Abstract

Keywords

Executive Summary

The initial adoption of Goods and Service Tax Network (GSTN) is one of the essential driving forces to influence the success of Goods and Service Tax (GST) in India. In addition, the diffusion of any technology (in this case, GSTN) is also affected by many variables, such as individual characteristics, organizational members, and social system. The theory of planned behaviour (TPB) and technology acceptance model (TAM) are widely used by researchers to understand the impact of these variables on behavioural intention. Thus, keeping in view the turbulence caused by GST, the present article tried to analyse the intention of business persons to use the GSTN by integrating TAM and TPB. The authors draw upon the literature to develop a structured questionnaire on the adoption of technology. Data has been collected from 204 small- and medium-sized business owners that have a GSTN number. Methodologically, structure equation modelling has been used to test the significance of the relationship among variables under study. Data analysis showed that many small business owners were facing technical issues at the time of filing GST. Results indicated that trust was one of the critical variables affecting the use of GSTN by business persons in India. However, perceived usefulness, subjective norms, and perceived behavioural control were found to have a significant influence on attitude towards GSTN that in turn affected the intention to use GSTN by the business person. The study presents steps for the government to improve the acceptability and understanding of the GSTN among small- and medium-sized business organizations for better compliance of the new tax regime. The study contributes to existing literature by testing the role of trust in facilitating the acceptance of an IT-based tax filing system (GSTN). In a developing country like India, where computer literacy is low, making such technology mandatory raises many challenges. The study provides insights in addressing challenges related to acceptance of GSTN by small- and medium-sized business organizations.

Information technology (IT) has become an important pillar of the new industrial revolution era due to its speed and accuracy in the task performed. In the new information era 2.0, it is more or less becoming mandatory for individuals and organizations to use IT and IT-enabled technology (Graham, 1998). It is estimated that expenditure and investment in IT in increasing worldwide. In the report, Outlook for the Global IT Market, Gartner Inc. said, ‘Worldwide IT spending is projected to total US $3.8 trillion in 2019, an increase of 3.2 per cent from expected spending of US $3.7 trillion in 2018’ (Gartner, 2018). Diffusion and acceptance of systems or technology among its potential users is one of the important aspects for success of IT and IT Enabled Services (ITES) companies. It is a growing research area as the diffusion of technology is a very complicated process which depends on a number of individual (personal factor) or environmental- and technology-related factors. Thus, the success of large technological investment, acceptability and quality of systems being developed, etc., has become an area of interest for researchers across the world (Linders, 2006). Researchers (Abu-Dalbouh, 2013; Khatibi, Thyagarajan, & Setharaman, 2003; Linders, 2006; Ndou, 2004; Wu & Chen, 2005) across the world are continuously working on the diffusion of many technologies, such as enterprise resource planning (ERP), mobile application, online shopping, and online taxation systems, in order to improve the quality of the technological solutions (IT system) being developed.

The Goods and Service Tax (GST) regime was implemented on 1 July 2017, as an indirect taxation system in India (Press information Bureau, 2018). It is a destination-based value-added tax (VAT) system. For filing GST, there is an online interface called the GST Network (GSTN) provided by the government in collaboration with the private sector. It is maintained by a non-profit company, in which non-government financial institutions hold a 51 per cent share (Goods and Service Tax Network, 2019). As per the GSTN company website, rupees 100 million is the authorized capital for providing IT infrastructure to the GST regime. The shift from a manual to an online tax filing system (GSTN) has brought many challenges, especially to small- and medium-sized business organizations (Fintrakk, 2017). For private organizations, providing services online is an augmented part of the delivery to attract and retain maximum customers with an objective of earning more profit. Whereas in the case of the government, the primary objective of promoting and implementing a new system or technology is to make government services convenient to citizens (Wu & Chen, 2005). Thus, government e-services are different from services offered by a company as the acceptance of the new technology depends on many extraneous factors (mandatory use, voluntary use, and imposition). Under the new tax system in India, filing tax online through the GSTN is mandatory. The Indian government is aggressively encouraging business organizations to use the GSTN for declaring and filing their tax. However, adoption and understanding of the system is still low among its end users, that is, business persons. Business organizations, especially small- and medium-sized organizations are facing challenges in filing their tax online regardless of the promotional and educational efforts made by the government. Owing to this, they need to hire professional accountants for filing the tax, which, to an extent, defeats the purpose of the GST regime (Fintrakk, 2017).

For evolving business persons’ behaviour towards the initial adoption of the GSTN, understanding the user’s expectation and behaviour is a prerequisite for designing the e-services since it could identify various barriers at the very first step. Initial adoption of an online taxation system involves two things, that is, acceptance of internet technology and online service providers.

In order to apply technology acceptance model (TAM) in the context of online/internet technology (GSTN, in case of this study), certain modifications were required in TAM (Davis, Bagozzi, & Warshaw 1989). Thus, the model has been modified by adding ‘trust’ in the studies undertaken by Gefen, Karahanna, and Straub (2003a) and Wu and Chen (2005) for exploring the acceptance of online shopping and an online taxation system. This extended model positioned the use of both systems’ features (internet technology and service providers), such as trust, ease of use and usefulness, and the result indicated that all these variables were the better predictor of behavioural intention (BI) to use e-service. Other variables, such as individual, communication method, organizational members and subjective norms (SN), also affect the acceptance of technology (Roger, 1995). Thus, the theory of planned behaviour (TPB; Ajzen, 1991) has been used to predict the influence of individual, organizational, and social factors in the process. Therefore, TAM has been augmented by trust and TPB to examine the adoption and acceptance of an online tax filing system called the GSTN in India. The findings of this research may provide some meaningful insights to resolve the issues (behavioural, technical, and social) associated with acceptance of GSTN by end users (small- and medium-sized businesses).

BACKGROUND

Understanding GST and challenges associated with GSTN will provide insights into potential remedial measures that can be taken to mitigate the technical bottleneck in the implementation process. Small- and medium-scale business organizations are the growth engine for any economy. In India, such an understanding of MSMEs holds the potential to make policy initiatives impactful.

How Can GSTN Not Be Accepted, When It Is Mandatory?

In India, GST is one of the much-awaited indirect tax regimes (Pollard, 2012). In 2017, the Indian government implemented mandatory filing by the online system, that is, GSTN. A significant amount of money has been expended on advertisements and training to facilitate the adoption of the GSTN. According to the Economics Times (2018), the Indian government has spent 1323.8 million on the advertising of GST. However, it has not translated into acceptance of GSTN by end users, especially in small- and medium-sized business organizations. Using the GSTN for filing the tax is one of the mandatory processes under the new tax regime. In a country like India, where people are reluctant to pay tax, even by going online, acceptance of the GSTN by small- and medium-sized businesses becomes a difficult task. Government seems quite aware of this fact, which is why the entire advertising budget has been spent on print media, whereas expenditure on electronic media is reported as ‘NIL’ according to the Bureau of Outreach and Communication under the Ministry of Information and Broadcasting (The Economics Times, 2018).

