Abstract

Over the last decade, Greater Manchester's city-regional centre has become an important site for build to rent (BTR) housing development in the UK. The growth of this new tenure raises important empirical and conceptual questions about how far and through what means BTR has extended in post-industrial cities like Manchester, as well as how to theorise the global–local relations involved in BTR development. Drawing on a self-built database of 155 development projects incorporating 45,069 new housing units, we show that new-build BTR units have outpaced ‘build to sell’ (BTS) units almost two to one in Manchester's city-regional centre since 2012. We also found stronger international investment in BTR relative to BTS, illustrating BTR's more globalised and financialised form. Our paper understands BTR growth in Manchester as the outcome of a transcalar territorial network – an assemblage of national policy objectives, local state actors’ urban regeneration activity and heterogenous global investor groups with different priorities all seeking a return. We highlight the important role of national and local state subsidies and local authority joint ventures in constructing a territory conducive for BTR investment in Manchester. We also show how the fungibility of BTR assets as a ‘networked product’ widens the investment appeal of the tenure type, broadening and deepening housing financialization.

Introduction

The financialization of housing has been identified as core to many contemporary urban development models (Aalbers, 2017; Fernandez and Aalbers, 2016; Revington and August, 2020; Wijburg and Aalbers, 2017). Initially associated with so-called ‘global cities’, there is emerging research on the flow of global capital into urban spaces previously on the margins of real estate investment, from the Ruhr metropolitan region (Wijburg et al., 2018), to the southern Mediterranean (Janoschka et al., 2020) and the ‘new real estate frontier’ of sub-Saharan Africa (Gillespie, 2020). These studies have highlighted the, at times, partial, complex and multi-dimensional way that financialised logics shape the urban landscape and the combination of global and local forces required to facilitate the flow of global investment into real estate assets.

The entanglement of global and local dimensions has encouraged authors within urban geography to reject the idea that financialization operates as an external global logic that imposes itself on particular localities and have instead understood financialization as a variegated process, embedded within path-dependent institutions and power relations that operate across and transform outcomes at different scales and sites (Brenner et al., 2010; Peck and Theodore, 2007; Ward et al., 2019). These studies pay close attention to the social and political contexts that enable capital to become anchored in urban space (Aalbers, 2017; McKenzie and Atkinson, 2020). Others, drawing on theoretical approaches grounded in networked approaches, understand the production and reproduction of the built environment as the outcome of transcalar territorial networks (TTNs) (Guironnet and Halbert, 2014; Halbert and Attuyer, 2016; Halbert and Rouanet, 2014) – the mobilisation and enrolment of investors, real estate developers, local/national state actors, resources, expertise and narratives around housing as a financial asset (Brill, 2018; Brill and Özogul, 2021; Robinson and Attuyer, 2021).

This networked approach has been applied to understanding the emergence of build-to-rent (BTR) assets and markets. BTR refers to large-scale, higher density housing, purpose-built for the rental market and typically owned on a long-term basis by institutional or other large investors (Nethercote, 2020). This work has greatly advanced our understanding of how global and local forces interact to bring about changes in the urban geography. However, those studies have primarily focused on ‘world’ cities such as London or Amsterdam to date, so there is only limited evidence of how local agency plays out in ‘secondary’ cities that are relatively disconnected from the centre of wealth and political power. Similarly, it is unclear whether the same type or types of investor operate in these more post-industrial spaces; and whether the changing characteristics and outlook of capital providers observed in the emerging scholarship on BTR (Wijburg et al., 2018), are also observable in British post-industrial cities, where there is a tradition of openness to global capital and BTR is growing rapidly. Finally, although the network metaphor has helped to illuminate the global and local forces needed to create assets like BTR, the organising potential of BTR assets themselves – their capacity to ‘draw-in’ new constellations of actors in secondary cities who would otherwise remain disconnected – is underexplored. These three axes – local agency, new financial actors and networked products – form the basis of our three research questions: what is the role of national and local state agency in the TTN around BTR housing development in ‘secondary’ post-industrial cities? To what extent do we observe new networks of financial actors and strategies mobilised around BTR within these secondary cities? And to what degree do the characteristics of BTR as a product influence the shape of these networks within the production of the urban built environment?

We answer these questions through an empirical study that examines the development of a market in BTR housing in the metropolitan city-region of Greater Manchester, England. Greater Manchester is selected because it is an archetypal post-industrial region whose combined authority pursues a ‘city-first’, property-led urban regeneration model (Tomaney and McCarthy, 2015; Upton, 2012) where BTR is the latest manifestation. In policy circles, the ‘Manchester model’ of urban governance and development is often considered the template for other regional city administrations (Haughton et al., 2016; Lee, 2017). And in recent times, this property-led approach has led Greater Manchester's city-regional centre to become the preeminent metropolitan hub for BTR investment in the UK, outside of London. Locating the financialised development of BTR in time and space, in this case, allows us to historicise and theorise the intertwined evolution of global and local processes involved in financialised urban regeneration, and explore its contingent and variegated expression.

Our paper makes two main contributions to the literature. First, we extend work on the critical role of the local state in constructing a territory for real estate finance through financialised urban development models (Beswick and Penny, 2018; Christophers, 2017; Robinson and Attuyer, 2021; Shatkin, 2017). We explore how TTNs are shaped by local government strategies established within the context of national state efforts to foster BTR as an asset class, and how the character of global real estate finance is shaped by the urban policy and planning it encounters in a secondary, post-industrial city. Second, we advance TTN theory by emphasising the organising role of BTR assets within the network, attracting and connecting actors who mobilise around housing as a financial asset (Beaverstock et al., 2021). We conclude that BTR enables the broadening and deepening of financialization by attracting a broader ecology of financial actors to enter residential real estate asset markets. We consider the future implications of this process as the specific economic and social contexts that give rise to BTR are likely to change within a post-pandemic, high-inflation environment.

Our paper is structured as follows: our next section reviews the literature on the financialization of housing, examining how authors have theorised the relation between global and local processes, before outlining the transcalar approach we adopt. We then discuss our research context, data and methods to explain case selection and our self-built database on property development in the Greater Manchester city region. Our first empirical section then sets the post-crisis growth of BTR in Greater Manchester in historical and national context, exploring local and national state agency that gives form to this particular manifestation of real estate financialization. Our second empirical section examines the investors, capital providers and developers involved in financing and producing BTR assets. A final section concludes.

The theorisation of global–local relations in housing financialization scholarship

Since the 1990s, scholars have observed the growing financialization of the global economy as a defining feature of contemporary capitalism (Aalbers, 2017; Froud et al., 2006; Krippner, 2005; van der Zwan, 2014). Under financialization, it is argued that the use values of land and housing become secondary to their status as financial assets which confer entitlements to rent akin to other paper claims on income, such as stocks and shares (Harvey, 2007). More recent work has emphasised the locally contingent expression of housing financialization, leading to calls that this process should be understood as the outcome of particular global–local relations located in specific institutional, economic and geographical contexts (Aalbers, 2017). From this a wealth of studies have emphasised the importance of understanding the embedding of financialised practice in local processes, specifically the role of local government as a site of financialised policy formation, and their role in harnessing global capital to achieve their policy objectives (Ashton et al., 2016; Fields and Uffer, 2016; Peck and Whiteside, 2016; Weber, 2010). Housing financialization, it is argued, is promoted by local governments through the privatisation of land (Christophers, 2017), the dismantling of rent regulation (Fields, 2013) and the pursuit of property-led urban regeneration schemes which, through generous land deals and planning concessions, encourage the rapid growth of house- and flat-building (Folkman et al., 2016; Rutland, 2010).

At the same time, other studies have added nuance to our understanding of the global dimension of these global–local relations, by focusing on the heterogenous characteristics of international finance. Housing assets, like any other form of collateral for financial markets, have the capacity to support a variety of financial actors with different risk appetites and return outlooks (Özogul and Taşan-Kok, 2020). Different blocs of financial actors may come to dominate real estate asset financing at certain discrete moments; and their preferences may shape the processes and outcomes of financialization at an urban scale, particularly when development projects are shaped by negotiations over viability and other localised agreements (Brill, 2021; Raco et al., 2019). A cluster of recent studies focusing primarily on the boom in rental residential investment have highlighted the different financial strategies available to rental housing investors, including rent increases in ‘prime’ locations, and opportunistic disinvestment and gentrification-led upgrading in more marginal areas (August, 2020; Bernt et al., 2017; Fields and Uffer, 2016). These opportunities have drawn in new financial actors such as real estate investment trusts (REITs), attracted to the security of longer-term rents in contrast to those who pursued shorter-term, speculative strategies in the pre-2008 period (Byrne, 2020; Nethercote, 2020). Some have argued that this therefore represents a new phase of housing financialization, which has moved from a speculative ‘financialization 1.0’ dominated by private equity and hedge funds towards a long-termist ‘financialization (2.0)’ (Wijburg et al., 2018).

