Abstract

Real-estate has become an integral part of financialised economies, but while scholars have turned to examine the emergence of carbon markets, the role of carbon in real-estate finance has been broadly overlooked. Real-estate as a sector has been historically slow to innovate, particularly in response to pressure from climate change. More recently, the attitude of UK build-to-rent (BTR) developers to carbon is changing, partly due to global initiatives including the United Nation's Sustainable Development Goals (UNSDGs), but also pressure from institutional investors. In this paper, we provide nuanced insight into the emergence of new logics within financialisation's governance in the UK BTR sector and examine how investors attempt to steer developers into adopting low carbon building materials and designs, while identifying barriers. First, we highlight the multiplicity of financialisation's logics wrapped within assets, highlighting the presence of a carbon logic, which creates pressure for low-carbon activity. Second, we contribute to debates on assetisation and financialisation by examining the tools and knowledge used to create low-carbon real-estate assets, and how carbon attributes are ‘retrofitted’ into existing asset classes.

Introduction

Real-estate construction has become an integral part of financialised economies (Wijburg et al., 2018). Despite a more recent turn to examine carbon markets (Asiyanbi, 2018; Knuth, 2021), the role of carbon in real-estate finance has been broadly overlooked (Bridge et al., 2020), with Edwards and Bulkeley (2017) arguing that more research is needed to understand how low-carbon, sustainable housing can help manage climate change. This dearth of research is problematic with the World Green Building Council estimating that 39% 1 of global carbon emissions originate from real-estate. Real-estate carbon emissions are broadly split into two categories: first, embodied carbon generates 11% of the total through construction processes in creating the fabric of buildings. For example, concrete creates significant carbon emissions, but these can be reduced using renewable alternatives, such as laminated timber. Second, operational carbon accounts for 28% of emissions through building energy needs. These emissions can be reduced through greater use of energy-efficient technologies, including heat recovery systems, smart technologies, and renewable energy generation (Attuyer et al., 2012; Bouzarovski, 2020). Often, buildings are demolished to create new assets better suited to changing investor demands. Much of the waste cannot be reused and is landfilled before the cycle recommences, generating further carbon emissions.

The Farmer Report (2016) has criticised the UK real-estate sector for its structural shortcomings: it is fragmented, slow to innovate and relies on outdated building processes and technologies. While architects and engineers have sought to embrace energy-efficient, low-carbon technologies to mitigate operational carbon emissions, and alternative materials to reduce embodied carbon, these innovations are often adopted by smaller mission-driven end-users, while many larger developers have continued to use established carbon-intensive techniques. In 2021, it was revealed how one of the United Kingdom's largest homebuilders in the build-to-sell (BTS) market had lobbied the government to reduce proposed targets for carbon emissions on new build homes. 2 However, the attitudes of UK real-estate developers towards carbon are beginning to slowly change, with global initiatives including the United Nation's Sustainable Development Goals (UNSDGs) and the World Green Building Council's Net Zero Carbon Buildings Commitment, advocating for urgent action, particularly in the construction of the urban environment.

This is reflected in the growth of interest in environmental, social and governance (ESG) investment funds, which have grown in recent years, with European sustainable funds reaching $1 Trillion in value in 2020. 3 The growth of ESG funds is partly linked to increased retail investor awareness, but more specifically the adoption of ESG sustainability strategies by large institutional investors such as pension funds in response to initiatives like the UNSDGs. For example, in 2018, UK-based financial services company Legal and General announced the alignment of its strategic priorities with UNSDGs. 4 This change does not indicate that all institutional investors are making a full pivot to ESG sustainability, far from it, but investors are beginning to scrutinise investment opportunities across different asset classes more carefully, with an interest in the embodied and operational carbon emissions of real-estate acquisitions, with more attention focussed on operational carbon emissions data, reporting and building design. This has begun to reshape attitudes towards building design and construction techniques, which has relocated profit maximisation under financialisation.

Institutional investor responses to carbon and real-estate assets vary spatially, reflecting the interests of capital and local property markets. Our overarching aim in this paper is to provide nuanced insight into the emergence of new logics within financialisation governance in the United Kingdom's build-to-rent (BTR) sector and to examine how investors attempt to steer developers into adopting energy-efficient technologies and embodied carbon alternatives, while uncovering the subsequent barriers encountered. Drawing upon semi-structured interviews, we seek to make two main contributions to the literature. First, we seek to address the dearth of research highlighted by Edwards and Bulkeley (2017) on carbon in real-estate finance. In doing so, we contribute to the literature on financialisation, by providing greater insight into Financialization 2.0 (Wijburg et al., 2018), which refers to a shift by which investors seek longer-term investments with stable rental yields rather than speculative returns, and how this change is shaping the BTR market. This leads us to argue for sharper attention to be paid to the potential for a multiplicity of financialisation logics wrapped within assets, as we find both short- and long-term capital logic at play in BTR. We also draw out the politics of a carbon logic that is not solely focussed on capital accumulation, and instead challenges the financial logic and adds to the instability of buildings as assets. As such, we observe differences between investor strategies, how they approach building design, and how their diverse approaches lead to varying degrees of success in reducing operational and embodied carbon emissions within projects.

Second, we aim to contribute to debates on assetisation and financialisation by examining the tools and knowledge used to retrofit carbon into real-estate assets. However, in contrast to previous studies, which seek to examine the development of novel financial products and instruments (Asiyanbi, 2018; Knuth, 2021), we explore how the instability of existing asset assemblages afford opportunities to retrofit carbon values into existing asset classes. In doing so, we provide insight into how new measuring tools, such as questionnaires and reporting standards, are developed to frame the assets, and render carbon visible, while providing new evidence into how power is applied to developers to steer them towards reducing carbon emissions. The remainder of this paper is as follows: In the Financialisation, sustainability and BTR section, we examine recent literature on financialisation, carbon in real-estate and the institutional BTR sector, to assist us in framing our analysis and how a multiplicity of financialisation's logics, including carbon, can be accommodated. The Findings section will examine our empirical data. The final section will conclude the paper.

Financialisation, sustainability and BTR

Approaching financialisation

Financialisation refers to a shift towards a finance-led regime of accumulation that accelerated in the 1980s (Ioannou and Wójcik, 2019). In seeking to map and examine the powerful and pervasive changes brought about by financial capital, geographical studies of financialisation, have more recently, investigated urban infrastructure financing (O’Brien et al., 2019), rental securitisation (Fields, 2018) and the intensification of household indebtedness (Hillig, 2019), for example. Aalbers (2017: 544) defines financialisation as the ‘increased dominance by financial actors, practices, markets measurements and narratives, which transforms firms, states and households’. Researchers of financialisation, for example, Ouma (2016) and Omstedt (2020), have mobilised social studies of finance lenses, to unpack the black box of artefacts, data and measurements within socio-technical assemblages to reveal the calculation of an asset's value and risk, unravelling how market actors standardise assets through market devices, processes, and calculative agency (Callon, 2007; Callon and Muniesa, 2005; Mackenzie, 2006; Preda, 2006).

In turning to examine the creation of new financial assets as an outcome of financialisation processes, researchers have drawn upon the term assetisation to analyse how objects are turned into new speculative assets (Birch, 2017). New entanglements of tools and knowledge establish the values of assets, crystallised in the present, by pulling together knowledge from various disciplines of finance, to conceptualise an asset's value (Birch, 2017), while reconfiguring the object to financialisation's logic (Langley, 2020). Through a lens of assetisation, researchers have sought to unravel how new assets are created, with studies including nature (Ouma, 2016), rental yields (Fields, 2018) and municipal bonds (Hilbrandt and Grubbauer, 2020), for example. Not only do such studies provide insight into how assets are created under financialisation, they reveal how the underlying ‘commodities’ can be intangible, for example, taxes and rents, but how these assets are unstable, and subject to ongoing attempts to bend and force them into fitting existing measurement tools and institutional norms (Fields, 2018).

Moving beyond technical devices, researchers have also sought to examine the supportive infrastructure needed to legitimise new asset class markets, with Hilbrandt and Grubbauer (2020) examining municipal bond markets, while Fields (2018) has highlighted the development of trade bodies and groups to develop legitimacy and visibility to new asset markets. In keeping with the creative destruction of capitalism, Brill and Durrant (2021) note how groups even attempt to delegitimise competing asset classes and investment opportunities. These supportive institutions assist in the co-creation of shared understandings and standards, providing market participants with the ability to further objectify and measure assets, while drawing collective meanings from data (Çalişkan and Callon, 2010; Kear, 2014).

