Abstract

The literature indicates that most housing in the urban areas of many countries in the global South is in informal settlements, provided through informal mechanisms that are often not well understood. This paper contributes to understanding the forces influencing real estate markets in informal settlements, drawing on a case study of the under-researched Ayobo community in Lagos, Nigeria. The paper examines the roles played by government agencies and other market actors, including buyers, sellers, informants, financiers and witnesses, in relation to the operation and regulation of informal land markets. The analysis of the data, drawn from a survey and interviews, reveals a thriving property market, which is socially if not formally regulated. The paper concludes that this flourishing informal market needs strengthening to effectively meet the housing needs of urban residents.

I. Introduction

Informal settlements have often been described as settlements that evolve outside urban land development processes and procedures.(1) Their evolution has been attributed to failure of the public sector to provide conditions through which the poor can access shelter formally, as well as the inefficiency of local authorities in enforcing urban development regulations.(2) These settlements are often laid out haphazardly with little or no government provision for communal facilities or basic infrastructural services. Nevertheless, their contribution to urban housing provision, especially for the poor, is increasingly acknowledged. For example, Sheuya(3) notes that 70–95 percent of new housing built in developing countries in the last few decades has been in informal settlements. Banks et al.(4) explain that, although informal settlements may not be completely illegal, they often have porous legality. Over time, the informal settlement market has thrived, suggesting the existence of regulation of some sort, with actors being conversant with their roles and rights.

Informal settlements are said to result from activities of individuals, often without official permits.(5) Banks et al.,(6) however, assert that informality sometimes emerges in collusion with the government, the state, and business interests within the state, often functioning as primary actors in informal settlements. In this context, private individuals and corporate bodies complement the efforts of the government in providing basic services, especially in areas of waste management, water supply, and – as related to this study – housing, often for private gain. In this way, the government is able to reduce costs.

Banks et al. and Roy(7) note that although earlier discussions on informality emphasized the urban poor, middle- and high-income groups are in fact also often major actors. People may be pushed into informal settlements not only by poverty, but by insecurity for tenants. Arbitrary rent increases in formal settlements can force even the middle-income and the rich to seek shelter in informal settlements, sometimes as landowners.(8) Informal settlements also provide business opportunities, as investments in landed properties often appreciate in value over time. While the poor seek for survival in informal settings, the rich and the middle class may cash in on the opportunity for wealth accumulation. Roy(9) argued that informality is not synonymous with poverty, but is rather an expression of class power, and that the expansion of informal settlements is based not necessarily on the cost of land as much as the ease of access. Roy(10) also suggested that affordability in informal settlements accrues from the absence of planning and regulation in those areas, which eliminates often long, bureaucratic and cumbersome procedures.(11)

In this study, an informal settlement is defined as a settlement that develops outside the government-regulated processes and procedures for urban land development. Informal settlements can develop within urban areas or at the urban periphery, often in areas not yet planned for by the government, including forested areas or peri-urban agricultural land.(12) These are different from squatter settlements, which are often on illegally occupied land. This study has mainly focused on the peripheral land around urban areas.

Many studies have examined various aspects of the workings of informal settlements in the global South. There is also copious literature on formal real estate markets worldwide. However, not much work exists on the mechanisms that drive the real estate market within informal settlements. Banks et al.(13) have highlighted the need to go beyond studying informal settlements through the lens of marginalization, and to consider the perspective of the various actors who operate within the informal market. This study does precisely that, examining the roles of the multiple actors involved in real estate transactions within one informal settlement in Lagos, Nigeria.

Lagos presents an interesting context for study as a fast-growing city with several large informal settlements. This paper investigates the real estate market here, primarily from the perspective of buyers. It draws on empirical data from owner-occupier residents in Ayobo, a large, rapidly consolidating informal settlement on the outskirts of Lagos. The paper also draws to a lesser extent on interviews with other actors.

Sections II and III of this paper present a review of relevant literature to identify and situate the paper within a wider context of previous studies. This is followed by a brief introduction to the area studied (Section IV); explanation of the methodological process adopted (Section V); and presentation and discussion of the outcomes of the investigation (Sections VI and VII), along with concluding remarks (Section VIII).

II. Informal Settlements as Part of the Global Real Estate Market

The formal real estate market has been unable to satisfy the housing needs of the growing urban population in much of the global South, much of which cannot afford what this formal market offers.(14) As a result, many urban residents opt for informal housing markets, identified by Landman and Napier(15) as a major entry point to the housing market for many households in the global South. Wekesa et al.(16) noted that 43 per cent of the population in low- and middle-income countries reside in informal settlements.

The real estate market, influenced by the behaviour of its agents,(17) is driven by myriad forces including sellers’ motivation, demographic variables, financial market constraints, policies, land supply, speculative bubbles and self-fulfilling beliefs.(18) It is often divided into the formal and informal real estate markets. The first is generally characterized by private competitive decisions and the dominance of price mechanisms and self-interest. Kihato(19) identified two challenges with this market in Africa: its slow response to forces of demand, and the inefficiencies of land administration and registration systems, including land and building regularization. In informal real estate markets, by contrast, transactions are assumed to be carried out with few or no judicial procedures or government sanctions, but rather are coordinated by social networks and hierarchies, and often typified by trust(20) and cooperative social relations.(21) Some scholars see the informal urban real estate market as distinct; others argue that it is merely a submarket of the urban real estate market. There is general agreement, however, that the informal real estate market has been successful in providing shelter in most countries.(22)

These informal settlements have their own social order,(23) characterized by relative stability and the respect that market participants have for informal property rights.(24) There are no formal rules. Social rules are generated and understood by the people involved, who know their rights and obligations. These often unwritten, orally communicated rules guiding informal real estate markets frequently emerge spontaneously, and are negotiated and enforced by varied groups often including the elites.(25) These rules are institutionalized in various ways. Thus, informal settlements may be highly regulated, even if not by the state. Roy(26) and Schindler(27) note that informality has more to do with deregulation than a lack of regulation. This has generated the unique management system and initiative often observed in these settlements.(28)

Two submarkets exist within the informal real estate market. The land submarket, involving transactions and transfers between land buyers and sellers, is socially accepted as legitimate, though not recognized as legal by the government.(29) The development submarket(30) involves the building or sale of structures on acquired land.