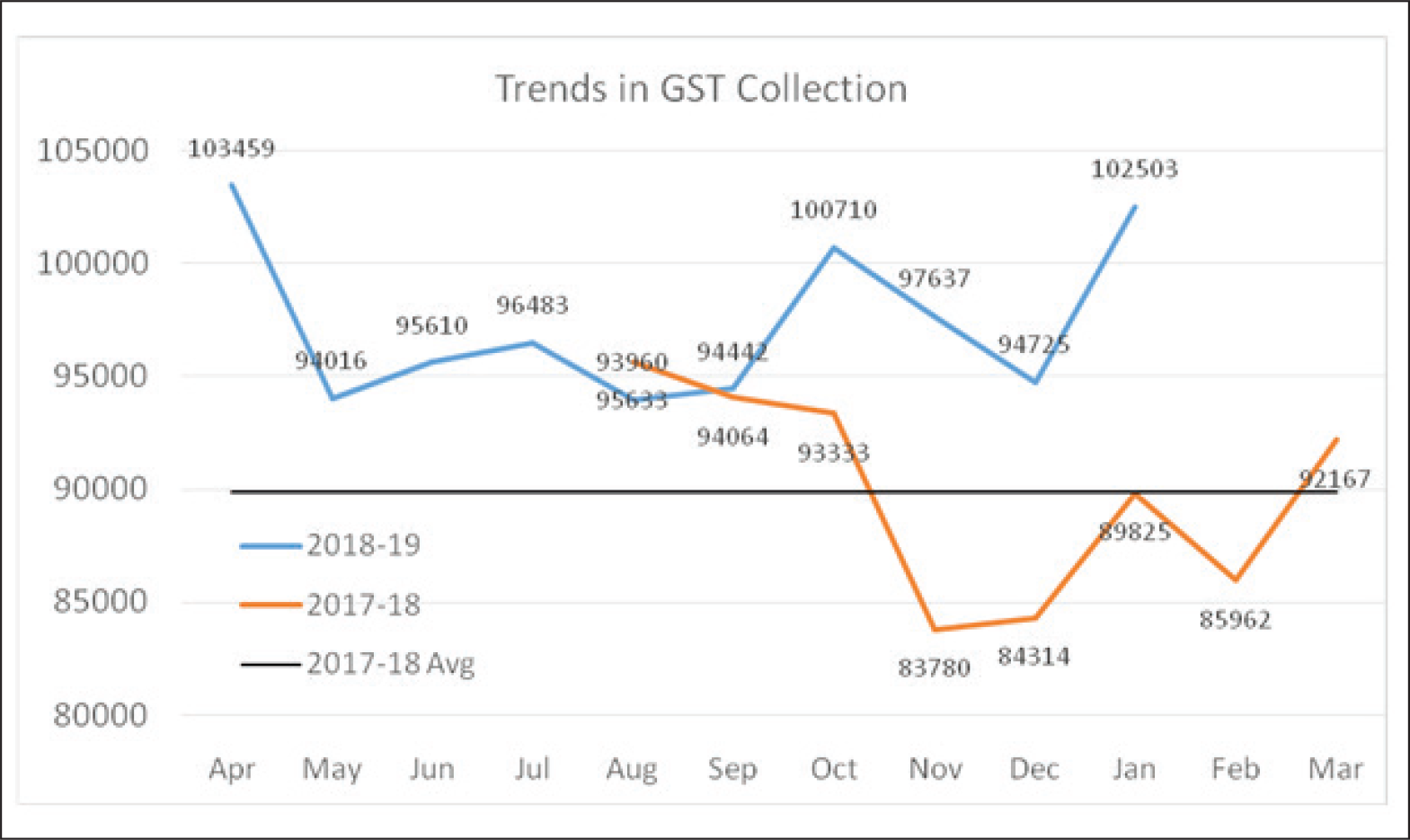

The revenue collection after GST, shows high fluctuations (see Figure 1). Although, the number of GST returns filing is increasing every month due to increased understanding of the GST system and network, a uniform pattern does not emerge.

The initial investigation at the ground level has suggested that small-scale business persons are hiring professionals to file their tax and returns. As a result, costs as well as complexities of the business are increasing. GST was implemented to make the indirect taxation process easy and simple so that it may eventually increase the number of taxpayers (compliances) and revenue collection. Thus, the fundamental purpose of GST has not been met as evidenced from the fluctuations in GST returns (Figure 1). In the 32nd meeting of the GST Council, the decision was taken to file a return annually with a quarterly payment of tax (GST Network, 2019).

The findings of this article may be useful in increasing the adoption and use of the GSTN by actual end users, that is, business persons themselves. Focusing on variables such as behavioural control, perceived usefulness (PU), perceived ease of use (PEU), attitude, SNs, and trust may increase the acceptance of the GSTN among potential users.

Can TAM Be Applied to Mandatory GSTN System Use?

TAM has been widely used by researchers to measure the acceptance of information systems in choice-based situations. However, it will be interesting to see if TAM can be applied to a mandatory system use. So, the main criticism of the TAM model (i.e., its applicability in volitional behaviour) will be clarified, and new variables (trust, the role of environmental settings, behavioural control) maybe introduced to increase the predictability of the model. TAM is limited in terms of its application in voluntary technology acceptance. Only a few studies (Gallivan, 2001; Linders, 2006) have attempted to use TAM in mandatory environmental settings and found that there is need to make the model robust by adding more variables (actual use, environmental settings, usability).

Literature Review and Theoretical Framework

GST and International Scenario

GST is a flagship tax regime implemented by the government in India, which consolidates all the indirect taxes on goods and services. However, the concept of ‘one nation, one tax’ is not new and has been adopted and implemented by countries worldwide. Mansor, Hafizah, and Illias (2013) discussed GST as new tax reform in Malaysia and concluded that GST would boost tax consumption revenue. In their study, they predicted that with a continuous reduction of the corporate tax from 28 per cent to 26 per cent in the year 2008, GST has provided comfort to businesses in tax compliances. Gupta, Singh, Kumar, Kumawat, and Hemraj (2017) found that VAT such as GST has adversely affected the economies of every country, especially developing countries. The author compared the VAT tax system in the USA and Europe and concluded that VAT as a tax is a burden for the economy. However, there is no uniformity found in terms of the structure of the GST regime (Firth & McKenzie, 2012; Mansor et al., 2013). Gupta et al. (2017) concluded that the Australian financial services industry is taxed on an input taxation basis, that is, the output mortgage service is not liable to GST and GST paid on input services to provide the mortgage services are also not allowed. The extra cost of input tax is passed on in the form of increased mortgage costs to customers, making the housing costly post-introduction of GST in Australia. Keating (2010) compared the anti-evasion provisions in Australia and New Zealand and found that in New Zealand, assessors found tax evasion difficult after implementation of the new law. Thus, all over the world, GST has been implemented with the objectives of simplification of taxation and increased tax compliance.