Housing financialization as a variegated process

These dimensions of local agency and financial actor heterogeneity highlight the importance of understanding how financialization operates across scales, and the scope for local agency in shaping how capital becomes ‘anchored’ in urban space (McKenzie and Atkinson, 2020). This raises the potential for ‘contingent, fragmented, incomplete and uneven’ forms of housing financialization in cities (Aalbers, 2017: 544), and so has implications for how we theorise financialised processes as an interconnected global and urban phenomenon. Key influences within this debate have been Brenner (1998) and Swyngedouw (2004), who criticised the idea that capitalism unfolds within a nested hierarchy of scales descending from the global to the local. Instead, capitalist processes are theorised as variegated, that is, embedded within path-dependent institutions and power relations that mediate and produce different outcomes across different scales (Brenner et al., 2010; Peck and Theodore, 2007). Cities are thus conceived not as spatial containers within which global logics unfold, but in relational terms as strategic sites for the reproduction of capitalist power relations that are the ‘medium and product of dense interscalar networks linking dispersed locations across the world economy’ (Brenner, 2019: 97). Variegation is an important concept, not only because institutional differences shape the effects of financialization, but because financial processes emanate from and refract through different, locally-situated social, economic and institutional structures, which play a constitutive role in financialised outcomes (Engelen et al., 2010; Ward et al., 2019). An analysis of urban financialization as a variegated phenomenon therefore emphasises its ‘embeddedness within broader landscapes of political economic activity, territorial organization, regulatory intervention, metabolic transformation and social struggle’ (Brenner, 2019: 235).

Collectively, studies that explore this kind of variegation pay close attention to how the anchoring of capital into specific local contexts drives financialization through common – if not necessarily convergent – trajectories (Ward et al., 2019). However, a parallel body of literature has argued for the need to move beyond concepts of variegation or financial hegemony, wary that these remain dependent on overarching frameworks in which explanatory factors are reduced to the structural determinants of capital accumulation (Robinson and Attuyer, 2021). Instead, authors drawing on the social studies of finance have called for more constructivist explorations of market creation, focusing on the agency of real estate actors in provisionally enrolling housing into financial assets through the coming together of money, resources, narratives, expertise and calculative devices (Fields, 2018; Weber, 2015, 2016). In comparative research, this focus on agency implies that rather than conceiving financialised outcomes as ‘variegations of a wider process’, specific urban configurations should be seen as the product of an assemblage of ‘specific (transcalar) territorializations, emergent across a diversity of actors and processes with different reaches’ (Robinson and Attuyer, 2021: 309). To understand how these processes unfold in our case study, and the agency of actors and processes in shaping Manchester's housing landscapes, we therefore draw on the idea of housing financialization as a TTN.

Build to rent within a transcalar territorial network

The concept of a TTN developed by Halbert and Rouanet (2014) and others (Guironnet and Halbert, 2014; Halbert and Attuyer, 2016) not only rejects the assumption that financialization is constituted first at a global level and only then unfolds within particular urban contexts, but also questions the conceptualisation of geographic scales as ontologically separate entities. Instead, flows of money, capital, people and resources are theorised as co-constitutive with the coming together of social relations that comprise a specific place. Whereas cities are theorised in this analysis as constructed from the provisional ‘fixing’ of such flows through space, flows themselves only become meaningful and significant when they are re-territorialised through specific cities (Halbert and Rutherford, 2010). A TTN in this framework therefore acts not as a dialectic of capitalist development, but rather an assemblage of actors and processes, operating across local, national and international scales, that are drawn into a constellation with one another through their ability to draw in resources and reshape urban forms (cf. Allen and Cochrane, 2007). TTNs thus play an active role in producing financialization through the creation of enabling conditions such as the internalisation of the risks of financial investment or rendering commensurable the profit expectations and strategies of international investors and local and regional developers, anchoring liquid capital into spatially fixed real estate.

TTN frameworks have been used to explore how the conversion of BTR housing into an investment asset is mediated by actors such as developers, producing outcomes that are not purely definable by cyclical market demand (see also Weber, 2016). This includes the role of housing crisis narratives about ‘undersupply’ in advancing policy support for the BTR tenure (Brill and Durrant, 2021), the ‘relational’ channelling of investment by developers (Ballard and Butcher, 2020; Taşan-Kok et al., 2021), and the role of developers, political networks and community consultations in mitigating development risk across multiple international sites (Brill and Özogul, 2021; Brill and Robin, 2020). A TTN approach is therefore attractive because it foregrounds the agency of real estate and local state actors within the process of financialization, as well as how corporate landlords reconfigure networks around housing at the point of market creation (Brill and Özogul, 2021). Whilst these studies have enriched our understanding of the creation of markets in BTR assets, their geographical focus has to date focused on ‘world’ cities such as London or Amsterdam, rather than ‘secondary’ cities that are relatively disconnected from the centre of wealth and political power.

It is possible to extend this approach to better understand these agential properties by understanding how the very different networks of secondary cities engage with and reconfigure themselves around the development of BTR assets. Here, extending the logic of TTN research, we argue that whilst networks of actors, firms and narratives construct assets as they bring their situated resource and expertise upon them, products/assets also shape networks – they possess particular technical, economic and legal characteristics, which shape their investment appeal and thereby attract some actors and not others (Beaverstock et al., 2021; Faulconbridge et al., 2007; Haberly et al., 2019). Products/assets therefore have some agency within a TTN. BTR is consequently a ‘networked product’ embedded within ‘a dialectical relation whereby a network of actors shape the product… but the product also shapes the network as its characteristics create “needs” that influence which roles and jurisdictions are enrolled in its structuration’ (Beaverstock et al., 2021: 2). The needs of such products can produce network stability, in that product features establish path dependencies through quotidian exchange relationships that ‘produce mundane, repeat interactions which build shared understanding, tolerances, and concessions which lower costs for incumbents’ (Beaverstock et al., 2021: 21).

The TTN approach therefore allows us to explore the relative balance of rental and for-sale properties in post-industrial ‘secondary’ cities that lack the scale and liquidity of property markets in global cities such as London. We will now first analyse the development of the BTR sector in the city-regional centre of Greater Manchester, before exploring how BTR influences the shape of these networks, and its role in the broadening and deepening of financialised processes.

Research context, data and methods

Our case study focuses on the BTR sector in Greater Manchester, selected for two reasons. First, Manchester is an archetypal post-industrial city which has aggressively pursued property-led urban renewal strategies. Consequently, it is a good case study for analysing the extent to which a regional city outside of London has successfully mobilised transcalar networks that have emerged between local actors and global capital over time in this post-industrial space. Second, Manchester has the largest BTR sector in the UK outside London. It thus provides a test-case for understanding how the historical interaction between actors and BTR assets gave rise to this very specific form of housing financialization.

Our findings draw on data generated over eight years of residential development in Greater Manchester's city-regional centre from 2012 to 2020. We assembled this data from a variety of sources: planning permissions, regional property market publications such as Place North West, local publications such as the Manchester Evening News, and the specialist trade magazine Inside Housing. The final dataset was generated in early 2021. The area covered includes Manchester city centre, the Salford districts of Greengate and Blackfriars adjacent to the centre, in addition to the Salford Quays area and the adjacent Pomona (Figure 1). It incorporates three local authorities: Manchester, Salford and Trafford. The period of 2012–2020 was chosen because of the scale and intensity of approvals for, and subsequent building of, high-density apartment blocks in those years. Our sample includes 155 development projects of over 15 units in size and covers 45,069 new housing units, split between Manchester (24,728 units, 54.9% of the sample over 91 projects), Salford (18,718 units, 41.5% of the sample over 59 projects) and Trafford (1623 housing units, 3.6% of the sample over five projects). We supplemented this data with that harvested from local and national government documents, press and industry reports and financial information. That yielded additional information on planning conditions, section 106/affordable housing agreements, as well as the issuance of public loans and grants.

Map of the city-regional centre of Greater Manchester. Source: The authors; Map data ©2022 Google.

From this data we built our own bespoke database. We identified key actors involved in each individual development: financiers, developers and property managers. We also separated out developments by tenure into five categories. (i) Build to sell (BTS): developments built for direct sale to individual buyers, either to owner occupiers or to small-scale landlords via buy to let mortgages. (ii) Build to rent (BTR): developments identified as having been specifically built, designed and marketed exclusively for the private rented sector. This includes apartments and townhouses that may be owned by institutional investors up to the level of an entire housing block or even neighbourhood, or held through split ownership between institutional and individual landlords, in addition to co-living developments. (iii) Mixed: housing built for a combination of purpose-built rent and sale to owner–occupiers within a single development. (iv) Affordable: subsidised tenures comprising social housing, affordable rent, shared ownership and rent to buy. (v) Unknown: developments where the tenure could not be identified. To avoid double-counting, we do not analyse housing as BTR when it forms part of an otherwise mixed tenure of development for combinations of owner–occupier sales and rent.

