Abstract

Many low-income households in rich countries have very little wealth, but the role of intergenerational wealth transmission in underpinning this deficit is not known. This article seeks to fill that gap by investigating patterns of past wealth transfer receipt for low-income versus other households in seven rich countries and assessing the contribution that these transfers, or their absence, make to current wealth levels. We find that households on low incomes are relatively disadvantaged in terms of intergenerational transfers received in the past, both in terms of the likelihood of having received any and the amounts received by those who do benefit from such transfers. The role that this disadvantage plays in the linkage between current low-income and low wealth is assessed and evidence presented that it is significant. Simulation of a universal wealth transfer scheme or ‘capital endowment’ on reaching adulthood for two countries shows that such a policy could lead to a marked decline in the proportion of low-income adults with negative or no wealth. This and alternative or complementary policy responses to these wealth deficits merit the most serious attention.

Introduction

Many low-income households in rich countries have little or no wealth, and this represents a major additional disadvantage with deep-seated implications for their living standards, economic security and wellbeing. This is clear from studies of the distribution of wealth and of poverty risk framed to capture both income and wealth (Azpitarte, 2011; Kuypers and Marx, 2018; Kuypers and Marx, 2019; Kuypers and Marx, 2021, in this issue). The vulnerability associated with having little or no property wealth or financial buffer to fall back on is of particular salience in a major economic shock such as the one caused by the current COVID-19 pandemic crisis (Kuypers et al., 2021). The role of intergenerational transfers of wealth in the accumulation of wealth and generation of wealth inequality has been a topic of long-standing research interest (for example, Gale and Scholz, 1994). However, the role that these transfers – or the lack of them – play in underpinning the wealth deficit faced by many low-income households has received little attention and has not been explored in a comparative framework.

This article aims to fill that gap by examining patterns of past wealth transfer receipt for low-income versus other households and assessing the contribution that these transfers, or their absence, make to current levels of wealth for these households. We do so in a comparative perspective using microdata from household wealth surveys for seven rich countries – Great Britain, France, Germany, Ireland, Italy, Spain and the United States. These countries are selected to cover a range of circumstances in terms of average income and wealth levels and their distribution as well as welfare state regimes. We focus on a limited set of countries for ease of exposition, but the analysis could be extended in future to other rich countries for which the required data from wealth surveys is recently available.

The article presents a brief overview of theoretical considerations and previous research and then describes the data sources and variables employed. Patterns of receipt of intergenerational wealth transfers for low-income versus other households are then examined, via a descriptive picture and estimated regression model. The role of intergenerational transfer receipt in understanding current wealth levels for low-income households and overall is then assessed. We then examine a policy now being widely advocated to address the wealth deficits of lower-income households, simulating the impact of a universal capital endowment, and conclude with a summary of our findings and their implications.

In brief, these findings are that households on low-incomes are on average relatively disadvantaged in terms of intergenerational transfers received in the past, and that there is suggestive if not robustly causal evidence that this plays a significant mediating role in the link between current low income and low wealth. A universal wealth transfer scheme or ‘capital endowment’ on reaching adulthood could lead to a marked decline in the proportion of low-income adults with negative or no wealth. This and alternative or complementary policy responses merit the most serious attention.

Theory and previous research

Studies exploiting the availability of survey microdata containing information on both income and wealth have considerably advanced understanding of the complex inter-relationship between them, showing that the correlation between income and wealth distribution is substantial but far from perfect (see for example Jäntti et al., 2008). National and comparative studies of wealth distribution make clear that mean or median wealth levels are particularly low for low-income households, of whom a substantial proportion report little or no wealth (see for example Rowlingson and McKay, 2011, for the United Kingdom, Wolff, 2017 for the United States and Balestra and Tonkin, 2018, for a comparative picture). Studies incorporating both income and wealth into an enhanced poverty measure highlight how ‘poverty risk’ framed that way varies with age and household structure in particular (Azpitarte, 2011; Kuypers and Marx, 2019). Low-income households with little or no wealth are likely to suffer the greatest economic and social disadvantages as reflected inter alia in life satisfaction (Halbmeier and Grabka, 2019). They are also particularly vulnerable to individual economic shocks or aggregate-level ones such as the Great Recession from 2008 or the COVID-19 pandemic crisis.

Why do many low-income households have so little wealth? The life cycle hypothesis dominates economic theories and analyses of household saving and wealth accumulation but Sherraden (2005) concludes that it fails to explain patterns of asset accumulation in low-income households. For some, low-income is sustained over a long period (rather than only at very specific points in the life cycle) leaving very little scope for saving and building up wealth, and for others, periods of relative prosperity do not suffice to allow sufficient savings. This is the case both for the accumulation of financial assets and for acquiring property. House purchase is often only possible where a substantial deposit can be built up to allow a mortgage to be secured, and this is increasingly problematic going well beyond those on low-income as illustrated by the extent to which it has become a preoccupation of housing research and policy debate. Limited access to credit more generally, for a variety of reasons including discrimination and ‘redlining’, also constrains the scope for low-income households to invest in capital and generate returns, with financial exclusion now recognised as a key barrier to wealth accumulation for the poorest in society. These processes are dynamic and cumulative, with lack of assets making it more difficult for people to plan ahead and make consumption and savings decisions with a longer time-horizon. Comparative studies of wealth inequality struggle to explain observed differences across countries, but point to the nature of the housing market and extent of home ownership as well as welfare state institutions as relevant factors – with, for example, more robust income protection over the life cycle seen as reducing the need for households to save and acquire assets to smooth consumption.

The role of intergenerational transfers in wealth accumulation and the generation of wealth inequality across the entire distribution has been a long-standing topic of research interest and the subject of a number of recent informative national studies (see for example, Crawford and Hood, 2016; Nekoei and Seim, 2019; Boserup et al., 2016), although comparative analysis has been much rarer (Bönke et al., 2017; Nolan et al., 2020, 2021; Palomino et al., 2021). It is clear that these transfers are a powerful mechanism by which the wealthy are able to pass on their advantaged economic status to their offspring, though the scale and nature of the effect on overall wealth inequality remains hotly contested. Very little attention has been paid to the impact of intergenerational transfers on the limited wealth held by low-income households, and in particular on the likelihood that they have no wealth at all. This has been treated to a limited extent in some national studies (for example Hills et al., 2013; Wolff, 2017) but not been investigated in any depth in a comparative framework.

