Abstract

Freeports are special economic zones, providing tax and customs benefits aimed at reducing economic friction and encouraging regional development. This place-based policy analysis of UK freeports draws upon qualitative interviews and deliberative workshops with leading industry, government, and civil society stakeholders in the two largest Freeport regions – Teesside and Liverpool. We find first, that purported tax, customs, and planning benefits are deemed less economically important than the agglomeration of innovation industries within a defined geographic boundary. Second, that stronger action on environmental and economic (in)justice is needed – Freeports could be a just transition mechanism if they can avoid capture by a ‘closed shop’ of industry players. Third, Freeports could facilitate cross-sectoral low-carbon economic regeneration, though they are subject to cycles of expectation, hype, and disappointment. We conclude that national policymakers must acknowledge the competing geographic and governance scales emerging within Freeport-hosting communities, as distributive environmental injustices between different locations remain broadly unaddressed. Finally, though cognisant of changes in political leadership on the horizon, we conclude that Freeports will increase the geographic spread of environmental injustice if this model of low-tax and low-regulation economics becomes a political norm within UK regional economic redevelopment strategy.

Keywords

Introduction – levelling up and the Freeport policy agenda in the United Kingdom

Following the 2019 UK general election, former Prime Minister Boris Johnson attempted to enact two core policy agendas. The first was to leave the EU: to ‘get Brexit done’. The second was to resolve regional economic disparities between London and the greater southeast, and other regions, the latter described as ‘left behind’ places. This policy agenda is articulated in contemporary UK Government policy as ‘Levelling-up’.

While levelling up is laudable given the emphasis on regional spatial inequality, government claims have been criticised for binding together conflicting economic and political narratives around regeneration (McCann and Ortega-Argilés, 2021), whilst lacking clarity, specificity, and targeted resourcing (Hudson, 2022). Moreover, Government strategy to simultaneously enable economic growth, ensure action on net zero, and secure the ‘red wall’ of former Labour-voting constituencies after EU-exit, were complicated by the challenges of economic shut-down during the COVID-19 pandemic, the inflationary pressures of post-Covid recovery, and ongoing crisis stemming from Russian invasion of Ukraine. The subsequent cost-of-living crisis driven by food and fuel inflation, reinforced socio-spatial economic inequalities at a time when the levelling up agenda came under intense political scrutiny.

Government levelling up strategy seeks to combine economic development with green growth by implementing climate change-relevant economic measures – notably the £12bn-backed 10-point plan for a ‘green industrial revolution’ (Vella, 2021), aligning innovation in low-carbon energy and transport to regional job creation. The planned economic recovery first described as ‘build back better’, is in some places facilitated by a high-profile land-use policy instrument of ‘Freeports’ in England (Webb et al., 2023), and counterpart ‘Green Freeports’ in Scotland (Minister for Just Transition Employment and Fair Work, 2022).

The Freeport policy’s origins lie in a report by Rishi Sunak at the time of the original Brexit referendum written for the free-market policy think tank, the Centre for Policy Studies (Sunak, 2016), that is, before he was Chancellor and later Prime Minister overseeing the Freeport policy. Sunak drew heavily on United States experience of Foreign Trade Zones (FTZ) to argue for Freeports as a key post-Brexit economic regeneration strategy (ibid). The UK’s closest historical equivalents are ‘enterprise zones’ and ‘Urban Development Corporations’ – discrete geographic areas in which companies are offered tax relief and accelerated planning permissions within the designated site. Freeports are an evolution of this approach, centred around major import-export hubs (including shipping, freight, and airports).

In the March 2021 Budget, Government announced the designation of eight Freeports in England. Each were later successful in their bids: East Midlands Airport, Felixstowe & Harwich, Humber, Plymouth & South Devon, Solent, Thames, Liverpool City Region (LCR), and Teesside. It is these last two – LCR and Teesside that form the focus and basis of this place-based critical policy study (as discussed below). Under this specific policy, the concept of the Freeport (which we capitalise to disambiguate this specific UK policy from the more general concept of ‘freeports’ as ports with special free-trade provisions) encompasses both a geographically defined region earmarked for industrial innovation and development, and a set of economic regulations, including tax and planning policy instruments bounded within those predefined regions.

Freeports are defined as logistical interfaces located outside the customs territory of a sovereign nation (in this case the UK) but located within its territorial borders, where the storage or processing of goods received from abroad is carried out before the goods are forwarded abroad (Lavissière, Fedi and Cheaitou, 2014). The UK’s new Freeport policy goes further to establish these sites as substantive special economic zones (SEZs) (Adam and Phillips, 2023), granting a range of economic benefits, primarily in the form of different types of tax relief and a set of simplified customs procedures. Businesses operating within Freeport sites could receive some or all of these benefits (the following summarised from Adam and Phillips, 2023; Department of Levelling Up, Housing and Communities, 2022; Simms, 2022; Webb et al., 2023): • Customs and tariff benefits: duty deferral while the goods remain on site and duty inversion if the finished goods exiting the Freeport attract a lower tariff than their component parts. • Stamp Duty Land Tax (SDLT) relief on land purchases within Freeport tax sites in England where that property is to be used for qualifying commercial activity up to 31st March 2026. • Enhanced Capital Allowances (ECA) – enhanced tax relief for companies investing in qualifying new plant and machinery assets. Firms will be able to reduce their taxable profits by the full cost of the qualifying investment in the same tax period the cost was incurred. • Enhanced Structures and Buildings Allowance (SBA) – enhanced tax relief for firms constructing or renovating structures and buildings for non-residential use within Freeport tax sites. • Employment tax incentives and National Insurance Contributions (NICs) rate relief – employers pay 0% employer NICs on the salaries of any new employee working in the Freeport tax site, applicable for up to 3 years per employee on earnings up to a £25,000 per annum threshold. An employee will be deemed to be working in the Freeport tax site if they spend 60% or more of their working hours in that tax site. The relief is available for up to 9 years from April 2022, with further government review mid-way through the scheme. • Business Rates Relief – up to 100% relief from business rates on certain business premises, available to new and existing businesses in Freeport tax sites for 5 years from the point at which the beneficiary first receives relief up to September 2026. Relief is funded directly by central government. • Local Retention of Business Rates – local authorities in which the Freeport tax sites are located will retain the business rates growth for that area above an agreed baseline, in a manner consonant with that of Enterprise Zones. This retention is guaranteed for 25 years, to allow Local Authorities greater certainty in long-term regeneration and infrastructure investment.

Importantly, not all Freeport sites offer all listed incentives – local areas negotiated with central government to determine the exact mix of incentives at each site. Still, collectively these incentives aimed to streamline construction, and provide support to promote regeneration and technological innovation (Webb et al., 2023).

