Abstract

Individuals’ need for extended working lives depends on the design of pension systems, including occupational pensions. This article examines variation in occupational pension generosity and coverage in Norway’s private sector. The analysis consists of microsimulations of future pension outcomes for cohorts born in 1953, 1963, 1973 and 1983. The first set of calculations estimate average pension levels for individuals with different pension packages who retire at 67; the second, how much longer workers in different cohorts will have to work in order to obtain a replacement rate of 70%. The overall finding is that while all workers in Norway must extend working life in the future, those with the most generous occupational pensions can retire about four years earlier than those with the least generous packages. This shows that the design and regulation of occupational pensions are crucial to the debate on extended working lives.

Introduction

Across Europe, pension systems are being reformed. Two broad trends are visible: first, architects of pension systems wish to encourage longer working careers; second, multi-pillar systems are promoted at the expense of traditional state pension systems (European Commission, 2018; OECD, 2019). The latter implies that occupational pensions, typically in the form of voluntary, contractual or even mandatory saving schemes organised by employers, play a more important role in the overall pension system. The two trends taken together challenge both established notions of retirement’s position in the life course (Kohli, 2007; Radl, 2012) and the traditional public–private mix in pension provision (Ebbinghaus and Gronwald, 2011). Both trends must also be assumed to affect men and women differently. Still, there is little academic discussion about the intersections between those two main trends and their implications in terms of gender. The literature on extended working lives (EWL) (e.g. Ni Léime et al., 2017; Taylor et al., 2016) and the literature on occupational pensions and the new pension mix (e.g. Natali, 2017; Pedersen et al., 2018) are both blooming, but they rarely talk to each other.

The aim of this article is to show, through an empirical study of one country, how occupational pensions shape retirement opportunities and work incentives for older male and female workers. The analysis will show how occupational schemes and the reformed public pension scheme interact to create new inequalities and complex incentives structures that sometimes deepen, and sometimes cut across, existing cleavages in the labour market. A series of microsimulations indicate how different pension packages will shape opportunities and outcomes in later life for different cohorts of men and women. The empirical question to be addressed, then, is: What does the transition towards individualised pension savings schemes mean for the retirement options and work incentives faced by older workers, and how, if at all, does this vary by gender? The empirical findings are discussed in terms of insights from the extended working lives-literature, where our main concern is: how realistic is it that workers will be able to act on the new incentives in the future?

The Norwegian case is relevant beyond its borders because the Norwegian system contains many mechanisms that are familiar across Europe. The public pension system that was established in the 2011 pension reform relies on Notional Defined Contributions (NDC), similar to Sweden and Italy. Occupational pensions are statutory, as in the UK, and part of the occupational pension system is subjected to collective bargaining, as in Sweden, Denmark and the Netherlands. Also, the retrenchment of the public pension and the corresponding call for better occupational pensions will be familiar in many countries. At the same time, Norway has some unique features that supposedly facilitate the success of the new pension principles. This includes comparatively well-regulated labour markets with relatively few precarious workers (Rasmussen et al., 2019) and high employment rates among women and older workers (aged 55–64; see Eurostat, 2020). Also, Norway is a Scandinavian country with an inclusive welfare state and ambitious policies to promote female employment (Pedersen and Kuhnle, 2017). Against this background it can plausibly be argued that if a state NDC system supported by mandatory occupational pensions does not produce sufficient incomes for future pensioners in Norway, it is not likely to do so anywhere else either. Or, to paraphrase Frank Sinatra: If you can’t make it here, you won’t make it anywhere.

A more pragmatic reason to select Norway as a case is access to data. Norway is in a rare position in that it allows access to register data on lifetime incomes that can be combined with data on company occupational programmes and collective pension agreements. One unique contribution of this study is that it does not analyse existing distributions, but estimates future pension outcomes for cohorts who have an active working career.

The next section elaborates on how occupational pensions matter for the debate on extended working lives. It is emphasised that such schemes create complex incentives structures for employers and employees, introduce elements of chance and hence increase the unpredictability of future outcomes, and potentially create rigidities that constrain workers’ choices. Next, the Norwegian case is presented, followed by a presentation of the datasets. In the analysis, the emphasis is on coverage rates of various schemes, future pension outcomes for men and women, and projections of how much workers must extend their working lives in order to obtain pension levels similar to those provided in the pre-reform system. The article ends with a discussion of the risks facing future workers, in the light of our findings here and insights from the extended working lives literature.

Occupational pensions and older workers’ employment: Two distinct research areas

As both the European Commission (2018: 99–107) and the OECD (2019: 9) have noted, recent and ongoing pensions reforms in Europe aim to extend working careers, and to reinforce occupational pension plans. Individuals who aim for a pension with a given replacement rate can thus do one out of two things: extend their career until they reach this level, or make sure they have an occupational pension that provides the desired replacement rate at the time when they wish to retire. The problem with both routes, obviously, is that there are a number of factors beyond individual control that influence both the ability to prolong working life and access to an occupational pension. The extended working lives-literature has engaged extensively with the former challenge – unequal ability to work longer (e.g. Wainwright et al., 2019) – but has less to say about inequalities in occupational pension coverage and how this influences the need to work longer. Studies have shown that workers with access to an occupational pension retire earlier (Hofäcker and Naumann, 2015; Midtsundstad, 2002), thus the design and coverage of occupational schemes are clearly relevant for the debate on extended working lives.