Theories of wealth transmission going back to the seminal works by Becker and Tomes in the 1970s and 1980s highlight the desire to pass on parental socio-economic status while retaining sufficient wealth for precautionary purposes, and more recently the balance between altruistic and strategic behaviours of both parents and their offspring. Apart from the crucial factor of whether parents of those in low-income households have wealth to pass on in the first place, disentangling the role of the intergenerational wealth transfers received from other factors in the accumulation of wealth is highly complex. Much depends on the extent to which wealth transfers are consumed or saved by recipients, and the returns generated on the amounts saved – which may both vary depending inter alia on the income of the recipients at the time of receipt and their prospective income from that point onwards. Low-income households may be more likely to consume and may also be able to generate much lower returns on amounts saved than better-off recipients who have better information, networks and investment opportunities, both limiting the impact of the transfer on their long-term wealth accumulation. Furthermore, receipt of wealth transfers will be associated with other background factors that serve to advantage recipient households versus others, such as parental education and social class. These will also contribute to an observed relationship with wealth outcomes, not all of which can be attributed to the impact of transfers per se. This makes the identification of the impact of wealth transfers in a truly causal sense extremely difficult, but the analysis of microdata from cross-sectional surveys that cover wealth, wealth transfer receipts and income can none the less be highly informative and suggestive.

Data and variables

We exploit the availability of microdata from surveys of wealth and related topics for large representative samples of households now available for a range of rich countries. The data on wealth and wealth transfers for France, Germany, Ireland, Italy and Spain are from the Household Finance and Consumption Survey (HFCS), for the United States from the Survey of Consumer Finances (SCF) and for Great Britain from the Wealth and Assets Survey (WAS). Full details on these surveys and the variables employed in our analysis derived from them are set out in the Supplementary Appendix, with only key points noted here.

We employ data from Wave 1 of the HFCS, the SCF for 2010 and Wave 3 of the WAS. The measure of net wealth covers real assets net of outstanding debt; the value of occupational pensions or entitlements to public pensions is not included. Information on transfers of wealth in the form of inheritances and gifts received by household members at any point is sought in the surveys; the precise way this is done and the measurement issues arising are discussed in the Supplementary Appendix, notably the range of challenges specific to the WAS that needed to be addressed.

Both wealth transfer receipts and wealth levels are at the household level. Nominal values for wealth transfers at the time of receipt are updated to 2010 values using the change in the consumer price index. Demographic characteristics refer to the Household Representative Person (HRP), measured as described in the Supplementary Appendix.

The income variable is total gross household income, rather than disposable income. This means that we are not able to distinguish those who would fall below conventional income poverty thresholds, so instead we focus on households in the bottom 20% of the gross (equivalised) income distribution as ‘low-income households’. Comparison with households in the corresponding part of the disposable income distribution shows a very high degree of overlap.

Wealth transfers and low-income

Wealth transfer receipt and income: A descriptive picture

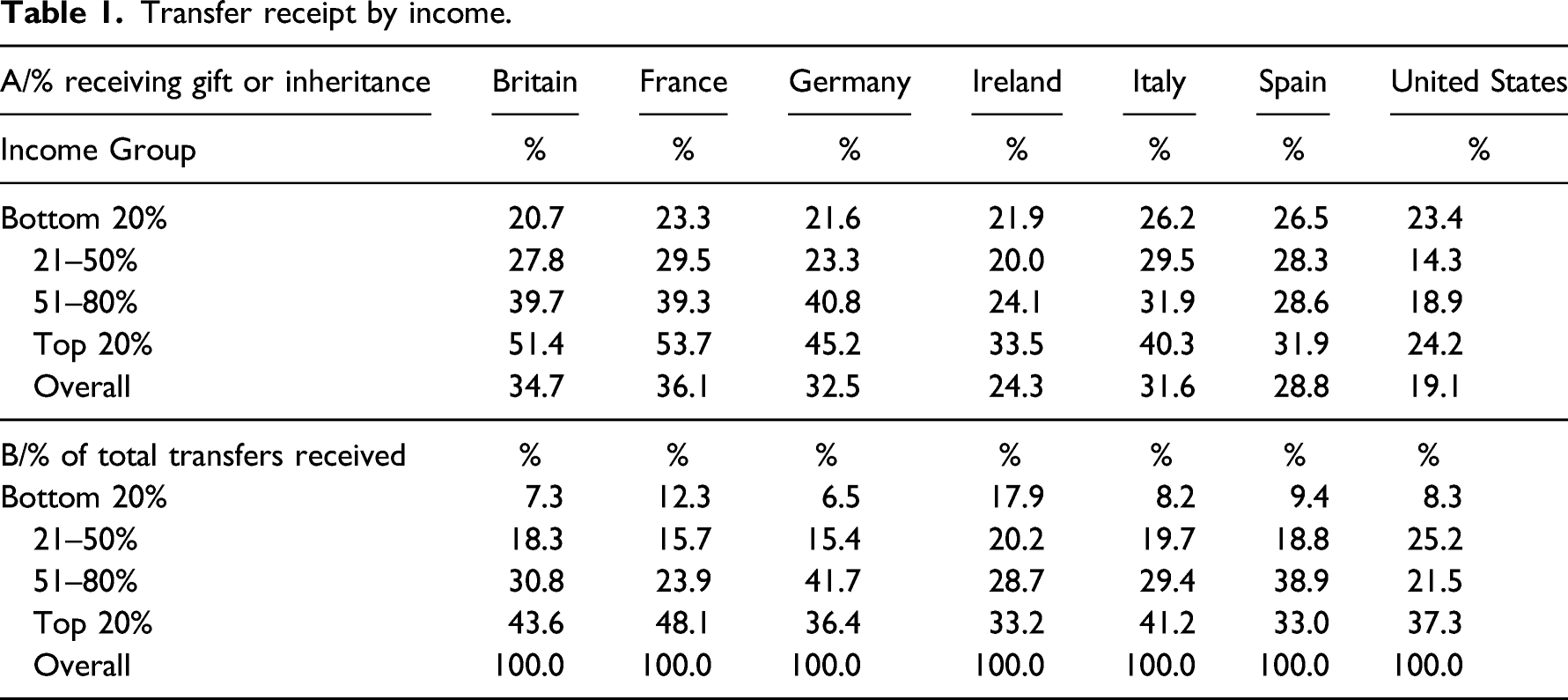

Transfer receipt by income.

