Abstract

In this paper we investigate what determines access to banking in Central and Eastern Europe (CEE). The research uses different waves of the OeNB Euro Survey – covering over 91,000 individuals during the period 2012–2020 – and pooled and multilevel logit models to analyse how the interplay of trust in institutions, socio-economic attributes and geographic contexts shapes access to bank accounts, savings deposits and loans across 10 CEE countries. The findings reveal significant disparities in banking inclusion across products: while institutional trust enhances access to current accounts and savings deposits, its impact on loans is weaker. Socio-economic factors and geographical contexts, particularly at the local NUTS3 level, also matter enormously for financial inclusion. National and local economic conditions are key in shaping variations in financial inclusion/exclusion across CEE.

Keywords

Introduction

Access to banking services still represents a formidable challenge across Central and Eastern Europe (CEE). In rural areas especially, the absence of nearby financial institutions creates ‘banking deserts’, where the basic infrastructure for formal banking is inaccessible. This lack of access disproportionately affects marginalised groups, including low-income and minority communities and contributes to broader socio-economic exclusion.

For many in these regions, formal banking is not merely an inconvenience. It is an unfulfilled promise of economic inclusion and stability. Compounding this is a deep-rooted mistrust of financial institutions, which persists even decades after the transition from real socialist economies to market-based systems. Experiences of hyperinflation, banking crises and policy failures have left an indelible mark, with many opting to keep their money ‘under the mattress’ rather than risk engaging with institutions they perceive as unreliable, exploitative or both (Gardo and Martin, 2010).

The pursuit of financial inclusion across a landscape scarred by mistrust deserves closer examination. Like a double-edged sword, expanding access to banking cuts both ways. Bringing previously excluded populations into the financial fold offers undeniable benefits. However, it simultaneously opens Pandora’s box of new vulnerabilities.

Consider the credit conundrum: easier access often leads vulnerable households down a slippery slope of mounting debt, with complex financial products bewildering those lacking financial literacy. This creeping financialisation of everyday life can transform promised liberation into economic precarity (Corrado and Corrado, 2015; Stenning et al., 2010). The digital revolution in banking presents a similar paradox. Banking apps and online services may reach remote villages, yet they construct invisible barriers for the elderly, the poor and the technologically uninitiated.

Yet we cannot dismiss the transformative potential of financial inclusion. Access to formal banking remains fundamental to both personal advancement and broader societal development. The challenge, then, lies not in whether to expand financial services, but in how to do so whilst simultaneously strengthening consumer protections and financial education. The path forward requires not blind expansion, but thoughtful balance.

Overall, despite the widespread transformation of CEE’s financial landscape since the fall of communism, access to banking remains strikingly uneven. Over the past three decades, state-dominated banking systems have given way to competitive markets through privatisation, regulatory reforms and the entry of foreign banks, primarily from Western Europe (Barisitz, 2007). These developments have brought stability and modernisation, yet their benefits have largely accrued to the inhabitants of urban centres, leaving rural areas and economically disadvantaged populations behind. This urban-centric focus reinforces disparities, creating barriers to financial literacy, inclusion and wealth accumulation (Dunham, 2019; Hegerty, 2020). Although foreign banks have contributed to diversify financial services, they often prioritise operations in profitable urban markets, exacerbating the challenges faced by residents living elsewhere in CEE countries.

Why does this imbalance persist? And what are its broader implications? For individuals, exclusion from formal banking restricts access to credit, savings mechanisms, and pathways to economic mobility. At the societal level, it entrenches inequality and thwarts efforts to promote inclusive growth. While much of the existing research highlights individual-level determinants – such as gender (Demirguc-Kunt et al., 2019; Morsy and Youssef, 2017), income (Barr, 2005; Blank and Barr, 2009; Seidman et al., 2005), education (Lusardi and Mitchell, 2014; OECD, 2016) and employment status – these alone cannot fully account for the deep-seated disparities in financial inclusion across the region. Instead, a more comprehensive approach is required to understand the systemic and contextual factors that sustain these inequalities.

Two underexplored dimensions – institutional trust and geography – are key to grasping these patterns. Low trust in domestic and foreign banks, governments and other institutions discourages engagement with formal financial systems, reflecting both historical grievances and ongoing perceptions of inadequacy (Gardo and Martin, 2010). This scepticism, rooted in the region’s communist past and subsequent economic crises, continues to shape financial behaviours, particularly among low-income households.

Geography further complicates this picture. Local economic conditions, regulatory environments and regional disparities in infrastructure significantly affect the availability and accessibility of banking services. Regulatory reforms and foreign investment may have modernised financial systems, but they have also cemented inequalities by prioritising urban markets at the expense of rural and peripheral regions.

Our research seeks to address these issues by examining the interplay of institutional trust, individual socio-economic characteristics and geography in shaping access to banking in CEE. The analysis is guided by three key questions: First, how does trust in institutions influence an individual’s likelihood of engaging with formal banking? We posit that higher levels of societal trust can increase the likelihood of holding bank accounts, savings deposits and loans, as trust facilitates confidence in financial systems and reduces perceived risks. Second, how does institutional trust interact with personal characteristics such as education, income, and employment to shape financial inclusion? While trust in institutions can facilitate access to banking, its impact is likely moderated by socio-economic attributes and broader systemic conditions. Third, how do different geographic contexts – local, regional and national – determine banking access, and how do these contexts intersect with individual characteristics? Disparities in the place people live, including urban-rural divides and regional economic differences, can, to a considerable extent, shape access to financial services, with wealthier and more developed regions offering greater opportunities for banking engagement.

These questions are particularly salient in the context of CEE, where the legacy of communism and subsequent market transitions have created unique dynamics of financial inclusion and exclusion. While regulatory reforms and foreign investment have diversified and expanded financial markets, they have also introduced new challenges, including the uneven distribution of banking services and persistent mistrust in financial institutions. By investigating these dimensions, we aim to contribute to (and fill gaps in) existing knowledge on financial inclusion in post-socialist contexts, providing insights into how systemic and individual factors interact to shape access to banking.

The structure of this paper is as follows: the next section reviews what scholarly research has said so far on banking access and financial inclusion, with a focus on the CEE region. This is followed by an outline of the data and methodology employed in the study. The findings are then presented and discussed, with particular attention to their implications for enhancing banking access, especially for underserved populations. Finally, the paper concludes with a recap of the main results and recommendations for policymakers and practitioners seeking to bridge gaps in financial inclusion across CEE.

What determines access to banking?

Why is there financial inclusion/exclusion?

Banking access and financial inclusion/exclusion are closely intertwined but distinct concepts. Access to banking refers to the ability of individuals to use services provided by formal financial institutions, encompassing savings, credit, insurance and payment systems. Financial inclusion/exclusion, by contrast, represents a more comprehensive framework that not only ensures access but also prioritises the effective use of financial services to unlock economic opportunities and improve quality of life (Birkenmaier et al., 2019; World Bank, 2023). Both concepts matter to achieving socio-economic stability, yet they address different aspects of financial engagement. Banking access hinges on the physical and digital infrastructure of financial institutions, whereas financial inclusion/exclusion depends on individual capabilities, such as financial literacy, to translate access into meaningful economic benefits (Birkenmaier et al., 2019; Garg, 2024; Teker et al., 2023; World Bank, 2023).

The dimensions of financial inclusion/exclusion extend well beyond service availability. Research identifies three interrelated components essential for effective inclusion: institutional accessibility, service appropriateness and user capability (Demirguc-Kunt et al., 2019; Wang and Guan, 2017; World Bank, 2023). Institutional accessibility ensures that banking services are within reach of the population, particularly for vulnerable groups (Pardue and Shelton, 2025). Service appropriateness highlights the necessity of tailoring financial products to meet the specific needs of different demographic segments, such as women, low-income households and rural communities (Demirguc-Kunt et al., 2019; OECD, 2016; United Nations, 2021). Lastly, user capability emphasises the importance of equipping individuals with the knowledge and skills required to find their way effectively in financial systems. In this regard, financial literacy emerges as a cornerstone of inclusion, serving as a bridge between availability and usability of services (Birkenmaier et al., 2019; Garg, 2024).

Traditional bank branches remain key to financial inclusion (Bramley and Besemer, 2017), but the rise of digital technologies has added new dimensions to this phenomenon. Digital financial services, particularly those driven by fintech innovations, offer opportunities to overcome geographical barriers and enhance access for underserved populations (Alexander, 2021; Friedline et al., 2020). Mobile banking applications, for example, expand the reach of financial services to remote areas, enabling individuals to conduct transactions without the need for physical branches (Afjal, 2023; Faust et al., 2023).