Studies of early retirement behaviour have identified a number of factors that may act as barriers to prolonged working lives. In a recent meta-analysis, Topa et al. (2018) find that workplace timing of retirement, organisational pressures, financial security and poor mental or physical health are the strongest predictors for early retirement (see also Fisher et al., 2016). These are factors workers themselves have limited control over. A number of studies have focused in particular on the negative stereotyping of older workers as an exclusionary mechanism. Older workers are assumed to be less flexible and less interested in new technologies (Solem, 2016), less competent and able to perform (Posthuma and Campion, 2007), and less ambitious (Carlsson and Eriksson, 2019) (for a review, see Harris et al., 2018). Different groups of workers are differently affected by the relevant factors; for instance, poor physical health is a stronger determinant for retirement among workers in physical jobs than for those in seated jobs (Andersen et al., 2020).

Negative stereotyping may imply reduced demand for older workers, and thus act as a barrier towards an extended working life. The EWL-literature however mainly overlooks that the design of occupational pensions can also be a barrier: some occupational schemes incur higher costs for older than for younger workers, making older workers more expensive. When occupational pensions are designed in this way, they will act as a direct financial disincentive to recruit and retain older workers, and may thus hinder extended working lives.

Gender scholars point out that the ideals of extended working lives may hold more challenges for women than for men, as gender intersects with age in ways that may make it harder for women to prolong working careers (Carlsson and Eriksson, 2019; Duncan and Loretto, 2004; Jyrkinen and McKie, 2012). Women workers also have caring obligations over the life course, and may be barred from extending their working lives by the need to care for ageing family members (Street, 2017).

Some groups may thus be less able than others to extend their working careers. Given our interest in occupational pensions, it must be asked if these – women, workers in physical jobs – are also the groups who most need to extend their careers due to a lack of occupational pension. The answer to this question is complex. Occupational pensions introduce an element of chance to employment relations (see Meyer and Bridgen, 2008) that cuts across conventional fault lines. Occupational pensions are more widespread, and typically more generous, in some parts of the labour market than in others, but – as Meyer and Bridgen (2008) convincingly show – there are strong elements of randomness. A mechanic who works for a major car manufacturer will be covered by a generous occupational pension; a mechanic who works for a typical car component supplier will not be covered at all. Highly skilled workers in small firms may not be covered, while unskilled workers in traditional industries are. Occupational pensions thus introduce new inequalities in the labour market that the extended working lives-literature typically does not address.

A third reason why occupational pensions are relevant to the debate on extended working lives is that this literature has increasingly turned to issues of flexibility, ‘job crafting’ (Tims et al., 2013) and bridge employment (Wang et al., 2008) in late careers. Retirement can no longer be seen as a clear-cut decision, but can be a process that takes years, and includes downscaling, part-time work, or self-employment (Furunes et al., 2015; Vickerstaff and Cox, 2005). At the same time, occupational pension schemes can create rigidities which put workers at risk if they downscale or change jobs. Scholars who study non-standard employment in late careers should acknowledge an occupational pension as a potential institutional barrier to such adjustments.

To sum up, occupational pensions shape opportunities and risks for workers approaching retirement in three potential ways: by creating incentives structures for employers and employees that are not necessarily in sync, by establishing inequalities that cut across class, skill and gender lines, and by limiting flexibility. To some extent they are ‘wild cards’ in the institutions that promote, or hinder, extended working careers (Meyer and Bridgen, 2008).

The European trend with retrenchment of state pensions and increased emphasis on occupational pensions also has implications for the debate on pension adequacy (European Commission, 2018). Mechanisms for risk sharing and redistribution, that are common in state schemes, are less likely to be found in occupational pensions. Most occupational pensions are mere savings schemes. Several studies have warned that a move towards occupational pensions – at the expense of broad, inclusive state pensions – will be particularly bad news for women (e.g. Frericks et al., 2009; Ginn and Arber, 1993). State pension schemes often contain universal minimum pensions, pension accrual for care work (Frericks et al., 2009; Ginn and MacIntyre, 2013; Halvorsen and Pedersen, 2019) and/or mechanisms for sharing of pension accrual between husbands and wives in the event of divorce. Such elements are much less likely to exist in occupational pensions, where accrual typically follows from labour market participation alone. Besides, many occupational pension schemes exclude employees who have only worked in the enterprise for a short period, and/or had very low incomes. This is likely to be to the disadvantage of women, who are more likely to have punctuated careers (Ginn and Arber, 1993).

Occupational pensions thus matter both for the incentives structures and opportunities facing older workers, and for the distributive outcomes after retirement. This study presents an empirical study of how this plays out in one country. The analysis will show that the need to extend working lives varies, depending on what pension package one has. This observation is linked to the ongoing debate about varying ability to work longer.

The pension system in Norway

The pension system in Norway was reformed in the early 2000s (Grødem and Hippe, 2018, 2019), and the main gist of the reforms was to alter the core logic of the system from defined benefit (DB) to defined contributions (DC). Put simply, DC schemes imply that each insured person ‘saves’ a given amount of his or her income for each contributing year, and that future pensions depend on the size of the notional savings account. In DB schemes, the pension provider guarantees a given benefit level, typically expressed as a replacement rate for previous incomes. In occupational DB schemes, employers save more for female employees to compensate for their prospective longer lives. In DC schemes, they do not. DC schemes allow for much better cost control than DB schemes, but they also typically imply that there is little or no risk sharing.