Since January 2021, the UK’s Trade and Cooperation Agreement sets out the terms of UK trade with the European Union. The UK has left the EU customs union, single market, and VAT area, so industries that have just-in-time processes of manufacture across European/global supply chains suffer the friction of tariff and non-tariff barriers to the EU – this has subsequent negative impacts upon economic productivity for certain UK businesses (Lawless and Morgenroth, 2019). Freeports intend to alleviate this friction by creating a secure customs zone where business can be carried out inside the UK’s land border, but where different customs rules apply. The rules are intended to attract both maritime transport and port logistics companies to Freeport sites, and through a regulatory differential with the EU, to attract other forms of economic activity (Corruble, 2021). This might include, for example: ‘big tech’ companies, minerals, renewables manufacture, and process engineering that might not otherwise be located at port sites. In terms of the physical scope of land use, each Freeport can be up to 600 ha in size, centred around one or more air, rail, or seaport, but potentially consisting of multiple sites extending up to 45 km beyond the port(s) itself to create a special economic zone.

Though the customs and tax instruments are core benefits to regional businesses, the Department for Levelling Up, Housing and Communities (DLUHC) described them as ‘more than a special economic zone’, because they also encompass a range of planning, regeneration, innovation and trade and investment support mechanisms (HM Treasury and Ministry of Housing Communities and Local Government, 2021). DLUHC claims that the aims of Freeport strategy are not only to develop economic growth, but also to serve social justice needs, to promote international trade, and to serve as hubs for innovation and green growth. The Freeport is thus a mechanism for policy convergence (Busch and Jörgens, 2005; Drezner, 2005) between post-Covid-19 growth and regional economic disparity strategy, innovation investment, and net-zero action.

Freeport policy reporting from national and regional government authorities is subject to expansive claims about economic regeneration, the geographic distribution of wealth, the success of post-EU-Exit trade, and the sustainability of industrial strategy in the UK. In this paper, we subject these broad claims to critical policy scrutiny (Diem et al., 2014) in two key regions of the North of England – The Tees Valley (Teesside) and the Liverpool City Region. Specifically, we explore expectation, hype, and policy coherence that surround this nascent regional socio-economic development policy instrument, drawing upon theoretical frameworks across Science and Technology Studies and Critical Policy Studies as described below.

Place-based analysis of Freeports

We adopt a place-based and critical policy analysis approach to explore dimensions of power, discourse and institutional frameworks inherent in the empirical study of policy networks and practices (Ball, 1997; Gale, 2001; Ozga, 2021) relevant to the Freeports phenomenon. A place-based approach recognises the role that geographically defined and community-level social research plays in shaping deeper understanding of complex processes of expectations around Freeport policy – including expectations surrounding the future of industrial strategy, regeneration, governance, leadership, innovation, and regional assets (Beer et al., 2021). This will necessarily draw out issues that connect the Freeport to local prosperity, dynamism and deprivation, health inequalities, environmental injustice, skills development, regional economic displacement, and risks of crime or financial mismanagement, as these issues are all embedded in local geographic contexts and stakeholder representation rather than national-level policy abstractions. We focus upon Teesside and Liverpool City Region Freeports to illustrate these dynamics in two so-called post-industrial regions of England.

We argue that new regional economic development strategies such as Freeports designation, shape the expectations of local actors, which in turn shape the outcomes and success of the strategy itself – a dialectical relationship. For example, the Mayor of Tees Valley Combined Authority Ben Houchen claimed that the Freeport would create a ‘tsunami of jobs and investment’ to ‘turbocharge’ the regional economy (estimated £3.4 billion economic boost and 18,000 jobs) (cited in Nolan, 2021). Likewise, the Liverpool City Region Combined Authority foresees an initial increase of £850m and 14,000 new regional jobs through new investment (Liverpool City Region Combined Authority, 2022). Proclamations like these provide an optimistic framing of the economic and social value of the Freeport. However, they are inherently future-oriented and abstract, with an emphasis upon the creation of new opportunities, infrastructures, and capabilities within the regions they affect. None of these purported benefits pre-exist themselves, except in terms of the imaginings, expectations, and visions that shape their potential (Borup et al., 2006). At the point at which we collected empirical data through qualitative methods of interviewing and deliberative workshops (discussed below), the social construction of the Freeport concept by both national and local actors (including those in local and regional government, industry, trades unions, and social movements) inherently involves a degree of future-oriented abstraction necessary to providing the dynamism and momentum upon which Freeport success or failure is determined (see, for example, N. Brown and Michael, 2003; Van Lente, 2012).

Though bold claims are needed to ‘boost’ the Freeport agenda, they are in turn subject to cycles of hype: in which overenthusiasm through excessive positive messaging, leads to a period of disillusionment, and then to an eventual understanding of the policy’s scope and sustainability. As Fenn and Raskino (2008) argue, innovators, tech firms, and (in this case) policy authorities commonly tout an innovation to raise expectations, only to then abandon it when it falls short of initial expectations: a process that happens over and again with very little reflection about how to break this cycle. Given the relative scale and novelty of the Freeport policy framework in the UK, empirical research to understand the ways in which stakeholder expectations (and crucially hype) shape power relationships, investment strategy, and political discourse to meet a ‘Levelling Up’ agenda within local places and context are key to estimating the relative future success or failure of the Freeport platform nationally.

