Abstract

Numerous international development targets aim to encourage and formalize remittances, because they can support development efforts while controlling and monitoring illicit capital flows. Despite continued efforts to promote formal remittance channels, informal remittances flourish among specific population groups. This study uses data from the Canadian Study on International Money Transfers to analyze the determinants of remittance modality or channel choice. Previous empirical work tends to classify remittances as either formal or informal. In contrast, this article considers a variety of channels. It shows that the dichotomization of formal versus informal remittances masks crucial differences across remittance channels. Due to Canada's unique geographical positionality, cash transfers operate distinctly from informal methods despite often being treated as a homogenous group in other studies. Interestingly, remitters are also more likely to use formal money transfer operators (most of which offer cash pickup options to recipients) than informal channels to send funds to countries with larger informal sectors. Within the context of Canadian remittance outflows, this invalidates the frequent assumption that more informal destination country economies push remitters to opt for informal transfer methods.

Introduction

According to the World Bank (2022), global remittances sent to low- and middle-income countries totaled 626 billion USD in 2022. However, these data cannot capture most informal remittance flows, such as cash hand-carried across borders, undisclosed postal goods, and other transfers. 1 This omission is significant because informal transfers could equal 1.5 to 10 times the amount of officially reported global remittances (O’Neill 2001; Sander 2004; Freund and Spatafora 2008).

Ascertaining the magnitude and extent of unreported informal remittance flows is a significant obstacle to understanding their scope and policy significance. Despite the measurement challenges, scholars have developed innovative methods for estimating the size of the informal or “shadow” economy. Efforts to estimate this central latent variable include the use of night lights satellite imagery as a proxy for economic activity (Tanaka and Keola 2017; Beyer et al. 2018), household survey data using other proxies (Henley, Arabsheibani and Carneiro 2009), and factor analysis and structural equation modeling (Medina and Schneider 2018). Furthermore, prior research infers that there exists a link between a larger recipient country informal sector and larger remittance flows using the balance of payment omissions and errors (Freund and Spatafora 2008), satellite imagery (Ghosh et al. 2009; Ghosh et al. 2013), or lower financial development as indicators of informality (Ezeoha 2013).

Although informal remittance channels have potential advantages in terms of cost, speed, accessibility, and anonymity (Kapur 2005; Pieke, Van Hear and Lindley 2007; Siegel et al. 2010), they may suffer from reliability issues due to a lack of transparency and regulatory oversight (IMF 2009). Nevertheless, informal remittance flows persist, at least partly because they feature lower costs than their formalized counterparts, despite international efforts to lower formal remittance costs (Freund and Spatafora 2008). For example, Canadian remittance outflows through banks and money transfer operators (MTOs) estimate transaction costs around 7.4 percent to send 200 CAD and 4.8 percent to send 500 CAD according to 2017 estimates of the World Bank's Remittance Prices Worldwide database.

Using a recent Canadian Study on International Money Transfers (SIMT), which surveyed 22,908 migrants born in official development assistance 2 (ODA)-eligible countries within Canada, this study addresses the following two research questions: Why do remitters opt for certain channels but not others? What incentivizes remitters to opt for informal methods? These questions seek to explain why informal channel use in Canada is only weakly linked to recipient country informality, and remitters continue to use informal channels despite numerous alternatives. Moreover, they inform policy discussions regarding large-scale international efforts to formalize flows and steer migrants away from informal channels.

The heterogeneous nature of money transfer methods increasingly necessitates an enhanced breakdown of remittances by various channels. Pieke, Van Hear and Lindley (2007) point out that the informal remittance categorization merely serves as a residual category for all unaccounted remittances, thus acting as a so-called “fake” categorization. This study contributes to a growing body of knowledge that nuances and elaborates the traditional dichotomization between informal and formal flows.

This article is divided into six additional sections. The next section discusses the benefits of the first-to-last mile model as a valuable roadmap to studying remittance decision-making. The third section provides a brief review of empirical research on remittance channel choice. The fourth section provides details on the reclassification of remittance channels, descriptive statistics on modality decision factors, and a brief discussion of data limitations. The fifth section covers the methodological approach using multinomial logistic regressions to study remittance channel choices. The sixth section outlines the findings on the determinants of remittance modality and decision factors by socio-demographic characteristics. Finally, the last section concludes with a summary of the findings and their policy implications.

