Abstract

The introduction of ChatGPT and other tools based on artificial intelligence (AI) has the potential to revolutionize the field of education. We study how the public release of ChatGPT and the increased attention on this new large language model from OpenAI are associated with the expected returns of publicly traded firms that operate in the education sector. We also perform separate subgroup analyses for the traditional education sector and the so-called education technology sector. Using linear and threshold CAPM-GARCH models, we find that after the public release of ChatGPT, both the education sector as a whole and the education technology sector have underperformed benchmarks. Our results show that increased attention leads to lower next-day returns in the education sector as a whole and the education technology sector in particular. Additionally, during periods of higher attention, expected returns tend to decline in these two sectors. We also show that the introduction of ChatGPT or the increased interest in this AI tool in the population does not affect the traditional education sector. The introduction of ChatGPT thus has a heterogeneous effect across the various education sectors we examine, with the education technology sector receiving most of the disruption.

Introduction

The interest in ChatGPT and artificial intelligence (AI) has recently expanded rapidly worldwide. In just a matter of months, the chatbot has become a global phenomenon with millions of users, and AI is now “on everyone’s lips.” According to OpenAI—the company behind ChatGPT—the chatbot reached 1 million users only five days after its launch in November 2022. For comparison, Instagram spent 2.5 months, Spotify 5 months, Dropbox 7 months, and Facebook 10 months to reach the same number of users (Buchholz, 2023).

ChatGPT is able to produce highly sophisticated answers to a wide range of question types and adjust the response to the academic level requested—in a matter of seconds. The new technology is particularly relevant in so-called writing-intensive courses (Herman, 2022; Lund & Wang, 2023), but tests have shown that it may also be efficiently used to solve problems within statistics, mathematics, quantitative methods, and programming, among many others (Frieder et al., 2023; Surameery & Shakor, 2023; Wardat et al., 2023). Recent video examples posted on YouTube also highlight its ability to analyze data (Freberg, 2023). In addition, it can produce excellent visualizations and interpretations of results—at the user’s request. Lo (2023) has reviewed how ChatGPT can be used in education and found that its usefulness is domain-specific. According to Kasneci et al. (2023) and Lo (2023), ChatGPT can be used by students on all levels of the education system; from the elementary level to universities. It can also be used as a tool in remote learning and empower students with disabilities. For example, ChatGPT can help students learn by correcting grammar and style, preparing reviews to aid text comprehension, and explaining key concepts. It can also be used to support assessments by generating questions and tasks from a given corpus. ChatGPT also offers innovations for instructors as well (Kasneci et al., 2023; Lo, 2023) by helping to prepare course materials (from translation to topic suggestions) or to help in the assessment process (preparing exams and questions). A recently published article even shows that the new technology can be efficiently used to assist with the production of research studies (Dowling & Lucey, 2023). The software is not without limitations, though, and numerous examples of how ChatGPT has offered strange and even false statements have been posted online and debated publicly. Na et al. (2024) have studied education-related subreddits on the social/discussion platform Reddit and performed a content analysis of posts that included the keyword ”chatgpt”. Their sample covered a sample from January 1 2022 until March 31, 2023, thus the onset of ChatGPT. They found that concerns were related to inaccuracy, lack of credibility, or depth of the answers. A study by Kasneci et al. (2023) argued that while LLMs (large language models) have the potential to improve the digital ecosystem for education, they also bring copyright issues and potential biases, and might lead to a high reliance of students and educators on model (un-authored) outcomes. Training of LLMs also tends to lag behind up-to-date knowledge (Lo, 2023). Memarian and Doleck (2023) agree with Kasneci et al. (2023) that ChatGPT might reduce the ability to learn and explore. To avoid that, good technical expertise is necessary with ChatGPT. Similar concerns were identified by Li et al. (2023), who studied discussions related to ChatGPT on the social platform X (Twitter), a tool that we also use to monitor the general public’s attention towards ChatGPT. Their analysis revealed that concerns are related to the impact on learning outcomes and skill development, but also towards policy and social issues, as the tool is not accessible to all. Interestingly, X users have also expressed concerns related to workforce replacement, which in turn might impact provided services and products in the education sector. X users, who, based on their account description, specialized in education and technology, were particularly engaged. These examples suggest that ChatGPT is an innovation that has the potential to disrupt the education sector.

As noted by Lee, Ju, and Lee (2023), the use of ChatGPT is rapidly increasing, but the research on ChatGPT in the consumer field is limited. We therefore contribute by filling a general gap in the literature as we study how the introduction of the new technology first released by OpenAI has financially affected the education sector. We use trading data from firms in the education sector that are publicly traded. We focus on publicly traded companies because the best estimate of the expected future earnings of any company is made by the people having their money on the line—investors. Saggu and Ante (2023), for example, already documented that the launch of ChatGPT had a significant positive impact on AI-related crypto assets. Apart from analyzing the education sector, we identify two distinct subsectors. One is the sector that is represented by firms that focus on operating universities and campuses and provide education-related services to these institutions. That is, the traditional education subsector. The second is represented by firms that offer digital tools and platforms to enhance learning and might be perceived either as direct competitors with the new technology offered by OpenAI or might benefit from the technology by using it in their courses. That is, the education technology (EdTech) subsector.

Investors can regard ChatGPT as both an opportunity and a threat. The introduction of this innovative language model, therefore, creates increased uncertainty over the future of the industry. Such increased uncertainty likely changes investor’s expectations and manifests into market returns. Our analysis is therefore based on both the standard linear and nonlinear (threshold) models of market return, where we examine how market returns of companies in the education sector and the two subsectors changed prior to, during, and after the introduction of ChatGPT. Our main results utilize Twitter-based 1 attention data to estimate the interest and awareness of the public regarding ChatGPT. We investigate whether an increase in attention influences the future development of stock prices and/or induces changes in the price dynamics for the education sector and the two subsectors. In that regard, we rely on the growing literature on the limited attention hypothesis (Andrei & Hasler, 2015; Barber & Odean, 2008), according to which investors gravitate toward so-called “attention-grabbing” investment opportunities. This implies that news and events deemed worthy of investors’ attention tend to be more rapidly incorporated into prices. Previous empirical studies have found that awareness of a particular topic or company can predict trading volumes (Preis et al., 2010; 1933; Bordino et al., 2012), abnormal returns (Bijl et al., 2016), and price variation (the variance of returns) (Aouadi et al., 2013; Audrino et al., 2020; Ballinari et al., 2022; Goddard et al., 2015; Guidolin & Pedio, 2021; Hamid & Heiden, 2015; Smales, 2021; Vlastakis & Markellos, 2012).

Our main contribution can be summarized in three major findings. First, we document that after the public announcement of ChatGPT, all three portfolios underperformed their benchmarks. This decline was particularly significant in the education sector and the EdTech subsector. Our second finding is that the decline in stock returns is associated with increased attention toward ChatGPT. Specifically, this heightened interest leads to lower returns for the overall education and EdTech portfolios on the following day. Third, for these two portfolios, we identify periods of increased attention that are associated with both lower returns and lower comovement with the respective benchmark. These results show that the introduction of ChatGPT to the public had a disruptive effect on the education sector, particularly affecting the EdTech sector.

The remainder of this study is organized as follows. The next section discusses ChatGPT and its potential impact on the educational sector. To explore this topic, we have chosen to include a conversation with the chatbot itself. In Section 3, we present the data and methodology used in the analyses. Section 4 presents the results, and in Section 5, we offer some concluding remarks, implications, and directions for future research.