Case study details: Teesside and Liverpool city region freeports

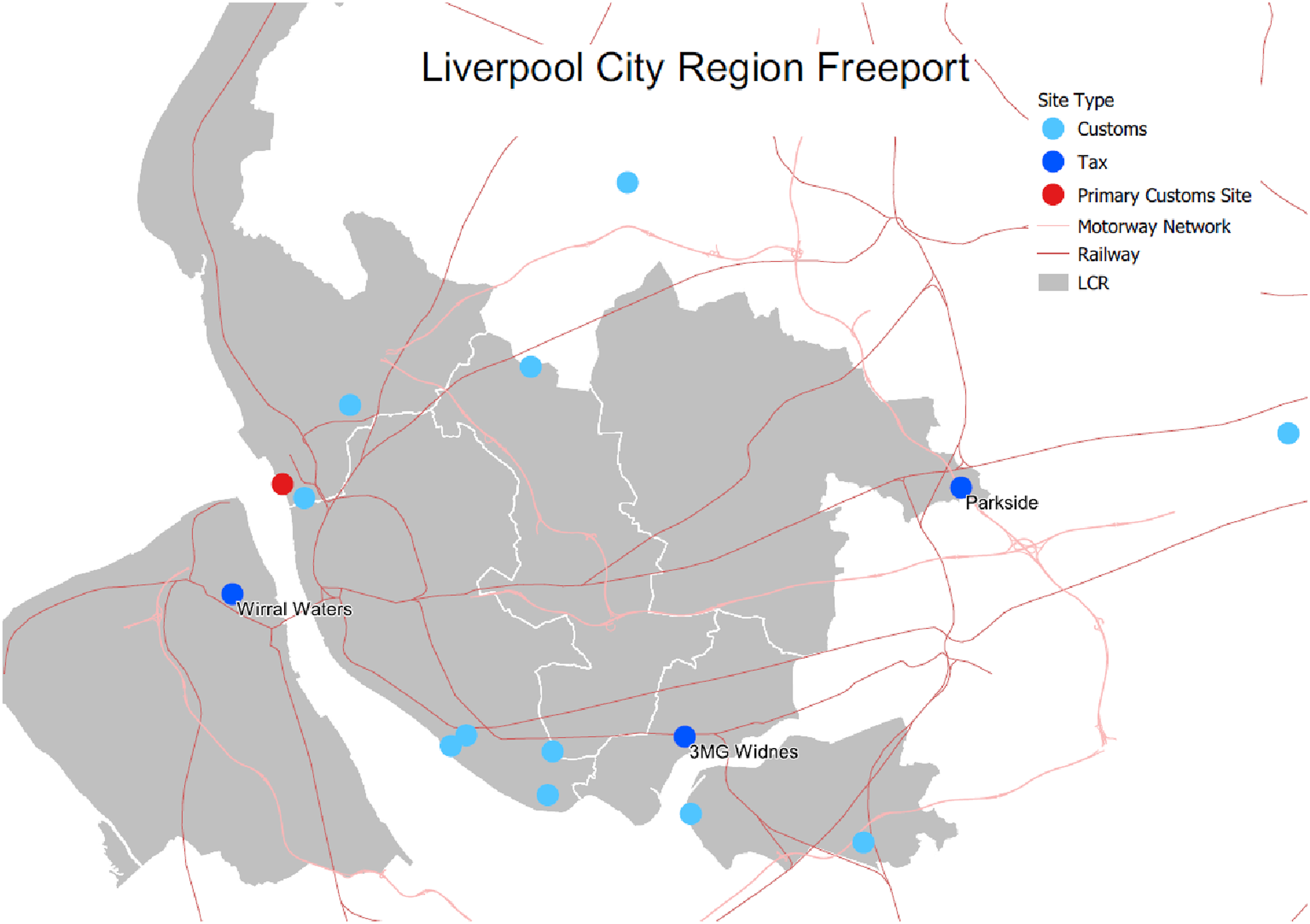

Our place-based analysis draws upon qualitative research into the two largest Freeport sites in England – Teesside and the Liverpool City Region. Both regions were key to the UK’s industrial history and have since experienced sustained socio-economic transformation. Liverpool, as a 19th century global trade hub and former ‘slaving capital of the world’ (Moody, 2020) for its role in shipping raw cotton to Lancashire garment production industries, has undergone more economic restructuring and urban change over the last 50 years than virtually any other city in Europe (Couch, 2017). The road and canal links between Liverpool and Manchester (‘Cottonopolis’) are reflected now in the distributed spatial structure of the Liverpool City Region Freeport plan (see Figure 1). Liverpool itself has been a place of contested urban redevelopment, within the city centre and around its waterfront and port (Fageir et al., 2021); and has benefited from a range of different forms of structural investment in rail infrastructure, housing (Kinsella, 2020), arts, and cultural heritage (Liu, 2019) as part of a sustained regeneration process. Liverpool City Region Freeport area.

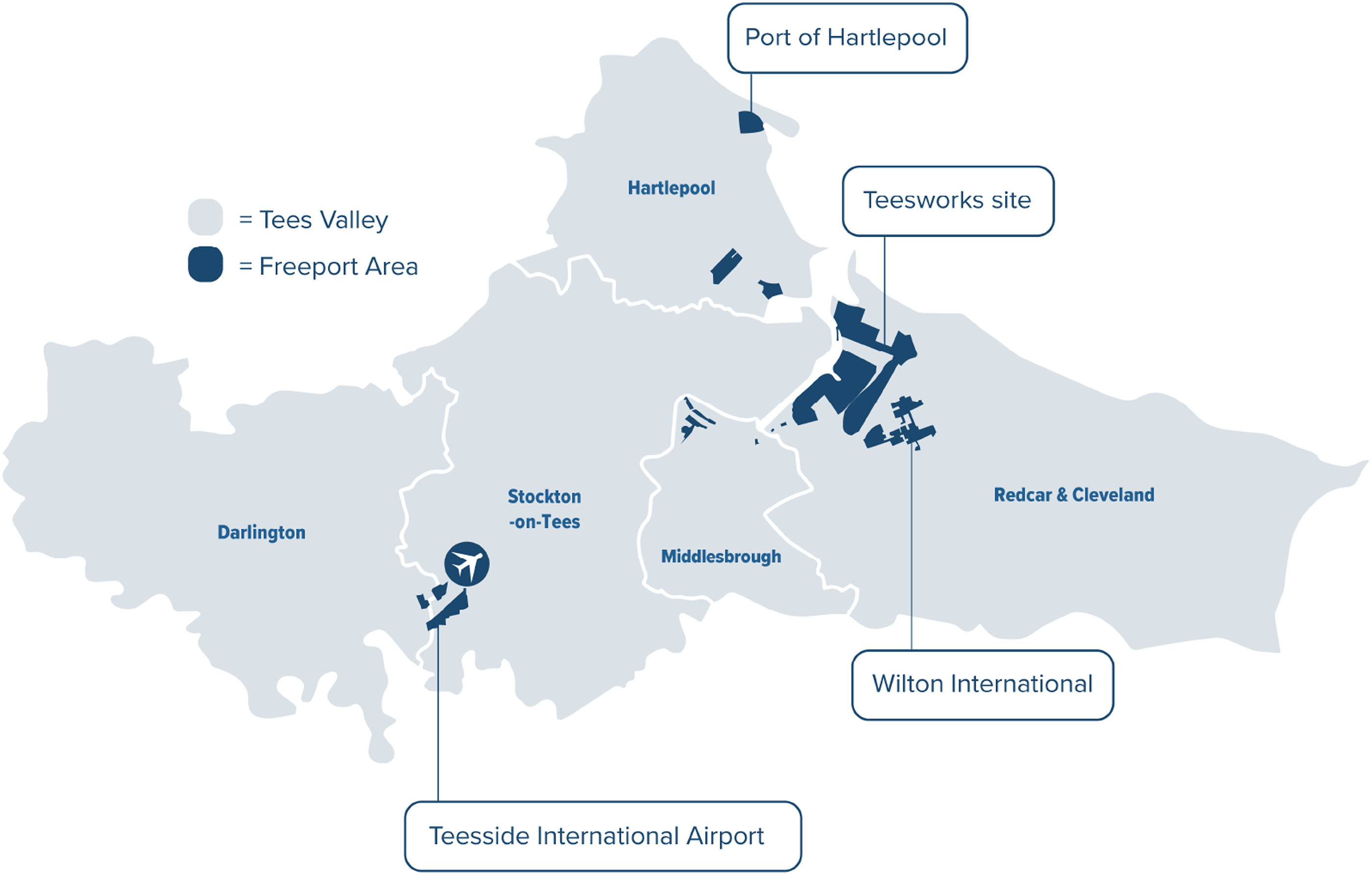

Teesside (Figure 2) by contrast is commonly defined as a ‘post-industrial’ region (Telford and Lloyd, 2020), characterised by periods of both urban obduracy and transformation (Hodson, 2008). Teesside’s industrial and economic history is dominated by the growth and then rapid decline of steel, coal, and chemical industries, and the emergence of a replacement economy of lower-wage occupations, including personal care, administrative, and service sector employment (Tees Valley Combined Authority, 2021b), which have profoundly impacted the socio-cultural identities of Teesside residents (Lloyd, 2016). The industrial heritage of Teesside continues to shape its economic future and influences the ways in which that future is conceived and envisioned (Warren and Pitt, 2018). Recent changes in political leadership and governance across what is now termed the ‘Tees Valley Region’ represent a concomitant evolution in its economic development. The Mayoral authority, currently led by Conservative Mayor Ben Houchen, has had a significant impact on the funding availability and use within the area (Smyth, 2021). The economic focus within Teesside has been upon the evolution of regional development policy (Chapman, 2005), the mobility of industry, and growing competitiveness and agglomeration of economic activity (Phelps, 2009). Teesside Freeport area.