Data was analysed at the Greater Manchester scale and at the local authority level providing a point of comparison at different scales. The data provides insights on the proportion of development accounted for by BTR, as well as the chains of ownership and investment in Manchester's real estate assets. It also reveals the treatment of land and housing by local government, including forms of direct and indirect subsidy such as land disposals or affordable housing planning requirements. This database allows us to put together a rich picture of the involvement of international investors in each individual build, as well as the local actors and interventions employed in the construction of these assets. It also allows us to assess whether each build involved large international investors or were sold overseas to smaller, buy to rent investor-landlords.

We acknowledge some limitations in our methodology. We have no primary information on financial actor motivations and strategies yet, for example. Our focus on a single city-region also precludes an in-depth comparative study of how these processes mirror experience in other cities. Whilst we capture the extent of development, our dataset does not provide qualitative evidence on the motives of investors in targeting Manchester. It is also possible our methodology has not identified developments such as office to residential switches not captured within the planning system, although this has been mitigated by extensive cross-referencing with regional property publications such as Place North West We have nevertheless produced a novel, empirically rich database in the hitherto under-researched area of BTR development as a driver of post-industrial urban renewal involving local state as well as global financial actors. This should provide foundations for future work on the strategic role of the local state in enabling financialization, including future interview-based qualitative research on the marketing of the city's real estate assets.

Capturing BTR investment for Greater Manchester: The role of state policy

BTR is a relatively new feature of the UK's housing system, where private renting has traditionally been dominated by relatively small-scale landlords. Yet since 2008, high-density residential development owned by institutional investors has grown significantly, accounting for 26% of residential properties over five storeys in size by 2021 (Tomusk, 2021: 9). This activity has been geographically concentrated in major cities, with 53% of new investment concentrated in London, and a further 34% in the ‘core’ regional cities of Manchester, Birmingham and Leeds (Rosser, 2021: 3). Of these cities, Manchester has the highest rate of BTR activity outside of the capital, accounting for 17% of completed BTR stock units compared to London's 50% in 2019 (Savills, 2020).

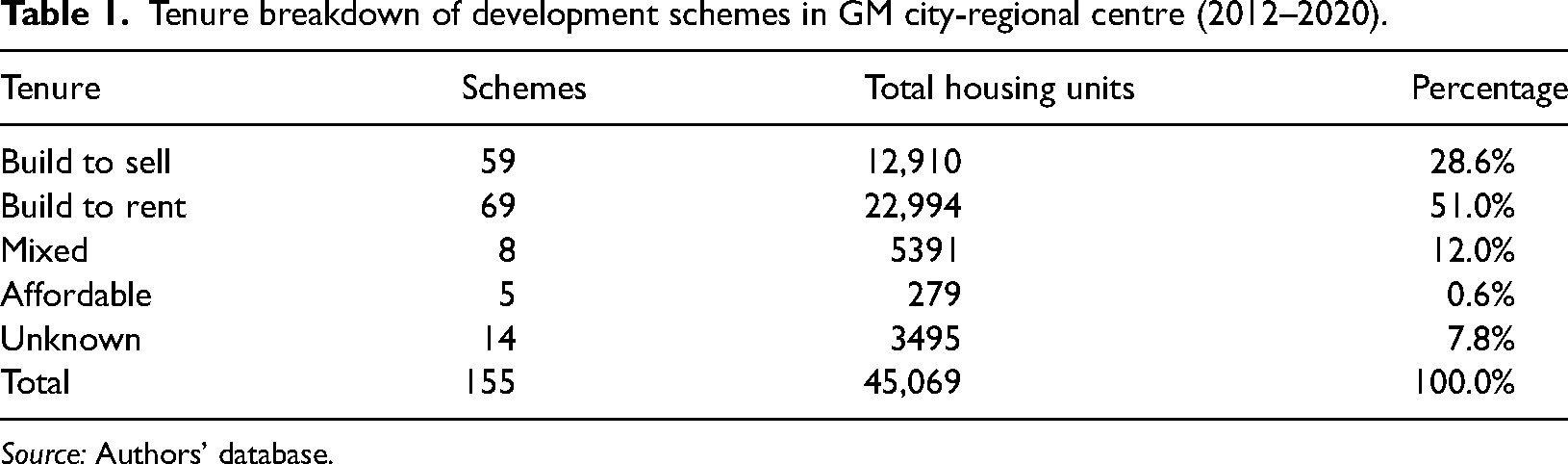

Our database shows that BTR has dominated development in the Greater Manchester regional centre: of the 45,069 housing units receiving planning permission from 2012 to 2020, 22,994 (51.0%) have been BTR (Table 1), compared to 12,910 BTS (28.6%), 5391 ‘mixed’ (12.0%) and 279 units across five schemes explicitly earmarked as affordable (0.6% – see the following section for a discussion of affordability). To understand how Manchester as a regional market was able to foster BTR development, we will first explore the confluence of national and local state policies that have attracted financial flows into residential real estate over this period.

Tenure breakdown of development schemes in GM city-regional centre (2012–2020).

Source: Authors’ database.

Creating a space for real estate finance: National state policies after the financial crisis

Corporate landlords became more prominent across Europe and North America in the 1990s as investors targeted favourable regulatory regimes, privatisation programmes and the erosion of rent control to acquire stock at scale in counties such as the US, Canada and Germany (August, 2020; Beswick et al., 2016; Fields and Uffer, 2016). This prominence spread after financial disruption in the 1990s, as the combination of falling property prices and households’ more limited access to mortgage finance generated opportunities for companies to acquire residential properties and exploit captive demand for private rent in cities such as Amsterdam, Berlin, Dublin and Madrid (Beswick et al., 2016; Brill and Özogul, 2021; Nethercote, 2020). BTR in the UK – understood as housing owned at scale and under single professional management (Wilson et al., 2017) – was initially relatively constrained, with residential property accounting for less than 1% of institutional investment into real estate in 2011, compared to 47% in the Netherlands (Bate, 2017: 17). The property industry was nonetheless successful in mobilising a narrative that institutional investment offered a supply-side solution to an urban housing affordability crisis among relatively young graduates living in cities who were excluded from home ownership (Brill and Durrant, 2021; see also Nijskens and Lohuis, 2019). This led to several measures to support BTR.

Property lobbyists argued that BTR faced nation-specific barriers that made the tenure less competitive in the context of the UK's comparatively inflated land values (Montague, 2012). These included narrow albeit stable risk-adjusted yields, an absence of formal recognition for the tenure in planning policy, a lack of investor experience in the sector and difficulty in acquiring land at scale compared to the higher prices offered by developers building for individual sale (Savills and LSE, 2017: 13). Accepting these claims, policymakers introduced a succession of initiatives designed to encourage the sector. Direct measures included a £1bn BTR Fund (2012–2016), BTR's inclusion in £10bn of loan guarantees for private and affordable housebuilding, and formal recognition for BTR in the 2018 National Planning Policy Framework (NPPF) (Bate, 2017). Additionally, indirect measures included the removal of tax breaks for smaller-scale landlords that left traditional buy-to-let less competitive, pressure on local authorities to dispose of surplus land assets to private developers, and the subsequent incorporation of the BTR fund into a generic Home Building Fund aimed at private development (Bate, 2017; see also Christophers, 2017).

Creating the local enabling conditions for BTR growth: The importance of council agency

Alongside these national initiatives are a series of local interventions which influenced the extent to which BTR was able to flourish in Manchester. Others have documented the important role of local agency in BTR development in London, when these national initiatives were accompanied by the development of close working relationships between BTR developers and local authorities in identifying landmark sites and ensuring facilitative planning guidance that could quickly process applications to delivery (Brill and Durrant, 2021). In Greater Manchester, the growth of BTR has arguably received even greater support from local state actors who, although lacking the same institutional powers of their London counterparts, have built a strategic orientation towards property-led regeneration over four decades (Hodson et al., 2020; Peck and Ward, 2002; While et al., 2004).

This orientation to property-led development has a particular history, which explains the historically strong network connections between the local council and developers. The Conservative government of the 70s and 80s cut local government funding whilst centralising the policy levers that would enable local authorities to address industrial decline on their own terms (Harding and Nevin, 2015; While et al., 2004). During that period, property developers in Greater Manchester levered their already strong local political networks with individual local authorities following the disbanding of the metropolitan-scale Greater Manchester Country Council in 1986 (Folkman et al., 2016). Ideologically, Manchester's local political leaders in the city's ruling Labour Party rejected the municipal socialism to pursue a form of ‘municipal entrepreneurialism’, inspired by the ideas of agglomeration economics (Peck and Ward, 2002), which prioritised attracting inward investment into property assets (While et al., 2004). The geographical benefits as a logistics and commercial centre for the north of England, combined with cheap brownfield land, a relatively flat topography and a city centre of warehouses and mills that hollowed out by de-industrialisation, formed the basis for a residential boom in central Manchester that took hold from the early 1990s (Folkman et al., 2016).

