Abstract

Empowering Indigenous communities through entrepreneurialism is touted as key for reducing Indigenous disadvantage, but little headway has been made. One core and persistent issue is difficulty accessing finance to support growth. To understand why and to guide future policy and research, we review the current state of research on Indigenous financing and develop a thematic framework around four themes: political-economic environment; antecedents to the financing decision; financial solutions; and financial preferences, decisions and outcomes. Indigenous entrepreneurs face unique intercultural, social and economic barriers to finance, and these need to be better understood to help accelerate Indigenous community development through entrepreneurial activity.

Keywords

1. Introduction

Australia, Canada, New Zealand and the United States are some of the most developed nations in the world, but their Indigenous populations experience greater levels of poverty and unemployment than their non-Indigenous populations and fare substantially worse across a range of socioeconomic outcomes (Cooke et al., 2007; McCalman et al., 2016). Supporting the creation, management and growth of Indigenous-owned ventures has been identified as one critical method for empowering Indigenous communities, due to the potential for increasing access to employment opportunities (Furneaux and Brown, 2008; cf. Parthiban et al., 2021, 2024; Qureshi et al., 2022). However, a central challenge inhibiting Indigenous entrepreneurship is the difficulty Indigenous entrepreneurs encounter when acquiring financial resources (Fuller et al., 2003; Furneaux and Brown, 2008; Hota et al., 2019; Ketilson, 2014; McDonnell and Westbury, 2002; Pinto and Blue, 2017; Shoebridge et al., 2012; Zapalska and Brozik, 2017). Despite decades of government policy aimed at bolstering the Indigenous business sector in developed nations like Australia, New Zealand, Canada and the United States, Indigenous employment and business ownership continue to be disproportionately low compared to other ethnic groups (Department of Prime Minister and Cabinet, 2018; New Zealand Government, 2021; Statistics Canada, 2024; U.S. Bureau of Labor Statistics, 2023).

The literature has attributed this to a lack of personal collateral, financial literacy, rigid eligibility criteria from financial institutions (Collins et al., 2016; Furneaux and Brown, 2008; Ketilson, 2014; Pinto and Blue, 2017) and historical legacies including institutionalised racism and unfair judicial systems (David and Mitchell, 2021; Papalia et al., 2019). This is particularly distinct for Indigenous entrepreneurs in the developed nations we focus on for our research: Australia, Canada, New Zealand and the United States, which are characterised by common colonial histories, manifesting in governance arrangements and institutions controlled by the non-Indigenous majority (Armitage, 1995; Cooke et al., 2007). However, there remains a lack of systematic knowledge or complete understanding of the full set of social, political and cultural factors governing Indigenous access to finance, the efficacy of current financial solutions, or in understanding Indigenous entrepreneurial financing preferences and decision-making processes.

Building on this, it is crucial to acknowledge that intercultural dynamics play a foundational role in shaping these processes within Indigenous communities. Despite the critical impact of these dynamics in the broader entrepreneurship literature (Bhatt et al., 2019; Bhatt et al., 2024; Mafico et al., 2021; Parthiban et al., 2020; Qureshi et al., 2016, 2023; 2024), their significance is often underappreciated and inadequately explored in the broader discourse on Indigenous financing. Intercultural dynamics are the social, cultural, political and economic interactions that occur between dominant and minority members in a society (Bhardwaj et al., 2021; Bhatt et al., 2022; Hota et al., 2023; Qureshi et al., 2018; Riaz and Qureshi, 2017; Sutter et al., 2023). These dynamics are particularly salient for entrepreneurs who navigate multiple cultural environments, such as immigrants (e.g. Mafico et al., 2021; Pidduck and Tucker, 2022). Yet, the nuanced interplay between social, cultural, economic and political elements, pivotal to Indigenous financing, has been largely overlooked. This oversight underscores the urgent need for a more comprehensive exploration of intercultural dynamics to enhance our understanding of Indigenous financing mechanisms and outcomes.

Compared to immigrants, for example, who usually adopt a new dominant culture by choice and often have access to financial support networks within their host and home countries (Bates et al., 2018; Dabic et al., 2020), Indigenous people have historically been forced to engage with dominant cultures due to colonialism. This experience has left lasting impacts, including a weakened financial support system within Indigenous communities (Ketilson, 2014). Consequently, while financing for both immigrant and Indigenous entrepreneurs are rooted in intercultural dynamics, these dynamics are likely more intense for Indigenous entrepreneurs due to differing financial product design and financial service needs.

Intercultural dynamics may also complicate the relationship between Indigenous entrepreneurs and financiers. First, relationship building is critical in any business or financing arrangement. However, historical injustices and ongoing systemic disparities have eroded the confidence of Indigenous populations and limited their engagement with mainstream financial institutions (David and Mitchell, 2021; Papalia et al., 2019). Consequently, building strong relationships with Indigenous entrepreneurs may require financiers to demonstrate intercultural competence by, for instance, respecting Indigenous values, showing a genuine commitment to supporting Indigenous economic development and adhering to cultural customs such as ‘Welcome to Country’, which is a distinct cultural recognition extended to Indigenous peoples as the traditional landowners (McKenna, 2014; Merlan, 2014). Second, Indigenous entrepreneurs often incorporate cultural values and practices into their business models, which can differ from mainstream business practices (Parhankangas and Colbourne, 2023) and require ethical considerations (cf. Bhatt, 2022; Hota et al., 2023; Zainuddin et al., 2023). This might include prioritising community well-being, environmental stewardship and cultural preservation over profit maximisation (Parhankangas and Colbourne, 2023). Therefore, financiers need to understand and respect these values, adjusting their evaluation criteria and support mechanisms accordingly. Third, due to colonisation and the historical context of injustices and oppression, Indigenous entrepreneurs may have different experiences and levels of familiarity with formal financial systems (Collins et al., 2016; Furneaux and Brown, 2008; Ketilson, 2014; Pinto and Blue, 2017). Tailored financial education policies and programmes that acknowledge and incorporate Indigenous knowledge systems will then be needed to bridge this capability gap.

When viewed collectively through an intercultural dynamics lens, Indigenous communities’ financing needs, processes and outcomes deviate from conventional financing norms and assumptions (Pidduck and Tucker, 2022). This makes creating a theoretically and empirically insightful body of knowledge challenging and may explain why the academic literature on Indigenous financing experience is fragmented, hindering theory development. This fragmentation obscures an understanding of how these financing barriers interrelate and which are most significant in what circumstances. Complimentary to this fragmentation is a significant body of grey literature that includes government documents, speeches, third-party reports and other unpublished work. Examples of this include discussions of loan programmes in the United States (Dewees & Sarkozy-Banoczy, 2008), Australia (Morley, 2014) and Canada (Schembri, 2022), a qualitative look at Indigenous financial resilience in Australia (Weier et al., 2019), and numerous research into social impact investing and non-traditional finance opportunities (CMHC, 2021; Lacerte and Hunter, 2023; Theodos et al., 2021). This potential mismatch between peer-reviewed output and grey literature production suggests a demand for more systematic research into Indigenous financing that is not currently being fulfilled by the academy at large. Indeed, a mismatch in the depth of discussion and analysis between the grey literature and academic research could represent a risk to the generalisability of academic research and its representativeness of the lived experiences of Indigenous entrepreneurs.

