Abstract

Infrastructure has grown rapidly as an alternative asset class, yet many of the complex processes that transform public infrastructures into lucrative financial assets are poorly understood. This article examines investments by an infrastructure debt fund, to show how financial innovations expand and diversify the infrastructure asset class by finding new ways to generate financial returns from infrastructures. Infrastructure debt is an emerging sector of the infrastructure asset class, where private debt funds create assets that generate returns by extending loans or bond financing to physical infrastructures. The analysis uses assetization as a conceptual framework to scrutinise the construction of financial assets, centring the role of rent generation and extraction to show how infrastructure debt funds create financial value. By bringing the performative work of asset construction into dialogue with the political-economic forces enabling rent extraction, the analysis augments existing literature on financialized infrastructures. The findings show how infrastructure debt assets are predicated on multiple rounds of assetization: initially, the essential nature of infrastructure services is exploited to generate and extract monopoly rents as long-term revenue streams, and in turn, debt funds extend claims on these revenue streams to extract rents through interest payments. In this way, infrastructure debt extends the infrastructure asset class and provides a new route to extract rents, raising concerns over the potential of these investment practices to contribute to inclusive regional development and just transitions to mitigate and adapt to climate change.

Introduction

The growth of the infrastructure asset class since the 1990s has been catalyzed by financial innovations involving complex financial, legal and ownership structures. Yet, there are large gaps in understanding how private investors have transformed infrastructures into financial assets. Showing how financial innovations seek to extract returns from physical infrastructures is crucial to explain the wider impacts of the infrastructure asset class on economic development, inequalities and decarbonization, as policy agendas seek to ‘crowd in’ private capital to remedy infrastructure deficits and deliver on net-zero agendas.

This article addresses gaps in existing literature by examining how financial innovations construct new assets that derive returns from infrastructures. The analysis focuses on infrastructure debt funds: vehicles that pool capital from investors and deploy it through private debt (loans) for infrastructure assets or utilities. Debt funds gained prominence after the 2008 Global Financial Crisis, as an alternative form of credit to commercial bank finance. Before the crisis, infrastructure investment took place primarily through equity funds, with debt provided by bank loans or wrapped project bonds. Post-crisis regulatory changes restricted banks’ capacity to hold long-term loans for infrastructure, allowing private debt investors to enter the market. Additionally, increased competition in the infrastructure market spurred investors to take riskier positions as lenders, in search of higher yields.

Infrastructure debt funds offer institutional investors, typically pension funds, insurers and sovereign wealth funds, exposure to infrastructure assets while retaining the certainty of fixed-income assets. Debt (or credit) is a fundamental part of the financial system and historically it has been deployed both for progressive purposes (Quinn, 2019) and the extraction of rents (Christophers, 2020). By bundling debt contracts into listed or unlisted funds, infrastructure debt funds deploy debt in a specific way to create a new type of infrastructure ‘asset’ that doesn’t require an equity stake in the underlying physical asset.

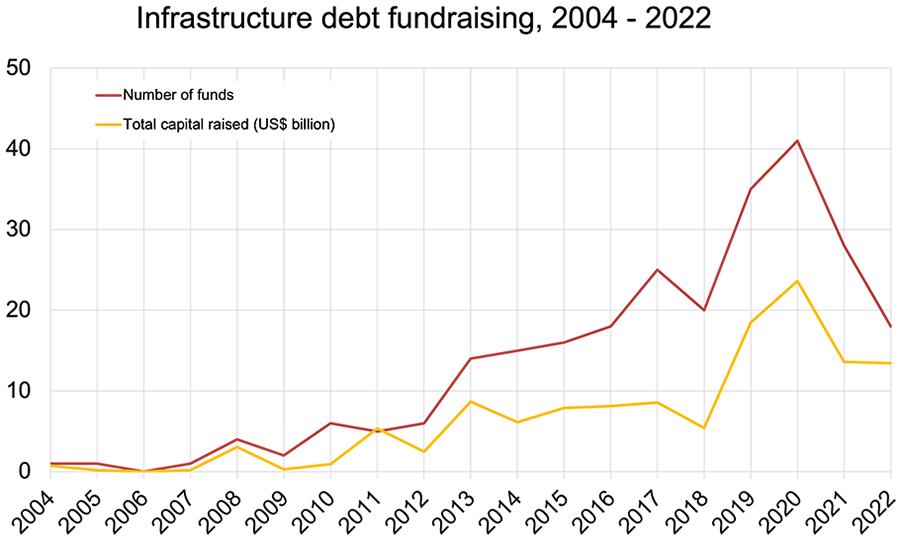

Infrastructure debt fundraising increased steadily from 2010 onwards, as shown in Figure 1. The increase in fundraising in 2020 was attributed to the relative appeal of safer assets during the economic volatility and uncertainty spurred by the COVID-19 pandemic (Infrastructure Investor, 2021).

Infrastructure debt fundraising, 2004–2022.

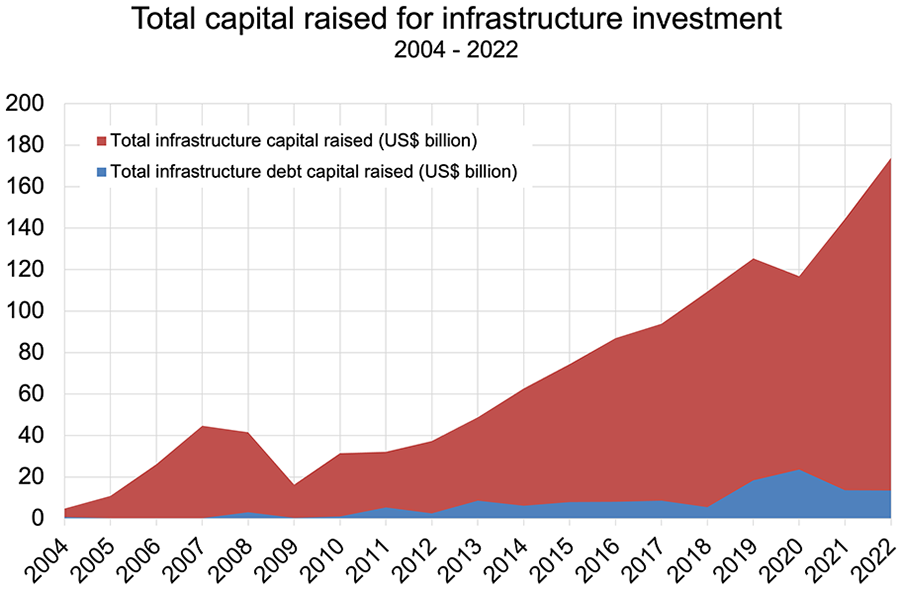

Infrastructure debt funds only make up a small proportion of fundraising for infrastructure investment, as shown in Figure 2. Yet, debt funds have been launched by leading asset managers such as BlackRock, Macquarie Group and Brookfield Asset Management and warrant closer attention to understand how financial innovations are diversifying the asset class. Furthermore, debt funds are closely intertwined with equity funds, often lending to assets already owned by infrastructure equity funds (Christophers, 2023: 275).

