Abstract

Private renting increasingly comprises a complex ecosystem of actors who assemble housing within the market, and collect rental income and data from tenants, and data on the material assets themselves. Our analysis – at the intersection of rentier and platform capitalism – focuses on landed (material real estate) and technological (digital infrastructure and data) property in Australia’s private rental system. Drawing out relationships between the various actors – landlords, rental property managers and real estate agencies, software developers and providers, property developers and investors – and both their properties and their uses of Proptech (property technology), we show how housing and technology are being leveraged for profit in new ways. In Australia, landed property retains its precedence for established (individual and institutional) landlords, whose interest in Proptech relates to enhancing or value-adding to rental housing assets. For Proptech and institutional real estate players seeking to consolidate both landed and technology property, capturing the tech landscape is increasingly important; indeed, securing control and/or consolidation of technology property is a key motivation for building and/or using Proptech among the largest property developers. Our findings show how rent extraction operates across and between different types and scales of property and market actors, and in new ways that differentiate the figure of the rentier while upholding the dynamics of the rentier model.

Introduction

Tensions are emerging in urban studies between the competing ideas of financialisation (Aalbers, 2017), assetisation (Adkins et al., 2021) and rentier capitalism (Christophers, 2020). In a provocative turn away from the financialisation literature, Christophers (2020: 5–6) argues that the: overall [economic] process can be understood as one not of financialisation, but rather of rentierisation, whereby, to paraphrase Krippner, one might say that profits have increasingly taken the form of economic rents – including but not limited to financial rents – rather than income from trade or commodity production.

Christophers’ broad rentierisation thesis cuts across work concerned with the role of monopolisation, gatekeeping and rent extraction in digitised capitalism (Birch and Cochrane, 2022; Khan, 2017; Sadowski, 2020) and in land and housing markets (Kay and Kenney-Lazar, 2017; Manning, 2021; Penny, 2022). Concomitantly, much has been made of the disruptive nature of digital platforms in housing, from Airbnb’s impact on the rental market (Gurran and Phibbs, 2017) to the discrimination that platforms potentially facilitate (Ferreri and Sanyal, 2022; Wolifson et al., 2023). The ability of platforms to reconfigure the territorial networks of consumption in the housing rental sector is underwritten by their function as flexible and agile mediators between people, places, buildings and rents. Shaw (2020: 1050) refers to this as platform real estate, a process that is ‘reliant upon digital technology and dependent upon the accumulation, storage and processing of digital information in a manner that is previously unprecedented in scale or in its application to […] the real estate market’. Unexplored, as yet, in this context of platform real estate, are the newly defined roles of a diverse set of actors – and their assets – in upholding rentierisation. This article attends to this gap, at the intersection of rentier and platform capitalism, through examining the role of digital technologies – known as Proptech – in rent extraction by various actors within Australia’s private rental housing sector.

As in many nations, rising house prices and rents across Australia’s capital cities have delayed or suppressed home ownership (Adkins et al., 2021). Consequently, private rental housing is no longer viewed as a short-term transitional tenure on the pathway to homeownership. The growth in renter households in Australia over the past decade – now around 26% of total households (Australian Bureau of Statistics (ABS), 2022) – is in large part due to the diminished opportunities for home ownership among younger people (Gurran and Bramley, 2017). Alongside the growth of the private rental market is increasing investment in new digital housing technologies. Known as Proptech, these industries attracted an estimated US$32 billion in venture capital investment funding in 2021 alone (Center for Real Estate Technology & Innovation (CRETI), 2021). In the private rental sphere, tenants’ rental journeys, from securing a property to eviction, are increasingly governed by such digital platforms, and their data are being gathered up by analytic infrastructures in the process (Fields, 2022). Changes to the scales of engagement facilitated by platformisation made digital technologies a key enabler of the post-crisis financialisation of housing in the USA, as large institutional investors were able to assess and invest in foreclosed properties at a distance (Fields, 2022). The growth in individual and institutional investment in rental housing in the post-2008 era has also allowed real estate tech companies to enter the practices and management of renting and tenancy. Credit-reporting companies, for instance, have capitalised on their data holdings to roll out rental platforms that screen the credit history, eviction history and previous lease payments of prospective tenants (McElroy and Vergerio, 2022; Migozzi, 2022). In this ecosystem of private rental, Proptech – beyond the material properties of the cloud computing servers largely controlled by Google and Amazon – as well as the intellectual property of the digital products and the digital data these products produce often constitute valuable assets. This Proptech landscape is up for grabs: who controls it, and to what extent, depends on the ability to create, buy or rent the housing and technology assets in question.

Focusing on the housing (i.e. physical real estate) and technological (i.e. digital and intellectual) property in Australia’s private rental system, in this analysis we develop a picture of the various actors, their property and how they are using Proptech. For some rentiers, both material and intellectual property are at play for rent extraction; we explore the relationships between these two forms of rentier capitalism. We show how housing and technology are being leveraged for profit in new ways within an antipodean landlord environment that involves different types of landlords assembling houses/apartments within the private rental market, collecting rental income from tenants and increasingly collecting data about the material assets and tenants in different ways.

