Abstract

This article explores the universal obstacles limiting sub-national governments from using municipal bonds. Specifically, it examines four case studies – Johannesburg, Douala, Dakar and Kampala – to understand their approaches to municipal bond issuance. The chief obstacle to municipal bond issuance for raising funds relates to the constitutional and regulatory systems in each country. This represents a significant departure from the commonly-held understandings that cities in the region are not eligible for long-term debt, lack capacity, or are not viewed as creditworthy by purchasers of municipal bonds.

The success of municipal bond issuance appears contingent on strong interlinkages between central and sub-national governments. This article critically reviews the powers granted to local governments under the countries’ constitutions, specifically the legislation that enables or prohibits municipalities from issuing bonds. Reform for a financially sustainable level of indebtedness for sub-sovereign governments is essential for the future growth of cities in sub-Saharan Africa.

Keywords

I. Introduction

Today, half of the world’s population lives in cities, which generate more than 80 per cent of global gross domestic product (GDP).(1) In 2015, the share of the national population that is urban stood at 39 per cent in lower middle-income countries and 30 per cent in low-income countries. By 2050, these figures are expected to be 57 and 48 per cent, respectively. During the period from 2006 to 2020, 9 of the 10 fastest-growing cities are projected to be located in the global South.(2)

The future development of emerging markets now depends significantly on how well urban population growth is managed in cities and towns. If well-managed, cities can be engines for economic growth and for expanding access to basic services for large sections of the population. But to date, the correlation between urbanization and economic growth has been weaker in developing countries than in developed countries.(3)

There is abundant evidence that countries in sub-Saharan Africa are struggling to face the challenges of urban population growth. The typical emerging city lacks control of land use or provision of adequate services. This means that traffic congestion wastes productive time and pollutes the air;(4) poor populations are concentrated on sites subject to a myriad of hazards;(5) and disparities between rich and poor create social tensions and insecurities that can turn the hopeful vision of life in a modern city into a nightmare, especially for the poor.(6) The economic potential of cities will not be fully realized until city governments have both the tools to manage the development challenges being thrust upon them and the resources to improve economic, environmental and social conditions.

Unfortunately, the world at large still under-invests in its infrastructure. To cope with massive population growth, human development needs, and climate change, as well as to sustain economic growth and productivity, more needs to be done to boost and retrofit infrastructure capacity. The world must invest an estimated US$ 1 trillion over its current allocations per year for the foreseeable future to meet basic infrastructure needs. These figures translate into global infrastructure needs of 3.8–6.6 per cent of GDP: 3.8 per cent in the global North, 6.6 per cent in the global South.(7)

Increasingly, institutional investors, companies and foundations have been approached to provide private capital to help fill this financing gap. One important source of funds, particularly in rapidly growing cities in sub-Saharan Africa, is municipal debt. This is because municipal bonds lend themselves to the lengthy repayment period required by sub-national governments, which in turn is driven by the willingness and ability of end users (citizens) to pay for the costs of the investments.(8)

II. National and Local Contexts in Emerging Markets

Municipal finance is especially important in emerging markets because of: (i) the relatively recent decentralization of power away from central governments towards provinces and cities; and (ii) the rapid unplanned urban population growth found in the world’s low- and lower middle-income countries. The shortcomings of municipal finance in countries across sub-Saharan Africa can be highly damaging because sub-national governments have clear mandates to provide certain public services and infrastructure. While the responsibilities delegated to local governments by law vary considerably from one country to the next, cities in developing markets often have mandates to provide: (i) local basic services and infrastructure, including water, sanitation, public transportation, public lighting, and solid waste management, among others; (ii) resilience building and climate mitigation and adaptation, including energy efficiency, flood management, and public building retrofitting, among others; and (iii) local social services and infrastructure, including health, education, and childcare facilities, among others.(9) These services, however, are expensive and require investments that exceed municipal budgets.(10)

The inadequacies of government transfers and the growth of urban areas makes functional decentralization more viable and more necessary, particularly as countries around the world often suffer from insufficient budgets to support cities with capital investment needs that may not be priorities for decision-makers at the sovereign level.(11) This is particularly pronounced in sub-Saharan Africa, where local governments are forced to compete against other political entities, including line ministries (which are often led by political appointees and cronies of the national government).(12) From a financial perspective, fiscal devolution is critical in allowing cities to demonstrate to potential sources of capital their commitment to city-level accountability for financial management and municipal efficiency in service delivery, which can help them to secure crucial investment. In some instances, this can also help to better institutionalize citizen expectations of government accountability and democracy.(13)

While urban needs and aspirations may grow, the financial options available to cities in most emerging markets have not kept pace with the growth and increasing complexity of the cities themselves. Cities are stuck in a vicious cycle of limited resources, leading to a constrained response, while the population of the city and the demand for services continue to expand. Ironically, many local government capital investments have high economic and social returns, and therefore should be attractive to governments (seekers of capital) as well as businesses (sources of capital).(14) For instance, there is strong demand for electricity and housing in most African cities, and investments in these sectors could plausibly offer commercial returns. Therefore, in a number of countries across sub-Saharan Africa, cities are looking to domestic capital markets as a potential additional source of finance; for sub-national governments, these transactions take the form of municipal bonds.

The conditions required to provide local governments with capital market access have been tested and developed in North America and Europe, initially in Italian city-states in the pre-Renaissance era, and with a more recent resurgence as early as the first decades of the 18th century for the construction of New York’s Erie Canal.(15) The critical challenges, particularly in developing countries, are bringing borrowers and lenders together in a market relationship, and managing the risks inherent in this type of financing.

There are countries where municipal bond issuance is not feasible. Where risks are too high, or financial markets lack liquidity or are too underdeveloped, raising local funds for municipal investments may be impossible (for example, in conflict-affected states). In other countries, such financing may be feasible where viable municipal projects can be developed. Public officials and the private sector may have little familiarity with strategies to raise funds for local development projects. However, with collaboration and technical assistance, experience shows that national governments, local governments, and private market actors can work together to create the enabling conditions, prepare projects for financing, and mobilize financial resources.

This article specifically focuses on the challenges and opportunities faced by municipalities in sub-Saharan Africa as they attempt to initiate transactions for capital-intensive projects. Following an analysis of sector gaps in emerging markets, it explores four case studies of cities that have attempted, and in some cases succeeded with, launching municipal bonds. This work has been informed by fifteen years of working on municipal finance with (among others) the United Nations, the World Bank, the Bill & Melinda Gates Foundation, the United Nations Sustainable Development Solutions Network, the C40 Cities Finance Facility, the United States Agency for International Development, the UK Department for International Development and the French Development Agency (AFD). It also builds on experience working with European banks focusing on emerging markets, including BNP Paribas and Dresdner Kleinwort Wasserstein. The author has worked in each of the four case study cities, either as a direct advisor to the municipal government or as part of my doctoral research.

III. Sector Challenges and Gaps in Sub-Saharan African Municipal Finance

a. Failure to create an enabling environment and framework for investment

Because financial institutions want to be reasonably secure in their decisions on long-term capital investments, the establishment of a transparent and sound regulatory framework for investment is a prerequisite for attracting capital flows.(16) Such a framework ensures that financial obligations are upheld for all parties to transactions. In the absence of this framework, institutional and individual investors lack confidence in domestic capital markets.