ChatGPT and Potential Challenges for the Educational Sector

OpenAI was formed in December 2015 and the now widely popular ChatGPT was released to the public on November 30, 2022 (Kirmani, 2022). The tool itself is based on the generative pretrained transformer (GPT) architecture, which is a type of neural network that has been trained on massive amounts of text data from the internet and other sources (Lund & Wang, 2023; Saggu & Ante, 2023). The first version of the transformer-based large language model was released in 2018 and had 117 million parameters. The second version (GPT-2) came in 2019 and had 1.5 billion parameters. GPT-3 was released in 2020 and had 175 billion parameters. In March 2023, GPT-4 was released, and this version is estimated to have more than one trillion parameters.

2

The chatbot has successfully completed a long list of tasks, including superior performance in a job interview for a coding position and generating movie scripts, stories, and song lyrics (Bhaimiya, 2023; Elias, 2023). How could the new tool potentially impact the educational sector? Inspired by the conversation (Lund & Wang, 2023) had with ChatGPT about a similar topic, we asked the chatbot to briefly explain how the new tool can affect the educational sector. Below, we provide a direct transcript of the conversation we had.

3

Q: “Can you give a brief description of various tasks ChatGPT can solve within the educational sector?” A: “Certainly! ChatGPT can be utilized for a wide range of tasks within the educational sector. Some of the key applications include: • • • • • • • • • • It’s important to note that while ChatGPT can provide valuable support in various educational tasks, it should not replace human educators. The model can assist in supplementing and enhancing the learning experience, but human interaction, critical thinking, and pedagogical expertise are still vital components of education.”

The educational tasks mentioned above, however, are key components of the business models of many companies operating within the educational sector, particularly within the EdTech domain. The release of ChatGPT to the public has the potential to disrupt the sector, creating considerable uncertainty about its future. It is, therefore, of particular interest to examine how the introduction of the new technology affects the market’s perception of such companies’ future prospects.

Material and Methodology

Education Sector

Our analysis is centered around three portfolios (sets of companies) that are created from U.S. based companies that belong to the “education services sector” (as indicated via the SIC Code 82).

4

In our analysis, we included only companies that have had a market capitalization of at least 50 million USD over our sample period and a volume of at least 0.1 million USD also over the sample period from January 1, 2022, until June 16, 2023.

5

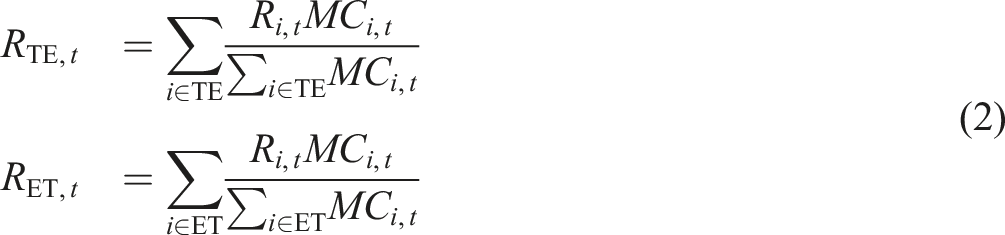

In total, 18 companies satisfied these requirements and were used to form our first portfolio that we refer to as the education sector. The average market capitalization of the portfolio over the sample period is 27.469 billion USD. Define Pi,t as the closing price on day t = 0, 1, 2, .., T and Ri,t = ln(Pi,t) − ln(Pi,t−1) as the continuous returns of stock i = 1, 2, …, N = 18, that is part of the Education sector. If we let MCi,t denote the corresponding market capitalization, the daily market capitalization weighted portfolio return of the education sector is given as

6

The introduction of the ChatGPT will likely have a larger impact on education technology companies, where products and services are facilitated through information technologies, by offering online learning tools, platforms, courses, learning management systems. In contrast, traditional education institutions mostly focus on owning and operating colleges, universities, and campuses. This led us to examine two distinct subsectors—the former is referred to as the EdTech sector, and the latter as the Traditional Education sector. Based on the products and services the companies offer, we assigned each company into one of the two subsectors, resulting in nine companies for each subsector. This classification is somewhat subjective, which is why we explore alternative subsector compositions in Section 4.3. The EdTech portfolio has an average market capitalization over the sample period of 16.600 billion USD, that is, the EdTech portfolio is about 50% larger than the portfolio of the Traditional Education subsector. The final list of all 18 companies, along with brief descriptions, can be found in Appendix A1. The resulting portfolio returns for traditional education (RTE,t) and EdTech (RET,t) are:

To estimate the potential impact of the public release of ChatGPT on the stock prices of the education sector, we use two methodologies that build upon the standard Capital Asset Pricing Model: i) the linear CAPM-GARCH model (Generalized AutoRegressive Conditional Heteroskedasticity) and ii) the threshold (in-mean) CAPM-GARCH model.

The CAPM-GARCH Model Framework

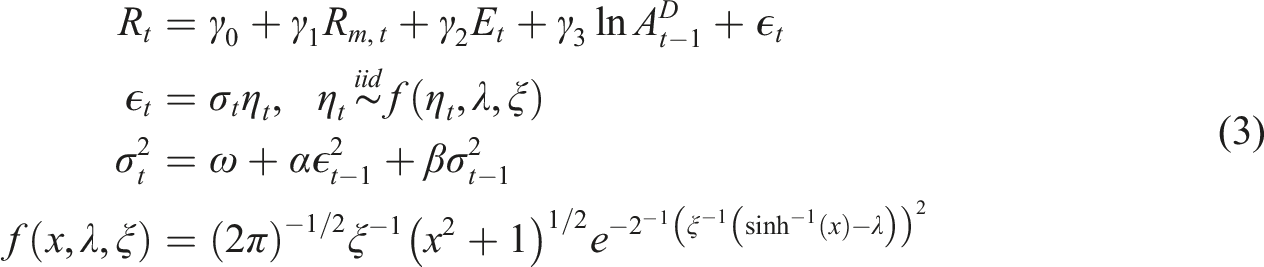

To examine whether the dynamics of the returns changed after the public release of ChatGPT, we estimate three specifications of the CAPM model for each of the three portfolios. In the first specification, we model portfolio returns only via market returns. This approach captures the sensitivity of the portfolio to market returns, Rm,t, that is the association between price changes on the market and the respective portfolio. Given the technological nature of ChatGPT and the widespread use of new technologies in education, we use the NASDAQ-100 as our representative market index, which we refer to as the technology market index. In the robustness section, we also include results that utilize the S&P 500 stock market index. To examine whether the period after the public release of ChatGPT has led to systematic changes to the returns of the various education portfolios, we introduce a second specification that includes the event dummy, E

t

. The event dummy takes value one from November 30, 2022, to the end of the sample period and zero otherwise. In the third specification, instead of using the event dummy, we include the Twitter-based attention measure, A

t

. The attention measure corresponds to the daily sum of geolocated tweets in the U.S. that contained the word “ChatGPT.” If the public release of ChatGPT affected investors’ expectations, we would expect that increased public interest in ChatGPT would lead to noticeable changes in the returns of education-related portfolios. This assumption is in line with the attention-based literature. However, it’s also possible that the relationship could be reversed—meaning that fluctuations in stock prices could actually drive public attention. To account for this possibility, we also incorporate lagged attention in our asset pricing equation (3). The advantage of using the attention to capture a specific event is that it i) does not need a specific event date and is thus useful if the effect is spread over a potentially long period of unknown length, ii) it shows variability, in contrast to an event-based indicator variable (i.e., E

t

). A general specification of the CAPM-GARCH model takes the following form:

Including the event dummy variable and the attention variables in the same model results in collinearity 7 that inflates the estimated standard errors. Such specifications are therefore not considered. The specification described above is just a comprehensive description of the most general specification. In the robustness section, we consider an alternative specification.