Yet, digital solutions are not without challenges (Drugă, 2024). The so-called ‘digital divide’ continues to threaten equitable access to banking, as disparities in technology adoption and internet connectivity persist. Many individuals, particularly those in low-income or rural areas, lack the resources or digital literacy necessary to engage with online banking platforms (Manta et al., 2023). Mobile banking is also accelerating the closure of physical branches in less profitable areas for banking. This process is pushing individuals in peripheral and/or remote areas onto digital platforms that many cannot navigate (Arroyo-Menéndez et al., 2022; Goedhart et al., 2022).

Therefore, the potential for mobile banking to bridge accessibility gaps is important yet it comes with challenges. The discourse on digital financial inclusion reveals a complex terrain where technological innovation intersects with social vulnerability (Oliinyk, 2024). Kossecki and Borcuch (2014) further underscore this dynamic, highlighting how rural, elderly and low-income populations face significant challenges in coping with increasingly complex digital financial systems. Without targeted interventions, these barriers risk transforming traditional exclusion into new, technology-driven inequities (Ishmuradova et al., 2024). Such risks highlight the complexity of digital financial inclusion, where the promise of innovation must be balanced against the realities of unequal access to technology and education.

As formal banking services remain inaccessible to many, alternative financial systems have emerged to fill these gaps. In CEE countries, financial exclusion has fostered a diverse landscape of alternative financial services, such as payday lenders, pawnbrokers and informal lending networks. Pawnshops have experienced revitalisation in post-socialist economies, while informal community-based lending networks remain particularly important in rural areas and among ethnic minorities (Gosztonyi and Havran, 2022). Other alternatives include non-bank financial institutions, app-based microloans and short-term consumer credit. These services have expanded rapidly, exploiting regulatory loopholes and targeting consumers with limited access to mainstream credit (Apostoaiei and Bilan, 2019; Baicu, 2019). While they may offer short-term solutions, they are frequently associated with high interest rates, lack of transparency, aggressive collection practices and a rise in household over-indebtedness, all contributing to overall wellbeing deterioration (Kojouharov and Rusev, 2016; Stenning et al., 2010; Tofan et al., 2019).

Institutional trust adds another layer of complexity, particularly in its role as both a driver and inhibitor of financial inclusion/exclusion. On the whole, institutional trust is central for economic development and the success of institutions depends on their legitimacy and capacity to implement policies, particularly in regions with a history of political and economic instability (Rodríguez-Pose and Ganau, 2022; Rodríguez-Pose and Ketterer, 2020). Muringani et al. (2024) further underscore the critical role of political trust in fostering regional economic development, arguing that trust mediates the relationship between social capital, governance quality and economic performance. They emphasise the need for institutional reforms to promote inclusive growth.

More specifically, trust in financial institutions can facilitate engagement, increasing confidence in the reliability and security of banking services. Conversely, mistrust acts as a barrier, deterring individuals from participating in formal financial systems (Buriak et al., 2019; Wang and Guan, 2017; Xu, 2020) and limiting access to credit (Rodríguez-Pose et al., 2021). This dynamic is especially significant for vulnerable populations, who often face additional layers of economic and social insecurity (de la Cuesta-González et al., 2021; Ferretti, 2018; Friedline, 2021; Pardue and Shelton, 2025).

In CEE, where historical legacies continue to shape perceptions of institutional reliability, the trust factor is particularly salient. The region’s communist past has left a lingering scepticism towards state-controlled systems and, by extension, formal financial institutions (Boda and Medve-Bálint, 2014; Sojka, 2015). Institutional trust in CEE is shaped by both individual-level factors, such as income and education and macro-level factors, including economic performance (Medve-Bálint and Boda, 2014). Addressing these trust barriers is as critical as enhancing physical and digital access to banking. Indeed, the advent of digital banking may further complicate trust-building efforts, as individuals unfamiliar with or wary of technology perceive additional risks in adopting these platforms (Ferretti, 2018).

The dynamics of banking digitalisation are therefore contributing to the persistence of ‘banking deserts’ in CEE, which disproportionately affect low-income and minority communities, reinforcing patterns of geographic and financial exclusion (Hegerty, 2020; Langford et al., 2024). Overcoming such barriers requires not only technological innovation but also concerted efforts to rebuild trust through transparent practices, consumer education and culturally sensitive policies (Birkenmaier and Huang, 2024).

The geography of banking access across CEE reveals considerable spatial inequalities, mirroring the broader contours of uneven development that have characterised post-socialist transformation. This territorial dimension adds complexity to understanding financial inclusion and exclusion.

Sokol (2017) positions post-socialist countries as distinctive laboratories for observing finance’s transformative impact on socio-economic landscapes. These nations have become stages for a new financial geography, with Western institutions assuming dominant roles in previously state-controlled economies. Within this framework, Gál (2015) identifies the emergence of ‘dual-banking systems’ fostered by financial sector foreign direct investment. The banking sector is carved between large international banks and smaller domestic institutions, a condition that reinforces spatially uneven financial development. These geographical imbalances manifest through pronounced centre-periphery dynamics. Regional banking centres like Vienna function as financial gateways to Eastern markets, exercising considerable control over CEE banking sectors through elaborate parent-subsidiary networks.

At more localised scales, Stenning et al. (2010) document how everyday financial practices are embedded within spatially differentiated landscapes, where access to formal banking services remains heavily influenced by location and sustained by enduring informal networks.

Such patterns are not merely localised anomalies but reflect deeper structural asymmetries within the broader European financial architecture. Capital typically flows from peripheral to core regions, thereby intensifying rather than alleviating regional inequalities. Recognising these geographical dimensions is essential for effectively addressing both financial exclusion and uneven development in CEE countries. These spatial patterns continue to bear the imprint of post-socialist transitions (Smith and Timár, 2010), with significant and persistent implications for regional inequality and economic resilience (Beckmann et al., 2018; Gál, 2004).

By examining the interplay between institutional trust, digital transformation and traditional banking systems, we aim to contribute to a more holistic understanding of financial inclusion. In CEE, where exclusion is often rooted in both structural inequalities and individual mistrust, these dimensions are inextricably linked, forming the foundation for targeted interventions to promote equitable access.

Banking access and institutional trust in CEE

Since the fall of communism, the banking sector in CEE has undergone dramatic changes. State-controlled systems have given way to diversified and competitive financial markets. This transition has been driven by regulatory reforms, privatisation of state-owned banks and foreign direct investment, particularly from Western European financial institutions (Barisitz, 2007; Barjaktarović et al., 2013). Such transformations have stabilised and modernised the financial landscape. Yet disparities in access endure, often reflecting broader inequalities. Socio-economic factors, regulatory environments and demographic variables – many of which correlate with GDP per capita – are critical in shaping patterns of financial inclusion (Barjaktarović et al., 2013; Beckmann et al., 2018).

Despite this progress, a fundamental question remains: to what extent does trust in institutions influence individuals’ likelihood of accessing banking services? Trust in domestic and foreign banks, governments and police can reduce perceived risks and build confidence in formal banking systems. We therefore posit that higher levels of institutional trust lead to a higher likelihood of holding bank accounts, savings deposits and loans. This relationship is especially relevant in CEE, where trust deficits stemming from historical economic instability have hindered financial engagement (Buriak et al., 2019; Xu, 2020).

Our first hypothesis is therefore formulated as:

Hypothesis 1: Higher levels of trust in institutions – including trust in domestic/foreign banks, government and police – lead to a higher likelihood of holding bank accounts, savings deposits and loans.

Determinants of access to banking

A large body of literature identifies several key determinants of banking access, including income levels, education, employment status, regulatory frameworks, remittances and bank credit-to-deposits ratios (e.g. Barjaktarović et al., 2013; Gosztonyi and Havran, 2022; Waliszewski, 2023). Financial constraints remain a major barrier for low-income households, limiting their ability to engage with formal banking services (Gosztonyi and Havran, 2022). Education, particularly at the secondary and higher levels, improves financial literacy, which in turn facilitates financial inclusion (Delis, 2012; Waliszewski, 2023). Employment status also significantly impacts access, with unemployed individuals – especially those with limited levels of education – facing higher risk of exclusion (Nowacka, 2019).

However, individual characteristics alone cannot explain the full scope of financial exclusion. A critical question is how institutional trust compares with other personal characteristics factors in determining access to banking services. For instance, while high levels of trust may encourage financial engagement, barriers like low income or inadequate local infrastructure can temper its effects. These interactions underscore the importance of considering trust alongside broader systemic and personal factors (Demirguc-Kunt et al., 2019; Medve-Bálint and Boda, 2014; Waliszewski, 2023). We can then formulate our second hypothesis around the idea that institutional trust interacts with socio-economic attributes such as gender, education and employment status. We posit that:

Hypothesis 2: Trust in institutions interacts with personal attributes (e.g. gender, education, employment status) to collectively shape an individual’s likelihood of engaging with the banking sector.