As noted above, the instability of asset assemblages necessitates continuous management and governance, which becomes more complex when new intangibles are recognised and bundled into financial assets (Birch, 2017). As assetisation involves rethinking what is valued in an asset, through co-production, governance and social relations (Birch, 2017), we argue it is possible to add new features to an asset class, and by extension, additional values such as ‘green value’ (Knuth, 2016), where instability affords opportunities to adjust and to create new financial assets and innovations. For example, US residential mortgage securitisation technologies spawned many international variants (Wainwright, 2015) through to more recent multifamily rental structures (Fields, 2018), drawing on similar templates, tools and standards, while Karpf and Mandel (2018) note how some ‘traditional’ municipal bond structures have been adjusted to incorporate ESG features, with accreditations such as LEED used to create green assets (Knuth, 2016).

Real change, or just fizz? (de)carbonising finance

Financialisation research has often focussed on the extraction of short-term profits, for example (Cupertino et al., 2019; Keenan, 2020), leaving non-financial realms comparatively overlooked, although interest in finance and carbon has begun to gather pace in academic debates on the built environment and real-estate. The earlier dearth of work is surprising, considering that financial institutions are becoming increasingly concerned about carbon credentials in their loan portfolios (Bridge et al., 2020), particularly as real-estate creates considerable carbon emissions. Many of these studies focus less on the embodied carbon of the assets, but rather on the reduction of operational carbon emissions. For example, researchers have considered the creation of new financial instruments that (ab)use energy efficiency, such as Thoyre’s (2021) study of how power companies extract energy efficiency from private homes through ‘negawatts’, or Knuth’s (2021) work on finance and the use of tax credit loopholes to fund renewable energy infrastructure. In examining individual assets, scholars have investigated carbon reductions through energy efficiency improvements in building upgrades and thermal enhancements via heating, energy recovery, cooling and lighting systems in response to policy and regulatory interventions (Attuyer et al., 2012; Bouzarovski, 2020; Rydin and Turcu, 2014).

In turn, these upgrades are evaluated by professional communities which scrutinise building design in response to energy efficiency accreditations from LEED, BREEAM and Green Star (Cidell, 2009). As McGuirk and Dowling (2021) observe, some institutional investors seek to align top-tier commercial office space credentials with sustainability, utilising a focus on energy governance, with standards and benchmarks, to connect to green finance instruments. For example, Attuyer et al.’s (2012) notable study examined how French investors placed pressure on commercial real-estate developers into improving the energy efficiency of their buildings, particularly in the light of regulatory changes, focussing on upgrading buildings, but only when the investment time horizons delivered ‘acceptable’ returns, and where owners and tenants shared the investment burden to reduce energy consumption. Analytically, Knuth (2016) takes this further to examine how retrofitting existing commercial buildings converts them into new green commodities, where the green status is akin to the discovery of a new resource, enabling an additional exchange value premium to be levied on new investors, once the value is crystalised through successful accreditation certifications. In contrast, comparatively less work has been considered residential real-estate, where Edwards and Bulkeley’s (2017) study takes exception in investigating retrofitting work.

At this point, it is useful to note how the UK BTR sector differs from the findings of these earlier studies. First, retrofitting is less desirable due to the tax environment. New build projects are value-added tax (VAT) exempt, whereas retrofitting and refurbishment work historically has not, leading investors to prefer to demolish and rebuild, better configuring the building to their needs while adding energy-efficient interventions. 5 Second, while new financial instruments have been created to capture green value and energy-efficient funding, in the UK, real-estate instruments have been simply ‘retrofitted’ to accommodate and wrap carbon into existing asset classes through assetisation, highlighting the slow and contested transition from a sole economic logic to the inclusion of a carbon logic.

BTR: designed for assetisation

More recently, researchers have turned to examine the growth of the private rental sector (PRS) (Byrne and Norris, 2019), investigating the permeation of financialisation's politics into new residential markets, such as social housing (Clegg, 2019), care homes (Horton, 2022) and purpose-built student accommodation (PBSA) (Revington and August, 2020), driven by financialised institutional investors such as pensions funds, Real Estate Investment Trusts (REITs) and private equity (PE). Enabled by governments at central and local levels, real-estate developers have begun enacting new entrepreneurial strategies and public–private partnerships to create new markets while accelerating the development of new construction projects (Aalbers, 2020). Policymakers have developed supportive legislative frameworks to facilitate these partnerships through tax increment financing (Weber, 2015), special purpose vehicles (Beswick and Penny, 2018) and REITS (Waldron, 2019), for example. Wijburg et al. (2018) have observed that these new corporate strategies represent a qualitative shift in the practices of financialisation, towards rentier capitalism. Wijburg et al. (2018) coin the transition from property speculation to a rentier model as ‘Financialization 2.0’. Under Financialization 2.0, timescales stretch, moving from short-term PE cycles of leveraged ownership over 3–5 years, to long-term ownership with a focus on rental yields. As we shall see later, this is also useful in rendering carbon visible, as it is also emitted over longer time periods as operational carbon emissions.

This strategic shift has triggered the design of new property assets to meet the desired returns of investors, rather than the use value of residents (Hofman, 2017; Newman, 2009; Waldron, 2019), where developers internalise the expectations of investors (Weber, 2015). Developers often create homogenised accommodation with 50–100 units as a minimum with a focus on enhanced amenities, often referred to as ‘hotelization’ (Nethercote, 2020). As will be demonstrated later, vertically integrated developers (VIDs), fusing the functions of PE, treasurer and developer, create ‘investment ready’ property portfolios that are directly aligned with their investors’ objectives, with rental income converted to investor yield (Brill and Durrant, 2021; Nethercote, 2020).

Initially developed in the United States, the BTR model has been implanted in the UK PRS ecosystem, challenging the historical long-tail of small-scale amateur landlords, and attracting capital from institutional investors seeking rents (Brill and Durrant, 2021). Neoliberal interventions in housing markets reduced investment in social stock and privatised the rental sector, assisted through tax subsidies. Quantitative easing cash became available to institutional investors, while homeownership rates were undermined; driven by increasing house prices, precarious work and wages, which in turn, have increased demand for the PRS market (Aalbers, 2020; Byrne, 2020; Byrne and Norris, 2019). This has furthered the demand for BTR developers, creating new ‘investment opportunities’ for institutional investors which will see construction continue apace.

Despite the recent turn to Financialization 2.0, Byrne and Norris (2019) and Brill and Durrant (2021) argue that as an area of research, institutionalised PRS and BTR remains understudied, particularly the mechanisms that are shaping the sector. As Aalbers (2020) notes, institutional investors are becoming more involved in construction and design, joining Nethercote (2020) to argue for more work on how building design and communities are shaped. As institutional investors are becoming increasingly dominant actors in the development landscape, they have the potential (to varying degrees) to act as positive agents of change by dictating more energy-efficient, low-carbon designs, in contrast to developers looking to quickly ‘flip’ low-cost properties for speculative gains.

Making space for multiple investor logic in financialisation?

Earlier financialisation research focussed on an implicit, short-term profit logic which emphasised cost reductions to squeeze value from organisations and maximise shareholder returns. More recent studies have hinted at the analytical possibilities of multiple logics that can interplay within assetisation. For example, Nethercote (2020), in calling for more empirical work into the PRS, argues that the transition to Financialization 2.0 reveals at least two different logics of capital: speculative, short-term capital and rentier, long-term capital. Similarly, Langley (2018) draws attention to the role of social logic through social impact bonds, while Hilbrandt and Grubbauer (2020) and Karpf and Mandel (2018) implicitly note the value of carbon within municipal bonds. Scholars have overlooked the ‘retrofitting’ of carbon into existing asset financial instruments, where institutional investors demand that an organisation reduce its carbon emissions as part of its activities, to meet the environmental goals of investment mandates.

