Abstract

Despite significant discussion surrounding the benefits of family social capital in family business research, precisely how it is built and maintained by enterprise families remains unclear. To explore how and when family governance practices can avoid the decay of enterprise family social capital, we examine the mediating role of family identity and the significance of both generational and business ownership. Testing of our moderated mediation framework using data from 175 enterprise families globally suggests that family governance can stimulate family social capital by strengthening family identity. We also find a negative moderating role for business ownership in this indirect relationship.

Introduction

I expect our modus operandi will continue harmoniously through this next generation. It’s not money . . . It’s just this personal, vicious anger they have . . . It is so emotional, you can’t believe it. It’s what hate does.

Family business research has focused extensively on understanding how families can ensure the success of their business (e.g., Le Breton-Miller & Miller, 2018; Simarasl et al., 2020; Tognazzo & Neubaum, 2020). Highly successful business families have been found to evolve into enterprise families as they share ownership of multiple assets (e.g., investments or real estate) and multiple entities (e.g., a family business, family office and/or family philanthropic foundations) across multiple generations (De Groot et al., 2022). The enterprise family concept is distinct from that of a business family in that a family enterprise does not necessarily include a family business. Research has shown that transgenerational success is not easily achieved by enterprise families (Williams & Preisser, 2003) and has highlighted that maintaining family social capital is imperative for enterprise sustainability (e.g., Berent-Braun & Uhlaner, 2012; Suess-Reyes, 2017). Family social capital is a form of internal social capital (Carr et al., 2011; Nahapiet & Ghoshal, 1998; Pearson et al., 2008) that alludes to the goodwill between family members (Adler & Kwon, 2002) and refers to the functionality of a family with regard to the quality of interpersonal relationships, common understandings, and a shared purpose (Adler & Kwon, 2002; Nahapiet & Ghoshal, 1998).

The erosion of family social capital in enterprise families has been demonstrated to occur naturally as the family grows (Lim et al., 2010). With the passing of generations and increasing number of offspring, family members no longer share similar childhood experiences, are typically dispersed both geographically and in age, and may, for instance, possess diverse experience, schooling, culture, and ethical values (Gersick et al., 1997). Such diversity is problematic because the transgenerational preservation of a family enterprise requires a functioning family system (Zachary et al., 2013). For instance, consider the multibillion-dollar Pritzker family empire, which was started from scratch in the early 1900s and broke apart spectacularly approximately a decade ago. Employing multiple lawyers to keep the family fight in closed courtrooms away from the public gaze, the heirs to the Pritzker fortune sued each other after allegations of plundering of family trust funds and mismanagement of the family’s vast portfolio of companies, including the Hyatt hotel chain, several cruise lines, and interests in the tobacco industry (Andrews, 2003; Chandler & Bergen, 2005; Das, 2013). Diverging interests and failure to communicate had led to splits within the family and eroded trust between the various members of this enterprise family.

The literature has focused on different elements related to family social capital, mainly the outcomes (e.g., Berent-Braun & Uhlaner, 2012; Herrero & Hughes, 2019) and conceptual properties (e.g., Arregle et al., 2007; Pearson et al., 2008). Less attention has been paid to the mechanisms that generate family social capital (De Massis & Foss, 2018; Long, 2011; Schmidts & Shepherd, 2015; Zellweger et al., 2019). In part, this gap stems from the tendency for the research to focus on small firms and early generation families in which there is a natural potential for strong family bonds (Distelberg & Blow, 2011; Klein, 2008; Le Breton-Miller & Miller, 2018; Miller et al., 2007). Albeit scarce, research considering the drivers of family social capital has pointed toward the family governance system (Mustakallio et al., 2002). Thus, research has neglected to explore family social capital decay and the strategies that enterprise families adopt to prevent this degeneration and how they maintain and enhance their family social capital.

This study provides several theoretical contributions to family business research. First, we advance research on family social capital by contributing to the development of an identity perspective of family social capital formation in enterprise families; that is, drawing on identity theory (Albert et al., 2000; Albert & Whetten, 1985; Ashforth et al., 2008), our study highlights family identity as a mechanism through which the family governance system affects enterprise family social capital, thus, opening the black box of the governance–family social capital relationship. By looking at how enterprise families can maintain social capital over time, we complement work done by Suess-Reyes (2017) on transgenerational orientation.

A second contribution is that we shift attention from the business to the family to understand the preservation of family social capital over multiple generations. While previous research has focused on family social capital as manifested in the business (Carr et al., 2011; Pearson et al., 2008), our study proposes that it is important to consider the governance system of the family behind the business to understand family social capital in enterprise families (Berent-Braun & Uhlaner, 2012; Gersick & Feliu, 2014; Suess, 2014; Suess-Reyes, 2017). Our focus on the family unit of analysis and specifically transgenerational enterprise families complements emerging literature on family firm heterogeneity in relation to social capital (Sanchez-Ruiz et al., 2019) by looking beyond the assumption of naturally existing strong bonds in small families as well as previous social capital literature that had tended to focus on early generation families (Distelberg & Blow, 2011; Klein, 2008).

Third, we advance family business research by considering the boundary conditions of the ability of governance to enhance family social capital. Specifically, through our identity lens, we highlight the contingency role of two types of ownership: generational ownership, which refers to the number of generations that share ownership of the enterprise family, and business ownership, which refers to whether an enterprise family owns a business. By considering the contingency role of generational ownership, we answer calls for the incorporation of the temporal context in the development of social capital (Gedajlovic et al., 2013). In addition, we advance previous insights that generational ownership affects decision-making in families (Eddleston et al., 2008) by considering how generational ownership affects the extent to which the family governance can be used to form a family identity. Furthermore, our focus on business ownership addresses the lack of understanding as to how family governance and ownership jointly determine family social capital (Gersick & Feliu, 2014; Suess-Reyes, 2017). By analyzing the contingency role played by ownership, our study answers a call for more research to open the black box of building and maintaining family relationships (Zellweger et al., 2019).

Overall, we test the proposed moderated mediation framework on proprietary data from a sample of 175 enterprise families from 27 countries on five continents with wealth in excess of US$30 million. We find empirical support for the notion that family governance practices can enhance family social capital. Furthermore, our empirical results suggest family identity mediates the relationship between family governance and family social capital. In addition, we find that the mediating effect of family identity is weaker in enterprise families with greater business ownership. However, we do not find empirical evidence to support the notion that generational ownership plays a moderating role in the mediating relationship of family identity. Ergo, we underscore the importance of considering both mediating and moderating effects to enhance understanding of how enterprise families may reinforce their social capital.

Theory and Hypothesis Development

Family Social Capital

Social capital generally refers to “the goodwill available to individuals or groups. Its source lies in the structure and content of the actors’ social relations” (Adler & Kwon, 2002, p. 23). As an umbrella concept, social capital encompasses all the resources that reside within relationships, including trust, cohesion, shared meanings, and norms (Kwon & Adler, 2014; Nahapiet & Ghoshal, 1998); these elements have been found to facilitate the pursuit of common goals (Adler & Kwon, 2002; Pearson et al., 2008) and strengthen the will of the group to pursue these goals (Suess-Reyes, 2017). Scholars have argued that social capital is advantageous as it generates specific resources, reduces transaction costs, and facilitates knowledge sharing, including transmission of tacit knowledge (Nahapiet & Ghoshal, 1998; Pearson et al., 2008). Social capital is an inherently multilevel phenomenon of interacting individuals nested in groups or networks within larger social aggregates (Payne et al., 2010). Accordingly, scholars have conceptualized social capital on the individual level through repeated exchange (Long, 2011), rational choice theory (Ostrom & Ahn, 2003), and as a resource made available to individuals by way of network closure (Coleman, 1988) all the way to up to large social aggregates such as class (Bourdieu, 1986) and civic society (Putnam, 1995).

Family business literature has suggested that family social capital is a distinct and especially potent form of social capital (Carr et al., 2011; Pearson et al., 2008) due to kinship ties, long-standing relationships dating to childhood, and the family enterprise’s shared history (Herrero, 2018). Family social capital refers to family functionality, shared understanding, and interpersonal relationships (Adler & Kwon, 2002; Nahapiet & Ghoshal, 1998). The concept is particularly relevant in the context of family businesses, as family social capital has been suggested as a source of distinctive familiness (Pearson et al., 2008), a transgenerational orientation (Suess-Reyes, 2017), a lack of adaptive capacity (Chirico & Nordqvist, 2010), or the transmission of dysfunctional aspects of family culture (Arregle et al., 2007; Kidwell et al., 2018). The lengthy and stable time horizons needed to develop family social capital (Arregle et al., 2007; Herrero, 2018; Pearson et al., 2008) have been found to be consistent with the notion of social relations as accumulated history that cannot be reduced to interaction on an individual level (Bourdieu, 1986); it is in this sense that we analyze group level antecedents concerning social capital.

