Abstract

This article argues that a European media industry has failed to materialize despite sustained policy efforts by the European Union. Apart from film and TV production groups, European broadcasters/streamers are more nation-centric and less regionally integrated than in the late 20th century. The first section charts the international expansion of European broadcasters and documents how their regional integration began to unravel in the 2010s. Looking at the determinants, the second section argues that legacy broadcasters struggle to lift their digital revenue and are under immense pressure from streaming giants whose scale has created an uneven playing field. Using the global value chain (GVC) framework, the article draws a distinction between European lead firms (broadcasters and streamers) and their suppliers (e.g., film and TV content production groups). It contends that while the EU legislative framework supports the latter, it does not protect the former from global market forces.

Introduction

In 1989, the European Community inaugurated a new era in media policy with the adoption of the Television Without Frontiers directive. It aimed at facilitating cross-border media flows and European media integration. This article argues that these efforts have been in vain and a pan-European media industry has failed to materialize. In the mid-2020s, Europe-based media groups are less geographically integrated than in previous decades and most transnational activities are conducted by US-based media conglomerates.

The first section charts the development of pan-European media groups in the 1980s and 1990s and documents how this expansion began to unravel in the 2010s. Transnational film and TV content production groups who act as suppliers to broadcasters and streamers are currently thriving in Europe. However, for market-facing lead firms (broadcasters and streamers), the era of European integration has come and gone. The second section analyses the causes of this regional disintegration. Legacy broadcasters struggle to increase their revenue in the digital era. They face enormous pressure from streaming giants whose scale has created an uneven playing field in the industry. The current EU legislative framework aims at supporting film and TV producers but does not protect European lead firms from global market forces. The conclusion argues that more support of European broadcasters and streamers is needed in order to stem their decline.

Theoretically, this article rests on the global value chain (GVC) framework. A value chain consists of a series of value-adding tasks performed by firms in the design, making and delivery of a product or service (Gereffi and Fernandez-Stark, 2016). The GVC framework is a holistic approach that takes the entire production network as unit of analysis, enabling us to distinguish the different types of firms operating within each value-adding segment. There is a key difference between lead firms that orchestrate GVCs and suppliers which perform various tasks for them. The former and latter differ in terms of scale and number (the former having higher revenue and market capitalization plus there are far fewer lead firms than suppliers). Relationships are asymmetric in terms of power and profit distribution (Gereffi et al., 2005). The distinction between lead firms and suppliers is crucial to understanding the evolution of European media in the digital era. This research contends that while European businesses perform well as suppliers, European lead firms have been weakened by larger scale competitors and are struggling.

European media's transnational era

At the same time European governments deregulated broadcasting (Lange and Renaud, 1989: 23–56; Regourd, 1999), the European Community's media policy opened up national borders by laying the foundations of a single media market. As a result, fledgling commercial broadcasters were free to seek opportunities away from home and target foreign markets by complementing existing TV offerings (Michallis, 2013). European media firms had three routes to Europe: investing in local free-to-air commercial stations, operating cross-border thematic channels on cable and satellite platforms and, more rarely, running transnational pay-TV services. Firms of various scale ventured abroad, from small businesses specializing in niche genres to media conglomerates controlled by moguls such as Berlusconi, Lagardère, Maxwell and Kirch (Maggiore, 1990: 79–88; Tunstall and Palmer, 1991: 11–44).

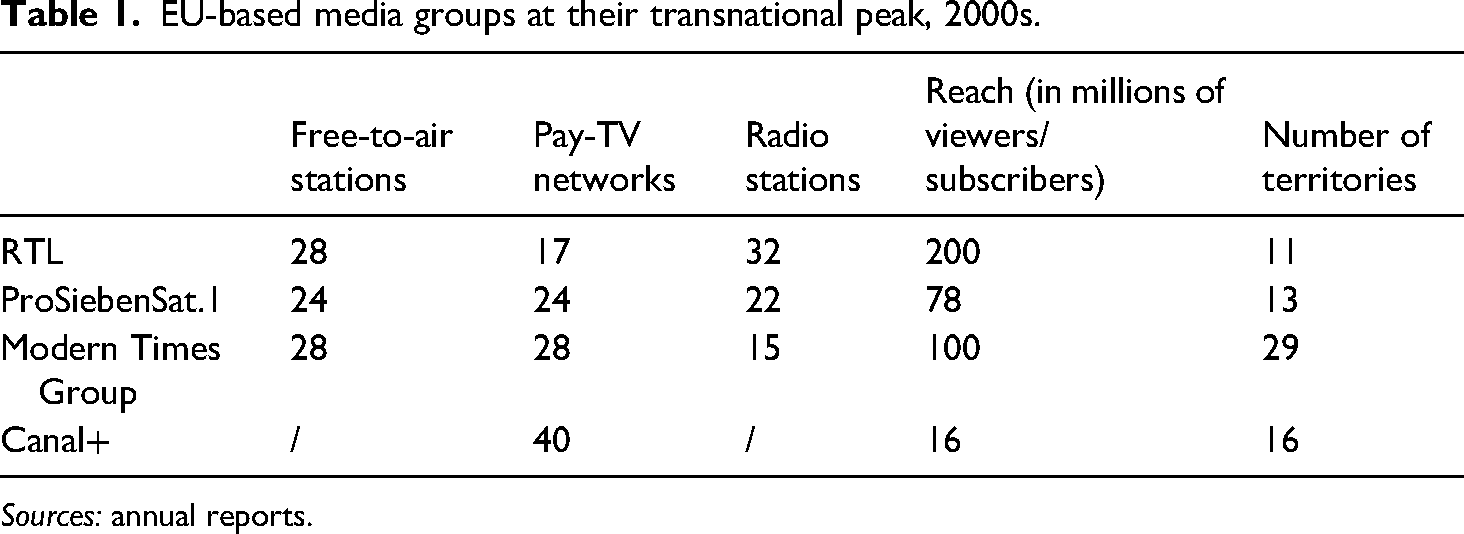

Four European media groups acquired an international reach beyond all others (Table 1). The Compagnie Luxembourgeoise de Télédiffusion (CLT) launched Europe's first commercial channel in 1954. CLT had shown an interest in international expansion due to the small size of its home market but had to wait for the liberalization of the European TV market and the launch of communications satellites to spread its wings (Negrine, 1988; Collins, 1992). By the mid-1990s, CLT operated 13 free-to-air stations and was a major player in TV ad markets in Germany, the Netherlands and Belgium. In 1997 CLT merged with UFA, a Bertelsmann subsidiary, giving it control over 22 TV networks and 20 radio stations in eleven countries. CLT-UFA merged with Pearson Television in 2000, consolidating its position as a major European TV producer (Esser, 2002: 18–19). Trading under the RTL brand, the company was the leading European entertainment network in the 2000s, with a total of 45 free-to-air and pay-TV channels and 32 radio stations. Every day, 200 million viewers were watching RTL channels across 11 countries (RTL, 2009: 174).