Geographic disparities and the structure of banking markets

Urban–rural disparities are among the most prominent features of financial exclusion in CEE. Urban residents typically have far greater access to banking services than rural populations, where the phenomenon of ‘banking deserts’ abounds. These disparities are compounded by the structure of the banking market, with foreign banks controlling between 60% and 90% of banking assets in many CEE countries (Beckmann et al., 2018). Such institutions often prioritise profitable urban markets while neglecting rural areas, exacerbating geographic inequities (Beckmann et al., 2018; Delis, 2012), meaning that local conditions will be important in determining accessibility to banking. While competition in the banking sector has generally increased, Radulescu et al. (2018) argue that its benefits remain uneven and are heavily influenced by local institutional quality (Delis, 2012).

Despite expectations that market forces should bridge these service gaps, ‘banking deserts’ reflect structural inequalities and profit-driven decision-making. The absence of traditional banking infrastructure in rural areas forces residents to rely more on predatory alternative financial services (Henry et al., 2017). This perpetuates the cycle of exclusion and financial instability (Dunham, 2019). Many households in CEE still live more than 5 km from the nearest bank branch, further highlighting the geographic barriers to financial inclusion (Beckmann et al., 2018).

Moreover, national regulations affect the likelihood of individuals engaging with banking services.

These patterns pose the questions of to what extent do local, regional and national contexts shape access to banking services?; and how do these intersect with individual characteristics? Geographic disparities, shaped by legislation, regional economic development and local infrastructure, determine banking access. Individuals in more developed regions or countries with favourable regulatory environments are more likely to use banking. However, individual factors such as income, education and employment status can moderate these regional effects (Barjaktarović et al., 2013; Beckmann et al., 2018; Rodríguez-Pose, 2018). We can then formulate our third hypothesis:

Hypothesis 3: National, regional and local factors determine banking access.

Overall, despite growing research on financial inclusion/exclusion, the existing scholarly literature rarely considers how institutional trust intersects with personal characteristics and geographical contexts to shape banking access in CEE countries, rather considering these factors separately or in isolation.

Data and methods

Data – OeNB Euro Survey

Our analysis relies on the OeNB Euro Survey database, a comprehensive cross-sectional dataset that provides insights into financial behaviour and attitudes across 10 CEE countries: Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Czechia, Hungary, North Macedonia, Poland, Romania and Serbia (Beckmann et al., 2024). The dataset used in the analysis covers nine survey waves conducted between 2012 and 2020. It encompasses over 91,000 individual responses, although after controlling for income – which is not declared by a considerable number of respondents – the number of responses drops to just over 67,000. Its sheer size makes this survey a vital resource for examining banking access, financial inclusion and institutional trust.

To ensure consistency and comparability, the OeNB Euro Survey employs a harmonised questionnaire that has been standardised across all participating countries. The questionnaire collects detailed data on institutional trust, financial service usage and socio-economic characteristics. In particular, it explores respondents’ confidence in a range of institutions, including domestic and foreign banks, governments and law enforcement. It also investigates patterns of financial service use by inquiring about engagement with banking products such as current accounts, savings deposits and loans. Furthermore, it captures comprehensive demographic and economic information, including household composition, income levels, employment status and educational attainment (Beckmann et al., 2024).

The survey employs a random route sampling methodology to select adult respondents, ensuring that the dataset is representative of national populations. Each wave includes at least 1000 observations per country, which bolsters the reliability of cross-country comparisons and enhances the robustness of the dataset for identifying regional patterns.

However, while the OeNB Euro Survey provides a precious empirical foundation, it is important to acknowledge its limitations. First, the reliance on self-reported data introduces a potential for biases, as respondents may misrepresent their financial situations or banking behaviours. This concern is particularly salient in the CEE context, where cultural norms and historical legacies – such as a reluctance to disclose financial information – can influence the accuracy of responses. Sensitive topics, including income, savings and debt, may be especially prone to underreporting or exaggeration. Additionally, although the random route sampling methodology is designed to ensure representativeness, certain demographic groups, such as residents of remote rural areas, may still be underrepresented. This sampling issue is particularly relevant given that rural populations often face the greatest barriers to financial inclusion, potentially skewing the dataset towards urban respondents and masking some of the most acute forms of exclusion.

Another limitation arises from the cross-sectional nature of the data. While the survey spans nearly a decade and multiple waves, it does not track individual respondents over time. Consequently, it offers limited capacity for analysing longitudinal changes in banking behaviours or trust dynamics at the individual level.

Despite these caveats, the OeNB Euro Survey remains an essential tool for understanding the dynamics of financial inclusion and institutional trust in CEE. Its extensive scope, harmonised methodology and detailed coverage of socio-economic and financial dimensions make it uniquely suited for investigating the complex interplay between trust, personal characteristics and territorial disparities in banking access. By leveraging the strengths of this dataset, we contribute to the ongoing discourse on financial inclusion and to provide evidence-based recommendations for addressing the barriers that persist across the region.

Methodology

Understanding the interplay between institutional trust, individual characteristics and local, regional, and national contexts in facilitating banking access in CEE requires a robust and multidimensional analytical approach. We resort to econometric methods designed to account for the nested structure of the data, with a focus on three key dependent variables representing banking access: owning a current account, holding a savings deposit and having loans. By adopting a dual modelling framework, the analysis not only captures the direct effects of institutional trust but also explores how these effects vary across geographic and temporal dimensions.

All variables included in the analysis are provided in Table A1. Additionally, to assess potential multicollinearity concerns, correlations between explanatory variables were also examined (see Table A2). While some expected correlations exist (e.g. between different trust measures, between income and employment status), all correlation coefficients for non-trust variables remain below 0.4, indicating that our models do not have significant multicollinearity issues. To address the moderate correlations between trust variables, separate models were estimated for each trust measure rather than including multiple trust indicators simultaneously.

The first stage of the analysis employs a pooled logit regression model. This method, widely used in studies of financial access (e.g. Ambrosius, 2016; Chipeta and Kanyumbu, 2018), is particularly well-suited for the repeated cross-sectional nature of the OeNB Euro Survey data. The pooled logit model assumes that observations are independent, but fixed effects are introduced to account for temporal and country-specific variations. Fixed effects for survey wave (year) and country enable the model to control for unobserved factors that may vary across time periods – such as macroeconomic conditions – or across countries, such as differences in financial regulations. This serves as the baseline model, estimating the probability of engaging with banking services while isolating the effects of institutional trust and other key predictors.

The model is expressed as follows:

where:

β0 is the intercept;

β1 represents the coefficients for institutional trust measures;

Trust i denotes set of institutional trust variables (e.g. trust in government, trust in banks, etc.) at individual level i;

γ1X includes control variables such as socio-economic, demographic and geographical factors (e.g. income, education, employment status, region);

γt represents time fixed effects, accounting for differences across time periods or survey waves;

δc captures country fixed effects, addressing variations across countries;

ϵ denotes the error term, capturing residual variation not explained by the model.

While the pooled logit model provides the baseline estimates, the complexity of relations considered and the nested nature of the different geographical scales in the analysis requires a more nuanced approach to account for hierarchical structures and geographic variability. Patterns of banking access are inherently nested within broader contexts, as individuals are influenced by local (NUTS3), regional (NUTS2) and national environments, as well as by temporal changes across survey waves. To address these dynamics, we resort to a variety of multilevel (mixed-effects) logit models in the second stage of analysis.

The base multilevel logit model accommodates the hierarchical nature of the data by incorporating random intercepts for geographic levels and survey waves. This approach allows for a more refined analysis of how banking access patterns vary within and across geographical contexts. It also enables the exploration of how institutional trust mediates banking access within these contexts, addressing an often-overlooked dimension of financial inclusion research.

The multilevel logit model is specified as follows:

where:

By integrating fixed and random effects, this multilevel framework provides a robust means of analysing both individual-level predictors and contextual influences on banking access. For example, it allows the model to examine whether higher trust in institutions leads to greater banking engagement in well-developed regions, or if this effect diminishes in less-developed areas with weaker institutional frameworks. The choice of multilevel modelling is also informed by previous research that stresses the importance of geographic and institutional contexts in shaping financial behaviours (Bermeo, 2019; Chowa et al., 2014). In CEE, these factors are particularly salient, as regional disparities and the legacy of institutional mistrust continue to influence access to banking services.

