Abstract

High-growth firms are at the forefront of academic research and policymaking in support of job creation. This article provides an overview of what we do and do not know about these firms. It is based on a systematic review of 159 papers published in higher-ranked academic journals from 1985 to 2022, supplemented by key papers published subsequently. The growing volume of research is channelled along what are becoming well-worn paths. It has entered a phase of diminishing returns before reaching any consensus on two pivotal questions: What are the antecedents of a high-growth episode, and why are these so short-lived? There is also growing scepticism among scholars on the feasibility and merit of having high-growth firms as a policy focus. It concludes by assessing the field and suggesting new research approaches and methods.

Introduction

This review develops an overview of the burgeoning research literature on the characteristics and impact of high-growth firms (HGFs). The extant literature has grown considerably since the Henrekson and Johansson (2010) meta-analytic review of job creators and the rate of increase is not slowing. This review is also timely as HGFs remain a dominant focus of entrepreneurship policy at the firm and regional levels – arguably at the expense of more systemic initiatives – when scholarly support for this HGF focus is waning. These firms came to prominence when David Birch observed the disproportionate contribution of ‘gazelles’ – smaller firms operating for no more than 5 years – to net U.S. job creation, findings that have since been confirmed elsewhere and in periods of economic growth and decline (Anyadike-Danes and Hart, 2009; Birch, 1979; Haltiwanger et al., 2013; Mason et al., 2015; NESTA, 2009). Birch’s findings added to a developing interest in the role of small firms stimulated, at least in the United Kingdom, by the publication of the Bolton Report (1971). Bolton does compare samples of ‘fast and slow growers’ but did not make specific policy recommendations on HGFs, presuming such performance to be self-rewarding (Bolton Report, 1971: 17–19). Birch himself expressed scepticism about his gazelles being a valuable instrument of public policy; yet, there has been a sustained focus on such firms. The field originated in large-scale numerical studies and has largely continued without the concomitant underpinning of qualitative theory-building approaches. Hence, there continues to be a lack of theoretical development in this body of work (Dobbs and Hamilton, 2007; Starbuck, 1965; Vinnell and Hamilton, 1999).

This article offers an overview of what we do, and do not know, about HGFs with a systematic review of papers published in higher-ranked academic journals from 1985 to 2022, supplemented by key papers published subsequently. The article is structured around the themes identified: counting and the share of HGFs; identifying the main drivers of HGFs; the nature of high growth, its persistence and repetition; the impacts of high growth, both internal on owners, managers and employees, and external on other local firms; and the continued policy focus on HGFs, even when scholarly support is waning. We conclude that while the literature on HGFs continues unabated, it requires theoretical development as it enters a phase of diminishing returns before having reached consensus on two key questions: What are the antecedents of a high-growth episode, and why are these so short-lived? We conclude with suggestions for new research approaches and methods.

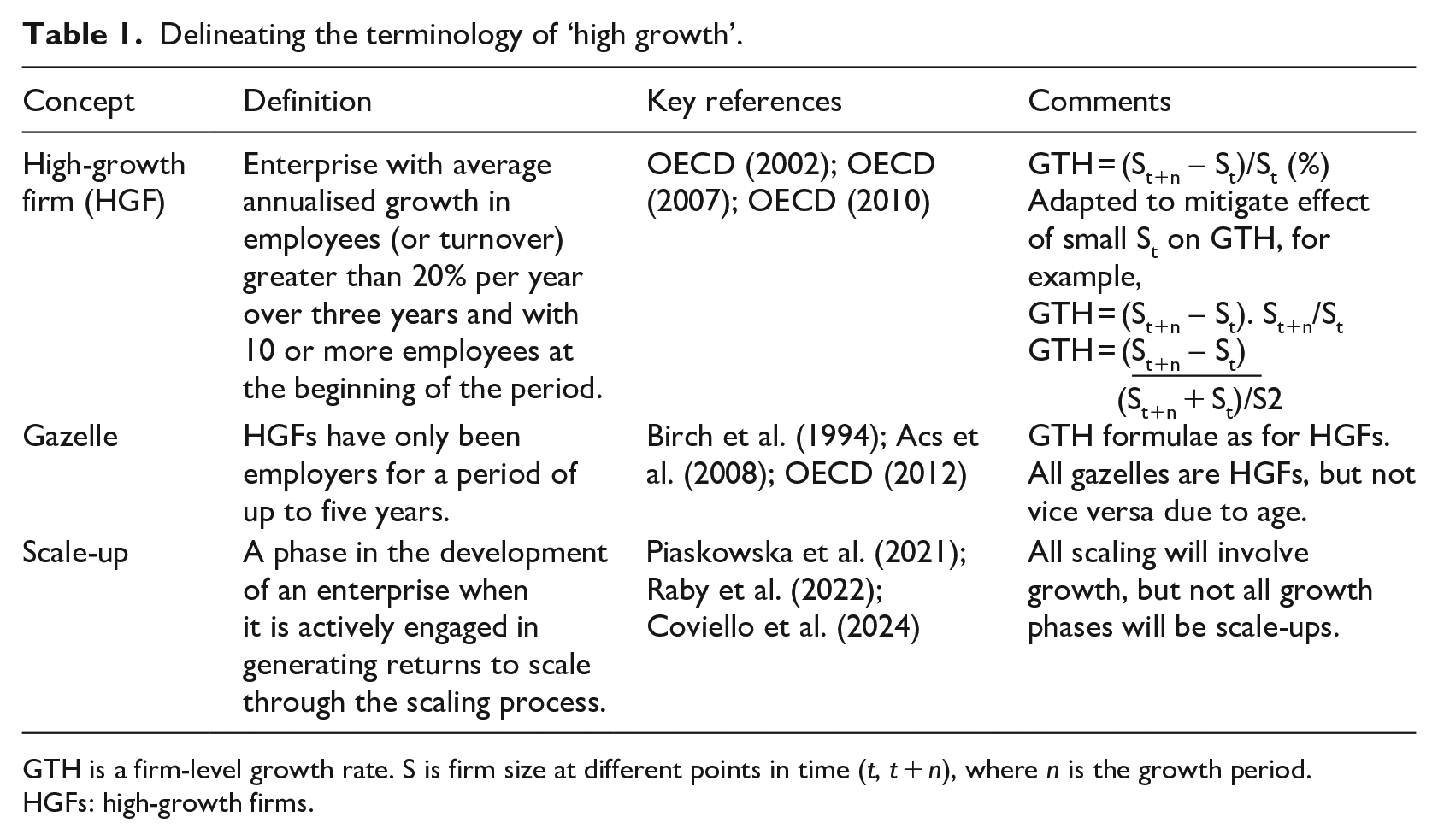

Definitional matters

Early analyses used the INC 100 or 500 listings of the fastest growers in the United States to construct comparative research samples of fast and slow growers (Baker et al., 1993; Feeser and Willard, 1990; Ginn and Sexton, 1990; Willard et al., 1992). These early studies included listed corporations and were not limited to new or small firms. The increased focus on the growth performance of younger and smaller firms stems from the first large-scale attempts to discover who creates jobs, hence gazelles (Birch, 1981; Birch et al., 1994). Once the importance of gazelle-like behaviour was recognised, counting them became a priority: scholars and policymakers wanted to know how many HGFs their industry or region had, a line of inquiry hampered by a lack of an accepted definition of what constituted an HGF. This definitional issue is ongoing, notwithstanding the efforts of the OECD (2002, 2007, 2010) to provide a standard definition.

One issue with the original Birch analysis is that the growth rate of the smallest firms is inevitably over-stated by the smallness of the growth rate denominator. It was also conceded that older firms could still exhibit gazelle-like growth. These issues were addressed in the OECD (2007) definition of a high-growth enterprise. Although analogous to that of a ‘gazelle’, this OECD definition removes the age criterion (5 years), and to prevent arithmetic bias due to the host of tiny businesses, it ignores all firms with fewer than 10 employees in the base year. Annual sales growth was then accepted as a legitimate numeraire, alongside or instead of employment numbers, which reflect growth in expenses and will understate the growth of more capital-intensive businesses. The need to delineate the terminology has been heightened as the domain of ‘high growth’ now stretches to include scale-ups (Coutu et al., 2014; Jansen et al., 2023; Piaskowska et al., 2021). Indeed, Coutu et al.’s (2014) report begins by simply taking the OECD (2007) definition of an HGF and applying it to a ‘scale-up’, confounding the large volume of prior research on HGFs that had little, if any bearing, on the scaling process. We support further research on scaling while concurring with Coviello et al. (2024) that scholars should not conflate scaling with high growth: scaling involves growth in output in pursuit of returns to scale, but the scale-up phase need not involve high or even continuous growth; Table 1 sets out the terminology adopted here.

Delineating the terminology of ‘high growth’.

GTH is a firm-level growth rate. S is firm size at different points in time (t, t + n), where n is the growth period.

HGFs: high-growth firms.

