Abstract

The U.S. trucking industry has the potential to be an early adopter of autonomous vehicles. The trucking industry hauls the majority of U.S. freight by weight and has a vast infrastructure network. Numerous business cases and routes may be able to utilize autonomous trucks. The trucking industry consumes more fuel and has more crashes than other modes of freight transportation. Trucking companies may be able to reduce costs through labor savings and increased utilization of trucks. All the dynamics of market size, infrastructure, fuel consumption, safety, and cost savings make the trucking industry a potential early adopter of autonomous vehicles. For autonomous technology to be applied to trucks in the United States there needs to be interest from technology developers, truck manufacturers, and trucking companies; government support to allow the testing and deployment of autonomous trucks on public roads; and acceptance from the public who will share the road with autonomous trucks. Given that autonomous truck deployments are in the beginning stages of being tested on public roads, there needs to be a comprehensive review of the market potential of autonomous trucks from the perspective of all involved stakeholders. To provide this comprehensive overview, this paper reviews the current dynamics of autonomous truck deployments in the United States, including deployment markets, business cases, adoption timelines, and logistics-, manufacturing-, operations-, technology-, and government partnerships. The paper concludes with the possible benefits of and barriers to autonomous trucks to illustrate what may drive or impede their U.S. deployment and market potential.

Keywords

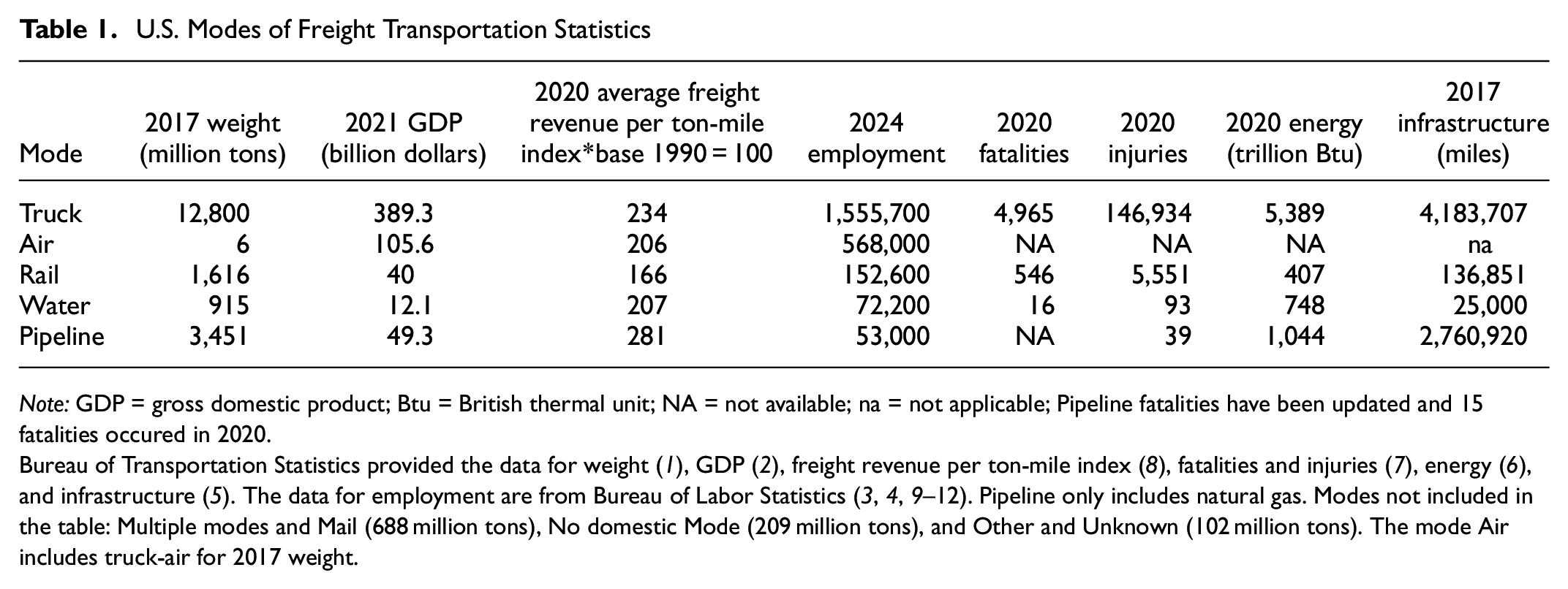

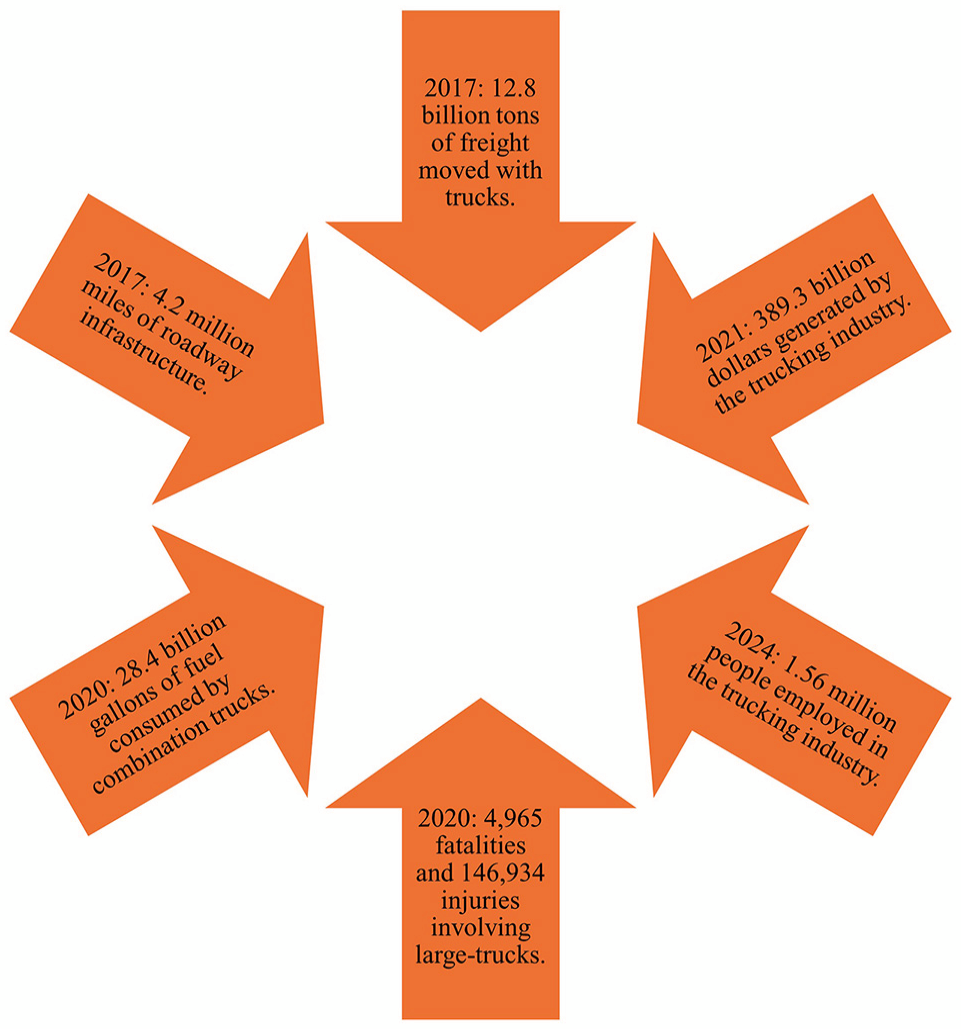

The trucking industry moved 65% of all goods by weight in the United States in 2017 ( 1 ). It contributed $389.3 billion to the U.S. gross domestic product (GDP) in 2021 with the for-hire sector responsible for generating $185.1 billion and the in-house sector $204.2 billion ( 2 ). The truck transportation sector employs 1.56 million people and 897,370 of those are heavy tractor-trailer truck drivers ( 3 ). Across all industries, heavy tractor-trailer truck drivers total 1.98 million ( 4 ). The U.S. trucking industry has prospered owing to the vast roadway system in the United States: with a total of 4.2 million roadway miles it has more miles of roadway infrastructure than other freight modes ( 5 ). The vast U.S. roadway system increases accessibility and allows for fast and reliable service. However, truck transportation also has higher fuel consumption and more crashes than other modes of freight transportation. In 2020, trucks consumed 44.8 billion gallons of fuel with combination trucks consuming 28.4 billion of those gallons ( 6 ). In relation to freight safety, 146,934 injuries and 4,965 fatalities occurred in 2020 from large-truck-related crashes ( 7 ). The trucking industry has experienced the second highest increase in average revenue per ton-mile since 1990. Pipeline transportation revenue increased 181% and truck transportation increased 134% (Table 1, Column 4). This translates into higher costs for shippers and consumers. The freight transportation statistics of the trucking industry compared with other U.S. transportation modes are given in Table 1. This table shows truck transportation to be the largest mode of U.S. freight transportation for weight moved, GDP, employment, and infrastructure. The data also indicate the need for improvements in relation to fatalities, injuries, and energy use. The market size and infrastructure in place in the United States makes trucking a potential early adopter of automation. Automation also holds promise for reducing crashes and improving fuel efficiency. Although the trucking industry appears to be a good market for autonomous vehicles (AVs), for autonomous trucks (ATs) to be deployed on public roads there will need to be shared interest and a recognition of the mutual benefits among the trucking industry, the government, and the general public.

U.S. Modes of Freight Transportation Statistics

Note: GDP = gross domestic product; Btu = British thermal unit; NA = not available; na = not applicable; Pipeline fatalities have been updated and 15 fatalities occured in 2020.

Bureau of Transportation Statistics provided the data for weight ( 1 ), GDP ( 2 ), freight revenue per ton-mile index ( 8 ), fatalities and injuries ( 7 ), energy ( 6 ), and infrastructure ( 5 ). The data for employment are from Bureau of Labor Statistics ( 3 , 4 , 9 –12). Pipeline only includes natural gas. Modes not included in the table: Multiple modes and Mail (688 million tons), No domestic Mode (209 million tons), and Other and Unknown (102 million tons). The mode Air includes truck-air for 2017 weight.

Background

Trucking Industry

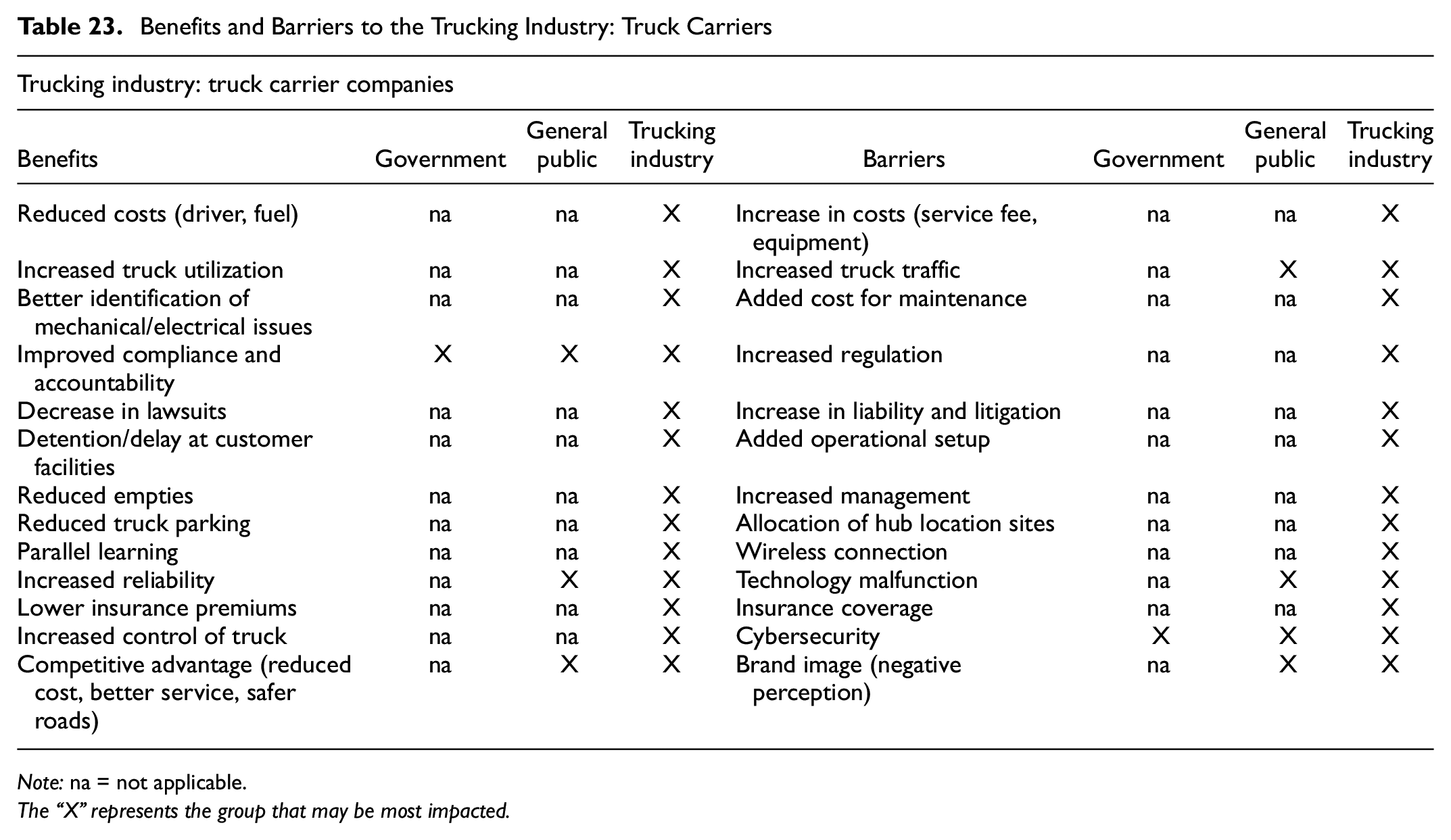

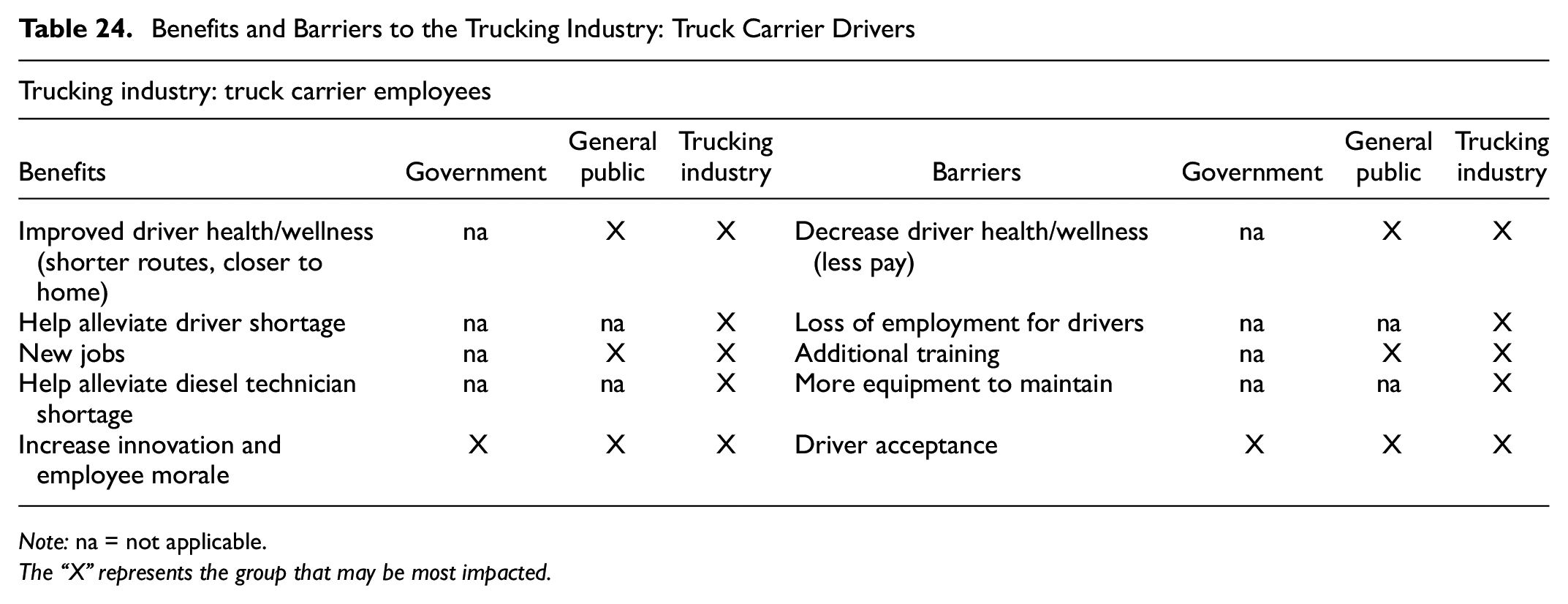

The trucking industry will help determine the initial use cases of ATs and their economic viability. For instance, certain truck carriers, routes, and types of freight may be better suited for initial deployments. These initial deployment scenarios are currently being tested by several logistics companies. The AT pilots currently taking place are on high-volume freight routes in the Southwestern United States. Whereas this is the predominant testing area for ATs, testing of platoons in North Dakota and autonomous box trucks in Arkansas and Toronto can also be found. ATs might be used on routes where it is difficult to hire enough drivers to meet the demand for truck transportation; they might be deployed to help offset peak demand for holidays or harvest or other seasonal truck moves; and could be used on routes that are less desirable for drivers. ATs could also be used to move goods to remote areas or on long-distance routes that require drivers to be away from home for long periods of time. How and where ATs are ultimately deployed will determine their market potential.

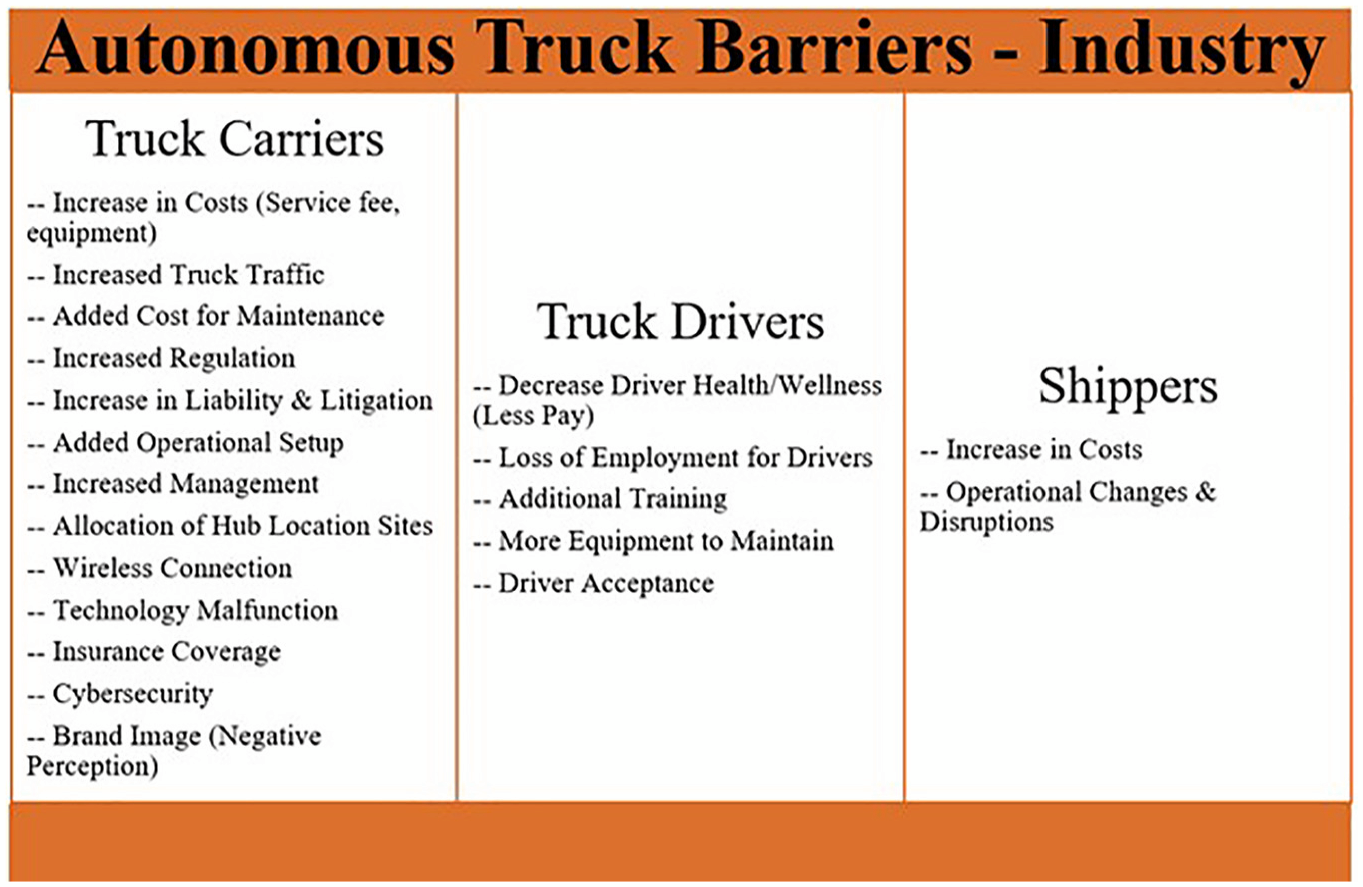

Interest in ATs is relatively new. Daimler Truck announced their vision for the future of automation in heavy-duty trucks in 2014 with Mercedes-Benz Future Truck 2025 ( 13 ). Since then, Daimler and several other companies have focused on developing Level 4 ATs. Level 4 ATs can operate in specific operating domains without a driver in the truck. The different levels of automation are described in detail in the next section. There has been rapid acceleration in testing, partnerships, and investor interest, with projected timelines for U.S. deployment before 2030. Daimler Truck is planning to deploy ATs in the United States in 2027 ( 13 ). Since the AT ecosystem is in the beginning stages of development, it is unclear what the relationship will be between AT companies, original equipment manufacturers (OEMs), trucking companies, and third-party logistics (3PL) companies. AT companies, OEMs, and 3PL companies could start building their own AT capacity. Even though it is unclear how these relationships will evolve, it is clear that companies within the trucking industry are interested. There are many benefits for trucking companies that adopt ATs, including labor savings, reduced fuel consumption, and higher truck utilization. At the same time, there are also barriers like job losses and concerns about the safety of other roads users. This balance will play out over time as more pilots and tests are performed with ATs. Given the industry’s nascent stage of development, the AT ecosystem of partnerships and commercial applications are provided in detail in this paper to provide clarity on the market potential for ATs.

