Abstract

Executive Summary

The article examines the numeracy and financial literacy of the Indian forest-dependent communities (FDC) involved in the joint forest management (JFM) programme, launched by the Government of India in 1990. An understanding of the financial literacy levels of the Indian FDCs may provide insights to policymakers regarding customized literacy programmes that can reduce exploitation from petty traders and local forest officials. The research draws sample data from FDCs of two geographical regions with differing resource endowments (Rayalaseema and the coastal region) in the Indian state of Andhra Pradesh. The results show that a third of the sampled members of the FDCs were able to answer the questions on probability and simple interest correctly. At least half of the sample had a clear idea on the time value of money and had less difficulty in computing when the mathematical questions were framed in the form of sentences which embedded situations from their daily lives. Participants, however, faced difficulty in recognizing mathematical symbols and performing simple computations in addition, subtraction, multiplication, and division. The average scores of the sample in the standard numeracy and financial literacy tests were 4.98 (out of 12 points) and 1.32 (out of 5 points), respectively.

The study also identifies some socio-economic determinants of (numeracy and) financial literacy. Education has a positive effect on both numeracy and financial literacy, while household size has a negative effect on numeracy, with no effect on financial literacy after controlling for education. Members of FDCs with habitations close to towns are likely to be more numerate and financially literate.

The study calls for a deeper comprehension of financial literacy that addresses the nuances of participatory forest management. Rigorous public programmes for imparting financial literacy to the FDCs will not only make the JFM programme more successful but also provide employment avenues to the women in the FDCs. Financial literacy programmes would also facilitate the ongoing digital inclusion programmes undertaken by the government in forest agency areas.

Across the world, forest-dependent communities (FDCs) are among the more disadvantaged sections of society. They have poor access to economic opportunities, health care, nutrition, and education. Isolated from the mainstream society socially, culturally, and geographically, the FDCs dwell in forests and its fringes in hamlets and depend on forests for their livelihood (Davies & Bennett, 2007; Kumar, 2002). In the last three decades, the FDCs have been influenced by forces of economic development, urbanization, technological progress, and evolving administrative models like participatory forest management. These changes may have impacted their economic behaviours, especially their numeracy and financial literacy (Bandi, 2013). As FDCs, a severely marginalized community, increase their interface with the mainstream society, they may become vulnerable to exploitation. For example, Rangasami (1985) shows that famines result in transfer of resources where FDCs sell their land, cattle, labour, and other assets at extremely low prices to its richer members and are forced to buy grains at exorbitant prices which lead to destitution and misery.

With the advent of financial liberalization in most emerging and developed economies, there is a growing interest in financial literacy, as financial decision-making at the household level influence the participation of households in the financial markets. However, most of the studies in financial literacy have focused on populations in the developed economies on specific issues such as stock market participation, retirement planning, debt, and mortgages, and conclude that the populations have poor financial literacy (Lusardi, 2012; Lusardi & Mitchell, 2007, 2008, 2011). Financial illiteracy is more severe in developing economies (Gaurav & Singh, 2012; R. Pal & Pal, 2012). There is a growing body of evidence of financial exclusion of large subgroups of population in India such as agricultural labourers, small landholders, and marginalized communities (Gaurav & Singh, 2012). Poor financial literacy is reported in India across urban (Agarwalla, Barua, Jacob, & Varma, 2012) and rural households (Rao, 2001) and fishing communities (Hapke, 2001). Deshpande (1981) brings out that Warli forest tribes of Maharashtra lack the ability to count and calculate.

In this backdrop, of the poor financial literacy of the marginal communities, the article attempts to assess the numeracy and financial literacy of FDCs and identify their socio-economic determinants. A study on the financial literacy of the FDCs is significant from several perspectives.

Besides advancing our knowledge on the subject, an understanding of the (numeracy and) financial literacy levels of the FDCs would be of help to public policy.

Kumar (2002) emphasized that the shared economy of the FDCs—where goods and services relevant to their livelihoods such as food, clothes, and credit—are not valued in terms of market prices but based more on reciprocal trust and evolved norms. Until the beginning of the 20th century, geographical and cultural isolation of the FDCs from the mainstream society prevented the development of a monetized economy (Bandi, 2013; Davies & Bennett, 2007). As implied in Rangasami (1985), such isolation rendered the FDCs and the other low-income groups vulnerable to exploitation by vested elements of the mainstream society. Realizing this inadequacy, public policy has attempted to enable the disadvantaged population through functional and financial literacy programmes (Lusardi, 2012). In India too, financial inclusion has become important and the government has launched massive financial literacy programmes targeted specifically at the weaker sections and low-income groups. The Indian FDCs have been exposed to the joint forest management (JFM) programme since 1990. JFM and the connected financial aid have enabled the Indian FDCs to participate more actively in forest management and undertake community projects involving investment decisions. FDCs are also required to interact with forest officials and assess the costs and benefits in the short, medium, and long run of undertaking forestry investments. It is expected that these JFM activities provide some exposure to the FDCs in financial transactions, banking, and interpreting land records that may influence their numeracy and financial literacy. An understanding of the financial literacy levels of the FDCs may be useful for policymakers to offer customized literacy programmes and improve welfare, and reduce their exploitation from petty traders and local forest officials.

The article presents the findings on the numeracy and financial literacy of FDCs from the Indian state of Andhra Pradesh. Using data from a sample of FDCs drawn from two geographical regions with differing resource endowments in Andhra Pradesh, the study identifies some of the key socio-economic determinants of financial literacy.

The results show that a third of the members of the FDCs were able to answer the questions on probability and simple interest correctly. At least half of the sample had a clear idea on the time value of money and had less difficulty in computing when the mathematical questions were framed in the form of sentences which embedded situations from their daily lives. Participants, however, faced difficulty in recognizing mathematical symbols and performing simple computations in addition, subtraction, multiplication, and division. The average scores of the sample in the standard numeracy and financial literacy tests were 4.98 out of 12 points and 1.32 out of 5 points, respectively, indicative of low financial literacy in conventional terms. A comparison of FDCs drawn from two geographical regions with differing resource endowments in Andhra Pradesh identifies some socio-economic determinants of financial literacy. Education has a positive effect on numeracy and financial literacy. Household size has a negative effect on numeracy, with no effect on financial literacy after controlling for education. Members of FDCs with habitations close to towns are likely to be more numerate and financially literate.

The study calls for a deeper comprehension of financial literacy among the FDCs that addresses the nuances of participatory forest management. Rigorous public programmes for imparting financial literacy to the FDCs will not only make the JFM programme more successful but also provide employment avenues to the women in the FDCs. Financial literacy programmes would also enhance the outcome of the ongoing digital inclusion programmes undertaken by the government in forest agency areas.

The rest of this article is structured as follows. The review of literature presents an overview of the existing studies on the numeracy and financial literacy of the FDCs. The Indian FDCs are described in the next section. Methodology and results are discussed subsequently, followed by a discussion of the main findings. The study concludes with some managerial and policy implications.

REVIEW OF LITERATURE

There is limited literature available on the numeracy and financial literacy of FDCs. Given this limitation, this review examines the available literature on the numeracy and financial literacy levels of FDCs in the Indian context, and in different parts of the world.

Numeracy, defined as the ability to understand and process basic notions of numbers and chance events, aids decision-making in the real world over a wide range of health, financial, and social issues (Peters et al., 2006). Innumeracy afflicts both the educated and uneducated people and the inability to logically reason out chance events may lead to irrational decisions and inefficient public policies (Grey, 1991, pp. 68–69; Paulos, 1988).

