Abstract

India is an agriculture-based developing country where financial technology and financial literacy play a crucial role in financial inclusion, poverty reduction, and rural development that cannot be avoided. This study examines the impact of financial inclusion on rural economic development through post offices, India Post Payments Banks, and regional rural banks. A total of 800 responses are collected initially through offline surveys and interviews using a structured questionnaire of rural youth from eastern Uttar Pradesh, and 650 viable responses are taken after eliminating incomplete, multivariate, and too consistent responses. This study employed PLS-SEM 4.0 for statistical analysis. The results show that financial inclusion positively affects rural economic development through these banks. The policymakers and stakeholders can use these findings, and they can also provide information through the campaigns about financial technology platforms and services that are available for rural people so that they can easily adopt technology and services.

Introduction

This study investigates the impact of financial inclusion (FI) on rural economic development (RED) through post offices, India Post Payments Bank (IPPB), and regional rural banks (RRBs). In Uttar Pradesh, India Post operates 15,420 branch post offices (India Post, 2024), complemented by 73 IPPB banking outlets staffed by IPPB personnel and an additional 16,014 banking access points (India Post Payments Bank, 2023). The RRBs in the state further strengthen FI with significant networks: Aryavart Bank, also known as Gramin Bank of Aryavart, operates 1,367 branches 1 Baroda Uttar Pradesh Gramin Bank, created through the merger of Kashi Gomti Samyut Gramin Bank and Purvanchal Bank, has 20,151 branches, 2 and Prathama U.P. Gramin Bank maintains 960 branches (Prathama U.P. Gramin Bank. 3 These institutions are essential for providing financial services and supporting fintech adoption in rural regions of Uttar Pradesh.

Improving RED is key to building resilience, thriving communities, and reducing poverty (Tim et al., 2021). Developing the economy in rural areas requires a detailed and customized strategy to address various challenges and opportunities. This implies that policymakers and development experts could prioritize these issues by devising tailored strategies to ensure fair and long-lasting development in rural regions (Nwokolo et al., 2024).

However, overcoming these resource and infrastructure constraints necessitates recognizing this new trend of preference among the youth not to be employed in traditional farming jobs but rather to enter multinational companies (MNCs). Even though MNCs ensure a good standard of living, it is pertinent to point out that the rural economy has traditionally contributed 25%–30% of GDP (Borsari & Kunnas, 2020). An increased trend of corporate employment negatively impacts the economy in rural areas, thus resulting in financial inequality that negatively impacts GDP (Zhang, 2023). Hence, to create a balanced economic environment favorable to national success, the focus must be redirected toward developing a solid cadre of indigenous farmers, craftspeople, etc., in addition to supporting the expansion of MNCs (Omeje, 2021).

The exacerbation of financial inequality due to burgeoning population levels underscores the imperative for fostering equal opportunities among citizens, pivotal for national development (Yuanchun et al., 2024). Central to this endeavor is the fulfillment of basic needs, a prerequisite for the equitable distribution of opportunities (Kuhn et al., 2024). However, providing financial services to millions poses formidable challenges, compounded by affordability constraints (Amit & Kafy, 2024). Consequently, governments must devise strategies to ensure the affordability and accessibility of financial services, thereby empowering citizens. According to Alazmi and Alazmi (2023), significant disparities prevent achieving integrated economic development. To attain these ends, it will be pertinent to institutionalize procedures for applying technology to assist national development with factors working toward FI.

Despite India’s impressive growth trajectory and government initiatives, a significant portion of the population is still marginalized from the country’s development narrative, resulting in exclusion (Khan et al., 2020). Moreover, the situation is compounded by the absence of business correspondents and satellite branches, as well as challenges with mobile banking (Mhlanga, 2023). The exclusionary dynamics within the financial system are also significantly influenced by social factors such as a lack of knowledge, communication barriers, and unfavorable attitudes from bank employees.

According to Ozili (2021), FI is an imperative approach that has to be put in place to address exclusionary dynamics. It thus calls for a cooperative approach with government agencies, banks, development organizations, and communities. According to Osabutey and Jackson (2024), successful implementation of FI programs will enhance the quality of life, reduce poverty, and support the more holistic development of the economy in rural areas 2024. This plan’s core is expanding the financial network to supply easy access to financial services for the entire population to drive efforts to reduce poverty and progress development. The Indian government has made various moves to achieve FI by implementing post office banks (POBs), IPPBs, and RRBs to offer banking services in all areas of the country.

Financial inclusion is a crucial strategy in response to these exclusive dynamics (Ozili, 2021). A cooperative strategy is required, including government bodies, financial institutions, development entities, and local communities. Successful implementation of FI programs can improve the quality of life, reduce poverty rates, and promote more diverse economic development in rural areas (Osabutey & Jackson, 2024). At the core of this strategy is the enlargement of the financial network to guarantee the smooth availability of financial services to all people, thus driving poverty reduction initiatives and promoting developmental goals. In India, the government has introduced different measures to promote FI, such as setting up POBs, IPPBs, and RRBs to provide financial services to remote regions.

According to Alhammadi (2023), enhancing access to financial services among the low-income populations will be an essential driver of economic growth. It has been established that offering relatively affordable financial services or FI is an essential method of increasing access to finance. The government measures were required to make financial services more accessible and, of course, free. During the past years, increasing usage of digital technologies and mobile phones has enhanced the public knowledge and inspection of various aspects of life, which includes financial concerns (Ashta & Herrmann, 2021).

The finance sector does not exclude the globe from this technological integration phenomenon as it increases dependence on online platforms and services daily (Suryono et al., 2020). The utilization of UPI has changed the style of financial activities since managing our finances has become pretty easy (Bhat & Singh Chauhan, 2024). Mobile applications have now become an important facilitator in conducting financial activities without much hassle. Consequently, investment has increased more sharply, and there is a changing trend in the investment trend. For example, scholars have researched over time on how the face of asset management strategies is changing, like Daugaard (2020). Such research reflects the dynamic nature of financial practices, which are largely influenced by the impact of technological progress and changes in consumer demand.

This study introduces a new angle in research on RED to examine the role of FI through channels that are much less used, namely, post offices, IPPBs, and RRBs. It centers its focus on the region of eastern Uttar Pradesh, while addressing an important research gap within the existing literature on the effects such financial structures have on younger populations in the rural world.

This study utilizes variables that have never been applied in previous research studies: post office, IPPBs, and RRBs (Kandpal, 2024; Kumar & Ahuja, 2024). Employing PLS-SEM 4.0 using the partial least-squares structural equation modeling approach offers an advanced statistical approach to depict the complex relationships of FI. This makes findings robust and insightful. This methodological approach enhances the rigor of the study and contributes a valuable, data-driven analysis of the impact of FI on rural youth, ultimately supporting targeted policy recommendations for FI strategies (Joshi & Tamta, 2023; Singh, 2024).

Research indicates limited information on the interconnectivity between financial literacy (FL), digitalization, and RED in India. Although the impact of FI on rural economies is acknowledged in contemporary literature, limited attention is paid to the significance of digital literacy (DL) and its impact on inclusive growth. This study bridges the gap by assessing the understanding and usage of rural communities concerning digital financial services. This will measure opinion within the public sphere relating to government programs while judging how well the current efforts promote FI. A survey-based study has been applied in uncovering the status of DL and financial access among the people residing in rural areas. From this approach, an understanding of the effectiveness and outreach of available programs could be analyzed from the citizen’s viewpoint to develop newer and improved policy ideas. The study concludes by discussing the interconnections between digital inclusion, FL, and RED and provides recommendations for improving economic empowerment in disadvantaged areas.