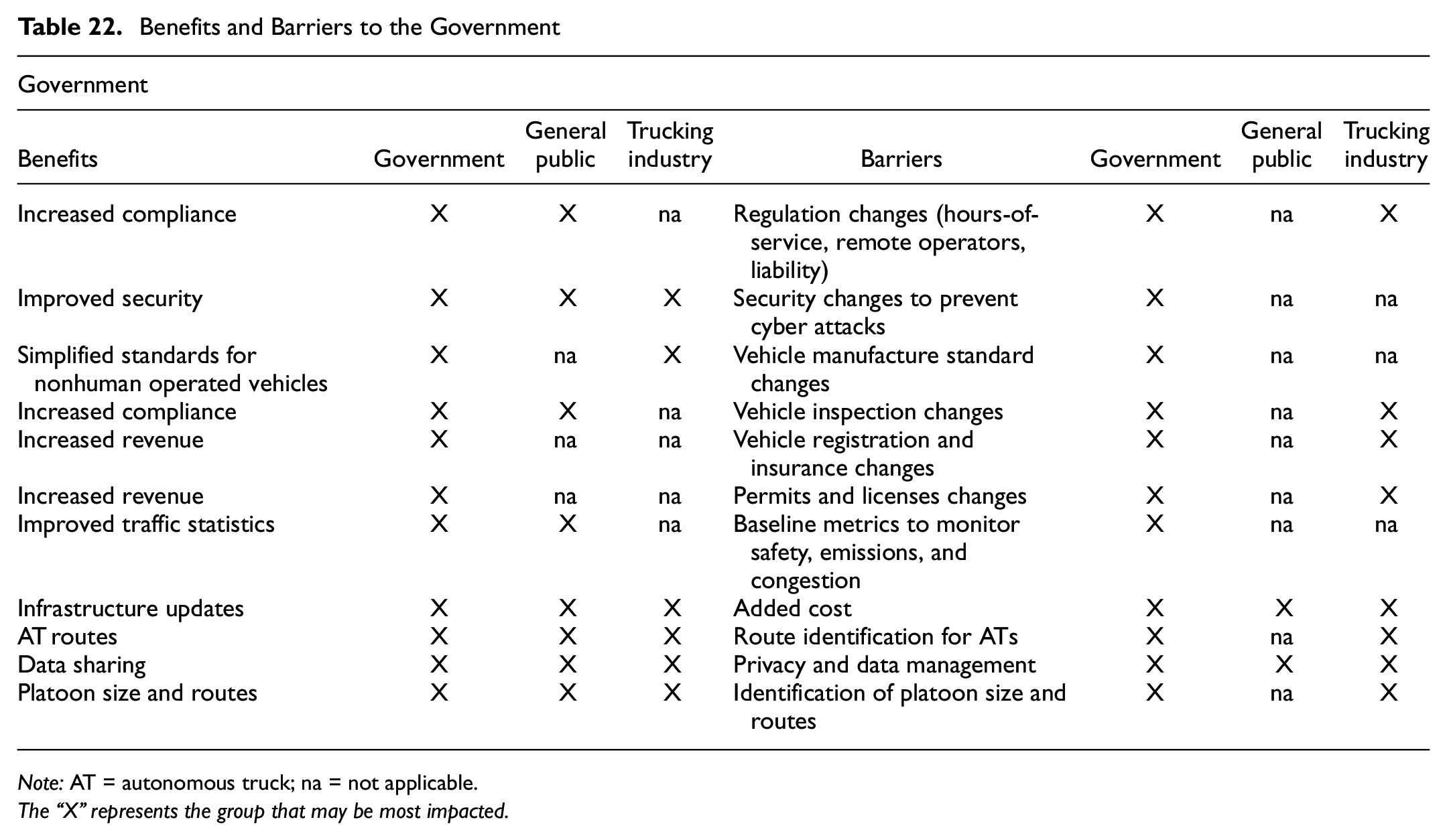

Government

The U.S. government will play a major role in the adoption of ATs by providing the infrastructure, maintaining roads, and regulating the operation of ATs. Roads in the United States are owned and managed by either the local (77.4%), state (19.6%), or federal (3.0%) government ( 14 ). The funds used to build and maintain the roads also come from local, state, and federal sources. Funding sources include fuel taxes, tolls, license fees, heavy-truck tire sales, truck and trailer sales, and weight-based heavy-vehicle taxes. The amount that each of these sources contributes varies by state ( 15 , 16 ). ATs may require upgrades to current roads to improve pavement condition, signs, and lane markings. In addition to traditional road improvements, new technologies may need to be added to roads to facilitate the deployment of ATs. These new technologies might include sensors that will enable connectivity among roads, vehicles, infrastructures, traffic signals, and other road users. It is also possible that new road systems will need to be built with dedicated lanes for ATs. All of these changes will require the government to be involved in the adoption of ATs. Regulation will also play a critical role in the adoption of ATs, determining where they can be deployed, what roads they can use, what conditions they can operate in, what hours they can operate, how they will handle edge cases (i.e., driving situations that ATs have not yet been trained to handle), and ethical situations that arise on the road—for instance, who will be liable when a crash occurs—and many other situations that could arise. Regulation of ATs in the United States is currently supported by the federal government, though regulation is being created at the state level. The U.S. Department of Transportation (U.S. DOT) published its first recommendations for automated vehicle policies in 2016 ( 17 ). U.S. DOT’s most recent publication, Automated Vehicles: Comprehensive Plan, was published in 2021 and focused on three goals: promoting collaboration and transparency, modernizing the regulatory environment, and preparing the transportation system ( 17 ). The U.S. government recognizes the need to allow innovation while ensuring safety. Presently, federal regulators believe individual states are best suited to maintaining this balance and to enact laws for ATs. As the AT industry matures and business cases are evaluated and tested, laws can be crafted to help safely introduce ATs.

Several federal agencies will be involved in the adoption of ATs including the Federal Motor Carrier Safety Administration (FMCSA), the National Highway Traffic Safety Administration (NHTSA), the Federal Highway Administration (FHWA), and the Commercial Vehicle Safety Alliance (CVSA). FMCSA regulates commercial trucking in the United States to improve safety on the roads ( 18 ). That agency will determine whether ATs have to obey driver hours-of-service (HOS) requirements and many other trucking regulations. In 2019, FMCSA issued an advanced notice of proposed rulemaking for the safe integration of automated driving systems for commercial vehicles ( 19 ). NHTSA sets standards for manufacturing vehicles known as Federal Motor Vehicle Safety Standards to help improve road safety ( 20 ). These standards include the corporate average fuel economy standards that regulate fuel efficiency for vehicles ( 21 ). NHTSA will play a role in determining how manufacturing and safety standards may change for ATs. In 2021, NHTSA issued a standing general order that requires the reporting of crashes that occur with advanced driver assistance systems ( 22 ). FHWA manages the building and maintenance of the U.S. highway system ( 23 ), and will play an important role in designing highways that are safe for the adoption of ATs. FHWA has many research and outreach programs to help deploy AVs, including a project to examine how a truck platoon approach to using technology would function in commercial applications ( 24 ). CVSA created inspection standards known as the North American Standard Inspection Program for commercial vehicles to help improve consistency in inspection and safety on the roads ( 25 ). Its inspection process will determine when ATs are in compliance and safe to operate on the roads. CVSA set guidelines for AT inspections in 2022 ( 26 ).

Significant preparations for ATs at the state level are also taking place. Texas Department of Transportation (TxDOT) recognized the need to prepare for AVs and created the Connected and Automated Vehicles Task Force in 2019 ( 27 ). The task force has several divisions to help handle the introduction of connected and automated vehicles including, Data, connectivity, cyber security, and privacy; Education, communication, and user needs; Freight and delivery; Licensing and registration; Safety, liability, and responsibility; and Workforce and economic opportunities ( 28 ). The committee directly related to ATs, Freight and delivery, may evaluate operational challenges, trials and deployments, delivery modes, infrastructure, maintenance, networks, and workforce development ( 28 ). With Texas being the current location of planned AT deployments, it makes sense that TxDOT is preparing for their introduction. The description of the AT ecosystem of partnerships and commercial applications in this paper will help to provide clarity on the geographical scope of ATs and the governments that will need to be prepared for their adoption.

General Public

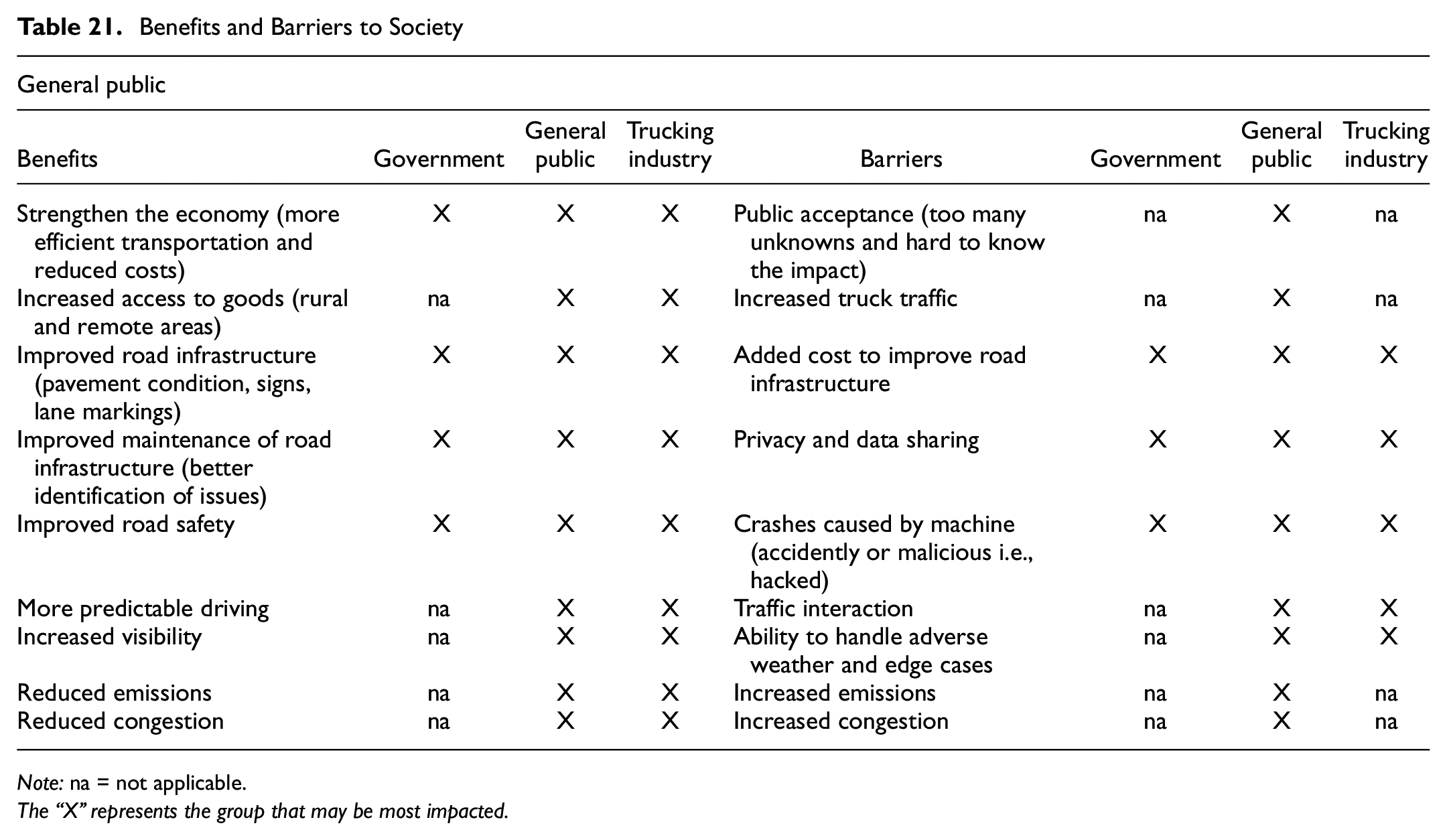

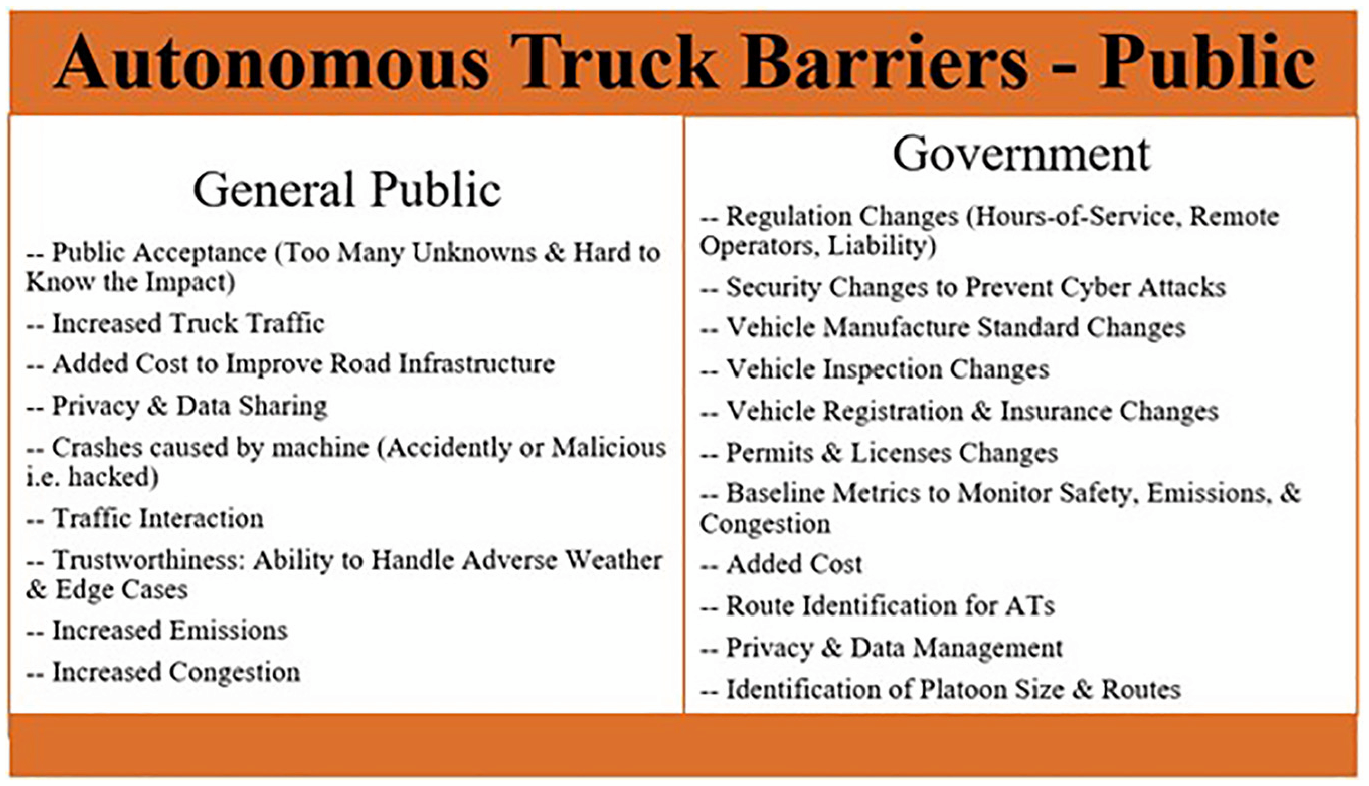

The people of the United States have a vested interest in how ATs are deployed because they may be sharing the road with them in the future. How people perceive ATs will determine whether they are adopted and what their market potential will be. How people perceive ATs will be determined by the information they receive about them. It will be important for people to have access to unbiased information to make informed decisions about ATs. Several of the benefits and concerns related to deployment of ATs can be viewed from either side. For instance, ATs might improve safety for all road users by eliminating human error, but they might equally introduce new types of errors that humans do not make, which could cause crashes. Such errors are most likely to occur during edge cases. The same logic applies to emissions and congestion: ATs may decrease emissions by operating more efficiently, but equally could increase emissions through increased vehicle utilization. Likewise, congestion might decrease because of the utilization of ATs during nonpeak operating hours, but increase as a result of the increased use of ATs. Therefore, public perceptions are likely to be formed by particular use cases of ATs and the testing of ATs in these use cases. The AV industry is beginning to focus on more-specific use cases. Presently, companies are focused on two main applications, robotaxis and freight delivery, rather than automation of passenger vehicles. Because this paper focuses on the market potential of ATs, the partnerships and business cases are provided in detail for ATs to help provide clarity on concerns that need to be addressed and, ultimately, how ATs will be perceived by the public.

Although the trucking industry, the government, and the general public will all need to reach a consensus on the deployment of ATs, the majority of the activity currently taking place is within the trucking industry. Partnerships are being formed and ATs pilots are taking place on public roads. Governments have begun to enact regulations that will adequately address the challenges of deploying ATs, though this is mainly within the states where the industry is currently testing ATs. Most people have had minimal exposure to ATs and it is unknown what their perception will be until ATs are tested in their area. Industry partnerships are the main focus of this paper because they provide the most comprehensive information on the market potential of ATs. This paper begins by discussing the historical roots of automation to provide context on how automation in vehicles has evolved. The current levels of automation, as defined by NHTSA, are then explained. The technology that facilitates the automation of vehicles is described in detail to outline the strategy for the deployment of Level 4 ATs. The AT ecosystem and the partnerships being formed are then elaborated, which includes the deployment markets, business cases, adoption times, and industry partnerships being formed. Finally, the benefits of ATs and potential challenges to their deployment are described to illustrate why ATs may be adopted and what might prevent their adoption. Concluding remarks are provided on the market potential of ATs in the United States, and on future directions of research.

History and Current State of Autonomous Vehicle Technology

Historical Roots of Automation in Vehicles

Kröger provides a historical account of automation in vehicles ( 29 ). AVs have been on the minds of Americans for over 100 years. The idea of AVs was first conceptualized with the mass commercialization of the automobile in the 1920s, and was seen as a way to remedy the crashes associated with the increased road traffic ( 29 ). The development of remote-controlled vehicles in the 1920s and 1930s further suggested the concept of AVs was feasible. The remotely controlled car would be followed by another car with a driver who would control it ( 29 ). The idea of a car being remotely controlled caught the attention of the public and demonstrations were given in 37 U.S. states, though the impetus of the demonstration was safety and not autonomous driving ( 30 ). In a further development, it was proposed that vehicles would be controlled by wires built into the highway. A test was performed on a highway in Nebraska in 1957 using this method ( 31 ). Researchers and innovators continued to explore this idea from 1930 until 1970.

Safety and convenience features such as cruise control began to emerge in vehicles in the late 1950s. In the United States, the cruise control mechanism created by Ralph Teetor first appeared in vehicles in 1958 ( 32 ). The conceptual move from using infrastructure to using vision through cameras on vehicles to make vehicles autonomous came about in the 1970s. Additional safety features also started to emerge during this decade with antilock braking systems (ABS) being fitted in vehicles. Interestingly, ABS technology was first tested in airplanes and trains: it began to be integrated into airplanes in the 1950s because of the safety and economic benefits ( 33 ). When ABS was initially introduced in the United States, it was an expensive technology that cost about 6% of the base price of the vehicle ( 33 ). In 1977, Tsukuba Mechanical Engineering made an AV that could recognize street markings using cameras ( 34 ). During the 1980s, in-depth research into AVs commenced, and in 1986 Ernst Dickmanns and his team at Bundeswehr University Munich equipped a van with computers, sensors, and cameras that was able to drive autonomously ( 35 , 36 ). This test prompted interest in the automotive industry about the possibility of AVs. Ernst Dickmanns and his team joined the European Eureka PROMETHEUS Project, which culminated with demonstrations in 1994 and 1995. In 1994, Dickmanns’ team created an AV that drove in Paris traffic, though a driver had his hands on the wheel, ready to take over if needed ( 36 ). In 1995, another autonomous demonstration was conducted from Munich, Germany to Copenhagen, Denmark under driver supervision ( 37 ).

Other AV projects started to emerge in the United States and Italy in the 1990s ( 35 ). Carnegie Mellon started working on AVs in 1986 ( 38 ). In 1995, students at Carnegie Mellon University created an autonomous system using cameras, GPS, and computers that controlled the steering of a van ( 38 ). They rode in the van from Pennsylvania to California and controlled the braking and accelerating. In 1991, the U.S. Congress passed the Intermodal Surface Transportation Efficiency Act (ISTEA), which initiated the development of AVs by U.S. DOT ( 39 ). As part of this Act, a demonstration was conducted in 1997 on Interstate 15 near San Diego to test various deployment scenarios for AVs. U.S. DOT created the National Automated Highway System Consortium to help engage public and private sectors for the demonstration. Four scenarios were tested during the demonstration: 1) a multiplatform scenario with buses and passenger cars that used sensors, 2) a platooning scenario with passenger cars that used sensors and magnets in the highway, 3) an alternative technology scenario that used radar-reflective tape, radars, and cameras, and 4) an evolutionary scenario that used advanced driver assistance technologies. After the demonstration, the U.S. DOT decided to focus on partially automated driving features.

Another driver assist feature, the Electronic Stability Program (ESC), became available in the 1990s. ESC is an extension of ABS that uses additional sensors to help correct the path of a vehicle by activating brakes on one or more wheels or activating the throttle. This helps to counteract driver overreactions to a situation that might result in a rollover. Even though this feature offers the potential to help reduce crashes, it was slow to be adopted by the auto industry ( 40 ). AVs started to gain traction in the United States with the first U.S. Defense Advanced Research Projects Agency (DARPA) Grand Challenge in 2004 ( 41 ). The DARPA Grand Challenge was created to stimulate AV research within the United States for military applications, but it ended up stimulating the race for AV deployment in commercial applications. No teams completed the first competition, but in 2005, five teams completed the 132-mi course over dessert terrain in the Southwest United States ( 41 ). In 2007, DARPA held an urban challenge in which AVs had to be able to handle on-road driving conditions such as merging, passing, and parking ( 42 ). Six teams completed the course at George Air Force Base in California, indicating that AVs could handle these typical driving maneuvers. One of the first U.S. AV companies, Waymo, was cofounded by Sebastian Thrun, who was on the winning team for the 2005 DARPA Grand Challenge ( 36 ). AV technology has advanced rapidly since 2005, and numerous companies are now competing in AV development and deployment.