To progress this argument, the remainder of this article is structured as follows. In the next section, we provide an overview of the research context and methods for studying Proptech in a somewhat distinctive antipodean landlord environment. We then turn to our empirical material identifying three key ways in which land, Proptech and rent intersect, these being the extraction of landed and platform rents; Proptech and data consolidation as a dual asset; and importantly, the continued underwriting of Proptech by land value. We conclude by reflecting on the increasing commodification of the tenant experience characterised by two forms of extraction: the use of Proptech to amplify rent from landed property, and the trend to consolidation of tech and data for market control.

Researching Proptech in the antipodean landlord environment

In Australia, individual and large commercial landlords are the key actors in the private rental sector (comprising both houses and apartments), with the Proptech sector emerging as a critical new intermediator. Similar to the UK (Wainwright, 2023), private residential rental properties in Australia remain largely in the hands of individual landlords. This group has long been supported by government policies and tax arrangements that have seen their asset base increase, both in terms of the total property in ownership and the fiscal value and rents of those properties (Adkins et al., 2021). As property inflation took on a structural role in 21st-century capitalism, individual landlords set about acquiring and operating real estate assets, enabling them to extract rent whilst pursuing future capital returns (Adkins et al., 2021). In this and similar contexts, the privileging of such landlordism has been discursively ‘rationalised around an individualised welfare strategy’ (Ronald and Kadi, 2018: 792), with the so-called petit rentier or mum and dad landlord politically valorised and framed as providing essential housing (Hulse et al., 2020). Consequently, around 2.55 million households or 26% of all households in Australia rent from private landlords (ABS, 2022; Australian Institute of Health and Welfare (AIHW), 2022), who may own one or more leased properties. These properties are often managed, for a percentage-of-rent commission fee, by property managers, who typically work for real estate agencies. Poor regulation of building quality, non-existent rent control and limited tenure security have led to poor-quality private rental stock, precarious living conditions and housing insecurity (Morris et al., 2017), and have generated tenant advocacy movements to redress these issues. Australia is one of the few places outside of post-socialist countries where these individual landlords generate at least 10% of their income from asset ownership (Goldstein and Tian, 2022: 1569). As such, the residential property market represents a substantial source of personal wealth in Australia, both in terms of holding property and through the generation of long- and short-term rents.

The institutional landlord landscape in Australia is predominately organised around what has recently been labelled build-to-rent (or build-to-sell later), a practice and development model that has been around for decades in Australia (Pawson and Milligan, 2013). As a stand-alone rentier strategy, the questionable profitability of the build-to-rent business model likely explains the property sector’s lobbying of government for financial and taxation incentives. Yet, profitability of the model itself is only one consideration. Large institutional landlords in Australia, such as Mirvac and Meriton, are vastly different to the large institutional landlords in the USA and UK, such as Blackstone. The latter are effectively large asset management companies with limited property development and tenancy management experience. By contrast, developers like Mirvac and Meriton have a long history of developing apartments for sale and, more recently, for rent. Large institutional landlords in Australia are large property developers who are experienced with staging the delivery, timing and volume of housing to the market, 1 and who increasingly possess property and tenancy management expertise.

Within this distinctive antipodean landlord environment, this study investigates the Proptech that is impacting private renting in Australia. Some technologies have been developed by, or for, established actors in the private rental sector, while others purport to be disrupting various aspects of the private rental sector, for example through short-term renting, flatmate finding, tenant-and-landlord matching and tenant bond insurance (Maalsen and Gurran, 2022; Porter et al., 2019). The uptake of Proptech is being shaped by who these landlords are, their various property development and tenancy management histories and their organisational practices. We approached this analysis with empirical material drawn from a three-year research project partnership with three large tenant unions, which investigates the current landscape and potential implications of Proptech for private rental tenants. We have conducted 14 interviews with key informants from the Australian real estate sector and Proptech sectors and with Australian tenant advocacy groups, as well as making observations of industry events.

This analysis concentrates on interviews with stakeholders in the Australian Proptech landscape and observation conducted at an industry workshop that included real estate entrepreneurs, real estate groups and Proptech developers. The aim of our analysis is to show which kinds of rentiers control (and/or create) and draw income from different types of material and technological property, and how. In Australia’s private rental market, rent extraction is operative across different types and scales of property and owners, and in ways that differentiate the figure of the rentier while upholding rentier dynamics.

Property, rents and rentiers … and their assets

In liberal democracies, the socio-cultural imaginary of property often invokes discrete and bounded spaces or objects. Sometimes this perspective misses the ‘inherently relational’ character of property as ‘a social institution that involves multiple people, all with interests in a shared resource’, and how ‘the terms under which we participate in these relations vary profoundly’ (Blomley, 2020: 38). Property is thus always about power, ‘creating complex relations of dependence, sovereignty, and privilege’ between people (Blomley, 2020: 38). Of particular importance to our analysis is how sovereignty enables property owners to charge those dependent on shelter and/or connectivity or information for the use of material and/or technological property they control. These hierarchical relations of access and use are the basis of and necessary precursor to rentierism.

