Abstract

Recent scholarship has highlighted ‘assetization’ as an increasingly prevalent process in which valuation practices from financial economics are imposed on new aspects of society. This paper analyses the establishment of the Norwegian ‘oil fund’ – currently the world’s largest sovereign wealth fund – as the outcome of such a process. It traces the shift in the Norwegian government’s valuation arrangements from valuing oil as ‘activity’ in the 1970s towards valuing oil as a ‘national asset’ from the mid-1980s, and shows how this shift happened through close exchanges between economic expertise and governmental procedures. The paper contributes to understanding assetization as a mode of governing by showing both how it happens through governmental tools and practices and how it can have direct material consequences. In the case of Norwegian oil, the introduction of new tools of valuation made the Norwegian government manage the oil resource in a new way, and led to a re-timing of the pace of its extraction. The outcome was speeding up the conversion of oil into financial holdings, and the establishment of the ‘oil fund’ as a new infrastructure for handling oil as a national asset.

Introduction

Recent scholarship has demonstrated how contemporary capitalism increasingly can be conceptualized as an ‘asset economy’ (Adkins et al., 2020) or as marked by processes of ‘assetization’ (Birch and Muniesa, 2020; Langley, 2021; Tellmann, 2022). Indeed, it has been argued that ‘an emerging “asset form” (. . .) has come to replace the commodity as the primary basis of contemporary capitalism’ (Birch and Muniesa, 2020: 2). The argument is that the central focus of economic life no longer lies in the production and circulation of commodities that are valued based on immediate market exchange, but rather in the ownership of assets understood as things ‘that can be owned or controlled, traded, and capitalized as a revenue stream’ (Birch and Muniesa, 2020: 2).

The term ‘assetization’ has been suggested to describe the process whereby something is qualified and valued as an asset (Birch, 2017; Langley, 2021; Ouma, 2020). Focusing on asset-making as a process highlights that the asset form does not follow from qualities inherent in the asset itself. Rather, objects have to be made into assets through practices that value them in terms of their capacity to generate future revenue. Crucially, assetization relies on financial valuation techniques, that is, the discounting of future revenue in order to calculate the ‘net present value’ of income expected to accrue in the future (Doganova, 2024). Assetization can therefore be seen as a phenomenon closely linked to that of financialization (Chiapello, 2015), but denoting a more specific process within the broader tendency of financial logics to encroach on ever new societal areas (Birch and Ward, 2022: 10).

In the emerging literature on the topic, different scholars have highlighted different aspects of such assetization processes. Some have focused on the technoscientific underpinnings of the emergence of new assets in areas such as biotechnology and digital platforms (Birch, 2017; Birch and Muniesa, 2020). Others have focused on the political economy of asset ownership and its role in contemporary capitalism (Adkins et al., 2021; Swyngedouw and Ward, 2022), or on the turning of natural resources into financialized assets (Gilbert, 2020; Ouma, 2020).

This paper analyses a case of the latter; namely the assetization of Norway’s oil resources that took place over the course of the 1980s and 1990s. The focus is not, however, on how oil was valued in financial markets or in the accounts of prospecting and extraction enterprises, as has been analysed in previous studies of geological asset-making (e.g. Gilbert, 2020). Rather, we focus on how the Norwegian government came to value and manage oil as a ‘national asset’ that is governed according to a financialized logic. The paper shows how, by adopting new tools for valuing oil as an asset, the Norwegian government not only changed the way in which oil was ‘seen’ by government ministries and political leaders, it also changed how it was governed in a material sense. The process led directly to the establishment of Norway’s so-called ‘oil fund’, which today is the world’s largest sovereign wealth fund, currently worth more than 1.6 trillion USD. 1 Valuing oil as an asset also led to an increase in the speed with which oil was being converted from a geological resource ‘in the ground’ to a financial resource ‘in the fund’. In this way, we show that processes of assetization do not only happen metaphorically: they may also led to a quite literal and material transformation of a natural resource and the infrastructure through which it is governed.

Given the current size of Norway’s ‘oil fund’, understanding the process that led to its emergence is interesting in its own right. At the same time, the case of the Norwegian oil fund allows us to better understand the process of assetization not just as an economic operation but also potentially as a way of governing. The case of the Norwegian oil fund demonstrates how assetization may happen in close exchanges between, on the one hand, government procedures and political objectives and, on the other hand, economic expertise and changing ways of valuing tied to a new type of economic reasoning. As the paper will show, when assetization emerged as the answer, this was both due to shifts in economic reasoning and a change in what was considered the relevant political-economic problem to be solved. The search for the optimal management of oil resources was intimately linked to the issue of time and timing: the timing of oil extraction, and the speed with which oil revenues were to be pumped into the economy, was part and parcel of the problem one was trying to handle by introducing new ways of valuing oil resources. In fact, it was in part what was called ‘the tempo question’ which led to the revaluation of oil as an asset.

Drawing on the conceptual vocabulary developed in Asdal and Huse (2023), the following analysis traces the shifting valuation procedures and ‘tools of valuation’ with which Norwegian oil was governed in two stages. Each of these stages, we show, correspond to a different ‘valuation arrangement’ in the Norwegian oil history: First, the arrangement in which Norwegian oil production was embedded from the early 1970s, which valued oil in terms of activity; and next, a shift towards a quite radically new valuation arrangement in the 1980s, where oil came to be valued as an asset. Within each stage, we focus specifically on the tools with which oil was valued, and the actors with which these tools were associated.