The financial crisis of 2008 threatened to throw this growth model off course (Deloitte 2017), prompting the council to use three main policy levers to encourage residential real estate development. First, housing and planning policies in both Manchester and Salford included the almost complete relaxation of affordable housing requirements negotiated with developers under section 106 of the Town and Country Planning Act 1990. 1 Out of a conservative estimate of the gross development value (GDV) of residential development in the city-regional centre of at least £8.3bn, 2 total section 106 payments amounted to just £33.3m in our total database (0.4%), of which £20.9m was for infrastructure (0.3%) and £15.4m for affordable housing contributions (0.2%). For Manchester, affordable housing payments in the city-regional centre from 2012 to 2020 came to just £9.2m, compared to £4.4m to Salford, and £1.9m for the much smaller relevant local authority area in our database of Trafford. Whilst s106 contributions can also be paid in-kind through the inclusion of ‘on-site’ affordable housing as part of a wider development, across our sample as a whole we could only identify 192 affordable homes provided in this way. When added to the 279 homes in our database earmarked specifically for affordable housing schemes (see Table 1 above), this brings the total amount of affordable housing receiving planning permission in the city-regional centre to 471 – just 1.0% of the total sample over this 8-year period. Whilst local authority powers to negotiate s106 contributions have been constrained by national planning guidance and viability assessments since 2012 (see Christophers, 2014; Colenutt et al., 2015), such low levels of affordable housing reflect deliberate planning policies designed to nurture ‘significant development proposals critical to economic growth’ (Manchester City Council, 2012: 117; see also Sagoe, 2019).

Second, policymakers at a city-regional scale gained greater strategic leeway to attract investment flows through the devolution of housing and spatial planning powers. This led to the creation of a Greater Manchester Combined Authority (GMCA) in 2014, which comprised the 10 constituent GM local authorities overseen by a directly elected mayor (see Haughton et al., 2016; Ward et al., 2015). 3 These devolved powers included the creation of a Greater Manchester Spatial Framework (GMSF) setting out planning policies at a city-regional scale, and schemes such as the Greater Manchester Housing Investment Fund (HIF) – a loan of £300m provided nationally and administered at city-regional level by the GMCA (Manchester City Council, 2017). Drafts of the GMSF have as yet made fewer explicit provisions for BTR in comparison to the comparatively stronger powers of the London Plan, which included fast-track measures for the tenure in 2017 (London First, 2019: 10). However, the HIF has played a key role as a source of bridging finance in de-risking BTR development for key strategic schemes in GM, lending out £167m of its initial round to one ‘mixed’ plus five BTR schemes comprising 3033 units – 67.7% of the 4483 housing units supported by the scheme. This uptake was replicated in grants and loans provided via nationally administered subsidies. In Manchester, £111.7m of the total £121.3m in infrastructure funding provided by central government to projects in our database went to BTR developments. In addition to the relaxation of affordable housing policies, local policymakers have therefore also sought to directly underwrite BTR investment in the city-region.

Third, local state actors moved beyond providing enabling measures and adopted a more proactive role as ‘executors’ of housing financialization through the strategic use of public land assets (see Beswick and Penny, 2018). The most significant example of this has been the agreement of a joint venture by Manchester City Council with the Manchester City Football Club owners the Abu Dhabi United Group (ADUG) in 2014 to develop private apartment housing in the strategically important location of Ancoats, a former industrial suburb on the eastern fringe of the city centre. 4 Branded as ‘Manchester Life’, under the terms of the joint venture the council leased public land in Ancoats to ADUG for projects, which to date have seen the construction of 1434 private housing units divided across eight schemes, 74.8% of which are BTR, and the remainder for private sale. 5 Senior councillors and officers sit on the boards of UK-registered companies under the partnership and the local authority holds a profit-sharing agreement with ADUG, the details of which have not been publicly disclosed (Collins, 2019). However, all rents and sales revenues are routed offshore through a company named Loom Holdings ultimately owned by ADUG registered in the secrecy jurisdiction of Jersey, obscuring the finances of the deal from public scrutiny.

The boom in BTR in the Greater Manchester regional centre

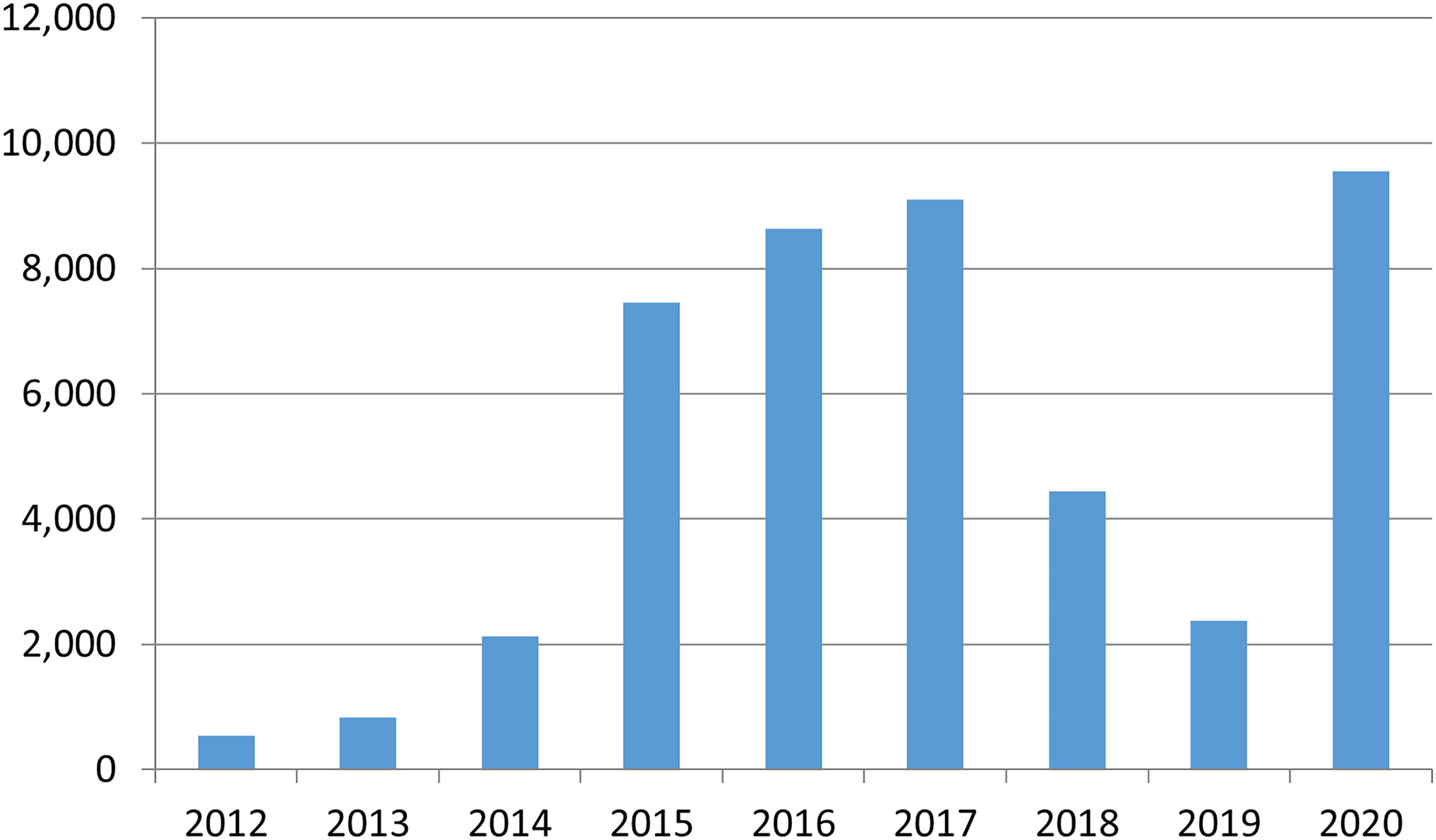

The combination of national policy and local council action form part of the TTN that led to the acceleration of BTR development after the financial crisis (Table 1). The financial crisis led to a fall in the number of residential units in the development ‘pipeline’, from over 4000 per annum in 2006 to under 500 units in the post-crisis years of 2010–2012 (Deloitte, 2017: 7). Yet since 2014, the number of housing units in the city-regional centre brought forward for planning permission have recovered (Figure 2), with Deloitte (2021: 5) estimating that the number of schemes under construction surpassed over 6000 apartments per annum by 2016. Our own database shows that of the total homes receiving planning permission since 2012, only 23.4% have yet been built, with 43.5% still under construction and 33.1% with works yet to start as of early 2021, demonstrating the still-unfolding nature of this development boom at the time of writing.

