Abstract

The study examined an intergenerational model of financial socialization and its outcomes that connects parents’ and their children’s self-perceived financial learning outcomes to satisfaction with financial management and parent-child financial relationships. The conceptual model was based on models of financial socialization processes contributing to healthy financial development of emerging adult students (Shim et al., 2010; Sirsch et al., 2020), but extended the links across two generations within the same family. Considering perspectives of both generations in a single model, it was tested in a sample of 482 pairs of Slovenian first-year university students and one of their parents. Structural equation modeling revealed that parental healthy financial learning outcomes (knowledge, behavioral control, behavior) shaped their children’s positive financial development (financial learning outcomes and satisfaction) and promoted the parents’ satisfaction with financial management. In turn, both the students’ and the parents’ financial management satisfaction positively predicted a joint measure of satisfaction with parent-child financial relationship. Similar links of financial learning outcomes to satisfaction with financial management and parent-child financial relationships were observed for both generations, even though parents and their children were financially socialized under different socioeconomic conditions.

Keywords

Introduction

Managing personal and family financial resources is an important domain of one’s functioning in a consumer society and within the family, as financial matters can strain or improve family relationships (Lindell et al., 2020). Moreover, healthy financial management is associated with a variety of positive outcomes, including physical and mental health, academic achievement (Serido et al., 2010; Xiao et al., 2009), and subjective financial well-being (Lanz et al., 2020; Shim et al., 2012), which, in turn, contributes to overall subjective well-being (Iannello et al., 2020; Netemeyer et al., 2018).

Financial management is rooted in family financial socialization, with parents playing a central role in children’s financial learning (Gudmunson & Danes, 2011; Jorgensen & Savla, 2010). While personal experiences (LeBaron et al., 2019; Tang & Peter, 2015) and other agents of financial socialization (e.g., peers, school, and media) gain influence in adolescence, parents retain the strongest role in financial functioning of emerging adult children (Shim et al., 2010; 2015) as they cope with achieving financial independence – an important feature of adulthood (Arnett, 2015; Zupančič et al., 2018).

One of the prerequisites for achieving financial independence is financial capability (knowledge, behavioral control, and skills to manage personal finances; e.g., Serido et al., 2013) gained through financial socialization. Although financial socialization is a life-long process, its outcomes in emerging adulthood tend to have long-term consequences (Ashby et al., 2011; Danes & Yang, 2014) and may be even more critical when people face uncontrollable life events, such as the financial crisis of 2008 (Sorgente & Lanz, 2017), or the global COVID-19 pandemic with its economic consequences.

The purpose of the present study

Many emerging adults, particularly students, remain at least partly dependent on their parents for financial support (see Serido et al., 2015 for the USA; Zupančič et al., 2018 for Europe). In Slovenia, the majority of individuals between the ages of 19 and 24 live with their parents (Lahe et al., 2021), either constantly (65.4%) or part of the time (26.4%). The Slovenian youth overwhelmingly report receiving all the financial assistance they need from their parents (Lep et al., 2021). Over two thirds (69.0%) of 19-24-year-olds expect parental financial assistance in the future, and 81.4% expect their parents to assist them financially in solving their housing situation (Lahe et al., 2021). The ongoing financial responsibility of the parents may challenge their management with the family/personal budget, financial planning, and satisfaction. While the factors of emerging adults’ successful financial development have been well documented (e.g., Jorgensen et al., 2017; Shim et al., 2015), research on financial management and well-being of parents who financially support their children beyond adolescence has been set aside (LeBaron & Kelley, 2020). To fill this gap, an evaluation of parental views on their own financial capability, the context they create for the financial development of their children, and their own financial well-being is called for. Joining the parental views with those of their emerging adult children would extend insights into the transmission of financial functioning from one generation to the next, especially for generations primarily socialized under different macroeconomic conditions. To our knowledge, no such study has been documented.

The established pathways to healthy financial development and well-being of emerging adults were predominantly based on emerging adults’ assessments of their financial socialization, financial functioning, and satisfaction (e.g., Serido et al., 2010; Sirsch et al., 2020). Hence, the associations may have been inflated due to the shared method variance. Although these studies contributed valuably to our understanding of financial development of young people, an integration of the perspectives of two successive generations within the same family into a single model is lacking. First, it would highlight intra-generational and intergenerational processes shaping financial management and financial well-being of both generations. Second, relying on multiple data sources would reduce the single-informant bias. Third, testing the current models across generations would afford information about the generalizability of the links ascertained for emerging adults to their parents whose primary financial socialization unfolded in (somewhat) different economic times or even macroeconomic systems.

Based on this rationale, we created a model considering self-views of emerging adults and their parents simultaneously, as well as cross-informant (intergenerational) links. We explored the processes through which members of two generations within the same family manage personal finances, and evaluate their financial management and financial relationships. Testing the model in Slovenia, we aimed to get an insight into its validity across generations who grew up in different economy systems. The parents of Slovenian emerging adults were financially socialized in market socialism before the country became independent in the early 1990s, but their children developed in a capitalist market economy. While healthy financial behavior and financial socialization were also important in Yugoslavia’s socialist regime (differing markedly from the better-known communist systems of Eastern Europe 1 ), current financial socialization models need to be tested for generations socialized under different conditions.