Total fundraising, 2004–2022.

Background: Development of the infrastructure asset class

Since the 1970s, the globalization of financial markets enabled a distinct turn in infrastructure financing as institutional investors and state actors sought to develop infrastructure as an asset class. Investors targeted infrastructure assets to diversify their portfolio and gain access to secure, long-term revenue streams provided by essential services. Yet, this asset class is now dominated by infrastructure funds and asset management practices that rely heavily on gearing and financial engineering to generate returns (Ashton et al., 2012; Christophers, 2023; Torrance, 2009).

Investors primarily invest in infrastructure through listed or unlisted infrastructure equity funds, or funds-of-funds. Although some institutional investors have in-house expertise to make direct investments, most choose to outsource these investments to third-party asset managers with specialized skills and expertise (Monk et al., 2018: 19).

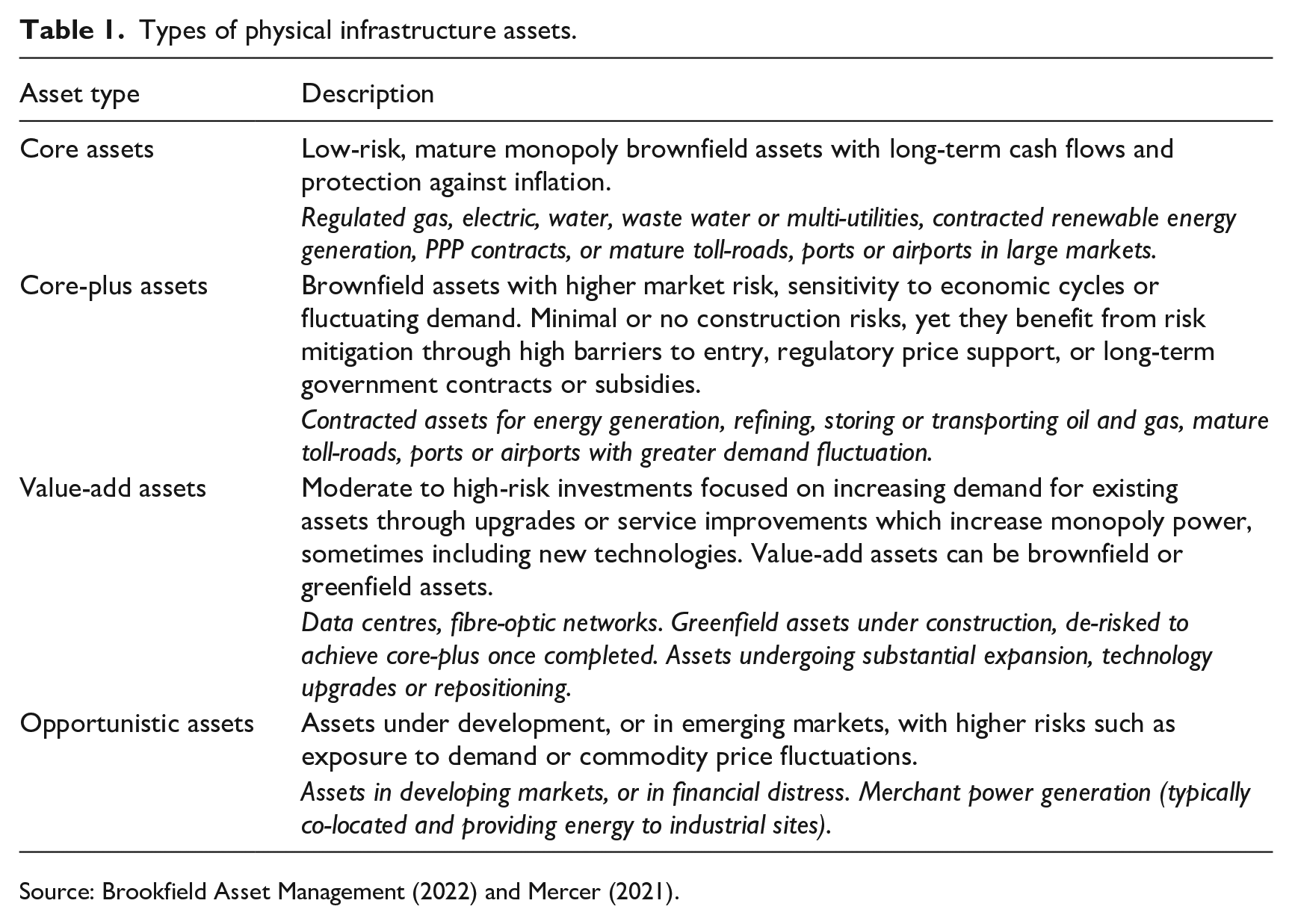

The monopoly characteristics of infrastructure systems or networks are central qualities from an investment perspective: Table 1 outlines the different types of physical infrastructure assets, based on the nature of the service they provide and the types of risk they are exposed to.

Types of physical infrastructure assets.

Source: Brookfield Asset Management (2022) and Mercer (2021).

Successive financial innovations have catalyzed the growth of the infrastructure asset class. Infrastructure equity funds were pioneered by Australian asset manager Macquarie in the 1990s. Funds helped to overcome the ‘lumpiness’ of infrastructures as large, indivisible assets which exceeded the investment capacity of many individual investors, by pooling capital and deploying to a diversified portfolio of assets (Weber and Alfen, 2016). In the wake of Australia’s privatization programme, Macquarie used equity funds to take advantage of new tax concessions for infrastructure loans, deploying investment capital produced through pension reforms (Solomon, 2009: 54). The resulting Macquarie Model invested through a ‘solar system’ of highly leveraged equity funds, which collected substantial management and performance fees for the parent company (Jefferis and Stilwell, 2007; Mann and Blunden, 2015).