The emergence of Proptech has augmented the forms of property that are operative in the private rental housing sector, meaning the sites and targets of rentier activity within the sector go beyond landed property. In addition to landed property (i.e. houses and buildings), technological property (i.e. digital ecosystems and data) is a growing basis for rent extraction. While a house owned by a landlord and occupied by tenants appears quite different from a digital platform operated by a software company and subscribed to by users, both the house and the platform are controlled by an economic actor who receives income ‘purely by virtue of controlling something valuable’ (Christophers, 2020; Sadowski, 2020: xvi, emphasis in original). Both material and technological property are at play in Australia’s private rental sector, and thus the relational dynamic between rentier landlords and tenant renters can vary significantly depending on which kind of property is involved.

Digital real estate technologies enable rent extraction through various configurations of landed and technological property. A conceptual distinction needs to be drawn between what we are calling ‘landed property’ and ‘technological property’, and the various rents that are respectively collected from them. For our purposes, the idea of landed property includes the land and its appurtenances, and it points to material property in and on land. In the political economy, there is a long and ongoing debate about the relationship between land and property, and the rents that can be garnered from bringing the two together. For Harvey (1982: 331), following Marx, land rent is ‘a payment made to landlords for the right to use land and its appurtenances’, and thus it is the total rent paid including any fixed capital on the land, such as buildings. 2 Individual landlords might make use of digital technologies, such as third-party rent-setting algorithms, to maximise land rent. And collectively, landowners (in concert with the state) ‘create artificial scarcity by keeping land off the market on the one hand, and [creating] exclusivity in land use on the other’ (Ward and Aalbers, 2016: 1769) to realise anticipated returns on their investment in land (Harvey, 1974; Harvey and Chatterjee, 1974).

Technological property is a category we use to indicate digital assets including the infrastructure, software and data that make up rental Proptech. Much like landed property, digital assets can be bought, sold and rented. We can thus add the ‘thing-ification of knowledge […] so that it can be alienated and exist as property’ (Birch, 2020: 14–15) to the abstraction of land for the same purpose. Indeed, as Sadowski (2020: 565) shows, ‘controlling access and collecting rent’ is the ‘underlying economic dynamic’ of most technologies and services created by digital platforms. While the focus of the digital rentier’s gatekeeping activity may be to data or software applications rather than the buildings to which landlords control access, the logic of rent extraction is the same (Sadowski, 2020). Here, we see how ‘resources and assets […] derived from technoscientific knowledge’ (Birch, 2020: 8), such as intellectual property and personal data (Nethercote, 2023), are an increasingly important site of contemporary rentiership.

Theories of digital rentiership emphasise how digital technologies are used to extract rent through the control – or enclosure – of a range of digital ecosystems, data and interactions (Birch and Cochrane, 2022; Sadowski, 2019). In the private rented sector, for example, property management software can become a resource from which Proptech companies derive income by renting access to landlords. This income stream corresponds to the concept of enclave rents, which arise though the creation and control of a digital ecosystem, ‘locking in users […] to a particular techno-economic arrangement’ (Birch and Cochane, 2021: 11). The idea of platform rent (Christophers, 2020: 179) attends specifically to the monopoly control of connectivity and the possibilities for rent extraction therein. Platform rent is especially salient in our current era of digital innovation; within a digitally networked system, expanding the number of users and their interactions is a crucial means of increasing the value of that system, within which the platform itself is understood as ‘a distinct mode of socio-technical intermediary … incorporated into wider processes of capitalisation’ (Langley and Leyshon, 2017: 11). Platform rentiers enable and expedite interactions between users; charging for access to and use of that forum ‘is nothing if not a rental charge’ (Christophers, 2020: 180).

Through the centrality of residential property ownership to middle-class politics and, in Australia, economic livelihoods (Adkins et al., 2022; Goldstein and Tian, 2022), the expanded role of corporate and institutional actors in rental housing markets (Fields, 2022; Nethercote, 2020) and the status of tenant data as a form of capital that can be aggregated and enclosed (Nethercote, 2023; Sadowski, 2019, 2020), the tenant experience is subject to multiple forms of rentier capitalism at the hands of different rentiers. Indeed, this multiplication of extraction extends the uneven social relationship that the private rental sector is premised upon, and which Byrne (2019) describes as the residential rent relation, characterised by an antagonism between accumulation and social reproduction, essentially two competing values of housing as an asset and housing as home (see also Madden and Marcuse, 2016). Proptech has the potential to deepen this antagonistic residential relation by further extracting value from the digital labour (Jarrett, 2022) that tenants undertake as part of their rental experience.