Although limited, research on the antecedents of family social capital has highlighted the importance of the family governance system (Sundaramurthy, 2008). The family governance system is a set of principles, policies, and rules followed by family members, which outline how various activities should be conducted to achieve the goals of the extended enterprise family (Angus, 2005; Berent-Braun & Uhlaner, 2012; Brenes et al., 2011; Kammerlander et al., 2015). Family governance practices are voluntarily mechanisms instituted at the family level that provide the structural settings in which interactions can take place (Suess-Reyes, 2017; Sundaramurthy, 2008). However, while previous research has highlighted the importance of family governance, there remains a lack of theoretical development and empirical investigation regarding the mechanisms through which the governance system affects the family’s social capital.

The literature has argued that social capital develops through repeated exchange (Arregle et al., 2007; Gudmunson & Danes, 2013; Long, 2011), that it exists on multiple levels and that it is the product of iterative processes occurring over time (Gedajlovic et al., 2013; Long, 2011). Family governance can shape individual relationships while individuals simultaneously create the relational governance through their relationships (Ostrom & Ahn, 2003; Uzzi, 1996). We acknowledge this bidirectionality in the relationship between governance and social capital, however, as the aim of our study is to understand how enterprise families prevent the decay of social capital, we are most interested in the direction of causality from governance to social capital.

While we know that family social capital is important for the functioning of the family, there is a lack of understanding regarding how the decay of family social capital can be prevented. In this study, we propose an identity perspective to improve understanding as to why family social capital erodes and how enterprise families can prevent this erosion over time.

An Identity Perspective on the Formation of Enterprise Family Social Capital

Identity has been empirically positioned as a precursor of organizational phenomena; a precursor that includes the elements of trust, norms, and the willingness to subordinate ones’ individual objectives for the benefit of the group (Borgen, 2001; Kramer, 2006; Kramer et al., 2001; Lewicki & Bunker, 1995; Ravasi & Schultz, 2006). Given that every organization has some concept of self-definition and how it relates to others, identity and identification are root constructs (Ashforth et al., 2008). An expansive list of both individual- and organizational-level identity outcomes have been identified, such as sense-making, affectional commitment, cooperation and engagement, information sharing, coordinated action, intrinsic motivation, social support, trust, perceptions of procedural justice, and personally costly citizenship behaviors (Ashforth et al., 2008). “Identity and identification are powerful terms because they speak to the very definition of an entity—an organization, a group, a person” (Albert et al., 2000, p. 13).

While at first, the family—particularly the founder—influences the identity of the business (Whetten et al., 2014), in the next stage, the situation reverses, as the family increasingly adopts the identity of the business (Wielsma & Brunninge, 2019; Zellweger et al., 2013). At later generational stages, enterprise families become blended, or hybrids, between an organization and a family. That is, enterprise families are not just about the family business anymore and take on organizational features themselves (Suess-Reyes, 2017; Uhlaner, 2006). For instance, in adopting family governance mechanisms to enable communication and decision-making, enterprise families become organization-like entities on the family level, defined by the entirety of their activities and assets, which act in pursuit of a specified purpose such as transgenerational wealth (De Groot et al., 2022).

While family size and complexity is not necessarily a linear process (Lambrecht & Lievens, 2008), enterprise families increasingly become like a business themselves (Litz, 2008). The very definition of the family itself becomes more complex. Such extended families are inherently political structures that are more like clans than families in the classic sense (Gersick et al., 1997). Hence, enterprise families constitute a hybrid identity system because of the interplay between the social identity and the organizational identity of the family exhibiting both individual and organizational features.

In transgenerational enterprise families the number of passive owners has been shown to increase over time as only a minority of family members are bound to have direct professional involvement in the enterprise (Le Breton-Miller & Miller, 2013; Sciascia et al., 2014). Identification brought about through elements such as family history can change the relationship of passive owners to the enterprise. Family identity elevates enterprise ownership from a functional notion of owning shares to a sense of emotional ownership whereby meaning is assigned to the enterprise (Waldkirch, 2015). At its core, the concept of identity concerns a shared understanding of “who we are” as a group and on the individual level the meaning that individuals assign to their membership of that group (Albert & Whetten, 1985, p. 220). The concept of family identity refers to the individual family members’ perceptions of belonging to the family social group (Ashforth & Mael, 1989). The family identity can lead to a shared sense of the family’s distinctiveness, endurance, and stability over time (Albert & Whetten, 1985), and creates central characteristics through story-telling and artifacts (Wielsma & Brunninge, 2019; Zellweger et al., 2013).

In other words, family identity is the mechanism that makes family members attached to the family enterprise. We explore strategies that enterprise families adopt to prevent family social capital decay and propose that the relationship between family governance and social capital in transgenerational enterprise families is mediated by family identity.

Family Governance and Family Social Capital: The Mediating Role of Family Identity

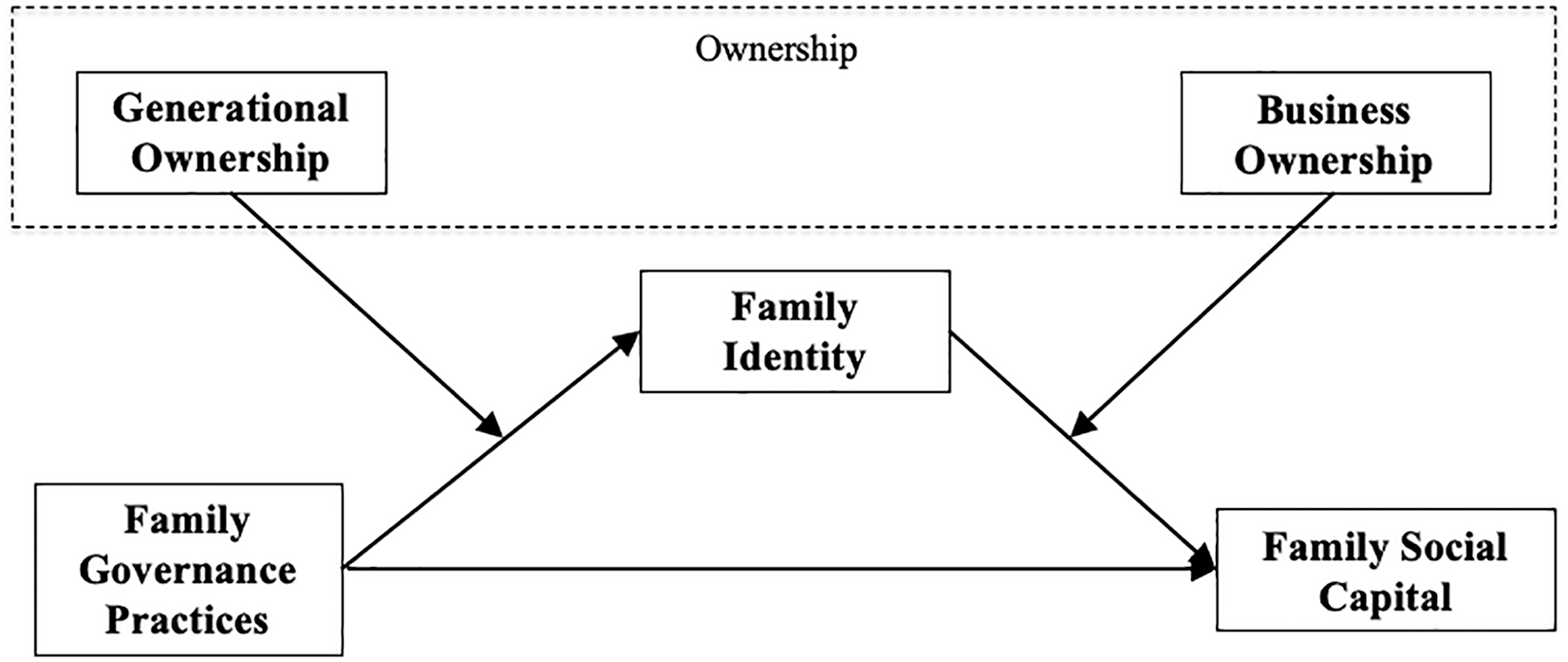

We propose that family governance practices can enhance family social capital through strengthening of the family identity. That is, there is a two-step process in which governance strengthens the family identity and family identity then further enhances the family’s social capital (see Figure 1).