While Birch’s findings have been reviewed and challenged (Acs et al., 2008; Davis et al., 1996), the focus has remained on smaller firms. Most recent studies of HGFs have adopted the OECD (2007) definition, which attempts to control for initial size by excluding all firms with fewer than 10 employees. Daunfeldt et al. (2016) point out that adopting the strict OECD (2007) definition would have excluded 95% of all the firms in his Swedish study. Hence, criticism of the OECD definition has led to various adaptations of the percentage growth rate formula to mitigate the effect of small initial size on growth rate – see examples in Table 1. Adapting the numerical definition of an HGF must be done carefully, as different formulas will select different sets of HGFs with different characteristics (Coad et al., 2014a; Hölzl and Janger, 2013). It is also the case that, as more extensive databases become available, scholars can statistically identify HGFs as those individual firms in the top percentiles of growth rate distributions and measure their growth over different intervals (Coad et al., 2017; Decker et al., 2016; Esteve-Pérez et al., 2022).

Methodology

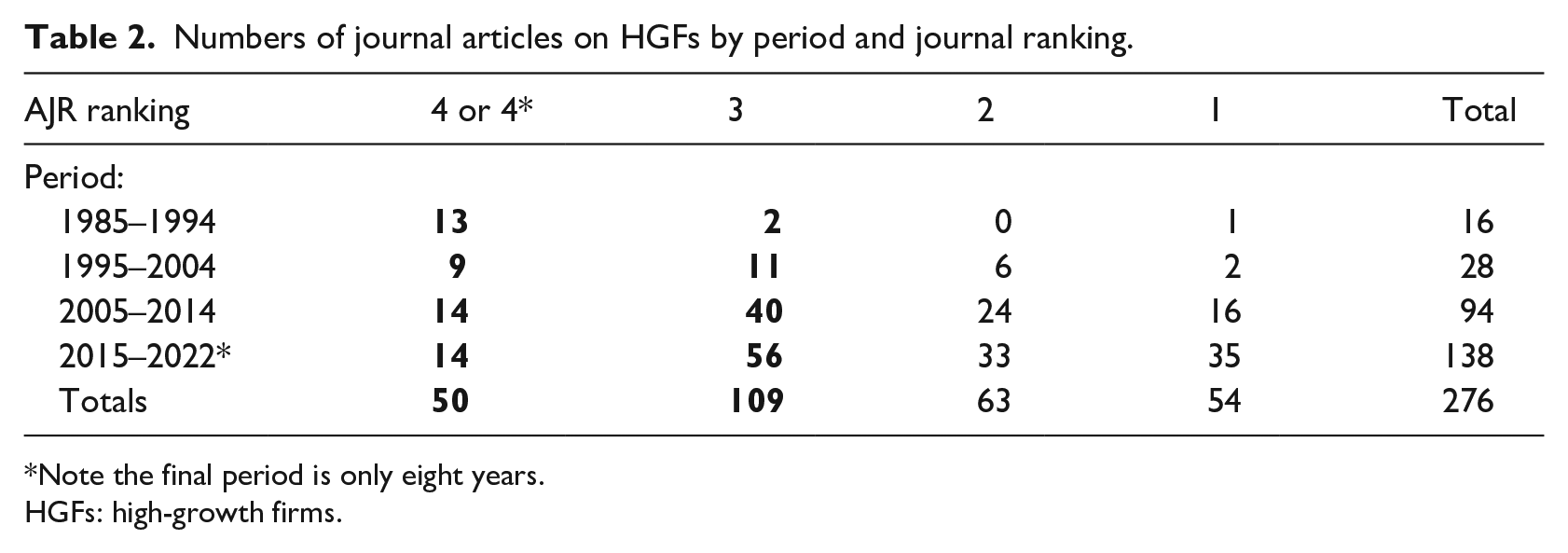

The systematic review adopted a transparent, structured and replicable way of choosing and evaluating the scientific contributions (Kraus et al., 2020). Our first literature search was conducted in September 2021 using dedicated Python-based text-mining software developed by UC Meta Network at the University of Canterbury. The search strings used were permutations of ‘high-growth, gazelles, firms, small firms’, and the initial search period extended from January 1985 to 2021. As Hambrick and Crozier (1985) are among the first commentators on HGFs, the review period commenced in 1985. The initial search of the SCOPUS database generated 748 literature items linked to the topic of high firm growth. SCOPUS is the largest database of peer-reviewed materials and has been used as the main platform in other recent reviews (Capolupo et al., 2023; Fulco et al., 2024; Magistretti et al., 2021). Therefore, only peer-reviewed journals are included, while books, book chapters and other non-refereed publications are excluded from the review. We read each abstract, or when the abstract was unavailable, the items were carefully reviewed to exclude those that did not fit our purpose. We excluded 414 items, many from the earlier years of the search period, in which ‘high growth’ featured as an independent variable explaining share price movements or the financial structure of publicly listed US corporations. This left 334 items, and our software then attached the Chartered Association of Business School’s Academic Journal Guide (AJG) 2021 ranking to each. Of the 334 items, 86 were not covered by the AJG, for example, published in foreign journals, leaving 248 AJG-ranked journal articles. In early 2023, following Miklian and Hoelscher (2022), we extended the search period to end-2022 and found an additional 28 eligible ranked journal articles, bringing our total to 276. We realised that this literature was continuing to expand faster than we could review it, so we followed Cefis et al. (2022) and limited this review to the 159 articles in journals that were ranked at ‘3’ or higher (4, 4*) in the AJG 2021 exercise. Table 2 shows the breakdown of these 276 papers over time and by journal AJG ranking.

Numbers of journal articles on HGFs by period and journal ranking.

Note the final period is only eight years.

HGFs: high-growth firms.

Excel spreadsheets were created with URL links to the 159 papers used in this review. We read and coded papers regarding methodology, theory, main results, findings and policy recommendations and shared the coding scheme to reach a joint view of how to structure the review. In the first period, 1985–1994, there were fewer than two papers per year, and over 80% were in the top-rated journals. In the final period, the annual average rate of paper production was over 17, but only 10% were in the top journals. Around 60% of the 159 papers under review came from six leading journals, which in descending order of prominence are: Small Business Economics (37 papers), Journal of Business Venturing (15), Industrial and Corporate Change (13), International Small Business Journal (12), Journal of Small Business Management (12) and Research Policy (7). In terms of research methods, 113 papers used quantitative methods, and the sophistication of these methods increased with time as larger datasets became available. Some of these 113 papers had a qualitative element, but the findings came from the quantitative analysis. Seventeen papers used qualitative designs, mainly interviews, and 12 used case study methods, usually with multiple cases. Finally, there were six review papers and 12 theory, conceptual or opinion-based papers.

Our initial descriptive themes were locations (national, regional and industries), people, education, innovation, strategy, definition, growth persistence, internal and external impacts and public policy. Due to the breadth of topics, we organised the articles into five main themes: counting, drivers, nature of growth, impacts and public policy, demonstrating the interconnectedness of the themes. By clustering the papers into these themes, we critically reviewed their contributions to advancing knowledge of HGFs, what we do and do not know about HGFs.

Counting HGFs in countries, regions and industries

The first theme is counting and the share of HGFs. Under this research stream, country matters, with Mason et al. (2015: 344) arguing that ‘the ability of a country to nurture the growth of [HGFs] is probably the most important element in enterprise development’. In this vein, Davidsson and Henrekson (2002) argue, based on their Swedish evidence, that national institutional settings and policies, such as taxation, discourage entrepreneurship, leading to a decline in start-ups, hence limiting the emergence of HGFs. From a very different country context, Fisman and Svensson (2007) report that the incidence of bribery in Uganda is three times more damaging to firm growth than any disincentive effect of taxation. Krasniqi and Desai (2016) also confirmed the role of national institutional drivers in a study of the prevalence of HGFs in 26 transition economies. They measured formal institutions (codified rules and laws) and informal institutions (unwritten values, norms, for example, on bribery/corruption), showing that the joint or interaction effect of the formal and informal settings was critical for a country’s HGF prevalence (the percentage of HGFs, defined here as firms with a minimum average of 10% pa over three years) – neither setting on its own was influential for HGF prevalence. The political instability that disrupts national institutional settings can also be particularly inimical to growth firms (Hill et al., 2019). Institutional settings are essential if we accept Huber et al. (2014), who state that increases in start-up rates and market growth have no perceptible impact on the prevalence of HGFs in Austria.

Moving to the regional level, Vaessen and Keeble (1995) successfully challenged the orthodox view that agglomeration economies would dominate the locational choices of growth-orientated firms. The broad consensus, however, is that the growth and development associated with HGFs occur predominantly in urbanised metropolitan areas because of agglomeration benefits, including accessing localised knowledge spillovers (Fotopoulos, 2022; Grillitsch et al., 2019; Li et al., 2016; OECD, 2022). In addition to agglomeration effects, other factors that have been shown to contribute to higher regional shares of HGFs include a specialised industry base with high digitalisation intensity (Friesenbichler and Hölzl 2020). One other point to note here is that several of these critical studies have used enterprise or company-level location data to measure HGF prevalence in an area (Friesenbichler and Hölzl, 2020; Grillitsch et al., 2019; Li et al., 2016). The findings indicate the HGF’s choice of where to locate their headquarters; it is reasonable to expect growth enterprises to be close to key service sectors (legal, accounting, technical support), all of which are concentrated in urban centres. Stam and Van de Ven (2021) find that a region’s share of business services is consistently associated with a greater prevalence of HGFs. Growth firms add secondary establishment units as they grow (Acs and Mueller, 2008), so the regional impact of HGFs depends on the spread of their establishment units as they grow in number. However, Hamilton and Satterthwaite (2019) show that the regional spread of HGF establishments is subject to the same agglomeration forces as the parent enterprises thus, accentuating the growing concentration of HGFs in the larger urban areas, with no significant spillover into peripheral areas. While supporting evidence of a solid regional effect, Pereira et al. (2020) point out that such studies must somewhat concede causation due to the selection effect as firms locate themselves and their establishments in stronger regional economies. We must also bear in mind that many founders, including those of HGFs, are likely to start their businesses where they live; some may have moved there in the first place to find employment (Harrison et al., 2004).