Housing units receiving planning permission in the GM city-regional centre, 2012–2020. Source: Authors’ database.

However, the particularities of Greater Manchester's TTN mean BTR occupies a different economic and spatial position within its urban centre relative to a global city like London. In contrast to the capital, where dense urban land use means BTR development is located in relatively outlying areas with good transport access (Brill and Durrant, 2021: 6), BTR development in Greater Manchester's regional centre tend to occupy prime, central locations. This is because of the availability of developable residential space, with opportunities to build single blocs with a unit size of 250 or above at a £10–£50m price point (Savills and LSE, 2017: 13). BTR developments also tend to be larger than BTS: the mean size per scheme of a BTR development is 350 units, compared to a smaller 218 units-per-scheme for BTS in Manchester. Lower land costs also produce average rental yields that are relatively higher in Manchester at 5.0% compared to London's 3.0% in 2019 (CBRE, 2019: 89–90). These features, in addition to the presence of a strong graduate retention rate that underpins rented housing demand, has led the city to become a benchmark for the BTR industry, with high yields predicted even as land in the city-regional centre is built out (Scott, 2022: 6).

These enabling and executing conditions show how the form of Greater Manchester's post-financial crisis residential boom has been shaped by local and national state actors, by excluding affordable housing and underwriting the risks of BTR development. However, this role of the state does not imply that financial actors themselves should be black boxed (see also Taşan-Kok et al., 2021). Enabling conditions only work if there are financial actors whose own risk/return calculations justify their entrance to a market. It is therefore important to understand how the economics of BTR operates as a ‘networked product’ (Beaverstock et al., 2021), constructing new relations by offering financial opportunities to investment actors who might otherwise avoid city centre property investment.

Global finance within the TTN: The broadening and deepening of housing financialization within Greater Manchester's city-regional centre

Territorialising Manchester: How BTR assets shape TTNs?

The post-financial crisis resumption of development in Greater Manchester's city-regional centre has been dominated by BTR (Table 1), suggesting it offers a stronger investment appeal than BTS assets in the Greater Manchester regional centre. This preference for BTR may in part reflect the less certain outlook for property prices in a secondary city like Manchester relative to London after the crisis – the appeal of fixed yields from BTR may have appeared less risky than a gamble on the direction of future property price increases at that time. BTR assets, in this sense, operate as ‘networked products’ (Beaverstock et al., 2021) – the outcome of the enabling and executing activities of the local council in combination with others which gave form to the asset; but also, by offering a different kind of return, meeting the needs of different parts of the global investment community – giving form to the TTN. We therefore see a different TTN for BTR assets relative to BTS assets in the Greater Manchester regional centre; but we also see differences in the TTN for BTR in this regional centre compared to those found in other studies of BTR.