Against this backdrop, we argue that a greater understanding of Indigenous financing requires a more organised interpretation of the current research and a detailed investigation of the complex intercultural dynamics influencing Indigenous entrepreneurs. With respect to intercultural dynamics, we pay attention to two interconnected issues. First is the socioeconomic side, where Indigenous entrepreneurs must overcome multi-generational disadvantage and economic exclusion while navigating Western financial systems. Second is the cultural side, where there is an inherent friction in Indigenous-non-Indigenous interpretations of the role of the firm, capital and community development. With this in mind, we systematically analyse the Indigenous financing literature.

We focus our review on Australia, Canada, New Zealand and the United States, as they share common colonial histories under a settler colonialism typology (Shoemaker, 2015) and common Anglo-Saxon institutions and economic development pathways. These countries also show differences in their post-colonial approach to addressing historical Indigenous disadvantage due to variations in national discourses towards Indigenous reconciliation. Improving outcomes for Indigenous communities is also gaining prominence in national debates across Australia, Canada and New Zealand. This includes the recent Referendum on Indigenous rights in Australia, the importance of Māori development in the New Zealand well-being budgeting model (Mintrom, 2019) and the creation of the National Centre for Truth and Reconciliation in Canada. Meanwhile, the United States government provides billions of dollars a year in funding for Indigenous programmes through the Bureau of Indian Affairs (U.S., 2022). Given the need for quality research to inform good public policy making, and given common legacies and development pathways between the four countries in this review, understanding what is working and in which context should be useful for policy makers interested in improving Indigenous outcomes through entrepreneurial activity.

To achieve these goals, we systematically map the dimensions of difference facing Indigenous entrepreneurs in receiving finance compared to non-indigenous entrepreneurs. Our study indicates an Indigenous financing ecosystem with more complex personal, cultural and market-related factors in comparison to non-Indigenous entrepreneurs. We find that many Indigenous-specific institutions designed to address access to finance often struggle to cover operating costs and maintain capital bases, leading to a shift towards more mainstream lending and a deviation away from their original mandate. This is supported by Ketilson (2014), who found that despite the original mandate of meeting the needs of Indigenous individuals and communities, Indigenous financing institutions experienced deteriorating financial health. This is attributed to operating deficits and loan-capital shrinkage, and in order to recover their financial position, mainstream lending practices had to be adopted.

Our research produces three important contributions. First, our analysis systematically links the currently fragmented body of research into a coherent thematic framework comprising four interconnected and path-dependent components: political-economy issues; antecedents to the financing decision; financial solutions; and financial preferences, decisions and outcomes. We outline what research currently exists across all relevant fields of study, map current research gaps and offer suggestions to guide future research. This provides a valuable starting point for entrepreneurship scholars to approach future Indigenous financing research. Second, through our systematic methodology, we position Indigenous financing as a distinct stream of research that cannot rely solely on findings from the conventional literature on entrepreneurial financing. Third, our results provide guidance to policy makers with an interest in using evidence-based public policy to help Indigenous entrepreneurs flourish.

2. Methodology

To systematically map the research covering both Indigenous entrepreneurship and finance, we conducted a search of the databases Scopus, EconLit, ProQuest, EBSCO, Emerald Insight and Web of Science, using the terms (‘entrepreneurial financ*’ OR ‘financ* resour*’ OR ‘capital financ*’ OR ‘venture financ*’ OR ‘debt financ*’ OR ‘equity financ*’) AND (‘indigenous entrepreneur*’ OR ‘indigenous business*’). We also conducted a search with more general terms including ‘finance*’ AND ‘indigenous’ AND ‘entrepreneur*’ OR ‘business*’ OR ‘enterpris*’ OR ‘employ*’; as well as ‘Māori entrepreneur*’. We also interchanged the term ‘indigenous’ with ‘aborigin*’, ‘first people’, ‘trib*’, ‘native’, ‘traditional owner’ and ‘first nation’. The search terms were applied to keywords, and our search strategy was consolidated with backwards and forwards citation searching. We limited our search to English language peer-reviewed journals and selected articles that met our criteria of simultaneously referring to: (1) financing; (2) entrepreneurship and (3) Indigenous populations in at least one of Australia, New Zealand, Canada or the United States. The abstract of each article retrieved was reviewed for their relevance across all three criteria. Where the abstract was not definitive, the entire article was reviewed.