Financial literacy, on the other hand, is defined as a set of numeracy skills necessary to make effective financial decisions. Empirical tests for financial literacy have been operationalized in two different ways. One view takes it to mean an understanding of basic financial concepts such as interest rates, inflation, and time value of money, while the other as the implied knowledge of financial products such as stocks, bonds, and mortgages (Hastings, Madrian, & Skimmyhorn, 2012). In either view, the causation from numeracy to financial literacy seems implicit. The definition of financial literacy thus can be parsed into three components: cognitive ability, analytical ability, and decision-making. The current research focuses more on the cognitive abilities of the Indian FDCs with reference to their numeracy and financial literacy.

Financial Literacy in the Indian Context

The present evidence points to severe financial exclusion among households across all income groups (R. Pal & Pal, 2012) as well as rural farmers in India (Gaurav & Singh, 2012). Half of the households in the country are unbanked, and 90 per cent of the villages are not served by a bank or its branch (Singh et al., 2014). However, the unbanked population does not seem to appreciate the need for a bank account and the economic benefits that flow from owning a bank account which include access to cheaper loans from the formal sector (Subbiah, 2014). The liberalization of the financial sector post-1991, which was pro-market in nature, has slowed down the pace of financial inclusion (Chakravarty & Pal, 2013). In general, financial knowledge among Indians is found to be quite low by international standards (Agarwalla et al., 2012).

Several countries, including India, have started financial education programmes to combat lack of financial literacy. However, evidence from American high school students in financial literacy tests suggests little correlation between financial education and performance (Mandell, 2008). A study of 1,200 households in Ahmedabad city in Gujarat, India, reports that financial education does not aid financial investment decisions which require mathematical calculations (Carpena, Cole, Shapiro, & Zia, 2011).

So while optimal stock of financial literacy of a person increases with income levels and returns to financial literacy, there is a trade-off involved. Acquiring any level of financial literacy requires time and money. Therefore, only those with higher incomes may be willing to spend resources to acquire financial education (Jappelli & Padula, 2011). Income does seem to positively impact financial literacy (Mandell, 2008).

Financial Literacy of FDCs

Our review of literature suggests that while there are limited studies which explicitly document the numeracy and financial literacy of FDCs, there are indirect evidences that exist.

With reference to numeracy, Kirby et al. (2002) reports moderate levels of numeracy among the Tsimane Amerindians, a horticultural and foraging society inhabiting the Bolivian forests. Similarly, McCall, and Minang (2005) report that the Tinto forest community, in learning to use the participatory geographical information system for promoting community-based natural resource management in the Cameroon, have learnt to interpret digital land records and quantitative information. In an ethnographic investigation, Canieso-Doronila (1996) reports that the tribal Filipinos, who gathered and sold rattan in bundles of 50 each in the market, used their fingers, palm, and claps to accurately count up to 1,000.

Financial literacy among FDCs seems to have developed through their interactions with the nearby towns. For example, Henrich and Mcelreath (2002) describe the economy of Mapuche and Huinca-traditional forest societies in Chile who live in a cash economy, pay for their services, and understand financial transactions, which indicates that members of these societies are reasonably financially literate. Similar evidence of numeracy and financial literacy due to market interactions have been noted in the Afar pastoral communities of Ethiopia (Davies & Bennett, 2007), traditional societies in Tanzania (D’Exelle, Campenhout, & Lecoutere, 2011), and the Dani forest community in Papua New Guinea (Diamond, 2012).

Evidence suggests that exposure to urbanization, technological advancement, proximity to urban areas, transactions in markets, and interventions for economic development that improve participatory management skills may have contributed towards numeracy and financial literacy of forest communities across the world. It can be assumed that forest communities may have acquired some numeracy and financial learning by observing the financial behaviour of townsfolk with whom they come in contact with as a result of urbanization (as in the case of traditional societies such as Mapuche, Huinca, and those from Tasmania) and participatory management (as with the Tinto).

The study examines the specific case of the Indian FDCs, their numeracy and financial literacy levels, and their determinants.

FOREST-DEPENDENT COMMUNITIES (FDCs) IN INDIA

The FDCs studied in the research include ‘forest dwelling Scheduled Tribes’ and ‘other forest dwellers’. 1

A forest dweller is a person who resides in and depends on the forests for their livelihood. According to the Scheduled Tribes and Other Traditional Forest Dwellers (Recognition of Forest Rights) Act, 2006, enacted by the Government of India, ‘forest dwelling Scheduled Tribes’ are people belonging to the Scheduled Tribes category who reside in and depend on forests for their livelihood activities. The ‘other forest dwellers’ are people who have resided in forests for at least three generations (a generation comprises 25 years) prior to 13 December 2005 and who depend on forests for their livelihood activities (Ministry of Law and Justice, Government of India, 2007).

The total forest cover in the country is 69.20 million hectares comprising 21 per cent of its geographic area which is 328.72 million hectares (Ministry of Environment and Forests, Government of India, 2011). Out of the total Scheduled Tribes population of 104.28 million, approximately 54 million reside in and around forests and depend on forests for their livelihood (Ministry of Tribal Affairs, Government of India, 2012).

The oldest and perhaps, the most isolated Scheduled Tribes group are the Andamanese hunter-gatherers who are believed to belong to the Negrito race and inhabit the forests of Andaman Islands since thousands of years ago (Kashyap et al., 2003). An account of the Indian forest dwellers is provided in Sundar (2014).

The British gave impetus to scientific forest management through the national forest policy, 1894, which laid emphasis on environmental stability through forest conservation. Post-Independence the government was concerned with forest depletion, and through the national forest policy, 1952, promoted forest expansion through farm and agroforestry. The continued depletion of forest cover and the inadequacy of the existing policing methods compelled the government to re-think its strategy to conserve forests. Accordingly, the Government of India formulated the national forest policy, 1988, which involved the local communities in forest conservation for the first time in the history of forest management in the country. This policy was made operational through the JFM programme in 1990 (Bandi, 2013).

JFM established a cooperative partnership between the FDCs and the state forest departments for rehabilitating degraded forest areas in the form of an agreement where the FDCs agree to protect the forests they inhabit from fire, grazing, and illicit timber removals. In return, the FDCs receive some rights over forest produce (such as fuel, fodder, and timber) and a share of penalty levied for forest offences. JFM has been instrumental in changing the socio-economic lives of Indian FDCs from being forest-centred to one based on money economy (Bandi, 2013). Sundar (2014) provides an account of the JFM programme and its status in Andhra Pradesh and the other states of India.

In Andhra Pradesh, 7,718 FDCs (called Vana Samrakshana Samithis [VSS] in the regional Telugu language) involving 1.4 million forest people are managing 1.52 million hectares of forest area. In terms of the JFM programme size, Andhra Pradesh stands sixth in the country (Bandi, 2013). Through the JFM programme, FDCs have been introduced to financial management. The current research documents the numeracy and financial literacy of FDCs in two geographically distinct forest regions of Andhra Pradesh.

METHODOLOGY AND DATA

The research draws samples from two geographically distinct forest regions in Andhra Pradesh with different social and economic orientation (the Rayalaseema and the coastal regions) to study the socio-economic determinants of numeracy and financial literacy of the FDCs. A priori, the members of VSS with higher household incomes, higher educational attainment, those working in forestry jobs under the JFM programme, and those who reside in relatively closer proximity to urban areas are expected to possess higher levels of numeracy and financial literacy. Women, unmarried adults, and those belonging to the Scheduled Tribes are expected to possess lower levels of numeracy and financial literacy.