Automation Levels in Vehicles

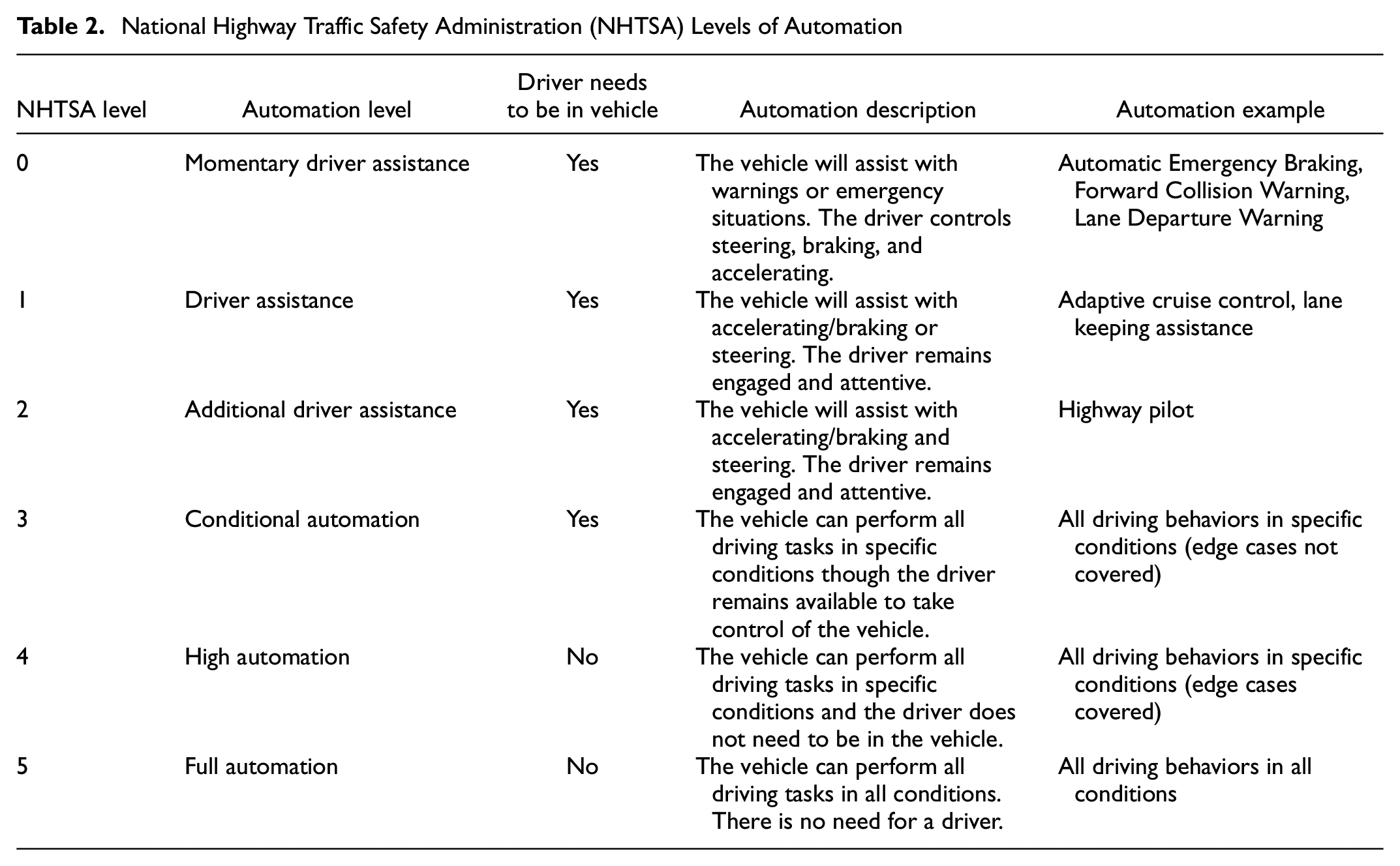

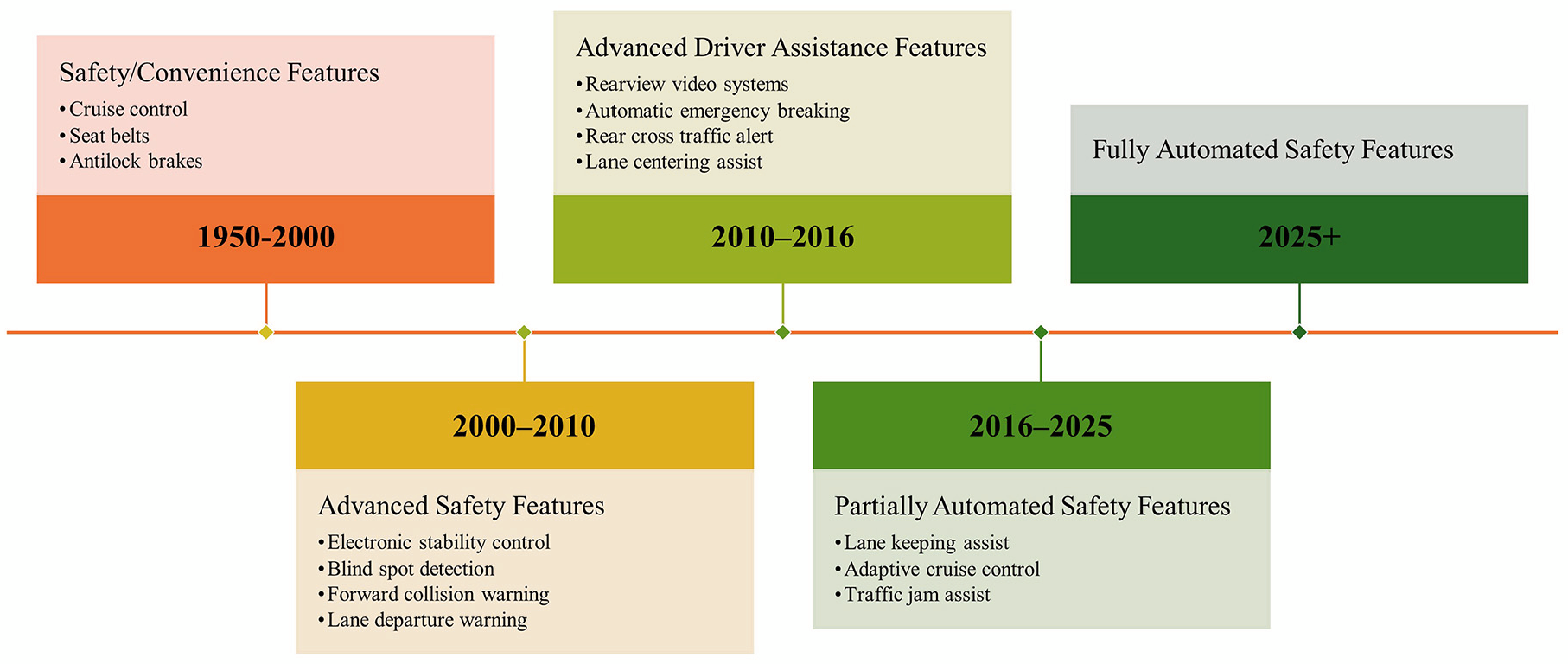

NHTSA has defined “Five Eras of Safety” for vehicles that have taken place since 1950 ( 22 ). The first era was between 1950 and 2000 and includes safety features like cruise control, seat belts, and antilock brakes. The second era, 2000 to 2010, has more advanced safety features like electronic stability control, blind-spot detection, forward collision warning, and lane departure warning. The third era, 2010 to 2016, includes advanced driver assistance features like rearview video systems, automatic emergency breaking, and lane centering assist. The fourth era, from 2016 to 2025, includes partially automated safety features like lane keeping assist, adaptive cruise control, and traffic jam assist. The final era, from 2025 onward, will include fully automated safety features. As vehicle technology has progressed, NHTSA has required vehicle manufacturers to adopt features that improve safety. For instance, in 2014, NHTSA announced that new vehicles under 10,000 lb must have rear visibility technology by 2018 ( 43 ). In 2023 they proposed a rule that would require automatic emergency breaking on passenger cars and light trucks ( 44 ). To help provide clarity on the automation of a vehicle, levels of automation have been defined. NHTSA provides six different levels of automation to define the relationship between the driver and the vehicle ( 22 ). For Levels 0, 1, and 2, the driver is in control of the vehicle while the system provides momentary assistance with braking, accelerating, and/or steering. For Levels 3, 4, and 5, the system drives, and the driver has varying roles of responsibility. For Level 3, the driver must be ready to take control of the vehicle if needed. For Level 4, the driver is not needed if the vehicle is operating within a specific operating domain. For Level 5, the driver is not needed and the vehicle can operate in all operating conditions. Table 2 describes the six levels of automation and the driving features that correspond to each level.

National Highway Traffic Safety Administration (NHTSA) Levels of Automation

Technology Used in Autonomous Vehicles

The technology used in AVs includes two main components, sensors and machine learning algorithms. The sensors include perception devices in the vehicle such as radar, lidar, and cameras that enable the vehicle to perceive the surrounding environment. Machine learning algorithms help the vehicle to make sense of all these data and to detect or predict what action the vehicle should take. The industry is currently pursuing the approach that automation technology should be within the vehicle and not the infrastructure. This approach allows the market dynamics of the technology to play out instead of relying on government-funded infrastructure updates. A hybrid approach might be used in the future that would employ sensors in the vehicles, in infrastructure, and on nearby pedestrians. This approach, known as vehicle-to-everything (V2X), crucially includes communication between the sensors on vehicles, infrastructure, and even other road users such as pedestrians. This is an area that is currently being researched and tested by U.S. DOT, although the industry is not relying on it vehicle communication technology for initial deployments ( 45 ). The additional information from infrastructure and nearby vehicle sensors could be combined with the perception technology in vehicles. This should increase the prediction accuracy of machine learning algorithms because all of the information could be used to determine the best next action. Because companies are currently pursuing the deployment of AVs using just perception devices, some additional detail is provided on these technologies.

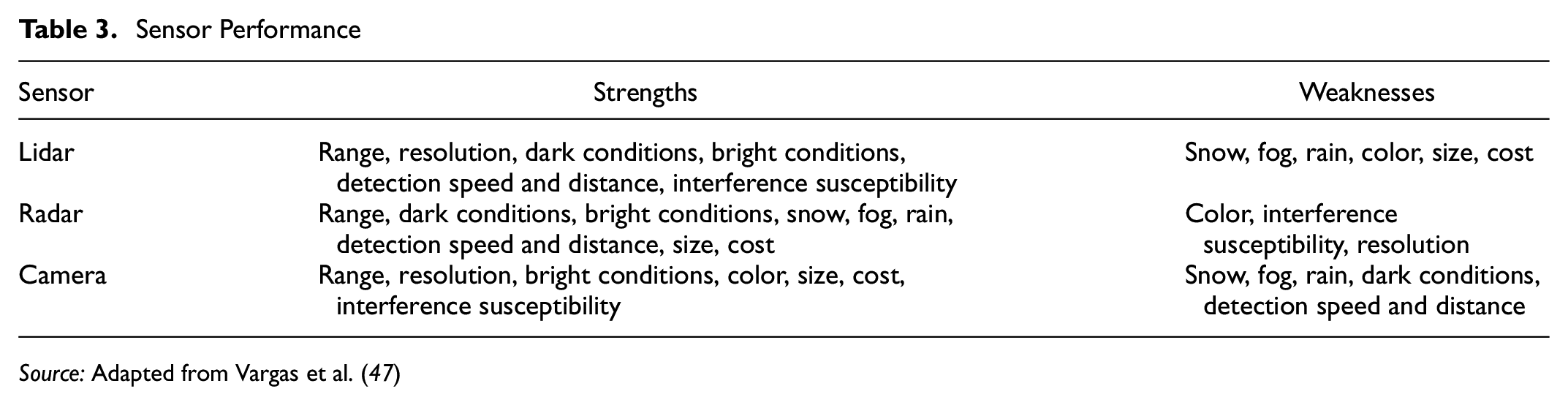

Yeong et al. undertook a review of sensors used in AVs ( 46 ). Radar (radio detection and ranging) uses radio waves to detect objects, lidar (light detection and ranging) uses light waves to detect images, and a camera uses a lens to pick up light emitted from the surfaces of objects. Each device has benefits and drawbacks. Radar uses electromagnetic waves to determine the speed and position of objects and is therefore not affected by environmental lighting or weather conditions. This makes radar useful for detecting objects at night and in adverse weather conditions. However, radar only provides a coarse image of the objects detected so it needs to be combined with cameras and lidar for improved object detection. There are three types of radar used in vehicles: short-, medium-, and long-range radar. Short-range radar is useful in parking assistance and collision proximity warning. Medium-range radar is useful for side-/rear-collision avoidance and blind-spot detection. Long-range radar is useful for adaptive cruise control and early detection applications ( 46 ). Lidar uses ultraviolet, visible, or near-infrared light to determine the distance to an object. The points received from lidar (known as a point cloud) can be used to generate three-dimensional (3D) representations of objects. Lidar has a large range, is accurate, and is able to quickly scan the environment, but performance declines in adverse weather conditions ( 46 ). Lidar, like radar, does not provide color information of the surrounding environment. Cameras use light from the surrounding environment to create high-resolution images. In AVs they are used to detect road signs, traffic lights, road lane markings, and barriers ( 46 ). However, the quality of camera images declines in adverse weather conditions and at night. Further, camera images may have an optical distortion that could result in an incorrect identification or location of an object. Analyzing camera images also requires a lot of computational power. Vargas et al. compared lidar, radar, and cameras across several categories including range, resolution, lighting conditions, weather conditions, detection speed and distance, size, and interference susceptibility ( 47 ). Each sensor has its strengths and weaknesses, which are summarized in Table 3 ( 47 ). By combining the data from all of the sensors some of the areas of weakness can be mitigated.

Sensor Performance

Source: Adapted from Vargas et al. ( 47 )

Sensors can be categorized as passive or active based on whether the sensor has their own source of light or illumination. Cameras are passive sensors that receive energy emitted from the environment to generate an output. Lidar and radar are active sensors that generate energy and then receive the reaction of that energy from the environment to generate an output. Given the different functionality of the sensors, their arrangement on vehicles is an important consideration. Where the sensors are placed will affect the type of information received and ultimately the accuracy of their perception of the surrounding environment ( 46 ). The placement of sensors on a Class 8 semitruck will be different than on a passenger car, and the perceived environment from the sensor will also be different. Class 8 semitrucks are heavy-duty trucks that have a weight limit greater than 33,000 lb. The size of semitrucks allows for greater visibility of the roadway, though it also presents challenges for turns, stopping distance, and maneuvering in traffic. Another data input for AVs is their location, which is obtained from a combination of sensors including GPS and inertial navigation sensing. AVs can also use the perception sensors to help locate where it is if a GPS signal is not available. Making the vehicle as independent as possible from outside data input makes it more akin to human driving, in which we rely on our eyes to make the best driving decisions.

Machine learning algorithms process and make sense of the data obtained from the passive and active sensors. Machine learning is a subset of artificial intelligence (AI). AI is the ability of machines or systems to mimic human behaviors, and machine learning refers to the algorithms used to train the machines or systems to learn from past experience ( 48 ). Machine learning is a type of software development in which the system is trained using data and algorithms so that it learns how to operate or perform a specific task without being explicitly programmed ( 49 ). This makes the system dynamic, so it is continually evolving and improving as it encounters new data or scenarios. The multitude of scenarios that the system must be able to handle is also why it is so difficult to train a vehicle to drive. A subset of machine learning is deep learning, which uses neural networks that are inspired from how the human brain processes information. Deep learning has improved object detection, and has exceeded human performance for image classification ( 50 ). Deep learning algorithms help AVs turn the data from the sensors into actionable information. However, deep learning is not the only type of machine learning algorithm used for AVs. Machine learning algorithms can be classified into five general types: 1) supervised learning, 2) unsupervised learning, 3) semisupervised learning, 4) reinforcement learning, and 5) deep learning ( 48 ). The algorithms that are used depend on the autonomous driving task. For instance, perception, motion planning, pedestrian detection, traffic sign detection, road marking detection, self-localization, automated parking, motion control, vehicle cybersecurity, and fault diagnosis all use different algorithms ( 51 ). Autonomous driving can be described under five main tasks: 1) sensing the environment, 2) perceiving the environment, 3) localizing the vehicle, 4) planning the next action, and 5) implementing the driving decision ( 49 ). Sensors gather information about the environment, and machine learning algorithms facilitate use of these data to understand, plan, and act on the information.

Commercial Application of ATs in the Trucking Industry

Deployment Market

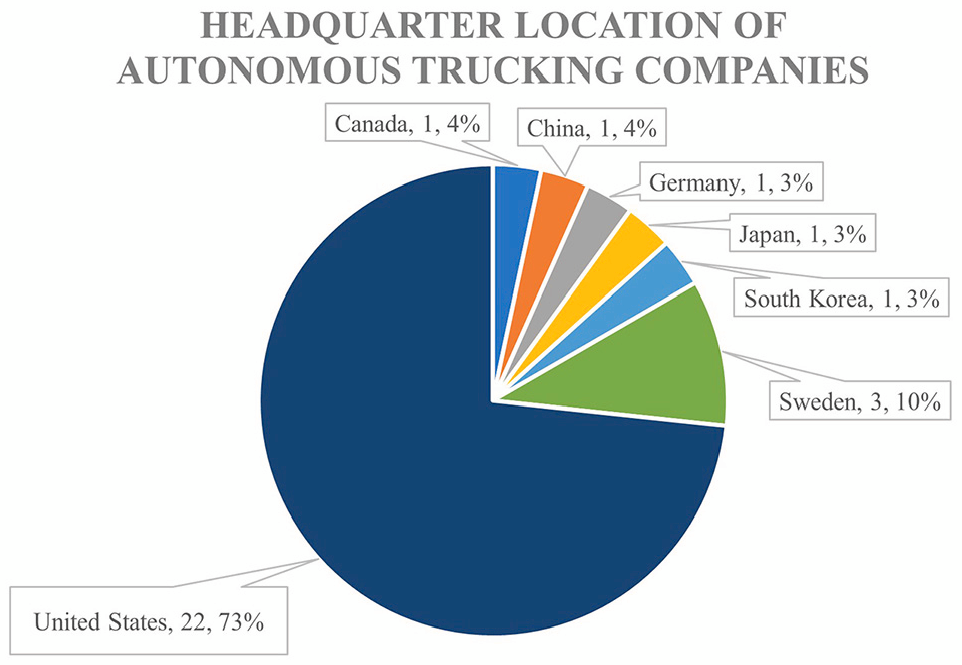

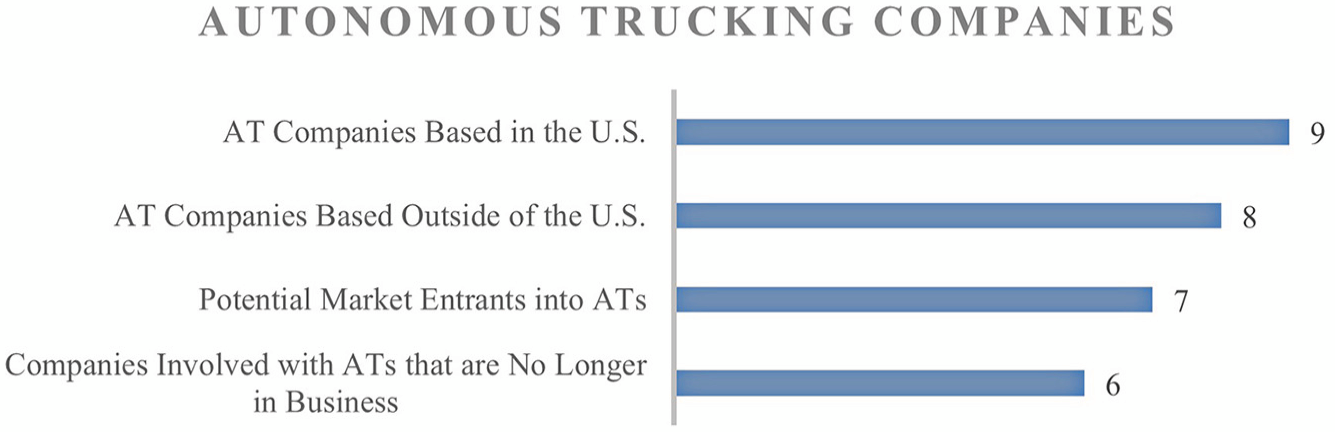

Several companies believe that the hardware sensors and the machine learning algorithms have advanced to the point where AVs could be deployed on public roads. The main deployment markets for AVs currently being pursued by companies are commercial applications in the movement of freight and passengers. Companies pursing the automation of trucks for freight started to take place in the United States around 2015. There are currently more than a dozen companies focused on developing autonomous driving systems for trucking applications. Three AT companies went public in the United States in 2021: Aurora, TuSimple, and Embark ( 52 – 54 ). The race to deploy ATs on public roads is taking place globally with tests being performed in China, Japan, South Korea, Sweden, Germany, Australia, Canada, and the United States. Whereas testing of ATs is taking place globally, there is a high concentration of AT companies with headquarters in the United States. Considering all of the companies that have pursued the AT market, even the companies no longer operating, 73% have headquarters in the United States, as shown in Figure 1. Some of the companies with U.S. headquarters are pursuing markets outside of the United States. Because of the economic and national advantages of improving logistics operations, several countries are moving to safely deploy ATs. Although in the future AT companies will most likely operate on a global scale, initial deployments may be more nationally focused because of security concerns, regulatory uncertainty, and market size. To better understand the possible deployment markets for ATs, the companies currently involved in development are categorized based on the location of their headquarters. Additional deployment markets are also covered by reviewing potential AT market entrants and AT companies that are no longer in business. As Figure 2 shows, nine companies are based in the United States, eight companies are outside, seven companies may enter the AT market, and six companies have gone out of business.

Location of autonomous truck headquarters (includes potential market entrants and companies no longer operating).

Deployment market of autonomous truck companies.

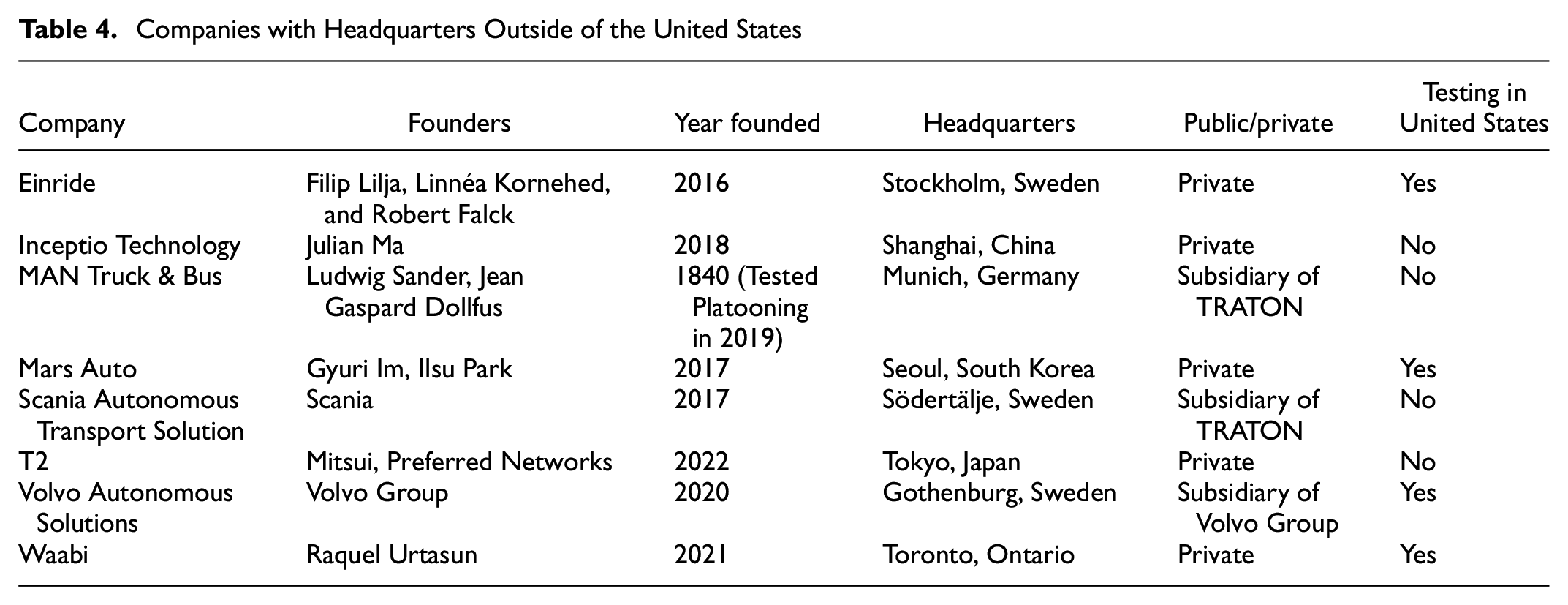

AT Companies Based Outside of the United States

Companies headquartered outside of the United States are listed in Table 4 and include Einride, Inceptio Technology, Scania Autonomous Solutions, Volvo Autonomous Solutions, Waabi, MAN Truck & Bus, Mars Auto, and T2. Four of the companies are in Europe and the rest are based in China, Japan, South Korea, and Canada. Three of the companies are large truck manufacturers large-truck and five are new entrants into the trucking industry. All of the companies recently became involved in ATs, with Einride being the earliest, entering the market in 2016. MAN Truck & Bus, a well-established large vehicle manufacturer, tested platooning in 2019 in Germany ( 55 ). Three of the companies are based in Sweden, and two of them, Einride and Volvo, are planning to utilize ATs in the United States. Einride has performed AT tests in the United States with GE Appliances and Volvo has been working with several logistics companies testing ATs in Texas ( 56 , 57 ). Scania Autonomous Solutions, another AT company based in Sweden, is primarily focusing on the European market. However, Scania did perform a truck platoon test in Singapore on public roads, hauling containers between ports ( 58 ). Scania and Navistar are both subsidiaries of TRATON and TuSimple had a partnership formed with both companies ( 59 , 60 ). The partnership Navistar had with TuSimple has ended, but TRATON is partnering with Plus to commercialize Level 4 ATs in the United States and Europe ( 61 ). With this partnership Plus will work with Navistar, Scania, and MAN Truck & Bus. MAN Truck & Bus is another subsidiary of TRATON that is working on Level 4 ATs in Europe. MAN Truck & Bus is focused on deploying ATs initially in Germany and then expanding operations to the rest of Europe. Companies in the Asia-Pacific region include Mars Auto, T2, and Inceptio Technology. Inceptio Technology is based in China and is focusing solely on the Chinese market. Other AT companies with China ties based in the United States include Plus, Pony.ai, and TuSimple. Mars Auto is currently focusing on the South Korean market, though it is planning to expand to the United States ( 62 , 63 ). T2 was created from investments from logistics company Mitsui and technology company Preferred Networks among other investors ( 64 ). They are focusing on deploying Level 4 ATs in Japan. Waabi is based in Canada but is also focusing on deploying ATs in the United States.