An Analytical Framework of Remittance Channel Choice

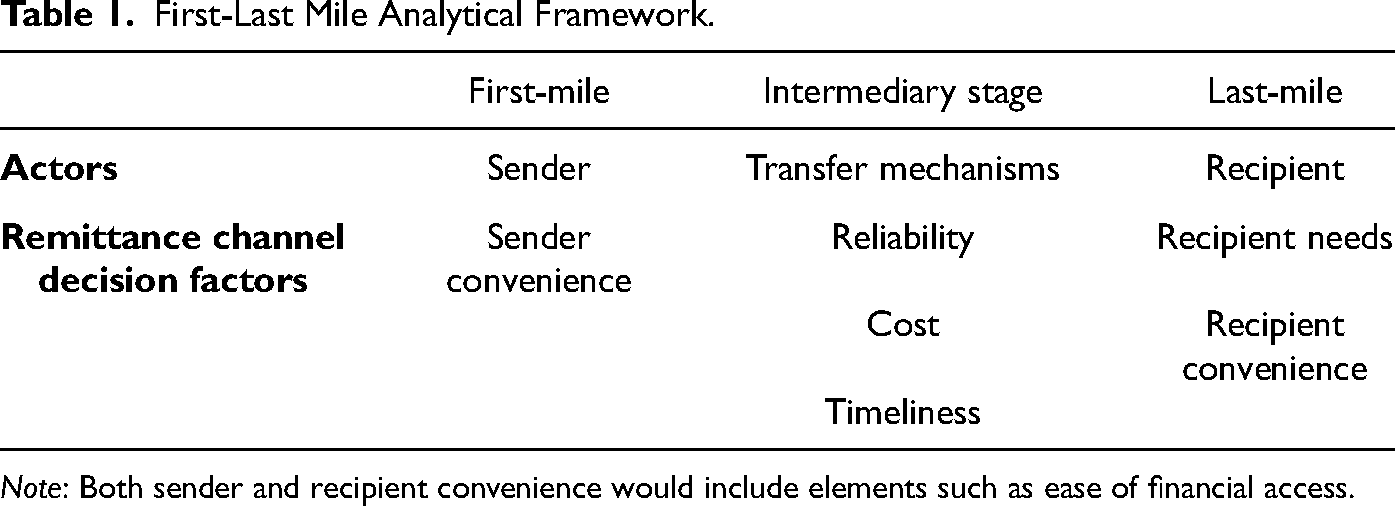

To explain remittance modality choices, this article uses the first-to-last mile framework (Hernández-Coss 2005a; Hernández-Coss 2005b) with six main determinants of channel choice. The parsimonious framework identifies three stages and their respective actors: the sender (first-mile), intermediaries such as remittance providers (intermediary stage), and the recipient (last-mile). 3 The six factors are sender convenience (including access to and knowledge of channels), recipient convenience, cost, timeliness of transfer, reliability of the channel, and recipient needs. Table 1 outlines a simplified version of the first-to-last mile framework detailing the actors and factors of each stage.

First-Last Mile Analytical Framework.

Note: Both sender and recipient convenience would include elements such as ease of financial access.

Sender convenience directly impacts the remitter in the first-mile. Lower levels of convenience may stem from a lack of access to certain types of channels or digital means. However, the legal status of migrants can also impede their access to certain transfer methods. For instance, undocumented or temporary immigrants may favor informal methods or cash due to frequent or relatively inexpensive travel back to their home country via relatives or diaspora networks (de Haas and Plug 2006; Karafolas and Konteos 2010; Siegel and Lücke 2013; Ferriani and Oddo 2019).

The second stage involves the interaction of market actors and fund transfer services. This stage involves all types of remittance service providers and intermediaries — including the remitters in cases where they hand-carry funds. The main determinants in this stage are transfer cost, transfer timeliness, and reliability of channels (Siegel and Lücke 2013). All else held equal, one can assume any given remitter prefers cheaper, faster, and more reliable methods. However, higher reliability and speed generally carry a higher cost trade-off for MTOs, banks, and credit unions (Dimbuene and Turcotte 2019). Informal methods may come at lower costs, but transfer speeds and reliability fluctuate immensely (Sander 2004; Ullah and Panday 2007; Freund and Spatafora 2008; Orozco 2010; Basu and Bang 2015; Orozco and Klaas 2020).

The last-mile refers to the end distribution to recipients. This stage weighs the importance of distribution channels based on the recipients’ needs and recipient access (including financial access). Recipients’ needs in terms of payment frequency, such as frequent transfers to health expenses or food and maintenance costs (Amuedo-Dorantes, Bansak and Pozo 2005), can impact channel choice. Beyond recipient needs, limited access to banking and financial tools in highly informal economies can constitute another critical determinant in choosing remittance systems in the last-mile. For instance, migrants habitually resort to informal systems where they, or the intended recipients, cannot access formal financial institutions (Puri and Ritzema 1999; Maimbo 2003; Amuedo-Dorantes and Pozo 2005; Freund and Spatafora 2008). Financial literacy, cultural factors, and language (Sander 2004; Pieke, Van Hear and Lindley 2007) can also be barriers to recipient convenience. For instance, banks often require access to formal financial networks, whereas MTOs generally offer cash pickup options at agent locations (Bradford 2008).

Despite the sender acting as the central decision-maker, the proposed framework assumes that they base their decisions on factors (or their perceptions of these factors). Per the framework, the sender uses backward induction (i.e., reasoning backwards in time starting from the end result — the recipient receiving the remitted funds) to study how each factor and each stage of the remittance process impacts modality choices.