Before 2011, the retirement age in the Norwegian National Insurance (NI) was 67 years, and full-time workers with average incomes and a 40-year contribution record would receive a net replacement rate at about 66% (NOU 2004:1, 2004). In the new Norwegian pension system, there is no guarantee of a given replacement rate. Indeed, 18.1% of a worker’s annual income – up to a cap at about 1.5 times the average annual income – is credited to the notional pension account, and the pension level depends on the size of this account when the worker retires. Simultaneously, the old concept of a fixed retirement age is replaced with flexible retirement on actuarially neutral terms. When a person retires, their annual pension is determined by the size of their notional savings account (pension wealth) and the number of years they are expected to live past retirement (the longevity adjustment). Employees can start drawing pension at any time between ages 62 and 75, but the earlier one starts drawing benefits, the lower the annual pension will be. This is the principle of actuarial neutrality, which implies that flexible retirement on actuarially neutral terms can be seen as a functional equivalent to raising the statutory retirement age. The new principles were phased in over time, and the first cohort that will have their pensions calculated fully by the new principles is the 1963 cohort (for more details on the pension reform, see Christensen et al., 2012).

Since 2006, all private firms have been obligated to establish an occupational pension scheme on top of the state system. The mandatory minimum requirement is that employers set aside 2% of each employee’s wage above a minimum level as per annum savings. Generosity varies from this minimum of 2% up to voluntary employer yearly savings rates of 7%. In addition, a top-up can be made for incomes above 1.5 times average to compensate for the lack of accrual in the NI system. Practically all the new occupational pension schemes in the private sector are pure DC savings schemes, and offer payment for a period of 10 years, or at least until the claimant turns 77 years. Most of the former traditional DB schemes in the private sector have been closed for new entries and transformed into DC schemes (Hippe et al., 2018). It should be emphasised that in order to qualify for the favourable tax treatment of occupational schemes, the scheme must cover all employees within the firm (i.e. savings rates in a DC scheme must be the same for all). If men and women are differently covered, then this is because they work in different enterprises or businesses, not because they are treated unequally within the workplace.

An additional occupational pension, known as AFP (AvtaleFestet Pensjon, contractual pension), exists at the sector level. This covers all companies that are covered by collective agreements. Unlike the firm-based occupational schemes, AFP is negotiated nationally. Since 2008, it has been based on savings (calculations) of around 4% of annual wages. Like the state NI pension, it will be paid on actuarially neutral terms, implying that early take-up translates into lower annual rates.

A crucial difference between the firm-based schemes and AFP is that the former are treated as savings that individuals ‘own’, that will not be reduced or lost as a result of job transitions, while AFP is a pension an employee must qualify for at the time of retirement. In order to be eligible for AFP in the private sector, the employee must be with an employer that is covered when they turn 62, and they must have worked in a covered firm for at least seven out of the last nine years. AFP, in other words, is a benefit that can easily be lost, even if one has contributed to the scheme (‘saved’) throughout the working career – and this can happen for reasons beyond individual control, such as health problems or plant downsizing (Hippe et al., 2017). This is a prime example of how design of pension schemes can create rigidities, as well as risk and insecurities, for older workers. 1

The implications of the differences in coverage can be illustrated by the corresponding variation in yearly accumulation of pension wealth. The annual savings rate in the NI is 18.1% up to a ceiling. Total annual accumulation for low-to-medium earners with the lowest occupational pension and no coverage of AFP will be about 20.1% (18.1% + 2% in occupational pension savings). By comparison, a low-to-medium earner covered by AFP and a generous occupational pension scheme will save 18.1% in the NI, about 4% AFP, and 5–7% in occupational pensions – that is, 27–29% savings per year. Many occupational pension schemes offer higher savings rates for incomes above certain thresholds, implying that the real savings rate can be above 30% for high-income earners.

The average actual retirement age in Norway, for those who were in employment at age 50, was 65.7 years in 2018 (Bjørnstad, 2019). This was an increase of 0.6 years since 2009. There has thus been an increase since the new pension system took effect in 2011, but the average retirement age remains below the previous pensioning age at 67 years.

Because all years of pension accrual count equally in the new system, many analysts feared that the pension reform would be detrimental to women. The new NI system, however, contains several elements that work to women’s advantage (Halvorsen and Pedersen, 2019). Pension accrual is awarded for care work. The cap on accrual for incomes above 1.5 times average annual incomes in effect promotes gender equality in outcomes, since far more men than women have incomes above this level (Halvorsen and Pedersen, 2019). Also, Halvorsen and Pedersen (2019) highlight the gender-neutral tables for calculations of life expectancy as the one element that contributes most to closing the (baseline) pension gap between men and women. This is an important observation, as more countries link individual benefit levels to overall expenditures (OECD, 2019: 25): If these mechanisms adjust for women’s longer life expectancy by paying women lower annual pensions, pension levels for women will undoubtedly be reduced (see Frericks et al., 2009: 713).

In what follows, three indicators of pension outcomes are shown. First, as a point of departure, coverage rates for the different programmes are presented. This is the traditional indicator in studies of occupational welfare. The second indicator is future replacement rates, measured as average lifelong pension wealth relative to average life income. A third set of calculations analyse the need to extend working lives to reach a certain replacement level, to measure how changes in the public–private mix and programme design affect incentives. This is done with particular attention to gender.

Data and analytical strategy

Our calculations are based on three datasets. The first is a set of individual income data covering the entire population in Norway born in 1990 or earlier. These data are based on tax income records and cover all income from work, as well as information about employment. These income data cover registered income over the life course for all residents in Norway in 2013, back to when the person was 17 years old, as well as a model estimating income until retirement (the TRIM model). The dataset has been made available by the Norwegian Labour and Welfare Administration (NAV). The income prognoses calculated in the TRIM model are also used by the social security administration. The model estimates future income from the actual behaviour of earlier cohorts.