EU-based media groups at their transnational peak, 2000s.

Sources: annual reports.

When ProSieben Media and Sat.1 merged in 2000, it became Germany's leading TV corporation. The company's largest shareholder, Kirch Media went bankrupt in 2002 (Iosifidis et al., 2005: 50–2). ProSiebenSat.1 recapitalized and set out its international expansion a few years later, acquiring Scandinavian Broadcasting Systems (SBS) in a US$ 4.4 billion transaction in 2007. SBS was a multinational media company operating in the Netherlands, Scandinavia and Eastern Europe. Following this acquisition, ProSiebenSat.1 became the second largest broadcaster in Europe, controlling 24 free-to-air stations, 24 pay-TV channels and 22 radio stations, reaching 78 million households across 13 countries (ProSiebenSat.1 Group, 2010: 51).

From the 1980s onwards, Stockholm's based Kinnevik dominated free-to-air commercial television in Scandinavia before the Modern Times Group, its subsidiary, became the regional pay-TV champion with the Viasat platform. It expanded its operations to the Baltics, Balkans, Central Europe and Russia. At its peak in the late 2000s, the group controlled 28 Viasat branded pay-TV channels and about 28 free-to-air stations in 29 markets. Modern Times Group was also the largest commercial radio operator in the Nordic region and the Baltic states (MTG, 2009: 30, 35).

France's Canal + launched in 1984 and became Europe's leading pay-TV company in the 1990s. The group expanded its footprint to Belgium, Germany (briefly), Spain, Italy, Benelux, Poland, and Scandinavia (Esser, 2002: 18–19). In 2001, the year following its acquisition by Vivendi, Canal + operated 40 thematic channels in 16 countries, which were distributed via its own pay-TV platforms or those held by third parties (Vivendi Universal, 2002: 20). The same month Vivendi acquired Canal+, it purchased Seagram to form Vivendi-Universal. Canal + became part of the world's third largest media conglomerate (Iosifidis et al., 2005: 52–54).

The 1980s and 1990s was marked by the presence of media moguls such as Berlusconi, Kirch, Lagardère, Maxwell, and Murdoch (Tunstall and Palmer, 1991: 105–205). While these men were renowned and their business interests crossed borders, their international activities remained relatively modest compared to those in their home market. Rupert Murdoch quickly realized the pan-European advertising market was too small to sustain transnational television and dropped two regional networks (Eurosport and Sky Channel) as soon as he launched his pay-TV platform in the UK (Chalaby, 2009: 34). He did, however, acquire a stake in Stream (an Italian pay-TV platform that would subsequently become Sky Italia), and would eventually expand to Germany (Esser, 2002: 19). Silvio Berlusconi showed the most interest in extending his footprint, probably because his stronghold on Italian media was such that there was nothing left to acquire. The magnate was part of the founding consortium that launched France's fifth terrestrial network and also took a stake in Spain's Telecinco (Tunstall and Palmer, 1991: 20, 31).

In any event, EU-based media groups reached their peak in the 2000s, their expansion efforts unravelling thereafter. The demise of Canal + as Europe's leading pay-TV operator came first, beginning soon after the Vivendi-Seagram merger. By 2003, it had scaled down its European operations and exited all foreign markets except Poland. RTL progressively sold its foreign assets the following decade, leaving the UK in 2011, Greece in 2012, Russia in 2013, India (joint venture) in 2014, Belgium and Croatia in 2022, and the Netherlands in 2023. Beyond Germany, the group remains in Hungary and France, where its attempt to merge its operations has been blocked by the French regulator. 1 Burdened by a significant amount of debt, ProSiebenSat.1 sold all its international assets in successive phases, starting with the disposal of its Dutch and Belgian operations in 2011, its Scandinavian portfolio the following year, and Hungarian and Romanian businesses in 2014. The firm subsequently sold its US-based TV content production business to concentrate exclusively on the German-speaking market (Austria, Germany and Switzerland).

The most spectacular fall from grace is Viaplay, the firm that succeeded Modern Times Group. Between November 2021 and November 2024, its market capitalization dropped by 99.6%. During a particularly inauspicious period in 2023, when Viaplay shares lost 72% of their value, the Nordic group replaced its CEO, laid off more than 30% of its workforce, wrote down approximately US$180 million of debt, and was forced to raise new equity. Viaplay abruptly exited most foreign markets, including the UK, the USA and the Baltic region, and set up plans to leave the few in which it still operates (Frackowiak and Solsvik, 2023). Viaplay has since regrouped in order to focus on the Nordic region.

There remain pan-European media groups but as the European Audiovisual Observatory notes, ‘9 out [11] of the most widespread TV and VOD [Video on Demand] groups in Europe are US-based’ (Schneeberger, 2024: 51). The two exceptions are Rakuten (Japan) and Huawei (China). The first European group is Vivendi/Canal + in 12th position (Schneeberger, 2024: 53–5). In addition to Poland, which Canal + never left, the company is re-entering selected European markets as a streaming platform, notably Austria, the Czech Republic, Slovakia and the Netherlands. Altogether, the group counts 6.5 million subscribers in Europe (Vivendi, 2024: 34).

MediaForEurope (MFE) is another European company with a multi-territory footprint. Formerly known as Mediaset, it is controlled by the Berlusconi family's Finninvest Group. In Italy, it operates Mediaset Premium, a pay-TV service, and the largest free-to-air commercial channels. Mediaset España, fully controlled by MFE, is Spain's largest commercial broadcaster. The company, however, is in trouble. ProSieben.Sat1 and RTL saw their market capitalization reduced by an average of 47% in the past five years, but in the case of MFE, it was a drop of 79% (Chalaby, 2025: 118–19).

