Abstract

Prior research has highlighted coopetition as a successful strategy for enterprise performance during a crisis; this has largely focused upon large firms therefore, limiting our knowledge of network coopetition in micro-enterprises. This article explores the impact of network coopetition on the robustness of micro-enterprises during COVID-19. A survey and interviews with craft food producers in Sweden were conducted; a measurement for firm robustness was created, indicating that 46% of respondents had successfully weathered the pandemic and were thus, considered robust. The findings show that micro-enterprises employing network coopetition as a strategy during the pandemic exhibited robustness. This article stresses the importance of micro-enterprises that broadly embrace network coopetition to withstand the negative effects of crises.

Introduction

Periods of crisis, such as the COVID-19 pandemic, affect firms in diverse ways (Cortez and Johnston, 2020), with many being forced to re-evaluate their business models (Crick, 2020). Recent research has stressed the advantages of cooperation with competitors in times of crisis suggesting that organisations ‘. . .explore the potential mutual benefits of using coopetition strategies to yield higher-levels of performance, meeting unprecedented demand, operating efficient supply chains, or indeed, simply surviving within a volatile market’ (Crick and Crick, 2020: 211). Brandenburger and Nalebuff (1996) introduced the concept of coopetition as a competitive strategy for business development in the 1990s; it has continued to attract growing interest (Bengtsson and Kock, 1999, 2014; Bouncken et al., 2015; Czakon et al., 2014; Raza-Ullah, 2021). The main challenge in coopetition is managing the dynamics between value creation and appropriation, where value creation is the synergy that occurs between actors and value appropriation is how that value is distributed (Gernsheimer et al., 2021; Mizik and Jacobson, 2003). Value creation and value capture being beneficial outcomes means that there must be fair opportunities for the enterprises involved to benefit from the coopetitive relationship via knowledge sharing, knowledge gain and increased market performance (Gernsheimer et al., 2021).

Research on coopetition initially addressed the management and performance of large firms (Bengtsson et al., 2010). Recent studies have, however, shown that coopetition can be successful for smaller firms (Della Corte and Aria, 2016; Gnyawali and Park, 2009). Less attention has, however, been directed towards the smallest firms, that is, micro-enterprises – those with zero, or fewer than 10 employees (EU, 2023). Literature exploring how coopetition in these enterprises is managed is scarce (Granata et al., 2018). Since micro-enterprises are the most common category of firms (90.6% globally, and 92.6% in the EU) (OECD, 2021), they constitute an important cornerstone for all economic development. Because of their size, micro-enterprises may have difficulty using their resources and competencies optimally; this can, in some cases, restrict their business performance (Chirico et al., 2011; Wales et al., 2013). Coopetition in networks is considered a successful strategy for micro-enterprises in close geographic proximity to optimally use their resources and competencies (Granata et al., 2018). Through network coopetition, micro-enterprises may simultaneously collaborate and compete in networks to access resources and competencies that complement their internal capabilities; such network coopetition can be formal or informal (Gernsheimer et al., 2021). In times of crisis, the use of network coopetition can be even more important for micro-enterprise robustness. Robustness in this context refers to an enterprise’s ability to withstand challenges and maintain functionality in times of crisis; this differentiates the term from the concept of resilience, which is comprised of a crisis impact followed by recovery (Munoz et al., 2021).

When firms are faced with a crisis whose consequences are not fully known, previous alliances and cooperation with competitors may be at risk (Katare et al., 2021). Since less attention has been paid to examining the impact of crises on micro-enterprises (Doern, 2016; Crick and Crick, 2020; Herbane, 2013), little is known about how they use coopetition as a strategy to withstand their affects, that is, whether coopetition results in robustness (Kallmuenzer et al., 2021). This article examines how network coopetition was used in micro-enterprises in the craft food industry during the COVID-19 pandemic and the extent to which coopetition was used as a strategy for robustness during this crisis. Accordingly, the aim of this article is to explore the impact of network coopetition on the robustness of micro-enterprises in times of crisis. The following research question guided the case study: How does coopetition affect micro-enterprise robustness in times of crisis? The Swedish case of REKO (fair consumption) serves as an example of network coopetition between craft food entrepreneurs (Aitojamakuja, 2022). Within REKO, competing producers from the local market voluntarily come together to collaborate, network and exchange knowledge: small-scale craft food producers together offer an attractive marketplace to customers, that is, they create shared value (Kramer and Porter, 2011).

The article is organised as follows. First, we review the literature on coopetition with a special focus on small business network coopetition in times of crisis. Second, we outline the methodology and propose an index that can be used to measure small business robustness. We then discuss the findings regarding the importance of network coopetition for micro-enterprise robustness in times of crisis. Implications for small business coopetition theory conclude the article.

Literature review

Coopetition in small enterprises

The concept of coopetition was introduced in the mid-1990s as a competitive strategy for business development (Brandenburger and Nalebuff, 1996). Since then, there has been a growing interest in understanding this phenomenon and the impact of coopetitive relationships on business value creation and value capture (Dowling, 2020; Gnyawali and Ryan-Charleton, 2018). Coopetition has been referred to as ‘a paradoxical relationship between two or more actors simultaneously involved in cooperative and competitive interactions, regardless of whether their relationship is horizontal or vertical’ (Bengtsson and Kock, 2014: 182), a definition that distinguishes coopetition from collusion (Ding et al., 2022). Coopetition arises out of a mutual interest in taking advantage of the interaction and expectations of mutual give and take; that is, creating a ‘win-win’ relationship (Bouncken et al., 2015; Bouncken and Kraus, 2013; Hitt et al., 2011; Pathak et al., 2013) to increase the opportunities for the firm to achieve more value beyond what could be achieved individually. Coopetition may strengthen mutual trust and benefits between the competing firms while reducing uncertainty (Bouncken and Fredrich, 2011; Morris et al., 2007). However, prior research has mainly investigated the motives and outcomes of coopetition in large and medium sized firms; very little continues to be known about coopetition among the smallest, that is, micro-enterprises (Granata et al., 2018; Lindström and Polsa, 2016; Thomason et al., 2013).

When several small firms are geographically located in the same area, their business intentions and goals are similars, and they strive for access to additional resources, coopetition is likely to occur (Bouncken and Kraus, 2013; Corbo et al., 2022). By collaborating with competitors, small firms may gain advantages in performance (von Friedrichs Grängsjö, 2003; Kallmuenzer et al., 2021; Kuhn and Galloway, 2015). Granata et al. (2018) emphasise that the management of micro-enterprise coopetition could occur in highly formalised structures. These results contrast with previous studies showing that strategies in micro-enterprises are otherwise characterised by more intuitive strategy development (Liberman-Yaconi et al., 2010). Nevertheless, small firms engaging in coopetition means mutual benefits must emerge for all actors involved, that is, improved market position and influence, while promoting long-term orientation (Kraus et al., 2019). Even though the initial level of coopetition analysis has occurred on the value net level (Brandenburger and Nalebuff, 1996), most attention has been given to the dyadic relationships between two enterprises (Czakon, 2018). Recent research has drawn attention to a shift beyond dyadic coopetition, recognising that collaboration between enterprises may even involve other stakeholders such as customers, rivals, complementors and suppliers in a joint effort to increase the ‘business pie’, offering more value than that cumulatively available from each individual actor (Brandenburger and Nalebuff, 1996; Czakon, 2018). This coopetition perspective shift has been presented as capable of opening up the network level of analysis in coopetition research (Sanou et al., 2016; Wilhelm, 2011).

‘Network coopetition refers to multiple actor interactions involving various firms covering the entire value net’ (Czakon, 2018: 2). Network coopetition includes coopetition among multiple enterprises towards a common goal of increasing market access, profitability and knowledge exchange (Czakon, 2018; Gernsheimer et al., 2021). This may involve many actors in a joint effort to enhance the offering with more value than would be possible for any individual stakeholder (Brandburger and Nalebuff, 1996; Czakon, 2018). One part of network coopetition that has recently gained increasing interest amongst researchers includes coopetition activities in niche industries where various collaborations can play an important role (Gernsheimer et al., 2021). Networks or communities that engage in coopetitive activities are likely to be characterised by mutual trust between the individual enterprises (von Friedrichs and Gummesson, 2006). This is especially true for micro-enterprises, as mutual respect is here a core foundation of coopetition (McGrath and O’Toole, 2017). Nevertheless, there are potential challenges and risks when firms become involved in network coopetition relationships, including distrust, tension and opportunistic behaviour, all of which are known to emerge from the contradictory foundation of coopetition among cooperating competitors (Crick, 2020; Crick and Crick, 2021; Doern et al., 2016; Raza-Ullah and Kostis, 2019).