Technology Acceptance Model (TAM) & Theory of Planned Behaviour (TPB)

The TAM has been adapted from the theory of reasoned action (TRA) given by Fishbein and Ajzen (1975). It is specially designed to understand and predict the acceptance of IT (Davis et al., 1989) by its potential users. TAM hypothesizes that use of technology depends on the intention to use, which, in turn, is influenced by the attitude towards that technology. PU and PEU are two important determinants of the attitude of the individual: PU is the belief of the user towards the helpfulness of technology for improving the current performance (Taylor & Todd, 1995), whereas PEU is the salient belief in effort free use of technology (Taylor & Todd, 1995). However, the cognitive component of PEU influences the PU as well. Intention is the degree to which the user agrees to use the technology. In a few studies, actual use of the system is measured by user satisfaction. However, in the original TAM, intention to use was included instead of user satisfaction. In a mandatory use situation, intention to use becomes more important than user satisfaction from technology, as the success of the scheme/system depends more on the actual use of the system by the users themselves, for example, taxpayers in the present case. Satisfaction from technology is an aspect of improving it, whenever the requirement arises, whereas intention to use is a continuous form of acceptance of the technology. Thus, intention is a good indicator to measure the diffusion of technology. In the case of GST as well, intention to use becomes much more relevant, as the use of GSTN is one of the prerequisites for its success.

Ajzen (1991) used the TPB for predicting human behaviour towards the acceptance of information technologies. According to TPB, a person’s behaviour for performing a specific action is directly influenced by his/her intention, which, in turn, is affected by attitude (AT), SN and perceived behavioural control. BI is the strength of an individual’s willingness to try or exert while performing a particular behaviour. Attitude is one’s feeling of a favourable or unfavourable assessment towards the targeted behaviour (Fishbein & Ajzen, 1975). Furthermore, favourableness of attitude has a direct influence on the behavioural beliefs about the probable consequences. SNs, on the other hand, refer to the perceived social and organizational pressure while trying to perform the particular behaviour (Ajzen, 1991). SN is the normative beliefs about the expectations of other persons towards the targeted behaviour. Perceived behavioural control is the perception towards ease of performing a particular behaviour and refers to the belief about the control of factors that may facilitate and hinder the performance of that behaviour. In sum, the TPB was proposed to eliminate the limitations of the TRA to depict the behaviour of individuals towards any action.

TPB differs from TRA in terms of addition of perceived behavioural control. However, many external variables were identified by various research studies to increase the predictability of the model. Later, many theories, such as the TAM by Davis et al. (1989), innovation diffusion theory by Roger (1995), the unified theory of acceptance and use of technology by Venkatesh, Thong, and Xu (2012), etc., were developed by researchers to understand the acceptance and diffusion of technology. The TAM (Davis et al., 1989) has been widely used by researchers to understand the acceptance of myriad technologies (Ma & Liu, 2004; Nath, Bhal, & Kapoor, 2013; Venkatesh & Morris 2000; Yarbrough & Smith, 2007). TAM is primarily based on the principle of TRA, which explains how to measure the behaviour and attitude vis a vis impact of belief on the attitude that is further impacted by external stimuli. Over a period of time, a number of variables were added by researches in order to increase the predictability of the TAM.

H1. PU significantly affects a business person’s attitude towards the use of the GSTN.

H2. PEU significantly affects the attitude to use the GSTN.

In the original TAM model, PEU was conceptualized to affect PU, but a vice versa relation was not indicated. Several studies have confirmed that if the individual user feels that using any technology is free from effort, he/she will find it useful as well, and one of the main objectives of any technology (in this case, GSTN) is to reduce the effort and time for completion of the task (declaration of tax). Thus, the following hypothesis has been developed:

H3. PEU significantly influences PU of the GSTN.

A few studies (Wu & Chen, 2005; Zhang et al., 2019) have attempted to understand the interplay of ease of use with trust in technology. Generally, it can be seen that if the user finds any technology free from effort, they are more inclined to use that technology, and later, continuous use develops a sense of trust in it. Therefore, the following hypothesis has been formulated:

H4. PEU significantly affects the trust of the user in the GSTN.

H5. Attitude significantly affects the intention to use the GSTN.

H6. SNs significantly affect the intention to use the GSTN.

H7. Perceived behavioural control significantly affects the intention to use the GSTN.