The forests allotted to the VSS in Rayalaseema are mostly degraded due to hot weather conditions and inadequate rainfall. On the other hand, the forests assigned to the VSS from the coastal region contain fertile soils (due to the presence of Godavari and Krishna rivers) which support economically significant forest plantations.

With the assistance of the Andhra Pradesh Forest Department, the Government of Andhra Pradesh, VSS from two districts (Chittoor and Kadapa) in Rayalaseema and one district (Nellore) in the coastal region were identified. The VSS participants for the numeracy and financial literacy tests were recruited using the VSS records, and the assistance of the chairperson and the local forest officials. The local forest officials and the chairpersons of the VSS explained the purpose of the study in the local language to the members of the VSS. All the members of VSS present in these meetings showed enthusiasm to participate in the study, and the adult members of VSS were enrolled as participants.

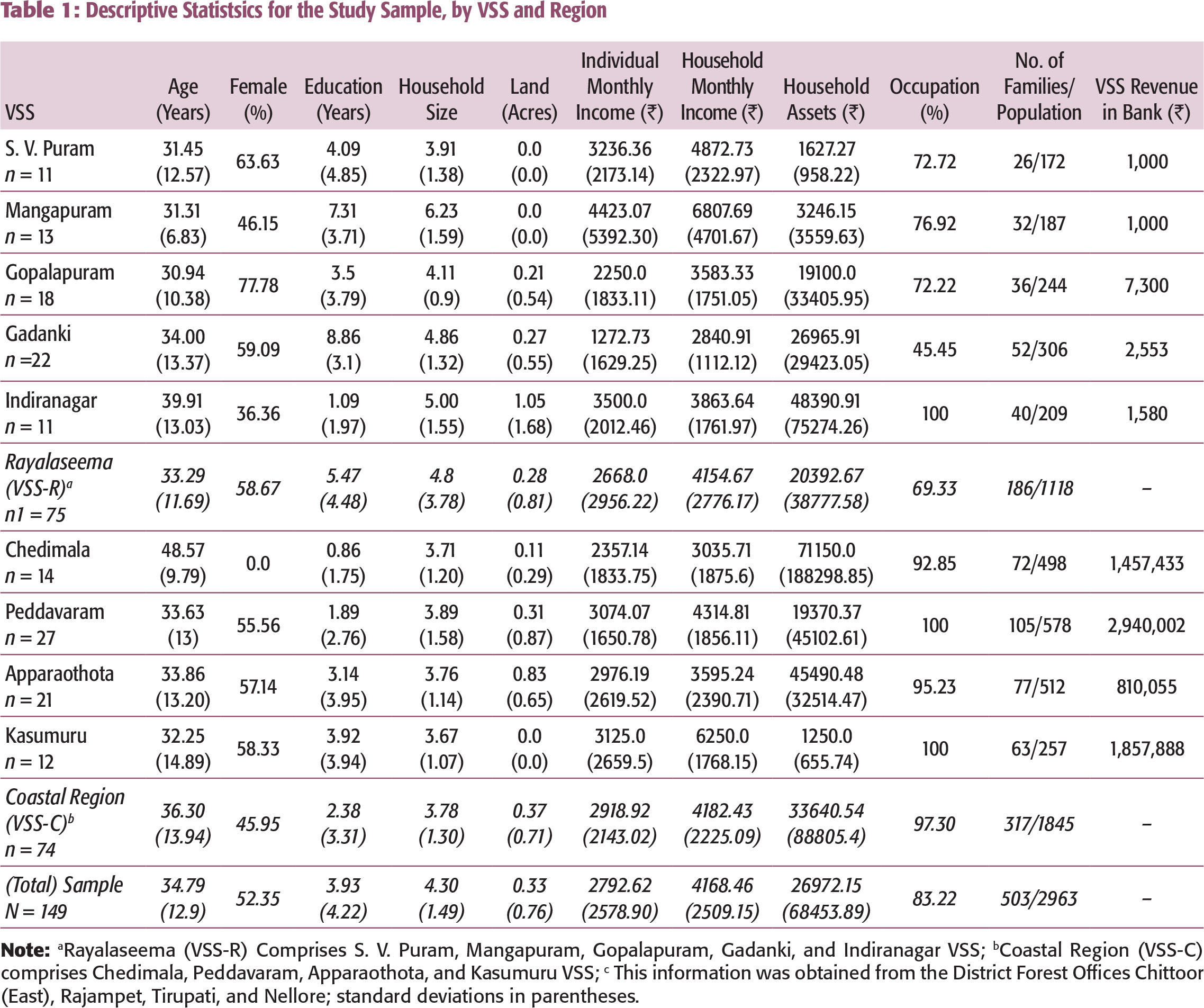

The fieldwork for data collection was done during the months of May and June 2013. A total of 149 VSS members participated in the study. Of these, 75 VSS members were from Rayalaseema, while 74 VSS members were from the coastal region. Hereafter, the Rayalaseema region is referred to as VSS-R and the coastal region as VSS-C.

Table 1 reports the descriptive statistics. On an average, the VSS participants were 35 years old and 52 per cent of the sample consisted of women. The participants were from households with an average size of four members. The average household income was ₹4,168 per month. The VSS participants had about 4 years of education. Approximately 43 per cent of the sample had zero years of schooling. About 83 per cent of the sample depended on the jobs under the JFM programme. The average landholding size was 0.33 acres. The average value of assets owned per household is ₹26,972.