The equity fund model expanded internationally, and infrastructure funds are now the most common investment vehicle. The rapid expansion of the infrastructure asset class since 2010 is partially attributed to ultra-low interest rates, which reduced yields on traditional asset classes such as public debt, driving many institutional investors to alternative assets in search of higher returns (Christophers, 2023: 112). Yet, the proliferation of infrastructure funds does not reflect widespread satisfaction amongst institutional investors. Monk et al. (2018) show how principal-agent problems arise when institutional investors outsource investment decisions to third-party asset managers: managers of private equity-style funds are incentivized to front-load their returns, leading to extractive practices and financial engineering, which is at odds with pension funds’ desire for stable, long-term returns and responsible asset management (Christophers, 2023).

Infrastructure debt funds are a newer innovation, which pool capital into an unlisted fund that issues debt to infrastructure projects or firms. As a form of private debt, infrastructure debt funds fall outside the purview of bank regulation. The growth of private equity funds during the 1990s spurred the development of private debt as an asset class, since private equity funds relied on substantial leverage to generate returns, thus creating demand for debt finance (Bakie, 2019). After the 2008 Global Financial Crisis, the Basel III/CRD IV regulations reduced banks’ ability to provide large, long-term loans for infrastructure projects (Gawlitta and Kleinow, 2015), allowing private debt providers to enter this segment of the market with less competition. Infrastructure debt offered institutional investors, typically pension funds, insurers and sovereign wealth funds, an opportunity to increase their exposure to infrastructure while retaining the certainty of fixed-income assets that were trading at very low yields (Alves, 2013). The emergence of infrastructure debt as a financial ‘asset’ shows how the infrastructure asset class extends to include any financial asset for which returns are derived from infrastructure development or operation.

Theoretical framework

This section reviews existing literature on the infrastructure asset class and contributions from scholars working on rent and assetization. Most research on the infrastructure asset class draws on the lens of financialization, elaborating the development of the infrastructure asset class across three themes: the types of legal, accounting and organizational reconfiguration deployed, the state’s role in enabling private investment, and the growth of private equity-style investment models.

Legal, accounting and organizational reconfigurations of infrastructures and their corporate entities is a key practical concern for investors. Since infrastructures are spatially-fixed assets, embedded within economies, supply chains and socio-economic relations, distinctive property relations need to be secured to ensure that the material flows enabled or generated, can be controlled and optimized through ownership and access rights (O’Neill, 2013). Capital structuring of projects and assets has evolved into a ‘nervous settlement’ between equity and debt providers who are vying to maintain control over assets while leveraging higher returns (O’Neill, 2019: 1316). Legislative and regulatory settings determining levels of service, maintenance and investment requirements, and pricing of infrastructure services, are pivotal to govern infrastructure ownership and the management of assets. However, legal and accounting reconfigurations have also proven effective in overcoming regulatory limits, transforming utilities into a web of corporate entities that can shift activities outside the scope of regulatory control (Bayliss et al., 2022).

The roles of national and local state actors in enabling financialization has gained greater recognition. State actors often set the preconditions for financialization, including austerity budgets, historic investment deficits and projected investment needs to reach net-zero targets (McArthur, 2023). Financialization can also emerge from complex central-local government power relations, budget-setting and devolution processes. In the UK’s centralized system of government, local governments entered into a range of financialized governance and operational arrangements amidst a prolonged period of fiscal austerity, creating new uncertainties and governance challenges (Pike et al., 2019).

The growth of private equity-style funds received increasing attention from the mid-2000, as funds took advantage of low interest rates, securitization, interest rate swaps and transaction fees to generate financial returns from infrastructure deals (Allen and Pryke, 2013). These models are mostly deployed in Europe, North America and Latin America, where privatization and investor-friendly regulations have created a favourable investment environment (Loftus and March, 2019; Pryke and Allen, 2019, 2022; Ward, 2020). They are less common in the Global South, yet, organizations like the World Bank Group encourage supportive regulatory frameworks and de-risking measures such as subsidies or guarantees to attract private investment (Bayliss et al., 2021; Furlong, 2022; Gabor, 2021). Although private-equity style funds comply with existing laws and regulations, they have attracted criticism for extracting large dividends while failing to make adequate investment in maintenance and upgrades, before exiting the investment and leaving the asset with significant debt-servicing costs and maintenance backlogs (Kehoe, 2014; Plimmer and Espinoza, 2017).

Despite the substantial contributions from literature on financialization, the conceptual limits of financialization impede a more incisive analysis of the infrastructure asset class. Financialization is variously interpreted as a new regime of accumulation, the growth of a shareholder value orientation in corporate behaviour, and the permeation of financial logics and practices in everyday life (van der Zwan, 2014). The multifaceted nature of the concept is not inherently problematic, yet its expansion into a ‘chaotic, motley idea’ (Christophers, 2015: 186) has undermined efforts to characterise the development of the infrastructure asset class, and in turn, the social, economic and political impacts on the societies that infrastructure assets are embedded within. Although financialization refers to the creation and extraction of value, it rarely defines what value actually is (Purcell et al., 2020). This omission, in conjunction with the vague definition of financialization, limit its explanatory power to show how and why infrastructures have been transformed into financial assets.

To address these shortcomings, scholarship on rent and assetization can augment existing research by engaging with value theory and the processes of constructing financial assets.

Rent is defined as ‘income derived from the ownership, possession or control of scarce assets under conditions of limited or no competition’ (Christophers, 2020: xxiv), or in Marxian terms, a social relation that enables surplus value to be captured and controlled (Baglioni et al., 2023; Purcell et al., 2020). Bryan et al. (2015: 318) qualify that finance capital increasingly seeks to capture surplus value from ‘production-beyond-the-workplace’, reflected in financial assets that target revenue streams from household utility consumption (Purcell et al., 2020) or beds in co-living developments (White, 2023). Since monopoly power is an essential quality to define infrastructure assets, shown in Table 1, rent is an apt starting point to scrutinise the value generated from infrastructure assets. Purcell et al. (2020) show how rent can be deployed to examine the source of the financial value extracted from public infrastructures, proposing a conceptual triadic relationship between value, rent and finance. Using the case of water utilities in England, this approach reveals two distinct moments of rent generation. First, the calculation of prices by the water regulator Ofwat, ‘conceals the formation of monopoly rent’ by ensuring investors’ financial returns, and second, the securitization of future revenue streams based on these monopoly prices. These insights show how financialized water utilities use monopoly power to charge prices higher than the cost of providing services, and create financial value by securitising revenue streams, transferring future rents to the present and extracting them through dividends.