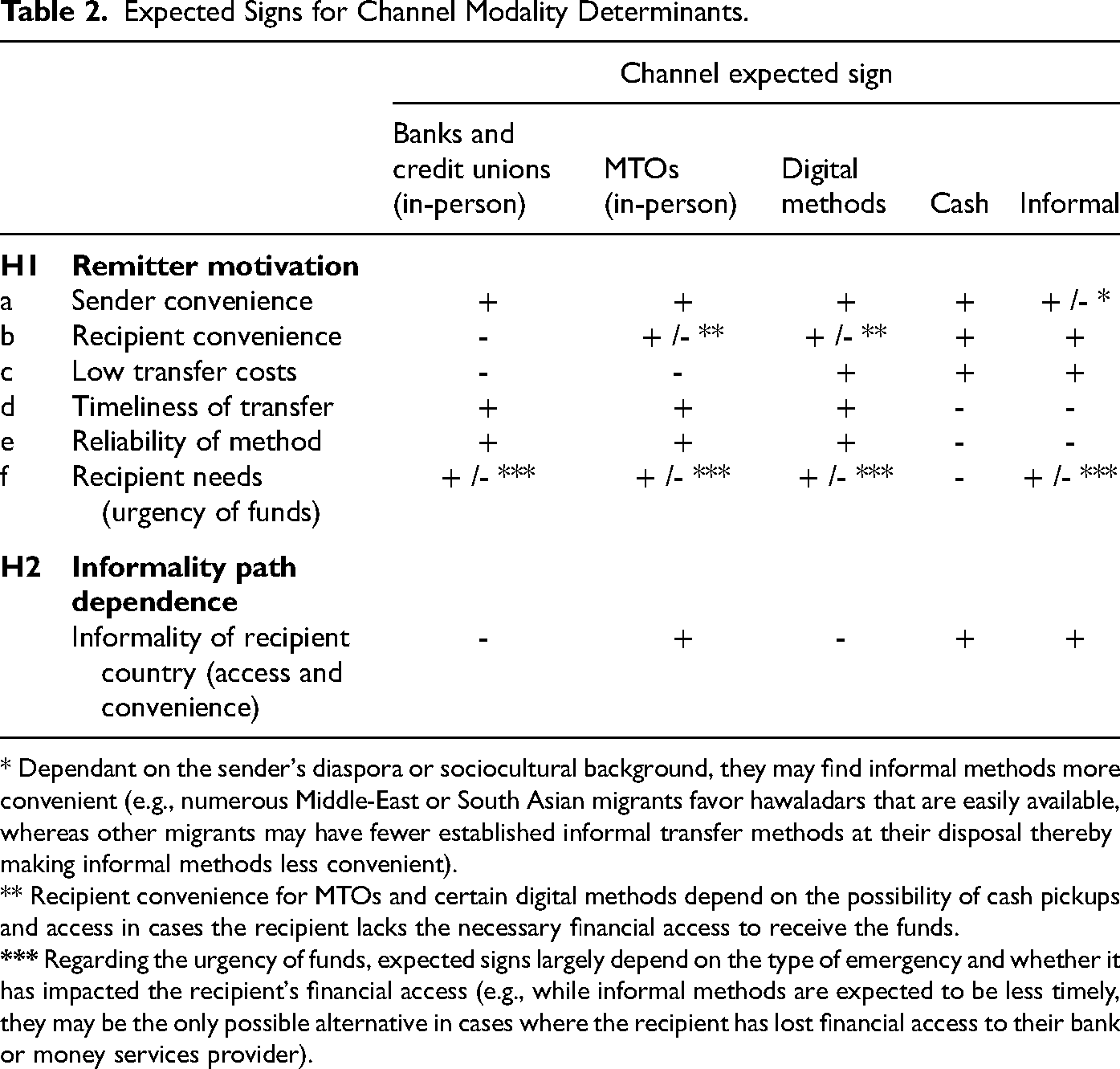

The framework yields two main hypotheses. The first hypothesis, that each factor in the first- to last-mile framework impacts channel choice, consists of six sub-hypotheses — one for each preference. Table 2 outlines the expected signs of each sub-hypothesis. For one, sender and recipient convenience likely vary based on personal circumstances (e.g., while a remitter without access to digital banking will likely not find digital methods as convenient, this may not be true for other remitters). Low transfer costs are hypothesized to be associated primarily with channels other than banks, credit unions, and MTOs. Conversely, timeliness and reliability are hypothesized to be higher for these channels and digital methods. Finally, recipient needs, particularly in terms of urgency of funds, may vary across channel use but are expected to lower the likelihood of selecting cash transfers that require direct travel to the recipient country.

Expected Signs for Channel Modality Determinants.

* Dependant on the sender's diaspora or sociocultural background, they may find informal methods more convenient (e.g., numerous Middle-East or South Asian migrants favor hawaladars that are easily available, whereas other migrants may have fewer established informal transfer methods at their disposal thereby making informal methods less convenient).

** Recipient convenience for MTOs and certain digital methods depend on the possibility of cash pickups and access in cases the recipient lacks the necessary financial access to receive the funds.

The second hypothesis addresses the misconception that more highly informal recipient country economies encourage remitters to choose informal channels over formal ones in Canada. While a country's informality can act as a proxy for lower levels of financial access (i.e., lower access to formal remittance methods), several formal channel providers offer cash pickup options via stores or other agent locations (Bradford 2008) to provide services in regions with reduced access to banks and other financial institutions. In the case of remittances leaving Canada, this article argues that migrants sending remittances to recipient countries with larger informal sectors are similarly likely to choose informal or competing formal methods.

