Abstract

Intra-family succession is at the heart of what makes family business unique. To explain why businesses are (not) transferred within the family, this article adopts a macroperspective, viewing succession as a specific transfer regime. Portraying the case of Germany since the 1990s, we show how this transfer regime has been changed. Using document analysis and expert interviews, we show when, how, and why the configuration of the intra-family succession regime was altered and an “exit regime” emerged. In this new regime, the family as owner is problematized, and ownership transfer is coordinated through matchmaking, which increases the importance of business intermediaries.

Introduction

All owners of family businesses have to give up their ownership to another owner eventually (Aldrich, 2015; DeTienne, 2010; Widz & Kammerlander, 2023). Ownership transfer is a process that involves an incumbent owner giving up their shares of the business, a succeeding owner willing to take over the shares, and the transfer of shares between them. Business owners can coordinate the ownership transfer of their business in a myriad of ways. They can gift, bequeath, or sell their shares to their children or other family members, to employees or former managers, to other businesses or foundations, or to investors or “go public” (Initial Public Offering, IPO) (DeTienne & Wennberg, 2015; Wennberg & DeTienne, 2014; Wennberg et al., 2010).

Among family business scholars, ownership transfer within the family is generally seen as the default option and has been studied extensively (Brockhaus, 2004; Decker et al., 2016; Handler, 1994; Rovelli et al., 2022). Family transfer of ownership, or intra-family succession, is understood as a multi-staged and emotional process of mutual role adjustment (Handler, 1990; Le Breton-Miller et al., 2004) that requires preparing and motivating the successors adequately (Gagné et al., 2019; Gilding et al., 2015; Gimenez-Jimenez et al., 2021; Lyons et al., 2024; Sund et al., 2015), managing the transition and potential family internal conflicts (Bozer et al., 2017; Calabro et al., 2018; Qiu & Freel, 2019), and the incumbents’ willingness to let go of control (Miller & Le Breton-Miller, 2005; Richards et al., 2019).

More recently, family business scholars have attended to selling the family business (Hsu et al., 2016; Niedermeyer et al., 2010; Widz & Kammerlander, 2023). While selling the business can occur within the family and in this case usually follows the logics of intra-family succession (which involves, e.g., family discounted prizes for successors; Zellweger et al., 2016), the selling of the business to an external party is understood to be remarkably different: A sale does not only coincide with an owner’s entrepreneurial exit but also with the detachment of the family from the business. Such an entrepreneurial exit is understood to involve strategic foresight (Chirico et al., 2020; Wennberg et al., 2010), the matching of sellers and buyers on a market (Stamm, 2023), and the valuation and subsequent sale of the business to an external party (Kammerlander, 2016; Wennberg & DeTienne, 2014). How well the transfer process is planned and executed impacts the business’s continuity and performance and the family’s unity (Ahrens et al., 2019; DeMassis & Foss, 2018). At times, the selling of the business can become repetitive in the case of portfolio owners (Sieger et al., 2011).

The extant literature approaches ownership transfer on the individual level, so how individual business owners decide to whom and how to transfer the business (DeTienne et al., 2015; Rovelli et al., 2022). Many studies acknowledge that these decisions are embedded in particular organizational, community, and cultural contexts (Jaskiewicz et al., 2016; Reay et al., 2015). However, ownership transfer is much less studied from a macroperspective. From this perspective, ownership transfer is in itself an institution, that is, a bundle of set expectations, norms, and practices that provides an unquestioned blueprint for the way ownership should be transferred—independent of the individual family business (DiMaggio & Powell, 1983; Widz & Kammerlander, 2023). We argue that intra-family succession formed a specific institutional configuration, and the expectations around intra-family succession helped us understand when, how, with whom, and why this type of ownership transfer happened (Baker & Welter, 2018). Only on the macrolevel of analysis can we understand the institutional changes of ownership transfer over time and that some expectations for ownership transfer become less binding and others become more legitimate.

To develop this perspective, we study ownership transfer from the angle of a sociology of ownership (e.g., Carruthers & Ariovich, 2004; Davies, 2012). We argue that intra-family succession is a specific ownership transfer regime (Krasner, 1982) and refer to this ownership transfer regime as “intra-family succession regime,” which involves particular understandings of the owning subject, the owned object as well as articulations of how business ownership should be used. We thus examine ownership transfer from a bird’s eye view and ask the following research question: How and why has intra-family succession as one specific ownership transfer regime declined and what ownership transfer regime has followed?

A relevant case in this regard is Germany, which has been known for its high number of multi-generational family businesses (Lehrer & Celo, 2016): More than 90% of the 3.3 million German businesses are owned by individuals or families (Gottschalk & Lubczyk, 2019). For a long time, intra-family succession was the preferred mode of ownership transfer regime, especially among small- and medium-sized business owners, also referred to as the German Mittelstand (Kay et al., 2018; Pahnke & Welter, 2019). Yet, surveys among business owners indicate a tremendous change: More and more business owners could imagine transferring their business ownership outside of the family. In 2019, the majority of business owners even preferred an external solution (Schwartz, 2019). In this article, we thus argue that the institutional configuration of an ownership transfer regime as intra-family succession has been in jeopardy and seek to explain how this change has unfolded. Learning about this shift in transfer regime sheds a new perspective on the role of the family in German capitalism by showing how families may gradually begin to lose their status as the automatic anchor of family business ownership and are instead giving way to more market-oriented, financially driven forms of an ownership transfer regime. This provides an entry point to learn more generally about institutional change of ownership transfer regimes.

Empirically, we trace the evolution of the intra-family succession regime in Germany from the 1990s until today, drawing on a rich collection of documents and expert interviews from business owners, their advisors, intermediaries, researchers, and policy-makers. By doing so, we identify how the dimensions of the intra-family succession regime were continuously critiqued and altered in a way that a new ownership transfer regime, which we label as the exit regime, became viable.

We make the following contributions. First, by introducing the concept of transfer regimes into the family business field, we show that intra-family succession is not only embedded in an institutional context (Widz & Kammerlander, 2023; Wiklund et al., 2013) but also presents an institutional configuration that can become a subject of change. Second, our sociological approach allows us to identify institutional change with regard to ownership transfer regimes. We show how the critique of various aspects of intra-family succession evoked an alternative solution by altering norms and regulations of the ownership transfer regime.

Theoretical Motivation

Ownership Transfer and Intra-family Succession

In order to understand how and why business owners transfer their ownership, previous research has looked at ownership transfer as the decision of the incumbent owner (DeTienne et al., 2015; Wiklund et al., 2013). Acknowledging that this decision may not only be driven by economic factors, scholars have emphasized the need to attend to the institutional context of ownership transfer (Bird & Zellweger, 2018; Jaskiewicz et al., 2016; Reay et al., 2015; Widz & Kammerlander, 2023; Wiklund et al., 2013). Institutions are a bundle of norms, rules, and practices that structure and guide social behavior and interactions within a given context (Berger & Luckmann, 1966; DiMaggio & Powell, 1983; Scott, 2001)—they are understood as the “societal rules of the game” (Widz & Kammerlander, 2023). Institutions can reduce uncertainty, risk, and transaction costs (North, 1990).

Family business scholars point to the family as an institutional realm that influences the decision for an intra-family institutional configuration of ownership transfer (Aldrich & Cliff, 2003; Miller et al., 2011; Thornton & Ocasio, 1999). The family provides norms and structures that influence decision-making with regard to the firm (Aldrich & Cliff, 2003; Berrone et al., 2010). The intention to pass on ownership within the family is influenced by the owner-family’s structure and their involvement in the business (Gersick et al., 1997; Wiklund et al., 2013; Zellweger et al., 2016). Of particular influence are marital ties between owners (Belenzon et al., 2016) and the way the owning family practices the work–family interface, that is, how much family life and the business intertwine (Heck et al., 2006; Hsu et al., 2016). Furthermore, gender norms structure the selection of future successors (Byrne et al., 2019). Overall, these studies emphasize that the family embedding of business ownership shapes the decision to pass on the business within the family.

It is important to note that passing on the business within a family is also an institutional configuration. Succession is thus not only a decision made to coordinate the ownership transfer, but simultaneously there is a blueprint for how this decision should be made. Keeping the business in the family is a transfer norm that is even codified in inheritance and/or inheritance taxation laws in some countries (Beckert, 2008; Bjuggren & Sund, 2005). This norm has been embraced in family business research as a definitional criterion for family businesses (Chua et al., 1999; Haag et al., 2023) and to explain family business behavior (Gómez-Mejía et al., 2011).

The institutional configuration of ownership transfer within the family, however, has been subject to continuous critique and change. Such institutional change, understood as changing the rules of the game, can be formalized in new laws, or be reflected in changing ownership practices (Carruthers, 2012). For example, the norm to keep ownership within the family is a mean for wealth concentration, and several countries have implemented statutory shares in their inheritance laws, that is, legal rules requiring that a fixed portion of a deceased person’s estate be passed on to certain heirs, regardless of the inheritor’s will (Beckert, 2008). Primogeniture and paternalistic transfers have been critiqued in the light of movements toward more gender equality and more pluralistic understandings of the family (Calabro et al., 2018; Di Belmonte et al., 2017; Le Breton-Miller et al., 2004). Further legitimate reasons for treating family members unequally in the transfer of ownership vary by country or even regions (Albertini et al., 2007; Esping-Andersen, 1990). These examples indicate implicit rules about which family members are legitimate new owners, how the transfer should occur, and how those excluded from the transfer should be treated as a subject for change, indicating institutional configurations of ownership transfer that can change over time.

