Abstract

This paper traces the social value and risk management strategies of a pension -backed build-to-rent (BtR) housing provider in the United Kingdom. Through these strategies, BtR is positioned as a ‘new’ socially and environmentally responsible model, appealing to institutional investors seeking to do ‘good’ while also filling fiduciary mandates to pay promised pensions. However, this paper reveals how the vision of a redefined rental market, advanced by a major BtR landlord, strengthens aspects of the existing landlord-tenant relationship while also introducing some limited innovations. The case shows that the BtR provider relies on conventional but problematic risk profiling techniques that hierarchically classify households according to ostensibly neutral credit, income, and employment criteria. The result masks the classed and racialised dynamics through which desirable tenants – implicitly cast as uniquely deserving of an elevated rental experience – are separated from those deemed too risky. Through a critical examination of constructions of ‘social value’ and ‘risk’, I show how household risk profiles are transformed into ethical risk for a range of investors. Furthermore, the sector specific investment risks identified by the firm define the limits of how and for whom renting can be reinvented. Therefore, while the risk assessments applied to tenants in BtR developments are not themselves new, their integration into the risk economies of ESG investing brings distinct challenges and opportunities for those interested in housing justice and housing rights.

Society’s quest for purpose, balance, connectiveness and fairness has been amplified by a succession of pivotal events. For Get Living, the need to innovate and evolve the resident proposition, empowering people to thrive in our neighbourhoods, is our driving mission.

Back in March 2016 when Quintain Living opened its first apartment buildings, our goal was to rip up the rental rulebook and make renting better for everyone. That meant being better than the uncaring estate agents (by not being one ourselves) and being more useful than the lazy landlords most Londoners get lumbered with.

A landlord you actually like.

Introduction

How did renting get reinvented as a mass-produced luxury with a mission to empower people and elevate society as a whole? This image of renting, now ubiquitous across the physical and digital spaces of the institutionally backed build-to-rent (BtR) sector in a growing number of cities across North America and the United Kingdom (e.g. Nethercote, 2020), is at odds with more familiar and long-standing notions of renting as a stigmatised tenure. What is unspoken in these notions of ‘reinventing’ or ‘redefining’ renting and being ‘caring’ and ‘likable’ landlords are the unique risks and opportunities associated with ‘generation rent’ – which includes growing numbers of stable, high earning households priced out of home ownership (Byrne, 2020). In this context, longer standing associations of renting with poor or working-class households, or as a merely temporary, transitional step for students and new immigrants who will soon step ‘up’ onto the property ownership ladder must be overcome. Across the strikingly similar claims to novelty highlighted in the epigraph, BtR providers therefore position themselves as providing solutions to the housing crisis, by ripping up the ‘rental rule book’ to provide an elevated, flexible, yet more secure experience of renting for those priced out of home ownership (Nethercote et al., 2023; Scanlon et al., 2018). To unpack these claims, the paper focuses on the environmental, social, and governance (ESG) practices of one of the UKs largest BtR landlords.

Once a niche investing phenomenon, ESG integration is increasingly mainstream with global assets under management (AUM) estimated to be between 30 and 40 trillion dollars in 2024 (Parrish, 2024). ESG has been subject to numerous critiques, from different ideological positions. It has been characterised as ‘deadly distraction’ and a form of ‘greenwashing’ that delays meaningful climate action and legitimises ongoing investment in fossil fuels (Baines and Hager, 2022; Fancy, 2021). Others have argued that, in the context of legally enshrined fiduciary duties that compel investors to consider beneficiaries individual financial interests over and above any other kinds of interests, the scope for achieving progressive social change through ESG is highly circumscribed (McCarthy, 2017; Parish, 2023). Meanwhile, in the United States, the Republican backlash against ESG as ‘woke capitalism’ – which precedes but has nevertheless intensified under ‘Trump 2.0’ – has led to a growing list of legal challenges and regulatory changes (ballotpedia.org, nd). Yet, to date, ESG has proven remarkably resilient. ESG and sustainability funds continue to log net inflows, particularly in Europe (Morgan, 2025) while analysts describe the foregoing as ‘growing pains’ (McKiernan, 2024) that may trigger ‘quieter’ (Jones, 2025) practices by institutional investors, but are unlikely to spell the end of ESG as such. 4

Nethercote et al. (2023) describe ESG as an investment strategy and decision-making practice that considers ‘future orientated and financially-material risks and opportunities’ (p. 5). However, ESG is not merely a neutral technique of financial analysis or inert object of governance. Instead, critical finance scholars have demonstrated how ESG itself functions as technique of governance (Archer, 2023; Parfitt, 2020). As such, emerging, investor led practices of determining what is included and excluded in definitions of social and environmental risks and values have significant potential to crystalise into broader norms, standards and laws pertaining to exactly which aspects of renting can be reinvented and in what ways (Nethercote et al., 2023). Further, as Brill and Özogul (2021) have shown in the London case, institutional landlords do not merely cultivate expertise to respond to or take (retroactive) advantage of policy environments but actively seek to shape policy as well.

This article makes three interconnected arguments. First, that ESG is a crucial element of how BtR landlords position themselves as new kind of landlord, which is caring and responsible, insofar as it transforms longstanding risks of landlordism into ‘ethical risks’ for global investors (Parfitt, 2020). Ethical risk refers to the ways in which ESG integration frames ‘the contest of social, ecological and political problems. . . [through] a derivative logic of ethics’ (Parfitt, 2020: 574). Second, this construction of ethical risk de-politicises (Nethercote, 2022a) the landlord tenant relationship by side-stepping the extractive relationship through a focus on responsive customer service and accessible yet luxurious consumption. Tenants are reframed as consumers with preferences, not people with rights. Third, the spatial dynamics of the foregoing suggest a reproduction of ‘racial logics of home and home making’ (Nethercote, 2022b: 935; Fields and Raymond, 2021), insofar as the life optimising innovations on offer are unlikely to be accessible to long-standing residents of the working class and racialised neighbourhoods in which they are situated.