Echoing Christophers (2020: 26), this situation prompts us to ask, does the intersection of rentier and platform capitalism further tilt ‘the balance of power from tenants towards landlords, especially in the case of residential property’? With the ideas of property, rents and rentiership outlined above, we move next into an analysis of rentier capitalism and the digitalisation of renting in Australia, and show how it is primarily organised around the social, technical and economic production of new rental technologies, as well as the reproduction of longstanding rental discrimination and exploitation. Theorising platform and rentier capitalism together allows us to go in search of a unique set of landed and technological property and their respective rents and rentiers.

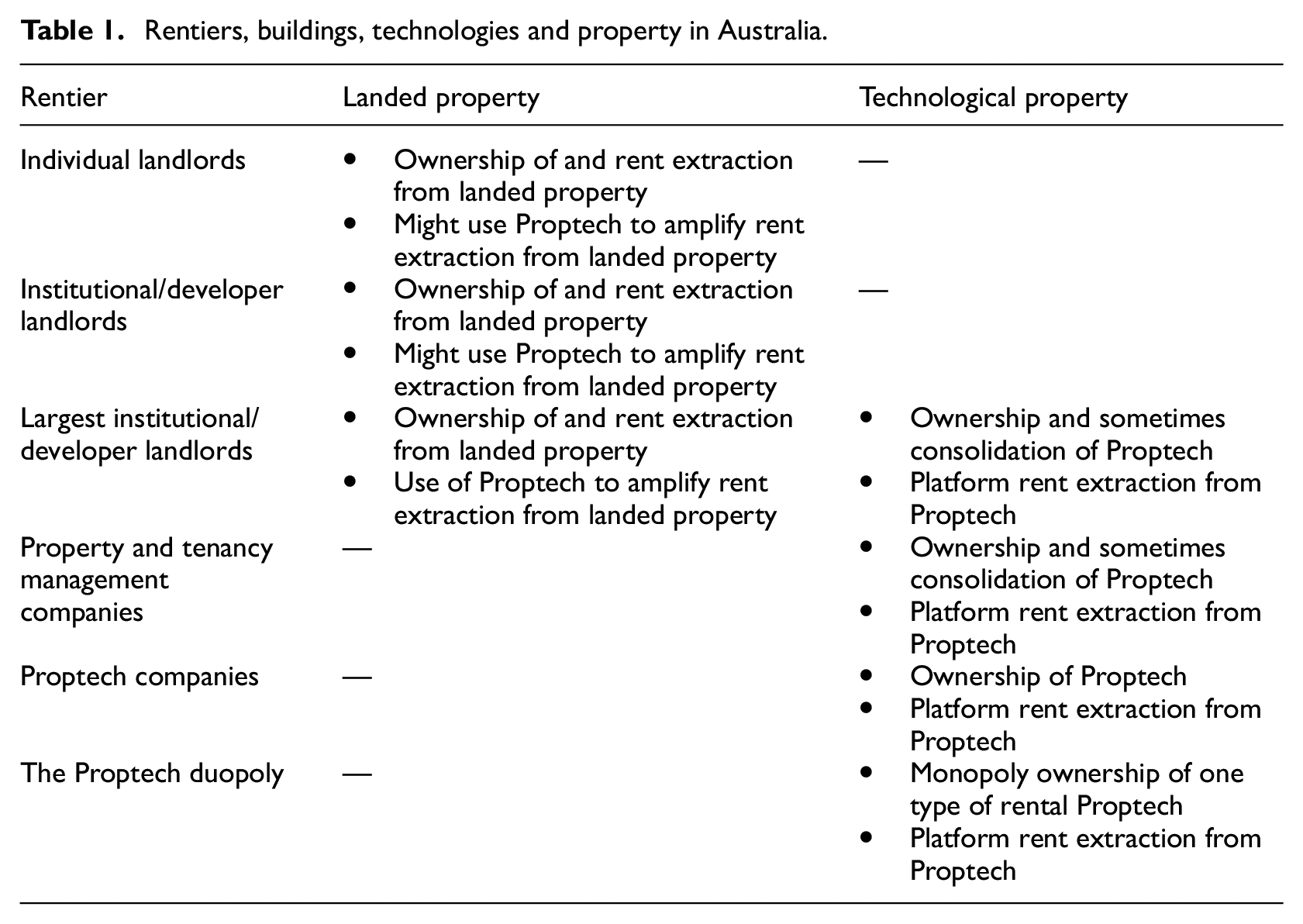

While Australia does not have a large corporate landlord sector per se, it does have large property developers who act as institutional-scale rentiers and are uniquely positioned to capture rent from both material and technological property. As summarised in Table 1, these players mobilise platform real estate to extract not only rents from their property portfolios but also platform rents, that is, income from the control of rental data and technologies (Nethercote, 2023). This group is stretching the traditional definition of a rentier by not only producing landed properties that are then rented, i.e. building rental housing and apartments, but, as will be discussed, also building Proptech. In contrast, we found that individual landlords largely use platform real estate to amplify rent extraction from their landed property only. Meanwhile, for the Proptech industry, rent is extracted through software-as-a-service models, with tenant data becoming a commodity itself (Sadowski, 2019, 2020).