Review of Select Empirical Works

There is much country-level work on remittance modality (Sander 2004; Freund and Spatafora 2008; Kupets 2012). However, data limitations and aggregations often require such studies to dichotomize formal and informal flows. Fewer studies focus on channel choice using large-sample analyses at the individual or household level. Though not a comprehensive review of existing literature, four such studies stand out.

Amuedo-Dorantes and Pozo (2005) study a sample of approximately 6,000 Mexican migrants returning from the United States using data from five waves of the Encuesta Sobre Migración en la Frontera Norte de Mexico. These data cover eight northern Mexican border cities and contain information on four main remittance channels: banks, MTOs, hand-carried cash or mailed cash, and others (acting as a catch-all variable for all other transfer types). As in this study, the authors use multinomial logistic regression analysis to examine remittance modality choices.

Amuedo-Dorantes and Pozo (2005) identify a potential for a simultaneity bias, whereby the channel choice impacts the amount sent and vice versa. Such a simultaneity bias could occur where discrete steps in remittance pricing (i.e., price brackets) introduce unintended diseconomies of scale. Amuedo-Dorantes and Pozo (2005) provide an illustrative example of remitters incurring a 15-dollar transfer cost to remit 200 dollars but would face a 20-dollar fee to remit 201 dollars due to the discrete-step pricing structure in several MTOs. Such a bias would violate the validity of their proposed model.

Amuedo-Dorantes and Pozo (2005) use the number of recipients (proxied using family size) as an instrumental variable to correct the simultaneity in causality between channel choice and the amount sent. The authors estimate the dollar amount remitted based on family size and other factors. The multinomial regression model then uses these predicted values to study remittance modality. Given family size is causally tied to the amount remitted but not the channel chosen, this approach restricts causality to the amount sent influencing channel choice. The main findings attest that access to formal finance is a key factor influencing channel decision-making. Moreover, those in non-permanent forms of employment, new arrivals to the United States, and those remitting to rural or poorer regions are more likely to resort to cash in the mail or hand-carried cash transfers.

Kosse and Vermeulen (2014) study the channel choice of 501 remitters in the Netherlands using the previous 12 months’ remittance data collected in a 2009 survey. The authors analyze five main transfer mechanisms: banks, MTOs, informal, automatic teller machines, and cash. Unlike Amuedo-Dorantes and Pozo (2005), Kosse and Vermeulen (2014) do not control for the simultaneity in channel choice and the amount sent. Instead, they posit that, while it is reasonable to assume migrants may remit less frequently to take advantage of economies of scale in transfer costs, their data are less likely to incur such biases since they span over 12 months. The findings of this study suggest that education, costs, access, and financial development of the receiving country play an important role in channel choice. Payment habits (e.g., preference for cash) are statistically insignificant once the authors consider remittance modality factors such as transfer speed, sender convenience, and the recipient's access to a bank.

Siegel and Lücke (2013) use a 2006 sample of approximately 4,000 migrant households in Moldova, of which 1,139 have bilateral remittance relationships with recipients abroad. They use multinomial logistic regression for three choices: formal services, informal operators, and personal transfers. They find that reasons not to use formal methods include lower informal sector transfer costs, immigration status (e.g., undocumented migrants), and duration of stay (e.g., temporary or seasonal work).

Karafolas and Konteos (2010) study Albanian immigrants’ experience in Greece using 2007 data that includes 300 permanent and 183 seasonal migrants. It examines three types of remittance channels: banks, MTOs, and cash carried by the migrants or their relatives. As in the previous studies, the authors use multinomial logistic models and find that remitters, particularly seasonal immigrants, typically prefer hand-carried transfers that are, contrary to this study, treated as synonymous with informal flows. Within the formal remittance sector, the authors suggest there are several distinctions between channels, with temporary and seasonal immigrants favoring MTOs over banks. This further supports the importance of distinguishing between different types of remittance channels.

Data

In 2015, Global Affairs Canada commissioned the SIMT, which Statistics Canada conducted in 2018 (Dimbuene and Turcotte 2019). Using a sample of 22,908 ODA-eligible country-born migrants to Canada, the SIMT is the first Canadian large-sample dataset to contain considerable detail about remittance activity. Moreover, given the absence of administrative data on remittance modalities, the sample of remittance senders aligns with research recommending sender surveys over recipient surveys prone to underreporting remittances (De Arcangelis et al. 2023).

The survey focuses on those migrants most likely to have a development impact abroad. The restriction to ODA-eligible country-born individuals is particularly relevant in the context of this research, given the spotlight on tackling the Canadian international development role of remittances as part of its global commitments.

The stratified random sample of respondents aged 18 and over as of April 1, 2018, who were born in ODA recipient countries, includes 40,000 randomly sampled persons. The random sample stemmed from two sources: the 2016 Longform Census used to cover naturalized Canadians and permanent residents, and administrative files from Immigration, Refugees and Citizenship Canada (IRCC) to cover immigrants who arrived after the 2016 Census, refugee claimants, and temporary residents.