The dataset also includes the organisation number for all employers, which made it possible to link the individual income data to detailed information about their employers’ occupational pensions. This was done by using public accounting data for private sector companies showing their pension expenditures as formally reported. Data were built by using the pension expenditure level relative to wage expenses in each firm, as well as balance sheet reports on DB schemes, to assess the nature and the savings level in the occupational schemes. This offered a good indicator on both the nature of the company pension scheme and the level of pension savings.

The third dataset contains information from the occupational AFP administration on individual company AFP coverage. The dataset currently covers the period from 2008 to the present (i.e. from the introduction of the new private sector AFP scheme), and includes all companies registered as paying members of the AFP scheme. Since benefits are calculated in the same way for all members, precise estimates for future pensions can be made.

Actuarial methods are needed in order to make estimates for future pensions that take both the state programme and negotiated schemes, as well as all individual company-based occupational schemes for each individual, into account. The analyses have been done in cooperation with actuaries in the company Lillevold & Partners, who are also the official actuaries for the AFP scheme.

The combined dataset allows for estimations of future pensions for all age groups, but to simplify the presentation only four cohorts are selected for this analysis: 1953, 1963, 1973 and 1983. As noted, the 1963 cohort is the first cohort to have their pensions calculated fully by the post-reform rules. Those born in 1953 are fully covered by the pre-reform system. Comparing the 1953 age group with those born in 1963 and later offers an opportunity to see the effect of the pension reform over time. The two younger cohorts will have all their benefits calculated according to new NI and AFP rules, and those who have worked in the private sector have been covered for most of their working lives by the mandatory (2006) occupational DC pensions. Including also younger cohorts, allows us to see how the new pension mix plays out as the system matures.

In the analysis, some technical choices had to be made. First, in order to address our research questions as adequately as possible, the ‘pension wealth’ in DC schemes (which is paid for a maximum of 10 years) is recalculated at the point of retirement into lifelong benefits, to allow for comparison with other elements in the pension package. Second, replacement rates are always calculated in relation to average lifetime earnings, not final wages. Third, in the calculations of replacement rates, those with the lowest lifetime incomes are excluded. Persons with lifetime incomes below our threshold will, in the vast majority of cases, only receive the guaranteed (minimum) pension from the NI.

In the calculations that follow, retirement age at 67 is used as a main parameter, even though the retirement age in the new system is flexible. This choice is made simply because many people still consider 67 years as a reasonable age to exit the labour market; thus, this serves as a familiar point of reference (see Radl, 2012, on the pervasiveness of age norms). Age 67 is a somewhat higher retirement age than the currently observed retirement age, which means that the new system is tested under the most favourable conditions: assuming continuation of the current trend towards longer working careers. Technically, those who were estimated to exit before 67 years have been assigned the same income at 67 as they had at 62.

The other main parameter used is a 70% replacement rate for lifetime incomes. This level is chosen because trade unions typically have looked at two-thirds of previous income as the standard ambition in their pension policy (Pedersen et al., 2018). Moreover, historically, this is a replacement rate found in the DB occupational systems for all public employees, as well as for many private sector workers in Norway. Therefore, the 70% replacement rate can be seen as an established reference point when calculating a future pension level that would allow employees to choose to retire.

There are some weaknesses in the data. Estimating future income from the actual behaviour of earlier age cohorts, as the TRIM model does, is problematic given the rapid ongoing changes in modern labour markets. The aim is, however, not to predict changes in future retirement behaviour, but to analyse the incentives structure inherent in the new pension system. For that purpose, the TRIM model specifications suffice. Second, the datasets do not contain information on all occupational schemes that a person has been a member of during her or his working career. The analysis is therefore based on the assumption that the current membership provides a correct picture also of the historical and future memberships. This is obviously simplification since there will be mobility in and out of the programmes.

Coverage and replacement rates in private schemes: Who gets enough to retire?

To reduce complexity, and to make this discussion relevant beyond Norway, analyses are restricted to the private sector. It should, however, be noted that in the dataset, 54% of women and 22% of men were covered by public sector occupational pension programmes, which reflected the segregation of the labour market in 2013. These programmes are broad, lifelong and include risk sharing, which means that the large group of women who work in the public sector are fairly well-protected in Norway (Hippe et al., 2018).