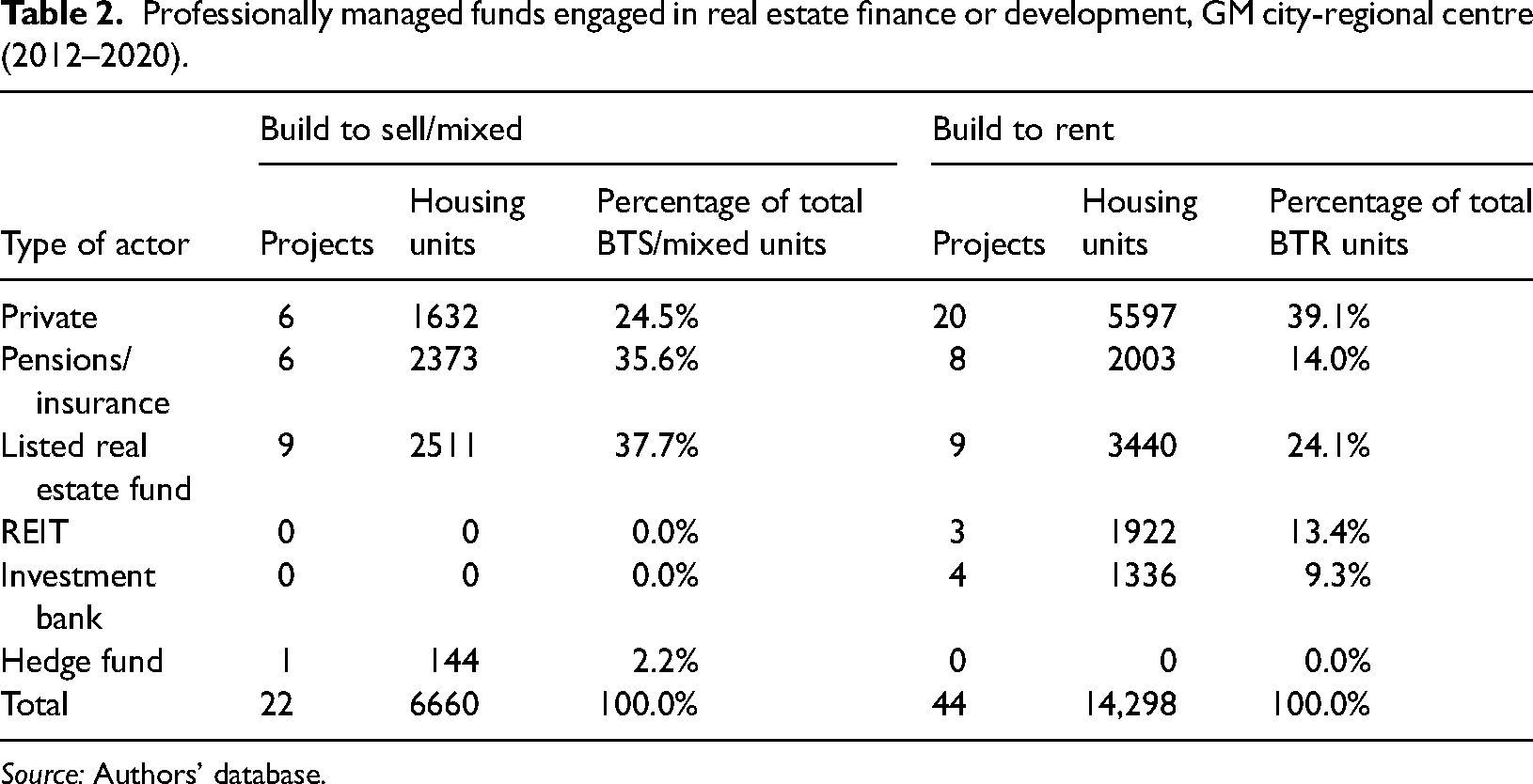

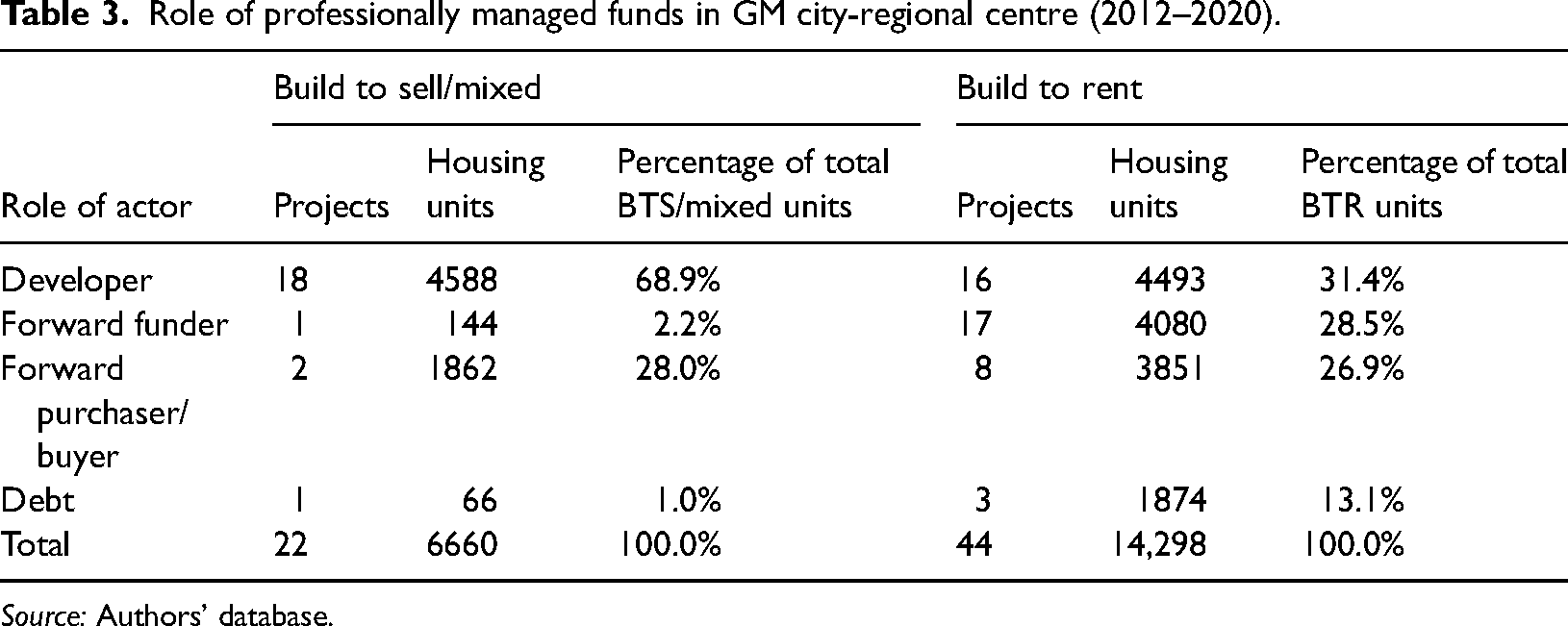

In total, 20,958 (46.5%) of the 45,069 housing units in our database were either developed or financed by professionally managed funds operating on capital markets, accounting for 66 out of 155 development projects. Within that subset of professionally managed schemes, BTR dominates in absolute terms, accounting for 14,298 housing units (68.2% of the 20,958) spread across 44 projects. This compares to 6660 units (31.8%) spread across 21 developments categorised as either BTS or ‘mixed’ (Table 2). Additionally, BTR supports a wider range of actors engaged in either financing or development. Just over one third were privately owned funds, including private equity funds, accounting for 39.1% of these specific BTR units in our sample, alongside 14.0% that involved pension funds and insurance companies. REITs were a minority of investors within our sample at just 13.4% of professionally managed BTR financing and development, suggesting a less prominent role for these vehicles in Greater Manchester than in European locations such as Dublin, Paris or Madrid (Vives-Miró, 2018; Waldron, 2018; Wijburg, 2019). By way of contrast, listed real estate firms have almost double the BTR investment activity at 24.1% than REITs. We also found evidence that investment banks were beginning to invest directly in property – representing 9.3% of BTR professionally managed activity. There is thus a deeper reservoir of capital providers financing and developing BTR property assets within the Greater Manchester city-regional centre, which requires some explanation.

Professionally managed funds engaged in real estate finance or development, GM city-regional centre (2012–2020).

Source: Authors’ database.

The heterogeneity of capital providers in our study may reflect the plurality of financial strategies that can be built around the relatively thin but stable margins that characterise BTR investment over the long-term (Nethercote, 2020). Our data indicates that BTR supports a greater variety of return strategies and risk appetites as investors can select their investment point within the development cycle (Table 3). BTS investment is heavily concentrated in the development stage, as other studies of BTS have shown (Romainville, 2017). 6 Investment in BTR, in contrast, is more varied, and goes beyond the simple supply of loans or the development of a scheme by a listed real estate fund. Financial actors can still ‘forward fund’ a plot by acquiring it and advancing funds to a developer for construction (28.5% of units where financial actors were engaged in financing or developing BTR). But they can also ‘forward purchase’ apartment blocks off-plan at scale (26.9%). By advancing funds to developers, investors receive a fixed-rate return on their investment and so avoid some construction-based risks if a project are delayed (Brill, 2021: 7). This feature attracts more risk-averse investors, and/or investors with a longer-term return horizon.

Role of professionally managed funds in GM city-regional centre (2012–2020).

Source: Authors’ database.

However, other financial actors do invest directly in development (31.4% of BTR housing units), often when institutional investment is present. Financial actors can either own a majority shareholding in real estate firms, such as the Saudi AIMS Investments’ holding in the developer Beech. There are also opportunities to tier investment vehicles to limit or extend risk/return exposure: for example, one listed entity, the Japanese developer Mitsubishi Estates, forward-funded BTR assets through a privately-traded equity fund, Europa V Capital. Within the time period of 2012–2020, we have also observed the development of a secondary market where BTR properties are ‘flipped’ in the same way as BTS once developed, such as the private equity firm Cabot Square Capital's sale of the ‘Tribe’ three-block former council housing development in Ancoats to the listed real estate company Grainger plc in 2017, indicating the possibility of taking speculative capital gains over patient, long-term yields from BTR assets.

The potential of BTR – as both a source of steady rental income and as an option on future capital gains – is therefore able to sustain a broader ecology of financial actors, enrolling a range of financial models, assets and practices in the process (August, 2020; Taşan-Kok et al., 2021). In so doing it acts as a networked product – by offering a set of risk/return options, it opens up investment opportunities for some actors, and so organises the financial and spatial networks that facilitate its expansion (Beaverstock et al., 2021). Our paper now examines how this fungible aspect of BTR assets – that they can collateralise a variety of different financial strategies – contributes to a distinct transcalar network.