The shift in valuation arrangement maps onto broader and indeed transnational contexts of changing economic thinking and political outlook in the last quarter of the 20th century, from economic planning based on Keynesian economics towards more market-oriented approaches. However, this change in economic outlook and policy came relatively late in Norway compared to other western countries (see Lie and Venneslan, 2010; Asdal, 1995) and can nevertheless not fully account for the change in valuation procedure. The shift can also be seen in a more specific context of natural resource management. As Gaudet (2007: 1035) points out, the OPEC oil crisis and new debates around resource scarcity was an important backdrop when the management of non-renewable resources reemerged as a topic in economic theory in the 1970s. The aim of this paper is not to delve into details about this specific context. Yet, we emphasize how the shift in the Norwegian case followed from attempts to handle the specific governmental problem of how best to manage non-renewable oil resources, and how the tools and procedures that were employed to accomplish this were closely linked to the government apparatus of the Norwegian state. In this way, the shift in valuation procedure that we identify must be understood as more than a case of ‘the neoliberals defeating the Keynesians’, to use Mitchell’s (2010) phrase. The assetization of Norwegian oil, we argue, is indeed a story of financialization based on new economic thinking. But it is also a story of very specific attempts to govern a non-renewable resource according to a set of societal goals; and about the interplay between tools of valuation and the shifting governmental problems that they are employed to address.

Methodologically, we analyse a series of governmental documents from the period 1974–1996. Selected documents that constitute key decision points in the management of Norwegian oil resources are analysed to determine the tools of valuation the management of Norwegian oil resources rely on, the problems that these tools engender, and how the documents respond to these problems. The documents are white papers produced by the Ministry of Finance (MOF) and Ministry of Industry and Energy (MIE) as well as so-called ‘Official Norwegian Reports’ produced by government-appointed advisory commissions. The document analysis is supplemented with existing literature on the governing of Norwegian oil resources.

Before turning to the case of Norwegian oil, however, the next section will expand on the concept of assetization and the analytical strategy of studying the specific tools and practices involved in the assetization process.

Assetization as a governmental practice

The centrality of assets to capital accumulation and financial economy has been highlighted by a long list of economists going back at least to Veblen (1908) as well as Keynes (1936). More recently, however, it has been forcefully argued that economic life has become increasingly centred on asset-ownership and the turning of objects into assets. Recent studies have highlighted how the ‘asset logic’ (Adkins et al., 2021) changes dynamics of accumulation in financialized capitalism (Langley, 2021), and analyses of markets such as the housing market have shown how capital accumulation is increasingly tied to asset ownership (Adkins et al., 2020; Tellmann, 2022). Furthermore, several scholars have been building on Science and Technology Studies (STS) and studies of valuation to focus on the specific practices through which assets are ‘made’ (Birch and Muniesa, 2020; Muniesa et al., 2017). This literature highlights the often quite technical tools involved in assetization processes, especially financial valuation techniques and technologies for creating and stabilizing expectations about future profitability in new technologies such as biotech, apps and digital platforms (Birch, 2017; Birch and Muniesa, 2020).

This paper draws predominantly on the latter tradition, taking its cue from Dewey’s (1939) view of valuation as a practical accomplishment (Muniesa, 2011) – as something that takes work. In line with this pragmatist tradition, a growing literature on valuation has emerged at the intersection of economic sociology, science and technology studies (STS) and related fields (Asdal and Huse, 2023; Chiapello, 2015; Doganova, 2024; Dussauge et al., 2015; Fourcade, 2011; Helgesson and Kjellberg, 2013; Muniesa, 2011). This literature builds on previous work in STS that focuses on ‘market devices’ – the technical devices that make markets and render things ‘economic’ (Callon et al., 2007; cf. Barry and Slater, 2002). A central contribution of this literature is to show how the tools that are employed in processes of valuation, calculation and market exchange also take part in shaping the economic realities that they describe. This is what Callon (2006) has labelled the ‘performativity’ of economics. Analysing the specific ‘tools of valuation’ (Asdal and Huse, 2023) at work – whether in markets or in governmental processes – thus provides a way of understanding how value is conferred and with what consequences.

Among the devices that have been shown to be key in assetization processes are tools that handle the relationship between present and future (Tellmann, 2022). In particular, this concerns the calculation of ‘net present value’ (NPV) by way of discounting expected future income, which is what allows for something to be valued as an asset – that is, as a claim on a future revenue stream (Birch and Muniesa, 2020: 25; Doganova, 2024). This valuation procedure involves a ‘particular temporal structure’ (Adkins et al., 2020: 17) that is future-oriented in the sense of bringing the future into the present. Valuing something as an asset, in other words, relies on a set of economic devices that in effect financializes the relationship between present and future; they become financial tools for ‘binding time’ (Tellmann, 2022) or ‘expropriating the future’ (Gilbert, 2020).

This relationship to time is particularly relevant in relation to the governing of natural resources. It is not a coincidence that, as Doganova (2024) has shown, the financial technique of discounting first emerged in forestry. Forestry is centrally concerned with the timing of harvesting trees in order to secure optimal results for both forest growth and timber revenue. Discounting techniques were first developed to make such decisions calculable. As we will show below, strikingly similar questions arise in the process of managing and governing oil resources.