The Conceptual Model: A Moderated Mediation Framework

The family governance system can stimulate a family identity for several reasons. After a multigenerational enterprise family reaches a certain level of complexity, more formal mechanisms are required to organize family interactions as well as the family’s relationship with the enterprise (Mustakallio et al., 2002). The most common family governance practices are family meetings, the family council, and the family constitution (e.g., Berent-Braun & Uhlaner, 2012; Mustakallio et al., 2002; Suess, 2014; Suess-Reyes, 2017; Uhlaner, 2006). Family meetings are recurrent formal or informal gatherings of family members where important matters relating to the enterprise are discussed (Habbershon & Astrachan, 1997). Family meetings have been found to contribute to creating shared beliefs (Habbershon & Astrachan, 1997) while simultaneously providing opportunities for social interaction. A family council consists of selected and elected representatives from different branches and generations of the family who develop an enterprise strategy and make decisions as a unit (Berent-Braun & Uhlaner, 2012). A family constitution is a jointly designed charter of principles and guidelines in which the family outlines rules, rights, and obligations (Berent-Braun & Uhlaner, 2012) as well as articulating its collective values (Botero et al., 2015). These protocols enhance trust and alignment (Botero et al., 2015). Family governance practices hold great potential to help enterprise families to unlock resources that will influence within-family exchange.

Family governance practices can enhance family identity because they enable ongoing communication (Suess-Reyes, 2017; Sundaramurthy, 2008), relationship building (Mustakallio et al., 2002), the development and articulation of family values and vision (Berent-Braun & Uhlaner, 2012; Botero et al., 2015; Zellweger & Kammerlander, 2015), and information exchange and procedural transparency (Sundaramurthy, 2008; Van der Heyden et al., 2005). In terms of outcomes, family governance has been linked to family unity (Brenes et al., 2011; Jaffe & Lane, 2004; Koeberle-Schmid et al., 2014; Martin, 2001), transgenerational orientation (Suess-Reyes, 2017), positive family dynamics (Suess, 2014), and the development of interpersonal trust through interaction between family members (Arregle et al., 2007; Sundaramurthy, 2008).

Furthermore, family governance can enhance the family identity because it positively influences associability, defined as the willingness of actors to subordinate individual in favor of collective goals (Berent-Braun & Uhlaner, 2012). Perceptions of a family’s enduring, distinctive, and central character have been shown to be largely rooted in its unique history and are expressed through stories, places, artifacts, and other forms of symbolism (Cornelissen et al., 2007; Ravasi et al., 2018; Zellweger et al., 2013) that connect the past to the present and the future (Ashworth & Graham, 2016). For instance, family real estate and legacy objects are typically managed in the family governance system through family meetings and family constitutions. Family meetings allow for storytelling as the building blocks of shared narratives (Ashforth et al., 2008; De Fina, 2013; Koening Kellas, 2005), traditions as symbolic interactions (Suddaby & Jaskiewicz, 2020), and celebration of family legacy as a signal of endurance (Ravasi et al., 2018). Family constitutions formulate the family’s central values and mission (Botero et al., 2015). Thus, governance practices are highly relevant because they provide coordination in extended families and serve as a communication forum that allows transgenerational enterprise families to maintain themselves as a group (Suess-Reyes, 2017; Sundaramurthy, 2008). Shared identities are dependent upon communication (Cornelissen et al., 2007; De Fina, 2013; Fiol, 2002; Hardy et al., 2005). Collective identities inherently rely on shared understandings, which are improved through family governance practices that promote the exchange of information and individual views. Thus, family governance can strengthen the family identity.

In a second step, family identity can enhance family social capital. The literature has suggested that a shared sense of identity has a positive effect on the level of trust between group members, thereby creating a positive cognitive relationship between individuals, and rendering it less likely that family members will engage in opportunistic and selfish behavior (Borgen, 2001; Kramer, 2009; Kramer et al., 2001; Lewicki & Bunker, 1995). A common identity has been found to be a direct antecedent of an enterprise family’s will to pursue common goals (Suess-Reyes, 2017). We acknowledge that in the majority of studies identity itself is categorized as a facet of the relational dimension of social capital (e.g., Nahapiet & Ghoshal, 1998; Pearson et al., 2008) given that group identities are inherently relational (Ashforth et al., 2008). Indeed, identifying with a group on the basis of its uniqueness and endurance has been shown to have a positive influence on an individual’s willingness to contribute to the collective (Kramer, 2009). The literature has suggested that identity-based trust is a more suitable construct for enhancing social capital in larger groups, such as extended enterprise families, than interpersonal trust (Kramer, 2009). This is because the interpersonal trust on the individual level in large groups is less likely than identity-based trust to be based on repeated exchange between individuals. Thus implying that identity is a fruitful lens for investigating social relationships in groups.

In other words, family identity can enhance the social capital of transgenerational enterprise families as the collective identity facilitates collaboration. In such families, the interactions that address the question “who are we?” are likely to be made in the family governance system, because collective identities cannot exist without verbal or symbolic communication. These arguments lead us to the following hypothesis:

The Moderating Role of Ownership

Family businesses are the predominant form of enterprise organization. The family business system can be characterized in a framework of three overlapping circles representing the family, the business, and the ownership systems (Tagiuri & Davis, 1996). With regard to ownership, Gersick et al. (1997) distinguished between ownership controlled by one individual (e.g., first generation), a sibling partnership in which ownership resides in the hands of daughters and sons (e.g., second generation), and a cousin consortium, where control effectively resides with many individual family members across several family branches (e.g., third generation and onward). Given that some structures may take a hybrid form or can change during times of transition, these ownership structures do not represent an automatic evolution and do not necessarily coincide with the generational stage (Gersick et al., 1997). In general, however, ownership tends to become more diluted over time (Le Breton-Miller & Miller, 2013; Nordqvist et al., 2014).

Enterprise families and their members may share ownership of a family business, but the evolution of the family can also lead to selling the original business and acquiring ownership of a portfolio of investments and perhaps other nonfamily businesses. In addition, enterprise families may choose to maintain ownership in one generation—perhaps the founding generation—before deciding to transfer parts of the ownership to the rising generation and to other generations beyond that. Generational ownership in family enterprises refers to the ownership being simultaneously held within one or more family generations (Eddleston et al., 2008). Whether or not there exists a family business and whether or not ownership is shared with multiple family generations have implications concerning the degree to which family identity impacts social capital.

Next, we argue that generational ownership affects the extent to which family governance practices promote family identity, and subsequently that business ownership affects the extent to which family identity enhances social capital. That is, by acting as a first-stage moderator in our moderated mediation framework (as presented in Figure 1), generational ownership shapes the effectiveness of family governance practices in enhancing family social capital. In addition, by acting as a second-stage moderator in our moderated mediation framework, business ownership shapes the effectiveness of family governance practices in enhancing family social capital.

The Moderating Role of Generational Ownership

The literature has been slow in differentiating between founder and later-generation families (Fang et al., 2018) as well as small and large businesses (Chrisman et al., 2012; Miller et al., 2007), although it is understood that these factors are a key source of heterogeneity among family businesses. Literature has noted that governance, goals, and resources can vary across family firms when controlled by different generations (Fang et al., 2018; Gersick et al., 1997). Generations and firm size have been found to be relevant factors regarding outcomes such as performance (Miller et al., 2007) and the definitions of family business (Miller et al., 2007). Generational perspectives have been demonstrated as relevant for the factors that positively impact entrepreneurship (Cruz & Nordqvist, 2012), behavior such as internationalization and family centric goals (Chrisman et al., 2012).

In this study, we argue that the family governance system can be particularly important in the development of a family identity in enterprise families with higher generational ownership, where generational ownership refers to the number of generations that are currently involved in ownership of the family enterprise. Later-generation family businesses are likely to have a more widely dispersed ownership group with multiple branches, whereby the family enterprise is larger and more complex than in earlier generations (Jaffe & Lane, 2004; Le Breton-Miller & Miller, 2013; Nordqvist et al., 2014). Scholars have argued that the interests of individual family members diverge increasingly, while family bonds and commitment to the family enterprise simultaneously decrease (Le Breton-Miller & Miller, 2013). Family branches have been shown to see individuals increasingly prioritize their own interests rather than those of the family or the enterprise as a whole (Gersick et al., 1997; Sciascia et al., 2014). Kellermanns and Eddleston (2007) showed that cognitive conflict—disagreement about goals and strategies—in a family is negatively associated with family business performance, while Eddleston et al. (2008) found generational ownership to be associated with relationship conflict.

Furthermore, communication and exchange are likely to increase in multigenerational ownership groups if a family governance system is implemented by the enterprise family. We argue that higher levels of generational ownership will enhance the influence of family governance practices on family identity as bonds will strengthen between family members across generations, which contributes to familism—a social structure in which family expectations eclipse those of individual family members (Bengtson & Roberts, 1991). The role of the family governance system is particularly important in enterprise families with higher generational ownership as with wider generational ownership comes less opportunism among active family owners at the expense of those who are more passive (Siebels & Zu Knyphausen-Aufseß, 2012). In other words, family communication, positively influenced by family governance practices, and multigenerational attention affect identification with the family enterprise (Cabrera-Suárez et al., 2015).