Transactions in informal settlements involve such individuals as small-scale entrepreneurs, local brokers, contractors, sometimes court clerks, and other local officials.(31) There has however been little empirical study on the roles of these actors.

III. Real Estate Market in Informal Settlements in Nigeria

As in most of the global South, the formal real estate market in Nigeria has failed to satisfy housing demand over the years. In fact, Sangodeyi(32) predicted a demand gap of 44 million homes by 2020. Consequently, a large part of the population, estimated at 70–80 per cent by Olajide(33) and Singhry and Umar,(34) resides in informal settlements. In Lagos, this includes two-thirds of the population.(35) Lagos has a multiplicity of land tenure and management systems.(36) Under the publicly managed tenure system, the government allocates land and possibly houses, and occupants have statutory rights of occupancy. Under private or customarily managed tenure, land belongs to communities of common ancestry (lineages and extended families), and occupants have customary rights of occupancy and use of such land.

In the urban fringes of Lagos, Ogbu and Iruobe(37) identify three categories of land. The first is in areas yet to be officially pronounced as belonging to the government, where communities continue to enjoy control. When the government acquires such areas, communities are either compensated or allowed to regularize their titles. The second category is in areas where part of the land is given to communities, during government acquisition. Communities may sell such land without government consent. The last category, the focus of this study, consists of agricultural land in adjoining rural areas, where communities have customary rights.

Ownership of such peripheral land in Nigeria, by constitution, lies with the federal government. However, de facto titles are often given by community heads, tribal leaders and other such ownership entities. Landholding farmers in urban peripheral areas in most African countries are said to sell their land out of the fear that the government may take it for urban expansion, with delayed and non-commensurate compensation, if any.(38) According to some scholars,(39) vacant land is often leased from families who claim to have these land rights. Those who acquire the land often build using locally available materials, relying on unlicensed (and hence more affordable) designers and artisans for construction. Owners of property on peripheral land seldom have access to mortgages or other subsidized finance, and often build without official authorization. Settlers first occupy the land and then begin the struggle for official recognition by the government. Basic services and infrastructure are not initially available, and although taxes may be evaded at first, they are paid on application for regularization of land and buildings by relevant government agencies.

The recognition in Nigeria of the customary land delivery system by parties involved in transactions provides sufficient tenure security for properties in these areas. Although not legalized, these transactions are often tolerated by the government and accepted by the communities. These informal settlements still have their drawbacks, however. Aluko, Olaleye and Amidu(40) observe that the cost of land in informal settlements in Lagos is actually higher than that in formal settlements. Ogbu and Iruobe(41) also argue that these land transactions are fraught with problems of fraud, mostly associated with omo-onile, the descendants of landowners. (State housing delivery in Lagos is also said to be pervaded by favouritism, discrimination and pervasive corruption.) To encourage persons in informal settlements in Lagos State to document their landed property, the state government introduced the Electronic Document Management System in 2015 to speed up the process. Residents still complain of the high transaction costs, however.

IV. The Study Area

Ayobo (Map 1), a major and representative informal settlement, is located on the outskirts of Lagos State in the Alimosho Local Government Area (LGA). Established in 1991, Alimosho LGA is one of the fastest growing in Lagos. Its population in 2006, estimated at 1.3 million, grew to 1.8 million by 2016, a population growth rate of 3.25 per cent per year.(42) Ayobo, one of 11 wards in the Alimosho LGA, housed approx. 70,000 persons as of 2006. The other wards in the LGA (Abule Egba, Pleasure, Egbeda, Ipaja North, Ipaja South, Ikotun, Shasha, Idimu, Egbe and Igando) also initially developed as informal settlements, but have been regularized over the years, with basic infrastructural services provided by the government. Property owners in those areas are also required to register their properties.

Lagos, including Ayobo

Ayobo, however, is a developing informal settlement, still without a government presence, and so presents a suitable site for this study. Ayobo is characterized by good terrain and availability of vacant/undeveloped plots, making it an attractive housing destination for poor households and, increasingly in recent times, for middle-income households in land-strapped Lagos. Previously used for agriculture by the original Awori landowning families, the conversion to residential plots has been attributed to a decline of farming activities in the area and the demand for residential land arising from the overwhelming urbanization in Lagos State. Many young people who would previously have engaged in farming have moved to more central areas, where paid employment is available. Infrastructural provision is largely absent in Ayobo, and the roads and stormwater drains constructed by residents are in a state of disrepair. The area has few recreational spaces.

Many of the inhabitants are either civil servants who work in government establishments in Ikeja, 17 kilometres from Ayobo; or artisans or businesspeople who have established businesses within or close to Ayobo. Residents commute in poorly maintained commercial vehicles, including tricycles and bicycles. Ayobo residents are 62.6 per cent renters, 29.7 per cent owner-occupiers, and 7.7 per cent with other tenure status, including freeholding. This study focuses on just the owner-occupiers.