Theoretical framework

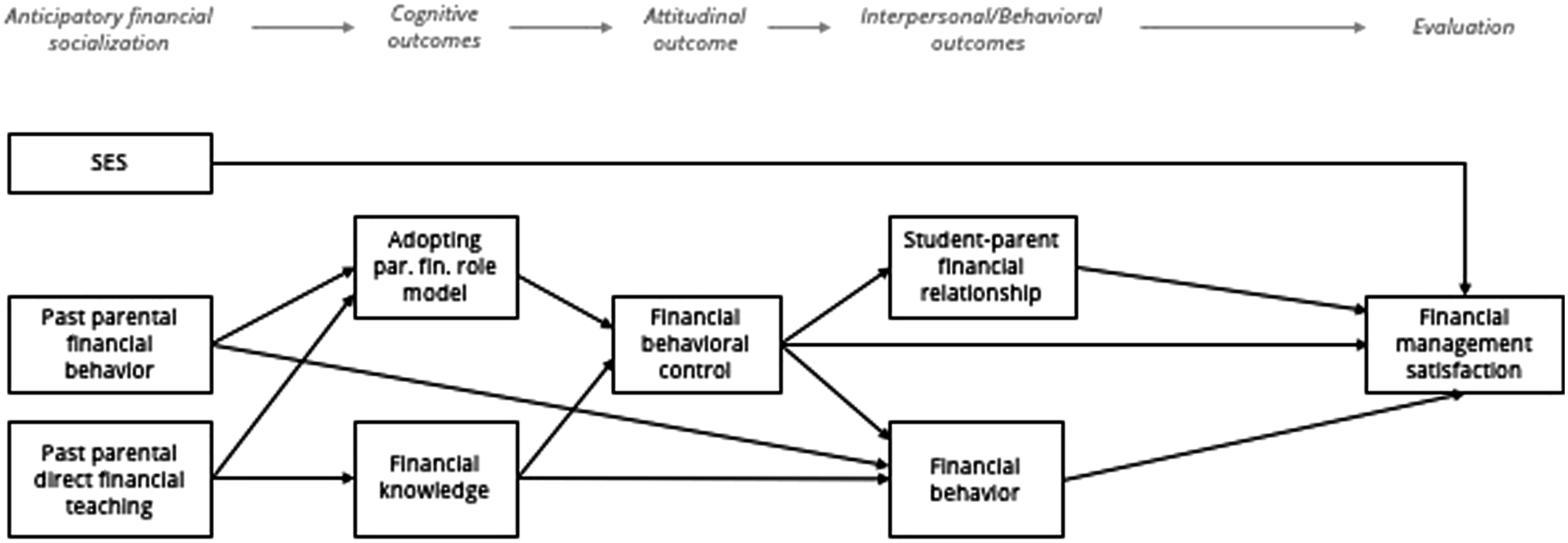

In building an intergenerational model, we were guided by two models of financial socialization processes (Shim et al., 2010; Sirsch et al., 2020) which draw upon the consumer socialization theory (Moschis, 1987) and the theory of planned behavior (Ajzen, 1991). Within this combined theoretical framework, Shim et al. (2010) conceptualized the Hierarchical Model of Financial Socialization Processes. It explains the pathways to college freshmen’s self-reported healthy financial behavior, satisfaction with financial management, and financial relationships with parents (behavioral indicators of financial learning outcomes) through a four-level hierarchical structure. Anticipatory financial socialization by parents (students’ perceptions of parental financial behaviors and direct financial teaching prior to their leaving for college, including parental SES), financial education in school, and work experience on Level 1 predict cognitive financial learning outcomes (objective and subjective financial knowledge combined, adopting parental financial role modeling) on Level 2, which in turn shape financial attitudes (students’ views on desirable financial behavior, subjective norms, financial behavioral control) on Level 3. Students’ financial attitudes further influence financial behavioral outcomes on Level 4. Testing the model in the USA also suggested direct positive links of parental SES (an antecedent of socialization processes, Moschis, 1987) to students’ satisfaction with financial management and of financial knowledge to healthy financial behavior (Shim et al., 2010).

Applying the model (Shim et al., 2010) to Austrian and Slovenian first-year university students, Sirsch et al. (2020) only considered parental financial socialization because very few individuals in these two countries engage in paid work before they enter university, no financial education courses are offered in schools and most adolescents do not attend such courses outside of school. In line with a more recent overview on financial well-being (Sorgente & Lanz, 2017), Sirsch et al. (2020) additionally proposed that healthy financial behavior and favorable financial relationships with parents promote students’ satisfaction with financial management, one of the core dimensions (behavioral) of subjective financial well-being (Sorgente & Lanz, 2019). The adjusted and empirically supported model (Sirsch et al., 2020) served us as the base for the present study. As presented in Figure 1, the Model of Parental Financial Socialization and Financial Management Satisfaction hierarchically connects parental financial socialization to students’ cognitive, attitudinal, and behavioral/interpersonal outcomes, and finally to satisfaction with financial management. Pathways of parental financial socialization to financial learning outcomes and satisfaction from the perspective of Slovenian students (adapted from Sirsch et al., 2020).

Development of the intergenerational model and literature review

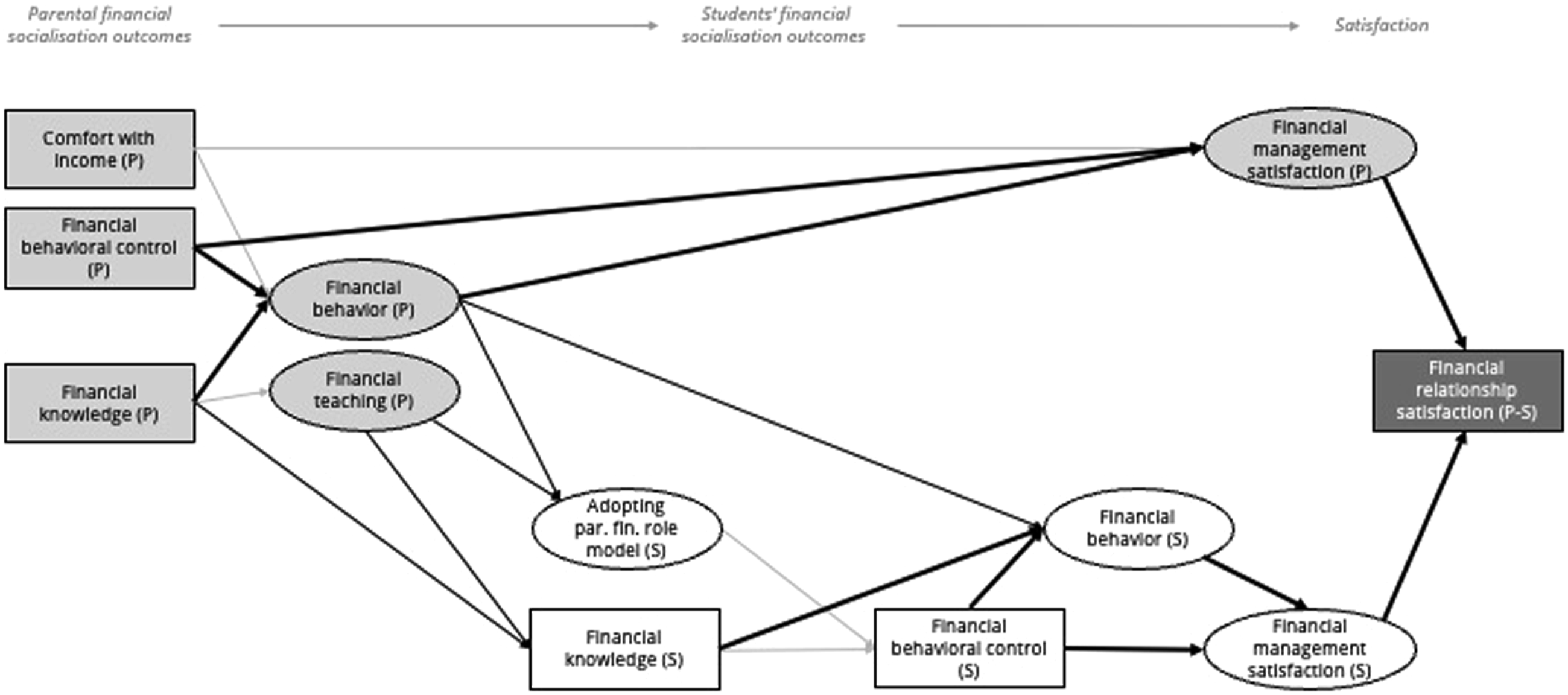

The proposed Intergenerational Model of Family Financial Socialization and Satisfaction (Figure 2) links parental views on their own financial socialization outcomes to (1) emerging adult children’s self-views on financial learning outcomes, which in turn predict their financial management satisfaction, and (2) parental satisfaction with financial management. The model also posits that a joint measure of satisfaction with parent-child financial relationships presents an outcome, attained through these processes. Conceptual model of intra- and intergenerational links of financial functioning with healthy financial outcomes for parents and their emerging adult children. (P) – parental self-ratings, (S) – student self-ratings; (P–S) – parent-student aggregate. Black arrows indicate intergenerational, grey intra-generational, and bolded ones similar links across generations.