A driver of network coopetition is co-location, that is, the spatial concentration of stakeholders (von Friedrichs and Gummesson, 2006; Grauslund and Hammershøy, 2021). Network coopetition can involve competing small or large firms, or a combination of both, and can be observed in the form of informal industry networks, while noting that these networks most commonly involve only micro-enterprises (Devece et al., 2019; Granata et al., 2018). In times of crisis, both the benefits and the risks of network coopetition may increase. Studies on the effects of coopetition strategies in micro-enterprises in times of crisis are still scarce (Czainska e al., 2021; Gast et al., 2019; Gernsheimer et al., 2021).

Coopetitive strategies in times of crisis

Crises are unexpected and rare events that have a major impact on society (Ratten, 2020). In times of crisis, certain resources can become scarce which may encourage or force firms to re-consider their business strategies (Katare et al., 2021). It has been shown that crises can have a particularly strong impact on smaller firms due to their lack of slack resources so they are more vulnerable to unexpected events (Doern, 2016; Runyan, 2006). Prior research suggests that collaboration among such firms may help them meet such challenges (Ireland et al., 2003; Ketchen et al., 2007) where they can use a combination of resources, competencies and survival traits to cope with environmental changes caused by crises (Katare et al., 2021; Sirmon and Hitt, 2003). These kinds of survival traits may also include coopetition in micro-enterprises, with evidence suggesting they: ‘are inclined towards cooperation due to their limited size and resources, along with their strong social ties’ (Kallmuenzer et al., 2021: 1). It has been noted that there is a strong link between small firms and extensive local coopetition where such firms collaborate with competitors to benefit their long-term business orientation by nurturing ties to the geographical area in which they operate (Gast et al., 2019; Guenther et al., 2022). Consequently, local network coopetition may be a survival strategy that plays a decisive role in the ability of small businesses to remain viable and robust when conditions change due to external factors (Darbi and Knot, 2022).

It has been suggested that collaboration between competing enterprises in times of crisis has a positive effect on the performance of participating firms (Bagshaw and Bagshaw, 2001; von Friedrichs, 2010; Mathias et al., 2018), as well as on non-economic exchanges such as information and social exchange (Bengtsson and Kock, 2000; von Friedrichs Grängsjö, 2003; Kotzab and Teller, 2003). For micro-enterprises, their size may be a restriction in terms of the ability to influence the market; consequently, they must rely on their own resources and develop strategies for resource complementarity in the local vicinity. It was shown during the COVID-19 crisis that many such firms searched for alternative ways to survive (Katare et al., 2021) through, for example, local network coopetition. Prior research has shown that inducing changes in business models and seizing opportunities in times of crisis has a positive influence on such firms (Guckenbiehl and Corral de Zubielqui, 2022).

An important prerequisite for successful coopetition includes the healthy balance between cooperation with competitors, and the nurturing of individual enterprise capabilities and knowledge. It has been shown that there can be barriers to collaboration between entrepreneurs and competitors, meaning that the establishment of coopetition requires a certain amount of effort (Veal and Mouzas, 2010). A lack of trust, in particular, may challenge coopetitive relationships (Raza-Ullah, 2021), making it difficult to find suitable partners; there is always a risk of trade-offs in terms of knowledge exchange where firms protect their competencies (Chiambaretto et al., 2020). Evidence suggests that micro-enterprises are more likely to engage in coopetitive activities where the benefits often exceed the risks, while larger firms have less to gain from coopetition with rivals (Bengtsson and Johansson, 2014; Gernsheimer et al., 2021). Firms involved in coopetition usually seek common ground for their coopetitive activities; this may decrease the risk of opportunistic behaviour, tension or failed partnerships (Crick et al., 2022; Gernsheimer et al., 2021; Fernandez et al., 2014). Despite the potential obstacles and opportunities associated with coopetition, especially in networks, research is still limited regarding network coopetition in niche industries and under special circumstances (Gernsheimer et al., 2021).

The COVID-19 crisis and robustness of small enterprises

As with previous crises (Love and Roper, 2015), some business sectors experienced a considerable loss of value during the COVID-19 pandemic (Sanderson Bellamy et al., 2021). Some of the challenges faced when general economic conditions change during a crisis include maintaining competencies (e.g. human and financial resources) and how to survive (Runyan, 2006; Schepers et al., 2021). Robustness refers to the ability to withstand a crisis while maintaining stability and, thus, how sensitive the organisation is to uncertain events (Munoz et al., 2021). Robust enterprises usually maintain operations throughout a crisis with the help of financial buffers and other resources, even though it is important to remember that during a prolonged crisis, the chances of maintaining robustness are reduced (Munoz et al., 2021; Runyan, 2006). By engaging in coopetition with other local firms, small enterprises may gain access to more resources and competencies, increasing their robustness and ability to withstand disruption (Kallmuenzer et al., 2021).

The OECD (2021) has shown that the impact of the COVID-19 pandemic varied in different countries and that several factors, besides geographical location, affected places, people and businesses. The pandemic had a significant global impact on society (ONU, 2020), radically changing the conditions for entrepreneurial activities. When a firm is affected by unpredictable external events that have a major impact on society, previously taken-for-granted business models are challenged such that they need to critically evaluate their strategies (Shafer et al., 2005). Although research often focuses on the negative effects of crises (Doern, 2017), these can also stimulate businesses to capitalise on new opportunities (Brünjes and Revilla-Diez, 2013). Robustness and survival may also depend on closer relationships with competitors in times of crisis (Crick and Crick, 2020; Katare et al., 2021). These kinds of strategies can be essential, especially for small- and micro-enterprises as small- and medium-sized enterprises and micro-enterprises were likely to have more limited access to government business support initiatives based on macroeconomic measurements inapplicable to such ventures (Boter and Lundström, 2005). Although a few studies have explored the way crises, such as the COVID-19 pandemic, disrupt the activities of entrepreneurs (Kraus et al., 2013; Sharma et al., 2022), little is still known about how micro-enterprises use coopetition as a strategy to withstand a crisis, that is, whether coopetition results in robustness.

Research design

Research context

During the COVID-19 pandemic, intrusive restrictions were introduced on a global basis. While many countries implemented a complete lockdown to stop the spread of infection, some countries chose a different path (ONU, 2020). Sweden implemented different restrictions, such as working from home, limited opening hours, limitation of group size when meeting and social distancing. Accordingly, in November 2020, the Swedish government decided that public gatherings and public events with more than eight participants would be temporarily prohibited, and that violations could result in fines and imprisonment (Swedish Ministry of Social Affairs, 2021). The demand for different craft food products saw significant changes, both increasing and decreasing due to new regulations and restrictions. Prior to the COVID-19 pandemic, small craft food producers largely generated income in local marketplaces such as fairs and farmers markets, where they usually encountered other business owners in informal networks. These local marketplaces were closed during the pandemic (Swedish Ministry of Social Affairs, 2021), and the absence of local marketplaces inhibited networking opportunities for knowledge exchange and resource sharing. However, prior to the pandemic, several craft food entrepreneurs had joined REKO as a complement to local fairs and farmers markets. REKO is an organic, loosely organised collaboration between non-industrial craft food entrepreneurs, centred around ethically, locally and organically produced products with transparency in the production processes (Aitojamakuja, 2022). Within REKO, entrepreneurs offer customers an attractive concept for locally produced food while competing to be the customer’s primary choice (c.f. Bouncken et al., 2015; Brandenburger and Nalebuff, 1996). REKO, as a result, offered an alternative distribution channel for many craft food entrepreneurs in Sweden during the pandemic with new entrepreneurs joining the collaboration.

The idea of REKO started in Finland in 2013 and was established as a buying and selling collaboration between local food producers and consumers in their immediate vicinity (Snellman, 2021). The REKO model offers a way for consumers and producers to meet directly through a REKO ring where craft food products are sold within a specific geographical area (Aitojamakuja, 2022).

As it is hosted on Facebook, everything is transparent, and you can see the sales and offerings of all the other producers. Whilst this might seem counterintuitive for business to some sellers, [. . .] this creates a healthy kind of competition where everyone is encouraged to perform and refine their products and presentation (Snellman, 2021: 59).