These two case study regions are exemplars of the ongoing political challenge of socio-economic renewal in regions dominated by legacy industries. Understanding how the Freeport might influence these processes of renewal is a key research priority under government commitments to ‘level up’ such regions.

Methods

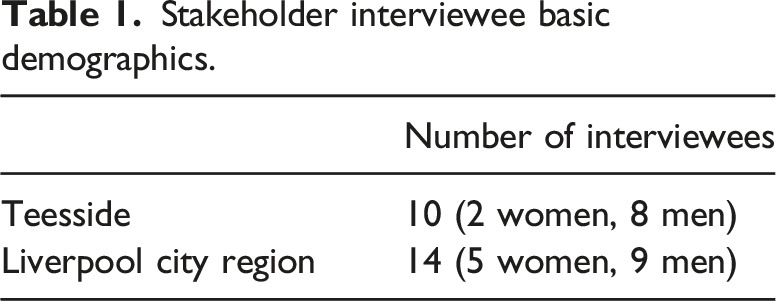

Stakeholder interviewee basic demographics.

We used a coding framework to capture relational and expressive values through a sequential process of description, interpretation, and explanation of qualitative data (Braun and Clarke, 2012). The interviews and initial coding were followed up by a series of three online deliberative workshops (2 in Liverpool and 1 in Teesside), each with 6–10 participants (total 24 participants). The workshops presented the coding framework and qualitative findings for further ‘truth-testing’, validation, and refinement with local stakeholders before publication. Workshops included some original interviewees and some additional stakeholders drawn from similar contexts. The coding process established a multi-level framework – from top-level thematic coding to establish the context and production processes of themes, followed by a more detailed examination of utterances, enabling us to draw connections between individual actor responses and a broader thematic coding framework. Due to ongoing local political sensitivities, we present the findings here in Chatham House-style presentation – utterances are unattributed to specific stakeholder actors to preserve anonymity, such anonymity having ensured data quality during the interviews, and this was assured as part of the research ethics review process.

Results

In the following section, we detail four primary thematic categories emerging from the coding framework. These ‘top level’ thematic categories concern: (a) Economic regeneration policy – ‘the only game in town’ (b) Low-carbon development – ‘the grit in the oyster’ (c) The Freeport as a just transition mechanism (d) Policy hype and governance challenges

Each is discussed in turn below, with supporting quotes drawn directly from interview utterances.

Economic regeneration policy – ‘the only game in town’

Reporting on the Freeport policy, whether positive (Dickins, 2022) or critical (Monbiot, 2022), often emphasises the light-touch customs and regulatory aspects of the sites – that Freeports are situated within the UK’s geographical space but outside the core customs territory. Though much of the media reporting and grey literature focused upon the customs and regulatory structure of Freeport sites, interviews with key stakeholders revealed that these aspects were of relatively low value and limited use to their business planning due to the administrative burden of running a customs operation under scrutiny by central government, and because of limits of geographic and temporal scope within the proposals (limits to 600 ha, and time limited to September 2026 for most tax incentive measures). Interviewees recognised that Freeports are not major free-trade zones but are closer in scope to enterprise zones of the 1980s, 1990s, and 2010s – geographically defined economic development zones with associated tax incentives. Indeed, there was a consensus across responses that the ‘Freeport’ name is a misnomer: some described foregrounding the customs benefits as a ‘red herring’. Contemporary Freeport policy is thus distinguished from the previous ‘freeport’ policy in the UK from the 1980s to 2010, which was much more directly aligned with customs benefits. This, in turn, creates specific regional economic development challenges.

One significant concern raised is the risk of geographically bounded tax incentives displacing economic activity from elsewhere, rather than incentivising new investment. Previous research has shown that 41% of the 58,000 jobs created in enterprise zones were relocated from elsewhere. Over half of jobs on UK enterprise zones between 1981 and 1993 were attributable to displacement and deadweight, usually from nearby high unemployment areas (Chaudhary and Potter, 2019). Swinney (2019) notes in reviewing the subsequent wave of enterprise zones designated by a later government in the 2010s, that at least a third of jobs were displaced from elsewhere, that the total number of new jobs was only a quarter of the number estimated by the Treasury in 2011, and that most jobs created were low-skilled. These displacement effects may be less pronounced for manufacturing and tech jobs than with services and retail (Hooton and Tyler, 2019), reflective of the comparatively weak UK manufacturing economy overall. Interviewees were cognisant of these risks: “The key thing is ensuring that there's some additionality and it’s not just displacement from other investment that would have happened elsewhere anyway.”

Freeports, like enterprise zones, are geographically bounded. Business rates relief and enhanced capital allowances are attractive incentives but experience in the 1990s shows that these instruments led to higher rents, thus offsetting economic gains (the largest beneficiaries were landlords) (Swinney, 2019). We found that our respondents expressed a range of opinions on the displacement issue, ranging from ‘concerned’, to ‘unworried’, to ‘positive’. However, across the interviews there was a general sense that the Freeport policy was, ‘the only game in town’: it was better to have one than not have one, due to the relative regional competitive advantage that it presented.

Though the customs changes within the Freeport designated space are notionally outside of ‘normal’ customs rules, interviewees were more likely to see the Freeports as a tool in efforts to create industrial clusters – a form of economic agglomeration, with the objective of creating good quality skilled jobs. “…the modality is a basic requirement… it’s as well as the customs and tax incentives but it is the building of an industrial cluster that you want and the point behind them, I suppose the overall arching goal… is to create a globally competitive clean technology cluster.”

Essential to this is the attraction of foreign direct investment (FDI) to maximise economic gains through global supply chain management and technology transfer, thus (hopefully) dispelling concerns about economic displacement from other port-regions (e.g. the Port of Tyne’s relationship with Teesside). The expectation of increased FDI raised hopes amongst some interviewees for a ‘manufacturing renaissance’ in which the economic multiplier effect from new low-tax investment in infrastructure stimulates economic renewal in the post-industrial regions of Teesside and LCR as the UK finds itself increasingly competitive, in these sectors – due to turbulence in the global economy (including, for instance, ‘near-shoring’), rather than Brexit per se.