V. Research Methods

This paper details the role of market actors in the informal settlements, drawing on data from a larger study investigating the housing tenure status of residents in Ayobo, as well as housing quality, housing aspirations of residents, waste disposal methods and housing procurement methods. The study also collected information on the responsibilities of persons involved in the property acquisition transactions, the material most relevant for the present paper. Data for this larger study were obtained from both primary and secondary sources. Secondary sources included a review of relevant scholarly papers and government documents. The primary data, both qualitative and quantitative, were gathered from the residents of Ayobo as well as selected government officials and Community Development Association leaders.

Quantitative data were sourced through a survey of residents represented by randomly selected household heads. Based on an earlier survey of Ayobo(43) and an OpenMapTiles image,(44) the number of residential buildings was computed as 2,395, and the number of households as 11,138. The formula adopted by a researcher earlier(45) was used to calculate the sample size with a confidence interval of 97 per cent. This gave 1,011 households as the minimum sample size. However, 1,200 copies of the questionnaire were distributed to allow for non-response.

Every eighth house was sampled on identified streets, and either one or two household heads were chosen as informants, depending on whether one or more households inhabited the building. Of the 1,200 copies of the questionnaire administered, 1,151 were retrieved. Information for this paper, with its focus on real estate transactions, was restricted to the 306 respondents (30 per cent) who indicated they were owner-occupiers. The quantitative data were analysed using version 17 of the Statistical Package for Social Studies (SPSS). Further analysis involved cross-tabulations to specifically segregate data on the socioeconomic characteristics of owner-occupiers in the study area.

In addition to these quantitative survey data, interviews were conducted with eight selected government officials (at both the state and LGA levels), 17 Community Development Association (CDA) leaders and eight other residents, making 25 residents in all. The CDA leaders were all property owners residing in the settlement. One was a land surveyor involved in the subdivision of the plots and was paid in kind with plots that he then put on sale. Two of the CDA leaders were from landowning families, who also built houses in the settlement. They often served as an interface between buyers and the landowning families, providing information on available plots, as well as selling land. One was also a lawyer, involved in preparing sale agreements in the settlement. The other CDA members interviewed were all buyers. Of the other eight residents interviewed, one had bought multiple plots in the area and was involved in resale. Information on other actors, such as financiers, was obtained from the buyers. Themes emerging from the interviews were identified through content analysis.

VI. Results

This section first presents the types of properties traded, and then discusses the roles of informants, sellers, buyers and financiers.

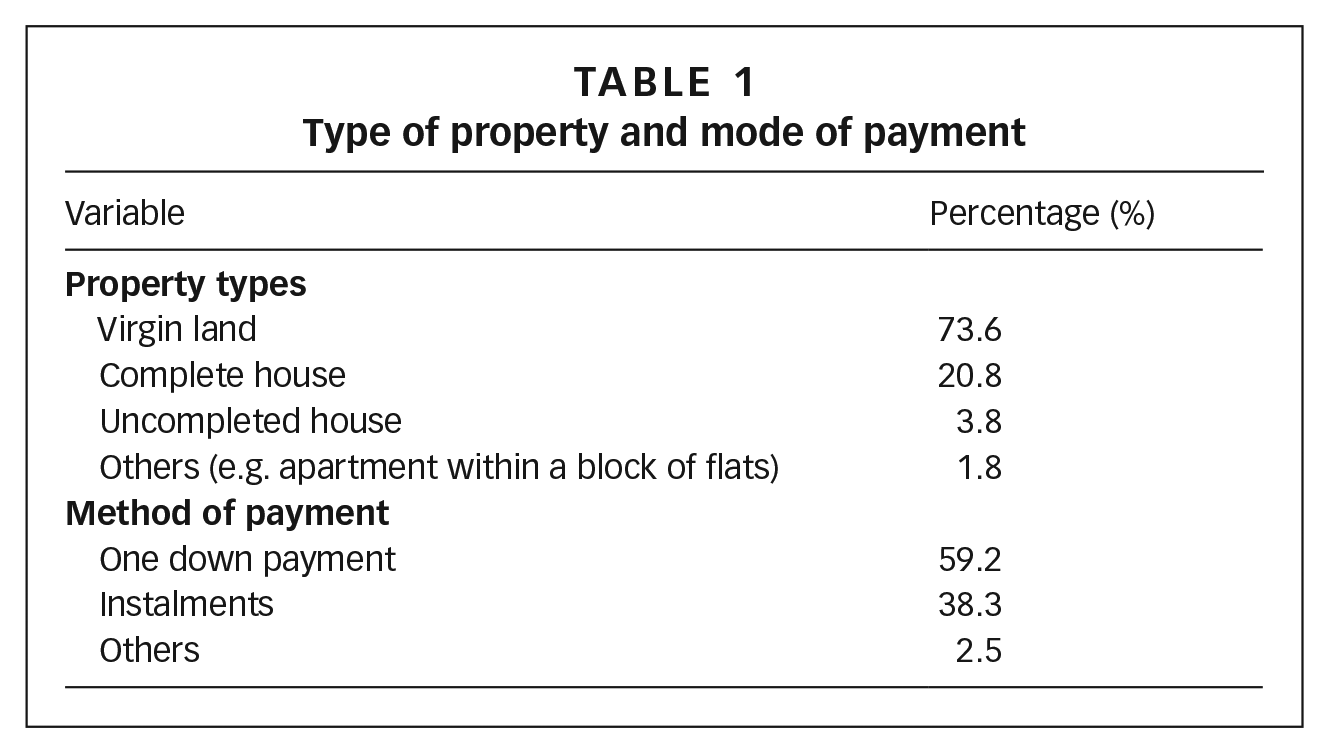

As indicated in Table 1, land is the most traded form of property. This is because of its low initial price compared to that of completed buildings. In addition, the purchase of land gives buyers the opportunity to build the types of houses they desire. Houses with land are also traded. Some respondents purchased uncompleted buildings; others bought an apartment within a block of flats. Over half (59.2 per cent) of the respondents had made one down payment for their property (Table 1). Almost three-quarters of these respondents made such payments from personal savings, as discussed later in this section, indicating that homeownership had been highly prioritized in spite of other needs. Some of the buyers noted that they had to prioritize homeownership because of the arbitrary rent increases they had experienced in the past as tenants. In addition, many respondents considered homeownership an investment with several benefits.