Assetization is the creation of property that generates a revenue stream, also known as rent-bearing property or fictitious capital (Birch and Ward, 2022). The assetization process comprises the enclosure of resources or services, the generation and collection of rents, and the capitalization of these rents as property. To secure revenue streams, assetization creates fictitious capital by pulling future value (rents) into present circulation, in a way that exerts material force (Birch and Ward, 2023). Assetization and financialization are intertwined, but not interchangeable: the creation of an asset through the enclosure, capitalization and rent extraction, is a key marker of the capitalist accumulation yet it does not necessarily imply financialization in terms of the dominance of shareholder value orientations (Birch and Ward, 2022). However, since many Western economies are characterized by rentierism, with financialized monopolistic assets such as housing, land, infrastructure, farmland and digital platforms (Aalbers, 2017; Christophers, 2023; Ouma, 2020), assetization and financialization frequently co-exist.

Assetization offers a meso-scale conceptual framework to bridge macro-oriented theories of financialization with micro-oriented analyses of capitalization: bringing into dialogue the social-constructivist lens, which conceives of assetization in terms of performativity and the deployment of expertise or market devices, and the Marxian value-theoretical approach, which focuses on processes of enclosure, capitalization and the creation of fictitious capital that makes claims on future wealth (Birch and Ward, 2022). The boundaries between social constructivist and political economy approaches blur when it comes to explaining how fictitious capital and property are crystallized, and existing research by Weber (2021) and Fields (2018) show the value of bringing the performative construction of financial assets into dialogue with the broader political-economic context.

Birch and Ward (2022) treat the creation of fictitious capital as the outcome of rent extraction mechanisms circulating as capitalized real abstractions. By focusing on real abstraction to capture the material impacts and social struggles around the process by which diverse use values are transformed into exchange value, this approach recognizes the interplay between valuation processes that are pivotal in rent extraction, and the social and class relations underpinning rent that allow investors to capture and control surplus value. Following this line of inquiry, this analysis responds to Birch and Ward’s (2023: 3) call for closer attention to the ‘material processes (re-)shaping the geographies of value chains and societal struggles over surplus’.

Methodological approach

To examine how infrastructure debt funds generate financial returns, this article develops an embedded multiple case study analysis of four investments by a single infrastructure debt fund. The debt fund, Allianz UK Infrastructure Debt Fund I, was chosen because Allianz Global Investors is a pioneer in the infrastructure debt market, as the first global asset manager to recruit a dedicated infrastructure debt team (Blewett, 2012). The Allianz UK Infrastructure Debt Fund I was the first UK-targeted infrastructure debt fund (Oakley and Stacey, 2013), targeting diverse types of infrastructure: a port expansion, a rural bypass road, student accommodation and a tolled motorway.

The analysis examines the assetization processes by which resources are enclosed, rents are generated and collected, and capitalized as property. The assetization process is brought into dialogue with its political-economic context to explore how financial tools and techniques are deployed within those power relations. This approach is informed by Weber (2021) and Fields (2018), and aims to avoid over-attributing agency to the performative work of financial tools and calculative practices.

Using each investment as the unit of analysis allows comparison between the types of enclosure, rent extraction and capitalization for each asset, and in turn, how the debt fund derives returns from each investment. The analysis reveals multiple moments of enclosure, rent extraction and capitalization for each underlying asset, since the revenue streams generated by debt investments extend claims on the capitalized rents generated by monopoly infrastructures. This approach reveals how debt funds operate across diverse asset types.

Case study analysis: Allianz UK Infrastructure Debt Fund I

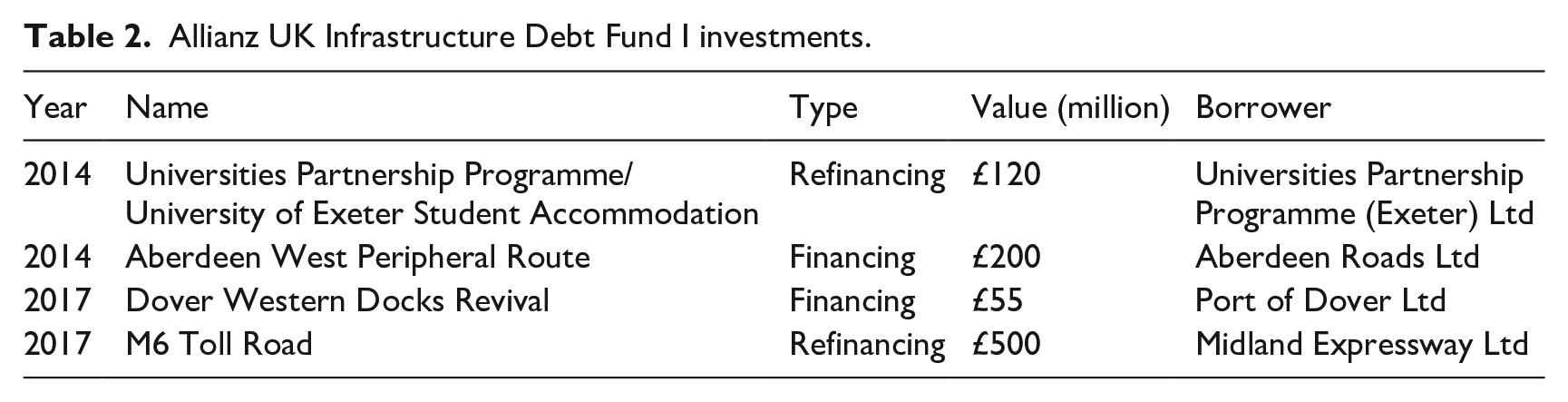

The Allianz UK Infrastructure Debt Fund I (IDF1) closed in 2015, raising £262 million from Japanese and British insurers and pension funds (Preqin, 2023b). Insurers typically invest in funds as limited partners, while asset managers act as general partners with control over, and responsibility for, investment decision-making and the management of assets. However in this case, Allianz SE’s asset management arm, Allianz Global Investors, developed their own in-house general partners, recruiting a team of infrastructure debt specialists (Blewett, 2012). Table 2 outlines key details of four of the fund’s investments. Their total value is £875 million, indicating that private placements 1 were likely used alongside capital from the debt fund.