Companies with Headquarters Outside of the United States

AT Companies Based in the United States

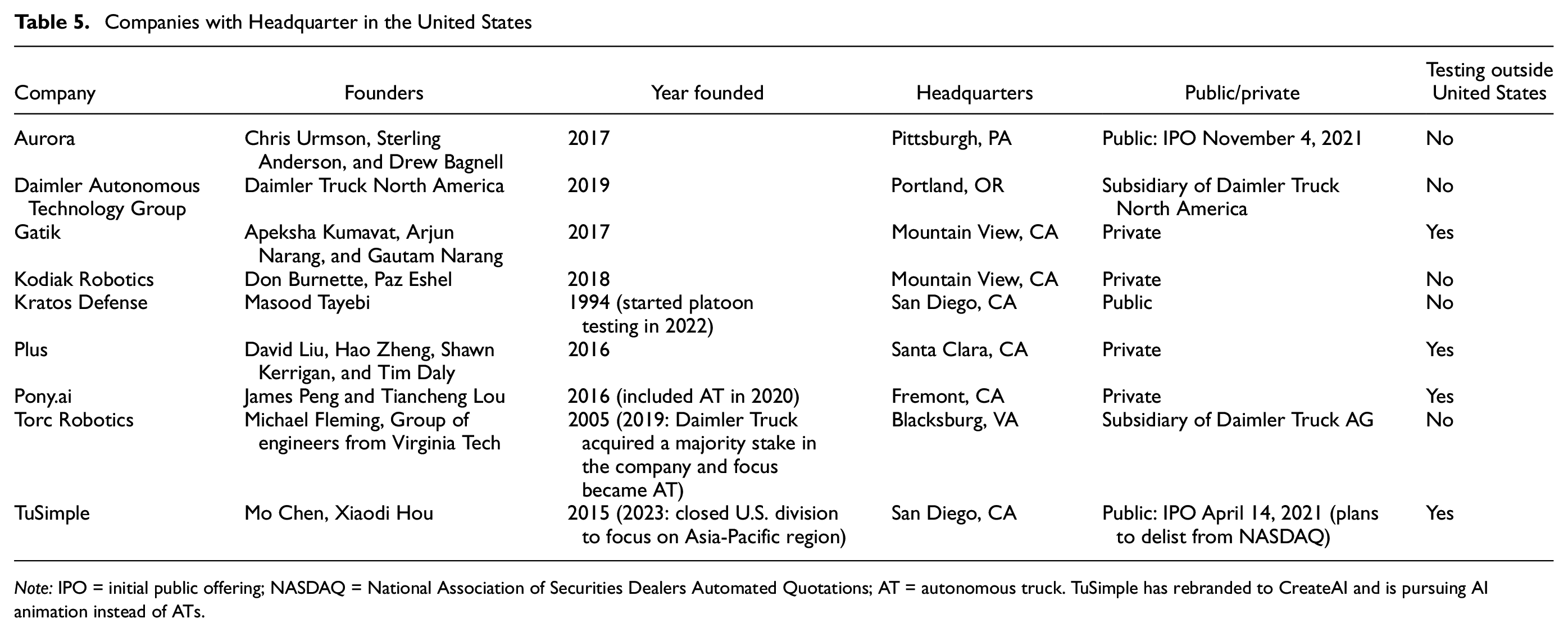

Companies that are headquartered in the United States are mainly focused on deploying ATs there, though some are also focusing on international markets. Table 5 lists all AT companies with headquarters in the United States. Like the internationally based AT companies, the U.S.-based companies became involved with ATs relatively recently, with TuSimple being the earliest in 2015. Kratos Defense is one of the most recent companies to become involved. Kratos began testing platoons in North Dakota in 2022 ( 65 ). The companies that are also focusing on international markets are Plus, Pony.ai, and TuSimple. Plus is working on deploying its technology in the United States, Europe, and China. Plus split their business into two companies in 2023, so the China operation is now a separate company ( 66 ). Pony.ai is working on deploying robotaxis in the United States, though it has recently performed AT tests in China. Pony.ai began forming logistics partnerships in 2022 to deploy ATs in China and has not formed any U.S.-based logistics partnerships ( 67 , 68 ). TuSimple was initially focused on the U.S. market and performed many over-the-road tests in the Southwestern United States with logistics companies. TuSimple has shifted to the Asian Pacific market, closed its U.S. operations, and delisted its stock from NASDAQ ( 69 , 70 ). TuSimple started testing ATs in Japan in 2023 with a local Japanese OEM ( 71 ). Japan revised its Road Traffic Act in April of 2023 so that Level 4 ATs can now operate under certain conditions ( 72 ).

Companies with Headquarter in the United States

Note: IPO = initial public offering; NASDAQ = National Association of Securities Dealers Automated Quotations; AT = autonomous truck. TuSimple has rebranded to CreateAI and is pursuing AI animation instead of ATs.

Companies headquartered in the United States that are mainly focused on deploying ATs there are Aurora, Gatik, Kodiak Robotics, Kratos Defense, and Torc Robotics. Aurora has been performing over-the-road AT tests in the Southwestern United States. The company plans to expand to other commercial deployments like delivery of local goods and robotaxis. Aurora also plans to expand to other markets outside of the United States, though its initial focus is on ATs in the United States. Gatik is working on automating box truck deliveries in the United States and Canada and has been performing autonomous runs with no drivers in the vehicles. Kodiak Robotics has also been performing tests in the Southwestern United States. Kodiak did form a partnership to test ATs in South Korea to expand into the Asian market, though currently, it appears its main focus remains the United States. Torc Robotics is another company undertaking tests in the Southwestern United States. Daimler, which is based in Germany, acquired a majority stake in Torc Robotics in 2019. Freightliner, which is owned by Daimler, is based in Portland, OR ( 73 ). Kratos has traditionally focused on military applications of AVs, though it has entered the commercial market with its platoons and autonomous truck-mounted attenuators in work zones.

Potential Entrants into the AT Market

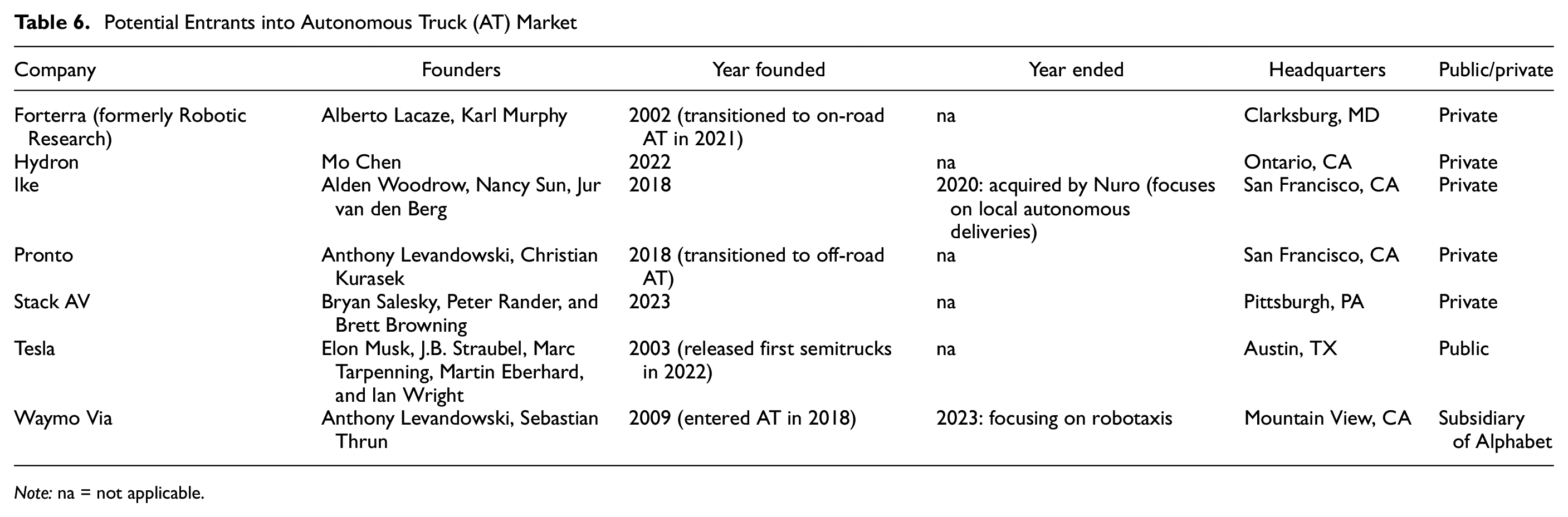

Potential entrants into the AT market are presented in Table 6 and include Ike, Pronto, Forterra (Robotic Research), Stack AV, Tesla, and Waymo Via, and Hydron. Ike was initially focused on ATs before being acquired by Nuro ( 74 ). Nuro is mainly focused on local deliveries though its autonomous driving system has been used on semitrucks ( 75 ). Pronto is now focused on off-road applications of ATs, though they were initially focused on on-road applications. It made the switch from on-road Class 8 truck automation to autonomous haulage units in closed sites in 2020 ( 76 ). Pronto is working with the Virginian Tech Transportation Institute on a project to showcase the deployment of ATs ( 77 ). Forterra has focused on off-road applications for AVs including military applications, though it began moving into commercial applications in 2021 ( 78 ). Stack AV is focused on using automation with Class 8 semitrucks, though its exact focus is not yet clear. Founders Bryan Salesky and Peter Rander previously started an AV company that Ford purchased and shut down in 2022 ( 79 ). Tesla is working on creating autonomous electric vehicles and recently released an electric semitruck to PepsiCo in 2022 ( 80 ). The semitrucks may be able to use Tesla’s autonomous driving system in the future. Waymo Via was the AT division of Waymo until it was closed in 2023 so the company could focus on robotaxis ( 81 ). Waymo created a partnership with Daimler, which it plans to keep in place. Waymo could shift back into ATs in the future. Hydron is planning to build autonomous-ready semitrucks. The founder, Mo Chen, cofounded TuSimple, and TuSimple is now focused on the Asian market.

Potential Entrants into Autonomous Truck (AT) Market

Note: na = not applicable.

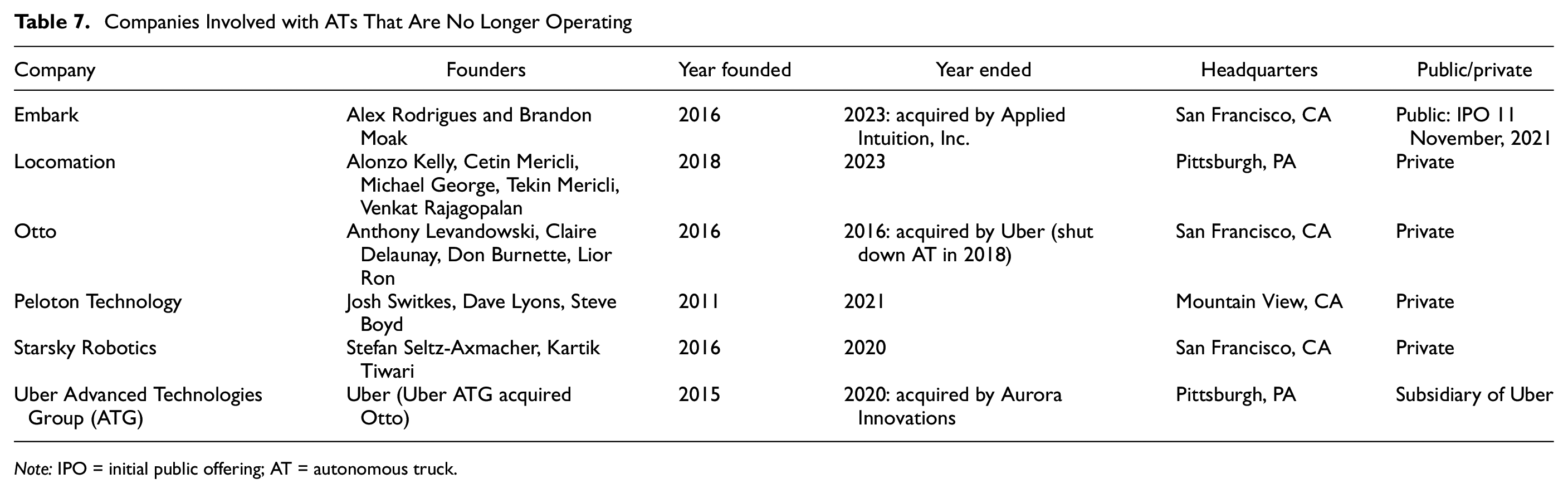

Companies Involved with ATs that are No Longer in Business

Companies that were involved with ATs but are no longer in business are presented in Table 7 and include Embark, Locomation, Otto (Uber Advanced Technologies Group), Starsky Robotics, and Peloton Technology. Most of these closures have taken place recently with five of the six companies closing since 2020. All of these companies were focused on deploying ATs in the United States. Embark, founded in 2016, was performing on-road tests of ATs in the Southwestern United States. It ceased operations in 2023 and was acquired by Applied Intuition, a software company that is helping companies to deploy AVs ( 82 ). Locomation, founded in 2018, was planning on deploying ATs using a two-truck convoy. It also closed in 2023 ( 83 ). Otto, founded in 2016, was focused on ATs and then was acquired by Uber ( 84 ). Uber kept the AT division open for a while and then decided to close it ( 85 ). Otto is well known for the autonomous test run it performed in Colorado, hauling Budweiser beer between Fort Collins and Colorado Springs in 2016 ( 86 ). Uber Advanced Technologies Group was later acquired by Aurora, which is now focused on ATs ( 87 ). Starsky Robotics, founded in 2016, was focused on ATs that would be monitored by a remote operator. It performed a fully driverless test in Florida in 2019 and closed in 2020 ( 88 ). Peloton was founded in 2011 and was focused on truck platooning. Peloton was testing its technology with customers and was planning on moving to Level 4 autonomous trucking where the driver could be removed from the following truck ( 89 ). Peloton ceased operations in 2021 ( 90 ).

Companies Involved with ATs That Are No Longer Operating

Note: IPO = initial public offering; AT = autonomous truck.

Business Cases Being Pursued by AT Companies

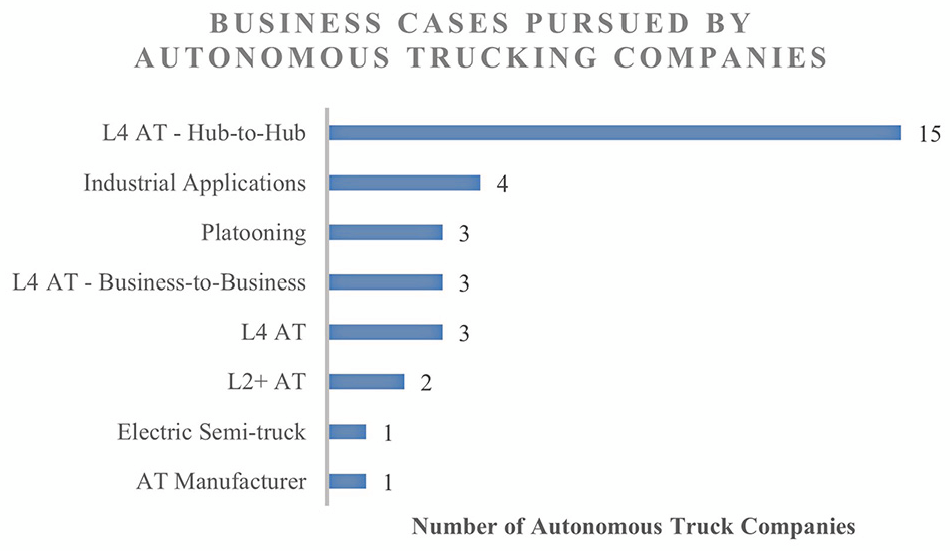

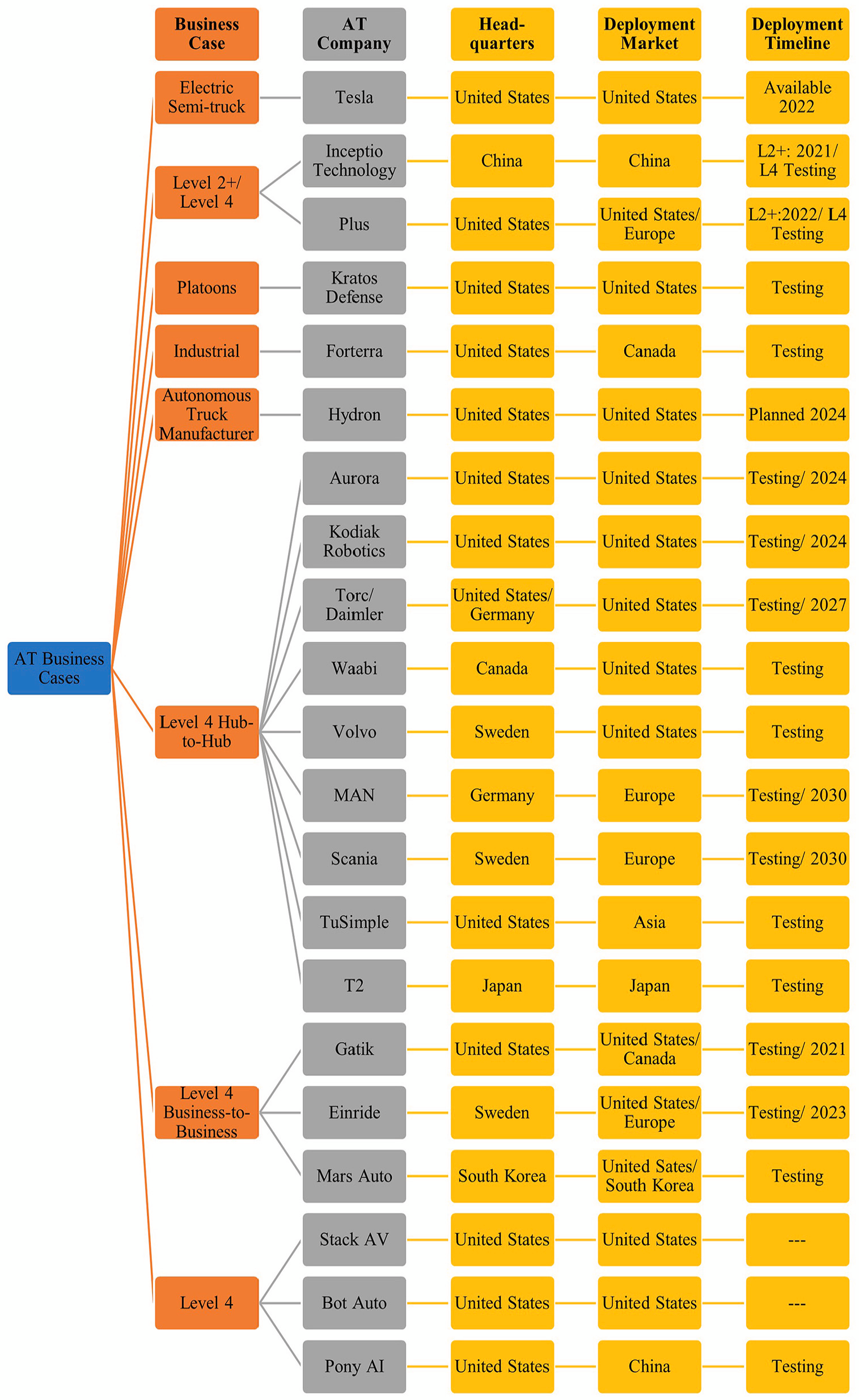

Whereas most AT companies started to emerge in 2015, the use of AVs in commercial applications has been common since the 2000s in closed environment like mines, ports, and distribution centers where tasks are controllable and very repetitive. Rio Tinto began using ATs in mines in Australia in 2008 ( 91 ). It reported in 2018 that ATs operated about 700 h more than conventional trucks, cut costs by about 15%, and no AT-related injuries had occurred ( 91 ). Utilization and cost savings along with improved safety make ATs a compelling investment for companies. Because of the many benefits ATs offer, U.S. logistics companies have started partnering with AT companies to test possible use cases. The move from closed environments such as mines to public infrastructure that is shared with noncommercial traffic represents a significant shift that will open several new business opportunities for companies. The business cases being pursued by AT companies are shown in Figure 3. A few things should be noted about Figure 3. Some companies are pursuing multiple business cases, so AT companies are included in multiple business cases. Figure 3 includes just the companies involved with ATs. There are many companies pursuing industrial applications in closed environments that are not included, since they are not pursuing ATs. Some companies in the figure are listed as Level 4 AT, because it is not clear what particular application they are going to pursue. Only one AT manufacturer is shown in Figure 3, though most major manufacturers are involved with ATs through partnerships or investing in AT companies. The one manufacturer included is a new company that is planning to manufacture ATs. Figure 3 also includes AT companies that are no longer in business, and potential market entrants. The predominant business case, as shown in Figure 3, is a hub-to-hub application of ATs.

AT business cases being pursued (Includes potential market entrants and companies no longer operating).

Hub-to-Hub Model

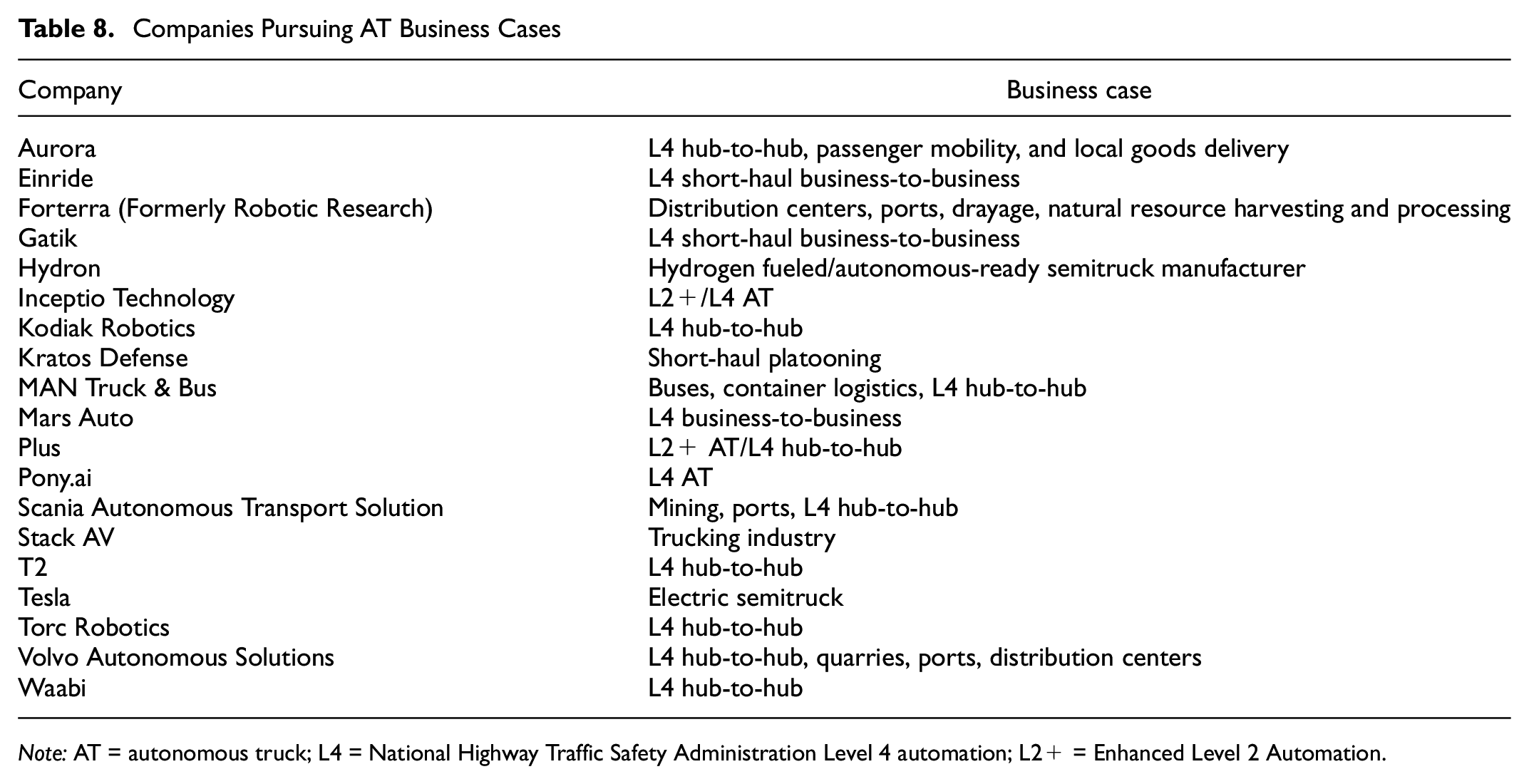

Table 8 presents the current business cases being pursued for ATs. One of the predominant business cases being pursued is Level 4 ATs that will operate in a hub-to-hub model. Aurora, Kodiak, MAN Truck & Bus, Scania, Torc Robotics, Volvo, Waabi, and T2 are planning to initially deploy ATs using this method. A hub-to-hub model is set up so that terminals are located outside of major cities. The AT would then operate between the hubs over interstate highways leaving the last mile for manually driven trucks. There are several reasons why this is the predominant approach to initially deploy ATs. This strategy may be easier to automate than deployments in urban areas because of a less complex operating environment. This will result in fewer stops, which will increase the utilization of the truck and help decrease the payback period of the initial investment. It will enable drivers to stay closer to home, which may improve driver morale and retention, and reduce lodging expenses. Another challenge and possible benefit of automating highway driving is reducing the number of high-speed collisions. Higher driving speeds on highways increase the risk of deploying ATs, although the potential benefits are increased if this can be achieved safely. The goal would be for trucks to operate at Level 5, meaning they could operate from dock to dock under any traffic conditions. This level of deployment may be several years into the future; for now, companies are focusing on finding repetitive operating conditions that have a compelling business case and can utilize Level 4 ATs in a hub-to-hub model.