However, while our multilevel logistic regression provides important insights into banking access, we acknowledge several key limitations. The cross-sectional nature of the OeNB Euro Survey data, which consists of repeated cross-sections rather than a panel that follows the same individuals over time, constrains our ability to track temporal changes in financial behaviours. This data structure prevented us from employing panel data methods, though our multilevel approach with fixed effects for survey waves helps capture temporal variation while our random effects account for geographic clustering. Finally, the binary categorisation of loans may obscure important variations in credit access. Future research could benefit from more granular data capturing loan types, sizes and specific lending criteria. Additionally, while our fixed effects and multilevel approach control for various contextual factors, unobserved variables may still influence the observed patterns of financial inclusion.

Results and discussion

Institutional trust and banking access

This section presents the results of the multilevel (mixed-effects) logit model, which captures the nested relationship between individual factors and geographic contexts – national, regional and local – that influence banking access and financial exclusion. Both the pooled logit (Model (1)) and multilevel logit (Model (2)) models identify consistent predictors of current account ownership. However, the multilevel approach offers a richer perspective by accounting for unobserved heterogeneity across countries. This is why our preferred model is the multilevel logit one reported in the paper. The findings from the pooled logit regression are included in the Appendix. 1 Both sets of findings align closely.

To address the first research question – whether trust in various institutions shapes individuals’ likelihood of accessing banking services – the analysis reveals that, as hypothesised, trust in institutions is a critical determinant of banking access across CEE. However, the influence institutional trust varies considerably by type of banking service, reflecting the interplay of trust with individual and contextual factors.

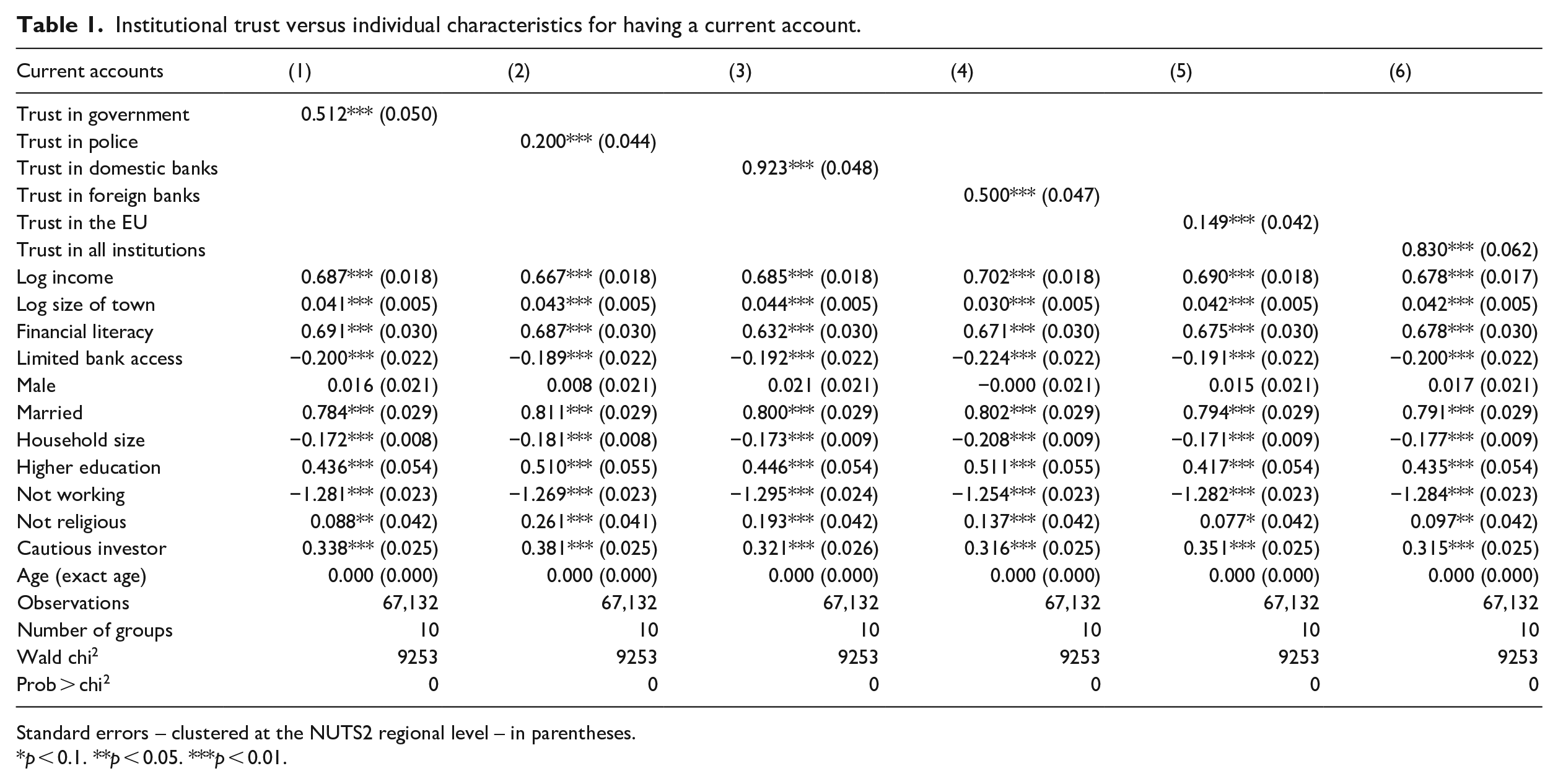

For current accounts (Tables 1 and A3), both pooled logit and multilevel models underscore how institutional trust shapes banking access alongside socio-economic factors. Trust in domestic banks shows the strongest positive association. This suggests that confidence in local institutions is a cornerstone of financial inclusion. This is followed by trust in government, foreign banks and overall institutional trust.

Institutional trust versus individual characteristics for having a current account.

Standard errors – clustered at the NUTS2 regional level – in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

In practical terms, a 1-unit increase in trust in domestic banks is associated with a 152% rise in the odds of holding a current account. Similarly, increases in trust in foreign banks, government and police are connected with 65%, 67% and 22% higher odds, respectively. Aggregated institutional trust, with a 129% increase in odds, underscores how confidence in institutions shapes access to current account. However, the pronounced impact of domestic trust suggests that improving trust in local banking systems is a must to increase financial access. This could involve enhancing transparency, strengthening consumer protections and improving service delivery, especially in regions with histories of widespread wariness in local institutions.

Socio-economic variables such as income, financial literacy and higher education consistently enhance the likelihood of account ownership. Conversely, being unemployed or part of a larger household diminishes the probability of having a current account. These results remain robust across both models.

The models diverge in their handling of country-specific effects. The multilevel model – by incorporating random intercepts for countries – captures unobserved national heterogeneity and reveals significant country-level variations in account ownership.

The country fixed effects in Table A3 point to Romanians and Bulgarians as the most disadvantaged CEE citizens regarding banking access. However, one must exercise prudence when interpreting these cross-national disparities. Rather than definitive indicators of national disadvantage, these coefficients may simply reflect particular country-specific circumstances that our model does not fully capture.

The broader implications of our analysis suggest that banking accessibility is shaped by factors extending beyond individual trust and socio-economic characteristics. National regulatory frameworks and systemic conditions appear to exert substantial influence on financial inclusion patterns across the region. This interplay between individual factors and national contexts underscores the complexity of financial inclusion dynamics in post-socialist economies.

These findings highlight significant gaps in our current understanding of how national-level variables interact with individual characteristics to determine banking access. Further research is clearly warranted to elucidate the precise mechanisms driving the observed variations. Particularly valuable would be studies examining how specific regulatory approaches, institutional arrangements and historical legacies in different CEE countries contribute to disparate levels of financial inclusion. Such research could provide more nuanced insights into effectively addressing banking access inequalities across the region.