Literature in the specific area indicates an unmet need for integrated research related to the interaction between FL and the digitalization of economic conditions in rural regions in India. Even earlier studies related to literature that establish various impacts of FI across rural economies and economic perspectives are less engaged in discussing DL and its potential outcomes or implications for achieving an economically inclusive growth paradigm. Hence, this study addresses that requirement by examining digital finance’s awareness and availability across Indian rural areas. It seeks to gauge public perception regarding government initiatives and assess the effectiveness of current measures in extending FI. The study intends to unveil the DL landscape and the extent of rural access to financial services through a survey-based approach. Exploring the ordinary citizen’s perspective aims to shed light on the efficacy and reach of existing schemes, thereby facilitating policy refinement and innovation. Ultimately, the study explores the correlation between digital inclusion, FL, and RED, offering insights for enhancing economic empowerment in underserved communities.

The article is divided into sections for a systematic representation of the issue. The following section is theoretical background, proving that the relationship we are trying to establish is possible. This is followed by a literature review that examines the interdependence of FI and RED, FL and FI, and FI and DL. The third section is about the data and method used in this article. Finally, we have the article’s result, discussion, and conclusion.

Theoretical Background

The study focuses on the connection of all of the presented factors. Besides the studies, we have separate theories that indicate the relation of some of the factors. Financial services such as investment, credits, and savings boost the financial system. Finance–growth nexus theory as described in Bagehot (1873) holds that easy access to financial services and products positively affects economic growth (Marwa & Zhanje, 2015). It is further emphasized that a sound financial system drives investment, entrepreneurship, and productivity toward economic development. In short, financial development leads to economic development. The financial development theory (Durusu et al., 2017) supposes that FI is intertwined with economic growth through financial development. With better inclusiveness, efficiency, and sophistication, financial systems can offer better resource allocation, risk management, allowance for innovation, and technological improvements, and, as a finality, faster economic growth can be achieved, according to Li and Li (2022). Economic development works equally well for everyone in the society. Therefore, the theory of inclusive growth argues that FI is integral to reducing income inequality, poverty, and social exclusion. The inclusive growth hypothesis postulates that FI is what has to be done to eradicate economic disparity, poverty, and social exclusion. Both options argued for inclusive growth by ensuring access to financial services among underprivileged and underserved communities, which was the key to long-term economic development (Park & Mercado, 2015).

Review of Literature

Before the discussion of the role of FI in facilitating RED through FL and DL, there is a critical need to understand the nexus of FI, FL, and DL toward achieving the aim of this research, which will light on how FI affects RED through post offices, IPPB, and RRBs. This section discusses such linkages and how they influence FI through FL and DL. This includes five subsections and ties back to the relationship regarding FI and financial and digital literacies, financial technology, and development in rural areas.

Financial Inclusion and Financial Literacy

It is expected that people who are more financially literate would utilize and comprehend a greater variety of financial services, such as banking, savings, credit, and insurance (Grohmann, 2018). By improving FI, an understanding of these results in greater accessibility and service consumption. Efforts have been made to increase awareness about the need for financial services and how to obtain them (Chen et al., 2023). The attempts also enhance financial inclusivity by making individuals more informed about their options. It is important to understand that while financial education can enhance FI, it is not a cure-all (Cassimon et al., 2022). Financial literacy education must be combined with action on these larger issues for FI to be successful.

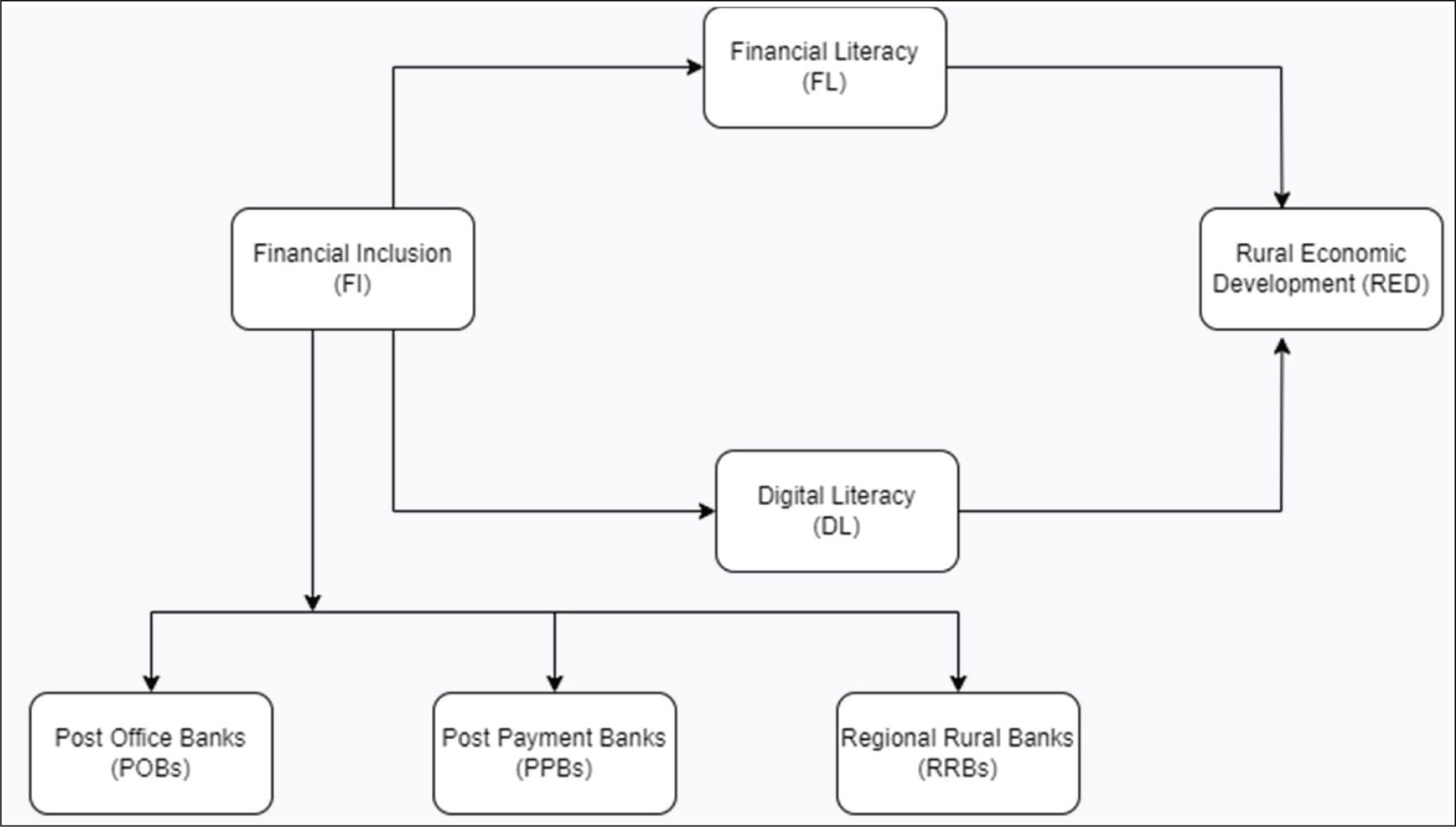

Post office banks have enhanced FL among the underbanked and rural communities. According to research on IPPB, this model will bridge the gap in access through affordable and widely available services, which can be used in far-flung communities through its extensive network of post offices (Azharuddin, 2024; Mohapatra & Ghosh, 2024a). Economic empowerment should be supplemented with an integral element, which is known as FL or simply the comprehension and ability to make informed decisions regarding money matters. Access to it has been proven to increase it significantly, and individuals are more likely to acquire FL in handling their accounts, transferring money, and saving in products if taught to understand savings products. Based on the literature, the theory we have included in this article is that FL programs connected to banking services encourage FI by giving people a fundamental understanding of the financial system (Bagehot, 1873; Durusu et al., 2017). As per the literature, we have assumed the following hypotheses (refer to Figure 1):

H1: POB → FL: Post office banks positively affect financial literacy. H2: PPB → FL: Post Payments Banks positively affect financial literacy. H3: RRB → FL: Regional rural banks positively affect financial literacy.