: Descriptive Statistics for the Study Sample, by VSS and Region

FINDINGS

Numeracy

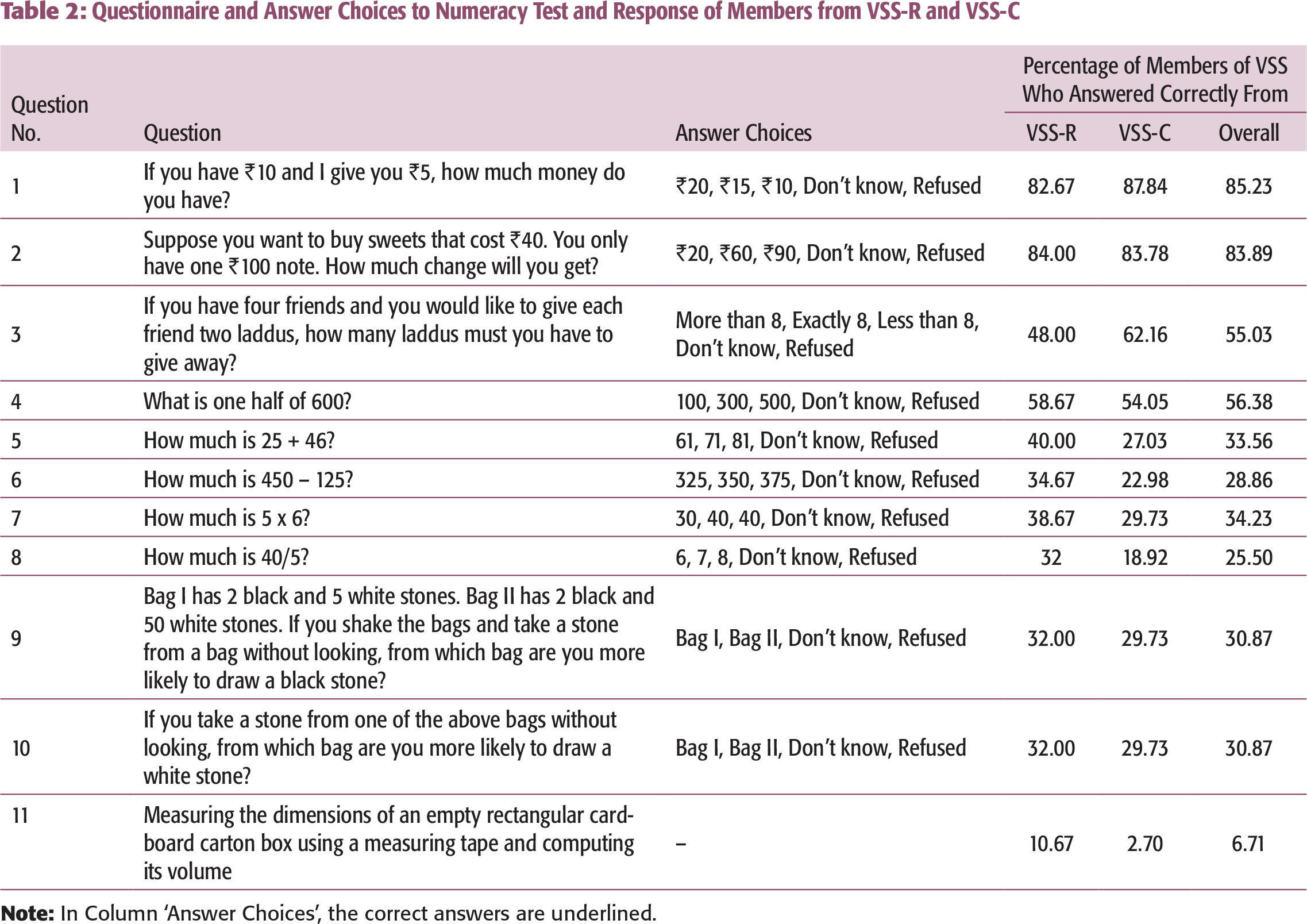

For eliciting numeracy, we use a simplified version of the standard questionnaire consisting of questions on addition, subtraction, multiplication, proportions, and probability which is suitable for samples with low educational attainment as demonstrated in Gaurav and Singh (2012). The standard questionnaire on basic math and probability adopted in the study was originally developed by Gaurav, Cole, and Tobacman (2011) to derive cognitive ability measures for estimating the impact of innovative financial education on the adoption of index-based rainfall insurance by farmers in Gujarat, India. The standard questionnaire used in Gaurav et al. (2011) emphasized more on debt literacy questions as these issues were more relevant to the Indian farmers. In comparison to farmers, the borrowing liabilities of Indian FDCs were lower as ascertained during the interviews. Accordingly, the standard questionnaire was simplified by omitting several complicated questions on debt literacy.

Further, scholars have designed questionnaires to estimate numeracy of population in the developed economies (Paulos, 1988; Peters et al., 2006), but these instruments may not be appropriate in the present study on Indian FDCs due to the low educational attainment in the sample.

: Questionnaire and Answer Choices to Numeracy Test and Response of Members from VSS-R and VSS-C

Table 2 presents the questions used for numeracy and the response rate of VSS members from the two regions. Members from both regions had less difficulty in computing when the mathematical questions were framed in the form of sentences which embedded situations from their daily lives as in questions 1–4. There were small variations in the performance between VSS-R and VSS-C.

The VSS members from both regions, however, faced difficulty in recognizing mathematical symbols and performing simple computations in addition, subtraction, multiplication, and division in questions 5–8. The members from VSS-R showed competency in recognizing mathematical symbols and scored higher in questions 5–8 compared to their counterparts from VSS-C (which is interesting as the former belong to the low-income VSS).

Only 30.87 per cent of the sample in the study could correctly answer questions 9 and 10 on probability and chance events. Further, 6.71 per cent of the sample was able to measure the dimensions of the carton box and correctly compute its volume. Only 4 per cent of the sample could answer all the 12 questions correctly.

Financial Literacy

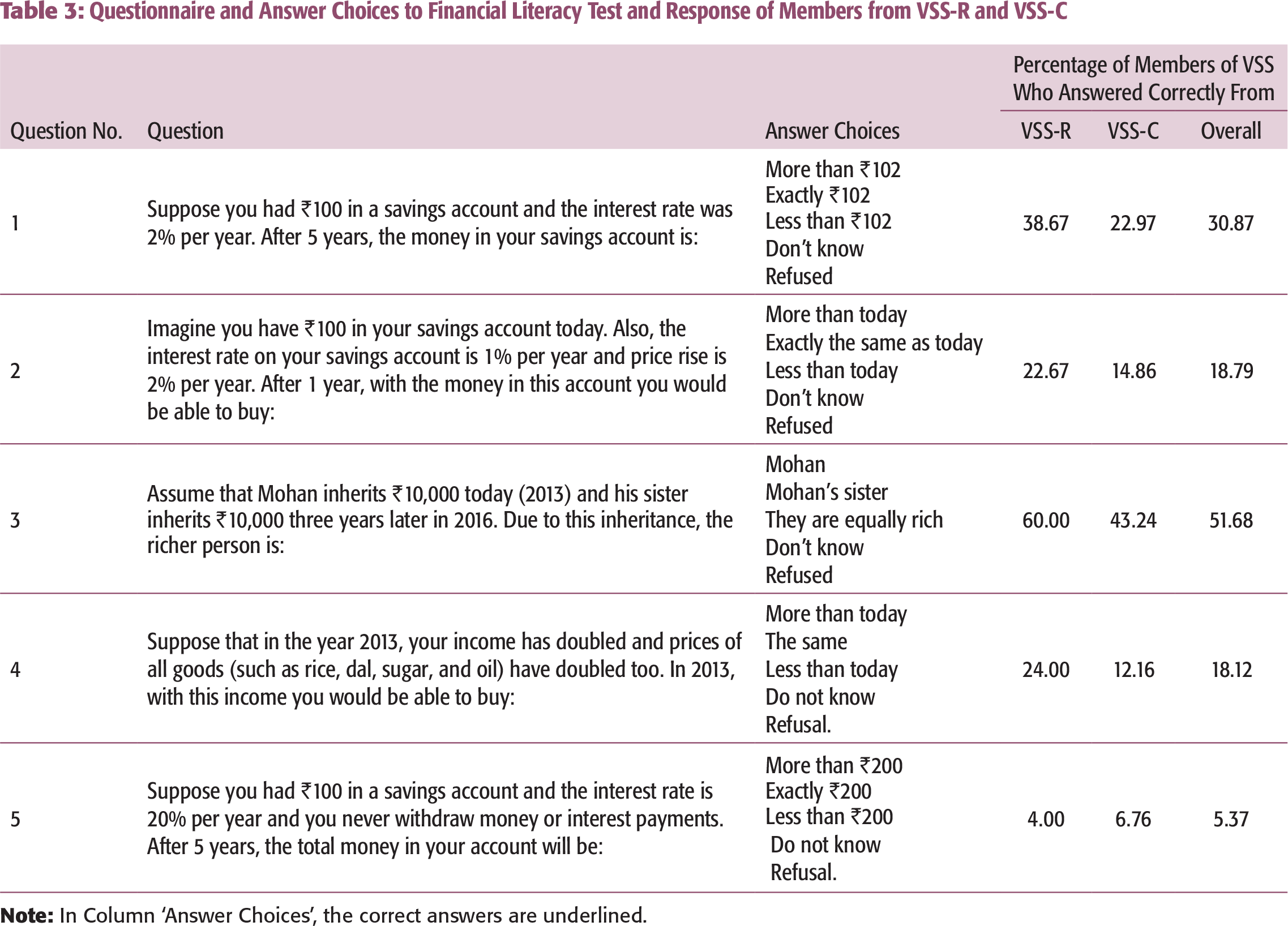

: Questionnaire and Answer Choices to Financial Literacy Test and Response of Members from VSS-R and VSS-C

As with numeracy, this questionnaire was phrased in the vernacular and read out aloud for those participants who could not read. A correct answer to each question was awarded one point. Wrong answers were awarded a zero. The maximum attainable score was five points.