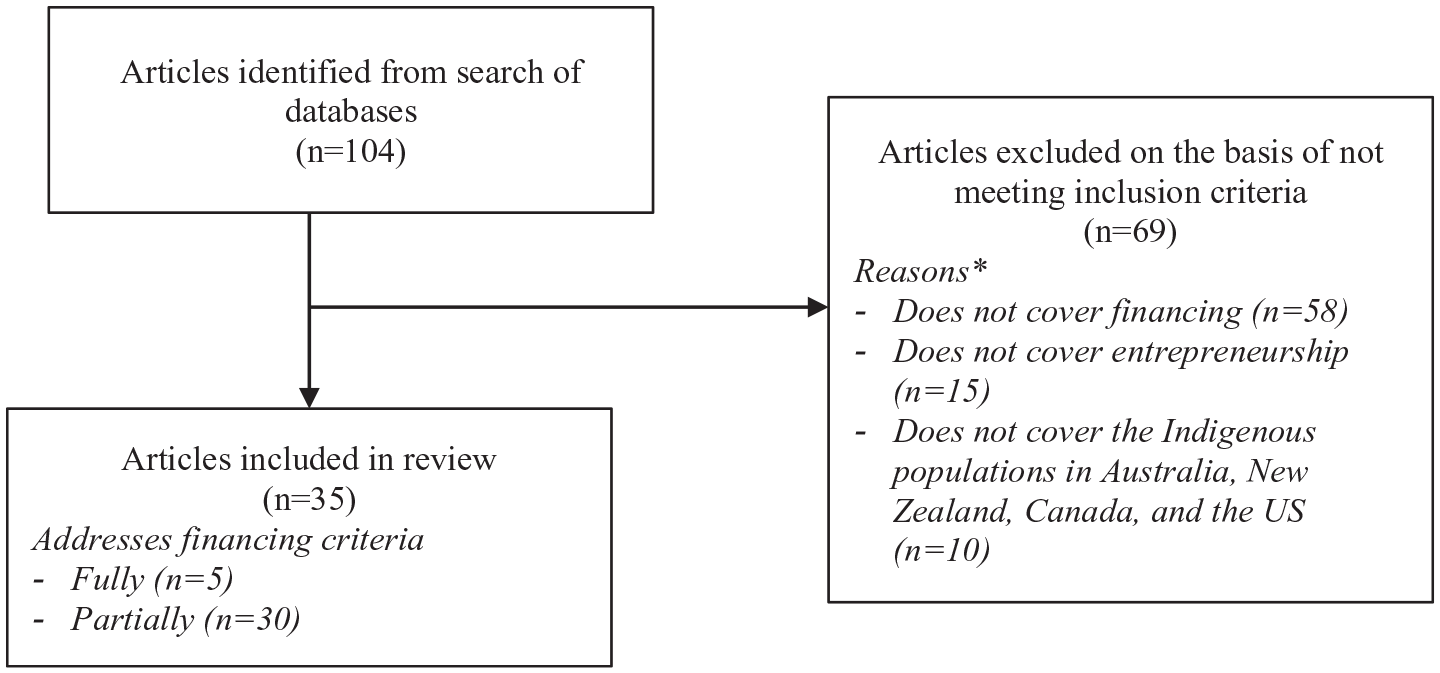

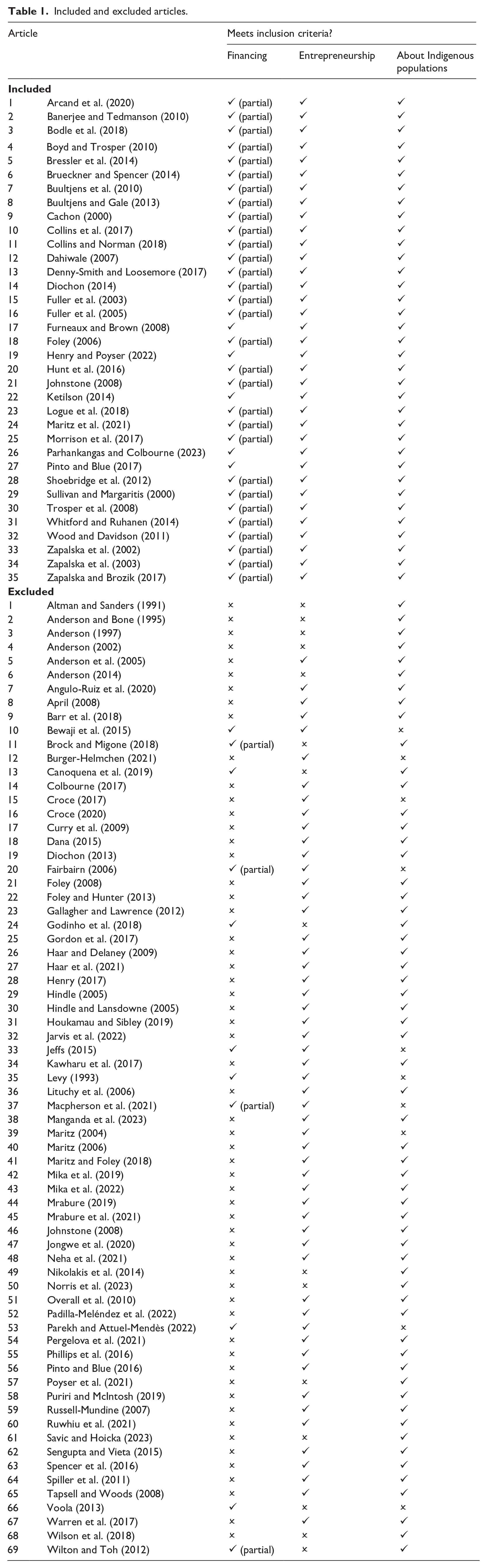

The results of the search are illustrated in Figure 1. In total, we found 104 articles based on our search terms but excluded 69 for not meeting one or more of the selection criteria. The majority of these (n = 58) did not address the financing element. We also excluded ten studies as they were not about Indigenous populations. For example, Voola (2013) addresses the financing criterion but it is more broadly related to disadvantaged individuals. Of the remaining 35 articles in our review, the financing criterion remained an issue, with only five articles fully addressing the criterion and 30 partially addressing this criterion. However, we included all 35 articles in our analysis to shed more light on this topic. A detailed list of included and excluded articles is provided in Table 1. Inductive coding was then used to identify the key themes in the literature, and thematic analysis was undertaken to synthesise the results.

Flowchart of search strategy, screening and inclusion.

Included and excluded articles.