Recent literature on the regional aspects of HGF development adopts an ecosystem approach. Stam and Van de Ven (2021) construct an index of an entrepreneurial ecosystem and show that this is positively related to the share of HGFs in a region’s business population, which in turn influences subsequent values of the index, where HGFs locate makes those areas more attractive to future HGFs. However, interestingly, Stam and Van de Ven (2021) conclude that while ecosystem elements can be measured, only a limited set of factors makes a difference to a region’s HGF share. They recommend further research on how a region’s entrepreneurial culture, social norms, economic structure and dynamics conspire to affect its entrepreneurial ecosystem. This approach is adopted by Muñoz et al. (2022) in their large narrative-based study of 71 local ecosystems in Chile. They find, somewhat perversely, that HGF activity across these ecosystem areas was higher in the absence of norms expected to be conducive to entrepreneurship or where the importance of celebrating entrepreneurial success was inhibited. Favourable HGF outcomes reflected the locally perceived market shifts from year to year due to market dynamism and openness. They argue strongly against the view that regional entrepreneurship policy should seek to maximise any proxy of entrepreneurial output based on a production line conception of an ecosystem. The focus should be on recognising and enabling complex local systems from which multiple forms of entrepreneurship can emerge (see Malecki, 2018). Classifying new businesses and, hence, HGFs to industries can be problematic if they produce outputs that do not readily fit into standard industrial classifications. Most of the industry-level classifications are at aggregated sector levels. Nevertheless, there is consistency in the finding that HGFs are not more prevalent in high technology, research-intensive industries and may even be less common in such industries (Coad et al., 2014a; Daunfeldt et al., 2016; Li et al., 2016). However, there is evidence that HGFs are more prevalent in knowledge-intensive industries (Daunfeldt et al., 2016; Henrekson and Johansson, 2010). Daunfeldt et al.’s (2016) observation that industries with most HGFs also had more firms experiencing rapid declines is also interesting. Still, it is consistent with the negative serial correlation of HGF growth rates (Léon, 2022) and the much earlier finding that the fastest growers were consistently those firms that had declined most in the recent past (Birch, 1979).

While country, regional and – to a lesser extent industry settings do matter – more recent studies have begun to detect a chronic decline in the shares of HGFs in the United States and Belgium, countries with institutional settings supportive of entrepreneurship and HGFs. Decker et al. (2016) find a marked drop between 2000 and 2007 in high-growth young firms, reflected in a clear reduction in the employment growth rate differentials between the fastest and slowest growing firms in the United States. They speculate that the causes of this decline could include firms growing by becoming more capital intensive and/or more international or growth firms’ owners becoming more attracted to an acquisition exit. Such changes will have significant consequences for sources of future employment growth and, noting the findings of Bos and Stam (2014), for the industry growth that lags the rate of increase in HGFs. These findings for the United States are supported over a different, more extended period by Sterk et al. (2021). Bijnens (2020) reported similar findings for Belgium over a 30-year period through to 2014: sustained compression of the growth rate differentials reflecting falling start-up rates and a reduced propensity of small firms to become HGFs. Most of the decline in the Belgian study is ascribed to ICT-intensive industries where high capital investment requirements may have forced smaller firms to stagnate or disappear through closure or acquisition, leaving the industry growth dynamics to reflect the employment patterns of surviving, larger firms who will evidence fewer extreme rates of employment growth. Whatever the causes of these declines in the prevalence of HGFs, the authors agree that the consequence will be lower levels of employment creation from the firms that have been lauded and supported for this purpose.

Drivers of HGFs

No matter how many HGFs are in any industry or place, more is deemed better than less in terms of employment creation, and a significant volume of research has sought to explain the phenomenon by isolating the drivers of high growth. This research focus is even more important considering the potential decline in HGFs mentioned previously. In this section, drivers of HGFs are classified and discussed in four sub-themes: people, education/training, strategy and innovation. We begin, however, with a discussion of the theoretical development in this area and end with our judgement of the conclusiveness or otherwise around each of these drivers of high growth.

Theoretical development

If management scholars were asked to identify the two dominant theories of small business growth, we suspect that most would cite only the seminal work of Edith Penrose, first published in 1959 (Penrose, 1968). This elegant treatment of business growth fuelled by slack resources in pursuit of economies of growth and/or size drew on extensive anecdotes that are confined mainly to footnotes. In recent times, the Penrose model has been co-opted into the resource-based view (RBV) of firm growth, although, in the context of the HGF literature, we would point out that Penrose’s is a theory of growth, not growth rate. Aside from a large digression into descriptive stages models, a line of approach terminated effectively by Levie and Lichenstein (2010), there has been little theoretical development. Interestingly, these authors begin to develop their dynamic state approach to business development, a novel theory that would allow scholars to investigate high-growth episodes within the wider context of overall development through time rather than treat these episodes in isolation from what the business was doing before and after the high-growth phase, and why. We believe this line of approach has potential and return to it later. Otherwise, the area lacks theoretical development and has been dominated by empirical studies. It is not as if this lack of theory has not been pointed out: ‘. . .the subject of organizational growth and development needs work toward a general theory, not work on a general theory. At present, it is a mistake to bet heavily on the ability to classify and group different organizations. . ..If a few people will commit themselves to (a) build formal models, (b)

This extract is from Starbuck (1965: 520), considered an authoritative review of the field, but the commitment to theory was not forthcoming. However, there has been some progress, albeit somewhat fragmented, in consolidating a body of knowledge. Raby et al. (2022) provide a useful characterisation of the three conceptual approaches adopted in this field, which they label ‘Random’, ‘Responsive’ and ‘Resourceful’. The Random approach is usually associated with Gibrat’s Law, published in 1931, which posits that changes in firm size over time are random. More recently, Gambler’s Ruin models have been revived to account for the essentially stochastic nature of a firm’s size trajectory over time (Coad et al., 2013). Responsive describes those approaches that model growth depending on how the firm adapts its (dynamic) capabilities to maintain a fit between the business model and the operating environment (Levie and Lichenstein, 2010). Resourceful growth is driven by how owners and managers organise and apply their internal resource bundles towards perceived growth opportunities.