However, as identified in the interviews and workshops, greater policy attention to skills development and education become key concerns. The regional benefits of Freeport economic development require a pipeline of opportunities, overcoming persistent skills gaps in the affected regions (Tees Valley Combined Authority, 2021a) particularly for low-carbon engineering (specifically in energy and transport). Nevertheless, for most of the stakeholders interviewed, the potential economic opportunity through high-skilled green job growth remained a key driver of local support for Freeports: “To me, the Freeport is that opportunity to sort of fast forward and re-pivot [to high-value, low-carbon jobs].”

We conclude, therefore, that stakeholders expect the process of agglomeration amongst high-skilled green growth sectors within a bounded geography to be the key driver of regional economic development, and the specific tax and customs incentives outlined in the Freeport bidding prospectus (HM Treasury and Ministry of Housing Communities & Local Government, 2021) are perceived as one tool to achieve this.

Low-carbon development opportunities – ‘the grit in the oyster’

There was a decarbonisation delivery requirement in the 2021 HM Treasury Freeport bidding prospectus: proposals had to demonstrate a decarbonisation contribution and the minimisation of environmental impacts (HM Treasury and Ministry of Housing Communities and Local Government, 2021). The details on both of these elements remained vague, however, when compared to other requirements. In practice, different elements could be emphasised, for example: energy use on the site(s); generation capacity; buildings design; import-export transport; commuter links; or shipping-related emissions. However, most interviewed stakeholders expected that Freeports would meet these obligations by becoming sites of low-carbon innovation within their respective regions, (LCR emphasising shipping and electric road mobility, and Teesside emphasising hydrogen freight, and carbon capture, utilisation and storage – see below).

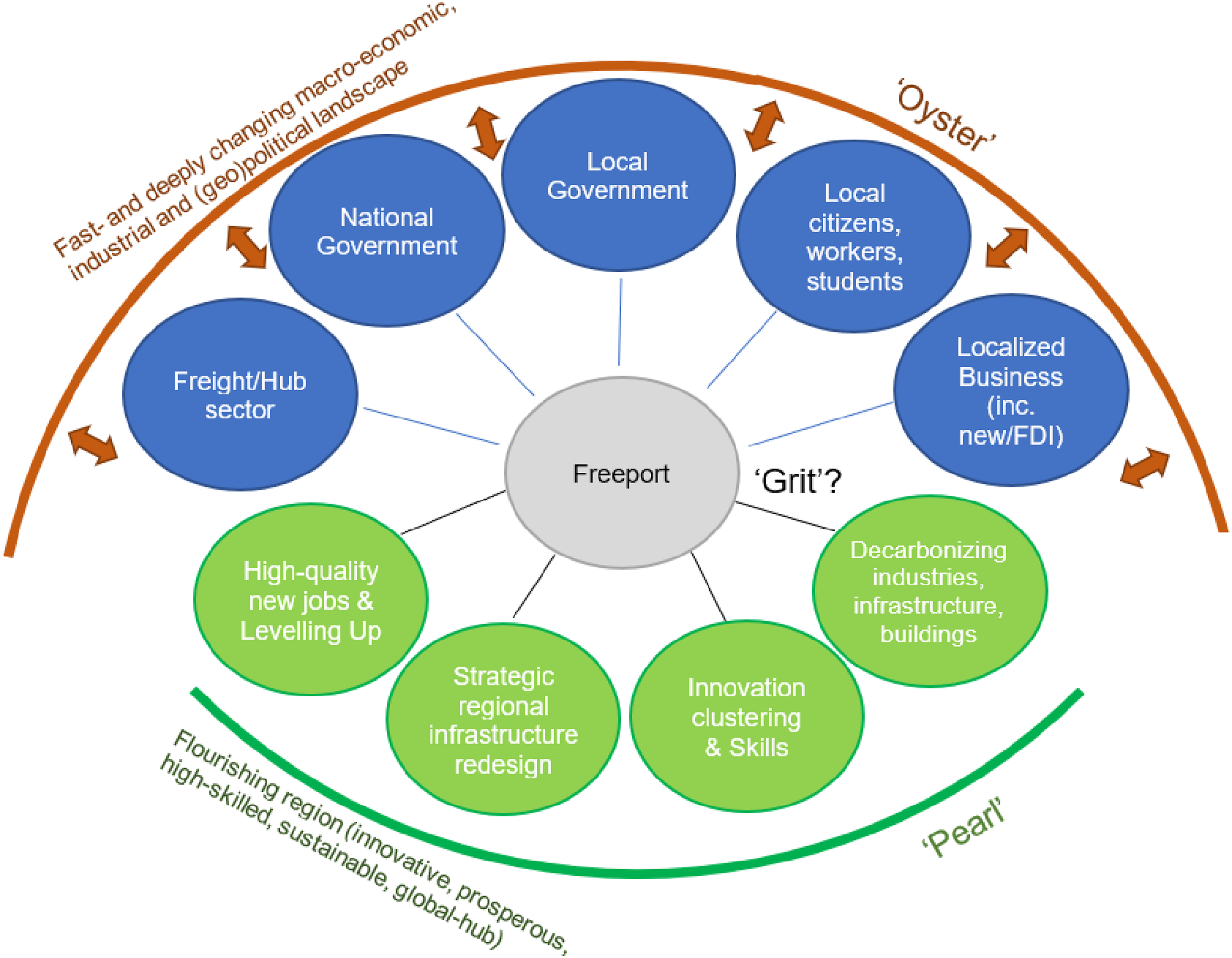

Though our respondents recognised the comparatively modest benefits offered by the policy to potential business participants, we suggest that Freeports could serve as the proverbial grit in the oyster (see Figure 3). Freeports policy alone does not constitute a ‘strong’ industrial net-zero strategy, though many significant regional stakeholders argued that it could promulgate a new vision and dynamism (i.e. the proverbial ‘pearl’) needed for deep and place-based decarbonisation. Freeports set out a ‘start-up’ culture whilst enjoying a significant regional profile, making them well-placed to play this role of decarbonisation ‘pearl’ for regional economic development. Completing the metaphor, the uncertain and ever-changing broader circumstances of global trade, digitalisation of industry, and manufacturing transformation may also here be the novel environment of the ‘oyster’ without which, reciprocally, the grit has little chance of such positive transformation (represented diagrammatically in Figure 3). The grit in the oyster – freeports as drivers of socio-economic development.

Mechanisms by which Freeports may foster such broader regional dynamism are examples of policy signals (Schubert and Sedlacek, 2005) to the private sector – signals to align market responses to import-export and low-carbon innovation strategy. For example, in Teesside, the opportunities of Freeport development dovetails with existing low-carbon industrial development strategy around hydrogen innovation (particularly the move towards so-called ‘green hydrogen’ through electrolysis of water production powered by renewable energy sources): “The future of the Tees Valley economy is best served if it’s about low-carbon industry because that’s where the big opportunity is. If Teesside can do hydrogen in a massive way, and carbon capture and storage… it’s the right choice to pick.”