Additional legal and policy changes are likely to be required to encourage municipal borrowing. The national policy and regulatory framework needs to make it legal and feasible for local governments to borrow and to mobilize the resources to repay the credit, and to establish other conditions that lower risks for investors. In many countries in sub-Saharan Africa, the municipal law either does not permit borrowing, or limits it such that there is a mismatch between revenue generation and debt service. The law also may not prevent newly elected local officials from repudiating the borrowing of their predecessors, which creates repayment risks for investors. A framework needs to be put in place that: (i) allows local governments and other local entities to raise private funds; (ii) provides the means to repay the funds, by using user fees, tariffs, and/or tax revenues; (iii) sets standards for the preparation and reporting of financial information; and (iv) provides adequate stability over time. National governments also must establish regulatory bodies that oversee markets and stipulate the terms of recourse in the event that local governments default. These rules create certainty for both investors and borrowers, and are likely to need some reform before sustainable market-based municipal financing mechanisms can be established.

Sources of capital have responsibilities as well. To be effective investors in municipal projects, institutional investors should be prepared to mobilize adequate resources to meet local governments’ investment needs; be transparent about their expectations by creating risk/return trade-offs that are clearly understood and agreeable to both all parties; and encourage the involvement of capable intermediaries, analysts, and trustees who are prepared to facilitate transactions in both the primary market and throughout the lifetime of the bond (i.e., through providing liquidity in secondary markets). These conditions are often absent in sub-Saharan Africa due to the nascent nature of the financial markets, lack of investor confidence, and lack of tools to mitigate risks.

b. Discrepancy and mismatch between investment needs and available finance

Domestic private finance in countries in sub-Saharan Africa without capital markets is dominated by banks that are risk averse and either do not have funds or are reluctant to lend long term. As a result, lenders are unlikely to consider investing in city infrastructure projects without credit enhancements (typically in the form of guarantees) or the provision of funds for on-lending from development banks. In developed countries, institutions such as credit rating agencies and investment banks help to develop municipal bond markets by helping to match up investor and borrower requirements. These entities either do not exist in sub-Saharan Africa or, where they do, they rarely work with municipal governments. This is often due to the inability and unwillingness of municipal leaders to shoulder the costs of a third-party rating, or the lack of political will for the transparency required in a credit rating exercise. International ratings agencies have had mixed success in establishing themselves in sub-Saharan Africa - the presence of the three largest global market players (Standard & Poor’s, Moody’s, and Fitch) is a checkerboard across the continent, and indigenous ratings agencies, which have typically started in response to a market absence in a single region, are still nascent.

c. Lack of creditworthy local governments and bankable plans/projects

With few exceptions, cities are political entities led by politicians who serve the electorate, and this can have a significant impact on the ability to raise finance from risk-averse investors. Cities cannot pierce the sovereign ceiling established by the economic and financial performance – the creditworthiness – of their respective countries. Accordingly, the potential capital sources for cities are limited to those who already view the sovereign government as offering an acceptable return, commensurate with their respective perceived risk of default. Further, because most central governments in sub-Saharan Africa are responsible for tax collection from residential and commercial properties, with subsequent transfers to municipal governments, all purchasers of municipal obligations need to analyze the likelihood of regular and in-full payments to cities. This typically takes the form of a premium over the stipulated returns pledged by the sovereign government in its debt issuances (viewed in aggregate as the sovereign bond treasury curve).

For most cities in sub-Saharan Africa, achieving access to capital financing at a reasonable cost from sources other than transfers and own revenues will require sustained attention to improving the policies and practices underpinning both their creditworthiness and the projects requiring funding. A World Bank study found that only a small percentage of the 500 largest cities in developing countries could be deemed “creditworthy”– about 4 per cent in international financial markets and 20 per cent in local markets.(17) Municipal bonds can finance either specific investments (such as a water treatment facility, a parking garage or a convention centre), or an investment plan or a programme of capital investments that vary in size and sector. With specific investments, local governments would often pay the transaction costs from revenues associated with the investment itself (water tariffs, parking fees or convention costs). In an investment plan or programme, repayment would be from all municipal taxes, fees, tariffs or other sources that capitalize a general account and can be drawn from to pay the principal and interest related to debt service.

To make a convincing argument about a municipality’s commitment to its most bankable projects, cities often need to demonstrate that they have a larger list of “wish-list” projects that constitute a more ambitious capital investment programme. From that overall list, and in concert with a more comprehensive vision, municipal leaders need to garner support for this vision from the general electorate to ensure the longevity of a master plan beyond any given municipal administration. Simultaneously, cities need to commit to building their own local capacity to: (i) provide accurate information about the operational and financial activities of the local government; (ii) identify and prepare sustainable bankable projects; (iii) provide a strong repayment stream and demonstrate or mobilize local willingness to pay; and (iv) manage the financed projects during the life of the bond issue or other financing to ensure continued operation and maintenance of the investments, and collection of associated revenues, where relevant. The magnitude, sophistication and linkages between each of the projects that are elements in the overall master plan help to underscore the creditworthiness of the municipality itself.(18)

IV. Case Studies of Municipal Bond Issuance in Selected African Cities

Experiments to launch municipal bonds across sub-Saharan Africa have met with mixed success, often driven by the challenges identified above. To demonstrate this point, this article continues with a review of four cities, chosen for their attempts to source debt finance for long-term, revenue-generating, capital-intensive projects. The four cities are the largest in their respective countries, serving as political and/or economic leaders. Each offers important lessons to other city governments, and their development partners, that are seeking to issue municipal bonds.

Case Study 1: Johannesburg, South Africa

Alone in sub-Saharan Africa, South Africa explicitly and constitutionally enshrines the right of municipalities to borrow, through the Municipal Finance Management Act (MFMA). The MFMA, implemented in 2004, ensures that borrowed capital is used only for infrastructure investments, as long-term debt can only be raised to finance capital expenditures and not to fund current expenses. Thus, a bond issuance cannot be used to balance the budget due to a shortfall in any given year. From the outset, there is no ambiguity about municipal debt including bonds; the schedule of terms in Chapter 1 defines debt as “a monetary liability or obligation created by a financing agreement, note, debenture, bond or overdraft, or by the issuance of municipal debt instruments”. Chapter 6, which deals with municipal debt, differentiates between short-term and long-term debt, stipulating that short-term debt may be incurred “only when necessary to bridge shortfalls within a financial year during which the debt is incurred” or to meet “capital needs within a financial year”, while provisions for long-term debt are more permissive, allowing debt for “capital expenditure on property, plant or equipment to be used for the purpose of achieving the objects of local government” or for “re-financing existing long-term debt”. Through this legislation, municipalities became free to pursue transactions in the capital markets, with the understanding that “neither the national nor a provincial government” would “guarantee the debt of a municipality or municipal entity”, except in certain clearly defined circumstances.(19) Therefore, unlike in most of sub-Saharan Africa, local governments across South Africa were given significant latitude to creatively pursue municipal debt through capital market transactions, while simultaneously understanding that there would be no safety net in the case of an inability to meet the debt service requirements stipulated in the transaction documents.

The main motive for the initial consideration of bond issuance derived from an attempt to diversify the city’s funding sources beyond an almost exclusive reliance on commercial and development banks. As banks were overexposed to Johannesburg, the City of Johannesburg had reached its credit limits with nearly every bank and was forced to issue at least one municipal bond to obtain more funds for capital investment.

During the apartheid era (pre-1990), the City had successfully launched a number of municipal bonds. But this was in the context of prescribed asset requirements, whereby insurance companies and other institutional investors were required to hold 54 per cent of their assets in instruments such as municipal and other domestic government bonds.(20)

According to the financial statements for 2003 (which were incorporated into the prospectus), the City of Johannesburg had outstanding debts to banks totalling 1,153 billion rand (approximately US$ 173.6 million). The financial institutions included commercial banks (Standard Corporate Merchant Bank, Absa Bank, Nedcor Group, Rand Merchant Bank, First National Bank) and development banks (Development Bank of Southern Africa). The city was current on all of its debts at the time, but faced severe difficulties in trying to originate any new loans.