Allianz UK Infrastructure Debt Fund I investments.

Since infrastructure debt makes claims on the revenue streams generated by infrastructures, it is predicated on the assetization of infrastructures to generate revenue streams from the physical asset’s operation, in the first instance. Thus, the analysis covers this initial assetization process to secure the infrastructure asset’s revenue streams, alongside the additional round of assetization to construct infrastructure debt assets. This approach reveals interdependencies between successive rounds of assetization, as heavy reliance on gearing for the initial round increases demand for debt, which debt funds can take advantage of amidst regulatory limits for commercial bank lending to infrastructure assets.

Refinancing of Universities Partnerships Programme/University of Exeter Student Accommodation

In December 2014, IDF1 purchased £149.7 million of index-linked 1.037% bonds from Universities Partnerships Programme (UPP) to refinance a concession for 2600 student accommodation places at the University of Exeter (UPP, 2022).

UPP began as the student accommodation division of construction and support services firm Jarvis, a firm specialising in managing privatized infrastructures and Private Finance Initiative (PFI) deals. UPP was sold to Barclay Capital in 2004 after Jarvis faced financial difficulties (Reece, 2004), and subsequently split into separate development and asset management businesses, and sold to Dutch pension fund PGGM and Chinese state-backed fund Gingko Tree Investment in 2013 (Robinson, 2010; Whitten, 2013). In 2018 UPP converted to a Real Estate Investment Trust, exempt from UK corporation tax (Hook, 2018). UPP has delivered 33,000 student accommodation places through partnerships with 14 universities in England and Wales (UPP, 2023). UPP’s investment model follows a similar logic to the PFI, allowing universities to shift debt finance for student accommodation off their balance sheets by procuring accommodation through long-term contracts for the financing, construction and maintenance of accommodation facilities. UPP typically enters into joint ventures with universities to guarantee high levels of demand through nomination agreements (Thomas, 2010), resulting in occupancy rates between 95% and 100% (UPP, 2022).

Student accommodation has emerged as a lucrative investment over the past decade (Knight, 2019; Revington and August, 2020). In the UK, fiscal austerity and threats to university funding created the impetus to divert university students to purpose-build student accommodation, procured through firms like UPP as an off-balance sheet alternative. Heslop et al. (2023) emphasise the key role of student accommodation in secondary cities like Exeter: with a proportionately large student population to accommodate, purpose-build student accommodation relieved pressure on local rental markets amidst a shortage of affordable housing. Removing the cap on recruitment for UK universities in 2015 further boosted demand for accommodation as universities increased international student enrolments (Infrastructure Investor, 2015). However, the affordability of student accommodation worsened as universities expanded their stocks of purpose-built accommodation, with rents increasing 61% between 2010 and 2021 and private providers charging 24% more than universities for bed spaces (NUS, 2021). During the COVID-19 pandemic, students at 55 universities threatened rent strikes against accommodation providers that charged full rent during lockdown periods. The strike action was successful in Exeter, yet the cost of waiving rents was met by the university, which was contractually responsible for rental income risk once students were contracted (UPP (Exeter) Ltd (2021).

The enclosure of services by UPP rests in their monopoly power: UPP Exeter reported an application-to-acceptance ratio of 5.3:1 in 2022, showing how demand for spaces significantly outstripped supply (UPP (Exeter) Ltd (2022). This is bolstered by support from universities and councils, aiming to ease pressure on their balance sheets and local housing supply, respectively (Heslop et al., 2023).

Rental price setting is key to generate rents from student accommodation. Student accommodation is not directly regulated in the United Kingdom, so providers like UPP are governed as private landlords with few constraints on increasing rents. Private providers have taken advantage of this, as student rents for purpose-built accommodation increased by 51% between 2010 and 2021 (NUS, 2021). Furthermore, the NUS (2021: 5) critiqued the use of benchmarking practices against competitors’ rates for private rentals, and long-term financing deals with rent escalators built in which restricted a university’s control over rental prices.

Finally, rents generated from Exeter’s student accommodation are capitalized into UPP’s equity shares. Since the joint venture between UPP and the University of Exeter gives UPP the right to extract monopoly rents for the provision of scarce student accommodation spaces, these future revenue streams can be directly discounted and capitalized into the value of equity shares. Although the sale price was not disclosed when UPP was acquired by PGGM and Gingko Tree Investment, financial reports estimated the firm’s enterprise value at £1.4 billion, based on the capitalization of the firm’s shares, debt, cash and liabilities (Alves, 2012).

Financing of the Aberdeen Western Peripheral Route

In December 2014, IDF1 lent £200 million through a 30-year, 4.22% fixed-rate bond investment with Aberdeen Roads Ltd for the Aberdeen West Peripheral Route (AWPR), a 26-mile bypass road in Scotland. Alongside the bond, ARL obtained loans from the European Investment Bank, Royal Bank of Canada and Barclays (Aberdeen Roads (Finance) plc, 2015).

ARL is a joint venture between construction and support services firms Balfour Beatty, Carillion and Galliford Try, formed to construct and operate the AWPR for 30 years under Scotland’s Non-Profit Distributing (NPD) model (Audit Scotland, 2020). The NPD is a variant of the UK’s Private Finance Initiative (PFI), and both the PFI and NPD use vertically-integrated, long-term contracts to procure financing, construction and maintenance for public assets, funded by unitary charges paid by the state. 2 Although the NPD model prevents the extraction of excessive profits by equity shareholders, it has been criticized for failing to deliver value-for-money as interest rates for private debt used to finance NPD schemes were up to 14.5%, substantially higher than the rates available for publicly-financed projects (Audit Scotland, 2020).

The AWPR’s construction phase was significantly delayed and £350 million over budget, attributed to severe weather, technical challenges and the collapse of consortium partner Carillion in early 2018 (Haslam, 2018). ARL was insulated from this risk, since the construction work was subcontracted on a fixed-price basis to AWPR Construction Joint Venture, with the right to impose liquidated damages to offset reduced unitary charge income resulting from the delay (ARL, 2021). The joint venture was between the same three firms that controlled ARL: Balfour Beatty, Galliford Try (trading as Morrison) and Carillion. After launching a legal case against Transport Scotland, claiming for exceptional costs, the construction firms eventually negotiated a £64 million settlement to resolve the dispute in early 2020 (Ross, 2019).