Intra-family Succession as a Transfer Regime

We assume that keeping the business in the family is part of a specific institutional configuration that shapes ownership transfer. We refer to this institutional configuration as regime, which Krasner (1982, p. 185) defined as “the principles, norms, rules, and decision-making procedures around which actor expectations converge in a given issue-area.” The issue-area in our paper is how the ownership of a business can be secured in the next generation. We suggest that there are cultural norms and (legally codified) rules guiding the decision to transfer the ownership of a business within the family. It is this institutional configuration that we refer to as intra-family succession regime.

To capture ownership succession as a specific transfer regime, we build on the heuristic put forward by Carruthers and Ariovich (2004), which distinguishes five interlinked dimensions of owning relationships. The transfer dimension defines how property moves between different owners. Ownership transfer is embedded in normative ideas of transfer and institutionalized ways of organizing it. The subject dimension defines who can own a business and includes natural and juridical persons. Who is seen as a competent and legitimate owner may vary by gender, marital status, kin relationships, education, or prior investment (Carruthers & Ariovich, 2004). The object dimension defines what can be owned. A “business,” when considered as an object of ownership, is not just a legal or economic entity but also a socially constructed concept (Pinnington & Morris, 2002). It can carry strong noncommercial social meanings—such as being seen as a public good or a personal object—that may make the idea of owning it seem inappropriate or controversial. The articulation of use dimension defines what can be done with the owned business and therefore defines within which limits property can be used. Business owners make claims on control of the business, particularly defining its structure and strategic development, and on residual income (Carruthers & Ariovich, 2004). The use of business ownership further includes a number of obligations such as compliance (e.g., paying taxes) as well as internal restrictions (e.g., norm to retain profits) (Lehrer & Celo, 2016). Finally, the enforcement dimension defines how property rules are maintained. The state and the judicial system play an important role in enforcing business owners’ property rights (Carruthers & Ariovich, 2004; Dagan, 2021).

Expanding on Carruthers and Ariovich (2004), we suggest that intra-family succession forms a specific configuration of these dimensions. The underlying definitions of the five property dimensions are constitutive for a transfer regime. In the intra-family succession regime, the family is defined as the owning subject, which restricts the transfer of the business to family members. Intra-family succession creates reciprocal promises and expectations that promote high levels of commitment within the business family, thus putting the long-term well-being of the family above short-term individual needs but also providing fertile ground for nepotism (Jaskiewicz et al., 2013; Sharma & Irving, 2005). Likewise, the business as an owned object carries a high symbolic weight and is perceived as a personalized object (Breuer, 2009; Lubinski & Gartner, 2023). The use is articulated by the family’s mission of nurturing the business, which justifies the accumulation of capital in the family’s hands but also obliges the family to retain the accumulated profits within the business for future benefit (Lehrer & Celo, 2016). Ownership succession is enforced by a legal system that sees the family as the main recipient of gifts and inheritances and can grant generous tax exemptions for business transfer (Beckert, 2008). Previous research has also highlighted the key role of fiduciaries in enforcing ownership succession (Strike & Rerup, 2016). Fiduciaries mediate personal relationships within the family (Bertschi-Michel et al., 2021), “offset dysfunctional family biases” (Le Breton-Miller et al., 2004, p. 315), and provide support in the formalization of the ownership transfer (Harrington & Strike, 2018).

This intra-family succession regime strongly encourages gift exchange within the family and intergenerational inheritance as the ideal form of transfer, although the sale within the family is also possible. Such a sale, however, usually involves specific expectations based on family cohesion, leading to discounted prices for family members (Zellweger et al., 2016). When choosing and legitimating a successor, family members reflect upon their life choices (Stamm, 2016) and mutually adjust their roles to successfully transfer the family business (Handler, 1990). Given reciprocity norms prevailing in the family (Long & Mathews, 2011), the committed incumbent and successor are likely to care about the various interests of family stakeholders and preserving the family legacy (Richards et al., 2019). Violation of the intra-family succession regime by family members can come at the cost of diminishing family cohesion, open conflict, or even exclusion (DeMassis et al., 2008). From this perspective, family business owners are unlikely to offer their businesses or shares thereof to external parties or may experience sale to strangers as a failure and family betrayal. The intra-family succession regime thus prevents the transfer of the business on a market for corporate control (Beckert, 2006; Callaghan, 2018).

With this enriched understanding of the intra-family succession regime, we will now examine under which conditions and in what ways this regime changed in the context of Germany. In order for a regime change to occur, the norms, rules, and principles underlying the transfer regime must shift (Carruthers, 2012; Krasner, 1982) in all dimensions of owning relationships (Carruthers & Ariovich, 2004). Such norms and principles must first become less coherent so that the practice becomes “increasingly inconsistent with principles, norms, rules, and procedures,” making the regime prone to change (Krasner, 1982). Such changes then gradually occur in legal frameworks, cultural perceptions of ownership, economic incentives, and social expectations surrounding ownership succession.

Method

Research Context

Individual and family ownership dominates in most countries around the world (Faccio & Lang, 2002), but Germany is a particular case, as it is known for an extraordinary high number of family-owned businesses that are often transferred across generations. Studies suggest that more than 90% of the 3.3 million German businesses are owned by individuals or families; in many of these businesses, ownership and leadership coincide (Gottschalk & Lubczyk, 2019). In particular, in the German Mittelstand, intra-family succession was a long-standing rule (Berghoff & Köhler, 2020; Kay et al., 2018; Pahnke & Welter, 2019). The next generation would not only take over the ownership but also become active in business management. Succession in Germany, for a long time, not only followed the norm of transferring the business within the family but also transferred the business to a single heir aligned with the tradition of the family fidei comiss, which was only abolished in the first half of the 20th century (Beckert, 2008; Colli, 2013). Since then, however, norms of treating all children equally in the inheritance have become more prominent (Albertini et al., 2007).

Over the past decades, German business owners’ intention to transfer their business within the family has been declining. In 2019, for the first time, a majority of German business owners even intended to sell their business externally (Schwartz, 2019). In the COVID-19 crises, this trend was interrupted, as business owners in light of the uncertainty of the crises re-oriented themselves toward the family. From here on out, however, we can once again observe a declining intention toward intra-family succession (Evers, 2024). In parallel, an increase in the number of business sales can be observed. Using income tax data, which allows to track the number of business owners selling their businesses (or shares thereof), Stamm and colleagues (2023) show that business sales have increased between 2001 and 2018 by 80% to more than 150,000 in 2018. In sum, the data indicate that intra-family succession as the dominant mode of ownership transfer regime is increasingly being subordinated to the external sale of the business. It remains widely unclear, however, how this change occurred.

Research Design

To capture the change of intra-family succession as institutional configuration, we follow Davies (2012) and apply a pragmatist research design. Pragmatism is a classic sociological approach that views knowledge and rules as dynamic and malleable based on their usefulness to solve real-world problems (Dewey, 1930; Mead, 1937). A pragmatist research design takes the norms, rules, and habitual decision-making procedures within a transfer regime as the starting point of analysis (Davies, 2012). These are understood as ongoing solutions to coordination problems that remain unchanged as long as the solution remains satisfactory in regard to meeting specific ends, while the means of doing so are constantly adjustable (Dewey, 1930; Mead, 1937). This means recognizing that “human agents are endowed with the capacity to judge, justify and criticize” owning relationships (Davies, 2012, p. 169). A pragmatist research design thus centers on institutional change as a spiral of acute problems of coordination that require pragmatic solutions, which eventually face new problems and require new solutions.

The coordination problem at hand in our case was the coordination of ownership transfer, the solution to which would historically be intra-family succession. Adapting a pragmatist methodology, we analyzed the reasons why intra-family succession was no longer considered to bring seamless solutions and studied how owners and their fiduciaries engaged in collective inquiry and experimentalism to find a next-best practical solution. In these attempts of finding next-best solutions, the dimensions of owning relationships may change and culminate in changed institutional procedures (Beckert, 2009)—in our case a change in the transfer regime (Carruthers, 2012; Carruthers & Ariovich, 2004).

Sources

We began our empirical investigation with a handful of expert interviews with fiduciaries of family owners such as lawyers, tax advisors, and business consultants who have been involved in ownership succession for at least 10 years. In contrast to business owners, who often only go through one succession in their life, these fiduciaries were constantly confronted with ownership succession issues in their interactions with business owners, other experts, and policy-makers (Bertschi-Michel et al., 2021). The interviews were semi-structured consisting of three main parts: a set of open-ended questions on the interviewee’s career and their experience with ownership transfer; second, a set of questions on their perception of how ownership transfer has changed asking for examples to substantiate their observations; and third, a set of questions with regard to the sale of businesses and what is particularly new about this form of ownership transfer. The interviews provided first insights into how the intra-family succession regime has changed over the past years and initial cues with regard to what initiatives, public discourses, events, or actors may be relevant to understanding these changes.