The city’s annual revenue for the fiscal year, which ended immediately prior to the bond issuance, totalled 4,651 billion rand (approximately US$ 700.45 million), with primary sources of finance being assessment rates, refuse removal fees, and subsidies/transfers from national and provincial governments. The two borrowings of 2004 – in aggregate 2 billion rand (approximately US$ 308 million) – represented slightly less than 50 per cent of the total annual revenue of the municipality. There was only a nominal discrepancy between the city’s budgeted revenues and those actually collected.

The City of Johannesburg, with its April 2004 issuance, marked the beginning of the post-apartheid municipal bond era in South Africa. The locally denominated, six-year transaction of 1 billion rand (approximately US$ 159 million) was viewed as highly attractive for investors, particularly because it was offered at a rate that was 230 basis points over the government benchmark bond, or at a nominal interest rate of 11.95 per cent. This relatively high price, coupled with a sense of national pride at pioneering Africa’s first municipal bond, generated overwhelming demand, and the bond was oversubscribed threefold at primary issuance.(21) The minimum increment size was 1,000,000 rand (or US$ 159,000), signalling an intention on the part of the city for investors to be either institutions or high net worth individuals.

Only two months later, the City issued a second bond, seeking to raise a total of 1 billion rand. To comfort investors that Johannesburg was not taking on an unsustainable amount of debt and to extend the maturity to 12 years, the municipality solicited an aggregate guarantee of 40 per cent (with two matching guarantees of 20 per cent each from the International Finance Corporation [IFC] and the Development Bank of Southern Africa [DBSA]). Due to the credit enhancement, and despite a doubling in the bond’s length, the premium paid by the City over the benchmark treasury curve was reduced to 164 basis points, with a nominal interest rate of 11.9 per cent, again based on prevailing interest rates at the time.(22)

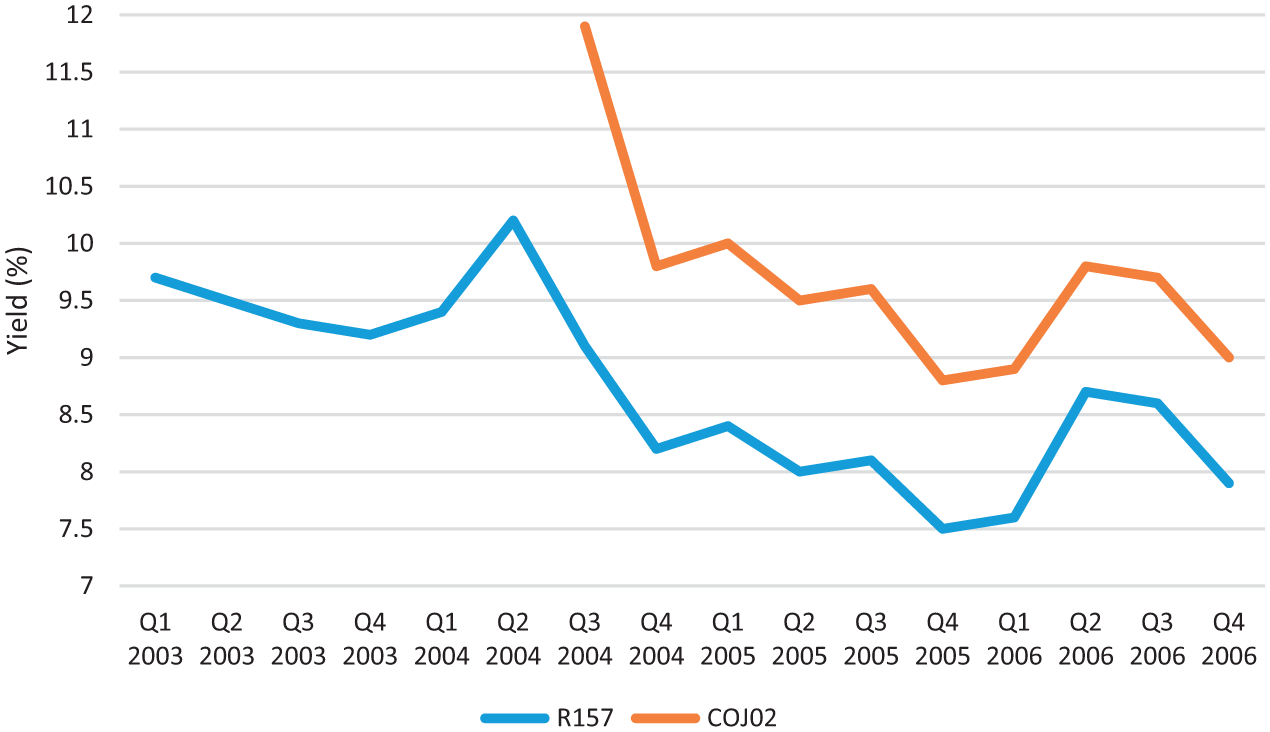

Figure 1 highlights the fact that municipal bonds, particularly those with external guarantees to reduce risk, will often track closely against sovereign bonds when considering yield to maturity. The second bond from the City of Johannesburg was priced at 11.9 per cent at the time of issuance in June 2004, and moved in line with the corollary sovereign government bond expected to mature in 2010. Although this is not always the case, it adds to the argument that municipalities will make to potential investors about the predictability of the performance of municipal bonds in the secondary (post-issuance) market.

Spread between the interest rate on the Johannesburg municipal bond (COJ02) and a South African sovereign bond (R157) with similar maturity rates, 2003–2006

Only 40 per cent of the proceeds of the first two bonds were used to finance the city’s capital expenditure programme. The rest was used to refinance existing, more expensive, debt that Johannesburg had accrued in the late 1990s, when it was experiencing financial distress. The refinancing of the onerous debt arrangements through the bonds is anticipated to have saved the city interest payments of about 20 million rand (approximately US$ 3.25 million, calculated on average amounts per year based on fluctuating interest rates) annually over the six years from bond issuance to maturity (2004–2010).

Investor appetite for municipal bonds issued by cities in South Africa remains strong. In 2011, Francesco Soldi, a Moody’s vice president, noted that “among the factors driving investor interest in bonds issued by large municipalities are strong investment-grade ratings on the South African national scale, their large and diversified budgets, and their above-average management expertise”.(23) Municipalities across South Africa continue to increase the level of sophistication of the financial instruments that they use to access capital for projects that are compatible with their visions for long-term growth. This is evidenced through the City of Johannesburg’s successful completion of a green municipal bond transaction in 2014, which was followed three years later by the City of Cape Town (July 2017).

Case Study 2: Douala, Cameroon

Of the four countries under review in this article, Cameroon demonstrates the lowest level of constitutionally empowered decentralization. The 1972 Constitution creates a highly centralized system where cities are administered not by mayors but instead by political appointees. Part X, on Regional Authorities, indicates that “regional and local authorities … shall have administrative and financial autonomy in the management of regional and local interests”, but that the most senior officers in municipalities shall be “delegates, appointed by the President of the Republic”. These delegates shall “exercise the supervisory authority of the State”.(24) Any funds borrowed by a sub-national government are explicitly guaranteed by the central government and, accordingly, are viewed as financial transactions whose debts accrue to the national, not sub-national, government.

Under the leadership of the central government-appointed delegate, the municipal council recognized that it was well positioned to raise finance in the newly formed stock exchange, particularly with the explicit guarantee of the national government. The city’s financial advisors conducted a cost–benefit analysis to compare the costs of commercial bank financing and a municipal bond issuance, which helped with the ultimate decision. According to the prospectus made available to investors, the city planned to use the funds raised from the bond issuance for road infrastructure, wastewater management, storm drains, solid waste management, and mass transit.