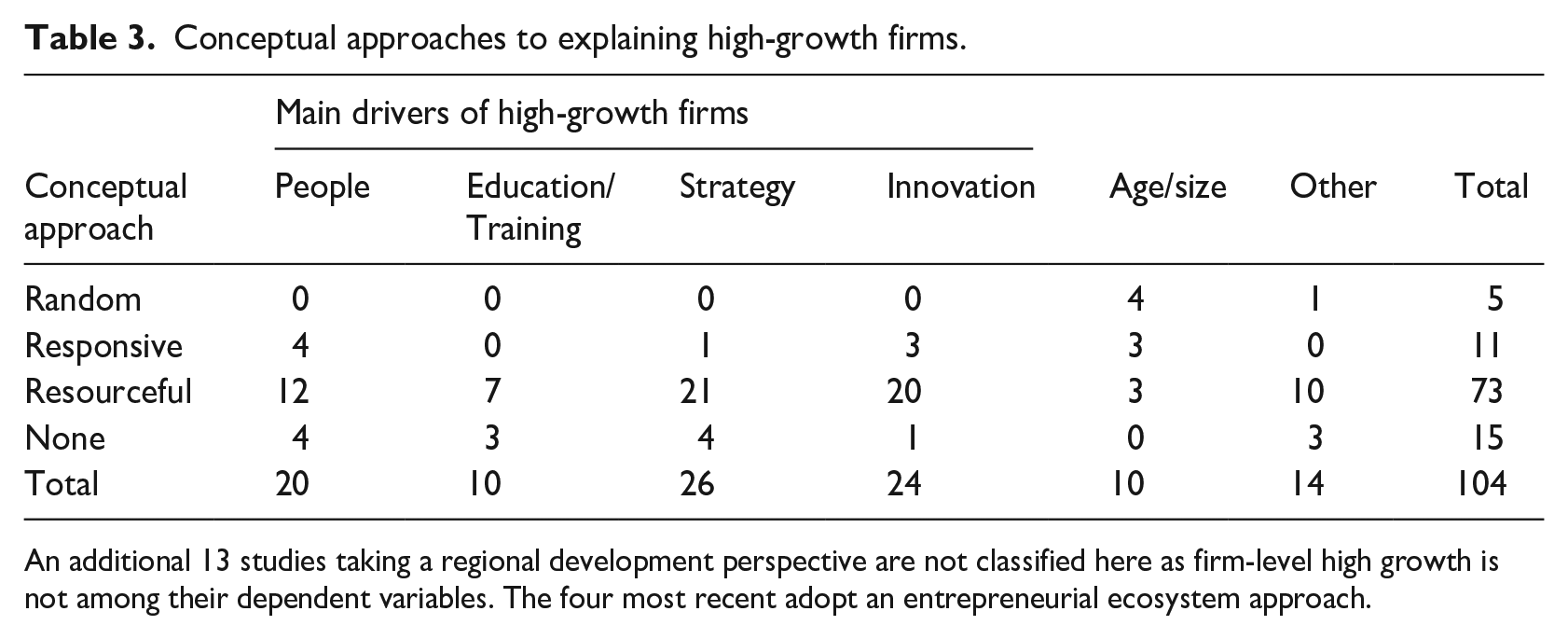

For an overview, Table 3 classifies 104 studies in which high firm growth is the dependent variable according to the conceptual approach adopted, if any. Note that we include firm age and/or size in Table 3 but do not treat them as drivers of high growth, although they help characterise HGFs and may have some value in targeting for policy purposes. Young firms are generally credited with creating most jobs, but when Haltiwanger et al. (2013) controlled firm age, they found no systematic relationship between firm size and age. We also tend to agree with Mawson and Brown (2017) when they contend that both age and size have become discredited as proxies for HGFs in the United Kingdom. The other column category, ‘Other’, includes a variety of approaches, including networking, financial modelling and international trade exposure. The row header ‘None’ means we could not associate any of the three main conceptual approaches to some studies. Some were early and useful contributions to the field involving the descriptive reporting of survey findings. More recent studies in this category had access to substantive databases that allowed them to be illustrative without theoretical support. The conclusion drawn from Table 3 is that most of these studies have focused on People, Strategy and Innovation using the RBV theory of firm development. This is unsurprising as the RBV opens a wide array of explanatory variables that can be measured at the firm-level.

Conceptual approaches to explaining high-growth firms.

An additional 13 studies taking a regional development perspective are not classified here as firm-level high growth is not among their dependent variables. The four most recent adopt an entrepreneurial ecosystem approach.

People

In their pioneering paper, Hambrick and Crozier (1985) alert us to the extraordinary self-awareness and management ability needed to avoid developing a sense of infallibility and cope with the turmoil associated with rapid growth, often in a cash-constrained context. Roure and Maidique (1986) find that founders of high-tech start-ups with more experience working together within larger teams and in other HGFs were associated with more successful ventures. Barringer et al. (2005), in their comparison of higher and lower-growth INC firms, find that the founders of HGFs were better educated, had more industry experience, were determined to achieve high growth, and had richer customer knowledge. HGFs’ founders also differed in personality type compared to their low-growth firm counterparts, being more intuitive in opportunity search with planned approaches to concluding this search (Ginn and Sexton, 1990). However, Willard et al. (1992) find no significant performance differences between founder and non-founder-managed firms. This finding is supported by Mason et al. (2015), who reveal that in most cases, the success of the HGFs in their multi-case study was not due to the founders but to the professional managers who managed growth post-start-up. Sims and O’Regan (2006) find that high-growth (gazelle) firms were privately owned and managed by their owners, and their CEOs identified self-organisation and agility as key drivers of growth. In the family business context, Minola et al. (2022) studied over 39,000 European small- and medium-sized enterprises (SMEs) and found that family firms are less likely to achieve high growth than non-family firms. This likelihood is reduced further if they have a family CEO, but higher levels of family ownership increase the chances of achieving high growth within family firms.

In a more general contribution, Sirmon et al. (2011) argue that the role of entrepreneurs and managers is an underdeveloped yet, critical facet of resource-based theory over the life cycle of firms. They see it incumbent on the entrepreneur/founder to put in place formalised procedures and a management hierarchy that will cope with the rapidly increasing size of their business and facilitate relationship building with key external stakeholders such as suppliers and investors. Supporting the need for delegation, Dillen et al. (2019) find that for high growth to persist over consecutive years, the critical factor was the rapid transition of the founder’s role from day-to-day management to a strategic focus on growth issues. However, O’Regan et al. (2006) conclude that while ownership and strategic orientation are favourable for growth in their sample of manufacturing firms, organisational capability has no bearing on growth. Confirming this, Ress-Jones et al. (2024) reported recently that the key to high growth lies in the individual founder-level dynamic capability to ‘sense and seize’ growth opportunities, not in organisational-level capabilities. Moen et al. (2016) conclude that high-growth motivation is associated with a strong international orientation and superior sales growth domestically and internationally, concluding that policy initiatives to stimulate high growth should focus on increasing international orientation (cf. Brown and Mawson, 2016b). Chetty and Campbell-Hunt (2003) vividly describe the chaos of managing through the ‘gusher’ phase, when smaller firms suddenly achieve their first breakthrough into large international markets. Such hyper-growth – minimum 20% annual sales growth for at least 4 consecutive years – seems to be explainable only by identifying extraordinary opportunities that can be pursued by accessing extraordinary resources (Cassia and Minola, 2012).

Women also found HGFs, and several important studies have been devoted to them. Morris et al. (2006) affirm that high growth is a choice for women founders. The growth orientation depends on whether the female founder(s) were pushed or pulled into entrepreneurship, and the modest- and high-growth founders differed sharply in how they viewed themselves, their families and the wider environment (Lawrence and Hamilton, 2001; Hansen and Hamilton, 2011). The paper by Gundry and Welsch (2001), heavily cited, characterises a large cross-section of ambitious women entrepreneurs in the United States (n = 832). They find, inter alia, that female founders of HGFs have stronger strategic growth and expansion intentions and display more entrepreneurial intensity. However, Nelson and Levesque (2007) found that the boards of HGFs are much more likely to be composed of men only and that women are also much less evident on the boards of venture capital-backed businesses in the United States. Similarly, Rasmussen et al. (2018) find that growth intentions, a key antecedent of actual growth, are reduced when company boards have a high proportion of women (independent directors). This Norwegian study’s main growth driver was the founder’s duality (joint board chair/CEO).

Education and training

International evidence shows that a country’s cognitive skills level is positively related to its Global Entrepreneurship Development Index, a national measure of entrepreneurial attitudes in a population, and the ease with which these can be converted into innovative, growing businesses. However, the final link to entrepreneurial activity levels was insignificant (Huber et al., 2014). Cognitive skill levels help create the pre-conditions for high-growth entrepreneurship, and cognitive ability is correlated with educational attainment. In their large-scale Swedish study, Grillitsch et al. (2019) identify three types of knowledge – analytical (science-based), synthetic (tacit, experience-based) and symbolic (brands, designs) – and show that it is how these knowledge levels are combined that affect firm-level innovativeness and hence growth. It has also been shown that a firm’s stock of intangible capital (organisational, product-related and ICT) increases the probability of gazelle-like growth, a tendency further enhanced by employees’ educational diversity when knowledge intensity is high (Ekland and van Criekingen, 2022). Hence, education does matter, but each HGF is a unique combination of opportunity, resources and capabilities that present idiosyncratic challenges to those pursuing growth and its consequences (Hambrick and Crozier, 1985).

Individuals start and manage these firms, employing others as they grow. Many come into these roles with previous education, training and experience. The questions are: How are these backgrounds related to the growth of the venture, and is there a benefit to further education and training? There are numerous descriptions of the unique challenges that the onset of high growth can suddenly create for these business owners, managers and employees (Chetty and Campbell-Hunt, 2003; Hambrick and Crozier, 1985). Barringer et al. (2005) find that the founders of HGFs in the United States strongly emphasise training and employee development. This focus on employee training and development is also reported by Hansen and Hamilton (2011) in their comparative study of growers and non-growers. The literature supports education and skills, management experience, cognitive ability and relevant domain-specific industry experience to comprise the human capital that drives high growth (Demir et al., 2017; Fafchamps et al., 2017). The lack of management skills in the wider high-growth setting – for current HGFs and potential HGFs - has been identified as a critical obstacle to growth. Developing these skills remains problematic (Lee, 2014; Rutherford et al., 2003).

González-Uribe and Reyes (2021) observed only 8% of participants in a high-growth-focused training programme rated standardised business training essential, while 74% found customised advice and visibility to be more effective (Dalley and Hamilton, 2000). However, issues of what to teach, how to teach and even who to teach remain unresolved. López et al. (2019) find that training in formalised management practices benefits only older HGFs (aged over 5 years) and does nothing for younger, emergent HGFs. In other words, age and/or stage of HGF development influence the relevancy of management training. In a major Swedish study, Coad et al. (2014b) found that HGFs in that country tended to hire from among the younger, less well-educated, immigrant and longer-term unemployed, while the more mature HGFs, those that had already grown, tended to hire from other firms. However, there may also be size and age effects. Giotopoulos et al. (2022) observe that it is the larger HGFs in their Greek sample that employed people with lower educational attainment and invested in formal training of the requisite skills, while smaller (younger, emergent) HGFs avoid the need to invest in formal training by hiring the specialised skills that they need.