The importance of ‘binding time’ means that assetization necessarily relies on a range of governmental and legal structures, like laws and enforcement of property rights and arbitration procedures that are required to underwrite claims to future income (e.g. Gilbert, 2020; Nadaï and Cointe, 2020; cf. Ouma et al., 2018). It is therefore not surprising that the governmental and political side of assetization has been a focus in existing work on the subject, and that assetization has explicitly been characterized as a ‘political-economic’ process (Birch and Ward, 2022: 5). Politics and government figures in a few different ways in this literature: One is in the focus on the state as a provider of ‘stability’ (Gilbert, 2020) through the establishment and maintaining of framework conditions such as law, as mentioned above. Another way of approaching the governmental side of assetization is to highlight the political consequences of asset-making, in the sense that turning things into assets has obvious consequences for example for the distribution of political agency and resources (Adkins et al., 2021). And finally, some studies have also focused on how framing something as an asset may be used as a strategy for specific governmental ends – that is, as part of the ‘machineries of public interest’ (Muniesa et al., 2017: 108) or as a ‘mode of governance’ (Birch, 2024). For example, Muniesa et al. (2017) has pointed out how the financial language of assets and investments can be employed as metaphors in a way that ‘prepares the terrain’ (p. 116) for changing the way that public services are provided by the state. Kean Birch argues that this can have important consequences for how governing happens: ‘First, something (e.g. knowledge) is being reconfigured as an asset; and second, how we then understand and act upon (i.e. govern) that something is being reconfigured as a result of our understanding and framing of it as an asset’ (Birch, 2024: 17).

This paper adds to the literature on the political and governmental side of assetization. First, it shows how assetization may happen in an intricate interplay between economic expertise and governmental practice. In the case we analyse, Norwegian oil, this happened not through an automatic or uncritical adoption of a financial logic, but as an outcome of efforts to handle specific governmental problems – that is, to manage a natural resource in the public interest. Second, our analysis demonstrates the centrality of time and timing in assetization processes, as the speed with which oil was to be extracted, was key to the problem that both government and economic experts sought to handle. And third, it demonstrates how valuing something as an asset may have very real and material consequences: The backbone of our story is how the new way of valuing oil led to the establishment of a new governmental infrastructure – the ‘oil fund’ – as well as a speeding up of oil extraction in order to convert geological assets into financial ones.

To advance this analysis, we combine insights from the field of valuation studies with an approach to politics developed at the intersection of Science and Technology Studies (STS) and governmentality studies (Asdal, 2008; Barry, 2001). This approach sees politics as a form of work that is located in the devices, practices and sites of government, that is, in reports, policy documents, procedures of public participation and administrative offices. It is through these devices, practices and sites that a natural resource like oil can be enacted as a governable object. Economic expertise and the tools it offers – like economic modelling and NPV calculations – can be an important element of such governmental practices, as tools that actively value the objects that they seek to govern. When they are brought into the apparatus of government, such tools of valuation may become part of what we call a ‘valuation arrangement’ (Asdal and Huse, 2023) – a mode of valuing that rests on a set of technical procedures and that at the same time produces a specific set of problems for government to address. The central shift that we track in the story that follows is a shift from one such valuation arrangement to another: from valuing oil in terms of economic activity to valuing the same resource as an asset. The tools we focus on within each of these arrangements were introduced by economists, but they gained traction and influence by being taken on board by advisory commissions and actors tied to government. In this way, economic expertise and reasoning were linked directly up with a governmental apparatus of policy documents, legislation and efforts to manage specific problems with respect to resource management. As we will show, assetization emerged as a process intimately linked to governmental practice, and as a solution to the problem of how to manage a natural resource such as oil and, quite concretely, how to optimally time the extraction of the resource.

Oil as a national asset: The case of Norway

Understanding the story of Norwegian oil through a distinction between two fundamentally different ways of valuing it is not an invention of this paper. In fact, the distinction can already be found in a textbook in economics written by a group of prominent Norwegian economists in 1985. ‘The petroleum resources on Norwegian territory can be seen from two different perspectives’, this book proclaims (Bjerkholt et al., 1985: 115). 2 From the following paragraphs, it seems clear that the first of these perspectives is the one that has dominated the government’s approach to oil in the 15 years that has passed from oil was first struck in the Norwegian part of the North Sea until the publication of the book. It seems equally clear that the authors – all with ties to key economic institutions in Norwegian society, such as the University of Oslo’s economics department and the governmental ‘Central Bureau of Statistics’ – favour the second perspective, which entails valuing oil as an ‘asset’ that forms part of the ‘national wealth’. The book, in other words, can be seen as an intervention – an argument by a group of influential economists that Norway’s way of governing its significant oil resources is in need of fundamental change.

Today, Norway’s management of its oil resources is often highlighted as an exception relative to the experience of other oil states (e.g. Urry, 2013), in that the economic benefits from oil have to a large extent been widely distributed across society, sustaining an expanding welfare state and retaining relatively low levels of inequality. This exception is usually explained by an elaborate setup of governmental tools and institutional infrastructures sometimes referred to as the ‘Norwegian model’ (Al-Kasim, 2006; cf. Ryggvik, 2015). The ‘Norwegian model’ includes a licencing system that ensures government control over exploration and production decisions, as well as a tax system which ensures that most of the profits are captured by the state and reinvested in what is popularly known as the ‘oil fund’ – a sovereign wealth fund officially named the ‘Government Pension Fund Global’ (Clark and Monk, 2010; Lie, 2018).