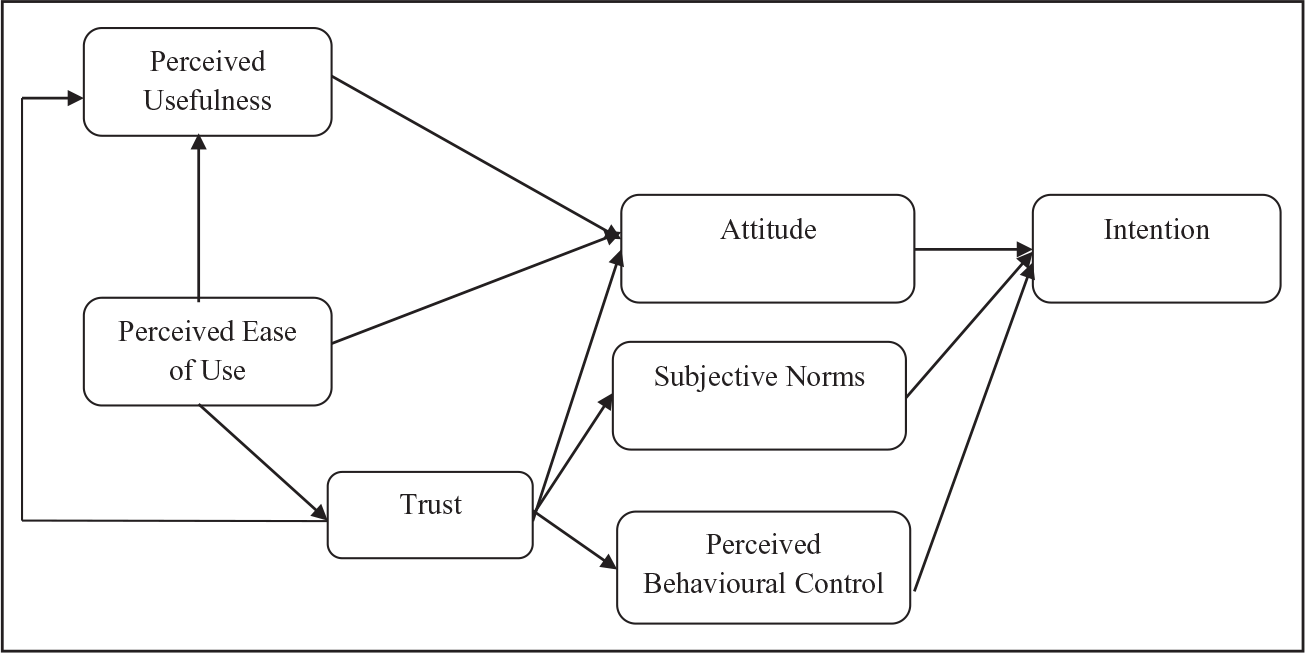

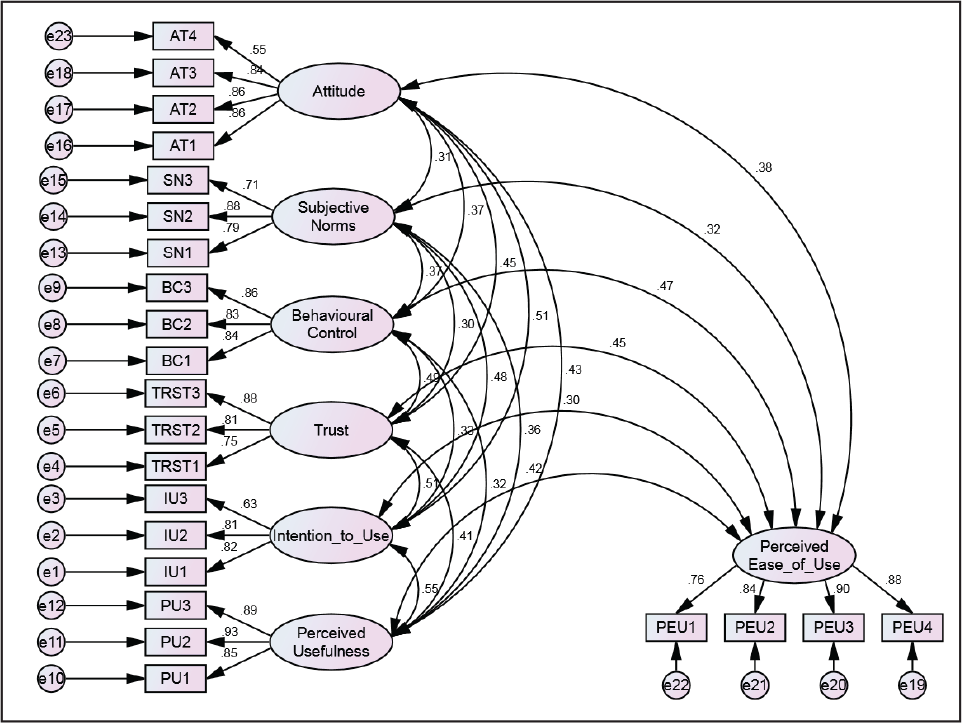

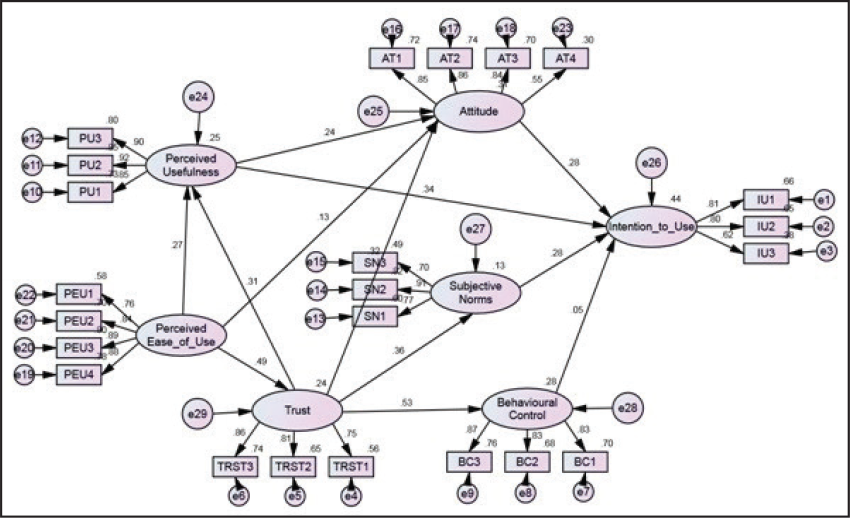

H8. Trust significantly affects the PU of the GSTN. H9. Trust significantly affects the attitude to use the GSTN. H10. Trust significantly affects SNs. H11. Trust significantly affects the perceived behavioural control. In this study, TAM and TPB have been combined to structure the research process (Figure 2).

PURPOSE OF RESEARCH

India is one of the few countries where GST has been implemented. However, it has taken more than a decade to get GST implemented owing to many factors (political, social, technological, and economic). The present study tries to explore the challenges faced by small- and medium-sized business organizations after the implementation of GST. As such, TAM and TPB have been integrated to find out the role of attitude, SNs, behavioural control, PU, PEU, and trust on intention to use the GSTN.

