Abstract

Successful retirement planning critically depends on access to accurate and up-to-date information. In this paper, we focus on the Australian Superannuation industry to examine the influence of digital technology in facilitating communication and information flow among its various actors. Using a qualitative research methodology, we conducted 22 semi-structured interviews with various industry actors including Superfunds, fund members, consultants, IT and digital solutions providers, and representatives from industry regulators. Our findings highlight the need for these actors to enhance their resource and knowledge-sharing capabilities, consumer need recognition, and information flow to ultimately enable Superfund members to improve their retirement planning and financial well-being.

1. Introduction

Retirement planning is as important as ever, with pension reforms placing increased risks and responsibilities onto individuals (OECD, 2020), who need to become more personally involved (Yeung, 2018). Planning for retirement involves individuals making decisions concerning fund selection, risk preferences, insurance, monitoring investment performance, and fee payments (Bateman et al., 2014). Each of these tasks critically depends on individuals having access to accurate and up-to-date information. Despite its importance, limited research has explored the implications of digital technology for the communication of retirement-related information (for exceptions, see e.g., Eberhardt et al., 2020; Hentzen et al., 2022; Pahlevan Sharif and Naghavi, 2020).

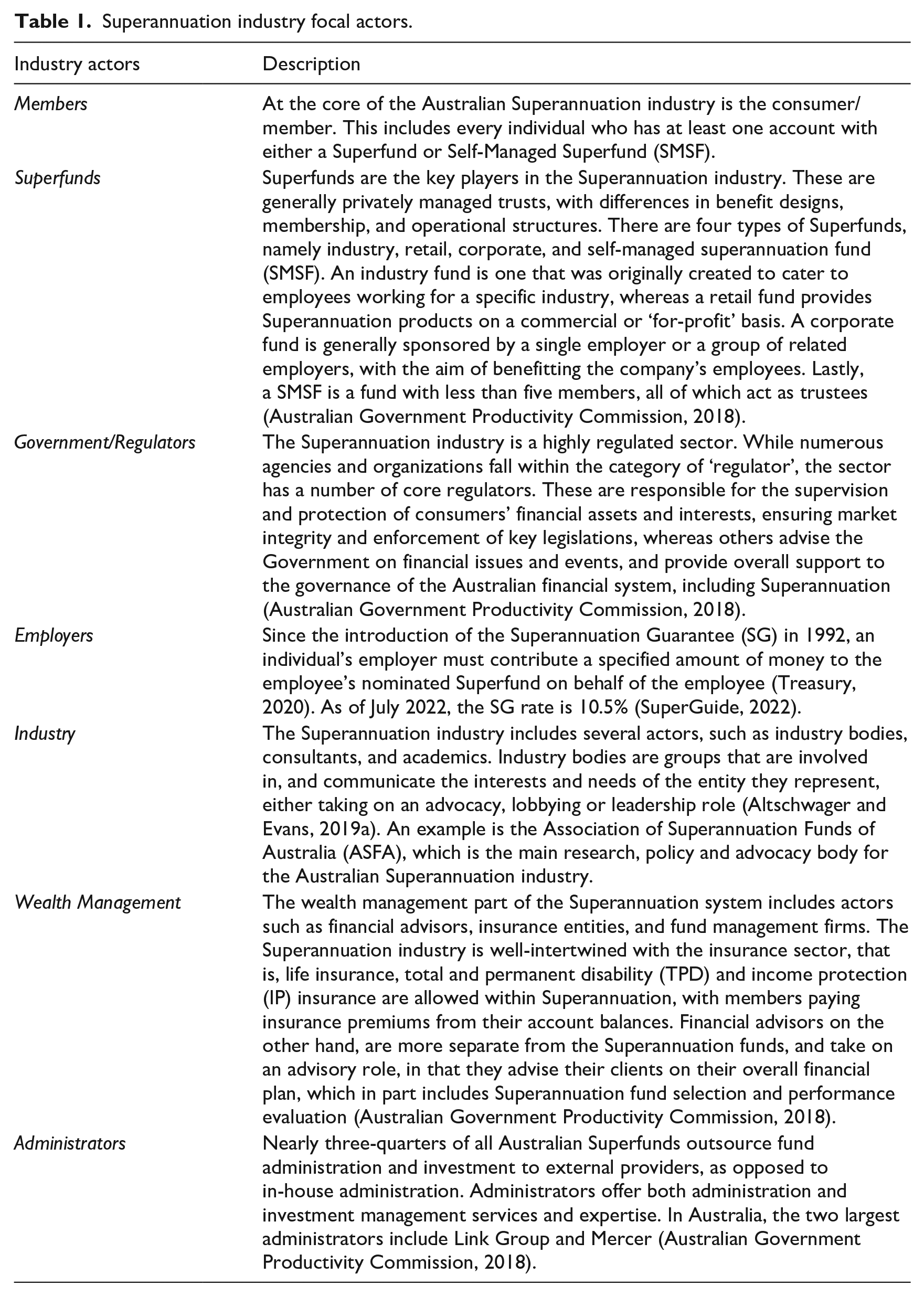

The Australian Superannuation industry provides a rich context for this study, as it lags in digital transformation efforts (ASFA, 2017), and experiences low member engagement due to its long-term nature, as well as its size and complexity (Altschwager and Evans, 2019a). In addition, members often struggle to evaluate investment performance and overall quality of service provided by their Superfunds (Eberhardt et al., 2019), further exemplifying the need to assess the use of digital technology and how that can improve transparency (Lusch and Nambisan, 2015). The focal actors of the Australian Superannuation industry are detailed in Figure 1 and explained in Table 1.

Superannuation industry focal actors.

Information flow among focal actors in the Superannuation industry.

Understanding the separate influences of individual actors in the Australian Superannuation system can potentially aid in a better understanding of different aspects of pension communication and consumer information search (Debets et al., 2022). External influences such as digital technologies also shape the service provider (Lusch and Nambisan, 2015). As such, digital technology can facilitate value co-creation through information provision and access (Nambisan, 2013). Despite digital technologies’ relevance and impact, little is known to date about how it can facilitate information flow and information-seeking behaviour in the retirement planning context.