The broadening and deepening of financial flows

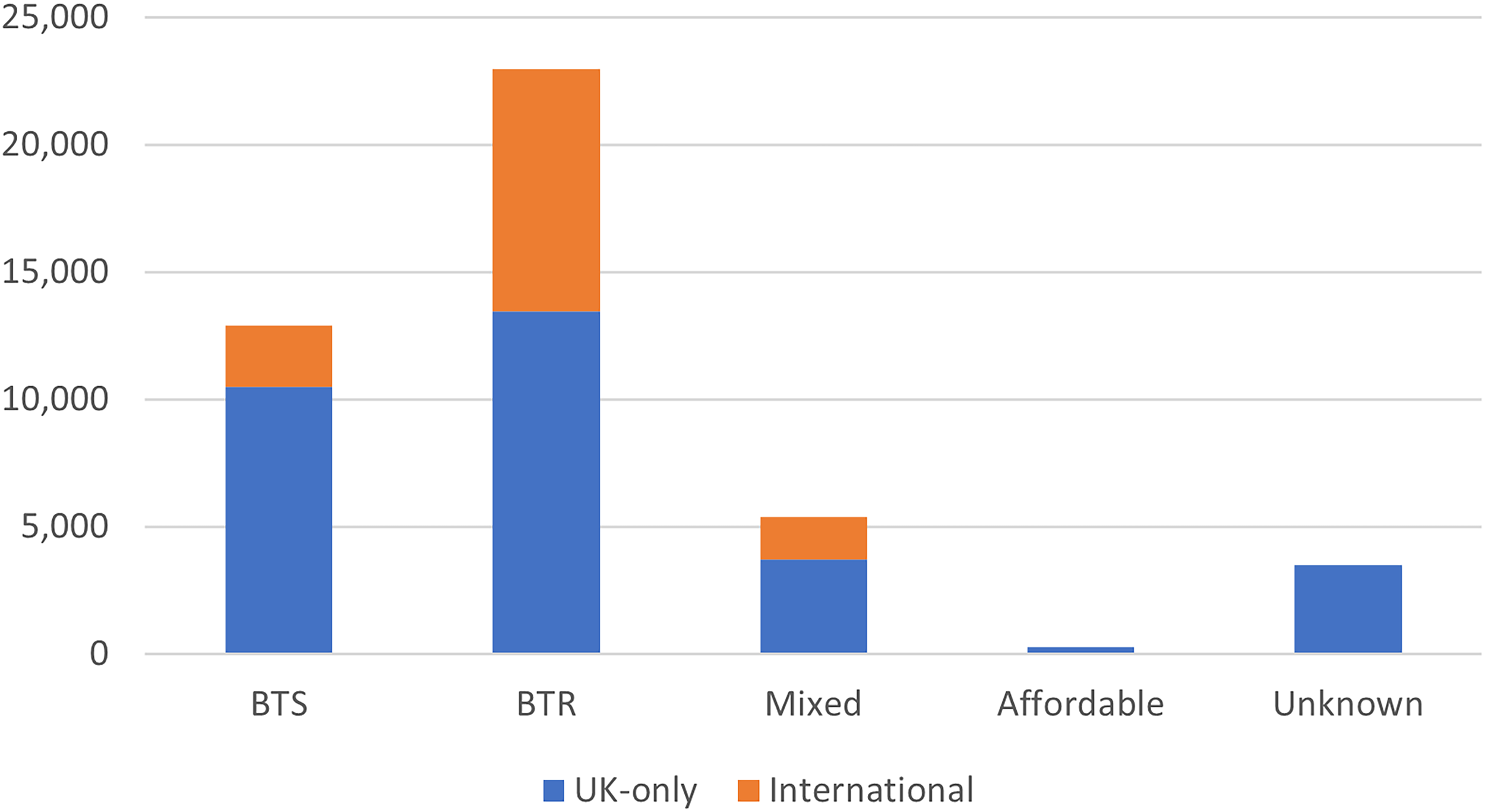

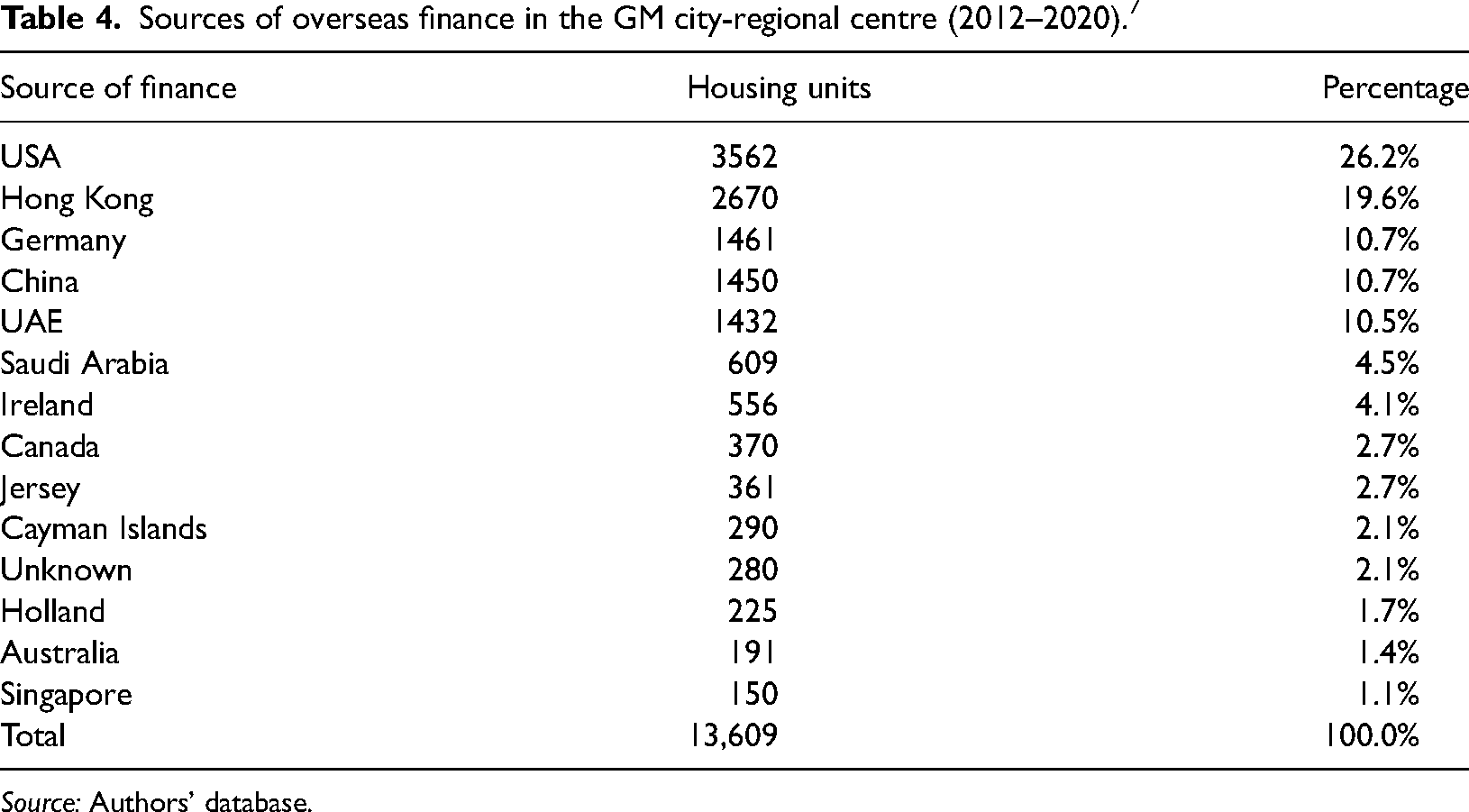

Manchester's residential property attracts capital flows from a range of transnational financial actors. Whilst most financing and development in our sample remains UK-based, international investment has become significant: 13,609 out of the 45,069 units in our own sample (30.2%) involved overseas financiers and investors (Figure 3). When broken down by tenure, this rate is higher for BTR than BTS, with 9532 out of 22,994 units in that category (41.5%) linked to overseas investment or development. In comparison, just 2411 out of 12,910 BTS units (18.7%) attracted overseas development finance, showing the greater attractiveness of BTR for international investors. Of the total 13,609 units involving overseas financiers and/or developers, 26.2% came from the USA, 19.6% from Hong Kong, and the remainder from locations including Europe, the Middle East and Asia (Table 4). The geographically dispersed sources of international capital indicate this broadening appeal of Manchester's BTR assets to overseas investors: BTR comprises 70.0% of those 13,609 units where we could identify overseas institutional investment.

Source of development finance by tenure in the GM city-regional centre (2012–2020). Source: Authors’ database.

Sources of overseas finance in the GM city-regional centre (2012–2020). 7

Source: Authors’ database.

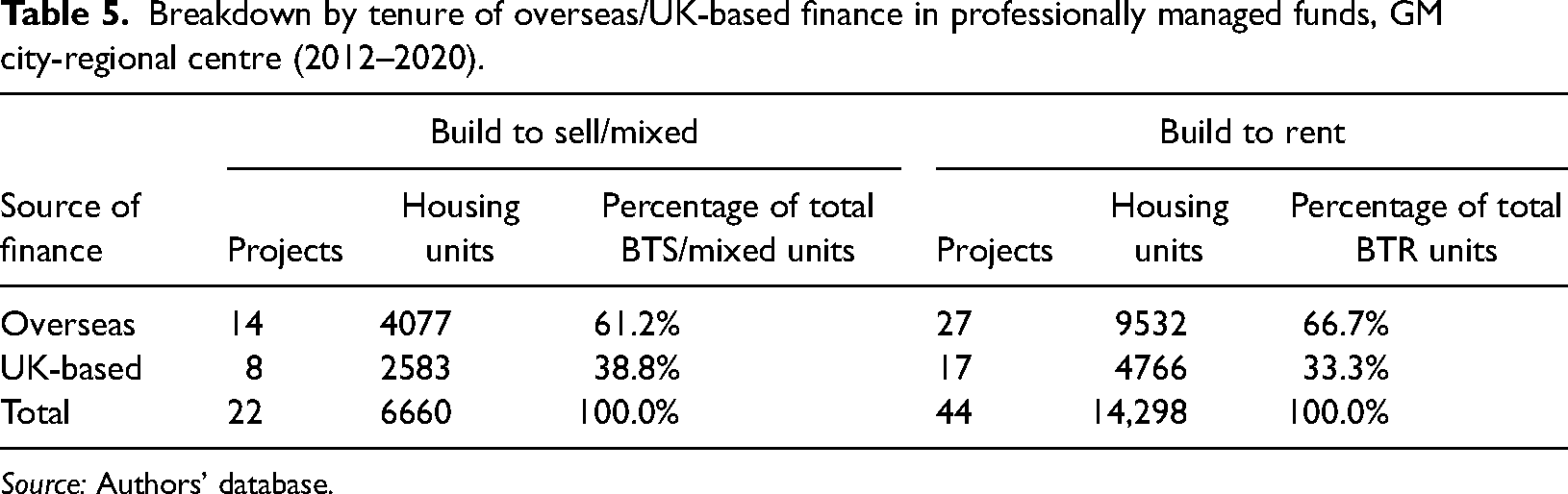

However, there are important subtleties within these aggregates. First, when we zoom in on the sub-category of the 20,958 housing units linked to professionally managed funds, BTR still dominates in absolute terms, with 66.7% of the 14,298 BTR units linked to overseas finance (Table 5). However, BTS/Mixed units linked to professionally managed funds, whilst accounting for a smaller number overall, also show a proportionately high level of housing units linked to overseas finance, at 61.2% of 6660 units. In other words, we find that when professionally managed funds are engaged in developing homes for sale in Greater Manchester, they are almost as likely to originate overseas. This may suggest that whilst BTR as a networked product can sustain a broader investor ecology, the transcalar networks it attracts are shaped by investors’ strategic preferences rather than whether they derive from foreign or domestic sources per se (see also Taşan-Kok et al., 2021: 390). Overall, overseas investors are nonetheless present in 64.9% of the 20,958 housing units linked to professionally managed funds in our dataset, showing the internationalisation of this investment market.

Breakdown by tenure of overseas/UK-based finance in professionally managed funds, GM city-regional centre (2012–2020).

Source: Authors’ database.