The paper builds on the work of others who have analysed BtR as distinct trend (Brill and Durrant, 2021; Brill and Özogul, 2021; Nethercote, 2022b; Nethercote et al., 2023; Scanlon et al., 2018) within the broader financialisation of rental housing (Aalbers, 2016; August and Walks, 2018; Wijburg et al., 2018). Responding to calls for greater specificity and detail (Nethercote, 2020), in the study of ‘global corporate landlords’ (Beswick et al., 2016) I present a case study of one of the UK’s largest BtR providers, Get Living, PLC. Get Living is a BtR focussed Real Estate Investment Trust (REIT; hereafter, landlord), originally founded to redevelop the athlete’s village in the wake of the 2012 London Olympics (Brill and Durrant, 2021; Corcillo and Watt, 2022). Today, Get Living is majority owned by three different pension asset managers, based in Australia, Canada and the Netherlands.

The pension backed nature of this provider is significant, considering academic theories of the social and environmental benefits of universal ownership as well as wider public understandings of pension investment as a straightforwardly benevolent activity. As Christophers (2023: 212) notes in Our Lives in Their Portfolios, this view is actively cultivated by asset managers like Blackstone, who justify and normalise otherwise predatory investment practices as the fulfilment of mandates to pay pensions to ‘ordinary people’: ‘to the extent our funds perform well, we can support a better retirement for tens of millions of pensioners, including teachers, nurses, and firefighters’. Yet, pension owned housing companies have also been at the centre of rent strikes and other controversies alleging they are undermining of the right to housing (Parish, 2023).

The remainder of the paper proceeds as follows: in the next section, I provide a discussion of my methodological commitments and associated research methods. I then provide an overview of the literature on rental housing financialisation and BtR development. In the subsequent section I connect this with the rise and significance of asset manager society, pension financialisaton and environmental, social and governance (ESG) factor investing as practical and theoretical ground for the present study. In the remainder of the paper, I present the empirical case by showing how the BtR provider defines and manages the risks associated with the rental housing sector across portfolio, asset and household scales. I further analyse how, through their ESG strategy and associated social value proposition, longstanding risks of landlordism are reformatted as ethical risks for global investors.

Methods: Relations, repeated instances and the transnational networks of financialised BtR

Global urban studies scholar Robinson (2016) argues that urban studies is always already comparative in ‘a world of cities’. Robinson’s (2016) method of ‘thinking cities through elsewhere’ offers an intellectually robust and potentially transformative way to study urban processes in a world that is messy, emergent, and fundamentally shaped by the hierarchies and injustices of coloniality, racialisation, and sexism. This approach is especially well suited to the study of asset manager society (Christophers, 2023), in that it can assist in understanding how investment decisions taken at a distance touch down in specific urban contexts. It also pairs well with the follow-the-money/follow-the-firm approach used by others who have illustrated the importance of transnational and trans-scalar territorial networks in the international rise of BtR (Brill and Özogul, 2021; Goulding et al., 2023). Unlike the comparatively opaque world of institutional control of financial assets, direct investing in so-called ‘real’ assets has the effect of clearly and directly connecting different groups of workers and renters in relatively durable ways, across time and space. Furthermore, as Parfitt (2020) has argued, ESG investing also has novel connective capacities. Not only does it foster connections between investors with similar risk appetites, but it also connects distinct social constituencies across time and space, through market mechanisms. Approaching pensions investing and ESG in this way reveals connections that are otherwise obscured by ‘a reading of financial risk that is stripped of its lived reality’ (Parfitt, 2020: 580). Such a reading can also contribute to challenging the separation of processes of financialisation from their ‘often violent impacts. . . on the ground’ (Fields and Raymond, 2021: 1626).

To examine how people and communities are connected across space and time by pension investing in real assets, the relationships this entails, and what it might suggest for shifting forms and relations of social reproduction and social solidarity, I first selected a pension fund on which to focus. I chose the Ontario Municipal Employees Retirement System (OMERS) for several reasons. It is the Canadian ‘Maple 8’ fund (see Skerrett, 2017) that holds the largest real estate and infrastructure allocations, 5 and was also an early entrant into real asset investing, compared to other large public sector funds in that category. Second, their real estate arm, Oxford Properties has a core focus on commercial and industrial properties. While OMERS had existing investments in both residential rental properties in North America and infrastructure in the UK, their investment into Get Living in 2018 represents, as far as the author is aware, their first entry into BtR in the UK.

Having thus identified Get Living as a case study of a portfolio company, I took three further steps. First, I identified the shifting network of owner-investors behind the BtR provider at the centre of the study. Second, I documented the ‘repeated instances’ through which the BtR provider is expanding its territorial footprint within London and beyond. And third, I analysed the ESG strategy of the firm in relation to the investment strategies and risk tolerances of one of its major owner-investors, OMERS. Specifically, my analysis of risk and social value emphasise OMERS understanding of its fiduciary duty to members as a duty to obtain ‘the highest returns for plan beneficiaries within acceptable risk limits’ (OMERS, n.d.). The acceptability of risk limits is in turn shaped by two interconnected future projections made by OMERS: an increasing reliance on investment income, coupled with decreasing tolerances for investment risk, as the demographic balance between working members and retirees continues to shift towards the latter (OMERS, 2021: 40).

Previous literature has documented the important role of US investors (Brill and Özogul, 2021) as well as Middle Eastern sovereign wealth funds in the UK’s property and rental housing markets (Goulding et al., 2023; Purcell and Ward, 2023; Ward et al., 2023). However, the involvement of Canadian institutions in the financialisation of UK housing markets has received less attention. This is an important area of research since the ‘Canadian model’ of pension investing is widely celebrated and held up as worthy of emulation, both on grounds of financial performance and social responsibility (Lachance and Stroehle, 2023; Lofto, 2019; Skerrett, 2017).

Data was collected using a multi-method strategy of document review and analysis (e.g. policy, annual reports, governance documents), targeted site visits to current and planned urban housing developments in the UK (n = 8), and in-depth interviews (n = 9) with a selection of experts in the fields of pensions, ESG, real asset investing and housing justice. It is important to note the purpose of the interviews was not to reach generalisable conclusions about how a relatively homogeneous group of stakeholders’ views or practices ESG. While such studies are important and illuminating (e.g. Archer, 2023) my aim was different and focussed instead on using interviews as signposts to gain insight from experts positioned differently vis-à-vis pension and ESG investing in housing. The following remark, offered in response to a question about the meaning of the term ‘social value’ in the specific context of rental housing investments, was influential in shaping how I approached subsequent textual analysis and ethnographic elements of the research: ‘Generally with ESG everyone’s going to say they do social value, but no one knows what the heck that means’ (Interview #3, ESG analyst, January 2023, my emphasis). This remark – while clearly not evidence of a consensus opinion – is what prompted me to look more carefully at questions of social value and social factor integration.