Our research aims to investigate the effect of digital technology on the Australian Superannuation industry, and its impact on information seeking behaviours and information flow. Therefore, our main research question is: How does digital technology influence the accessibility and flow of information as well as consumer information seeking behaviours within the Australian Superannuation industry? In addressing this research question, we contribute to the limited research exploring individuals’ information search behaviours in the retirement planning context (Eberhardt et al., 2020; Hoffmann and Plotkina, 2020) and the influence of separate industry actors on individuals’ access to important streams of information (e.g. projected living standards, fund performance) (Saghiri et al., 2017).

Our findings show that actors such as Superfunds, fund members, and technology providers differ in their uptake of digital technology and related innovation. Retirement information complexity continues to be a significant factor in increasing member confusion and lack of engagement, further enhanced by a poor digital presence and communication of the industry actors. These findings contribute to the growing interest in digital pension communication (Debets et al., 2022; Eberhardt et al., 2020) and information search (Dahl et al., 2021; Haluza et al., 2017). Our findings also extend the literature on digital information search and information flow (Dahl et al., 2021; Peltier et al., 2020), highlighting opposing views on actor responsibilities, which can negatively affect digital communication efforts. We find that the purpose and role of certain industry actors, such as regulators and Superfunds, are unclear to fund members, negatively affecting trust perceptions and increasing demands for transparency around service provision and communication. In addition, consumers are increasingly engaging in self-servicing behaviours, limiting communication efforts from Superfunds. Changing consumer expectations place increasing pressure on key actors within the Superannuation industry to improve communication, information access, and service value. We demonstrate that views on education, information acquisition, and dissemination differ among consumers and other industry actors. For example, while members look to employers to be educated on Superannuation-related matters, Superfunds perceive themselves to be responsible for increasing members’ knowledge of such issues instead.

2. Background

From a services marketing perspective, service encounters occur between consumers and service providers in dyadic interactions (Ostrom et al., 2015). The accessibility of online service provision has increased drastically, forcing service providers to rethink and change their business models (Kohtamäki et al., 2019; Senyo et al., 2019). Companies (partially) delivering services online can use flexible, accessible, and synchronized systems that facilitate multidirectional information exchanges. The Superannuation industry is complex and involves numerous actors that seek to facilitate the delivery of positive financial outcomes for the consumers. According to Merton (2014), ‘an effective retirement system must guide savers to good retirement outcomes through clear and meaningful communication and simplicity of choices, during both the accumulation phase and the postretirement pay-out phase’ (p. 11). Meanwhile, research on digital pension communication is limited, either taking a consumer/member (Eberhardt et al., 2019, 2020) or Superfund/regulator perspective (Debets et al., 2022), underlining the need for the present research.

2.1. Information flow in the superannuation industry

Without appropriate information, consumers are unable to make informed decisions about how much they should save or invest, what level of risk they should adopt, and when they should retire (Eberhardt et al., 2020). As such, the first step in planning for retirement involves the consumer acquiring relevant and timely information. Digital technology has enabled organizations and institutions to facilitate information creation, dissemination, sharing, and coordination (Larivière et al., 2017; Nambisan, 2013). However, failure to integrate technologies and systems negatively affects the speed and accuracy of information exchanges, limiting inter-actor collaboration and communication (Sklyar et al., 2019a). In addition, while digital technology enables consumers to access vast amounts of information, it can also complicate the information search process as they become increasingly responsible for searching, interpreting, and applying information themselves, affecting their decision-making behaviour and perception of the service provided (Golman et al., 2017).

To date, Superfund communication and subsequent information flow are primarily unidirectional. For example, Superfunds often send quarterly statements to members. This view of Superfund providers as sole information providers facilitates low member involvement in decision-making processes (Ratner et al., 2008). Occasionally, other actors such as governments, consumer advocates, or financial advisors influence the availability and flow of information and overall communication. Unidirectional information flows are ineffective the more complex the information and the lower the knowledge or interest of the consumer (Bateman et al., 2014). Optimal service delivery requires industry actors to engage in bidirectional communication and resource exchange, allowing the service provider to adjust their communication strategies and service offerings to align with changing consumer needs (Gustafsson et al., 2012; Sklyar et al., 2019a). Due to the complex nature of retirement planning, service providers need to help consumers by integrating resources and knowledge exchange through improved information flows (Baccarani and Cassia, 2017). The success of the Australian Superannuation industry in terms of member retirement preparedness will depend on actors’ interaction and subsequent utilization of communication flows to improve the awareness and service experience (Vargo and Lusch, 2016).

2.2. Information seeking and avoidance behaviour

Although various studies have highlighted the importance of information seeking behaviour for improving financial knowledge, decision-making, and financial well-being (Pahlevan Sharif et al., 2020; Pahlevan Sharif and Naghavi, 2020), the topic has not been extensively investigated in the retirement planning literature (Hoffmann and Plotkina, 2020; Sharif et al., 2020). Information can be acquired passively (e.g. an unsolicited service provider email) or actively (e.g. engaging oneself in an Internet search or discussing with one’s personal network) (Sweeney et al., 2010).

Digital technology has enabled consumers to access vast amounts of information, and simultaneously complicated the information search process. Consumers become increasingly responsible for searching for, and interpreting information, which both affects their decision-making behaviour and perception of the service provided to them. To avoid being overwhelmed, consumers may engage in information avoidance behaviours (Golman et al., 2017). Information avoidance refers to an individual’s failure to acquire information, in part, because that information would require them to think about or engage in undesirable activities or experience unpleasant emotions (e.g. thinking about old age and associated health issues) (Sweeney et al., 2010).