We then searched for documents that would protocol the changes of norms, practices, and justifications indicated by fiduciaries and other field actors in intra-family succession, such as pamphlets, news articles, laws, and law commentaries. Based on the initial interviews and the collected materials, we would identify the next set of relevant interview participants and documents based on what we had already learned and thus adhering to the principles of theoretical sampling (Glaser & Strauss, 2006). For example, a corporate banker would tell us about how the introduction of a credit rating according to the reform of banking supervisory law (referred to as Basel II) would make it necessary to ask business owners about their succession plans. We would then look at the Basel II regulations, guidelines for banks on “soft-factors” in the rating process, and announcements of events around Basel II and succession. Or, a member of the chamber of commerce would tell us about the relevance of the succession forecasts by the Institute for Research on Mittelstand (IfM) in Bonn. We would then gather all of these reports and news articles about these reports and talk to IfM researchers. Over 3 years (2019 to 2022), we conducted 30 interviews with 24 experts, including lawyers, consultants, representatives of the chambers of commerce, academics, and firm platform providers. More importantly, we compiled a rich collection of documents including, for example, all chamber of commerce succession guides, postings for succession events, articles in industry magazines on succession, images and texts of business platforms, plenary discussions and legal documentation on tax breaks for business sales, and statistics and all succession forecasts. Our data collection considered the various stakeholders of ownership transfer. For example, the business owners’ perspective was included through case studies or journalistic interviews. The collected data materials allowed us to trace the origins of the gradual change in the intra-family succession regime from the 1990s until 2023. Table 1 provides an overview of the sources utilized for this study.

Overview Sources.

Analysis Method

A pragmatist approach to institutional changes in the intra-family succession regime allows us to focus on a gradual and descriptive understanding of ongoing collective inquiries and negotiations between current and potential owners, fiduciaries, and policy-makers who try to create solutions that are best suited to resolve the succession problems they experience. This framework suggests to study how families, their advisors, and policy-makers negotiated alternative rules of ownership transfer. This focus on the practical dimension of negotiating changes of ownership transfer considers the interweaving of facts, values, knowledge, and action while at the same time acknowledging actor’s dependency on the institutional context in which these factors emerge (Ogien, 2014). For example, the transfer of a business to the first-born son (primogenitor) was an institutionalized value for intra-family succession, which has become impractical for many families as it collides with norms of meritocracy and equal bequeathing to children (Stamm 2016). We examine what happens when actors take the tentative goals they develop while dealing with everyday challenges and weave them into an accepted understanding of new owning relations (Dewey, 1930). As those tentative goals are gradually adopted, they harden into new ground rules for how family businesses may be transferred. A pragmatist approach thereby holds that the property dimensions (Carruthers & Ariovich, 2004) of the ownership transfer regime develop in the course of practical activity, and new forms of institutionalized ownership transfer may come into being.

During the analysis of the data materials, we first sorted the documents and interview narrations by time and used a pragmatist perspective to identify four main phases: roughly speaking, we see that intra-family succession was first problematized by key stakeholders, then various collective inquires started followed by experimentalism with new forms of ownership ship transfer and eventually the norm to transfer a business within the family was weakened by a new openness for selling the business. These phases, however, remained rather vague and partially overlapped in time. We thus engaged in an intense coding-process to understand the reconfiguration of the transfer regime across these four phases.

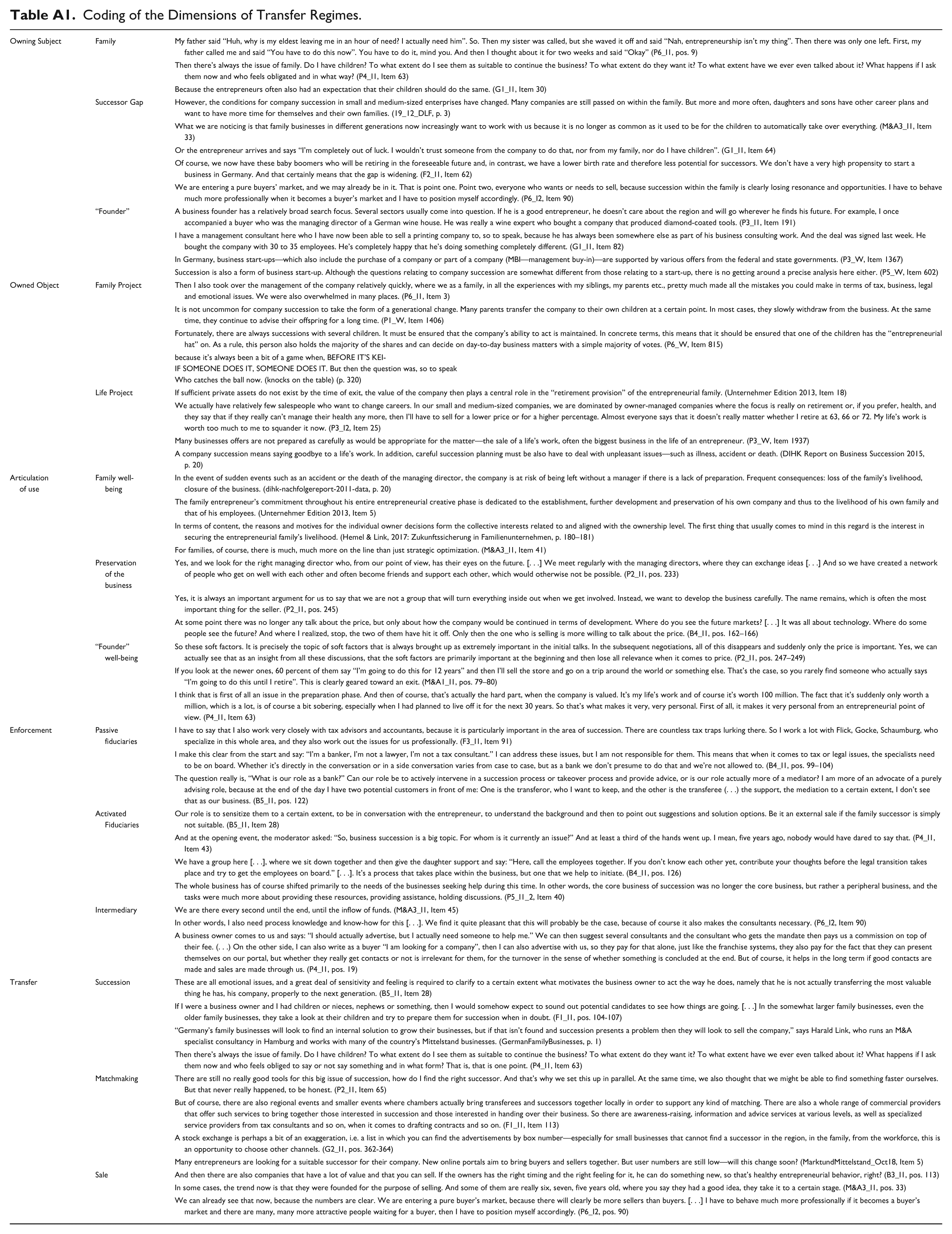

Using grounded theory methodology, and adopting the epistemological approach of pragmatism, our analysis proceeded through iterative rounds of open, axial, and selective coding (Glaser & Strauss, 2006). The interpretation of codes was guided by Gioia’s advancement of grounded theory methodology, which suggests constructing a transparent, visual narrative that explicitly maps the progression from our first-order codes directly derived from our informants to more abstract, second-order themes that capture the underlying dynamics of the change in ownership transfer regime. Table A1 in Appendix depicts this progression. The two authors coded the materials separately and regularly discussed their results in coding sessions with invited researchers to ensure inter-coder reliability. We used MaxQDA software to assist in managing and tracking the codes, ensuring that consistency and transparency were maintained throughout the analysis.