The factors potentially underlying this variation across countries in the frequency of reported receipt of intergenerational transfers are many. These relate in the first instance to the ability of the household surveys to capture these transfers, and to do so in a consistent fashion across countries. There are differences across the surveys in how transfers are measured although those between the HFCS and SCF are considerably more modest than those between them and the WAS (as detailed in the Supplementary Appendix). There may also be some variation both across and within countries in how respondents interpret the questions – for example what represents a ‘substantial/large’ gift – and in recall reliability for questions involving long-term retrospection. The extent to which the surveys capture the top of the distribution will also vary, reflecting differences in design and implementation. Turning to factors that would be expected to lead to different patterns of intergenerational wealth transfer, these include most obviously differences in demographic structures, including in the age profile of the population, family size and how that has evolved over time and household structures. Differences in the composition and nature of wealth and in its distribution are likely to be central influences on transfer patterns: the importance of housing versus financial assets may be particularly salient as transfer behaviour may vary between types of wealth (so the point made by Dewilde and Flynn, 2021, in this issue, that particular attention should be paid to housing in studying wealth across countries is of particular relevance here). Finally, differences across countries in relevant institutional settings, notably with respect to taxes, pensions and the funding of long-term care, may be expected to affect transfer behaviour. Tracing these effects is highly challenging, but a comprehensive description of relevant differences across countries would represent an important first step (for example, Nolan et al. (2020) includes an in-depth discussion of how wealth and wealth transfer taxes vary across these countries and over time.)

Returning to the survey findings, households in the bottom 20% are generally less likely to have received an intergenerational wealth transfer than those in the top 20% or the rest of the top half. However, there is only a modest difference in the likelihood of receipt between the bottom 20% and the rest of the bottom half of the income distribution. The United States is an outlier, with households in the bottom quintile actually more likely than others in the bottom half or much of the top half to have received an intergenerational wealth transfer. The average amounts received by recipients in the bottom income quintile are also relatively low. As a consequence, as Table 1 also shows, households in the bottom 20% of the income distribution most often received only about 7–9% of the total amount reported as being transferred via inheritances or gifts, though Ireland is an outlier at 18%.

The likelihood of having received an inheritance or gift will be strongly related to where individuals are in their life cycle, so the proportion reporting transfer receipt is a good deal higher where the reference person is aged 55 and over compared to younger ages. Comparing within most age groups, those in the bottom 20% are generally a good deal less likely to have received a transfer, and received relatively more modest amounts, than those on higher-incomes (Supplementary Appendix Tables 2 and 3).

Modelling transfers receipt and income

We now probe the relationship between low-income and intergenerational wealth transfers by regression analysis. Our focus here is on how transfers vary along income levels at different ages, controlling for potential confounding factors such as household size, gender and level of education of the household head. The specification of an appropriate regression equation is, however, complicated by the nature of transfers: they are non-negative, often zero and very much skewed to the left when positive. Whereas some studies (for example, Crawford and Hood, 2016) have estimated separate models for the probability of receiving any transfer and for the amounts received among recipients only (with log-linear equations), we adopt a more parsimonious GLM approach with a link function suited to the nature of data on transfers – the Poisson link. Accordingly, the expected transfer received by a household with equivalised total income

To allow for the estimation of a flexible relationship between transfers, income and age, we express

The model parameters are estimated by pseudo maximum likelihood with heteroskedastic consistent standard error estimates. Then, as shown by Santos Silva and Tenreyro (2006), consistent estimation of the parameters of equation (1) does not actually require transfers to follow a Poisson distribution. What is relevant is only the specification of the – effectively log-linear – relationship between covariates and the conditional expectation of transfers as expressed in equation (1). The Poisson GLM regression specification de facto only imposes mild (and fairly standard) assumptions and is well suited to the nature of our data on transfers.