3. Method

3.1. Data collection

This study adopts an exploratory qualitative research design using primary data from semi-structured interviews, supplemented with secondary data from publicly available sources, to investigate digital communication and information flow in the Australian Superannuation industry. Secondary data include publications obtained from the Australian government and Superannuation regulators (i.e. Treasury (2020). This publicly available data provide valuable insight into the issues identified by the Australian Government facing the Superannuation industry and is integrated in our qualitative analysis as a background to present our interview findings against.

Regarding the qualitative data collection process, we conducted the interviews in two phases. First, we interview ‘industry experts’, including Superfund managers, technology specialists, and a representative from a regulator. Second, we interview Superfund members. In both instances, interviewees are selected through purposive sampling, which increases the probability of uncovering insights from informed and experienced individuals with knowledge of the focal topic (Gioia et al., 2013). Due to the scope of this study, all participants in the first phase had to work within their organization’s technology department or be employed by a company providing services to the Superannuation sector. As for members, they had to have at least one Superfund account. In total, we interviewed 22 participants resulting in 902 minutes of recorded audio data.

3.1.1. Phase 1

Given the large number of Superfunds (217 as of June 2018; Australian Government Productivity Commission, 2018), the researchers contacted fund managers, including managing directors, heads of member engagement, and digital or technology managers, of the 30 largest Superfunds in Australia, via LinkedIn. While initially the response was slow, after the first two interviews, a snowball approach developed, with participants offering to pass on the project information and researcher contact details to their network and industry colleagues. Throughout the data collection process, we applied the constant comparison method of Shah and Corley (2006), paying close attention to whether each interview contributed new information, stopping when we reached theoretical saturation. To ensure consistency, the same researcher performed all interviews (Turner, 2010), lasting between 30 and 65 minutes each. They were conducted online due to COVID-19 travel restrictions at the time of performing the study. While conducting virtual qualitative research involves methodological and ethical challenges, we sought to ensure we conduct high-quality and rigorous research through careful considerations around recruitment, data collection and analysis (Roberts et al., 2021).

3.1.2. Phase 2

The interviews were conducted either in person or online, lasting between 20 and 42 minutes each. Superfund members’ age ranged between 21 and 50 years, and they were employed in professions ranging from consultant, dietician, secretary, student/university teaching assistant, to engineer. 1 Engagement with their Super savings varied, with some participants being highly engaged, whereas others adopted a ‘set and forget’ approach instead. We had a relatively balanced gender distribution of 5 male and 7 female participants, with half having a diverse immigration background. We thus captured the opinions from interviewees with varying backgrounds, experiences, and engagement (see Table 2).

Interview participants.

3.2. Data analysis

Due to the nature of this study, we draw on the Gioia methodology (Gioia et al., 2013), which recognizes people as knowledgeable agents with the ability to express and discuss their emotions and thoughts, as well as follow an iterative analysis approach as suggested by Pratt et al. (2006). The Gioia methodology comprises of a systematic and inductive approach, aiding in the development of concepts by referencing and drawing on expressed human experiences to develop several code orders, themes, and dimensions. First-order-codes enable the researcher to link the quotes extracted from the interview data to theory, while themes require the researcher to zoom-out, followed by higher level abstraction resulting in aggregate dimensions. To ensure that the data accurately reflected what each participant had said and thus achieved descriptive validity (Maxwell, 1992), all audio recordings were transcribed and coded using the popular NVivo software (version 12).