The city and related city corporation had no direct loans, although it received financing in the form of concessionary finance from the World Bank and the French Development Agency, totalling approximately CFA 94 billion, or US$ 128,000,000. These long-term funds were used for infrastructure improvements around the city, particularly around the port.

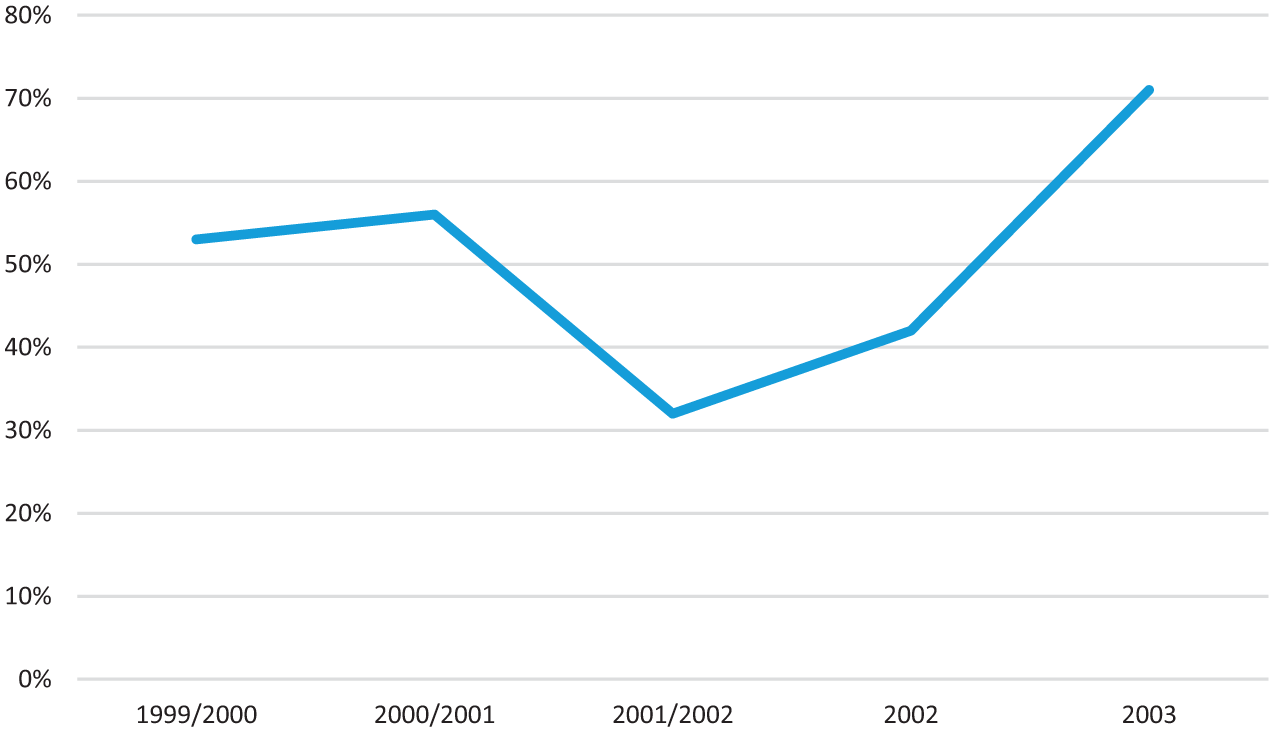

According to its financial statement (which was incorporated into the prospectus), the City of Douala’s total receivables for its most recent audit were CFA 13 billion, or US$ 17.7 million (from fiscal year 2003). During due diligence, investors expressed concern that the actual revenue significantly deviated from the estimated revenue as proposed in the budget by nearly 50 per cent; the budget called for revenues of CFA 23 billion, whereas the actual collections were only CFA 13 billion. This discrepancy underscored system-wide inefficiencies in accurate financial projections and collections, and could be viewed as indicative of a potential eventual inability to meet the debt service obligations called for in the bond agreement. Further, two of the city’s three main sources of revenue – transfers and taxes – that help to cover its operational and investment expenses are derived from the central government. In the years leading up to the bond issuance (from 1999 to 2003), tax revenues collected by agents of the sovereign government and transferred to the city represented – on average – more than 50 per cent of the city’s total revenue, as shown in Figure 2.

Tax revenues transferred from central government, relative to total city revenue, 1999–2003

The city of Douala, the financial capital of Cameroon, issued a five-year bond in 2005 through a special purpose vehicle called CUD Finance (Communauté Urbaine de Douala Finance). This was designed to assist the municipality with raising funds for urban management and development. This CFA 16 billion bond (approximately US$ 22 million) was jointly initiated by the central government and its representation in Douala in an effort to diversify the city’s financial resources. It was fully backed by the central government in accordance with the constitutional constructs of Cameroon’s unitary government. The transaction was unique in that it represented not only the first municipal bond in the region, but also the first issuance at the Douala Stock Exchange since its inauguration in April 2003.(25)

Unlike the bond issuance in Johannesburg, the smallest increment was far more accessible to retail investors; the minimum increment for Douala’s bond transaction was CFA 1,000,000, or US$ 1,400 (compared with Johannesburg’s 1,000,000 rand minimum size, or US$ 159,000). Additionally, the bond issuance was completed in three tranches, which differed in terms of the interest offered. The first tranche was offered with a fixed interest rate, the second with a variable interest rate, and the third without any coupon payments, but with a premium paid at the time of the maturity. This approach allowed the city an opportunity to defer some of the costs of borrowing and helped to make the bond more appealing to a wider pool of investors.

Unfortunately, the city’s bond issuance was plagued with questions of financial and regulatory irregularities that ended in the dismissal and imprisonment of the government’s delegate, Etonde Etoko, within 18 months. Allegations of fraudulent exchanges between tranches and improper licensing of the financial arranger for the transaction were investigated and deliberated in Cameroonian courts for months. Although this did not hamper the city’s ability to honour its debts, and investors received their principal and interest in full and on time, perceptions of illegality have given municipal leaders reason to doubt the likelihood of a follow-on financial transaction.(26)

Case Study 3: Dakar, Senegal

The Senegalese constitution authorizes the creation of sub-national governments within a rigid unitary government system; nearly all of the activities that a sub-national government undertakes, regardless of size of population or budget, are under the strict regulation of the prefect (the Senegalese equivalent to a governor or provincial leader). According to Article 77 of the code governing local governments, a municipality is a “local authority” and a “legal entity governed by public law”. These local authorities have explicit permission, under Law 96-09 of March 1996, to enter into debt arrangements for capital investments with financial institutions that allow cities to achieve their long-term financial goals.(27)