US-owned TV networks are far more likely to cross borders than their European counterparts. Out of 8621 commercial TV channels operating in Europe, 1156 (23%) are in American hands and 7465 are European (Schneeberger, 2024: 20). Sixty-seven percent of US-owned networks cross borders (775), while the overall percentage of transnational TV channels is 22% (Schneeberger, 2024: 22).

The European TV content production sector

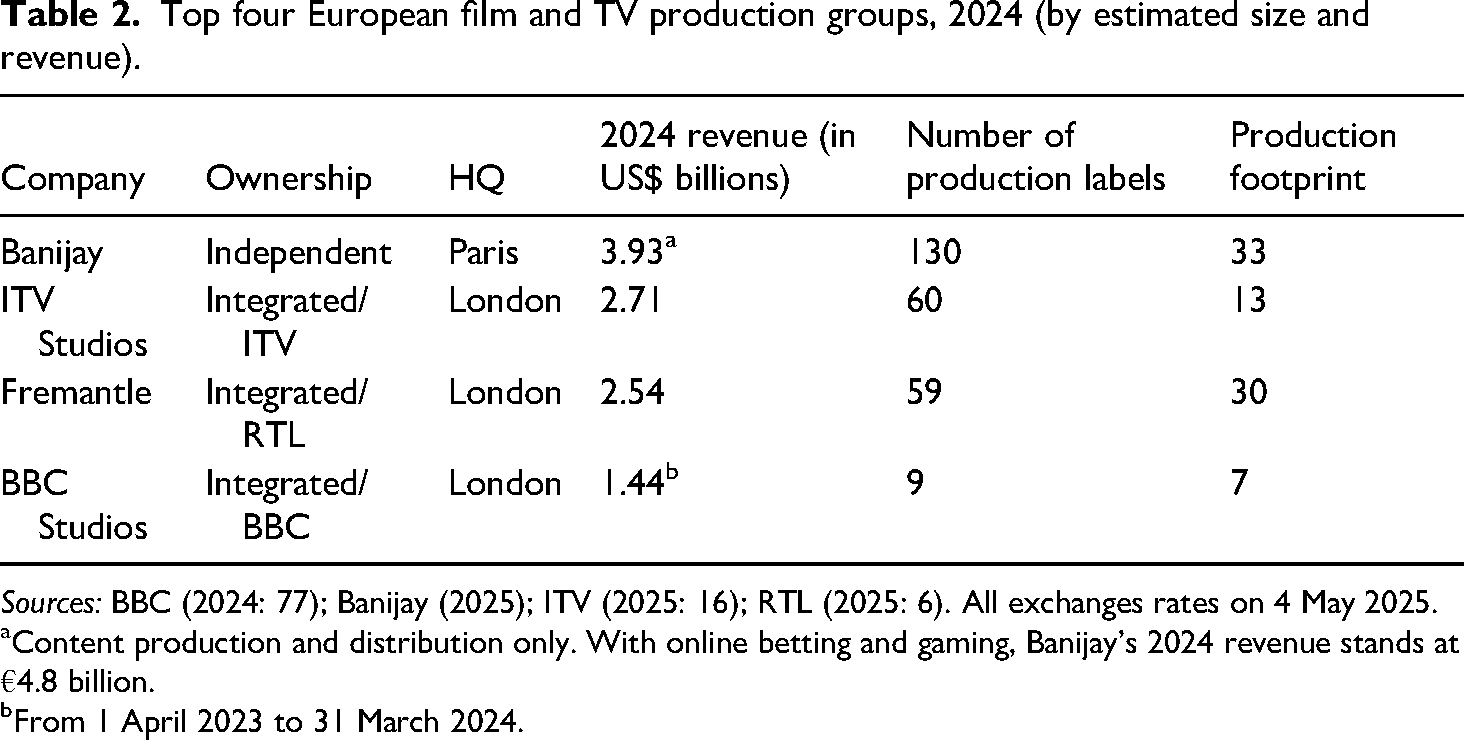

By contrast, the European TV content production sector is regionally integrated, having gone through decades of consolidation. In the 1990s, the initial wave of consolidation was concentrated in the UK and Scandinavia and the trend subsequently spread. By the end of the 2000s about two dozen TV content producers, each controlling tens of labels, managed multiple assets in Europe's key markets (Esser, 2016). Consolidation continued unabated and about ten global film and TV production conglomerates are currently operating in Europe. Over the years, US-based firms such as Warner Bros., Discovery and Liberty Global have made acquisitions in the sector (Esser, 2016: 3595), but the four largest TV content production groups remain in European hands (Table 2). Paris-based Banijay is a super-consolidator, bringing under one banner six firms, notably Shine and Endemol, which themselves went through years of mergers and acquisitions. The company has brought hundreds of labels under one roof, even though the current number is reduced to 130 because of internal consolidation. The other TV production groups, ITV Studios, Fremantle and BBC Studios, are owned by European broadcasters.

Top four European film and TV production groups, 2024 (by estimated size and revenue).

Sources: BBC (2024: 77); Banijay (2025); ITV (2025: 16); RTL (2025: 6). All exchanges rates on 4 May 2025.

Content production and distribution only. With online betting and gaming, Banijay's 2024 revenue stands at €4.8 billion.

From 1 April 2023 to 31 March 2024.

Consolidation in the sector is driven by multiple factors as scale brings a range of benefits. Production is inherently a risky business, being dependent on creativity and the decisions of relatively few commissioners. Acquisitions help a consolidator diversify by covering multiple TV genres and enrich its catalogue with new intellectual property. Large groups support creativity by setting development funds and encouraging cross border conversations among their production labels. Economies of scale are obtained through the centralisation of certain services. Above all, consolidation helps producers mitigate the asymmetrical power relationship between them and lead firms. Streaming giants typically operate on a cost-plus basis, offering upfront payment in exchange of the exclusive global rights for an indefinite amount of time. Larger producers have the resources to soften this position and negotiate a better deal, such as the reversion of some rights after a time period (Chalaby, 2023: 105–113, 147–151).

While transnational TV production groups are a credit to European integration, European nation-states are unequally represented in the sector. Despite Brexit, the UK remains Europe's largest production centre, where most of these groups are based. With Spain, the UK is where US-based streaming services concentrate their investment and the two countries account for 53% of their spending in regional content (Fontaine, 2024: 18).