The core data on which the empirical sections of the present paper are based are textual documents including the websites, press releases, annual reports, sustainability reports and other special reports and ‘grey’ literatures produced by or in collaboration with Get Living and its major investors, past and present. 6 This textual data was supplemented by eight site visits to existing and in-progress Get Living developments in London, Greater Manchester, and Glasgow between the winter of 2022 and summer of 2023. These visits collected data using embodied ethnographic reflection as well as photography. This data enables a richer engagement with the placemaking strategies of the firm and its various partners, which are, ultimately, central to its claims to be producing social value by remaking landlord tenant relations for the better.

Build-to-rent and housing financialisation

The financialisation of housing, which initially focussed on mortgage-backed securities for owner-occupied housing, (Aalbers, 2016) has widened to include single family (Fields, 2018) and multifamily rental housing as well (August and Walks, 2018; Wijburg et al., 2018). The term ‘financialisation 2.0’ (Wijburg et al., 2018: 1099), has been used to describe a process whereby longer-term investment strategies of holding assets to extract rents displaced an earlier, speculative strategy of ‘buy low and sell high’.

Much of the work on the financialisation of rental housing has tended to focus on the acquisition of existing homes (August, 2020; August and Walks, 2018). However, as cities in the Global North experience a boom in new, private, investor financed and purpose-built rental housing the literature on ‘build-to-rent’ is likewise expanding (Brill and Durrant, 2021; Brill and Özogul, 2021; Nethercote, 2020). Thus, while the financialisation of the private rented sector is not an entirely ‘new’ phenomenon, BtR is conceptualised as a novel development insofar as this form of housing is being developed at significant scale and pace by investors, from the ground up, as first and foremost an asset class (Brill and Durrant, 2021; Nethercote, 2020). As Nethercote (2022a: 2) explains, ‘BTR involves institutional landlords such as pension funds, private equity firms, hedge funds, real estate investment trusts (REITs) and publicly listed real estate firms who develop purpose-built rental accommodation for retention under single ownership and operation as rent-generating assets’. The transnational and networked nature of this type of landlord means that wealth is not only transferred across class, from tenants to investors, but across space and scale as well (Beswick et al., 2016; Goulding et al., 2023).

The financialisation of housing has been associated with the erosion of affordability across multiple pathways, including via the financialisation of social and state owned housing providers (Aalbers et al., 2017), elimination of protections for renters, such as rent control and rent stabilisation regimes (August, 2020; Wilde, 2019), the relaxation of affordability quotas in development agreements (Scanlon et al., 2018), and the strategic use of increasingly capacious and vague definitions of ‘affordability’ itself (Corcillo and Watt, 2022; Tranjan, 2023). In tandem with these, the BTR industry has also questioned the need to build new affordable housing, asserting, without evidence, that supply aimed towards the higher end of the market will ‘naturally’ create affordable supply through the ‘filtering effect’ (Scanlon et al., 2018).

This erosion of affordability has been directly connected to strategies used by ‘global corporate landlords’ (Beswick et al., 2016) to produce large-scale gentrification cycles and drive investment returns: rents are increased, units are neglected and working class and racialised tenants are pushed out either because they can’t afford to stay, or because buildings are identified for demolition or needing major renovations. This financial strategy of ‘gentrification by upgrading’ of existing units (August and Walks, 2018) has, in turn, been linked to the quantitative disappearance of affordable housing stock as well as the qualitative deterioration of living conditions, including over-crowding, disrepair, mould and pests (Crosby, 2020; Zigman and August, 2021). These processes – which have notably provoked significant and organised tenant resistance – have been described as both environmental racism (Parish, 2023) and as a form of ‘death dealing’ financial violence which systematically places racialised and working-class bodies at increased risk of injury, illness, and death (Fields and Raymond, 2021; see also Lewis, 2022). Furthermore, these racialised dynamics and effects on tenants are not merely an unfortunate bi-product. Rather, they are an indication of the fundamentally racial character of capitalism (Robinson, 2000) and its constitutive housing and property markets (Fields and Raymond, 2021; Nethercote, 2022b).

Unlike gentrification by upgrading existing structures or units, BtR promises to inject new supply of rental homes, and thereby to play a key role to play in alleviating the so-called housing crisis. Furthermore, because institutional investors can leverage considerable sums, the industry argues that it is uniquely positioned to build at scale. The promise of institutional BtR development is not only framed in terms of supply and scale, but also as involving a different and better kind of landlord, one who is uniquely able to generate new forms of ‘social value’. These claims must be documented and evaluated considering the wider context and literature outlined above.

Pension funds, asset manager society and the role of ESG analysis

The growth of the strategy of direct ownership and control of housing and other essential infrastructures is what Christophers (2023) has referred to as asset manager society (AMS). AMS is distinct in that it specifically denotes ownership and control over the things that people depend on directly for their day-to-day social reproduction: housing, water, energy, transit, communication, health and education infrastructures. Thus, ‘Whereas growing asset manager investment in financial assets such as publicly listed shares and bonds powerfully reshapes business and the economy, growing asset manager investment in the “real” assets that are housing and infrastructure powerfully reshapes social life itself’ (Christophers, 2023: 15). AMS involves a range of different yet interconnected actors, including pension funds (Lewis, 2022; Theurillat et al., 2010; van Loon and Aalbers, 2017; Parish, 2023) and real estate investment trusts (REITs; August and Walks, 2018; Bonshoms-Guzmán, 2023; Garcia-Lamarca, 2021). REITs are a vehicle for pooling real estate assets which enjoy preferential tax status (August and Walks, 2018; Bonshoms-Guzmán, 2023). Initially developed in the US in the 1960s (Goulding, 2024) they have since spread to many other jurisdictions including Canada, Ireland and Spain (August and Walks, 2018; Garcia-Lamarca, 2021). REITs have also played an important role in demonstrating the wider viability of multifamily housing as an investment vehicle (August, 2020).