Statistics Canada provides probabilistic weights from both the 2016 Census portion of the sample frame and the IRCC administrative immigration files portion of the frame. The principle behind estimation in a probabilistic sample is that each unit in the sample represents the broader effects within the Canadian population.

Reclassifying Remittance Channels

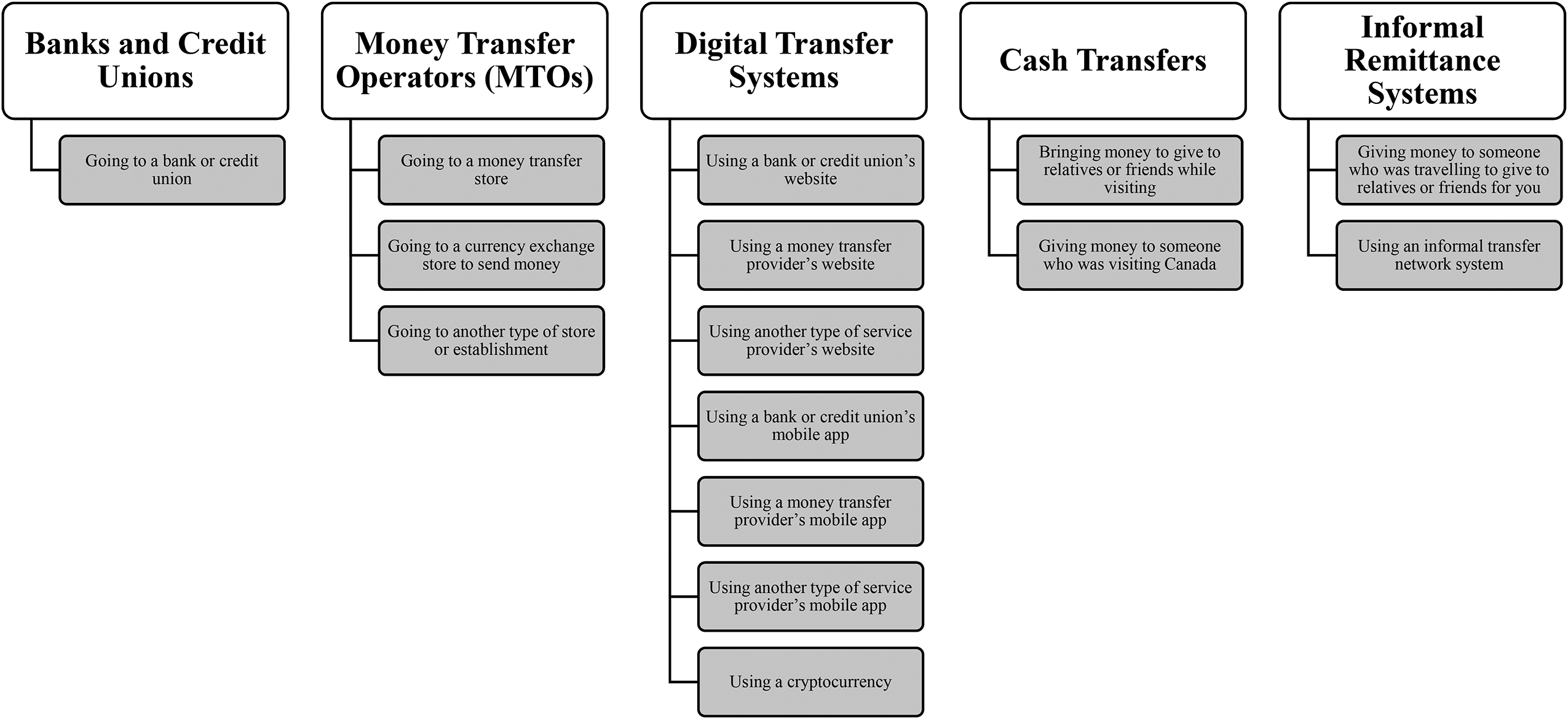

The SIMT provides 15 defined remittance channels. However, many of these channels share similar characteristics or are analytically prohibitive due to their small subsample size. Consequently, this study collapses channels into broader categories of remittance mechanisms. This addresses issues of sample size, simplifies differences and commonalities across channel types, and facilitates meaningful comparisons to previous studies of remittance modality choices. Analogous channels are grouped according to similarities in usage and the respective characteristics of remitters using them. Figure 1 illustrates the aggregation of channels used in this study.

Channel category aggregation. Source: SIMT.