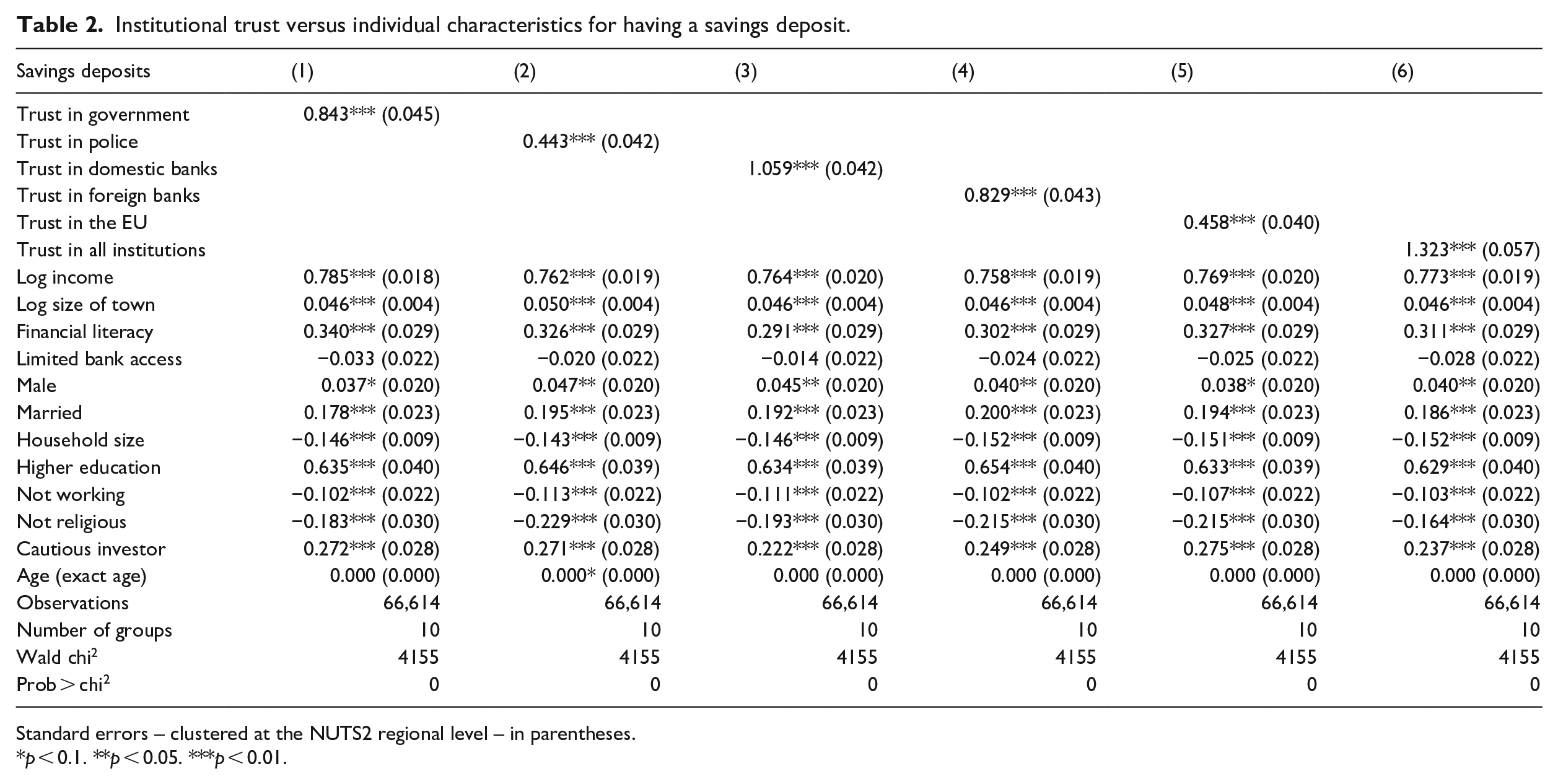

In the case of savings deposits (Tables 2 and A4), institutional trust is also linked with financial engagement. Among the various dimensions of trust, confidence in domestic banks appears the most influential factor. This strong association underscores the foundational importance of localised trust in enabling individuals to participate in savings activities. Trust in all institutions also has a significant and positive connection to holding a savings deposit, emphasising the cumulative impact of institutional reliability on savings behaviour.

Institutional trust versus individual characteristics for having a savings deposit.

Standard errors – clustered at the NUTS2 regional level – in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

Other institutional trust variables, including trust in foreign banks, government and police, also display positive but comparatively smaller coefficients. Meanwhile, trust in the EU, while statistically significant, has a more modest connection. This suggests that while supranational trust contributes to savings behaviour, it is less germane than trust in domestic institutions and broader localised confidence.

The probabilities derived from these coefficients reveal the scale of institutional trust’s impact. A one-unit increase in trust in domestic banks corresponds to a striking 188% increase in the odds of holding a savings deposit, making it the strongest link. For trust in all institutions, the odds increase by 276%, reflecting the robust role of generalised institutional confidence. Trust in foreign banks, government and police yields respective increases of 129%, 132% and 56%, while trust in the EU increases the odds by 58%.