Type of property and mode of payment

Buyers in the settlement did not just buy property for personal use. For some it was a business investment on the part of developers, who built houses for sale, deciding what to build in line with market survey findings. Developments may or may not be backed by the services of other professionals like architects and planners.

Interviews indicated that property transactions in the study area took varying formats, not always proceeding in a linear manner. The description of the process is somewhat streamlined for the purpose of this paper. For a transaction to take place there must be a buyer and a seller, who are usually not aware of each other’s intentions. Information about their requirements is shared with others who assist in scouting for opportunities, transmitting information between the parties and facilitating their meeting. Buyers rely on information from friends and family or they go through agents. Land is often purchased from landholding families or from individuals who had earlier purchased land from these families.

Large parcels of undeveloped land are subdivided into uniform or near-uniform plots with conventional street grids, often without regard for zoning laws or service provision standards. According to the land surveyor who was interviewed, the main objective is to end up with as many plots as possible. Infrastructural development takes place when the settlement is established. Residents purchase basic services for themselves in accordance with their means, and businesspeople within or outside the settlement cash in on this opportunity by providing the requisite services like water, waste management and transportation.

When the buyer and seller meet, the site and/or building are inspected and negotiations take place. When agreement is reached, it is sealed with payment, and the sales agreement is signed in the presence of witnesses, often community leaders and persons known to the buyer. On purchase, buyers are issued letters of agreement or certificates of title. De facto titles issued by community heads, tribal leaders and other ownership entities are trusted by buyers, who are often advised to carry out their transactions with these leaders, rather than the land touts, who are more frequently associated with fraud. The duration of the process depends on the readiness and reasonableness of the parties. Land is then demarcated using bush poles (poles or length of wood gathered from the forest), trees, tyres or corner pieces (survey beacons), in the absence of cadastral surveys. Selling families often have a layout plan, indicating plots and access roads. Each buyer, however, is expected to carry out the survey for the particular plot purchased.