Table 3 presents the questions used for financial literacy and the response rate of VSS members from the two regions. Only 30.87 per cent of the sample was able to correctly answer question 1 on simple interest (compared to 90.8% for Netherlands where the original questionnaire was administered; Van Rooij, Alessie, & Lusardi, 2011).

Similarly, only 18.79 per cent of the sample in the present study was able to correctly answer question 2 on inflation and roughly half the sample responded correctly to question 3 on time value of money (as compared to reported 26.8% and 90% for rural farmers in Gujarat, the only comparable recorded evidence available from India described in Gaurav and Singh, 2012).

It was observed during the administration of tests that several members of the VSS in the sample guessed the answer to question 4 on money illusion with no attempt being made to logically reason out the solution. This was ascertained as part of interviews with the participants after the test was over. Only 5.37 per cent of the sample could correctly answer question 5 on compounding.

Determinants of Numeracy and Financial Literacy

We use ordered response models to identify the socio-economic determinants of numeracy and financial literacy.

The test scores achieved by the N members of the VSS in the numeracy and financial literacy tests in the present study can be classified into J achievement levels. These achievement levels can be taken as an ordered dependent variable, and using an array of relevant individual, household, and institutional socio-economic variables as independent variables, we employ ordinal logistic regression (Cameron & Trivedi, 2005). The model specification is as follows:

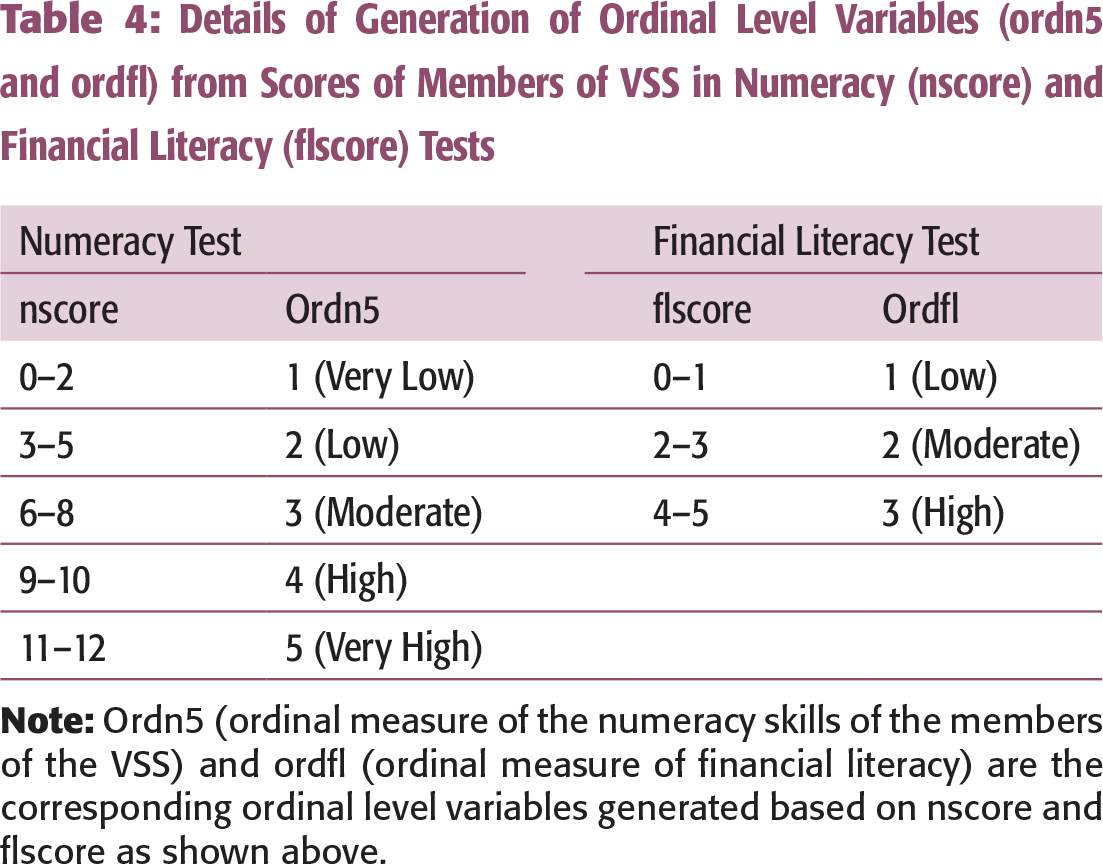

Table 4 shows the details of the construction of the dependent ordinal variables from the scores achieved by the members of the VSS in the numeracy and financial literacy tests. The observed levels of achievement by the members of the VSS in the numeracy test are yi = 1 (very low), yi = 2 (low), yi = 3 (moderate), yi = 4 (high), and yi = 5 (very high). Similarly, the observed levels of achievement by the members of the VSS in the financial literacy test are yi = 1 (low), yi = 2 (moderate), and yi = 3 (high).

