Abstract

While delivering decent, affordable housing at scale is essential to global sustainable development, one formidable blockage is a lack of accessible housing finance for end users. People on low incomes have been perceived by lenders as high risk. They are excluded from financial systems and are forced to self-build using informal credit at exorbitant rates. This article engages with this problem, discussing practical examples and potential ways forward. It does so through case studies of models from Reall (a UK-based international development organization and social enterprise that promotes affordable homes) and its partner organizations in India, the Philippines, Nepal, Mozambique and Pakistan. The article evaluates the strengths and limitations of these models, and their potential for scaling up. Reall’s partners demonstrate that decent houses can be delivered at a cost that is accessible for potential low-income homeowners, while proving the viability of lending to borrowers in the bottom of the income pyramid. This is essential for demonstrating the commercial viability and impactful investment opportunity represented by affordable housing in urban Africa and Asia.

Keywords

I. Introduction

Rapid urbanization and an endemic lack of affordable decent shelter have compelled millions of people to live in overcrowded informal settlements. At least one-third of the urban population in the global South lives in such settlements, often lacking access to basic services such as electricity, running water and sanitation.(1) Access to decent-quality living conditions is essential for realizing the positive future envisioned in the UN Sustainable Development Goals and New Urban Agenda.(2) For the billions of people on low incomes across the global South, housing offers more than simply shelter – it represents the ownership of a financial, economic, social and cultural asset with the potential to break the poverty cycle. Improving access to housing can also yield several societal benefits, including increased political participation, macroeconomic growth and job creation.(3) However, the scale of the challenge remains enormous. The World Bank estimates that 3 billion people worldwide will need housing and basic infrastructure by 2030. This requires a staggering 300 million new housing units over the next decade.(4)

Meeting this challenge is not feasible without a massive capital injection to facilitate land acquisition, property construction and mortgage finance.(5) Yet the problem is not solely one of mobilizing investment. Throughout low-income nations, systemic barriers constrain the supply of decent housing that meets the demand at an appropriate cost. On the supply side, delivery and affordability are hindered by a lack of affordable land with access to jobs and services, insecure title inadequate resources for national housing initiatives insufficient incentives for developers to work at the low end of the market, and lengthy approvals and permitting processes.(6)

Effective demand for housing is constrained by the inaccessibility of affordable finance and mortgages (especially for those working informally). Typically, financial systems and housing finance delivery mechanisms in these countries have been geared towards high-income elites, and people on low incomes have been perceived as too risky to lend to due to their irregular employment patterns and cash flows, weak property rights and zero collateral. This risk is compounded for lenders by a prevalent lack of credible information and data on the characteristics of such people and efficient ways to assess affordability.(7) Consequently, people on low incomes across Africa and Asia have tended to build substandard housing, paid for with informal credit and micro-loans, often at exorbitant rates.

It is vital to develop innovative new models and approaches to housing finance. These should be attuned to the needs of people who live and work informally, while being commercially viable, scalable and replicable to enable construction and improve the lives of millions residing in poor conditions. This article engages with and offers insights on this challenge through case studies from Reall. Reall is a UK-based international development organization and social enterprise with over 30 years of experience in the sector. Reall promotes affordable housing in urban Africa and Asia for people in the bottom 40 per cent of their respective income pyramids, collaborating with partner organizations in sub-Saharan Africa and South or Southeast Asia.(8)

Specifically, this article presents case studies of housing finance initiatives by Reall partners in India, the Philippines, Nepal, Mozambique and Pakistan. All of these partners have innovated to reduce the cost of constructing housing – for instance, by changing regulations to reduce minimum plot size, shortening approval timeframes, facilitating access to affordable land, and streamlining design. However, such innovations cannot reach full impact without a supply of finance for people on low incomes, to acquire housing at an affordable cost. For affordable housing developers, a lack of end-user housing finance is a key systemic barrier that hinders scale-up and sustainability. This article therefore unpacks and explores housing finance as a fundamental issue that restricts both access to housing and scale of delivery.