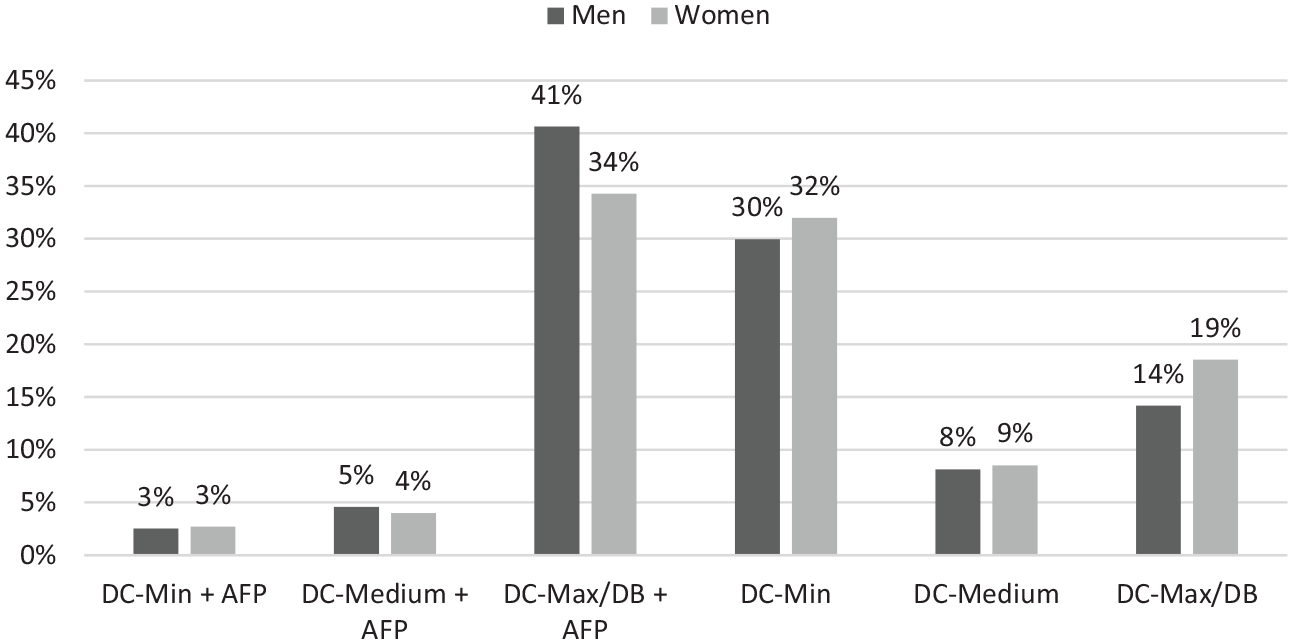

The analyses that follow distinguish between minimum, medium and maximum occupational pensions. Minimum pensions provide only the minimum savings rate (2%), medium pensions provide savings rates at 4–5%, and DC Max/DB refers to schemes with the highest savings rates (6–7% and often additional savings for incomes above the NI ceiling) plus the DB schemes that remain in the private sector. Figure 1 shows the coverage of schemes with varying generosity for men and women by whether or not they also have access to the AFP scheme. As noted, AFP is an additional occupational pension, covering all firms who are regulated by collective agreements.

Combinations of AFP and different occupational schemes in the private sector for both men and women.

Figure 1 indicates a certain polarisation in the private sector, in the sense that those who were covered by the most generous occupational schemes were also more likely to be covered by the additional contractual AFP scheme. Companies with collective agreements and well-organised trade unions are often larger firms, typically found in the manufacturing, oil and gas sectors. They combine AFP membership with generous company-based occupational pensions and thus offer a relatively generous pension package. Men were overrepresented among employees in these best-off companies: 41% of men had the best package, compared to 34% of women. Correspondingly, women were slightly overrepresented among the worst-off in the private sector: 32% versus 30%.

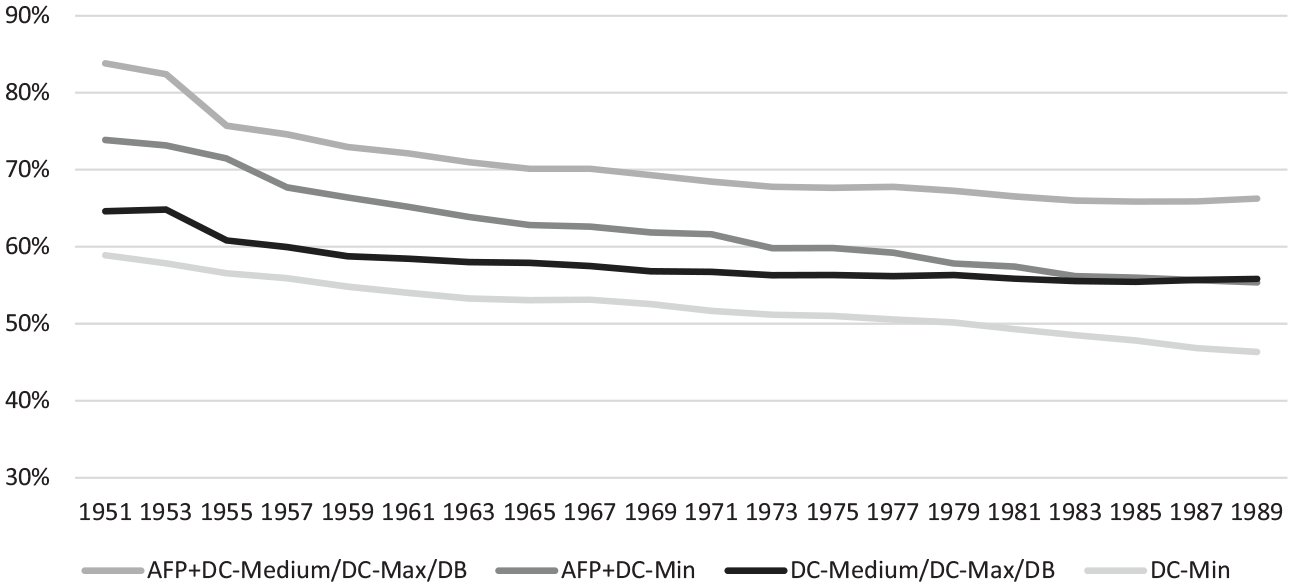

Calculations presented in Figures 2 and 3 dig deeper into how differences in coverage will play out over time in terms of benefit levels. Figure 2 shows average replacement rates for those who exit the labour market entirely at 67, illustrating the variation in benefit levels created by differences in coverage by schemes of varying generosity. The figure compares total pension packages, including both the NI scheme and the various occupational pensions. It shows that replacement rates decline over time for all pension packages: those born in 1953 have relatively high replacement rates, while replacement rates will be lower for all later cohorts. This is true even when the virtual working career is extended to 67 years for all. Replacement rates will fall to a very low level for private sector employees with the most meagre pension package. For cohorts born in the 1980s and later, this package will produce total replacement rates below 50%.