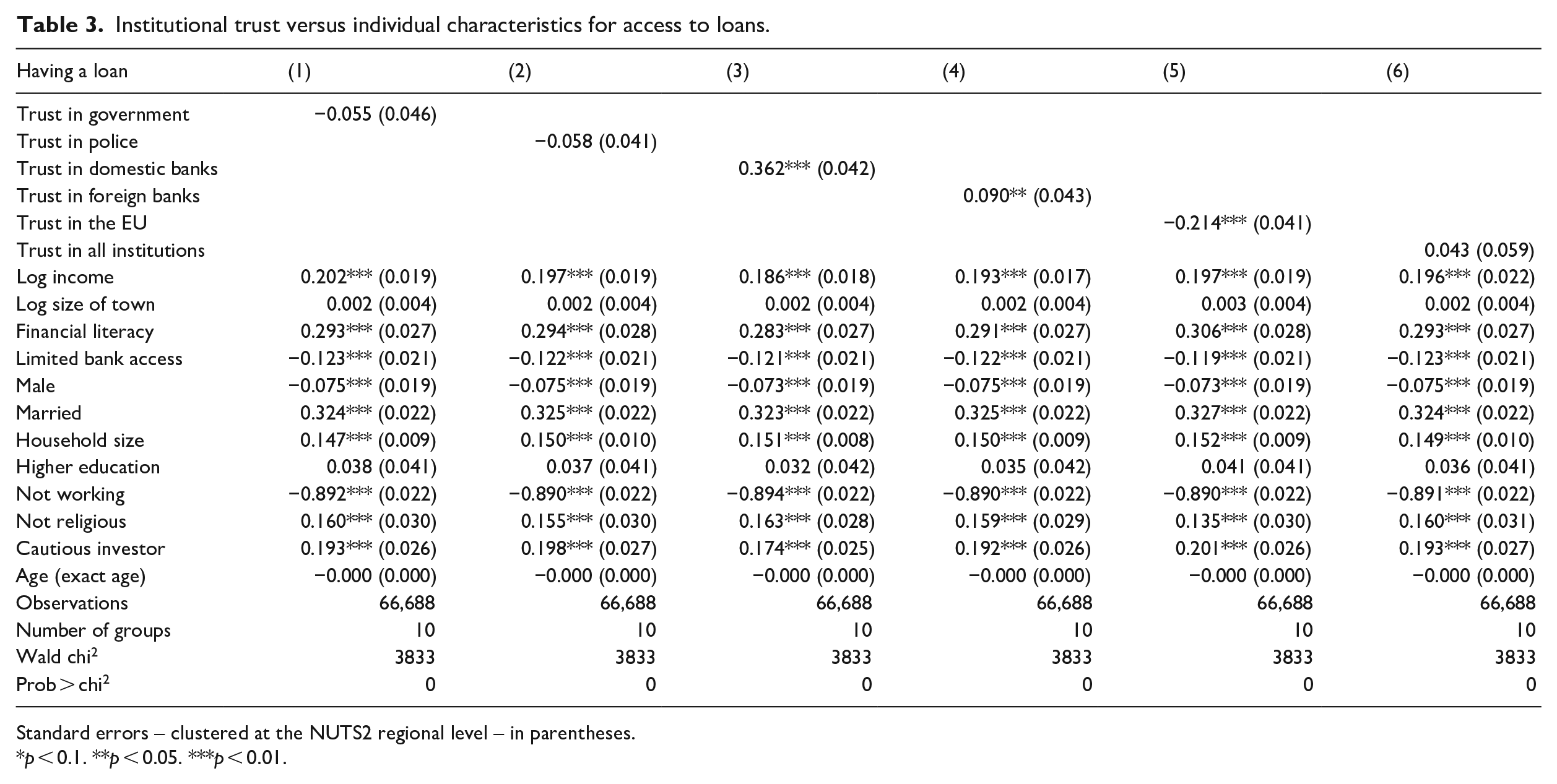

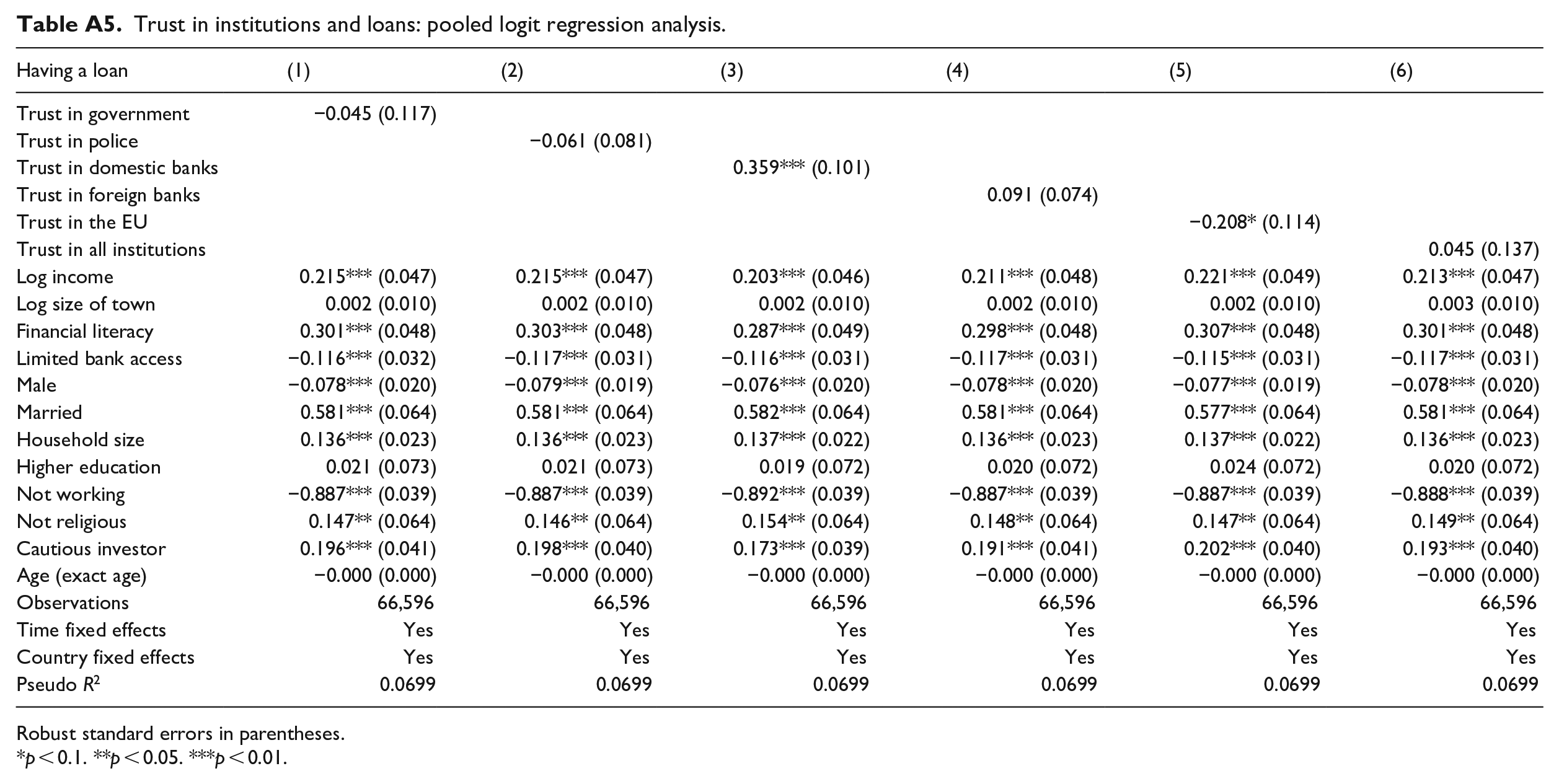

The analysis of institutional trust for access to loans reveals a distinct pattern compared to savings deposits and current accounts. Among the trust variables, only trust in domestic banks and foreign banks (Table 3) – and only trust in domestic banks, in the case of the pooled logit analysis (Table A5) – exhibit positive associations with loan ownership, though their effects are notably smaller than those observed for other banking products. Trust in government and police show negligible and statistically insignificant negative relationships, while trust in the EU demonstrates a small but significant negative link. Aggregated trust in all institutions displays no meaningful association, highlighting the relatively limited role of generalised institutional confidence for loan access.

Institutional trust versus individual characteristics for access to loans.

Standard errors – clustered at the NUTS2 regional level – in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

The probabilities derived from these coefficients are as follows: a one-unit increase in trust in domestic banks corresponds to a 44% increase in the odds of having a loan, while trust in foreign banks raises the odds by a modest 9%.

The muted connection between trust and loan access – especially in comparison with the far stronger relationship with current accounts and savings deposits – is interesting to understand the banking market structure in CEE. It somehow reflects a system where foreign banks tend to dominate in many national markets (Beckmann et al., 2018). According to Gál (2015) foreign banks became the major suppliers of credit in the region before the global financial crisis, providing about 80% of total credit. Austrian banks have established a particularly strong regional presence in several countries including Croatia, the Czech Republic, Hungary and Romania, where they represent a substantial portion of foreign-owned branches (Beckmann et al., 2018). However, while the survey data provides key information on individual banking behaviours and trust attitudes, it does not identify specific financial institutions used by respondents or their ownership structures. This limitation prevents us from directly analysing how the foreign versus domestic bank divide shapes the trust-access relationship. This is a key direction for future research. Nevertheless, previous research suggests significant differences in lending behaviour between foreign and domestic banks. Niţoi et al. (2021) highlight that foreign banks increased loans more rapidly in boom periods but also cut back their lending more during turbulent times compared to domestic banks. These differences in market presence and lending strategies may help explain why institutional trust shows weaker associations with access to loans compared to other banking products, as lending decisions may depend more on standardised metrics than on relationship-based approaches.

Hence, institutional trust, which appears critical for encouraging engagement with foundational financial products like accounts and deposits, becomes less influential in the more complex domain of lending. Instead, individual-level factors such as income stability, employment status and credit history take precedence in determining loan eligibility. As a whole, the comparatively smaller coefficients for loans suggest that other factors, such as creditworthiness, income stability and personal circumstances, play a more decisive role in borrowing behaviours. Unlike accounts and deposits, which mainly depend on individual initiative and basic eligibility, loans involve a two-sided decision-making process. While trust may influence an individual’s willingness to apply for credit, lenders make final decisions based on creditworthiness, risk assessments and financial stability. These are criteria that can outweigh trust for loan access. This key difference in product structure might explain why institutional trust shows a weaker relationship with loans compared to other banking services.

These results align with broader patterns in household debt studies, which emphasise the importance of stable income streams and financial security in lending decisions (Cottarelli et al., 2005; Hake and Poyntner, 2019). Notably, household size shows a positive association with loan ownership, with each additional household member increasing the likelihood by 16%. This suggests that borrowing decisions are influenced by household needs and resource constraints, adding complexity to financial behaviours in CEE.

Overall, these findings confirm Hypothesis 1 as higher trust in institutions – particularly domestic banks – significantly increases the likelihood of using basic banking services. They also highlight the need for differentiated policy approaches. While trust-building initiatives are essential for promoting broad financial inclusion, expanding access to loans requires more targeted interventions. Policies must address economic barriers, enhance credit assessment processes and support vulnerable groups to foster greater equity in access to banking but, particularly, in credit access. By recognising these nuanced dynamics, policymakers can develop strategies tailored to the specific challenges of financial inclusion across CEE.

Institutional trust versus individual characteristics and banking access

The results so far underscore the relationship between institutional trust, individual socio-economic characteristics and banking access in CEE. However, how does institutional trust compare with other personal characteristics and regional factors in determining banking inclusion? When individual characteristics are incorporated alongside institutional trust, the findings reveal a complex interplay between institutional trust, individual socio-economic characteristics and regional factors in shaping banking access in CEE. The role of institutional trust in determining banking access is always mediated by personal attributes and geographic contexts, with variations depending on the type of banking product.

For current accounts (Table 1), financial literacy stands out as a – if not the – key enabler, increasing the likelihood of ownership by 97%. This reinforces prior research emphasising the importance of financial literacy as a tool for financial inclusion and enabling the effective use of banking services (Delis, 2012; Waliszewski, 2023). Income is another significant factor; each unit increase in log income corresponds to an 97% rise in the likelihood of owning a current account. Education further amplifies this effect, with higher education boosting the odds by 55%. Notably, marital status is associated with a 121% higher probability, suggesting the potential role of family stability in shaping financial behaviour.

However, not all individual characteristics promote inclusion. Employment status shows a strong negative association with current account ownership, with unemployment linked to a 72% decrease in likelihood. Larger household sizes are also linked with lower account ownership, with each additional member lowering the probability by 16%. These findings highlight the vulnerabilities of economically disadvantaged groups, aligning with previous studies on barriers to banking access in post-socialist economies (Botrić and Broz, 2017; Corrado and Corrado, 2015). The size of town where respondents live provides a modest but positive connection, increasing the odds by 4%, likely reflecting the better availability of banking infrastructure as population density increases. For savings deposits (Table 2), socio-economic factors have even stronger sway. Income, financial literacy and education emerge as relevant indicators, with a unit increase in log income raising the odds of holding a savings deposit by 117% and financial literacy contributing a 37% increase. Higher education enhances the likelihood by 88%, underscoring its role in long-term financial planning. While unemployment reduces the odds by 10%, household size again shows a negative association, with each additional member decreasing the probability by 14%. Marital status and cautious financial behaviour also increase the odds of holding a savings deposit by 21% and 27%, respectively. Urban residency adds a smaller but positive effect of 5%, suggesting that while geography also matters.