For the initial assetization of the AWPR, the NPD contract acted to enclose services, eliminating competition by giving exclusive ARL guaranteed, long-term revenue streams (unitary charges) from the state, once the asset was operating. As explained above, construction risks were delegated to the construction firms to limit ARL’s financial risk. Generating rents from the AWPR project relied on the setting of unitary charges within the NPD contract. Similar to utility prices, unitary charges generated rents by building in a ‘normal’ rate of return, alongside contingencies for loan interest, operating and maintenance costs for the asset (Audit Scotland, 2020; Bayliss et al., 2022). Once unitary charges are negotiated, they are secured in for the full term of the contract and backed by an effective state guarantee, unless the consortium failed to deliver the contracted services.

Rents generated by the AWPR were capitalized into equity shares in ARL. The NPD model prevents the creation of dividend-bearing shares, yet, shareholders benefit from capital gains on shares traded throughout the contract’s term. Although the sale prices for equity share acquisitions by Semperian and BBGI were not disclosed, Balfour Beatty revealed in 2021 that the sale price to BBGI was ‘in excess of the directors’ valuation, consistent with the company’s strategy of optimising value through the disposal of operational assets whilst continuing to invest in new opportunities’ (SCN, 2021). This statement reflects to the practice of selling equity shares at a substantial premium after the riskier construction phase of the project was complete, at which point the asset could enjoy a long-term monopoly with revenues guaranteed through unitary charges. This effectively pulls future monopoly rents into the present, generating immediate windfall gains for the equity seller, and securing predictable revenue streams for the buyer.

Financing for Dover Western Docks Revival project at the Port of Dover

In 2017, IDF1 purchased a £55 million, 30-year, 3.63% fixed-rate bond to finance the Dover Western Docks Renewal (DWDR) (Dover Harbour Board, 2017). This project expanded the Port of Dover’s capacity to increase ferry traffic at the Eastern Docks, by constructing a new marina, pier, and cargo berths. The bond was part of a financing package including £35 million revolving credit facilities from Royal Bank of Scotland and Lloyds Bank, and a £75 million loan from the European Investment Bank (Mavroleon and Caon, 2017).

As a trust port, the Port of Dover has no shareholders: it is run by the independent Dover Harbour Board 3 (DHB) and governed by its enabling legislation (DfT, 2016). DHB applied to privatise the port in 2010, claiming that the port could only borrow to invest in the DWDR as a private company. However, after local residents mobilized in an anti-privatization campaign, the application was rejected by the government on the basis that ‘the scheme would not ensure a sufficient level of enduring community participation. . . and other options [than privatization] were available to secure the proposed redevelopment’ (Butcher, 2013: 13). In 2014, the port’s borrowing powers were extended to ensure it could take on debt, secured against the port’s assets (MMO, 2014a). Concerns were raised about these borrowing powers enabling ‘back door’ privatization, since the loans were secured against the port’s assets and received no state guarantees. However, the Marine Management Organisation assured that trust ports could not sell assets without statutory authorization and the government’s consent (MMO, 2014b).

Sea ports are critical regional and economic assets for the UK as an island nation, enabling international trade and tourism by acting as the interface between different transport modes (Weber and Alfen, 2016: 112). The Port of Dover is positioned on the English Channel at a key gateway to continental Europe, 22 miles from the Port of Calais. The Port of Dover is a major trading and ferry port, handling 33% of UK-EU trade, 31% of heavy freight vehicles entering UK seaports, 160,000 cruise passengers and 1.3 million tourist vehicles annually (Dover Harbour Board, 2022a). As set out in Table 1, ports are defined as ‘core assets’: low-risk investments with high barriers to competition since they require suitable locations, determined by the coastal geography, and major investments to build docks, piers, breakwaters, refuelling stations, terminals and storage facilities.

The Port of Dover’s monopoly power over a key shipping and logistics route, due to its location and connection to England’s land transport networks, enables the enclosure of ferry and freight operators. Since the port’s revenues are mainly generated by harbour dues, charged to ships and for the processing of goods and passengers, the generation of rents relies on the prices set for these dues. Harbour dues are governed by The Harbours Act 1964. The strength of this legislation, and the Port of Dover’s power to extract rents, was tested in 2011 when P&O Ferries and DFDS Seaways filed complaints against the Port of Dover for increasing harbour dues, resulting in a public inquiry (Griffiths, 2010). The ferry operators challenged the decision to increase harbour dues in 2010, claiming that this took advantage of the port’s monopoly power to generate excessive profit for DHB. The Board’s defence rested on the ‘extremely broad discretion’ that the legislation conferred on the Board to exercise their power ‘to demand, take and recover such ship, passenger and goods dues as they think fit’, and the exemption of dues for ships, passengers and goods from the limitation of setting reasonable charges (Rodgers, 2012: 28). The inquiry found in favour in the Dover Harbour Board, confirming the Board’s ability to exercise monopoly power.

The capitalization of the rents generated by the Port of Dover is inhibited by the port’s legal status as a trust port. Although trusts ports operate largely on a commercial basis, they have no share capital and profits are either reinvested into the port’s development or used for the benefit of stakeholders (BPA, 2021). In turn, the inability to capitalise the Port of Dover’s rents into property mean that neither the Port, nor the DWDR, can be transformed into a financial asset. Yet, the moves made by the Dover Harbour Board in 2010 to increase dues to maximise the generation of rents, in anticipation of the port’s privatization, show how this is a critical precursor to transforming the port into a financial asset.

Refinancing for the M6 Toll Road

In 2017, IDF1 made a £500 m bond investment in the M6 Toll, a 27-mile expressway north of Birmingham, to refinance the operating company’s existing debt 4 for the remaining 32 years of the concession. The M6 Toll is operated by Midland Expressway Ltd (MEL), the firm that was awarded a concession to build and operate the toll road in 1991. This case shows how multiple rounds of assetization were enacted on the underlying toll road monopoly, using both equity and debt instruments to make claims on the rents generated by the toll road.