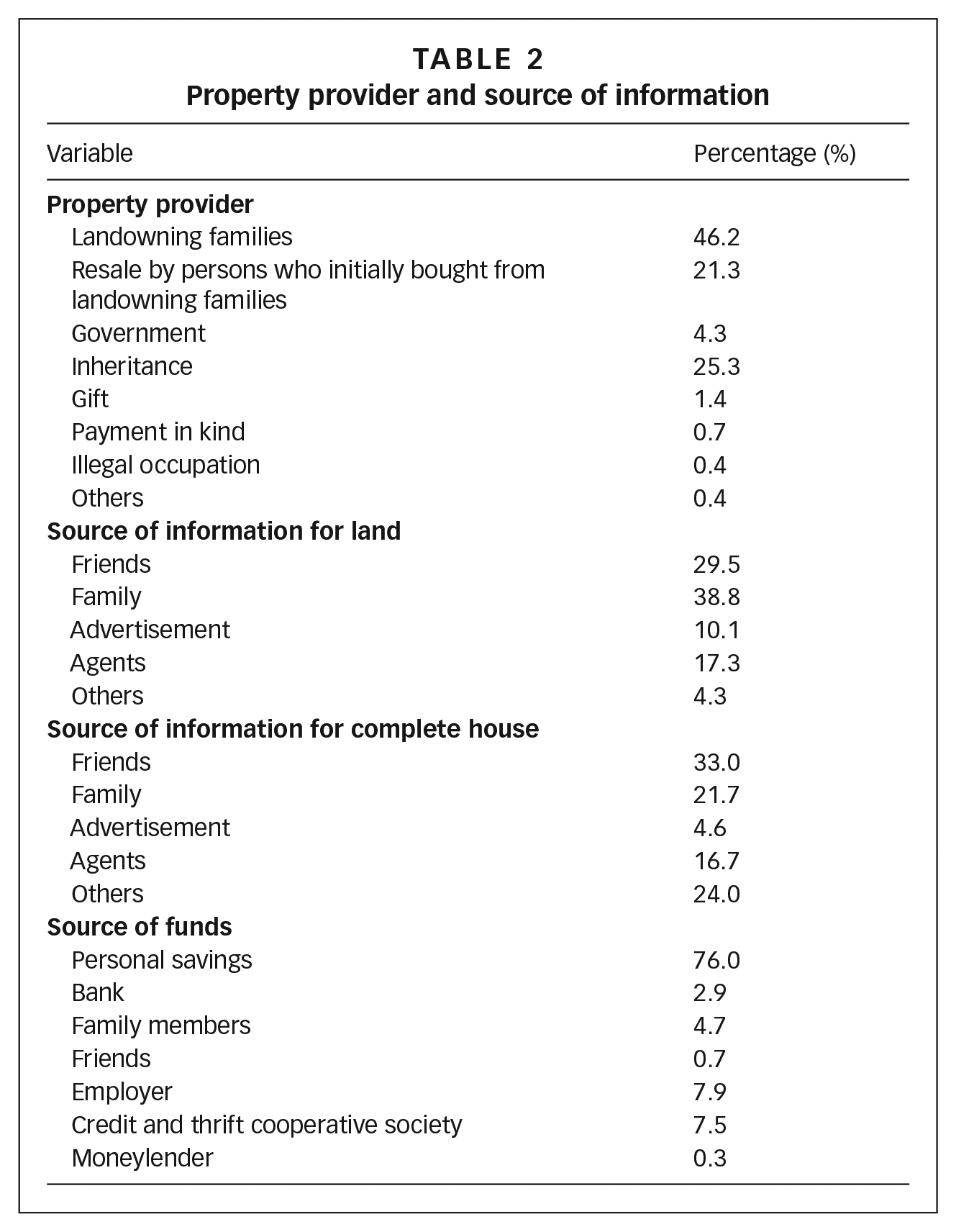

Interviews revealed the importance of a good information flow between actors in the transaction. To be useful, information has to be correct and communicated in a clear, timely manner, even though the flow can best be described as informal. Table 2 presents the source of information for the properties purchased by the homeowners in this study. Social networking amongst family and friends played a vital role, and those alerting potential buyers to land were mostly relatives and friends (68.3 per cent) living in the study area or with other links to the area. Agents played a role with regard to the information on the transactions in only 17.3 and 16.7 per cent of land and house purchases respectively. Informal networking was preferred for two reasons: reliability and cost-effectiveness. Although lawyers also feature as reliable informants, buyers noted that lawyers often charge to connect potential buyers with sellers. Lawyers are categorized as part of “others” in the study. Those providing information may also participate in the negotiations between interested parties, often as witnesses. Traditions play an important role in such transactions, and it is reportedly customary and socially acceptable for those so favoured (especially the buyers) to show appreciation with gifts at the end of the transaction. Mainly symbolic, these often consist of a bottle of wine or another type of alcohol.

Property provider and source of information

The sellers were members of landowning families, land speculators or private developers. The private developers mostly sold completed buildings. From Table 2, it can be seen that about half of the sellers (46.2 per cent) were from the families that had previously farmed the land. The two members of the Community Development Association who were from such families, explained that the family head, assisted by a few family elders, usually handles transactions, with proceeds distributed equitably to all deserving family members. Sometimes younger family members feel disenfranchised, and interviews revealed that they might resort to fraudulently posing as landowners and engaging in multiple sales of the same land to different unsuspecting buyers. Their activities have occasioned several land disputes in the area.

There is evidence that some buyers later resell their property. Over 20 per cent of the respondents had acquired their property from sellers who had earlier bought from landowning families. Some had purchased it intending to reside there, but were forced to sell due to an event such as loss of employment or death of a spouse. Others not so constrained might sell due to a job change or a desire to return to their ancestral home. Land speculation was also a factor. In some cases, these sellers had acquired several plots at a low cost and held them while they appreciated. One of the residents interviewed, who was involved in resale, confirmed for instance that he had moved into the area at the onset of settlement, when land values were lower, and purchased in acres. He thereafter began to sell when the value of the plots appreciated. The interviews with residents who were buyers also confirm this – some having bought land from people who purchased directly from landowning families earlier, and sold again long after development in the area commenced.