II. Reall and “Affordable Housing”

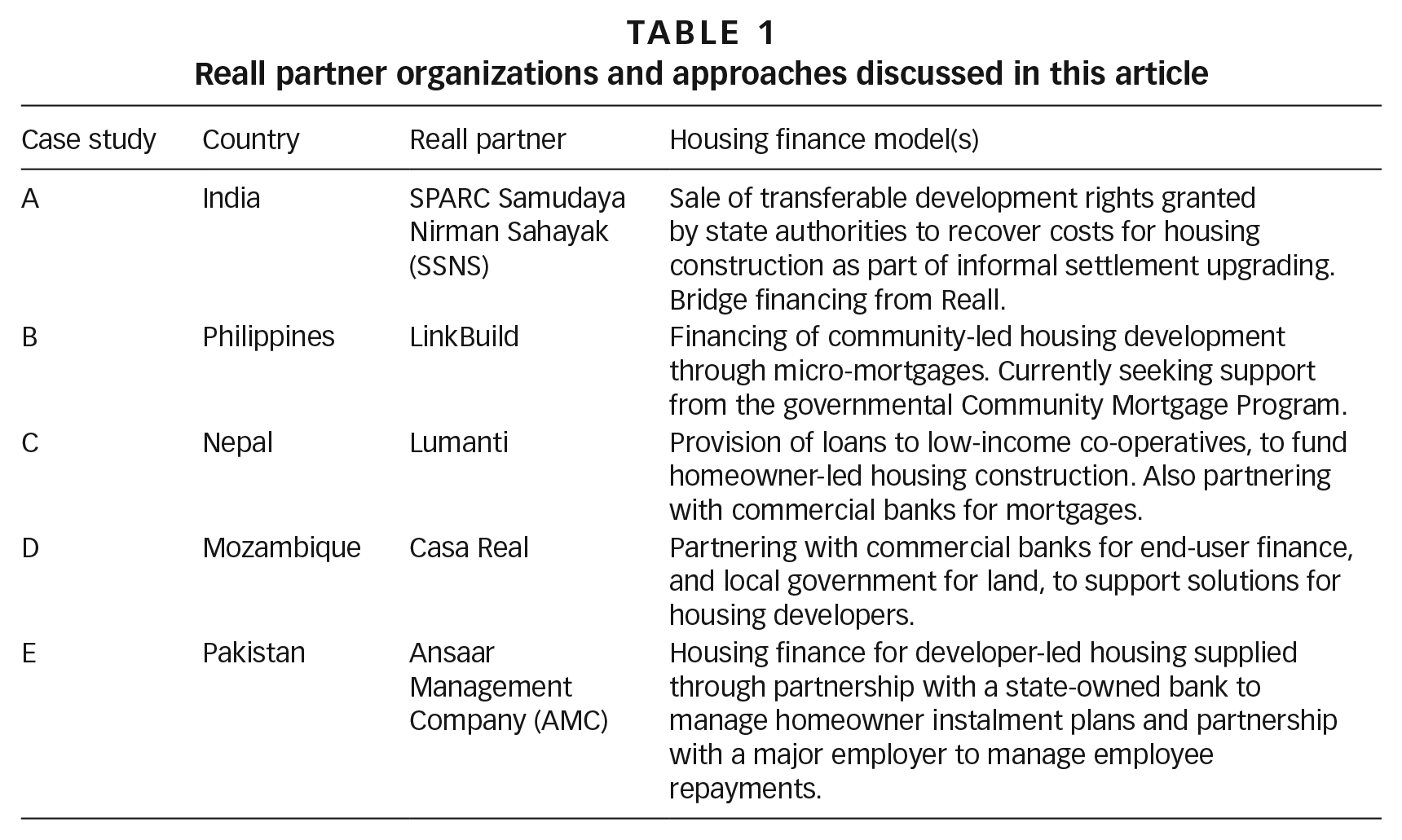

Reall’s partners are heterogeneous in approach. Some emerged from a conventional development NGO background; more recently Reall has entered into partnership with commercially oriented housing developers. Reall acts as a financial intermediary among development finance, impact investment and the partner organizations, which might otherwise struggle to attract capital investment. While some occupants of Reall-supported housing may previously have resided in “informal” settlements, the majority of Reall partners do not operate directly in such environments or engage in informal settlement upgrading work. Instead, Reall partner organizations deliver “formal” housing – defined as housing that has secure tenure, is built to agreed standards, adheres to all relevant laws and regulations, is fully equipped with basic services, and uses permanent building materials. The five Reall partners discussed in this article are summarized in Table 1.

Reall partner organizations and approaches discussed in this article

While there is no universally agreed definition of “affordable housing”, Reall partners aim to facilitate decent-quality housing for a cost of around US$ 10,000 per house to remain affordable to people in the bottom 40 per cent of the population, based on a national or regional income assessment.(9) Reall expects that the total monthly housing cost for occupant families should not exceed approximately one-third of their total monthly income.(10) This aligns with standard international practice, which assumes that an expenditure-to-income ratio exceeding 30–35 per cent is “unaffordable”, as the household will be cost burdened and at risk of not being able to afford other necessities.(11)

As the case studies and learnings demonstrate, improving housing “affordability” also encompasses other factors: providing secure tenure,(12) persuading mainstream lenders to include low-income groups by using effective assessment methods, reducing interest rates and surcharges on housing loans, reducing processing and collection costs for loan repayments, increasing opportunities to borrow for longer periods of time, lowering deposit requirements, and more generally widening the financial inclusion of people working informally. This article approaches “affordable housing” from this multifaceted perspective.

In the absence of fully functioning and inclusive housing markets, many Reall partners have provided “micro-mortgages” to low-income individuals and families. These are loans provided over five years to fund the construction and acquisition of “core” housing (a small house to which the owner can incrementally add features and rooms over time).(13) Micro-mortgages are intended to fill gaps between housing microfinance and more formal commercial housing products – providing loans for longer periods of time and at lower rates of interest than comparative housing microfinance products, but for briefer periods than commercial mortgages.

The micro-mortgages provided by Reall partners have helped people on low incomes to improve their living conditions, and their loan repayment data are evidence that low-income groups are a viable investment opportunity. This model also ties up capital for long periods of time over stages of land acquisition, housing construction and home loans. This lack of liquidity constrains the long-term sustainability of the organizations concerned, while preventing building at scale (an important mechanism for lowering costs further). Reall thus is increasingly exploring opportunities to leverage private sector finance, overcome systemic constraints and reform housing markets. This requires compelling evidence that affordable housing is a credible investment opportunity.

The experiences of Reall partners suggest that the maximum five-year loan period can be restrictive for low-income groups, and the longer terms associated with formal mortgages would be beneficial if implemented with favourable terms and administered efficiently to reduce costs to providers. Many of Reall’s partners have consequently explored new models and partnerships in which third parties provide housing finance. These are discussed further in the case studies below.

III. Methods

This article’s sample of cases reflects a cross-section of approaches, models and partnerships being implemented across Reall’s network. Through a comparative analysis, the paper will illustrate the possibilities for improving access to affordable housing finance for people near the bottom of the pyramid in low-income countries. The analysis emphasizes key learnings that can improve future effectiveness and overcome systemic blockages.