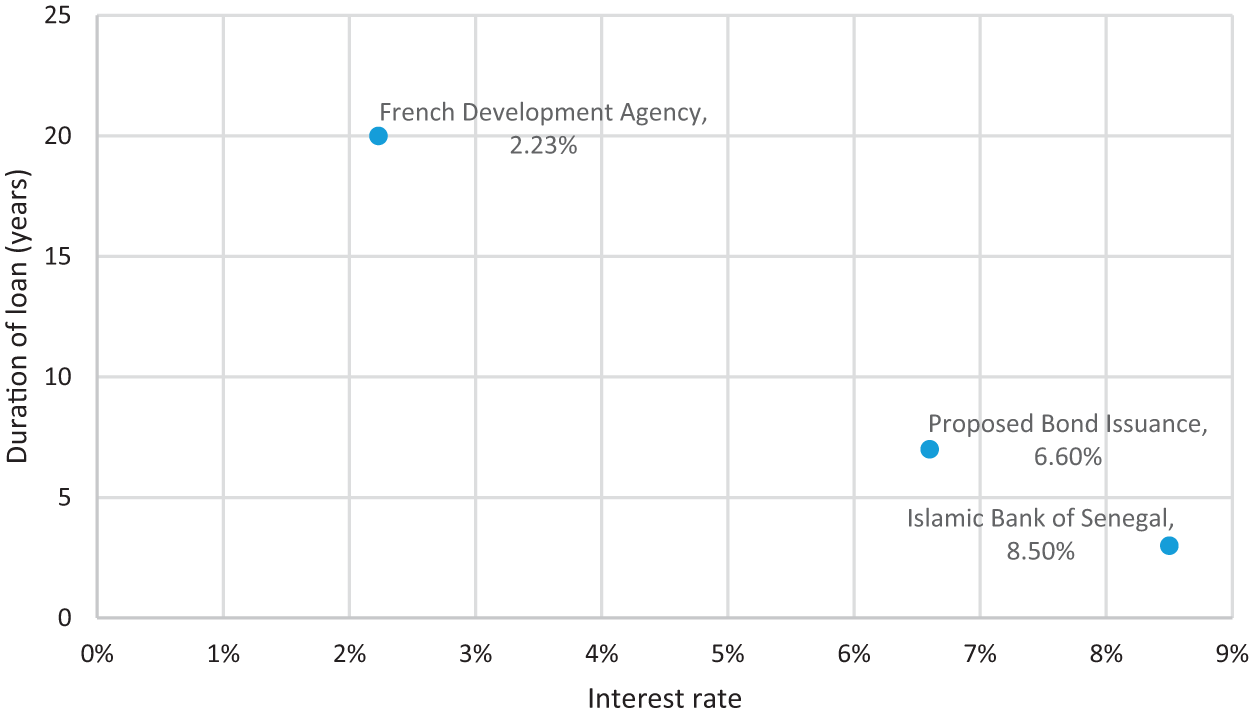

Senegal’s capital city, Dakar, experimented with municipal finance through transactions as early as 2008. As one of his final acts in office, Pape Diop, then mayor of the City of Dakar, signed a loan with the French Development Agency to fund a 10 million euro programme to furnish the city with street lights along well-travelled thoroughfares. This loan was the first of its type from the French Development Agency to a West African capital city without a central government guarantee of repayment. It demonstrated a belief from external lenders that the City of Dakar could be viewed as a creditworthy borrower. This loan was possible without a central government guarantee because language in the constitution granted municipalities across the country the power to enter into long-term debt obligations without central government intervention.(28) Subsequently, the city has borrowed from other concessional lenders (like the West African Development Bank’s loan of FCFA 9.7 billion [approximately US$ 17.56 million] for the rehabilitation of roads) and from commercial banks (like the Islamic Bank of Senegal for FCFA 2.07 billion [approximately US$ 3.74 million] for the installation of traffic lights at the city’s busiest intersections).

Having borrowed successfully from lenders in bilateral transactions and demonstrated its creditworthiness (particularly in its ability to repay a market-rate loan from the Islamic Bank of Senegal), the leadership of the City of Dakar was confident that it would be able to successfully source finance from the debt capital markets for long-term debt. More important, a municipal bond would help to fill the gap between commercial bank lending (which was more expensive and shorter term than a municipal bond) and development finance institution lending (which was more restrictive and did not allow for a single large injection of capital into a project). Specifically, the French Development Agency offered a concessionary-rate loan to the city over 20 years at 2.23 per cent, where new disbursements for an extension of the lighting district would occur only upon the completion of other preliminary sections. In comparison, the Islamic Bank of Senegal’s loan to the city was for three years at 8.5 per cent, and funds were received in full at the time of the signing of the loan covenant for the installation of traffic lights at key intersections across the city. (The proposed bond issuance would have fallen between the two rates, at 6.60 per cent for seven years [Figure 3].)

Municipal finance in Dakar

Because the City of Dakar was successfully borrowing from both development financial institutions at concessionary rates and commercial banks at market rates, with repayments on time and in full as per the loan agreements, it was well poised to demonstrate its readiness to issue a municipal bond.

Building off its demonstration of success in on-time and in-full debt service, the city embarked on a process to launch a municipal bond. This started in late 2011 after a careful review of the constitution and confirmation with expert lawyers and government representatives that a municipal bond issuance was legal and fell under the definition of rights in the legal codes governing the rights of cities. In 2011, the City of Dakar received a US$ 500,000 grant from the Bill & Melinda Gates Foundation to analyze the feasibility of launching a municipal bond. Dakar was uniquely positioned amongst its peer primary cities in the region due to its (i) visionary leadership, (ii) adoption of a strategy to address urban planning, and (iii) past performance as a borrower from external sources.

Dakar and its advisors concluded the time was right, because in 2011, at the start of the bespoke Dakar Municipal Finance Program, Senegal had these capital-positive characteristics:

Unlike many of its neighbors in francophone Africa, Senegal was politically stable, having enjoyed continued peace and smooth transitions of power since independence in 1960.

Senegal’s macroeconomic environment was relatively stable; interest rates were hovering around 3.5 per cent, and over the previous six months, inflation was a low 2.6 per cent to 3.1 per cent.

Domestic demand for bonds was strong, as the central government had issued sovereign bonds on the local market. Since its 1996 founding this bourse, governed by the CREPMF (the Regional Council for Public Savings and Financial Markets), had steadily grown in the size and issuances.