Threshold CAPM-GARCH Model

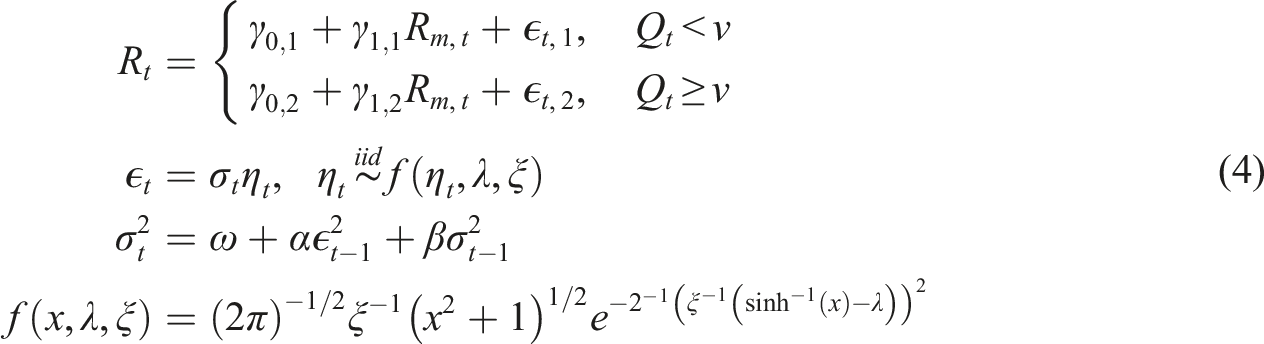

The public release of ChatGPT might have induced a structural break in i) the expected education portfolio returns and ii) the comovement the education portfolio returns have with the market returns. Hence, if market expectations about the future prospects of the firms operating in the educational sector start to change, we might observe a decoupling from the dynamics of the general market and increased exposure to the attention. A break in comovement is not captured in the linear CAPM-GARCH model. In such cases, the threshold regression offers an estimate of such a “kink point.”

8

Motivated by the threshold linear regression (see, e.g., Hansen, 2022), we allow state-variable-induced changes in the mean equation of equation (3). Specifically, the model implies that the returns behave according to one of the two models (regimes), depending on the state in which a given state-variable Q

t

is:

The model is linear in the coefficients, except for the threshold parameter ν. The model is estimated in two steps. In the first step, we estimate the threshold in the mean equation by minimizing the residual sum of squares. In the second step, we estimate the resulting CAPM-GARCH specification under different regimes. To assess the validity of our specifications, we check the serial correlation of the standardized and squared standardized residuals (e.g., ϵ t /σ t ) and test for the asymmetric volatility effects via the Engle and Ng (1993) test. We estimate robust standard errors following the approach of White (1982). Further robustness checks are provided in the corresponding section.

Results

Preliminary Data Analysis

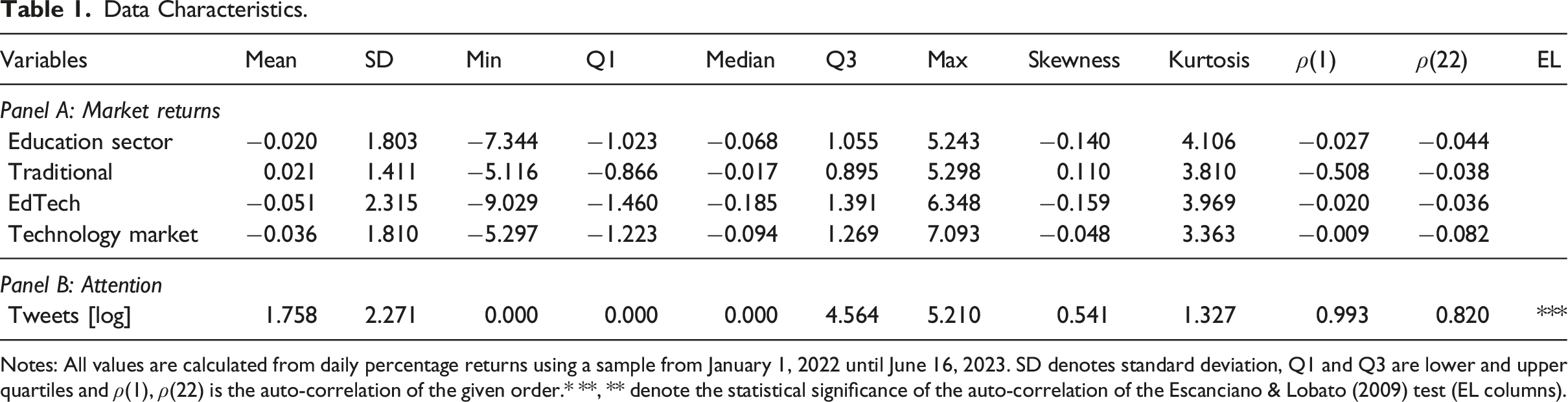

Data Characteristics.

Notes: All values are calculated from daily percentage returns using a sample from January 1, 2022 until June 16, 2023. SD denotes standard deviation, Q1 and Q3 are lower and upper quartiles and ρ(1), ρ(22) is the auto-correlation of the given order.* **, ** denote the statistical significance of the auto-correlation of the Escanciano & Lobato (2009) test (EL columns).