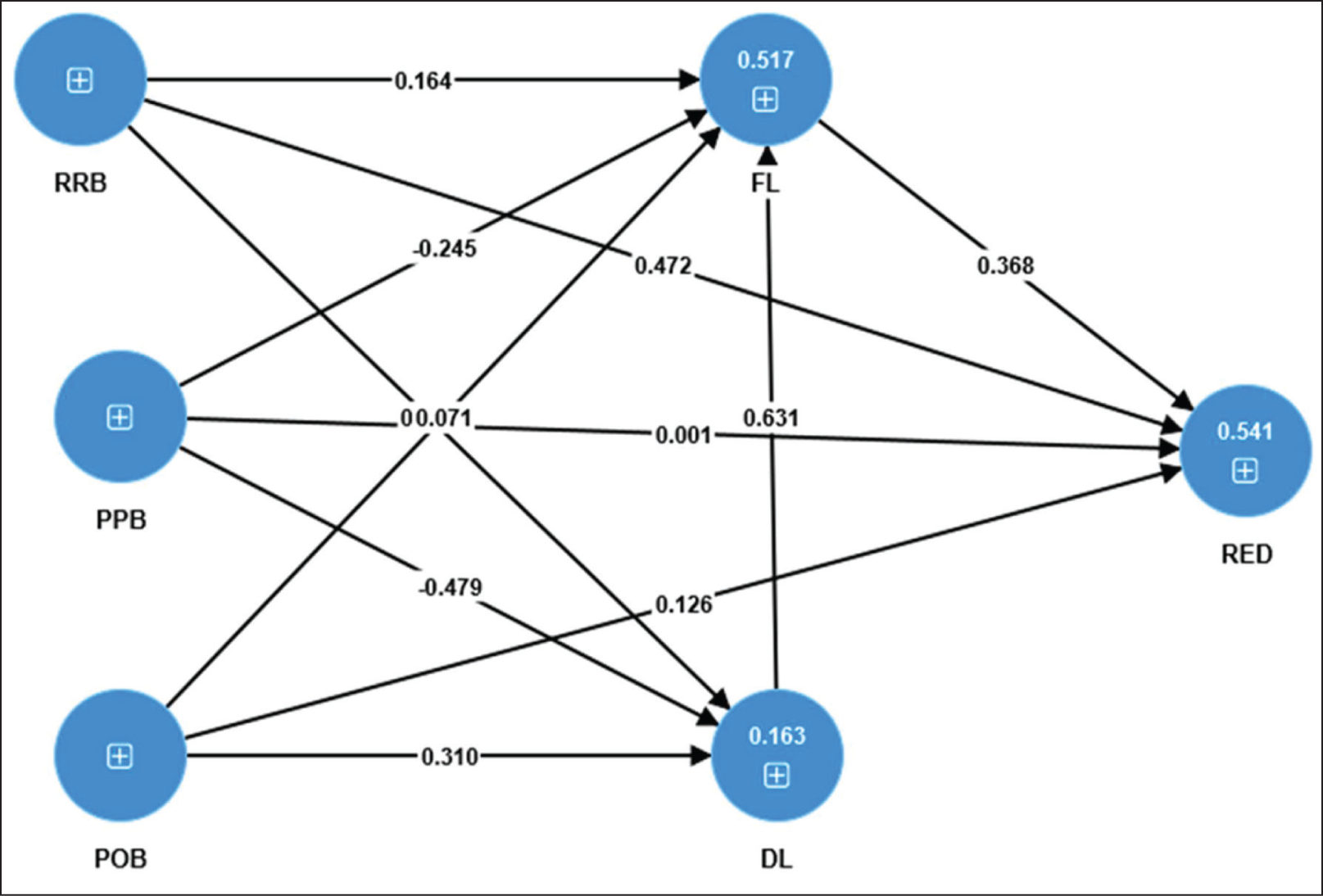

The Above-given Picture Illustrates the Concept This Study Aims to Develop. Here, FI Stands for Financial Inclusion; POBs Stand for Post Office Banks; IPPBs Stand for India Post Payments Bank; and RRBs Stand for Regional Rural Banks. These Three Variables Are Considered Proxies for FI. FL and DL (Digital Literacy) Mediate the Relationship Between the Proxies and the Dependent Variable, Rural Economic Development (RED).

Financial Inclusion and Digital Literacy

Online payment, digital wallets, and mobile banking offer financial services to the underbanked and unbanked communities. However, for one to use such services confidently and securely, he or she must be digitally literate. A better understanding of the digital space makes people use these systems, make proper financial choices, and prevent fraud or other security risks on online sites (Gomber et al., 2017). When people employ digital technologies, they are also required to be financially literate so that one can make prudent financial choices. It assists users in managing digital budgeting and planning tools, understanding their financial data, and accessing online sources of financial education (Peeters et al., 2018). Two factors complement each other, of which DL is one that allows for easy accessibility and usage of digital financial services, which are in the core of FI. The three together result in economic prosperity and at the same time personal financial security. The most common modern occurrence in digitally transformed financial systems is simultaneous with increases in DL and FI.

Indeed, these encompass DL and FI, augmenting financial involvement. Financial inclusion extends available, affordable financial services for individuals involved in any banking, savings, or credit toward underprivileged groups. From this perspective, individuals fairly access it (Al-Shami et al., 2024; Ariana et al., 2024). The greater this access to mobile financial applications and digital banking interfaces, the better the possibilities for an enhanced DL base. Digitally literate people can better utilize digital finance services because they know how to use them. Digital literacy is encouraged through digital financial services as it incorporates these services in developing countries, even in marginalized and rural areas where digital financial services are often found (Adel, 2024; Kamble et al., 2024). As per the literature, finance–growth nexus and financial development theory (Bagehot, 1873; Durusu et al., 2017), we have assumed the following hypotheses (refer to Figure 1):

H4: POB → DL: Post office banks positively affect digital literacy. H5: PPB → DL: Post Payments Banks positively affect digital literacy. H6: RRB → DL: Regional rural banks positively affect digital literacy.

Financial Literacy and Digital Literacy

Financial literacy and DL are related yet different concepts driving society today. Plenty of online sources provide financial management tools or applications that require digital competence to be used properly. They allow people to keep track of their budget, how much money they spend on things, or even make the right monetary decisions. Many individuals these days invest in stocks and other cryptocurrencies through online tools. Such crucial know-how about how these websites work, researching investments, and executing trades safely goes with DL (Tran et al., 2020). With increased online financial transactions, individuals must be digitally literate to recognize and avoid scams and phishing attempts. It is, therefore, through understanding these cyber security techniques that a financial asset is protected. Contemporary technology users must be digitally literate to access and control all their financial assets and information. Skills must be acquired and sustained as one navigates the contemporary financial market. The constituent elements of DL, such as FL, will increase further with technological advancement.

Financial literacy and DL are critical to attaining FI. Financial literacy gives knowledge and abilities for making educated financial decisions, allowing people to use digital transaction platforms 9 (Cahyono & Rizqi, 2024). Digital literacy complements FL by providing users with technical abilities for navigating online banking and mobile payment systems. This interaction is especially crucial for vulnerable populations as it promotes inclusive growth in the digital economy (Ferilli et al., 2024; Umar & Dalimunthe, 2024). On the basis of the literature, we adopted the following hypotheses:

H7: FL → DL: Financial literacy positively affects digital literacy.