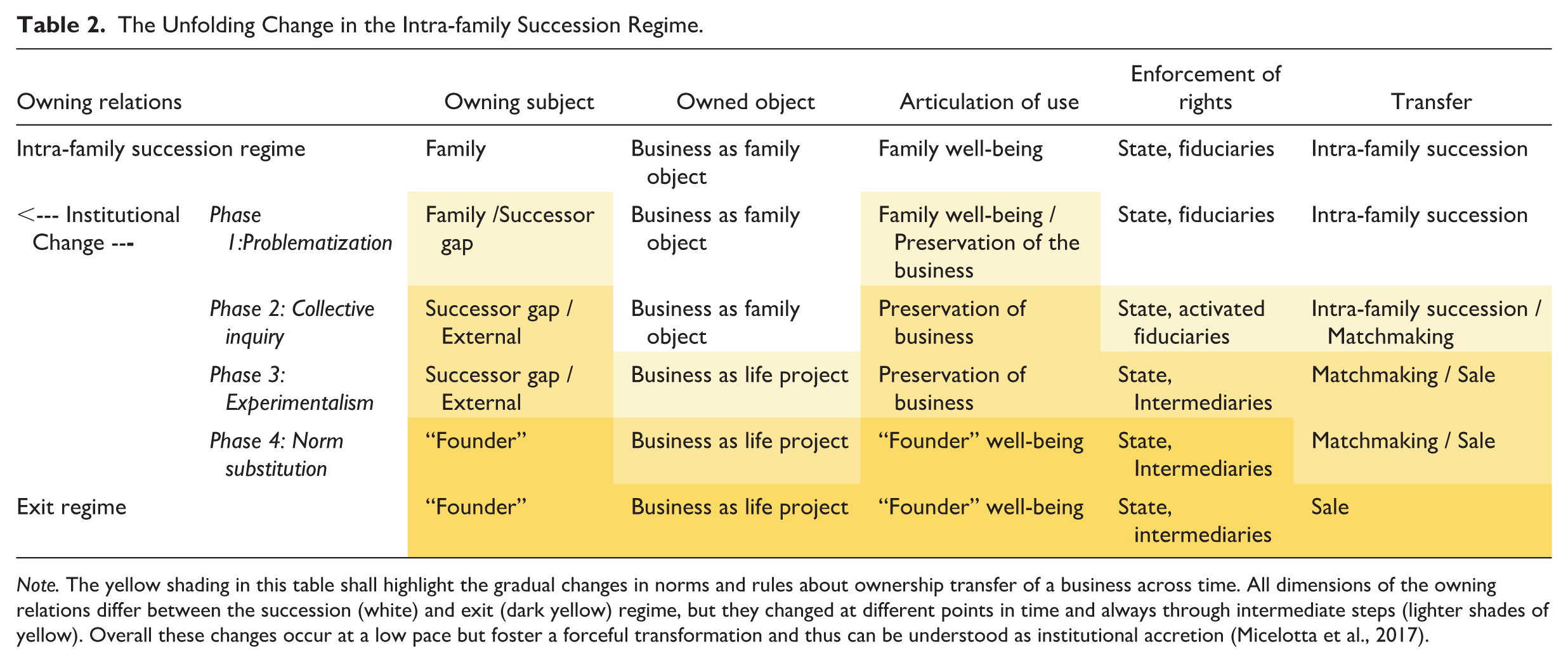

In the course of the analysis, we found that the dimensions of a transfer regime as proposed by a sociology of ownership and presented in the previous section were helpful to structure our emergent code system. We thus clustered our codes around the expectations toward owning subjects, owned objects, the articulation of use, the enforcement of property rights, and rules of transfer (see Table A1 in Appendix). By doing so the pattern of the institutional change of the ownership transfer regime across the four phases became more visible as presented in Table 2. Depicted on the top is the intra-family succession regime in the five dimensions of an ownership transfer regime. In each of the four pragmatist phases, multiple dimensions of the intra-family succession regime were contested and altered. Eventually, all dimensions were reconfigured in such a way that a new transfer regime emerged, which we call an exit regime, as depicted in the bottom row. The term exit refers to the owning family’s departure by selling their ownership of the business (Wennberg & DeTienne, 2014).

The Unfolding Change in the Intra-family Succession Regime.

Note. The yellow shading in this table shall highlight the gradual changes in norms and rules about ownership transfer of a business across time. All dimensions of the owning relations differ between the succession (white) and exit (dark yellow) regime, but they changed at different points in time and always through intermediate steps (lighter shades of yellow). Overall these changes occur at a low pace but foster a forceful transformation and thus can be understood as institutional accretion (Micelotta et al., 2017).

When reading Table 2 from top to bottom, it becomes obvious that the shift from intra-family succession to exit did not occur immediately in any dimension of the transfer regime. Rather, this change involved a number of interim steps before the new exit regime eventually emerged: The actors gradually reacted, found next-best solutions, and eventually permanently re-evaluated ownership transfer solutions. For example, the definition of who can be seen as legitimate owning subject first changed from the family to a “successor gap.” This “successor gap” is an intermediate state, in which the family is increasingly questioned to be able to provide competent new business owners. Only in a next step, external buyers are framed as new legitimate owners.

We eventually were able to describe how the expectations for intra-family succession became increasingly doubted; the family was no longer seen as the best solution for ownership transfer. Each dimension of the intra-family succession regime—who should be an owner, what is the owned subject, how should it be used, and how ownership transfer should occur—was gradually renegotiated and reframed. This shift promoted new expectations toward ownership transfer that stress sales and a matchmaking between entrepreneurial incumbents and new, external buyers. We identified intermediaries as main change agents in the shift toward an exit regime, as they turned from on-demand fiduciaries to indispensable matchmakers.

Findings

We present our findings in the order of the phases we identified, abstracting insights on the dimensions of transfer regimes to better understand the change of intra-family succession. We will focus on the transfer of ownership rather than leadership, although this analytical distinction may not be as clear-cut in the field and in the presented quotes.

Phase 1: Problematization: The Rising Uncertainty of the Intra-family Succession Regime

In the 1980s, business practitioners began to notice and voice problems in the institutionalized transfer of business ownership within the family. Tax advisors, lawyers, business consultants, and corporate bankers in concert with the chambers of commerce agreed that many family business owner-managers failed to hand over power in a timely and efficient manner, thereby jeopardizing the well-being of the business. The issue of letting go was regularly picked up by business magazines (e.g., Handelsblatt, Wirtschaftswoche, and FAZ) and industry reports (e.g., Sparkasse, German Chamber of Commerce), which thus painted a consistent public picture of an ownership succession planning problem. For example, in 1986 an article in Wirtschaftswoche magazine explains the issue as follows:

In family businesses, owners often struggle with the organization of the business. Founder-owners consider themselves indispensable, employees in the middle management are trusted with leadership responsibilities too late, or endless family disputes complicate the work of the management. (Wirtschaftswoche, 1986, own translation)

This early problematization of intra-family succession points to the responsibility of the incumbent business owners. They are portrayed as strong-minded founders and leaders who have succeeded in growing a business. At times, however, they are overly depicted as old men “who cling to corporate power with all kinds of embarrassing disruptive maneuvers” (Wirtschaftswoche, 1990, p. 54, own translation). This conveys the impression that the transfer of business ownership within the family is a difficult task that needs early planning and mediation among family members.

Inefficiently planned and potentially failing intra-family succession had been portrayed as a major threat to the German Mittelstand by consultants and in the media. An article in Wirtschaftswoche (1990), for example, referred to intra-family succession as the “Achilles’ heel” of the Mittelstand. The weight that has been attached to the succession problem in the public discourse is key to understanding the doubts that emerged around intra-family succession as a viable option for ownership transfer. The problematic aspects of intra-family succession began to insert doubt among all involved parties with regard to the family as the owning subject, but without generally questioning the business itself being an object that is assigned to the family. This emphasizes the emerging uncertainty surrounding the intra-family succession regime, which concurrently raised questions on the viability of the habitual mode of ownership transfer. Given the issues of intra-family succession, the solution to the ownership succession problem must be tailor-made to every family business, with one measure being out of the question: “the opening of the family business to the outside” (Wirtschaftswoche, 1990).

As the uncertainty of ownership succession grew stronger, the issue began to be scientifically systemized. The IfM in Bonn, for example, predicted the number of successions expected in the next 5 years based on the number of business owners reaching retirement age (Freund et al., 1995). It thus no longer tied ownership succession to the intergenerational longevity of a business but to the current business owner’s career. 1 This was an important move that already set the stage for redefining the owned object as a life project rather than as a family possession—a notion that we will return to later. In addition, the forecast connected the number of businesses going through a potential ownership succession to the number of employees affected, which was estimated to be up to half a million (Freund et al., 1995, p. 60). This shed light on the macroeconomic dimension of the changing intra-family succession regime and further advanced the idea that ownership succession must function to preserve these businesses. A failed ownership succession in the Mittelstand could turn out to be a severe problem for the German economy.

Through the work of the IfM, the very meaning of the ownership succession problem shifted in light of a predicted succession gap: at the center of attention was no longer the incumbent who is incapable of letting go of control but the lack of successors. The growing number of aging business owners, especially in the baby boomer cohorts, stands vis-à-vis the shrinking number of potential successors. As our interviews showed, this is explained with three main arguments: First, as birth rates stagnate, there are fewer children and hence fewer family internal candidates that could potentially take over. Second, the children of business owners strive for independence and autonomy and are not interested in or qualified for taking over the business. Third, the proclivity for entrepreneurship in Germany is low. The parents, as one interview participant put it, “do not want to impose the burden of entrepreneurship on their children” (B2). The arguments share the perception that the ownership succession problem is no longer an issue of letting go but rather a looming new owner gap.

The IfM forecast functioned as an important tool because it brought public and political attention to the looming wave of ownership transitions, underlining that a large number of aging business owners would soon face the challenge of finding a successor. It pointed strongly to a probable and deeply incisive transformation of family capitalism regarding the owning subject. While family members were still considered the preferred candidates for ownership succession, family-related reasons were given to explain why this family continuity became doubtful. As a consequence, the rhetoric of a successor gap degraded intra-family succession to the less likely option for ownership transfer. The family itself was no longer expected to be the exclusive possibility for the intra-family succession regime but left behind a void in defining a new owning subject. Meanwhile, the expected purpose of ownership succession had also shifted from serving the well-being of the family to preserving the business.