REKO is not only a distribution platform. It also offers a network for collaboration and knowledge exchange between competitors with a mutual goal of increasing customer value while benefiting the individual enterprises. REKO is built on seven principles (Hushållningssällskapet, 2021): only food and direct by-products from own food production; only sales of own products; no intermediaries; the products are pre-ordered prior to each delivery; each order is an individual agreement between buyer and seller; trust between all parties in the form of an honest and fact-based dialogue; and cost-free participation. Contact is often made via Facebook groups but can also be made in other ways (Kumar et al., 2021). With REKO, producers gain a better negotiating position in relation to the retail trade. Deliveries were able to continue during the pandemic thanks to cooperation with local municipalities, which decided on delivery locations (often large car parks or similar spaces) where customers could remain in their cars – a form of ‘drive-through REKO concept’ (Snellman, 2021).

Study and sample

We primarily used a quantitative method in our exploration of how coopetition affects micro-enterprise robustness in times of crisis. The quantitative study was motivated by the fact that prior research has mainly been interpretative and that there is a demand for studies that can increase ‘the validity and generalisability of the research’ (Bouncken et al., 2015: 592). However, due to the complex nature of the phenomenon, a number of interviews were included in order to achieve an in-depth understanding of the research question (Bouncken et al., 2015).

The data collection process consisted of a web-based survey sent to 160 food micro-enterprises, along with interviews with 14 craft food enterprises located in eight Swedish municipalities. One of the municipalities was the central town of a region with over 64,000 inhabitants; the other municipalities were very rural, having 5,000–15,000 inhabitants in 2022 (Statistics Sweden, 2023). The respondents mainly operate micro-enterprises with a few having up to 25 employees. The web-based survey was conducted in the autumn of 2021 and included enterprises with activities in the craft food industry in the county of Jämtland. The respondent addresses were extracted via the website Eldrimner (www.eldrimner.com) and the Facebook pages of eight REKO rings. The response rate was 32% (51 responses). The respondents were anonymised, and the data were processed in SPSS. Questions raised in the survey, in addition to the characteristics of the firms and respondents, included how the firm was affected by the pandemic, what measures had been taken and expectations for the future. Appendix 1 shows that the majority of respondent firms were micro-enterprises (88%), 35% were REKO producers before the pandemic, with 28% joining during the pandemic. The 14 in-depth interviews aimed to further explore the research question and were conducted in Spring 2022 using structured questions about how producers had managed during the pandemic, their attitudes towards coopetition within REKO, and the level of coopetition during the pandemic. Each interview lasted 45 minutes. Two researchers participated in each: the answers were transcribed and analysed using thematic content analysis to discover common issues (Miles and Huberman, 2003). Most of the respondents were working full time in the firm with a small number of employees; most firms were family-owned with membership in one or several REKO rings (see Appendix 2).

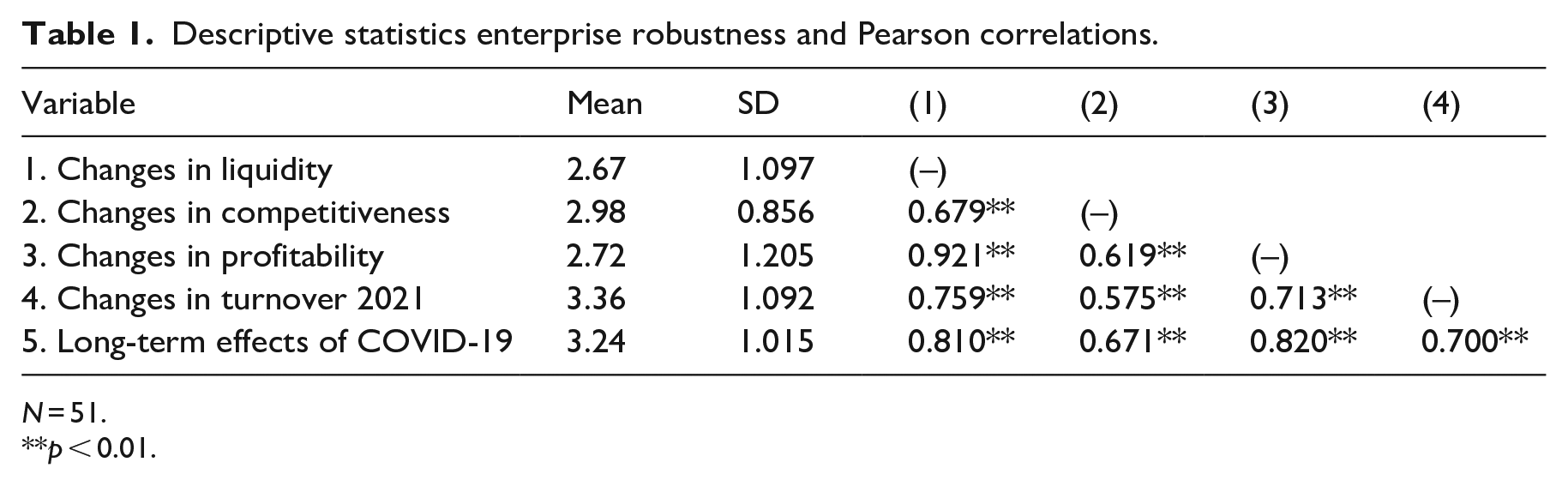

Based on the survey data, we constructed a measure to identify robustness for the craft food entrepreneurs during the COVID-19 pandemic, following prior research highlighting the importance of (1) coping with changes in the business environment (Bouwman et al., 2008), (2) survival and long-term sustainability (Schutte and Mberi, 2020), and (3) the continued operation of the business despite closures and restrictions (Mignenan, 2021). We created the measure (Table 1) based on the following question in the web-based survey: How has the COVID-19 pandemic affected the enterprise in terms of liquidity, competitiveness and profitability? We used a five-point Likert-type scale, anchored by 1 = Much lower than before the COVID-19 pandemic, to 5 = Much higher than before the COVID-19 pandemic. Note that the comparison year that the respondents referred to was 2019, that is, before the pandemic. We also included the following two questions: How is turnover expected to be in 2021? and What is the long-term effect of the COVID-19 pandemic expected to be? with a five-point Likert scale of 1 = strongly negative to 5 = strongly positive.

Descriptive statistics enterprise robustness and Pearson correlations.

N = 51.

p < 0.01.

Table 1 shows the strong correlation between the variables. The coefficient alpha for enterprise robustness was 0.93. To be classified as a robust enterprise, the enterprise robustness value had to exceed 3 (i.e. unaffected by the pandemic).

We used different variables based on prior research to explore the research question.

Dependent variable

Robustness

Robust enterprises were coded 1; the others were coded 0; 46% of the respondents were considered as robust enterprises.

Independent variables

Cooperation

The question: How has cooperation with other enterprises changed during the pandemic? was used to explore the effect of cooperation. We used a five-point scale anchored by 1 = significantly reduced to 5 = significantly increased (mean value, 2.8).

Coopetition refers to the notion that cooperation and competition can coexist and includes both value creation and value appropriation (Brandenburger and Nalebuff, 1996; Bengtsson and Johansson, 2014). To explore coopetition, we asked: Is the enterprise a REKO producer? Possible answers were: (i) Yes, the enterprise was a REKO producer even before the pandemic; (ii) Yes, the enterprise became a REKO producer during the pandemic; and (iii) No, the enterprise is not a REKO producer. The answers were dichotomized and we coded the first two alternatives as coopetition with 1 and the third alternative with 0.