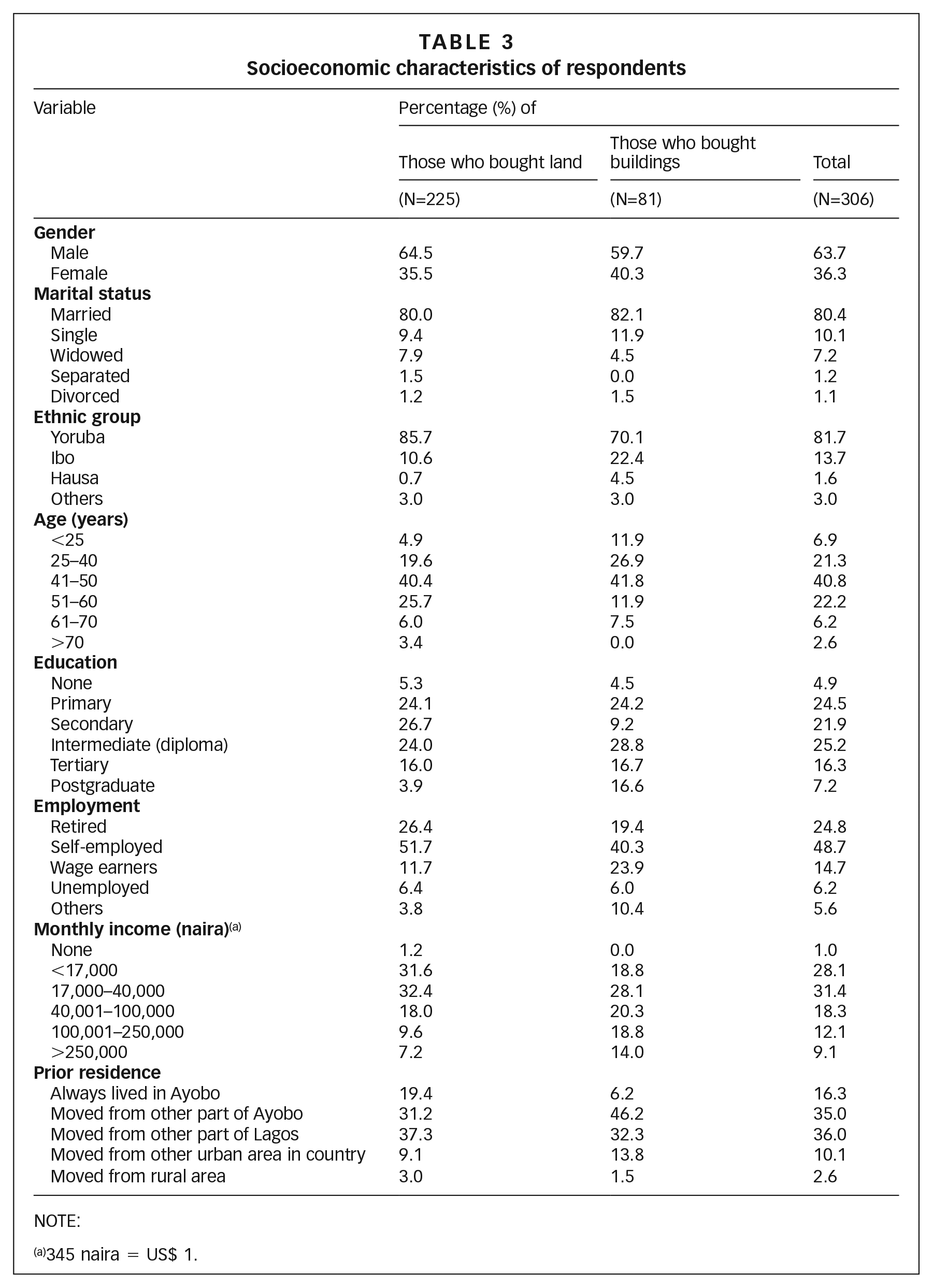

Most of the owner-occupiers in this study had identified and bought either already constructed houses or undeveloped land on which they built their houses. There were also some respondents who had acquired their houses as an inheritance or gift, or by other means. Findings on the socioeconomic characteristics of these respondents are presented in Table 3. They are predominantly married men, aged over 40 with at least primary education and corresponding income levels (Table 3). Most respondents were of the Yoruba ethnicity (81.7 per cent), lending credence to the findings of earlier researchers that peri-urban settlements are characterized by small homogeneous pockets based on common ethnic and kinship backgrounds.(46)

Further disaggregation of data (also presented in Table 3) shows some minor demographic differences between those who purchased built houses and those who bought land on which houses were subsequently built (p>0.5), although these differences did not reach significance. Of those who purchased already built houses, almost two-thirds had primary, intermediate or secondary education, and an additional one-third had gone beyond this for tertiary or higher schooling. The group that purchased land only was less likely to have had tertiary education (19.9 per cent), but most of them had primary, intermediate or secondary education.

Socioeconomic characteristics of respondents

NOTE:

345 naira = US$ 1.

Respondents had a wide range of incomes, although over 60 per cent could be considered low income. This is using a benchmark of 40,000 Nigerian naira (US$ 116), or about US$ 3.80 a day, a more realistic amount for an urban area than the usual World Bank poverty lines. The monthly cost of living for an individual is estimated at between 41,800 and 43,200 Nigerian naira.(47) The cost of living in this context is based on the cost of basic needs, which include food, shelter, clothing, children’s education and transportation. As shown in Table 3, of the entire sample, only 39.5 per cent earned this much, or more than this amount. There was a clear difference in this regard between those who bought land only and those who bought completed buildings. Only about one-third (34.8 per cent) of those who bought just land earned as much as or more than this living cost. More than half (53.1 per cent) of the respondents who bought already constructed houses earned more than this amount. It is interesting to note the number of those in the highest income group (9.1 per cent earning more than 250,000 Nigerian naira or about US$ 724 monthly) who also own homes in this informal settlement. These households resided in the parts of the settlement under private estate managers. Interviews revealed that some people in this category moved into the area because it was close to their places of work; others moved because they were able to access large plots here to construct buildings to their taste. The results also show that almost half (48.7 per cent) of the owner-occupiers were self-employed. Most of the respondents had moved in either from other parts of Ayobo (35.0 per cent) or from Lagos (36.0 per cent). Only 16.3 per cent had been born in the community, and a mere 2.6 per cent had moved here from rural areas. Those who moved from other parts of Ayobo used to be tenants, but purchased properties and became homeowners.

Acquisition of a residential property is arguably the most capital-intensive investment households (especially poor households) embark upon. The study sought to determine how respondents (in this case the buyers) sourced money to finance their property acquisition. Unlike in the global North, where funding is usually accessed from well-functioning mortgage institutions, the majority of the respondents financed the transactions from their personal savings. Given that many were self-employed, it is likely that their businesses financed their property bids.

A few relied on their employers and credit and thrift cooperative societies, which exist in many Nigerian workplaces (both public and private) today. Membership in such cooperatives can facilitate access to quick customer-friendly loans without collateral or bureaucratic encumbrances. In these cooperative societies, members’ regular savings qualify them both to access loans without collateral and to earn dividends at the end of the business year. Loan applicants are expected to provide a guarantor, who should also be a member of the cooperative society, and who has savings commensurate with the amount being applied for. Such loans, made available within a week or two, can then be used to meet the needs of the applicant, to be paid back as convenient. Many people who have access to such loans use them to purchase land and build houses.(48) These cooperative societies also assist in bulk purchases of building materials. Although there are different kinds of cooperatives, some for multiple purposes, land and housing cooperatives have the sole purpose of pooling resources to purchase land together and build houses. Members can then pay for property in instalments, usually through direct debit from salary. The fact that cooperative societies are attached to workplaces, and that only 14.7 per cent of the respondents were wage earners, explains why so few used this approach for funding housing in the settlement.