Phase 2: Collective Inquiry: Campaigning and Systematic Intervention

Realizing the practical problems of ownership succession, policy-makers, business associations, and fiduciaries engaged in raising awareness for succession issues. A good example is the “Go NRW” initiative of the Ministry of Economic Affairs in North Rhine-Westphalia in 1996. A business consultant and later professor of family business who was involved in the campaign recalls:

We rented large billboards all over the country, which was highly innovative at the time, and made posters, huge ones. They showed a younger man and a small child, and the small child asked the father: “Tell me, Dad, are you actually already a boss?” Or there was a poster with an older man and a small child, who asked: “Grandpa, why are you still working?” (F2)

This campaign is informative in multiple ways. In terms of content, it underlines several important characteristics of the intra-family succession regime at the time, such as an adherence to the norm of family continuity as the guiding principle in ownership transfer as well as a strong male-centric tradition. It also stresses how strongly ownership succession was problematized in the context of business owners’ reluctancy to organize their stepping down, as argued above. However, the choice of a billboard campaign itself signals the economic dimension and breadth attested to succession as a problem of public interest.

Directly addressing policy-makers, in 1999, another IfM report underlined the severe disruptions to the intra-family succession regime and prompted further collective inquiry: if firms—as expected by the successor gap narrative—could no longer be transferred within the family, an over-the-counter (OTC) market for firm sales could be a viable solution. Although at the time such a market in Germany had already been established with increasing M&A activities, it was not fit for the small- and medium-sized businesses that were affected by the predicted succession gap, as their low transaction volumes were not considered to be profitable. In effect, a “market failure in the field of external business succession” (Schroer & Freund, 1999, p. 82) was the IfM’s conclusion. If one wanted to ensure the continuity of these businesses, as the IfM report implied, an entirely new support structure was needed that allowed business owners to manage their ownership transferred to external buyers.

This paved the way for a visible shift in the enforcement of property rights: while before, ownership succession was enforced informally within the family with on-demand support by fiduciaries, these fiduciaries and business associations now no longer remained in an informing role but rather spread the word about potential dangers of the succession problem, thereby intervening in the field in a more systematic manner. One of our interview participants, who works at a chamber of commerce as a succession advisor, explains: “Until 2000, all the players largely relied on succession being handled somehow within the family. Then, in the early 2000s, the IfM took up the cause and pushed the issue. And that’s how it got flushed into the chambers” (G1). The chambers, business associations, practitioners, and policy-makers began to organize events on succession, where tax advisors, lawyers, and often business owners would teach others how to navigate succession more efficiently and, by informing current business owners, simultaneously campaigned for the topic’s relevance.

This new proactive role of fiduciaries was complemented by a shift in prevailing norms and practices around business succession, which enlarged the pool of potential successors (owning subject). For example, in 1999, the German Chamber of Commerce (DIHK), the Central Association of the German Trades (ZDH), and the Deutsche Ausgleichsbank joined forces to support ownership succession in small- and medium-sized businesses by forming an initiative named “Change/Chance.” They focused on female successors, which stood in contrast to the focus on male successors often found in (German) family capitalism. This included raising awareness both of daughters as potential successors, thus breaking with a strong patriarchal tradition in intra-family succession, and of the many qualified female employees or entrepreneurs who could become future business owners.

In 2001, the then Federal Ministry for Economic Affairs and Technology also began to engage in directly addressing succession issues. It launched the “nexxt” initiative, partnering with the above key associations and organizations to stimulate a favorable climate for ownership succession in Germany. As stated on the initiative’s website in 2002, “nexxt is intended to raise public awareness of the issue of business succession more clearly than before.” 2 What we want to stress here is the scale of collective inquiry into ownership succession that had increased significantly by the turn of the millennium. The activities that were initiated included events and consultancies informing widely about succession and the necessity of succession planning and pushing for potential owners beyond the family to be considered.

Campaigning and collective inquiry led to the expectation that ownership succession entails the practical problem of finding a successor. This expectation turned into a loud call for action and hived off the scientific description of owner succession. An IfM researcher reflects:

After years, economic policymakers and other actors finally became aware of the succession issue and acted. But later I felt as if we had let a genie out of the bottle. The whole thing developed its own dynamic. And the extent of the succession problem became bigger and bigger. (F1)

Remarkably, the various campaigning activities and systematic interventions were carried out by a broad set of actors including the state and business associations but also fiduciaries, who began to actively inform and educate business owners on succession issues. Through these campaigning activities and systematic interventions, the new support structure that the IfM called for began to emerge and the pool of legitimate successors slowly extended beyond the family circle.

Phase 3: Experimenting With New Forms of Ownership Transfer: The Rise of Intermediaries and Matchmaking

During the 2000s, the intense public discourse on succession continued and manifested in a number of policy changes. The most obvious of these changes is the 2008 reform of the German inheritance taxation. This reform was, as others have shown (Berghoff & Köhler, 2020), influenced by major family business lobbying and implemented generous tax exemptions for intra-family business transfers. While this would appear to support an intra-family succession regime, an important change was introduced: the tax exemption was now conditional on business continuity (see §13a and §13b German Inheritance and Gift Taxation Act, ErbStG). This reform thus aimed to maintain family ownership and wealth while at the same time embracing the emerging doubts that intra-family succession is the best solution for the business, as painted in the succession gap narrative. To make use of the tax exemption, business owners now had to prove through wage quotas (a requirement to maintain a certain level of employee wages) and holding periods (a minimum number of years the business must be retained without sale) that the business’s continuity was ensured.

Other policy changes informed by the succession gap narrative are less well known. For example, in 2004, the new Basel II regulations aimed to secure proper banking conduct and prevent bankruptcies by evaluating debtor creditworthiness (see 2006/48/EG of the European Parliament as of June 14, 2006). For small- and medium-sized businesses, Basel II mandated internal ratings considering both hard and soft facts, including succession plans; lacking such plans would reduce creditworthiness, incorporating succession gaps as a risk criterion. Similarly, a large-scale tax reform in 2001 aimed at creating a more favorable investment climate in Germany (see Steuersenkungsgesetz 2001 [Tax Reduction Act]). It also contained a tax break for individuals aged 55 or over for private gains from selling businesses (see §§14–23 German Income Taxation Act, Est).

These policy adjustments manifest the issue of a succession gap and the need to preserve businesses. All these policy adjustments contributed to a reinterpretation of the owned object as a life project rather than a family possession and set the stage for the rise of intermediaries as indispensable agents in the transfer of business ownership, as we will illustrate more in-depth on the last-mentioned tax reform in the following.

Germany’s coalition of the Social Democratic Party (SPD) and the Greens (Bündnis 90/Die Grünen) proposed a large-scale tax reform in 2000. The initial bill was rejected in the Bundesrat—the German federal council—for the way capital gains from business sales was treated in income taxation. In comparison to previous regulations, the new bill no longer included a reduced tax rate for capital gains from private partnerships. However, sales of stocks of a business were tax-free (the capital gains tax was only introduced in 2009). The opposition complained about unequal treatment of business owners across different legal structures and privileges for those owning stock corporations, while small- and medium-sized family business owners were disadvantaged.

3

A revised bill developed through a mediation committee reintroduced the reduced tax rate. New to this adjustment was the condition that the tax reduction could only be used once in a lifetime and by business owners who were over the age of 55 or unfit to work (a condition previously only found in Section 16 of the German Income Tax Act, ESt). Members of the opposition claimed a victory for the German Mittelstand. For example, Hans-Artur Baukhage (Freie Demokratische Partie, FDP, “Free Democractic Party”) explained in the Bundesrat (the Federal Council):

This has a special quality, especially in view of the increasingly urgent issue of business succession, which is of central importance to small and medium-sized enterprises. As of 2001, the transfer of a business to its successor will be much less hampered by the tax burden. And the SME owner who wants to retire in the truest sense of the word will be left with sufficient retirement income from the sale of the business, even after taxes. (Bundesrat 2000, plenary protocol 753, p. 284, own translation)

This quote is exemplary for the overall tone in the plenary debates on this bill. In light of the narrated acute problems of ownership succession, this quote not only underlines that the sale of the business is a legitimate option and the preservation of the business is the ultimate goal but also points to a reinterpretation of the owned object that had been looming since the IfM’s first forecast: the business is no longer expected to be a family possession but the business owner’s life project, meaning that its transfer can be legitimized not only through inheritance within the family but also through its sale as a culmination of personal achievement and a means of securing retirement. Ownership transfer, as the quote implies, is expected to occur at the end of the owner’s career, and the sales proceeds are supposed to fund their retirement. The reduced tax rate linked to a certain age limit is thus seen as a mechanism to ease the sale of a business, and it manifests this reinterpretation of the owned object in the legal structure.

We further argue that this and the other policies provided a legitimate reason for fiduciaries and business associations to seek conversation about ownership transfer with business owners and to develop mediating services, thereby taking on the role of what can now be regarded as intermediaries. While a fiduciary simply assisted during the ownership transfer, an intermediary is an essential third player in this social exchange relationship (Simmel, 1990). For example, for commercial bankers, it became “standard practice to address the issue of succession, in the case of owner-managed businesses, i.e., family businesses” (B4) in the course of assessing the credit rating of a business. The corporate banker no longer acted on demand by the business owner but actively questioned the transfer of ownership. From this position, intermediaries offered to assist business owners in finding a potential new owner through their networks. Eventually, such mediating services grew into an integral part of a new form of enforcement of ownership transfer. Compared to earlier transfer activities, which still focused on intra-family succession, there was now a much stronger reference to matchmaking.