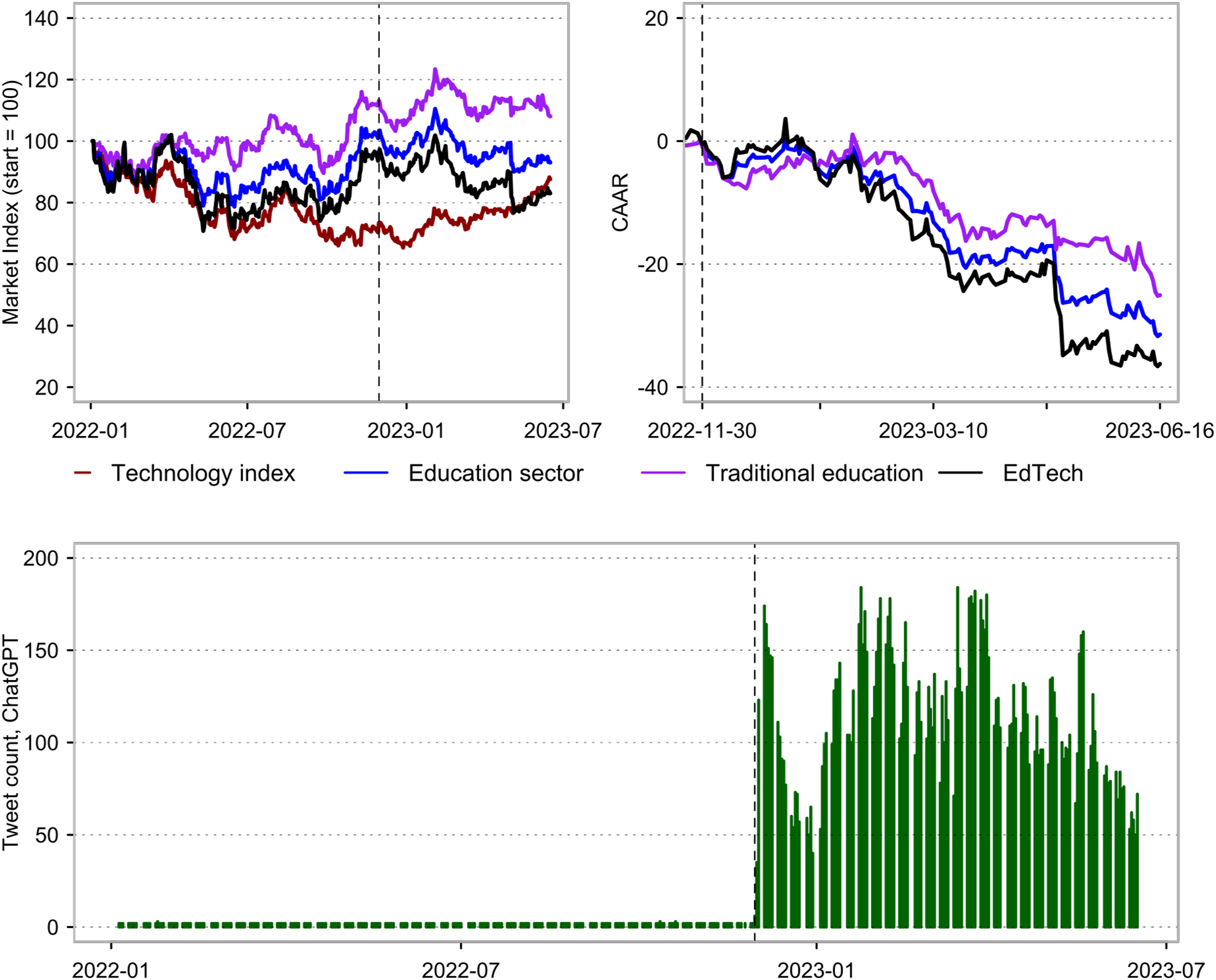

In Figure 1, we visualize the key variables in the study. Before the event date, the education sector outperformed the benchmark market index (see the upper-left panel of Figure 1). However, following the public release of ChatGPT, the performance of the education portfolios seems to decline in comparison to the market portfolio. This can be more formally examined by the cumulative average abnormal returns (CAARs). CAARs measure a portfolio’s return relative to expectations; a positive CAAR indicates that the asset performed better than anticipated. These are visualized for each portfolio in the upper-right panel of Figure 1.

10

The underperformance over the following eight months that coincides with the period after the public release of ChatGPT is considerable, with the EdTech subsector being the most affected. The upper-left panel shows a comparison of the education sector (blue line), the traditional education subsector (purple line), the EdTech subsector (black line), and the technology market index (NASDAQ-100). The upper-right panel shows cumulative average abnormal returns (CAAR). The CAARs are calculated for the period starting 5 days prior to the release date of ChatGPT (November 30, 2022). The CAARs are found as the cumulative market cap-weighted sums of abnormal returns of individual companies making up the education sectors. The abnormal returns were calculated using a single market model with the technology index representing the market returns. The estimation window goes from early 2022 until November 22, 2022. The results using an expanding estimation window are similar. The vertical dashed line corresponds to the introduction of ChatGPT to the public on November 30, 2022. The lower panel shows daily attention to “ChatGPT” on Twitter in the United States.

The “buzz” about ChatGPT started with its release on November 30, 2022. Before that, there were only a few tweets posted in the U.S. containing the word “ChatGPT” (see the lower panel of Figure 1). The attention to “ChatGPT” seems to be related to the observed decrease in the value of the EdTech sector. These preliminary results suggest an underperformance of the education sector and its subsectors. We will formally test whether we can attribute these changes in the pricing dynamics to the period around the event date and to the attention toward ‘ChatGPT’.

Empirical Results

CAPM Model Framework

Education Sector

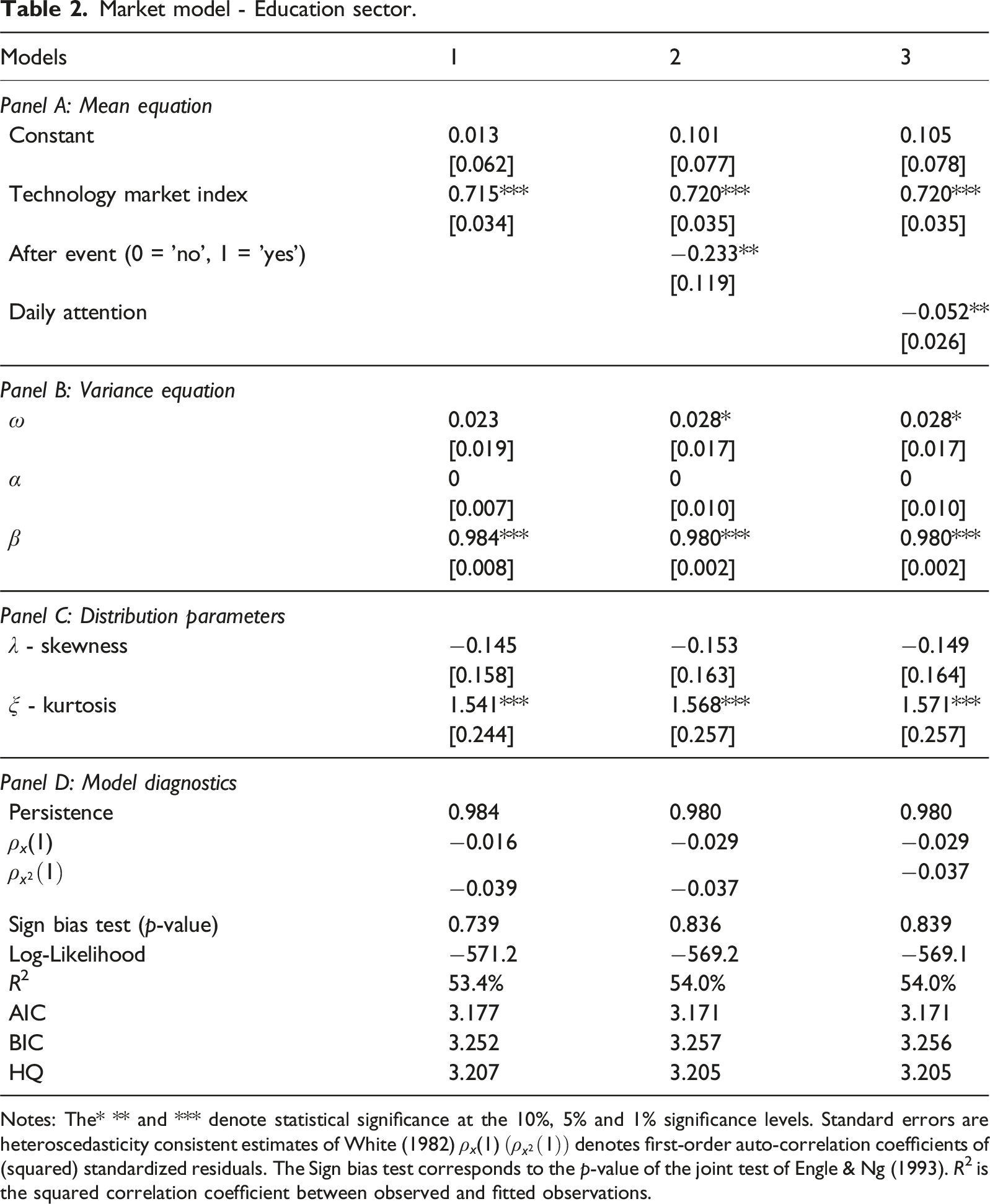

Market model - Education sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

In Model 2, we add an event dummy variable, taking value one from November 30, 2022, to the end of the sample period. The results show a negative, significant, and substantial long-term effect of −0.233. The education sector underperformed the benchmark index after the public release of ChatGPT, at least until the end of our sample period in June 2023. In Model 3, we include a one-day lagged attention measure. The results show that the lagged Twitter-based attention measure has a negative and significant association with next-day returns of the education sector with a coefficient of −0.052. A doubling of the current day’s attention (a 100% increase) induces a −0.052% decrease in returns. The results suggest that at least part of the decline in the performance of the education sector can be attributed to the increased attention to “ChatGPT.” For both Models 2 and 3, we have not observed any significant changes in the dynamics of the error terms. Volatility persistence and heavy-tail behavior of shocks only slightly improved the fit.