Rentiers, buildings, technologies and property in Australia.

Proptech: Technologies for streamlining tenancy operations

With the total economic value of Australia’s residential real estate sector reaching AU$9.1 trillion in 2021 (Core Logic, 2022), extraction opportunities abound for potential technologies to facilitate the development, acquisition, operation and management of rental properties and tenants. Australian Proptech developers operate in a space of AU$512 billion in annual residential sales and a further AU$15 billion in sales commission, AU$360 billion in annual construction revenue and AU$4 billion of annual residential rental commissions (Proptech Associate of Australia, 2022). For Proptech developers, these numbers represent market opportunities. Yet, for landlords – both individual and institutional – high valuation of their landed assets reflects their continued importance as vehicles for profit. While enabling new forms of property management, Proptech in this context, for landlord rentiers, is mainly used to maximise the capital value and rental opportunities from existing rental housing. Many, although not all, of the individual and property developer landlords we spoke with for this study were primarily interested in using Proptech to enhance or value-add to their primary landed asset. For these actors, any platform rents that were generated through Proptech were a bonus.

There is a plethora of Proptech companies in Australia. They can emerge and dissolve quickly, with some companies being acquired by larger companies and a smaller number retaining ownership of both the technology and data to rent out as ‘services’ to larger companies. The ecosystem of private rental sector Proptech in Australia spans the entire rental and property management process, from buying and selling properties to managing tenancies and buildings. The bigger Proptech players are looking to create whole-of-system Proptech products, which bring together a cross-section of this Proptech ecosystem in one product. There is a disparity between sale and rental commissions, when measured in those time frames, a disparity reflected in Proptech investment itself. A Proptech manager from a large property and tenancy manager company suggested that: The challenge with property management is that it’s hard to get close to the money in the same way that you get close to the money when you’re doing a sale. So as a result, you’ve ended up with this lack of investment in property management software with lack of coordination in the way that it’s approached. (Proptech lead, large property and tenancy management franchisor)

One build-to-rent developer we interviewed lamented the lack of rental profits being generated by the Proptech sector as a result of this lack of a coordinated approach: ‘[The housing] asset operations and management space [are] drowning in technology, although most of it is kind of not adding up to a lot of value’ (Proptech lead, large developer landlord). For this developer, creating ‘value’ means creating efficiencies that will increase profitability from land rents (see also Nethercote, 2020). Tenant management itself is, however, ripe for Proptech innovation and solutions; its innumerable and widespread problems, in Australia, extend from poor maintenance to slow bond returns. Yet, in addition to a lack of real estate sector knowledge by opportunistic Proptech developers, most Proptech companies are not tenant-experience focused. Rather, their Proptech ‘solutions’ focus on developing valuable assets for the private rental sector by either commodifying the tenant experience as a data source or commercialising it through introducing new fee-based services to drive down management costs and, in turn, increase land rents.

Some Proptech products servicing this market aim to network property managers into tenancy management in new ways, while others attempt to do away with property managers altogether. Others, again, are focused on ‘value-add’ functions that aim to drive up existing rents or create new rents. One Proptech developer spoke of applying ‘x-as-a-service’ models (common in tech, see Sadowski, 2020) to properties to improve residential affordability through maximising rent extraction. For example, one property developer suggested that: Red tape gets in the way […] If your own investment property can be revenue generating, then that helps with affordability […] Being able to have greater flexibility for time-of-day use [and] using residential properties as commercial spaces […] When I’m out of my apartment during the day, why can’t it be used as daycare centre? It’s sitting empty. Or why can’t the building’s amenity space be used as a daycare centre when nobody’s there? (Proptech developer, large developer landlord)

We see this type of utopian thinking more broadly across the build-to-rent and individual rental sectors in Australia, where property developers and larger real estate agencies are developing what they call the ‘digital asset’ side of their private rental sector business by drawing on the ‘smart’ or ‘autonomous’ building discourse. The private rental sector is using Proptech in an attempt to optimise the day-to-day management and administration of both property (i.e. assets) and tenancy (i.e. people) management, for example by using ‘smart’ real estate technologies to monitor, optimise and control energy and water use (i.e. building performance), adding virtual reality, keyless entry and online payment applications to streamline tenancy management and ‘value-adding’ to the rental property by offering cleaning, dog walking, post and other services for a fee and enabled by Proptech. ‘More insidiously’, argues Nethercote (2020: 860), ‘digital technologies may be deployed by landlords to, for instance, profile tenants and thereby favour and exclude those most amenable to their investment imperatives’. The property manager and the economics of the rental transaction were centred in a forward-looking statement from one Proptech industry observer, with little thought given to the potential tenant’s experience: [The property manager is …] going to be able to do higher volume, because a lot of the admin is just going to be automated […] Why should a real estate agent […] open up a door for somebody to come in and take a look around for five minutes? […] That’s a terrible use of their time. So, there’s […] a lot of areas where there’s greater efficiencies that can come in, and tech can help with that. And then they can concentrate on the stuff that is higher value. (Proptech industry observer)

The emphasis here is on the role of technology in property management for streamlining various production and rationalising operations.

