that institutional trust is related to more willingness to pay taxes (Tuxhorn et al., 2021; Lachapelle et al., 2021; Habibov et al., 2018). Indeed, citizens with an egalitarian ideology support a larger government when they trust institutions more than when they perceive that institutions are corrupt (Svallfors, 2013).

Finally, more educated citizens are likely to believe that welfare state beneficiaries are deserving of public support. Citizens with a lower social status, conferred by lower education, are more likely to hold negative views of welfare state beneficiaries, since they want to maintain a distinction between themselves and those further down the social hierarchy (Van Oorschot, 2006). In contrast, more educated citizens do not need to stigmatize the welfare state beneficiaries to maintain their social status (Attewell, 2022). Previous research has established that taxpayers are more willing to pay to fund state spending allocated to citizens whom they deem deserving (Stanley and Hartman, 2018). Building on these four mechanisms, we pose the following hypothesis:

Education has a positive association with willingness to pay. The second main variable influencing willingness to pay is income, for which we expect even more contradictory effects. On the one hand, higher-income citizens are more likely to be net contributors to the welfare state: income reduces the need for social benefits and increases the amount of tax paid in proportional and progressive tax systems. Indeed, Sumino (2016) finds that higher income is correlated with support for lower levels of taxes. On the other hand, a sufficient level of income is a necessary condition for willingness to pay. Individuals living in precarious financial situations may feel that an additional tax burden is unfair or that it would significantly decrease their wellbeing. Although they want more public expenditures, they may prefer to shift the tax burden to higher-income individuals. Edlund and Johansson Sevä (2013) show that low-income Swedes are more likely to want ‘something for nothing’, that is, higher public spending but lower taxes. In fact, higher-income individuals may be more likely to perceive the current income distribution as fair (Alesina and Angeletos, 2005), improving their institutional trust and ultimately their willingness to pay. Hence, theoretically, income, and, to a lesser extent, education, may have either positive or negative effects on willingness to pay. We expect that left–right ideology regarding the role of the state in ensuring redistribution to reduce inequality influences the weight that being a net contributor to the state has on citizens’ preferences. The left puts more value on the public services that taxes are paying for, is ideologically committed to income redistribution and accepts to confer collective responsibilities to the state. Moreover, ideology filters citizens’ perception of taxes, as the left believes that taxes are lower, less progressive and less detrimental to the economy than do the right (Stantcheva, 2021). While the left draws on ability-to-pay principles and highlights the importance of taxes in sustaining public services, the right tends to reject higher taxes. Additionally, self-interested motives have more legitimacy among the right (Armingeon and Weisstanner 2022). Therefore, we expect that since the left perceive taxes and state intervention more positively, left-wing respondents’ preferences are less likely to be driven by whether they are net contributors to the state. Higher education and income, which are associated with being a net contributor to the state, should have a negative association with willingness to pay among right-wing respondents (Armingeon and Weisstanner, 2022). Right-wing citizens with higher income and education may prefer private insurance, further reducing their support for taxation. In contrast, among the left, high education is particularly likely to be associated with willingness to pay since education is associated with many non-material motivations to be willing to pay taxes. Moreover, among the left, those with a higher income should be more willing to pay than those with lower income, since they have more financial means to do so. This moderation of ideology on income or education is put forward by Armingeon and Weisstanner (2022) who show that income doesn’t reduce support for redistribution among left-leaning citizens and by Abou-Chadi and Hix (2021) who demonstrate that among left-wing voters, those with higher education support redistribution more so than those with lower levels of education. Therefore, we expect that:

Ideology mediates the relationship of education and income on willingness to pay taxes. Our expectations regarding income, education and ideology are reflected in differences between the preferences of occupational groups, which represent social classes in contemporary political sociology. Occupations are interesting to study for two reasons. First, their preferences matter since they are the foundations of the coalitions that political parties aim to mobilize. Occupations define social classes and represent the socio-structural makeup of parties’ supporting coalitions (Abou-Chadi and Hix, 2021). The composition of parties’ supporting coalitions is crucial to explaining welfare state politics (Gingrich and Häusermann, 2015; Beramendi et al., 2015), but previous research has not established if tax policy preferences differ by occupations. Second, occupations embody the three variables that we are interested in, as they differ in their ideology, education, and income levels, allowing us to validate our main findings and to propose an even more parsimonious model of tax policy preferences. We use Oesch’s (2015) class scheme based on wage levels, type of employment contract, of tasks conducted and on the degree of autonomy and authority of an occupation. Comparative political economy research has established that left-wing parties’ constituencies are the highly educated socio-cultural professionals working in jobs requiring interpersonal interactions, often in the public sector, and the low-skilled service and production workers (Gingrich and Häusermann, 2015). The typical centre-right coalition is composed of small business owners, managers and business professionals preferring less state intervention (Beramendi et al., 2015). Previous research has revealed several tensions within these coalitions between each constituencies’ preferred types of public spending, or their preferences about immigration, social values, and globalization (Beramendi et al., 2015; Häusermann et al., 2022). This article argues that taxes, and more precisely, willingness to pay taxes, represents an additional source of tension within the centre-left coalition. With their high education and their ideology associated with support for state intervention (Abou-Chadi and Hix, 2021), sociocultural professionals should be the occupational group the most willing to pay higher taxes. The only working paper focusing on the tax policy preferences of different constituencies finds that socio-cultural professionals are the occupational group the least likely to perceive that governments have reached the limits of the levels of taxation (Häusermann et al., 2019). In contrast, low-skilled service and manufacturing workers share both lower incomes and education and should thus be less willing to pay higher taxes, despite their ideology in favour of state intervention. We propose the following hypothesis:

Service and production workers are significantly less likely than sociocultural professionals to be willing to pay higher taxes.