This system for turning oil resources into government riches has indeed made oil a major part of Norway’s ‘national wealth’: Today, official statistics and government documents usually represent the nation’s total wealth as made up principally by the country’s ‘oil assets’ (i.e. remaining oil and gas reserves) together with its ‘financial assets’ (i.e. oil revenue captured in the sovereign wealth fund) and ‘human capital’ (e.g. MOF, 2017: 113). Oil, in other words, is valued as a very particular kind of asset: As part of the nation’s public wealth, as something which should benefit and be governed by the public, but which nevertheless should be governed as an asset.

As the economics textbook from 1985 alerts us to, however, this has not always been the case (cf. Asdal, 2014; Nilsen, 2001). In the words of the textbook’s authors, the view that had so far dominated Norwegian oil policy was that the petroleum resources ‘represent the basis for productive activity’ (Bjerkholt et al., 1985: 115). That is, the value of oil is as a natural resource that generates industrial development and activity. In what follows, we trace the transformation from governing oil in terms of its activity-generating capacity and towards governing it as an asset. We focus in particular on the shifting tools of valuation this transformation implied, how these tools were employed and how they both generated problems and were intended to solve specific problems with regards to managing the oil resource.

Governing oil for a ‘qualitatively better society’

From the moment oil was struck on the Norwegian continental shelf, it was clear that the newly discovered resource would be of great value to Norwegian society. But in what precisely did this value reside? One answer could be that it resided in its market price as a commodity. The 1973 OPEC crisis, which followed shortly after the discovery of Norwegian oil, led to a dramatic rise in the oil price apt for fuelling expectations about large profits. However, the Norwegian government encountered the situation differently. Shortly after the OPEC crisis, the Ministry of Finance (MOF, 1974) presented a white paper on ‘the role of petroleum activity in Norwegian society’ which proved foundational for the direction of Norwegian oil policy for more than a decade (Hanisch and Nerheim, 1992: 406; Nilsen, 2001). What is striking is how the ministry values oil not in terms of its price in commodity markets. Rather, oil was valued primarily based on the level of economic activity it would bring to society as a whole.

Values are indeed central to this policy document: As the white paper formulates it, the recent oil discoveries ‘will make the nation richer’ (MOF, 1974: 6, emphasis in original). Yet, these riches are not primarily tied to the immediate market price of oil, but rather to the level of investment, consumption and most prominently employment, which oil will bring. In other words, the oil is valued for its properties; as a raw material for industrial development and, following from this, as a catalyst of jobs. In short, as the title of the white paper also makes clear, it is valued quite literally as ‘petroleum activity’ (petroleumsvirksomhet).

In this valuation arrangement – valuing oil as activity – a set of distinct tools of valuation are involved. These tools are closely linked to the existing apparatus for economic planning which Norway had built in the postwar years to implement a social-democratic program of a market economy with strong government involvement. The central documents of this planning apparatus were the 4-year ‘long term programmes’ and the annual national budgets, both prepared by the MOF and based on macroeconomic modelling developed by the Central Bureau of Statistics (now Statistics Norway, an independent government agency). It was a particular macroeconomic model built by economists from these institutions – the input-output model ‘MODIS’ – which was now employed to calculate the value of oil for Norwegian society along two axes: First, in the form of an estimate of the ‘direct effects on Norwegian employees and businesses taking part in exploration, extraction, base activities, supplying platforms and equipment etc., and through processing in the form of refining, petrochemistry etc.’ (MOF, 1974: 7). These direct effects were estimated in monetary terms, but were then immediately translated into an estimate of the number of jobs the activity would add (about 15,000 in 1974).

Second, there was a detailed focus on how income from oil and gas production would result in increased public and private consumption, which would further increase economic activity and employment. The issue is not the exact levels of income to be expected (which ‘around 1980 (. . .) is estimated to be between 10 and 15 billion Kroner per year’ (MOF, 1974: 45)). Instead, the key concern is the effect this income will have on different economic sectors as it is spent: ‘Every billion Kroner (in 1974 prices) of oil income that is spent domestically will by 1980 easily require an additional 7,000-8,000 employees to produce the goods and services demanded’ (MOF, 1974: 7).

In other words, the value of oil is tied not primarily to its market price or the income it generates. Rather, it resides in the employment and activity it brings about – first directly through its production, and then indirectly when the income is put into circulation. This is in line with what the economics textbook mentioned above describes as the dominant view of the 1970s and early 1980s. As mentioned in the introduction, Norwegian economists, including those at the MOF and the Central Bureau of Statistics, stayed close to the Keynesian view on the importance of counter-cyclical measures longer than in most other European countries (Asdal, 1995; Lie and Venneslan, 2010), and at this point, the dominant view was that economic policy was to support and strengthen industrial activity.

At the same time, these model estimates engendered a series of concerns that followed directly from the activity that oil would bring. The MOF’s modelling showed how the ‘estimated growth in employment numbers’ as a result of ‘growing petroleum activity’ and ‘use of petroleum revenue’ would lead directly to an ‘estimated decline in other industries’ (MOF, 1974: 8). The concern was that this structural reorganization would lead to drastic changes in Norwegian society, especially if oil industry development proceeded too quickly or if domestic spending increased substantially, thereby ‘overheating’ the economy. Thus, concerns about the phenomenon known as Dutch disease – a short-term boost to economic activity due to the rapid depletion of exhaustible resources (e.g. Ross, 1999) – was closely tied to the way in which oil was valued, and presented a problem for government to address: How to balance the structural changes brought about by increasing activity against the benefits of oil. This problem was regarded as ‘the most important question to address with regard to petroleum activity’ (MOF, 1974: 8, emphasis in original).