Average replacement rates for individuals who retire at 67 years, by birth cohort and occupational pension package in the private sector.

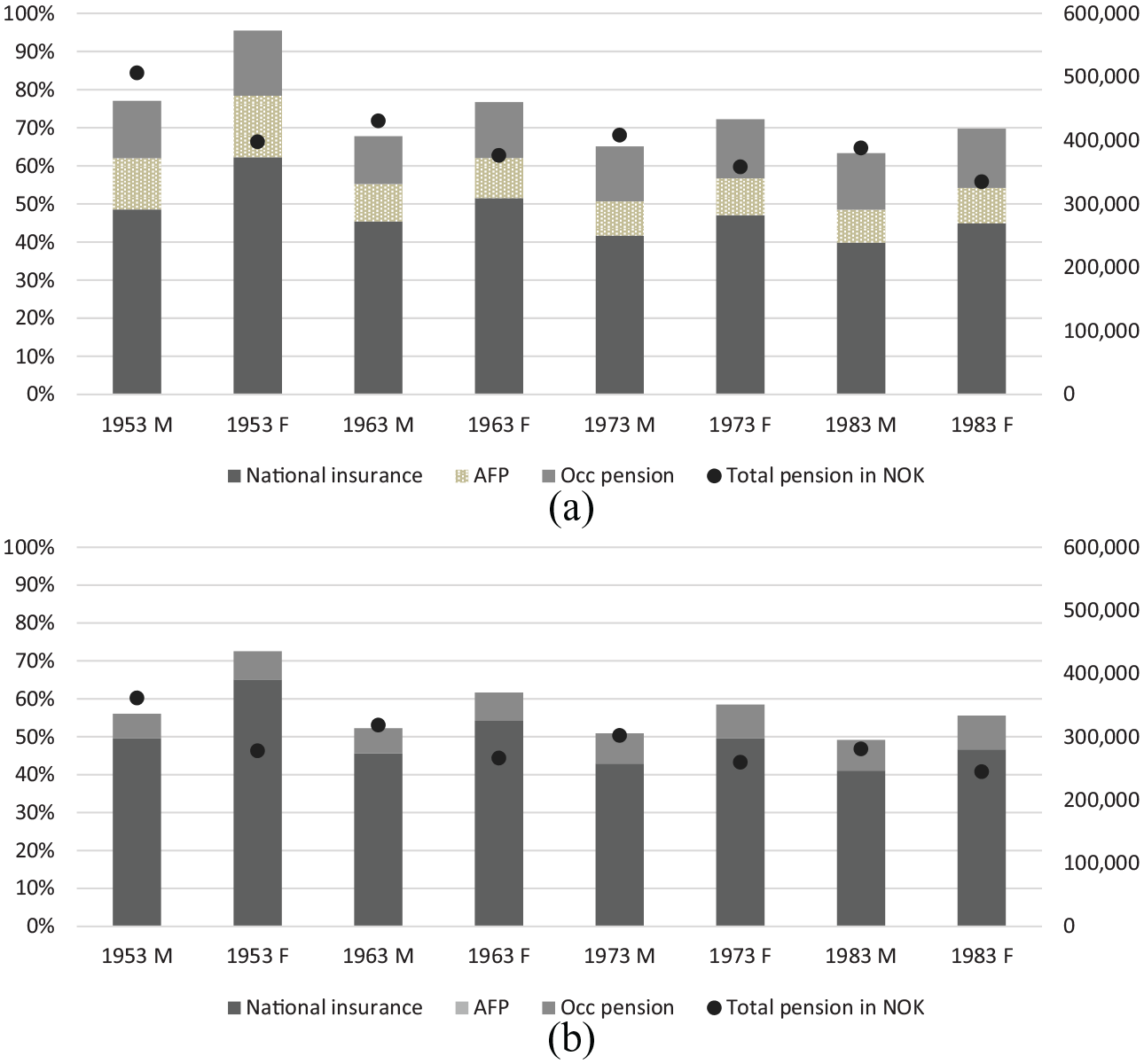

Replacement rates and annual pensions for individuals who retire at 67 years, by gender, in the private sector (cohorts 1953, 1963, 1973 and 1983): (a) with AFP and (b) without AFP.

Figure 3(a) and (b) bring gender back in by showing the average replacement rates and annual pensions (NOK) for men and women in different cohorts who retire at 67, for different cohorts and by access to AFP. Irrespective of pension packages, the figures illustrate three main points: first, they confirm that pension levels will decrease over time. This is true for comparisons of both replacement rates or absolute levels. Second, the figures show that whether future pensions are presented as replacement rates or as absolute levels has important implications for the interpretation in terms of gender. Women achieve higher replacement rates than men, but they still receive less money. This is a reflection of women’s lower lifetime earnings. Third, NI pensions make up a larger part of women’s pensions than of men’s. Even with increased emphasis on occupational pensions, women still rely more heavily on the established state pensions.

Overall pension levels, whether expressed as replacement rates or absolute levels, are highest for those covered by collective agreements (AFP). Figure 3(a) indicates that the combination of AFP and generous DC schemes will give men and women in the private sector relatively high replacement rates also in the future. Women in the 1983 cohort will obtain a replacement rate at around 70%, and annual pensions around NOK 335,000 (€33,500; £28,000), if they retire at 67. The private sector without collective agreements is a different matter: not only do employees in this sector lack AFP, they also typically have lower occupational pensions (see Figure 1). As a result, both replacement rates and absolute levels are lower. Women in the youngest cohort can look forward to pensions at around NOK 250,000 (€25,500; £21,000), and a replacement rate at about 50%, even if they respond to the work incentives in the pension reform and work until they are 67.