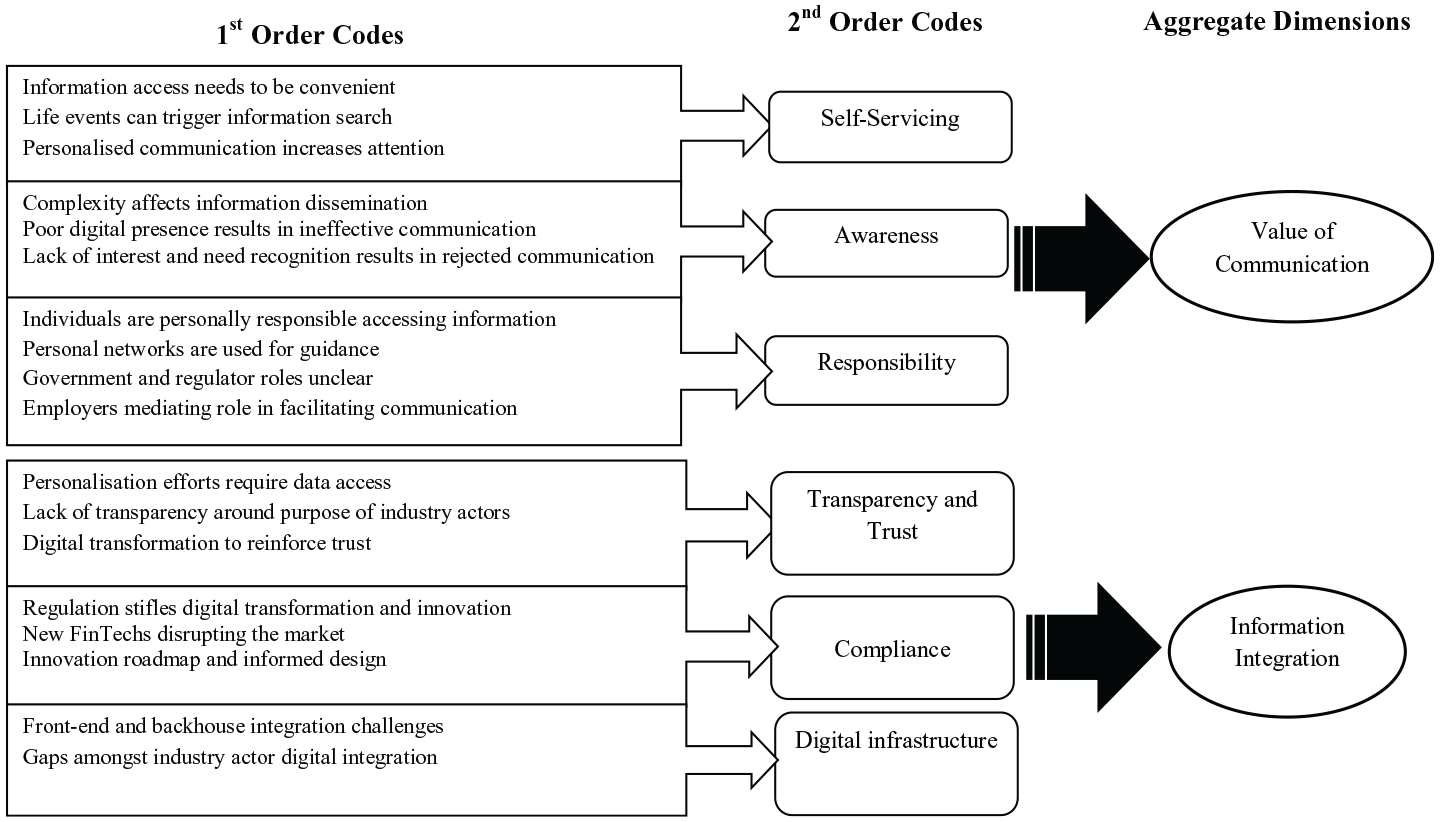

The coding process began with reading all transcripts twice, to get a general understanding and overview of the data and identify broader topics. We then grouped together similar phrases expressed by the interviewees, resulting in an initial grouping of 120 categories, with subsequent re-coding of similar or related categories, reducing the number into 18 first-order codes (Raja et al., 2018). Following axial coding as per the approach of Strauss and Corbin (1998), the first-order codes were systematically examined to uncover relationships among the categories and then grouped into six second-order themes, thus reducing the number of first-order codes to a more manageable quantity (Gioia et al., 2013). Finally, the emerging and overlapping findings informed the final themes (Archibald, 2015) through investigator triangulation, which we then arranged into two aggregate dimensions. See Figure 2 for the coding structure of our study.

Coding structure.

4. Findings and discussion

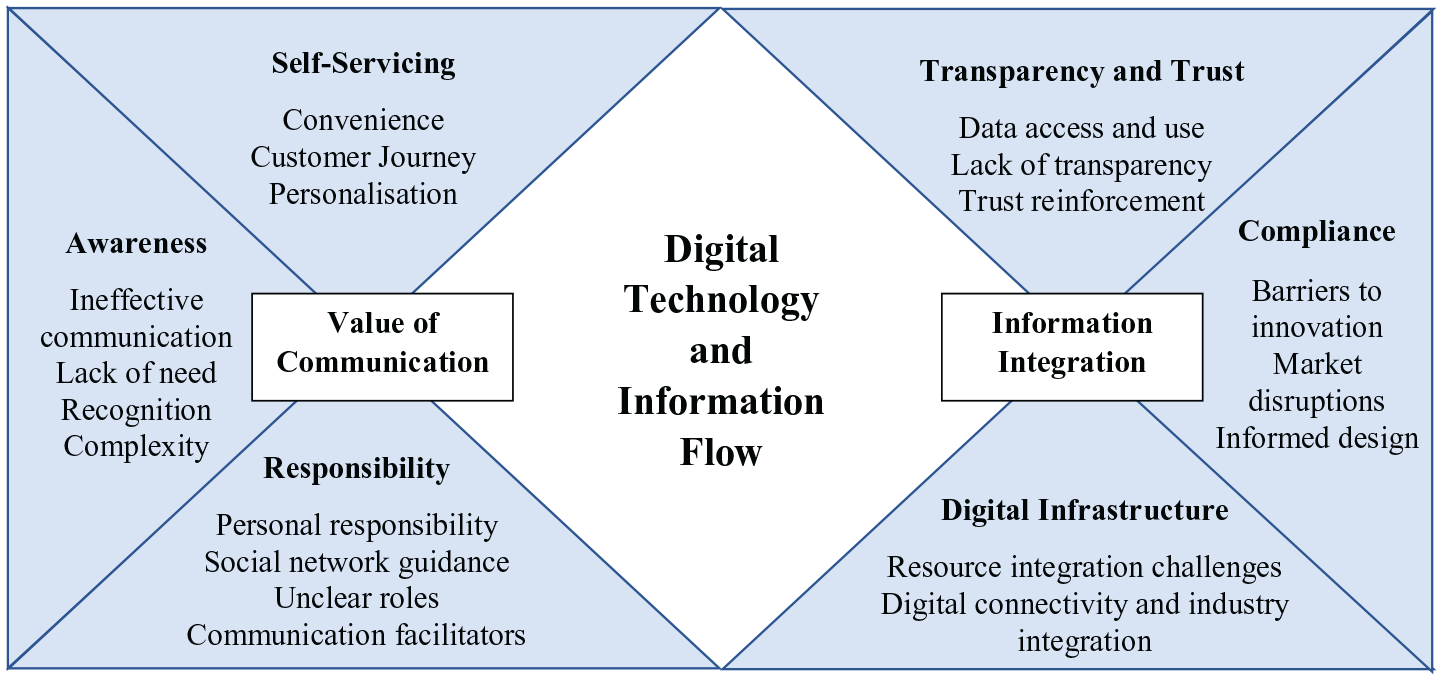

Our study focuses on exploring how digital technology can aid the accessibility and flow of information, as well as enhance collaboration among six key industry actors, including members, their family, friends (social network), and employer(s), Superfunds, regulators, and technology administrators. As such, the following findings highlight consumers’ and service providers’ opinions and perceptions, which ultimately drive their behaviour. While regulators and employers were not interviewed separately, they were included in the conceptual framework as the interviewed members and experts continuously referred to them. In line with (Larivière et al., 2017), who suggest that service providers, technologies, and consumers are vital in creating, disseminating, and sharing information, we identified two dimensions, and six themes within these two dimensions, that illustrate how digital technology influences communication and information flow among actors in the Superannuation industry. The dimensions and corresponding themes are Value of Communication (comprising Self-Servicing, Ignorance, and Responsibility) and Information Integration (comprising Transparency and Trust, Compliance, and Digital Infrastructure). The conceptual framework in Figure 3 summarizes the findings.