Subsequently, we seek to draw out different logics in BTR development – particularly a carbon logic – and while we do not deny the overriding power of the financial logic in seeking greater returns, we argue that within assetisation, researchers need to be attentive to the presence of additional logics – both financial and non-financial. Doing so could sharpen insight into the tensions within asset assemblages. This has the potential to advance studies of financialisation in two ways: first, while assetisation creates ill-fitting and unstable financial assets under the gaze of calculative tools, part of their instability may originate from the competing logics within an assemblage, rather than just the trials of flattening data (c.f. Fields, 2018). Second, this approach may enable researchers to uncover additional activities and values underlying financial assets, in particular environmental pressures. In our paper, we focus on short-term and long-term financial logics in addition to a carbon logic. These logics can be complementary or contradictory, resulting in a dynamic interplay that varies between different types of institutional investors and in turn, necessitates the creation of new tools, knowledge, standards and calculatory frames.

Research design

In our paper, we draw upon a series of semi-structured interviews and secondary sources to inform our analysis. Specialist websites, including UK ESG Social Housing, support our interviews in understanding the development of new market standards for data and a review of developer websites to examine their approaches to carbon sustainability strategies. Between 2020 and 2021 we conducted 45 interviews with a range of participants involved in BTR development and sustainable construction. This included directors (CEOs and COOs) of PE funds, VIDs, pension funds and housing associations (HA) active in BTR, market rent and PBSA sectors. In addition to this, we interviewed boutique finance houses, industry representatives, policymakers, architects, financial analysts, civil engineers, sustainable construction entrepreneurs, and business accelerator programmes. Our interviewees were active in developing new real-estate assets, investing and/or owning assets, designing projects and developing sustainable construction products to mitigate carbon emissions.

Potential participants were identified through a combination of Internet searches and snowballing, to identify a mix of actors and informants. Our interviewees were provided with the opportunity to discuss issues they thought pertinent, that were not initially introduced by the researchers, enabling us to develop greater insight earlier on in the project. The interview structures investigated development strategies, approaches to sustainable construction, sustainable construction technologies used, data, standards and tools used to manage carbon and limitations to broader adoptions of sustainability in building designs. The interviews ranged between 45 min and 2 h in duration, and each interview was recorded and transcribed, before being thematically coded and analysed. The use of supporting secondary sources enabled triangulation of the empirical data, while enabling the responses to be placed within a wider context.

Findings: logic and technology diversity in sustainable construction

Transitioning to low carbon real-estate?

Our interviewees reported increased investor interest in ESG. For some investors, plans to reduce operational and embodied carbon emissions had become increasingly important to their investment screening processes. Subsequently, the net zero carbon agenda has begun to move from specialist ESG asset classes into mainstream property investment funds. As highlighted below, changes in corporate governance and the redefined strategic objectives of institutional investor management, shaped by non-executive directors and client mandates, sought a push to align with UNSDGs: … ten years ago investors didn't really care about ESG, it was more about … reasonable return over gilts, decent credit rating, you’re done-type thing … it's only in the last year or two that really ESG has come to the fore on top of all of those fundamental factors … we’ve even sat in meetings with large direct pension fund investors where they’re saying ESG is now as fundamental for them as measuring core credit fundamentals. (Financial consultant)

… I don't think asset managers all of a sudden developed a conscience and realised this is a really important thing to do … its being driven by market pressures and the people that sit behind them. (Professional advisor)

The corollary of this for real-estate construction has been broadly twofold. First, investment funds have begun to place greater pressure on developers to include energy-efficient technologies in buildings constructed for their portfolios. Second, real-estate investors themselves are under increased pressure from their institutional clients, such as pension providers, to reduce their exposure to assets which do not include interventions to reduce operational and embodied carbon. Arguably, UNSDGs and the Net Zero Carbon Buildings Commitment, have led to momentum for change within the sector, reshaping decision-making processes.

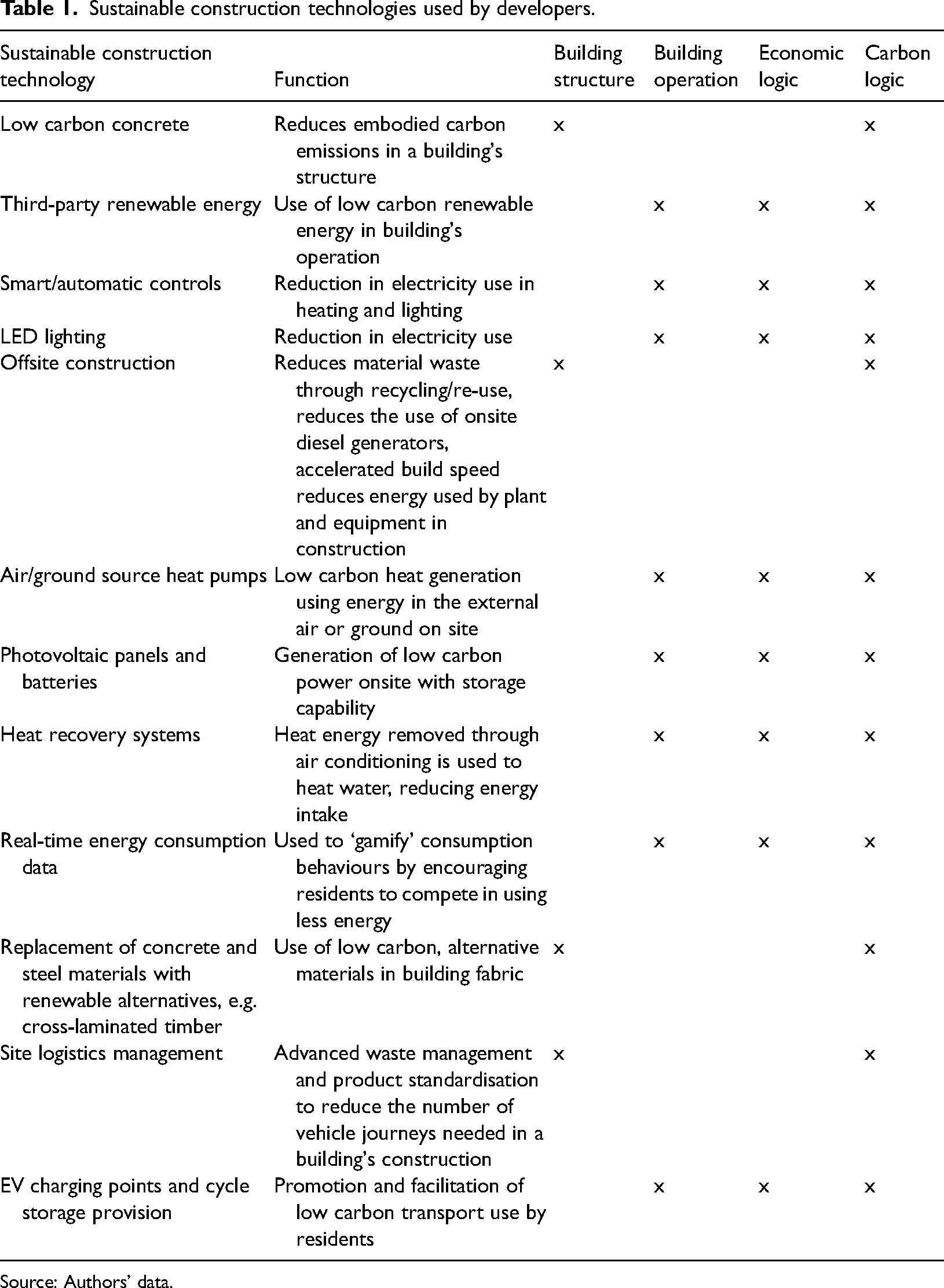

Table 1 summarises the energy-efficient technologies and embodied carbon material alternatives frequently included in the construction of new BTR assets, based on the projects of our participants. Given the nature of BTR construction and operation, it is impossible to not produce carbon emissions. Subsequently, the aim of developers is to reduce carbon emissions ‘as far as possible’, and in some cases, offset the remaining carbon. Unsurprisingly, additional energy-efficient technologies incur costs. For example, energy recovery, air and ground heat pumps, solar photovoltaic micro generation and smart IoT devices increase building costs, while low carbon concrete takes longer to cure, extending construction lead times, therefore reducing the available time to collect rents. This increases the capital expenditure and funding needed for a project, while potentially reducing profits. However, as will be explored later, the interplay between finance logic and carbon logic is more complex, where greater upfront expenditure can lead to lower long-term debt financing and operational costs. This explains why the investors and developers were primarily more active in using energy-efficient technologies, as they mitigate operational carbon emissions and reduce operating costs, through reduced energy bills over time.