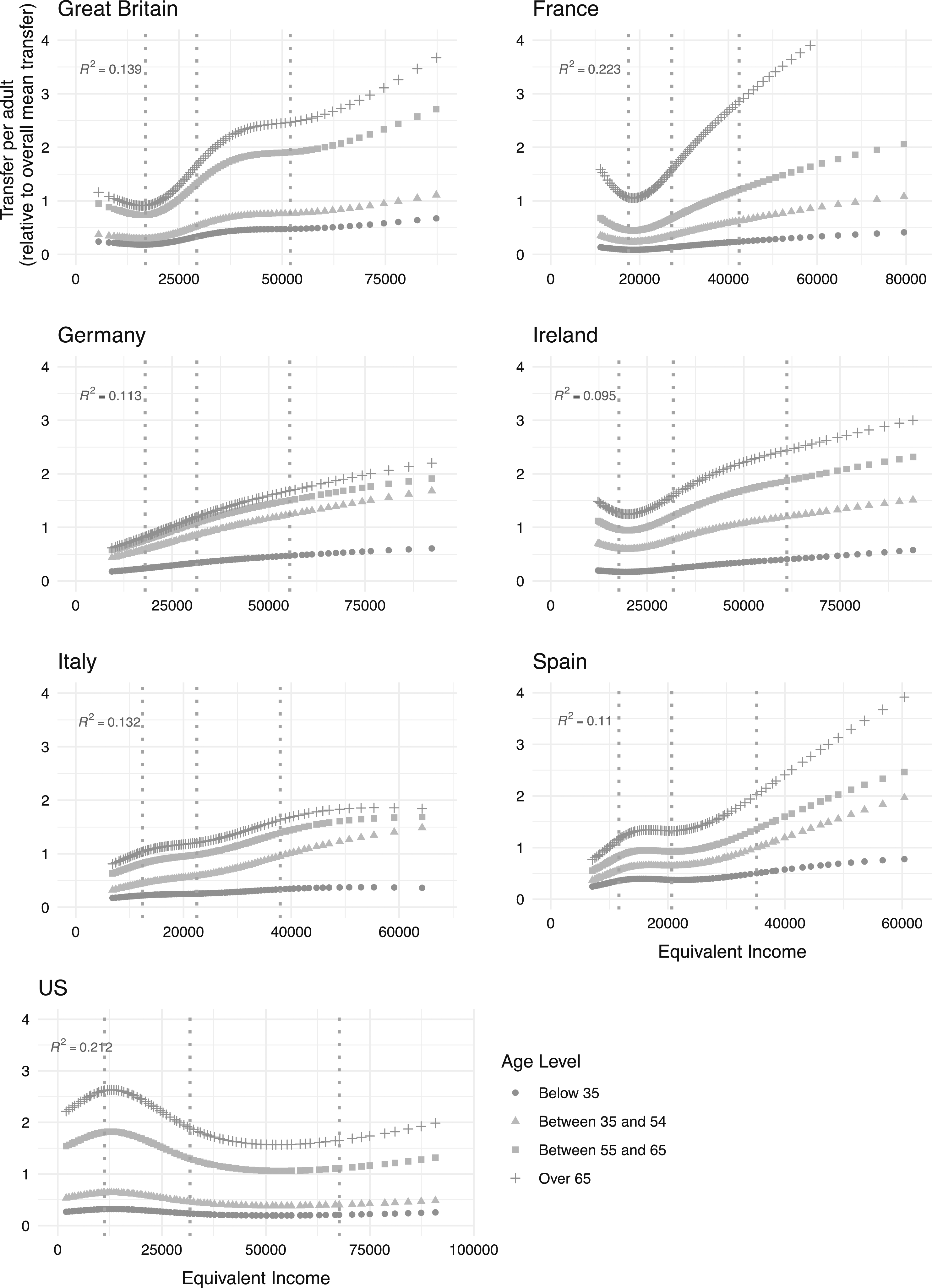

Figure 1 shows the expected transfers received at different levels of income for four different age levels for each of the seven countries, with the three dotted vertical lines marking the 20th, 50th and 80th percentiles of the equivalent income distribution. The general shape across the income distribution presents some common features across most of the countries. As expected, the amount of intergenerational transfer received is clearly related to income, even controlling for various socio-economic variables. We see that even at older ages the expected level of intergenerational transfers is low across the first tranche of the income distribution in all countries. In Great Britain, France, Germany and Ireland, the association of transfers with income is flat (or even slightly negative) below the 20th percentile; it then ‘takes off’, having the highest slope in the broad middle part of the distribution, and flattening at very high incomes. In Italy, the relation is almost linear across the entire distribution, although flattening at the top for the older age groups. Spain and the United States display a flatter slope around the middle of the distribution and a stronger association with income at the tails. Poisson regression prediction of expected wealth transfer receipt per adult by income and age group, per country (predictions averaged over household demographic characteristics at the reported age and income levels).

The level of predicted transfers is larger for older age groups across the income distribution. The inflexion point in income terms is similar across the three older age categories, but the slope with income tends to be rather flat for the youngest households in all countries. As one might expect, the predicted value of transfers for households under 35 appears to be weakly correlated with income in all countries. In the United States and Great Britain, a weak relationship between transfers and income is also observed for the 35–54 age group, while in France we see a distinctly greater income-transfer slope for the over 65s than for other age groups. Overall, though, households currently on low income have for the most part been seriously disadvantaged in terms of intergenerational transfer receipt compared with those higher up the distribution – and not just those towards the top.

Intergenerational transfers, low-income and wealth

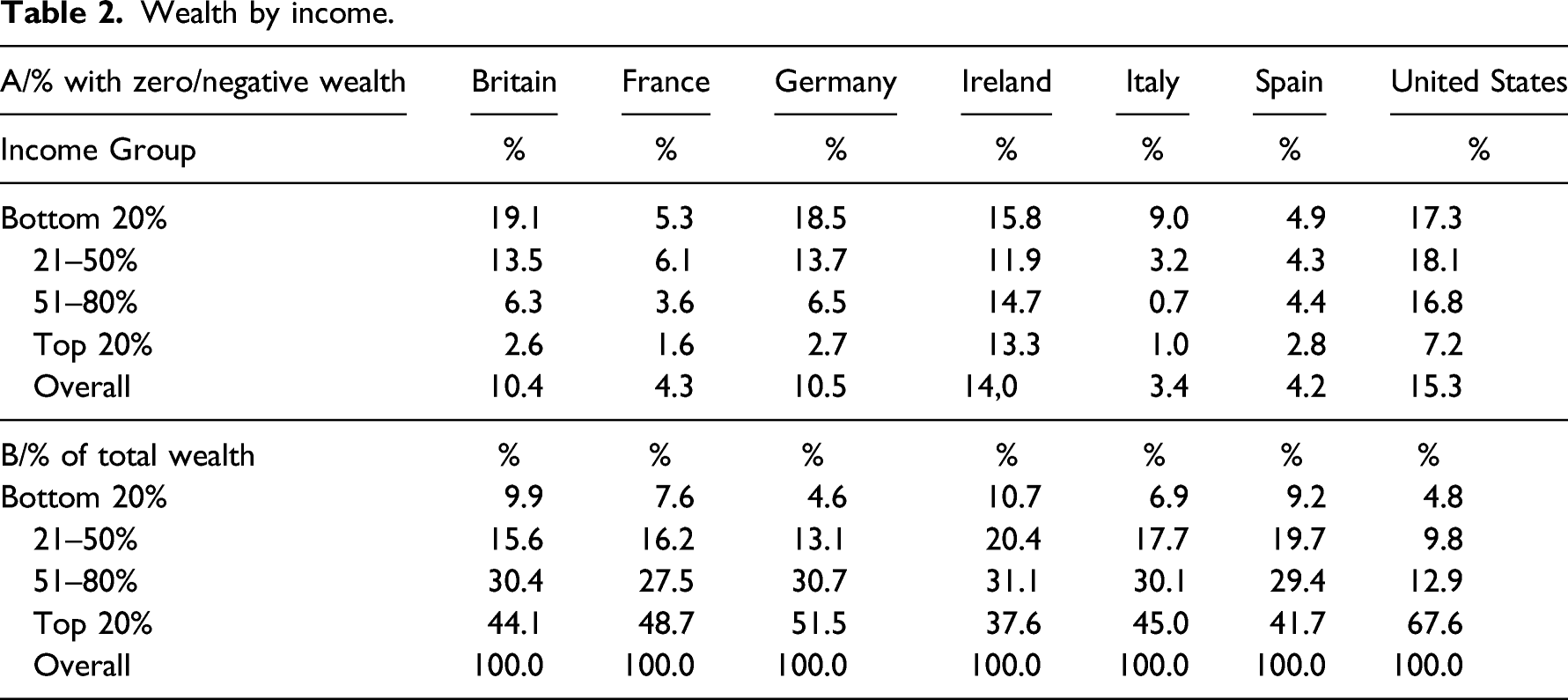

Wealth by income.

If one distinguishes age groups, older households have a lower proportion of zero-wealth holders, but low-income households are particularly likely to have no wealth, and have low mean and median wealth levels on average, within each age range. Housing comprises a particularly high share of total wealth for those in the bottom income quintile, with other assets (including financial) less important there than higher up the distribution.