Financial Inclusion and Rural Economic Development

Access to financial services enables people and communities to save, invest, and manage their finances, thereby fostering RED. This increases economic activity, creates jobs, reduces poverty, and generally improves welfare in rural areas (Lopez & Winkler, 2018). Access to financial services among the rural people tends to increase their ability to establish and grow their businesses. These increases entrepreneurial and innovative capacities at local levels as more new products and services get invented while economic diversity gets improved. Increased investments in rural infrastructure, for instance through roads, schools, and healthcare facilities, may result from improved access to financial services (Cattaneo et al., 2022). Stable and increasing service demand may influence the investment decision of financial institutions in the area. Financial inclusion will help alleviate poverty through enhanced income opportunities for the rural populace and asset development for rural communities. As soon as people can get access to financial instruments, they have a chance of improving their living conditions overtime. Usually, the stress in FI programs goes to FL and education. Individuals from rural backgrounds could be educated on making informed financial decisions, managing their resources appropriately, and making future plans that would accumulate economic development. From the literature, finance–growth nexus and financial development theory (Bagehot, 1873; Durusu et al., 2017), we assumed the hypotheses as follows (refer to Figure 1):

H8: POB → RED: Post office banks positively affect rural economic development. H9: PPB → RED: Post Payments Banks positively affect rural economic development. H10: RRB → RED: Regional rural banks positively affect rural economic development.

Digital Literacy and Rural Economic Development

Governments, NGOs, and other stakeholders are important in facilitating DL in rural areas through targeted training programs, infrastructure development, and policy initiatives. Digital divide and enhancing digital skills can unlock the full potential of digital technologies for sustainable economic development in rural communities. Digital literacy is very central to the development of rural economics as it equips the individual and the community with the necessary skills and information to use digital technologies appropriately in economic activities. Digital literacy proficiency enables rural businesses to participate effectively in e-commerce and beyond local boundaries. This will result in increased sales and overall prosperity of farm businesses. According to Khan et al. (2021), sensors, drones, and farm management mobile applications have become a part of modern agricultural practices. Digital literacy for farmers will come handy because the more they know, the better they are at practicing precision agriculture, and the more efficiently they can use resources, increasing productivity as a whole. As per the literature finance–growth nexus and financial development theory (Bagehot, 1873; Durusu et al., 2017), we have assumed the following hypothesis:

H11: DL → RED: Financial literacy positively affects rural economic development.

Data and Methodology

With the assistance of the IPPB, POBs, and RRBs in Uttar Pradesh, this study focused on rural youth’s FI and digital FL. An offline survey and interview (Cox et al., 2020; Lyons & Kass-Hanna, 2021) were undertaken to gather data for this study. For this experiment, we chose a non-probability convenience sampling strategy. We used a structured questionnaire to collect responses from participants while considering the study’s context and the viability of the survey method. We utilized filter questions to confirm that respondents had recently used financial services to keep our sample current. Various reflecting metrics were used to assess the conceptual model’s constituent parts. The survey instrument underwent pilot testing on 100 participants after being finalized. Out of the 800 offline questionnaires distributed in the Indian state of Uttar Pradesh, the “survey” gathered 735 responses from rural youth. However, only 650 viable responses were left after eliminating incomplete, multivariate, and too consistent responses.

The study uses PLS-SEM 4.0 for statistical analysis. According to Mateos-Aparicio (2011), “PLS-SEM estimates partial model structures by combining principal components analysis with ordinary least squares regressions.” The study adopted a two-stage approach to analyze the result, namely (a) measurement model evaluation and (b) structural model evaluation (Henseler et al., 2009).

Result

Measurement Model

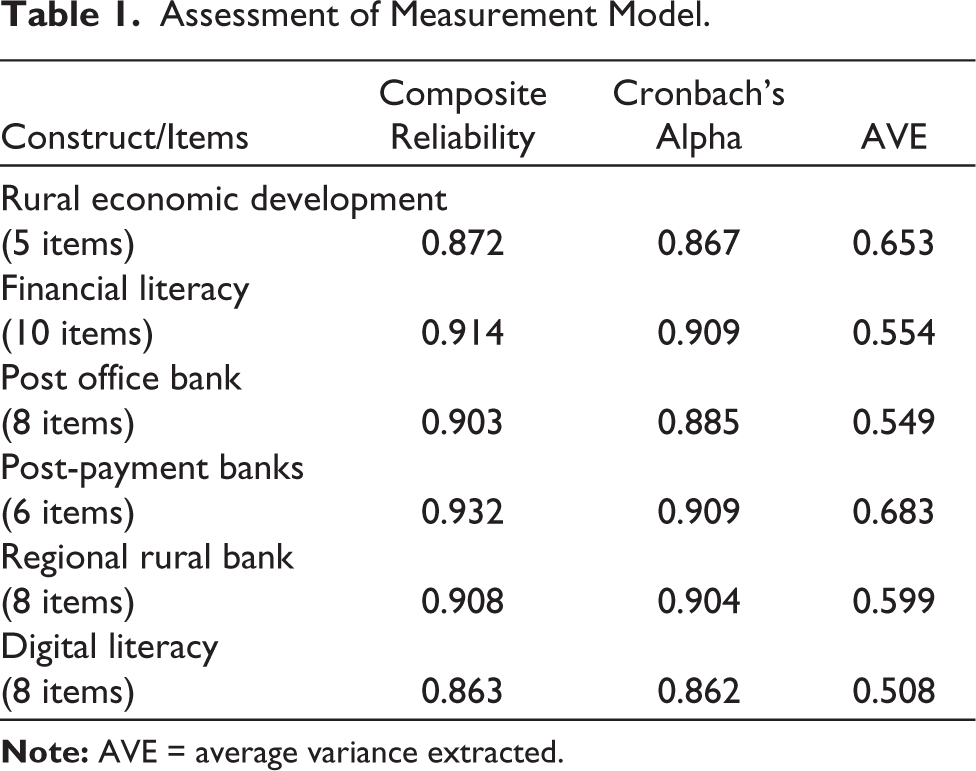

Evaluating the measurement model includes internal consistency reliability, convergent, and discriminant validity (DV). According to Ramayah et al. (2016), internal consistency reliability assesses the extent to which the items measure a specific latent construct. Hair et al. (2017) recommend composite reliability (CR) as a measure of internal consistency. Richter et al. (2016) emphasize that the threshold for each construct, a value above 0.7, is satisfactory for CR.

All model constructs were reflective, and the first step was assessing the measurement model. The preliminary step is assessing the indicator loadings. The loadings were as follows: RED from 0.77 to 0.83; Financial Literacy (FL) varied from 0.66 to 0.84; post office bank and financial inclusion (POSBFI) from 0.66 to 0.82; Post et al. inclusion ranged from 0.69 to 0.88; regional rural bank and FI from 0.71 to 0.82; and the understanding of fin-tech and digitalization (DL) from 0.67 to 0.74. For the construct to explain more than a percent of the indicator’s variance, recommended loadings should be 0.708, thereby maintaining acceptable item reliability. The assessment of the measurement model in Table 1 indicates the CR, Cronbach’s alpha, and the average variance extracted (AVE).

As Table 1 shows, all the constructs had CR between 0.86 and 0.93, with Cronbach’s alpha ranging from 0.862 to 0.909. These values are considered good (Hair et al., 2021). The AVE reported a value higher than the threshold of 0.5. Thus, convergent validity is established (Hair et al., 2021).