Sustainable construction technologies used by developers.

Source: Authors’ data.

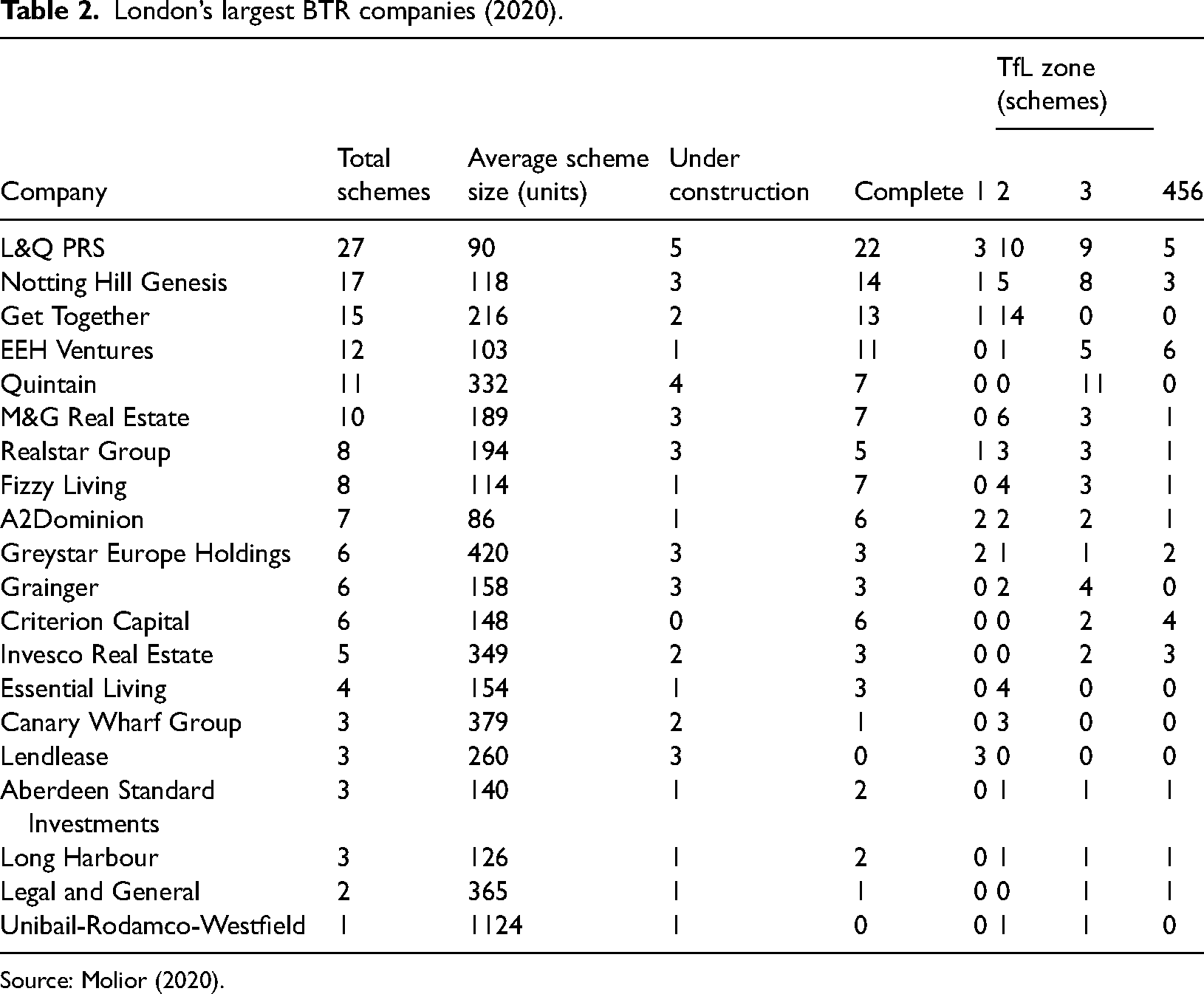

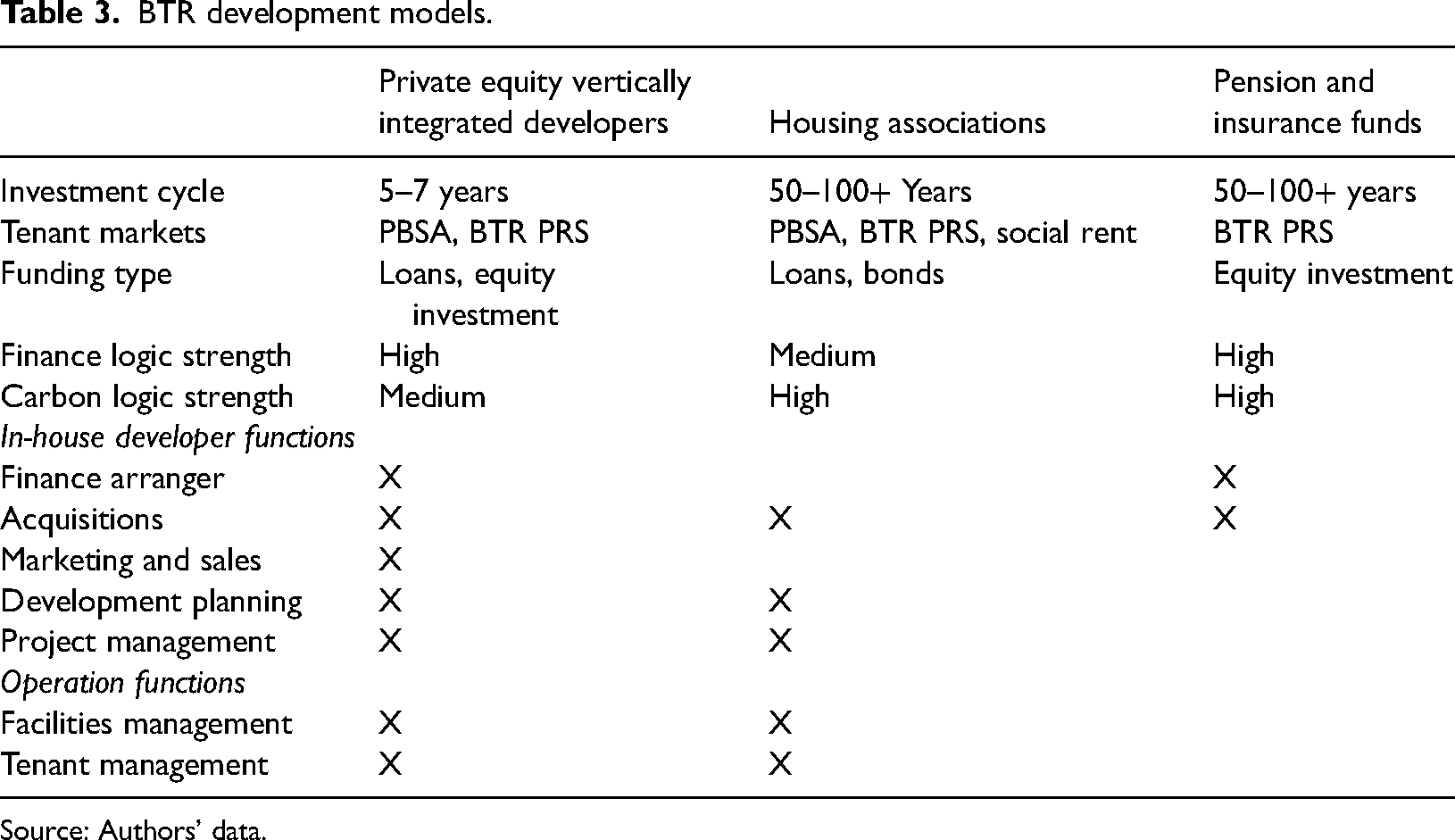

Energy-efficient technology adoption is influenced by the investors themselves and the type of capital they are deploying: short-term or long-term. Table 2 shows data compiled by Molior, a consultancy that monitors the BTR market. Their snapshot of the London market highlights the main developer types, including long-term capital developers such as HAs (e.g. A2 Dominion) and pension and insurance providers (e.g. L&G), and short-term capital developers, predominantly PE (e.g. Greystar). Their relationship with institutional investors is complex and their roles overlap. For example, PE funds may purchase existing buildings, but they may also own in-house property development arms called VIDs, which create new assets. While they function as a PE fund and developer, their activities are influenced by external investors, including other PE funds who buy directly into the equity of VIDs and their assets, participate in joint-venture projects or invest in closed fund portfolios. Similarly, pension providers have also created in-house developer arms where new BTR assets may ultimately become part of their pension funds, but first, they enter their group's asset management funds, which in turn are invested in by other institutional investors. Table 3 illustrates the three models and their characteristics, including investment timeframes, tenant markets, funding types, the strength of logic and their functions as developers and operational property managers.