In short, the valuation arrangement described above valued oil for its activity-generating capacity, and not so much for its generation of new cash flows. This way of valuing oil came with a very specific governmental problem: How to avoid too much activity and an overheated economy. Consequently, the 1974 white paper expresses an ambivalent and rather sceptical view on the expected growth. The statement that oil ‘will make the nation richer’ can thus be read not just as something to celebrate, but also as a sort of warning (Lie and Venneslan, 2010).

While presenting the governmental problem of controlling the activity oil would bring to avoid overheating, the white paper also envisioned a distinct way of managing this problem politically. The overarching goal that the document set out was to ‘utilize these new opportunities so as to develop a qualitatively better society’ (MOF, 1974: 6, emphasis in original). In other words: The solution to successfully managing the increasing activity brought about by oil was to use this activity to build an economy that not simply grows in quantity, but that primarily improves in quality. The white paper linked this goal to the wider project of the social-democratic government at the time, to ensure ‘greater equality in living standards, (. . .) further expansion of the welfare state (. . .), strengthening local communities’ and to ensure that ‘democratic institutions gain real control’ over the further development of society (MOF, 1974: 6).

To achieve this ‘qualitatively better society’, the issue of timing and speed was central. It was imperative that the oil industry’s growth was kept at a ‘moderate’ level. Only in this way could the structural changes foreseen by the ministry’s macroeconomic models be managed and controlled. The Keynesian models of the MOF – in combination with a social-democratic political programme – thus established what became known as the ‘tempo question’ as the key challenge to the governing of oil (Nilsen, 2001; Ryggvik and Kristoffersen, 2015): If oil extraction proceeded too quickly, this would cause problems in the economy and put the goal of a ‘qualitatively better society’ at risk. The political task therefore became to control the pace of development through democratic institutions, in order to ensure an optimal temporal distribution of the activity.

Long discussions followed over the course of the 1970s and 1980s about how to manage the ‘tempo question’. To ensure that the oil industry did not grow too quickly, there was generally broad agreement about using a range of interventionist measures, including state ownership and industrial policy (Hanisch and Nerheim, 1992). By keeping the pace of extraction at a ‘moderate’ level, it would be possible to coordinate industrial activity to ensure good societal outcomes, and to balance the growth against existing industries and distribution between different geographical regions in the country.

Introducing a new valuation arrangement: ‘Purely . . . economic calculations’

The tempo question was discussed in numerous policy documents and expert reports throughout the first two decades of Norwegian oil production, mostly based on the same tools of valuation outlined above. Over the course of the 1980s, however, a series of new tools for valuing oil emerged. These new perspectives were first introduced by academic economists, as exemplified by the previously mentioned economics textbook (Bjerkholt et al., 1985). The emergence of new valuation tools can therefore be linked to a generational change among Norwegian economists who at this time were ‘catching up’, so to say, with a shift towards a more neoliberal outlook that had already taken place among their peers in other parts of the Western world. The early 1980s also saw changes in the global oil market, with a move away from long-term contracts and OPEC price control and towards a spot market with fluctuating prices and a more important role for traders (Claes, 2001: 77–78).

It took time, however, before the new tools of valuation that economists introduced were taken up by the MOF and made part of official policy documents. Two expert commissions provide particularly good entry points for understanding how this shift happened. Both commissions were established by the MOF to produce a so-called ‘Norwegian Official Report’ (NOU), which are advisory reports commissioned by government to underpin political decision-making (Christensen and Holst, 2017; Tellmann, 2017).

The first of these reports, published in 1983, was written by the so-called ‘tempo commission’, which was established precisely to answer the key question of how to manage the timing of oil extraction (Government of Norway, 1983). As part of its discussion of the tempo question, this report introduced a new way of valuing oil, which differed markedly from the mode of valuation that was prevalent in the 1974 white paper analysed above. The new mode of valuation discussed in the commission’s report centred on the idea of managing oil according to a financialized logic: One possible way of choosing the pace of extraction is to consider the petroleum resources as a stock (lagerbeholdning). One may choose to deplete the stock over a shorter or longer period of time. The choice of depletion rate can thus be made purely on the basis of economic calculations (Government of Norway, 1983: 84 emphasis added).

Following on from this assertion, a separate section of the report headlined ‘Present-value considerations’ laid out the tools with which such calculations could be made. The approach largely followed the procedure set out by Hotelling (1931) for how to maximize the economic gains of exploiting ‘exhaustible assets’: First, by forecasting future oil prices, as well as future production costs, to determine the expected future cash flow from oil production. This procedure turned future oil into an economic entity with a precise monetary value. Then, in a second step, the expected future income was recalculated by discounting it. To explain the technique of discounting, the commission’s report provided an analogy: Money available today is expected to yield a return, either through interest rates if placed in a bank, or through a return on investments in financial markets. In other words, present money is worth more than future money because its value is expected to grow over time. Having provided this analogy for the general reader, the valuation procedure was now applied to oil: If the discount factor is ‘interpreted as a bank interest rate, any level of [future] oil production could be discounted with the assumed interest rate to a capital stock today, a so-called “present value”’ (Government of Norway, 1983: 84).