Self-employed residents were more likely to make use of daily contributory savings schemes, which have been found to encourage a saving culture. Respondents explained that, depending on the number of contributors, one person collects all the contributions at the end of the month. This is rotated until all members have benefitted from the scheme. With this access to bulk money, participants can meet specific needs, including property acquisition.

The contribution of family and friends to financing property was found to be negligible, probably because they have similar socioeconomic status. The contribution of banks and moneylenders is also minimal because of banks’ usual distrust of poor borrowers, coupled with the delays and inflexibility associated with bureaucratic processes. Moneylenders were shunned because of their exorbitant interest charges and lack of mercy in case of default.

Usually property transfers in urban areas, the status of the settlement notwithstanding, are documented, with the type of documentation depending on expense and the level of tenure security conferred. Documents vary from payment receipts and written agreements to the more expensive, and bureaucratically demanding, Certificate of Occupancy (C of O). Only 16.5 per cent of respondents, mostly higher-income households, obtained a C of O as their proof of ownership.

After agreement is reached on a land transaction, the plot is demarcated, generally by land surveyors engaged by the seller, and a letter of agreement for the transfer is prepared and signed in the presence of witnesses. Witnesses are usually trusted persons, invited by the parties, who can confirm that the transaction has taken place. In cases of disputes, their testimony weighs heavily on decisions taken. In the past, neighbours, friends and family members served as witnesses. Increasingly, lawyers are now called as witnesses and may, in addition, prepare the agreement documents. This practice is however not so popular yet, as lawyers often charge as much as 10 per cent of the cost of the land as legal fees for their services. Therefore, only people who can afford their charges engage them. Instead buyers rely on court clerks to draft the agreement, and informants to serve as witnesses. This adds a layer of legality to the transactions in these settlements. Due to recent developments, both the survey plan and the agreement documents are now registered with appropriate government agencies.

The role of the government and its agencies is minimal in property transactions in settlements like Ayobo, in contrast to what happens in formal parts of the city. In terms of taxation and regulations, the government has little influence on these informal settlements. Residents, however, approach appropriate government agencies for tenure regularization on the basis most convenient to them. In the rare cases where buyers opt for a Certificate of Occupancy, this must be issued by government. Very few respondents obtained government approval of their building plans prior to construction, and most of those who currently have this approval revealed that they obtained it after completing their houses. While 33.5 per cent of the respondents had approved building plans, only 16.5 per cent had a C of O. Land and building owners can apply for both building approval and a C of O in the process of regularization of tenure.

VII. Discussion

The results of this study show that the housing market actors in the Ayobo informal settlement have well-defined roles. As in every other informal settlement market, there are sellers, buyers and informants.(49) In addition to these, however, this study identified other agents associated with the sales. These include lawyers, court clerks and land surveyors. The fact that most of the purchased land was sold by landowning families confirms that this land was not invaded. The recognition given by the government to the sales agreement and the fact that a number of persons have also obtained their C of O indicate a changing governmental attitude towards accommodating informal settlements. Interviews with the CDA leaders, corroborated by the government officials, revealed that the community had initiated talks with relevant government agencies in order to benefit from the regularization window provided by the state government. The government’s change in disposition can be attributed to the need for political support from residents of informal settlements, which have large populations. Another reason is the need to generate public funds. A more tolerant attitude to informal settlements like Ayobo will arguably give the government greater leeway to levy taxes on property in order to generate funds.

Although the roles of buyers, sellers and informants of landed properties in Ayobo, as well as the characteristics of sellers and informants, conform to descriptions found in the literature, the characteristics of the buyers varied from accounts found in previous studies on informal settlements. The relatively large proportion of respondents in this sample who earned more than Nigeria’s proposed minimum wage (41 per cent) may be explained by the fact that the focus here is on owner-occupiers, who were buyers of the properties. If renters (62.6 per cent of local residents) were also considered, the proportion of the poor would rise considerably. This probably explains why a similar study in Ethiopia,(50) which considered all residents in informal settlements including renters, found a higher percentage of those in poverty. However, in line with the literature, the fact that almost 60 per cent of the buyers earned less than the monthly cost of living indicates that informal settlements can actually provide an opportunity for the poor and low income to become homeowners,(51) either by buying a house or by purchasing land and then building a house at their own pace. It makes sense that more than 70 per cent of the respondents were more than 40 years old, as it takes time to accumulate savings, which most of the respondents depended on to pay for their landed property. The average age at which persons enter into the workforce in Nigeria is 22.

It is also interesting to note how many of the buyers were from the high-income group. Observation of the informal settlement showed that particular streets housed these elites. The streets had more plentiful basic infrastructure, provided through contributions of residents. Some of the homeowners in this category indicated that they chose the settlement because access to land was less cumbersome. Some also indicated that the area was close to their workplaces. Interviews revealed that the streets inhabited by the elites had mostly been constructed by private estate developers.

Sellers in informal settlements have been noted in the literature to be mostly landowning families. This study, however, found that land speculators and private developers were also involved in the sale of property in the informal settlement. The involvement of private estate developers facilitates the provision of infrastructure, as they charge their (generally elite) clients for provision of these services. Land speculators in this study were mainly residents who moved into the area early when land was very cheap and purchased more plots than they needed. These additional plots were held as investments and disposed of when prices had appreciated or there were other compelling needs, such as housing improvements, children’s school fees, burials or celebration of children’s marriages.