London’s largest BTR companies (2020).

Source: Molior (2020).

BTR development models.

Source: Authors’ data.

These crossovers can be complex as a pension provider can be its own BTR developer and customer, while also buying-in existing buildings, and taking in external capital from institutional investor clients. The different types of investment objectives shape how much they engage and invest in energy-efficient technologies, with investor diversity creating an uneven landscape of more progressive low carbon buildings, and others that are effectively ‘green washed’ with minimal carbon mitigation. What is particularly notable is how interviewees explained the geographical distribution of investors, where PE funds active in the UK BTR are mostly US-based, whereas pension fund and institutional investors were UK-based or European. The paper will now turn to examine the logic and contradictions of different types of developer capital and explore how carbon's green value is revealed and assetised.

Short-term capital: PE funds

While short-term capital remains active within the UK's BTR market, long-term capital, as discussed in the next section, has begun to challenge speculative investors, as explained below: [PE] high return, short time in, don't want to take much risk. They would typically have a five-year plan and if they can sell it in three, they will … There's been a kind of shift in the last probably two to three years of less private equity and more core money entering our sector. What that has done is lowered returns because core funds don't need a high return or don't expect a high return and therefore when they’re competing against private equity firms, they can afford to pay more. And that's kind of slowly squeezing out the private equity guy. (VID Director 1)

A consequence of this transition has been the emergence of VIDs. PE property funds have moved from purchasing buildings and have integrated the developer function within their organisation. VIDs comprise design and development teams, act as block managers and have treasury units that will directly raise project finance from other financial institutions. The advantage of internal design, development and treasury is that the building's capital expenditure, operational costs, specifications and amenities can be closely aligned with particular tenant markets and investment objectives, giving VIDs exacting control over the building's characteristics, making it easier to ‘assetize’ (Birch, 2017). Subsequently, VIDs facilitate greater returns tailored to the demands of short-term PE capital, which is increasingly under pressure from the long-term core capital of pension funds.

Finance and carbon logics

Short-term PE capital has an aggressive financial logic that seeks to reduce expenditure, but ‘add value’ by constructing BTR in place-making projects. This makes BTR assets more desirable to onward buyers and maximises profits for VIDs and PE investors. As highlighted in Table 1, energy efficiency technologies also generate operational cost savings, by reducing consumption costs. As such, their inclusion produces measurable, lower operational costs, increasing rental profits under assetisation. However, the focus on short-term capital accumulation means that the savings from some energy efficiency technologies will often not pay for themselves in the 3–5 or 5–7 year investment cycle timeframe required by PE investors, leading them to be selectively used: … we’re not just looking at the pure capital cost, we’re looking at the lifecycle of that product and the payback period that's invested in … obviously, if something costs an extra £100 000 and it takes you 20 years to get payback for it, then that's not going to work. But if the payback's seven years or something like that, then of course you’re going to spend a bit more money. (VID Director 2)

In the above case, the interviewee had calculated the additional capital investment needed to install an energy recovery system and microgeneration units. The system would eventually introduce cost savings to the building by reducing energy bills, but initially, the project would require additional borrowing from investors to fund its installation, which would incur increased interest payments. Subsequently, there would be a break-even point whereafter the savings would equate to increased profits, but only once some of the savings had been used to reduce the additional borrowing. For some energy-efficient technologies, this point could be reached sooner than others, but if the time period exceeded the investment cycles of PE investors, it was of limited interest. In another example, microgeneration technologies were mooted and then rejected, as the developer calculated they could increase profits by using the required roof space as an exclusive garden for tenants paying higher rents, rather than reducing operational costs through enhanced energy efficiency.

Despite the selective use of energy-efficient technologies, as an effect of short-term capital's logic, PE investors have begun to introduce a carbon logic, requiring developers to adopt energy efficient and embodied carbon mitigations, which in turn generates internal change. However, the carbon logic in the sector is passive and arguably weaker, in contrast to long-term capital – examined in the next section. The quote below summarises the VID approach, whereby PE investors are supportive, to a point, but are not seeking to actively drive substantial change. While the VID, below, sought to follow changes within the broader construction industry, the responsibility and effectiveness of the mechanism driven by the carbon logic was owned by VIDs rather than PE investors, reflecting the priority of the short-term financial logic: … institutional investors, sovereign wealth funds, high-worth individuals would invest in the fund … I think they’re more passive. We’re shaping the agenda. They’re supportive of it, but they’re not driving it. It's more supporting us as we come up with the approach. I mean, obviously, [PE Fund] recognise that access to capital is going to be more constrained unless you can demonstrate that you’re delivering on some of the challenges. (VID Director 3)

Of particular interest, here, is how access to capital and development finance may be more difficult to secure if carbon reduction plans are unambitious. However, as that future scenario sits beyond short-term capital accumulation timeframes, PE investors continue to be more passive, relegating the importance of the carbon logic. This integration of energy-efficient technologies is more actively driven, bottom-up, by the designers within VIDs, who noted that UK government legislation is ineffective in driving change, where instead, professional identity and the mimicry of larger corporations were seen as a more effective steer for improved carbon stewardship and governance: … the government's committed to zero carbon by 2050. Legislation wise, no, because we don't have to be there by 2050. However, most large corporates all have their own ESG strategies and policies. All those have all come out and said, you know, we’ll be carbon zero by 2030. As a public listed company, ESG policy and strategy is something that you’re expected to have … It's not necessarily policy and regulation, it's more around what your investors, what the public, expect. (VID Director 2)

Logic contradictions and instability

Assetisation involves seeking to align diverse elements such as tools, data and knowledge in an attempt to create coherent assemblages (Callon and Muniesa, 2005; Preda, 2006), although the outcomes are often unstable, requiring ongoing renegotiation and flattening (Fields, 2018). As highlighted above, the finance logic of short-term capital conflicts with the carbon logic seeking to reduce carbon emissions, despite the potential for reduced operational costs. The contradiction between the two logics creates instability in the assetisation of BTR PE assets, which often led to VID professionals interested in carbon reduction having to push against attempts to remove energy-efficient technologies, where their plans for positive change were blocked by PE investors, who took a comparatively more active interest in protecting the priority of the financial logic: … long-term sustainable solutions might not be on the agenda and some of these nice to haves, or perceived nice to haves, might get value engineered out … so, we do have a battle on most schemes to try and protect a lot of the stuff that we can see will have an impact … there are instances and clients who will have a shorter term view and it's about making a development profit ultimately, rather than sustainable long-term gains. (VID Director 3)

One particular strategy, driven by the PE finance logic, concerned site project development and undermined the opportunity for other developers to deploy carbon logic in their BTR assets. Many institutional investors do not embrace development risk, where a site is acquired and time is spent seeking planning permission, submitting designs and undertaking public consultations, as they do not have these capabilities, but do have a need to deploy capital quickly, where the planning process can take years. Some VIDs monetise this risk through project developments, where they effectively format land, where rules constrain its future use as an asset (Bradley, 2021), by purchasing sites, creating designs and obtaining planning permission, before selling the project on to other developers to build: … we have a really strong planning team, we can get these consents really quickly and bring them to market fairly rapidly … we exit from post-planning … we do sometimes tend to then package these up and then sell them to someone else to deliver because that gives us a quick turnaround … I guess we do a lot of housing and residential, but a large proportion of it we don't actually end up delivering. (VID Director 4)

This creates a problem in that these projects often minimise the potential for energy-efficient and embodied carbon alternatives due to the additional costs for onward developers.