Pathways within both generations: Self-views of parents and emerging adults

Given financial socialization is a life-long process, the financial learning outcomes (knowledge, attitudes, and behavior) of emerging adults’ parents have been acquired through their continuous financial socialization by various agents (including their family of origin; Danes, 1994) and their own financial experiences. As shown by the models of healthy financial outcomes in emerging adults (Shim et al., 2010; 2015; Sirsch et al., 2020) within the framework of consumer socialization theory (Moschis, 1987) and its more recent conceptualization in family financial socialization theory (Gudmunson & Danes, 2011), financial knowledge and attitudes shape financial behavior, which in turn contributes to financial well-being. The perceived behavioral control, an attitudinal factor that promotes behavioral intention (Ajzen, 1991; Shim et al., 2009), also directly influences positive financial behavior and well-being (Shim et al., 2010; Sirsch et al., 2020). Likewise, financial controllability (Shim et al., 2015), locus of control (Jorgensen et al., 2017) and delayed gratification (Norvilitis & MacLean, 2010) clearly predict healthy financial behavior. Research further suggests that healthy financial behavior predicts financial (and/or general) well-being (e.g., Serido et al., 2010; Xiao et al., 2009).

Financial knowledge captures an objective (ability to demonstrate actual financial understanding) and a subjective part (perception of this understanding; Butterbaugh et al., 2019). Shim et al. (2010) found that the combined construct strongly associates with several attitudinal and behavioral financial learning outcomes, but the objective test had a considerably lower factor loading (and poor reliability) on the construct than the subjective measure. As the studies relying on the subjective measure (Shim et al., 2009; Sirsch et al., 2020) obtained significant associations with the outcome variables and our survey was quite long, we opted only for the subjective knowledge.

Concerning attitudinal factors, we referred to the perceived financial behavioral control which reflects one’s sense of control over financial matters. We also defined healthy financial behavior as one’s perception of responsible spending, saving, and investing. Likewise, we focused on the subjective financial well-being, specifically satisfaction with financial management – a comprehensive evaluation of own financial behavior (Sorgente & Lanz, 2019).

We applied the previously identified pathways connecting financial knowledge and behavioral control to satisfaction through healthy financial behavior in Slovenian students (Sirsch et al., 2020; Figure 1) to both generations. Precisely, we proposed the parallel pathways of subjective financial knowledge and perceived financial behavioral control to healthy financial behavior (Hypothesis 1.1), and from financial behavioral control and behavior itself to financial management satisfaction (Hypothesis 1.2). Figure 2 shows these pathways in bold.

Intergenerational links of parental financial socialization to financial learning outcomes

Studies founded on the consumer socialization theory (Moschis, 1987) and the family financial socialization theory (Gudmunson & Danes, 2011) have accumulated evidence that children acquire financial knowledge and form financial attitudes, consumer skills, and money management strategies through various implicit and explicit socialization processes by interacting with parents. Whereas implicit financial socialization refers to the unconscious transfer of concepts, observation, expectations, or emulation of parental behavior (Jorgensen & Savla, 2010; LeBaron et al., 2019), explicit financial socialization represents parental teaching of financial content or skills through discussing money, and delivering financial instructions and explanations (Gudmunson & Danes, 2011; Serido & Deenanath, 2016).

Implicit financial socialization unfolds through parent-child communications and relationship quality, parental expectations, and financial role modeling. Through these, the children internalize family financial attitudes, expectations, norms, and behaviors, upon which self-regulation of financial behavior develops (Danes & Yang, 2014; Gudmunson & Danes, 2011). Parental role modeling occurs as children observe parental financial behaviors and then emulate them (Serido & Deenanath, 2016); it appears particularly important because children not only observe and emulate behaviors of socialization agents, but also make decisions about the extent to which they adopt them as role models (indicating internalization; Lanz et al., 2020).

Both implicit financial role modeling (Serido et al., 2010; Shim et al., 2015) and explicit financial teaching (Deenanath et al., 2019; LeBaron et al., 2020) shape emerging adults’ attitudes and behavior. In this study, we considered healthy parental financial behavior as an indicator of implicit parental socialization that affects children’s adopting parental role modeling (internalization of parental financial behavior) and parental financial teaching as an indicator of explicit socialization.

To encompass the intergenerational view, we adopted the links from the student model (Sirsch et al., 2020). Instead of linking students’ recollections of parental financial socialization to their cognitive learning outcomes (Figure 1), we introduced the respective intergenerational associations (Figure 2). As parental financial socialization remains influential in emerging adulthood (Serido et al., 2015; Shim et al., 2015), we also accounted for an indicator of current financial socialization. Specifically, we associated the parents’ views on both their direct financial teaching before the children entered university and positive financial behavior at present with students’ adoption of parents as financial role models (Hypothesis 2.1), and the parents’ anticipatory financial teaching with students’ subjective financial knowledge (Hypothesis 2.2).

Healthy financial behavior of parents (either self- or child perceived) directly and/or indirectly (through adopting parental role modeling and self-control) influences the behavior of their emerging adult children (Sirsch et al., 2020; Tang, 2017; Figure 1). Similarly, parental financial knowledge induces knowledge-based cognitive learning about money management (Tang & Peter, 2015). Therefore, we connected both parents’ healthy financial behavior and subjective financial knowledge to these characteristics of their children (Hypothesis 2.3).

Additional links from the view of each generation

From the view of emerging adults, we retained the hierarchical four-level structure that connects financial socialization to cognitive outcomes first, to attitudinal outcomes next, and to behavioral outcomes thereafter (Shim et al., 2010). We included the intermediate link of the cognitive to the attitudinal outcome by relying on the documented (Shim et al., 2010; Sirsch et al., 2020) beneficial associations of both students’ cognitive financial learning outcomes (adopting parental role modeling and knowledge) with self-perceived financial behavioral control (Figure 1). A significant role of these outcomes in predicting financial attitudes and behavior of students was also shown by other studies (e.g., Shim et al., 2009; 2015). This led us to surmise that both positive cognitive outcomes of the emerging adults’ financial learning would predict their perception of stronger financial behavioral control (Hypothesis 3).

Within the parental view, we connected parents’ self-perceptions of financial understanding to their involvement in explicit financial socialization, given parental financial knowledge and motivation effectively support children’s financial learning (Retting & Mortenson, 1986; Tang & Peter, 2015) and parental financial instructions appear particularly conducive to children’s positive financial development (LeBaron et al., 2020; Vosylis & Erentaitė, 2020). Thus, parents who perceived themselves more financially knowledgeable were expected to report higher levels of teaching their children financially (Hypothesis 4.1).