There is, however, a caveat. TV producers, while essential to the TV value chain, are not part of its dominant segment. They act as suppliers to lead firms which govern this chain. When producers deliver a global hit for a streaming giant, they do not get a financial reward. Typically, the producers of Adolescence, which became the third most-watched Netflix show in April 2025, did not receive a bonus from the commissioning firm. They get a margin on the making the show, while the series may be worth hundreds of millions of dollars in extra subscription revenue to the streamer (McVay, interview 2025).

Operating in the global SVoD market requires large investment but the rewards for lead firms are far greater than what suppliers will ever get. While Banijay, which is exceptionally large for a producer, announced US$3.8 billion of revenue for its content division in 2024, Netflix reported US$39.0 billion in revenue for the same period (Banijay, 2025; Netflix, 2025: 21). The gap is even wider in terms of market capitalization which, at the time of writing, stood at US$4.3 billion for Banijay and US$480 billion for Netflix. As far as lead firms are concerned, the era of pan-European media has come and gone for EU-based media groups. Facing financial difficulties, they have retreated from foreign markets to concentrate on their domestic operations. The next section analyses the causes of this attrition.

Analysis

The reasons that lead a business into financial difficulty are always specific to that singular company. Management may be too conservative in their approach, make risky investments, misjudge market trends or overvalue the firm's assets. For instance, when Viaplay embraced streaming, the Nordic firm expanded to the UK and the USA, two of the most competitive media markets. Failure to get a return on investment in these two countries contributed to the firm's financial collapse in 2023 (Thomson, 2023). Nonetheless, several trends conspire against European broadcasters, including a challenging advertising market, the rise of US-based streaming giants and a European legislative framework that is not offering them any protection. This section analyses each factor in turn.

A challenging TV advertising market

The TV ad market has grown from US$26 billion to US$29.3 billion in Western Europe between 2000 and 2024 (Statista, 2024). It equates to an increase of 12.8% over 25 years, or a yearly growth rate of approximately 0.5%, well below the average inflation rate of the Euro area for the same period which stands at 2.1% (European Central Bank, 2025).

This evolution is reflected in the progression of European media groups’ annual revenue. ProSiebenSat.1 earned €3.1 billion in 2008 and €3.9 in 2024, and RTL earned €5.8 billion in 2008 and €6.3 billion in 2024 (ProSiebenSat.1 Group, 2009: 2; ProSiebenSat.1 Media, 2025: 2; RTL, 2009: 76; RTL, 2025: 7). This represents an increase of 25.8% for ProSiebenSat.1 and 8.6% for RTL over 17 years, a yearly average growth rate of approximately 1.5% for the former and 0.5% for the latter, both below the average inflation rate of 2.1% for the Euro area during the same period (European Central Bank, 2025).

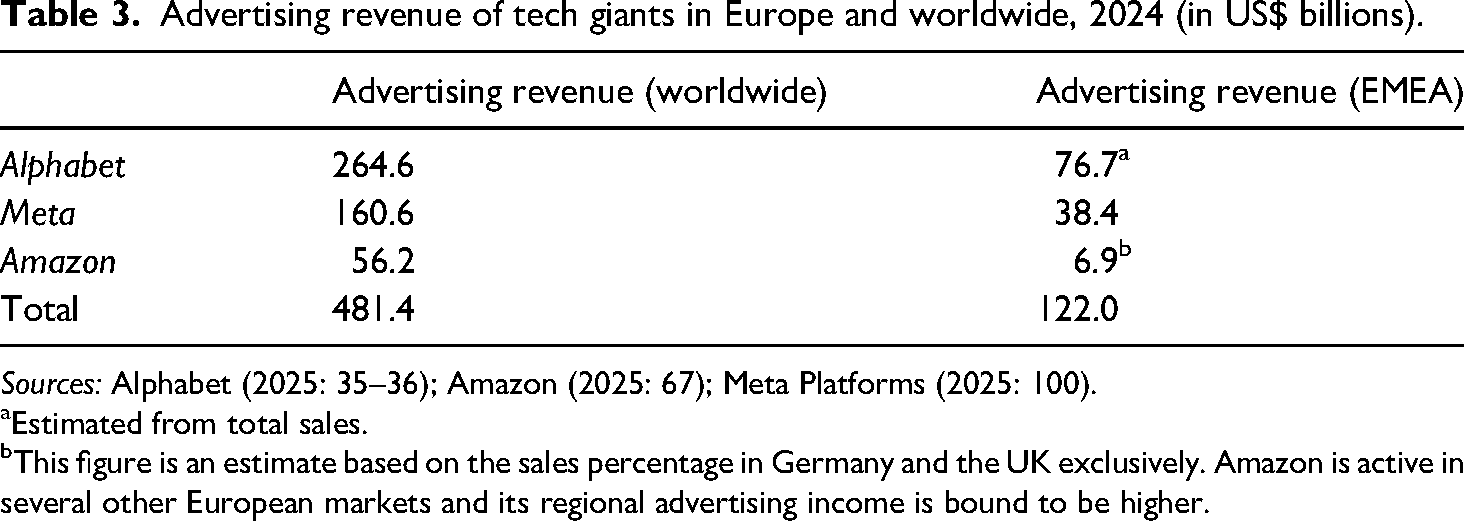

By way of contrast, the digital ad market has grown by a factor of 14 in 29 European markets since 2006, to reach an estimated US$96 billion in 2023 (IAB Europe, 2024: 16). Advertisers are following customers online, with the benefit of having various means of directly targeting them. While the online advertising market is growing, it is highly concentrated, with the lion's share in the tech giants’ hands. Alphabet, Amazon and Meta collected US$481 billion in advertising revenue worldwide in 2024, of which US$122 billion in Europe (Table 3).

Advertising revenue of tech giants in Europe and worldwide, 2024 (in US$ billions).

Sources: Alphabet (2025: 35–36); Amazon (2025: 67); Meta Platforms (2025: 100).

Estimated from total sales.

This figure is an estimate based on the sales percentage in Germany and the UK exclusively. Amazon is active in several other European markets and its regional advertising income is bound to be higher.