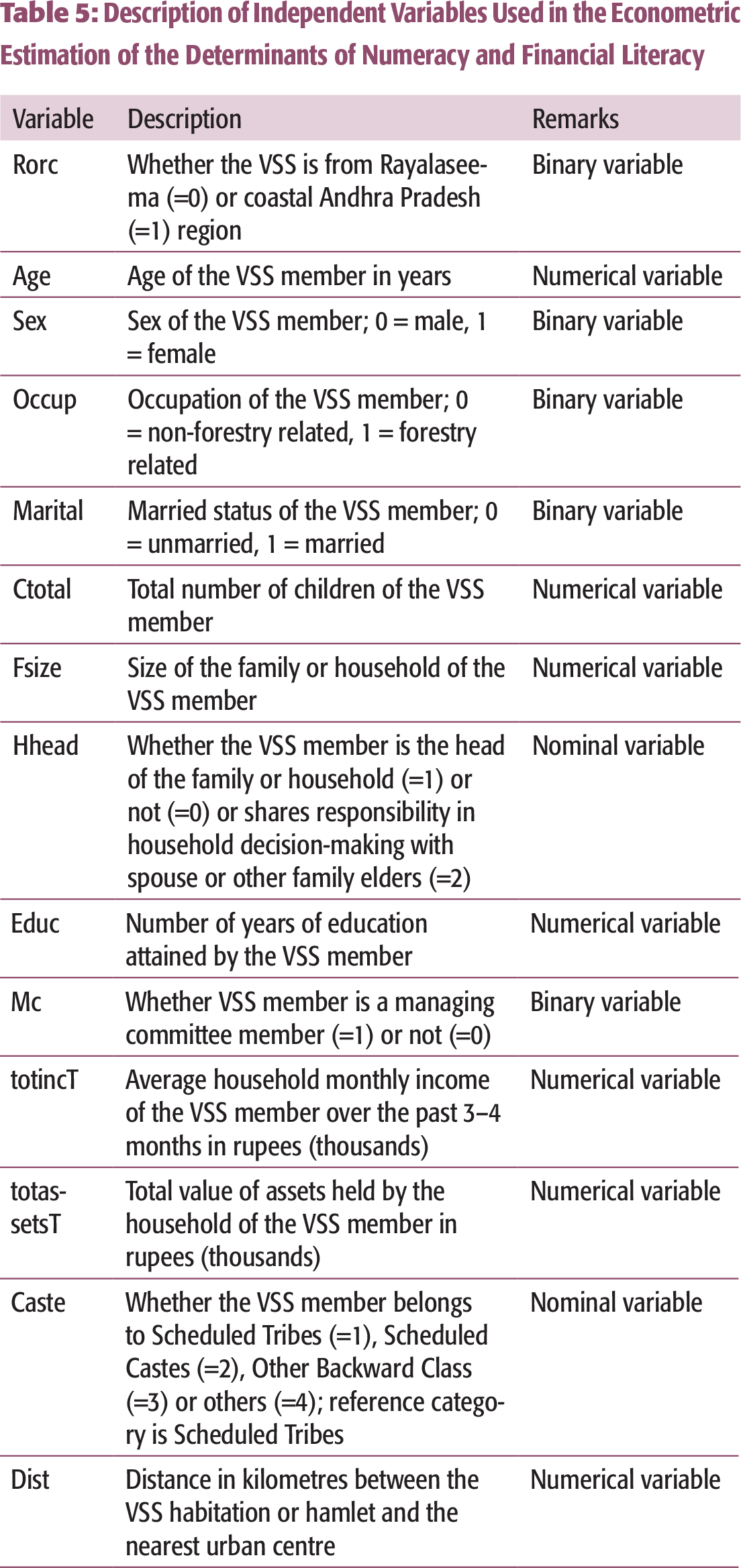

Table 5 provides details of the independent variables used in the regression model. The dependent variables in the above regressions are the log odds ratio of ordn5 and ordfl for numeracy and financial literacy.

A priori, it is expected that household income of members of VSS show a positive association with their numeracy and financial literacy as members of VSS with higher incomes are more likely to be exposed to cash transactions. Empirical evidence indicates that this is likely to be so (Lusardi, 2012; Lusardi & Tuffano, 2009).

Tables 2 and 3 revealed that, numerically, the mean scores of members of VSS-R were higher in the numeracy and financial literacy tests than those from VSS-C. There is no theoretical grounding for the observation. To control for this, the binary variable (rorc) was included.

Young adults, men and persons with higher educational attainment possess higher numeracy and financial literacy as compared to the aged, women, and persons with lower educational attainment (Lusardi, 2012). The variables Age, Sex, and Educ (education) have been included to control for these.

Members of VSS who earn incomes from forestry jobs are expected to have higher numeracy and financial literacy than those from non-forestry jobs since forestry-related jobs increase exposure of the VSS members to JFM activities. Hence, Mc (whether member of managing committee or not) and Occup (occupation dummy variable) have been included in the model.

: Details of Generation of Ordinal Level Variables (ordn5 and ordfl) from Scores of Members of VSS in Numeracy (nscore) and Financial Literacy (flscore) Tests

: Description of Independent Variables Used in the Econometric Estimation of the Determinants of Numeracy and Financial Literacy

Members of VSS with higher number of children (Ctotal) and bigger family sizes (Fsize) may not have the resources to acquire skills in financial literacy. On the other hand, heads of VSS households (Hhead) would be expected to be more numerate and financially literate due to their higher responsibilities.

Scheduled Tribes (caste) are expected to be less financially literate as they face social exclusion (Lusardi, 2012).

Finally, members of VSS that are nearer to towns (Dist) are expected to be more numerate and financially literate as they may be influenced by contact (Friedman, 1953).