Family characteristics (e.g., SES), influence the family financial socialization processes (Serido et al., 2010; Vosylis & Erentaitė, 2020), as well as financial satisfaction of emerging adults (Shim et al., 2010; Sirsch et al., 2020). Connections of higher SES (parental education and objective family income) to more favorable outcomes suggested that wealthier parents (often better educated) tend to form a more favorable learning context (including parental financial behavior) for positive financial development of their children (Luhr, 2018; Serido et al., 2010).

Instead of relying on emerging adults’ reports of the SES in predicting their financial management and satisfaction (Shim et al., 2010; Sirsch et al., 2020), we related parents’ perceptions of the family economic condition to their own financial behavior and satisfaction with financial management (Figure 2). First, Slovenian parents run the family household and have a more accurate insight into the family income than their co- or semi-residing children who receive all necessary parental financial support (Kuhar & Reiter, 2014; Lahe et al., 2021). Second, the social class stratification, including income inequality, in Slovenia is among the lowest in the world (OECD, 2019), suggesting a modest association of the objective income with the level of education. Third, an objective income measure is not applicable in Slovenia as an individual’s income is considered a private matter and parents are reluctant to report about it (Sirsch et al., 2020). Fourth, subjective measures of economic status (peer or temporal comparisons) provided by Slovenian parents predicted their financial behavior and its self-evaluation (Lep et al., 2021; Zupančič et al., 2018). These guided our selection of parental comfort with the family income to capture parents’ perception of their economic condition and to assume that higher levels of comfort associate with both healthier financial management and satisfaction with this management (Hypothesis 4.2).

Satisfaction with parent-child financial relationships

Parent-child interactions and relationships directly or indirectly predict various aspects of emerging adults’ financial well-being (e.g., Allsop et al., 2020; Lanz et al., 2020). A broad set of indicators have been used in studies of financial learning outcomes, such as quality of communication in general (Lanz et al., 2020) and financial communication specifically (Jorgensen et al., 2017; Serido et al., 2010), perceived parental financial expectations (Serido et al., 2010), relationship quality (Allsop et al., 2020), quality of attachment (Jorgensen et al., 2017), family rituals/routines and parental monitoring (Allsop et al., 2020). However, Shim et al. (2010) and Sirsch et al. (2020) treated the quality of financial relationships as an outcome of the process of financial socialization. Accordingly, we aimed to predict how parents and children evaluate their relationships due to financial matters (satisfaction with financial relationships).

Financial issues may be particularly important for parent-child relationships in emerging adulthood because the relationships restructure and attainment of financial independence becomes a prominent task of young people (Arnett, 2015; Tanner, 2006). Given the relationships involve recurrent interactive exchanges between the partners that shape the relationship quality in dynamic ways (e.g., Kuczynski, 2003), satisfaction with financial management in each partner may contribute to the evaluation of their financial relationship. Although disputes over financial matters during parent-child interactions could undermine each partner’s satisfaction with financial management (Sirsch et al., 2020), dissatisfaction with personal financial management could also lead to interpersonal conflict over money and deteriorate the relationships. Not intending to imply a unidirectional association, we suggested that favorable evaluations of financial management in both parents and emerging adults contribute to the joint measure of satisfaction with parent-child financial relationships (Hypothesis 5).

This study

Based particularly on the models of family financial socialization processes that explain the pathways to healthy financial outcomes in emerging adult students (Shim et al., 2010; Sirsch et al., 2020), we conceptualized an intergenerational model by extending the pathways to the processes through which members of two generations within the same family manage personal finances, and evaluate their money management and interpersonal financial relationships. Our model describes predictive relations that originate with parents’ financial socialization outcomes and comfort with their household income (all creating the financial learning context for their children), lead to both parental financial management satisfaction and the children’s financial learning outcomes across three levels of outcomes (cognitive, attitudinal, and behavioral) and subsequently to the children’s financial management satisfaction. Finally, financial management satisfaction of both parents and children contributes to a joint measure of parent-child financial relationship satisfaction. The model includes the links that are similar across generations, the intergenerational links, and the generation specific links (Figure 2). By expanding the models of parental financial socialization leading to successful financial outcomes in emerging adults to their parents, our study fills a gap in the literature. It further allows to test the current models for two generations who were financially socialized under different macroeconomic conditions.

Method

Participants

The sample comprised 482 parent-child pairs (all residing in Slovenia) – university freshmen (97% of Slovenian nationality; 45.2% males and 54.8% females) and one of their parents (21.8% fathers and 78.2% mothers). The students’ mean age was 19.96 years (SD = 0.81; Mdn = 19.83, 18–25) and was comparable to the age structure of Slovenian first-year students (SURS, 2022). They attended one of two (out of three) Slovenian public universities; 62.9% were enrolled in one of the social science programs, 28.2% in technical/nature science programs, and 5.8% in humanities; 44% of the students co-resided with parents, 51.5% partly resided in parental home (during the weekdays, they resided in a student dorm/rented apartment), and 7.5% lived with other relatives or otherwise moved out of parental home. Most (77.4%) thought parents have an obligation to financially support their children’s education (noting it is tuition-free) and 95.2% responded affirmatively to the question Do your parents provide the level of financial support you believe they should?

The mean age of participating parents was 48 years (SD = 5.23; Mdn = 48.08, 34–65); 64% of them had a secondary education (high school, technical, or professional), 29.9% postsecondary education (college or university), and 6% finished only 8 years of obligatory schooling; 83.4% of the parents were employed full-time, 5.8% part-time or had occasional jobs, and 10.8% were either unemployed or retired. Most of the parents (87.5%) lived with a partner (were married or cohabited), 8.9% were single or divorced, and 3.3% widowed; 54.7% had two children, 22.2% three children, 15.7% one child, and 7.4% had more than three children.

Procedure and measures

The study is based on data collected within an international research collaboration initiated by prof. Mihaela Friedlmeier (Grand Valley State University, Allendale, MI) who attained institutional board approval. We contacted first-year students in their classroom and invited them to participate voluntarily and anonymously. We asked them to invite one of their parents, an additional first-year student of another study program and one of his/her parents to participate. We provided students with a link to a platform with separate student and parent forms, consisting of informed consent and the survey. The participants entered a unique code assigned to each student-parent pair used for linking their responses. The students completing the full assignment received course credit.

Self-report questions and scales were based on Shim et al.’s (2010) measures but adjusted and validated for use in the Central European context (Sirsch et al., 2020). For the present study, we provide the measurement model and internal reliabilities of the scales in Supplementary material (Table S1). All scale scores were calculated as item-averages.

Subjective financial knowledge was assessed using a single five-point scale item asking about the participants’ (both students and parents) overall understanding of money management (1 – very low; 5 – very high).

Financial behavioral control was measured by a single five-point scale (1 – difficult; 5 – easy) assessing how difficult it is for the participants to stick to their money-management plans.

Financial behavior was reported along a five-point scale. The participants assessed how often (1 – never; 5 – very often) they engaged in three positive financial behaviors (spending within budget, saving each month, investing for long-term goals). After spending within budget was removed due to low factor loading (see Results), the resulting two-item factor had sufficient reliability (ρ = .70 for parents and .72 for students).

Satisfaction with financial management was assessed by three items regarding the participants’ current satisfaction with paying their bills, managing purchases, and not being worried about money (1 – strongly disagree; 5 – strongly agree; ω = .74 for parent and .68 for student self-report).