Empirical analysis

Cross-national research on public opinion on taxation tends to use questions that are not specifying to the respondent that she would herself be paying more taxes to fund the additional spending she wants. This article innovates by being one of the first pieces of academic research using the OECD (2018) RTM survey, which is one of the few publicly available cross-national surveys asking respondents about their own willingness pay higher taxes. Unfortunately, the RTM survey doesn’t include ideal measures of ideology, as we discuss in detail below. Hence, we complement the RTM with the ISSP survey that has better measures of ideology and that also allows us to adequately measure respondents’ occupations. Moreover, the ISSP allows us to control for two important variables that are not included in the RTM: trust and political sophistication. However, the ISSP survey doesn’t ask direct questions on willingness to pay. The RTM survey includes 20 OECD countries (N = 22,488), while the ISSP survey includes 22 OECD countries (N = 28,508). 1

Analysis with the risks that matter survey

The RTM survey asks a question about willingness to pay for different types of expenditures. The question is, ‘Would you be willing to pay an additional 2% of your income in taxes/social contributions to benefit from better provision and access to: [10 different policy choices are offered, the respondent can choose more than one option].’ The dependent variable is a dummy coding respondents as willing to pay if they accept paying 2% higher taxes. This question is particularly relevant since it specifies to the respondents that they would themselves be paying more taxes, in exchange for receiving better services. More than 65% of respondents are willing to raise their own taxes if they would receive additional services in exchange.

We measure income as the decile position of the respondent’s household in the country-specific household disposable income distribution, based on the OECD Income Distribution Database of 2017. Education is measured as a nine-category variable based on the respondent’s highest educational level attained, from no formal education to completed university. Ideology is measured as an additive index based on the three most relevant questions in the RTM survey to measure left–right ideology on the extent to which the state should intervene in the economy to reduce inequality. The first question, ‘Should the government tax the rich more than they currently do in order to support the poor?’, has a five-degree scale answer ranging from ‘definitely not’ (scored −2) to ‘definitely yes’ (scored 2). The second question, ‘Why do you think people live in poverty?’, is scored as the sum of respondents who say that people are poor because they are unlucky and/or because of injustice, minus the sum of responses mentioning that poverty is caused by laziness and/or is inevitable. The third question, ‘To what extent do you agree or disagree that most people receive public benefits without deserving them?’, is scored between −2 for respondents who strongly agree and two for respondents who strongly disagree. Hence, each variable is a five-category scale ranging from −2 (right) to 2 (left), summed to create an additive index (Alpha = 0.63). Since fewer than 0.5% of respondents score −6 or 6, they are collapsed to −5 and 5 to create a right/left index ranging from −5 to 5. Including a question about fiscal redistribution to predict willingness to pay taxes does not bias the results, since the two variables are only very weakly correlated (r = −0.06). Nevertheless, as shown in the Supplemental Appendix, the results are robust to replicating the interaction with each individual component of the index.