European broadcasters are actively chasing digital revenue but progress is modest. In 2024, it represented 16.1% of ITV's total income (£556 million of £3488 million, ITV, 2025: 16), and digital advertising represented 6.5% of RTL's total income (€405 million of €6254 million, RTL, 2025: 32).

European broadcasters are operating in a segment of the online ad market, streaming, which has just become more competitive. In addition to Alphabet's YouTube, which scooped US$36.1 billion in advertising revenue worldwide in 2024 (Alphabet, 2025: 36), 2 large Subscription Video on Demand (SVoD) services have now entered the market: Disney + and Netflix launched ad-supported subscription plans in late 2022 and Amazon Prime Video followed suit in 2024.

Competition from streaming giants

Streaming is a game best played at scale for two reasons. European broadcasters primarily use a media delivery infrastructure that is national in scope, even though they receive programmes from the European Broadcasting Union and expand their reach via communications satellites. If they have any type of public service obligation, they must keep a terrestrial mode of transmission to ensure universal reach (e.g., Ofcom, 2024). Streamers, some of them being cloud-native, deliver content over the internet exclusively using Content Delivery Networks (CDN) (Ali et al., 2025). The most common configuration for streaming video delivery is hybrid, in the sense that streamers primarily use outsourced delivery services which they complement with their own proprietary CDN. The bulk of the workload is typically contracted out to cloud providers such as Amazon Web Services or Microsoft Azure, which are combined with edge specialists such as Akamai or Equinix. These providers own infrastructure and offer global services, and thus economies of scale are at play in internet protocol-based television delivery. As the number of connections increase, the average cost per connected user decreases irrespective of geography. Further, the fixed costs of developing streaming technology for an online platform remain the same regardless of the number of viewers/subscribers.

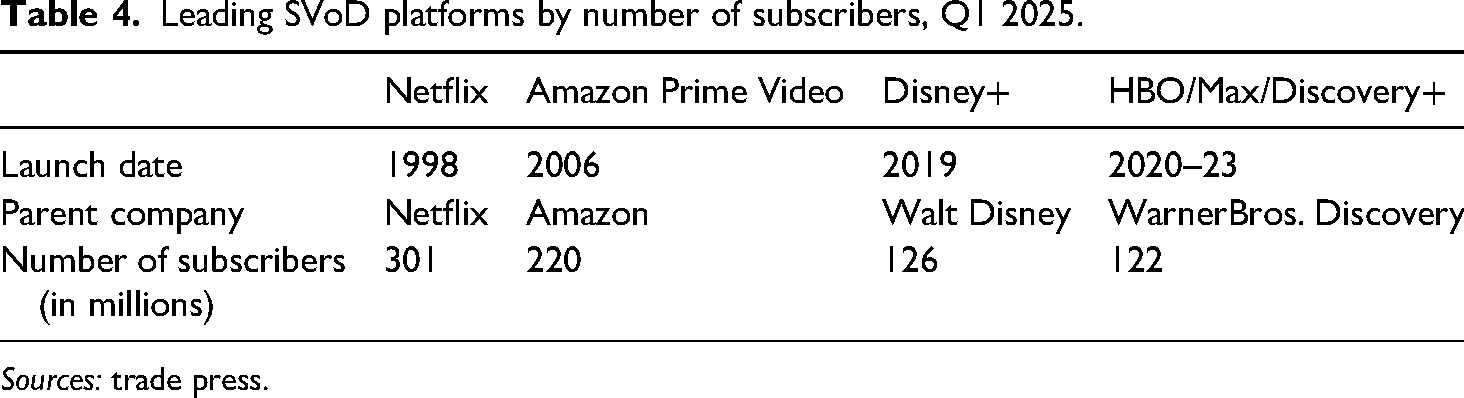

Streaming giants operate in the platform economy, where network effects come into play (Eisenmann et al., 2006; Gawer, 2014: 1240–1241; Stallkamp and Schotter, 2021: 69–73). In essence, the value of a streaming platform increases as more people use it. The mechanism is particularly visible in the case of video-sharing platforms, which bring several markets together (advertisers, content providers and users). Market sides reinforce each other, users patronizing the platform with most content, advertisers and content providers targeting and posting on the most frequented platforms. Network effects explain why two platforms, YouTube and TikTok, control the video-sharing market worldwide (Dean, 2024). The SVoD market is equally dominated by a handful of platforms with 100 million plus subscribers (Table 4).

Leading SVoD platforms by number of subscribers, Q1 2025.

Sources: trade press.

Three of these services, Netflix, Amazon Prime Video and Disney+, account for 85% of viewing time across Europe (Grece and Tran 2023: 14). The reason behind this concentration is that network effects also apply to the SVoD space, albeit in a more oblique way. Logically, the platforms with the most subscribers have the largest revenue, enabling them to invest in new content and, in turn, retain and attract more subscribers. However, even global platforms operate in a series of distinct markets and a large subscriber base in country A does not guarantee the same in country B. Thus, an SVoD platform must find a way of mutually reinforcing the multiple markets within which it operates for network effects to occur (Chalaby, 2025: 116–117). It is Netflix that best operationalises this strategy, as the service has not only 301 million subscribers worldwide but dominates the SVoD space in all European markets in which it operates.