However, in the LCR, there is a more specific focus upon transition in the local automotive industry (around electrification and batteries) and the decarbonisation of shipping and port infrastructure: “There is an opportunity for Merseyside in terms of the decarbonisation agenda. So, we could create something which is like a net-zero port.”

Though the policy coherence between Freeports and net-zero innovation was mentioned and outlined by most stakeholder interviewees, there was also considerable expressed scepticism from some stakeholders about its practicality: “I think there’s fundamental questions that need to be asked in terms of: is this okay from a climate emergency point of view? Should we be doing it? And if the answer’s yes, then great, well then let’s build the port with infrastructure that’s suitable for 2022 and beyond. Whereas everything seems to be very dated, an old-fashioned model of – the market will provide – and we know that never works out well."

There was also an equivocal appetite for Freeports driving the net-zero agenda: “Decarbonisation needs to be considered when all investment cases are made but the Freeport is not going to drive the net-zero agenda.”

Decarbonisation was seen by some as something that was ‘happening anyway in parallel’, rather than something led by the Freeport strategy, as one interviewee stated: “On decarbonisation, there’s a requirement to be, to hit national targets, 78% reduction by is it 2038 and being net-zero by 2050? But what does that even mean for a Freeport?”

Freeports were expected to be an adjacent or complementary strand of the net-zero agenda. However, given that Freeports were perceived by many respondents as ‘the only game in town’ they were also construed as important mechanisms to ‘build critical mass’ for collective action on climate change – again, the proverbial grit in the oyster. For example, it was noted that Freeports could host key technological system demonstrator projects, enabling expedited decisions on technological choice amongst various options currently in play. Here, for instance, it seems that several Freeports, including LCR and Teesside, are collaborating in hydrogen freight vehicle testing. There were also calls for Freeports across England to become better coordinated, to provide strong collective action on climate change: “Why don’t the whole set of Freeports work together to lobby central Government regarding the freight decarbonization technology choices they are all making?”

Freight decarbonisation was discussed in terms of the procurement of new shipping vessels, and new infrastructures for shipping and land-freight. Stakeholders commonly identified a political deadlock that creates carbon lock-in – that without a government steer on the types of low-carbon transport technology and supporting infrastructure available (e.g. electric vehicles, hydrogen etc.) a broader sector-wide transition will not happen. Respondents argued that the government is reluctant to ‘pick winners’ and so looks to the private sector to decide which technology to support. If Freeports can prove successful in aggregating a systemic regional strategy for freight transport decarbonisation, this might then scale upwards to changing national transport policy strategy in other sectors beyond the geographic bounds of the Freeport sites.

Additionally, Freeports, as important hubs for reducing carbon in transportation and industry, serve as a vital link between central government and private businesses. Their collective influence and technology experimentation can help bridge the gap between the government and the private sector, easing the stand-off between the two. Having only 8 Freeports is potentially positive as it enhances collaboration and strengthens their influence in Whitehall. Freeports could foster transformative changes at various political and geographic scales, creating new regional economies and dynamic socio-technical paths aligned with the broader momentum of regional and national decarbonisation. This extends beyond their initial purpose and stated policy focus in Freeport guidelines, as mentioned by one interviewee: “We need collaboration and a joined-up strategy for decarbonization. Can Freeports help organize that meeting of minds?”

We posit that Freeports can evolve from being just geographical hubs for low-carbon innovation to becoming forums that facilitate a holistic vision – hubs that involve multiple stakeholders in planning and executing net-zero transitions across different industrial activities. This aligns with the shared perspectives from the project team and various regional stakeholders in interviews and workshops in LCR and Teesside. This comprehensive approach aims to position Freeports as platforms for system-level transformation: “Having the ability to regenerate, think about it, plan it, do it in a bit better fashion as a committed local strategy … they’ve identified places wider in the city region where they can focus port activity related to the thing that would then spread the wealth from the port into some of the other parts of the city region, but also takes advantage of thinking a bit more in a pre-planned fashion of how you’d want to do that"

Expectations around the Freeport’s role in low-carbon economic development range from the sceptical to the cautiously optimistic. However, we note that stakeholders sometimes took surprising stances along this spectrum, for example, some business stakeholders expressed strong scepticism while some environmental groups expressed cautious optimism. The key consideration is the scope and role of multi-stakeholder involvement in the development of the Freeport planning and implementation process. Freeports can either remain a ‘closed doors’ decision negotiated between local implementation partners (e.g. combined authorities, regional development agencies, and businesses) or else can be subject to broader processes of participatory engagement with a broader range of stakeholder actors, allowing greater opportunity for envisioning a low-carbon economic development platform that meets the needs of local communities as well as local businesses and FDI institutions.

The Freeport as a just transition mechanism

One dominant strand of interviewee expectations concerned a fair or just transition for Freeport-affected regions. Just transitions require political outreach in Freeport design beyond businesses and local government to examine community socio-environmental impacts and to engage broader heterogeneous publics in decision-making and benefit distribution. The Teesside, LCR (and other) Freeport regions across England are (or were) home to carbon-intensive legacy industries (e.g. steel manufacture and shipping). The decline of fossil fuel-intensive industries and the emergence of a post-industrial economic landscape is (potentially) exacerbated by the ‘top-down’ implementation of net-zero policies (Emden and Murphy, 2019; Hudson, 2005). The rapid shift to reducing greenhouse gas emissions from industrial development and transport could lead to job losses within legacy sectors, and thus a need for skills training and job transition support within specific communities (alongside the significant need and appetite for such training already noted above: i.e., regarding both training of the young and re-training of those already working, but in high-carbon industries). As one interviewee states: “We have some industries that are going to die away because they are not consistent with net-zero. So, the big issue here I think is about how we can transition people across from one set of industries to the other.”

Net-zero is presented as a potential socio-economic threat to certain segments of existing Teesside and LCR communities. We observed significant concerns that existing local jobs would be lost – again, compounding long-standing challenges of unemployment from decline of once locally dominant industries – due to the imperative to reduce carbon emissions, and that any new jobs created in the quest for green growth would either be located elsewhere, or would not be available to workers who were negatively impacted (e.g. due to skills mismatches): “…we have got a lot of communities up here who are really vulnerable to, not to climate change, but to decarbonisation because they are in those jobs.”