It is also worth noting that gender differences are much bigger in the 1953 cohort than in any subsequent cohort. This is mainly a reflection of the increased employment among women in the younger cohorts: as women and men behave more similarly in the labour market, they also receive more similar pensions. This is mainly reflected in replacement rates, which decrease more for women than for men. Annual pensions in NOK decrease for both genders, as the effects of the pension reform (which reduces pensions) cancel out the effect of increasing average earnings (which increases pensions). The decrease by this measure is, however, much more pronounced for men. Similarly, the detrimental effect of moving from ‘mainly DB’ to ‘mainly DC’ for women is hidden in aggregate figures: women who were covered by the old DB schemes have lost out, but this effect is smaller in the aggregate compared with the gains made by women who in 2006 went from having no occupational pension to having a small or medium-sized one. These patterns illustrate the complexity of pension calculations – a number of factors are at play simultaneously, reflecting changes in behaviour as well as the multifaceted effects of complex schemes.

Life expectancy and the need for employment extension

A key point of the reformed Norwegian pension system is that employees can increase their annual pension by working for longer. In the following analysis, therefore, the restriction ‘everybody works until 67’ is abandoned in favour of the question of how much longer men and women in various cohorts, with various pension packages, will have to work in order to obtain a 70% replacement rate. These data cannot predict who will work longer, but they allow for a discussion of opportunities and incentives inherent in the new system for different groups.

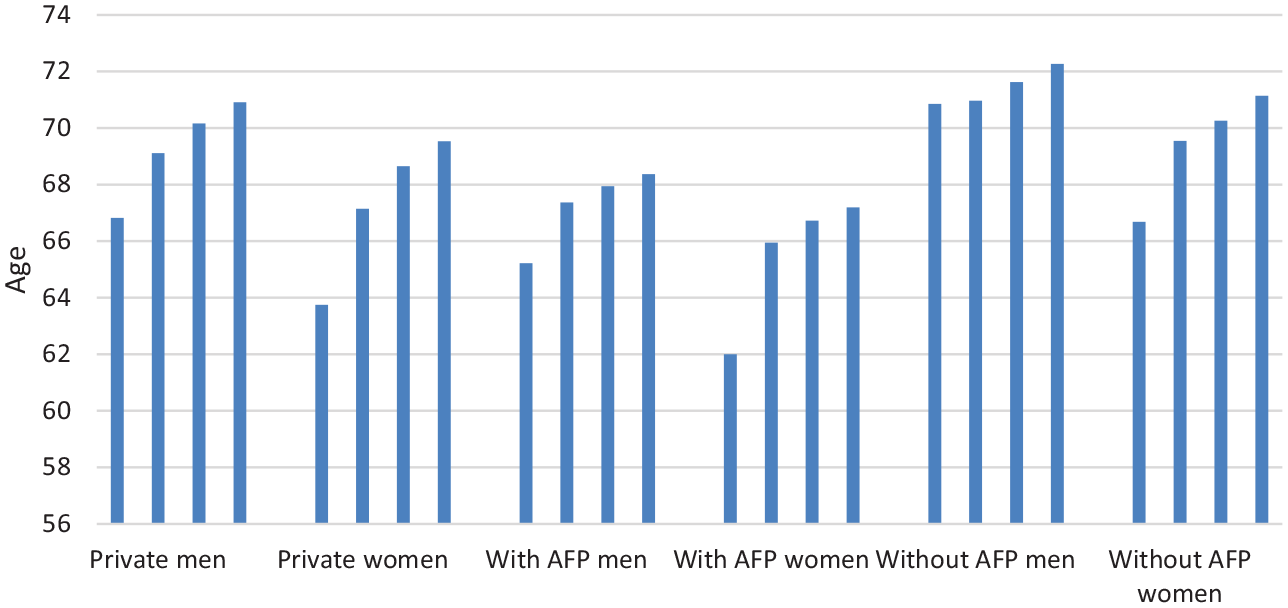

Figure 4 shows the age at which different groups can retire in order to reach a replacement level of 70%.

Median age to achieve a 70% pension replacement rate in the private sector for both men and women, with/without AFP (cohorts 1953, 1963, 1973 and 1983).

Looking first at the average outcome for the private sector in Norway at large, it can be seen that men born in 1953 will obtain a 70% replacement rate if they retire at age 67. Women born in 1953 can retire at 64. Men and women born in 1983, working in the private sector, will have to delay retirement until age 71 and 70, respectively. In other words, the average man will have to delay retirement by four years, and the average woman by six years, in order to obtain the replacement rate aimed for in the pre-reform system.

These findings for the private sector at large are striking, but they conceal important differences between employees with different occupational pension packages. The relative increase is of the same magnitude for all groups: regardless of pension packages, all private sector employees have to work three to five years longer in order to obtain the 70% replacement rate. Women without AFP will, on average, have to extend their working careers from 67 to 71. Those who have AFP – and thus, as shown in Figure 1, are much more likely to also have generous firm-based occupational pensions – can retire much earlier. Men with AFP will have to postpone retirement from 65 to 68, while women with AFP must extend their working careers from 62 to 67.

Figure 4 confirms that which occupational pension package one has access to has major implications for how much longer one will have to work in order to obtain what has traditionally been regarded as a good pension. However, despite differences in levels between groups, the main message from Figure 4 is that everybody will have to work longer in the future. Men, women, those with generous pensions and those with minimum pension packages – nobody will be able to retire before age 67 in the new pension system if they expect to maintain their material living standards in retirement.