Satisfaction with parent-child financial relationship measured the extent to which the participants experience conflict and stress in their parent-child relationship due to financial matters (1 – strongly disagree; 5 – strongly agree). We inversed the rating scale so that higher scores represented greater satisfaction. Students’ separate ratings in relation to each parent were aggregated (averaged) with their parent’s rating into a joint measure (ω = .85).

Adopting parental role modeling captures the extent to which the students adopt the financial role of their parents. They expressed their agreement (1 – strongly disagree; 5 – strongly agree) with three items (making financial decisions based on what the parent has done in similar situations, looking at the parent as a role model in managing money, acknowledging the parent as the best financial advisor), separately for each parent. The scores were subsequently aggregated (averaged) into a joint measure (ω = .81).

Direct parental financial teaching measures the extent to which parents engaged in three teaching methods of financial management while raising their child (discussing financial family matters, speaking about the importance of saving and teaching about smart shopping; 1 – strongly disagree; 5 – strongly agree). The scale had acceptable internal reliability (ω = .70).

The parents also reported the comfort with household income by indicating how they feel about their household income (1 – finding it very difficult on present income, 2 – finding it difficult on present income, 3 – coping on present income, 4 – living comfortably on present income). This item was created for the purpose of data collection in the international study coordinated by M. Friedlmeier.

Results

Measurement model, descriptive statistics, and intercorrelations

First, we evaluated the measurement structure of the items using R package lavaan (Rosseell, 2012) to examine the validity of the measures, which is often a shortcoming in the literature on financial socialization of emerging adults (LeBaron & Kelley, 2020), and proceeded with testing the structural model to test our hypotheses. As some scores did not distribute normally, we used robust maximal likelihood estimator, and imputed missing values using FIML method. Where students provided ratings for each of their parents, we modeled the variables to group into two factors (one for each parent) with a second order factor (i.e., adopting parental role modeling and satisfaction with parent-child financial relationships), and estimated item-level covariations. To capture the perspective of both informants, we conducted the CFA for aggregated data on satisfaction with parent-child financial relationships, which was modeled as a second-order factor, including factors of students’ and their parent’s ratings (averaged by item).

The measurement model fit the data well (χ2 = 464.28, df = 339, p < .001, CFI = .98, TLI = .97, RMSEA = .039, 95% CI [.022, .036], SRMR = .047). The factor loadings (Table S1 in the Supplementary material) were substantial and significant, except for spending within a budget (loading below .40). We excluded this item and used the remaining two items as a measure of financial behavior. The internal reliabilities were acceptable across the constructs (Table S1 in the Supplementary material); coupled with a good fit of the measurement model, this suggested sufficient validity of the used measures. Mostly significant and at least moderate correlations between the constructs in our conceptual model enabled us to proceed with testing our hypotheses within the structural model (see Table S2 of the Supplementary material for descriptives).