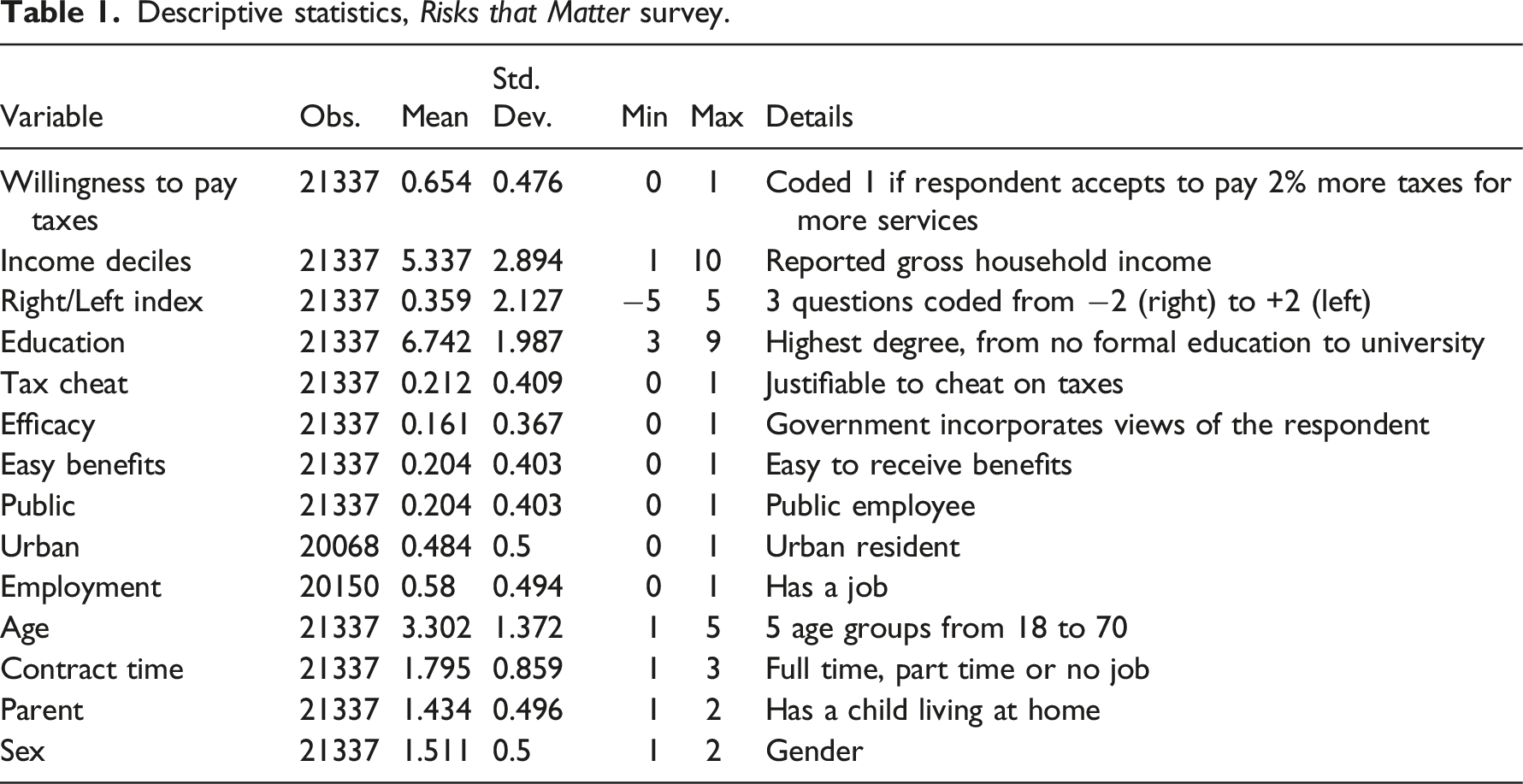

Descriptive statistics, Risks that Matter survey.

Intraclass correlations reveal that only 2.4% of the variation in willingness to pay is explained by differences between countries, suggesting that very little relevant information can be extracted from a mixed effect multilevel model. Therefore, we use an OLS regression with country fixed effects, along with standard errors clustered at the country level. In the Supplemental Appendix, we present similar results with models replacing the fixed effects with macro-level controls and random effects or using logistic regressions rather than OLS.

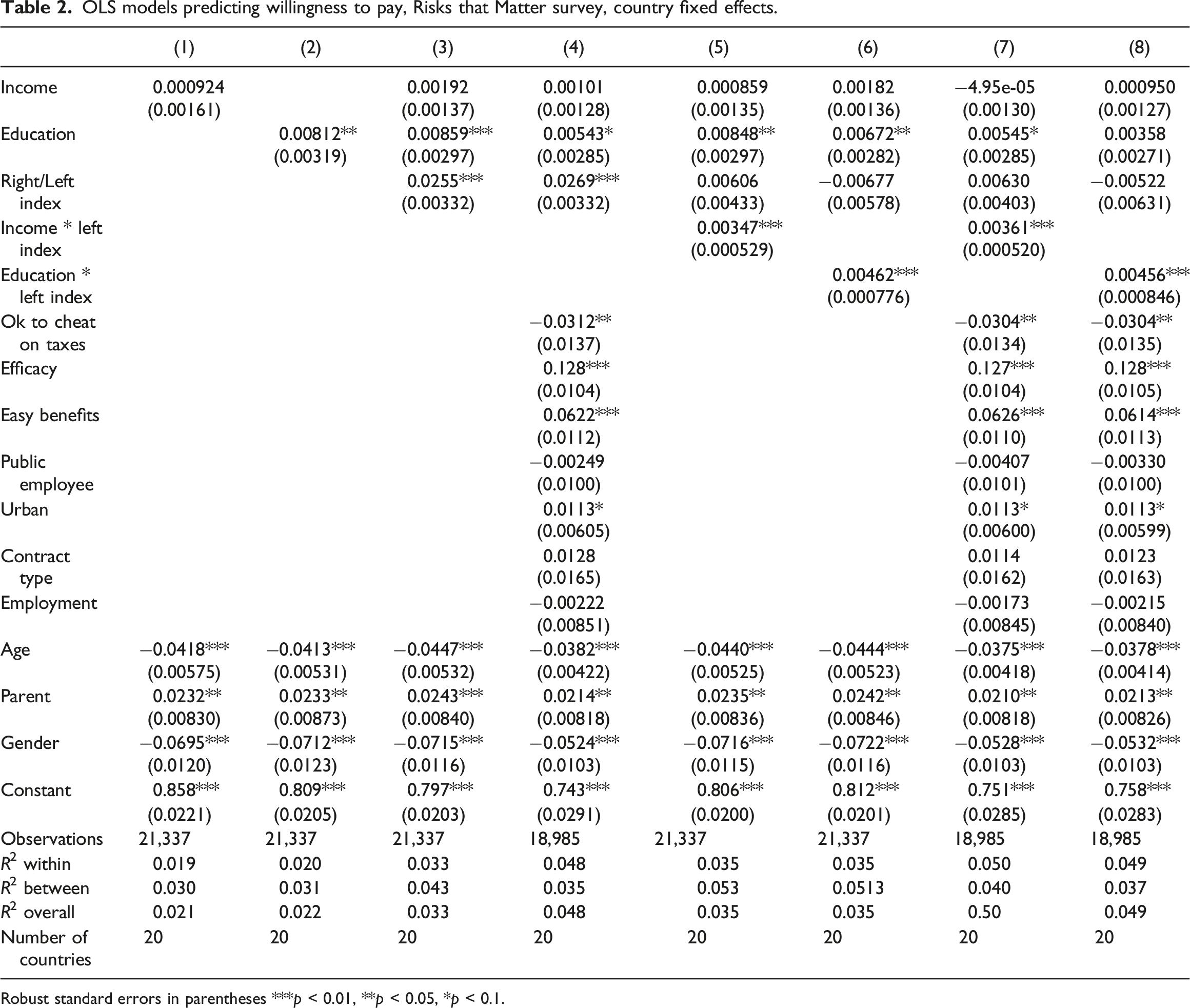

OLS models predicting willingness to pay, Risks that Matter survey, country fixed effects.