Loans, once again, present a distinct pattern (Table 3). Income stability and financial literacy are more weakly connected to loans than other simpler financial products. A unit increase in log income raises the odds of obtaining a loan by 22%, while financial literacy boosts the likelihood by 34%. Employment status has a particularly strong influence, with unemployment reducing the probability by 59%. Larger households are also more likely to hold loans, with each additional member increasing the odds by 16%, reflecting greater borrowing needs. Unlike accounts and savings deposits, proximity to bank branches reduces loan access by 12%, while higher education shows no significant effect. These results suggest that creditworthiness and having a job are more critical for loan access than for other financial products.

The probabilities highlight both similarities and divergences across the three financial products. Income and financial literacy consistently increase the odds of financial engagement but have the strongest effects for savings deposits and the weakest for loans. Unemployment sharply reduces access across all products, particularly for loans, reflecting the reliance of credit markets on stable income streams. Household size negatively impacts accounts and savings deposits but positively influences loans, likely due to higher borrowing needs in larger households.

The enduring influence of historical legacies further complicates financial inclusion in CEE. The region’s post-transition period was marked by hyperinflation, banking collapses and economic mismanagement in the 1990s, eroding public confidence in financial institutions (Bonin and Wachtel, 2003). These trust deficits persist, particularly in the context of lending, where scepticism towards formal systems remains pronounced. However, regulatory reforms and EU integration processes have mitigated some of these concerns, leading to greater institutional stability and transparency. The entry of foreign banks and the adoption of EU financial standards have further bolstered confidence, although these improvements are uneven across countries and populations (Bonin and Wachtel, 2003; Kowalewski and Rybinski, 2011).

Nonetheless, lingering effects of the global economic crisis and the rise of Euroscepticism pose new challenges. Political instability and declining trust in EU institutions risk undermining confidence in domestic financial systems, complicating efforts to enhance financial inclusion (Sojka, 2015). To address these challenges, policymakers must prioritise trust-building initiatives, improve financial literacy, and tailor interventions to address socio-economic vulnerabilities and geographic disparities. Only by integrating these approaches can the region achieve more equitable access to financial services.

Geography and banking access

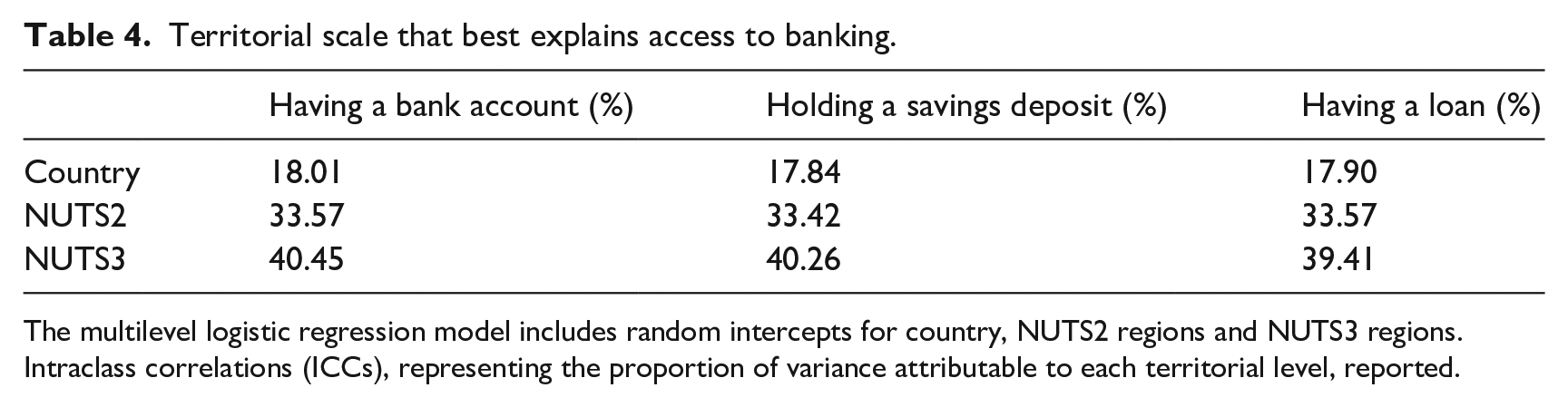

To what extent does geography influence financial inclusion? To show how living in a particular locality, region or country helps determine the probability of an individual in CEE having a bank account, a savings deposit or a loan, we resort to a multilevel logit regression with a four-level hierarchical structure: (a) 91,031 individuals; (b) living in 261 small NUTS3 regions; (c) in 62 large NUTS2 regions; (d) in 10 CEE countries.

We use the Broyden-Fletcher-Goldfarb-Shanno (BFGS) optimisation technique, with modified convergence criteria, tolerance set to 1e-4 and using the nonrtolerance option. This approach allows us to explore the probability of an individual having a current account, holding a savings deposit or having a loan in different geographical contexts. We include random intercepts at each geographic level, where individuals are clustered within NUTS3 regions, which are nested within NUTS2 regions, which are in turn nested within countries. This modelling method allows for the examination of variance components at different geographic scales while accounting for the nested hierarchical structure of the data.

The findings in Table 4 highlighting the interplay between national policies, regional dynamics and local conditions for access to banking in CEE. Where individuals live – at the country, regional (NUTS2) or local (NUTS3) level – significantly determines their access to banking services.

Territorial scale that best explains access to banking.

The multilevel logistic regression model includes random intercepts for country, NUTS2 regions and NUTS3 regions. Intraclass correlations (ICCs), representing the proportion of variance attributable to each territorial level, reported.

Local factors at the NUTS3 level – think counties or urban areas – emerge as the dominant force, explaining roughly 40% of the variation in banking access, regardless of whether we consider current accounts, savings deposits and loans. This suggests that, for CEE citizens, their postcode might matter more than their passport when it comes to financial services. Regional factors at the NUTS2 level account for about a third of the variation, while national differences explain less than 20%. The consistency of these proportions across different banking services is remarkable, suggesting these geographic patterns are structural rather than product-specific.

Localised factors at the NUTS3 level account for approximately 40% of the variation in banking access, highlighting the profound importance of local contexts in shaping financial inclusion. Despite our dataset not directly measuring specific local characteristics – such as bank branch density, community economic vitality or targeted financial literacy programmes – the substantial explanatory power of NUTS3-level variation strongly suggests that local conditions significantly influence financial inclusion patterns.

This territorial dimension of banking access aligns with research that documents how the uneven distribution of financial services at the local level creates pronounced spatial disparities in access across CEE countries (Dal Maso and Sokol, 2019; Gál, 2015). This work reinforces our finding that geography matters substantially when examining financial inclusion. Indeed, the analysis suggests that where one lives may be nearly as important as individual socio-economic characteristics in determining access to banking services.

Variation at the regional level (NUTS2) can reflect factors such as regional infrastructure, administrative capacity and economic development.

Finally, at the country level, geographic factors also matter but explain less (around 18%) of the variation (Table 4). There are considerable differences across CEE countries in access to banking (we have already mentioned the lower propensity of Bulgarians and Romanians in accessing banking products). These disparities suggest that national legislations, financial systems and broader economic contexts create environments that either promote or hinder basic banking access, though our models control for rather than directly measure specific policy or regulatory differences Countries with robust regulatory frameworks and inclusive policies offer more supportive financial ecosystems, whereas weaker systems perpetuate exclusion. Our approach does not establish the causal mechanisms in this relationship but the results align with previous studies on the structural inequalities of post-socialist financial landscapes (Mošnja-škare, 2024).

The results suggest that both national policies, but even more localised factors – such as the availability of banking services, local economic activity and cultural attitudes towards savings – are decisive for financial inclusion. While the national environment establishes the broader narrative for financial access, local and regional conditions create the most immediate barriers or enablers, such as the physical presence of bank branches or community-level financial education initiatives. Moreover, urban centres have emerged as hubs of modern financial markets in these post-socialist economies, benefitting from concentrated investments and institutional support. Conversely, peripheral and remote regions remain underserved, perpetuating core-periphery divides and reinforcing socio-economic disparities (Klimczuk and Klimczuk-Kochańska, 2019). This evidence brings to the fore the deeply geographical nature of financial inclusion/exclusion in CEE countries and the different integration paths followed by post-socialist economies into European financial networks. Asymmetric power relations between financial centres and peripheries are also at the root uneven development. Our trust-based analysis adds a new dimension to this geographical understanding by demonstrating how institutional confidence mediates financial engagement within these spatial contexts. These findings confirm Hypothesis 3: national, regional, and, especially, local contexts collectively shape access to banking services. National regulations and policies set the framework for financial inclusion, but local conditions mediate access, often creating an uneven financial landscape. Within-country disparities highlight how local infrastructure, economic vitality and community-specific factors can either amplify or diminish the effects of institutional trust on financial engagement.