Conceptual framework.

4.1. Value of communication

4.1.1. Self-servicing

Due to the consequential nature of financial decision-making (i.e. asset allocation or financial investments), consumers are recommended to seek out professional advice. A recent report from ASIC (2019) revealed that nearly half (41%) of Australians want to get personal financial advice in the future, while 27% have already received financial advice in the past. However, personal financial advice and wealth management are often expensive and exclusive (Van Thiel and Van Raaij, 2017). Easier and faster access to information reduces transaction costs and increases service transparency (Chen et al., 2021; Ding et al., 2007). This ease of access to information has initiated changes in consumer behaviour, one of which is increased self-servicing behavior:

People would like to help themselves first before they go and ask someone else to help them. (Manager - Superfund)

In the context of retirement planning, self-servicing technology facilitates an increased sense of control for the consumer. As our analysis shows, technology can be useful in facilitating decision-making by providing more education options and offering approachable advice, making the retirement planning process more convenient for the consumer. While consumer self-servicing technology should restrict hasty and uninformed behaviour given the consequential nature of retirement planning, it should allow for consumers to self-identify their needs:

There’s a digital transformation happening where services are moving online, where people are getting conditioned to self-diagnose, to self-service. So, you know, if you need to do a transfer in your banking, you’re doing it yourself. You wouldn’t even, [the Millennial] generation wouldn’t even think about going to the bank. (Manager - Superfund)

In addition, due to the long-term nature of retirement planning, communication between the core industry actors (members and Superfunds) is often sporadic. However, the earlier individuals plan for retirement, the better the outcomes generally are Garcia Mata (2021). Superfunds continuously seek to facilitate engagement through ‘journey triggers’. Consumer journey mapping requires tracking the touch points of the consumer-service provider interaction:

So, from your youngest to your oldest, [. . .] you might be getting engaged, getting married, buying a house, or your first child getting ready for retirement. And we use these moments of truth to form trigger journeys. (Manager - Superfund)

While relatively underexplored in the current literature, digital technology can assist service providers in capturing these ‘moments of truth’ or life events. While the interviews revealed that most members want a more personalized retirement management experience, they were unaware of what personalisation entails. In addition, as highlighted in a guide published by the Australian Securities & Investments Commission (ASIC, 2012), service providers must be aware of the type of personalized information that members need. That is, service providers should make a distinction between factual information, personal advice, and general advice. Personalisation provides numerous opportunities and benefits; however, risks such as privacy and security concerns remain a challenge (Chellappa and Sin, 2005).

While personalized communication entails numerous benefits for the member (i.e. education), concerns around the costs and complexity of managing consumer data were raised during the interviews with managers. Additional costs for the service provider include investments in digital technology and data analysis capabilities (Vesanen, 2007). Benefits for members include an improved consumer experience and overall retirement preparedness (Dellaert, 2010; Lloyd, 2020), while service providers may see an increase in consumer satisfaction, consumer loyalty, and competitive advantage (Vesanen, 2007).

4.1.2. Awareness

Complexity of the Australian Superannuation system and information remain key barriers to effective retirement planning. Inter-actor information flows are often interrupted due to members abandoning their information search:

People kind of don’t really, can’t really engage very well with the amount of information that’s out there. There is too much, there’s too many superannuation funds. There’s too many technical terms as a real financial literacy gap between what funds think you should know and what people actually know [. . .]. (Consumer Advocate)

Superfund managers recognized that it is the service providers’ job to simplify information and make it understandable to every consumer. Yet, most acknowledged that their funds still have a long way to go:

That is going to be a key focus of our new program of work, where we’re really starting to transform the digital or [. . .] the experience of our members and the way we communicate is a key component of that. (Manager - Superfund)

4.1.3. Responsibility

Education is an important foundation for effective communication (Eberhardt et al., 2020). However, during the interviews, the question about responsibility regarding the provision of retirement-related education revealed mixed opinions. While some interviewees declared to engage in self-education, others mentioned that they predominantly seek advice from their social network (e.g. a family member):

He (interviewee’s father) bought properties and he also had shares and I think he looked at kind of that long-term investments and he’s always expressed how important superannuation is as well as, making your money work for you, I suppose. (Member - Male Engineer)

While a person’s social network may provide a valuable source of financial education, there are risks of deferring financial decision-making to others (Ward et al., 2019), which could negatively affect the present and future financial well-being of individuals (Netemeyer et al., 2018). Service providers appear to be aware of this happening, and the risks involved:

Defer all that thinking over to your superfund or over to your parents or over to your partner or over to your financial advisor. But to a degree you definitely need to be informed and educated because there is a limit to which you can have someone else make those decisions for you. You can’t just defer all your decisions. (Manager - Superfund)

Members listed their high schools, employers, and the government as actors responsible for the financial education of consumers. Findings from an interview with a senior policy advisor at a regulator corroborated the statements regarding members’ expectations that the government and regulators should be more involved in members’ financial education:

My team, specifically at the moment is doing a program called [. . .], where we’re utilizing behavioural design to design and test interventions that support people and one of our focus areas is how [. . .] might we support people to plan for their future, so retirement and Superannuation and all those [. . .] upstream behaviours and micro decisions that people have to make. (Senior Policy Advisor - Regulator)

Adopting a more critical perspective, one consumer advocate suggested that the Australian government is responsible for fixing the ‘broken’ business model, claiming that Superfunds are too conflicted concerning member engagement. Another interview revealed that most members thought employers could educate employees on superannuation matters, as they are the first direct link between funds and members:

I think I first found out about retirement funds when I started working, I mean, we were immigrants from the States, so I didn’t have a, I didn’t grow up there. [. . .] because like when you earn money and you understand that part of that money goes somewhere else, then you know, your brain will start clicking to it. (Member – Male Accountant)