Together, then, the two tools of valuation – calculating the future cash flow and discounting it to bring it into the present – produced the net present value of Norway’s oil resources – that is, the current worth of the future income that Norway’s oil resources was expected to yield. In other words, the oil was now turned into an asset, very much as defined in recent literature on assetization, as a ‘claim on a future revenue stream’ (Birch and Muniesa, 2020). As previously noted, this valuation procedure involves a future-oriented temporal structure, focusing on future income rather than the oil’s immediate worth (cf. Tellmann, 2022). It also foregrounds and values oil as a financial entity, making oil resources commensurable with bank deposits or investments in financial markets. Furthermore, the new tools of valuation also have consequences for the governing of oil. In fact, the new valuation-procedure gave rise to a new problem for government, fundamentally recasting the ‘tempo question’, as we will further explore below.

As mentioned, the report here followed what economists refer to as the ‘Hotelling rule’. Interestingly, when developed and published in 1931, the empirical context for Hotelling’s concern with the economics of exhaustible resources, was the emergence of the conservationist movement and arguments for preserving natural resources. ‘It may seem’, Hotelling then reasoned, ‘that the exploitation of an exhaustible natural resource can never be too slow for the public good’ (Hotelling, 1931: 138). It was however not until the mid-1970s that his argument gained traction, namely in the years following the Limits to Growth debate (Meadows et al., 1972) and the oil crisis of the 1970s (for this, see Ferreira da Cunha and Missemer, 2020; Gaudet, 2007). At this time, economists like Robert Solow and William Nordhaus brought Hotelling’s work into the economic mainstream, from which it became a ‘natural resource’, so to say, for Norwegian economists to employ in relation to the issue of the management of oil (e.g. Bjerkholt et al., 1985).

Assetization as re-timing: From ‘moderate’ to ‘as quickly as possible’

One implication of valuing oil as an asset is that it becomes commensurable with other assets – primarily financial ones (Chiapello, 2015, cf. 2024). This is frequently seen in Norwegian policy documents, where the ‘oil asset’ is placed alongside ‘financial assets’ and ‘human capital’ as making up the nation’s total wealth (e.g. MOF, 2017: 113). Such a commensuration with financial assets was already present in the 1983 commission report, which stated that the ‘alternative to leaving the petroleum in the ground and earn rent according to its real price increase (. . .) is to extract, sell, and earn normal market rent on the income’ (Government of Norway, 1983: 84). In this way, oil is placed in the same category as financial holdings, as in principle convertible with them. This in turn affects the speed with which the oil is to be extracted from the ground. Thus, it goes to the core of what was regarded as the key problem of governing oil, namely the ‘tempo question’.

The answer to this timing problem was however not a given. The two ‘alternatives’ confronted the government with a choice. One could either follow the path preferred since the 1970s of a ‘moderate’ pace of extraction. This would imply betting on the value of the asset increasing over time and in this way enhancing the value of the asset. Alternatively, one could seek a more rapid extraction pace in order to convert oil assets into financial capital. This could enhance the value of the asset not due to an increasing price in commodity markets, but through the return on financial investments after the oil is extracted and sold.

The quote above about deciding the pace of production ‘purely on the basis of economic calculations’, refers to this choice. And it is a choice conditioned upon the employment of precisely the tools of valuation of economics integral to the assetization operation, namely forecasting and discounting. In putting these tools of valuation to work, purely economic calculations could decide which of the two alternatives above would ensure the best result. With oil valued as an asset, the best result equals the highest possible ‘present value’ of Norwegian oil resources. Importantly then, the ‘tempo question’ was reframed as a calculative challenge that could be solved by what was referred to as ‘purely economic’ tools of valuation.

As if to underscore the ‘purity’ of these technical procedures, the commission’s report includes two sets of calculations by independent experts. Whereas the report itself is written by the politically appointed members of the commission, with different disciplinary and political backgrounds, the calculations are instead produced by independent academic economists, and presented as two separate appendices to the report. Both appendices present an unequivocal answer to the tempo question: The present value of Norwegian oil resources will increase by converting the oil assets into financial ones (Government of Norway, 1983: 160). Furthermore, the uncertainty of future oil prices means that the best way to minimize risk would be if ‘the values are realized’ – that is, extracted, sold and reinvested into financial assets – ‘as quickly as possible’ (Government of Norway, 1983: 143).

For these economists, in other words, valuing oil as an asset led directly to a recommendation for speeding up oil production. They thus contradicted the long-standing goal of maintaining production at ‘moderate’ levels, which had followed from the macroeconomic modelling of employment and structural economic change. Instead, they argued for the maximization of present value by speeding up production, as the decisive factor for governing the country’s oil resources.

This provided a quite different answer to how oil should be governed for the public good: from being a question of how oil might enable a ‘qualitatively better society’, the question became how to maximize the financial value of the resource. As mentioned above, other scholars have pointed out how assetization is a time-question that renders the future present (Muniesa and Doganova, 2020; Tellmann, 2022). The case of Norwegian oil, however, is not only a question of representing the future in the present. The assetization operation also works on the question of time at a more fundamental level, by re-timing the very governing of the resource. This re-timing implied a transformation of the ‘tempo issue’ from being about a moderate speed of extraction to opening up for extracting the oil ‘as quickly as possible’. The consequence of this move was, as we will see in the following, a whole new infrastructure for converting and storing oil, not in the ground, but in a fund.