Control variables

Control variables included:

■ Age of Business. We used the starting year. Mean value, 2007

■ Age of Respondent. We used the year of birth as a measure of age. Mean value, 1968

■ Gender. Women were coded as 1, men as 0

■ Education. We used a four-point scale anchored by 1 = compulsory school, 2 = upper secondary school, 3 = higher education (3 years), 4 = higher education (more than 3 years). Mean value 2.73

■ Numbers of Employees. Mean value 2.5

■ Access to Broadband. The following statement was used: The enterprise has access to well-functioning broadband. A five-point scale anchored by 1 = not at all/to a very low extent to 5 = to a very high extent. Mean value 3.58

■ Personal Network. The following question was used: To what extent have personal networks been significant during the pandemic? A five-point scale anchored by 1 = not at all/to a very low extent to 5 = to a very high extent. Mean value 3.18

■ Financial Buffer. To what extent did you have a financial buffer before the pandemic? A five-point scale was used anchored by 1 = not at all/to a very low extent to 5 = to a very high extent. Mean value 2.44

■ Received support. The following question was used: What is the total amount of support during the pandemic? A nine-point scale was used, anchored by 1 = The enterprise did not receive any support to 9 = More than €500,000. Mean value 2.07

Data analysis

We first conducted a one-way ANOVA test to examine how coopetition affected firm robustness. We then continued analysing the data using a binomial logistic regression model, which estimated the probability of different occurrences, in this case, the robustness of small firms in times of crisis. The logistic regressions were performed in three steps. We first controlled for the influence of five of the respondent characteristics on the likelihood of robustness. In Step 2, we then added different prerequisites such as access to broadband, network, internal preparedness (i.e. a financial buffer), and access to financial support. In Step 3, we added the variables cooperation and coopetition to the variables used in Steps 1 and 2. Maximum likelihood estimations were used to calculate the logit coefficients, which denote changes in the log odds of the dependent variable. We assessed the fit of the models using Pearson’s Chi-squared test and pseudo-R2. Using the Wald statistics, we tested the significance of the individual independent variables. The Findings and Analysis section below presents the craft food producers in the study and how the pandemic impacted their operations. We then continue analysing the characteristics of coopetition enterprises and the attitude towards coopetition between enterprises in local proximity. The ANOVA test is used to identify the differences between the enterprises, and the qualitative data are presented using quotations, interspersed with the results from the quantitative study. Finally, we test the Robust index and explore RQ1, that is, how coopetition affects the robustness of micro-enterprises.

Findings and analysis

The quantitative sample and the COVID-19 pandemic’s impact on craft food producers

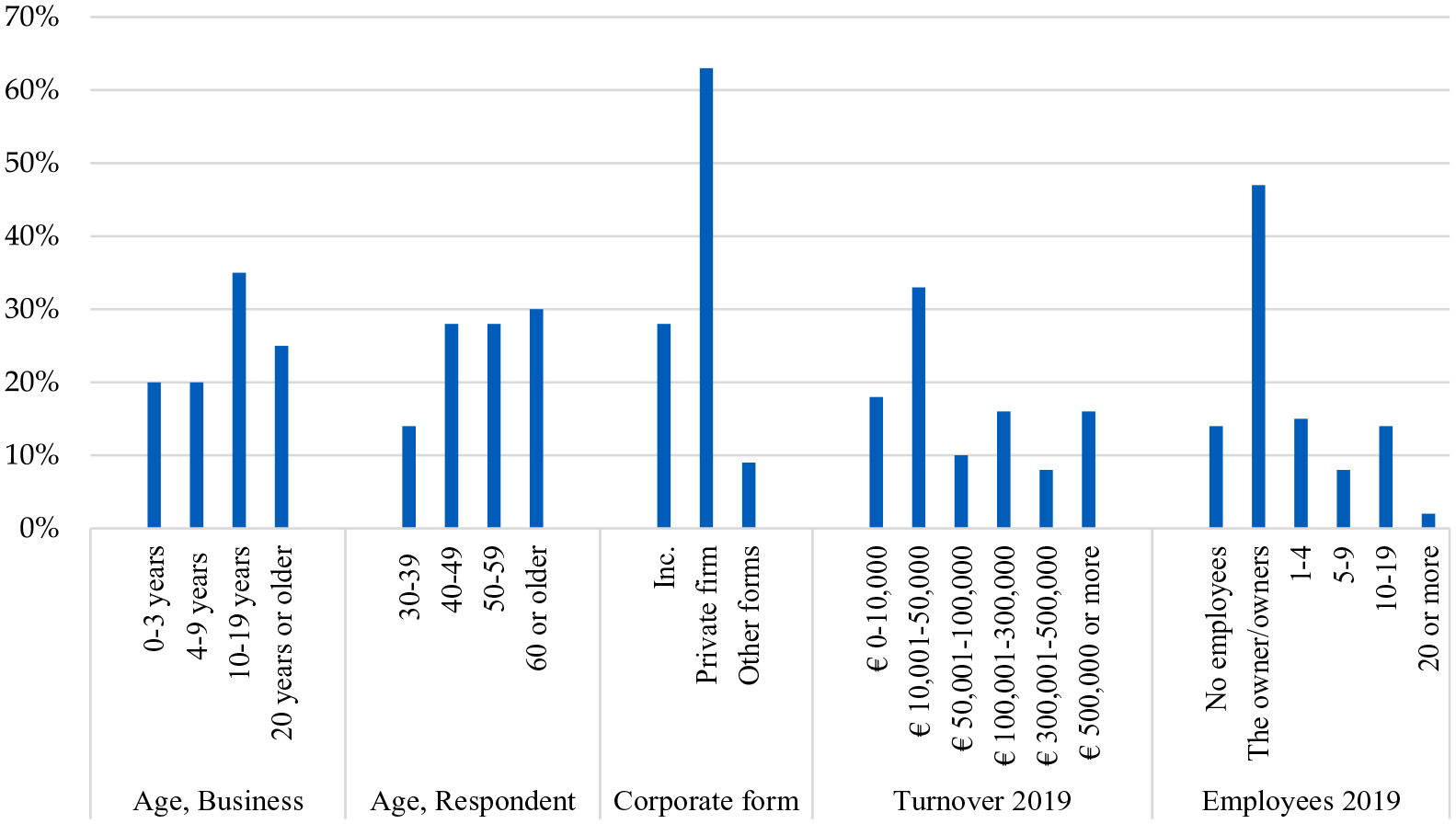

The results from the questionnaire showed that most of the respondents have been operating their businesses for a considerable time; 35% were more than 10 years old, and 25% were more than 20 years old. The average age of the business owners was 52. Those who responded to the survey tended to have a high level of education, and most of them had the business as their main source of income (70%). The most common business form was private enterprise (63%), and about 67% of the businesses had only one owner. Sixty-three percent of the respondents were women. The turnover in 61% of the enterprises was less than €100,000, and 61 % had no employees (Figure 1).

Data sample description.

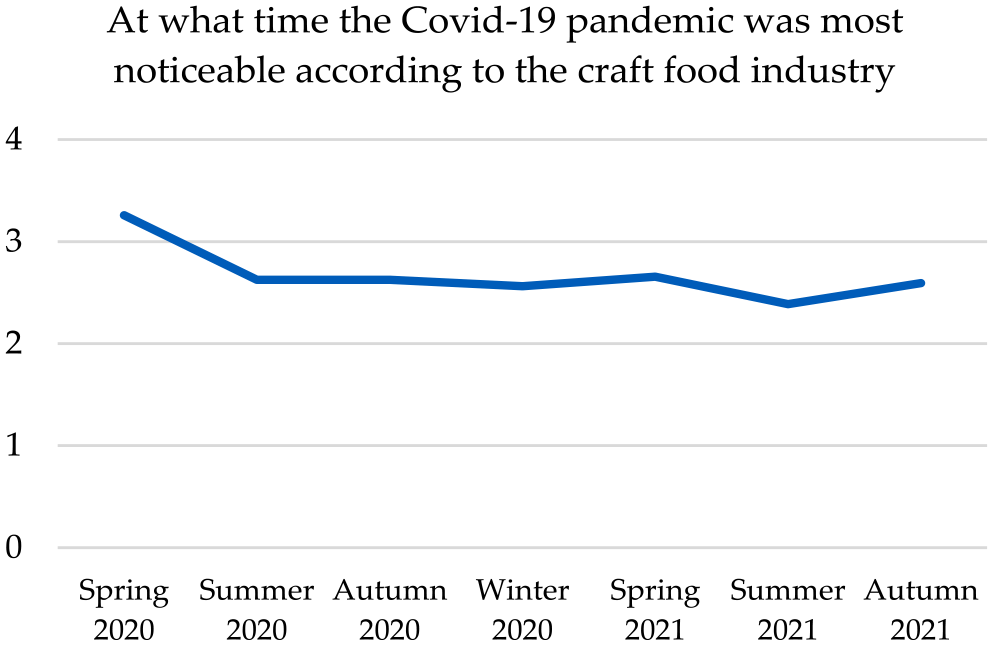

Most of the respondents (60%) stated that the COVID-19 pandemic affected the general craft food industry (at an aggregated level) to a high or very high degree. Since this crisis continued for an extended period of time, it may also have affected businesses differently depending on the season. One question posed was therefore: At what time was the pandemic most noticeable for your enterprise? The results show that the pandemic was most noticeable in the beginning in the spring of 2020. However, the craft food entrepreneurs included in the survey stated that their businesses were not extensively affected by the pandemic. This can also be seen in the results in terms of financial support, as 60% of the respondents did not receive any at all. Figure 2 shows that the impact of the pandemic diminished over time. This result is also confirmed by prior research, where different phases of the crisis were identified, that is, tougher phases and phases of recovery (Gursoy and Chi, 2020).