METHODOLOGY

Data Collection Instrument

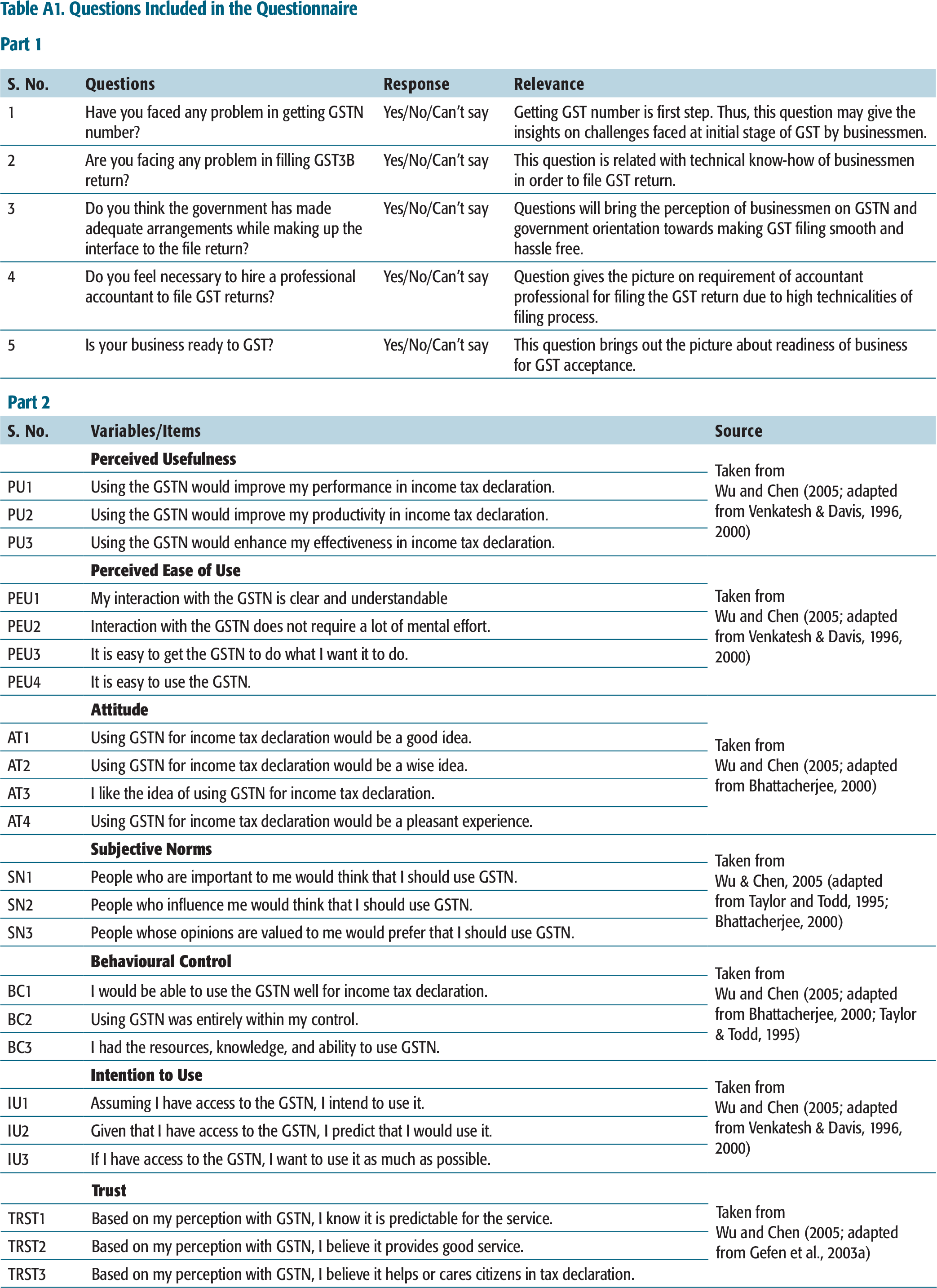

Data were collected from small- and medium-scale business organizations using a structured questionnaire. The study was conducted into two parts. In the first part, along with basic demographic information, a structured questionnaire with five simple (categorical) close-ended questions was used. Respondents were asked to give their response to GST in yes/no/cannot say answers. The instrument was kept as simple in order to get a clear picture and maximum responses. In the second part, the same set of respondents was given a structured questionnaire related to the adoption of the GSTN for filing the tax return. This part attempted to understand the behaviour towards GSTN and was based on the TAM and the TPB. PU, PEU, attitude, SNs, behavioural control, intention to use, and trust (Bhattacherjee, 2000; Gefen et al., 2003a; Taylor & Todd, 1995; Venkatesh & Davis, 1996, 2000; Wu & Chen, 2005) variables were used to measure the acceptance of respondents towards GSTN. The two-page questionnaire contained 23 items on different variables (seven variables). Respondents were asked to give their response on a five-point Likert scale (1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, 5 = strongly agree). The questionnaire is available as Table A1.

ANALYSIS AND RESULTS

Demographic Profile

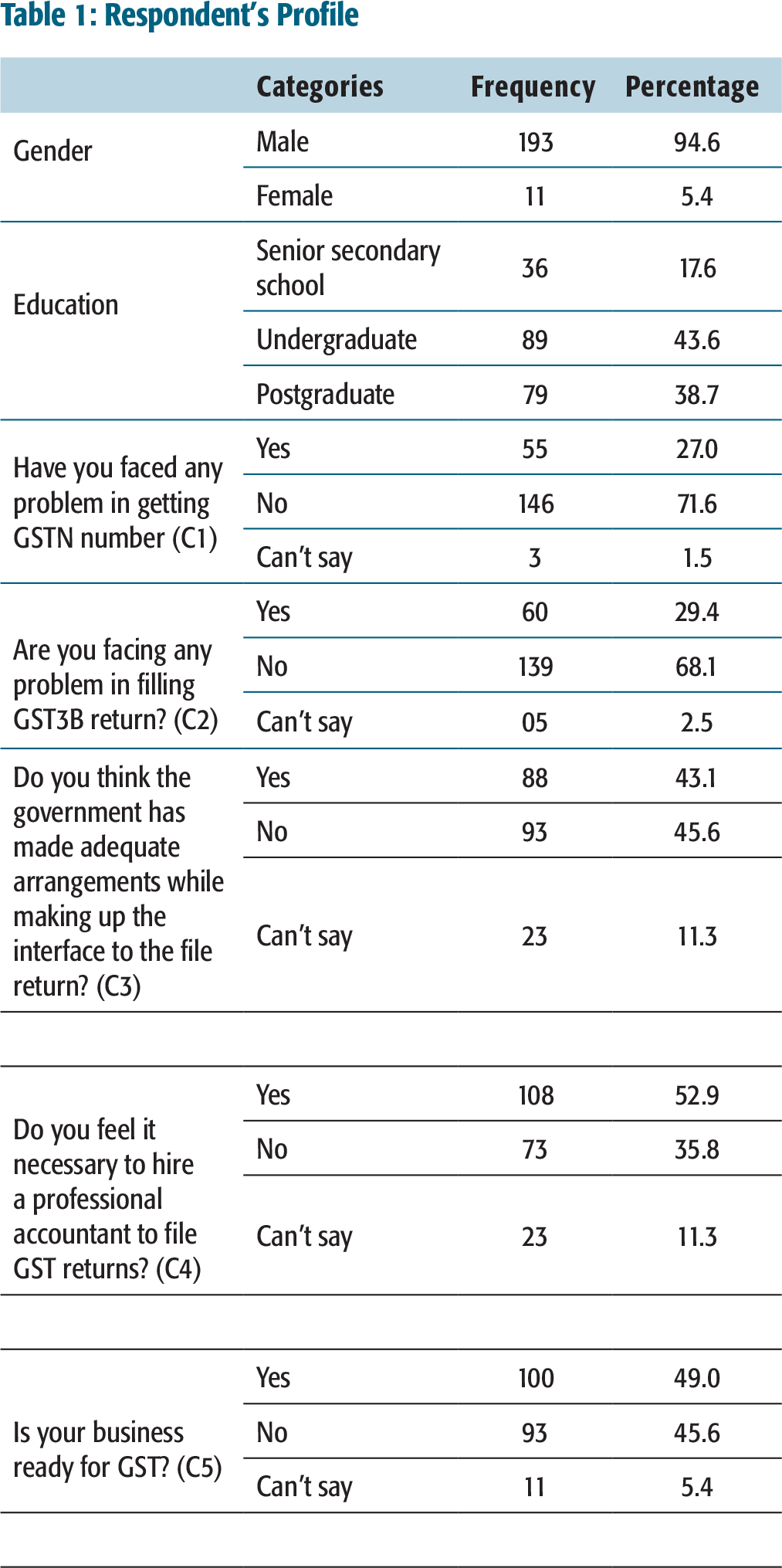

The sample constitutes 94.1 per cent male and 5.9 per cent female respondents as the majority of the business owners in India are male (See Table 1). Table 1 depicts the response of small- and medium-sized enterprises towards the newly hailed GST system. It can be seen that at the time of GST registration, only 27 per cent of respondents faced a problem. About 71.6 per cent indicated that they understood GST registration easily. However, an increased number of respondents have faced problems at the time of filing their GST return. Table 1 shows that 52.9 per cent of respondents felt the need to hire a professional accountant for filing their returns. Subsequently, 49 per cent of respondents said that their business was not ready for the new taxation regime.