Strategy

Growth is a choice and does require strategic intent by entrepreneurs who will view themselves, their business and the external environment in ways quite different to those responsible to non-growth-oriented firms (Gundry and Welsch, 2001; Hansen and Hamilton, 2011; Morris et al., 2006). The human capital embodied in people is critical to the emergence of HGFs. However, as noted previously, Cassia and Minola (2012) find that hyper-growth stems from coupling exceptional opportunities with crucial strategic resources, especially knowledge-based ones. Entrepreneurship, as embodied in the people, was essentially a moderating variable. In other words, strategy is also essential: the right people pursuing the wrong opportunities or these exceptional growth opportunities with the wrong resources will not develop an HGF – strategy should matter. Yet, Brush and Chaganti (1999), in seeking to explain firm employment growth in a sample of 195 small firms in what they regard as unglamorous (non-dynamic) industries, find that strategy mattered considerably less for firm performance than firms’ human and organisational resources. Their strategic prescription for higher growth rates is to be young, small and in a growth industry. However, earlier, Buller and Napier (1993) found that their fast-growing firms had fewer human resource activities. Conversely, Parker et al. (2010) show that the strategy that led to growth in one five-year period did not sustain high growth into the following period. Their sample of 121 mid-market U.K. companies showed an average sales growth of 36% in 1992–1996, falling to only 8% in 1996–2001. Interestingly, one of the successful strategies was B2B, selling to other businesses rather than customers directly, an observation that others have made (Hinton and Hamilton, 2012; Mason et al., 2015). Growth firms need to capitalise on new opportunities by rapidly moulding their capabilities and strategies to explore and be able to adapt their strategy (Brown and Mawson, 2016b; Colombelli et al., 2014).

Moving from opportunity and resources, the importance of the positioning school of strategy to HGFs emerges from Demir et al.’s (2017) review. It refers to a formal process involving strategic planning and competitive positioning involving differentiation over multiple products (see also Baker et al., 1993). Using the multiple case study design, Bamiatzi and Kirchmaier (2014) explained how firms achieve high growth in declining industries. They report that the key to growth in these adverse settings was a dual product (not market) differentiation strategy through innovation and customisation to buyers’ specifications. Cost control was important, but aggressive price competition was avoided. None of the 20 case study firms sought to be cost leaders or targeted a perceived market niche. However, the work of O’Regan et al. (2006) involving 207 manufacturing firms finds that HGFs compete primarily based on price. The work by Chandler et al. (2014), also set in declining industries, finds that the HGFs had developed through differentiation to offer more distinctive value propositions, which they then communicated more aggressively than was the norm in these industries. It concurs with the findings of González-Uribe and Reyes (2021) that the capabilities needed for high growth were being able to identify the correct market need (then customisation) and getting recognised in the market (communication). There is also evidence that, once decided, HGFs are then less likely to change their product/market focus, including foreign markets – assuming that these are successful (Feeser and Willard, 1990). Colombelli et al. (2014) also find that while high growth stimulates new knowledge and exploratory search behaviours, this is confined to complementary fields proximate to the firms’ existing technical capabilities. Do formal business plans help in all this strategy for high growth? Baker et al. (1993) studied INC 500 growth firms and found that HGFs convert their strategic planning into business plans used mainly for internal management. However, while Fletcher and Harris (2002) find that engagement in a strategy process is associated with growth, they do not find any association between the existence of a written business plan and business growth.

Rather than focusing on the antecedents of high growth, Piaskowska et al. (2021) offer new insights into how some firms sustain ‘hyper’ growth rates of over 40% per year while scaling their activity in pursuit of economies of scale. These authors have a sample of unicorn and emerging unicorn businesses with a market valuation of at least $US 500 million when the research was done. All 184 firms in the sample had some digitisation in their business models, but the extent of this varied. The authors show how four growth-enabling activities – financing, innovation, digitisation and acquisition – cluster parsimoniously into four scale-up modes, that is, identifiable patterns of activities used by these scaling firms. The evidence from this study confirms a clear link between elements of the business model (digital platform vs traditional pipeline; digital vs physical product) and the scaling mode. Jansen et al. (2023) extend the discussion on scaling by offering a conceptual schema that can be applied to all firms, digitised or not. These authors usefully extend the scope and discourse on high growth by formally introducing a ‘hyper-growth’ category above what we recognise as ‘high growth’. The hyper category is populated by ‘scale-ups’, young firms up to 10 years old that have grown to 50 or more employees, and ‘superstars’, mature firms over 10 years of age with annual growth of at least 40%. These authors offer a helpful research agenda based on their contention that scaling is a dynamic capability of the organisation that will allow firms to ‘grow exponentially through the expansion, replication and synchronisation of resources and practices over time’ (Jansen at al., 2023: 590). Piaskowska et al.’s (2021) paper is a major early contribution to this research agenda. While the conceptual schema in Jansen et al. (2023) does not extend explicitly to exponential growth, we take this mean accelerating annual growth rates as investigated in Belitski et al. (2023). These contributions foreshadow a welcome extension to the growth domain that should not conflate with the extant research on HGFs (Coviello et al., 2024).

Innovation

A high-growth episode, especially in sales, reflects increasing demand for the firm’s product or service but need not be derived from successful innovation. Most HGFs do not compete in R&D-intensive areas and are typically not university spin-offs. However, in the previous section, we alluded to an association between product innovation and higher firm growth rates in declining industries (Bamiatzi and Kirchmaier, 2014). The extant literature confirms a nexus between successful product innovation and firm growth, although the support is not altogether unanimous. Studies finding a positive association between innovation and high(er) growth are those by Koellinger (2008), Goedhuys and Sleuwaegen (2010), Eckhardt and Shane (2011), Czarnitzki and Delanote (2013), Segarra and Teruel (2014) and Demir et al. (2017). Innovation creates or revitalises the product life cycle that otherwise would fall away quickly in fast-changing markets. Romano (1990) finds innovation in HGFs to be a predominantly pro-active internal process stimulated by technology, R&D and the need for a competitive edge in the product market. More recently, Mawson and Brown (2017) found that, despite being small, some HGFs with a strong external orientation also use acquisitions to augment their innovativeness. Some studies provide more nuanced insights into the nature of the innovation-HGF nexus. Carnes et al. (2017), following Sirmon et al. (2011), argue that innovation is a necessary and ongoing challenge for firms to maintain growth over time. However, most firms, particularly HGFs, struggle to do this. They found that growth-stage firms, relatively young, smaller firms with informal structures, are more likely to attain HGF status. The leaders of such firms are called upon to accumulate resources as quickly to avoid resource constraints on growth and develop capabilities for innovation. The studies by Hölzl (2009), García-Manjón and Romero-Merino (2012) and Ahn et al. (2018) suggest that an innovation-based growth strategy will only be justified in those regions and/or industries that are already innovation-led and technically sophisticated, areas where most HGFs are not. Successful innovation becomes the basis for the competitive edge/advantage that ultimately underpins growth in such sectors.

Growth history has also been shown to matter for the innovation/HGF nexus. Coad and Roa (2008) report that innovation has a growth pay-off only in those firms that have already been fast-growing, a finding echoed in subsequent studies by Stam and Wennberg (2009) and by Mazzucato and Parris (2015) in their historical analysis of high-growth enterprises in the U.S. pharmaceutical industry. This longitudinal single-industry study provides valuable insight into how the industry’s changing competitive environment affects the innovation/HGF relationship. Using R&D intensity as a proxy for innovation, Mazzucato and Parris (2015) find that increased R&D intensity is justified only when the competitive environment is highly competitive, with low levels of industry concentration, unstable market shares and rising levels of R&D intensity. In such an environment, higher R&D intensity benefits only those firms with a recent growth history at or above the median level, with the most potent effects observed for HGFs. In more sedate environments – high concentration, stable market shares, stable R&D investment – not even HGFs can expect a payoff from increased R&D intensity. This relationship between a pro-innovative investment strategy (i.e. increasing R&D intensity) and growth may then become self-propelling, following Colombelli et al. (2014), because the ensuing sales growth can stimulate new knowledge that improves the market scope of the business. However, these authors note that the increased scope remains close to the firm’s technological core. Grillitsch et al. (2019) take this one step backwards and demonstrate how combining knowledge types (analytical, science-based, synthetic, experiential and symbolic meanings) promote general firm growth, not just within the subset of HGFs.

While the evidence points to an association between product-based innovation and growth, especially within the set of existing HGFs, we did point out above that this is not totally supported in the literature. The Dutch study by Uhlaner et al. (2013) finds a relationship between product innovation and firm growth, one moderated by firm size, that is, the effect is more favourable in smaller firms. However, they also report from their regression analysis that process innovation is more likely than product innovation to explain differences in SME growth rates. An earlier study by O’Regan et al. (2006) of manufacturing firms finds that their innovativeness did not significantly affect high growth rates. Despite this null finding, the authors concede that R&D investment and innovation will be likely if such growth is sustained over extended periods. Finally, one of the larger studies in this area finds that an industry’s share of HGFs is inversely related to its R&D intensity, with HGFs being disproportionately found in knowledge-intensive service industries and concludes that the relationship between R&D and achieving HGF status is ‘at best, highly complex but most likely negative’ (Daunfeldt et al., 2016: 14).