In 2006, the two large succession initiatives “Change/Chance” and “nexxt” joined forces to create a “national exchange platform that bundles all offers and provides a single infrastructure that in the end all businesses can use” (P5). This platform was tailored to find potential new owners for small- and medium-sized businesses. The key idea was to offer a digital infrastructure for contact ads of business owners and potential buyers. Such platforms had been set up previously by “Firmenboerse” (“Firm stock market”) (1995), “Unternehmensbörse GmbH” (“Business Stock Market”) (1997), and “Concess” (1999). These early attempts operated mostly regionally and struggled to gain traction on their sites. The nexxt platform aimed to build a national matching platform for Mittelstand businesses and quickly grew to be the largest business platform in Germany. To appear on the nexxt platform, an advertisement must be entered or approved by these regional partners, meaning that business owners cannot use the platform without being in touch with an accredited intermediary that helps moderate the ownership transfer. This set-up helps intermediaries to enter into a conversation with business owners, allowing them to actively search for potential new owners.

Today, business owners can rely on a mature support structure that positions intermediaries as an indispensable part of ownership transfer. The coordination of ownership no longer only occurs within the family, assisted by fiduciaries, but is increasingly mediated by advisors, industry associations, banks, and platforms. If they need to, business owners can join regional transfer networks and clubs (e.g., the Nachfolgenetzwerk [“Succession-Network”] in the federal state of Baden-Württemberg), gather information through transfer events and reports (e.g., Nachfolgemonitor [“Succession Monitor”]), use consultations offered by their chambers of commerce (e.g., Stabwechsel [“Change of Baton”]) or business consultants (e.g., Nachfolgeexperten e.V. [“Succession experts”]), and when searching for a potential new owner beyond the family, they can use online platforms to find a suitable candidate or hire a specialized broker. As soon as the infrastructure was set up for matchmaking in this way, the professionalization of an OTC market specific to family-owned firms was only steps away. Instead of being a private family affair, ownership transfer thus became an increasingly managed, professional service, similar to real estate or financial advising. This marked a shift from informal, family-centered practices to a more standardized, expert-led process of ownership transfer—turning what was once a personal transition into a semi-institutionalized market supported by professional intermediaries.

Phase 4: Norm Substitution: Reframing New Owners From Next Generation Family Members to “Founders”

Although policy-makers and intermediaries had long embraced the succession problem and provided a complex support structure, the willingness of business owners to engage publicly in the topic of ownership transfer only reignited in the 2010s. While attendance of events in the years before was slow and offers of consultancy were rarely used, things now changed. For example, one of the business consultants we interviewed recalls:

We had a big conference in Munich, there sat about 800 business owners in a room. And at the opening event, the moderator asked: “So, business succession is a big topic. How many of you are currently dealing with it, for whom is it currently an issue?” And that’s when at least a third of the hands went up. I mean, five years ago, nobody would have dared to do that. (B3)

This quote illustrates how, after decades of campaigning, interventions, and policy adjustments, the taboo around talking publicly about one’s succession problems had been broken. Another interview participant reinforces this notion, elaborating that “the willingness to openly communicate this [succession] to the outside world has increased significantly” (P4). The coordination of ownership transfer had escaped the secrecy within the family and become a topic that business owners regularly discussed with business intermediaries and their peers. The constant confrontation with the topic in conversations with business intermediaries and in the public discourse paved the way for this new openness of business owners to talk about ownership transfer and consider alternatives to intra-family succession, including selling the business.

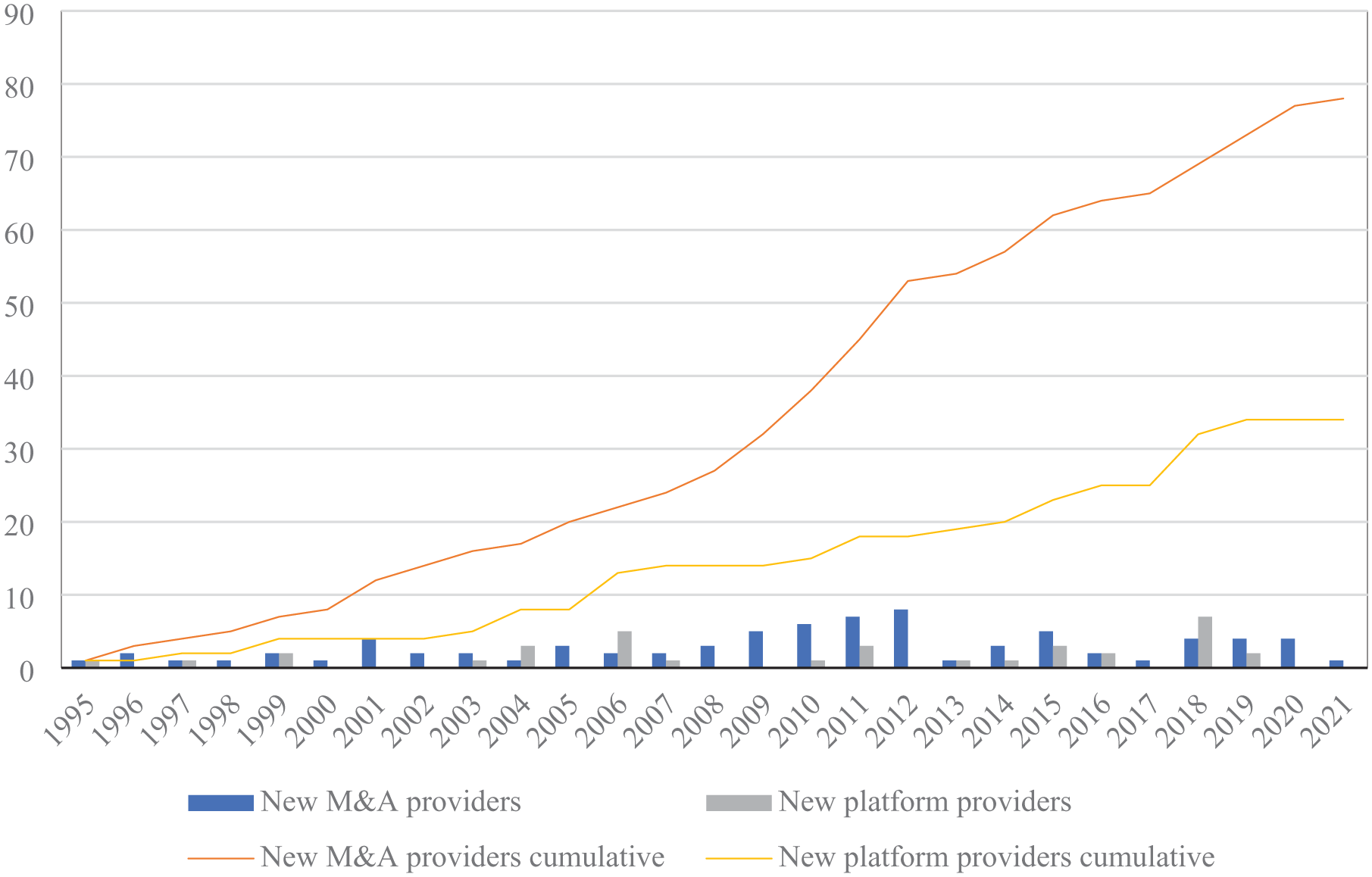

A number of intermediaries viewed this new openness toward selling the business as an opportunity. The market for advising on ownership transfer developed into one of the fastest-growing segments of the consulting market (Murmann, 2019), and more and more intermediaries became engaged in the expansion of the market for OTC sales of family-owned businesses. For example, during the 2010s, the numbers of M&A advisories that specialized in the Mittelstand grew substantially, as did the number of firm platform providers (see Figure 1). For the year 2021, we could identify 78 M&A advisories active within the German Mittelstand as well as 34 firm platform providers. Accordingly, one of our interview partners who operates such a platform explains that “the M&A consultants are increasingly trying to create their own platforms (. . .) and then generate their business through them” (P2).

Development of M&A Providers and Platforms for Business Sales From 1995 to 2021.

On the rise were also private equity investors that had discovered the succession problem as an investment opportunity. A textbook example is the Droege Group, a family business founded in 1988 which successfully capitalized on the idea of the succession gap as a business opportunity. At an early stage, they offered private equity to Mittelstand businesses—arguing that as a family business themselves, they understood the culture and goals. As Boehm (2020, p. 230, own translation) has shown, today “it is impossible to imagine the German succession market without private equity companies.”