Discussion and conclusion

Old age pension schemes in Europe are changing. Longer employment careers are encouraged, and occupational schemes expand to fill the gaps when state pension schemes are retrenched. Taken together, these two trends create new potential vulnerabilities. For those who cannot compensate lower state pensions with occupational schemes, there is a need to work longer in order to obtain a higher pension income. The ability to do so may, however, be limited, depending on the demand side in the labour market, and also unequally distributed. Distribution effects of occupational schemes are different from those found in state schemes, as occupational schemes typically are pure savings schemes with little or no risk sharing and no compensation for periods spent outside paid employment. Our ambition in this analysis has been to investigate what ongoing transformations of Norway’s pension nexus imply in terms of opportunities to retire and incentives to extend working lives, with particular emphasis on gender.

Our main finding is that, in the near future, everyone will have to work longer in Norway. It was an explicit ambition of the Norwegian pension reform to create incentives to extend working lives, yet policy-makers have been vague – deliberately, one must assume – on how much longer individuals should expected to work. The increased emphasis on occupational schemes as top-up pensions has added to this haziness: such schemes increase replacement rates for those covered and thus dampen the incentive effects in the public scheme. The present article is the first attempt to model the combined effects of the NI pension scheme and the various occupational schemes, and the findings are stark: practically everybody in the 1983 cohort must work four years longer than employees in the 1953 cohort in order to achieve a replacement rate of 70%. Many future employees will have to work until they are 71–72 in order to obtain this pension level. This implies that if employees in the private sector respond to these incentives, future labour markets will receive a supply-side shock of potential workers above the age of 60, or even 70.

In discussions of class and gender in relation to pensions, occupational pensions can be seen to some extent as wild cards (Meyer and Bridgen, 2008). The Norwegian case is probably typical in that it contains both elements of systematic advantage and elements of chance. The outline above describes how Norway has two occupational schemes, with different governance structures and qualifying criteria, operating in parallel: sector-wide AFP and firm-based savings schemes. Figure 1 shows that the two converge: the two biggest groups in the Norwegian private sector are those who are covered by AFP and generous firm-based schemes, and those who have meagre firm-based schemes and no AFP. An important observation is, however, that these cleavages do not necessarily follow horizontal or vertical cleavages in the labour market: an electrician working in a large firm in the oil industry will be in the most advantaged group; a business economist working for a medium-sized hospitality firm is likely to be among the disadvantaged. Occupational pensions thus criss-cross the labour market, cutting across class-, skills- and gender lines.

Because of these wild card elements, it should not be assumed that those with the most meagre occupational pensions are typically ‘working class’ or ‘low qualified’. Access to AFP is, however, conditioned on working in an enterprise covered by collective agreements, suggesting that those with the greatest need to extend working life typically work in the least organised part of the labour market. This suggests that the employees who most need to extend their working careers are also the ones most likely to be employed on temporary or zero-hours contracts, and also to have the least flexible working hours. In this sense, Norwegian occupational pensions mirror and deepen existing cleavages in the labour market and increase the odds of extending these into retirement.

Similar reflections can be made regarding women’s situation. This analysis has arguably chosen a case that maximises the odds of not finding strong gender effects: Norway is a country with high female labour force participation, a well-regulated labour market, and – since new legislation passed in 2006 – full coverage of occupational pension schemes. Still, calculations indicate that women continue to obtain lower pensions than men, and will continue to do so even in the youngest cohorts included here. Women are slightly overrepresented among those with the least generous pension packages in the private sector in Norway. This suggests that when women work in the private sector, they are more likely than men to work in industries or enterprises where industrial relations are relatively weak, and where fringe benefits are more meagre (Ginn and Arber, 1993). The discrepancy is, however, not very large, and it is balanced by the fact that around half of employed women in Norway work in the public sector.

At the same time, the findings indicate that the (reformed) NI is more important to women than to men, relatively speaking. This suggests that women are indeed disproportionally at risk when public pension schemes are scaled back, as the redistributive elements often found in state schemes – guaranteed minimum levels, accrual for care work – are unlikely to exist in occupational schemes. Moreover, these findings indicate that a well-organised labour market with solid industrial relations benefits women. Governance of pensions that guarantee high coverage rates and lifelong benefits, whether as legislation or through collective agreements, lead to better outcomes for women.

The analyses show that both the need to work for longer, and the ability to do so, is unequally distributed in the labour market, and that those who have the biggest need to extend their working lives may be disproportionally found among those who have the least ability to do so. The most important contribution this article makes to the literature on extended working lives is in showing how occupational pension schemes structure the need to extend working lives – in ways that sometimes confirm, and other times cut across, well-known social division in the labour market. In Norway, a key feature is whether the workplace is covered by collective agreements. Case studies from other countries may highlight other institutional features; indeed, there is a need for a series of studies that outline new vulnerabilities, risks and opportunities in the light of the changing pension mix in different national settings in Europe and beyond. Increasing reliance on occupational schemes and policies to extend working lives are two overarching trends in European pension reforms, yet there is little research on the intersections between these two trends – what the two combined imply for men and women’s retirement options and pension adequacy. More studies along these lines would improve our understanding of risk in old age in countries with different labour markets and welfare states. Moreover, future studies should analyse how employees actually respond to the incentives in the reformed pension systems, and the consequences new retirement patterns have for inequality and life satisfaction in old age.

Footnotes

Acknowledgements

We are indebted to Pål Lillevold and Hans Gunnar Vøien in the actuarian company Lillevold & Partners for their role in the data analysis, and to three anonymous referees for constructive comments to earlier versions.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: this article is written with funding from the EVAPEN programme of the Norwegian Research Council, grant no. 238205/H2.