Robust standard errors in parentheses ***p < 0.01, **p < 0.05, *p < 0.1.

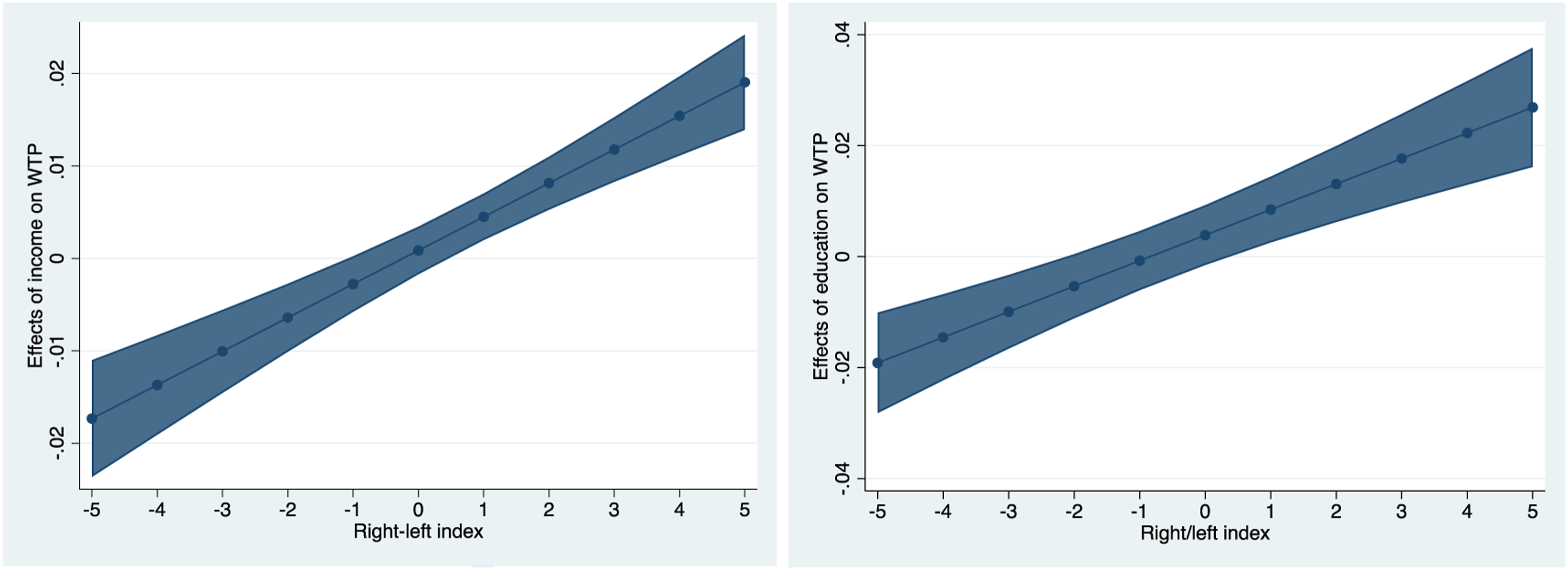

Models 5 to 8 reveal a significant interaction between income or education and ideology. Figure 1 relies on models 7 and 8 to present the marginal effect of income (left panel) or education (right panel) conditional on the right/left index to predict willingness to pay. Both panels reveal that ideology moderates the association of income and education on willingness to pay. For right-wing respondents, higher income and education is associated with less willingness to pay, whereas for left-wing respondents, higher income and education increases willingness to pay. For a right-wing respondent scored −3, a one SD increase in income/education diminishes willingness to pay by 6% of a standard deviation for income and 4% for education. For a left-wing respondent scored 3, a one SD increase in income and in education increases willingness to pay by 7% of a standard deviation. In the Supplemental Appendix, we ensure that the relationship between education, income and willingness to pay is linear and devoid of thresholds (Hainmueller et al. (2019) and show that the results are robust to listwise deletion ensuring that each model has the same number of cases (we do the same for the ISSP analysis). Average marginal effect of income (left panel) and education (right panel) on willingness to pay, based on models 7 and 8 of Table 2.

Analysis with the ISSP

In the ISSP Role of Government survey, the main question about tax policy preferences asks respondents about their perception of current levels of taxes (much too high, too high, about right, too low, or much too low) of different income groups (high, middle, and low incomes). In contrast to the main question analysed with the RTM survey, it is not a direct question on willingness to pay. Still, we create two variables measuring support for higher levels of taxation with these questions.