Although the first and second generations of a family enterprises can rely on natural bonds in the nuclear family and more frequent interaction, later generations of that same family would require a salient family identity as an overarching mechanism to create associability and maintain shared meanings (Berent-Braun & Uhlaner, 2012; Suess-Reyes, 2017). Thus, we propose that generational ownership affects the extent to which family governance practices promote family identity:

The Moderating Role of Business Ownership

We argue that business ownership may render enterprise family identity less effective in enhancing family social capital. Enterprise families either retain ownership control of their core family business or sell the original firm and diversify into a financial family with a portfolio of investments and business interests (Hamilton, 2018; Jaffe & Lane, 2004). Enterprise families that do share ownership in a family business and have not yet divested their interests may run into blockholder conflicts as a result of a divergence of ownership and interests between majority and minority owners (Miller & LeBreton-Miller, 2006; Zellweger & Kammerlander, 2015).

The literature has distinguished between a family’s ability and its willingness to pursue certain goals (De Massis et al., 2014). Transgenerational intent is frequently used as a proxy for the willingness to pursue goals that maintain the enterprise (Chrisman & Patel, 2012). Enterprise families have been found to possess this willingness to maintain the enterprise. Although the literature has positioned ownership of a business as a key source of identification for the family (Berrone et al., 2012), we argue that business ownership in the enterprise family context may weaken the effect of family identity in enhancing family social capital because there is greater potential for owner-to-owner conflicts, which in turn increase information asymmetry and blockholder conflicts among owners that then erode trust within such enterprise families. In such situations, it stands to reason that there will be a negative effect on family cohesion and social capital.

The influence of family identity on family businesses has been explored extensively in the literature (e.g., Berrone et al., 2010; Dyer & Dyer, 2009; Whetten et al., 2014). In many cases, the family business has been found to be seen as an extension of the family itself (Berrone et al., 2012). However, in later generations of enterprise families, the family business has been shown to be more likely to influence family identity than vice versa (Wielsma & Brunninge, 2019). The original business provides a common foundation for the family’s identity that families with portfolio investments have to, and often do, compensate for, through a family office, philanthropic foundation or legacy assets. These shared entities and assets may lead to less damaging conflict among family members. Business ownership increases the potential for conflict because of power asymmetries and divergence of interests and expectations among owners (e.g., business as a “cash cow” versus business as a transgenerational dream) (Kellermanns & Eddleston, 2008). Strong social relations require stability and evolve over time (Arregle et al., 2007). However, studies have suggested that in later generations, as the number of passive owners grows, the business functions less and less as a common point of identification (Gómez-Mejia et al., 2011). Moreover, psychodynamic effects such as dispersion of business ownership and identity conflict (Berrone et al., 2012; Schulze et al., 2001) make it more difficult for family members to fulfill both family and business expectations (Gersick et al., 1997).

In other words, families with a business automatically have a common basis for identification, but that effect diminishes in later generations. Given that power in enterprise families that share ownership of a family business is likely to be more unequally distributed between passive and active owners as a result of information asymmetries, there is greater potential for conflict that will impact the family’s social capital. Based on these arguments, we therefore suggest that business ownership plays a second-stage moderating role in the indirect relationship between family governance practices and family social capital, leading us to our third hypothesis:

Methods

Data Collection and Sample Description

For our empirical analysis, we chose to look at enterprise families across the globe, because such families are difficult to access and there have been insufficient studies using the family as a unit of analysis. This is despite the major impact of enterprise families on our society (Habbershon & Pistrui, 2002) in terms of economic growth (White, 2017), employment (Shanker & Astrachan, 1996; White, 2017; Zahra, 2005), technological innovation (Zahra et al., 2004), as well as philanthropic (Boris & Wolpert, 2001) and start-up capital (Steier, 2001).

We contacted 1,020 enterprise family leaders and family office executives around the world. The contact list was established by combining our own network of enterprise families in Europe and the Americas with the worldwide network of the Global Enterprise Families Institute, the knowledge center, and think tank of Family Office Exchange. We dispensed duplicates as both networks overlapped to some extent. To specify the sample for analysis, an enterprise family was defined as a family with wealth in excess of US$30 million (Wealth-X & UBS, 2016), and shared ownership of multiple entities and assets. In a personalized letter per enterprise family, we asked the most prominent and knowledgeable family leader or the chief executive of their single family office via email to respond to our online Qualtrics survey. The overall response rate was close to 22% after two waves of gentle reminders. No incentives were used to entice respondents, other than our sharing of findings. Nonrespondents proved to be a random selection of the universe of invitees when looking at the enterprise family characteristics such as generations, size, branches, location, or wealth. After deleting incomplete or fatuitous responses, we were left with a total of 175 observations in the final sample.

The fieldwork was completed from May to October 2019. We conducted a pilot test of the survey instrument by approaching three enterprise families in our own network. The results of this pilot were used to modify the questionnaire to obtain the final survey in English. It became clear to us that words such as “legacy” and “destiny” did not resonate as well with our respondents as “vision” and “heritage”: the word “legacy” is associated with “what you have to become,” and the word “destiny” is associated with “what you are stuck with.” We revised the survey to eliminate ambiguities in our questions and added some additional questions. The survey contains five blocks of questions: respondent and enterprise family information, family relationships, family governance, family continuity, and values and goals (see Appendix). All measurements are at the family level (not the individual level) as respondents were asked to answer about the enterprise family.

Our sample comprises families with roots in North America (52%), Europe (23%), Latin America (15%), Asia-Pacific (7%), and the Middle East & Africa (3%). The oldest family enterprise in our sample dated back to the early 1700s, representing 12 generations. The largest family spanned 12 branches, and some families were made up of more than 1,000 members. In our sample, about a third were billionaire enterprise families, whose average wealth was in excess of US$250 million. The family enterprises within the sample had been controlled by the family for one generation (17%), two generations (23%), three generations (25%), four generations (11%), five generations (11%), six generations (8%), or more (5%). In our sample, on average two generations of the enterprise families controlled one or more family businesses (82%), a family office (82%), or a philanthropic foundation (77%). However, 17% of the families who owned family businesses did not have a family office to manage their investments and personal affairs.

Measurement and Construct Validation

The dependent variable we used in our study was family social capital. We measured family social capital with a validated 12-item scale, adapted from Carr et al. (2011) to reflect the enterprise family context. In other words, we measured family social capital that exists among family members who are within the family enterprise. As the family enterprise does not necessarily include a family business (18% of our survey sample) the scale from Carr et al. (2011) was adapted by emphasizing on (all) “family members in this family enterprise . . .” instead of on (only) “family members who work in this firm . . .” All items were measured using a 5-point Likert-type scale, ranging from 1 (strongly disagree) to 5 (strongly agree). This internal social capital scale is based on aggregating four items each for the three dimensions of social capital: structural, cognitive, and relational (Nahapiet & Ghoshal, 1998). Reliability analysis indicates that the scale has good internal consistency, with a Cronbach’s alpha of .92.

The independent variable we used in our study was family governance practices. We adapted the scale from questionnaires that measure family governance (Berent-Braun & Uhlaner, 2012; Mustakallio et al., 2002; Suess-Reyes, 2017) to reflect the enterprise family context. The scale uses four items and measures the extent to which families use four family governance practices: family constitution, family code of conduct, family council, and family gatherings. All items were measured using a 5-point Likert-type scale ranging from 1 (do not know), 2 (not considered at this time), 3 (in discussion), 4 (underdevelopment) to 5 (already in use). Reliability analysis indicates the scale is internally consistent, with a Cronbach’s alpha of .70.

The mediator variable we used was family identity. We measured this using six items drawn from scales that measure family firm identification (Berrone et al., 2012; Hauck et al., 2016), family business identity (Frank et al., 2016), and family firm socioemotional wealth (Debicki et al., 2016). These items were adapted by changing “family business” into “family enterprise” to incorporate the enterprise family context. All items were measured using a 5-point Likert-type scale ranging from 1 (not at all) to 5 (a great deal). Exploratory factor analysis shows construct validity, and reliability analysis indicates the scale has good internal consistency, with a Cronbach’s alpha of .86.

We used two moderator variables: generational ownership and business ownership. We measured generational ownership by asking how many generations hold a share of ownership in the family enterprise (including the family business, family office, investments, and foundation). This moderator variable was operationalized as a categorical variable ranging from one to three generations, referring to ownership by grandparents, parents, or grandchildren. The moderator variable business ownership was measured dichotomously by asking whether the enterprise family held ownership of one or more operating family businesses (yes/no).