COVID-19 pandemic impact over time.

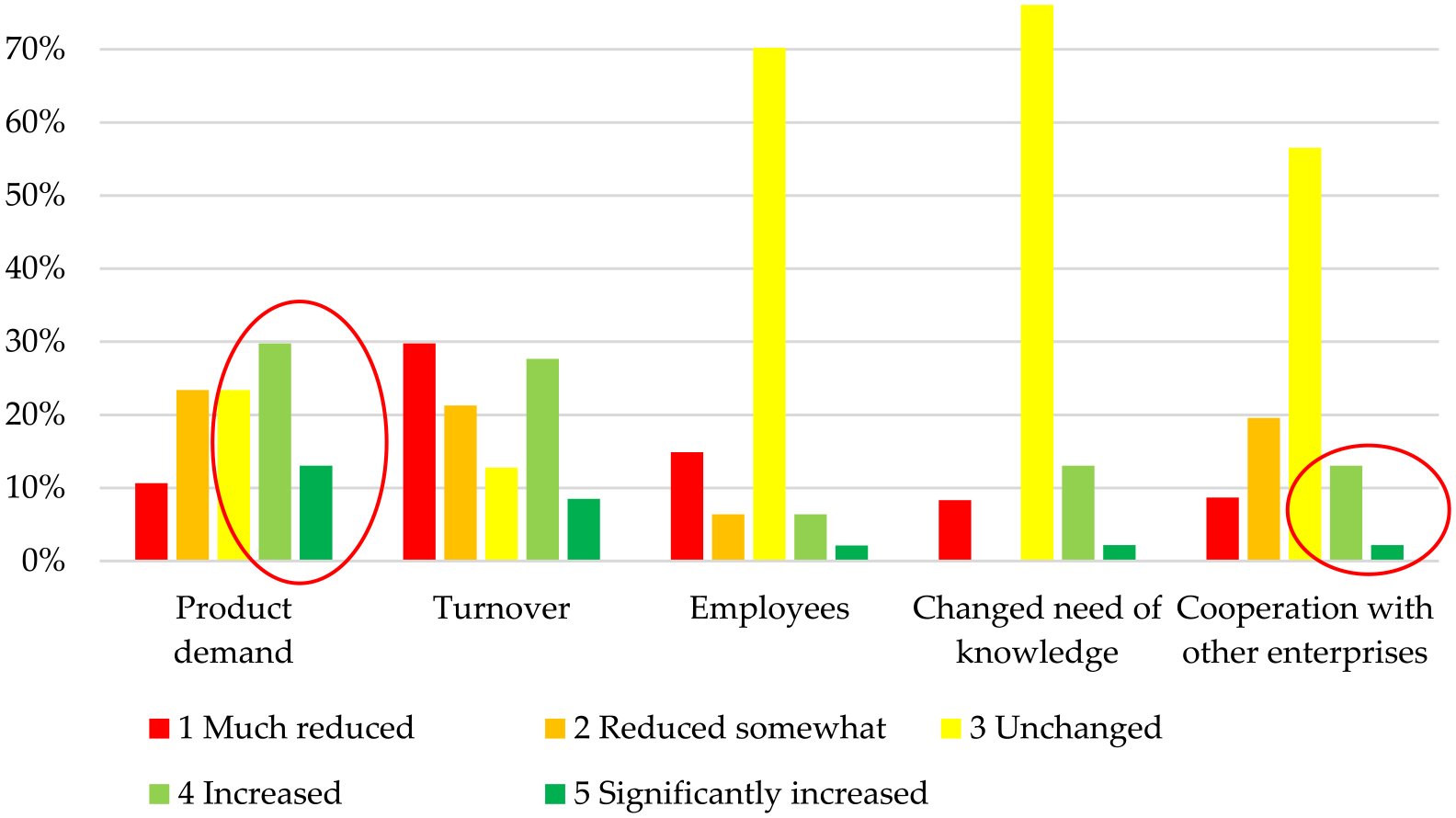

Evidence indicates that the COVID-19 crisis affected firms in various ways (Schepers et al., 2021). Figure 3 shows how the pandemic affected various aspects such as demand, turnover, number of employees, changed knowledge needs and collaboration compared to the situation before the pandemic. Figure 3 furthermore shows that the pandemic primarily presented challenges in terms of reduced turnover (51%). It is, however, notable that 43% of respondents experienced higher product demand and 37% had higher turnover during the pandemic. The majority (70%) reported that the number of employees was unchanged compared to before the pandemic.

COVID-19 pandemic and business challenges.

In terms of increased strategic challenges such as the need for new knowledge or changed cooperation, the respondents did not report that the pandemic presented a need for increased knowledge. About one-third (36%) reported that they collaborated with other, similar firms, to a high or very high degree before the pandemic. This collaboration was unchanged for the majority of the firms (57%). A smaller number reported a decrease (29%) compared to their collaboration before the pandemic. Fifteen percent reported increased collaboration during the pandemic.