Proptech and the data consolidators: The dual asset-holders

While land rents from rental buildings are evidently still important when analysing the Proptech sector, for some actors intermediation logics, enacted via platform rents, are an important reason for building, using and/or consolidating Proptech; we call this group the Proptech and data consolidators. Furthermore, the fate of small-to-medium Proptech companies is often tied to a small cohort of large property and tenancy companies, property development companies and Proptech companies who are controlling, or seeking to control, the key land and technology assets in the private rental market. Considerations of control of Proptech assets are front of mind for these players in their decision-making around Proptech use: ‘We’ve got to think about how much do we want to control a supply chain’ (Large property and tenancy management employee). As such, Proptech asset control typically falls into one of three modalities: buying a ready-made Proptech product, partnering with a Proptech company to develop the product together or funding, designing and building the Proptech in-house to meet their needs. In the two latter cases, the large players may effectively ringfence the market through an in-house proprietary Proptech product or by on-selling or renting their new Proptech product to others. Due to their market share, these large players also wield disproportionate power in shaping the requirements and demands of Australian Proptech, as one real estate agency franchisor suggested: As a singular software provider, to make one [Proptech] product that suits everybody seems […] basically impossible, because at the high end of the market, you’ll have a group like us, and we won’t partner with anybody unless they customise the crap out of their software. So, we make it hard for Proptechs to get started. And we’re not the only one who does that. And franchise groups represent about 49% of the market […] And then at the other end, it’s a very, very, very long tail of individual businesses that […] don’t care, they just want the cheapest thing possible, they don’t want to deal with the switching cost of going to a new provider. (Large property and tenancy management employee)

As such, some of the larger real estate and property development players are dual asset-holders, that is, they hold both landed and technological property on their books. One large property developer, poised to enter the Australian build-to-rent space following overseas success (Van Leeuwen, 2022), was also entering the software-as-a-service space with an end-to-end business platform developed through the company’s new digital technology arm that they could lease to other companies. As they told us: Players come along […] and they build something proprietary for themselves and you don’t unlock any of the value […] So, we’re trying to offer something up that has a degree of open source to it so the other parties [… who are] interested in being able to develop land or operate an asset [can use] technology [to] do that more effectively. So that’s our business approach, is to try and create something that will serve the industry more widely. (Proptech lead, large developer landlord)

This software-as-a-service approach, as the developer continued, is about extracting platform rents from the other players in the private rental sector: ‘We’ll provide that mainly as a software-as-a-service’ (Proptech lead, large developer landlord). The significant market power of such companies is used to consolidate their Proptech holdings. As their data assets grow through the Proptech systems they control, the market power of such key players grows too. For example, one Proptech product is marketed as ‘providing the property industry with data and insights. Harnessing over 60 years of applied experience [to offer] solutions across the supply chain’ (Lendlease, 2022). The data generated from this type of market power can be leveraged to build Proptech assets, which are then rented out to other, often smaller, companies in the private rental system. As one real estate franchisor explained, their approach to improving their digital systems was tied to their goal of increasing their market share, that is, their share of this landed and technological property market: We offer both first-party and third-party software bundled together to hopefully provide the best possible suite of tools available in the industry […] So that we can have a competitive advantage over other [franchise] groups […] but also as a viable alternative to […] a business owner operating […] independent[ly …] We have a preference to either build them ourselves or acquire them and own them […] Where we can’t build it ourselves, we’ll look for a [Proptech development] partner, or […] a supplier. (Large property and tenancy management employee)

As summarised in Table 1, landed property is still crucially important when analysing the Proptech sector. This dual-form of rentierism – where rents are generated from both physical housing assets and Propetch technologies and the data they produce – was initially enabled by the existing value of physical housing assets.

Land still underwrites Proptech: Rent rolls and listings platforms

The collection and consolidation of rental and renter data has increased dramatically with the platformisation of the private rental sector. The intermediation of this data allows potential new capital streams through the property and Proptech sectors. One real estate industry observer reflected on the seemingly ubiquitous nature of the platform logic in our daily lives and its inevitable entry into the private rental sector: You see with banking […] hardly anybody goes into a branch anymore. So, you can actually have this full digital experience from top to bottom. I mean, the amount of information that the banks have on us to be able to customise things to our needs, etc. Our industry is going to go in that direction eventually as well. Because every industry is going in that direction. (Proptech industry observer)

We explored how housing is being leveraged for profit in new ways, and by whom, by tracking the collection and consolidation of data about rentals (i.e. data on the material rental properties and rental housing as an income stream) and renters (i.e. data on people as an income stream). Individual renters’ data in aggregate (i.e. human data as an income stream), in the form of rent rolls, is an emerging asset class that is held on the books of the largest landlord companies in Australia. Rent rolls are a good example to explore because they assemble material property and human data as property together. These rent rolls are typically managed by real estate managers/agencies. A rent roll includes information on the property, its rent generating history and potential, tenant histories and payment behaviour that is also used to flag any issue they may have paying rent, the amount of bond deposited and so on. Rent rolls can be bought and sold, and if an agency acquires a rent roll it means that not only does this company’s material portfolio of rental properties and property management increase but the amount of data about these properties and tenants also increases.