Pension funds have been implicated in housing financializaton strategies, both through securitisation processes (van Loon and Aalbers, 2017) as well through direct investment in the mode of financialisation 2.0. Pension funds are a particular kind of investor, insofar as they have legal obligations to pay promised pensions over long time horizons, given the intergenerational nature of their obligations or ‘liabilities’ (e.g. to workers and retirees). To fulfil their fiduciary mandates, these liabilities need to be appropriately ‘matched’ to profit and income streams (Skerrett, 2017; van Loon and Aalbers, 2017). In the post-Global Financial Crisis period, investors have increasingly sought ‘alternatives’ to stocks and bonds. Real estate and infrastructure are land and place-based assets that afford monopolistic access to reliable income (rent) streams (Christophers, 2023). As such, they provide investors with options that are less volatile than public markets and higher yielding than other lower risk options like bonds (Lofto, 2019). These types of investments are attractive for pension funds because of the promise of steady, predictable, and relatively long-term income streams, as well as the diversification of risks and long time horizons (Christophers, 2023). According to a survey of Canadian pension asset managers, real estate is also viewed as low risk as it is more amenable to direct and co-investing strategies, affording investors a better view of risks and opportunities (Lofto, 2019).

Leveraged investing is attractive to asset managers from the perspective of both profitability and risk management. From a risk management perspective, debt allows the asset manager to shift or ‘quarantine’ the risk of asset value depreciation, and does so by tying the debt to the asset thereby placing it on the balance books of company or holding company which is the immediate legal owner (Christophers, 2023). The ability to raise debt is important for REITs, since real estate development is capital intensive, but REITs tend to be cash poor, due to laws regarding the disbursement of dividends (Feng and Wu, 2021). In the UK, REITs must distribute 90% of rental income as dividends (Goulding, 2024). Thus, access to capital is crucial for expansion and new development in a model that relies on scale. Importantly, ESG disclosure by REITs has been linked to higher firm valuations, lower cost of corporate debt and more favourable ratios of unsecured to secured debt (Feng and Wu, 2021). Institutional backing of REITs has also been linked to both the likelihood of engaging in voluntary ESG disclosure, as well as the robustness of disclosure (Feng and Wu, 2021).

Alongside AMS, ESG has grown rapidly as a core strategy for understanding and managing risks across investment classes and in real estate and infrastructure specifically (Archer, 2023; Feng and Wu, 2021; Nethercote et al., 2023). ESG integration is an investment strategy and decision-making practice that considers ‘future orientated and financially-material risks and opportunities’ (Nethercote et al., 2023: 5). Like credit ratings, the field of ESG ratings is populated by proprietary metrics (Eccles et al., 2020). Investors are a primary audience for third party ESG data, which is posited to be alpha-generating insofar as it renders both risks and opportunities visible and knowable to investors (Parfitt, 2020). In the case of climate change, for example, materially relevant factors are diverse and may include risks and opportunities arising from changing laws and policies related to climate adaptation and mitigation, as well as physical risks and opportunities arising from climate events (Christophers, 2017). In theory, the accurate identification and disclosure of risks facilitates the accurate pricing of those risks (Christophers, 2017). Thus, ESG is ostensibly capable of smoothing out the contradictions of capital and obviating the need for socially or environmentally protective regulation (Parfitt, 2020).

Yet the portrayal of ESG as a strictly technical device of risk management obscures its relationship to questions of power and ethics (Parfitt, 2020). This tension is well captured by pension law and investing experts Bauslaugh and Gartz (2019) when they explain: ‘The purpose of ESG factor integration from the perspective of a pension fund should not be to stop climate change, improve workplace diversity or end child labour. That is more of what is referred to as SRI’. However, they continue, ‘Legislation, regulatory guidance and statements from agencies, such as the United Nations blur these distinctions’ (Bauslaugh and Gartz, 2019, my emphasis). 7 This isn’t just slopy prose or lack of conceptual clarity. Rather, it suggests that ESG practices work to redefine ethics through the lens of risk: ‘Rather than an ethically driven worldview, ESG integration offers a range of exposures to ethical risk, from which investors may choose’ Parfitt (2020: 582). Thus, while ESG is distinct from SRI, the former has ‘taken centre stage in the mainstreaming of [a] narrative of the possibility of benign, sustainable capitalism’ which has origins in the latter (Parfitt, 2020: 577).

Within the broader ESG umbrella the ‘E’, and climate considerations specifically, tend to enjoy the most attention (Parish, 2023). ESG analysis entered the property sector via a concern with the high levels of emissions associated with heating and lighting buildings (Gradillas et al., 2021). Yet, while the ‘S’ is the least clearly defined area this is quickly changing (Nethercote et al., 2023). Social factor considerations have historically focussed on labour relations and supply chain issues. However, this category increasingly includes other ‘social megatrends’ like global inequality, Indigenous rights, and artificial intelligence (AI; Nethercote et al., 2023). In the realm of housing and real estate investment, additional sector specific risks that have been identified include ‘the delivery of diverse and affordable housing options and tenant satisfaction’ (Nethercote et al., 2023, p. 3). In the context of rental housing investment risks go beyond exogenous factors like climate events and regulatory change to include reputational risks (Harman and Ruiz, 2023; Parish, 2023). These risks are related to the social licence to operate in a market centred on the buying and selling of shelter – an internationally recognised human right which is essential for human life and social reproduction. In this context, questions of risk extend beyond legal and regulatory compliance to include wider perceptions of whether a business is responsible and ethical.

Reinventing renting as ethical risk: Risk tolerance, ESG and the BtR model

In this section of the paper, I show how BtR builds from but also alters the risk management practices of landlordism, by reformatting these as ‘ethical risks’ for global investors. While ESG metrics in housing direct attention towards micro-scale phenomenon, such as the outcomes of tenant satisfaction surveys or the credit risk of individual tenants and households, it is important to analyse these in relation to more macro-scalar processes – such as portfolio, company and asset level definitions and strategies of risk management – through which asset manager society necessarily functions. The analysis is presented in three steps: first I highlight direct and co-investment, leveraged investing and ESG disclosure as key risk strategies attached to Get Living, as a pension portfolio company. Second, I discuss how tenants and tenant households, surface in relation to questions of risk in company reporting and disclosure documents. Third, I place these dynamics in the context of classed and racialised dynamics of gentrification in the three London neighbourhoods where Get Living is renting units.