Characteristics of coopetition enterprises

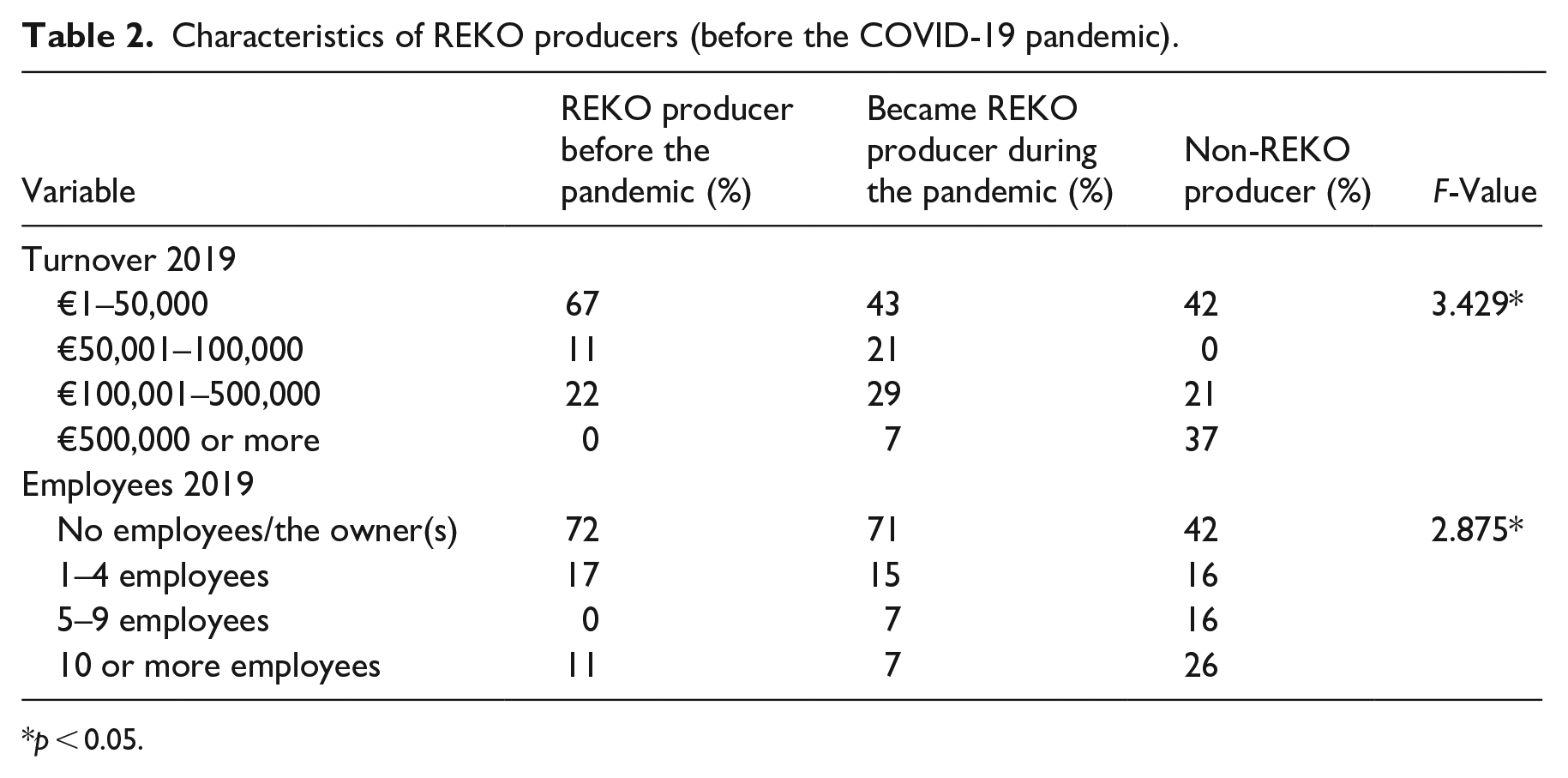

The REKO producer respondents mainly operate micro-enterprises; there are significant differences in both turnover and the number of employees between the craft food producers who are part of REKO and those who are not. For example, the majority of the respondents in the survey who were not REKO producers had a turnover in 2019 of over €100,000, and almost a third of the non-REKO producers had more than 10 employees, that is, they were considered small firms rather than micro-enterprises (see Table 2).

Characteristics of REKO producers (before the COVID-19 pandemic).

p < 0.05.

Table 2 also shows that those who joined REKO during the pandemic were somewhat larger compared to those who joined before. The ANOVA test shows significant differences (p < 0.05).

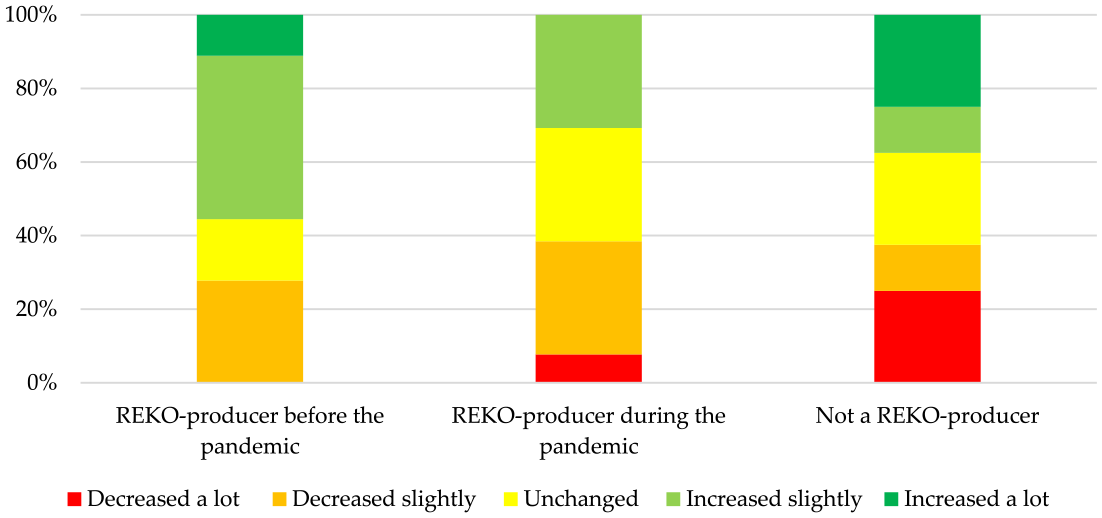

Figure 3 shows that the demand for craft food products increased during the pandemic; this is in line with prior research (Skoglund and Rennemo, 2022). A further investigation of change in demand shows that there were significant differences between those who were REKO producers compared with those who were not (see Figure 4).

The demand for craft food products compared to before the COVID-19 pandemic.

Figure 4 shows that none of the respondents who joined a REKO ring before the pandemic considered themselves to have a significantly reduced demand. This was also confirmed by the interviews: ‘We experienced higher sales numbers during the pandemic, and we believe that people valued small enterprises even more during the pandemic’ (R7, 2 owners). However, 33% of those who did not participate in REKO experienced decreased demand. Those who were involved in REKO before the pandemic were also most likely to state that they had increased (44%) or highly increased (11%) demand for products during the pandemic. However, the results show that 25% of those who were not REKO producers also had highly increased demand.

The interviews confirm the importance of REKO for the very smallest producers: ‘We have had 100% of our sales and distribution through REKO’ (R2, 2 owners), and ‘Our sales through REKO are about 65%–70% out of our total. We needed higher sales numbers during the pandemic, and we thought that REKO could be good for our marketing’ (R9, 2 owners and 1 part time employee). The larger producers mainly joined REKO at the start of the pandemic; when revenues did not decrease as much as anticipated, they withdrew from REKO. ‘We joined REKO in the autumn of 2020, but it was nothing for us. Too much administration and too long journeys in relation to sales. But it is good that REKO exists for the smaller producers’ (R6, 7 employees).

The importance of REKO also extended beyond distribution issues: ‘We participate in REKO and other collaborations to manage risks better’ (R14, 10 employees). The respondents also used REKO as a network for inspiration and knowledge exchange with other entrepreneurs. As one of the interviewees stated: ‘Other values that are connected to REKO include knowledge exchange, for sure. Networking is also an important part of REKO. Producers inspire each other through the interaction’ (R5, owner and five employees). These findings support prior research by Brunetto and Farr-Wharton (2007), who observed that networking and collaboration increased a range of new business opportunities that benefit small firm development. An owner of one of the larger firms interviewed stated that ‘Since we joined REKO during the pandemic, we have a better direct connection with our private customers, however, we are not at all dependent on REKO for our survival’ (R14, 10 employees).

Coopetition and enterprise robustness

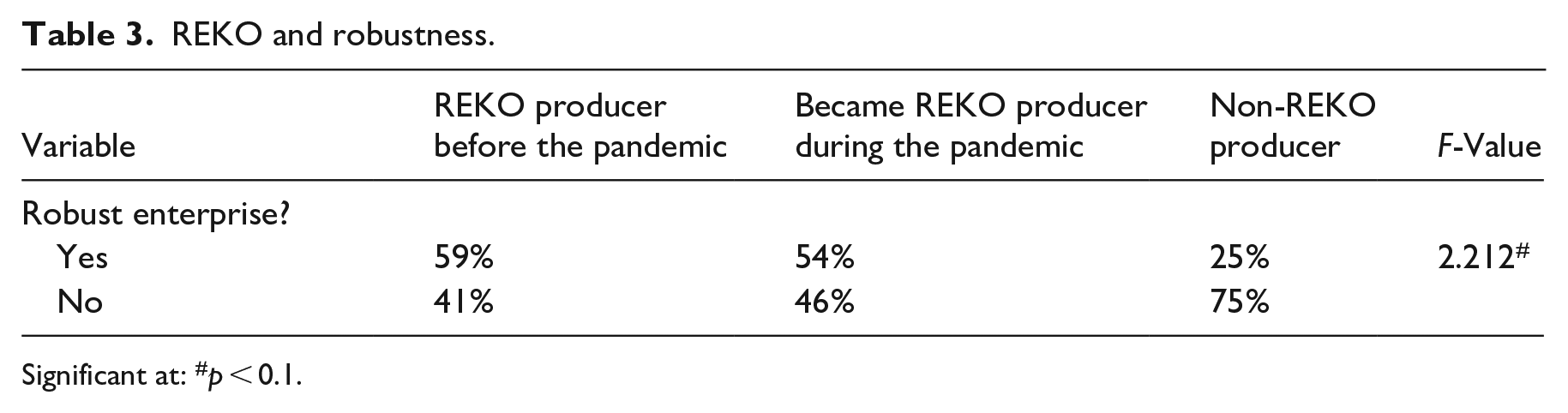

To answer the research question, that is, to explore how coopetition affects micro-enterprise robustness, we initially conducted a one-way ANOVA test to determine whether coopetition affected enterprise robustness in times of crisis. We found a positive relation between coopetition and robustness (p < 0.1). Table 3 presents the results.

REKO and robustness.

Significant at: #p < 0.1.

The table shows that the majority of those who joined REKO before the pandemic, as well as those who joined during the pandemic, are considered robust enterprises.