The Traditional Education and EdTech Subsectors

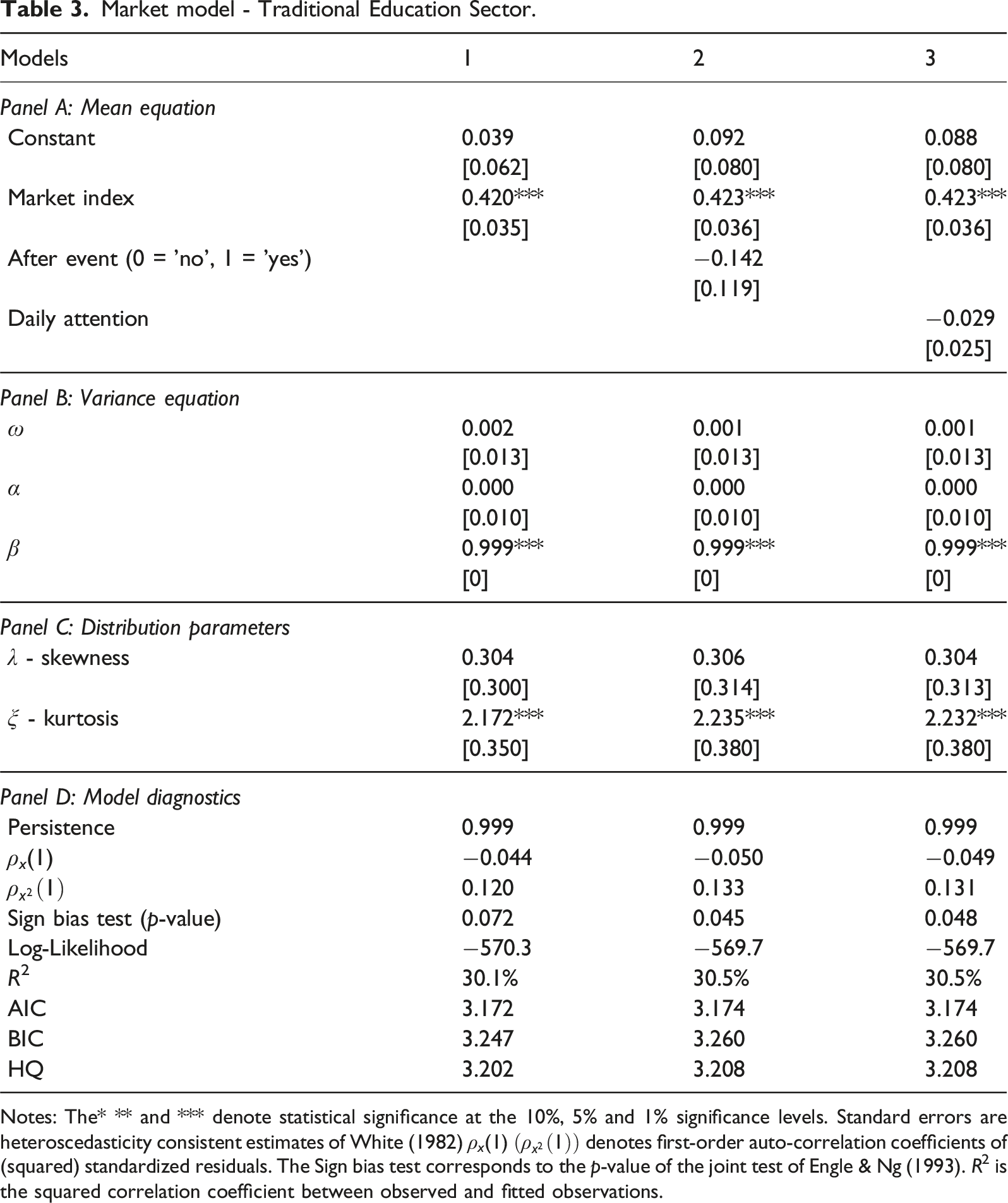

Market model - Traditional Education Sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

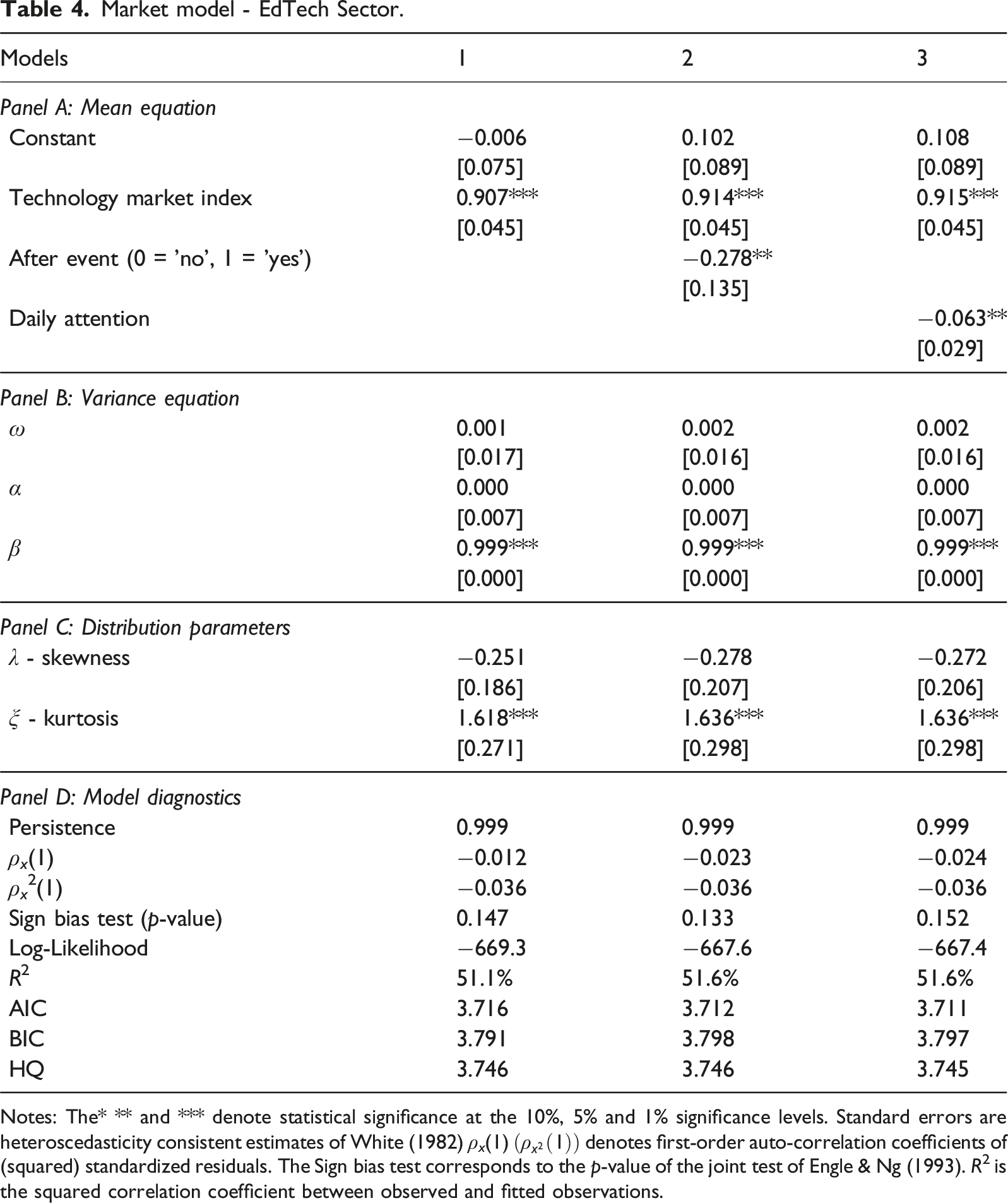

Market model - EdTech Sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

We also observe that while volatility is highly persistent for both portfolios, the EdTech sector has lower kurtosis. The fit of the model for the EdTech sector is also much higher. These results imply that the two subsectors have distinctive price dynamics that are captured for the whole sample period and the after-event period. In the next section, we will explore the differences between the pricing dynamics in greater detail.