The first one is a measure of unwillingness to pay: a dummy variable coded 1 if the respondent thinks that taxes on middle incomes are too high or much too high and coded 0 otherwise. This variable assumes that citizens share a misperception about the real income distribution: few voters perceive themselves to fit within the ‘high income’ category since they tend to situate themselves within the ‘middle-class’ even if they are richer than the objective position of the middle-class in the income distribution (Cansunar, 2021). In fact, support for taxing middle incomes varies little across income groups (Ansell et al., 2021), suggesting that respondents of all income groups may be thinking about themselves when revealing their preferred level of taxes on middle-income groups. To ensure that respondents are thinking about taxes on themselves when asked about taxes on middle-income groups, we restrict the sample to respondents who perceive themselves to be in the middle class, based on answers to a question on self-perception of class position. This question is asking respondents to place themselves in the group where they perceive themselves to belong using a 0 to 10 scale. We create a subsample of middle-class respondents with the remaining 75% of respondents who place themselves in the middle groups (4–7). We use a subsample based on middle income respondents as a robustness check presented in the Supplemental Appendix and find similar results. We prefer to use perceived class positions in the main analysis since respondents’ knowledge of their position in the income distribution may not be accurate. About half the respondents in the subsample think that taxes on middle incomes are too high.

The second dependent variable follows Barnes (2015) and Sumino (2016) and measures preferences for higher levels of taxes in general. Respondents receive a score of +1 each time they consider that taxes on one of the three income groups are too low, 0 when they think they are about right and −1 when they are too high. The sum is then divided by 3, so that the variable Taxlevels ranges from −1 (thinking taxes are too high on each income group) to 1 (thinking taxes are too low on each income group). The average score is relatively low: the mean of the Taxlevels variable is −0.26, a third of respondents score 0 and only 12% score above 0, revealing that very few respondents prefer a higher overall tax burden (Barnes, 2015). The two tax variables are correlated at p = 0.71.

To calculate respondents’ income from the ISSP, we divide each countries’ household incomes into deciles, taking into account the size of the household, by dividing the household’s income by the square root of the number of household members (Armingeon and Weisstanner, 2022; Cansunar, 2021). We measure education as a 7-category variable ranging from no formal education to upper-level tertiary (graduate degree). Vote choice is used as a measure of ideology. We use the ISSP’s coding of parties and code respondents as 1 if they voted for left or far left parties, two for centre and liberal parties and 3 for right, conservative and far-right parties. This reduces sample size because it includes only respondents who voted in the last election (16,821). The Supplemental Appendix reveals that the results are robust to using preference for government redistribution between the rich and the poor as an alternative measure of ideology.

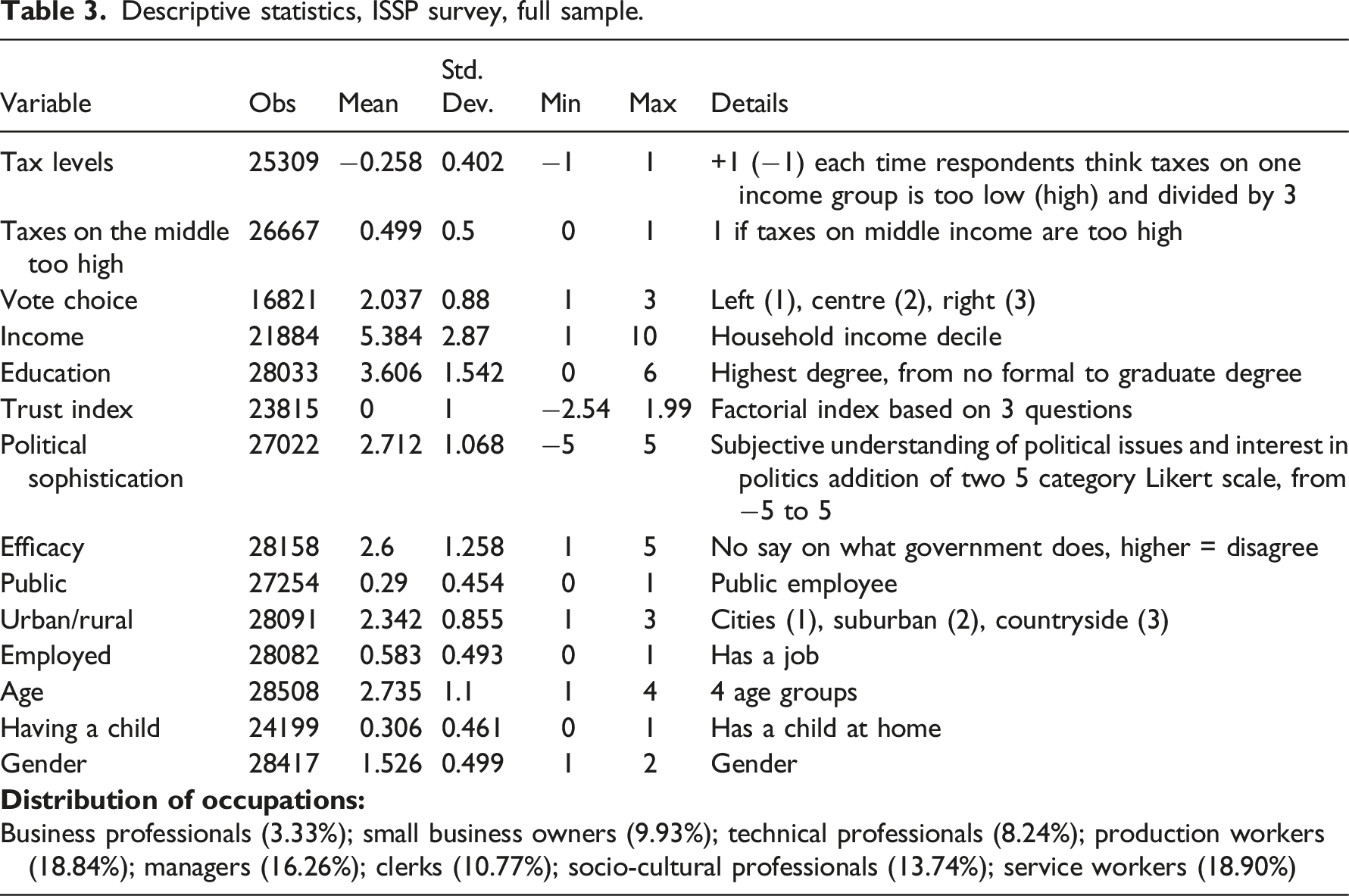

Descriptive statistics, ISSP survey, full sample.