Multiple control variables were used to ensure a correct model specification, including various characteristics of the enterprise family (family generations, family size, family branches, and region of origin). To measure the longevity of the family enterprise, we asked respondents to indicate for how many generations the enterprise had been owned by the family. Family size was measured by asking the total number of family members (including spouses) that the family comprised. Family branches was measured by asking the number of families that were part of the extended enterprise family group. The region was determined by asking the location of the enterprise family headquarters. As our final control variables, we asked the enterprise family whether they operated a family office or had a family philanthropic foundation. The detailed operationalization of all variables can be found in the appendix.

Analysis and Results

Descriptive Statistics

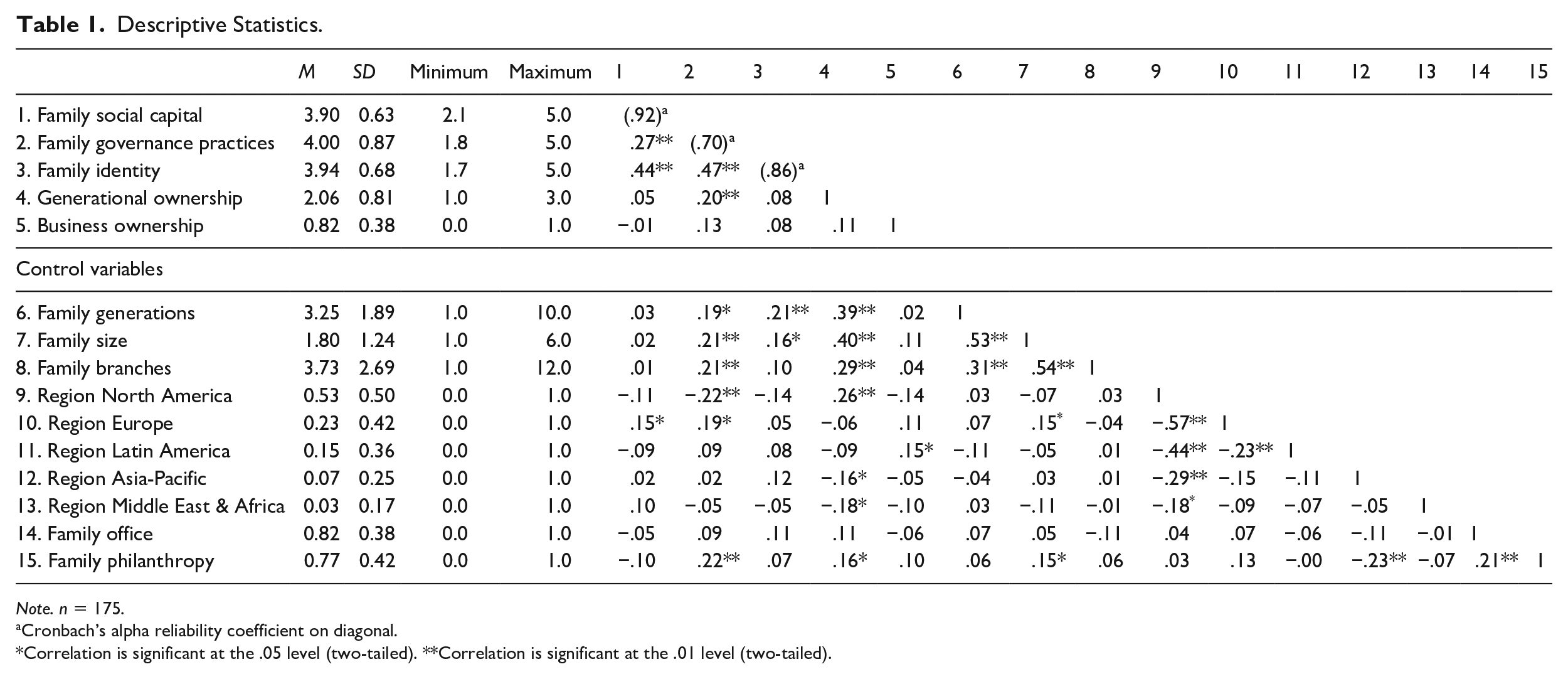

Table 1 reports the bivariate correlation coefficients for all variables included in the analysis, as well as the mean and standard deviation for each variable. Reliabilities for the variables, constructed from multiple items, are reported on the diagonal in Table 1. Across the sample as a whole, the average number of generations of the family enterprise is 3.25, the size of the family is below 75 members, and there are around four family branches. Social capital shows a low but positive correlation with family governance practices (r = .27, p < .01), and a moderate and positive correlation with family identity (r = .44, p < .01). Family identity shows moderate positive correlation with family governance practices (r = .47, p < .01). In addition, family governance practices shows a low and positive correlation with generational ownership (r = .16, p < .05). The moderator variable generational ownership shows a low and positive correlation with the independent variable family governance principles (r = .20, p < .01).

Descriptive Statistics.

Note. n = 175.

Cronbach’s alpha reliability coefficient on diagonal.

Correlation is significant at the .05 level (two-tailed). **Correlation is significant at the .01 level (two-tailed).

With reference to the control variables used in our model, the correlation table indicates that generational ownership is positively correlated with family generations (r = .39, p < .01), family size (r = .40, p < .01), family branches (r = .29, p < .01), and the North America region (r = .26, p < .01). Family generations is positively correlated with family identity (r = .21, p < .01). Family size is positively correlated with family governance practices (r = .21, p < .01) and with family generations (r = .53, p < .01). In addition, family branches is positively correlated with family governance practices (r = .21, p < .01), family generations (r = .31, p < .01), and family size (r = .54, p < .01). The table of correlation coefficients also shows that enterprise families in North America show low and negative correlations with our model variable family governance practices (r = −.22, p < .01). European enterprise families show low and positive correlations with model variable family governance practices (r = .19, p < .05). Finally, there is a positive correlation between family philanthropy and family governance practices (r = .22, p < .01).

We test for the possibility of common method bias using a Harman’s one-factor test (Podsakoff & Organ, 1986), because all data were gathered using the same survey questionnaire. We included all items of the variables in our model in an unrotated factor analysis and evaluated the number of factors emerging from the data. A single factor with an eigenfactor value greater than 1.0 was extracted. This factor explained 32.8% of variance. Since this is much lower than the cut-off value of 50%, this indicated that there was no common method bias.

Because of moderate independent variable correlations, we did not expect multicollinearity problems. However, we assessed the variance inflation factors (VIFs) for the variables in our model. The VIF scores are between 1.00 and 1.07, and well below the generally used cut-off value of 10 (Kutner et al., 2005), thus suggesting that the independent variables included in our analysis are robust against multicollinearity problems. In terms of potential social desirability bias, all respondents were assured absolute confidentiality, which increases the probability of obtaining conscientious and true answers (Podsakoff et al., 2003).