The M6 Toll provides a bypass route for congested sections of the public M6 motorway north of Birmingham. Since the M6 is the main north-south motorway route connecting the south of England, Wales, and the Midlands with Manchester and Scotland, there is high demand for domestic and freight travel. High traffic volumes and heavy congestion on the existing M6 were essential prerequisites for the M6 Toll to impose monopoly power, since it relied solely on toll revenue without guarantees or availability payments from the state. The M6 Toll has faced persistent criticism for high toll prices, and heavy goods vehicles initially boycotted the route (Dare, 2018; The Sentinel, 2004). The absence of price regulation on tolls enabled MEL to generate rents from their monopoly power over road transport through the Midlands. From the outset, MEL’s owners emphasized that the unlimited ability to raise tolls was a key feature of the M6 Toll for investors. A director of MIG stated openly that although the state anticipated competition between the M6 Toll Road and the existing public highway would prevent the toll charges from becoming excessively high (Marston, 2003), ‘the reality is that as the free road gets more and more congested, the toll road behaves more and more like a monopoly. . . if motorists don’t complain about [the toll] being too high, then we won’t have done our job’ (Marston, 2003). MEL took advantage of their monopoly power, with tolls increasing by 38% (HGVs) and 280% (cars) between 2003 and 2022 (M6Toll, 2023; Salter, 2003).

In the first instance, the revenue streams generated through rent extraction were capitalized into the equity shares for MEL, which were initially held by Macquarie Infrastructure Group when the road began operating. MEL’s ownership changed hands several times, however, when the contract was tendered it was held by Australian investment bank Macquarie Infrastructure Group (MIG) (75%) and Italian operator Autostrade (25%) (Morley, 1999). MIG subsequently deployed a private-equity style model which relied heavily on debt to acquire the asset and to extract investment returns through financial engineering (Bayliss et al., 2022). In 2005 MIG bought out Autostrade’s stake and refinanced MEL, increasing debt to almost £1 billion and subsequently extracting a £392 million dividend (Smith, 2006). The refinancing deal included a bullet loan with an ‘accreting swap’ mechanism that reduced interest payments in the loan’s earlier years, allowing MIG to extract dividends (Project Finance, 2007). The debt’s structure was predicated on revenue growth forecasts that assumed toll revenues would outpace the loan’s increasing interest rates across the 9-year term. Analysts estimated that the M6 Toll would only need to divert 10%–15% of the existing M6 traffic flow to reach MEL’s revenue targets (Project Finance, 2001). However, these projections under-estimated the impacts of public opposition and the 2007/2008 Global Financial Crisis: quarterly traffic volumes fell by 31% between 2006 and 2009 (Project Finance, 2011). Although the financial impacts were severe for MIG, the parent company Macquarie was insulated from most financial risks.

In 2010 MIG was restructured into two funds, bundling the M6 Toll with other under-performing toll roads into Macquarie Atlas Roads (MAR) (Alves, 2010). By 2011, the M6 Toll’s creditors began selling debt at a substantial discount to infrastructure and distressed debt funds (Lea, 2011; Sakoui and Hammond, 2011), and from 2013 MAR began exiting the investment, deconsolidating the M6 Toll from its accounts and eventually divesting its interest in 2017 (MQA, 2017). While selling at a loss impacted MAR’s returns, Macquarie was largely shielded as it typically only held a small equity share in funds, relying on income streams from commissions and transaction fees (Christophers, 2023: 72). Following MAR’s exit, the remaining consortium of banks and funds sought to sell the asset to recover the accumulated £1.9 billion debt (Powley and Plimmer, 2016). IFM Global Infrastructure Fund acquired the M6 Toll June 2017 (Jones, 2017), shortly before the AllianzGI fund’s bond issuance. The AllianzGI fund enacted a second round of assetization, taking advantage of MEL’s need to refinance by providing debt financing that makes claims on future rents generated by the toll road.

The construction of infrastructure debt assets

This section draws on the findings from IDF1’s four investments to examine how the debt fund constructed debt assets from the underlying infrastructure assets.

Regulatory constraints on commercial banks arising from Basel III/CRD IV regulations set the context for private debt funds to enclose debt provision for infrastructure assets, acting as financial rentiers in this market segment. Since specialized expertise is required to appraise infrastructure assets, and to issue and manage loans, asset managers like AllianzGI that have invested in this capability can exert monopoly power over private debt for infrastructure. Beyond IDF1, asset managers are increasingly deploying capital from infrastructure debt funds to their own infrastructure equity funds, which also exploits their ability to limit competition (Christophers, 2023).

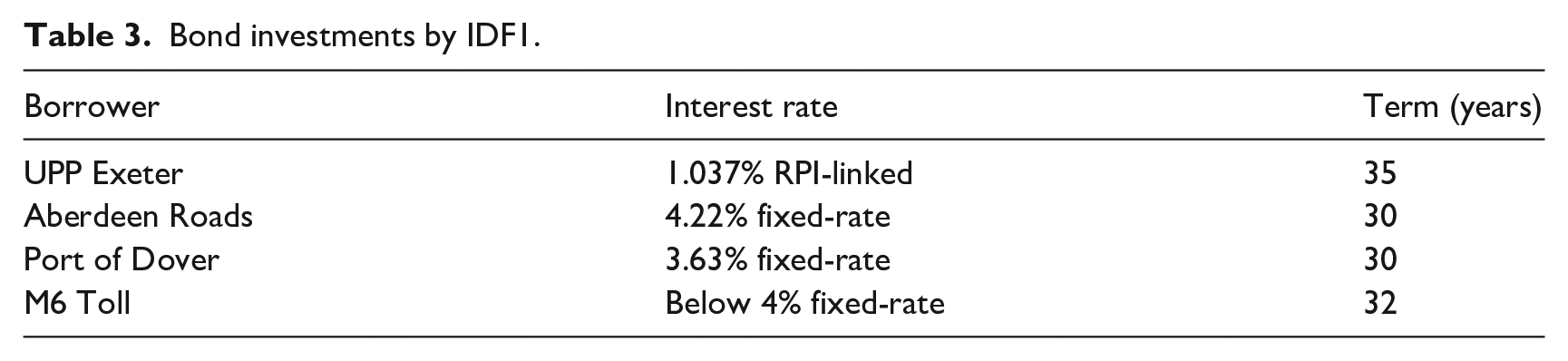

Infrastructure debt investments generate rents by charging higher interest rates than those of commercial banks, to produce long-term revenue streams. By extending debt finance, these funds make claims on a portion of the monopoly rents generated through the initial assetization of infrastructure systems or facilities. Table 3 summarises the interest rates charged on the bonds purchased by IDF1. The fixed rate bonds were all issued several percentage points above the UK’s long-term interest rates, which varied between 0.7% and 2.5% between 2014 and 2017 (OECD, 2023).

Bond investments by IDF1.