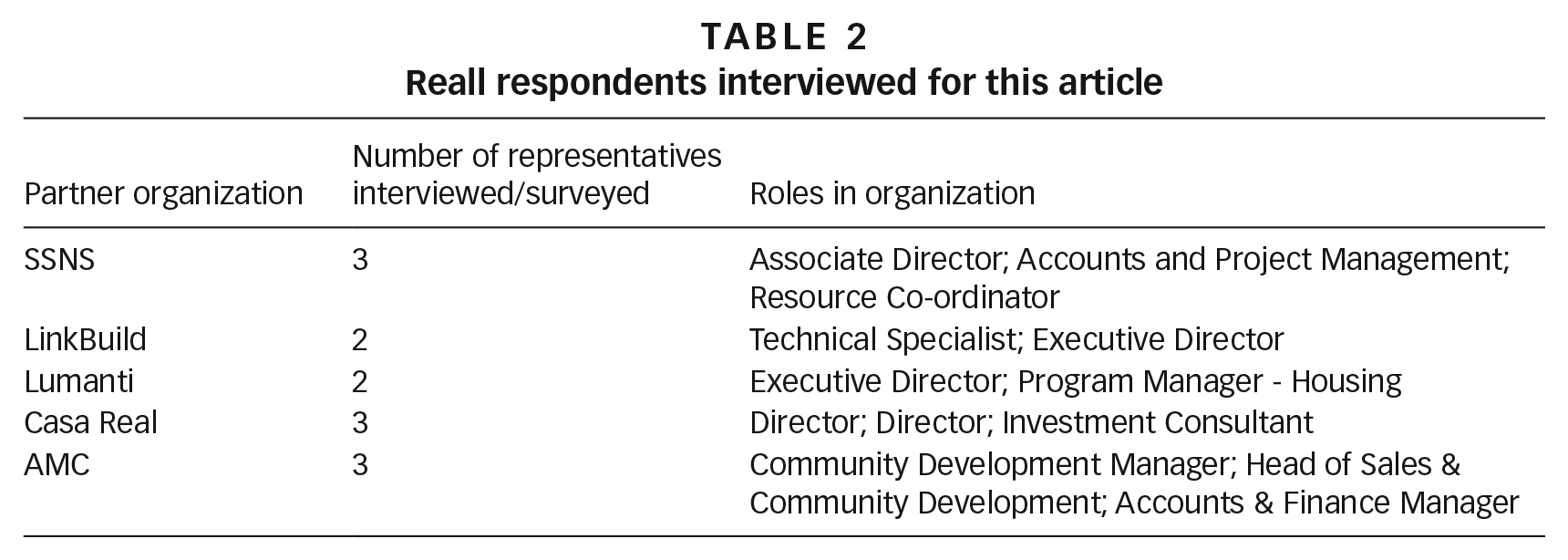

The case studies are grounded in qualitative data collected by the authors from the respective partners. This includes data from written interviews, written surveys, extended correspondence, and the sharing of reports and internal documents. Respondents were chosen for their particular involvement in or knowledge of partner housing finance initiatives and issues. These individuals are identified in Table 2 by their organization role.

Reall respondents interviewed for this article

The case studies highlight successes and challenges, the wider political and economic environments, the partnerships that have been brokered, and key lessons for improving markets and realizing scale. This information is strengthened with relevant quantitative data including the number of houses delivered, the capital invested, the type of housing finance loans facilitated, the accompanying interest rates and other conditions of these loans, and occupant income and repayment data. This information is provided to Reall through mandatory reporting and is periodically audited. As we are employed by Reall’s Evidence Team, we have unrestricted access to this information for research purposes.

Our association with Reall raises legitimate concerns about our independence. However, we are trained academic researchers, and the analysis presented here reflects our own views as practitioners rather than those of Reall as an organization. No case study is presented as a perfect solution. Rather, this article offers reflections and learnings as a contribution towards a wider dialogue on the escalating global housing crisis.

IV. Reall Partners and Affordable Housing Finance Models

a. India: SPARC Samudaya Nirman Sahayak (SSNS), transferable development rights and sustainable low-income housing

As most African and Asian governments lack the capacity to build millions of housing units themselves, the responsibility is borne by other actors. Yet the work of Reall’s Indian partner (SPARC Samudaya Nirman Sahayak or SSNS) highlights the important role of the state in fostering amenable policy frameworks. SSNS was formed in 1998 as the construction arm of the Society for the Promotion of Area Resource Centres (SPARC). SPARC is an NGO focused on housing and infrastructure issues relating to the urban poor.(14) SSNS is Reall’s longest-standing partner; the two organizations together developed the Community-Led Infrastructure Finance Facility (CLIFF) in the early 2000s as a mechanism for channelling bridge finance to organizations working in informal settlements.(15)

SSNS upholds a community-led approach in all of its work, building houses and toilets in collaboration with professionals and the government (Photo 1). In doing so, SSNS seeks to improve the lives of people who reside in substandard conditions, while demonstrating successful delivery models that encourage others to enter the market. SSNS always works closely with community members when designing projects and will often tailor designs specifically to individual needs. In high-rise projects, layouts and designs are planned and executed by professional contractors with community input. This participatory approach is essential to developing sustainable communities. Many SSNS projects have been undertaken in cities in Maharashtra State such as Mumbai and Pune, with some implemented in the states of Odisha, Karnataka and Telangana.

Interior of SSNS TDR-financed housing in Mumbai, India

All major SSNS projects operate by leveraging government subsidies and schemes under existing informal settlement upgrading programmes, with three types of schemes invested in by Reall through the CLIFF programme. These are the generation of transferable development rights (TDR); the Basic Services to Urban Poor (BSUP) scheme; and the construction of communal toilets. CLIFF funding has also supported individual housing upgrades and toilet construction. As an innovative approach to housing finance, TDR is discussed here.(16)

TDR works because the Indian government sets official restrictions on the height and area relative to plot that buildings can occupy (measured by floor space index, or FSI).(17) Builders are granted additional development rights by the regional authority, if they also construct housing for eligible low-income occupants.(18) These valuable development rights can then be used on site to further densify a building, or can be sold to other developers on the open market for profit. SSNS has harnessed this mechanism to generate funds for in-situ informal settlement upgrading, with pre-finance and startup bridge capital provided by Reall and other lenders. The housing is provided at no cost to the eligible families, ensuring that the most vulnerable people can benefit. Eligibility is determined solely by the length of time a potential homeowner has lived in an officially recognized informal settlement, rather than by income level. Data provided by SSNS to Reall indicate that all the individuals and families they work with fall comfortably within the bottom 40th percentile for income in their respective locations.(19)

SSNS has constructed over 6,500 housing units with Reall’s support since 2001, of which 2,370 are part of TDR informal settlement upgrading projects in Mumbai. All in-situ upgrading requires a large commitment from beneficiary families, which in the case of Mumbai high-rise developments may spend several years living in shelters on the site periphery. It is mandated that all developments are managed by a co-operative member society, financed with an initial investment of INR 40,000 (US$ 555 in November 2019) per apartment.(20) Households are subsequently expected to make regular monthly payments to meet maintenance costs.