Similar regression models to the RTM are used to analyse the ISSP survey using country fixed effects along with standard errors clustered at the country level. Since the Taxlevels variable is continuous, we use an OLS regression to model both variables, but present similar results with logistic models in the Supplemental Appendix. The intraclass correlation is higher in the ISSP than in the RTM (7% for the taxlevel variable and 8.6% for taxes on the middle class) but multilevel models reveal similar results to the main models.

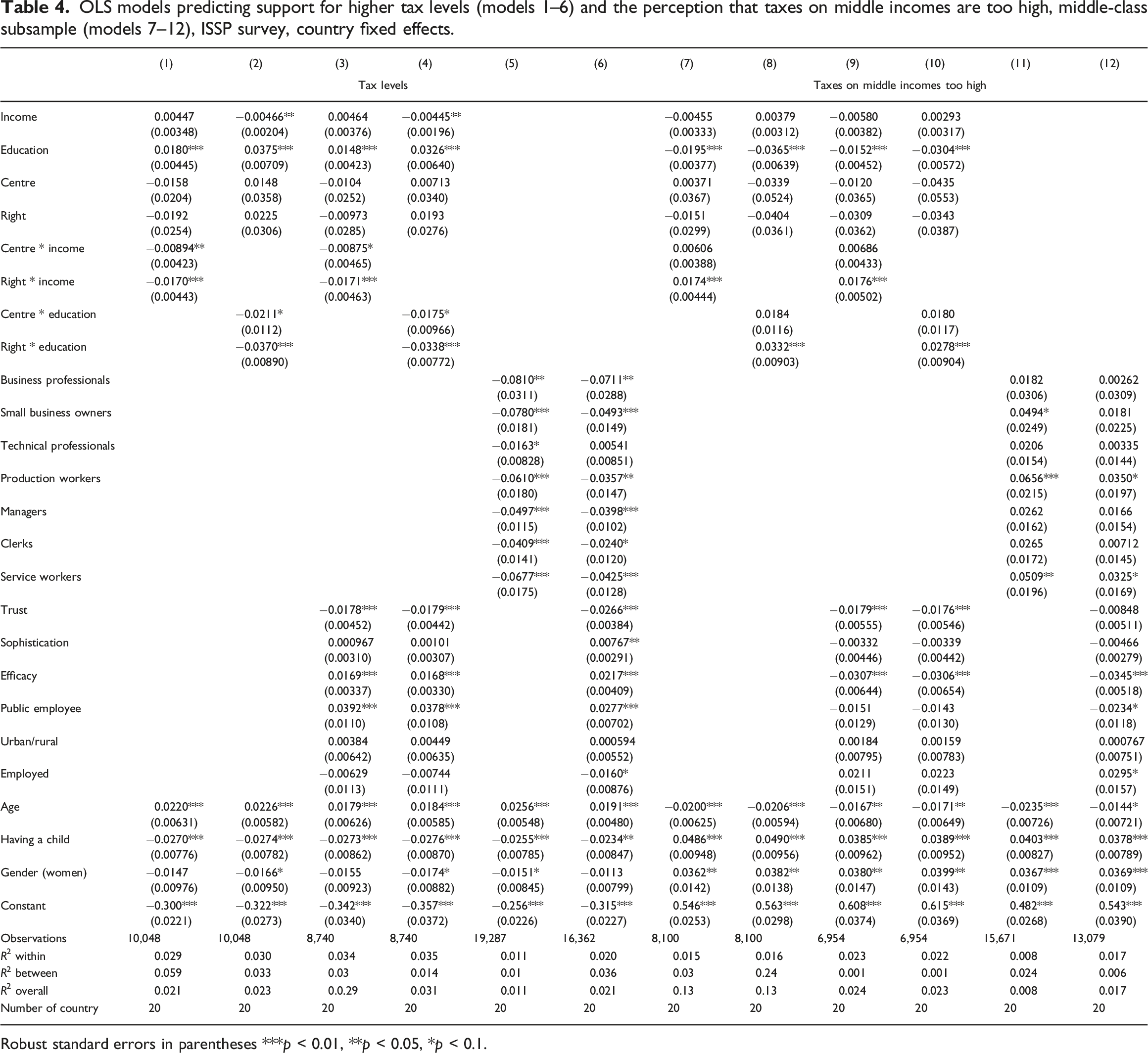

OLS models predicting support for higher tax levels (models 1–6) and the perception that taxes on middle incomes are too high, middle-class subsample (models 7–12), ISSP survey, country fixed effects.

Robust standard errors in parentheses ***p < 0.01, **p < 0.05, *p < 0.1.