Over the past decade, Get Living has grown to be one of the UKs largest BtR landlords, and claims to be leading the industry in creating a new vision and reality of rental experience in the UK (Get Living, 2021, 2022). Their business model focuses on owning and managing what they describe as ‘premium’ rental apartments. Valued at £2.73 billion in 2022, Get Living’s portfolio includes four ‘operationalised neighbourhoods’: three in East and Southeast London and one in Greater Manchester (New Maker Yards), totalling 4567 rental units. 8 They have numerous additional developments planned at new and existing sites in London and other regional cities across the UK, and project a future portfolio of anywhere between 12,000 and 15,000 units. New development plans also include suburban single-family development on the edges of Surrey and Chiltern Areas of Outstanding Natural Beauty (AONB) on the outskirts of Greater London (Get Living, 2022). Notably, in 2023 Get Living cancelled a planned development due to the Scottish government’s adoption of rent control measures (Lormier, 2023).

Get Living is illustrative of several of the interconnected risk management strategies identified in the literature review: Direct equity investing by pension asset managers, leveraged investing strategies to drive expansion and quarantine risk, and the adoption of ESG disclosures to attract and retain investor confidence.

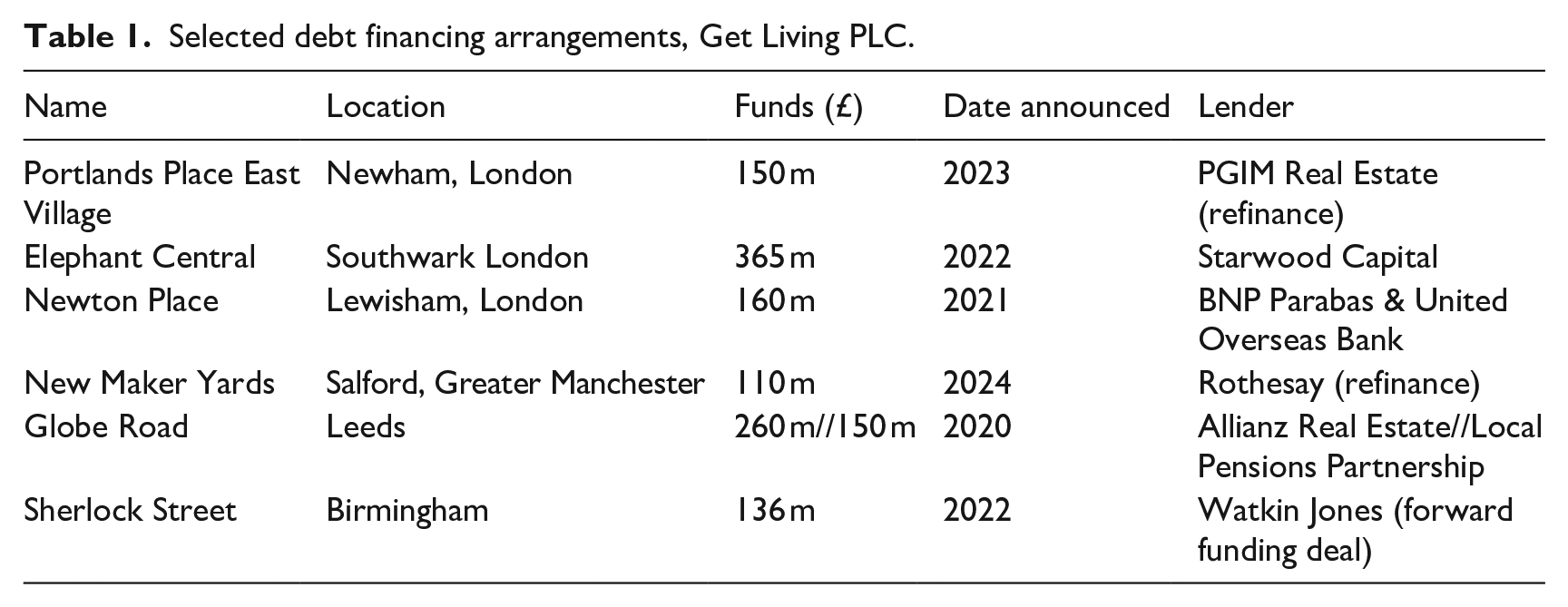

Get Living was founded in 2013 by Qatari Diar (QD), the real estate investment arm of Qatar’s sovereign wealth fund, for the purpose of purchasing and redeveloping the athlete’s village in the wake of the London summer Olympics (Corcillo and Watt, 2022). Dutch pension asset manager APG joined in 2016, and Oxford Properties (real estate arm of OMERS) joined the venture in 2018 (Get Living, 2020). At the time of writing, Get Living is owned by three different investment vehicles: The DOOR consortium led by Delancey and OMERS/Oxford Properties owns a 39% stake; APG likewise owns 39% and Australian pension asset manager Aware Super (AS) holds the 22% (Get Living, 2023a). 9 In addition to these direct equity co-investors, there are also several debt investors, as listed in Table 1 (below).

Selected debt financing arrangements, Get Living PLC.

As previously discussed, AMS development projects are typically tied to specific debt financing arrangements. This offers several advantages to investors including the ability to ‘quarantine’ risks to specific assets (Christophers, 2023). Table 1 provides an overview of debt financing arrangements tied to specific Get Living Properties and the investors that have provided these loans. In their 2022 annual report Get Living (2022: 46) reported ‘access to debt facilities totalling £1,729.8 million’. In the audited financial statements for 2022, refinancing of existing debt facilities, tied both to New Maker Yards (Salford, Greater Manchester) and the Portlands Place development in the East Village (Newham, London) were identified by the independent auditor representing a key ‘material uncertainty. . . that may cast significant doubt on the Group’s and parent Company’s ability to continue as a going concern’ (Get Living, 2022: 60).

The above highlights the importance of being able to attract and retain the confidence of investors, which in turn speaks to the reliance of the REIT model on debt for continued expansion. As Get Living documents highlight: ‘The PRS (private rental sector) industry is highly competitive’ (Get Living, 2022: 90). On the other hand, ‘Barriers to entry into the sector remain high’ so organisations like Get Living ‘are well placed to gain relative advantage’ through their command of ‘a strong balance sheet, prime assets, a pipeline [of new development] and a leading brand’ (Get Living, 2023b: 9).