Companies Pursuing AT Business Cases

Note: AT = autonomous truck; L4 = National Highway Traffic Safety Administration Level 4 automation; L2+ = Enhanced Level 2 Automation.

Level 4 Versus Level 2+ Automation

Level 4 is being pursued by most companies because a driver does not need to be in the vehicle, which removes the complication of driver handoffs necessary in Level 3 automation. In 2012, Waymo explored the possibility of using Level 3 automation; they found that drivers overrelied on the technology and the transition from passenger to driver in complex situations was challenging ( 92 ). The handoff problem, combined with the cost savings of removing the driver makes Level 4 more compelling for logistics companies. Even though Level 4 is the goal for most AT companies, some are pursuing Level 2+ ATs because the technology is commercially available. Plus and Inceptio Technology are companies that decided to take this approach. Plus is retrofitting semitrucks with Level 2+ technology that includes advanced lane centering, merge handling, collision avoidance, blind-spot detection, an integrated event data recorder, driver attentiveness system, and predictive fuel optimization ( 93 ). Its plan is to commercialize this technology while developing and testing a Level 4 system. For its Level 4 system, Plus is planning to use a hub-to-hub model. Inceptio Technology is following a similar approach to Plus where it is currently deploying Level 2+ trucks to customers in China ( 94 ). It plans to deploy Level 4 ATs in the future. Platooning is another automation strategy. The approach involves tethering two trucks together using wireless communications so they can travel close to each other. Platooning may use driver assistance features, although the system does not have to be autonomous. Kratos Defense and Security Solutions has partnered with Minn-Dak Farmers Cooperative to test truck platoons to haul sugar beets in North Dakota and Minnesota ( 65 ). Kratos is also testing platoons in Northern Minnesota to haul biodiesel between refining plants. It also has plans to test platoons in Ohio and Indiana for a 3PL company ( 95 ).

Short-Haul Business-to-Business Market

Another segment of the trucking market that is being pursued is the short-haul, middle-mile market. This consists of routes between manufacturing facilities and warehouses or warehouses and retail stores. Gatik, Einride, and Mars Auto are pursuing this market, which offers the possibility of earlier deployment times because of shorter routes and the use of smaller trucks. Gatik uses Classes 3 to 7 box trucks that have a gross vehicle weight rating (GVWR) of 10,000 to 33,000 lb, compared with Class 8 trucks with a GVWR exceeding 33,000 lb ( 96 ). Because of the lower weight and slower speed, the severity of crashes is reduced. Owing to the lower barriers to entry of this market, Gatik has started to deploy autonomous box trucks with no driver. There is also the possibility that automated box trucks may move some of the freight that is typically hauled with Class 8 semitrucks. This is being seen in a partnership between Gatik and Georgia-Pacific where the companies are testing automated box trucks to make deliveries to Sam’s Club locations instead of using Class 8 semitrucks ( 97 ). The move toward using automated smaller vehicles that make more deliveries instead of manually driven larger vehicles is also being tested in the mining industry. Volvo Autonomous Solutions is building a smaller autonomous haul truck for mines, which it believes will increase efficiency and allow for electrification ( 98 ). Einride has designed a cabless electric truck that they are planning to deploy in ports and between warehouses. Mars Auto is similarly pursuing AT applications between warehouses, though on longer routes.

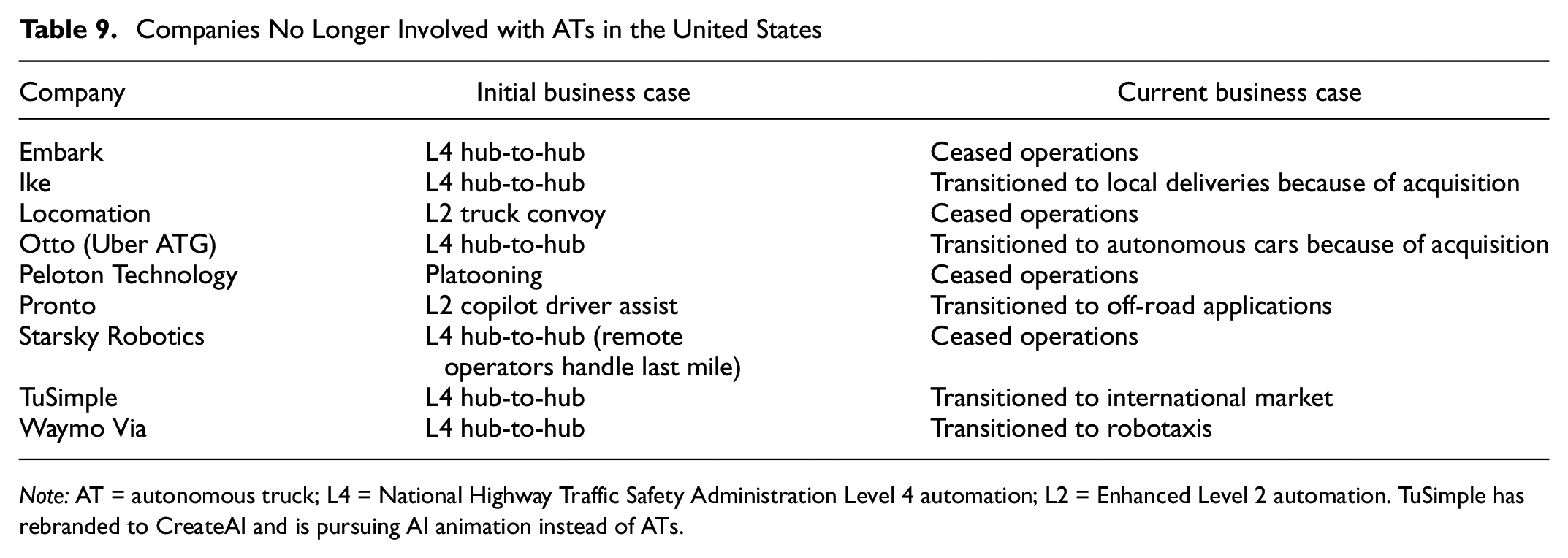

There has been a lot of movement in the AT market with companies entering and exiting. Table 9 lists all companies that were at one point involved with ATs in the United States. Embark, Ike, Otto (Uber ATG), Starsky Robotics, TuSimple, and Waymo Via all planned to deploy Level 4 ATs in a hub-to-hub model in the United States. Embark had several partnerships with logistics companies to test its deployment method, however, the company ran out of funding to stay in business. Waymo Via decided to shift their focus back to robotaxis. Ike was acquired by Nuro and is now focusing on automating local deliveries. Otto was acquired by Uber and eventually shifted from ATs to self-driving cars. Starsky was unable to commercialize their product to stay in business, and TuSimple left the United States to focus on the Asian market. There have also been shifts between off- and on-road applications for ATs. Pronto was initially focused on on-road applications of ATs but is now working on off-road applications in mines. Forterra (Robotic Research) has mainly focused on off-road applications of AVs though it is now entering on-road applications. Kratos is making the same shift from off-road AVs for military vehicles to on-road applications. Other companies that focused on platooning are no longer in business. Peloton Technology and Locomation were planning on deploying platoons of trucks. Locomation had a three-phase approach to get to Level 4 ATs. The first phase was to be a two-truck convoy with a driver in the lead vehicle and a driver sleeping in the second vehicle. The second phase was to remove the driver resting in the second vehicle. The third phase would have been Level 4 automation of a single truck and no driver. Kratos is the only company that is still pursuing platooning as a viable commercial deployment option.

Companies No Longer Involved with ATs in the United States

Note: AT = autonomous truck; L4 = National Highway Traffic Safety Administration Level 4 automation; L2 = Enhanced Level 2 automation. TuSimple has rebranded to CreateAI and is pursuing AI animation instead of ATs.

Commercial Adoption Timelines and Deployments

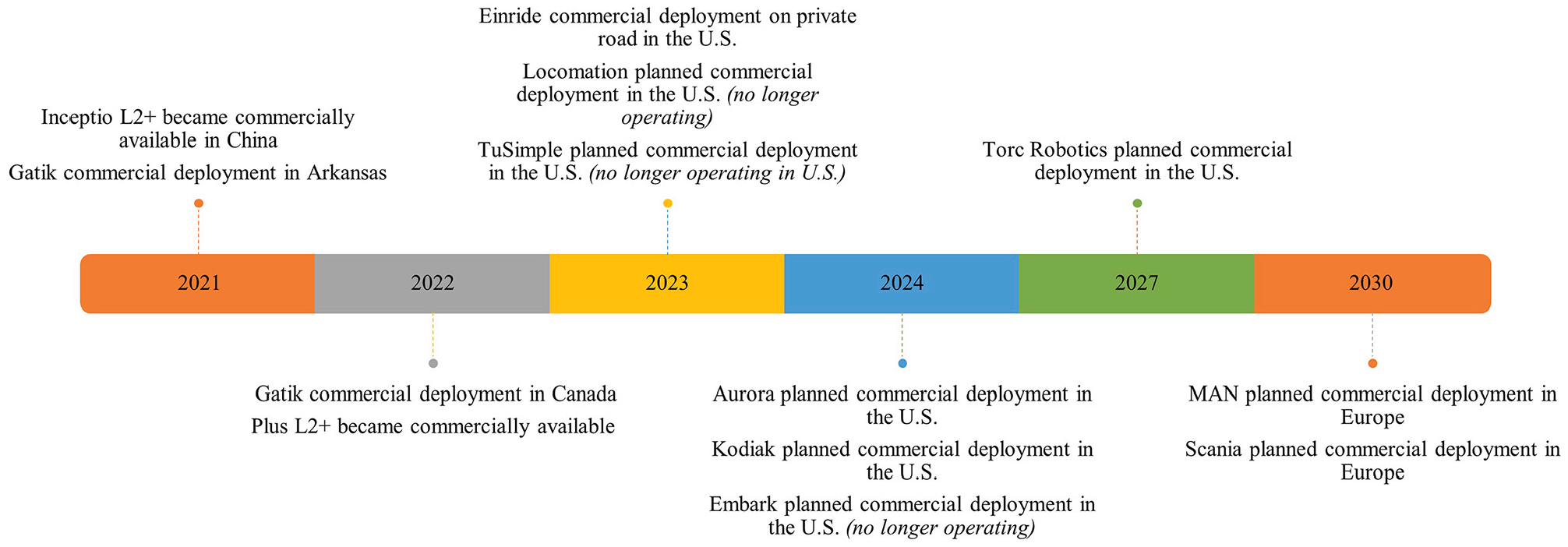

Commercial deployment of Level 4 ATs is planned to take place by the end of the decade, as shown in Figure 4. AT commercial deployments started in 2021 with Gatik making deliveries for Walmart in Arkansas using their autonomous box trucks. In 2021 and 2022, Level 2 autonomous systems became available in the United States and China. In 2023, Einride started making daily deliveries using their cabless AT for GE Appliance on a private road that is open to the public ( 99 ). Aurora, Kodiak, Torc Robotics, MAN, and Scania all plan on deploying Level 4 ATs by 2030.

Timeline of commercial deployment of autonomous trucks.

Companies that are Still Operating

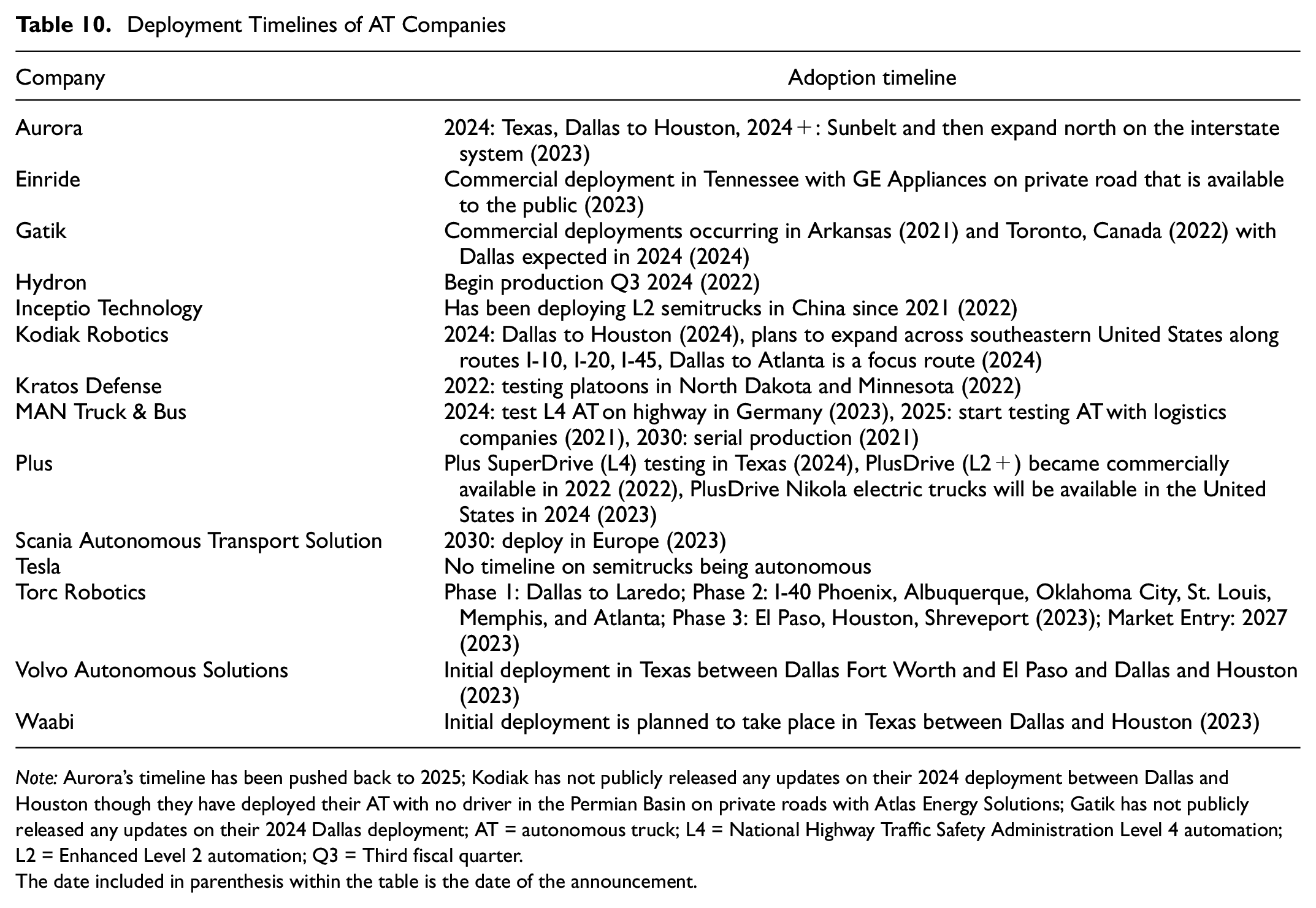

Companies pursuing Level 4 automation are still in the testing phase, though many are planning to deploy Level 4 ATs within the decade. The deployment timeline and locations are listed in Table 10. Aurora, a publicly traded company, planned on deploying ATs between Dallas and Houston, TX, in 2024 though their timeline has been pushed back to 2025 ( 100 ). Kodiak, a private company, has recently announced that it has an autonomous-ready truck that will also be deployed between Dallas and Houston in 2024 ( 101 ). Torc Robotics has announced that its target for deployment of ATs is 2027, initially in Texas between Dallas and Laredo ( 102 ). Volvo has not set a timeline for when it plans to deploy ATs, but has indicated that its first freight corridors will be Dallas–Fort Worth to El Paso and Dallas to Houston, TX ( 57 ). This is similar to Waabi, which plans to offer its AT service first in Texas between Dallas and Houston in partnership with Uber Freight ( 103 ). Although all of these companies are initially targeting Texas as their deployment location, many are planning on expanding throughout the Sunbelt region (i.e., xxx) and then throughout the entire United States. All of these companies are pursuing the hub-to-hub model, so the deployments are planned to take place on major interstate routes. We can see where expansion is planned for ATs with Torc Robotics’ adoption plan. After deploying between Dallas and Laredo, TX, Torc plans to expand along Interstate 40 between Phoenix, Albuquerque, Oklahoma City, St. Louis, Memphis, and Atlanta ( 102 , 104 ). The company then plans to return to Texas and add routes to El Paso, Houston, and Shreveport, LA. The two companies pursuing ATs in Europe, Scania and MAN, are planning to have a Level 4 AT commercially available by 2030 ( 105 , 106 ). Plus and Inceptio Technology have Level 2+ automation that is commercially available for installation in trucks. PlusDrive became commercially available in 2022 and will be installed in Nikola electric trucks in 2024 ( 107 ). Plus SuperDrive, their Level 4 technology, is currently being tested in the United States and Europe ( 61 ). Inceptio Technology has been using its Level 2+ automation in China since 2021 ( 108 ). The other commercially available product is Gatik’s autonomous box truck. Gatik has partnered with companies like Walmart to use Level 4 autonomous box trucks for routes between warehouses and retail stores. It removed the safety driver in Arkansas in 2021 for the Walmart routes and in Toronto, Canada, in 2022 for the Loblaw routes ( 109 , 110 ). In 2024, Gatik is planning to remove the safety driver for routes in Texas ( 111 ).

Deployment Timelines of AT Companies

Note: Aurora’s timeline has been pushed back to 2025; Kodiak has not publicly released any updates on their 2024 deployment between Dallas and Houston though they have deployed their AT with no driver in the Permian Basin on private roads with Atlas Energy Solutions; Gatik has not publicly released any updates on their 2024 Dallas deployment; AT = autonomous truck; L4 = National Highway Traffic Safety Administration Level 4 automation; L2 = Enhanced Level 2 automation; Q3 = Third fiscal quarter.

The date included in parenthesis within the table is the date of the announcement.

Companies that have Ceased Operating

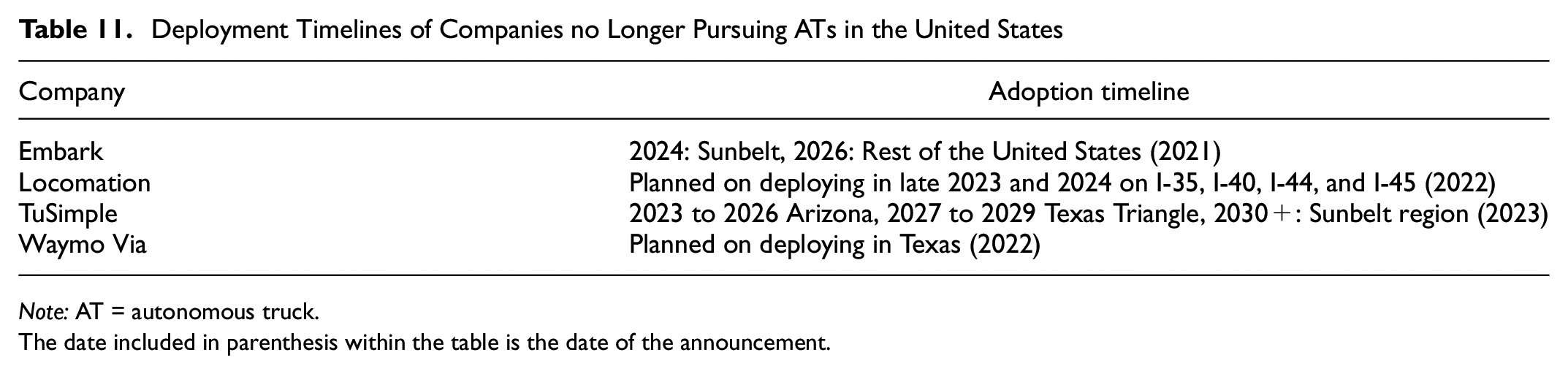

For companies that are no longer pursuing ATs in the United States, we see a similar trend in the deployment timelines and locations in their original plan (see Table 11). Embark was working on building a network of transfer points that ATs would have operated between including, Oakland, Los Angeles, Phoenix, El Paso, Dallas, San Antonio, Houston, Atlanta, and Jacksonville. This would have allowed AT coverage across the Sunbelt region. Its initial timeline was to begin deploying ATs across this network in 2024 and then expand to the rest of the United States ( 112 ). TuSimple had a similar vision. It planned to use ATs in Arizona between 2023 and 2026, the Texas Triangle (the area outlined by the major urban areas of Austin, Dallas–Fort Worth, Houston, and San Antonio) between 2027 and 2029, and the Sunbelt region after 2030 ( 113 ). The company saw this progression beginning slowly with about 10 ATs between 2023 and 2026 and then growing to 100 and then to thousands of trucks between 2027 and 2029, and finally to 10,000 trucks after 2030 ( 113 ). The ATs were to be initially be operated, maintained, and monitored by TuSimple with the goal of the logistics company taking it over in the future.

Deployment Timelines of Companies no Longer Pursuing ATs in the United States

Note: AT = autonomous truck.

The date included in parenthesis within the table is the date of the announcement.

The adoption timeline of ATs will depend on when the technology can operate successfully under all the necessary driving conditions, and when they are proven safe to operate on public roads. Several companies are adopting a safety case to validate that their autonomous driving system is ready to operate on public roads. For example, Aurora’s safety case consists of five main categories: proficient, fail-safe, continuously improving, resilient, and trustworthy ( 114 ). The AT is proficient if it can operate safely during normal operations. It is fail-safe if it can handle faults and failures. It is continuously improving if all potential risks are evaluated and resolved. It is resilient if it can handle unavoidable events, and it is trustworthy if all conditions of the safety case have been met. Kodiak is using simulation and real-world data to validate that its AT system is safer than a human under diverse operating conditions ( 115 ). Many AT companies are performing voluntary safety self-assessments to demonstrate the processes they have in place to safely deploy ATs. Companies send their safety assessments to NHTSA: these are publicly available. Aurora, Ike, Kodiak, Mars Auto, Nuro, Plus, Pony.ai, Stack AV, Torc Robotics, TuSimple, Waabi, and Waymo Via all completed voluntary safety self-assessments ( 116 ). Locomation, Starsky Robotics, and Uber also completed voluntary safety self-assessments, but these are no longer available because the companies ceased operating.