3. Results

3.1 Current state of the literature

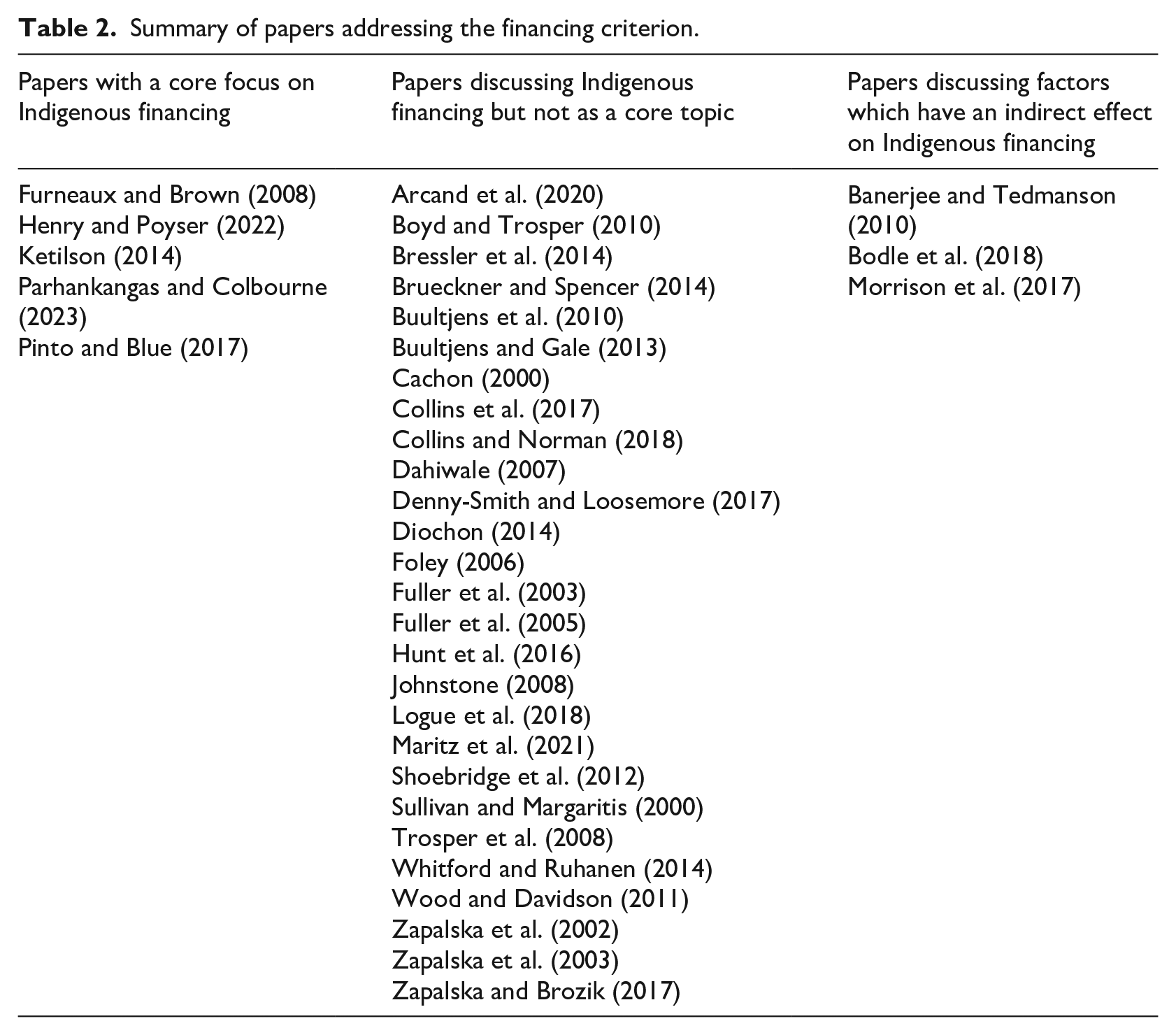

The literature on Indigenous financing can be broken into two groups: one where financing represents a central topic for discussion, and a second group where financing is included as part of a broader discussion of Indigenous entrepreneurialism. Of the five articles in the first group, one is on Indigenous Australians, one is from New Zealand and the other three are from Canada. No literature fit for inclusion in this group examines Indigenous financing in the United States. In the Australian context, Furneaux and Brown (2008) explore various capital constraints facing Indigenous Australian entrepreneurs, including financial capital, and outline examples of programmes and financing solutions to overcome this. While this paper technically satisfies our three criteria, it is primarily a literature and programme review from 2008 and is outdated and lacks empirical evidence. For New Zealand, Henry and Poyser (2022) examines how Māori history, culture and values inform the investment approach of the Māori Asset Holding Institution, an institution set up to administer Māori resources. For Canada, Ketilson (2014) studies the role of Aboriginal Finance Institutions (AFIs) (now known as Indigenous Finance Institutions) in financing entrepreneurs in Canada, while Pinto and Blue (2017) explore the inclusion and exclusion of Aboriginal groups from access to mainstream business resources and opportunities. Finally, Parhankangas and Colbourne (2023) investigate crowdfunding as an innovative method of accessing capital in Canada.

The other 30 studies we include only partially address the financing element, despite them being substantively about Indigenous entrepreneurialism. In particular, most briefly discuss financing without it being the focus of the paper, while others indirectly discuss factors with direct impacts on financing such as the broader political-economy, accounting standards and asset valuation. Table 2 outlines a summary of these papers.

Summary of papers addressing the financing criterion.

All the included studies and the majority of excluded studies fully meet our other two criteria (Indigenous and entrepreneurship), demonstrating that there is plenty of literature on Indigenous entrepreneurship generally, but with a significant gap in research competency on understanding the financing elements of Indigenous business ownership.