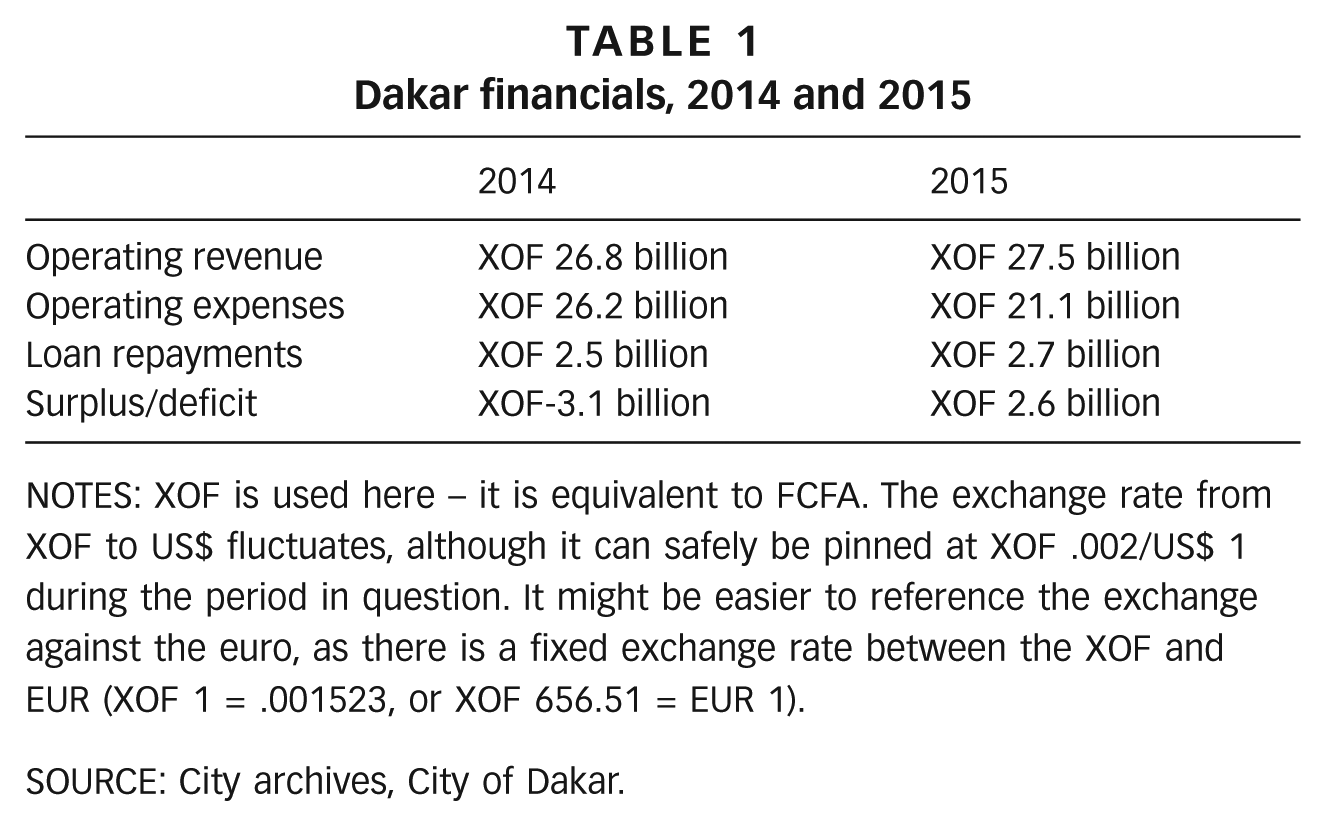

The Bill & Melinda Gates Foundation provided an aggregate grant of US$ 5.5 million (which included the US$ 500,000 for the project feasibility study) for a period from 2011 through 2017. The intended outcome was an “improvement in the quality of life for the urban poor” through the “mobilization of domestic finance through a transaction in the regional capital market”. Throughout the period, the city worked to improve the city’s financial management systems, to alter its approach to comprehensive planning, and to influence investors’ perception of the city’s creditworthiness. Part of this included investor-sounding exercises, through which the city learned that it would be most likely to achieve full capitalization of the transaction with the aid of a credit enhancement (i.e., a guarantee from an external body). After a thorough cost–benefit analysis, the city opted for a 50 per cent principal guarantee from the Development Credit Authority of the United States Agency for International Development. By 2015, the city had successfully completed all regulatory steps required to issue a bond in the Abidjan (Côte d’Ivoire)-based capital markets(29) and built sufficient demand from institutional investors through roadshows and other individual appeals to be confident that the transaction would be a success.(30) Further, the 2015 credit rating, conducted by Bloomfield Credit Ratings (a local ratings agency based in Abidjan), showed increases in revenue, decreases in operating costs, steady repayments of loans, and a net surplus relative to the prior year (Table 1).

Dakar financials, 2014 and 2015

NOTEs: XOF is used here – it is equivalent to FCFA. The exchange rate from XOF to US$ fluctuates, although it can safely be pinned at XOF .002/US$ 1 during the period in question. It might be easier to reference the exchange against the euro, as there is a fixed exchange rate between the XOF and EUR (XOF 1 = .001523, or XOF 656.51 = EUR 1).

SOURCE: City archives, City of Dakar.

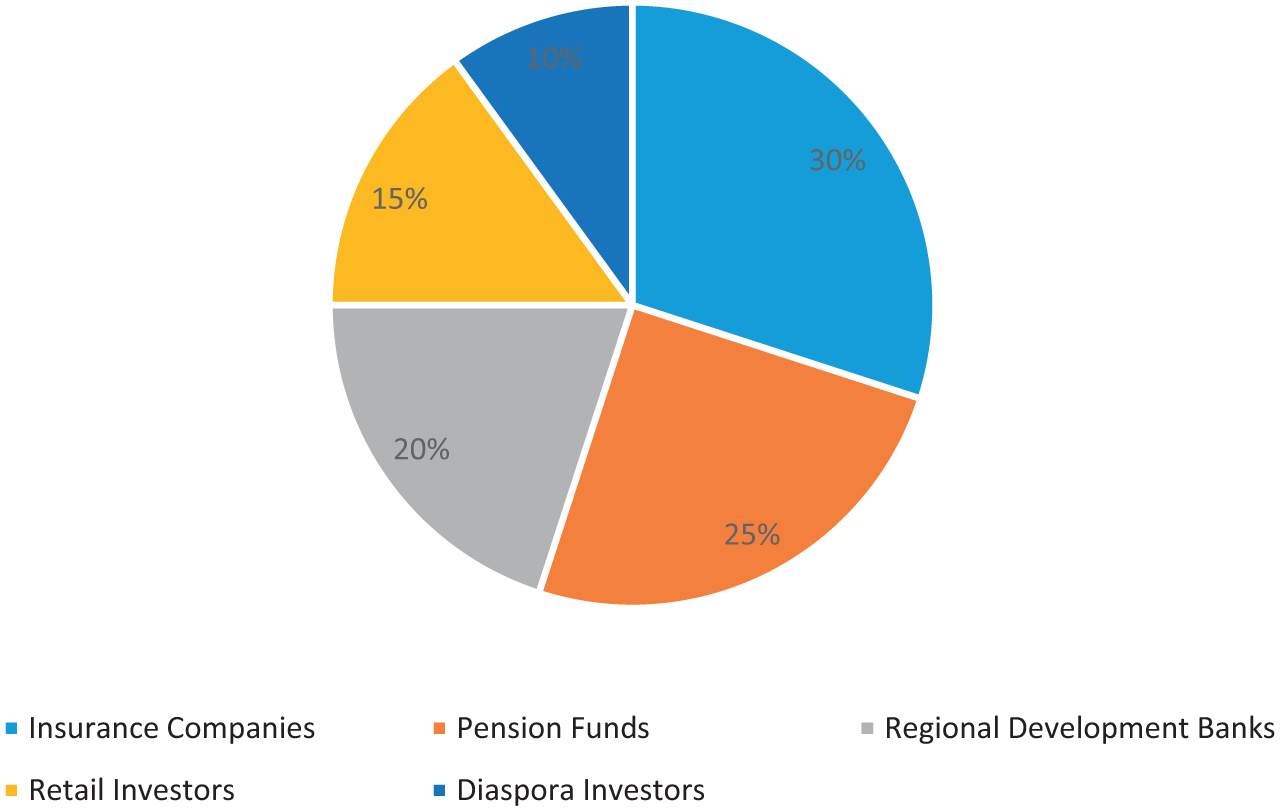

Designed for full accessibility to retail investors, the Dakar bond’s minimum increment was CFA 10,000 (or approximately US$ 18). Large institutional investors had the option, however, of placing a large order at the time of subscription. This asset class, based on these investors’ pledges to purchase (also known as soft orders), made up approximately 72 per cent of the total demand for the transaction on the eve of issuance (Figure 4).(31)

Expected distribution of Dakar’s municipal bonds in the primary issuance

According to the filing with the local market regulator (the CREPMF), the city planned to use the funds raised from the bond issuance for the installation of a new marketplace, with stalls and kiosks offered for rent at subsidized rates to offer a wider range of opportunities to the city’s many street vendors. Approximately 25 per cent of the funds would be spent on the acquisition of the centrally located parcel of land (already demonstrated to be under contract to the city), with the remaining 75 per cent for the design and construction of the physical marketplace. Written confirmation of non-objection to this proposed transaction from the government ministry handling local governments, coupled with a careful reading of the constitution, made the municipality confident that its efforts, and those of its supporters, would result in a transaction.