Structural model

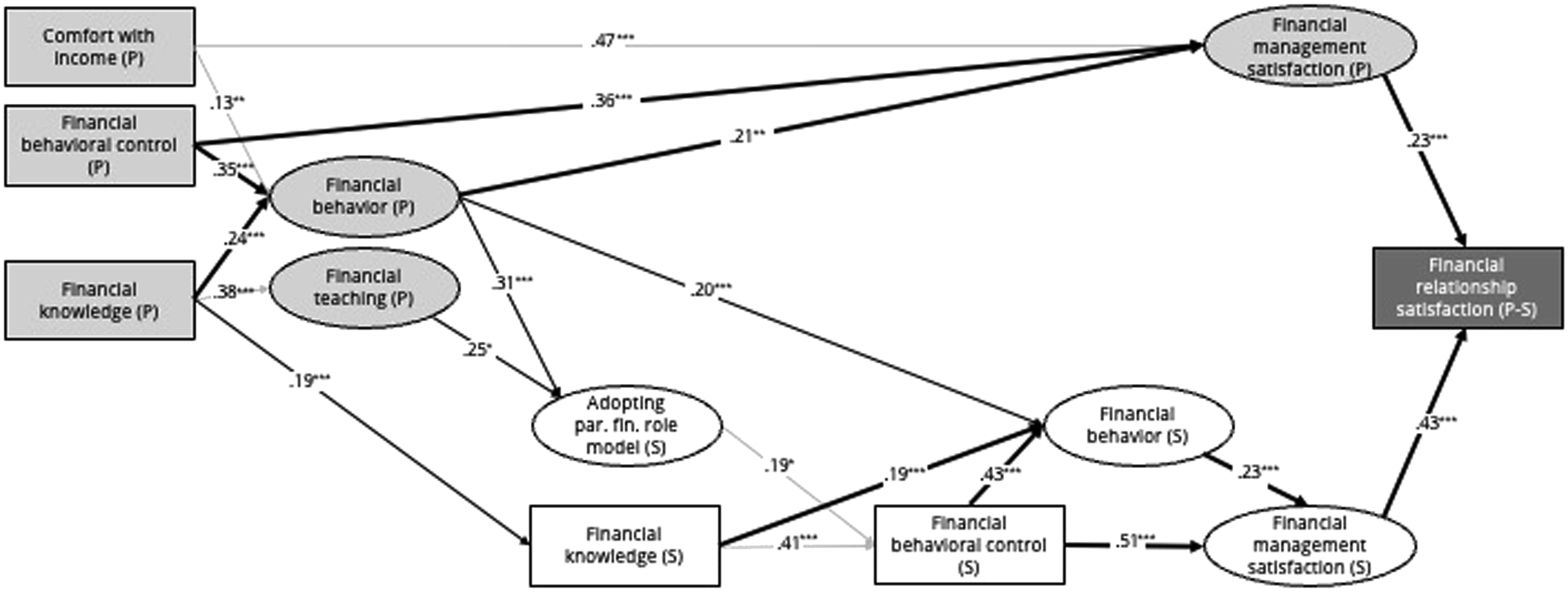

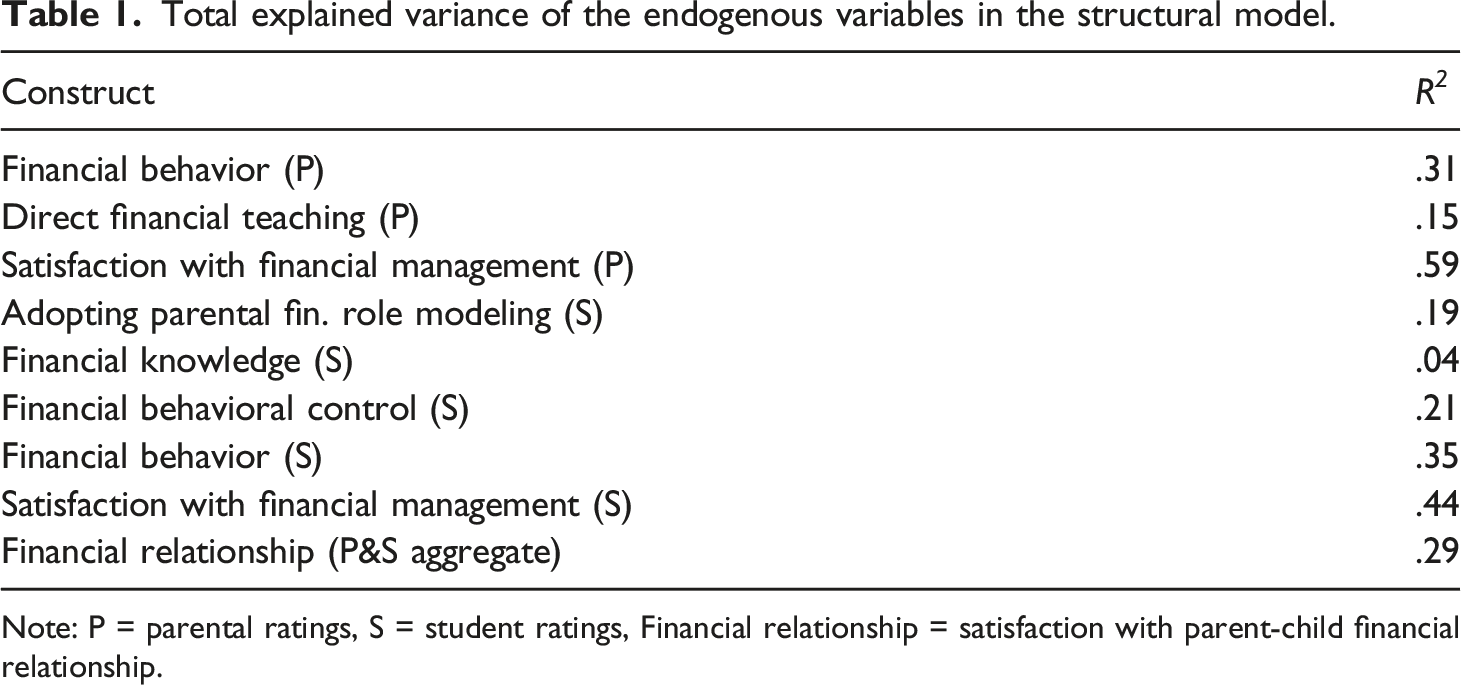

Next, we tested the initial structural equation model (Figure 2) of the predictive relations among the constructs under study. The initial model fit the data well (χ2 = 734.26, df = 495, p < .001, CFI = .96, TLI = .95, RMSEA = .033, 95% CI [.028, .038], SRMR = .064). However, one of the proposed paths was not significant (i.e., direct financial teaching to students’ subjective financial knowledge, refuting H2.2). After removing this path, the model retained its fit (χ2 = 736.22, df = 497, p < .001, CFI = .96, TLI = .95, RMSEA = .033, 95% CI [.028, .038], SRMR = .065). Further modifications based on the inspection of modification indices were not tested. While the exclusion of the non-significant path could artificially inflate the model fit, the fit of the two models remained virtually the same. With the aim of deriving a more parsimonious model, we retained the respecified model. The final model with standardized regression coefficients is presented in Figure 3 and the shares of explained variance for the endogenous variables are presented in Table 1. Structural model of the intra- and intergenerational links of financial functioning with financial management satisfaction and parent-child financial relationship. (P) – parental self-ratings, (S) – student self-ratings; (P–S) – parent-student aggregate. Black arrows indicate intergenerational, grey intra-generational, and bolded ones similar links across generations. All coefficients are standardized. *p < .05, **p < .01, ***p < .001. Total explained variance of the endogenous variables in the structural model. Note: P = parental ratings, S = student ratings, Financial relationship = satisfaction with parent-child financial relationship.

Intra- and intergenerational links

Parents who perceived themselves more financially knowledgeable reported higher levels of direct financial teaching (H4.1) and comfort with household income (H4.2) was related more to their satisfaction with financial management (β = .47, p < .001) than to their financial behavior (β = .19, p = .002). As predicted (H2.1), positive parental behavioral outcomes (financial behavior and direct financial teaching) influenced their children’s adopting parental financial role modeling, while parental subjective financial knowledge and behavior directly and positively contributed to the children’s financial knowledge and behavior, respectively (H2.3). Even though the effect sizes of these paths were small to medium (between .19 and .31, p < .001), the model explained a significant portion of variance in adoption of parents as role models (R2 = .19) and students’ financial behavior (R2 = .35). Consistent with H3, both adopting parental role modeling and students’ financial knowledge contributed to their stronger financial behavioral control with small and medium effect sizes of .19 (p = .015) and .41 (p < .001), respectively.

Similar paths across generations

The model supports a similar pattern of links in both generations as predicted in our first hypothesis. Higher levels of subjective financial knowledge and behavioral control were associated with healthier financial behavior in both children and the participating parents with medium effect sizes (H1.1). Likewise, healthier financial behavior and better self-perceived financial behavioral control contributed to higher levels of financial management satisfaction (H1.2), which, in turn, promoted parent-child financial relationships (H5; bolded links in Figure 3). The effect sizes of pathways toward financial management satisfaction were higher in emerging adults (βs = .23 and .51, p < .001) compared to parents (βs = .21 and .33, p = .002 and < .001, respectively). Likewise, the effect size of emerging adults’ satisfaction with money management in predicting satisfaction with financial relationships was nearly double the effect size of parental one.

The model explains a significant portion of the endogenous variables in the structural model (except for students’ financial knowledge; R2 = .04), and around a third of the variance in satisfaction with parent-child financial relationships. The pairwise comparisons between constructs assessed by both students and parents suggest that comparable portions of the variance in financial behavior and satisfaction with financial management are explained in both samples.

Discussion

This study examined the conceptual model of pathways of financial functioning toward satisfaction with financial management and parent-child financial relationships in samples of Slovenian university freshmen and one of their parents. With a slight adjustment (exclusion of one pathway), the proposed model fit the data well and accounted for substantial portions of variance in the financial management satisfaction (both samples), and in aggregated evaluations of parent-child financial relationships. The findings added to the understanding of the processes linking family financial socialization with aspects of financial satisfaction by considering the perspectives of both generations within the same family and looking ‘back’ at the associations of parental financial learning outcomes with financial parenting.

Before discussing the main findings, it should be noted that healthy financial behavior in our study refers only to regular saving (proactive behavior aimed to build up resources) due to low factor loadings of spending within budget (preventive behavior aimed to prepare for uncertainty) on the respective latent construct. Acceptable, albeit low, factor loadings of the same indicator were revealed in both Austrian and Slovenian students (Sirsch et al., 2020), whereas another item of preventive financial behavior (tracking monthly expenses) from the respective scale used by Shim et al. (2010) was omitted for the same reason. Moreover, drawing from evidence in Chinese students (Gan et al., 2007), Serido et al. (2010) showed that relying on two separate factors of emerging adults’ positive financial behavior also proved beneficial in the USA. All together this suggests that preventive and proactive financial behaviors should be considered separate constructs in future research.