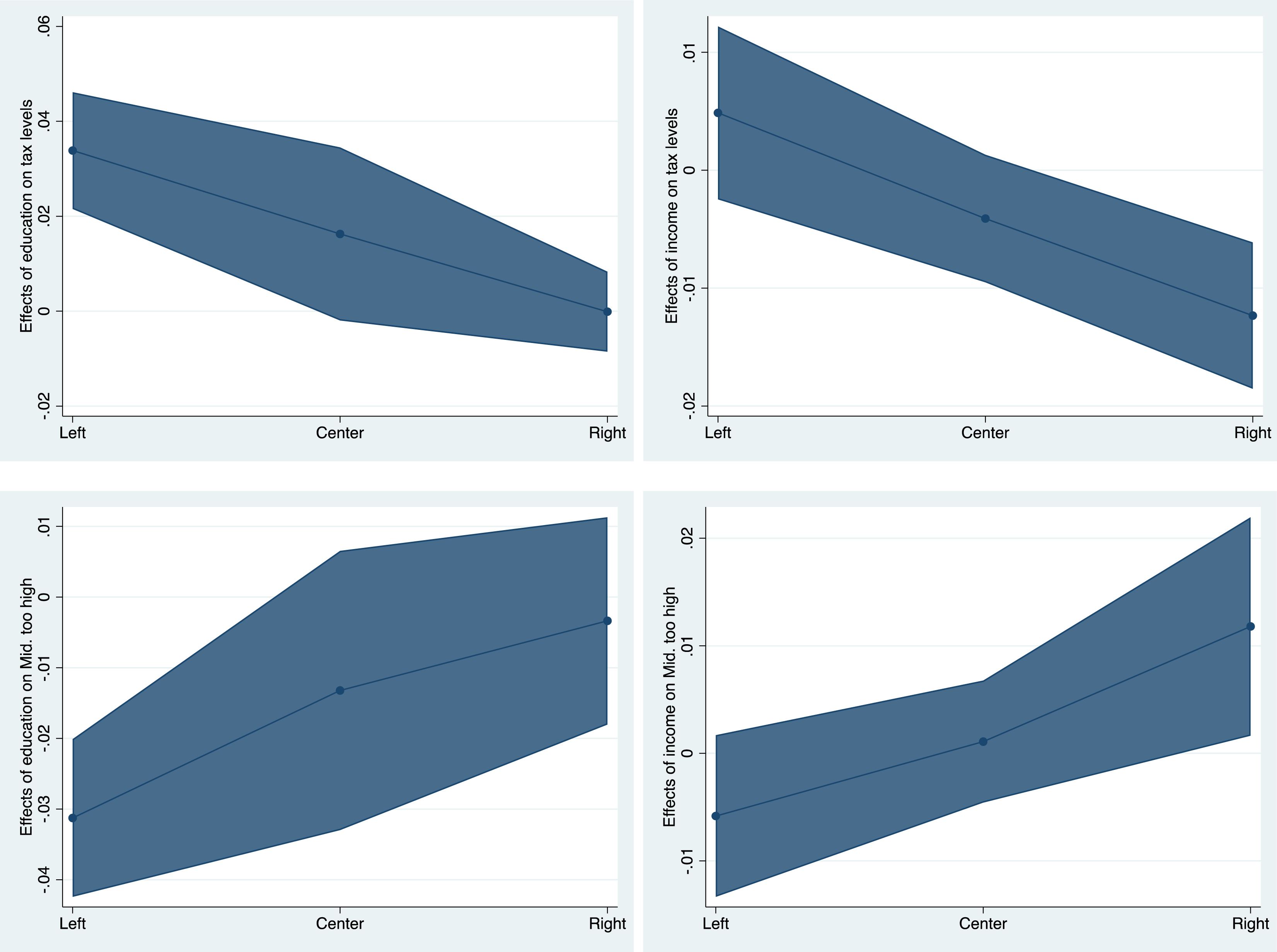

Figure 2 presents the interaction between income/education and vote choice based on models 3, 4, 9 and 10. Education increases willingness to pay among left voters: a one SD increase in education raises support for tax levels by 12.5% of a standard deviation (for the tax level variable). In contrast, education is not significantly associated with willingness to pay among right and centre voters. A one SD increase of income reduces willingness to pay for right-wing voters by 8.6% of a standard deviation (for the tax level variable) but has no association with willingness to pay among left and centre voters. The size of the association of the interaction of income and education is similar when taxes on middle incomes is the dependent variable. Average marginal effect of income and education, conditional on vote choice to predict tax levels (upper row) and too high taxes on the middle incomes (lower row), based on models 3, 4, 9 and 10, Table 4.

An analysis presented in the Supplemental Appendix confirms that occupations differ by income, ideology and education as expected. Socio-cultural professionals are the group the most likely to vote for the left, followed by production and service workers and technical professionals. Self-employed professionals, small business owners and managers are the main constituencies of right-wing parties. Socio-cultural professionals are the most educated group, just above managers and business professionals, but have lower incomes than these two groups. Production and service workers are the least educated and have the lowest income.