MEASUREMENT MODEL

Respondent’s Profile

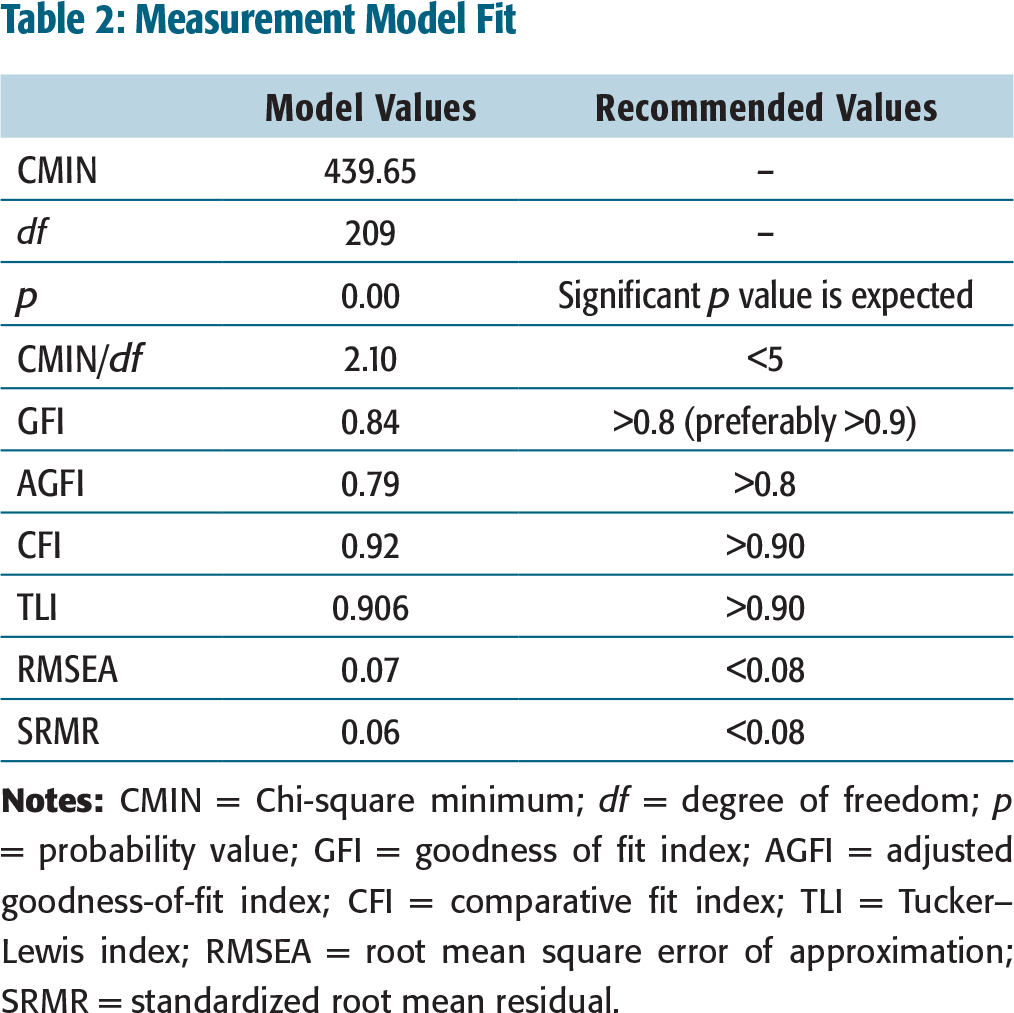

Measurement Model Fit

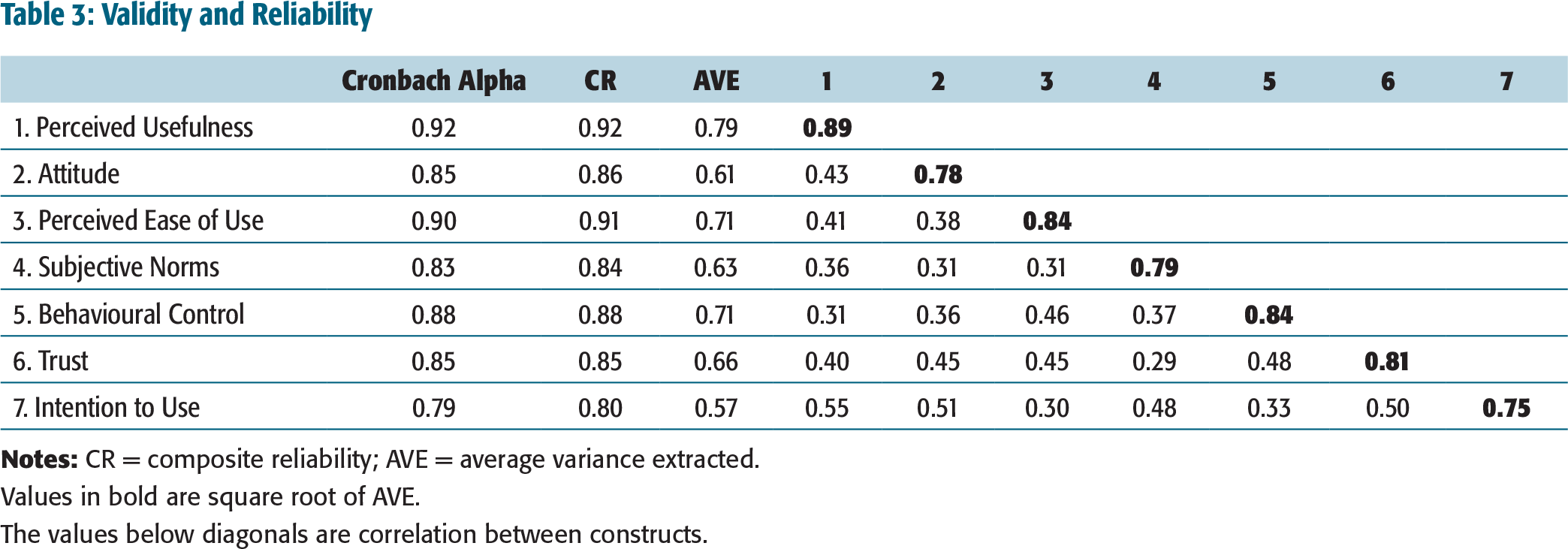

CONSTRUCT VALIDITY AND RELIABILITY

Reliability

Reliability of a construct refers to the extent of internal consistency of the measures, that is, whether observed variables are internally consistent to the corresponding measure or not (Hair et al., 2010). Generally, Cronbach’s alpha coefficient is used to assess the internal consistency of the measures, and alpha value higher than 0.7 indicates internal consistency in the measures (Nunnally, 1978). Another measure of reliability is composite reliability (CR), which is considered to be superior to Cronbach’s alpha (Chin, 2010). CR value more than 0.7 indicates the internal consistency of the measure (Hair et al., 2010; Nunnally, 1978). Table 3 gives the value of both Cronbach’s alpha as well as CR, and, as these values are above the threshold limit of 0.7 for each construct, it indicates that the constructs under study were internally consistent and reliable.