Industry Partnerships

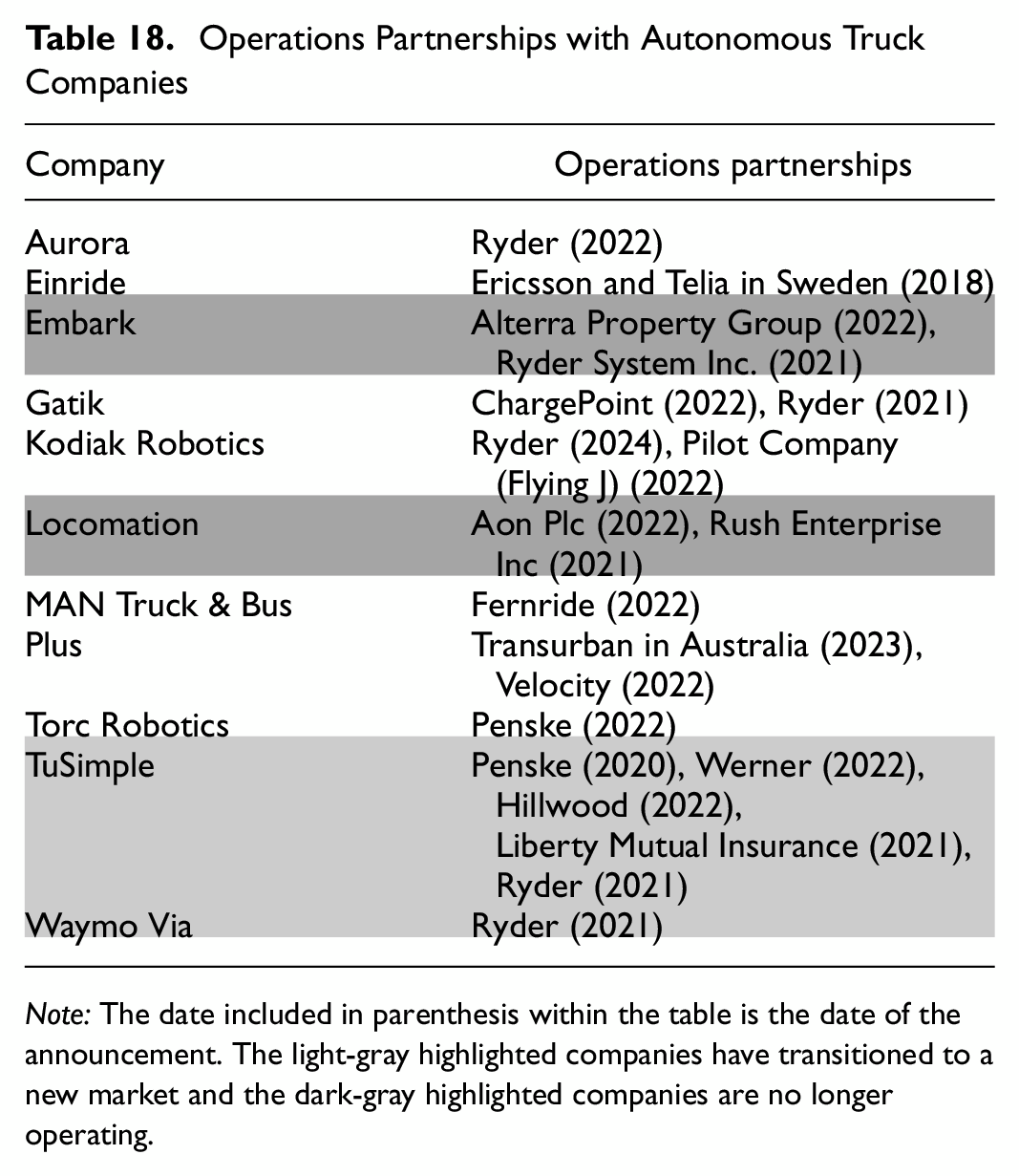

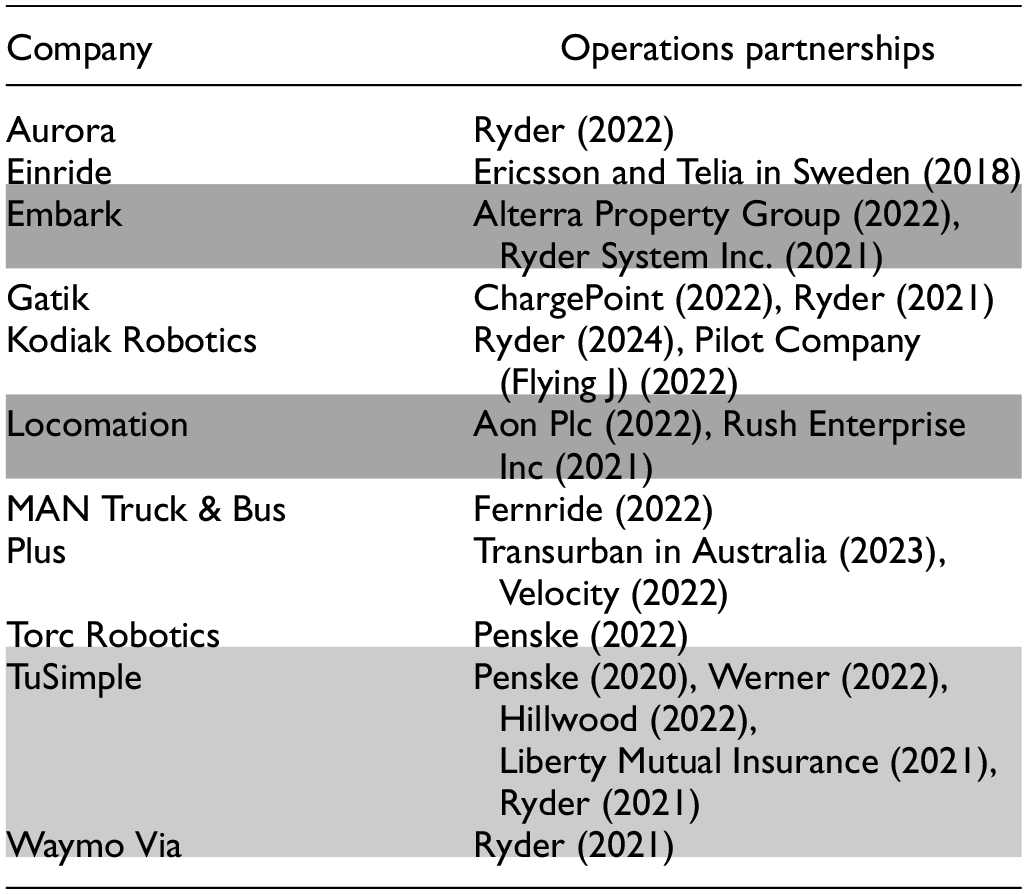

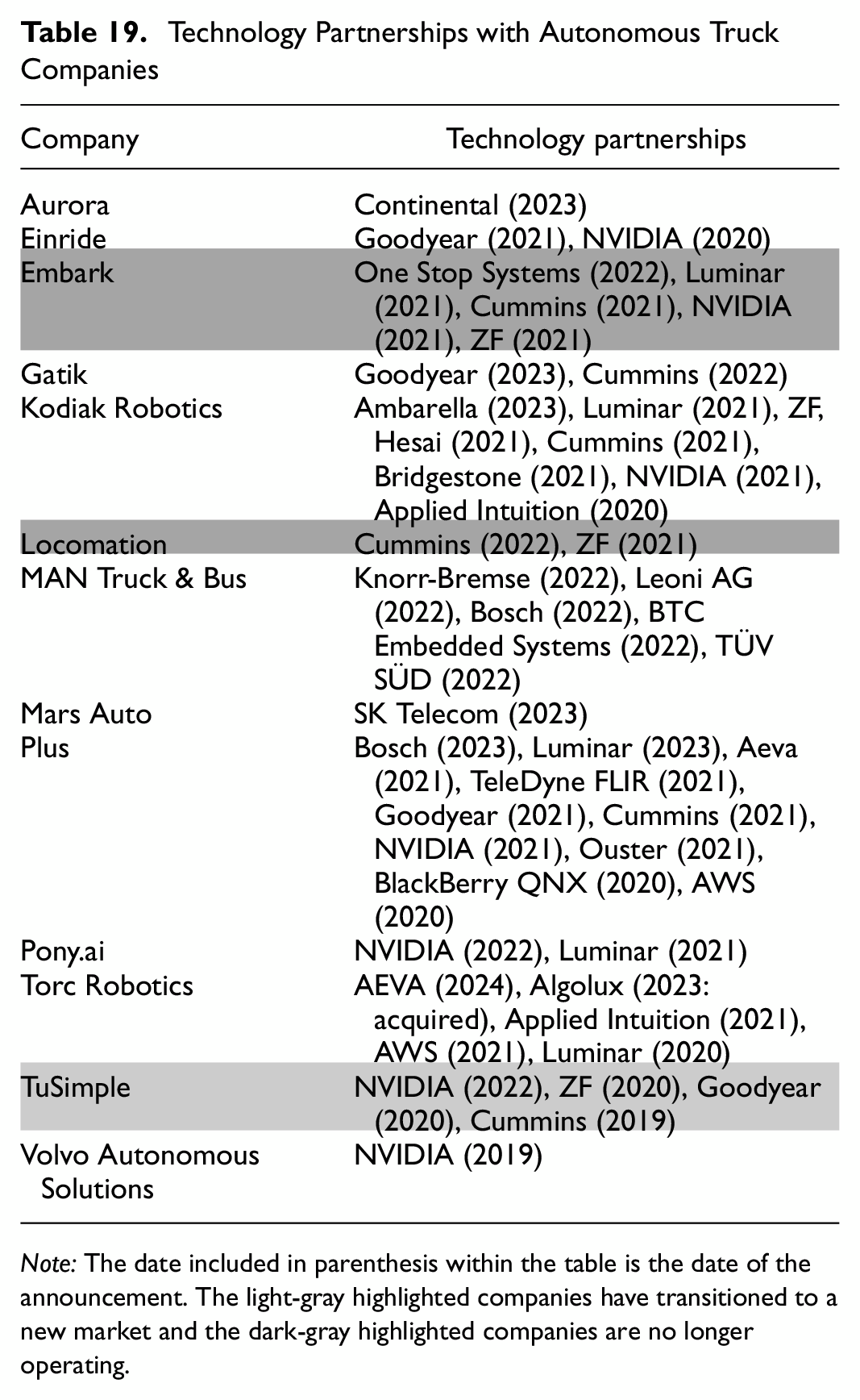

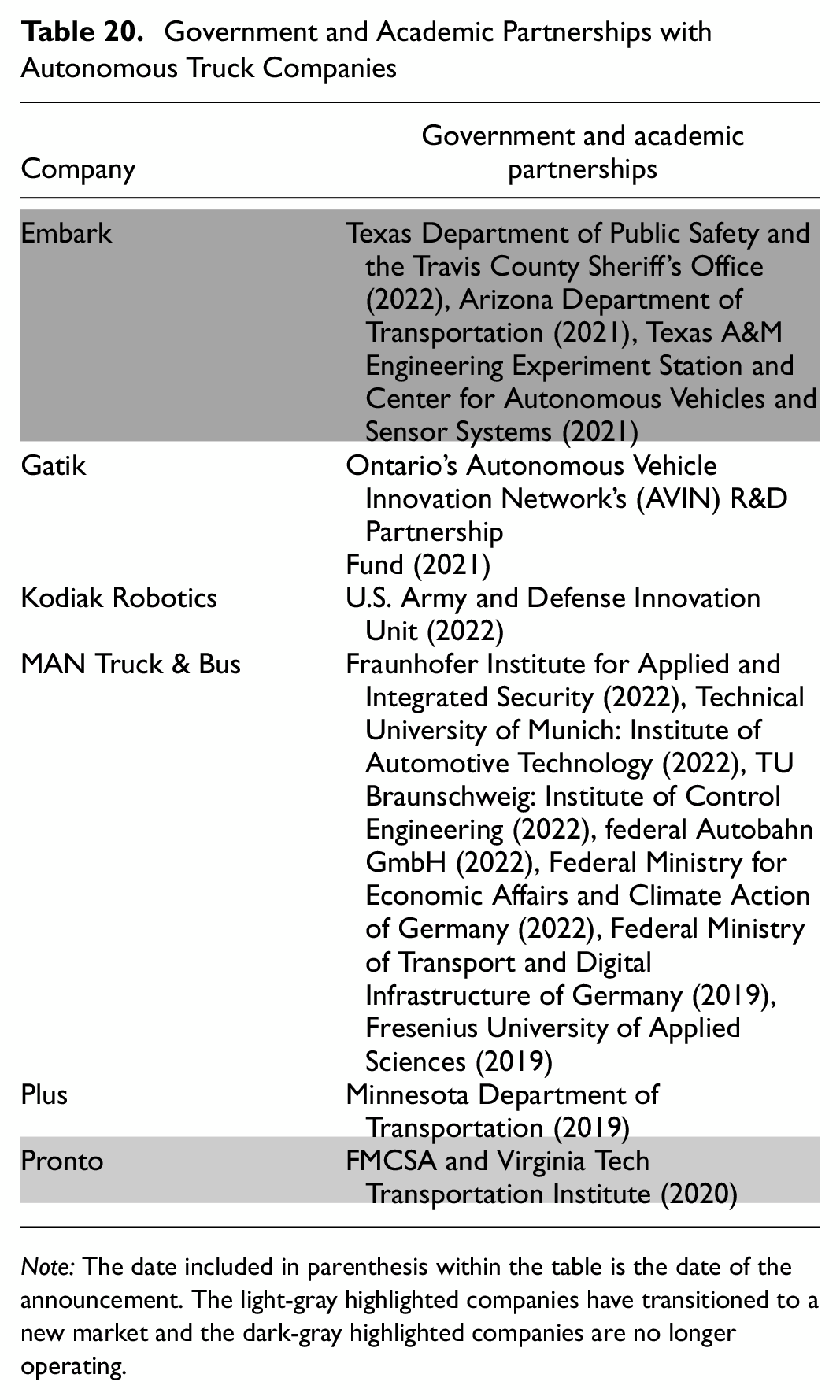

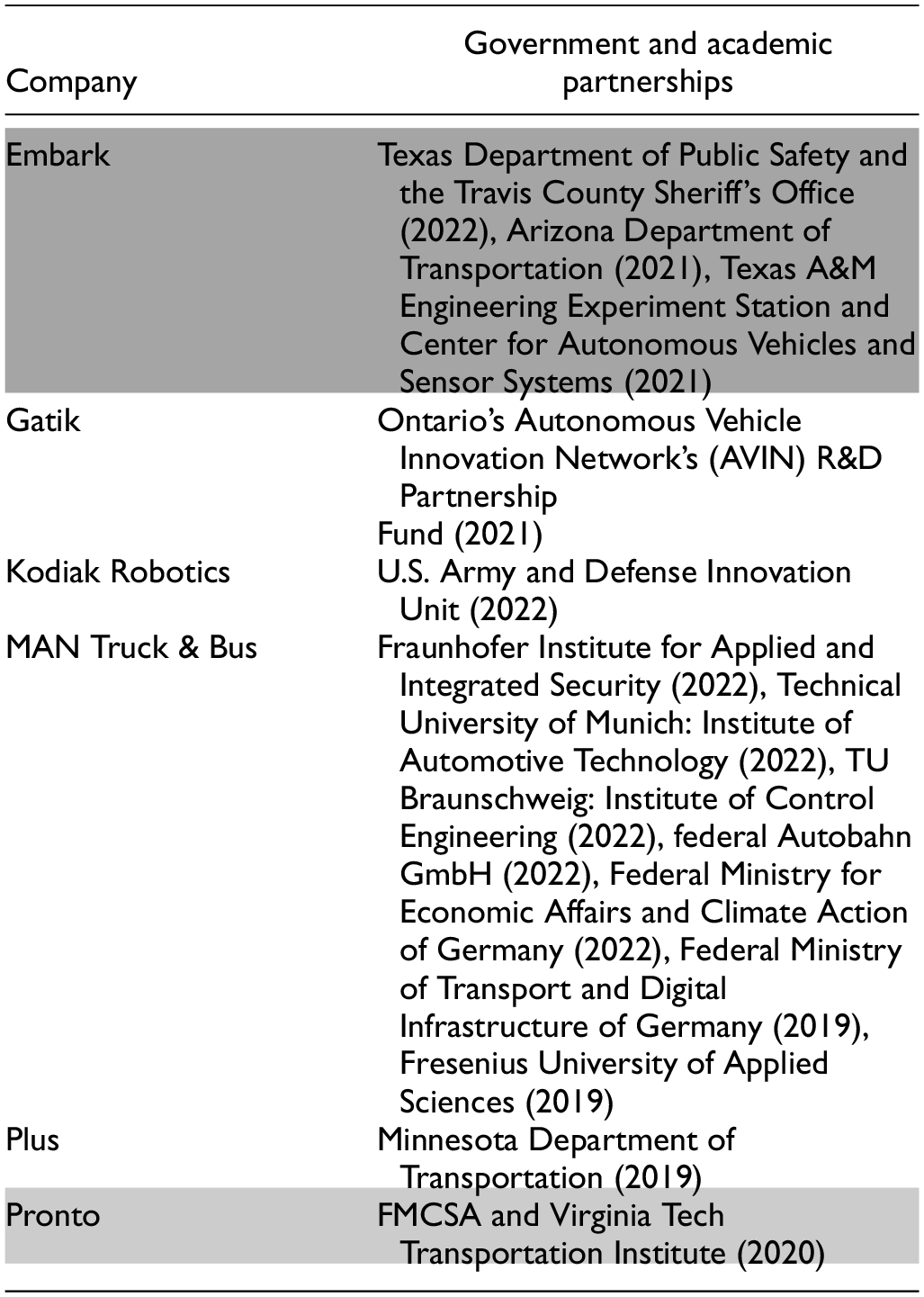

To deploy ATs on public roads, many stakeholders need to be involved. This ecosystem of stakeholders is developing within the United States so that ATs can be deployed at scale. AT companies are partnering with logistics companies, truck manufacturers, and other companies to assist with the operations of AT deployments; with technology companies for equipment; with research and academic institutions to conduct tests; and government agencies to deploy ATs on public roads. The majority of these partnerships were formed in 2020, 2021, and 2022. The logistics partnerships are being formed to see how ATs will work within the operations of a trucking company and to test real-world operating conditions. The manufacturing partnerships facilitate integration of the autonomous driving system into the systems of established truck manufacturers. In the United States, AT companies are not planning on manufacturing their own trucks. Truck manufacturers have well-established relationships with trucking companies which will bridge the gap for newer AT companies. Operations partnerships include all of the extra details needed to deploy ATs at scale: companies to help with maintenance, AT hub facility allocation, insurance, charging facilities, manufacturing for the mass production of sensors, telecommunication providers for 5G service, and companies building smart infrastructure. Technology partnerships assist with the equipment, data, and testing of ATs. Such partnerships include sensor companies, Tier 1 suppliers of auto parts, cloud service providers, and simulation providers. Government and academic partnerships are needed to safely deploy ATs on public roads and include state Departments of Transportation (DOTs) and highway patrol offices, universities, and research agencies. Many other partnerships will form as the industry evolves and matures.