While higher interest rates are usually assumed to reflect higher levels of risk, the case study shows how the debt fund targeted low-risk monopolies: the Port of Dover’s monopoly over ferry and freight traffic, UPP’s monopoly over student accommodation, the AWPR’s monopoly as created by the NPD contract and the M6 Toll’s monopoly over a road transport alternative to the congested M6 through Birmingham. Projects were also be structured to shield lenders from specific risks, such as ARL’s transfer of construction risk to a separate joint venture, or UPP Exeter’s use of nomination agreements from the University of Exeter to maximise occupancy.

Lastly, the construction of debt assets relied on the capitalization of revenue streams from interest payments. The partnership structure of debt funds provided a vehicle to pool the anticipated revenues from interest payments and capitalize these into shares in the debt fund. These funds give the general partner – in this case, Allianz Global Investors – direct control over decision-making and management for the debt investments, while pooling capital from other investors for the fund to deploy. The debt fund’s rate of return for limited partners is determined by the monopoly rents extracted through financial rentiership, which are then discounted and subject to commissions and fees due to the asset manager.

Discussion

This section brings the findings into dialogue with the political economy of infrastructure investment in the UK.

The findings show how infrastructure debt funds create fictitious capital by pulling future value into present circulation, using debt contracts or bonds as a rent-extraction mechanism to extend claims a share of the revenues generated from monopoly infrastructure assets. The creation of infrastructure debt assets is contingent on a supply of monopoly infrastructure assets to lend to, and debt funds’ position in credit markets following regulatory restrictions on commercial bank lending. 5 Debt funds’ advantage in credit markets is reinforced by high demand for debt from infrastructure equity funds, which use debt to securitise revenue streams and extract dividends from their assets. 6

The creation of fictitious capital by IDF1 exerts material force over the operation of infrastructure assets over the 30–35 year term of the debt assets: the M6 Toll, the Port of Dover, the UPP/Exeter student accommodation and the AWPR must continue generating revenues to service this debts, limited scope to adapt or redevelop them repurposed for different uses. For inflation-linked debt, such as that used for the UPP/University of Exeter project, revenues must service substantially higher debt-servicing costs during periods of high inflation, further worsening affordability for students. The central role of rent extraction from monopoly assets identified across the four investments supports Christophers (2020) claim that financialization is a vector of a broader structural shift, involved in the rentierization of the UK economy.

Assetization processes are not ultimately propelled by the performative work of constructing debt assets. Bringing the construction of infrastructure debt into dialogue with the political economy of infrastructure investment shows that persistent fiscal austerity, and political and institutional support for increased private investment, are key drivers for assetization. Budget constraints or unwillingness to increase public debt underpinned decisions to pursue private finance for all four cases in this analysis: universities sought to shift accommodation off their balance sheets, the state raised private finance through an ad hoc deal for the M6 Toll and the NPD model for the AWPR. The impetus to find an alternative to public finance for the Port of Dover led to the deal with IDF1. Political support for private investment has enabled the market to develop substantially in the UK. The state has privatized a wide range of public assets since the 1980s and pioneered policies and institutions that enabled the development of the infrastructure asset class, such as the Private Finance Initiative, Pensions Infrastructure Platform, Green Investment Bank, and the UK Infrastructure Bank (Christophers, 2023).

Efforts by debt funds and their creditors to stake long-term claims on monopoly rents were contested. The freight operators’ boycott of the M6 Toll and the students’ rent strikes challenged the enclosure and extraction of rents. Yet, these social struggles failed to counter enclosure and rent extraction due to the complex corporate and legal structuring of the deals: although the M6 Toll failed to meet revenue targets, 7 MIG were still able to extracting dividends before restructuring its ownership and exiting the investment. Where struggles did gain traction, such as the student rent strikes, compensation was provided by the university, since UPP and the creditors had contractual protection from this specific risk. Furthermore, debt providers escaped direct opposition in these social struggles, since their identity is not always publicly disclosed, and when it is, their financial liability can be limited by contractual protections.

Conclusion

Debt funds offer investors new routes to extract returns from the rents generated by infrastructure assets, using debt to create fictitious capital which pulls future value, or rents, into present circulation. Since private debt funds can extract rents without holding an equity stake in the underlying infrastructure, debt funds may give investors access to rents from a much wider range of assets than those available to equity funds. Although the relatively low level of fundraising for infrastructure debt shows that equity funds still dominate the market, the qualitative difference in the nature of the investment is significant, as well as the interdependence with equity funds that rely on significant gearing.

The creation of infrastructure debt assets has significant material impacts that extend across the temporal scale of the debt, and the spatial scale of the infrastructure asset. The debt fund imposes spatialized, long-term rigidities on value chains as the UK faces a major transformation to reach net-zero by 2050: the M6 Toll is locked in to maximising traffic revenue despite net zero policy targets to reduce road traffic by reallocating trips to rail or coach travel, and although the UPP student accommodation project does set ambitious net-zero targets, it locks in urban land for premium, unaffordable student accommodation for decades to come.

The ways that infrastructure debt funds generate revenue streams show rent extraction is a fundamental feature of the infrastructure asset class, since investors targets assets with monopolistic qualities and price regulation that enables the generation of monopoly rents. While analyses of equity funds showed that investors can extract returns through dividends, regardless of the actual operational and financial performance of the asset, this article shows how debt funds also extract rents regardless of performance, as long as revenue streams are sufficient to service the loans provided by debt funds. These dynamics raises concern about the genuine potential of the infrastructure asset class to contribute to inclusive regional development and just transitions towards net zero.

While three of the four cases analysed showed contestation over investors’ efforts to extract rents, the scope for social struggle and resistance was undermined by the limited public disclosure of debt deals, which in many instances give the lenders anonymity and protection from public opposition. Investors also rely on contractual protections that limit the financial impacts of opposition, such as rent strikes or boycotts, by delegating such risks to public actors or isolating them through complex networks of holding companies and intermediaries.

Further research on assetization is needed to elaborate on the diverse processes by which rents are generated and extracted. In particular, examining the mechanisms, legal and accounting tools deployed to create debt assets from energy and digital infrastructure sectors has strong potential as these types of infrastructures have distinctive network structures and opportunities for competition, monopoly and regulation. Additionally, further examination of equity funds’ reliance on debt to generate returns is needed, amidst the unfolding impacts of higher interest rates across the infrastructure asset class.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: No additional funding was provided for this research, it was conducted as part of the author’s employment at University College London.