CONVERGENT AND DISCRIMINANT VALIDITY

Convergent validity refers to ‘the extent to which observed variables converges to their corresponding latent constructs’ (Hair et al., 2010). Convergent validity is assessed using the average variance extracted (AVE). If this value is more than 0.5, it indicates that observed variables are explaining a minimum of 50 per cent of the variance in the construct (Fornell & Larckel, 1981). Table 3 gives values of AVE for each construct under study. The table shows that AVE values for all the constructs are more than the threshold value, that is, 0.5 as suggested by Fornell and Larckel (1981) which confirms that observed variables are converging to the corresponding latent constructs. Discriminant validity, on the other hand, refers to the extent of the uniqueness of a construct compared to other constructs of the model. It shows the ‘extent to which two constructs are truly distinct from each other’ (Hair et al., 2010). To establish discriminant validity among constructs, the square root of AVE value was compared with the inter-construct correlation. A higher value of the square root of AVE compared to correlation value indicates that the two constructs are distinct to each other (Fornell & Larckel, 1981). Table 3 gives the square root of AVE in diagonals and correlation among the constructs, below the diagonals. It is clear from these results that all constructs are unique and distinct as the diagonals values (square root of AVE) are higher than the correlation values.

Structural Model

Validity and Reliability

Values in bold are square root of AVE.

The values below diagonals are correlation between constructs.

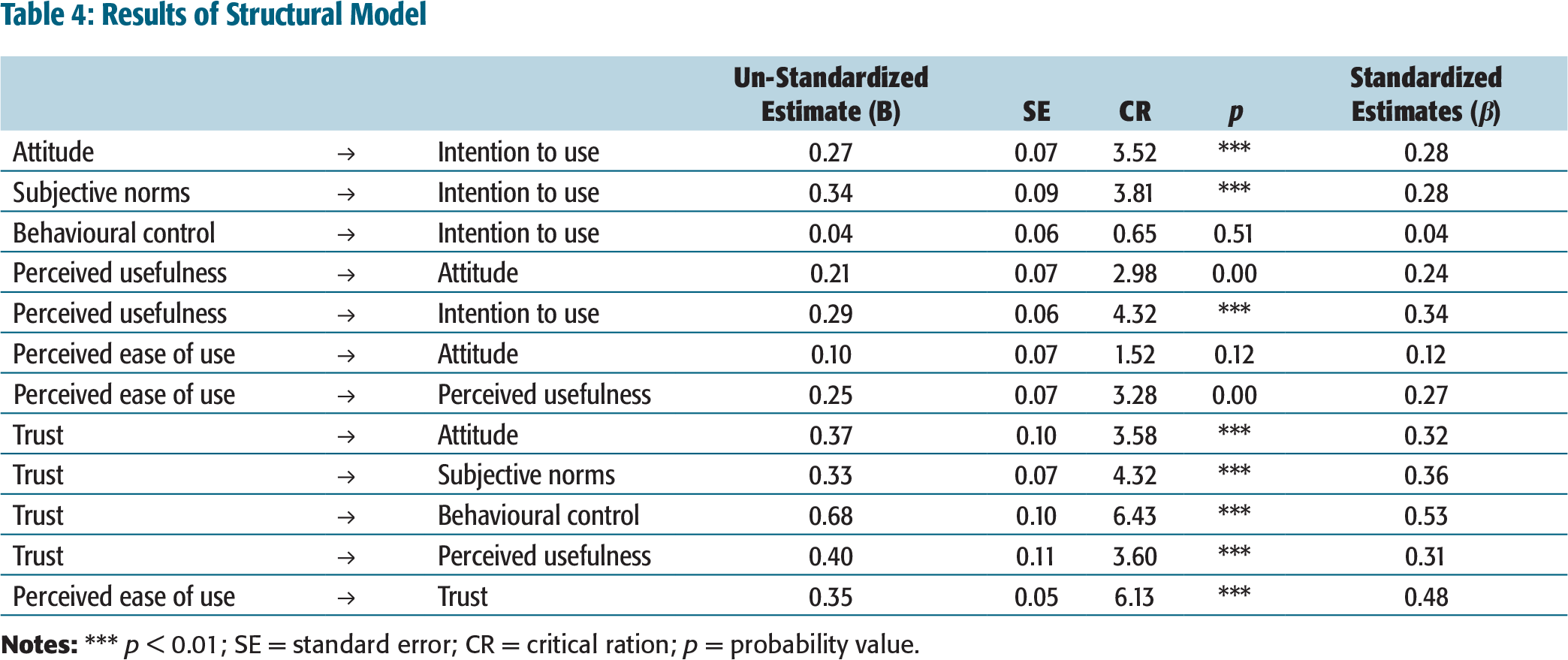

Results of Structural Model

In the TPB (Ajzen, 1991), attitude was conceptualized as one of the primary determinants of BIs. The results (Table 4) in the present study also confirmed and supported this hypothesis as attitude (B = 0.27; SE = 0.07; p < 0.01) had a significant positive influence on intention to use the GSTN, an online system of tax filing. Another important variable in the TPB, that is, SNs (B = 0.034; SE = 0.09; p < 0.01), was also found to have a significant positive influence on intention to use GSTN. However, perceived behavioural control (B = 0.04; SE = 0.06; p > 0.05), the third important determinant in TPB, was not found significant in the adoption of GSTN. Thus, out of three determinants of the TPB, two (attitude and SNs) were found significant, whereas behavioural control was not a significant factor in determining intention to use GSTN.

PU and PEU were hypothesized to be the primary predictor of an individual’s intention to adopt specific technology in the TAM (Davis et.al., 1989). In the present study, both these variables were hypothesized to affect attitude along with a direct path between PU and intention to use. The results of the structural model showed that in the adoption of GSTN, perceived usefulness was found to influence attitude (B = 0.21; SE = 0.07; p < 0.05) as well intention to use (B = 0.29; SE = 0.06; p < 0.01). However, the relationship between PEU and attitude was found non-significant (B = 0.10; SE = 0.07; p > 0.05). The TAM also postulates that the ease of using technology would lead to enhancing its usefulness. This hypothesis has been supported by the results (B = 0.25; SE = 0.07; p < 0.05) in the present case.