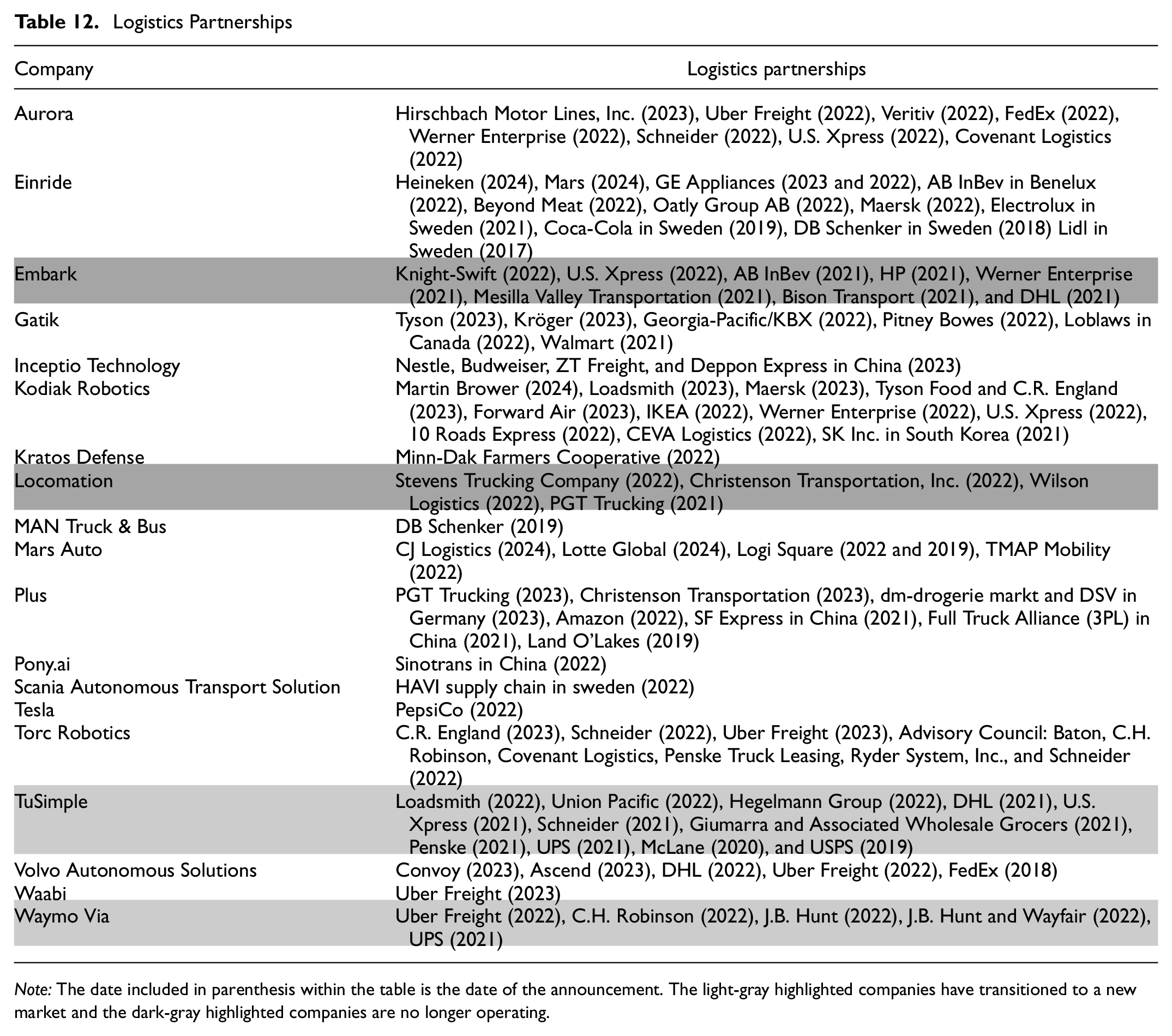

Logistics Partnerships

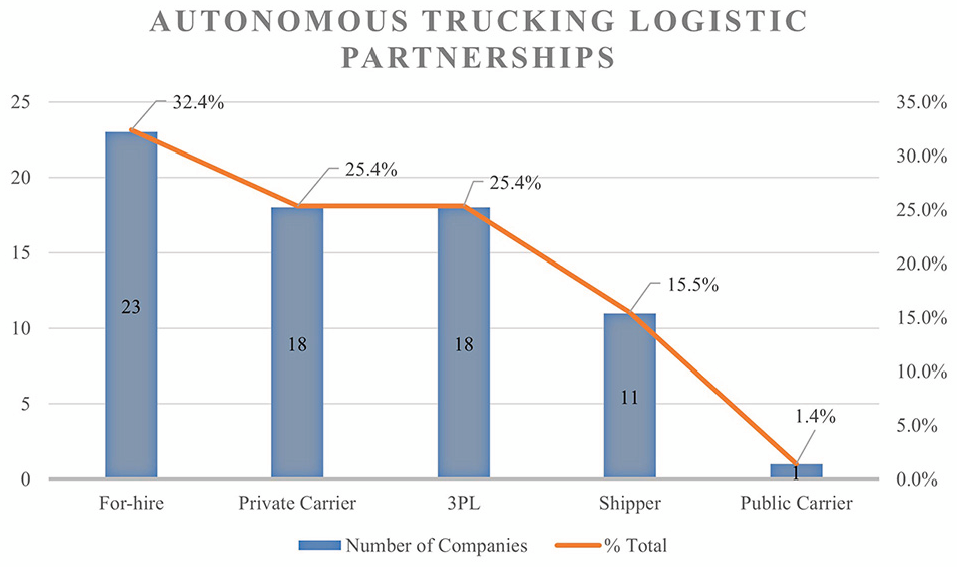

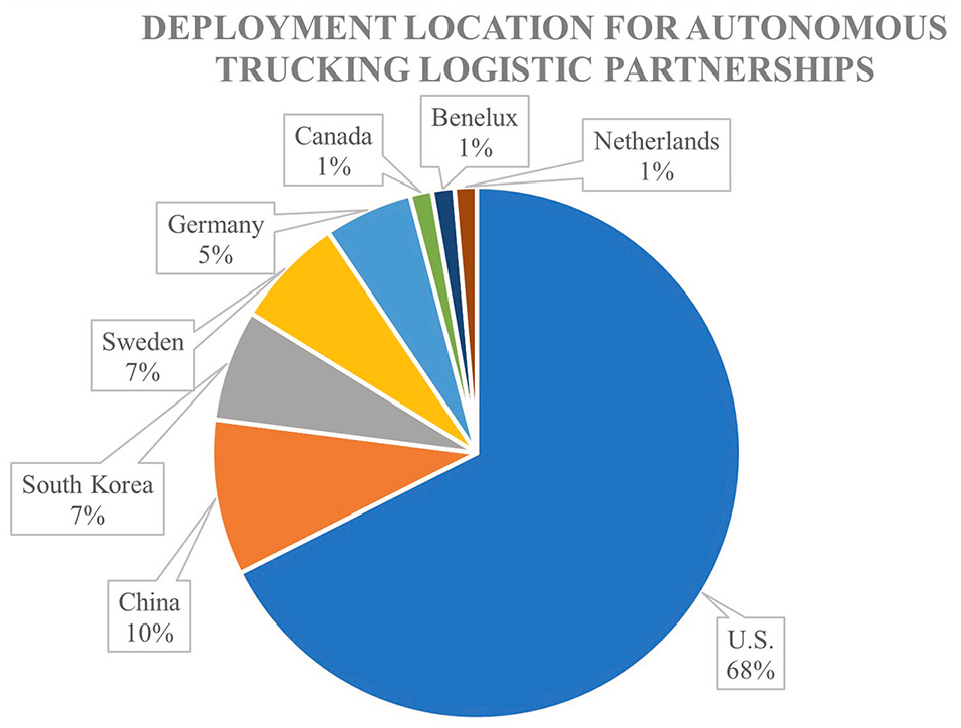

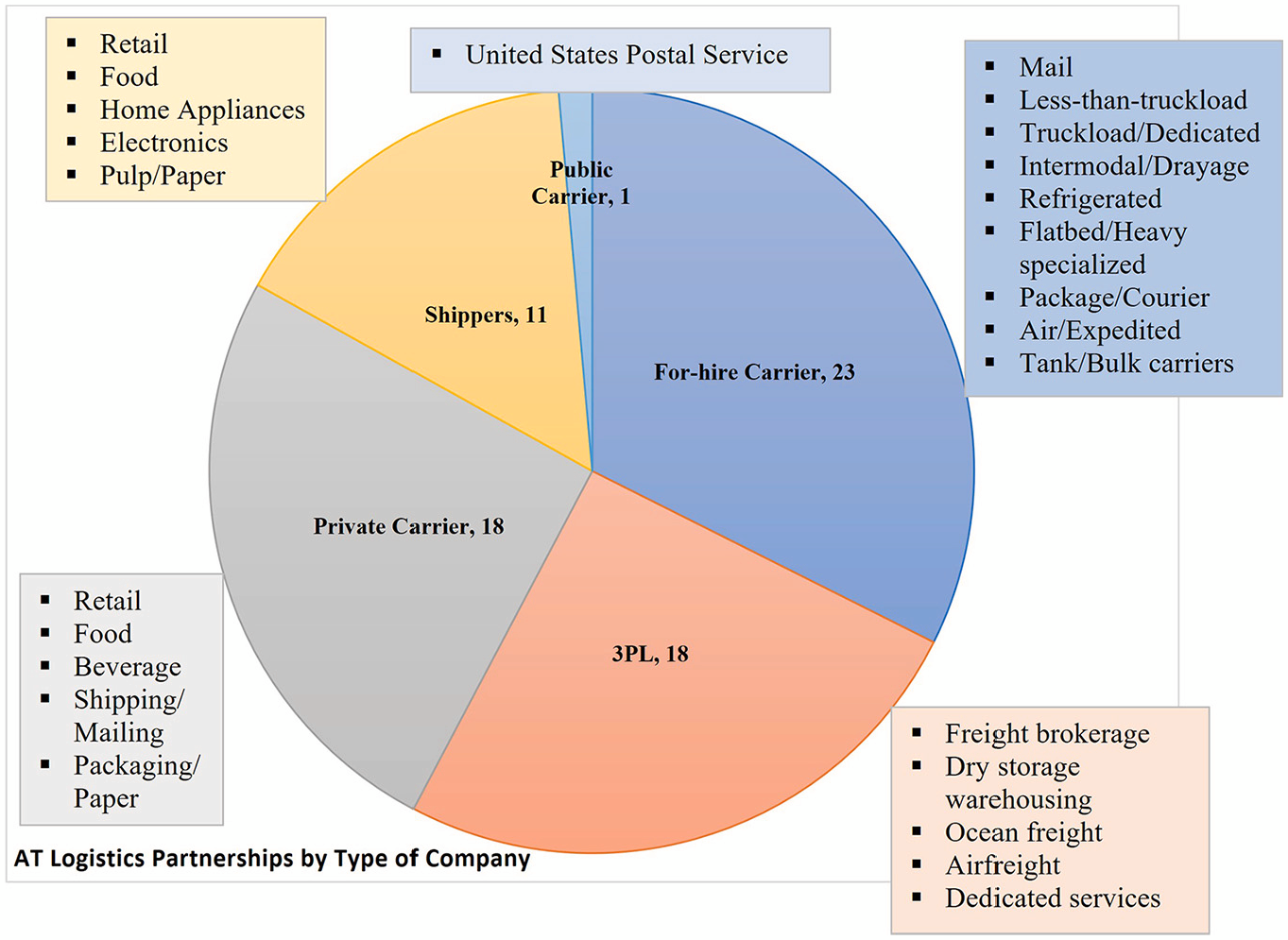

AT companies have formed logistics partnerships with at least 71 companies in the transportation industry. These include for-hire, private carriers and public carriers, logistics companies, and shippers. For-hire companies account for 32% of the companies, and private carriers, 3PL companies, and shippers make up 25%, 25%, and 15%, respectively, as shown in Figure 5. Figure 6 illustrates the deployment locations for logistics partnerships. The United States is the predominant location where companies are planning to deploy ATs. Table 12 presents the logistics partnerships for the leading AT companies and the year the partnership was announced. Some of the partnerships may be extensions of former partnerships, so the year may not be reflective of the start of the partnership. For the partnerships included in the table, most developed relatively recently with 19, 40, and 20 partnerships formed in 2021, 2022, and 2023, respectively. This accounts for 86% of the partnerships. This list does not include partnerships that were formed by companies that were no longer involved with ATs in 2023: Ike, Otto, Peloton, Pronto, and Starsky Robotics. Whereas most of the logistics partnerships being formed are to test ATs on public roads, this is not the case for all of the partnerships. Some are to explore the integration of ATs into the operations of logistics companies, to identify the needs of the industry, and to explore how ATs can help solve problem areas. Other partnerships were formed to explore deployment strategies and to identify the best routes on which to deploy ATs. Finally, some of the partnerships are reservations to utilize ATs once they are ready for commercial use. Although there are varying degrees of involvement in the logistics partnerships listed, all the partners have an interest in adopting ATs. To show the interest in ATs from the industry, companies that have ceased operations are included in Table 12. The gray highlighting in the table represents AT companies that have ceased operations (dark gray) or transitioned to a new market (light gray). None of the companies highlighted in light gray are now involved with ATs, except TuSimple, which shifted focus from the United States to international markets.

Autonomous truck (AT) logistics partnerships by type of company.

Deployment location for autonomous trucking logistics partnerships.

Logistics Partnerships

Note: The date included in parenthesis within the table is the date of the announcement. The light-gray highlighted companies have transitioned to a new market and the dark-gray highlighted companies are no longer operating.

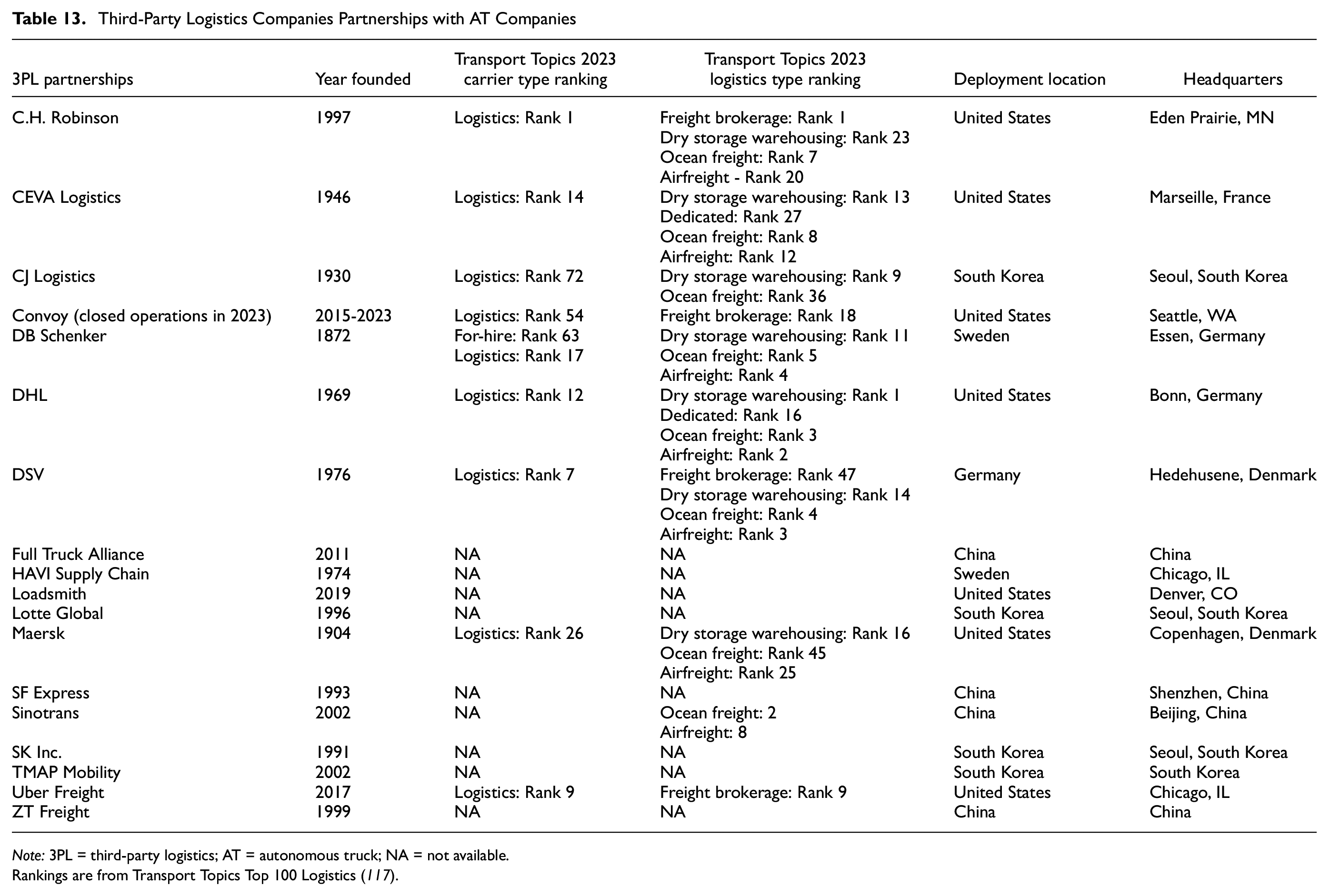

Third-Party Logistics Companies

AT companies have partnered with 18 different 3PL companies. These partnerships are planned to take place in the United States, China, Sweden, South Korea, and Germany. The United States is the main deployment location with 39% of the companies planning on deploying ATs there, 22% are in China and South Korea, and the remaining 17% are in Europe. The logistics companies involved have services for freight brokerage, dry-storage warehousing, ocean freight, airfreight, and dedicated services. According to Transport Topics 2023 rankings, the logistics companies are some of the largest in the industry including the largest freight brokerage company, C.H. Robinson, and the largest dry-storage warehouse provider, DHL ( 117 ). Newer 3PL companies, Uber Freight, Convoy, and Loadsmith, are also testing ATs. In Loadsmith’s case, the company plans to build a freight network to utilize ATs ( 118 ). ATs may offer an easier access point for traditional 3PL companies that just connect shippers and carriers, to begin to offer their own AT capacity. This is seen in the partnerships that C.H. Robinson and Uber Freight have been forming with AT companies. C.H. Robinson and Uber Freight are traditional 3PL companies that do not own trucks but instead offer a service to help connect carriers and shippers. C.H. Robinson is exploring the possibility of how ATs could be utilized on its network, and Uber Freight is working with AT companies to evaluate deployment strategies ( 119 , 120 ). In both cases, 3PL networks could turn into AT networks that are set up for the deployment of ATs. Table 13 contains all of the 3PL partnerships formed and their Transport Topics 2023 ranking.

Third-Party Logistics Companies Partnerships with AT Companies

Note: 3PL = third-party logistics; AT = autonomous truck; NA = not available.

Rankings are from Transport Topics Top 100 Logistics ( 117 ).

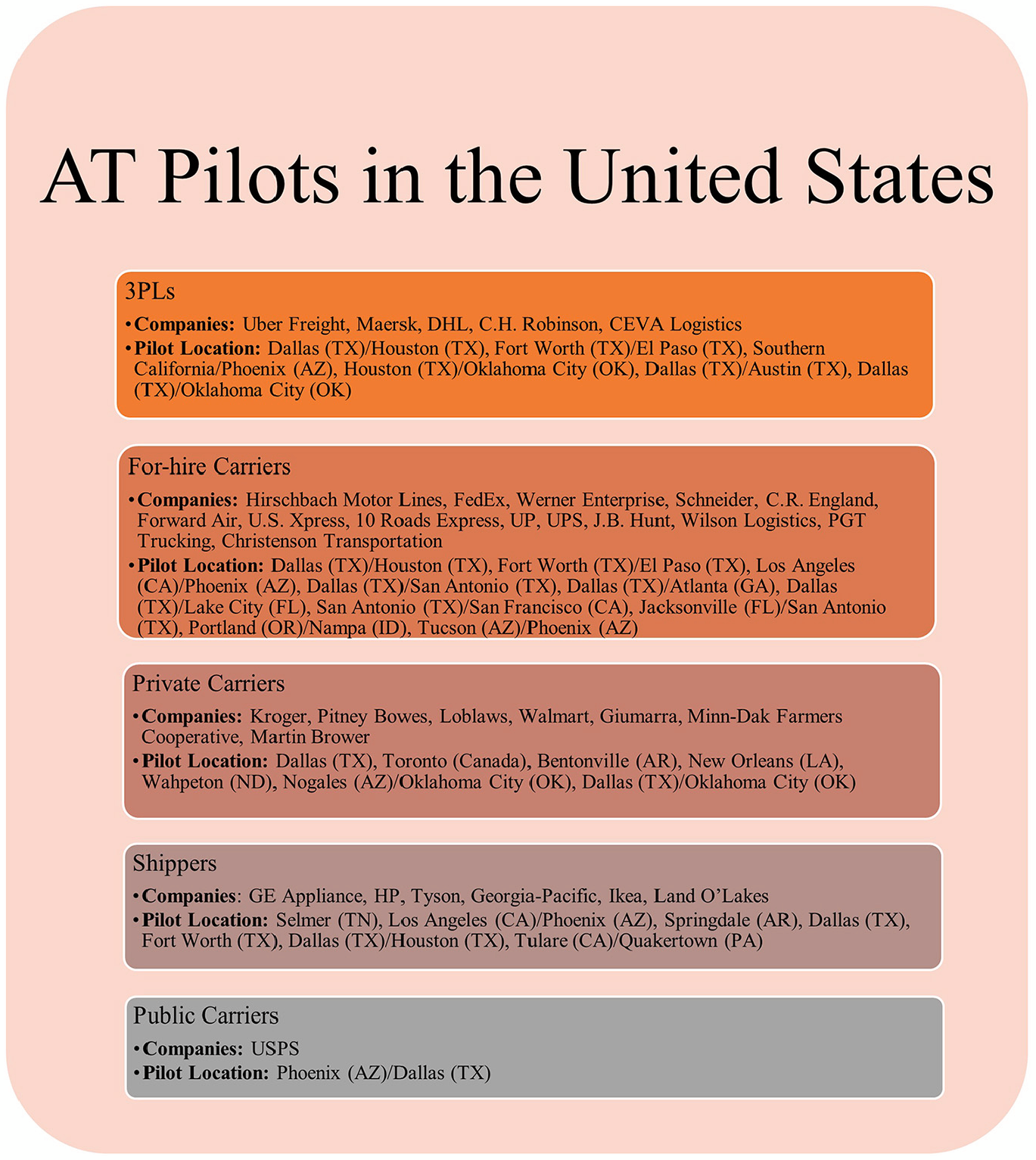

Uber Freight, Maersk, DHL, C.H. Robinson, and CEVA Logistics have all announced they plan to pilot ATs on public roads in the United States. Uber Freight is hauling freight in Texas between Fort Worth and El Paso with Aurora, and between Dallas and Houston with Waabi ( 103 , 121 ). With Aurora, Uber Freight’s customer Veritiv was chosen for the pilot to test ATs during the peak holiday season for shipping. The other partnerships are with Torc Robotics, Volvo Autonomous Solutions, and Waymo Via. Torc Robotics is using Uber Freight’s data and insights to analyze shipper volumes, and their network to plan deployment strategies for routes and hubs for ATs ( 122 ). The Volvo and Waymo partnerships were formed to integrate their autonomous driving system with Uber Freight’s network ( 120 , 123 ). Waymo plans to own the ATs initially and then eventually the customer would purchase the ATs, pay a driver-as-a-service fee, and then have the option to deploy them on the Uber Freight network. Maersk formed a partnership with Kodiak to test ATs between Houston, TX, and Oklahoma City, OK ( 124 ). Maersk views ATs as a competitive advantage that will create a sustainable solution for their customers. They joined Kodiak’s partner development program to explore other routes that may be a good fit for ATs. Another partnership with Kodiak is CEVA Logistics, who are testing ATs between Dallas–Fort Worth and Austin, TX, and Dallas–Fort Worth and Oklahoma City, OK ( 125 ). CEVA Logistics is searching for ways to improve their customers’ supply chain operations and considers ATs to be a possible solution. DHL formed partnerships with Embark, TuSimple, and Volvo. Embark had a partnerships development program like Kodiak to help facilitate the adoption of ATs. The goal of the program was to operationalize ATs by seeing how they would fit within commercial operations, finding the routes that would be best suited to ATs, and planning deployment strategies for hub locations. DHL joined the partnerships development program with Embark and piloted ATs from Southern California, CA, to Phoenix, AZ ( 126 , 127 ). The partnership with TuSimple was to haul freight between San Antonio and Dallas, and with Volvo the focus was to test out the hub-to-hub model ( 128 ). C.H. Robinson had a partnership with Waymo Via to explore the possibilities of utilizing ATs in supply chains ( 119 ). This involved initially piloting ATs between Dallas and Houston. Waymo Via was planning on using C.H. Robinson’s size, scale, platform, and customer relationships to facilitate pilot opportunities and to scale up the deployment of ATs.

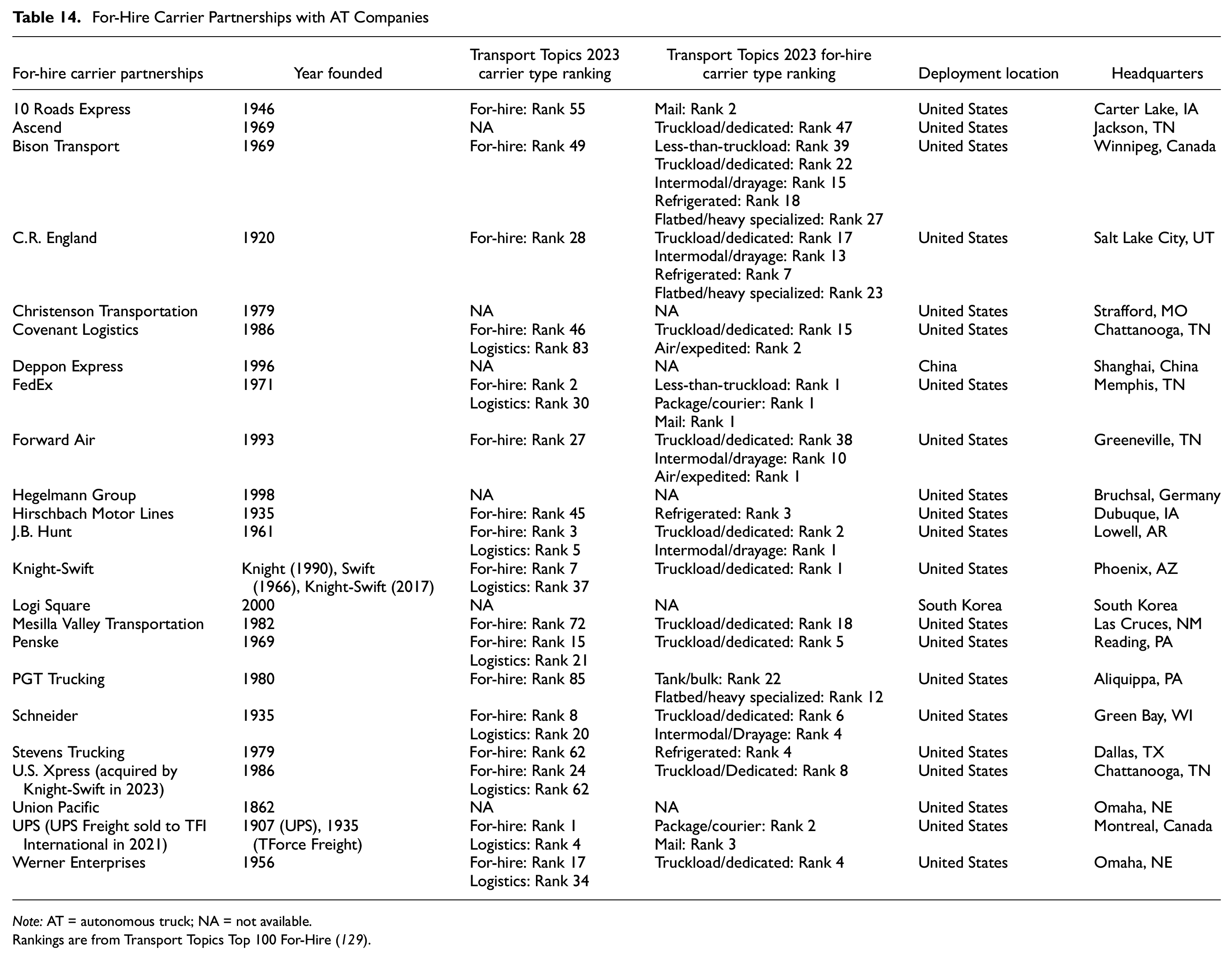

For-Hire Carriers

For-hire carriers represent the largest segment of companies that are testing ATs. There are 23 for-hire companies that have an interest in utilizing ATs and 21 of the companies are planning to deploy ATs in the United States. Two of the companies, Deppon Express and Logi Square, are based in China and South Korea, respectively. The for-hire carriers include mail, less-than-truckload, truckload, dedicated, intermodal/drayage, refrigerated, flatbed/heavy specialized, package/courier, air/expedited, and tank/bulk carriers. Some of the for-hire companies offer logistic services to customers although they also own their own trucks. For instance, J.B. Hunt and UPS are the fifth- and fourth-largest logistic providers in the United States. Although there are several types of trucking companies testing ATs, truckload is the predominant type, accounting for 35% of the for-hire carriers. According to Transport Topics 2023 rankings, the top three for-hire carriers, UPS, FedEx, and J.B. Hunt, have been involved with AT tests ( 129 ). Three companies not included in the top 100 for-hire carriers, Ascend, Christenson Transportation, and Hegelmann Group, are also interested in using ATs or platoons. Hegelmann has mainly focused on the European market and only recently started expanding into North America. Although Ascend is not in the top 100 for-hire carriers, they are the 47th largest truckload/dedicated carrier. The other smaller for-hire carriers that are interested in using ATs or platoons are Mesilla Valley Transportation and PGT Trucking. Also, one Class I railroad, Union Pacific (UP), has been involved with ATs. UP was planning on using TuSimple’s ATs to help move freight in Arizona from Tucson to Phoenix. TuSimple is now focusing on the Asia market, so this deployment route is no longer being pursued. ATs still offer the opportunity to help improve the last-mile over-the-road movement of rail freight and will likely be implemented in the future. Table 14 contains all of the for-hire carrier partnerships formed and their Transport Topic 2023 ranking.