These consequences were not immediate, however, because at this point, the report from the 1983 commission takes an interesting turn. Despite the unequivocal results of the economic calculations, the commission’s report does not fully endorse the recommendations of the independent academic economists. In fact, the commission disputes a core assumption of the calculations, namely that it would be possible to convert oil income directly into financial savings. The commission members argued that as government income increased, political pressure to increase spending would prove impossible to resist. ‘A crucial weakness in reasoning based on present value’, the report points out, is that the ‘possibility of separating earnings from spending’ is severely limited by ‘how our political and institutional system works’. Therefore, ‘the criteria chosen [for determining the pace of extraction] must be based on more realistic assumptions’ than those of the academic economists (Government of Norway, 1983: 88).

Summing up, we have seen that the commission’s report introduced a new way of valuing oil, enabled by a set of tools of valuation: The tools of forecasting that established an expected future cash flow from oil, and then discounting it to calculate its ‘present value’. By this procedure, oil is rendered financial and provided with a future-oriented monetary value, and oil is valued as an asset to be safeguarded by maximizing its present value.

By valuing oil as an asset, these tools also reframed the fundamental question about how oil should be governed. However, at this particular point in time, the new tools were not seen as sufficiently aligned with the political reality of governing oil. They therefore had few immediate consequences. This situation would however change over the coming years.

Economic tools and governmental infrastructures: Establishing new realities

Despite the 1983 commission’s reluctance to embrace the implications of valuing oil as an asset, academic economists continued to develop the understanding of oil in this direction. In particular, the idea of separating earnings from spending through the establishment of a separate fund for oil revenue was debated among economists as well as political leaders (see Lie and Venneslan, 2010: 343–347). At the Central Bureau of Statistics and the University of Oslo’s economics department, economists attempted to model how to maximize the present value of the ‘oil asset’ and the optimal rate of conversion from oil resources to financial assets. One outcome of this work is the previously mentioned textbook, which contrasts the traditional valuation of oil in terms of activity with the new approach of valuing it as an asset (Bjerkholt et al., 1985). Another example is the work of a young researcher working within the same group of economists, Jens Stoltenberg, who calculated the optimal rates of conversion between oil assets and financial assets (Stoltenberg, 1985). When a new government commission consisting almost exclusively of economists was established by the MOF in 1988, it was able to draw on the existing academic work to further advance the asset orientation.

The report from the 1988 commission placed the entire discussion about oil and gas production under the heading ‘Concerning the management of petroleum assets’ (Government of Norway, 1988). The main message was that the oil resources represent an asset that is being depleted as oil is being produced and sold, unless the income from this production is converted into savings as financial holdings. On this basis, the commission recommended to establish a fund that would capture oil revenue in order to build up financial assets abroad (Government of Norway, 1988: 95).

This time, the idea of separating income from spending and reinvesting oil revenue in financial markets was met with less resistance. In 1990, the government proposed a law establishing a ‘government petroleum fund’. In their proposal, the government highlighted ‘that petroleum income leads to a corresponding reduction in the petroleum asset’ (MOF, 1990: 5, emphasis in original). This implied that financial assets had to be built up to avoid a depletion of the nation’s total asset base. The proposal for a ‘government petroleum fund’ was meant to address this risk: By transferring state revenue from oil production into the fund, the oil asset would not be depleted, but simply converted into a new financial form. In this way, the fund was constructed as a governmental infrastructure that enabled the kind of asset management that economists had argued for since the early 1980s.

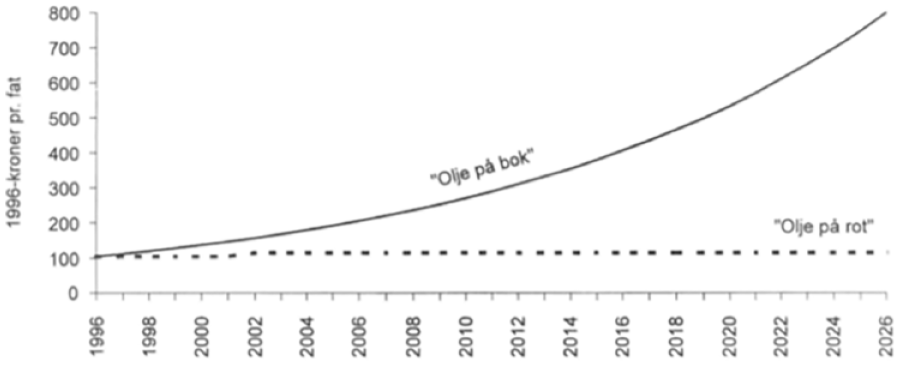

The ‘government petroleum fund’ was established in 1990, and quickly became known colloquially as the ‘oil fund’. (The official name was later changed to ‘The Government Pension Fund Global’.) Although it took several years before the first transfer of revenue to the fund was made, its proponents argued that converting oil resources into financial holdings was the safest way to maximize the present value of the oil asset. For example, in a white paper from the Ministry of Industry and Energy in 1996, the value of ‘oil in the ground’ was compared directly to the value of ‘oil in the fund’ (MIE, 1996). Based on the same tools of valuation outlined above, the document showed the value of the former as stagnant and the latter growing indefinitely (see Figure 1). To explicate the choice facing political decisionmakers, oil was compared to a forest that may either be cut or left standing: Leaving it in the ground as ‘rooted timber’ (på rot) would yield a lower future value than harvesting it and converting it into financial holdings (på bok). As the overarching goal for the government’s oil policy, according to this policy document, was to ensure ‘as high as possible a value of the oil and gas resources’ (MIE, 1996: 21), the answer was already given: Maximizing the present value of oil meant aiming for a rapid conversion from ‘ground’ to ‘fund’. Increasing the speed with which oil is produced was thus presented as the responsible course of action for preserving the value of oil into the future.