Just transitions thinking encourages regional policy makers and employers to consider the social impacts that rapid transformation of the regional economy will make to communities, livelihood opportunities and other forms of socio-environmental impacts (such as health inequalities). In the LCR’s description of the Freeport benefits, they describe how benefits will ‘spill over and support impacts across an economic geography’ (i.e. the wider Liverpool City Region) (Liverpool City Region Combined Authority, 2022). Yet as one interviewee stated: “One of the underlying questions here and challenges here is local benefit versus regional benefit”

As a matter of environmental justice, in October 2021, thousands of sea creatures including crabs and lobsters washed up on Teesside’s beaches. Residents living in the Marske and Saltburn areas found piles of dead crustaceans that were ‘waist deep in places’ (Drury, 2021). Defra launched an investigation into the mass die off, stating that the most likely cause was an algal bloom and not the work of dredging for the Teesworks site (within the Teesside Freeport area). This finding was strongly disputed by diverse stakeholders including fishers, conservation campaigners, and an independent marine scientist who maintained that the die-off was caused by high levels of a chemical called pyridine from coal tar – a chemical present in the Dorman Long coal tower that was demolished in September 2021 and disposed of at sea (Price, 2024). Later, independent analysis by CEFAS concluded that it was ‘very unlikely that pyridine, as a single chemical entity, was the cause of the crab and lobster mortalities during autumn 2021’ (Cefas, 2023), though uncertainties as to the real cause remain. The impact on the coastal economy for local fishers along the north-east coast was deeply significant, not least because financial compensation from government was not forthcoming. Local media reported that progress on the Teesworks site prioritised some forms of economic development at the expense of others, and that ecological damage was the cost of such rapid industrial regrowth in the region (Kirby, 2023). Just transitions thinking around Freeport development must therefore consider alternative industries and ecologies to ensure fairness and wellbeing are central to industrial development planning.

Among our interviewee and workshop participants, similar concerns were raised around how the costs (in terms of negative socio-environmental impacts) of Freeport designation and associated increases in port-related activity would fall on certain communities (e.g. those along existing freight routes or near heavy industry), while the benefits (in terms of new, higher-skilled, better paying jobs) would be enjoyed by others. “They just don’t want to have an expanded port at all costs. They live in the neighbourhood, they’re raising families, and they don’t want their environment to- They want a quality of life, they don’t want their environmental health reduced or the risks associated."

The Department of Levelling Up, Housing and Communities (2022) described how: ‘Freeports support the Department for Transport’s ambition for a freight strategy which builds on the UK’s status as a global facing port nation. Freeports will amplify UK ports of all modes as hubs for innovation and investment, transforming our freight systems’. This transformation does not automatically lead to decarbonisation, however. Increased road freight from and between the port systems will have negative impacts upon air quality if current diesel freight systems are used. This will almost certainly be the case for the majority of journeys in the foreseeable short- and medium-term. New road infrastructure to support site workers and shipping will further exacerbate these impacts. And even if such additional emissions are comparatively small (e.g. estimated by Arup, in analysis for the Liverpool Freeport, at 2% over 5 years in the Liverpool case), this is still geographically concentrated and on top of existing emissions and air quality impacts that are already highly detrimental for health and concentrated in already-deprived areas (e.g. generating a 10-year loss in life expectancy along the main road to access the Port of Liverpool vis-à-vis standards further north in the same borough), a source of considerable local grievance and political tension.

One specific concern amongst stakeholders is the lack of joined up thinking between the Freeport site development and local public transport and non-road freight infrastructure. For example, in Teesside, public transport is planned at the scale of the local authority, rather than the supra-regional level of the Tees Valley Combined Authority. In LCR, controversy remains over the planned dual carriageway down the middle of the 3.5 km long Rimrose Valley country park to relieve existing congestion through residential areas into the Port. Clearly, decarbonisation and air pollution planning for connective transport networks to and from port regions is not ‘baked in’ to the Freeport process – thus exacerbating carbon lock-in from fossil fuel powered transport within the locality – and concern frequently returned to such issues in our interviews with stakeholders. “It’s like, well yes, people do need jobs, but it doesn’t have to be done in this high-handed manner, it ought to be done through democratic planning, consensus and using the right sites in the right way, linking with the right types of transport.”

As multiple interviewees suggested, the decarbonisation of the Freeport requires a stronger set of mechanisms for a wider segment of community actors to shape the outcomes of Freeport site development, link to local environmental justice concerns, and integrate with existing community-level infrastructure, such as bus and rail services and renewable energy generation capacity and to ensure that transparency and accountability in public financing of Freeport development is observed.

Policy hype and governance challenges

One stakeholder described early discussions of the Freeport planning process: “The Freeport was really used as a metaphor for economic optimism.”

Like other elements of the Levelling Up agenda discussed elsewhere (Hudson, 2022), Freeports have been discussed by local policy authorities primarily in abstract, positive but non-specific terms. This leads to a top-down policy strategy that sparks considerable distrust in the delivery mechanisms and implementation processes, specifically regarding the level of support and investment from central government, even as and when ‘levelling up’ was an explicit and much-trumpeted government priority: “I was pretty underwhelmed by the Levelling Up paper if I’m honest…. there’re great broad-brush principles in there that you couldn’t disagree with. It’s always the devil in the detail.”

The lack of clarity and specificity in what levelling up means in practice, combined with bold claims of their significance for regional development leads to the attendant problem of a cycle of hype (Fenn and Raskino, 2008; Jennings et al., 2021): the widely touted ‘tsunami of jobs’ in Teesside, or promises regarding hydrogen economy transformation raise the risk of national and local boosterism – in which heightened public expectations over socio-economic development outcomes lead to disappointment and disenfranchisement if the short- to medium-term benefits don’t match public perception of outcomes: “I think the biggest problem will be overselling the benefits the Freeport can bring… The biggest danger, the biggest risk, is it not, in terms of communities losing faith in projects is to oversell and underdeliver.”

The short-term nature of Freeports (with the current policy expiring in 2026) problematises their promise to drive longer-term transformation of regional decarbonisation and economic growth. Previous area-based initiatives including, for example, the Urban Development Corporations of the 1980s and 90s, ran over longer periods as well as having more significant spending power (Imrie and Thomas, 1999), thus allowing for visible if not transformative impact: “You haven’t got an awfully long period to benefit from things like the National Insurance contribution holiday and things. So, I don’t know whether there is scope in Government policy to kind of look at it and say, ‘Hey, this is working really well, we can extend it.”

One major concern is the lack of transparency in Freeport governance creating confusion for local businesses in designing longer-term growth strategy, uncertainty over the level of local government support they will receive, and damaging investor confidence: “There’s no transparency whatsoever… the way the port is integrated into the rest of the geography, I don’t think it’s very clear at all.”

Poor transparency is an acute political problem in Teesside. In 2022 and 2023, the Freeport under The Tees Valley Combined Authority (TVCA), and its connected entities, including the South Tees Development Corporation, came under intense scrutiny from journalists such as Richard Brooks at Private Eye and Middlesbrough Labour MP Andy McDonald around issues of alleged ‘corruption wrongdoing and illegality’, what MacDonald saw as ‘truly shocking, industrial-scale corruption’ in Teesside (cited in M. Brown and Quinn, 2023). Levelling Up Secretary MP Michael Gove called for an independent inquiry (from a panel appointed by him – a move that was criticised by Shadow Levelling Up Secretary MP Lisa Nandy for not involving the National Audit Office). The review concluded that although there was no finding of corruption, the project was ‘excessively secretive and could not ensure public money was being well spent’ (Partington and Brown, 2024). Clearly the success of the Freeport in that region requires a radical transformation in transparency and accountability in order to ensure social justice, and secure investor confidence in net-zero innovation across the industrial Teesworks site.