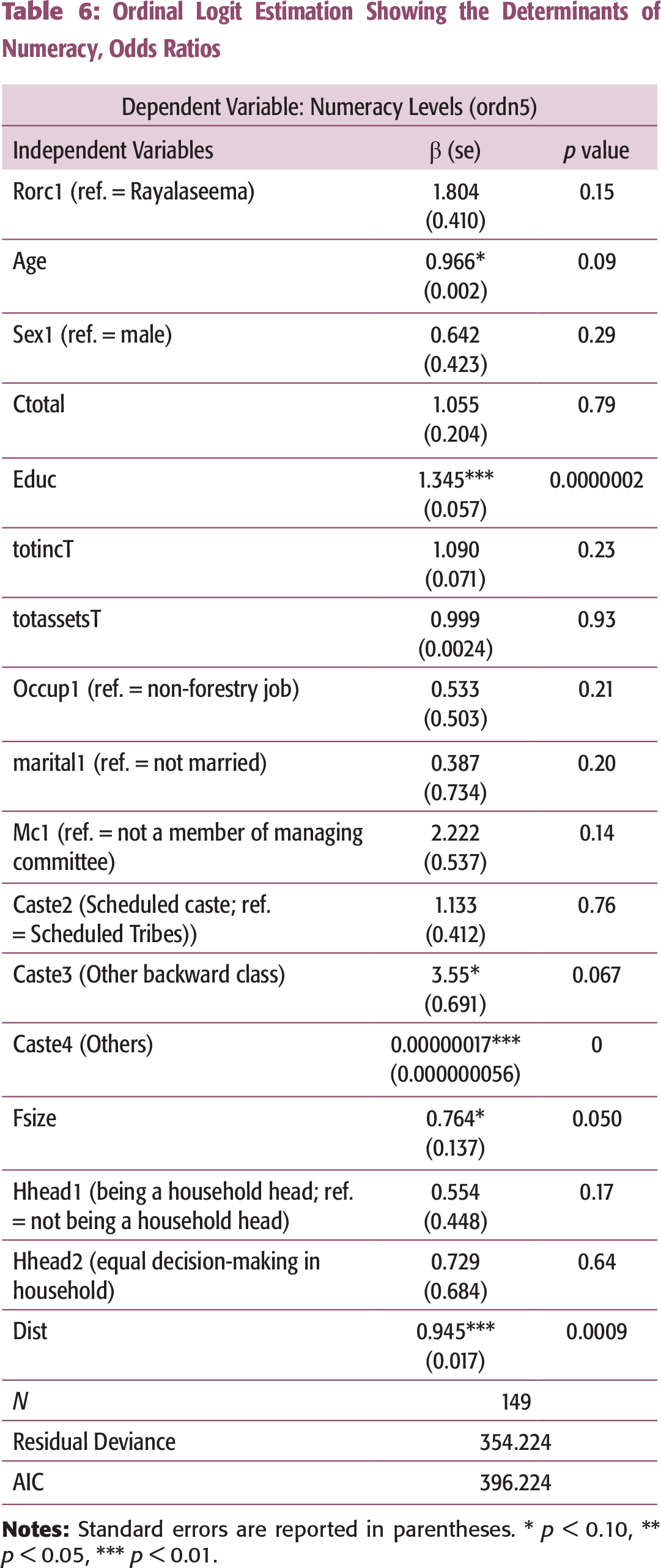

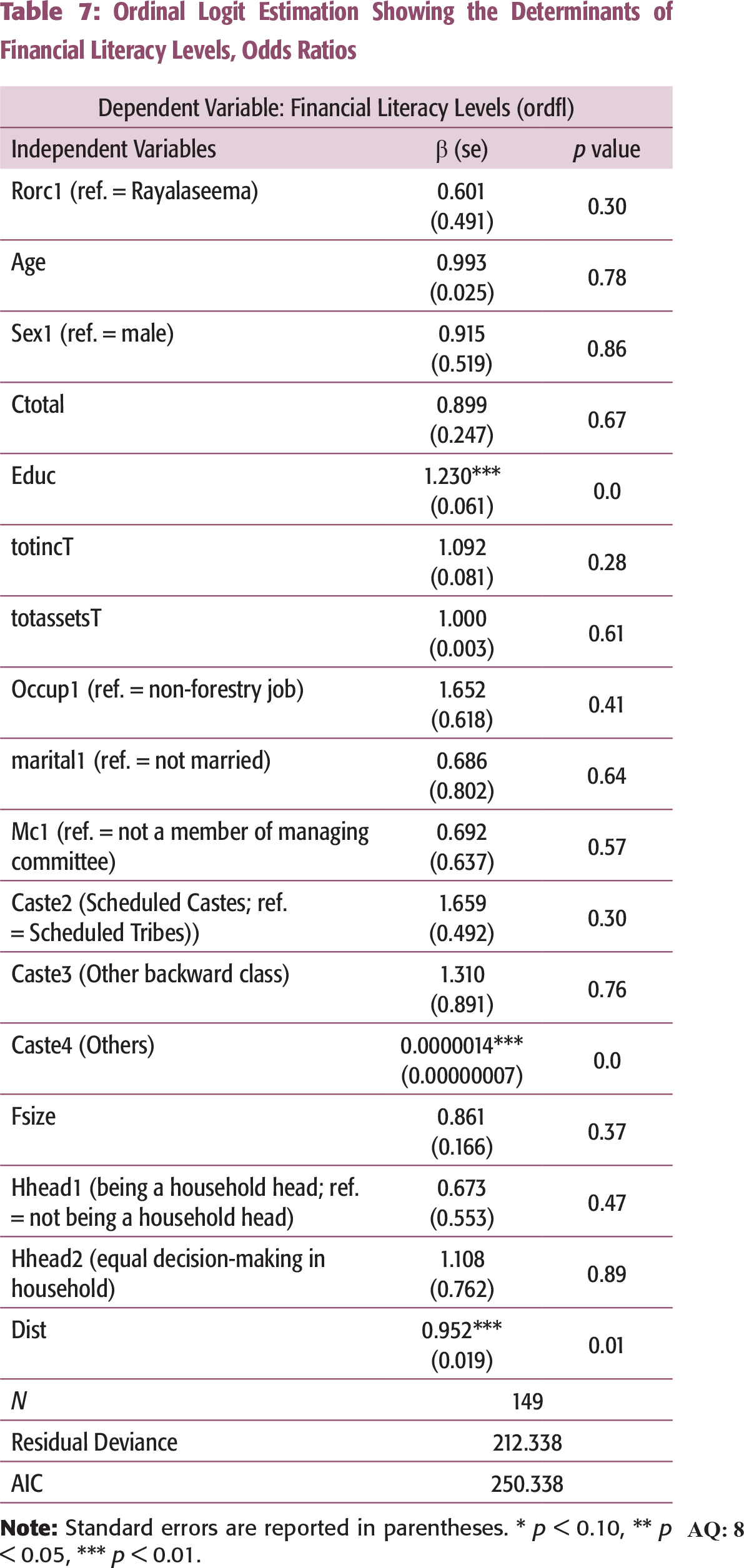

Tables 6 and 7 present the odd ratios of ordn5 (ordinal measure of the numeracy skills of the members of the VSS) and ordfl (ordinal measure of financial literacy) respectively.

An increase in one year of educational attainment of a member of a VSS increases the odds of attaining any level of numerical ability and financial literacy by 34.52 per cent and 23 per cent, respectively (similar results have been reported by Jappelli & Padula, 2011; Gaurav & Singh, 2012; Lusardi, 2012; Lusardi & Mitchell, 2007; Van Rooij, Lusardi, & Alessie, 2011).

: Ordinal Logit Estimation Showing the Determinants of Numeracy, Odds Ratios

: Ordinal Logit Estimation Showing the Determinants of Financial Literacy Levels, Odds Ratios

Note that this is different from the finding from the sample of rural farmers of Gujarat (Gaurav & Singh, 2012), but this could be because the average levels of educational attainment of members in FDCs is much lower (less than 4 years of schooling) than those of the Gujarati farmers (almost 9 years of schooling, which may permit larger positive externalities of education).

Finally, for every increase in one km distance between the VSS hamlet and the town, the odds of attaining any level of numerical ability and financial literacy by a member belonging to that VSS reduces by 5.5% and 4.8% respectively. This could be because members of VSS may visit towns for purposes of trade, entertainment, and to interact with forest officials on JFM activities.

An important assumption underlying the ordinal logistic regression used in the study is the ‘proportional odds’ assumption (Agresti, 2007). For both the numeracy and financial literacy regressions, the proportional odds assumption holds moderately.