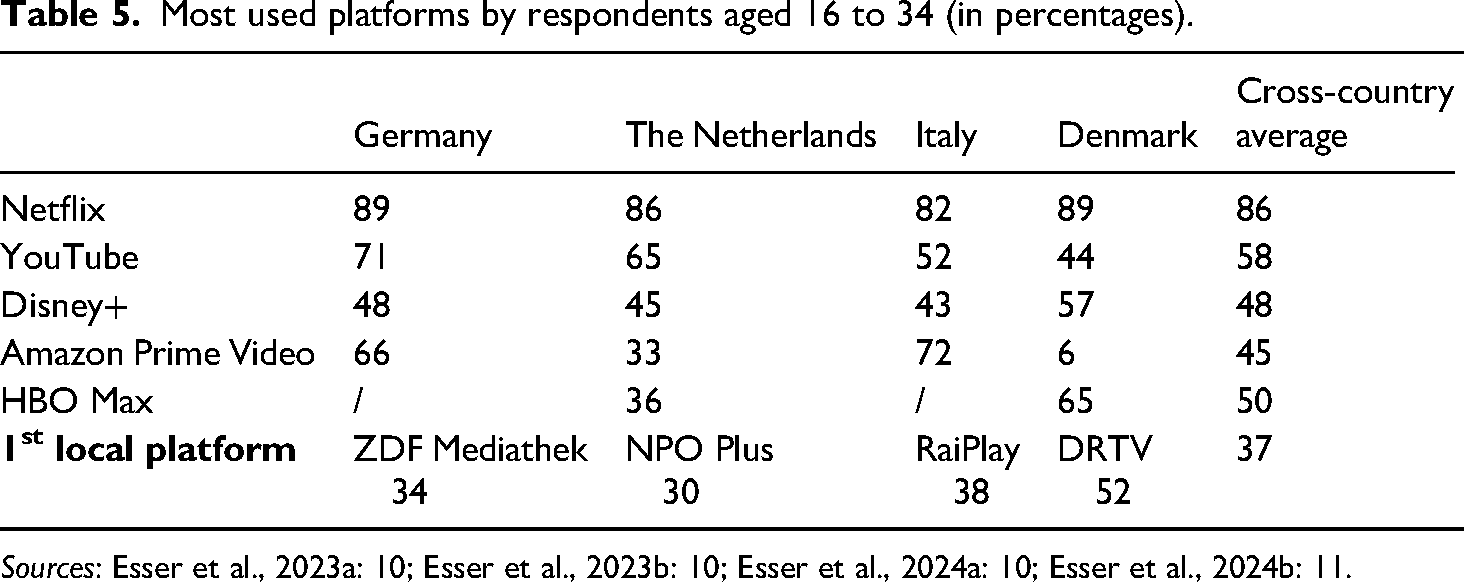

For instance, Netflix emerges as the clear leader in a recent large-scale audience survey in four European countries. The online service is the most used service among 1813 respondents aged 16 to 34, followed by YouTube and Disney+, in Germany, Italy and the Netherlands. In Denmark, Amazon Prime Video is substituted by HBO Max. The best placed local providers are DRTV in 4th rank in Denmark, RaiPlay in 5th position in Italy, ZDF Mediathek in 6th spot in Germany, and NPO Plus in 9th rank in the Netherlands (Table 5).

Most used platforms by respondents aged 16 to 34 (in percentages).

Sources: Esser et al., 2023a: 10; Esser et al., 2023b: 10; Esser et al., 2024a: 10; Esser et al., 2024b: 11.

Transnational network effects occur when stories primarily aimed at viewers in territory A also appeal to those in territory B, and vice versa. Thus, an increase in subscribers in any country is mutually beneficial as it translates into additional content potentially relevant to viewers in both territories. Additional Korean subscribers mean more local content but as Korean shows are popular worldwide, they benefit users in other territories (Stallkamp and Schotter, 2021: 64–73). Netflix is now investing more overseas (US$7.9 billion) than in its home (U.S.) market (US$7.5 billion) as it discovered that non-English content travels well (Aquilina, 2024). The online service executives have often spoken publicly about the importance of content mobility, as recently illustrated by Ted Sarandos, Netflix co-CEO, at the 2024 Royal Television Society Convention:

When we greenlight a series or movie in the UK, or Mexico or Korea, we do it because we think our British, our Mexican and our Korean audiences will love it. And you know what? When you make something authentic that appeals to certain people in a certain place, it tends to appeal to a lot of other people in a lot of other places, too (Sarandos, 2024).

Netflix never competes with local platforms on a level-playing field because it leverages its entire library in the markets it ventures into. A certain amount of local content is needed to compete in any territory, but the streamer brings to the table a large and diverse library that works transnationally. Eventually growth slows down and numbers can decline, but the gap remains wide between these market leaders and any European streaming platform.

Legislative framework

The European Union has long engaged with media industries and a GVC analysis reveals that the impact of its policies on segments of the streaming chain varies. Only the film & TV content production sector has been offered support. By contrast, European policies have exacerbated competition for local lead firms by opening wide the doors of the European market to US-based broadcasters and streamers.

The European Commission's (EC) interest in television began in the 1980s. The Television Without Frontiers Green Paper was published in 1984 and was followed by a draft directive two years later. This led to a lobbying battle between the UK-led camp that sought to loosen media regulations in favour of market forces, and a protectionist-minded group steered by France (Collins, 1994: 53–80). The Television Without Frontiers Directive (TWFD, Directive 89/552/EEC) was approved in October 1989 and came into force in 1991.

While the real intent of the EC has long been the object of a debate, there is little doubt that its initial foray into media policy had strong liberal flavour (Burgelman and Pauwels, 1992). The Council of Europe had proposed a draft convention in 1987 that was far more restrictive and protectionist in scope, but a combination of commercial lobbying and EU politics limited its influence (Collins, 1994: 28–40). While TWFD made concessions to the protectionist camp and included some of the Council's clauses the Directive fell in line with the objectives of the 1957 Treaty of Rome and the 1986 Single European Act (Collins, 1994: 69). Both treaties aimed to form a European-wide single market, which became reality in 1993 with the quadruple freedom of movement for people, goods, services and money.

TWFD was ground-breaking because it was the first supranational agreement to legalise transfrontier television. The Directive required all 12 Member States of the European Community to ensure freedom of reception of television broadcasts from other Member States. They could suspend a channel that infringed upon the provisions that pertain to protection of minors and prohibition of hate speech. As a concession to the protectionist argument, the Directive stipulated that broadcasters had to reserve ‘a majority proportion of their transmission time’ for European works (Directive 89/552/EEC). However, it added ‘where practicable and by appropriate means’, which meant that in practice US-based broadcasters never had to worry about these quotas (Directive 89/552/EEC). TWFD participated in the single market project by aiming to form a pan-European TV space which combined transnational distribution of content and scaled-up broadcasters able to operate across borders (Broughton Micova et al., 2018: 229).

TWFD was revised in 1997 and the new Directive confirmed the country of origin as the place of jurisdiction while clarifying the criteria of establishment. This clause, however, would become a major bone of contention during the consultation period ahead of the next revision. Protectionist Member States demanded more control over channels broadcasting over their territory and contested the principle of the country of origin as sole place of jurisdiction. Rules were tightened to prevent flagrant abuse but the principle remained. During the consultation process, it was agreed to include non-linear online services within the remit of the Directive. After years of negotiations, the renamed Audiovisual Media Services Directive (AVMSD) was approved by the European Parliament and Council in December 2007. The text, which still referred to ‘television broadcasting’ in its sub-heading (Directive 2007/65/EC), was amended by another Directive that came into force in March 2010, which this time made reference to audiovisual media services (Directive 2010/13/EU).