Parental financial learning outcomes, financial parenting and financial management satisfaction

Scarce studies linking financial parenting with emerging adults’ financial development (e.g., Allsop et al., 2020; Tang, 2017) included parent and child views. Even when this was the case, the research focused on emerging adults’ financial functioning and well-being. By incorporating the parental perspective into our model, we showed that the benefits of parents’ (self-rated) healthier financial learning outcomes (cognitive, attitudinal, and behavioral) are twofold. They provide a favorable context for the children’s financial development, and promote the parents’ satisfaction with money management which, in turn, enhances the joint parent-child evaluations of their relationships in respect to financial matters.

Our results highlight the connections of parents’ financial learning outcomes (acquired in part within their own family of origin; Danes, 1994) with the financial socialization context they create for their children, and with their own financial management satisfaction. The more parents believed they knew about finances, the more engaged they were (in their view) in proactive financial behavior and in providing financial lessons to their children (as mentioned within H1.1 and proposed in H4.1, for behavior and teaching respectively). Although we relied on subjective financial knowledge, this kind of knowledge is related to objective knowledge, but also captures self-efficacy and self-confidence about financial functioning, which influence attitudes and behavior more than solely knowledge of financial facts (Shim et al., 2010). Thus, presumably being more confident in passing on their understanding of finances and money management to the next generation, subjectively more knowledgeable parents may tend to engage in financial discussions/explicit instructions with their children more frequently.

Given saving is a function of one’s ability and willingness to save (Lep et al., 2021; Otto, 2013), the multi-faceted nature of subjective financial knowledge (Shim et al., 2010) may increase parental motivation to save and thus enhance the corresponding proactive behavior. Likewise, higher levels of self-perceived financial behavioral control and more favorable feelings about household income (financial ability) directly predicted more frequent saving and greater satisfaction with money management in our parent sample (consistent with H1.2 and H4.2, respectively). These findings concur with direct and/or indirect influences of objective measures of family financial status on subjective financial well-being of emerging adults (e.g., Serido et al., 2010; Xiao et al., 2009).

Parental subjective assessments of their financial status may be particularly useful in examining financial satisfaction when objective measures are hardly available or assumed poorly reliable. In Slovenian parents, for example, subjective ratings of the family income in a relative sense (social or past comparison) explained substantially greater portions of variance in their financial satisfaction and life satisfaction than the level of education (Zupančič et al., 2018). The subjective income (though related to the objective income, Diener & Oishi, 2000) also refers directly to individuals’ perception of financial conditions based on their own criteria, and so do the global life satisfaction (Pavot & Diener, 2008) and financial satisfaction (Diener & Oishi, 2000) depend on more than the objective income (e.g., on personal and contextual factors).

Intergenerational links

We found positive self-perceived financial learning outcomes of parents beneficial to the financial development of their children. Along with abundant single-informant studies (e.g., LeBaron et al., 2020; Shim et al., 2015) and sparsely used multiple-informant approach (Allsop et al., 2020; Lanz et al., 2020), our study suggests that the role of parental socialization in financial functioning of emerging adults is robust. First, parents’ views of the context they create to socialize their children financially predict the children’s views of their own financial learning outcomes. Second, parents’ financial learning outcomes are based (in part) on past financial learning in a different socioeconomic environment than the one in which their children grew up; yet, the parental outcomes have an important value for the children’s healthy financial development.

Specifically, parents’ self-reported financial knowledge and saving translated directly to their children’s self-ratings of the corresponding outcomes (H2.3). Furthermore, financial parenting as reflected in parents’ saving and delivering financial instructions encouraged their children to adopt parents as financial role models (H2.1). Consistent with the findings based on students’ data (Shim et al., 2010; Sirsch et al., 2020), the cross-informant associations in our model support the importance of both observing healthy financial behavior of parents (which the children tend to enact) during daily interactions and parental targeted lessons about financial matters. While the direct link of parent-to-child (saving) behavior suggests an emulation of what is modeled by the parents, not necessarily with a clear intention of the children to perform and/or accept, adopting parental role modeling involves internalization (Lanz et al., 2020) of parental financial behavior and instructions, reflecting willingness to enact and/or consider what has been observed/taught. The process of emulation should not be downplayed, however, as it appears not only to underlie behavior, but also motivational beliefs (e.g., about one’s own financial knowledge, as shown in our study) and specific motives for financial behavior (e.g., saving; Lep et al., 2021).

In contrast to Hypothesis 2.2, the parent-recollected financial lessons did not significantly shape the emerging adults’ subjective understanding of money management. This suggests that the previously identified link of emerging adult students’ recollections of parental instructions on how to manage finances to their financial knowledge (Shim et al., 2010; Sirsch et al., 2020) was likely subject to the same-informant bias. Nevertheless, both students’ cognitive financial learning outcomes (knowledge and adopting parental role modeling) further contributed to higher levels of their self-perceived capacity to regulate financial behavior in our study (H3).

Similarity of links across generations

We supported the Hypotheses 1.1, 1.2 and 5, proposing consistent links across two generations within the same family. Precisely, greater subjective financial knowledge and financial behavioral control promoted proactive financial behavior (saving), and better self-perceived financial behavioral control also enhanced satisfaction with money management (H1.1 and H1.2, respectively). Both parents’ and their children’s financial management satisfaction, in turn, predicted aggregated score of satisfaction with parent-child financial relationships (H5).

Likewise, the pattern of associations between the selected financial learning outcomes and aspects of financial satisfaction (i.e., knowledge, behavioral control → behavior → satisfaction with financial management → satisfaction with financial relationships) appears robust since parents and their children were socialized financially under different socioeconomic conditions. As financial socialization is an enduring process (Danes & Yang, 2014; Gudmunson & Danes, 2011), the parents have likely adapted their financial functioning to the change from market socialism to capitalist market socioeconomic system. In fact, the changes in Slovenia were not as substantial as in Eastern European countries. Before the transformation of the system, the country (Yugoslavia, but especially its federal republic Socialist Republic of Slovenia) was characterized as the most “Western” among socialist countries and shared some societal (e.g., individualization, pluralization; Kuhar & Reiter, 2014) and economic trends with its capitalist neighbors. Nevertheless, our results imply that the general processes of financial socialization responsible for successful personal money management may operate in the same way under different macroeconomic conditions.

Good management of personal/family finances essentially requires a general understanding of how to manage limited resources in a given context of individuals’ needs, desires, and objective demands, as well as self-regulation of behavior to resist temptations or avoid risky financial actions (Sirsch et al., 2020). Moreover, the sense of control over financial behavior is critical to how individuals behave, regardless of actual control (Danes & Rettig, 1993), and likely applies to how they evaluate their financial management, as indicated by the compatible pathways in our samples.

In addition to emerging adults’ relationships with parents shaping various aspects of subjective well-being (e.g., Lanz et al., 2020; Serido et al., 2010), our results show that satisfaction with money management of both parents and their children contributes to the positive evaluation of their financial relationships. This suggests a likely ‘co-responsiveness’ of satisfaction with financial management and satisfaction with financial relationships between family members. Consistent with transactional models of parent-child relationships (e.g., Kuczynski, 2003), both partners’ evaluations of personal money management enter the emotional nature of their relationship, which tends to affect satisfaction with financial management. This may be particularly salient in families with emerging adult children because on their way toward financial independence, young people still depend financially on their parents (especially students) but concurrently undergo an important restructuration of their socioemotional relationships with parents (Padilla-Walker et al., 2013; Tanner, 2006).