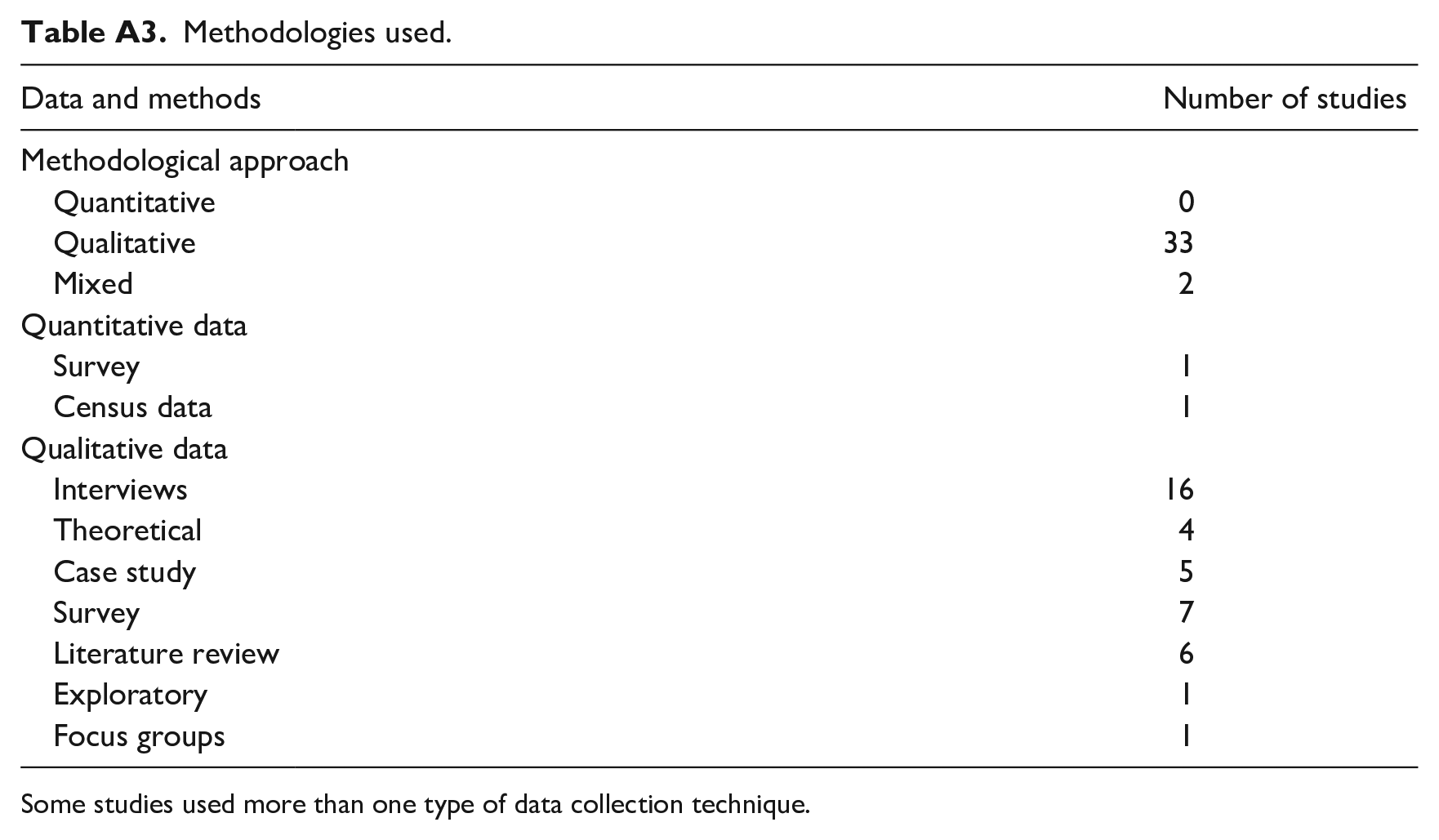

Within our search results, the earliest article is from 2000, with a slight increase in publications from 2005 onwards (refer to Appendix 1). There is a significant spread of publication outlets, spanning general policy, entrepreneurship and sector-specific (e.g. tourism, construction). However, no single journal, or academic field-specific set of journals, dominates Indigenous financing research. Most studies consider financing in terms of formal arrangements between entrepreneurs and government/financial institutions. However, there is some recognition that personal funds and informal arrangements such as loans from friends and family are important capital sources. Most studies (n = 33) adopt a qualitative approach, with interviews as the primary method of data collection (n = 10). Quantitative methods (surveys and secondary analysis with census data) are used in two papers but only as part of a mixed methods approach (Collins et al., 2017; Morrison et al., 2017). Further details on the descriptive analysis of included studies are provided in Appendix 1.

3.2 Major themes

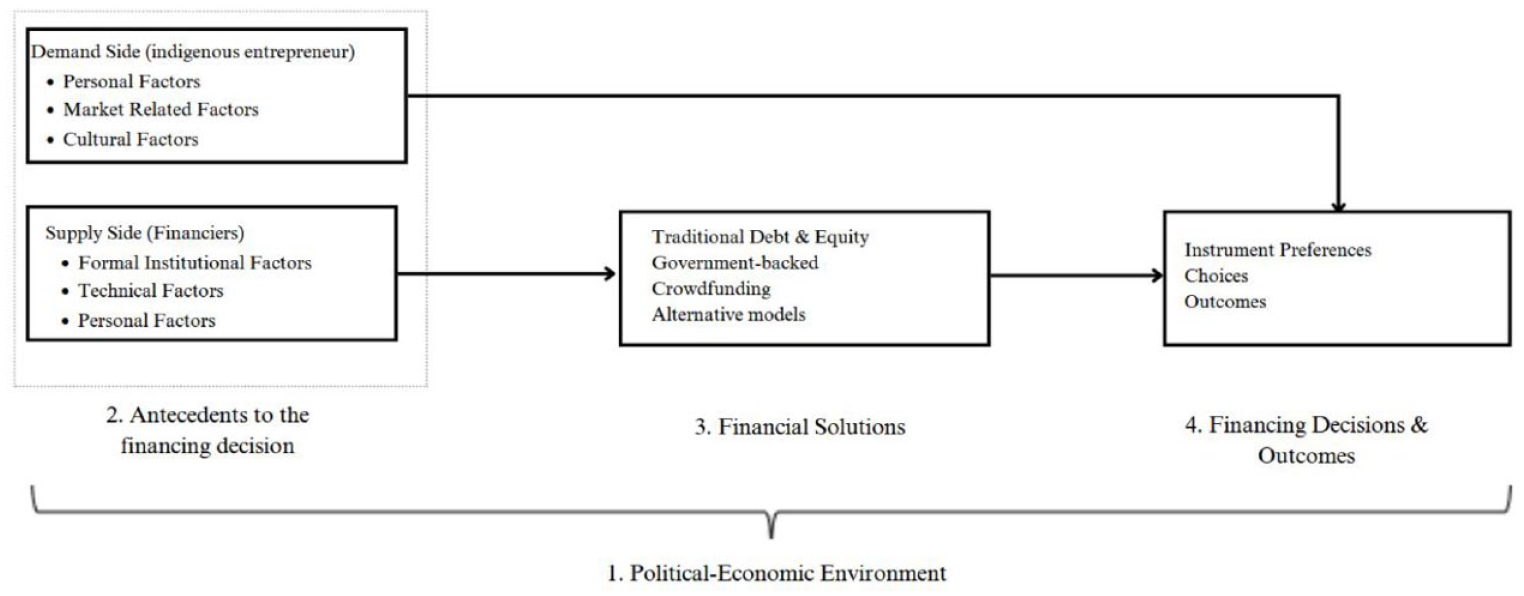

Following our review, we identify four major themes: issues in political-economy; antecedents to the financing decision; financial solutions and financing choices, preferences and outcomes. The connection and relationship between themes is illustrated in Figure 2. Each theme is outlined as follows.

Research themes.

3.2.1. Theme 1: Political-economic environment

The literature points to a political-economic environment that strongly favours mainstream socioeconomic systems i.e. ‘whiteness’, where governance arrangements and institutions governing the economic exchange and the control of resources, such as access to finance, reflect and favour the dominant, non-Indigenous culture (Banerjee and Tedmanson, 2010; Henry and Poyser, 2022; Pinto and Blue, 2017). This can be considered a liability of difference, a key a-priori point of difference between how the financial market functions for Indigenous entrepreneurs versus their non-Indigenous counterparts. It represents the end result of what Pidduck and Tucker (2022) refer to as an intercultural dynamic and acts as an antecedent to the financing decision-making process for Indigenous entrepreneurs and finance providers.

The concept of ‘liability of difference’ is inspired by the firm-level concepts of ‘liability of foreignness’ and ‘liability of newness’, and it highlights the unique challenges Indigenous entrepreneurs face in accessing financial resources within a political-economic environment that favours mainstream socioeconomic systems and the dominant non-Indigenous culture. This liability represents a fundamental distinction in how financial markets operate for Indigenous entrepreneurs compared to their non-Indigenous counterparts, influencing decision-making processes concerning financing for both Indigenous entrepreneurs and financial institutions (Bruton et al., 2015; Hahm et al., 2013; Mrabure et al., 2021). Instances of the liability of difference are also evident in various contexts, underscoring the disparities faced by different groups in accessing financial resources such as gender and immigrant enterprises (Gurău et al., 2020; Munyon and Kane-Frieder, 2015; Panic, 2017).

Comparing the ‘liability of difference’ with the ‘liability of newness’ and ‘liability of foreignness’ reveals both parallels and distinctions. The ‘liability of newness’ is a macro-to-meso level concept that refers to the challenges new firms face due to a lack of experience, external ties and legitimacy (Bruderl and Schussler, 1990; Stinchcombe, 1965), while the ‘liability of foreignness’ pertains to the difficulties foreign firms encounter in unfamiliar markets (Zaheer, 1995). In contrast, the ‘liability of difference’ focuses on disparities by specific groups such as Indigenous entrepreneurs due to cultural and socioeconomic differences (cf. Lassoued et al., 2024). In essence, the liability of difference serves as a crucial concept for explaining the systematic barriers and disparities that Indigenous entrepreneurs (and other marginalised groups) face in accessing financial resources and navigating the economic landscape.