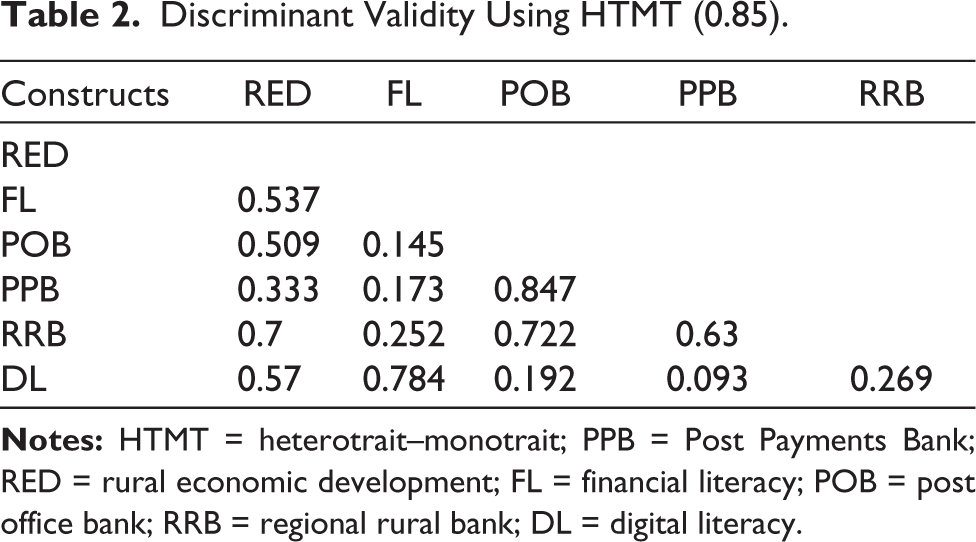

Once the construct reliability and the convergent validity are established, DV is checked, “the extent to which a construct is empirically distinct from other constructs in the structural model.” The traditional metric was the Fornell and Larcker (1981) criterion, and the recent metric accepted is the heterotrait–monotrait (HTMT) ratio of the correlations (Voorhees et al., 2016). According to Hair et al. (2019), “The HTMT is defined as the mean value of the item correlations across constructs relative to the (geometric) mean of the average correlations for the items measuring the same construct.” Henseler et al. (2015) suggested a threshold value of 0.90 for structural models. Table 2 indicates the HTMT values for the construct.

From Table 2, it is evident that all values were lower than 0.85. According to HTMT (Henseler et al., 2015), a value above 0. indicates that DV is absent. For conceptually distinct constructs, a lower, more conservative threshold value of 0.85 should be considered asserted (Henseler et al., 2015). Our study reported all values lower than the conservative threshold, establishing DV.

Assessment of Measurement Model.

Discriminant Validity Using HTMT (0.85).

Structural Model

The collinearity was examined to ensure bias in the regression results before assessing the structural equation. The ideal threshold variance inflation factor (VIF) values should be close to 3; however, VIF values of 3–5 are acceptable (Mason & Perreault, 1991). VIF values above 5 indicate probable collinearity issues among the predictor constructs. The study reported that the VIF value for the outer model was lower than 3.124, and for the inner model, the VIF values were below the conservative threshold of 3.

The structural model assists the researcher in evaluating the causal relationship between the constructs. Hair et al. (2017) suggested using the bootstrapping technique with resampling (5,000 resamples) to estimate the statistical significance of the hypothesized model. The results of the structural model are indicated in Table 3.

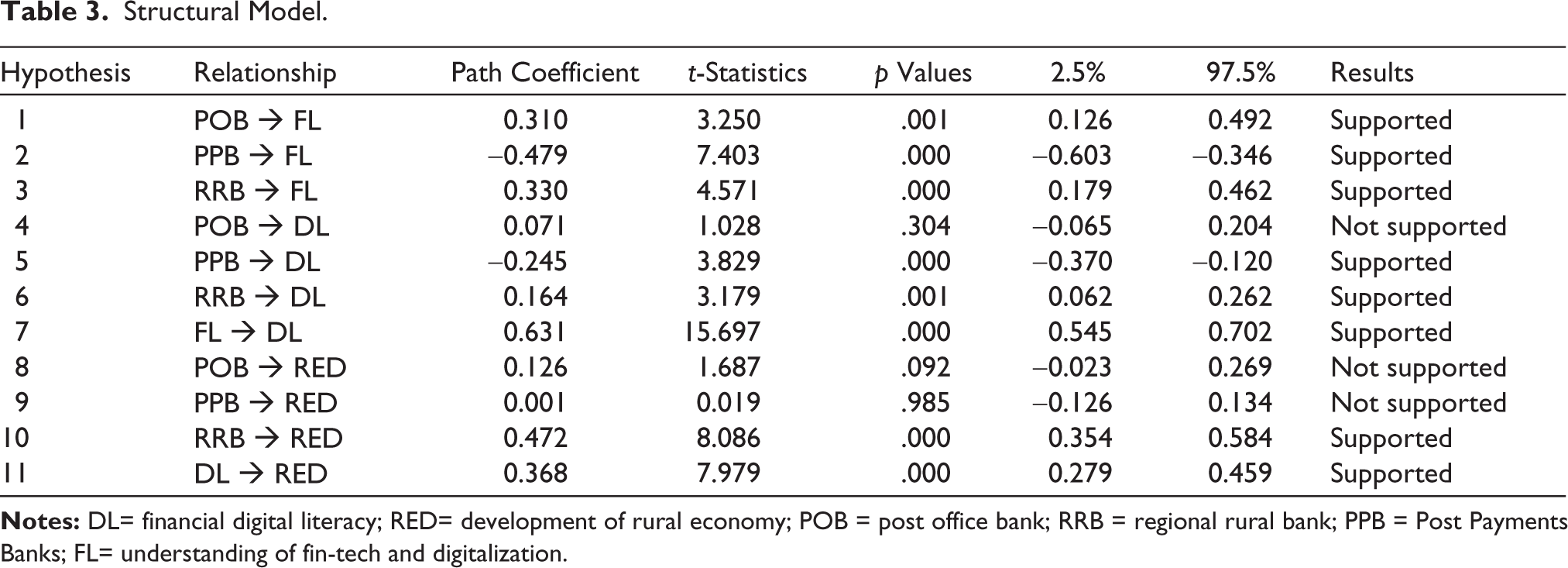

Table 3 depicts the details of the hypotheses. The findings are confirmed through t-values and the percentile bootstrap confidence interval. The study adopted 1.96 as the cut-off criterion for t-statistics (Hair et al., 2019). The results reveal that all hypothesized relationships, except H4 and H8, are significantly supported. Results depict that POB (H1: β1 = 0.368, p < .01, [0.279, 0.459]) had a significant direct effect on FL. PPB (H2: β2 = 0.123, p < .09, [–0.263, 0.269]) had a significant direct effect on FL. RRB (H3: β3 = 0.071, p < .3, [–0.65, 0.204]) had a significant direct effect on FL. POB (H4: β4 = 0.310, p < .001, [0.126, 0.492]) had an insignificant direct effect on DL. PPB (H5: β5 = 0.01, p < .98, [-0.126, 0.124]) had a significant direct effect on DL. RRB (H6: β6 = 0.245, p < .01, [–0.370, –0.124)] had a significant direct effect on DL. FL (H7: β7 = 0.479, p < .01, [-0.603, –0.346]) had a significant direct effect on DL. POB (H8: β8 = 0.472, p < .01, [0.354, 0.572]) had an insignificant direct effect on RED. PPB (H9: β9 = 0.164, p < .01, [0.062, 0.262]) had a significant direct effect on RED. RRB (H10: β10 = 0.330, p < .01, [0.179, 0.462]) had a significant direct effect on RRB. DL (H11: β11 = 0.631, p < 0.01, [0.545, 0.702]) had a significant direct effect on RED.

Coefficient of Determination

R2

As suggested by Ringle et al. (2018), the R2 value of the endogenous construct represents the within-sample predictive power of the structural model. The authors asserted that the R2 values of 0.25, 0.50, and 0.75 represent the “weak,” “moderate,” and “strong” traits, respectively. The adjusted R2 value reported is 0.532 indicating moderate trait fundamentally targeting construct RED.