Threshold Regression Framework

Education Sector

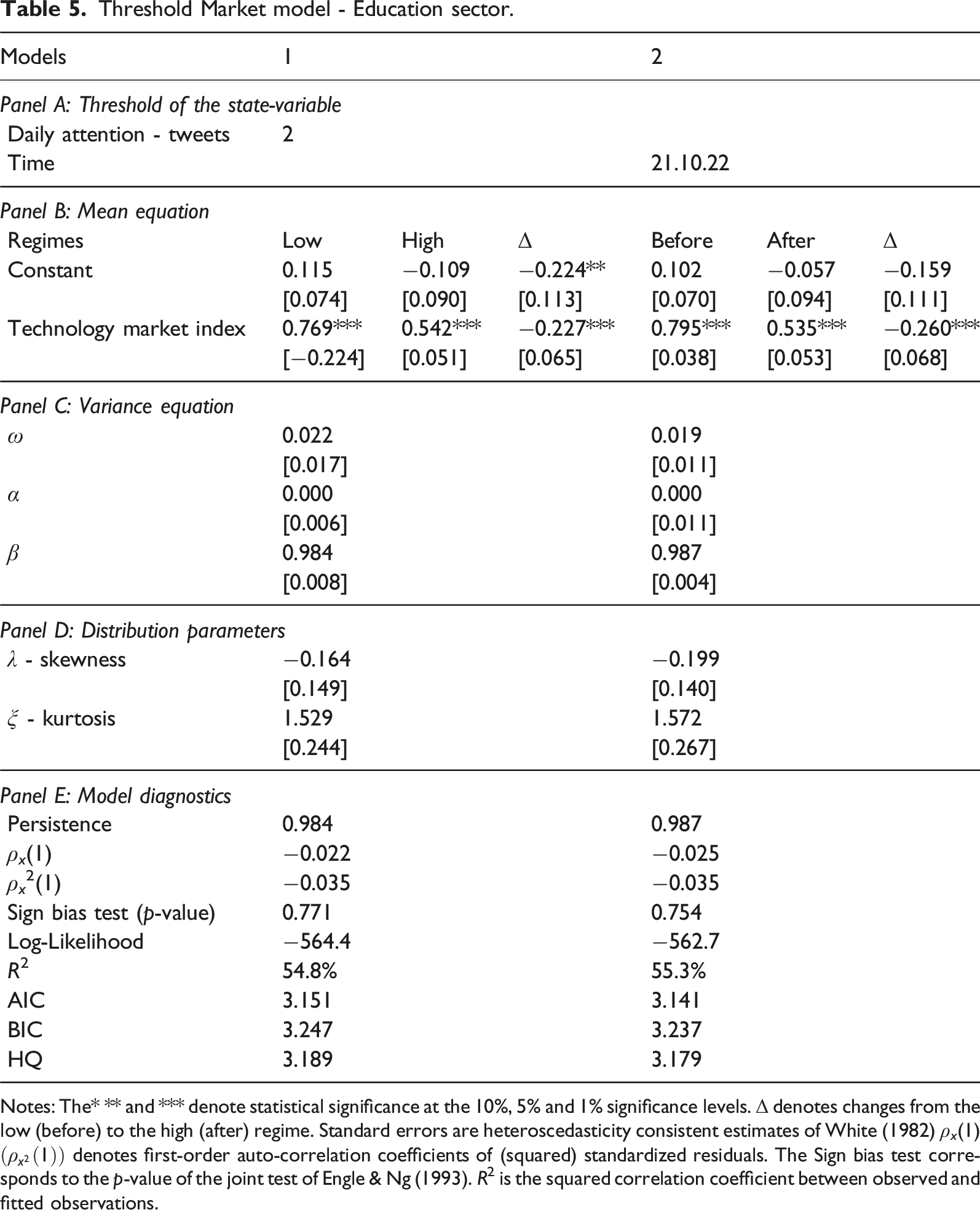

Threshold Market model - Education sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Δ denotes changes from the low (before) to the high (after) regime. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

In Model 2, we estimate the same model specification but now use the linear time trend rather than the number of tweets as the state variable. The threshold date is estimated to be October 21, 2022. During the ’Before’ period, which corresponds to the observations before October 21, 2022, we observe higher comovement with the market, while after that period, not only the comovement but also the expected returns have declined. These results are comparable to the attention-based results of the first specification.

Concerning model diagnostics, both models show high persistence of the latent volatility of the shocks, with significant kurtosis of the shocks. Overall, the results allow us to associate structural changes in the pricing dynamics to both attention and the period around the release of ChatGPT to the public.