These views deviate from the (Australian Government Productivity Commission, 2018) key recommendation, which seeks to reduce employer involvement in default fund decision-making. No interviewed member suggested that Superfunds need to educate them on retirement planning matters, which highlights the disconnect between these two actors and the lack of understanding on the member’s side as to the purpose of and services provided by Superfunds. The role and responsibilities of an employer also became evident during the analysis, for example, regarding paying Superannuation into employees’ designated fund. This responsibility, however, can involve challenges:

There’s a huge problem with unpaid Super in our industry. So, and you know, when we did research on our app, you know, the key information that our members wanted to see, was there a balance and their last contribution and what date it was paid. So that’s all they want to see up front. (Manager - Superfund)

Most employers have a default Superfund that they offer to new employees, thus facilitating a continuous influx for the employer-associated Superfunds. Challenges with employer involvement around default fund selection were highlighted in the final report and supplemented documents of the Australian Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (Financial Services Royal Commission, 2018), which suggested that: [. . .] at least to some extent, employers choose a default fund based on relationships with executives and employees of superannuation funds [. . .] evidence suggests that performance of the fund, net benefits to members, and other product features are subsidiary considerations for employers in selecting a default fund, if they are considered at all. (p. 91)

Numerous interviewees stated that they went with their employer’s default Superfund. At the same time, some admitted to having multiple Superfund accounts due to their changing employers over the years, each with different default funds.

While governments and employers are increasingly shifting the risks and responsibilities to the individual (Eberhardt et al., 2020), members appear not fully aware of this shift and its consequences. This stark contrast between members’ responsibility perceptions and service actors’ actual take-up of responsibility highlights a widening gap with potentially severe consequences such as reduced quality of life and well-being during retirement (Australian Government Productivity Commission, 2018; Eberhardt et al., 2020).

4.2. Information integration

Several Superfunds outsource their digital marketing and investment management to external companies such as digital agencies or other third-party vendors due to cost considerations or lack of in-house expertise or required system infrastructure (Treasury, 2020). Consequently, Superfunds are increasingly tasked with enhancing the effectiveness of such industry actors through seamless, efficient, and agile integrations of processes and systems, as well as in contributing to an overall more collaborative information exchange, centred around service provision, relationship building, and value creation (Lloyd, 2020). For example, suppose a digital communication channel is managed by a third-party vendor, and a member reaches out to request specific information. In that case, the vendor must be able to quickly retrieve that information from the Superfund. However, if systems and processes are not integrated, this task might prove complicated and slow, negatively affecting the member’s service experience.

Although value creation comes in different forms (Sweeney et al., 2015), we focus on resource integration. Resource integration includes assembly, mastery, and optimization of resources such as information from multiple industry actors (Bruce et al., 2019). Service providers such as Superfunds and government institutions can help individuals by integrating their resources (i.e. digital channels or member information) and facilitating continuous information flow. Sklyar et al. (2019a) suggest that the more strongly industry actors are connected, the more trusting and collaborative action in efficient and effective resource integration will occur. Extending these findings, we highlight the importance of transparency and trust, compliance, and overall digital infrastructure as key determinants of successful Superannuation service integration, while acknowledging that digital systems can help, but are not a cure-all.

4.2.1. Transparency and trust

For effective communication and information exchange, industry actors need to integrate their systems digitally. Trust is important to drive efficient and effective multi-actor information sharing and collaboration, reduce transaction costs, and increase flexibility in changing market conditions (Delina et al., 2012). As a precursor to trust (Busser and Shulga, 2019), the importance of transparency has increased through the proliferation of the Internet (Hanna et al., 2019). In terms of transparency, members can now access retirement information via different channels and sources:

[Members] want to do it [communicate] through a channel where they already were as well. So, like they didn’t want to have to necessarily engage with the fund via say a different platform, [. . .], if we can engage through the MyGov platform, that’s probably like a, was a place where we’re at already. Just makes it kind of life admin of it all so much easier rather than say having to remember login details for a superannuation fund, have a separate app or do something like that. (Consumer Advocate)

Service providers need to ensure that information is available from multiple sources. Doing so raises the issue of resource integration. Well-connected industry actors integrate more resources faster than those with weaker ties (Sklyar et al., 2019a), corroborating Superfund manager statements on attempting to consolidate information and having a ‘single source of truth’. Different member-facing actors need to tell the same story and provide the same, consistent, and regulatory-compliant information, as illustrated by this statement from a Superfund manager:

Actually, I quite like that idea. Because I come on the myGov um, website. Um, so I like the fact that I can get into the ATO through that. So, you know, if, Super might even be in there, I don’t know. But [. . .] I think if there was a one-stop shop that can tap into all of the different organizations yes. I like that idea. (Manager - Superfund)

While personalisation has been identified as an opportunity to improve communication (e.g. between Superfunds and their members), our analysis revealed a lack of transparency of the industry and the available information as potential barriers to such personalisation. That is, while Superfunds believe that their organizational purpose is to act in the members’ best interest, members perceive (their) Superfunds as simply being another profit-oriented organization:

I think, because it’s like a, uh, it’s like an organization, like any other, I think their best interest is their own profitability and their own, they’re responsible to their own stakeholders. (Member – Female Dietician)

Regulators are aware of the challenge surrounding members’ trust towards their Superfunds:

I think that one of the challenges that the Superannuation funds have, which is not unique to them, but you know, to the whole financial services industry, is the lack of trust that people have. So it’s probably higher trust in workplaces and the government to provide impartial information that they [members] are seeking versus [. . .] their Superannuation company who might have like an ulterior motive. (Senior Policy Advisor - Regulator)

These conflicting views on the service provider’s purpose may be attributed to a lack of transparency and members’ understanding of the functioning of the Superannuation system. Our analysis revealed that system and information complexity was associated with members either not searching for information, not knowing where to search, or giving up their search after a short time due to multiple frustrations.