As also discussed previously, a core aim of ESG analysis is to make risks visible to investors and thereby support the optimisation of risk adjusted returns. Get Living developed their ESG strategy in 2020 and began issuing public facing (as opposed to regulator facing) annual reports in 2021. Get Living is also a participant in the Global Real Estate Sustainability Benchmark (GRESB), an ESG ratings provider focussed on real estate and infrastructure specifically (Feng and Wu, 2021; Gradillas et al., 2021). Their most recent (2023) annual report contains a list of ‘top 5 reasons to invest’. Reason number four is ‘A robust ESG strategy’ (Get Living, 2023b: 11). Their reporting expanded in 2023 to include a stand-alone ESG report in addition to annual reporting. Reporting for 2023 also signalled the addition of asset-specific ESG plans and targets, in addition to company-wide ESG reporting (Get Living, 2023b, 2023c). This addition of asset level ESG reporting aligns with the debt finance strategy outlined above, by making risk visible at the same scale as the debt finance agreements. Importantly, as a REIT which rents property exclusively within the UK, Get Living is subject to ‘minimal legal obligation’ compelling ESG disclosure. The firm’s ambitious and evolving strategy in this regard reflects a desire to operate ‘at the same level as our investors’ as well as a desire to be viewed as a leader, and to ‘stay ahead of growing disclosures requirements’ (Get Living, 2023c: 5).

In Get Living’s reporting documents, tenants and tenant households surface in relation to kinds of risk, such as ‘business’, ‘credit’ and ‘market’ risks. As this section will show, these risks are, in turn, articulated to specific claims about creating ‘social value’ and ‘elevating the resident proposition’.

One of the business risks identified in Get Living PLC’s regulatory filings relates to what they call ‘resident churn’ or ‘potential lack of customer satisfaction’ resulting in turnover ‘at higher than anticipated rates’ (Get Living, 2019: 3). Elsewhere, the possibility of non-payment of rent is identified as a key credit risk. Get Living (2022: 90) explains: ‘The PRS. . . relies on payment of financial obligations by private individuals, whose economic circumstances can alter from time to time’. This may result in rental arrears and even the need for legal proceedings. Market risks include changing consumer behaviours, including ‘higher expectations from landlords’ resulting from the changing demographics of long-term renters (Get Living, 2023b: 19). They further assert that ‘sustainability and social impact will continue to form an important consideration within consumer decision making’ (Get Living, 2022: 19). These statements paint a picture of the lower-risk tenant household as one that is: stable, predictable, capable of consistently meeting their ‘financial obligations’ to the landlord and its creditors, and ‘sustainability’ minded.

These risks are reformatted as ethical risk through Get Living’s social value strategy and broader claims to be on a ‘mission for wider good’ (Get Living, 2023b: 9). The overall business and value creation strategy is described as one which aims to build ‘the exemplar BtR platform, driven by a clear vision and mission, creating sustainable neighbourhoods that are fit for the future and delivering long-term investor returns’ (Get Living, 2022: 12). At the resident level, social value creation includes offering ‘a better way to live and rent’ (Get Living, 2022: 33) emphasizing industry standards like social events, concierge service, ‘free’ internet, and co-working spaces, as well as locational benefits like proximity to shopping, transit, and environmental amenities. As the main landing page of the website further describes: Traditionally, renting comes with compromise – space, décor, location, pets. . . Add to this the times we live in and now more than ever, we are all trying to find our balance and improve our quality of life. Whatever your living is, you can find your perfect balance with us. (Get Living, n.d, a)

In addition to these matters of individual taste and freedom, Get Living also promises to improve renter’s household finances and security of tenure. For example, the Group offers ‘long-term contracts’ of between 1 and 3 years, as well as a ‘resident only’ break clause. On the question of cost, Get Living claim to self-regulate rent increases, by linking these to the consumer price index (CPI). They also claim to voluntarily waive their legal right to claim a deposit, equivalent in value to of 5 weeks of rent. This policy is presented as progressive and industry leading having ‘turned a few heads in our industry’ (Get Living, n.d, a). However, these supposedly sector-changing promises are only available to certain tenants: the highest earning, with high credit scores. Those who are working part time, and/or volunteering, and/or receiving some retirement income but do not fulfil credit and income criteria above must either pay all rent, up-front, for the duration of the (1 year minimum) lease, or pay a deposit equivalent to 5 weeks rent and have a guarantor. Likewise, students of any income and credit rating as well as people with poor credit, regardless of income level, must pay all fees up front or pay the deposit and have a guarantor (Get Living, n.d, b). As noted by Get Living (2022: 90) ‘The effectiveness of the Group’s [credit check and guarantor] policy in this regard is evidenced by the Group’s consistently high [rent] collection rates of 97%’

Together, these strategies address the risks outlined above: ‘resident churn’, the need for ‘customer satisfaction’ in a highly competitive sector, and of course, the credit risk of tenant non-payment. However, by articulating social value claims to some relatively conventional risks of landlordism, Get Living positions itself as good and innovative landlord, providing an elevated experience of renting for tenants while generating ethical risk driven returns for investors. Yet, while Get Living has introduced certain ‘innovations’ other, and arguably more problematic aspects of landlordism remain. These include a preference for tenants profiled as low risk through credit checks and employment and income disclosures and a firm opposition to rent control.

While credit, income, and employment criteria are constructed as ‘neutral’ and ‘objective’ metrics, their deployment should be understood in relation to the ‘inextricable connection between racism and capitalism’ (Fields and Raymond, 2021). In the context of the racialised labour, housing and credit/debt markets in which characterise capitalist societies, these metrics and their incorporation into investment risk management strategies can be understood as a form of abstraction which creates an appearance of neutrality as it transforms individualised biases against racialised bodies into automated systems (Fields and Raymond, 2021). Furthermore, this form of abstraction is necessary for the creation of what Parfitt (2020) calls ‘ethical risk’ in the sense that it links the imperatives of investment risk management to normative claims to be changing renting for the better, for everyone. However, the risk appetites of investors – not justice or ethics per se – are what ultimately defines the parameters of what kinds of change or innovation are possible. Yet, as a material reality risk is experienced very differently not only between investors and households (Parfitt, 2020) but also between different kinds of households. As the final section of the paper will show, this construction of risk maps on to existing geographies of gentrification and uneven development in ways that present profound challenges to the narrative that everyone wins.