Blindfolding (Q2)

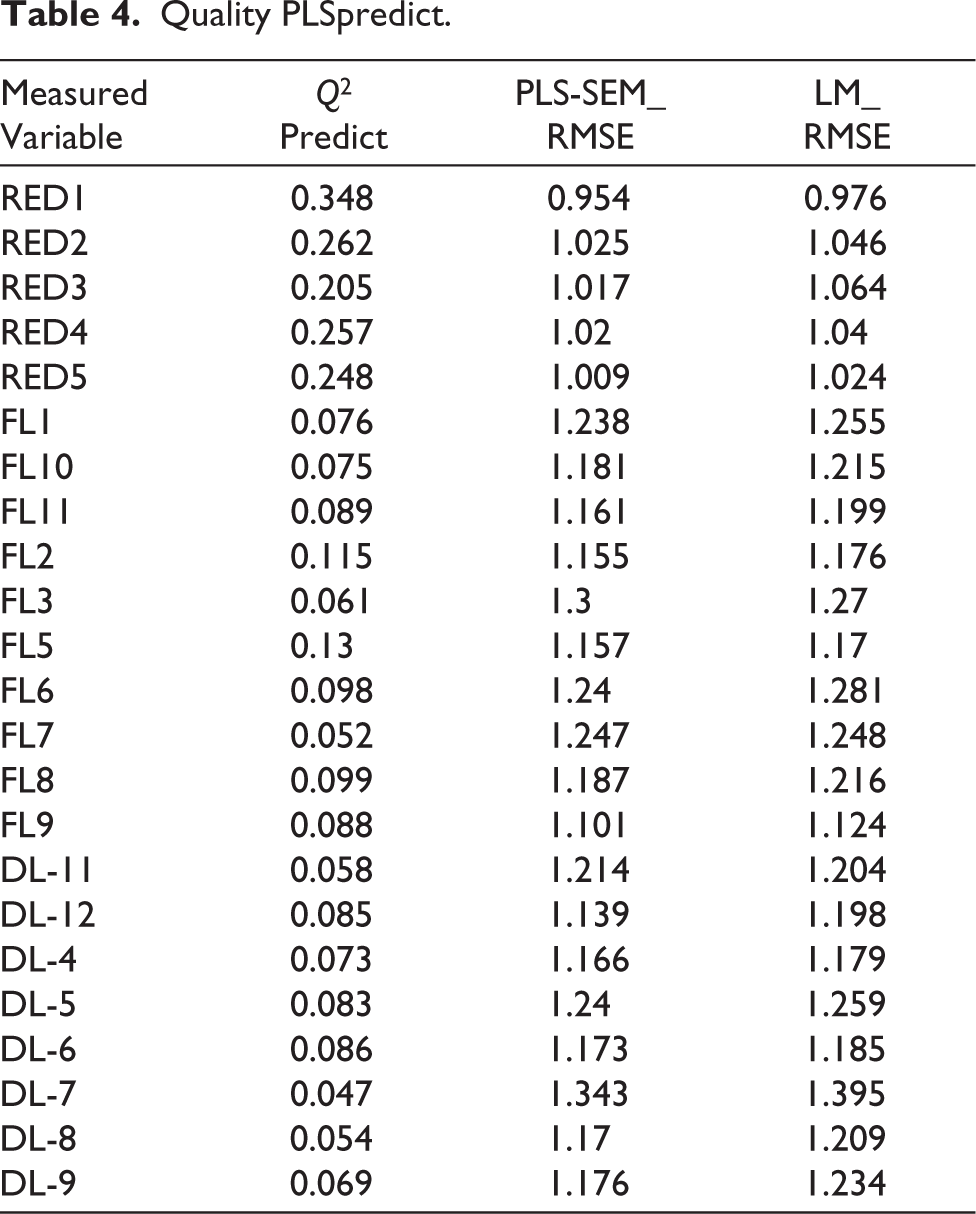

Hair et al. (2019) suggest using the Q 2 blinding folding approach to evaluate the predictive ability. A nonzero value for all the endogenous constructs ensures the model’s predictive accuracy. The model for the study reported a nonzero value. Refer to Table 4.

Structural Model.

Quality PLSpredict.

Out-of-sample Predictive Quality-PLS Predict

Finally, following the procedure of PLSpredict proposed by Shmueli et al. (2016), the researcher assessed the out-of-sample predictive quality of the model. For all the indicators of DRE, the PLS-SEM results have a more minor prediction than the linear model benchmark. Therefore, the model established a moderately high predictive power (Shmueli et al., 2019), as given in Table 4.

Mediation Analysis

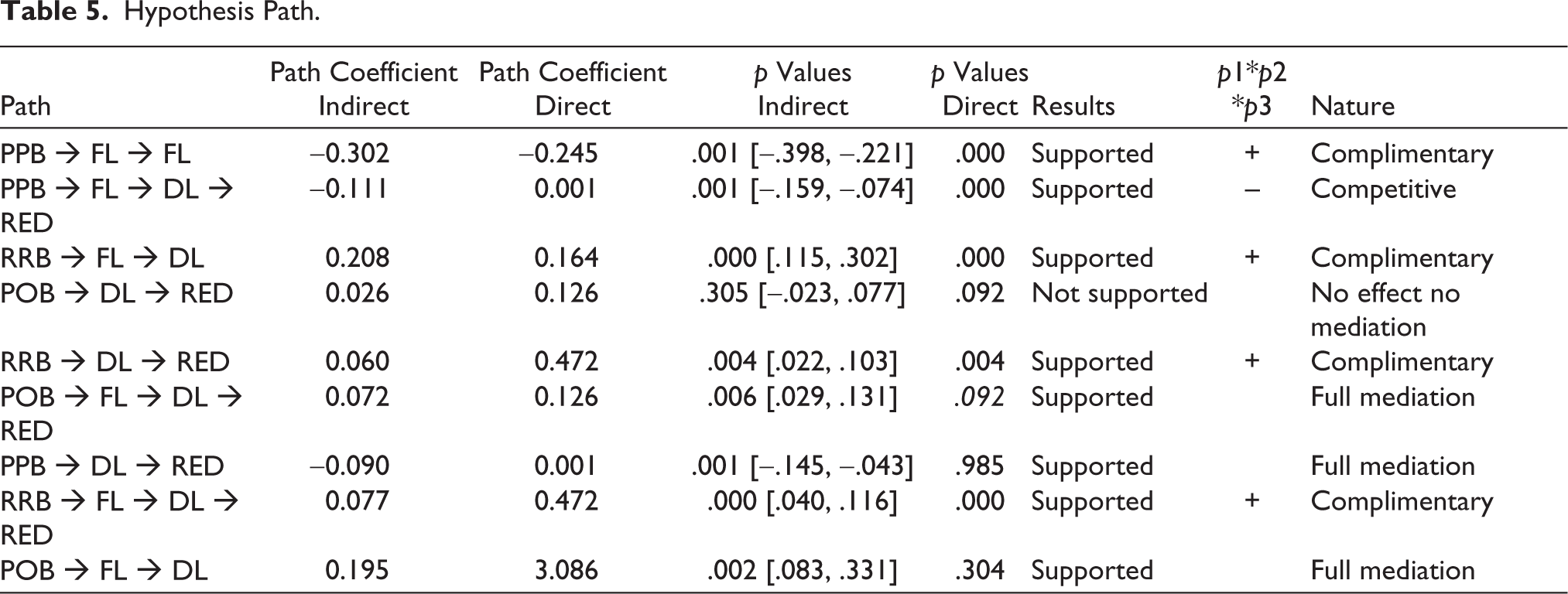

The significance of the direct, indirect, and total effects must be examined to assess the mediation effect. The direct effect is determined by the value of the path coefficient. The indirect effect is the product of the direct effect of RRB, PPB, POB, and FL to DL. The other indirect effect is also the product of PPB, RRB, POB, FL, and DL to RED. The sum of the direct effect and indirect effect is the total effect. To obtain results, 5,000 subsamples were bootstrapped with 315 observations per subsample. The other setting had no sign change option to determine the significance of the path coefficients with a p value of less than .05 two-tailed. To establish and test the significance of mediation hypotheses, 5,000 subsample bootstrapping was done. To support the hypothesis, the 95% confidence interval should not contain a ‘0’ value. Figure 2 and Table 5 show the remediation analysis results.