6

The aim of PE project developments is to keep the design's capital expenditure costs low, to create more market interest from potential buyers, who will ‘bid-up’ the final project price: They’ve got to show a 20% to 25% profit on the scheme, or the bank that's lending the majority of the money for the scheme won't back it. How are they going to show that kind of margin … where can they cut money? I know: materials. (Low carbon technology entrepreneur 1)

Buyers include those with unambitious carbon mitigation plans. Subsequently, this PE strategy locks-out energy efficiency options in the assetisation process, because if a long-term investor seeks to exercise a carbon logic within their BTR investments, they can struggle to find available sites, as those available for acquisition already have designs that cannot be changed, where the granted planning consent excludes or minimises the addition of energy-efficient, low-carbon technologies.

Long-term capital: HAs and pension fund asset management

Long-term capital was predominantly deployed by the United Kingdom and European pension providers, with the assets constructed by HAs and the developer arms of pension fund asset managers. HAs have become more diversified over time, moving into BTR, and have become adept at raising finance to fund their construction from international investors (Wainwright and Manville, 2017). As not-for-profit entities, HAs manage below-market rent social housing, but they also engage in for-profit BTR and PBSA developments to subsidise social housing. Subsequently, they develop their stock to hold and rent over long-time horizons and have a focus on quality and sustainability, owing to their historically charitable purpose: As the grid decarbonises, so will our buildings. And ultimately we’ll end up with zero carbon energy homes … being an asset owner, it's in our interest. Because ultimately, if we’re going to have a decarbonized country by 2050, there's no point me building gas guzzling houses today, because I’m going to have to retrofit them in ten years’ time. And that's not a good use of our cash. (HA Director 1)

Similarly, real-estate funds managed by institutional investors, which are then repackaged into pension funds focus on long-term time horizons. Seeking low-risk assets, which generate consistent returns, pension funds have historically drawn upon commercial property portfolios, but more recently, these investors have been growing their direct exposure to residential BTR. Pension funds seek to mitigate long-term risks, which includes protecting their assets from future climate change risks, and by extension, have developed mandates that require reduced carbon interventions within their BTR stock: Everything we look at is a 50–100 year time horizon, and that's dictated by pension fund lifetimes, so our business is thinking about the risks and issues in 50 years’ time … it generates a long term index link to pension fund holders. (Institutional investor 1)

The long-term capital strategies of investors and developers make climate change a clear business risk, where contributions to net-zero are a core part of business aims. In contrast to short-term PE capital, these extended investment cycles make it easier to offset the capital expenditure costs of energy-efficient technologies against operational savings.

Finance and carbon logic

Turning to examine the finance logic deployed by long-term investors, sustainability was seen as a complementary value proposition that could increase rental income. Technologies that reduce energy consumption also reduce operating costs, but increased tenant interest in sustainability led some developers to view energy-efficient features as desirable or even fashionable, that could be added to place-making attempts, which could command higher rents: Thinking about PRS, a build-to-rent development, and whether you could charge a higher rent for a more sustainable home, I believe that if the whole brand of the place was about sustainability, I think that could command slightly higher rents from people. Because it could be seen as a trendy place to live, and that will all contribute. (HA Director 2)

This resonates with the work of Attuyer et al. (2012) who observe how building owners and tenants share the costs of energy efficiency interventions, although in this example those costs are not one-off payments by tenants, but rather ongoing higher rents. However, while the costs of energy efficiency technologies are rolled into building costs and the requisite financing, which is funded by tenants through their rent, some HA tenants benefitted from decreases in their energy bills, where savings through onsite microgeneration technologies, led to lower utility bills for households. Rather than charge a market rate for this, HAs recognised it reduced financial pressure on households, reducing tenant arrears at minimal cost to the providers and protecting their rental revenue streams.

VID interviewees emphasised how sustainability sits uneasily against financing, with a tension between maximising the number of units that could be built on a project within budget, which may be reduced if funding is needed for more energy-efficient technology. However, this predicament is flipped for long-term capital. A building with lower emissions can be used to enhance its value, and the price of financial instruments secured against it. Importantly, the ESG focus of some funds increases investor demand for low carbon developments, making financing cheaper when energy-efficient technologies are embedded within buildings: [Investors] they’re raising ESG-specific funds and so you tend to get more demand for those issuances, and although there's no hard and fast rule about this, if you speak to capital market desks, they’ll generally say it's maybe five basis points of pricing benefit … I think the whole sector will move in that direction gradually … if you save yourself even a couple of basis points on a £200 million bond issue over 30 years, you’re going to pay for [the extra carbon management costs] very quickly. (Financial consultant)

It is interesting to note a challenge of commensurability here, where reduced carbon emissions are turned into a basis point advantage, but where precise carbon measurement is still contested, as seen in the next section. As indicated earlier, a governance shift has been undertaken by institutional investors and their desire to focus on climate impact is beginning to feed into investment mandates. This is driven by a carbon logic at the centre of new corporate strategies, rather than just a financial logic as summarised by the following participant: … there's a pivot of the weight of funding that wants to be investing in societally positive outcomes and disinvesting from areas of economic activity that are not delivering a successful societal future. So, the easiest thing is moving out of particularly dirty coal mining and investing more in electric futures, low carbon futures … we’re countercyclical to what some of those other organisations are doing. (Institutional investor 1)

New corporate strategies of long-term capital investors have inserted a carbon logic within financialisation, where their governance seeks to align the plans and activities of BTR developers, which in turn, re-shapes their approach to building design and energy efficiency, for example, and to render that activity visible, through the collection of data: We’ve just got a new corporate strategy … over the next few years, one of our strategic aims is all about our increasing adoption of sustainable goals, environmental sustainability …. We’re going through a complete review of our existing stock and how we improve our EPC's. We are moving to ESG reporting in our accounts and we’re reviewing our design standards for new homes. (HA Director 2)

Logic contradictions and instability

As indicated earlier, the interplay between finance and carbon logic is complex and they are not necessarily mutually exclusive. However, logic tensions emerged for developers when some fund investors may be open to short-term reductions in performance through greater capital outlay, while others may not. Investor diversity within collective property funds could see some investors withdraw if returns dropped too far, requiring long-term fund managers to negotiate a balance between financial and carbon returns for different investors: We have to start managing our investors and say, in some respects there are some buildings that we’ve traditionally had in the fund that we may not have in the fund if we are very much focused on ESG. But in short-term, that may also impact returns … But are they willing for us, essentially, to probably take a bit of a, relative to other funds, hit? (Institutional investor 2)

The creation of low-carbon BTR assets and linked bonds created further logic contradictions with perverse incentives. For example, in the quote below, investor pressure, predominantly from European institutional investors with an ESG focus has created more demand for bonds backed by assets with operational and embodied carbon mitigations, which in turn pushes down funding costs for developers and reduces investor returns. This can comparatively increase the borrowing costs for developers that are less carbon focussed and decrease their bond prices, due to lower demand, providing higher returns to willing investors if a developer's stock has higher carbon emissions: And to be honest, I guess certain investors, they do like HAs that have a bit of a lower sustainability score, because they can probably pick them up cheaper … so it's not because you have a worse sustainability performance that they will not invest in you. They might even like you, because they see that upside that you will have. (HA Director 3)

The differences between short and long-term capital logics and the contradictions and complementarities between finance and carbon logics have led to a multiplicity of operational and embodied carbon mitigations being integrated within new BTR assets. The next section turns to examine how the carbon values of new BTR stock are wrapped into existing financial assets and instruments.

Carbon revealing: new legitimacy and measurement?