For-Hire Carrier Partnerships with AT Companies

Note: AT = autonomous truck; NA = not available.

Rankings are from Transport Topics Top 100 For-Hire ( 129 ).

Hirschbach Motor Lines, FedEx, Werner Enterprise, Schneider, C.R. England, Forward Air, U.S. Xpress, 10 Roads Express, UP, UPS, and J.B. Hunt have all announced plans to pilot ATs on public roads in the United States. Most of these pilots are planned to take place in Texas between Dallas and Houston, Fort Worth and El Paso, and Dallas and San Antonio. Other pilots are taking place between Dallas and Atlanta, Tucson and Phoenix, Dallas and Lake City, Florida, and a roundtrip between San Antonio, San Francisco, and Jacksonville. Hirschbach Motor Lines, FedEx, Werner, and Schneider are partnering with Aurora to test ATs in Texas ( 130 – 133 ). Werner views ATs as a source of supplemental capacity to help meet the rising demand for truck freight movement. The company is piloting ATs on a subset route of their busiest route between Atlanta and Los Angeles. This is a common theme seen across multiple for-hire carriers. They view ATs as a scalable solution on certain routes that will help them balance their network. This hybrid model allows them to utilize drivers in a more structured way on routes that may be more desirable to drivers. C.R. England, Forward Air, Werner Enterprise, U.S. Xpress, and 10 Roads Express are partnering with Kodiak to test ATs in Texas and between Texas and Georgia ( 134 – 138 ). U.S. Xpress is piloting the Dallas to Atlanta route, which they see as a good route for ATs because it is too long for a same day return trip and not economical for a sleeper team. 10 Roads Xpress piloted Kodiak’s ATs on a roundtrip route between San Antonio, San Francisco, and Jacksonville. A route that is this extensive and that covers a wide geographical span is less common. Most companies are piloting specific routes that are within the same state or that span states in the same geographical area. C.R. England and Schneider have partnered with Torc Robotics to see how ATs can fit within their operations and to pilot ATs ( 139 , 140 ). Torc Robotics also has an advisory council of companies in the industry to help guide the development of their AT system. The advisory council includes Baton, C.H. Robinson, Covenant Logistics, Penske Truck Leasing, Ryder System, Inc., and Schneider ( 141 ). Kodiak and Aurora have also formed an industry advisory council to help scale ATs. Kodiak has members from logistics companies, Werner, UPS, Walmart, and Loadsmith, and Kodiak has former executives from Swift and Paper Transport ( 142 , 143 ). UPS has partnered with TuSimple and Waymo Via to test ATs for their air freight division ( 144 , 145 ). Waymo Via also partnered with J.B. Hunt to test ATs in Texas. One of the pilots hauled freight for a customer of J.B. Hunt, Wayfair ( 146 ). TuSimple performed a fully driverless test between Tucson and Phoenix with UP ( 147 ). All of the other pilots with logistics companies have been performed with a safety driver in the AT.

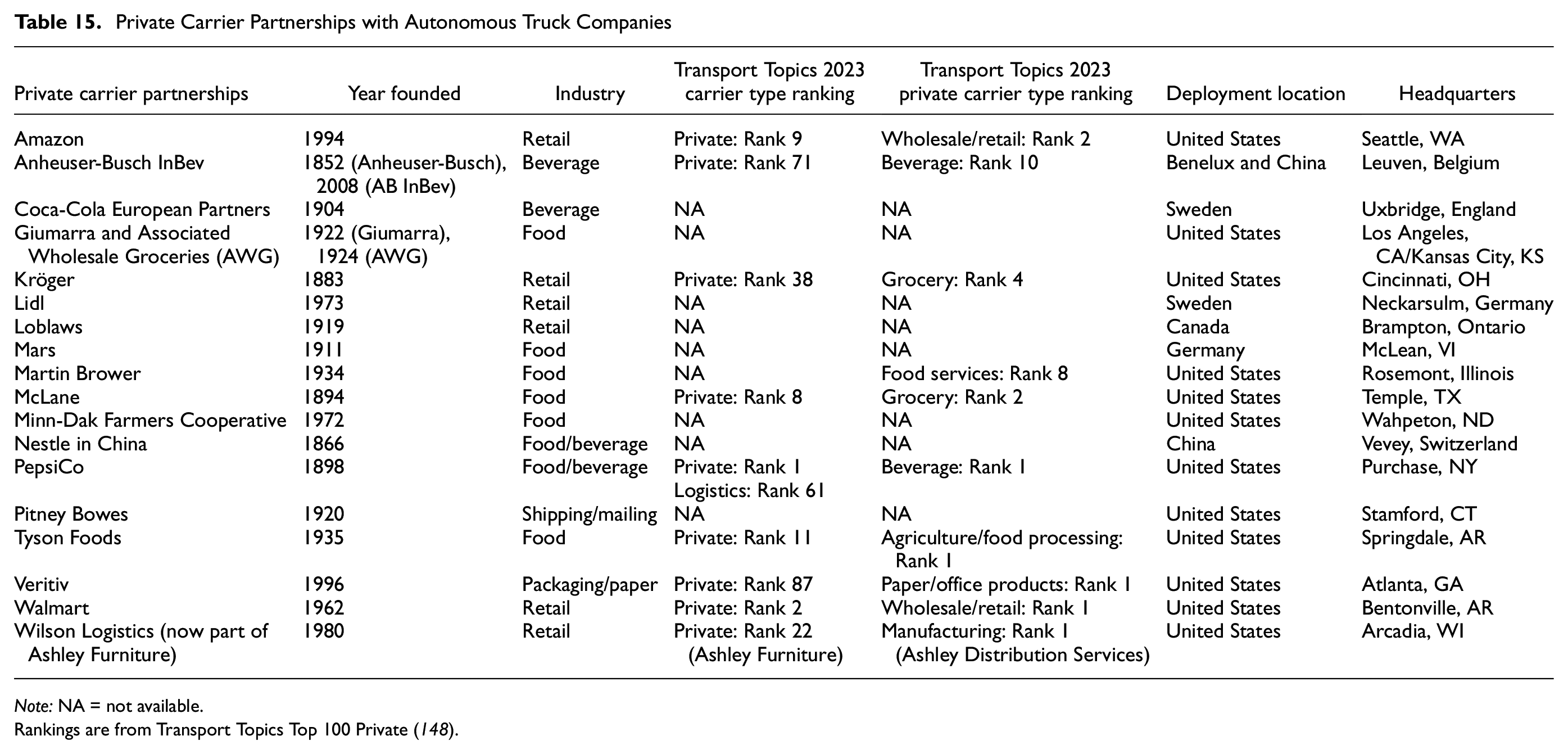

Private Carriers

Eighteen different private carriers are interested in utilizing ATs. Deployment locations include Benelux (i.e., Belgium, Netherlands, Luxemburg), China, Canada, Germany, Sweden, and the United States. Retail, food, and beverage companies are the most common, accounting for 89% of the private carriers. The only two companies not included in these industries are Veritiv and Pitney Bowes. The private carriers are some of the largest in their industry according to Transport Topics 2023 rankings ( 148 ). Walmart is the largest retailer. PepsiCo is the largest beverage company. Tyson is the largest food processing company. Veritiv is the largest paper/office provider and Ashely is the largest manufacturing company. Note that PepsiCo is listed because it ordered Tesla’s electric semitruck ( 80 ). Tesla’s electric semitrucks are not autonomous, although they could be if Tesla achieves Level 4 automation with its autopilot. This is also the case with some of the partnerships that Einride has formed. For instance, Lidl is planning to use Einride’s manually driven electric trucks ( 149 ). Other companies partnering with Einride, like Coca-Cola, are planning on using Einride electric ATs ( 150 ). Table 15 contains all of the private carrier partnerships formed and the Transport Topic 2023 ranking.

Private Carrier Partnerships with Autonomous Truck Companies

Note: NA = not available.Rankings are from Transport Topics Top 100 Private ( 148 ).

Kröger, Pitney Bowes, Loblaws, Martin Brower, Walmart, and Giumarra have announced plans to pilot ATs, and Minn-Dak Farmers Cooperative is piloting platoons on public roads in the United States. Most of the pilots are taking place with Gatik utilizing box trucks for regional deliveries. Kröger and Pitney Bowes are piloting ATs in Dallas, which is the next location Gatik plans to deploy fully autonomous box trucks ( 151 , 152 ). Loblaws and Walmart are already utilizing fully autonomous box trucks in Toronto and Bentonville, AR ( 109 , 110 ). Another food service company, Martin Bower, has partnered with Kodiak to test ATs between Dallas and Oklahoma City ( 153 ). Minn-Dak Farmers Cooperative is testing two-truck platoons in North Dakota. Minn-Dak sees platoons as a way to help meet demand during peak harvest season when demand exceeds driver availability ( 65 ). Giumarra performed an AT pilot from Nogales, AZ, to Oklahoma City hauling products for Associated Wholesale Grocers ( 154 ). Giumarra believes ATs may help supply food to rural communities and food deserts in the United States.

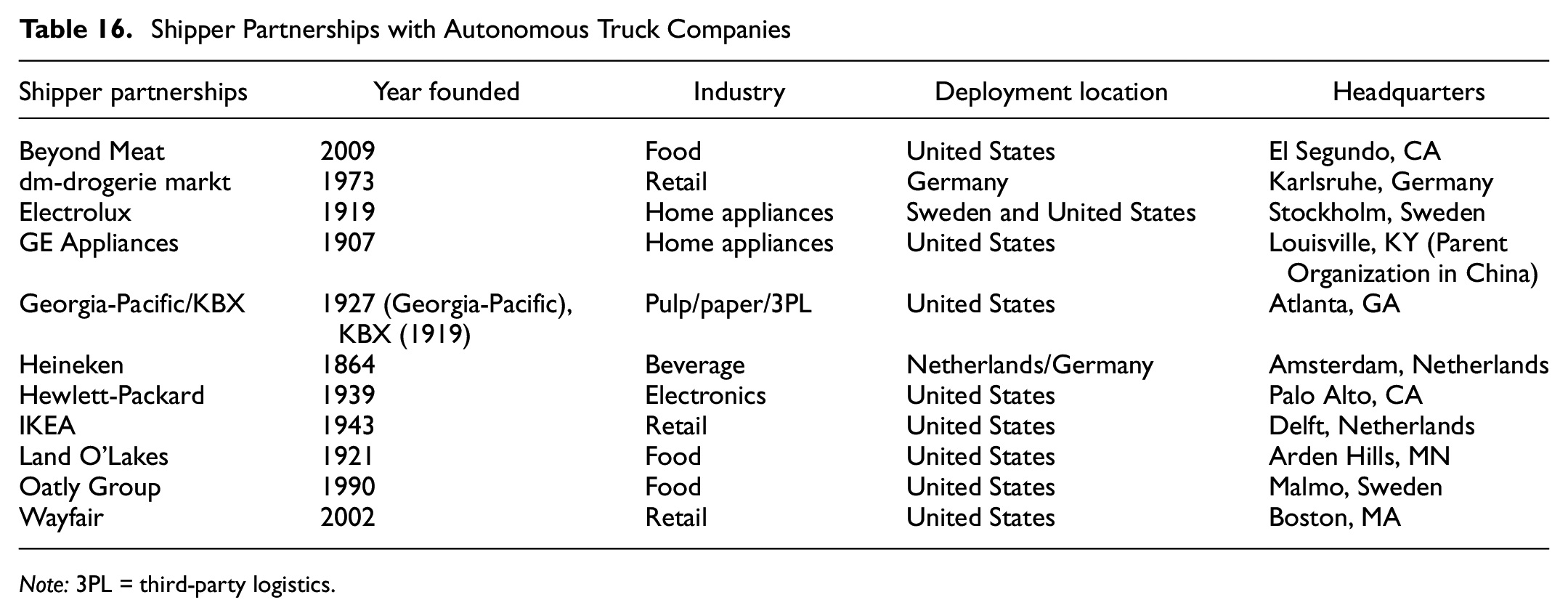

Shippers

The companies listed as shippers do not have their own network of trucks, but rely on other carriers to move their freight. The shippers that have expressed interest in ATs include food companies, appliance and home goods companies, electronic companies, and retail companies. Partnerships are taking place in the United States, Germany, Sweden, and the Netherlands. Some of the partnerships are focused on electrification. Beyond Meat, Oatly Group, and Heineken are planning to utilize Einride’s manual electric trucks. Einride is working on developing a Level 4 autonomous electric truck and electric trucks that are manually driven. The rest of the partnerships are focused on Level 4 ATs except dm-drogerie markt who is working with Plus on a highly automated system at Level 2+ automation. Table 16 contains all of the shipper partnerships formed and their Transport Topic 2023 ranking.

Shipper Partnerships with Autonomous Truck Companies

Note: 3PL = third-party logistics.

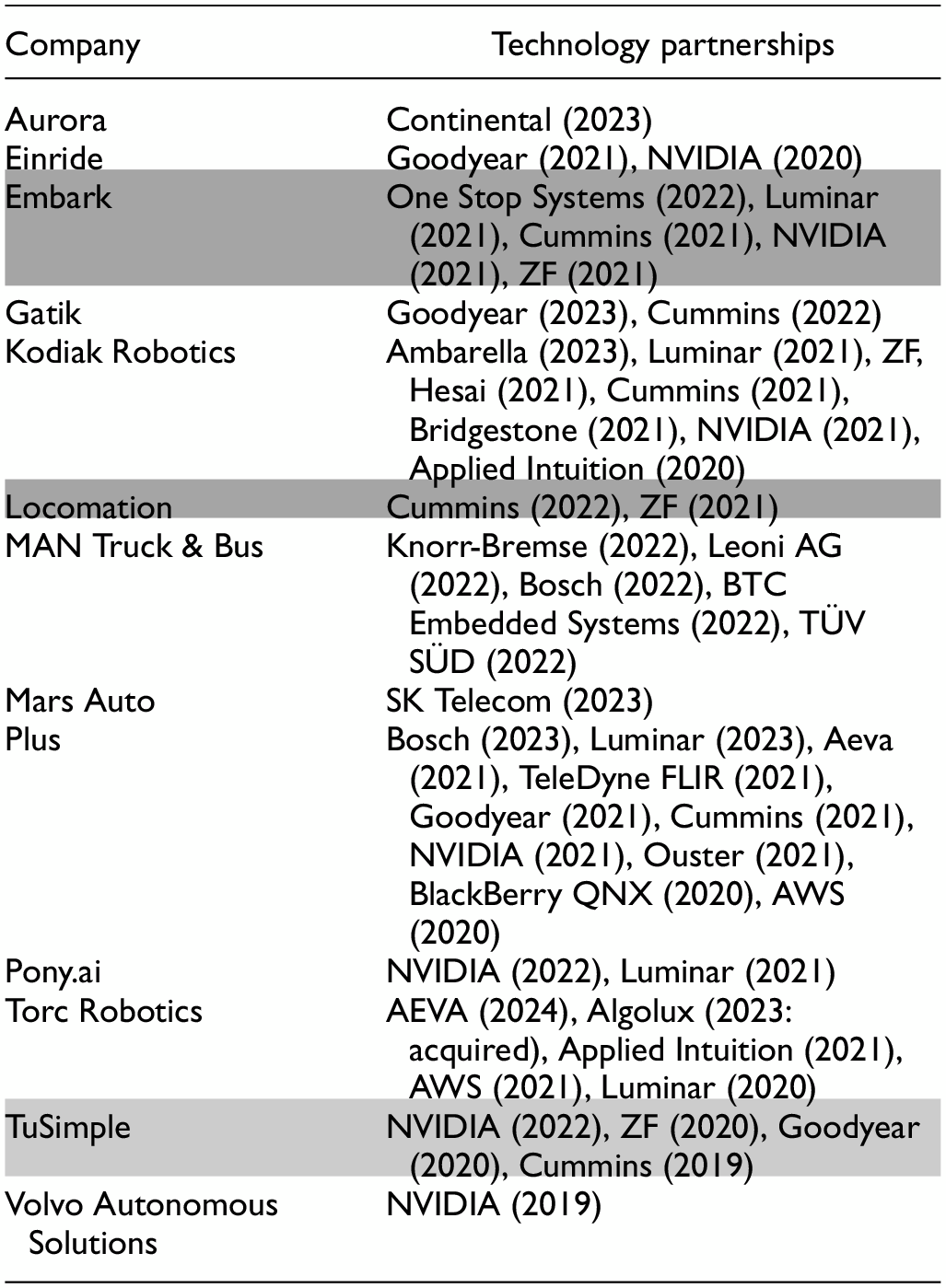

HP, Tyson, Georgia-Pacific, and IKEA have announced plans to pilot ATs and Land O’Lakes has piloted advanced driver assistance systems on public roads in the United States. HP partnered with Embark to haul printers between Los Angeles and Phoenix utilizing Embark’s ATs ( 155 ). Tyson and Georgia-Pacific partnered with Gatik to utilize autonomous box trucks in Springdale, AR, and Dallas–Fort Worth ( 156 , 157 ). Tyson is testing the use of box trucks to make more frequent trips instead of using Class 8 semitrucks. Georgia-Pacific is working with KBX, a sister company, to use autonomous box trucks to make deliveries from its locations to Sam’s Club locations. IKEA has partnered with Kodiak to test ATs between Dallas and Houston. IKEA is looking for ways to improve safety and working conditions for drivers on long trips ( 158 ). Land O’Lakes performed a pilot with Plus using its Level 2+ advanced driver assistance system from Tulare, CA, to Quakertown, PA ( 159 ). Land O’Lakes see autonomous systems as a way to help meet peak demand in the future.

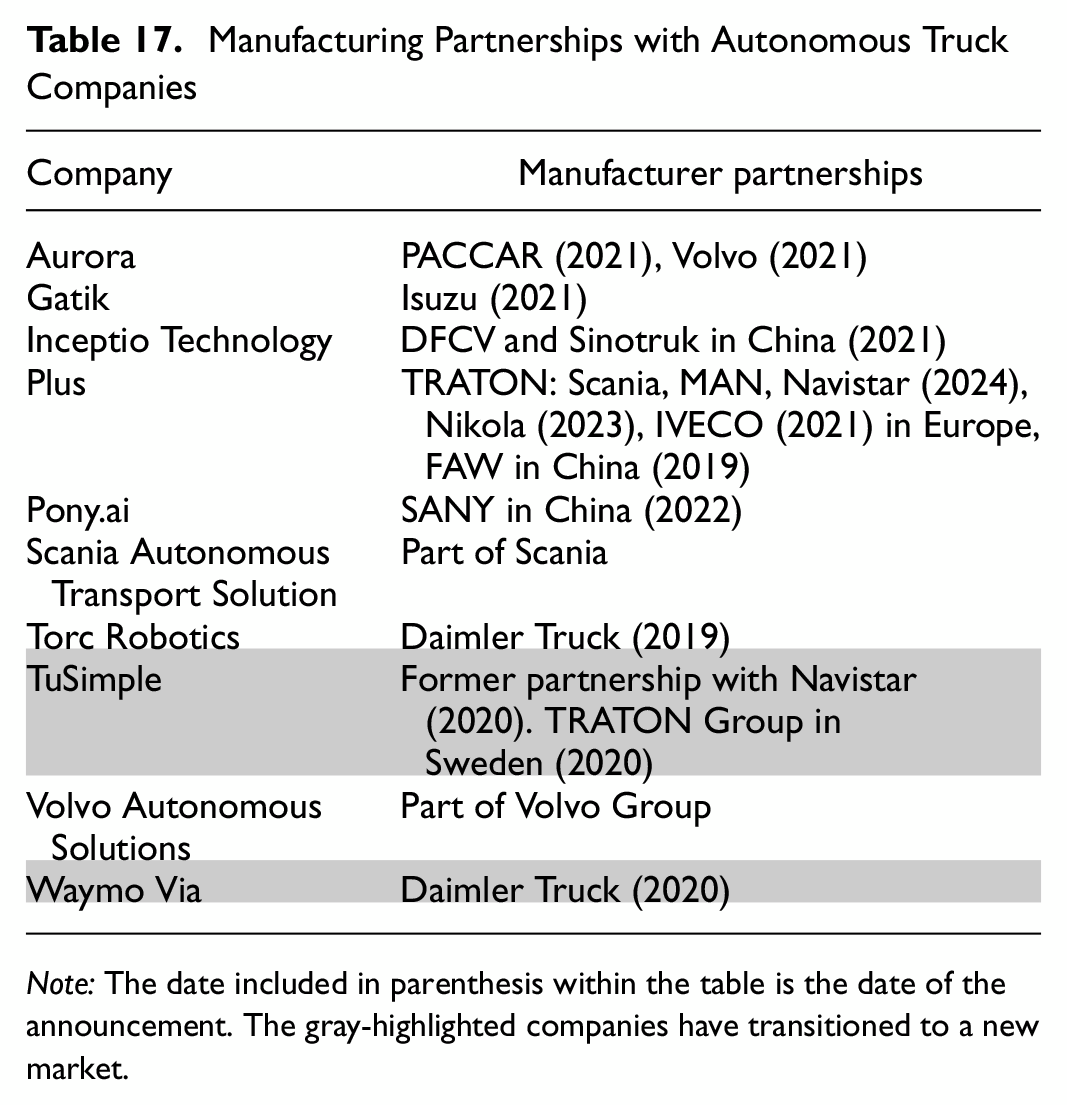

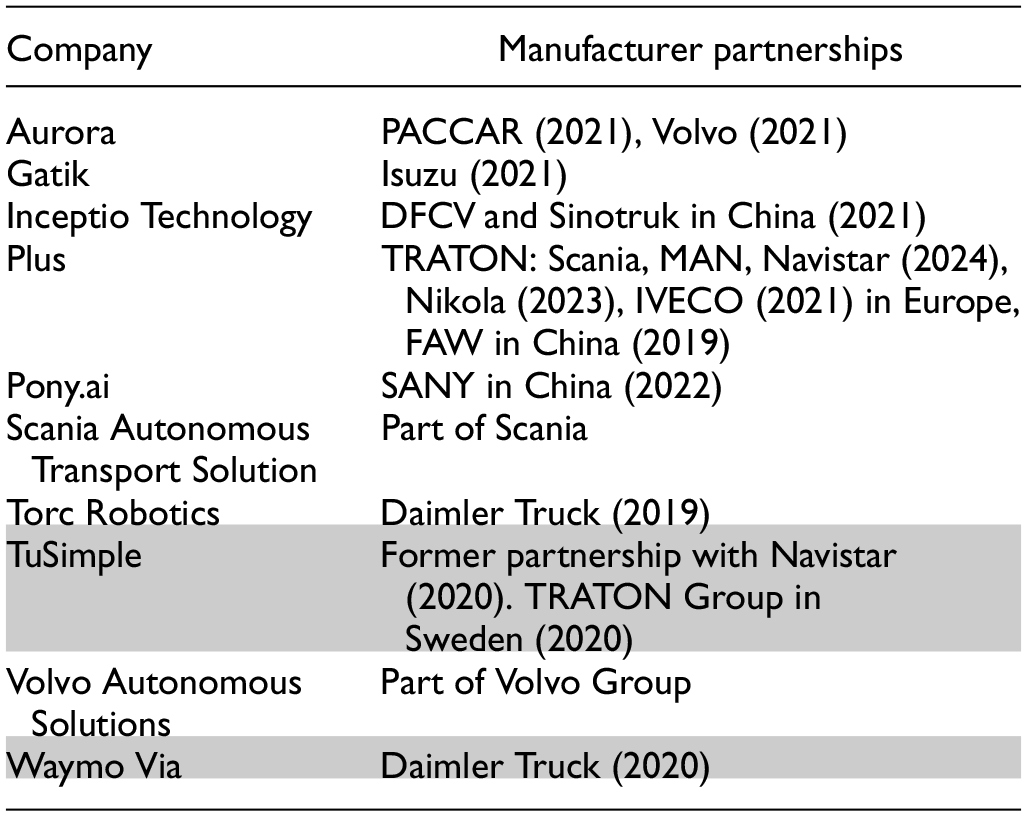

Manufacturing Partnerships