As with other data in the private rental system, Australian rent rolls are subject to market consolidation when a crisis presents a business opportunity. This was particularly true for major real estate franchisors during the COVID-19 pandemic, as observed by one industry analyst: [With the amount of] disruption there was to the rental market at the onset of COVID-19 […] a lot of property management services were just dissolved, because the costs for managing all these investment properties was becoming too much. And so, these businesses would sell their rent rolls to other agencies. So, major real estate agencies are looking after a lot more rental properties. (Large property and tenancy management employee)

For the real estate agencies who control the management of most of Australia’s private rental stock, a rent roll both represents the landed properties being profited from and is a technological property in itself. This technological property can be bought and sold on the private market to provide valuable data insights across a range of real estate and Proptech sectors. With the digitalisation of rent rolls, renters’ personal information and rental histories may be controlled or owned by Proptech companies (e.g. platform providers), whose products are used by real estate agencies, property managers and build-to-rent developers. The Proptech sector views rent data as a potentially valuable platform income stream, and this means the collection, sharing, rent and sale of rent rolls will likely continue. For example, YieldStar, rent-setting software offered by US real estate tech company RealPage, feeds aggregated and anonymised rent data (gathered from users of the software) into a price-generating algorithm that often nudges landlords to push rents beyond what they would charge without the algorithm’s recommendation (Vogell, 2022). The sale of rent rolls themselves is an example of Proptech technology and data combining to create additional income streams beyond the physical housing asset.

Many Proptech companies and some developers we interviewed positioned these platform incomes as a key consideration for their business models, because the rents returned on the physical housing assets were captured beyond their company. In other words, they were interested in designing Proptech products to assist, speed up, streamline etc. the rents returned on the physical housing as a technological service that they can then sell or rent to real estate agencies, property managers and build-to-rent developers, while always looking for data creation and rental opportunities that can be kept in-house as a Proptech opportunity. Sadowski (2019) suggests that this data-as-capital logic is a critical characteristic of the extractive nature of platform capitalism and key focus of platform companies (Srnicek, 2016; Zuboff, 2015).

The costs involved in maintaining a rent roll mean the larger companies are better positioned to make consolidation a reality within the industry. One major real estate franchisor we interviewed explained the challenge that individual real estate agencies face in managing these rent rolls: A rent roll is a depreciating asset […] unless you grow it […] It costs money to invest in it, because you need to add a person who looks after growing the rent roll, so that’s an investment [and] that’s eating into […] profit. So, it’s really hard to kind of balance growing it, keeping everybody happy – being your tenants and your landlords – and getting the right technology to support you. (Large property and tenancy management employee)

Larger companies are not only more capable of buying more rent roll data but also more interested in developing or supporting the development of software to create, maintain and consolidate rent rolls and better able to do this.

Rental managers and agencies are using software-as-a-service – either rented to them or bought outright, or through new partnerships between Proptech developers and property management companies – to maximise their rent roll returns: With the delivery of these new technology platforms, our expectation will be that […] we can start to look at the system managing the properties. And a property manager is somebody that manages relationships and exceptions to the system. So, we expect that to change the economics of property management business and return profitability, and hopefully grow the asset value of rent rolls. (Large property and tenancy management employee)

Yet, under these arrangements, the software-as-a-service providers often capture valuable data. One key software-as-a-service data provider we interviewed, a large tech consolidator, stated they have 1.2 million Australian residential properties under their management. For reference, there are around 2.55 million privately rented residential properties in Australia (ABS, 2022): To give you a bit of an idea of scale for it, for example, we provide data of actual rental receipts and vacancies, and so on, to the Australian Bureau of Statistics, and those rental figures feed into inflation calculations […] so we’ve got a good lens into what’s actually happening. (Proptech lead)

Proptech consolidation does not receive as much frontstage public commentary as it should, as it is largely occurring on the private rental sector backstage. Yet it is an important process to analyse. Since we spoke with this large software-as-a-service company, they acquired another large Proptech company. Along with another software-as-a-service company owned by a UK private equity firm, these two companies are the major players consolidating Australian property asset management technologies: ‘They’ve [i.e. the two major tech consolidators] got very, very deep pockets, and they’ve got a very big portfolio of businesses. They’re the two holding companies that are effectively consolidating the industry’ (large property and tenancy management employee). Other major players in renter/rental data in Australia are property listings platforms Realestate.com.au and Domain.com.au. Between them, they have captured most of what is a relatively small, although still highly valuable, market, with REA – Realestate.com.au’s parent company – recently described as ‘“one of those rare […] businesses in Australia” […], meaning the company has a competitive advantage that’s so sustainable over the longer term that it just cannot be broken’ (Han, quoted in Manning, 2023). An industry observer we spoke to concurred with this view: Realestate.com.au and Domain are very good, very sophisticated. I will say, even when I moved to the US, and I saw Zillow and StreetEasy, I was surprised that […] Realestate and Domain were actually leaps ahead […] more consolidated. So, if you want to rent a property [in Australia], you only go to those places. (Proptech industry observer)