Modality Factors

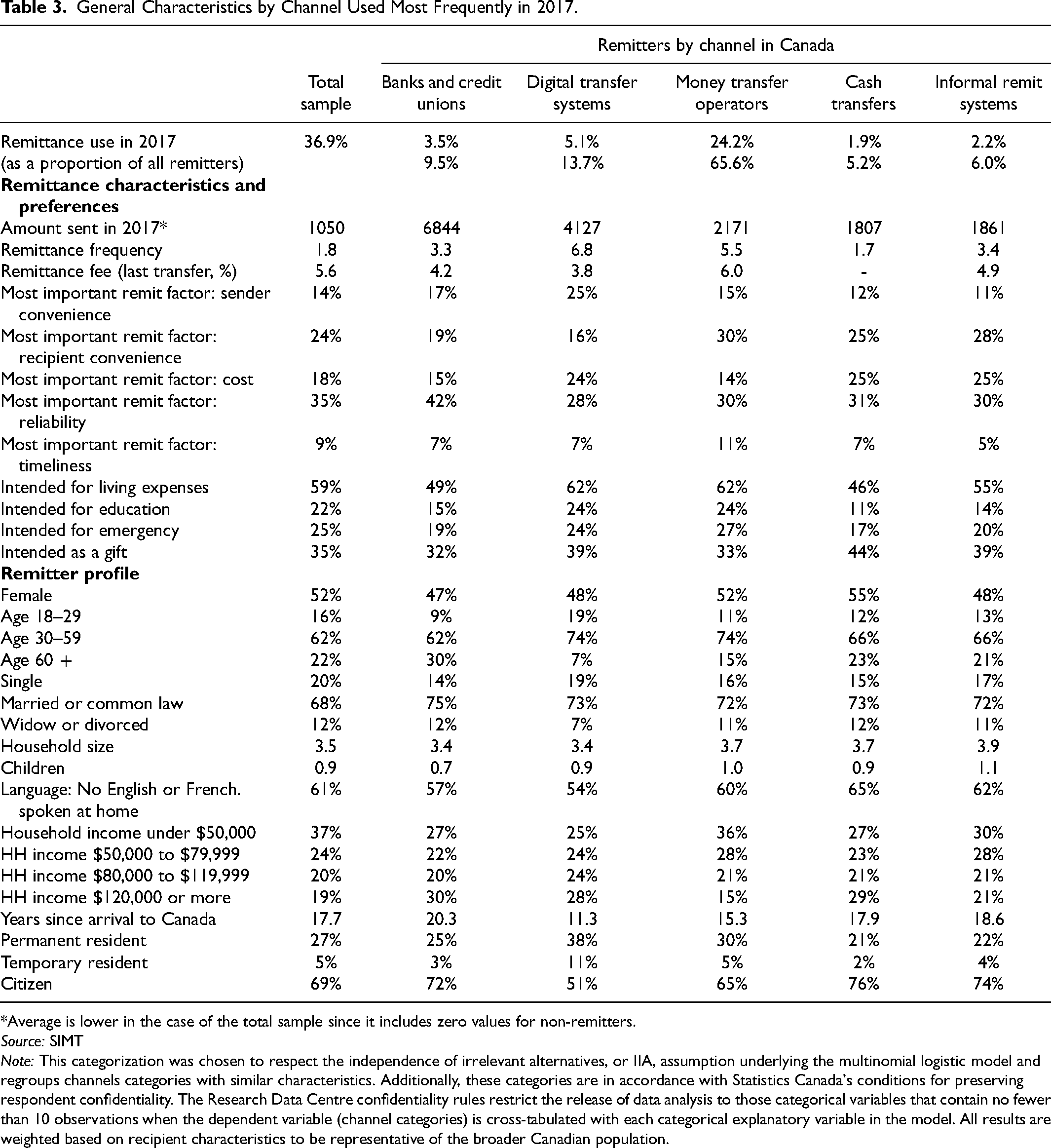

The factors outlined in the first-to-last mile framework impact the remittance channel choices of migrants. Table 3 presents summary statistics for the study variables by channel most frequently used in 2017.

General Characteristics by Channel Used Most Frequently in 2017.

*Average is lower in the case of the total sample since it includes zero values for non-remitters.

Source: SIMT

Note: This categorization was chosen to respect the independence of irrelevant alternatives, or IIA, assumption underlying the multinomial logistic model and regroups channels categories with similar characteristics. Additionally, these categories are in accordance with Statistics Canada's conditions for preserving respondent confidentiality. The Research Data Centre confidentiality rules restrict the release of data analysis to those categorical variables that contain no fewer than 10 observations when the dependent variable (channel categories) is cross-tabulated with each categorical explanatory variable in the model. All results are weighted based on recipient characteristics to be representative of the broader Canadian population.

Table 3 also indicates that almost two-thirds of remitters favor in-person MTOs. At first glance, it is puzzling that so many remitters favor in-person MTO transfers, given that transfers via other channels are cheaper on average. One likely explanation is that remitters using in-person MTOs (including other forms of in-person stores) often identify recipient convenience and transfer timeliness as the most important factors influencing their remittance choices. The usage of in-person MTOs is also higher among lower-income remitters.

The SIMT survey asks respondents to identify among five key factors that influenced their remittance decisions. Survey respondents identify reliability as the most important factor impacting remittance decisions. Remitters who most frequently use in-person banks or credit unions to remit are the most likely to consider reliability the most important remittance factor. Informal (25.3 percent), cash (25.2 percent), and digital methods (23.9 percent) have the largest portions of respondents claiming cost is the most important factor in making remittance decisions.