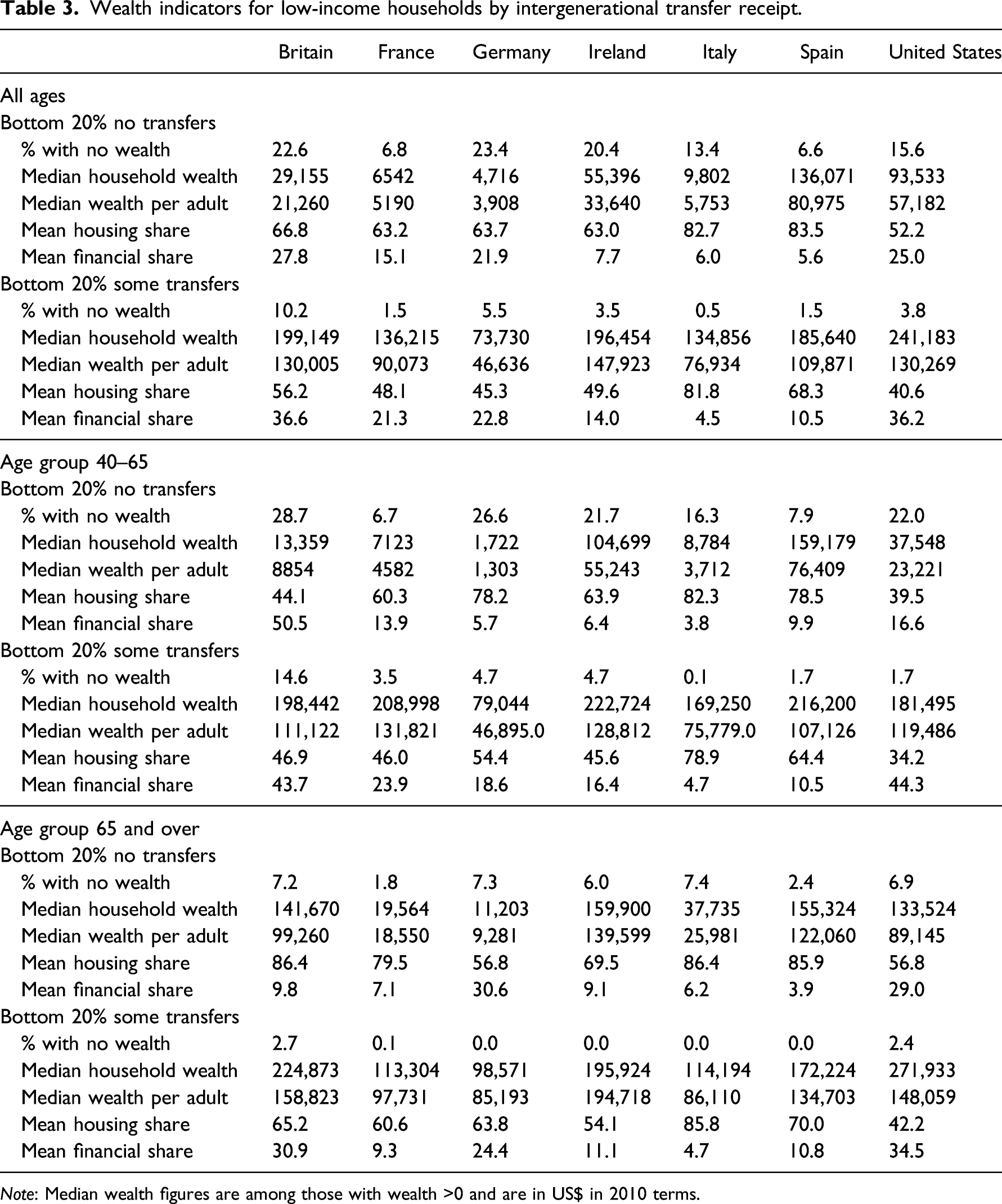

Wealth indicators for low-income households by intergenerational transfer receipt.

Note: Median wealth figures are among those with wealth >0 and are in US$ in 2010 terms.

Table 3 also reveals an association between having received intergenerational transfers and wealth composition. Among low-income households, transfer recipients have more liquid assets in their portfolio, with a much lower share of housing wealth in all countries and in most age groups, while their share of financial wealth is greater. This is significant in light of the importance of liquid assets in buffering short-term income shocks or meeting unexpected expenses (especially when access to credit is restricted) as noted in the introduction.