Second, rather than institutional investors determining housing production in a top-down way, we find regional developers capable of innovating connections within the transcalar networks linked to residential property in Greater Manchester's city-regional centre. For instance, whilst BTR is often understood as the ownership of housing for rent by an institutional investor at the scale of an apartment block or higher (cf. Nethercote, 2020), within our database we could identify only 37 out of 70 schemes (representing 13,513 vs. 24,502 housing units) where ownership involved the purchase of the whole block. This is partly because some schemes do not disclose a final buyer when undergoing development. But there are other cases where developers have retained the ownership and management of BTR apartments, and then leased out portions or individual units to either professionally managed funds or buy-to-let landlords. 8 Select Property, for example, is a UK-based BTR developer-operator owned along with its sister company Vita Group by the Cheshire-based entrepreneur Mark Stott. Rather than selling BTR developments to a single institutional investor on completion, Select overseas the development and management of BTR housing blocks whilst administering the lease of individual apartments off-plan to a range of smaller-scale UK and overseas investors. These strategies diversify leasehold occupancy across institutional and non-institutional landlords even as the overall development remains exclusively reserved for the private rented sector, multiplying the networked connections that may be formed around BTR.

Developers also play an important bridging role within these transcalar networks, forging new relations with actors in different jurisdictions, rather than inertly responding to investment logics set at a global scale. Select Property, again, established its business by opening a lettings office under its Select brand for the sale of properties in the UAE in 2004 in partnership with Gulf developers (Select Property Group, 2022). This finding complicates an understanding of financialization as the subjection of local housing markets to globalised investment markets, and affirms a need for future research to explore the agency of developers as bridging actors within the transcalar networks mobilised around residential real estate (see Ballard and Butcher, 2020; Mouton and Shatkin, 2020). It also raises definitional questions and future research could categorise the different products offered under the banner of ‘BTR’, a subject that is so far underexplored in the literature.

Third, in addition to acting as a bridge between the global and the local, regional developers also act as intermediaries bridging across the tenure categories of BTR and BTS. Some prioritise the construction of BTR apartments, including Renaker, a property developer based in North West England. Between 2012 and 2020, Renaker put forward for development nine schemes comprising 5851 apartments, 65.4% of which were for BTR, and just 10.9% for BTS. However, whilst Renaker focuses on BTR, 33.8% of the housing units it has constructed have been within ‘Mixed’ developments combining homes built for different tenures. For instance, Renaker's four-block, 1508 apartment Deansgate Square complex is a mixed scheme, where the ownership of two blocks have been transferred to the institutional investor Legal and General for long-term rent, whilst the remainder have been built for sale to owner occupiers and individual purchases by landlords. This suggests a more fluid property landscape that may be specific to the Greater Manchester regional centre, but highlights the potential for individual actors to operate across the TTNs of BTR and BTS as they pursue strategies of speculation and long-term rental yields simultaneously.

The entangling of financial actors, financial strategies and international capital suggests we are not seeing a binary transition from a speculative form of financialization to a longer term, yield-based model. For instance, Wijburg et al.'s (2018) study of the Ruhr argues the 2008 crash created new opportunities for rental financialization. Falling property prices and the rising debt costs meant many private equity investors withdrew from the market by selling their properties to REITs and independent listed funds. These trusts and funds sought assets with safe and predictable cashflows for their investors, and so tolerated lower returns in exchange for additional security, leading to a shift from a speculative ‘financialization 1.0’ towards a long-termist ‘financialization 2.0’.

Whilst these developments are important, we caution against generalising from the Ruhr experience. Although their study recognises financial actor variegation, it is too blunt a conceptualisation if it presents these changes as universal. Investment flows in Manchester suggest BTR development continues to be financed by private equity and other non-bank financial actors, illustrating their ongoing influence in property markets (Hendrikse and Fernandez, 2019). Rather BTR has led to a broadening and deepening of financialised processes within Greater Manchester's real estate. Broadening, as a diversity of actors with different return expectations, risk appetites, temporal outlooks and ownership strategies are drawn into the TTN for BTR development in Manchester, attracted by the fungibility of the asset class. Deepening, as ‘shadow’ or non-bank actors adapt and improvise to connect these new global sources of capital to local real estate assets, whilst extending their own reach by taking direct or indirect stakes in BTR assets. Financial actor strategies are thus contingent, improvisatory, and adaptive, connecting the variegated transcalar flows of financial capital to real estate assets. As documented in the capital anchoring literature, the capacity of those circuits to ‘land’ depends on their being harnessed by actors such as regional developers and local authorities working at a different scale whose decisions are path dependent and locally constrained. However, what a TTN framework enables us to see is that the nature of the product also shapes the networks mobilised around it, broadening and deepening these capital flows.

Conclusion

Our paper shows the importance of tracing the different relations between local, national and international actors involved in BTR development in ‘secondary’, post-industrial cities such as Manchester (see Ho and Atkinson, 2018) in order to understand housing financialization as a variegated process. Between 2012 and 2020, local state actors in Manchester and Salford played an enabling and executing role in fostering almost exclusively private development in the city-regional centre, in contrast to London where borough councils attempted to harness planning gain in peripheral sites to generate revenue streams for their wider budgets (Robinson and Attuyer, 2021). Whilst our work complements other studies which show that rental housing has become a major anchor for global finance over the past two decades (McKenzie and Atkinson, 2020), it highlights significant differences in the TTNs that institute BTR assets within specific urban morphologies.

This paper has advanced debates on the transcalar nature of financialization. By foregrounding the agency of assets themselves within TTNs we have shown both the fixity and fluidity of BTR as a networked product; fixity, insofar as the economics of the product present risk/return characteristics, which open up opportunities to some investors and foreclose others; fluidity because – as a stream of future cashflows – BTR can accommodate both yield-based and speculative strategic investment opportunities, thus potentially reaching a wider ecology of investors. Our approach makes visible a greater diversity of financial actors with quite different investment strategies involved in Greater Manchester's BTR asset class relative to BTS. These range from a deepening of financial flows, for example through vertically integrated models of direct ownership by institutional investors, to a broadening of financial flows through means such as developers retaining the ownership of apartment blocks whilst leasing properties to an array of institutional and non-institutional landlords. A TTN approach also demonstrates the overlapping ways in which BTR investment has been shaped by the local, national and international networks within which those BTR assets are embedded. BTR is, in this sense, a ‘networked product’ (Beaverstock et al., 2021) – it is not only brought into being by the networks of actors and expertise involved in its creation, but – through the investment opportunities it offers – shapes the relations between different actors in the network. The agency of the local state in Manchester's ‘regional’ market has acted to de-risk property investment by dropping affordable housing requirements, making investment more appealing to a wider range of investors, thickening the TTN for BTR in Manchester. Thus, underlying BTR assets are networks of divergent political agendas that seek to use post-industrial urban space as a strategic site to corral and harness flows to meet local political outcomes. Within this network intermediary actors play an important role, such as developers who connect with global capital providers to support a broadening and deepening of financialised flows within locally-bounded real estate (Ballard and Butcher, 2020; Brill and Özogul, 2021; Mouton and Shatkin, 2020).

Finally, our analysis of Greater Manchester raises questions about the conjunctural nature of financialization as a spatially and temporally embedded process that may be vulnerable to crisis – particularly in urban spaces that have previously been marginal to globalised residential development. Whilst Manchester City Council is currently in the process of embarking on a new affordable housebuilding programme, this activity is largely focused outside of the city-regional centre (Manchester City Council, 2018). The COVID-19 pandemic has exposed pre-existing trends towards online working that, in the context of rising city centre rents and a looming cost of living crisis, may hold the potential to threaten occupancy rates as younger generations are priced out of urban areas (De Fraja et al., 2021; Ward, 2021). Simultaneously, a rise in interest rates by central banks in response to inflation holds the potential to increase the costs of capital for developers, undermining the economic conditions that have overseen Greater Manchester's post-crisis residential boom. Whereas the decade since the financial crisis has seen the resumption of a free-for-all of private development, these conjunctural factors leave open the possibility that the stability of networks mobilised around residential real estate may give rise to market instabilities as Greater Manchester's housing landscapes are left exposed to future uncertainties.

Future work could address how the councils changing ‘enabler-to-executor’ role extends the TTN – for example, by examining the role of tax havens in their joint ventures, and the potential for such offshore structures to raise concerns about local accountability and transparency. In this sense, the work TTNs may overlap with work in financial geography, exploring the role of ‘paper’ geographies of finance (Haberly et al., 2019) in shaping Manchester's post-crisis residential geography, if the use of secrecy jurisdictions facilitates a rapid-build out of housing whilst enabling the resumption of state-led gentrification on the eastern fringes of the city-regional centre.

Footnotes

Acknowledgments

The authors thank the anonymous reviewers and the editors of this article for their constructive and insightful comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Economic and Social Research Council (grant number ES/V002597/1: ‘Manchester, The Centripetal City: The Lessons Of Property-Led Regeneration For Core Cities And Their Proximal Towns In The Northern Powerhouse’).