Cost remains the primary factor discussed in policy circles (MacIsaac 2021). Leading international initiatives, such as the Sustainable Development Goals or the Global Compact for Safe, Orderly and Regular Migration, focus on lowering formal channel transfer costs. Remitters most frequently remitting via digital transfer systems, cash transfers, or informal channels are the most likely to identify the cost of remitting as their primary factor influencing remittance choices. Table 3 also provides the average remittance fees remitters paid, but only for their last transfer. 4 Note that cash carries no explicit cost. 5

Recipient convenience and sender convenience are other central factors included in the SIMT. Respondents who value recipient convenience tend to favor in-person MTOs and informal channels. 6 In contrast, respondents who identify sender convenience as their most important factor are most likely to remit through digital channels, and least likely to resort to informal or cash transfers.

Respondents are least likely to identify timeliness as the most important factor influencing their remittance decisions. Respondents most frequently using in-person MTOs are likelier to report timeliness as an important factor. Meanwhile, those most frequently remitting via informal channels are the least likely to list timeliness as their top consideration.

Financial Literacy and Remittance Knowledge

Lower financial literacy and digital literacy remain significant obstacles for certain remitters to access formal transfer methods (Sander 2004; Pieke, Van Hear and Lindley 2007). This could partially explain the reliance on informal methods among less financially or digitally literate migrants with lower access to forms of formal finance. It could also explain why in-person MTOs continue to dominate the remittance market since, despite higher average fees, they are a more readily available form of formal transfer.

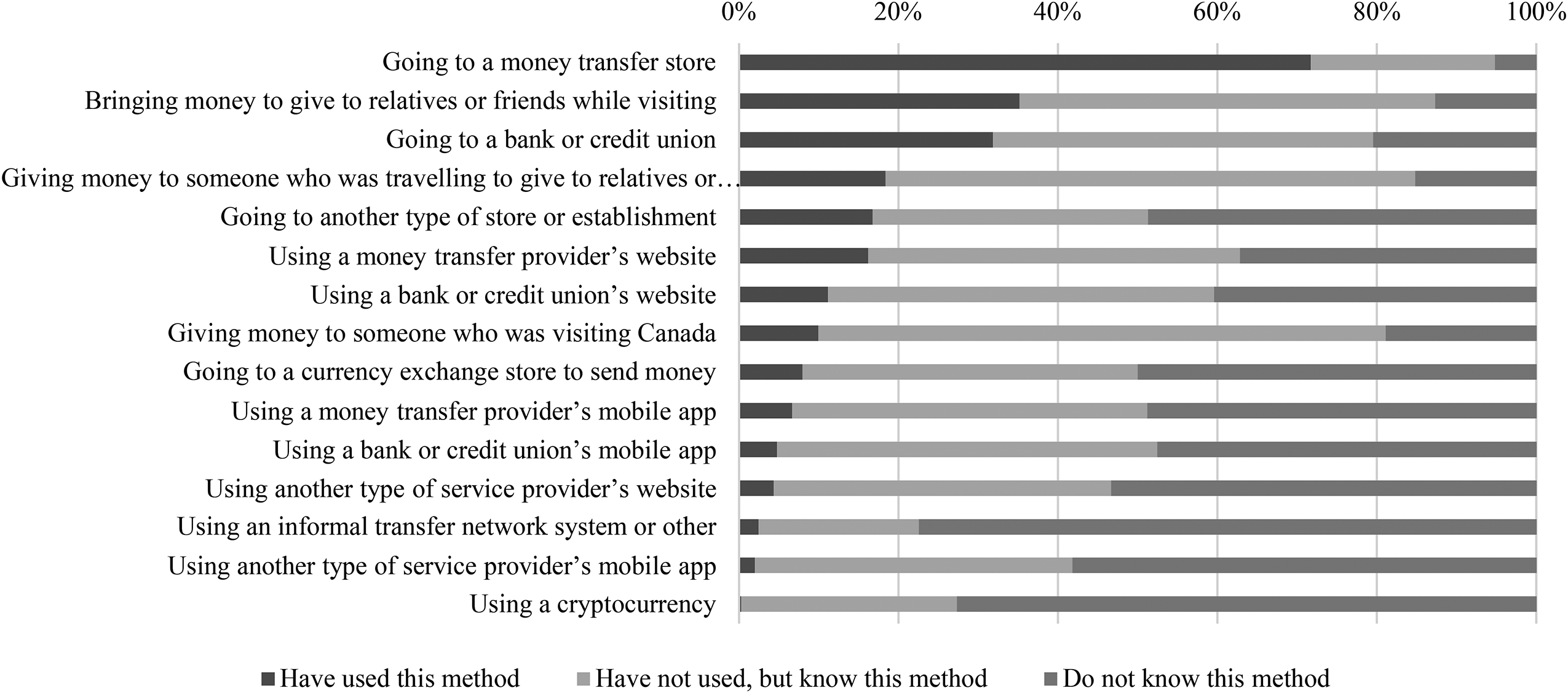

Figure 2 provides descriptive statistics of migrants’ awareness and knowledge of available transmission methods. Migrants’ remittance channel knowledge and usage are lowest for cryptocurrencies, informal networks, and numerous digital apps to transfer funds. In contrast, migrants’ usage and knowledge of in-person MTOs, cash, and bank and credit union transfers are substantially higher.