Our analysis also revealed that while most members initially use the Internet for information search, complexity remains. As highlighted by the Australian Government Productivity Commission (2018), regulators play an increasing role in enhancing transparency and reducing complexity of information. Digital technology can increase information transparency and thus set the foundation for inter-actor trust development (Venkatesh et al., 2016). In addition, as highlighted in the Retirement Income Review by the Treasury (2020), digital technology can assist in providing members with more efficient and affordable financial advice. However, the review also highlighted numerous barriers, such as limited retirement advice tools, lack of trust regarding digital advice, lack of member willingness to pay for digital advice, and regulation.

4.2.2. Compliance

Due to the critical and financially sensitive nature of the Superannuation industry, and to protect consumers from risk such as the misappropriation of retirement savings, Superfunds and Digital/IT providers need to report to and comply with rules and legislations determined by various regulators. During the interview process, it became evident that although most Superfund managers viewed the regulations as necessary, they did highlight some challenges regarding digital transformation and member engagement:

[. . .] the pressure from the regulators definitely comes on us. There is a way of tackling it, which, we really try to handle the pressure. Why the pressure works negatively for the Superannuation sector is that a compliance person says, well, we’ve got this regulation here and you have to say this. Now a compliance person is not a copywriter. It is not their job to engage people. (IT/ Digital Solutions Provider)

We find that Superfund managers and Digital/IT providers view regulation as barriers to innovation, with most resources being allocated to implementing new regulatory changes. With the continuous influx of new regulation, many managers postpone committing further resources to develop digital technology to not risk spending members’ money on something that regulation wants changed within a few months:

And so that’s another way that the regulation or the potential for regulation impacts us as industry and impacts our digital assets. Because people will steer away from things. [. . .]. And we have enough on our plates to keep us up just to keep us up to date with changing regulation rather than to be concerning or considering how products might need to evolve because of regulation moving forward. (Manager -Superfund)

Our analysis suggests that Superfunds perceive a lack of collaboration and communication among themselves and regulators. While regulation is said to stifle innovation and digital transformation, competitors such as emerging FinTechs companies appear to have surpassed traditional Superfunds regarding communication and engagement efforts with consumers. Although these organizations can offer great user experience and education, expert opinion highlights a lack of true holistic disruption to the Superannuation industry (Stevens, 2017). We also find that while several interviewees stated that regulators hinder innovation, the interview with Senior Policy Advisor from the regulator revealed that these organizations and the government as a whole have been impacted by digital technology already, which leads to the question of who or what is the actual barrier to digital innovation in the Superannuation industry?

So, a lot of our work is sort of transformed, [. . .] from face to face or like hard or physical resources like pamphlets and onto sort of online resources, online tools [. . .] and sort of the whole government itself has had a huge significant push to that, and indeed [. . .] utilizing data. (Senior Policy Advisor -Regulator)

Interviewed managers acknowledged that FinTech competitors and other industries condition consumers and create demand for digital communication and information access. That is, FinTechs appear to have enhanced the Australian Superannuation value chain, as opposed to the anticipated disruption (Stevens, 2017). It is the regulators’ responsibility to collaborate with other service industry actors to ensure that innovative ideas that can benefit consumers are not blocked by unnecessary regulation. However, regulators should also act with caution, to not overlook important aspects of consumer protection.

4.2.3. Digital Infrastructure

According to Peltier et al. (2020) ‘inter-actor communication encounters are key mechanisms that turn information reciprocity and collaboration into value co-creation of service innovations’ (p. 726). For collaboration and value co-creation to occur, industry actors must be digitally interlinked. While initial steps have been taken to facilitate such linking, our analysis revealed some shortcomings. One interviewed digital agency manager said that as a $3 trillion industry, he expected Superannuation:

to be reasonably [. . .] technologically advanced and it certainly isn’t, sort of the back end isn’t. You know, it’s an industry that’s run on Excel spreadsheets which really limited our ability to be able to build, [. . .] real-time applications.

This issue is not new to the Superannuation sector. In fact, following a review of the Super system in 2010 (i.e. the Cooper Review), the ‘SuperStream’ programme was introduced to modernize and automate data processing and transactions in the Super system (ATO, 2019). However, 12 years after the release of the Cooper Review, efficient system integration in the industry remains a work in progress. Information and data need to be passed from the fund to the IT provider and back-office. While most funds deal with multiple administrators, this disconnect has stimulated some Superfunds to ‘insource’ their administration back to their own firm:

And the biggest issue is [. . .], there’s about for [every] superannuation fund that outsources, there’s at least five entities involved in your fund. Your trustee, your administrator, your insurer providing life insurance. And then the custodian, which is the one that actually holds the money and manages that. And they’ve all got different systems, often multiple different systems. (Manager–Superfund)

Yet superfunds don’t just need to be connected to administrators, they also need to be linked with other industry actors such as regulators and employers. Apart from increased efficiency and reduced transactional cost, linking industry actors also helps ensure that each actor involved in the service provision has access to the same view of the consumer (Sklyar et al., 2019a).

5. Contribution and implications

5.1. Theoretical contributions

We make several contributions to research. First, in terms of adding to the digital information search literature (Dahl et al., 2021; Haluza et al., 2017), we highlight the effect of information complexity on information search behaviour and how poor utilization of digital technology can further widen the retirement preparedness gap. Consumers, unaware of their increased personal responsibility, either fail to search for information due to lacking need recognition or active avoidance. Others may give up the search due to information complexity. Consequently, service providers perceive low consumer involvement and as a result may reduce digital communication efforts.

Second, we demonstrate that opposing views and expectations of industry actors regarding responsibility for information search and dissemination affect both the perceived value of communication and industry integration efforts. Service provider engagement depends largely on inter-actor relationships and the ability and willingness of actors to integrate resources and facilitate information exchanges (Chandler and Lusch, 2015). Failure to successfully integrate resources and systems negatively affects the effectiveness and performance of the service provider and is thus a substantial concern (Vargo and Lusch, 2016).