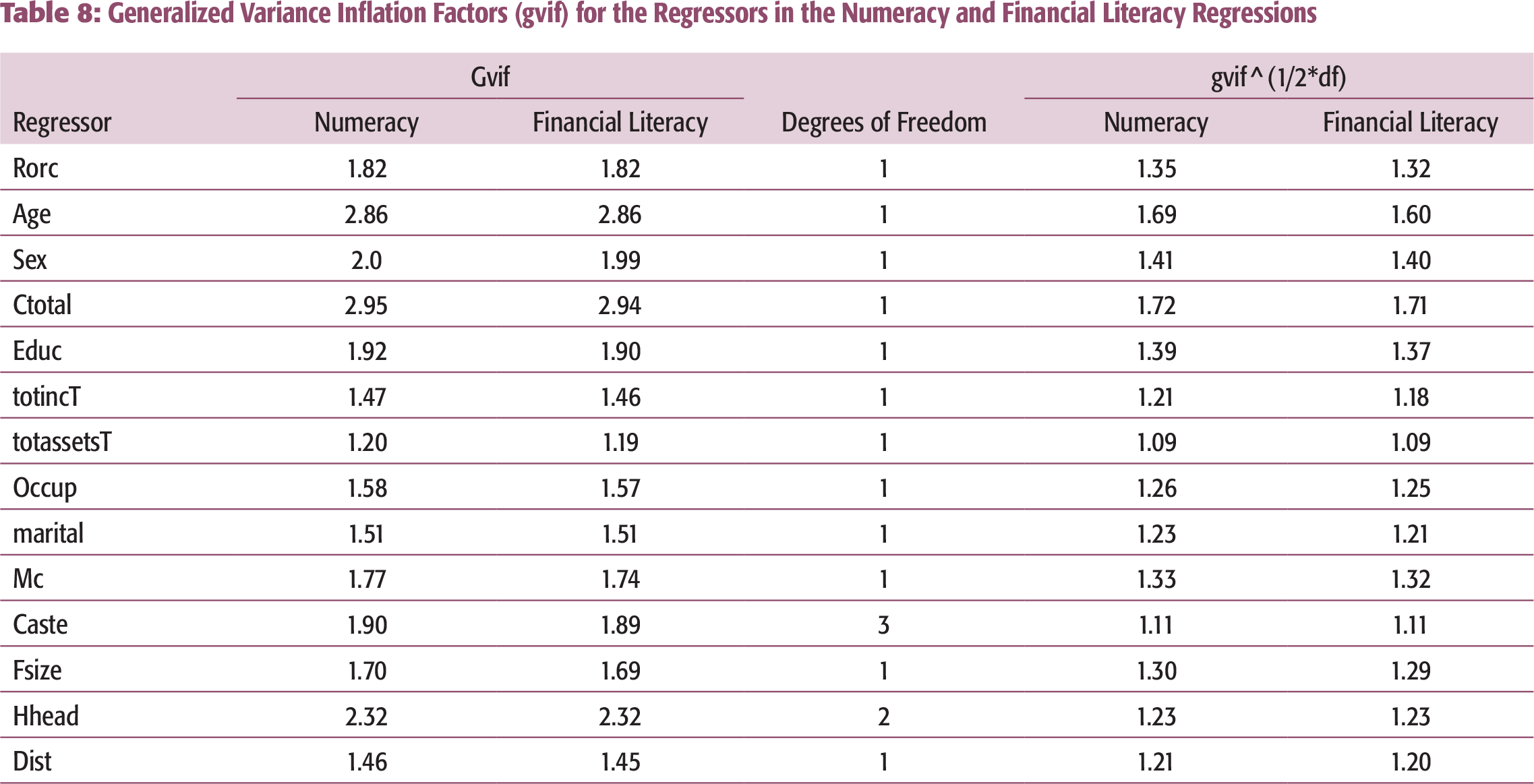

Generalized variance inflation factor (gvif) were computed for the regressors as a test for multicollinearity for both the regressions. The gvif (corrected for degrees of freedom) is less than 2 for the regressors indicating that multicollinearity is not an issue.

From the Shapiro–Wilk test (W = 0.99; p value = 0.91), we fail to reject the null that the residuals are normally distributed at α = 0.05 for the numeracy regression. For the financial literacy regression (W = 0.93; p value = 0.00001), we reject the null, but the model is robust to deviations from the normality assumption (Kerns, 2010).

From the Breusch–Pagan test for testing homoskedasticity (BP = 21.49; df = 17; p value = 0.21 for the numeracy regression; BP = 15.31; df = 17; p value = 0.57 for the financial literacy regression), we fail to reject the null that the variance is the same for all residuals at α = 0.05.

A look at the Pearson’s correlation coefficient suggests a moderate correlation (of 67.8%) between the numeracy test score and the financial literacy test score of VSS members. An ordinal logistic model with scores from financial literacy as the dependent variable and scores from numeracy as independent dummy variables showed that higher numeracy of members of VSS is associated with higher financial literacy (details available on request).

DISCUSSION OF FINDINGS

: Generalized Variance Inflation Factors (gvif) for the Regressors in the Numeracy and Financial Literacy Regressions

The study sample in Rayalaseema scored numerically higher in both tests than those from the coastal region. Also, educational attainment contributes to numeracy and financial literacy. This hints at a comparatively higher educational attainment of the sample from Rayalaseema which is reflected in the sample: The sample from Rayalaseema had an average of 5.47 years of schooling, while those from the coastal region had about 2.38 years. This may be an artefact of the small sample size.

However, this suggests that the sample from Rayalaseema may attach more importance to acquiring education. In support of the above inference, Chittoor district from Rayalaseema (four VSS of the study) has a literacy rate of 72.36 per cent, while Nellore district from the coastal region (five VSS of the study) has 69.15 per cent (Government of Andhra Pradesh, 2012).

The review of literature suggests that income positively impacts financial literacy (Mandell, 2008), but the results of the current study do not fully support the evidence from the literature (the beta coefficient on the income variable has the expected sign, but is statistically insignificant; see Table 7). One possible explanation could be that participatory forest management and interaction with markets in urban areas, mediated by the JFM programme, may have enabled higher (numeracy and) financial literacy levels in the Indian FDCs. The processes through which participatory forest management mask the impact of higher incomes of Indian FDCs on their financial literacy levels is not fully clear as the existing literature does not shed light, and could be an area of future research.

The questions designed in the study to assess numeracy are a subset of the standard questionnaire used in the literature, and hence the present results may not be directly comparable to the results derived from standard numeracy tests. Also, limitations noted regarding the use of standardized questions designed for financial literacy apply to the current study too (Van Rooij, Lusardi, & Alessie, 2012). Finally, the selective sampling adopted in the study may not allow generalization.

CONCLUSIONS AND IMPLICATIONS FOR PUBLIC POLICY

The study, besides being a contribution to the numeracy literature of the FDCs in the Indian state of Andhra Pradesh, describes how standardized tests for measuring numeracy and financial literacy could be customized for low-income and low-educational groups, and their determinants identified in the emerging economies’ context. The sample studied show some exposure to the notions of simple interest and the time value of money, but faced difficulty in recognizing mathematical symbols and performing simple computations in addition, subtraction, multiplication, and division, as compared to answering similar mathematical questions framed in embedded situations from their daily lives. With reference to socio-economic determinants, education and proximity to towns seemed to have a positive effect on numeracy and financial literacy, while household size has a negative effect on numeracy, with no effect on financial literacy.

Review of evidence on numeracy and financial literacy worldwide suggests that FDCs have acquired some degree financial literacy through their interactions with the outside world. The current study too indicates that the Indian FDCs have some exposure to financial transactions due to the JFM programme, increased interactions with public officials of the forest department, and proximity to towns. All the interactions have led to moderate levels of numeracy and financial literacy. This finding has several implications for public policy.

First, this financial learning may enable the FDCs to more effectively utilize their resource endowments. In indirect support of this inference, Chakrabarti, Datta, Howe, and Nugent (2005) reports that forests and environmental resources in India have been more efficiently managed by FDCs through JFM than by the government using indicators such as resource extraction levels and distribution of benefits. However, much more needs to be done on the financial literacy, as the forest department records show that several VSS or forest communities in Andhra Pradesh collapsed after funding (from multilateral banking institutions) stopped due to the closure of the JFM project between 2012 and 2014. As of 2014, about 2,500 VSS or forest communities (down from 7,718 in 2005) were actively functioning in Andhra Pradesh, but were supported through funding from other sources. While several other reasons such as political interference, lack of interest among stakeholders, and inhospitable geographical terrain are attributable to the partial failure of the JFM programme, lack of functional and financial literacy of the FDCs also led to leakages and prevented the FDCs from reaping benefits from the JFM programme. While one of the principal aims of the JFM programme was to enable local self-governance of the FDCs, in many instances, the JFM programme dwindled into a wage employment programme, with vested elements benefiting from leakages and ignorance of the FDCs. Public policy needs to focus on sustained literacy programmes on the functional, and the financial, fronts, which would go a long way in rekindling the aspirations of local self-governance among the FDCs.

Second, financial inclusion 2

Financial inclusion refers to universal access to financial services (banking, insurance, credit, and equity) at a reasonable cost; see Planning Commission (2009) ‘Report on Financial Sector Reforms’.

Third, evidence shows that women in marginalized communities have lesser entitlements compared to men, due to the lack of access to employment and income. Hence, women in marginalized communities are more burdened with housework; receive less compensation, seeds, and land; have less decision-making power; and are vulnerable to abuse by spouses (Kerr, 2005). Financial literacy may provide women in FDCs with more employment avenues and improve their social status.

Finally, the Reserve Bank of India has focused on improving financial literacy of poor households to achieve financial inclusion (Joshi, 2013). The thrust given by the central bank may help microfinance evolve as a tool to provide savings, credit, and insurance to the marginalized communities, including the FDCs. The results of this study could significantly contribute to the development of a suitable financial literacy programme by the microfinance institutions.

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.