As of November 2019, SSNS has spent INR 1.13 billion (US$ 15.71 million) on TDR projects, including INR 358 million (US$ 4.97 million) of Reall funding, fresh and revolved. In return, SSNS has received INR 1.15 billion (US$ 15.98 million) in TDR reimbursements and sales to other developers. This demonstrates that SSNS has roughly broken even on TDR activities to date, with bridge financing. However, if SSNS were to receive the full total of what it expects in terms of future TDR reimbursements and selling rights to other developments, it would report a surplus of INR 1.24 billion (US$ 17.25 million). This demonstrates that the TDR model is effective at financing housing development and construction in a sustainable fashion, while benefitting people on low incomes who have resided in informal settlements for long periods.

While results show the TDR model is convincing, the generation and sale of TDR rights is a drawn-out process that takes years to yield results. SSNS has thus far only operated and maintained liquidity with the support of Reall and CLIFF bridge finance. For the model to become self-sustaining, the TDR process and the policies that govern it must be streamlined and made more efficient. This model is also only replicable elsewhere if other governments emulate the Indian example, which requires substantial financial resources and political reforms. Furthermore, the TDR model is inherently geared towards densely populated urban environments where land costs are high, and densification is attractive for developers. The model is less suitable in contexts where land is cheaper and more plentiful, such as in peri-urban or rural areas.

Responding to these constraints, SSNS will share responsibilities for all future TDR projects with external developers. In this new approach, SSNS will mobilize communities and set design standards while the developer will undertake construction and use their resources to push through the TDR approvals process. SSNS has already initiated one project under this model, partnering with a developer (Renaissance Infrastructure) to deliver 900 units in Kanjurmarg, Mumbai. Sales of the initial batch of TDR payments will first cover Renaissance’s construction costs, with the remainder shared equally between the two parties. This project is now approaching completion, and it will be vital to ascertain whether partnership with an external developer can reduce TDR processing timeframes and improve the overall efficiency and sustainability of the model.

b. The Philippines: LinkBuild, community loans via government initiatives

Reall operates in the Philippines via the Philippine Alliance – a network of five organizations that brings together low-income community associations from cities across the Philippine archipelago.(21) Within the Alliance, Reall partners with LinkBuild, a housing enterprise promoting bespoke incremental housing products for self-organizing communities financed by community savings through micro-mortgage loans. These loans are delivered through Community Resources for the Advancement of Capable Societies (CoRe-ACS), a microfinance institution and Alliance member. While this model has improved the lives of residents in many communities, a lack of scalability has prompted LinkBuild to investigate alternative, government-backed initiatives to community finance and housing construction.

In the existing model, land is purchased or mobilized, with LinkBuild constructing core houses. Homeowners are selected by LinkBuild, if they satisfy certain eligibility conditions.(22) In parallel, CoRe-ACS conducts credit and background checks, administers loans and collects payments from community members. CoRe-ACS loans are micro-mortgages provided for five years with interest charged at a rate of 18 per cent. LinkBuild constructs all the main features of a core house, including doors, windows and toilets, while the individual household is responsible for organizing the installation of utilities and services. LinkBuild’s houses are designed with input from the community and every project is tailored to individual needs (Photo 2).

LinkBuild-built house in San Isidro Municipality, the Philippines

Many Filipinos with low incomes prefer micro-mortgages to longer-term products, due to an aversion to taking on long-term debt and a preference for building homes incrementally over time. LinkBuild data indicate that its occupants are well within the bottom 40 per cent of the income pyramid bracket, while their average monthly housing expenditure is “affordable” in relation to overall income (22 per cent).(23) However, many seek additional finance from other sources in order to complete construction work, which complicates the affordability of their housing. The short loan term and relatively high interest rate can also be problematic for people with irregular employment patterns (such as seasonal workers).(24) This has contributed to a low collection rate by CoRe-ACS for micro-mortgages, reflected in a loan Portfolio at Risk (PAR) > 90 days value of 38.2 per cent in 2019.(25) This low collection rate also reflects administrative and organizational limitations in how CoRe-ACS has conducted credit checks and assessed income flows in the past.

While LinkBuild’s emphasis on community input ensures that all of its projects are sensitive to the needs of the urban poor, this can drain organizational time and resources. The acquisition and development of land to build upon is also fraught with bureaucratic and political challenges. These include the identification of suitable land, and a raft of administrative hurdles (including long approval times and processing delays) that result in project postponements.(26)

In response to these challenges, LinkBuild is now brokering a partnership with the Social Housing Finance Corporation (SHFC), a Philippine government agency mandated to undertake low-income social housing programmes. SHFC is responsible for administering the Community Mortgage Program (CMP), a government financing initiative that enables the urban poor to purchase the land they have been living on, legitimize their status and take out long-term mortgages. Interest is charged at a fixed rate of 6 per cent for 25 years (significantly lower and longer than CoRe-ACS micro-mortgages). Originally launched in 1988, the government’s role in the CMP is to finance and regulate, with community associations responsible for administering loans and collecting repayments. The CMP is incremental, in that it gradually finances land acquisition, site development and house improvement over time.(27)

By partnering with the SHFC, LinkBuild seeks to become a housing provider for the CMP. This will potentially unlock government finance for communities at more affordable terms, while relieving the financial pressure on LinkBuild to maintain a loan facility, thus enabling a faster pace of construction. Involvement in the CMP can also resolve the enduring challenge of land acquisition – a historically formidable challenge across the Philippines. This in turn makes it possible for LinkBuild to scale up and increase its impact.

This proposed new model of working is not without its own challenges. CMP-supported housing projects demand a minimum collection efficiency rate of 80 per cent, with projects suspended when this is not met. The community association is responsible for collecting payment from members, and also replacing defaulting members with qualified substitute borrowers. This can result in the new borrowers coming from higher income brackets. LinkBuild mitigates this possibility by carefully screening and assessing all of its association members.