Limitations and future directions

Along with the strengths, there are limitations to our study. It was cross-sectional and correlational, which does not preclude the possibility of influences in the opposite direction. Longitudinal data in a cross-lagged panel design are needed to account for this shortcoming. Moreover, follow-up studies would capture development directly by examining how associations of financial functioning with financial satisfaction and parent-child financial relationships change and how gradual attainment of key markers of adulthood (e.g., full-time employment, moving out of the parental home) may affect these changes.

A non-random sampling confines our generalizations. Although our student sample matched the population of university freshmen by age, gender, and living situation, social science students were overrepresented. Also, emerging adults in tertiary education make up about half of the Slovenian population of 19-to-24-year-olds (SURS, 2022). The remaining half may differ systematically from students in terms of family socialization, their own financial experiences, and financial resources. Indeed, Mitchell and Syed (2015) found several differences in developmental trajectories of financial independence and sources of financial support between students and non-students. Further research needs to examine the models of financial socialization processes in employed, unemployed, and emerging adults with disabilities from an intergenerational perspective.

Considering our parent sample (both mothers and fathers), its structure by education, employment, and marital status also closely resembles the national population. Given social stratification in Slovenia is low (OECD, 2022b), the level of gender equity high (including a comparable rate of mothers and fathers working full-time), and university education is tuition-free, this was expected. Studies of financial development and well-being in countries with high social stratification, substantial tuition fees and student loans should also address the representativeness of students’ parents, as the student samples may be socially biased.

Although it is normative in Slovenia that each parent contributes equally to the family budget and is equally engaged in parenting, the oversampling of mothers may have influenced our results. Data worldwide shows that mothers spend more time on housework, including childcare and parenting, than fathers (OECD, 2022a) who might be more or less engaged in financial parenting (Agnew et al., 2018), are more liberal (Furnham & Milner, 2017), and the contribution of their education and employment to children’s financial knowledge is less prominent compared to mothers (Chambers et al., 2019), even in most “egalitarian” societies. Lacking the Slovenian data on actual gender involvement in financial parenting, however, we refrain speculating to what extent our results might be biased. Comparing maternal and paternal roles in financial education of children would certainly prove valuable; there is some data suggesting that an equal role of the mother and father in financial socialization promotes their children’s financial development (Allsop et al., 2020).

Our survey included very short scales or single-item measures. Consequently, we did not capture more nuanced components of the constructs (e.g., preventive financial behaviors), what financial concepts were taught by parents (LeBaron et al., 2018), and what was adopted by children (e.g., specific motives for saving, Lep et al., 2021). The differences in students’ assessments of maternal and paternal financial role modeling that could have contributed to the their financial learning outcomes to varying degrees were blurred in the combined measure. Likewise, the aggregation of students’ evaluations of their financial relationship with each parent (while only one parent reporting on parent-child relationship) introduced greater variance of scores and might have decreased the correlations between student and parent ratings, making the effect on the joint relationship measure harder to detect. While all but one of the proposed links were supported, however, we believe our approach did not notably undermine the results. Finally, future studies would benefit from observational data (e.g., during financial teaching tasks; Allsop et al., 2020) rather than relying solely on questionnaire measures.

Conclusion and implications

Based on the hierarchical model of Shim et al. (2010) and its adaptation to the context of Central European students (Sirsch et al., 2020), we created and examined an intergenerational model of financial socialization and its outcomes. We supported the pathways of parental financial socialization (parents’ self-perceived financial knowledge, healthy financial behavior, and financial instruction) to emerging adult children’s self-perceived financial learning outcomes (cognitive outcomes, behavioral control, financial behavior), and to their financial management satisfaction. We can thus conclude that these pathways, previously based on single data sources, are robust. Across the two generations, we further found similar links of self-perceived financial knowledge and financial behavioral control to healthy financial behavior, and of behavioral control and behavior to financial management satisfaction, even though the parents and their children were financially socialized under different macroeconomic conditions. Moreover, satisfaction with financial management in both generations favorably contributed to their evaluation of parent-child financial relationships. As the financial learning outcomes of parents’ own financial socialization (partly acquired within their family of origin) provided an encouraging context for their children’s financial development, as well as for financial satisfaction of both generations, this suggests that the proposed processes of financial socialization are likely similar across socioeconomic systems of (post)industrialized societies.

Our findings imply that parents and professionals should give greater recognition to the financial parenting in children’s healthy financial development by increasing parental awareness that financial knowledge, attitudes, and behaviors are passed on from one generation to the next through observational learning, explicit instruction and spontaneous communication already in early childhood (e.g., Danes, 1994). However, to create an encouraging financial learning environment and contribute to their own satisfaction with money management and financial relationships with their children, parents should be financially knowledgeable, able to regulate their financial behavior effectively, skilled in managing personal/family financial issues (Sirsch et al., 2020), and know what to communicate to their children (LeBaron et al., 2018).

Adult education programs, financial counseling services, and banking institutions could increase their engagement in financial education by offering courses, workshops and/or individual counseling sessions. School principals may invite professionals to give talks, organize discussions and roundtables about financial parenting, and encourage students’ parents to attend. In this way, parents could get useful information, advice, and support to improve their financial management and financial education of their children. School teachers of home economics (or related courses) could contribute through targeted instruction and by placing more emphasis on financially relevant content in students’ daily life, which could be particularly valuable for children and youth from less favorable family environments. University career centers could play a role in advising students on how to alleviate the deficits of their family financial socialization (see Butterbaugh et al., 2019 for therapeutic interventions). This would be beneficial not only for young people’s financial management, their relationships with parents, and financial future (Ashby et al., 2011; Danes & Yang, 2014), but also for their future financial parenting.

Supplemental Material

Supplemental Material - Intergenerational model of financial satisfaction and parent-child financial relationship

Supplemental Material for Intergenerational model of financial satisfaction and parent-child financial relationship by Maja Zupančič, Mojca Poredoš and Žan Lep in Journal of Social and Personal Relationships

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Javna agencija za raziskovalno dejavnost Republike Slovenije (Slovenian Research Agency) within the research program Applied Developmental Psychology (research core funding No. P5-0062).

Author Note

This research is a part of the collaborative international project Financial Socialization of Emerging Adults: The Roles of Parents, Work and Personal Values coordinated by Mihaela Friedlmeier, Grand Valley State University, Allendale, MI. It was funded by the Slovenian Research Agency within the research program Applied Developmental Psychology (research core funding No. P5-0062).

Open research statement

As part of IARR's encouragement of open research practices, the authors have provided the following information: This research was not pre-registered. The data used in the research cannot be publicly shared but are available upon request. The data can be obtained by emailing: maja.zupancic@ff.uni-lj.si. The materials used in the research cannot be publicly shared but are available upon request. The materials can be obtained by emailing: maja.zupancic@ff.uni-lj.si.

Supplemental Material

Supplementary material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.