Beliefs regarding the future and business growth differed between those who were part of the REKO group and those who were not. Approximately 50% of those who participated in the REKO group believed that the pandemic would have long-term positive effects. By comparison, 31% of those who were not REKO members believed that the pandemic might have positive effects for their business. Among those who were members of REKO, 61% believed that sales would increase in the future compared to the 25% among those who were not members (p < 0.01).

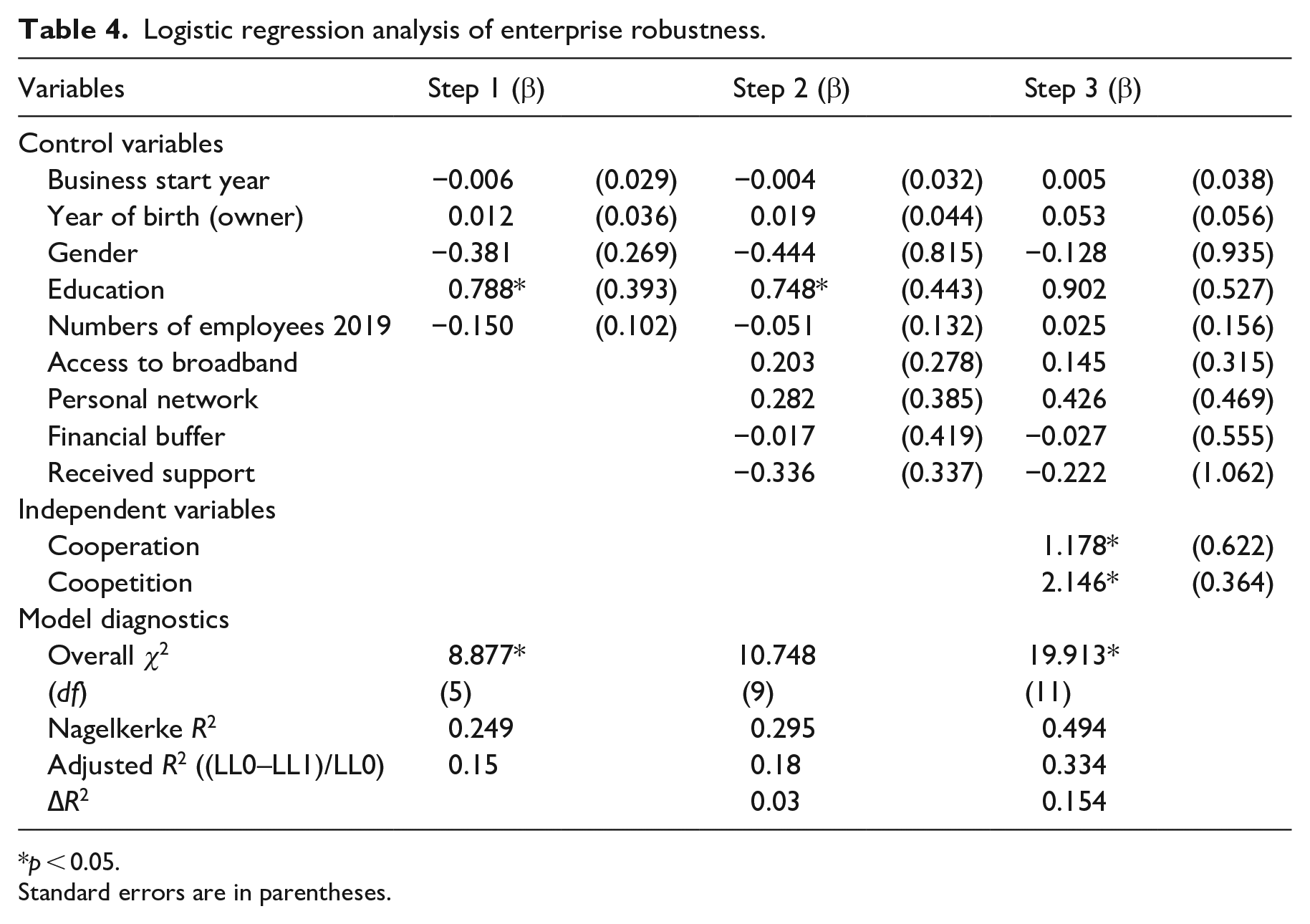

A logistic regression was performed to further explore the factors that affect enterprise robustness. In an analysis of age (business and individual), gender, education level, number of employees, broadband access, personal network, financial buffer, access to support, and increased cooperation and coopetition due to REKO membership, we found two significant factors that increased the likelihood of robustness: increased cooperation during the pandemic (p < 0.05) and membership in REKO (p < 0.05).

The results in Table 4 indicate that after testing the effects of the control variables, independent variables such as cooperation and coopetition explain much of the variance in enterprise robustness (ΔR2 = 15.4%), with a significant, positive effect for cooperation and coopetition in Step 3.

Logistic regression analysis of enterprise robustness.

p < 0.05.

Standard errors are in parentheses.

The interviews illustrated that REKO producers also cooperated with competitors in other ways: ‘We also cooperate regarding purchases and through markets and festivals, etc.’ (R7, 2 owners). Collaborations mainly took place in the business areas of sales, transportation, organisational development and idea exchange; they were executed to increase revenue, implement effective sales and add local value. A respondent from one of the larger firms in the study highlighted a reason why they did not use coopetition within REKO during the pandemic: ‘We did not need to collaborate much in order to survive the pandemic. We received governmental business support and that helped us a lot’ (R13, 25 employees).

Discussion

Coopetition in micro-enterprises in challenging times

REKO may be defined as network coopetition between craft food entrepreneurs, as it has provided, and continues to provide, a local network for small craft food producers to come together, allowing competing small- or micro-enterprises to achieve the same goal: that is, contribute to local development via local craft food (Czakon, 2018; Granata et al., 2018). During the COVID-19 crisis, when local fairs and marketplaces were closed, the craft food producers worked in cooperation with local municipalities to keep the REKO rings open despite the restrictions arising from the crisis. Since there were not many other distribution alternatives for small craft food producers, REKO membership (both producers and customers) increased during this time and became an avenue for achieving enterprise robustness. The findings show that the craft food producers changed their business models or strategies in this manner to remain robust during the crisis and manage risk better (Guckenbiehl and Corral de Zubielqui, 2022). This result adds to prior research that pinpoints the increase in coopetition among small enterprises in particular, where there is a need to share resources and knowledge to reduce uncertainty and risk (Ireland et al., 2003; Kallmuenzer et al., 2021; Ketchen et al., 2007; Schröder et al., 2021; Wales et al., 2013).

The results also show that about one-third of the craft food producers were involved in REKO before the crisis while a slightly higher proportion were not; this was explained by the fact that the informal yet, structured form of network coopetition in REKO proved to also have some negative effects. For example, it was time-consuming and costly to adapt to the practices of other entrepreneurs involved in the network coopetition with specific dates and times to gather and distribute products. There was also a significant administrative burden. Furthermore, the loose coopetition ties between producers in the REKO network did not only have positive effects; it was necessary to have a commitment from all parties to function properly and avoid the risk of opportunistic behaviour, tensions or failed partnerships (Gernsheimer et al., 2021). The commitment issue of opportunistic behaviour has also been supported by evidence showing that network coopetition may include both positive and negative aspects (Crick et al., 2022; Lindström and Polsa, 2016; Thomason et al., 2013).

Despite some of these negative aspects, the smallest craft food entrepreneurs still engaged in network coopetition because of the COVID-19 crisis. This was partly due to a lack of alternative distribution channels but also to the opportunities and potential for exchanging knowledge and experiences. Our findings contribute to the evidence presented by Gernsheimer et al. (2021). For the larger firms in our sample, the negative aspects outweighed the positive aspects of network coopetition during the crisis. Hence, network coopetition proved to be less beneficial for larger firms. Extant evidence suggests that smaller firms are more likely to collaborate with others, with such collaboration fostering an ability to explore new markets and reduce uncertainty (Bengtsson and Johansson, 2014; Hitt et al., 2011; Morris et al., 2007). As our results show, one explanation for this difference being that the larger firms were more likely to receive governmental business support during the pandemic; this is more beneficial for them in terms of business robustness (see also Growth Analysis, 2023).