‘A simplified illustration of the value of a barrel of oil in the fund compared to the value of a barrel of oil in the ground’, in Kroner per barrel (1996 prices). The solid line is marked ‘Oil in the fund’ – literally ‘oil on book’, that is, bankbook. The dotted line is marked ‘Oil in the ground’ – literally ‘oil on root’, as in ‘rooted’ or standing timber. Figure from the Ministry of Industry and Energy (MIE, 1996: 20).

The minister presenting this striking illustration of proper asset management to parliament was Jens Stoltenberg, formerly a researcher at the Central Bureau of Statistics and part of the group of economists who calculated optimal rates of conversion from oil resources to financial capital. As a Labour politician, first as minister of industry and energy and later as finance minister, he was well placed to implement new tools for valuing and governing oil as an asset. After taking over as prime minister in 2000, he followed up the establishment of the oil fund by introducing the so-called ‘fiscal policy rule’ (Mjøset and Cappelen, 2011). The rule says that the government should never spend more from the fund than its expected real returns. The rationale is that as long as the rule is followed, it will ensure that the fund’s financial assets are left as a source of income for eternity – as a substitute for the oil resources from which it has been ‘converted’. 3

By creating the oil fund, and later the fiscal policy rule, the government thus established in practice the administrative apparatus that would allow a deliberate conversion of oil assets into financial ones. In this way, economists in powerful positions helped connect the new valuation practices to the governmental tools that enabled oil to be managed as an asset commensurable with other assets. In less than two decades, this fundamentally changed the realities of how oil was being governed: In 1983, the ‘tempo commission’ had dismissed the economists’ idea of separating earnings from spending as completely out of touch with ‘how our political and institutional system works’. With the establishment of the oil fund and the fiscal policy rule, however, the ‘political and institutional system’ had been remade precisely to enable this separation. The fund and the rule together comprised a governmental infrastructure for managing oil as an asset, safeguarding its future and maximizing its value by physically converting it from oil in geological reservoirs to holdings in international financial markets.

Conclusions: Assetization and government

The story of how Norwegian oil came to be valued as an asset is clearly a process of assetization, in which new tools from financial economics is put to work to value Norwegian oil resources as a ‘claim on a future revenue stream’ (Birch and Muniesa, 2020). The story illustrates how assets can come about through ‘the machineries of the public interest’ (Muniesa et al., 2017: 108) – that is, the devices and procedures of government – in interplay with new forms of economic expertise. The ‘purely economic calculations’ that academic economists presented to the Norwegian government played a key role in revaluing oil as an asset. To gain influence, however, these calculations had to be enabled and realized by a government apparatus of reports, rules and institutions that provided the conditions under which they could be seen as ‘realistic’. The resulting valuation arrangement was successful precisely because it cut across the spheres of economics, markets and government to enable a new formulation of what it meant to govern oil in the public interest. To put it very simply, the most important economist in this story was the economist who became a government minister and was able to put the state apparatus to use in order to value and govern oil as a state-controlled asset.

It is not surprising that governmental action in the form of legal and institutional frameworks is a prerequisite for turning natural resources into assets. What the case of Norwegian oil brings out, however, is how the role of the state may go well beyond the establishment of frameworks within which things can be turned into assets. In this case, the shift towards a radically new valuation arrangement happened as a way of handling specific governmental problems related to the management of natural resources. It happened through an extended government apparatus, most notably advisory commissions where expert reasoning and advice is brought into government; and it also happened within government, by way of white papers, propositions and legal arrangements and decisions. But importantly, it did not happen only at the metaphorical level or as a new way for government agencies to ‘see’ or talk about oil. To the contrary, the new valuation arrangement led to a quite literal transformation of the country’s oil resources, as it established an infrastructure – the ‘oil fund’ and a set of related policies – that allowed for a speedy conversion of ‘oil in the ground’ into ‘oil in the fund’. To some extent, this shift also transformed the state, by redefining its role into that of an investor seeking to maximize the present value of its assets. Turning Norwegian oil into an asset thus enabled a specific way of governing which in turn acted upon and changed both the oil and the state that governs it.

The problem that government sought to manage by valuing oil as an asset was intimately linked to the issue of time and timing: The so-called ‘tempo question’ centrally concerned the timing of oil extraction, and the speed with which oil revenues were to be pumped into the economy. Providing a way of answering this question through ‘purely economic calculations’, it was the temporal structure of the asset form as essentially a means of making future revenue calculable and actionable in the present, which made it attractive for government. Tracing the shifts in what was considered the relevant political-economic problem to be solved, and their respective answers, thus sheds light on how assetization can emerge as a governmental strategy. Furthermore, situating these processes historically also serves to remind us that the financialized ‘asset economy’ is, after all, a relative new phenomenon: until quite recently, very different modes of valuation were dominant in governmental practice.

Footnotes

Acknowledgements

Earlier versions of this paper have been presented at 4S 2021, the Nordic STS Conference 2021, and the workshop ‘Toolbox of Environmental Governance’ at KTH, Stockholm. The authors are thankful for comments received from participants at these conferences as well as from Liliana Doganova and three anonymous reviewers.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work has been supported by grants from the Norwegian Research Council (grants 268056 and 301733) and from the research programme ‘Future Challenges in the Nordics – People, Culture and Society’ (project ‘Fossil Free Futures’).