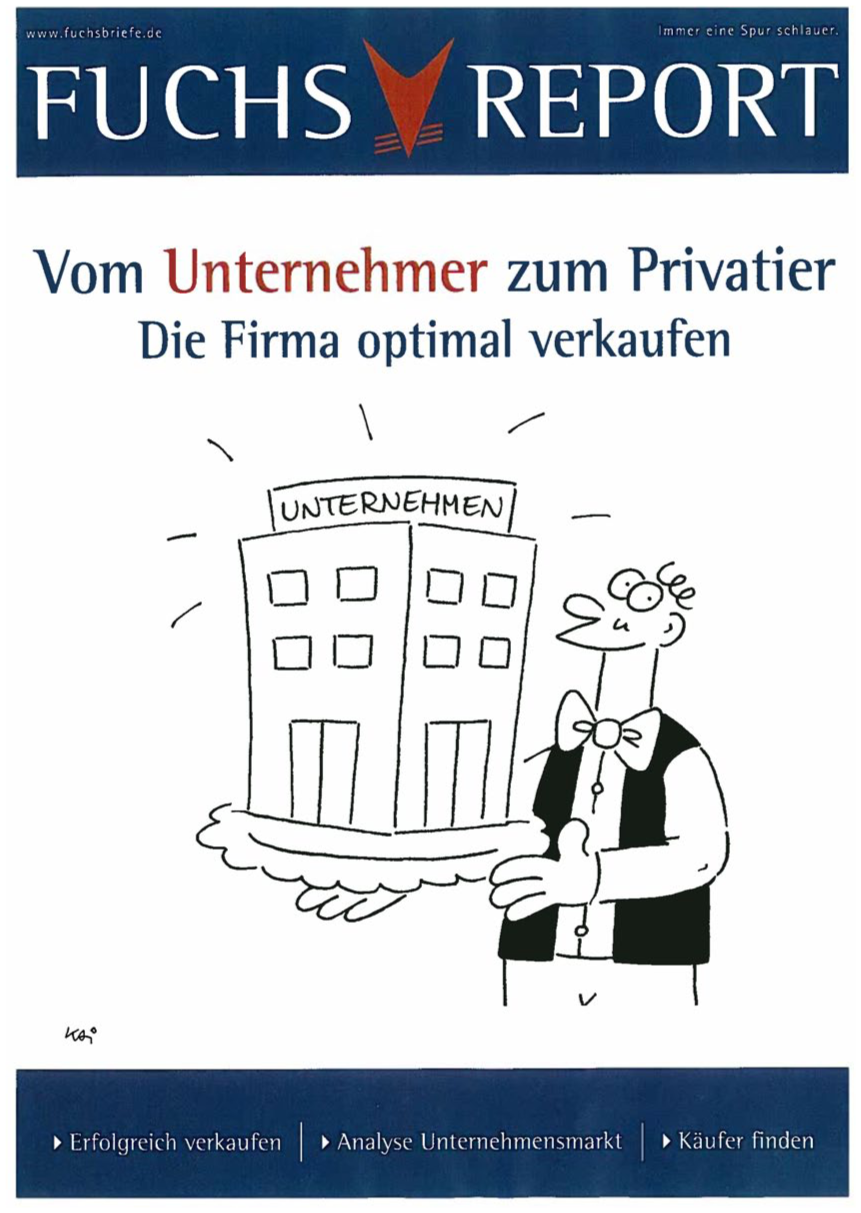

At this point, it becomes clear that the relationship between family ownership and financialized ownership is being reconfigured, and the intermediaries of ownership transfer are now in a powerful position to reinterpret the very nature of ownership in this context. We particularly observe a reinterpretation of the owning subject, who now turns from being a person reluctant to let go and without any family successor into a successful entrepreneur who makes a sensible economic decision in selling the business. The cover shown in Figure 2 of the practitioner-oriented business magazine Fuchs Report from 2011 playfully depicts this reinterpretation. It shows a middle-aged man (the business owner), dressed up for a special occasion, presenting the sparkling business like a fancy cake on a silver platter. This depiction emphasizes the task of presenting the business at a particular point in time and to the taste of a potential buyer. The headline reads, “From entrepreneur to privatier—how to sell the business best.” This quote hints at the wealth business owners might expect once their sale has been accomplished, whereupon a life as a privateer will allow them to live off their dividends and asset gains (Christophers, 2020).

“From Entrepreneur to Privatier”.

This new interpretation of ownership transfer focuses on the moment of transfer and frames the selling of the business as an act performed by a competent entrepreneur. One of our interview participants referred to selling one’s business as “a healthy entrepreneurial action” (B3) and viewed the business sale as “a truly economic action, in which one of course seeks their own benefit” (B3). The business owner is no longer narrated as being reluctant to let go but as harnessing an entrepreneurial opportunity. With the sale becoming an entrepreneurial act, ownership transfer in the form of a business sale becomes linked to an exit orientation previously only known from the start-up scene.

As ownership transfer turns into an entrepreneurial opportunity, the new owners are similarly placed in an entrepreneurial context. Buying a business is thereby perceived as a form of “founding” in no way inferior to starting a business. The boundaries between these two forms of entrepreneurship are continuously blurred. For example, a recent brochure by the nexxt initiative reads, “No matter if you found a new business or take over an existing one [. . .] you are a founder.” With no differentiation made between these two categories, new business owners also appear more willing, credible, and competent than before. The transfer of ownership has now completely lost its attachment to the family and its continuity; in its place steps a strict focus on business continuity, with transfer being an entrepreneurial milestone in managing and building a healthy business.

Finally, the exit orientation is also apparent in a new emphasis on the financial aspects of business sale, pointing toward a new articulation of use: the well-being of the entrepreneur. Our interview partners connected a high sale price with the fulfillment of individualized life plans (e.g., traveling the world, buying a boat) or with funding a comfortable retirement. For example, they describe how these business owners “want to be sure that they are well provided for financially” (P6), they want to “enable themselves to make a living privately” (B2), or they “just want to have a few more good years” (M&A3). On the websites of business platforms or in newspapers, the sale of a business is often accompanied by pictures of yachts, golf clubs, or sports cars, suggesting that selling the business could make business owners rich and give them the life of a privateer. 4 Remarkably, this financial prosperity is portrayed on the level of the exiting individual and not as family wealth.

Discussion

The Reconfiguration of a Transfer Regime

This article set out to understand a puzzling empirical observation on ownership succession in Germany: while selling a business outside of the family was seen as taboo for decades among family business owners, in the late 2010s, a majority of family business owners could imagine doing just that and continue to do so (Evers, 2024; Schwartz, 2019). We proposed to approach this puzzle from the perspective of a sociology of ownership, which views intra-family succession as a particular ownership transfer regime, which changed across time—and we offer a multi-level explanation of how this regime gradually changed.

More specifically, we show how the intra-family succession regime was critiqued across five dimensions and next-best solutions were found, which eventually constituted a new transfer regime, which we call the exit regime (as depicted in Table 2).

First, we show how the family as the owning subject was increasingly questioned starting in the 1990s: The older generation is portrayed as unable to manage the transfer process, while the succeeding generation is portrayed as unwilling to take over or does not exist due to family demographic changes. At first, this void is tackled by expanding the circle of potential owners within the family (e.g., to daughters) and later to external candidates. It is only in the 2010s that this void was filled with a reframing of the owning subject as individual “founders.”

Second, the owned object continues to be the business but is no longer viewed as an object that needs caretaking by the family (Berghoff & Köhler, 2020) but is now seen as the result of entrepreneurial efforts and managerial skills, a token of a life project of the “founder.” As such, the business remains personalized and is not fully financialized (Carruthers, 2015; Krippner, 2011).

Third, the articulation of use stood in the tradition of steward ownership, which required the family to put their needs behind the growth and development of the business to secure the family’s long-term well-being (Berghoff & Köhler, 2020; Lehrer & Celo, 2016). Later, however, the business owners, who secure preservation of the business, can make claims on control of the business, including any residual income achieved through its operation but also through its sale.

Fourth, we observe how the role of intermediaries in enforcing ownership transfer has changed substantially. While in the intra-family succession regime ownership transfer is a family internal affair only supported by fiduciaries, in the exit regime intermediaries turn into indispensable match-makers of ownership transfer (Bessy & Chauvin, 2013). These match-makers promote and professionalize a market for selling privately owned businesses.

Fifth, the mode of ownership transfer shifts from an intergenerational transfer within the family that is organized via gifting and reciprocity to a coordinated matchmaking of current and future “founders” on a market for privately owned firms. The sale of business as a particular form of exit (e.g., Wennberg & DeTienne, 2014) is essential to this new mode of ownership transfer.

Research shows that with the rise of this exit regime, indeed, the number of business sales has increased by 80% between 2001 and 2018 (Stamm et al., 2023). Exit captures the focus on the owning entrepreneur, who leaves the business to transition into retirement or to new ventures, and it captures the focus on the continuity of the business, which continues to exist even after its owning entrepreneur has exited. In the exit regime, the act of selling the business is no longer viewed as leaving the firm behind but as the ultimate entrepreneurial act. Exit is followed by the entrance of a new “founder”-figure, who continues to grow and nurture the business. The norm of intra-family succession thus shifts to a new norm of “founder” succession.

It is important to note that the term “founder” for the new owning subject and central figure in the exit regime is an in vivo code and thus reflects the terminology used in the field. The notion of a “founder” is used across the documents and interviews we analyzed and therefore plays a significant role in reframing the acquisition of business as in no way inferior to starting an entrepreneurial journey of one’s own in the common sense of the word. We thus adopt the term but use it with quotation marks to highlight its different semantic. It is particularly noteworthy that these new owners are not referred to as buyers, which would imply a market logic. Rather, the use of the term “founder” points toward a renewing of the business as an entrepreneurial venture. This reframing embraces norms of individualization (Beck, 1992) and cultivates entrepreneurialism (Brattström, 2022).