Studies of financialisation have provided much-needed insight into how new types of investment are assembled through assetisation (Asiyanbi, 2018; Birch, 2017; Ouma, 2016). Despite investors turning to focus on energy-efficient technologies in real-estate; newly defined BTR carbon asset classes and instruments have not yet emerged, in contrast to green municipal bonds, for example (Hilbrandt and Grubbauer, 2020). Instead, bonds, linked loans or shares are issued, but are accompanied by new forms of carbon data, presented to the calculatory frames of investors, as operational emission efficiencies or embodied carbon mitigations. These are not directly woven into the asset assemblage, but exist as accompanying signifiers that attempt to render carbon visible as a discursive construction (Bridge et al., 2020). As such, low-carbon BTR bonds are rare, and attempts at standardisation are problematic, owing to the multiplicity of different carbon standards and measures, in addition to self-reported data. In this section, we seek to draw attention to three approaches of administrative carbon capture and calculation: investor questionnaires, UK ESG Social Housing Standards and Ritterwald. These three types of capture and calculation are important as the frameworks are used to organise data and make carbon visible, enabling institutional investor screening and transparency of potential investments. Not only is the data used to report carbon exposure to the clients of institutional investors but the devices of questionnaires and standardised frameworks enact investor power and their intentions to purchase, which influences developers to implement energy efficient technologies and embodied carbon alternatives.

The first type, sees institutional investors screen the buildings and developers through their own processes using internal knowledge and questionnaires, as calculatory frames (Callon and Muniesa, 2005; Preda, 2006), to render embodied carbon visible and to project future operational emissions (c.f. Birch, 2017). In place of an established and legitimate market category defined by collective meanings and common standards (Çalişkan and Callon, 2010; Hilbrandt and Grubbauer, 2020; Kear, 2014), these frames varied between different types of developers and their subsequent clients, with pension arm property funds and HAs under tougher carbon scrutiny to meet the mission-driven, long-term mandates of EU and UK institutional investors, against more passive US-driven PE. Questionnaires were sent by institutional investors to VIDs, HAs and pension property funds. They sought a variety of quantitative and qualitative data which often borrowed existing construction industry metrics in an attempt to leverage legitimacy from alternative supportive institutions and social infrastructure (Birch, 2017; Çalişkan and Callon, 2010). For example, the proportion of Energy Performance Certificate (EPC) ratings of a building or portfolio were often used as a proxy for energy efficiency and operational carbon: … it's looking at which schemes are EPC B or A. So, generally we wouldn't buy schemes if it's an EPC C or D, so we’re pivoting our investment into higher performing projects … and then the work we’re doing this year is measuring the embodied carbon of various construction types. So, we can start to target lower embedded carbon schemes and not invest in higher embedded carbon schemes. (Institutional investor 1)

While these metrics carried legitimacy, they too are unstable and imperfect, having been critiqued as ‘tick-box’ approaches which lead to buildings designed around checklists, rather than holistically creating the most sustainable buildings (O’Malley et al., 2014). Alternatively, problems for international investors emerged, in that some building accreditation schemes are not recognised in all national markets, or are too strict, leading to cherry-picking, based on how seriously investors approach sustainability. This led some investors to draw upon other existing accreditations. For example, the UK-based BREEAM accreditation system developed a ‘Home Quality Mark’ in 2015, as a scoring system which includes attempts to measure environmental footprint, through operational emissions and the impact of home construction.

7

The more international GRESB accreditation focusses on energy consumption, renewables generation, for operational carbon, while scrutinising materials for embodied carbon and mitigation through recycling.

8

Given the diversity of institutional investor questionnaires and the data they seek, developers have taken to creating their own dashboards of data, capturing information on the inputs into their buildings to create a richer set of information that can be used to create a claim for low-carbon credentials within the screening questionnaires of different institutional investors. As more institutional investors have developed a greater interest, their requests for data have become more demanding: … a lot of investors, three to five years ago, would short-hand GRESB performance … Over the past year, what we’re starting to see is, investors asking us for more underlying data, again, predominantly, around climate. So, energy data, carbon data. How we’re aligned on a net-zero pathway … we’ll gather energy data, wood data, waste data. So, it's some quantitative and then some qualitative. (Institutional investor 2)

The challenges in translating carbon into a discursive construction (Bridge et al., 2020) with this ad hoc approach, is that it makes comparability between assets of different developers difficult for institutional investors, as there is an absence of relational systems (Knox-Hayes, 2009). For PE-backed VIDs, there was less pressure and scrutiny on their activities, through a carbon logic, due to short-term profit logic relegating the benefits of sustainable technology. This reflected the aims of their investors, commonly US PE funds, with clients including KKR and Blackstone, Greystar, sovereign wealth funds and HNWIs. While VIDs were required to showcase and report carbon reduction activity as discursive content (Bridge et al., 2020), the mechanisms were more passive, based on self-reported narratives, where energy efficiency activity is desirable, but is not used to justify and shape investment decision-making, as with HAs and pension-backed property funds: …. we now have an ESG section both in our internal reports and in our reports to our investor clients. The investors are calling for us to make reference to ESG and what ESG measures are included. (VID Director 3)

… we go through an ESG questionnaire which we created, and we collect data from what we’ve done, as well. We know how many trees we’ve planted, and cars parking space for bikes, and stuff. (VID Director 5)