Conclusions

After decades of post-socialist transition, Central and Eastern Europe still harbours a troubling paradox: whilst these economies have largely embraced market capitalism, millions of their citizens remain locked out of the most basic financial services. Our research has dissected the anatomy of this exclusion, revealing a complex web of institutional mistrust, individual vulnerability and geographical disadvantage that continues to shape who gets access to banking and who does not.

The findings challenge any notion that financial inclusion is simply a matter of building more bank branches or designing cleverer products. Instead, we expose three fundamental findings about banking access in post-socialist Europe.

First, trust operates as both the engine and the handbrake of financial inclusion, but not in the way conventional wisdom suggests. Our analysis reveals that whilst confidence in domestic banks can double the likelihood of opening a current account or holding savings, this same trust becomes almost irrelevant when people seek credit. This asymmetry is no accident. It reflects the profound structural changes that have remade CEE banking, where foreign institutions now dominate lending through standardised, algorithm-driven processes that care little for local relationships or community standing (Barisitz, 2007; Barjaktarović et al., 2013). The implications are stark: rebuilding trust in financial institutions, while necessary, is insufficient to address the full spectrum of financial exclusion.

Second, individual characteristics matter enormously, but they interact with systemic barriers in ways that amplify disadvantage. Employment emerges as the great divider. Losing one’s job does not just reduce income, it can trigger a cascade of financial exclusion that affects everything from basic current accounts to essential credit (Botrić and Broz, 2017). Meanwhile, financial literacy acts as a powerful multiplier, but only for those already positioned to benefit. The irony is that those most in need of financial services – the unemployed, the poorly educated, the economically marginalised – face the highest barriers to accessing them, a pattern that has persisted even through recent crises (Waliszewski, 2023).

Third, and perhaps most revolutionary, geography trumps almost everything else. Where you live in CEE matters more than your passport, your education or even your income when it comes to banking access (Beckmann et al., 2018). Local conditions at the county level explain twice as much variation in financial inclusion as national policies do. This finding shatters the comfortable assumption that EU integration and regulatory harmonisation have created a level playing field. Instead, it reveals a financial landscape carved up into haves and have-nots, where postcode determines access to economic opportunity. This is a stark reminder of the persistent spatial inequalities that have characterised post-socialist transformation (Smith and Timár, 2010).

These insights carry profound implications for policymakers who have too often treated financial inclusion as a technical problem requiring technical solutions. The reality is messier and more political. Building trust requires more than slick marketing campaigns. It demands genuine reform of banking practices that have prioritised profit over people. Addressing individual vulnerabilities means confronting the structural inequalities that leave so many CEE citizens economically precarious, particularly as traditional safety nets have eroded (Corrado and Corrado, 2015). And tackling geographical disparities requires acknowledging that market forces alone will not serve peripheral communities that banks view as unprofitable.

The digital revolution offers both promise and peril in this context. Online banking could theoretically leapfrog traditional infrastructure limitations, bringing services to remote areas at lower cost (Manta et al., 2023). Yet digitalisation also threatens to create new forms of exclusion, particularly affecting older citizens and those without reliable internet access. This is a concern that extends far beyond banking to the broader challenge of digital inclusion (Drugă, 2024). The challenge for policymakers is to harness technology’s potential, simultaneously ensuring it does not compound existing inequalities.

A more nuanced approach to financial inclusion is also needed; one that recognises the interplay between trust-building, individual empowerment and place-based intervention. Effective strategies must simultaneously strengthen confidence in domestic financial institutions, address socio-economic vulnerabilities through targeted support and tackle geographical disparities with locally-tailored solutions (Leyshon and Thrift, 1996). This might involve everything from community banking initiatives in underserved areas to digital literacy programmes that help vulnerable groups cope with online financial services safely. In other words, there is a need for approaches that recognise the everyday financial struggles of low-income households in post-socialist cities (Stenning et al., 2010).

The stakes could hardly be higher. Financial exclusion is not just about banking. It is about who gets to participate fully in modern economic life. In societies still grappling with the legacy of socialist transformation, ensuring equitable access to financial services is essential for social cohesion and democratic stability. Our findings suggest that achieving this goal will require policymakers to think less like technocrats and more like social engineers, crafting interventions that address the complex interplay of trust, capability and place that determines who prospers in post-socialist Europe. The development of regional financial centres and the concentration of banking services in major urban areas (Gál, 2015) has only amplified these challenges, creating stark disparities between centre and periphery.

The transformation of Central and Eastern Europe’s financial landscape is far from complete. The question is whether the next chapter will be written by market forces that have already created such stark inequalities, or by policymakers willing to reimagine financial inclusion as a public good requiring active intervention. Our research helps provide the map. Now it is up to those in power to choose the destination, mindful that the spatial dimensions of exclusion require solutions as geographically nuanced as the problems themselves.

Footnotes

Appendix

Trust in institutions and loans: pooled logit regression analysis.

| Having a loan | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Trust in government | −0.045 (0.117) | |||||

| Trust in police | −0.061 (0.081) | |||||

| Trust in domestic banks | 0.359*** (0.101) | |||||

| Trust in foreign banks | 0.091 (0.074) | |||||

| Trust in the EU | −0.208* (0.114) | |||||

| Trust in all institutions | 0.045 (0.137) | |||||

| Log income | 0.215*** (0.047) | 0.215*** (0.047) | 0.203*** (0.046) | 0.211*** (0.048) | 0.221*** (0.049) | 0.213*** (0.047) |

| Log size of town | 0.002 (0.010) | 0.002 (0.010) | 0.002 (0.010) | 0.002 (0.010) | 0.002 (0.010) | 0.003 (0.010) |

| Financial literacy | 0.301*** (0.048) | 0.303*** (0.048) | 0.287*** (0.049) | 0.298*** (0.048) | 0.307*** (0.048) | 0.301*** (0.048) |

| Limited bank access | −0.116*** (0.032) | −0.117*** (0.031) | −0.116*** (0.031) | −0.117*** (0.031) | −0.115*** (0.031) | −0.117*** (0.031) |

| Male | −0.078*** (0.020) | −0.079*** (0.019) | −0.076*** (0.020) | −0.078*** (0.020) | −0.077*** (0.019) | −0.078*** (0.020) |

| Married | 0.581*** (0.064) | 0.581*** (0.064) | 0.582*** (0.064) | 0.581*** (0.064) | 0.577*** (0.064) | 0.581*** (0.064) |

| Household size | 0.136*** (0.023) | 0.136*** (0.023) | 0.137*** (0.022) | 0.136*** (0.023) | 0.137*** (0.022) | 0.136*** (0.023) |

| Higher education | 0.021 (0.073) | 0.021 (0.073) | 0.019 (0.072) | 0.020 (0.072) | 0.024 (0.072) | 0.020 (0.072) |

| Not working | −0.887*** (0.039) | −0.887*** (0.039) | −0.892*** (0.039) | −0.887*** (0.039) | −0.887*** (0.039) | −0.888*** (0.039) |

| Not religious | 0.147** (0.064) | 0.146** (0.064) | 0.154** (0.064) | 0.148** (0.064) | 0.147** (0.064) | 0.149** (0.064) |

| Cautious investor | 0.196*** (0.041) | 0.198*** (0.040) | 0.173*** (0.039) | 0.191*** (0.041) | 0.202*** (0.040) | 0.193*** (0.040) |

| Age (exact age) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) | −0.000 (0.000) |

| Observations | 66,596 | 66,596 | 66,596 | 66,596 | 66,596 | 66,596 |

| Time fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Country fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Pseudo R2 | 0.0699 | 0.0699 | 0.0699 | 0.0699 | 0.0699 | 0.0699 |

Robust standard errors in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

Acknowledgements

We thank the editor and the three anonymous reviewers for their insightful and constructive feedback on earlier drafts of the manuscript, which significantly improved the quality of the paper. We are also grateful to Oesterreichische Nationalbank (OeNB) – EuroSurvey for providing access to the datasets.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data availability statement

The data used in this study was obtained from the Oesterreichische Nationalbank (OeNB) – EuroSurvey. The dataset can be obtained through a formal request to Oesterreichische Nationalbank. Interested researchers can contact OeNB directly to request access to the EuroSurvey data for research purposes. Access to the data is subject to OeNB’s data sharing policies and procedures.