This duopoly on the listings side of both sales and rentals makes using these two platforms essential to those managing the leasing of properties, many of whom rent advertising space for their listings through these platforms (see Table 1). A major real estate agency franchisor explained the duopoly’s relationship to the market: ‘I guess we’re their number one customer. They are a service provider to us’ (large property and tenancy management employee).

The duopoly’s market capture and thus market power is not directly built upon the ownership of material property, although both companies own real estate. Rather, their Proptech profiting is organised around scarcity and monopoly, fitting with Marxist notions of monopoly (Collins, 2021), where the duopoly’s market power is built upon the consolidated ownership of rental and renter data, which in this Australian case has been captured by these two Proptech companies. A tenants’ union advocate talked about these two Proptech companies as having large rental ‘data reserves’ and ‘commercially useful data’, which is a concern for renter rights: Realestate.com.au, Domain [and] Rent.com.au […] have the biggest data reserves around renting. And they’re for-profit vehicles, whose main customers are [on the] landlord side, and so they don’t really have – other than driving traffic – they don’t really have a reason to be tenant friendly. Their incentives are certainly weighted towards keeping the property investors and the agents happy. And so that means that when they look at data, when they analyse it, they are analysing it with that lens. And also, they tend to charge for access to the more commercially useful data. (Tenant Union, senior staff member)

This Proptech duopoly started by digitalising the paper property listings that have long appeared in newspapers and magazines (Rogers, 2017: 150). But they rapidly evolved into larger platforms, expanding beyond property listings to digitalise more of the rental spectrum, from processes associated with finding and purchasing rental properties, through listing and managing rental applications, through maintenance and other service provision. This platform rentier duopoly – along with the smaller, yet still popular, Rent.com.au – offers a diverse suite of Proptech tools for property managers and renters. Collecting data and sometimes money from renters through, for example, renter background checks and other ‘services’ purporting to help renters find and secure a home, they are also able to utilise their market knowledge to provide ‘insights’ to renters – such as tips for securing rental properties and lists of suburb average rental costs, which underwrite and normalise rental prices. By leaning on their data reserves and the services, tools and calculators they offer potential renters, they further consolidate their market capture and power.

Conclusion

This analysis of the emergence of private rental Proptech takes seriously the need to investigate the emergence of new rental technologies alongside longstanding land rent extraction in Australia. In drawing out who controls the Proptech, and to what extent, we have shown how control of Proptech depends on the ability to create, buy or rent the housing, Proptech and data in question. Our analysis focused on both the landed property (material real estate) and technological property (digital infrastructure and data) in Australia’s private rental system, which are held on the balance sheets of a range of real estate and property actors and tech start-ups, and which comprise some of the basic building-blocks of rentier platform capitalism. The picture of the various actors and assets developed above shows that for some rentiers both landed and technological property are at play for capital rent extraction. We draw out two key findings, which are summarised in Table 1.

First, landed property rents are still important to established landlords. Individual petite rentiers and property developer landlords are long-standing actors in the private rental sector, with the Proptech sector emerging as a critical new actor in the well-established private rental sector. Many developer landlords were primarily interested in using Proptech to enhance or add value to their primary asset, which is landed property in the form of rental housing. For these individual and property developer landlords, any platform rents they generated were a bonus, or part of emerging strategies to expand profit models. Their primary reason for using Proptech was to increase the capital value and rental opportunities of their rental properties.

Second, intermediation and platform rents are important; some of the larger property development and real estate actors are looking to consolidate tech and data holdings. These data and tech consolidators are using market capture to create market power that is not directly built upon their ownership or control of physical property. This Proptech strategy fits within long-established rent theory, organised around scarcity and monopoly. The market power of these players is built upon the consolidated ownership of data-as-capital. Collection and consolidation of rental and renter data has increased dramatically with the platformisation of the private rental sector.

These extractions represent the growing commodification of tenant experience and the amplification of the antagonistic residential rent relation. Many large property developers, real estate managers and Proptech companies are thinking across multiple income and rental streams when they make Proptech decisions, and many are dual asset-holders, holding both landed and technological assets. Rather than produce much-needed solutions for its many problems, tenant experience is instead commodified and commercialised in this process – commodified as a data source and commercialised as a site through which to introduce new fees-for-services, ultimately increasing land rents. Moreover, by forging new governing relations, the increasing digitalisation of both private rental processes and rental and renter data alongside them opens up a new set of questions for the regulation of these industries.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Australian Research Council grant LP190100619.