Along with extending the TAM and the TPB to explain the adoption of GSTN, the study also proposed trust (Wu & Chen, 2005) as an external variable to these models. The proposed research model in the present study hypothesized a direct relationship between trust and all three measures of TPB (attitude, SNs and behavioural control). Results supported all three hypotheses as trust was found to have a significant positive influence on attitude (B = 0.37; SE = 0.10; p < 0.01), SNs (B = 0.33; SE = 0.07; p < 0.01) and behavioural control (B = 0.68; SE = 0.10; p < 0.01). Trust was also hypothesized to influence PU, which was supported by the results (B = 0.40; SE = 0.11; p < 0.01). Also, PEU was found to have a significant positive influence on trust (B = 0.35; SE = 0.05; p < 0.01) (See Figure 4).

DISCUSSION

GST implementation brought many challenges with it, especially for small- and medium-sized enterprises. Lack of resources and misunderstanding many subtle accounting issues led to many operational problems. Data showed that more than one-third of business persons from the sample were facing a problem at the very first step, namely getting the GST registration number and filing returns. Challenges at the very outset tend to develop a negative attitude among business persons that discourages them from filing the GST return by themselves. The data also reflects that a large number of respondent were facing technical issues in filing GST3B returns. Computer literacy was also one of the foremost hurdles business persons encountered while filing GST. There were also many other issues like trust on system, system complexities, political disagreement/agreement, etc., related to the initial adoption of the GSTN by its users. While considering both types of issues, internet related (internet connectivity, efficacy to work with e-technology, etc.) and e-vendor-related (ease of interface, belief on e-vender, etc.), the TAM in integration with trust seems appropriate for exploring the acceptance of online tax service (GST).

Online taxation (GSTN) is one of the types of e-service under the GST regime and diffusion of this service must be an important concern of the government and policymakers. Using an extended form of TAM with TPB and trust, the study tries to increase the predictability of intention to use an online taxation system (GSTN). Empirical results showed that trust is one of the strongest antecedents of the four determinants of intention to use technology, PU, SNs, behavioural control and attitude. Results indicated that the explanatory power of BI in the integrated TAM and TPB model with trust had increased substantially. Trust emerged as the most crucial non-technological factor influencing the acceptance of GSTN. Empirically, trust was found to have a positive relationship with PU, which, in turn, affected the attitude towards GSTN. Thus, for developing a positive attitude towards GSTN, government and the GSTN company must ensure that small business owners must trust the network (GSTN). Trust in IT and the system they are going to use is one the prerequisites for ensuring the adoption of technology. In the analysis, trust was also found to be a significant antecedent of SNs and behavioural control. People tend to motivate other people for using a particular technology if they believe in the security features of the technology. In order to increase the behavioural control for using the online indirection tax system, that is, the GSTN, online tax providers must develop a trust-building mechanism for small business owners. Training for skill development, guarantee statements, communication programmes and user-friendly interface can enhance the trust building further. PU of the online tax filing system came up as a strong antecedent to affect the attitude of the user towards GSTN. However, without proper consideration to trust, even a well-designed online taxation system with significant PU will not serve the purpose to attract the user (a small business owner, in this case).

Indeed, in India computer literacy is one of the challenges that government faces while implementing any e-service for the citizens. Ability to understand and work on the computer and related services is one of the prerequisites for willing adoption of the GSTN. For small business owners the trust factor plays an important role for adoption of any mandatory technology. These problems can be overcome with the help of e-readiness assessment, raising awareness among the public and private organizations, stimulating collaboration and coordination among stakeholders and investing in human development. The present study also brings forth some peculiar findings, such as PEU was found to be an insignificant determinant of attitude, along with perceived behavioural control in affecting the intention to use. The probable reason behind this relationship may be the mandatory use nature of GSTN to file taxes. Whether a user or business person wants to use it or not, they have to leverage it for filing the tax, possibly with the help of a professional accountant.

Contrary to the expectations, behavioural control was also insignificant in affecting the attitude owing to the mandatory nature of GSTN. Mandatory use of GSTN for filing the returns is likely to have created the belief among business persons about the enforced use of technology, either by hiring professionals or any other means, although the government has exempted small business owners with a turnover below 2 million (this has now increased to 4 million) from GST. Thus, it can be anticipated that with the span of time, small- and medium-sized businesses might be able to understand GSTN properly and trust building will also take place, and as a result return filing and revenue collection may increase (Figure 2). One of the key objectives of the GST system is to increase the number of taxpayers under the new regime. Research on tax avoidance has indicated that tax evasion and avoidance is not only an economic deterrence but behavioural factors, tax rates, penalties, complexities of system, and information access are also influential factors (Kirchler, Maciejovsky, & Schneider, 2003; Olsen, Kasper, Kogler, Muehlbacher, & Kirchler, 2019; Wärneryd & Walerud, 1982). Thus, by reducing the complexities of GSTN, government and policymaker can enhance the coverage of taxpayers for the newly implemented GST.

LIMITATIONS OF STUDY AND FUTURE DIRECTIONS

The present study is based on small-scale business organizations. Large-scale organizations may not face these problems since a large pool of resources facilitate the challenges related to GST implementation. The impact of some demographic variables (educational status, state-wise difference, age, types of business) has not been explored, so that may have a moderating effect of acceptance of GST. Third, the intention to use GSTN to file a tax return may also be influenced by tax compliance and avoidance behaviour of the business person. As studies have indicated that taxpayers are more reluctant to pay the tax than about going online, measuring the tax avoidance behaviour may give a clearer view on the adoption of the GST system. A study in this direction may give better insights on acceptance of a mandatory information system for any policy initiative.

CONCLUSION

GST is one of the watershed decisions in the history of the indirect taxation system in India. However, small- and medium-sized organizations are still facing many challenges at an initial level, such as getting a GST number, filing returns, and understanding the input tax credit system. There are many contributory factors, even though some are disguised, affecting the acceptance of GST among small- and medium-sized businesses. The study concludes that in order to increase the acceptability of GSTN, one of the mandatory use systems under the new tax regime, trust plays a significant role. Trust in technology affects the attitude, SNs and behavioural control and jointly influences the intention to use technology (GSTN). Thus, if the government wants to increase the acceptance of the GSTN among business persons, creating trust in the system (GSTN) is a critical factor. Organizing workshops/trainings and investing in advertising GSTN may have a positive impact.

Further, PEU was found to affect the trust, which, in turn, affects the PU and both jointly influence the attitude of business persons towards technology (GSTN). Indeed, making the system user-friendly may be the potential enabler for the acceptance and use of GSTN.

Appendix

Questions Included in the Questionnaire

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.