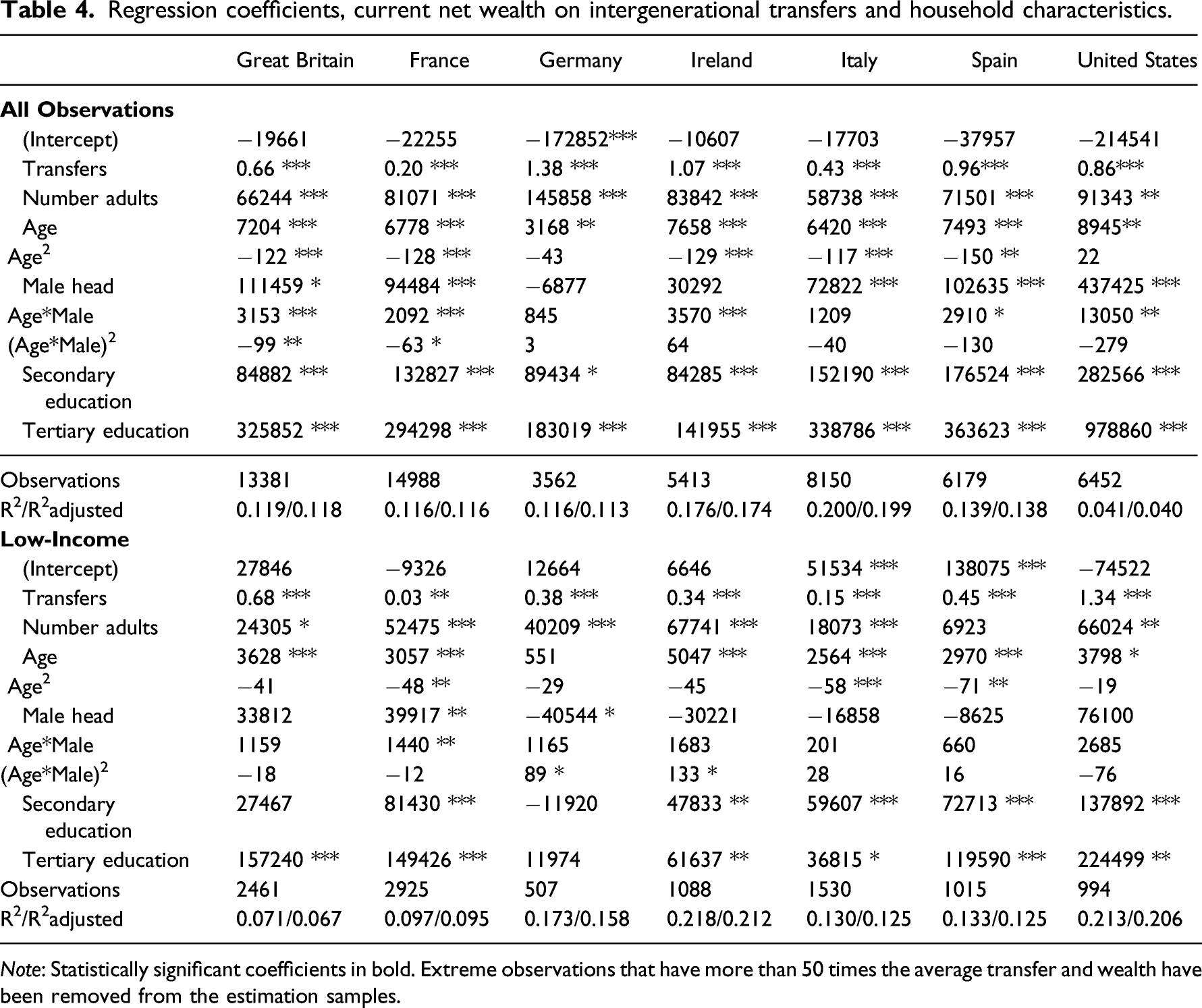

To investigate these relationships formally, we regress (using OLS) the net wealth levels of households on the amount (per adult) they received in intergenerational transfers, controlling for the number of adults in the household, the interaction between age and gender of the household head (raised to their quadratic power) and her/his education level (based on three dummies), that is

Regression coefficients, current net wealth on intergenerational transfers and household characteristics.

Note: Statistically significant coefficients in bold. Extreme observations that have more than 50 times the average transfer and wealth have been removed from the estimation samples.

Restricting analysis to low-income households only, we see from the lower half of Table 4 that the intergenerational transfers coefficient

The variation across countries in the size of the key ‘transfer’ coefficient for the entire sample and the low-income group, and in the gaps between them, clearly merits in-depth investigation. There is no obvious pattern relating to, for example, levels of wealth inequality in the country or broader welfare regime type. It is worth noting however that differences across countries in structures and levels of taxation of wealth transfers, often thought to influence inheritance and gift behaviour of the better-off and wealthy, are unlikely to play much of a role for low-income recipients as the transfer amounts involved would in most cases fall outside the scope of what is actually liable to tax. It is also worth reiterating that transfer receipt will often be associated with other background factors advantaging recipient households versus others, which also contribute to the observed bivariate relationship with wealth outcomes and how it varies across countries. Seeking to explain such variation across countries is extremely challenging – as reflected in how difficult it has been to convincingly explain why wealth inequality itself differs so much across countries – and is beyond the scope of this article. Our primary contribution is to establish that intergenerational transfers appear to play a significant role across all the countries studied in underpinning wealth outcomes for low-income versus other households.

Supporting wealth accumulation for low-income households

We have seen that low-income households are disadvantaged in terms of intergenerational wealth transfers, and that this has major implications for their total wealth holding and the likelihood of having no wealth in particular. Wealth is an important dimension of household and individual prosperity as it influences consumption possibility in the present and the future, affects choices about education and entrepreneurial activity, and acts as a fundamental buffer against material hardship and vulnerability (as brought out in Rodems and Pfeffer, 2021, in this issue). In keeping with the Sen (1999) ethic of ‘substantial freedom’, some level of resources could be also seen as one of the powerful enablers of freedoms we have reason to value. One policy response currently receiving renewed attention is a state-funded direct wealth ‘endowment’ to individuals, on a universal or means-tested basis, to support accumulation of some baseline level wealth. Atkinson (2015), for example, proposes a universal inheritance payable on reaching adulthood, an idea with a long historical pedigree, echoed recently in the United Kingdom by the Resolution Foundation and in Italy by the Forum on Inequality and Diversity. Milanovic (2019) also sees universal capital transfers as key to ‘deconcentrating capital ownership’, while Piketty (2019) proposes a very substantial capital endowment of approximately 60% of average adult wealth (about €120,000 in France) at the age of 25 years. 2

The case for a universal endowment that is received in early adulthood places particular emphasis on the importance of decisions made around that time and the long-term consequences these can have for income and for wealth accumulation over the life course. The substantial security that such an endowment would represent and the financial resources it would make available from such an age could have deep behavioural effects. These could potentially serve to increase human capital and the return to it and thus wealth accumulation over time, through a variety of channels. Enhanced security and availability of financial resources are likely to increase willingness to continue in or return to education. They might well also lead to a higher propensity to change jobs and move to where job opportunities are greater, as well as to take entrepreneurial risks. (It is worth noting that this case is not undermined by our finding that the slope of the wealth transfer–current income relationship is relatively flat at younger ages, resting as it does on the potential long-term effects of an early wealth endowment on the wealth deficits of low-income households over the life course.)

Despite the growing interest, little empirical research has been done to understand how the wealth distribution might be affected by such a wealth endowment. Feiveson and Sabelhaus (2018) is an important exception, looking at a static exercise distributing the total wealth value attributable to inheritances and gifts in the United States Survey of Consumer Finance as equal amounts across the population. They find that this could reduce the top 10% share of total wealth in the United States from 73 to 57% or even to 40%, depending on how wealth transfers are capitalised over time.