Hypothesis Testing

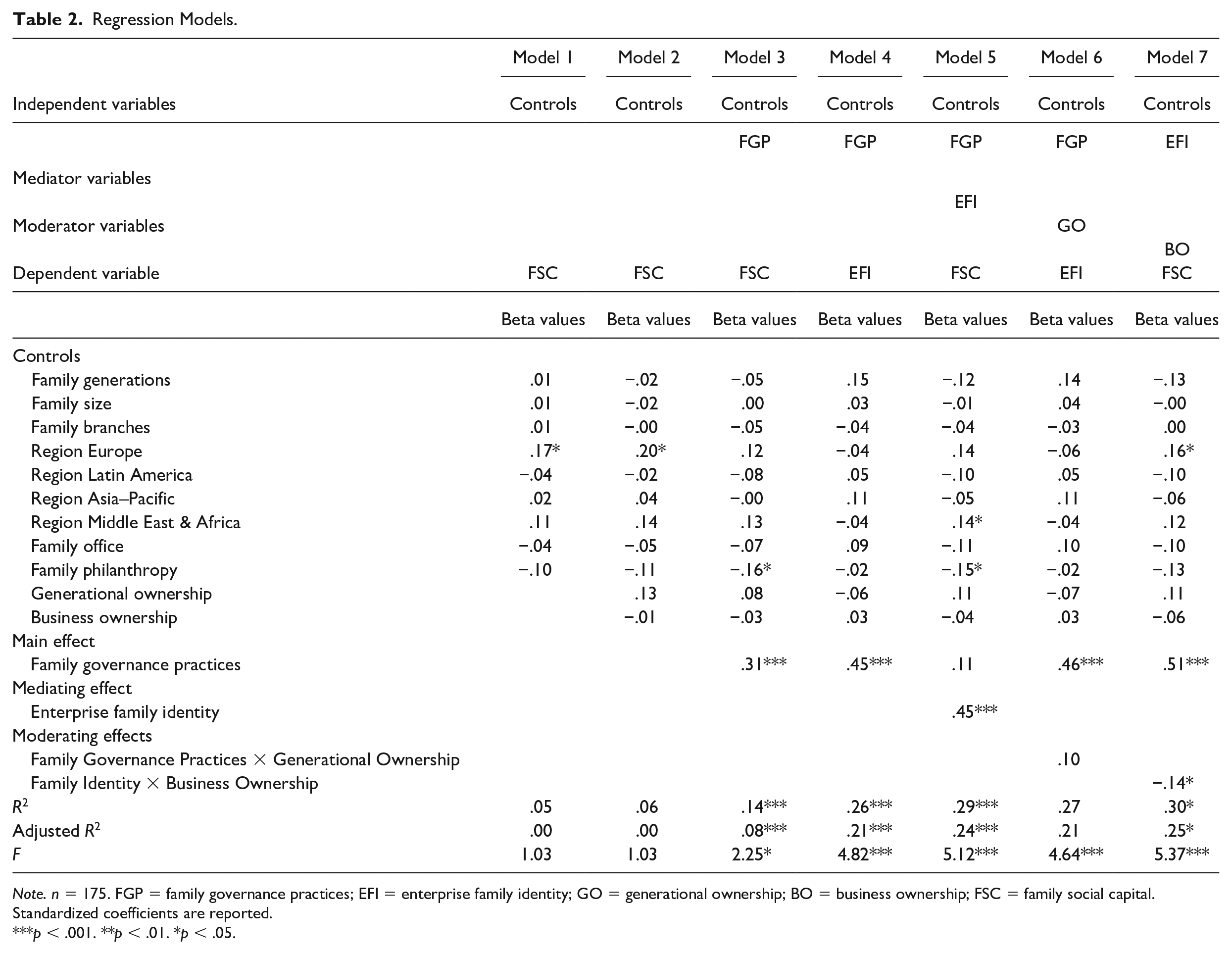

The results of our analysis for the empirical testing of Hypotheses 1, 2, and 3 are reported in Table 2. We test the proposed moderated mediation framework first using the procedure outlined by Baron and Kenny (1986). We then quantify the indirect effects and confidence intervals using a bootstrapping approach (Preacher & Hayes, 2008).

Regression Models.

Note. n = 175. FGP = family governance practices; EFI = enterprise family identity; GO = generational ownership; BO = business ownership; FSC = family social capital. Standardized coefficients are reported.

p < .001. **p < .01. *p < .05.

We use multiple ordinary least squares regressions to check for compliance with Baron and Kenny’s (1986) four requirements for mediation: (a) the independent variable significantly predicts the dependent variable; (b) the independent variable significantly predicts the mediating variable; (c) the mediating variable significantly predicts the dependent variable; and (d) when the mediating variable is introduced, the effect of the independent variable on the dependent variable is significantly reduced, and the mediating variable significantly accounts for variability in the dependent variable. Model 1 shows the effects of the control variables, and in Model 2, we add the main effects of the moderating variables. In Model 3, we test the first mediation requirement. Model 4 represents the second requirement of the mediation analysis, and Model 5 represents the third requirement. In Models 6 and 7, we test our moderation variables.

We first regress the dependent variable on to the control variables by considering standardized regression coefficients (β) and the significance of these weights (Model 1). None of the control variables, except for the Europe region (β = .17, p < .05), prove to be significant. Adding our moderator variables as controls in Model 2 again shows only Europe (β = .20, p < .05) to be significant and positive.

Testing for Mediating Effects

Assessing the standardized regression coefficient and the significance of this weight in Model 3, we conclude that the independent variable family governance practices (β = .31, p < .001) have a highly significant and positive effect on the dependent variable family social capital. The results suggest that family governance practices explain about 8% of variation in family social capital (p < .001); the analysis of variance (ANOVA) shows F = 2.25, with p < .05.

In Model 4, we test the effect of family governance practices on the mediating variable family identity. No control variables are significant in Model 4, and family governance practices is positively and highly significantly related to family identity (β = .45, p < .001). In Model 5, we assess how family identity mediates the relationship between family governance practices and family social capital. We find that the effect of family governance practices on family social capital ceases to be significant when family identity is included in the regression as a mediating variable (β = .11, p > .10). However, the relationship between family identity and family social capital is positive and highly significant (β = .45, p < .001).

The findings in Models 3, 4, and 5 provide confirmation of all four requirements of mediation for family identity. We accept Hypothesis 1 and find full mediation of family identity supported by the regression analysis. To test for the significance of the mediating effect of family identity, we carry out a bootstrapping procedure (Preacher et al., 2007), including control variables as covariates. The results confirm the significance of the indirect effects of family governance practices on family social capital via family identity (p < .01) at the 95% confidence intervals for this effect. The direct effect of family governance practices on family social capital is not statistically significant (p > .01). Hence, the results of the bootstrapping approach indicate support for Hypotheses 1.

Testing for Moderating Effects

In Model 6, we test the moderating role of generational ownership. The results suggest Hypothesis 2 is rejected, as the coefficient of the interaction between family governance practices and generational ownership does not have a statistically significant effect on family identity (β = .10, p > .10).

In Model 7, we test the moderating role of business ownership. The empirical results show that the interaction term between family identity and business ownership has a negative and significant effect on family social capital (β = −.14, p < .05). This finding supports the notion that business ownership has a moderating role for the indirect effect through family identity, as proposed in Hypothesis 3.

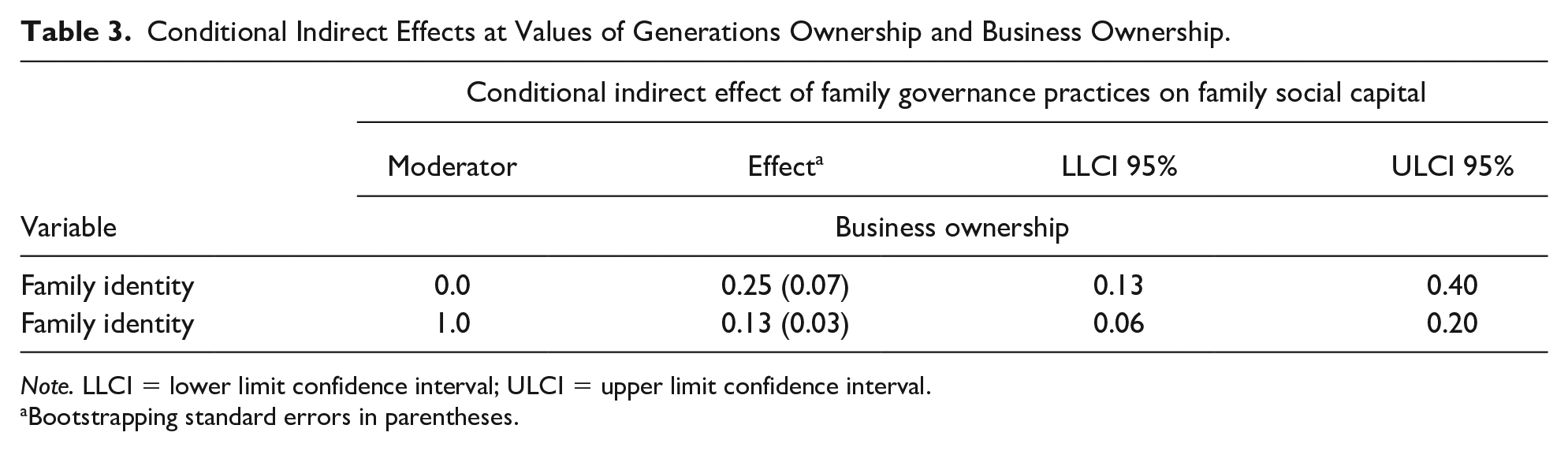

To gain further insight into how the indirect effects differ depending on business ownership, we used a bootstrapping procedure (Preacher et al., 2007), including control variables as covariates, to quantify the indirect effects at the 16th, 50th, and 84th percentile levels of business ownership. The index of moderated mediation (Hayes, 2018) showed statistically significant results for the conditional effects of family governance practices on family social capital at different values of business ownership (index = −.13, p < .01).

Table 3 reports the indirect effects and 95% confidence intervals at different values of business ownership. All indirect effects are positive and significant, as the null of 0 does not fall between the lower and upper limit of the 95% confidence intervals for each effect. We thus infer that business ownership significantly moderates (p < .01) the indirect effect of family governance practices on family social capital. In line with Hypothesis 3, we can observe that the indirect effect of family governance practices on family social capital is weaker at higher levels of business ownership. The coefficient declines from .25 (low, p < .01) to .13 (high business ownership, p < .01).