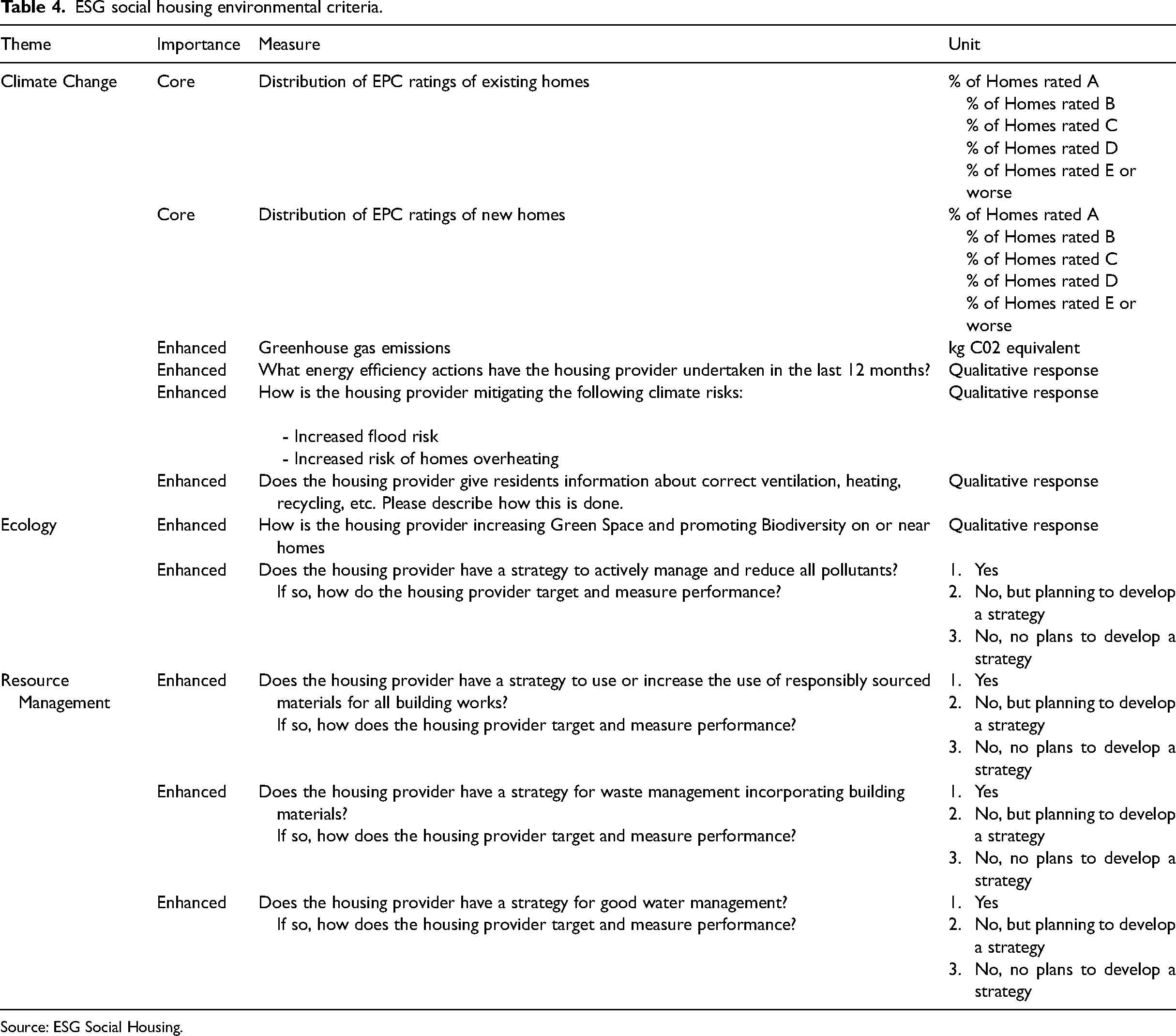

A second approach emerged in 2020, which sought to develop legitimacy in a BTR sub-sector through the development of a new trade group (c.f. Fields, 2018), which aimed to harmonise procedures to establish modes of measurement and visibility (Knox-Hayes, 2009). HAs, investors and stakeholders sought to standardise carbon measures and questionnaires by forming an industry steering group called UK ESG Social Housing to create a Sustainability Reporting Standard (see Table 4 for the relevant carbon extract categories). The aim was to create a questionnaire, acting as a calculatory frame, that would highlight ESG and carbon in the sector and bring standardisation, but also legitimacy through a shared, co-created set of criteria (c.f. Kear, 2014) that would show the sector in its ‘best light’: [General frameworks] weren't really designed for this sector. They might be designed for utility companies or maybe just generic corporate questionnaires … a lot of the positive impact that comes from housing associations weren't being picked up through that process … and so, we instinctively felt like housing associations should be doing better, but we need to setup a scorecard whereby they can demonstrate their environmental credentials … we wanted to make sure that we didn't over-ask information. So, if there was a standard or a metric which is already a requirement of the statistical data returns, for example, we’d use the same metric. (Professional advisor)

ESG social housing environmental criteria.

Source: ESG Social Housing.

There is currently no such system used by property funds administered by pension investors, or PE funds. Although standardisation in the HA sector could be translated to the other developers, it could be argued that in seeking to downplay the carbon logic for some PE investors, the absence of a common system with more robust standards could be more beneficial to prioritising the profit logic (c.f. Brill and Durrant, 2021). What is notable about the HA standard is its focus on operating carbon through energy efficiency, not embodied carbon. This can be explained by attempts to develop the adoption momentum of the standard, where capturing operational data is easier than attempting to measure embodied carbon in historical, legacy assets in portfolios of which no building material data exists. The group also stopped short of setting performance benchmarks, which makes calculation and direct comparability between different developers complex and the definitions of ‘green’ illusive (Karpf and Mandel, 2018). While the qualitative fields enable diverse data to be captured and partially flattened for comparison, in not being quantified, flattening as a relational achievement cannot be fully completed, so the data is not directly comparable. For example, while the presence of a strategy for ‘responsibly sourced materials’ can be partly codified, its specific details and use of such materials could vary widely, between two institutions ticking ‘yes’.

The third mechanism concerns the development of new accreditation and more challenging reporting. While focussing on ESG, the accreditation covers carbon emissions as highlighted in the quote below: … we have internal sustainability standards for the business rather than specifically construction … it's more around carbon usage for the business … so we have a specific ESG reporting … it's called a Ritterwald Accreditation about how we run our business in all aspects of sustainability. (HA Director 4)

Certification from the Ritterwald 9 consultancy focuses on ecological criteria, especially energy efficiency, resource reduction measures, and use of renewable and alternative energy, where data is structured around ‘criteria catalogues’. In contrast to being a collective development of supportive infrastructure for the sector (Hilbrandt and Grubbauer, 2020), the framework is independent. Formally known as the Certified Sustainable Housing Label, the accreditation is aligned with the ICMA's Green Bond principles to develop greater legitimacy in the sector. Certification and assessment of the developer by the Ritterwald not only standardises the data by BTR HAs, but also sets minimum standards and is regularly reviewed, in contrast to the UK ESG Social Housing group, where the certification process provides a comparable and independent measuring frame. Ritterwald has attracted more interest from ESG leaning EU institutional investors and pension funds and is currently being adopted by UK HAs to align their net zero carbon strategies. PE-backed VIDs and pension fund developed BTR arms do not have a comparable standard, which introduces further variation regarding operational and embedded carbon in the BTR sector.

Conclusion

Recent financialisation research has drawn attention to investors moving away from speculative capital deployment, to a long-term rentier focus (Wijburg et al., 2018), as illustrated by the growth of studies on the PRS and BTR (Byrne and Norris, 2019; Clegg, 2019; Revington and August, 2020). BTR assets generate substantial carbon emissions leading investors and developers to respond to the carbon challenges highlighted by UNSDGs and the Net Zero Carbon Buildings Commitment. Yet despite the commodification of carbon through assetisation (e.g. Asiyanbi, 201; Hilbrandt and Grubbauer, 2020; Karpf and Mandel, 2018; Knox-Hayes, 2009; Ouma, 2016), studies of carbon and real-estate remain limited (Bridge et al., 2020).

In this paper, we provided two main contributions to the literature. First, we sought to draw upon the notion of different logics at work within financialisation, extending the idea of short and long-term capital investment (Wijburg et al., 2018). In doing so, we aimed to unpick short and long-term financial logics and a carbon logic that was seeking to alter organisational behaviour by prioritising, or at least including, the importance of moving to net zero carbon activities in new BTR construction. Second, we set out to contribute to recent work on assetisation, by examining how new frames, devices and data are retrofitted around existing asset class instruments, in an attempt to render carbon visible, to feed into investor decision-making, but to also pressure developers to reduce their assets’ carbon.

We observed a movement of BTR developers towards the use of energy-efficient technologies and alternative embodied carbon materials due to its increasing importance to long-term investors, driven by their management, non-executive governance and clients. Our findings note a variety of stakeholders with different financial logics, including PE and pension investors, which were shaping the diversity of developers including HAs, VIDs and the pension developer arms. Despite a movement of new long-term capital into the residential real-estate market, previously dominated by PE, we noted the emergence of VIDs to create BTR assets that were tailor-made to suit the logic and aims of PE. The findings revealed how energy-efficient technology can reduce operational costs, in addition to following a carbon logic, but that it was often challenged by the financial logic. While PE investors were interested in shaping VID approaches through a carbon logic, it was often passive, with less formal oversight, with the drive from designers and professionals within VIDs, but with a more active interest if the carbon logic was seen to challenge the profit logic, leading to the value engineering ‘out’ of energy efficient technologies, demonstrating logic interplay.

In highlighting differences between short-term and long-term capital, pension developers and HAs viewed the climate crisis as a business risk to be managed. As such, developers with a long-term focus sought to capture operational savings through energy-efficient technologies. Of particular interest was how these technologies could reduce financing costs for developers, and how long-term capital investors were more active in shaping developers’ processes, through adopting new corporate strategies to respond to the carbon logic. However, despite the increased focus on the performance of the carbon logic, some investors still argued for superiority of the finance logic, and due to contradictions between the logic, low-cost financing for sustainable BTR created new higher return assets from less sustainable construction projects.

We examined how embodied and operational BTR carbon, current and future, was captured through tools to make it visible to potential investors and to provide additional knowledge to complement existing assets. In doing so, we identified three approaches. First, in the absence of market-wide social infrastructure as well as co-created standards and legitimacy, a dispersed and independent series of investor questionnaires were used to capture carbon, using existing construction metrics. Second, a new HA sub-sector working group developed new reporting standards which sought to harmonise questionnaires and data for comparability, engaging stakeholders from the sector. Finally, the paper explored the emergence of a new independent certification which externally ratifies carbon measures and checks ongoing performance. While some investors are taking an active role in carbon reduction, others are not, and stronger market standards and intervention is needed, particularly concerning planning standards, to ensure all developers actively reduce carbon.

We close in calling for further research into financialisation and carbon in real-estate finance, following Bridge et al. (2020). We suggest it could be useful to examine multiple logics within financialisation, particularly complementary and contradictory interplays, which vary depending on the different types of capital at work. This leads us to argue that while asset instability in assemblages can result from ‘flattening’ data and models for compatibility (Fields, 2018), conflicting logic interplay can also destabilise assets, where short-term capital logics displace carbon logics. This leads us to argue that other logics, for example, social justice, could also be accommodated within asset assemblages, rather than to assume that only finance takes precedence.

Footnotes

Acknowledgments

The authors are grateful to the participants of this study who generously gave their time as well as the anonymous reviewers and editor of the Journal who provided excellent and constructive comments.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.