SEM Analysis of the Material.

Hypothesis Path.

Findings

As the study undertakes PLS-SEM, the preliminary step was to assess the measurement model through the indicator loadings. All the constructs had CR between 0.86 and 0.93, with Cronbach’s alpha ranging from 0.862 to 0.909. The values are considered to be good. According to HTMT, a value above 0.90 indicates that DV is absent. Our study reported all values lower than the conservative threshold, establishing DV. The collinearity was examined to ensure bias in the regression results before assessing the structural equation. The study reported that the VIF value for the outer model was lower than 3.124; for the inner model, the VIF values were below the conservative threshold of 3. The findings are confirmed through t-values and the percentile bootstrap confidence interval. The study adopted 1.96 as the cut-off criterion for t-statistics. The results reveal that all hypothesized relationships, except H4 and H8, are significantly supported. Results depict that POB (H1: β1 = 0.368, p < .01, [0.279, 0.459]) had a significant direct effect on FL. PPB (H2: β2 = 0.123, p < .09, [–0.263, 0.269]) had a significant direct effect on FL. RRB (H3: β3 = 0.071, p < .3, [–0.65, 0.204]) had an insignificant direct effect on FL. POB (H4: β4 = 0.310, p < .001, [0.126, 0.492]) had an insignificant direct effect on DL. PPB (H5: β5 = 0.01, p < .98, [–0.126, 0.124]) had a significant direct effect on DL. RRB (H6: β6 = 0.245, p < .01, [–0.370, -0.124)] had a significant direct effect on DL. FL (H7: β7 = 0.479, p < .01, [–0.603, -0.346]) had a significant direct effect on DL. POB (H8: β8 = 0.472, p < .01, [0.354, 0.572]) had an insignificant direct effect on RED. PPB (H9: β9 = 0.164, p < .01, [0.062, 0.262]) had a significant direct effect on RED. RRB (H10: β10 = 0.330, p < .01, [0.179, 0.462]) had a significant direct effect on RED. DL (H11: β11 = 0.631, p < .01, [0.545, 0.702]) had a significant direct effect on RED. The study asserted that the R2 values of 0.25, 0.50, and 0.75 represent the “weak,” “moderate,” and “strong” traits, respectively. The adjusted R2 value reported is 0.532, and the key target construct is RED. To interpret these metrics, researchers must compare each indicator’s root mean squared error (or mean absolute error) values with a naïve linear regression model benchmark. To obtain results, 5,000 subsamples were bootstrapped with 315 observations per subsample. The other setting had no sign change option to determine the significance of the path coefficients with a p less than 0.05 two-tailed.

Discussion

The current investigation plunges into the interplay among key elements of financial inclusion—specifically, POBs, PPBs, and RRBs—and their direct ramifications on RED. By incorporating FL and DL as moderating variables, the research aims to discern nuanced variations within these relationships. Hypotheses H1, H2, and H3 are not rejected, affirming the role of POBs, PPBs, and RRBs as strategic tools for augmenting FI. However, H4 is rejected, while H5 and H6 are upheld, reflecting the limited digitalization of Indian post offices. H7 remains unchallenged, underscoring the facilitative role of digital activity in enhancing access to financial services. Conversely, H8 is refuted, emphasizing the inadequacy of post offices alone in disseminating financial independence awareness. Conversely, H9 and H10 are validated, attributable to their extensive citizen outreach. Additionally, H11 is supported, elucidating the catalytic effect of digitalization on economic growth by fostering nationwide connectivity. Notably, while FL emerges as a significant mediator in the relationship between the constructs and RED, DL in isolation does not substantially influence RED. Only through the joint moderation of FL and DL do the impacts of FI on RED manifest distinctly.

This study extends the current body of literature by consolidating disparate constructs and investigating their impact on RED, focusing on FL and DL. While previous research has explored various facets of FI and rural development separately, this study uniquely combines these constructs and examines the moderating influence of literacy (Pradhan et al., 2021; Varghese, 2015). Findings are also in line with (Adel, 2024; Kamble et al., 2024). The current findings are also supportive to Khan et al. (2021), Cattaneo et al. (2022), and Lopez and Winkler (2018).

As per the study’s findings, the social and practical implications for enhancing FI in rural areas are to spread financial and digital literacy. Policymakers can promote FL and digital awareness by organizing community-focused educational initiatives in regional languages, helping rural populations understand and adopt digital financial platforms. Also, important facilities should be provided such as internet and electricity infrastructure. Stakeholders, including fintech companies, can develop accessible, user-friendly solutions tailored to rural needs and partner with local governments or NGOs to expand their reach. Post Payments Bank’s negative effect on FL and DL implies that PPB can create barriers to accessing necessary resources or education that are critical for improving FL. For instance, policies or programs that limit access to financial education, or fail to address diverse socioeconomic needs, can prevent individuals from gaining the skills necessary to make informed financial decisions. Therefore, policies and programs need to be improved and more robust.

Conclusion

The research results show a direct connection between certain factors and rural economic development. The inclusion of moderators, specifically financial literacy and digital literacy, uncovers subtle differences in this connection. The study uses three indicators of financial inclusion: post office banks, Post Payments Banks, and regional rural banks, demonstrating their direct influence on the economic progress of rural regions. Importantly, the presence of these moderators changes this relationship, especially emphasizing how both financial and digital literacy contribute to promoting economic growth in rural areas.

While financial literacy explains the influence of these constructs on rural economic development, the study suggests that digital literacy alone has minimal effect on the impact of financial inclusion or its constructs on rural economic development. However, when considered in tandem, financial and digital literacy significantly influence the relationship between financial inclusion and rural economic development, emphasizing the necessity for comprehensive literacy across both domains for sustainable societal development.

This study used primary data on rural youth from India Post Payments Bank, post office, and regional rural banks in Uttar Pradesh. This study used 650 viable responses to analyze the result using PLS-SEM 4.0 for statistical analysis. That is the limitation of the study and future studies can explore other Indian states or countries and use secondary or primary data as per availability, as well as apply another suitable methodology.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Appendix