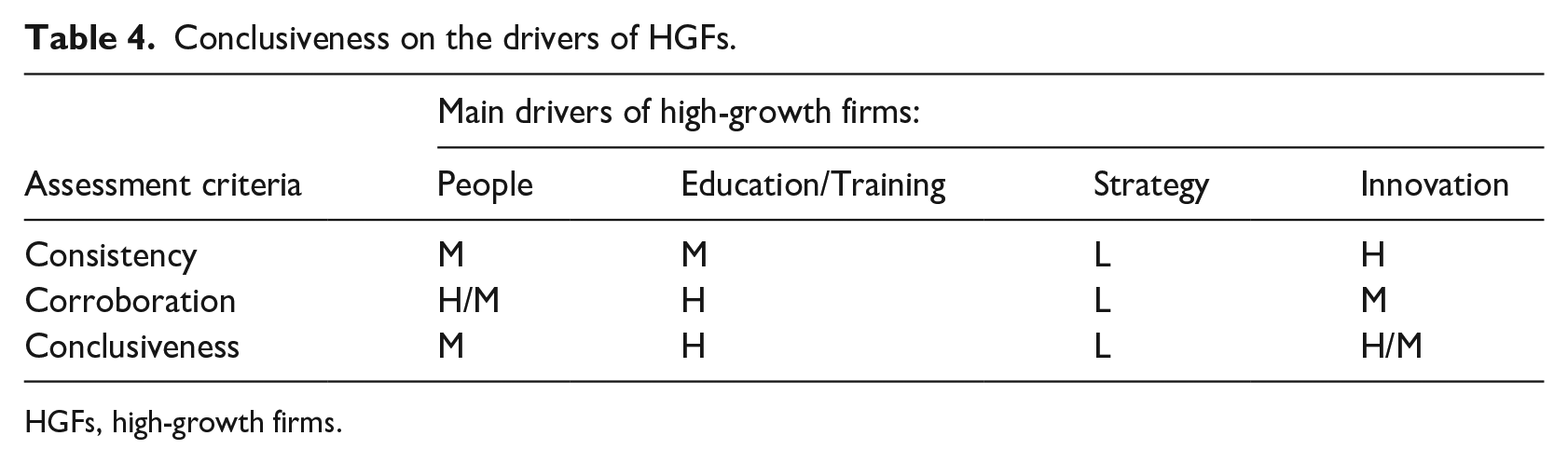

Conclusiveness on the drivers of high growth

An anonymous reviewer urged us to make a subjective assessment of the field, following Bloom et al. (2019), who rated the ‘conclusiveness’ of the research evidence they reviewed based on the number and credibility of papers reviewed. We form our judgements of the HGF field in terms of the consistency of approach, corroboration of results, 1 and conclusiveness of findings. An inconsistent approach would involve a plethora of explanatory variables; corroboration would be weak if the same independent variables have contrasting effects in different studies; and a lack of conclusiveness would indicate that we judge consistency and/or corroboration to be particularly low. Table 4 has our subjective judgements, expressed simply as High (H), Medium (M) or Low (L).

Conclusiveness on the drivers of HGFs.

HGFs, high-growth firms.

In the People area, the greatest focus has been on founders, their growth ambition and relevant experience. Some studies find no such clearcut founder effect on business growth (Mason et al., 2015; Willard et al., 1992). Education and Training investigate broadly the amount of knowledge available in the firm – owners, managers, employees – and while there is corroboration that this human resource is positive for high growth, the return may not be the same for all HGFs (Goedhuys and Sleuwaegen, 2010; López et al., 2019). The Strategy area has the largest number of papers (see Table 3) and, perhaps inevitably, the widest array of explanatory variables with relatively low corroboration. The consensus from different studies involves a strong strategic focus and market orientation. The Innovation studies are more consistent, with most resorting to R&D-based measures, followed by patent activity, as proxies for product innovation. However, the relationship between R&D expenditure and high growth is complex and not ubiquitous (Coad and Rao, 2008; Daunfeldt et al., 2016). To reiterate, these are subjective ratings based on our engagement in this literature, and others within each field may have a different view. That notwithstanding, the field would be advanced with more consistent variable selections, enabling us to build on previous work. As pointed out, most papers reviewed here are quantitative multivariate designs, and each driver's importance is gauged by its statistical significance. It would be helpful if scholars could report effect sizes or provide descriptive statistics that others could use to compute effect sizes (Starbuck, 2006: 157–160). Finally, we are reminded of Gibrat’s law that high growth is just a random event, a proposition revitalised by Coad et al. (2013): the lay reader scrutinising the variation explained in many of these empirical studies may conclude that Gibrat (1931) was not far wrong!

Nature of growth in HGFs

Delmar et al. (2003) identify seven growth patterns associated with HGFs. The literature reviewed here focuses on four paths where SMEs are expected to dominate: ‘super absolute growers’, ‘super relative growers’, ‘erratic one-shot growers’ and ‘employment growers’. The other paths, more likely to be followed by larger firms, for example, ‘steady sales growers’, ‘acquisition growers’ and ‘steady overall growers’, have featured less in the HGF literature. Explaining high firm growth is challenging due to its lack of persistence across consecutive periods and the rarity of any repetition in later years. Coad and Srhoj (2020) also find that the intra-firm variation in annual growth rates exceeds the inter-firm variation. Definitions and growth intervals continue to matter. For example, compared with those used in early studies, Daunfeldt et al. (2016) have a much larger sample (164,808 firms, 1401.684 annual observations) and can define their HGFs as firms in the top percentile of the growth distribution for 3 years, a definition that would be problematic for small samples. Esteve-Pérez et al. (2022) measure growth rates annually and find that in 25% of cases, high growth rates (top decile) persist into the next period (year), much higher persistence over time than would be observed if the growth interval was 3 years or longer. Other important studies that use large datasets to drive the analysis include Coad et al. (2014b), Coad et al. (2017), Grillitsch et al. (2019) and Coad et al. (2020). With such caveats in mind, we now discuss what we know about the growth paths of HGF over varying periods.

Growth persistence, repetition and acceleration

Turning now to the nature of the growth path itself, when high growth is measured in percentage terms, as is often the case following OECD (2007), arithmetic dictates that larger growing firms are less likely to become or remain HGFs. Most research on growth is concerned with the persistence of high growth over consecutive periods and, somewhat less frequently, the repetition of a high-growth episode after periods of non-growth or decline. The consensus finding on the persistence of high growth is summed up in Daunfeldt and Halvarrson’s (2015) depiction of them as a ‘one-hit wonder’, that is, the chances of an HGF retaining this growth status in a consecutive 3-year period is low (prob = 0.01). This lack of persistence is also noted in Vinnell and Hamilton (1999), Hölzl (2014), Coad et al. (2017), Satterthwaite and Hamilton (2017), Erhardt (2021) and Esteve-Pérez et al. (2022). Léon’s (2022) study in Senegal sums up the general lack of persistence by likening HGFs to cheetahs, who start quickly but run out of breath, rather than to gazelles. While there appear to be very few instances of persistent high growth, scholars have observed enough to try to identify the causes of persistence. Lopez-Garcia and Puente (2012), using annual employment data, find that past high growth does explain future high growth, and Ranniko et al. (2019), using annual and 3-year growth intervals, also find that high employment growth rates are more likely to persist than high rates of sales growth. The growth interval is vital to any gauge of high-growth persistence. As noted above, Esteve-Pérez et al. (2022), in their study of Spanish manufacturers over a 20-year period, found that 50% of firms had a high-growth episode and that in 25% of such cases, the high growth persisted into the following year. This accords with some of the findings in Hamilton’s (2012) tracking of the growth paths of the 60 fastest (employment) growers from 1994 to 2007, where the probability of consecutive growth years in the New Zealand manufacturing sector was 22.4%. However, persistence over more extended periods is much less likely, and this underlines Léon’s (2002) suggestion that it would be more useful to consider why high growth does not persist (rather than the somewhat futile attempts to explain why it does).

Attempts to explain high growth and its persistence have had mixed results. Davidsson et al. (2009) find strong evidence that high prior profitability was critical for sustained and successful growth. Pursuing growth without a base of high profitability was much more likely to leave firms with low profitability and low growth. These findings of Davidsson et al. (2009) have recently been replicated in a large multi-country European study by Ben-Hafaïedh and Hamelin (2023). Davidsson et al. (2009) and Ben-Hafaïedh and Hamelin (2023) urge a downplaying of the pro-growth ideology in entrepreneurship and more emphasis on profitability. In a large-scale study on a panel of French manufacturers, Coad (2010) finds that employment growth drives subsequent sales growth. While growth in employment, sales and productivity contribute to future profit growth, profit growth does not drive future growth on any of these three dimensions thus, inhibiting growth persistence (c.f. Davidsson et al., 2009). Lopez-Garcia and Puente (2012) also find that past growth employment helps to predict future growth. Moschella et al. (2019) used a large panel dataset for China from 1998 to 2007 to explain persistence using measures of a firm’s internal attributes, viz., productivity, profits, investment pattern, innovation and financial structure. They find that none of these internal measures explains high-growth persistence. Hence, either they have omitted vital variables unrelated to those included or the key to persistence lies in features of the external environment (Clarysse et al., 2011). Bianchini et al. (2017) pose the same research question as Moschella et al. (2019) do find that HGFs can be characterised to some extent by internal variables such as their productivity and leverage (financial structure) but find no significant differences in explanatory variables between HGFs and persistent HGFs, suggesting that persistence depends on unobserved contingencies, internal and/or external to the firm, or ‘mere luck’ (Bianchini et al., 2017: 653). Moen et al. (2016) argue that increasing growth motivation with an increased international orientation would extend growth performance. Dillen et al. (2019) use a case study design and conclude that the key to high-growth persistence is the rapid transition of the founder/owner from a functional (managerial) role to a strategic (director) role, supported by a high-quality human capital base. The pivotal role of the founder/owner in high-growth persisting is also highlighted by Rasmussen et al. (2018), who find that growth persistence is less likely when more independent directors and females are on the board: female directors bring too much focus on internal control while independent directors (male or female) create personal goal conflict with the owner/founder, bringing personal goals that conflict with those of the owner/founder.