Furthermore, the CMP process is riddled with bureaucratic delays. Loan processing and approval can take two years to complete. The resulting slow release of funds for construction can lead to contractors not being paid and work being halted. These delays can undermine project implementation and hinder scaling up. For now, Reall bridge financing is required to cover any shortfalls and funding gaps. In the longer term, these limitations could be mitigated with concerted political reforms, increased funding and rationalizing of bureaucratic processes.

c. Nepal: Lumanti, community co-operative loans and bank loans

In Nepal, Reall collaborates with Lumanti, an NGO established in 1994 to alleviate poverty through improving shelter. Soaring land prices and accelerating rural-to-urban migration has produced an endemic lack of affordable housing in urban areas across Nepal, and a rapid growth of informal settlements.(28) Lumanti has pursued a holistic approach that includes informal settlement upgrading, housing, savings and credits, water and sanitation, research and advocacy.(29) The organization works in several cities across Nepal, including Kathmandu and Pokhara. Since partnering with Reall in 2011, Lumanti has harnessed US$ 2.9 million of project funding to facilitate the construction of 1,903 new home self-builds, 272 home upgrading self-builds, and a block of 24 rental apartments built by Lumanti. These homes have been developed employing two separate models for housing finance – one mobilizing community co-operatives, the other commercial banks.

For several years Lumanti has supported the renovation and construction of homes, by providing low-interest loans to 17 separate community associations of low-income women across Nepal. Interest is typically charged on these loans at an annual rate of 8 per cent. While it is the responsibility of the co-operatives to determine eligible community members and manage their repayments, income data indicate that all members fall well within the bottom 40 per cent of Nepal’s income pyramid.(30) These homeowners typically build their own houses, with Lumanti overseeing and supporting the work (Photo 3). Lumanti has facilitated the construction of 1,155 housing units across 21 projects under this co-operative model, with almost all projects reporting a 100 per cent repayment rate. As this reflects the repayments of each co-operative as a group to Lumanti, it does not necessarily reveal the status of individual homeowner repayments.

Lumanti-built housing community in Pokhara, Nepal

This model is effective because it is grounded in the communities where Lumanti operates, which ensures that the needs of the urban poor and vulnerable women are accounted for. As the homeowners are simultaneously the co-operative’s own customers and shareholders, they are empowered to take ownership of timely repayment. The co-operatives also tend to have strong links with their respective municipalities, to leverage additional funds for infrastructure development. However, given the vast scale of the housing challenge in Nepal, working through community co-operatives alone can only represent one contribution to the broader problem.

Aware of these limitations, Lumanti has partnered with mainstream banks to leverage additional resources and make finance more affordable. The engagement of the commercial banking sector is pioneering in Nepal. It is made possible by Lumanti’s provision of loan guarantee funding, which reduces lending risk. In this model, Lumanti and the municipality jointly select qualifying homeowners, with a particular emphasis on poor and vulnerable households that can demonstrate the ability to repay. The banks provide loans to them for up to NPR 400,000 (US$ 3,460 in November 2019) at a subsidized interest rate of 8 per cent, well below the national average (12 per cent). These loans are provided over seven years, to support basic housing construction on occupants’ land. Lumanti has supported the construction of 1,026 units over five locations under this bank guarantee model. One of these locations reports a 100 per cent repayment rate, while the remaining four report a PAR > 90 days value of 0 per cent, 4 per cent, 21 per cent and 29 per cent respectively.

While this is a significant accomplishment for Lumanti, the subsidized interest rate is dependent on the guarantee fund being deposited. This suggests mainstream banks are reluctant to lend to people on low incomes without securitizing and de-risking arrangements. One of the major challenges now confronting Lumanti is persuading the banks not to discriminate against such individuals and to take their follow-up commitments seriously. As the banks have little to lose financially from these loans (since Lumanti provides a guarantee), they are inclined to focus their follow-up on their higher-income clientele instead. This increases Lumanti’s administrative burdens. If formal housing finance is to be genuinely unlocked at scale for people on low incomes, more enduring attitudinal changes must be stimulated among commercial lenders.

Although these initiatives are slowly unlocking formal housing finance in Nepal, there remains a need for systemic reforms that can enable delivery at scale. The Nepal Rastra (Central) Bank could immediately assist by reducing interest rates for the low- to middle-income segment. The frequent liquidity problems and credit crunches within the Nepali banking sector are also profound structural constraints that require careful political and economic management by the Nepali government.(31) In particular, there is a need for the state to provide tax incentives, subsidies, flexible bylaws and land grants that can encourage other actors to enter the market.

d. Mozambique: Casa Real, affordable mortgages in Beira

Mozambique is an extremely low-income country. Many of its cities are hindered by endemic infrastructural challenges, while housing affordability is constrained by high construction costs and inaccessible finance.(32) Reall’s partner in Mozambique is Casa Real, a social enterprise established in 2017 to make decent housing accessible in Beira (Mozambique’s second city). Supported by capital from Reall, Casa Real has built a pilot project of 10 quality homes on land provided by the Beira Municipality (Photo 4).

Casa Real-built houses in Beira, Mozambique

In parallel, Casa Real has negotiated with mainstream banks to unlock mortgages at accessible terms and rates for Beira’s citizens. This engagement was expedited by the Dutch government, which supported an impact advisory firm (Fount) to lobby several mainstream banks and the Central Bank of Mozambique. Association with the Dutch government was an important boost to Casa Real’s legitimacy and credibility, and many of the banks were attracted by the potential of new markets for loans. The Beira Mayor and the Municipal Council were also important enablers, permitting the sale of houses with “condominium” titles. This avoided legal restrictions on minimum plot sizes, which are otherwise too large and unaffordable for low-income households. Close partnership with the municipality also facilitated the provision of suitable land, prioritization in accessing services, and other forms of support in producing affordable housing for Beira’s population.(33)

These developments paved the way for Absa Mozambique (formerly Barclays) to launch a new housing mortgage product in 2019. These mortgages are targeted at Casa Real customers with monthly incomes lower than MZN 15,000 (US$ 237 in November 2019). This roughly correlates with the bottom 50 per cent of the income pyramid in Beira.(34) While Casa Real’s ambition is to lower this threshold further and enable poorer households to access mortgages, for now this income level is the lowest the bank is prepared to consider, and it represents a substantial improvement on previous mortgage conditions.(35)

Absa provides financing for a maximum 95 per cent of the property selling price, which is approximately US$ 10,000 for people on low incomes. The customer is expected to pay a deposit of at least 5 per cent, although Casa Real has worked to alleviate this by negotiating a reinsurance product for the banks to provide mortgages without a down payment condition.(36) Absa charges interest on the loans at the national “prime rate” (18 per cent as of October 2019), plus a relatively small margin of 0.25 per cent.(37) These terms represent a substantial improvement on the established formal mortgage lending conditions in Mozambique, which have typically charged interest at a rate of 30 per cent for 20 years with a daunting deposit requirement of at least 20 per cent.(38)