Conditional Indirect Effects at Values of Generations Ownership and Business Ownership.

Note. LLCI = lower limit confidence interval; ULCI = upper limit confidence interval.

Bootstrapping standard errors in parentheses.

Discussion

Strong internal social capital is essential for family enterprise longevity as it can generate distinctive familiness (Pearson et al., 2008), develop a collective will to preserve shared family wealth (Berent-Braun & Uhlaner, 2012), improve interaction (Arregle et al., 2007; Pearson et al., 2008), and mitigate destructive relational conflicts (Eddleston & Kellermanns, 2007). Although the existing research has suggested an array of outcomes of social capital, how enterprise families can strengthen their social capital and prevent its natural erosion remained unexplored.

Our findings have several important implications concerning family business research. First, our empirical findings support the importance of adopting an identity perspective regarding social capital formation in enterprise families. We acknowledge that the context of the organizational and family life cycle is important (Gedajlovic et al., 2013), that family businesses are heterogenous, and that enterprise family social capital formation differs from that of smaller firms and businesses (Chrisman et al., 2012; Sanchez-Ruiz et al., 2019); in the enterprise family, shared cognitions or interpersonal trust are less likely to be based on immediate kinship and interactions within the nuclear family (Herrero, 2018). Adopting the idea that group identities rely on a conception of central, enduring, and distinctive characteristics (Albert & Whetten, 1985; Ashforth et al., 2008), our finding that family identity is important for preventing the erosion of family social capital in enterprise families aligns with previous determinations that identity positively affects levels of trust, reduces the likelihood of opportunistic behavior, and increases willingness to contribute to a group (Kramer, 2009; Lewicki & Bunker, 1995).

Second, our findings advance the understanding of how family governance enhances social capital in enterprise families. Specifically, our study opens the black box of the family governance–social capital relationship by highlighting family identity as the mechanism through which governance stimulates the formation of family social capital. By theorizing and empirically testing the underlying mechanism of this relationship, we advance previous research that found evidence that family governance positively influences an array of outcomes related to the functioning of the enterprise family, such as improved decision-making through social interaction and a shared vision (Habbershon & Astrachan, 1997; Mustakallio et al., 2002). In this way, our finding regarding the mediating role of family identity is in line with previous assertions that family identity is a mechanism for cultural transmission in organizations and families (Konopaski et al., 2015; Zellweger et al., 2013). Moreover, although the effects of family governance on family business performance have already been established (e.g., Berent-Braun & Uhlaner, 2012; Blumentritt et al., 2007; Brenes et al., 2011; Martin, 2001; Mustakallio et al., 2002; Poza et al., 2004), our study advances understanding of how family governance aids social capital in the context of extended enterprise families (Strike, 2012).

Third, our findings advance knowledge on when our proposed identity perspective of family social capital is most effective. To examine this element, we empirically tested two boundary conditions: generational ownership and business ownership. Although we proposed that generational ownership will affect the extent to which governance practices strengthen the family identity, we did not find empirical support. Our initial assertions were related to the idea that the factors that distinguish the environment of family enterprises from regular families include the lengthy time span of involvement and intergenerational cooperation within the enterprise, the emotional side of family interaction and the long-term transgenerational vision. Furthermore, family members have different roles as they are simultaneously, for example, parents, aunts, uncles or cousins, as well as being owners, managers or functionaries within the family system (Le Breton-Miller & Miller, 2015). Our finding is intriguing as it suggests that generational ownership may not be crucial in determining how effective family governance is in terms of enhancing family identity. Literature has suggested that identity declines in later generations because family members no longer see the enterprise as an extension of themselves (Gómez-Mejia et al., 2011; Le Breton-Miller & Miller, 2013). Our finding suggests that the effectiveness of enterprise family governance in preventing the decline of family identity does not depend on the number of generations that share ownership of the enterprise. Rather, it suggests that family governance is important regardless of the generational ownership.

Furthermore, we found evidence that the extent to which family identity stimulates the development of family social capital depends on business ownership, such that the effect is less strong for enterprise families that own a business. Our finding thus conflicts with the socio-emotional wealth literature, which has argued that the business is the key carrier of identity and family relationships as business families see their firm as an extension of themselves and that this relationship declines in later generations (Berrone et al., 2012; Gómez-Mejia et al., 2011). Contrarily, our finding suggests that enterprise families do not depend upon a core business to maintain their identity and social relationships. We are not the first to question the applicability of socio-emotional wealth to large family businesses and wealthy families (Chrisman & Patel, 2012; Le Breton-Miller & Miller, 2013; Nason et al., 2019; Zellweger, 2017). Enterprise families do not necessarily depend upon a business as a carrier of identity as they can substitute their affective endowments through family legacy assets or philanthropic endeavors (Feliu & Botero, 2016), which all speaks to family firm heterogeneity playing a role in identity and goals in these cases (Ponomareva et al., 2019). Although some family businesses adhere to a socio-emotional wealth logic in which the business is the core of the families’ raison d’être, others may adopt the identities of entrepreneurial families (Nason et al., 2019) or transgenerational enterprise families. Our findings underscore the importance of accounting for heterogeneity into account for adequate theory building (Memili & Dibrell, 2019).

Overall, we respond to the recent call for more research to examine the building and maintaining of family relationships (Zellweger et al., 2019) by analyzing the contingency role of generational ownership and business ownership to qualify the indirect effect of family identity in the relationship between family governance practices and family social capital. Thus, our study advances family business research by developing and empirically testing on a unique data set in a moderated mediation framework that considers both how and when family governance practices enhance enterprise family social capital.

Limitations and Future Research Directions

This study had certain limitations, which should be addressed in future research. First, a limitation of the study is that only one respondent per enterprise family was surveyed on matters that concern the whole family. In addition, we gathered all data using a single-survey questionnaire and carefully attempted to minimize common method bias by focusing our research on items and scales that were least likely to generate social desirability in the responses. Even though all respondents were active in the core of the enterprise and “close to the fire,” it could be argued that different members of the same family might have different views on the family’s social capital and identity. Future studies could attempt to provide longitudinal analysis and to survey multiple members of the same family to increase confidence in the causal claim of our model.

Second, we measured family governance practices as a categorical variable, which does not allow for analysis of how governance practices are used to produce effects or enable one to “zoom in” on the content of the family governance process. Future studies of family governance could examine the context and content of family governance practices (Suess-Reyes, 2017, p. 769).

Third, our study sample consisted of enterprise families from North America, Europe, Latin America, Asia-Pacific, and the Middle East & Africa. It is likely that cultural styles around the world would differ enough to have impact in this research, as would the levels of social capital and family dynamics (Jaffe & Grubman, 2016). Although, in our study we controlled for the geographic region of the family, in future research, it would be valuable to specifically study regional differences in this context.

Fourth, in the identity literature, shared representations are symbolic manifestations of collective identities that reinforce each other (Ravasi et al., 2018; Schultz & Hernes, 2013). Thus, overall, identity is both a catalyst for the cognitive dimension and reinforced by it. As a limitation, Nahapiet and Ghoshal (1998) acknowledged that the dimensions are interrelated and highlighted that opposite direction of causality is conceivable. Our primary aim was to study how a decline of social capital can be prevented in enterprise families, therefore we abstained from separately focusing on the relational and cognitive dimensions of social capital. We invite scholars to explore these separate social capital dimensions in future research.

Fifth, social capital research is inherently multilevel in nature (Payne et al., 2010): Social capital is influenced by the behaviors of individuals and that of collectives and can be conceptualized on the individual level of analysis whereby interacting individuals create social capital on the group level (e.g., Coleman, 1988; Long, 2011; Ostrom & Ahn, 2003). Furthermore, social capital can also be theorized on the group level of analysis (Putnam, 1995). Our study did not allow for integration of the multilevel nature of social capital into the model because we gathered data on the enterprise family (group) level and lacked data on the individual level. Future research may consider the individual level of family social capital.

Sixth, life cycle considerations have been neglected in social capital research (Gedajlovic et al., 2013; Nordstrom & Steier, 2015). The temporal aspect, which corresponds with altering network structures, is an important contextual factor for the analysis of social capital (Gedajlovic et al., 2013; Sanchez-Ruiz et al., 2019). Beyond changes in the relational structures within families, relationships are also likely to be shaped by evolving enterprises. Therefore, how families actively manage these changes and how governance shapes relationships in a temporal context is an important future research area within the collective level of analysis.

Seventh, more analyses on what types of enterprises, organizations or endeavors enterprise family may use to achieve their nonfinancial goals most effectively will shed light on these families that do not necessarily depend on the family business as carrier of their identity (De Groot et al., 2022).