The next update did not come long after, made necessary by the growth of user-generated content and rapidly changing market realities. The succeeding AVMSD was approved by the European Parliament and Council in November 2018 (Directive 2018/1808). It is the text that is currently in force, and at the time of writing the process of consultation for the next update is well under way. The 2018 Directive reinforces these clauses against incitement of hatred, terrorism and violence and provisions for the safeguarding of minors against harmful content. It retains the core principle of the country of origin as sole place of jurisdiction. However, the main purpose of the European lawmakers was to extend the scope of obligations placed on VoD services and video-sharing platforms.

The preceding Directive remained more specific about the obligations faced by broadcasters than streamers. While Article 17 required broadcasters to ‘reserve at least 10% of their transmission time’ and ‘10% of their programming budget for European works’, no quota was specified among the provisions applicable to VoD services (Directive 2010/13/EU). Article 13 simply requested Member States to ensure that VoD platforms ‘promote, where practicable and by appropriate means, the production of and access to European works’ (Directive 2010/13/EU). As with previous versions, the inclusion of ‘where practicable’ considerably lightened the burden of obligations for online services (Directive 2010/13/EU).

By contrast, AVMSD 2018 is more forceful, including all media providers in its dispositions and being unequivocal in its obligations on VoD services. Online media providers must ‘secure at least a 30% share of European works in their catalogues’ and ensure their prominence (Directive 2018/1808, Article 13). A Member State whose audience is targeted by a VoD service established in another Member State can require a financial contribution to national funds in order to support local content production (Directive 2018/1808, Article 13). Further, Member States remain free to add provisions to those listed by the Directive. Within the limits of country-of-origin principle, thirteen Member States have subjected VoD services to additional regulations, and eight have introduced sub-quotas for linguistically specific content (Belgium, France, Hungary, Italy, Poland, Portugal, Slovenia and Spain) (European Commission, 2024; Raynaud and Naudascher, 2024: 28).

France has imposed the most stringent quotas. Aligning the obligations to VoD platforms with those already in place for legacy operators, French authorities require 60% of European works and 40% of French-language content in VoD catalogues (Raynaud and Naudascher, 2024: 28). The Italian government maintains the 30% quota for European works but stipulates that half of this must be produced in Italian (Raynaud and Naudascher, 2024: 28).

VoD platforms benefit from single market rules and only quotas imposed by the country of origin apply (Raynaud and Naudascher, 2024: 28). Netflix and Warner Bros. Discovery, whose European headquarters are in the Netherlands, are answerable to the Dutch government, which has not imposed further obligations beyond AVMSD 2018. There is, however, one derogation to the country-of-origin principle, which is the financial contribution to national funds for local production. Flanders, France, Germany and Italy are among countries that request non-domestic VoD platforms to support local production, a contribution dubbed the ‘Netflix tax’ (Kostovska et al., 2020). In France, for instance, foreign platforms must pay 2% of their national revenue to the Centre National du Cinéma (Kostovska et al., 2020: 429). 3

Limits and unintended consequences of the Eu legal framework

Successive versions of the TWFD/AVMSD have been in place for 35 years and this section attempts to assess the impact of the European audiovisual media policy from a GVC perspective. While scholarly literature pertinently focuses on most recent policy developments, there is a risk of losing sight of European media regulations’ primary purpose. The fundamental objective of TWFD was to create a multinational market within which media companies – preferably European ‒ operate seamlessly. The country-of-origin principle simplified cross-border operations by providing businesses one place of jurisdiction for their cross-border operations. The question is: who benefited the most? When TWFD was first put forward, the hope was for European lead firms to expand across borders and acquire the necessary scale and scope to compete against US-based giants.

TWFD/AVMSD duly created a pan-European media market and at the peak of the transnational period of broadcasting, it looked like the EU's bet would come good. These media firms were benefitting from the single market and beginning to form an integrated pan-European TV industry. In the 2000s and 2010s, however, they lost their footing and progressively retreated to domestic markets. Today, Europe's main transnational operators are US-based firms. Throughout television's broadcasting era, national broadcasters, public or private, remained the primary destination for news and entertainment in their respective ecosystems. As the industry shifts towards streaming this is no longer the case, and US-based online platforms have become Europe's primary source of entertainment. Young Europeans prefer global platforms for longform content. Not only do streaming giants dominate the European home entertainment market but they are market leaders in all European countries (above).

Faced with this new reality, some Member States plan to reinforce AVMSD's protectionist measures. As part of the process of consultation for the next AVMSD update, two French officials suggest that the country-of-origin principle should be curtailed and Member States be given more power to hold streaming giants accountable, and that the quota of European works should be raised to 50%. Further, British, Swiss, Turkish and Ukrainian programmes should no longer qualify as European Works (Raynaud and Naudascher, 2024: 37–50). 4

If adopted these measures would confer new constraints for global streamers, although their efficacy is doubtful as they are difficult to monitor and European authorities rely on platforms to self-report evidence of compliance (Idiz et al., 2021: 430–431). Also reports are submitted on an annual basis, thus non-EU content can be rotated or removed before the deadline, and catalogues simply cut back to comply (Lotz, 2019). French, German and Italian cinema has benefitted from governmental funding for decades, yet it performs poorly internationally (Kostovska et al., 2020: 427). While French films have a healthy market share of domestic cinema admissions, only 9% of their ‘total cinema admissions were made in non-European markets’ (Kostovska et al., 2020: 430). Quotas and subsidies shield local film producers from market forces but may prevent them from stepping outside the cocoon of auteurist and metropolitan cinema (Vanderschelden, 2007).