To determine eligibility for Indigenous-specific support, various definitions of an ‘Indigenous business’ have also been developed based on mainstream businesses (Collins and Norman, 2018; Foley and Hunter, 2013). However, these definitions of business in the Indigenous context are problematic and closely related to Western definitions of the purpose and functioning of private enterprises. Rather, there is no typical Indigenous business and significant variation exists in the proportion of Indigenous ownership, business structure and geography (Collins and Norman, 2018; Morrison et al., 2017). Business models often fall outside of the mainstream (Brueckner and Spencer, 2014), and the emphasis on profit and commercial viability as a criterion for financing does not always align with the Indigenous definition of success (Buultjens and Gale, 2013; Henry and Poyser, 2022; Hunt et al., 2016; Pinto and Blue, 2017), despite profit still existing as one goal for Indigenous businesses (Shoebridge et al., 2012).

Accounting standards play a critical role in facilitating the provision of financial information and making decisions on the allocation of resources, especially in capital markets. However, in the literature, this is predicated on mainstream notions of market and value (Arcand et al., 2020; Buhr, 2011). A particular issue in valuing an Indigenous business venture using current accounting standards is that no standard recognises communally held and intangible Indigenous cultural heritage or cultural, intellectual property as assets (Bodle et al., 2018). Indeed, while these often have considerable commercial and community value, their cost ‘on acquisition’ needs to be reliably measured to be counted as assets for accounting purposes – a concept that does not reconcile with how Indigenous cultural assets work. Since many lending technologies/debt products require collateral to minimise risks for the lender (Berger and Udell, 2006), asset definition and recognition practices will impact the financing options available to Indigenous businesses.

3.2.2. Theme 2: Antecedents to the financing decision

Research exploring the antecedents to financial decision-making indicates challenges on both the demand side, represented by Indigenous businesses or entrepreneurs, and the supply side, which includes financial providers.

On the demand side, there is a clear difference between Indigenous and non-Indigenous experiences across three sub-categories: personal, market-related and cultural. Personal factors were the most widely reported in the sample. They are primarily due to socioeconomic disadvantage and historical legacies and include lower levels of reported income and assets (Collins et al., 2017; Fuller et al., 2005; Furneaux and Brown, 2008;), low levels of education, financial literacy and experience (Cachon, 2000; Furneaux and Brown, 2008; Whitford and Ruhanen, 2014), and a lack of general business skills in planning, management and marketing (Fuller et al., 2005; Zapalska and Brozik, 2017; Zapalska et al., 2002). Fuller et al. (2005) also suggest that Indigenous entrepreneurs lack familiarity with the procedures of mainstream financial institutions, including being able to prepare suitable business and financial plans. While these issues are not uncommon for other entrepreneurs, Indigenous business owners also report intimidation, discrimination and low levels of support. This impacts their decision to seek finance and creates challenges in accessing support (Denny-Smith and Loosemore, 2017; Logue et al., 2018; Wood and Davidson, 2011; Zapalska and Brozik, 2017). Market-related factors refer to a historical lack of partnerships between Indigenous organisations and financial institutions and government, with financial institutions often not physically present in local Indigenous communities (Furneaux and Brown, 2008). Finally, cultural factors represent intercultural friction between Indigenous entrepreneurs and non-Indigenous financing groups. These include the additional driver of community needs, social issues and kinship obligations that underpin Indigenous financing decisions, particularly for females (Morrison et al., 2017; Wood and Davidson, 2011).

On the flip side, issues on the supply side can be grouped into three sub-categories: formal institutional factors, technical-related factors and personal factors. Formal institutional factors include the application process, which is viewed as confusing, lengthy and challenging to navigate (Shoebridge et al., 2012; Wood and Davidson, 2011) and often includes complex eligibility requirements and strict loan conditions (Pinto and Blue, 2017; Zapalska and Brozik, 2017). Shoebridge et al. (2012) also report that interest rates for government-supported loans are often on par with mainstream commercial lenders rather than at concessional rates as advertised. The absence of financial institutions on reserve territory or specific services tailored for remote or regional Indigenous clients was also highlighted as a barrier (Cachon, 2000; Maritz et al., 2021). Technical-related factors relate to the assessment of the Indigenous entrepreneur using standard loan criteria such as creditworthiness, capital and capacity to repay, which financiers measure in terms of adherence to Western values rather than complex Indigenous values (Foley, 2006; Pinto and Blue, 2017). Personal factors comprise poor cultural understanding and education by financiers and policymakers (Foley, 2006), where interests can be compromised in favour of non-Indigenous interests (Pinto and Blue, 2017).

3.2.3. Theme 3: Financial solutions

How financial solutions are designed and marketed to Indigenous entrepreneurs is an outcome of the intercultural dynamic between entrepreneurs and financiers. While there is literature on Indigenous financial solutions, what does exist tends to focus on Indigenous-specific financial institutions, as authors generally recognise them as necessary in supporting Indigenous entrepreneurs (Ketilson, 2014; Sullivan and Margaritis, 2000). Other articles on financial solutions generally focus on non-traditional financing arrangements, including venture capital (Buultjens and Gale, 2013), crowdfunding (Parhankangas and Colbourne, 2023), microfinance (Furneaux and Brown, 2008) and social impact investing (Poyser et al., 2021).

On the government-supported side, organisations built to help Indigenous entrepreneurs include the Indigenous Finance Institutions (IFI) in Canada, the Māori Development Corporation (MDC) and Māori Asset Holding Institution (MAHI) in New Zealand, and Indigenous Business Australia. Despite their importance, recent literature on their effectiveness is lacking. What does exist includes a suggestion by Ketilson (2014) and Johnstone (2008) that many IFIs struggle financially, which leads to mission drift towards more mainstream lending, while Sullivan and Margaritis (2000) argue that mission drift at the MDC has led it towards venture capital and merchant banking. Johnstone (2008) also notes the limitations of these purpose-built institutions which are unlike mainstream institutions that have long-standing knowledge, experience and existing structures in place.

Government programmes are essential, however, in bridging intercultural divides as they combine mentoring, networking and professional support with access to financial capital. This is seen as an important way of addressing commonly cited reasons for Indigenous business failure: a lack of managerial skills, experience, education and deficient capital (Cachon, 2000; Dahiwale, 2007; Furneaux and Brown, 2008; Maritz et al., 2021; Shoebridge et al., 2012; Sullivan and Margaritis, 2000; Zapalska and Brozik, 2017; Zapalska et al., 2003).

As with the literature on government financing, the literature on non-traditional financial solutions is also sparse. Key examples include a 2008 study by Furneaux and Brown (2008) looking at the Family Income Management Scheme, a piloted microfinance tool built around Indigenous Australian family structures and the pooling of local capital, and a 2013 study by Buultjens and Gale (2013) who subjectively argue that venture capital is unsuitable for Australian Indigenous micro-businesses due to unrealistic expectations around short-term returns. Others, however, argue that venture capital can be helpful as it brings much-needed external expertise, including technical and managerial skills, and knowledge of government processes to Indigenous-owned enterprises (Boyd and Trosper, 2010; Logue et al., 2018; Whitford and Ruhanen, 2014).