Unfortunately, the City of Dakar ultimately did not launch its bond in 2014 as originally planned, due to a last-minute intervention by the central government. This unexpected challenge, based first on questions of constitutionality and later amended to reflect concerns about the impact on the country’s overall level of indebtedness, prompted the city to file a lawsuit against the central government. Although unsuccessful in overturning the central government’s opposition to the bond issuance, it has left the door open for future attempts to introduce municipal bonds in Senegal.(32)

Case Study 4: Kampala, Uganda

Similar to other anglophone countries, the Ugandan constitution sets out clear and well-defined responsibilities for sub-national governments. To further empower the capital city of Kampala in line with a broader municipal development plan, the government passed legislation in 2010 to designate the Kampala Capital City Authority (KCCA) as a government agency that reports directly to the Office of the President (through the Kampala Capital City Act). Through this change in Kampala’s accountability, with more oversight by national leadership, the city’s level of decision-making is now less driven by its electorate than other cities in Uganda.(33)

Section 54 of the Act specifically provides KCCA with specific borrowing powers, stating that “the Authority may, from time to time, with the approval of the Minister, raise loans from financial institutions, by way of debenture, issue of bonds or any other method, in amounts not exceeding ten percent of the locally-generated revenue of the Authority; provided that the Authority demonstrates ability to meet its statutory obligations”. Curiously, and frustratingly for KCCA, less financially restrictive legislation exists for all local governments in Uganda. These are allowed to borrow and to issue bonds in Ugandan shillings subject to the rules under Section 20 of the Local Government Act of 1997, and with the approval of the Ministry of Local Government and Capital Market Authority. Borrowing is allowed by law, but confined to a maximum of 25 per cent of own-source revenues.(34) The 1995 Constitution further commits, in Section 197, that “urban authorities shall have autonomy over their financial and planning matters”.(35)

The leadership at KCCA carefully reviewed options for financing long-term debt and ultimately settled on a municipal bond because of the relative length of the repayment period between bonds and loans. With a longer period, the city would be able to better manage its financial needs and potentially structure in a grace period (similar to that incorporated into the City of Dakar’s proposed issuance).

Of the municipalities or municipal corporations considered in this article, KCCA is the only one that has no self-initiated debt. Since its establishment, KCCA has not borrowed from any entity, although its accounts show a loan inherited from its successor – the City of Kampala. This loan, originated in 1991 for an infrastructure project completed in 2000, was a portion of a larger transaction between the Republic of Uganda and the World Bank. Although the national government has repaid the World Bank in full for the transaction, the loan between the national and sub-national governments has not been satisfied. Some investors are concerned about this non-existent credit history for KCCA (and weak credit history for Kampala), as it fails to demonstrate the likelihood or predictability of on-time payments from KCCA as an issuer in the capital markets.

Although the city is optimistic about its ability to raise funds from investors through a bond payment, the constitutional questions on debt limits raised earlier in this article significantly constrain the potential for a successful issuance. To reiterate, current legislation restricts the amount of debt that KCCA can assume to 10 per cent of internally generated revenue on an annual basis. Therefore, despite the strong growth in internally generated revenue from the inception of KCCA in 2012, a municipal bond of US$ 2.4 million (or 10 per cent of the US$ 24 million raised in 2015) is unlikely to be viewed as attractive to the municipality, due to the high fixed transaction costs to issue a bond relative to the fees associated with the origination of a bank loan.

Because the city has not formally progressed on initiating the transaction, due to the constitutional debt limits, there is limited information on the way that proceeds would be used. In an October 2014 interview with the Daily Monitor, the Ugandan Capital Markets Authority’s spokesperson indicated that he understood that the city planned to “issue a municipal bond to finance infrastructure in the city”.(36) The African Securities Exchange Association similarly reported that KCCA planned “to issue the country’s first municipal bond by June 2015 to finance the infrastructure development needed to change Kampala into a modern commercial hub”.(37)

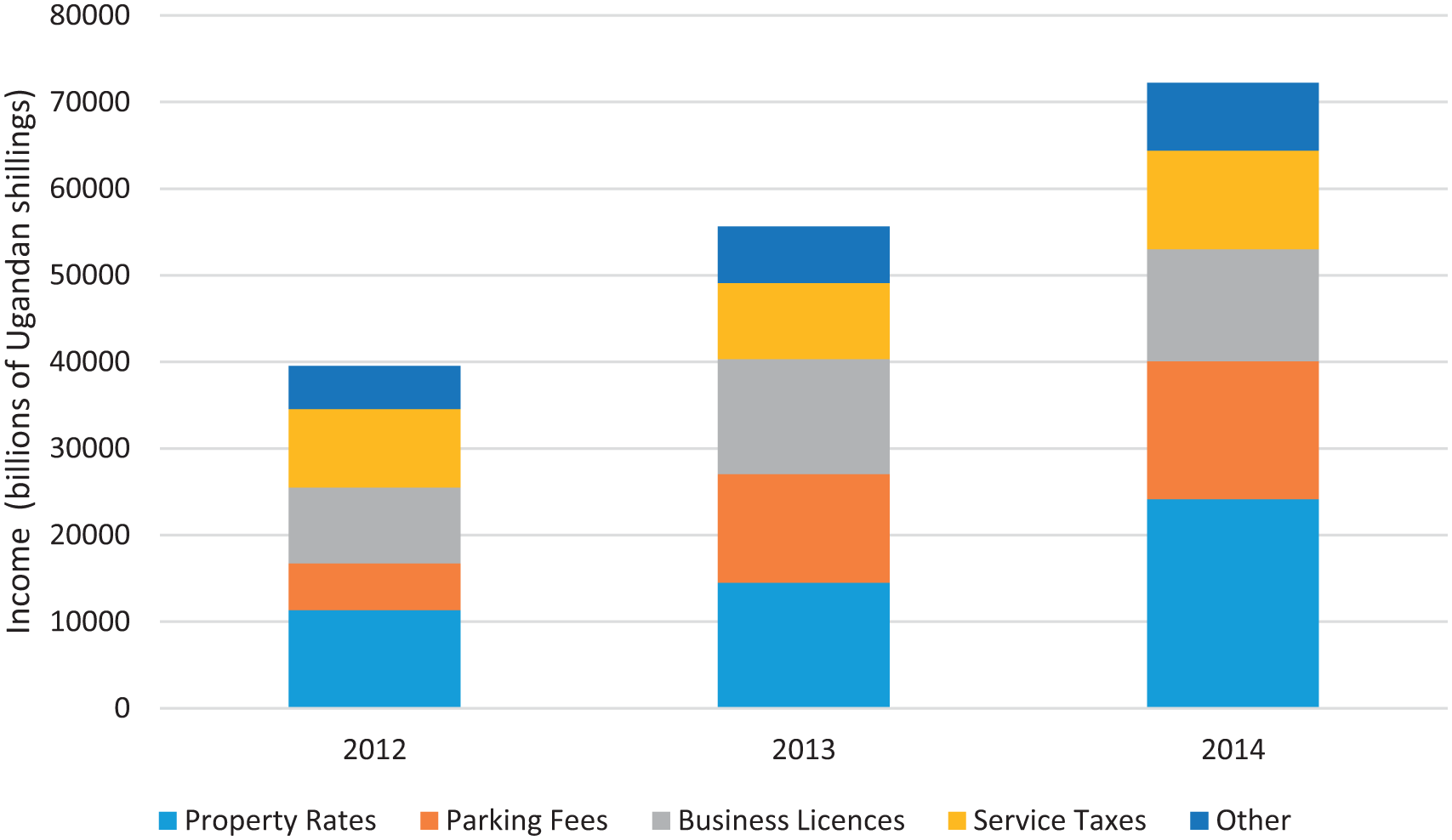

In 2012, the Republic of Uganda passed legislation that created the Kampala Capital City Authority (KCCA), a new political entity established to supersede the City of Kampala and with responsibility for delivering urban services throughout the capital. Recognizing the centrality of predictable revenues and collection efficiency, KCCA immediately designed, validated and implemented a plan to overhaul the existing system of tax collection. Although there was initial resistance from some of the delinquent taxpayers, revenues have steadily increased from 30 billion Ugandan shillings (US$ 9 million) during the 2010–11 fiscal year to 81 billion Ugandan shillings (US$ 24 million) in 2015–2016. This growth of 89 per cent after inflation, in just five years, is largely attributed to the financial success of KCCA.(38) Internally generated revenues over the period from 2012 to 2014 have grown dramatically, from 39,523 million Ugandan shillings in 2012 to 72,222 million Ugandan shillings in 2014 (Figure 5).