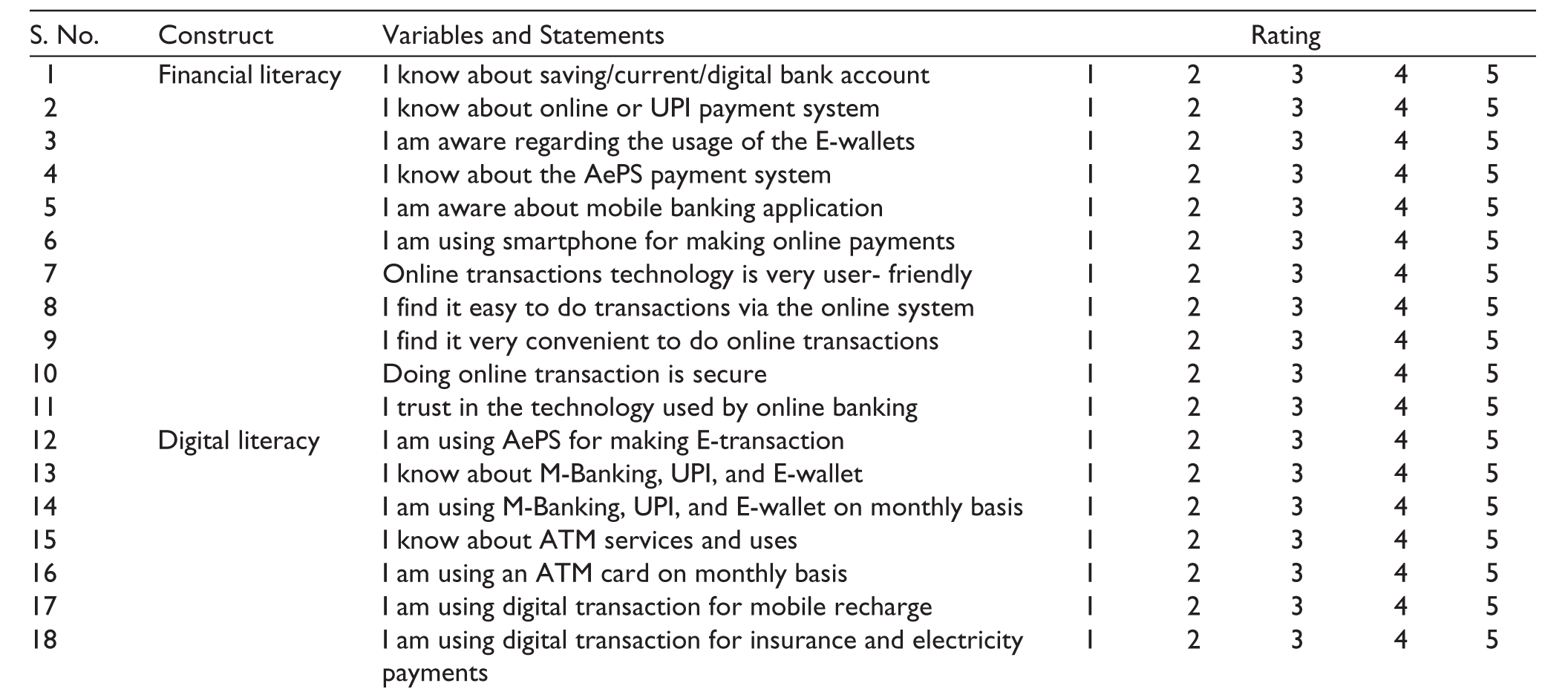

| S. No. | Construct | Variables and Statements | Rating | ||||

| 1 | Financial literacy | I know about saving/current/digital bank account | 1 | 2 | 3 | 4 | 5 |

| 2 | I know about online or UPI payment system | 1 | 2 | 3 | 4 | 5 | |

| 3 | I am aware regarding the usage of the E-wallets | 1 | 2 | 3 | 4 | 5 | |

| 4 | I know about the AePS payment system | 1 | 2 | 3 | 4 | 5 | |

| 5 | I am aware about mobile banking application | 1 | 2 | 3 | 4 | 5 | |

| 6 | I am using smartphone for making online payments | 1 | 2 | 3 | 4 | 5 | |

| 7 | Online transactions technology is very user- friendly | 1 | 2 | 3 | 4 | 5 | |

| 8 | I find it easy to do transactions via the online system | 1 | 2 | 3 | 4 | 5 | |

| 9 | I find it very convenient to do online transactions | 1 | 2 | 3 | 4 | 5 | |

| 10 | Doing online transaction is secure | 1 | 2 | 3 | 4 | 5 | |

| 11 | I trust in the technology used by online banking | 1 | 2 | 3 | 4 | 5 | |

| 12 | Digital literacy | I am using AePS for making E-transaction | 1 | 2 | 3 | 4 | 5 |

| 13 | I know about M-Banking, UPI, and E-wallet | 1 | 2 | 3 | 4 | 5 | |

| 14 | I am using M-Banking, UPI, and E-wallet on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 15 | I know about ATM services and uses | 1 | 2 | 3 | 4 | 5 | |

| 16 | I am using an ATM card on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 17 | I am using digital transaction for mobile recharge | 1 | 2 | 3 | 4 | 5 | |

| 18 | I am using digital transaction for insurance and electricity payments | 1 | 2 | 3 | 4 | 5 | |

| 19 | I trust in the functioning ability of online banking | 1 | 2 | 3 | 4 | 5 | |

| 20 | I can easily pay my bills without any delay | 1 | 2 | 3 | 4 | 5 | |

| 21 | I have proper savings for emergency needs | 1 | 2 | 3 | 4 | 5 | |

| 22 | I know about different types of deposit options available in the bank | 1 | 2 | 3 | 4 | 5 | |

| 23 | I have sufficient Internet knowledge for doing online transactions | 1 | 2 | 3 | 4 | 5 | |

| 24 | Development of rural economy | I am using Internet services for digital banking | 1 | 2 | 3 | 4 | 5 |

| 25 | I have a proper electricity facility and it helps to use digital services | 1 | 2 | 3 | 4 | 5 | |

| 26 | I have good road connectivity and it helps to visit the bank branch and other financial needs | 1 | 2 | 3 | 4 | 5 | |

| 27 | I have smartphone and it supports to use digital banking services | 1 | 2 | 3 | 4 | 5 | |

| 28 | I have ATM and its services is easily available nearby me | 1 | 2 | 3 | 4 | 5 | |

| 29 | Regional banks and financial inclusion | I know about regional rural banks | 1 | 2 | 3 | 4 | 5 |

| 30 | I have an active bank account in a regional rural bank | 1 | 2 | 3 | 4 | 5 | |

| 31 | I know about regional rural bank product and services | 1 | 2 | 3 | 4 | 5 | |

| 32 | I have a regional rural bank’s ATM card | 1 | 2 | 3 | 4 | 5 | |

| 33 | I am using regional rural bank ATM on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 34 | I am using AePS in my regional rural bank account | 1 | 2 | 3 | 4 | 5 | |

| 35 | I know about M-Banking, UPI, and E-wallet | 1 | 2 | 3 | 4 | 5 | |

| 36 | I am using M-Banking, UPI, and E-wallet on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 37 | Post office banks and financial inclusion | I know about post office bank | 1 | 2 | 3 | 4 | 5 |

| 38 | I have an active post office bank account | 1 | 2 | 3 | 4 | 5 | |

| 39 | I know about post office bank product and services | 1 | 2 | 3 | 4 | 5 | |

| 40 | I have a post office bank’s ATM card | 1 | 2 | 3 | 4 | 5 | |

| 41 | I know about M-Banking, UPI, and E-wallet | 1 | 2 | 3 | 4 | 5 | |

| 42 | I am using M-Banking, UPI, and E-wallet on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 43 | I am using post office bank ATM on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 44 | I am using AePS in my post office bank account | 1 | 2 | 3 | 4 | 5 | |

| 45 | Post payments banks and financial inclusion | I know about India Post Payments Bank | 1 | 2 | 3 | 4 | 5 |

| 46 | I have an active bank account in India Post Payments Bank | 1 | 2 | 3 | 4 | 5 | |

| 47 | I know about India Post Payments Bank’s product and services | 1 | 2 | 3 | 4 | 5 | |

| 48 | I have an India Post Payments Bank’s ATM card | 1 | 2 | 3 | 4 | 5 | |

| 49 | I am using an India Post Payments Bank’s ATM card on monthly basis | 1 | 2 | 3 | 4 | 5 | |

| 50 | I am using AePS in my India Post Payments Bank account | 1 | 2 | 3 | 4 | 5 | |

| 51 | I know about M-Banking, UPI, and E-wallet | 1 | 2 | 3 | 4 | 5 | |

| 52 | I am using M-Banking, UPI, and E-wallet on monthly basis | 1 | 2 | 3 | 4 | 5 | |

1. Only for Rural Youth in Uttar Pradesh