Many of the studies cited in the previous section also allude to the repetition of high-growth phases by the same firm in non-consecutive periods, if only to point out the rarity of repetition (Daunfeldt and Halvarsson, 2015; Erhardt, 2021; Esteve-Pérez et al., 2021; Rannikko et al., 2019). Given the difficulty of explaining the occurrence of single episodes of high growth, it is unsurprising that we struggle to account for episodes that repeat after some time. In their case study of a manufacturing firm from its founding in 1945 to 1993, Vinnell and Hamilton (1999) identified three high employment growth episodes with gaps of eight and 20 years between their starting years. Each of these episodes had different a different driver. The first (1956-57) reflected a move to a new, larger factory in a location with a good supply of skilled labour. The second (1964-71) was hiring a dedicated sales force, which proved chronically unprofitable and had to be rapidly curtailed. From 1984 to 1986, the business was again fast-growing and profitable due to successful product innovation. In any event, Coad et al. (2020) find that more moderate and smoother growth paths (less volatility in sales) are better for growth and survival than a growth path with intermittent bursts of high growth.

A recent extension to research on firm growth paths is identifying firms that have an acceleration in their annual growth rates (Belitski et al., 2023). Accelerated growth, say in sales, is identified when the ratio of a firm’s sales to average industry sales continuously increases over 3 consecutive years. These authors use the U.K.’s Business Structure Database to examine the growth paths of three to four million active independent firms over 2000–2017, finding that less than 2% of firms achieve accelerated sales growth and less than 1% have accelerated employment growth. 2 This is an interesting new departure in a field that needs new directions, facilitated by the increasing accessibility of large databases that ensure that research samples are close to underlying populations. These authors find, inter alia, that it is smaller and, more so, younger firms that are more likely to exhibit growth rate acceleration, findings that also apply to HGFs, which must accelerate their growth rate, especially at the beginning of their growth phase. These newer small firms may also be growing their sales in line with the well-known product life cycle, which includes accelerated growth rates in the exponential range of the life cycle. It is also worth noting that growth acceleration per se may not always lead to an HGF. This link will depend on the firm's starting size and the annual growth rates of the firm and its industry. Smaller firms accelerating in low-growth or declining markets may struggle to achieve the quantum needed for high-growth status. It is more important, in our view, to investigate the accelerating growers among larger firms.

Impact of HGFs

Despite the often-transient nature of a high-growth phase, this experience affects the well-being of the business and those directly involved – owners, managers and employees. HGFs also have external effects that affect other firms in their vicinity, such as employee loss, productivity gains and the broader entrepreneurial ecosystem.

Internal consequences

Is high growth a good thing or a bad thing, and how does being an HGF influence the well-being of the business and those directly involved with it? Mitra (2005) finds that firms with higher growth expectations also increased their IT spending as cash flow permitted, while those with lower growth expectations maintained IT spending irrespective of cash flow. The enhanced IT infrastructure then reduces the operating costs of the growth firms in ensuing periods, that is, makes them more productive as they grow. Coad (2010) also shows how increased productivity contributes to subsequent high growth in employment and profits. This relationship between productivity and growth in HGFs is further elucidated by Du and Temouri (2015). These authors use an unbalanced panel of over 26,000 U.K. registered businesses over 10 years and find, supporting Coad (2010), that increases in total factor productivity are associated with a high-growth episode and, in turn, a high growth itself stimulates further growth in their measure of total factor productivity. However, the benefits of these relationships between productivity and firm growth remain internal and captured by the firm and its owners.

However, pursuing high growth comes with business risk, with Eklund et al. (2020) reminding us that such entrepreneurial behaviour and failure are two sides of the same coin. High employment growth rates equate to the growth rate of a significant expense, particularly in an SME. Rapid sales growth entails the risk, albeit manageable, of over-trading when cash receipts lag the expanding level of sales. Generally, seeking to grow the assets of a business faster than the rate of return earned on these assets will eventually require funding by new equity injection or, more likely, by increased debt. Coad and Srhoj (2020) associate the likelihood of a business achieving HGF status with prior low inventory levels, higher employment growth, and high short-term liabilities, such as bank overdrafts. While Coad and Srhoj (2020) do not claim any causality in their findings, they do profile a somewhat risky background from which to launch into higher employment growth rates, bearing in mind that this common growth numeraire is a direct business expense. Satterthwaite and Hamilton (2017) and Coad et al. (2020) document lower survival rates in the fastest-growing firms, while Erhardt (2021) finds that the exit rates of HGFs are well below those of non-HGFs. Coad et al. (2020) point to the improved survival prospects associated with moderate rather than extreme growth rates, corroborating previous findings by Pierce and Aquinis (2013) and Zhou and van der Zwan (2019). These prospects can be improved further along smoother (sales) growth paths (Coad et al., 2022).

From the earliest days of management research on HGFs, scholars have also been stressing the personal risk to those individuals directly involved with such firms, including internal turmoil, poor decision-making and key individuals suffering burnout, all against a background of rapid growth and cash starvation (Hambrick and Crozier, 1985). Muurlink et al. (2012) present a case study design and describe how high growth pressures create rigidity and conservatism in decision-making where failed responses are allowed to continue, raising the risk of high-growth failure. Cassia and Minola (2012) also raise questions about what they term ‘hyper-growth’ on the health and survivial of such firms. Some scholars have also linked high growth with the expansion of international sales (Brown and Mawson, 2016b; Feeser and Willard, 1990; Moen et al., 2016), but businesses moving in this direction also need to be aware of the added stresses that come with any eventual success in overseas markets (Chetty and Campbell-Hunt, 2003; Corbett and Campbell-Hunt, 2002). One of the most insightful papers is by Freel and Gordon (2022). Following Hambrick and Grozier (1985) and Muurlink at al. (2012), Freel and Gordan (2022) use a case study design to investigate the ‘dark side’ of entrepreneurship, the internal dynamics created by a high-growth experience, specifically the pressures on the lead entrepreneur and the firm as it grows. They find that high growth carries the seeds of its demise as entrepreneurs are satisfied with what they have and recoil from the stresses of managing high growth, including any adverse effects on employee well-being. Coping with high growth needs the development of a solid human resource capability and a delegated organisational structure, which removes the lead entrepreneur from the daily fray of this growth (Davidsson, 1989; Dillen et al., 2019). These findings are supported by Brown and Rees-Jones (2024), who document how the mental well-being of entrepreneurs can be affected adversely by the experience of high growth and advocate for better relational support structures.

External effects

The review also acknowledged that the main external effect of HGFs – and the primary reason for extensive academic research and policy interest – is their ability to create employment faster than other firms. On this, it is worth noting that Acs and Mueller (2008) find that the employment impact of fast-growing gazelles, while initially positive, becomes negative after two years, and significant long-term effects are only manifest in those fast growers that remain in business for at least five years. Using longitudinal data, Satterthwaite and Hamilton (2017) find that while HGF growth does not persist, these firms tend to retain the employment numbers created in their growth phase. Bijnens (2020), while reminding us that a small number of HGFs contribute disproportionately to aggregate employment growth, also reports that HGFs raise aggregate productivity as employee numbers grow in these firms. This broader effect of HGFs on the performance of other firms is vital in justifying public policy support for HGFs. In a significant study of U.K. manufacturing, Du and Vanino (2021) find strong evidence for the spillover of HGF labour productivity into the productivity of non-HGFs in the same industry and region. However, this was contemporaneous with a decline in employment in the non-HGFs, an effect more pronounced in peripheral (non-urban) areas where the overall labour supply can be expected to be thin.

These effects of employment shifts to HGFs from non-HGFs but with productivity gains in the latter group are explained by competitive pressures coupled with non-HGF learning from HGFs. Another recent paper based on a large Hungarian data set (De Nicola et al., 2021) confirms that the productivity impact of HGFs is not confined to themselves, linking the presence of HGFs with improvements in productivity, income and employment in other local firms either in the same industry or in upstream supplier industries. The spillover effects are stronger over shorter distances. These spillovers into the performance of other non-HGFs are significant in justifying continued public policy support for HGFs, as these are benefits that are not captured and privatised by HGF owners. Crown et al. (2020), in their major establishment-level study of the impact of HGFs in local markets across the United States, find that the presence of HGFs disproportionately benefits other establishments located in the non-metropolitan areas of the United States and those operating in the same industry as the HGFs. However, in any discussion of the effect of high growth on productivity, we must carefully consider the (short) periodicity of an HG phase and the duration of its productivity-enhancing effect. Bisztray et al. (2023), while pointing out that sales-based HGFs contribute five times more to productivity growth than employment-based HGFs, also find that this productivity effect is strictly confined to the high-growth phase. Following Penrose (1968) on the economies of growth (rather than size), Cassia and Minola (2012) explain that a prospective HGF starts with considerable accumulated and under-utilised resources, which fuel the growth process and are consumed by it. During this process, growth exploits the stock of resources, and productivity rises. Still, the growth-induced rise in productivity can be as transient as the growth episode.