As part of its agreement with Absa, Casa Real identifies customers, facilitates agreements with employers, assists in opening bank accounts, provides relevant documentation for the houses (such as real estate and municipality certificates), and transfers ownership of the houses to the bank prior to loan disbursement. Casa Real also bears all costs for valuing the houses. While this is potentially very expensive and time-consuming, Absa have innovated by agreeing a general valuation for each housing typology, rather than for individual homes. This saves up to US$ 200 annually per house and represents a significant cost saving in the Mozambican context.(39)

Unlocking affordable mortgages in Mozambique is a substantial achievement that highlights several important learnings. Firstly, Absa required extensive risk mitigation before it would commit, and Casa Real established its own brand as a legitimate and credible developer with a convincing business case. In this they were aided by partnering with the Dutch government, fostering confidence that the work was more enduring than a one-off “NGO” project.

The inclusion of a financial consultant on the project team enabled Casa Real to negotiate with the banks in the language of business cases and returns on investment, rather than a message driven mainly by social impact. This was important, as the banks were initially unconvinced that a quality home could be built for US$ 10,000. Casa Real also encouraged a perception of potential long-term engagement among the banks, by developing and promoting a vision of an investable pipeline with a coherent strategy for land acquisition and construction. This was aided by the Beira Municipality’s public commitment to deliver 25,000 houses for lower-income groups by 2035, which further assured the banks of the long-term opportunity.

Nonetheless, Casa Real still had to build the actual units before the banks could be fully persuaded of their viability, and this was ultimately a defining factor in proving their credibility. Once work had begun, Casa Real and Fount maintained bank interest through regular communications and progress updates, emphasizing the building of quality homes and neighbourhoods to ensure customer appeal and bank confidence. The underlying quality of Casa Real’s houses was emphatically demonstrated in the context of the damaging impact of Cyclone Idai, which struck Beira in March 2019. In stark contrast to the wider city, the structures withstood the storm’s impact extremely well, suffering minimal damage with only the roofing sheets requiring repairs.(40)

Casa Real’s experience suggests that developing an inclusive, affordable and commercial bank-backed housing finance product is most effective when underpinned by a convincing proof of concept (building quality houses); patient engagement with banks and commercial lenders via a financial intermediary; and a convincing long-term vision to instil lender confidence that developing a new product is worthwhile and commercially viable with a path to scale.

e. Pakistan: Ansaar Management Company (AMC), housing development and commercial bank mortgages

In Pakistan, Reall partners with the Ansaar Management Company (AMC), a social enterprise established in 2008 to make quality housing more accessible. AMC works within or close to large cities, including Faisalabad, Lahore, Multan and Peshawar. Operating as a private property developer, AMC focuses on developing sustainable mixed-tenure housing to be sold on the open market with the aim of building safe and sustainable communities. AMC emphasizes high design quality of both the houses and their surrounding neighbourhoods. Houses are developed with an internal courtyard (for cultural reasons) and positioned around a large green space in a quadrangle formation (Photo 5). AMC also works with residents to build capacity and implement community management committees, which provide financial and physical contributions for the upkeep and maintenance of communal areas and infrastructure. To date AMC has constructed 683 houses and plots with Reall support, with over 4,000 more awaiting development (making AMC one of the largest partners in Reall’s portfolio).

AMC-built housing and community spaces in Faisalabad, Pakistan

The affordable housing challenge is vast in Pakistan. The national housing deficit is estimated at 10 million units, rising by an additional 350,000 every year. Accelerating urbanization and population growth further stretch the demand. Unfortunately, a weak and incoherent banking and finance sector has restricted the accessibility of housing finance to a tiny, high-income social elite.(41) Despite this challenging environment, AMC has successfully developed a mortgage product for people on low incomes in partnership with the Housing Building Finance Company Limited (HBFCL), a semi-state-owned institution operating in the public interest.(42) As a result of over three years of negotiation, HBFCL now provides a mortgage product to AMC customers with a minimum monthly income of PKR 25,000 (US$ 161 in November 2019). This is a substantial move “down market”, as reflected by the fact that AMC occupants fall within the bottom 40 per cent of the income pyramid.(43) The mortgages are loaned at a fixed interest rate of 12 per cent(44) for a term of up to 20 years, with a deposit requirement of up to 25 per cent. The mortgages are available to people in both formal and informal employment.(45)

The development of this mortgage product is an impressive accomplishment. While HBFCL was originally established to provide mortgages to lower-income segments of the population, the institution deviated and shifted towards higher income brackets due to perceptions of risk and a lack of credible suppliers. It could not have been persuaded to move back “down market” without AMC reducing risk and ensuring lending security by providing land certificates and building desirable homes that adhere to all quality standards and signoff procedures. AMC’s efforts have been reflected in a loan acceptance rate of 98 per cent by HBFCL for its customers.

The willingness of HBFCL to consider people in informal employment is important, as Pakistan’s informal economy is estimated to account for more than 70 per cent of all employment nationally outside of the agricultural sector.(46) To qualify, such individuals must satisfy certain conditions, including paying up to a 25 per cent deposit, submitting a signed affidavit stating their monthly income, and providing post-dated cheques on a recurring basis.(47) In practice, HBFCL has still found it difficult to accurately assess informal income flows (relying for this on an independent valuator). The majority of individuals making use of this mortgage facility are in documented, formal employment. Much more can be done to make this model truly inclusive, such as by refining income assessment methods, reducing processing costs, relaxing deposit conditions, and improving procedures to support informally employed individuals. While the microfinance sector has mastered such methods, microcredit providers tend to charge interest at rates exceeding 35 per cent – well above the 12 per cent annual rate offered by HBFCL.