Earlier studies identified small-scale entrepreneurs, local brokers, contractors, local officials, and sometimes court clerks as actors in the real estate market.(52) However, this study found that land surveyors and lawyers were also involved in the process. The lawyers draft the sales agreement, while the land surveyors subdivide the large agricultural lands into plots and demarcate boundaries, according to standards. These are professionals, registered by appropriate professional bodies to carry out related tasks according to standards stipulated by the Nigerian government. It was also observed that sales agreements are registered, in the same way that survey plans prepared by land surveyors are. There is, in other words, an apparent level of formality in these seemingly “informal” transactions, and professionals have been able to tap into hitherto ignored job opportunities.

As also described in previous literature, the role of the government in the Ayobo settlement was that of regularization. Soliman(53) noted over 20 years ago that settlers in informal settlements in Egypt could change their tenure status from illegal to legal when they reached an agreement with the authorities for regularization. This procedure in Nigeria, according to Ghebru et al.,(54) has different steps. Requirements for application include submission of land survey plans, architectural drawings of the building, structural drawings for a building exceeding one floor, and payment of application fees. An on-site assessment of the land and building is then carried out by the planning authority officials, after which the applicant is charged for the regularization, with a penalty for building without approval. At this stage, it is often difficult to enforce zoning laws and land-use requirements, since the structure is already constructed. Homeowners in informal settlements, however, appreciate this tolerance on the part of the government as they are able to legalize the ownership of their landed property, while the government benefits from the reduction in the housing deficit.(55)

Although the literature suggests that the rules guiding market transactions in informal settlements are unwritten,(56) this study reveals that transactions are well documented, and registered with government agencies, where appropriate. The government is clearly aware of transactions in this market, and in this context one might consider these transactions less unregulated than deregulated, as also pointed out by Schindler.(57)

Much of the literature suggests that people move from rural areas into informal settlements in peri-urban areas, usually in search of employment.(58) Results from this study also point to the role of migration between urban areas, given that most respondents moved from other parts of Ayobo and Lagos, and fewer than 3 per cent of respondents came from a rural area. This finding is similar to that of Adam in Ethiopia, where residents of the informal settlement investigated were from the urban centre surrounding the site.(59) A major reason the homeowners in this study moved to their current sites was for the more secure tenure that they claimed homeownership offered. This corroborates the assertion of Ubale et al.(60) that people move into informal settlements not only for affordable land and housing, but also to beat tenure insecurity, which is rife in urban centres.

The findings also point to the fact that these homeowners may not have moved in search of employment, given that about half were self-employed, and another one-fifth retired. This may also explain the reliance on personal savings as the predominant source of funds for the transaction, and on daily contributory schemes. These homeowners may not have met the criteria for formal loans, and for people in this category, friends and family members may be in the same “struggling/hustling” class with little to spare. Adedeji and Olotuah(61) also found the main sources of funds for property acquisition in Nigeria to involve personal savings and private mutual arrangements. Similarly, Gumbo(62) and Sheuya(63) identified the significance of personal savings in property acquisition in Zimbabwe and Tanzania respectively. The ways that homeowners, who in our study were mostly self-employed, are able to come up with sufficient finance through personal savings may however call for further investigation.

VIII. Conclusions

This paper has examined the property market in an informal settlement in Ayobo, part of Lagos, Nigeria. The focus is on the role of market actors, an aspect of the informal market that has not to date received much attention in Nigeria. In addition to the buyers, informants and sellers, this study indicates that professionals are involved in the real estate transactions in informal settlements. These include lawyers and land surveyors, adding a layer of legitimacy to the hitherto illegal transactions, as agreements and land subdivisions are registered with appropriate government agencies. The findings of this study indicate that all these market actors are aware of their roles, even when responsibilities are not formally regulated, and furthermore that transactions within the informal settlement market are often documented. The implication of this is that the informal settlement market is stable and likely to continue so, especially in view of the unabating urbanization in many low- or middle-income countries like Nigeria. It is therefore suggested that government policies make room for location-specific procedures when formalizing operational rules for such markets.

The study also adds to the existing body of knowledge with empirical evidence on the socioeconomic characteristics of homeowners in this informal settlement, demonstrating the fairly sizeable presence of middle- and even higher-income owner-occupiers. This challenges the belief that informal settlements, especially those characterized by unauthorized housing in urban peripheral areas, provide homes for the poor only. Rather, the study supports the notion that informal settlements provide an avenue for the low-, middle- and high-income groups to access housing and become homeowners.

The findings of the study also raise further questions. The strategies employed by the low-income homeowners in Ayobo in accessing their property need to be further investigated. How do they manage to set aside sufficient savings to finance the purchase of land and housing, given that many of them earn a bare minimum? What types of houses are they building and how long do they take to complete? The existence of the resale market in the study area also needs to be further investigated. The role of speculation on this front, suggested within the literature, needs to be backed with empirical evidence.

The fact that owners in Ayobo most often purchase land rather than completed buildings has implications for standardization and quality of the emergent buildings. Urban planners and architects might therefore take this into consideration, with the design of organic communities and housing that can develop over time. Considering that most developments are carried out without architects, with additions being determined by the homeowners, it may be pertinent to explore modular construction technologies that allow for incremental development, while maintaining standards.

The informal settlement studied here seems to have developed from urban–urban migration. There is a need for future studies on categories of informal settlements that result from rural–urban migration, but also those that result from urban–urban migration. The predominance of the respondents who were self-employed and retired may also indicate that movement into the informal settlement in the study may not be in search of employment opportunities, which rural–urban migration is noted for.

Despite the findings of this study, it should be noted that this study has only been carried out in one informal settlement in the urban peripheral area of Lagos. The results of this study may need to be confirmed in similar informal settlements in other areas of the country and in other countries where informal settlements exist.