Finally, recent research by Parhankangas and Colbourne (2023) explores Indigenous crowdfunding campaigns in Canada. They look at 1381 campaigns from 2010 to 2020 and find that, on average, campaigns raise about $4537, with 75% of all campaigns receiving some funding. They categorise campaigns into four key areas: commercial, cultural, community and activism, with practices differing across each regarding the roles of funders and entrepreneurs, degree of reliance on outgroup members, and allocation of benefits.

3.2.4. Theme 4: Financial preferences, decisions and outcomes

The final theme from the literature with meaningful differences between Indigenous and non-Indigenous approaches to financing is a combination of financial preferences, decisions and outcomes. Across the literature, one prevalent theme is that most Indigenous entrepreneurs choose to rely on some form of government support due to barriers to accessing mainstream finance (Ketilson, 2014; Shoebridge et al., 2012; Wood and Davidson, 2011; Zapalska and Brozik, 2017). This suggests a potential difference between the actual financing decisions and the financial preferences of Indigenous entrepreneurs. For example, in a literature review, Wood and Davidson (2011) suggest that self-employed Indigenous females predominantly utilise government finance, followed by personal, and then commercial funding. However, where the entrepreneur’s spouse is non-Indigenous, 95% of those couples choose, and thus prefer, traditional bank-provided debt. Access to capital is a critical marker of business success, with the entrepreneurs in their review tending to operate in the formal sector full-time if they get funding or in the informal sector in a part-time or casual capacity otherwise.

Likewise, Shoebridge et al. (2012) suggest that entrepreneurs choose government funding programmes simply because they believe they have little chance of success when going through traditional funding channels. This is despite participants finding government programme applications confusing, lengthy and frustrating, with the programmes often leading to suboptimal business outcomes. Comparatively, Pinto and Blue (2017), in a case study of the government-supported CAPE programme in Canada, found that although some entrepreneurs were attracted to the CAPE funding model, restrictive access based on business size and length of operation reduces access for those businesses most likely to benefit from this programme.

However, there were some studies which found that there was little uptake of government programmes, with reliance instead on personal networks (Bressler et al., 2014; Dahiwale, 2007; Diochon, 2014; Hunt et al., 2016). Potential reasons include risk aversion, ineligibility due to rigid criteria, and cultural taboo when discussing financing matters with external parties (Diochon, 2014; Hunt et al., 2016).

4. Discussion and research agenda

Despite Indigenous entrepreneurs facing unique intercultural, economic and social challenges, the literature on Indigenous financing lacks theoretical cohesion and direction. Nevertheless, current research shows clear differences between the financing ecosystems facing Indigenous versus non-Indigenous entrepreneurs and clear differences in socioeconomic and cultural approaches to financing that limit Indigenous enterprise growth and development. To advance the study of Indigenous financing, we propose a research agenda organised around the four main themes as informed by the extant literature. We also develop policy recommendations based on our findings.

4.1 A systematic research agenda

4.1.1. Political-economic environment

Within the extant literature, the political-economic environment is seen as being reflective of, and favouring, the dominant culture, with acute flow-on effects for financing (Banerjee and Tedmanson, 2010; Bodle et al., 2018; Brueckner and Spencer, 2014; Buultjens and Gale, 2013; Collins and Norman, 2018; Foley and Hunter, 2013; Henry and Poyser, 2022; Pinto and Blue, 2017). However, other than an appreciation that the environment supporting Indigenous businesses requires a different approach, little is known about designing more appropriate structures that support Indigenous enterprise development. This might include developing standards, frameworks and more equitable tools for assessing socioeconomic and cultural impact, and in developing flexible policy to support a more holistic economy that recognises the different ways in which Indigenous ventures engage with capitalism.

4.1.2. Antecedents to the financing decision

The literature broadly characterises antecedents to the financing decision according to those addressing the demand side (Indigenous entrepreneurs) and supply side (financiers). While there is wider coverage of demand-side factors, our current understanding of which factor(s) are most significant is low and lacking academic rigour. There is also a limited understanding of Indigenous-specific cultural and social demand side aspects such as ownership-related factors (e.g. preferences for financing arrangements) and family-related factors (e.g. family wealth and altruism), despite them being identified as necessary in other disciplines of the entrepreneurial finance literature (Malki et al., 2022). In addition, much less is known about supply-side factors. Future research could expand the coverage of different elements, such as business-related factors, given the identified lack of understanding by financiers of the appropriate scale and types of Indigenous businesses likely to have commercial success (Fuller et al., 2003).

In addition to focusing on overcoming supply and demand-side issues, future research could also investigate ways of working within or around current constraints, including through the use of community collectives focused on community-led development (Bhatt and Qureshi, 2023), or decentralised finance such as crowdfunding (Parhankangas and Colbourne, 2023). This includes looking at ways of helping Indigenous entrepreneurs negotiate their autonomy when confronting external power structures (Bhatt et al., 2024), including those created by a westernised financial system, and research into funding models capable of helping communities create common goods (Bhatt et al., 2023; Mahajan and Qureshi, 2023) as a way of addressing internal and external marginalisation (Bhatt et al., 2024).

4.1.3. Financial solutions

This area is the least understood and is associated with significant research gaps. What is clear is that the myriad of financial products available to Indigenous entrepreneurs represents a significant divergence from traditional financing. Financial solutions also represent the result of a competitive and collaborative intercultural dynamic between the needs of Indigenous entrepreneurs and the wants of westernised governments and financial service providers. Future research could investigate current and emerging funding models and financing solutions available to Indigenous entrepreneurs. This could include mapping and evaluating the available options, investigating the effectiveness and longer-term outcomes of business loan programmes administered by government institutions, understanding the role of intercultural dynamics on financial product offerings and understanding how different financial institutions’ business models and structures support or hinder Indigenous entrepreneurs.

4.1.4. Financial preferences, choices and outcomes

Much of the literature shows clear differences between the financing choices of Indigenous compared to non-Indigenous entrepreneurs. This partially stems from their reliance on government support due to difficulties accessing mainstream finance (Foley, 2006; Ketilson, 2014; Shoebridge et al., 2012; Wood and Davidson, 2011; Zapalska and Brozik, 2017), although it has also been found there has been little uptake of some government programmes due to risk aversion, ineligibility and cultural taboo (Bressler et al., 2014; Dahiwale, 2007; Diochon, 2014; Hunt et al., 2016). However, the literature is generally limited in size and scope, and it does little to tell us about which forms of financing products and government assistance result in optimal business outcomes or why. While recent work in the grey literature shows that Indigenous businesses perform well financially, these results may present an incomplete picture given that the sample relies on registered Indigenous businesses which are more likely to be larger businesses (Polidano et al., 2022). More comprehensive data is needed to measure and track performance to enable a better understanding of a broad range of Indigenous businesses. Future research should also include more methodologically robust and externally valid work looking at business outcomes from different financing decisions while also considering systematic differences between preferences versus choices being made by Indigenous entrepreneurs (Diochon, 2014; Wood and Davidson, 2011). It would also benefit from quantitative (or large-n) outcome studies, including comparative work to consider how outcomes vary based on different choices, jurisdictions, populations and sectors.