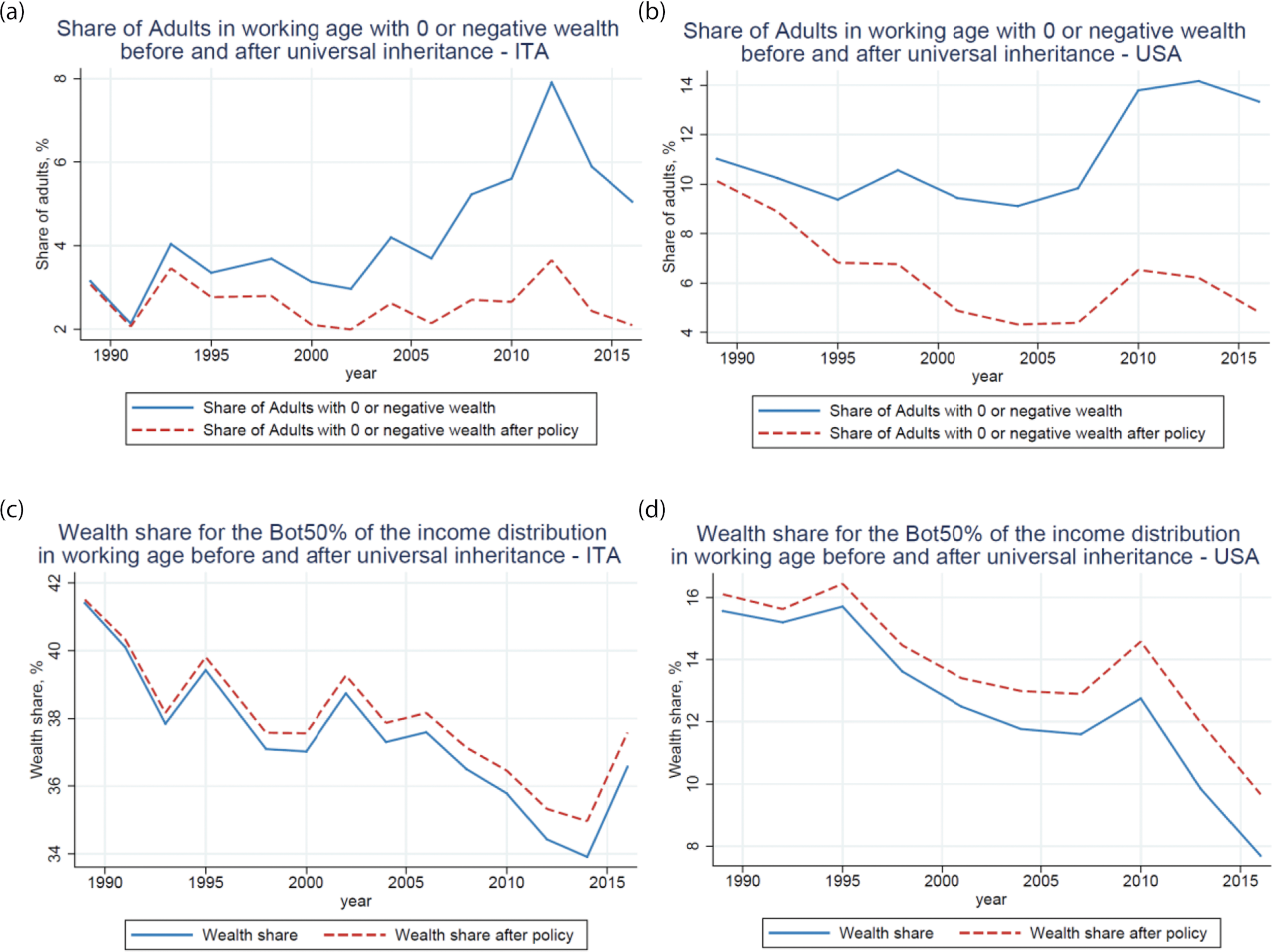

Here we investigate the potential impact of a universal inheritance for young adults with a particular focus on the implications for the wealth of lower-income households as well as overall wealth inequality. We use just Italy and the United States as case studies, because the Survey of Household Income and Wealth for Italy and the Survey of Consumer Finance for the United States provide cross-sectional wealth data over a much longer period than is available for the other countries included up to now. These surveys allow us to take 1989 as base and simulate the static, mechanical effect from one year to the next of a universal inheritance implemented whereby everyone reaching 20 years old received 10% of national net personal wealth per adult in the year in question. 3 Whereas in the rest of the article we took the household as the unit of analysis, in this simulation we counted people, ranked by wealth per capita, to capture the impact of the individual endowment at that level (initial individual wealth before receipt of the endowment has to be derived as an equal split of household wealth among its adult members since the underlying surveys only measure wealth at that level).

The endowment is added each year to the individual wealth stock of those who reach 20 then, and assumed to simply hold its value from that point onwards rather than be partially consumed or invested to generate a greater return. By 2016, all adults between 20 and 47 would have received it, and under these simplifying assumptions the individual net wealth of each recipient would be increased by roughly €9000 in Italy and $27,000 in the United States in 2016 (in 1989 the figures are roughly €2500 in Italy and $13,000 in the United States). To put these numbers into perspective, the endowment would be equivalent to 50 and 80% of the respective country 2016 median disposable income according to OECD statistics. Seen through the lens of individual net wealth distribution among adults (observed using the survey data), the transfer would be enough to put recipients just above the 20th percentile in Italy and the 40th percentile in the United States. The monetary transfer would affect roughly four million young adults in the United States and six hundred thousand individuals in Italy every year and costs about €5 billion in Italy and $90 billion in the United States each year (equivalent to approximately 3 and 8% of the total annual inheritance flow estimated in each country) (Acciari and Morelli, 2020; Alvaredo et al., 2017).

Focusing first on working-age adults, Figure 2 shows that the mechanical effect of this ‘inheritance for all’ policy beginning in 1989 would be to sharply reduce the share with zero or negative net wealth by 2016, from 5 to 2% in Italy and from 13 to 4% in the United States. Most of these dynamics, especially in the United States, are driven by the share of working-age adults with negative wealth, consistent with the high share of student debt there. Working-age adults in the bottom half of the income distribution increase their share, with only the top 10% seeing a decline. Impact of universal inheritance scheme (beginning in 1989): Italy versus the United States.