The final external impact of HGFs, one that can be overlooked, is on the broader ecosystem that spawned or attracted them in the first place. We suggested earlier that the personal and financial capital investments of remaining the owner of an HGF may cause the business to falter and/or make acquisition exit more attractive. These outcomes release experience and capital back into the local ecosystem in the shape of new angel investors and new start-ups, bearing in mind that many high-growth entrepreneurs are also portfolio entrepreneurs (Morrish and Hamilton, 2022; Mason and Harrison, 2006).

HGFs and public policy

Along with this research stream, there has been a strong policy focus on supporting HGFs. However, while scholarly support for this has become much more sceptical in recent years, there remains a wide range of pro-HGF publicly funded programmes, such as the EU’s Horizon 2020 programme with an initial budget of 80 billion euros to support ‘the most innovative SMEs with high-growth potential’. The EU also launched a pilot programme, ESCALAR (European Scale-up Action for Risk Capital), with a budget of 300 million euros; Mexico has a High Impact Entrepreneurship Program, and, somewhat appropriately, South Africa has its own National Gazelle programme geared towards growth acceleration. We would have included formal assessments of these policies, but none were readily available (see Mina et al., 2021; Zhang and Guan, 2023). The United Kingdom provides a range of help to growing businesses support programmes, which are discussed and assessed in the recent paper by Brown and Rees-Jones (2024), where they draw the important distinction between transactional support programmes (providing money) and relational support involving personalised mentoring. Despite the large amounts of funding that can be accessed through these programmes, Brown and Rees-Jones (2024) find that entrepreneurs under pressure in their HGFs prefer more relational support from qualified, credible coaches and mentors (Dalley and Hamilton, 2000).

It will be interesting to observe the interplay between the evolving research evidence on HGFs and their ongoing prominence in entrepreneurship policy agendas (Smallbone and Welter, 2020). Two points emerged from this review. First, scholars have sometimes seemed overly keen to advocate for policy initiatives to support HGFs without articulating how and when such transient firms can be identified and why public support is justified. Second, some scholars have advocated for and against pro-HGF policies, sometimes in papers published around the same time. Policymakers may, therefore, continue to set their agendas despite a growing body of research that is becoming increasingly sceptical of the feasibility of and justification for government support for HGFs (see Arshed and Drummond, 2020).

It is useful to begin at the beginning and, as others have done (Anyadikes et al., 2015), draw attention back to what David Birch wrote on policy for the small, young, unstable and hard-to-reach firms that generated most new jobs (Birch, 1979: 48): ‘It is no wonder that efforts to stem the tide of the job decline have been so frustrating – and largely unsuccessful. The firms that such efforts must reach are the most difficult to identify and the most difficult to work with. They are small. They tend to be independent. They are volatile. The very spirit that gives them their vitality and job generating powers is the same spirit that makes them unpromising partners for the development administrator.’ Fischer and Reuber (2003) collated the perspectives of business owners, government policymakers and private sector advisors (venture capitalists, bankers, consultants) on support for rapid-growth firms. While all three groups agreed that management was critical, the private sector advisors believed that governments had no role. The business owners concluded that government support was unnecessary and should not be relied upon. The policymakers chose to differ, believing that governments have multiple critical roles regarding rapid-growth firms. If this study were replicated today, we expect the findings to be similar.

Several papers have advocated policy changes to the finance system to de-risk commercial lending to support innovative firms with growth potential (Brown and Lee, 2019; Coad and Srhoj, 2020; Hutton and Lee, 2012; Riding et al., 2012). Brown and Lee (2019) elucidate that this support should be targeted at small firms with growth potential rather than those already achieving high growth, a qualification made previously by Koski and Pajarinen (2013). Other calls have avoided such precise targeting and advocated for a broader scope and more systemic policy changes to facilitate innovation and growth (Hölzl and Janger, 2013; Segarra and Teruel, 2014; Terjesen et al., 2016). Mason and Brown (2013), in support of HGFs in Scotland, advocate for tailored government support for high-potential new ventures with conditions attached that prevent supported firms from being acquired by foreign companies. The same authors, with others (Mason et al., 2015), have also argued for a sector-agnostic approach to any government support for HGFs and that such support is more effective than subsidising start-up ventures because of the marginal nature of many start-ups. But almost all HGFs are, at best, transient, if not marginal. Still, in the Scottish context, Brown and Mawson (2016b) find that most Scottish HGFs have taken opportunities to expand overseas, with only 52% of their employment remaining in Scotland – they recommend policy support targeted at those HGFs with the greatest home economy impact. How such firms would be identified and monitored for compliance is not discussed. Many of these proposals or conditions for the channelling public money into HGFs depend on being able to locate high-growth potential ex ante, something that may become possible with the advent of AI technology (Hart et al., 2021), but practical attempts to do this have had only moderate success (Fafchamps and Woodruff, 2017; González-Uribe-Uribe and Reyes, 2021). Although Birch has advocated for selective HGF-oriented policies, scholars are aware of the policy-related issues outlined previously, which Birch raised some 35 years ago (Birch, 1979, p48). Nightingale and Coad (2014) talk persuasively about the pattern of increasing positive interpretation as research evidence moves into the policy arena, suggesting that policymakers are either unaware or choosing to ignore the growing scepticism about the benefits of HGFs. Brown et al. (2017) are also critical of the policymakers and challenge the ‘mythologies’ around HGFs that these individuals are perpetuating when the real question is whence these so-called mythologies. Nevertheless, these authors are correct in pointing out that the volume of evidence is now critical of government initiatives to support current or potential HGFs.

There are two main arguments against government support being dedicated to HGFs. First, as we do not yet understand what triggers (or ends) a high-growth episode, it is impossible to ‘pick winners’ before their high-growth phase, and selecting such firms during their high-growth phase is too late due to its short duration. Among the first to take this position was Birley (1987), based on her studies of employment growth in new ventures in Indiana. She advocates broad support for all ventures rather than trying to pick winners because employment growth is not the primary objective of founders, with future size primarily dictated by the start-up's employment size. This problem of identifying which firms to target and then how best to support either their faster and/or more persistent growth is now widely acknowledged (Anyadike-Danes et al., 2015; Coad et al., 2014a, 2014b; Daunfeldt and Halvarsson, 2015; Daunfeldt et al., 2016; Erhardt, 2021; Hölzl, 2014; Léon 2022; Terjesen et al., 2016). The second line of argument is that since these firms are either already growing (or have the potential to do so), providing public support will only reduce incentives within the firm (Brown and Mawson, 2016a; Daunfeldt et al., 2016; Koski and Pajarinen, 2013). This line of argument also links to the broader issue of public versus private benefits and the notion of market failure as the basis for government intervention (Mina et al., 2021; Terjesen et al., 2016): if a small group of firms expect to benefit from a rapid growth phase, are the consequent public benefits in terms of employment and productivity sufficient to justify financial support from the public purse? In 1971, the Bolton Report thought not. We cannot argue with Hart et al. (2021) that the preoccupation with HGFs, driven by policymakers’ dream of ‘picking winners’, has been at the expense of developing a better understanding of the growth process, one that is not circumscribed by somewhat arbitrary definitions of ‘high growth’ that very few firms, even growing ones, will ever achieve far less sustain (Coad et al., 2020).

Discussion and future research paths

High rates of business growth result from a complex and idiosyncratic process involving features internal to the firm and changing aspects of the local environment. Having immersed ourselves in this literature, we now appreciate two polar positions on HGFs. First, some might conclude that there is no such thing as an ‘HGF’. Some firms are lucky (or perhaps not!) to experience an episode of high growth, only one, and typically during its early years (Coad et al., 2013). Definitions are more trouble than they are worth by circumscribing high growth to a very exceptional transient episode in a firm’s life. Such definitions then send policymakers on a quest to find such firms, but by the time their growth is manifest, it is too late for policy intervention. The notable and ongoing focus on a relatively small number of HGFs has been to the detriment of research on the horde of more mundane SMEs that may never attain high-growth status (Aldrich and Ruef, 2018; Ben-Hafaiedh and Hamelin, 2023; Hart et al., 2021; Kuratko and Audretsch, 2021). These ordinary or mundane firms provide the professional industry infrastructure and other agglomeration economies that attract and sustain HGFs in different places. These non-HGFs also provide sustained employment and form the vital seedbed from which new HGFs will inevitably emerge. However, which firms attain this status, when, where, and why remain open questions that render it problematic to attempt to target policy support at HGFs.

The alternative view is that HGFs are an important and predictable phenomenon subject to managerial agency. Hence, scholars must continue defining, exploring, and understanding HGFs, even if the phenomenon makes up only a few per cent of the business population. These ongoing efforts are being facilitated by the increased use of extensive databases, which allow us to identify different types of growth, for example, accelerating, exponential and scaling. The failure of efforts to confirm a causal model of high growth using internal drivers suggests that idiosyncratic external factors are behind these growth episodes, both their onset and demise, for example, servicing a large B2B supply contract or receiving a large export order (Lee, 2014). Put another way, the growth path of an HGF will be unique in the same way that a fingerprint is unique to an individual (Vinnell and Hamilton, 1999). However, one internal factor Freel and Gordon (2022) identified is the negative effect of the high-growth experience on the motivation of owner-managers who may not have had a substantial growth ambition. Hence, the high-growth process carries the internal seeds of its own demise, and we see this as a line of inquiry worth pursuing.