In addition to this mortgage product, houses are bought via AMC’s instalment plan (or sometimes with cash for plots). The instalment plan is designed for those who are ineligible for a bank loan, and in some cases the plan allows the sales process to start before conversion to a mortgage. AMC has also brokered a deal with a large industrial employer (Sitara Chemical Industries) to purchase AMC-built homes at the point of completion to provide to their employees. They then assume responsibility for managing repayments. The benefits of this employer partnership are clear – AMC’s capital investment is freed up for other purposes, including larger-scale construction, while the housing finance blockage is resolved.(48)

The AMC/HBFCL mortgage product is still in early phases of development, with 59 mortgages granted to date and eight more in the immediate pipeline. Early results have been positive, with average repayment rates of 80 per cent in 30 days, 90 per cent in 60 days, and 99 per cent in 90 days. What this demonstrates is that people on low incomes can successfully repay long-term mortgage loans and represent a viable economic opportunity for investors. Successfully proving that this sub-commercial model works is essential in Pakistan, to encourage more banks to step into the sector. Further evidence of success and scale will be required, alongside banking reforms such as those recently called for by the State Bank of Pakistan.(49) Political and legal reforms should also be forthcoming, in particular addressing the consistent bureaucratic hurdle of obtaining “no objection certificates” from development authorities before commencing projects.(50)

V. Conclusions

It is important to identify and develop housing finance models that work in different low-income urban environments. There is no universally adaptable approach, and in practice a toolbox of diverse solutions is required. Yet these case studies do highlight a number of important learnings and implications for the policy and practice of delivering decent housing to people on low incomes in Africa and Asia.

Making housing genuinely more “affordable” for lower-income segments requires a wide range of financial measures, in addition to cost-cutting methods during land acquisition and development. These include lowering established interest rates for housing finance products (as realized by several Reall partners); reducing or outright removing large deposit conditions (as Casa Real did); and extending the term lengths of housing loans to spread out costs for people on low incomes (Lumanti, LinkBuild, AMC and Casa Real). In practice these initiatives require innovative planning, effective implementation, patient nurturing of partnerships, and careful attuning to the experiences of low-income groups.

Virtually all of the Reall partners discussed in this article are engaged to some extent in extending housing finance to informal workers. In a world where two billion people make their living in the informal economy (more than 60 per cent of the global employed population), this is both a massive obstacle and an untapped opportunity for affordable housing progress.(51) Extending financial inclusion and formal housing finance to this underserved group requires robust de-risking efforts, including building lender confidence through more informed understanding and assessment of client income data (AMC); introducing insurance and reinsurance products to mitigate the lender’s risk (Casa Real); using loan guarantee schemes (Lumanti); delivering quality homes and estate management to ensure that properties retain value (Casa Real and AMC); and adapting learning from community savings and credit groups where relevant (Lumanti).

Empowering low-income groups to enter the formal financial market and secure affordable mortgages is enabled by more robust credit reporting, and more varied opportunities for people to build and share their credit histories.(52) For this reason, Reall is investigating new partnerships with organizations that can pioneer innovative new approaches to credit scoring and the assessment of loan affordability for the informally employed.(53) Reall is also exploring ways to feed partner loan repayment data into national credit bureaus (where they exist), and create such bureaus where they are absent. This will decrease information asymmetries between borrowers and lenders, and enable the latter to more accurately evaluate risk and improve portfolio quality. Loan collection processing and labour costs should also be streamlined and reduced using more efficient and agile mechanisms, such as mobile banking.(54)

The examples presented here all demonstrate the need for new partnerships and collaborations that can overcome systemic blockages. This includes working with commercial developers to share construction costs and recycle capital more rapidly (SSNS), and persuading large employers to take responsibility for employee repayments and enable the faster cycling of funds (AMC and Sitara Chemical Industries). The latter also empowers individual employees and trade unions to hold their employers accountable for decent living conditions.

Partnering more closely with commercial banks is a key innovation for unlocking affordable housing finance, and the experiences of several Reall partners shed light on how this can be achieved in practice (Lumanti, Casa Real and AMC). Casa Real and AMC demonstrate that influencing mainstream banks to move “downmarket” and recognize the viability of lending to people on low incomes requires a sustained effort to develop organizational credibility and investor confidence, underpinned by delivering quality houses. To successfully transform housing markets to become more inclusive of people living on low incomes, it is critical to broker similar partnerships with commercial banks across Africa and Asia. This accelerates financial sector deepening and macroeconomic growth, paving the way for private investment in affordable housing at scale.

There is a clear need for housing practitioners to collaborate closely with governments. The state will always have a role to play in fostering enabling environments for affordable housing delivery, so that access to housing and finance for those at the bottom of the pyramid is recognized and supported. State engagement involves not just the granting of subsidies, but also fast-tracking approval processes, rationalizing land acquisition laws, mobilizing capital investment, zoning land, encouraging public–private partnerships, and rethinking floor space index limits. Official support for affordable housing should also extend to the local level, where policy is implemented. The circumvention of minimum plot size laws by Casa Real in Beira highlights the utility of positive municipal relationships.

The examples presented here all demonstrate that “affordable” housing finance can be successfully unlocked for clients living on low incomes. However, the number of people being served directly by Reall partners is a relatively modest dent in the global housing deficit. Reall’s work proves that decent houses can be built at a cost that is accessible for potential low-income homeowners and sustainable for providers; the evidence and data this produces also proves the viability of low-income urban borrowers to lenders and demonstrates the scalability and developmental impact of affordable housing in Africa and Asia. Further demonstrations of the commercial viability and impactful investment opportunity of affordable housing are urgently required, to leverage new sources of finance and act as a catalyst for transforming markets and delivering affordable homes at scale.

Footnotes

1.

For the most recent global statistics on informal settlements, see UN-Habitat (2015). For more on the health and wellbeing challenges of living in informal conditions, see Ezeh et al. (2017) and ![]() .

.

2.

These two agreements are closely connected, with the New Urban Agenda seen as the delivery vehicle for the Sustainable Development Goals in urban settlements.

5.

9.

Reall uses the Canback Global Income Distribution Database (C-GIDD), minus government social expenditure, to understand household income data for countries at the national, regional and city levels. Reall checks mean partner client income against C-GIDD data, to determine what income percentile their occupants tend to fall within. For more information see C-GIDD’s website, accessed 1 December 2019 at ![]() .

.

11.

12.