As argued by Fields and Raymond (2021: 1626) financial accumulation is structurally dependant on processes of abstraction that create distance between those parties that enable and benefit from financialisation and the ‘often-violent impacts of the projects on the ground’. The construction of ethical risk, as detailed above, is precisely such a form of abstraction which agglomerates calculations of ‘risk’ and separates these from their material and embodied contexts. Placing the foregoing analysis of risk in its urban contexts suggests that these abstract discussions of risk and related claims regarding social value obscure and legitimise ‘the reproduction of racial hierarchies in housing and property’ (Fields and Raymond, 2021: 1626). Further, as Nethercote (2022b) has shown, the process of creating life-optimising spaces of home for some, is structurally dependant on the presumption that existing practices of making home are deficient and must therefore give way to ‘revitalisation’.

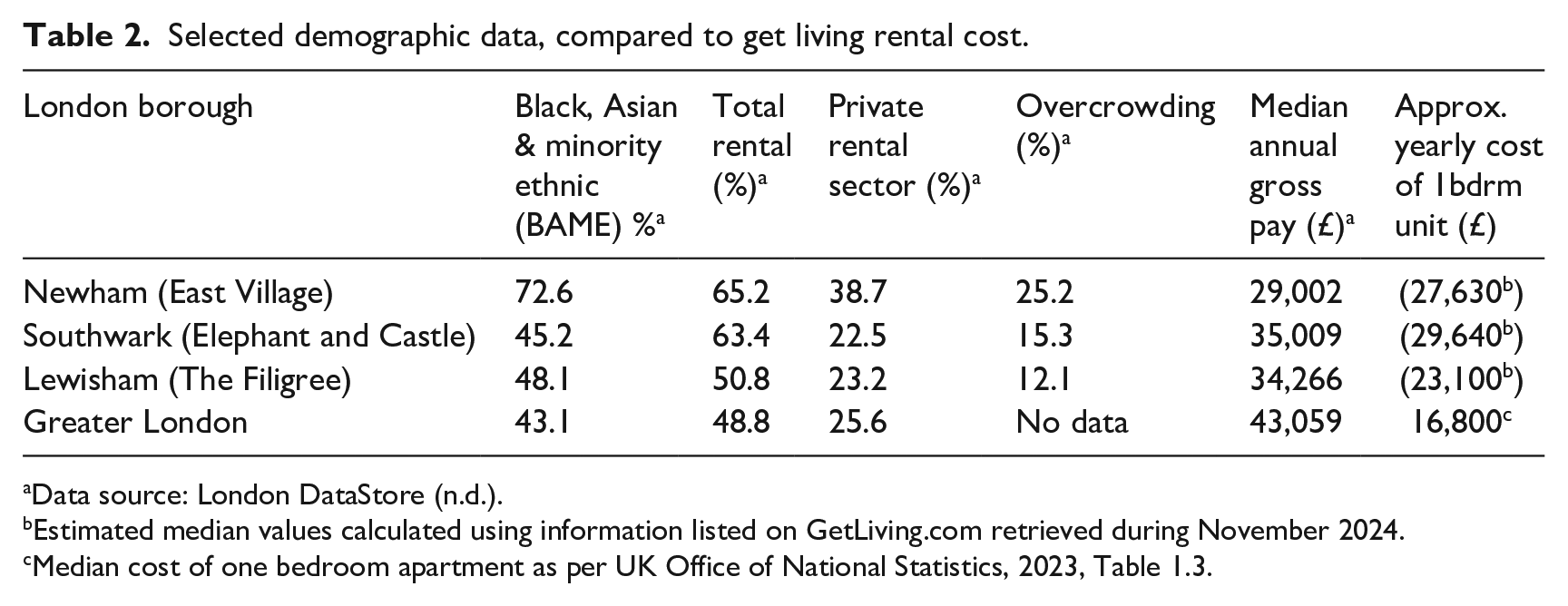

Previous research on gentrification in East and Southeast London has documented significant classed and racialised ‘socio-spatial inequalities and segregations’ (Corcillo and Watt, 2022, p. 16) in all three Boroughs where Get Living is currently renting apartments (see Table 2) (Corcillo and Watt, 2022; Ferreri, 2020; Lees and Ferreri, 2016; Wallace, 2020; Watt, 2013). In their study of the East Village, in Stratford, Newham, Corcillo and Watt (2022) collected demographic data to understand how the population of the East Village compares to its surrounding area. In marked contrast to the broader borough in which is it located, some 68% of surveyed residents of the East Village identified as White British or other white. Yet, while 73% of Newham residents identify with the broad category of Black, Asian and Minority Ethnic (BAME), only 32% of the largely young professional demographic inhabiting the East Village identify in this way (Corcillo and Watt, 2022; London DataStore, n.d.). Both Southwark, the location of the Elephant and Castle regeneration, and Lewisham Central, the location of the Filagree, are also areas with ongoing struggles around racialised gentrification processes (Ferreri, 2020; Lees and Ferreri, 2016; Scanlon et al., 2018; Wallace, 2020).

Selected demographic data, compared to get living rental cost.

Data source: London DataStore (n.d.).

Estimated median values calculated using information listed on GetLiving.com retrieved during November 2024.

Median cost of one bedroom apartment as per UK Office of National Statistics, 2023, Table 1.3.

As Table 2 (above) illustrates, each of the three boroughs in which the developments are located have BAME populations above, and median incomes below, that reported for the Greater London Area as a whole. Population data show that within the broader BAME category, the top three largest groups for each borough are Indian, Bangladeshi and Black African (Newham); Black African, Black Caribbean and Other Black (Southwark) and Black African, Black Caribbean and Other Asian (Lewisham; London DataStore, n.d.). Particularly notable is the intersection, in Newham, of a substantial majority racialised population, with lower annual earnings, high proportions of the population living in private rental sector housing, alongside significantly higher rates of rates of overcrowding, a key indicator of housing unsuitability.

These data are at the Borough level. In order to obtain a more granular image, I further analysed Lower Layer Super Output Area (LOSA) maps of local deprivation (mysociety.org n.d.) in comparison with the geographic location of development sites. LOSAs are a composite, relative deprivation indicator, which compares deprivation in the smallest geographic data areas to England as a whole. This analysis revealed that all three developments are sited in some of the most deprived areas in their respective Boroughs, in LOSAs in the second and third lowest deciles (e.g. deciles with second and third highest deprivation, as compared with England as a whole). Nearly three quarters (72.5%) of all LOSAs in Newham fall within the bottom three deprivation deciles. In Lewisham this number is 51% while in Southwark it is 52% (mysociety.org, n.d.).