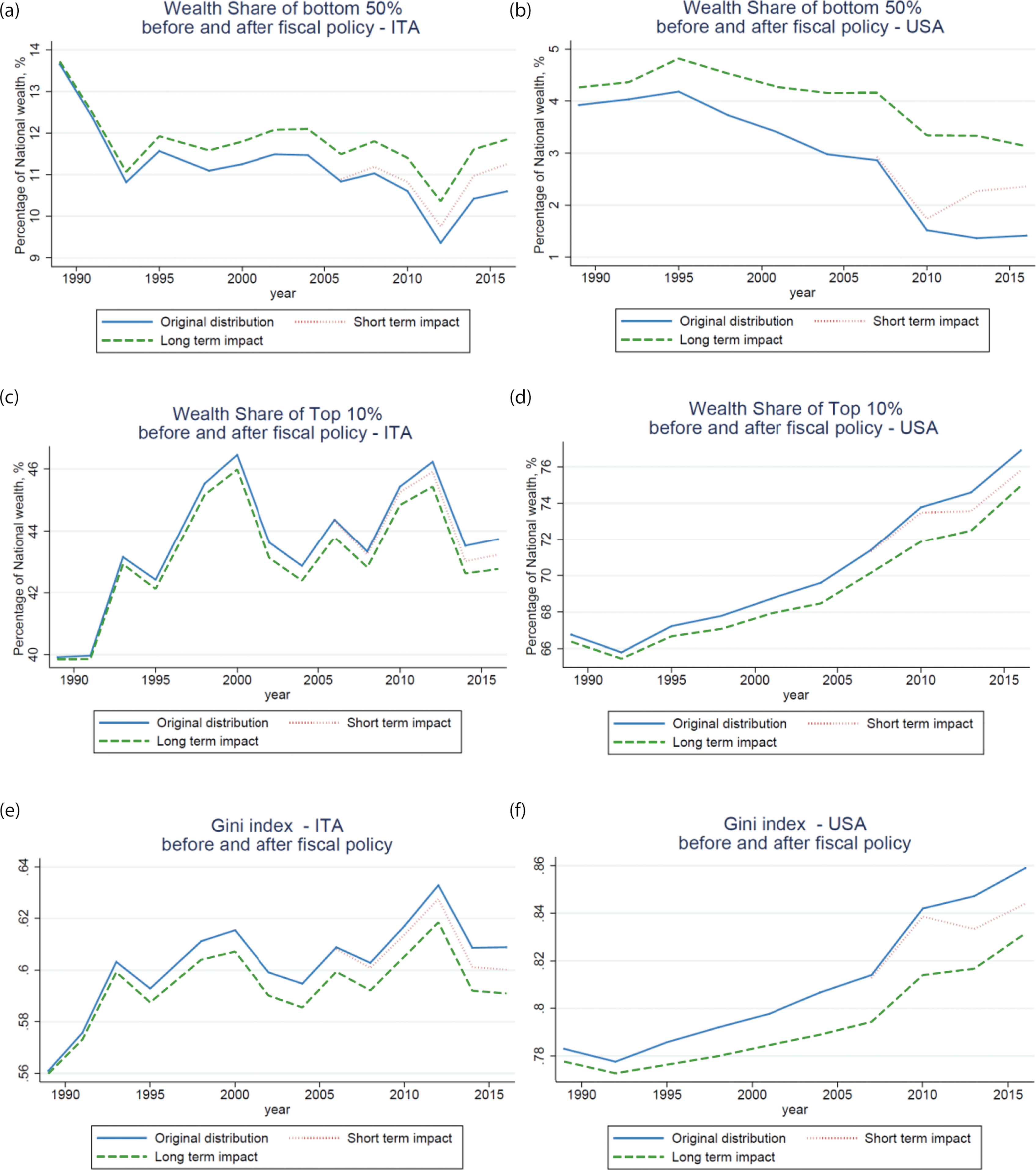

Looking at all adults in Figure 3, the top panels show that the share of the bottom 50% of adults ranked by household wealth per capita again increases, by about 1 percentage point in Italy and 1.5 percentage points in the United States. The middle panels illustrate the corresponding declines in the share of the top 10%. The bottom panels show that the Gini summary inequality measure for net wealth per adult (including negative and zero values) is reduced by almost two Gini points. These impacts all cumulate from 1989, so it is also interesting to look at a much shorter time-scale, if the scheme had been introduced in 2006. We see in each panel that by 2016 there would already have been a substantial impact, so the objection that the effects take much too long to come through to be politically feasible loses force. Impact of universal inheritance scheme on wealth inequality in Italy and the United States: long-term effect (beginning in 1989) vs short-term effect (beginning in 2006).

The results of this static simulation exercise provide some insight into the potential effect of a capital endowment policy despite clear limitations in the way it is framed. It does not allow for differential consumption of the universal endowment by wealth or income level, and also ignores the investment returns that could at least partially counteract such consumption effect. It also does not attempt to capture behavioural effects that could potentially serve to increase human capital and the return to it and thus wealth accumulation over time, via the channels already noted whereby enhanced security and resources increase willingness to invest in education, change jobs and take entrepreneurial risks. These can be expected to have considerable effects on ‘permanent income’ and the opportunity to accumulate wealth.

The exercise also excludes the funding side of the equation, whereby progressive taxes on lifetime wealth transfer receipts or a tax on wealth stocks could substantially increase the overall impact on wealth distribution. Atkinson (2015) for example proposed to radically transform the current United Kingdom estate tax into a progressive tax on total wealth transfers received by every individual over the course of a lifetime and above a specified minimum, a structure that is currently in place in some rich countries at present (such as Ireland) and actively debated in others, while Piketty’s universal transfer would be funded by a recurrent and steeply progressive personal wealth tax in combination with highly progressive income and inheritance taxes. Simulating the combined effect of wealth transfers on consumption and investment behaviour and such taxes would require a complete micro simulation model and would represent a very valuable extension of the analysis in this article.

Conclusion and implications

This article has presented a novel comparative investigation of the role that intergenerational wealth transfers – or their absence – play in the combination of low-income with low wealth facing many of the households conventionally measured as poor, using microdata from household wealth surveys for seven rich countries – Great Britain, France, Germany, Ireland, Italy, Spain and the United States. In doing so it seeks to bring together what have for the most part been parallel research literatures on the wealth deficits of low-income households and on the intergenerational transmission of wealth.

Households on low incomes in these cross-sectional surveys were found to be seriously disadvantaged on average in terms of intergenerational transfers received compared with those higher up the income distribution. We also presented suggestive evidence that this plays a significant mediating role in the link between low-income and low wealth. Receiving a large intergenerational wealth transfer is seen to break the connection between low-income and low wealth, allowing most of the (relatively few) low-income households who received them to escape the ‘double-poor’ (by both income and wealth) trap. Simulation of a widely advocated strategy to address the wealth deficits of lower-income households by a universal capital endowment on reaching adulthood, using Italy and the United States as case studies, suggested that this could lead to a marked decline in the proportion of adults with negative or no wealth and increasing the aggregate wealth share of those who currently have little or none.

This and alternative or complementary policy responses to the wealth deficit of low-income households merit further investigation and the most serious attention in a context where economic precarity and wealth inequality are giving rise to such concern. Future analytic exercises should also seek to incorporate behavioural responses of transfer recipients in terms of consumption and investment choices, as well as the funding side of the equation. In that context, the potential for funding such an endowment via taxation of flows of inheritances and gifts as well as wealth stocks, as advocated by, for example, Atkinson (2015) and Piketty (2019), should also have a central place. An important part of that research agenda will also be the further exploration of the factors that give rise to the wealth deficits faced by many low-income households, including intergenerational wealth transfers. The variation across countries in both wealth and wealth transfers as captured by surveys provides an important analytic resource; tracing the underlying structural factors at work while taking the complexities of accurate measurement into account is a central, seriously challenging, aspect of this research.

Supplemental Material

sj-pdf-1-esp-10.1177_09589287211040419 – Supplemental Material for Inheritance, gifts and the accumulation of wealth for low-income households

Supplemental Material, sj-pdf-1-esp-10.1177_09589287211040419 for Inheritance, gifts and the accumulation of wealth for low-income households by Salvatore Morelli, Brian Nolan, Juan C Palomino and Philippe Van Kerm in Journal of European Social Policy

Footnotes

Acknowledegments

The authors acknowledge the valuable research support by Demetrio Guzzardi and thank colleagues at INET Oxford, Arthur Kennickell and Marco Ranaldi (GC-CUNY), and two refeees for helpful comments and discussion.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Financial support from the Nuffield Foundation is gratefully acknowledged, the authors are responsible for the views expressed.

Notes

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.