Contributions

We offer two main contributions: First, we introduce the sociological concept of transfer regimes to the family business field. In doing so, we show that intra-family succession is not only embedded in an institutional context (Widz & Kammerlander, 2023; Wiklund et al., 2013), but is itself constituted as an institutional configuration subject to change. An institutional change of a transfer regime involves a substantial change of the rules of the game (Carruthers, 2012; Widz & Kammerlander, 2023) and concludes when all dimensions of the regime have undergone transformation. As demonstrated in this article, this change relies on the critique and renegotiation of existing definitions, necessitating the search for next-best solutions (Beckert, 2009).

Second, our sociological approach enables us to identify and elucidate the dynamics of institutional-level change concerning ownership transfer regimes in the case of Germany and thus enriches a theoretical debate on institutional change (Carruthers, 2012, 2015; Fligstein & McAdam, 2012; Scott, 2001). We demonstrate how critique of various aspects of intra-family succession prompt alternative solutions and transform the expectations, norms, and regulations governing ownership transfer regimes. This reconfiguration occurred through intermediate steps (as highlighted in Table 2) and involved a new solution to the fundamental coordination problem underlying ownership transfer, that is, the matching of incumbent and succeeding owner. Highlighting this shift and its underlying structure does not ignore that many businesses are still transferred within the family (or that business has been sold before); however, intra-family succession is now expected to be problematic and requires additional legitimation, while selling the business as a form of ownership transfer has gained legitimacy. Micelotta et al. (2017) refer to this transformative change as institutional accretion: a change that is slow in pace but forceful in its scope. This institutional change serves as part of the institutional embedding for individual decision-making on ownership transfers.

In addition, we highlight the crucial role of fiduciaries, who articulate critiques of intra-family succession and contribute to the emergence of essential intermediaries for ownership transfer. While previous studies have focused on the involvement of intermediaries in individual succession processes (Bertschi-Michel et al., 2021), our research emphasizes the varying influence of intermediaries across different transfer regimes. In the emerging exit regime, an ownership transfer without the use of an intermediary becomes virtually impossible. Intermediaries are needed to educate business owners about the ownership transfer, search for a match, support the sales process, and assist in post-sales reorientation. With the shift from a succession to an exit regime, the transfer of business ownership is commodified (Carruthers & Ariovich, 2004; Davis & Kim, 2015) and now coordinated through match-makers, which puts the matchmaking intermediaries in a powerful position.

Implications

This new understanding of intra-family succession as a specific transfer regime comes with implications for research on family business, practitioners, and policy-makers. This understanding elevates the level of analysis to focus on the expectations toward ownership transfer regimes as institution (Widz & Kammerlander, 2023; Wiklund et al., 2013). This institution is malleable. Future research on family businesses should be more cautious in presupposing the intention to pass on a business within the family (Chua et al., 1999; Gersick et al., 1997; Haag et al., 2023; Miller & Le Breton-Miller, 2005). Rather, the expectation to pass on a business within a family lineage, and the associated long-term outlook of family businesses, is a social construct tied to a specific institutional configuration, or in other words, a specific ownership transfer regime. Future research needs to look into this relationship more closely and critically, asking under what conditions a multi-generational outlook in family businesses arises. For example, the concept of socio-emotional wealth embraces a long-term outlook of the family as a key feature of family businesses (Gómez-Mejía et al., 2011). This concept was originally developed with regard to families owning oil mills in Spain (Gómez-Mejía et al., 2007) and has since developed into a general approach to studying all family businesses (Swab et al., 2020; Wu, 2018). This means the assumption that all families seek a long-term attachment of their family to the business has been transported to other contexts—such as different countries, industries, or policy environments—where different transfer regimes may in fact apply. In sum, we suggest that this assumption should be treated with more sensitivity to historical and regional contexts.

Furthermore, the understanding of fiduciaries and intermediaries as change agents implies that intermediaries play a more important role in ownership transfers than previously assumed. Lawyers, tax consultants, and M&A advisors have always supported ownership transfer (along with their strategic interest to be involved in these transfers). However, when matchmaking rather than intra-family succession turns into the expected way of how to coordinate ownership transfer, these advisors turn into an indispensable element of ownership transfer. As such, business owners become dependent on the expertise and network of advisers, which puts the advisors in a powerful position. Future research should thus reflect more closely on the status of advisors in the transfer process. This calls for an explanation of which cultural and contextual factors enable advisors to turn into indispensable intermediaries, as well as a critical reflection on how their power is used.

The developments uncovered in our study shed light on ongoing transformations in ownership transfer practices and offer important insights for how such transfers may continue to evolve in Germany. It is likely that we will continue to see a growing preference for passing on a business beyond the family and a high demand for new “founding-owners.” This not only creates more opportunities for intermediaries who are interested in purchasing businesses but also creates new power structures that may potentially shift the composition of the business-owner population in Germany. It is important to acknowledge that this shift is still ongoing. Its possible course can be influenced by various factors, especially with regard to the ongoing normative negotiation of the owning subject and the enforcement of ownership transfer. If the businesses for sale are bought by “founders,” that is, private individuals and their families who are committed to the development of the business, the current imaginaries of the exit regime are substantiated and reinforced. If, however, these imaginaries remain fictions, and the businesses are bought by financial market actors such as private equity investors, the new exit regime may bring greater instability, as short-term investment logics could lead to more frequent restructuring, ownership turnover, and weakened commitments to long-term business development. Given that new owners are likely to change the face of business ownership in Germany, policy-makers should monitor to whom businesses are sold. In any case, the shift toward an exit regime shortens the time frame of business owners from thinking along generations and lineages to thinking in terms of one’s own career and a potential new owner, or even more short-term thinking in terms of the most lucrative exit. This shorter-term perspective of business owners may have consequences on the risk-taking and resilience of businesses, as owners may prioritize immediate profitability over long-term investments, be less willing to engage in innovation with delayed returns, and reduce commitment to workforce development or regional ties, all of which can weaken a firm’s ability to weather economic shocks or adapt to structural change.

Limitations, Future Research, and Conclusion

While our study is based on a rich body of material that covers a time span from the late 1980s until 2023, it also comes with a number of limitations. In our accounts of business owners, advisors, and policy-makers, we had to rely on interviews conducted in the present or on past reports about ownership transfer published in the media or materialized in process-generated data. Ideally, this study could have also included historic ego-centered materials such as interviews conducted on succession in the 1990s or personal accounts in letters or other archival material. This study also is limited in its time and geographic reach and could be complemented by a comparative design that either goes further back in time or systematically compares other countries or regions. Such comparisons could help identify whether the observed shift toward an exit regime is specific to reunited Germany or part of a broader trend and how different economic, cultural, or policy contexts shape ownership transfer regimes.

Future research dedicated to ownership transfer regimes as institution that can be shaped in various institutional configurations could map the world regions, where succession vis-à-vis exit regimes are present—or maybe even other types of transfer regimes—and how they changed across time. We thus call for more comparative and historically informed research in family business (Evert et al., 2015; Rovelli et al., 2022; Suddaby et al., 2023), as such studies can be informative to identify various configurations of transfer regimes and how these structure different decision-making processes in family businesses. In the United States, for example, a similar problematization of intra-family succession can be observed in the 1980s. Comparative research could study if and how this problematization shifted the transfer regime in the United States—and how their pathway differs from the one in Germany or other countries.

We further call to investigate the consequences of the shift in transfer regime. In particular, more research on the reproduction of private ownership of businesses through matchmaking is needed. These matches will define the future ownership structure of the business population. This endeavor is challenging, as business exits are not currently monitored, and to the best of our knowledge, there is no data set available that provides information on who purchased businesses. Future research should study if this shift goes along with a concentration of ownership, a new time perspective of new business owners, or effects on the resilience and risk-taking of businesses.

To conclude, we detect an institutional shift in transfer regime, which can be described as a slow-paced bottom-up process driven by the accumulation of uncoordinated actions and seemingly inconsequential changes in interactions. During this shift, the expectation to transfer a business within the family is increasingly questioned and replaced by an openness to find an external new owner match. Intermediaries turn into indispensable change agents as they coordinate matchmaking. This slow shift in transfer regime undergirds field-level transformations that may have major consequences for businesses, the economy, and society.

Footnotes

Appendix

Coding of the Dimensions of Transfer Regimes.

| Owning Subject | Family | My father said “Huh, why is my eldest leaving me in an hour of need? I actually need him”. So. Then my sister was called, but she waved it off and said “Nah, entrepreneurship isn’t my thing”. Then there was only one left. First, my father called me and said “You have to do this now”. You have to do it, mind you. And then I thought about it for two weeks and said “Okay” (P6_I1, pos. 9) |

| Then there’s always the issue of family. Do I have children? To what extent do I see them as suitable to continue the business? To what extent do they want it? To what extent have we ever even talked about it? What happens if I ask them now and who feels obligated and in what way? (P4_I1, Item 63) | ||

| Because the entrepreneurs often also had an expectation that their children should do the same. (G1_I1, Item 30) | ||

| Successor Gap | However, the conditions for company succession in small and medium-sized enterprises have changed. Many companies are still passed on within the family. But more and more often, daughters and sons have other career plans and want to have more time for themselves and their own families. (19_12_DLF, p. 3) | |

| What we are noticing is that family businesses in different generations now increasingly want to work with us because it is no longer as common as it used to be for the children to automatically take over everything. (M&A3_I1, Item 33) | ||