Sources of income for Kampala Capital City Authority, 2012–2014

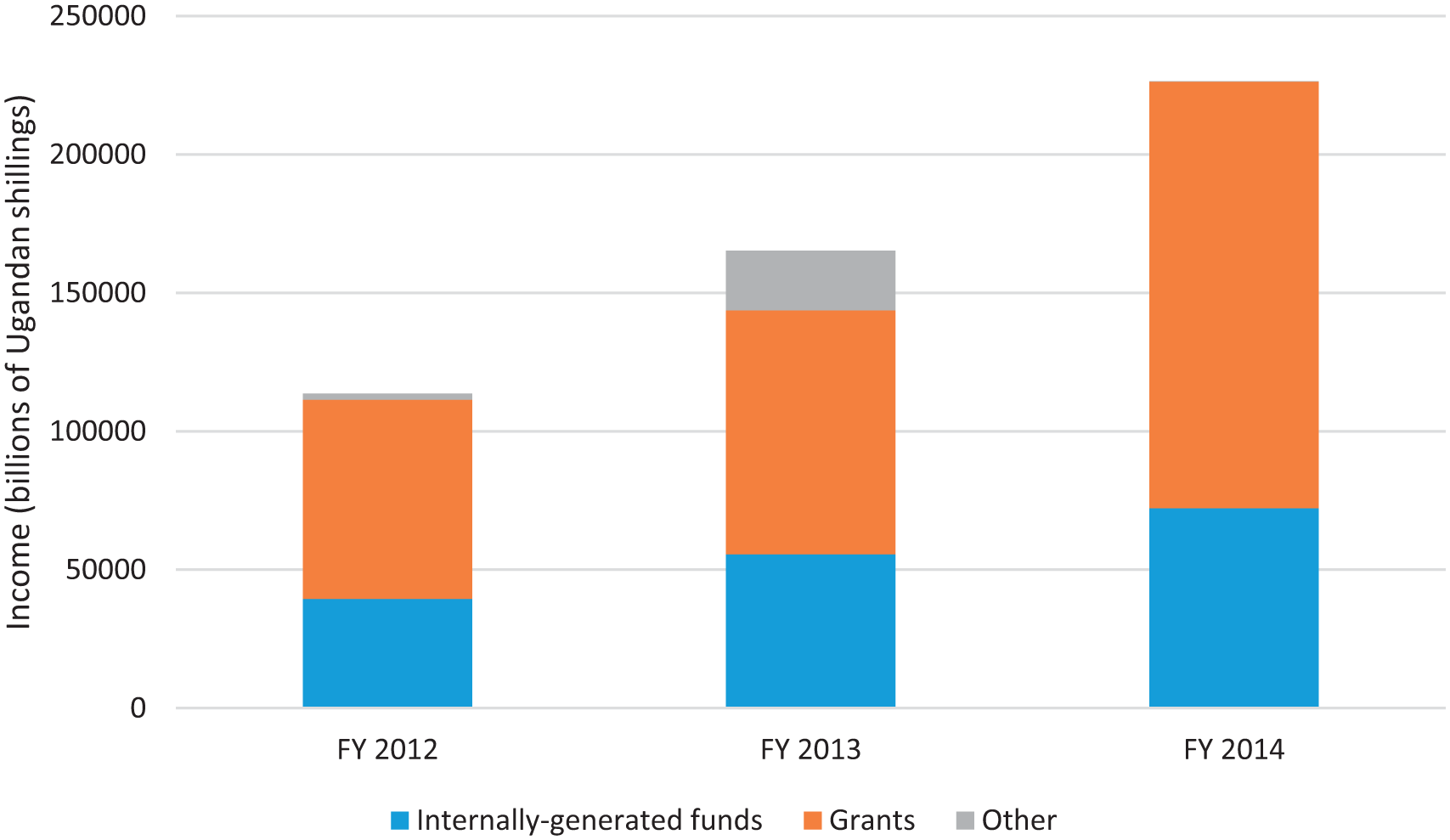

KCCA’s leadership recognized that the percentage of total income coming from grants (averaging around 62 per cent per annum from 2012 through 2014 – Figure 6) was unsustainable, and that a new source of funding would be required to meet long-term capital investment needs. KCCA has been working steadily towards a bond issuance, with the knowledge that it cannot ultimately proceed without a constitutional amendment that allows Kampala to borrow more than is currently permitted. Further, Stephen Kaboyo, a financial sector analyst in Kampala, warned in 2014 that there may be a “challenge for KCCA in making a good case that they are in good financial condition and that they have a reliable surplus of revenues over expenditures that can be used to make interest and principal payments”.(39)

Total income for Kampala Capital City Authority, 2012–2014

V. Conclusions and Recommendations: The Future of Municipal Bonds in Sub-Saharan Africa

The short-term outlook for municipal bonds in sub-Saharan Africa will remain fairly bleak without a significant change in the institutional enabling environment for municipalities. To date, the only African cities that have achieved success in the municipal bond market are in countries whose constitutions provide full autonomy for sub-national governments (as in South Africa), or those that assume an extremely paternalistic view (as in Cameroon). In South Africa, the cities of Johannesburg (2014, for 1 billion rand) and Cape Town (2017, for 1.5 billion rand) have brought green municipal bonds to market. However, elsewhere in sub-Saharan Africa, without a commitment in practice to match the rhetoric of decentralization, municipal bonds are still an ambition, not a reality.

This article argues that municipal bonds could be a significant tool to meet the long-term capital requirements of sub-Saharan African cities. These case studies demonstrate that the domestic financial sector will consider municipal investments where there is evidence that sub-national governments can be reliable sources of repayable debt in domestic currency at regular intervals and with a predictable interest rate. For investors like insurance companies and pension funds, which likewise have the ability to forecast their financial requirements, this is a critically important consideration to factor into decision-making. The primary constraint to the issuance of municipal bonds in sub-Saharan Africa is therefore not necessarily investor appetite.

However, successful issuance of municipal bond issuance is contingent on strong and supportive interlinkages between central and sub-national governments. These case studies suggest that municipal bond issuance in sub-Saharan Africa is stymied by the wider regulatory and political environment. This paper offers a critical review of the explicit and implicit powers granted to local governments under the constitutions of four exemplar countries, focusing on the legislation that enables or prohibits municipalities from issuing bonds.

The replicability and scalability of transactions by some cities (like Johannesburg and, subsequently, its peers across South Africa) are in large part due to the transparency, accountability and efficiency of the institutionalized democratic systems. By comparison, the inability of other cities (like Douala) to repeat their inaugural bond issuance shows the challenges of tapping into capital markets in non-transparent systems. It further underscores the need to establish enabling legislation in constitutional systems that are found between those of South Africa and Cameroon – such as Senegal and Uganda – to responsibly encourage the development of municipal finance systems in a way that will lead to the ultimate success of bond issuance for cities across sub-Saharan Africa. Reform to existing regulatory and legal environments across sub-Saharan Africa, governing a financially sustainable level of indebtedness for sub-sovereign governments, is an essential step in ensuring the quality and improved livelihoods of all stakeholders impacted by the future growth of the region’s cities.