All housing loans are given on the basis of secure tenure in the context of complete housing rights or rights to use land. This is especially important for the provision of finance by commercial financial providers to de-risk lending, which partially explains why such providers are reluctant to provide financial support to people residing in informal settlements.

13.

A “core” house is defined differently by Reall partners across country contexts. A cost of US$ 10,000 or less typically represents a core house that includes a bedroom, a cooking/living space and a bathroom as a minimum, with options to build additional rooms in the future.

15.

For more on the origins and development of CLIFF, see McLeod and Mullard (2006); Morris et al. (2007); and ![]() .

.

16.

While the focus of this case study is on transferable development rights, SSNS has undertaken extensive construction through the Indian government’s Basic Services to Urban Poor (BSUP) scheme, which operated from 2005 to 2017.

17.

Floor area ratio (FAR), also known as floor space index (FSI), is defined as the ratio of the floor space that can be constructed as per zoning and building regulations on the plot area. The FSI limit differs from city to city, depending on development strategies.

18.

19.

SSNS reports in 2019 that its housing occupants have a mean monthly household income of US$ 134.86. When correlated with C-GIDD data (see reference 9), this indicates that the mean SSNS end-user is within the bottom 10 per cent of incomes in their respective region.

20.

This INR 40,000 investment is split evenly between the developer and the Slum Rehabilitation Authority.

22.

These selection criteria include endorsement by the HPFPI, a regular source of cash flow, and a positive credit check result.

23.

The mean LinkBuild end-user is within the bottom 20 per cent of incomes in their respective regions, with a mean housing expenditure-to-income ratio of 22 per cent.

24.

For this reason, CoRe-ACS is currently proposing an eight-year loan period for all new housing loans.

25.

Portfolio at Risk (PAR) > 90 days is the principal balance of open loans overdue by at least 90 days, or open loans with no repayment for at least 90 days. PAR > 90 days is typically believed to correspond to bad loans.

26.

In the Philippines, “Land distribution is highly skewed, and much of the land is moderately or severely eroded. Despite various land reforms, significant numbers of rural people remain landless, and there is a swelling urban population living in informal settlements.” While considerable swathes of lands have been redistributed, “some of the most productive and fertile private agricultural lands remain in the hands of wealthy private landowners. Lack of access to land and natural resources by most of the population is a key cause of poverty, a driver of conflict and an obstacle to development.” For more, see ![]() .

.

27.

For more on the Community Mortgage Program, see Ballesteros et al. (2017); Karaos and Porio (2015); and ![]() .

.

29.

Daly et al. (2017). See also Lumanti’s website, accessed 1 December 2019 at ![]() .

.

30.

The mean Lumanti end-user is roughly within the bottom 10 per cent of incomes in their region.

31.

33.

The Mayor of the Beira Municipal Council (Daviz Simango) is a vocal advocate for low-income housing who has worked with the Dutch government for several years. He has done so despite representing an opposition political party (the Democratic Movement of Mozambique) at the national level.

34.

The MZN 15,000 maximum income cap roughly corresponds with the bottom 50 per cent of the income pyramid in major Mozambican cities such as Beira.

35.

Prior to the launch of Absa’s product, mortgages in Mozambique tended to be restricted to a tiny high-income elite.

36.

This reinsurance product will be provided by Home Finance Guarantors Africa Reinsurance (HFGARe). HFGARe facilitates access to housing finance through the “implementation of a Collateral Replacement Indemnity, which is a cover of last resort to lenders that make home loans available to this market segment”. Lenders thus “effectively swap assumed risk for the insurance premium, which in turn provides a platform for affordable, available home ownership finance”. See HFGARe’s website, accessed 1 December 2019 at ![]()

37.

The prime rate, officially known as the Prime Rate Financial System (PRFS), was introduced in June 2017. The PRFS has fallen steadily since its introduction.

39.

As part of its partnership with Casa Real, Absa has undertaken a thorough internal review of all relevant processes with a view to streamlining and cutting costs for lower-income customers.

42.

The House Building Finance Company (HBFC) was established in 1952 by the government of Pakistan and in 2011, the name was changed to House Building Finance Company Limited (HBFCL). The company’s objective is to provide affordable housing finance solutions to low- and middle-income groups.

43.

The PKR 25,000 income minimum roughly correlates with the bottom 10 per cent of the income pyramid in Pakistan, and AMC’s own research concludes that its end-users are within the bottom 30 per cent of incomes.

44.

The benchmark is KIBOR (Karachi Inter Banking Offering Rate). Traditionally mortgages were offered at KIBOR plus 1.5 per cent with the interest floating. To overcome inflation and price increases, HBFC developed a fixed-rate product of 12 per cent interest for low-income families.

45.

HBFCL uses parameters such as income levels and age to assess potential homeowners. Monthly repayments are made either directly or by salary deduction.

47.

The client provides 13 post-dated cheques – one for each monthly mortgage payment over the next 12 months, plus an additional cheque for the remaining balance. At the conclusion of month 12, a new round of post-dated cheques is submitted for the next year (plus the remaining balance), and the existing cheque 13 is destroyed. This is repeated annually until the balance is paid off.

48.

In addition to AMC’s partnership with Sitara Chemical Industries, Reall’s partner in Nigeria (the Millard Fuller Foundation, or MFF) has partnered with the Federal Road Safety Corps (FRSC) to facilitate housing to its employees.

49.

In 2019, the State Bank of Pakistan (SBP) called for the introduction of innovative housing finance products that can cater to all income sectors. These include fixed-rate mortgages, step-up payment options, interest-only period products, and discounted rates for borrowers through arrangements with other entities. See ![]() .

.

50.

The no objection certificate (NOC) is a “proof of authorization” that can be shown to local authorities when implementing projects, and it is a legal requirement in Pakistan to obtain a NOC before work can commence. The process to obtain NOCs is also extremely convoluted. For AMC, failing to secure the NOC results in an inability to initiate construction and establish proper infrastructure. Importantly, a missing NOC also results in the mortgage provider not approving the project. This is a significant blockage that can only be resolved through political reform.

52.

53.

This includes an innovative new platform that applies machine learning, AI and stochastic modelling to process and analyse loan applications, and use these analytics to reduce processing costs and input them into larger financial services architecture (such as credit rating agencies).