Third, we add to research on digital information flow (e.g. Peltier et al. (2020). It is important to compare multiple viewpoints, moving beyond investigations of the dyadic relationship between the service provider and consumer and accounting for consumers’ numerous information sources. Our findings on digital information flow offer insights on how digital technology impacts the complex Superannuation industry. Information flows are affected by industry integration efforts, which in turn are impacted by regulatory compliance challenges.

Finally, we find that seamless resource integration and exchange among Superannuation industry actors facilitated through digital technologies is still in its infancy. Needed collaboration among actors to integrate through digital technology is lacking and the actors’ failure to collaborate has resulted in inefficient use of digital technology. As a result, conflicting information is communicated to Superfund members, which can increase their perception of information complexity and eventually fuel active information avoidance (Sweeney et al., 2010).

5.2. Practical implications

Our findings have several implications for practitioners. First, it is critical that service providers such as Superfunds, regulatory bodies, and digital agencies within the Australian Superannuation industry increase collaboration and integration efforts to improve back-office efficiency and enhance consumer service experience and outcomes (Sklyar et al., 2019a). Especially in retirement planning, improved consumer outcomes and service quality are important, as failure to deliver implies that members will not have sufficient savings to fund their retirement, negatively affecting their future (financial) well-being (Sorgente and Lanz, 2017). For example, the ATO Superannuation dashboard needs to accurately represent members’ savings balance, which it currently often does not. Digital technology needs to be the foundation of collaboration, with actors having to decide on what information is relevant to members, what information can be personalized, and what information members search for and where. Superfunds should invest in data capturing and analysis capabilities to enhance their personalisation efforts.

Second, through resource integration, actors providing Superannuation services have the chance to enhance transparency and build trust within the Superannuation industry (Sklyar et al., 2019a). Members will benefit from increased transparency around fees and fund performance to be better equipped to make informed decisions. Regulators may wish to consider where members go for information about Superfund performance and improve the communication on those platforms. Regulators should also have a greater understanding of innovation efforts and increase collaboration with Superfunds instead of maintaining their current restrictive approach.

Third, Superfunds are advised to analyse the effectiveness of their communication strategies. Suppose members avoid information sent by their Superfund and instead search for information from other sources, some of which may be incomplete or false. In that case, the Superfund will likely still be held responsible. Failure to engage consumers in retirement planning will fall back onto the service providers and affect members’ future financial well-being. As such, we suggest that Superfund managers increase their efforts to utilize digital technology, big data, and consumer journey mapping to build stronger and more engaged relationships to enhance the overall member experience.

Finally, from a public policy perspective, regulators need to find a balance in their mandate between stifling innovation to protect consumers versus encouraging innovation so that firms can develop a better consumer experience (Australian Government Productivity Commission, 2018). Regulators should not seek to primarily introduce regulation, but instead, work together with Superfunds to uncover the underlying reasons for when members encounter problems. Since the cost of uninformed members eventually falls on taxpayers, increasing information access and facilitating information flow in the service industry needs to be encouraged (Feltus et al., 2017).

5.3. Limitations and future research

Despite its contributions and implications, our study has some limitations, which offer promising pathways for future research. First, due to the size and complexity of the Australian Superannuation industry, this study focuses on member and Superfund manager interviews, with a few exceptions (i.e. Superannuation consultant, regulator, consumer advocate, and IT/digital solutions providers). Future researchers may want to build on our findings and investigate the role and responsibilities of other focal industry actors (i.e. additional regulators, industry bodies, financial planners, or employers) in the digitalization of the Australian Superannuation industry. That is, future research may adopt a more holistic, multi-actor ecosystem lens to investigate how individuals engage in the retirement industry. The service ecosystem perspective seeks to emphasize the dynamic and contextual interactions between ecosystem actors (Sklyar et al., 2019b). Adopting this perspective will also allow consideration of the plethora of drivers affecting service delivery, quality, and overall value of the service exchange (Edvardsson et al., 2011). In addition, while we attempted to compare consumers’ perceptions of their Superfund with the managers’ perceptions of the same Superfunds referenced by the members, ensuring this overlap of data proved challenging due to the limited response from Superfunds to our interview invitations.

Second, while we are among the first to explore digital communication and information flow in the Australian Superannuation industry, further investigation is needed. In particular, consumer journey mapping research is still in its infancy, with little empirical work focused on the consumer journey and consumer experience (Lemon and Verhoef, 2016). Future research may want to investigate how journey mapping and event triggers can facilitate long-term financial planning behaviour (Altschwager and Evans, 2019b) and the role of data in enabling journey mapping (Micheaux and Bosio, 2019). In addition, future research may investigate how omni-channel communication can benefit or hinder information flow within a complex multi-actor ecosystem.

Third, while the researchers reached theoretical saturation during the interview process, the limited number of interview participants still poses a limitation of the current study. Additional qualitative research is needed to account for other industry actors’ perspectives, which we were unable to interview. A quantitative research study using a survey may be suitable to contrast the perspectives of consumers and those of their respective Superfunds. That is, future research may wish to focus more on this interesting aspect and investigate how Superfund managers’ perceptions around member needs differ or align with members’ perceptions and needs.

Finally, an interviewed Superfund manager asked, ‘What do people want from a digitally enabled Superfund?’ While ample research has focused on identifying factors encouraging or preventing consumer retirement planning and engagement with retirement savings, the attention has recently shifted towards exploring the role of digital technology in this regard (Hentzen et al., 2022; Hoffmann and Otteby, 2018). We therefore suggest researchers conduct qualitative and quantitative studies to uncover the needs and wants of consumers, with a specific focus on digital technology and credence services such as Superannuation.

Despite these limitations, ours is the first study to investigate the important role of digital technology in the communication and information flow in the Australian Superannuation industry, thereby making both contributions to theory and practice.

Footnotes

Acknowledgements

The authors thank the Associate Editor, Dr. Nitika Garg, and two anonymous reviewers for comments that improved the manuscript. The authors also thank attendants of the 2021 Research Camp of the Marketing Discipline at the University of Adelaide Business School for helpful feedback.

Final transcript accepted on 30 March 2023 by Nitika Garg (AE Marketing).

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.