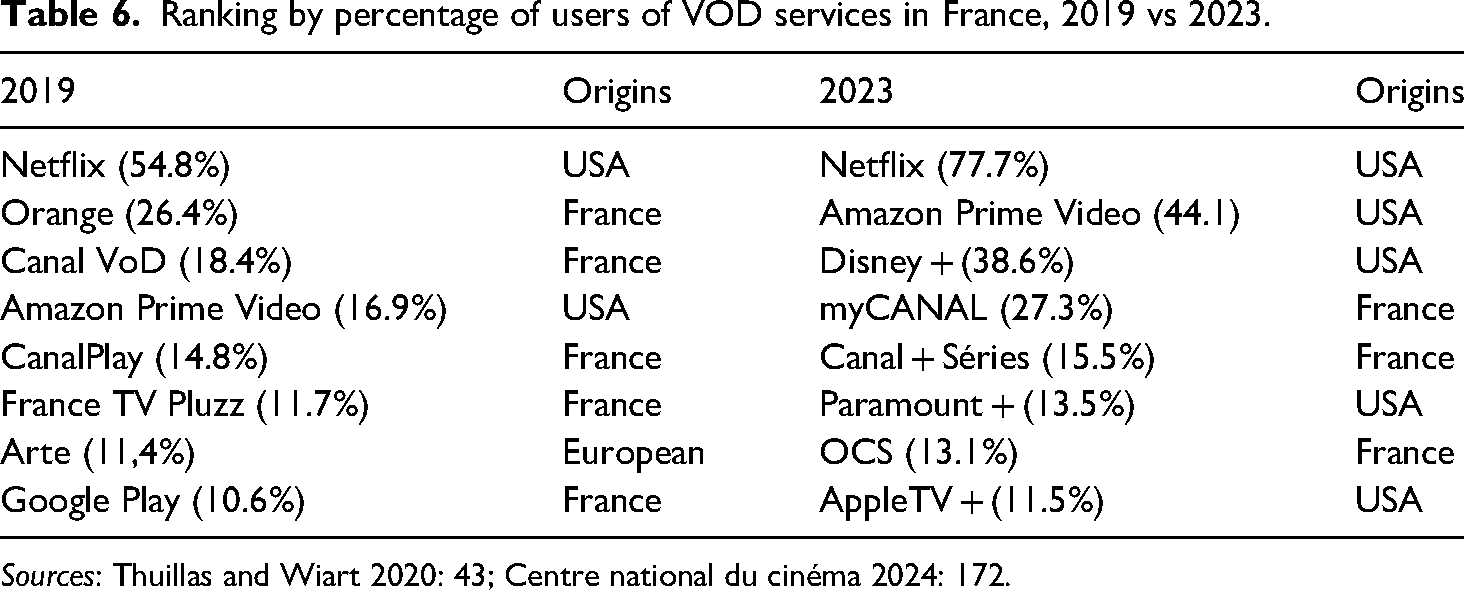

By law, these measures must remain non-discriminatory between domestic and non-domestic platforms and thus will not change market realities. Quotas provide support for the European content production sector but will not help local platforms claw back market share from streaming giants. In France, despite stringent quotas and demands for financial contribution to local production funds, local VoD platforms have lost considerable ground to streaming giants in recent years. Reflecting the findings of the aforementioned four-country study, Table 6 shows that only two of the top eight VoD services operating in France were of American origin in 2019, while in 2024 five of the top eight VoD services operating in France originate from the USA, including the leading three. France, whose resistance to Hollywood goes back to the 1930s, is unable to stem the US tide despite sustained policy efforts.

Ranking by percentage of users of VOD services in France, 2019 vs 2023.

Sources: Thuillas and Wiart 2020: 43; Centre national du cinéma 2024: 172.

There is a plethora of local streaming platforms in Europe and the belief they can push back against streaming giants is rarely justified, as the example above demonstrates (Schneeberger, 2019). It may be possible in a market with large lead firms and a strong TV content production base. The UK is the only country that fulfills these conditions in Europe, and BBC iPlayer was the fastest growing VoD platform in 2024 (Clover, 2024). Operating in the streaming market necessitates huge investment and small operators struggle to keep up with streaming giants. 5

Europeans subscribe to an average of 3.2 VoD services, and either Amazon Prime Video, Disney + or Netflix figure in their shopping basket, and often all three (Tongue, 2024). The reality is that streaming giants have the largest and most attractive catalogues and all data points to strong market concentration. This fundamental market reality is not currently addressed by EU media policy.

Conclusion

European authorities have supported the film and TV production sector for years but they may need to come up with new measures to protect European lead firms and particularly public service media. None of the streaming giants are European and while the EU requires investment in local content, they remain in control of whom they work with and the nature of programmes they commission. Netflix, for instance, invests in local stories with a view to making them travel, which means it does not necessarily select those that a local media service would choose. Further, the nature and structure of these stories may be altered as they are adapted to a transnational audience. Netflix commissioners intervene during the production process making narratives amenable to its subscribers across borders (Idiz, 2024: 2140–2141).

In its pursuit of cultural diversity, EU policy makers aim to promote a kaleidoscope of programmes reflecting national cultures rather than deterritorialized content that denatures cultural specificity (Vanderschelden, 2007: 47). In addition, Europe has no control over ownership of these platforms and, depending on whose hands they fall into, this may prove an issue in the future. Public service media are instruments of national self-representation that reflect a country's idiosyncrasies, strengths and weaknesses better than any other platform. It is an ability and a privilege Europe must retain.

Without its own large platforms, Europe has no power of projection and is increasingly dependent on US-based streaming services to export its culture. This is why French President Emmanuel Macron was reduced to begging Netflix not to relocate Emily in Paris to Rome: ‘We will fight hard’, he told Variety ‘and we will ask them to remain in Paris! ‘Emily in Paris’ in Rome doesn‘t make sense’ (in Keslassy, 2024).

Europe's performance in the streaming market reflects its lack of clout in the digital economy. Its leading streaming platforms are all US-based and so are cloud operators. As the Draghi report notes, ‘the largest European cloud operator accounts for just 2% of the EU market’ (Draghi, 2024: 24). Europe stands well behind the USA in artificial intelligence (AI) investments. In 2024, Amazon, Google, Meta and Microsoft invested a combined US$105 billion on new AI capital expenditure, on top of operating costs (Cappella, 2025).

The Draghi report makes several recommendations, including simplifying overbearing and at times contradictory regulations, strengthening the single market, and investing in connectivity and digital technologies (Draghi, 2024: 30, 63, 67). As far as streaming goes, the current problem for Europe is that its ‘external vulnerabilities’ in the digital economy (Draghi, 2024: 56) are translating into cultural dependency.