The Traditional Education and EdTech Subsectors

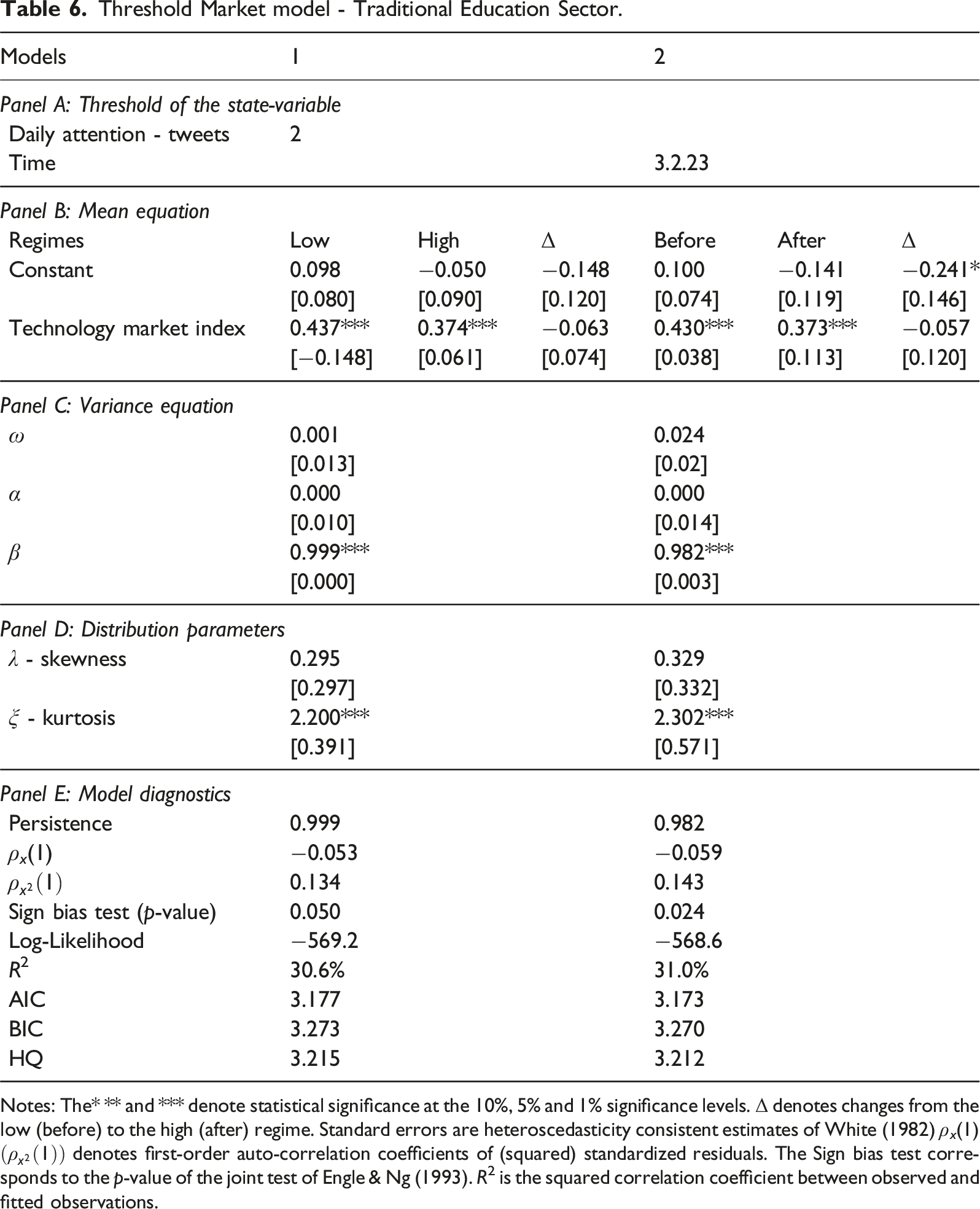

Threshold Market model - Traditional Education Sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Δ denotes changes from the low (before) to the high (after) regime. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

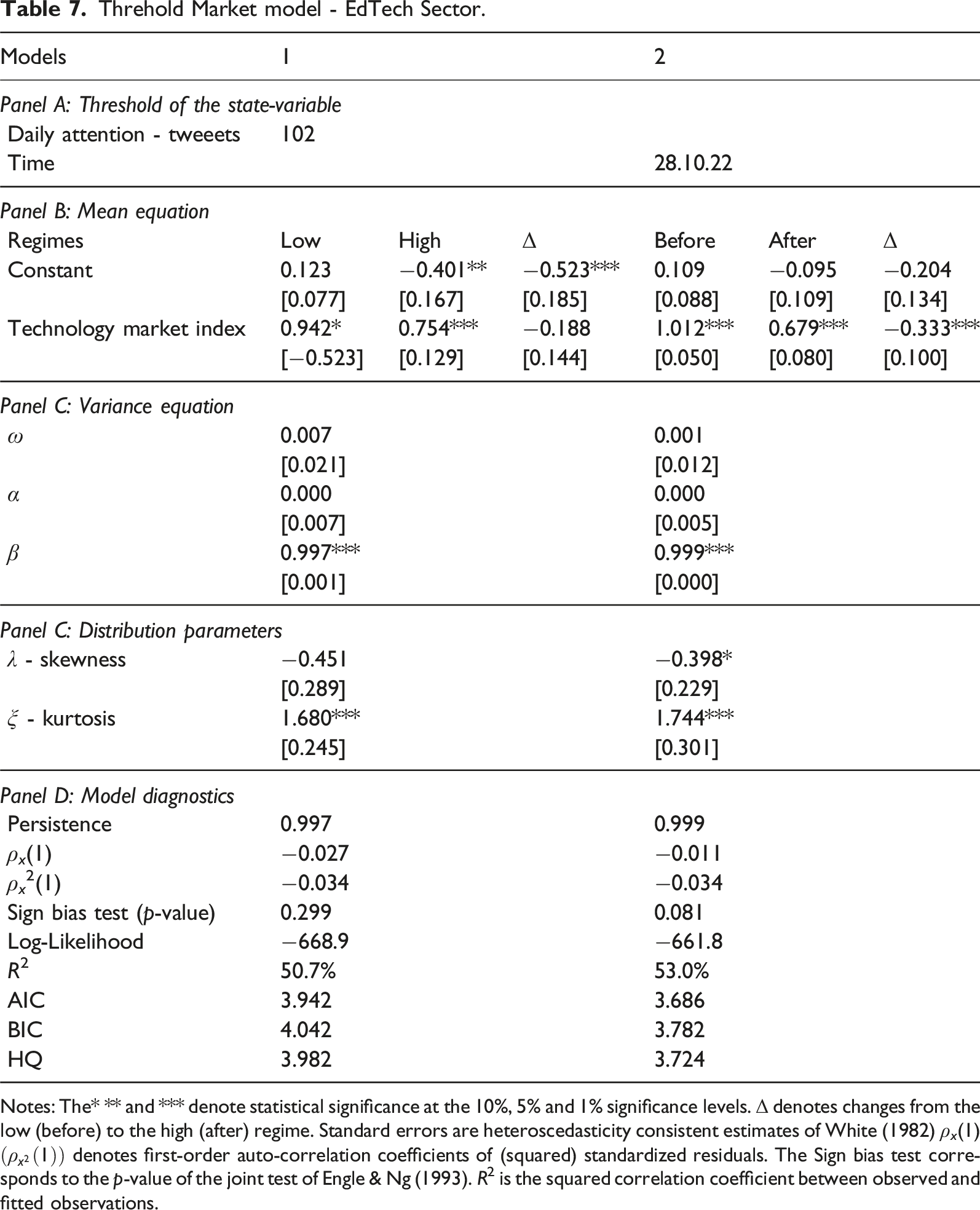

Threhold Market model - EdTech Sector.

Notes: The* ** and *** denote statistical significance at the 10%, 5% and 1% significance levels. Δ denotes changes from the low (before) to the high (after) regime. Standard errors are heteroscedasticity consistent estimates of White (1982) ρ

x

(1)

After switching the state variable to a linear time trend, the optimal threshold was identified to be on February 3, 2023, for the traditional education sector. In Figure 1, we observe that around February–March 2023, the traditional education portfolio started to decouple from the technology market index. Furthermore, we note a sharp decline in the cumulative abnormal returns depicted in the upper-right panel of Figure 1. After the threshold period, the returns of the traditional education sector underperformed and became slightly less sensitive to the development of the technology market index. The optimal threshold for the EdTech sector is estimated to be October 28, 2022, and is associated with a shift in expected returns from 0.109 to −0.095, albeit statistically insignificant. However, the sensitivity to the technology market index decreased from 1.012 to 0.679, a significant −0.333 decline. Moreover, we also observe that the shocks (see Panel C of Table 7) show high kurtosis and are also skewed to the left, that is, extreme negative shocks are more likely.

To summarize our main empirical results, the linear CAPM-GARCH models show that upon the public release of ChatGPT, the expected returns declined in the education sector. Moreover, the increased attention of the general public toward ChatGPT was followed by lower returns the next day, on average. The nonlinear threshold CAPM-GARCH model associated the changing pricing dynamics of the education portfolios with increased attention. The threshold CAPM-GARCH models also reveal that ChatGPT has a much stronger association with the EdTech sector than with the traditional education sector. Overall, the evidence shows that investors’ perception of the education sector, particularly the EdTech subsector, changed considerably after the release of ChatGPT and with increased attention toward ChatGPT.

Discussion and Robustness Analysis

In this section, we discuss the sensitivity of the results reported in the previous section concerning i) alternative model specifications, ii) use of equally weighted portfolios, iii) use of a different market index, and iv) assuming different variance equations and error distribution assumptions. All the results from these analyses are available upon request.