Furthermore, as Table 2 demonstrates, the estimated annual cost of renting a one-bedroom apartment in a Get Living property in the two London boroughs where units are currently available ranges from 67% to 95% of the median individual annual gross pay in those boroughs (Table 2). Furthermore, rents in these properties are significantly higher – in some cases almost double – than the median costs of a 1-bedroom apartment in all of London, the most expensive rental market in the UK, and among the most expensive globally (Beswick et al., 2016).

Get Living’s marketing materials invite prospective tenants to ‘Live in a neighbourhood where everyone can connect and thrive’ (www.getliving.com). Yet, as the foregoing suggests these apartments are not only unaffordable for existing residents. Instead, it appears as though certain kinds of tenants will necessarily be actively excluded through the application of strict credit and employment screening for access to these ‘premium’ apartments in gentrifying, lower income and racialised neighbourhoods. The construction of BtR as first and foremost an asset class means that the audience for the abstracted risk profiles of tenant households consists of a range of global investors, many of whom have brands that are tied to ideas and discourses around sustainability. Here, ESG plays a key role in smoothing the tensions between the violence of financialised investing in shelter and the ostensibly public and benevolent nature of pension investing and the fulfilment of fiduciary mandates in the 21st century.

Concluding discussion

As we can see from the above, unlike the image of slum lords at scale which emerges from some of the literature on rental housing financialisation and the behaviour of REITs and private equity, operators in the BtR sector are often at pains to present themselves as a new kind of landlord: compassionate, responsible, and possessed of a kind of ethical proximity to tenants, rebranded as ‘residents’. Professional, white-collar tenants, presumably, expect and deserve ‘professionally managed apartments’. Indeed, the picture presented above suggests that it is quite likely that some tenants are benefitting from this ‘revitalised’ experience of renting.

However, this vision of renting remade calls for skepticism, on three interconnected counts: rights and consumerism, the relationship between risk and racialisation, and the matter of ethical risk. Regarding the first, this study suggests that the BtR model explored above recasts renters as consumers rather than people with rights. Whereas under international human rights law all people theoretically have universal entitlements to safe and affordable housing, security of tenure, and non-discrimination, consumers are cast as selecting these as matters of preference and purchasing power. However as documented above it seems clear that few longstanding residents of the areas in which these developments are being built will have the income and credit history to live in these premium apartments. Furthermore, the sector specific investment risks identified by the firm define the limits of how and for whom renting can be reinvented.

Second, the connection of longstanding landlord practices like credit checks to asset managers investment and ESG strategies suggests that tenants’ financial lives are being ‘anchored’ (Langley, 2018) in the market in novel ways. While BtR landlords may be market following in the means used to screen tenants, the hype surrounding the fee waiver and other ‘innovations’ in the sector need to be read in the contexts of both the construction of Get Living as a portfolio company that aligns with investors evolving risk-return calculi and the specifically racialised and working-class areas experiencing gentrification where all three London properties are located. While the marketing promises places where everyone can connect and thrive, the risk appetite demands tenants who can demonstrate the capacity to pay for a premium product. Those without well-paying jobs and immaculate credit are confronted with what for many may be an impossible demand – a full year of rent or a 5-week deposit backed up by a guarantor. This renovated vision of renting is not for them.

Third, on the matter of ethical risk, the BtR model described above does not satisfactorily resolve questions relating to what it means to support the social reproduction of present and future retired workers in one place via financialised investing in essential housing and infrastructure elsewhere (e.g. Lewis, 2022). While the model described above does mark some important differences from other financialised landlords, the risk management and profit generation model both depends upon and reproduces existing dynamics of racialised housing and property markets. Furthermore, the model raises questions about how social value is defined and operationalised as ESG disclosures and reporting become increasingly standardised and regulated. Arguably, one of the most pressing demands that organised tenant movements are making across the UK and North America is for (the reinstatement of) meaningful rent controls, given the role of escalating costs (e.g. affordability) in displacement (e.g. security of tenure) and other forms of financial hardship (e.g. food and energy poverty). Yet, in 2023 Get Living announced they were pausing their development in Glasgow, Scotland, because of the Scottish government’s plans to introduce rent control, as a key policy tool to maintain affordability across the rental housing market. Arguably, it is the interconnected nature of the three pillars of the right to housing – affordability, security of tenure and habitability – that lies at the heart of growing tenant’s rights movements, rent strikes and demands for rent control in both the UK and Canada.

These dynamics raise questions about the relationships between pension beneficiaries, investors, and those whose lives, bodies, and communities are the objects of investment. The construction of ethical risk presents the social and public ‘goods’ that are intended to result from flows of pension capital between renters in the UK and workers in Canada, as in the example furnished here, as accruing both in the communities where rental housing is built, and the communities to which investment funds are patriated. However, risk is differently lived by the relatively privileged but internally diverse groups of workers whose retirement savings are buttressed by fiduciary principles, and those who are, by definition, left out of this vision of renting reinvented. This is further complicated by the fact that these financial flows are managed by professionals with different backgrounds and interests from both the workers and renters on either side of the investment. Thus, it is important to note that while the value of the capital invested on behalf of pensioned workers may flow freely across the Atlantic, it does not necessarily follow that their values or perceptions of ethics and justice are embodied in or even sought by fiduciary boards in these processes (Weststar and Verma, 2017). These tensions are structurally and legally enshrined characteristics of pension investing in housing and infrastructure.

Footnotes

Acknowledgements

The author thanks Jessa Loomis and Melissa García Lamarca for insightful comments on previous drafts of the paper. This paper was presented at the Royal Geographic Society conference in London in 2023 and Urban Affairs Association conference in New York in 2024 and has benefitted from discussions among panellists and attendees at these sessions. All errors and omissions are the sole responsibility of the author.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project has received funding from the European Union’s Horizon 2020 research and innovation programme under the Marie Sklodowska-Curie grant agreement No. 101033614.

Ethics statement

This study received ethical approval from the De Montfort University IRB (approval #474768) on August 15, 2022.