Coopetition and robustness in times of crisis

Our evidence shows that a majority of the craft food entrepreneurs coped with the COVID-19 pandemic well, as also shown by Skoglund and Rennemo (2022). Many craft food entrepreneurs even experienced a boost in sales as consumers turned to locally produced food. However, not all used network coopetition as a strategy given that a key challenge in coopetition is the balance between value creation and appropriation (Gernsheimer et al., 2021; Mizik and Jacobson, 2003). We also wished to investigate how coopetition affects micro-enterprise robustness in times of crisis, creating a measurement for enterprise robustness as a result (see the Methodology section). We created this measurement of robustness as previous frameworks analysing business endurance during crises have not fully captured how micro-enterprises navigate such crises but rather, focus upon recovery (Akgüna and Keskina, 2015). We found that, extending research by Love and Roper (2015), network coopetition may play an essential role in maintaining robustness in times of crisis (Crick and Crick, 2020; Crick et al., 2023). We also found that network coopetition that extended to the period before the pandemic also proved decisive for enterprise robustness, adding to work by Veal and Mouzas (2010) who argue that it takes time to establish trustworthy relationships before coopetition can take place. In particular, a lack of trust may challenge coopetitive relationships (Raza-Ullah, 2021). This is especially evident for micro-enterprises, as mutual respect in this case is a core foundation of network coopetition (McGrath and O’Toole, 2017). As previous research has shown, there are potential challenges and risks when enterprises become involved in network coopetition relationships: distrust, tension and opportunistic behaviour, all of which are known to emerge from the contradictory foundation of coopetition among cooperating competitors (Crick, 2020; Crick and Crick, 2021; Raza-Ullah and Kostis, 2019). Our study shows that the local proximity of the firms, together with the shared values and principles of the REKO concept, reduced much of this kind of distrust and tension (Kramer and Porter, 2011). The openness created by using social media as a communication channel additionally contributed to un-opportunistic behaviour between the producers. Our evidence illustrates that the craft food entrepreneurs who engaged in network coopetition before the pandemic generally coped better with challenges and uncertainty than those who joined during the pandemic, or who did not join at all. An explanation for this could be that these entrepreneurs were already familiar with the coopetition concept and were already benefitting from the social capital created by the members of the REKO community (von Friedrichs and Gummesson, 2006).

The respondents in our study also stressed that the network coopetition through REKO generated increased knowledge exchange and the formation of networks between craft food entrepreneurs. The collaborations also provided opportunities to reach a broader market, increase revenue and seek inspiration from other producers (competitors). This supports prior research showing that coopetition promotes knowledge exchange (Brunetto and Farr-Wharton, 2007; Lindström and Polsa, 2016; Morris et al., 2007). We found that the likelihood of robustness amongst small craft food producers was higher for the entrepreneurs who engaged in network coopetition through REKO – and it was observed that this form of network coopetition was most valuable and beneficial for the very smallest enterprises during the pandemic. The larger firms had access to government support; this made network coopetition through REKO more of a complementary. In the same sense, the smallest enterprises were excluded from business support prompting more network coopetition through REKO (c.f. Growth Analysis, 2023).

Evidence shows that coopetition is most likely to occur through formal structures (Granata et al., 2018). In contrast to these results, we suggest that network coopetition can be rule-driven, while at the same time having an informal structure. It appears that formal structures are not necessarily needed when the smallest enterprises coopete in local networks; this loosely organised form characterising local network coopetition can be used as a business survival strategy for these enterprises (Darbi and Knot, 2022). We, as a result, suggest that REKO is a type of rule-driven network coopetition with informal structures. In line with prior research (see Granata et al., 2018), we found that in times of crisis, coopetition through network coopetition is less likely to occur between firms that exceed the micro-enterprise definition (more than 10 employees), while network coopetition is extensively used by micro-enterprises to manage uncertainty. It has been shown that a crisis can have a particularly strong impact on smaller enterprises due to a greater lack of preparedness and resources; this makes them vulnerable to unexpected events (Doern, 2016), while the informal network offered by REKO did not benefit the larger firms as they determined that the additional costs did not exceed the benefits. These firms did not experience the added value of network coopetition, that is, added value beyond increased sales. Moreover, the larger firms have a different capacity to withstand crisis and were also more likely to be eligible for government support. A lack of resources pushed the smaller micro-enterprises towards network cooperation; this led to greater robustness.

Limitations and future research

Although this article has made a contribution to our understanding of how network coopetition affects micro-enterprise robustness in times of crisis, it has some limitations, one being the industry studied. We observed that the craft food entrepreneurs navigated and coped with the pandemic relatively well; thus, future research should focus upon industries that experienced negative consequences. As our study was conducted in Sweden, we cannot determine if specific aspects related to this country, such as government structures, societal restrictions and culture, have affected the impact of the COVID-19 pandemic. We suggest that future research should be conducted in other cultural contexts or countries. Finally, we examined enterprise robustness, that is, the ability to withstand a crisis and maintain functionality during one, which is in contrast to the resilience concept, which refers to a crisis impacts and recovery from them (Munoz et al., 2021). Since many industries were adversely affected by the pandemic, future research may advantageously investigate the effect that network cooperation has on an enterprise’s ability to recover.

Conclusions

The aim of this article was to explore the impact of network coopetition on the robustness of micro-enterprises in times of crisis; we developed an approach to improve the measurability of enterprise robustness. Our findings illustrate how network coopetition contributes to value creation and value capture in small craft food firms in times of crisis, and how such collaboration affects business performance and robustness. The theoretical implications of this study are manifold. First, the findings reveal that coopetition in micro-enterprises increased during the COVID-19 pandemic, highlighting its relevance as a viable concept of research in crisis situations (Gernsheimer et al., 2021). Second, the results show that micro-enterprises using coopetition as a strategy were more robust compared with those who did not – strengthening its applicability to research on firm robustness (Munoz et al., 2021). Third, the greatest benefit was attained by those firms who used coopetition as a strategy even before the pandemic, that is, the smallest micro-enterprises. These enterprises were robust to a higher degree compared to the industry average. Fourth, network coopetition was less beneficial for the larger micro-enterprises, that is, for those with three or more employees; they mainly joined during the pandemic reporting that the benefit did not outweigh the costs of joining. This suggests that while changing business models and strategies during a crisis can be beneficial (Guckenbiehl and Corral de Zubielqui, 2022), this is not always the case. Fifth, the study results highlight that network coopetition can be rule-governed and still have an informal structure of cooperation between competitors.

The practical implications of this study include how the smallest micro-enterprises used network coopetition as a strategy to a greater extent than larger firms while during the COVID-19 pandemic, they were more robust than such firms. This knowledge can be valuable in future crises as it shows that micro-enterprises can obtain an advantage in times of crisis by collaborating with competitors, as well as by using network coopetition. Micro-enterprises, along with small firms, are the most common business form making a significant contribution to the global economy (OECD, 2021). It is, therefore, essential that we increase our knowledge about their robustness. Although some studies have explored the manner in which crises such as the COVID-19 pandemic disrupt the activities of entrepreneurs (Sharma et al., 2022), there are few studies showing how different national strategies affect the robustness of small businesses in terms of the business support offered to compensate for issues such as reduced income, lost jobs, and a weak market (Engidaw, 2022, Growth Analysis, 2023). Further studies will be needed on the robustness of small- and micro-enterprises in times of crisis.

Footnotes

Appendices

Craft food respondents interviews.

| Respondent | Occupation | Main product | Employees 2022 | REKO producer |

|---|---|---|---|---|

| R9 | Full time | Food crafts | Owner | Yes before |

| R10 | Full time | Dairy | Owner | Yes before |

| R7 | Full time | Candy | 2 owners | Yes before |

| R11 | Full time | Meat | 3 | Yes before |

| R5 | Full time | Bread | 6 | Yes before |

| R3 | Full time | Hand crafts | Owner | Yes during |

| R8 | Full time | Bread | Owner | Yes during |

| R2 | Full time | Eggs | 2 owners | Yes during |

| R12 | Full time | Food crafts | 2 | Yes during |

| R1 | Full time | Goat cheese | 2 | Yes during |

| R14 | Full time | Fish | 10 | Yes during |

| R4 | Seasonal | Beverages | Owner | No |

| R6 | Full time | Reindeer meat | 7 | No |

| R13 | Full time | Candy | 25 | No |

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was partly funded by the Interreg Sweden-Norway Programme.

Author biographies

, PhD, is senior lecturer in Business Administration at Mid Sweden University. Her research interests include SMEs, business growth, social entrepreneurship and women’s entrepreneurship.