Within-Portfolio Variation

Part of the variation in portfolio returns might be driven by a few stocks in the portfolio. For example, returns of a few larger companies in the education sector might be declining, which impacts our conclusions for the whole (sub) sector. The heterogeneity of cross-sectional returns can be captured by the cross-sectional absolute deviation:

Equally Weighted Portfolios

Our main results are based on the market capitalization weighted portfolios (see Equations (1) and (2)), and the results might be driven by large companies only. We reestimate the linear CAPM-GARCH models with equally weighted portfolio returns. Our results hold and are very close to our initial estimates reported in Tables 2–4.

Under the nonlinear threshold CAPM-GARCH model, with attention being the state variable, we obtain results that do not change our main conclusions. For the education sector, the optimal threshold moved from 2 to 101, and we find higher decoupling for the high-attention period and a larger decline in expected returns. The results for the traditional education sector show changes in a similar direction but are not significant, similar to the main results. For the EdTech sector, we find the same optimal threshold at 102 daily tweets, but the sensitivity of returns does not change between the low- and high-attention regimes. On the other hand, we find a larger decline in expected returns. Hence, the results still show that the EdTech sector was affected negatively and the most among the portfolios.

The Benchmark Market Index: S&P 500

Our main results are based on the use of the NASDAQ-100 market index, which is overrepresented by growth-oriented, technology-driven companies. As an alternative, we reestimate all our models with the S&P 500 as the benchmark market index. Although the numerical results are most affected by this change in the market index, in summary, our main conclusions hold. The EdTech subsector shows a decline in expected returns associated with the event and increased attention in these analyses.

Specifically, for the linear CAPM-GARCH model, we find higher comovement across all education sectors, that is, the education sector is more sensitive to changes in the S&P 500 than to changes in the NASDAQ-100. We find a significant decline in expected returns after the public announcement of ChatGPT for the education and EdTech sectors and also a negative and significant coefficient for the lagged attention to the ChatGPT variable with similar magnitudes as reported in the main results.

Under the threshold model with the attention measure as the state variable, we find that for the education and EdTech portfolios, the optimal threshold is 102 daily tweets. In the high-attention regime, we do not find significant changes in comovement but a larger decline in the expected returns. The price dynamics of the traditional education subsector have not changed significantly. This shows that the choice of the benchmark index has not changed our main conclusions.

Alternative Error Distributions and Variance Equations

In the linear CAPM-GARCH models, we observed a high level of volatility persistence driven by the persistence of latent volatility. For such empirical scenarios, a suitable alternative might be the integrated GARCH model of Engle and Bollerslev (1986). Such models led to similar results, with the EdTech subsector having slightly larger effects. We also considered the asymmetric model (Glosten et al., 1993), but we found only occasionally significant negative asymmetric volatility effects, and the results again remained unchanged.

Finally, we considered two additional error distributions, the skewed Student-t and the skewed generalized error distribution (see Fernández & Steel, 1998). Our results remained robust also when using these alternative error distributions.

Alternative Assignment to EdTech and Traditional Education Subsectors

The assignment of companies into EdTech and Traditional education subsectors is to some extent subjective as not all products and services of a company are necessarily part of the EdTech or traditional education sector. However, not all companies have the same impact on the subsector’s portfolio returns. Therefore, we decided to study how our results change after we exclude the two largest (in terms of market capitalization) companies from each subsector (one at a time), as these companies have the highest impact on the returns of the respective subsector. This accounts for company choice uncertainty but also for assignment uncertainty of the largest companies.

For the EdTech subsector the two companies are Grand Canyon Education (LOPE) and PowerSchool Holdings (PWSC). Removing LOPE or PWSC led only to minor changes in the results, and not of qualitative importance. For example, the threshold date moved to October 26, 2022, after excluding LOPE from EdTech, as opposed to October 28, 2022. For the traditional education subsector, removing Graham Holdings Company (GHC) was also inconsequential with the threshold date moving to November 11, 2022. Otherwise, the results were qualitatively unchanged. The removal of Strategic Education did not lead to any major changes in the single equation model for the traditional education sector. Neither the ChatGPT event dummy nor the attention measure has a significant effect in this model. However, the threshold model now suggests that the most likely regime shift occurred on May 26, 2022. Yet there are only minor changes between the before and after regimes, which is consistent with our previous findings.

Conclusion and Implications

In this study, we argue that ChatGPT has the potential to disrupt the education sector. We use data from the U.S. stock markets to test the impact of the public release of ChatGPT in late 2022 on the price behavior of the education sector and two subsectors that we created: i) the traditional education sector and ii) the EdTech sector. The former is represented by companies that operate campuses and universities and offer traditional services in the education sector. The latter includes firms that operate in the intersection between education and technology.

Using a sample from January 2022 until June 2023, we first find that all three portfolios (overall, traditional, and EdTech) underperformed the benchmark market index after the public release of ChatGPT. However, using a linear CAPM-GARCH model with flexible error distribution, we were unable to confirm that the underperformance of the traditional education subsector is associated with the event or with the attention of the general public toward ChatGPT. Our second result is that contrary to the traditional education sector alone, the overall education and EdTech subsector show that i) after the event, expected returns significantly declined and that ii) increased attention toward ChatGPT is associated with a decrease in next day’s expected returns. These results are much stronger for the EdTech sector, which shows that ChatGPT will likely have a larger impact on technology-driven education companies (e.g., Udemy, Coursera, Chegg, PowerSchool).

We complement our analysis using a nonlinear threshold CAPM-GARCH, where the mean equation coefficients are subject to a structural change as a function of the attention toward ChatGPT (or linear time trend). The analysis reveals our third main result that for the overall education and particularly EdTech subsector, the expected returns decline in the high-attention regime. We also find that returns of the education sector and its subsectors decouple with the benchmark market return, possibly indicating disruption of a long-run relationship. This result was not confirmed when using the S&P 500 instead of the NASDAQ-100 as the benchmark market index. Although the results under the S&P 500 indicated a larger decline in the expected returns in high-attention regimes and after the announcement of ChatGPT. Overall, our main results remained robust when considering different mean and variance equation specifications and changes from the market capitalization weighted education portfolios to equally weighted portfolios.

Our results suggest that, at least from a short-term perspective, investors expect that the introduction of ChatGPT and the resulting revolution of LLMs poses challenges to the EdTech subsector. 11 Such challenges can be attributed to the threat that some of the services and products will be replaced. For example, language polishing and translation services are being routinely replaced by LLMs already. It might also be the case that new opportunities emerge from ChatGPT and related AI technologies (such as competing LLMs, like Microsoft copilot, for example). Companies may, for example, integrate new tools into their existing toolbox to increase student learning beyond what the stand-alone chatbot applications can offer. Innovations thus create threats and opportunities as well. Our analysis is short-term in nature and the market may well have overreacted though (see, e.g., Howe, 1986). The situation could thus turn around when investors have more information about the potential future impact of the new technology. Yet there are good reasons to believe that the entry of ChatGPT and similar LLMs have the potential to disrupt the educational sector completely. Future studies should, therefore, focus on replicating and extending the present study when more data becomes available.

Disclosure

Statement: During the preparation of this work, the authors used ChatGPT in an interview to obtain insights into how the new tool could affect the education sector. After using this tool/service, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.

Supplemental Material

Supplemental Material - Has ChatGPT Disrupted the Education Sector in the U.S.?

Supplemental Material for Has ChatGPT Disrupted the Education Sector in the U.S.? by Erik Haugom, Štefan Lyócsa and Martina Halousková in Social Science Computer Review

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Grantová Agentura České Republiky, nr. 22-27075S.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.