4.2 Implications for policy

Governments play a central role in helping Indigenous businesses gain access to affordable and culturally appropriate finance. But this role is complex and involves multiple support mechanisms, the most important of which has historically been as a direct lender to Indigenous businesses (Shoebridge et al., 2012). However, government responsibility goes beyond lending and includes being an enabler of financial opportunity and promoter of private financial markets. Some examples include the provision of treaty payments to eligible organisations in New Zealand (Poyser et al., 2021), by providing seed capital for the Indigenous Finance Corporations in Canada (Ketilson, 2014), and by acting as a loan guarantor for eligible tribes and individuals in the United States (U.S., 2018). Overall, however, our review suggests a lack of academically rigorous evaluations of Indigenous financing programmes. Given this, more research into government-supported financial solutions is needed if we are to improve our understanding of which programmes are working and where, and to scale up successful programmes to help Indigenous enterprises more effectively. Implications for policy makers are also evident in each of the four overarching themes we identify in the literature.

4.2.1. Political-economic environment

One key issue in political economy is the liability of differences facing Indigenous entrepreneurs in accessing financing. Given government’s role in setting the political-economic environment for Indigenous finance access, one specific policy take-away from the literature is the need to reassess how current social, political and cultural differences prevent Indigenous flourishing through finance, and the complex interplay of these factors. The second is a need to reassess how government-funded financial solutions adhere to mainstream versus Indigenous social-economic systems thinking and how that leads to limited impact and limited well-being gains for Indigenous entrepreneurs and communities.

4.2.2. Antecedents to the financing decision

Evidence from the literature suggests that policy makers need to improve the ways they engage with and support Indigenous entrepreneurs in making good financing decisions. This includes looking at ways of helping Indigenous entrepreneurs overcome the myriad of supply and demand-side barriers they face, and evaluating whether current programmes are achieving their stated goals. Policy makers also need to better understand these barriers to help simplify and better tailor existing financial offerings.

4.2.3. Financial solutions

The literature points to issues in how financial products are structured, including those run by government agencies. Evidence supports a role for policy makers in investigating new and non-traditional financing solutions as drivers of Indigenous well-being. These products are worth policy maker attention as they may lead to better goal alignment between financial providers, policy makers and Indigenous enterprises. Within the academic literature, research connecting novel finance to Indigenous welfare is sparse but does include an evaluation of crowdfunding programmes (Parhankangas and Colbourne, 2023) and the use of socially responsible investing (Nikolakis et al., 2014). Within the grey literature, however, much has been written, providing guidance to researchers and policy makers on potential programme interventions. These non-traditional financing solutions are myriad but include community-owned assets (Skudra et al., 2020; Theodos et al., 2021), impact investing (Lacerte and Hunter, 2023; Nous Group, 2017), Indigenous equity investing (CIB, 2023), and through Indigenous social financing intermediaries like the CDFIs in the United States (Dewees and Sarkozy-Banoczy, 2008) and Indigenous Finance Institutions in Canada (Ketilson, 2014; NACCA, 2023).

4.2.4. Financial preferences, choices and outcomes

One implication from the current research is the need to redefine success when designing and implementing Indigenous financing programmes. In particular, the literature shows that narrow western definitions of success can be problematic. And, while financial success does matter to many Indigenous entrepreneurs, understanding what a successful Indigenous financing programme looks like requires taking a multi-dimensional approach to programme evaluation that considers the unique issues and complex decision-making processes that inform Indigenous entrepreneurial decision-making. This could lead to more flexible loan programmes that are better able to measure success in line with Indigenous development and entrepreneurial expectations. Payser et al. (2021) offer one option, which is to take measurement strategies from social impact investing and to use them when designing Indigenous financing programmes. Indeed, given it has been suggested that Indigenous communities are the original social investors (Adamson and Klinger, 2008), learnings from social impact investing measurement are likely already in alignment with the broader goals of Indigenous entrepreneurs. For policy makers, such complexity may require taking a well-being policy approach where a broad range of outcomes, both subjective and objective (Gordon, 2024), are considered when evaluating different financial solutions. This is also closely aligned with the New Zealand well-being budgeting approach, where Māori community health and well-being are explicitly considered during the budgeting process (Mintrom, 2019).

5. Conclusion

Empowering Indigenous communities through entrepreneurialism is touted as key to reducing Indigenous disadvantage, but difficulty accessing finance remains a core and persistent issue. Indigenous communities’ financing needs, processes and outcomes deviate from conventional financing norms and assumptions and therefore requires a more organised interpretation and detailed investigation of the complex intercultural dynamics they face.

This paper systematically reviews the current state of research on Indigenous financing and offers a thematic framework around four key themes: political-economic environment; antecedents to the financing decision; financial solutions; and financial preferences, decisions and outcomes. We find that despite unique intercultural, economic and social challenges in this population, the current literature lacks theoretical cohesion and direction due to the lack of unifying frameworks. To advance the study of Indigenous financing, we propose a research agenda organised around these four themes by mapping current research gaps. We also offer suggestions to guide future research and policy-making. In doing so, we position Indigenous financing as a distinct stream of research, rather than attempting to adapt findings from the conventional literature on entrepreneurial financing.

Key practical and research implications

Footnotes

Appendix 1

Methodologies used.

| Data and methods | Number of studies |

|---|---|

| Methodological approach | |

| Quantitative | 0 |

| Qualitative | 33 |

| Mixed | 2 |

| Quantitative data | |

| Survey | 1 |

| Census data | 1 |

| Qualitative data | |

| Interviews | 16 |

| Theoretical | 4 |

| Case study | 5 |

| Survey | 7 |

| Literature review | 6 |

| Exploratory | 1 |

| Focus groups | 1 |

Some studies used more than one type of data collection technique.

Acknowledgements

The authors are grateful for the support of the Editor-in-Chief of AJM and two anonymous reviewers for their feedback and helpful comments.

Correction (December 2024):

In the published version of this article, the reference “Mahadevan et al. (2023)” was included. However, as the article has since been retracted, both the reference and its citation have been removed.

Final transcript accepted on 11 July 2024 by Andrew Jackson.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the Australian National University’s ASCEND Grand Challenge Project – Australian Social Cohesion, Exploring New Directions.