At the national scale, commitments to net-zero transformation in transport infrastructure and energy generation require other forms of strategic commitment to target zero-carbon sectors – the Freeports alone cannot sustain this even where (as discussed above) they could be highly significant in enabling or kick-starting regional co-ordination. Concerns were raised over the future of the Levelling Up agenda and the role of the Freeport within this national-level economic rebalancing strategy. With a change of leadership underway in the Conservative party at the time of data collection, (the successive resignations of Prime Ministers Johnson and Truss, and the growing sense of the declining power of the Conservative Party), suddenly the future of a northern England-focused regional development strategy was thrown into doubt. Freeports have remained a core regional economic strategy under Prime Minister Sunak as a mechanism to rebalance the economy between urban centres and regional and coastal periphery. However, action towards legally binding net-zero commitments are now less certain given the challenges of tax rises and spending cuts under the new administration and weakening commitments to phase out fossil fuel-intensive transport systems. Nonetheless, interviews with public and private sector partners in the case study regions suggest that policy commitment to existing announced sites will remain strong: there is a growing momentum behind net-zero transition coming from multiple governmental and non-governmental drivers nationally and locally. Moreover, despite concerns about economic and socio-environmental threat from Freeports, optimism was also expressed surrounding continued green sector job growth encapsulated in current and future Freeport policy strategies. “There is no reason why we [Teesside] can’t become the centre of hydrogen production for the UK and an exporter of hydrogen technologies as well. There is absolutely no reason why we couldn’t really hold on to that. So, I find it hard to see the negatives”.

And: “Liverpool has masses of resources that can support the transition away from carbon fuels so yes fundamentally matching the two together [economic growth and decarbonisation] seems to make perfect sense."

Despite concerns over governance transparency, political support under changing political regimes, and (potentially) a change of Government in 2024 and beyond, respondents sensed a continuing momentum behind this format of low-carbon innovation-through industrial agglomeration, using Freeport tax and tariff incentives to spur investment.

Conclusions and policy recommendations

The Freeport policy agenda has stimulated considerable hype around the regional development and green growth trajectories of ‘left behind’ places. Freeports have become a focus point for regional actor expectations of economic growth, low-carbon transition, and skills development – though our interviewees exhibited cautious optimism about their value as economic and low-carbon policy instruments. Freeports (and Levelling Up) are tied to specific political leadership (Johnson and Sunak) at a specific point in time. They are a product of post-Brexit and post-Covid economic recovery thinking. Nevertheless, we find that Freeports are likely to stay – they have stimulated a range of stakeholder expectations concerning the economics of agglomeration within former industrial regions; namely, the potential value of Freeports as bounded sites that in turn send a policy signal to spur foreign direct investment and other market mechanisms to cluster net-zero industrial innovation in these sites. Previous special economic zones have sometimes turned to lower value economic activities (e.g. low value manufacturing, call centres, or retail). By contrast, there appears clear emphasis from the Freeports to target higher-value sectors and jobs, which if successful could serve as a just transition mechanism that helps to alleviate the persistent regional economic development challenges of post-industrial economies such as LCR and Teesside.

The optimism expressed around Freeport economic activity serves as a powerful driver of regional ambition at a time when economic uncertainty over inflation, tax rises, and a cost-of-living crisis in the UK (as across Europe) potentially diminishes the prospect of economic regeneration in the former industrial regions of England and Wales. The lack of specificity in Freeport implementation means that stronger connections between clusters of low-carbon industries and local skills planning is needed to ensure that such a just transition within the host region can be achieved – that marginalised local communities will directly benefit from new jobs in established and emerging low-carbon industries within the Freeport innovation clusters.

Despite the initial hype around Freeport policy, our stakeholder interviewees expressed, first, that the Freeport alone is not capable of delivering all the ambitions that governmental and stakeholder rhetoric have imbued it with, and that concerns over transparency and poor site governance stymy investment opportunities. Nevertheless, Freeports have value as the ‘grit in the oyster’ – a geographically distinct focal point for cross-sectoral co-ordination to develop a systemic vision for local and regional economic regeneration and just transitions. Taking on such a role requires strategic foresight. However, such foresight cannot be assumed, especially considering the varying organisational leadership within individual Freeports. This uncertainty arises because adopting a regional convening role exceeds the original policy’s intended scope. Despite these challenges, our stakeholders anticipate that well-executed Freeports serve as effective policy signals – aligning market responses with international trade and low-carbon innovation strategies. This alignment is expected to foster the creation of potentially transformative regional clusters, particularly in areas such as regional transport planning and its decarbonisation. Given the extensive geographical reach of Freeports, there is a heightened need for explicit and energetic attention to this agenda by Freeport governing authorities.

Finally, issues of transparency and good governance require stronger engagement across different scales of government and civil society; even many local politicians interviewed feel under-informed about the Freeport strategy and disengaged from its development. This engagement should extend to broader stakeholder networks within the communities that host Freeports, not just businesses and local authorities. Wider engagement with a range of stakeholders has the potential to substantively improve decision-making, enhance legitimacy and credibility, and contribute to a more just transition to net zero and economic regeneration in the face of high-profile political controversies in Teesside in particular.

Freeports-as-engagement-initiatives could potentially shape future ‘Levelling Up’ strategies at different geographic and governance scales – going beyond the narrow remit of a low-tax investment site. Stakeholders interviewed posit this need for engagement in Levelling Up as an issue that we could describe as having both distributive and participative justice elements. The imperative to level up at a macro/nation-scale must be matched with attention to effects at a micro/local-scale. Levelling Up within the local/regional economic geographies is as important as levelling up between those geographies and more affluent parts of the UK. The distribution of social, environmental, and economic costs and benefits within and around Freeport designations requires significantly more attention than is currently allowed within existing policy. Connected to the issue of good governance is an urgent need for wider engagement on Freeport strategy development and its potential successors to ensure that all relevant stakeholders can contribute to these considerations. This relates to a challenge of regional-versus-local benefit and cost: do the benefits of port development ‘spill over and support impacts across an economic geography’ (Liverpool City Region Combined Authority, 2022) or are they only bounded within economic geographies of the sites themselves? Moreover, do the environmental costs fall on communities that do not reap the economic benefits? In short, the positive potential for Freeports to effect broad-based gains across the range of issues with which they have been originally tasked remains, but as a nascent economic policy instrument, Freeports remain under threat from the broader economic and political forces at play across the UK economy.

Footnotes

Acknowledgements

This project was funded through the Engineering and Physical Sciences Research Council grant: DecarboN8 – An integrated network to decarbonise transport EP/S032002/1, Seedcorn Fund: CarbonFreePorts: Freeports as opportunities, not threats, for place-based decarbonisation of transport. The authors wish to thank the participants for their engagement with the research, and the managers and administrators of the DecarboN8 Network for their support.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: this work was supported by the Engineering and Physical Sciences Research Council; DecarboN8 - An integrated network to decarbonise transport EP/S032002/1, Seedcorn Fund: CarbonFreePorts: Frepports as opportunities, not threats, for place-based decarbonisation of transport.