In Table 4, socio-cultural professionals, the most pro-tax constituency, are used as a reference category. We do not include education, income, and ideology in models 5, 6 11 and 12 since the ISCO codes that are used to classify occupations include education and our main objective is not to show that occupations predict attitudes on top of our three main predictors. Rather, we wish to use occupations as a parsimonious proxy of the interaction of ideology and education or income. These models reveal that service and production workers are significantly more likely than socio-cultural professionals to believe that taxes on the middle are too high and to prefer lower tax levels. In model 5, being a production or a service worker relative to a socio-cultural professional reduces the tax level variable by 0.06 or 0.07, which is about 15% of a standard deviation. The estimation of the equivalent of model 11 with a logistic model reveals that being a production worker relative to a socio-cultural professional increases the probability of thinking taxes on the middle-income groups are too high by 25% (18% for service workers). Interestingly, service and production workers are the only two occupations that are consistently more likely than socio-cultural professionals to believe that taxes on the middle are too high. All constituencies except technical professionals are less likely to prefer higher tax levels than socio-cultural professionals.

Hence, this analysis suggests that occupations that are typically on the left and that have higher income and education are the ones with the highest willingness to pay taxes. In contrast, occupations with high income/education that are on the right, or low income/education left-wing occupations are less likely to be willing to pay taxes. In the Supplemental Appendix, we incorporate the interaction of education/income and vote choice in models including occupations. The interaction remains significant when including occupations, but the difference between socio-cultural professionals and service/production workers largely disappears, reflecting that the interaction catches part of occupations’ impact. The difference between occupations associated with the right and socio-cultural professionals remain intact, at least for the tax level variable.

Discussion and conclusion

This study highlights the pertinence of interacting ideology with material interests to analyse individual preferences (Armingeon and Weisstanner, 2022). While preferences for tax progressivity and redistribution tend to decrease with income, opinions about willingness to pay are more complex: for individuals sharing a left-wing ideology, low-income citizens tend to be less willing to pay than high-income citizens. Citizens need to have the means to pay additional taxes and a sufficient level of education to connect taxation and spending. Contributing to studies on the impact of education on political preferences (Attewell, 2022; Gelepithis and Giani, 2022), we have highlighted the positive impact of education on willingness to pay, which is especially strong among left-wing individuals.

The results of the ISSP survey mirror those of the RTM survey and allow us to confirm our three hypotheses. There is one difference between the results of the two surveys: in the RTM, education and income increases willingness to pay among the left and decreases it among the right, whereas in the ISSP the association of education with willingness to pay is positive and significant among the left and insignificant otherwise, while the association of income is negative and significant among the right and insignificant otherwise. This divergence can be explained by differences in wording of the questions and in the measurement of ideology, but it suggests that the association of education with willingness to pay is clearly positive among the left, whereas the association of income and willingness to pay is only positive in the RTM models.

The nature of the questions represents a limitation of the study. We assumed that respondents are thinking about their own taxes when they are asked about taxes on middle incomes. While the question of the RTM survey is more direct, it asks respondents to pay almost exclusively for social policies; only one possible response concerns public safety. Respondents’ ideology is therefore more likely to be correlated with willingness to pay than if the responses included more items associated with the policy preferences of the right such as defence, the police, or the justice system. Moreover, the effect sizes of our main variables are relatively small, but our main contribution was to show that ideology determines which of the positive or negative effect of income dominates.

Our other main contribution is to highlight the tax preferences of different social classes, measured with occupational groups. The analysis conducted in this article reveals an additional tension within centre-left coalitions concerning taxes (Kemmerling, 2014): not only is there a tension between sociocultural professionals on one side and low-skilled service and production workers on the other side concerning social values and the prioritization of investment and consumption (Beramendi et al., 2015; Häusermann et al., 2022), but our analysis of tax policy preference reveals that they also diverge on their willingness to pay. Sociocultural professionals are willing to raise their own tax burden considerably more than production and service sector workers. The unwillingness to pay of service and production workers is related to income and education: even if they would benefit from more public services, they may feel that additional taxes are a cost that they cannot afford to bear. Further research should analyse if institutions and public policies help to reduce the differences between occupational groups’ tax policy preferences.

Our results suggest that many left-wing voters refuse to raise their own tax burden. The unwillingness to pay of a large proportion of their constituents puts centre-left parties in a difficult situation: they need to raise taxes if they want to increase spending, otherwise they must implement cutbacks in some policy areas to fund additional spending in other policy domains, which may also contribute to tensions between their constituencies. Nevertheless, the willingness to pay of sociocultural professionals offers a silver lining for centre-left parties. Piketty (2019) criticized the shift in the electoral constituencies of left-wing parties, describing contemporary social-democratic parties as the ‘Brahmin left’ attracting educated citizens who are less interested in income redistribution. However, these educated progressive voters are willing to pay higher taxes. This contrasts with the traditional core constituency of the left which doesn’t have the means and the will to sustain higher taxes. If progressive parties can propose a unifying policy agenda bridging tensions between groups, social-cultural professionals may represent key voters willing to contribute to a more generous welfare state.

Supplemental Material

Supplemental Material - Explaining willingness to pay taxes: The role of income, education, ideology

Supplemental Material for Explaining willingness to pay taxes: The role of income, education, ideology by Olivier Jacques in Journal of European Social Policy.

Footnotes

Acknowledgements

The author wishes to thank Elizabeth Gidengil, Silja Häusermann, Bilyana Petrova, Dietlind Stolle, David Weisstanner and participants to conferences at the Université de Montréal (2019), the Center for the Study of Democratic Citizenship (2019), McGill University (2019), the Canadian Political Science Association (2019), the Society for the Advancement of Socio-Economics (2021) and the ECPR joint Sessions (2022).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Fonds de recherche du Québec Société et Culture postdoctoral scholarship.

Data availability statement

Data will be made available in an online repository upon publication and the author is willing share to the data throughout the peer review process.

Supplemental Material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.