Implications for Practice

The continuity of a family enterprise requires effective decision-making built on transparent and appropriate family governance, which needs to have meaning to family members (Gray, 2007; Jaskiewicz et al., 2014; Martin, 2001; Suess-Reyes, 2017). This meaning depends on transparency, inclusion and representation. Our study highlights how family governance practices can help to strengthen family identity, thereby enhancing family social capital.

Family identity is central to pursuing a collective goal of transgenerational wealth preservation. This shared sense that the family enterprise has meaning beyond its financial benefits is based on a unique and valuable legacy that provides a common frame of reference for family members and encourages stewardship. Family identity increases the nonfinancial (and thus difficult to measure) value of the enterprise and makes family members more committed to preserving the enterprise for the future.

As we did not find empirical support that generational ownership will affect the extent that family governance strengthens family identity, this suggests the effectiveness of governance in enterprise families is not dependent on the number of generations sharing enterprise ownership. In other words, the family governance may increase the likelihood that enterprise families continue working on their shared goals regardless of increasing family size and complexity.

In addition, enterprise families do not necessarily depend on business ownership to maintain the family identity to enhance family social capital. Although many factors will play into the decision to hold on to, or divest from, a legacy business, conceivably, this implies that concerns regarding the role of the business for maintaining the family as a group does not necessarily has to be a decisive factor in that decision-making.

Our study contributes to family business and entrepreneurship literature by demonstrating that family governance practices enhance social capital in enterprise families. The analysis was based on a data set of 175 enterprise families from different regions globally. Our results indicate that family identity is directly and positively related to family social capital. In addition, the results show that the indirect effect of family identity on family social capital is weaker with business ownership. As far as we are aware, these results are the first to use quantitatively based research to confirm that family governance practices are beneficial for the social capital of enterprise families. The results enable us to outline a moderated mediation framework that considers both how and when family governance can enhance social capital.

Footnotes

Appendix

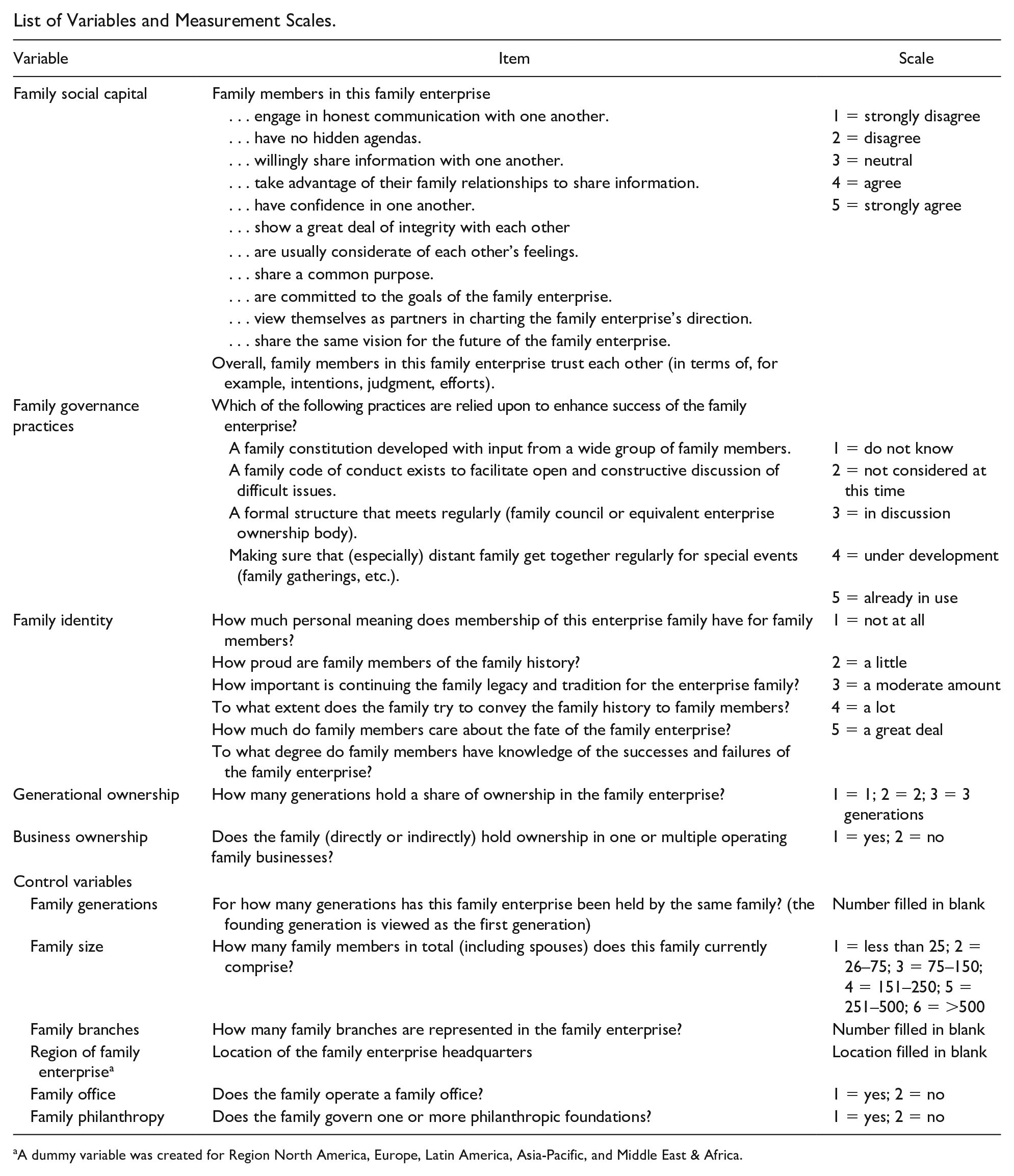

List of Variables and Measurement Scales.

| Variable | Item | Scale |

|---|---|---|

| Family social capital | Family members in this family enterprise | |

| . . . engage in honest communication with one another. | 1 = strongly disagree | |

| . . . have no hidden agendas. | 2 = disagree | |

| . . . willingly share information with one another. | 3 = neutral | |

| . . . take advantage of their family relationships to share information. | 4 = agree | |

| . . . have confidence in one another. | 5 = strongly agree | |

| . . . show a great deal of integrity with each other | ||

| . . . are usually considerate of each other’s feelings. | ||

| . . . share a common purpose. | ||

| . . . are committed to the goals of the family enterprise. | ||

| . . . view themselves as partners in charting the family enterprise’s direction. | ||

| . . . share the same vision for the future of the family enterprise. | ||

| Overall, family members in this family enterprise trust each other (in terms of, for example, intentions, judgment, efforts). | ||

| Family governance practices | Which of the following practices are relied upon to enhance success of the family enterprise? | |

| A family constitution developed with input from a wide group of family members. | 1 = do not know | |

| A family code of conduct exists to facilitate open and constructive discussion of difficult issues. | 2 = not considered at this time | |

| A formal structure that meets regularly (family council or equivalent enterprise ownership body). | 3 = in discussion | |

| Making sure that (especially) distant family get together regularly for special events (family gatherings, etc.). | 4 = under development | |

| 5 = already in use | ||

| Family identity | How much personal meaning does membership of this enterprise family have for family members? | 1 = not at all |

| How proud are family members of the family history? | 2 = a little | |

| How important is continuing the family legacy and tradition for the enterprise family? | 3 = a moderate amount | |

| To what extent does the family try to convey the family history to family members? | 4 = a lot | |

| How much do family members care about the fate of the family enterprise? | 5 = a great deal | |

| To what degree do family members have knowledge of the successes and failures of the family enterprise? | ||

| Generational ownership | How many generations hold a share of ownership in the family enterprise? | 1 = 1; 2 = 2; 3 = 3 generations |

| Business ownership | Does the family (directly or indirectly) hold ownership in one or multiple operating family businesses? | 1 = yes; 2 = no |

| Variable | Item | Scale |

| Control variables | ||

| Family generations | For how many generations has this family enterprise been held by the same family? (the founding generation is viewed as the first generation) | Number filled in blank |

| Family size | How many family members in total (including spouses) does this family currently comprise? | 1 = less than 25; 2 = 26–75; 3 = 75–150; 4 = 151–250; 5 = 251–500; 6 = >500 |

| Family branches | How many family branches are represented in the family enterprise? | Number filled in blank |

| Region of family enterprise a | Location of the family enterprise headquarters | Location filled in blank |

| Family office | Does the family operate a family office? | 1 = yes; 2 = no |

| Family philanthropy | Does the family govern one or more philanthropic foundations? | 1 = yes; 2 = no |

A dummy variable was created for Region North America, Europe, Latin America, Asia-Pacific, and Middle East & Africa.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.