Knowledge and awareness of remittance alternatives. Source: SIMT.

Informality of the Recipient Country as a Determinant of Channel Selection

While highly informal remittance recipient economies may attract larger informal flows, they could also attract higher volumes of certain formal competitors. This section provides summary statistics of remittance modality choices by the recipient country's informal sector size. It shows that highly informal destination countries favor informal and competing formal channels, particularly in-person MTOs.

Informality is measured using Medina and Schneider's (2018) estimates of the “shadow” economy (i.e., the size of the informal sector as a proportion of GDP). Given that informality is stable across countries and years (Medina and Schneider 2018), estimates for 2015 are used.

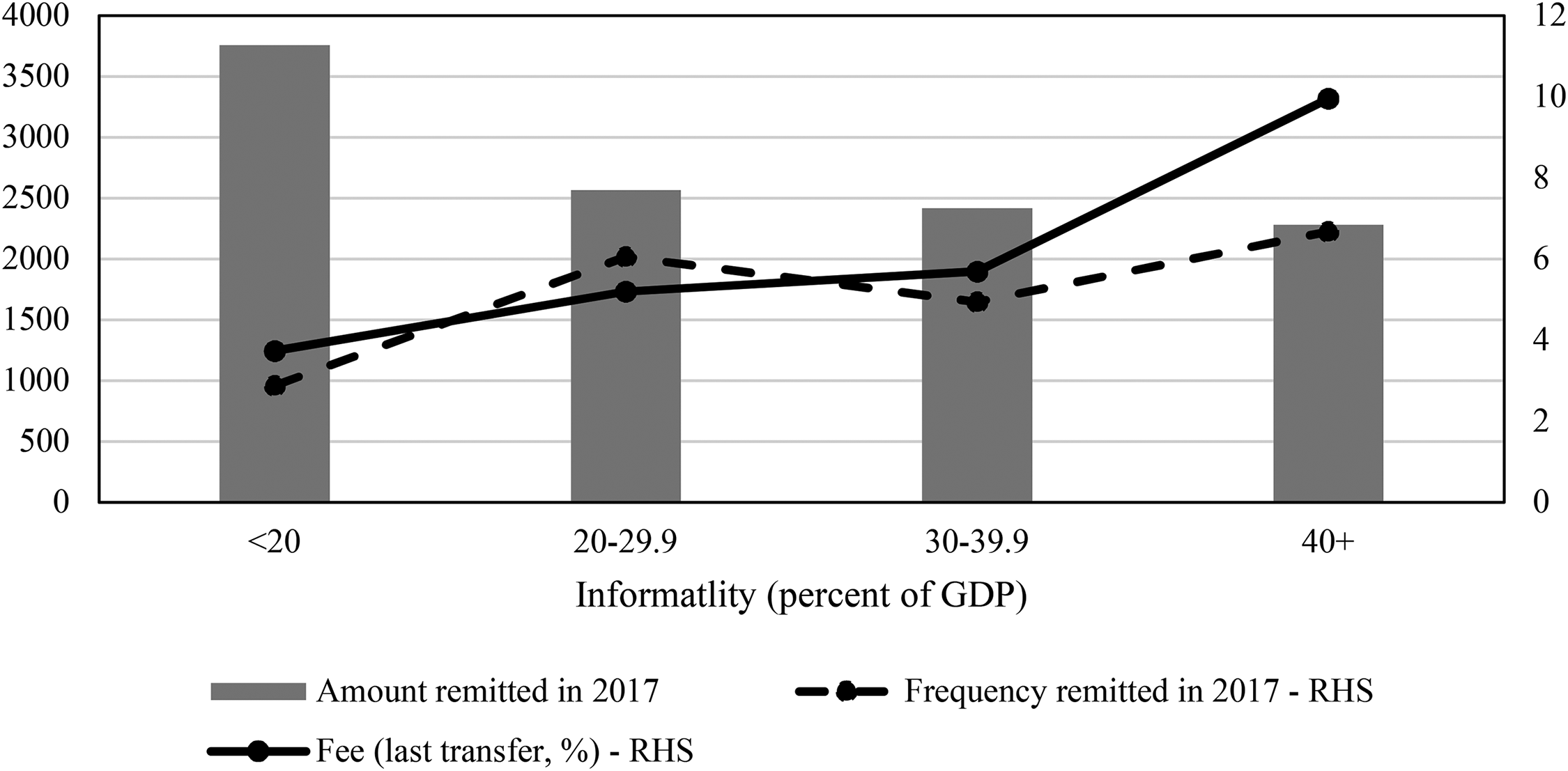

Figure 3 provides a breakdown of remittance frequency, amount, and transfer costs by the destination country's informal sector size. Highly informal regions that receive remittances from Canada tend to have higher mean prices (across informal and formal channels). This is likely largely attributable to smaller amounts sent per transaction at higher frequencies (i.e., lower economies of scale). Moreover, informal economies tend to receive smaller annual remittance values; however, this could also capture an income effect since informality is higher amongst low-income countries.

Remittance characteristics by destination country shadow economy size. Sources: SIMT and Medina and Schneider (2018).

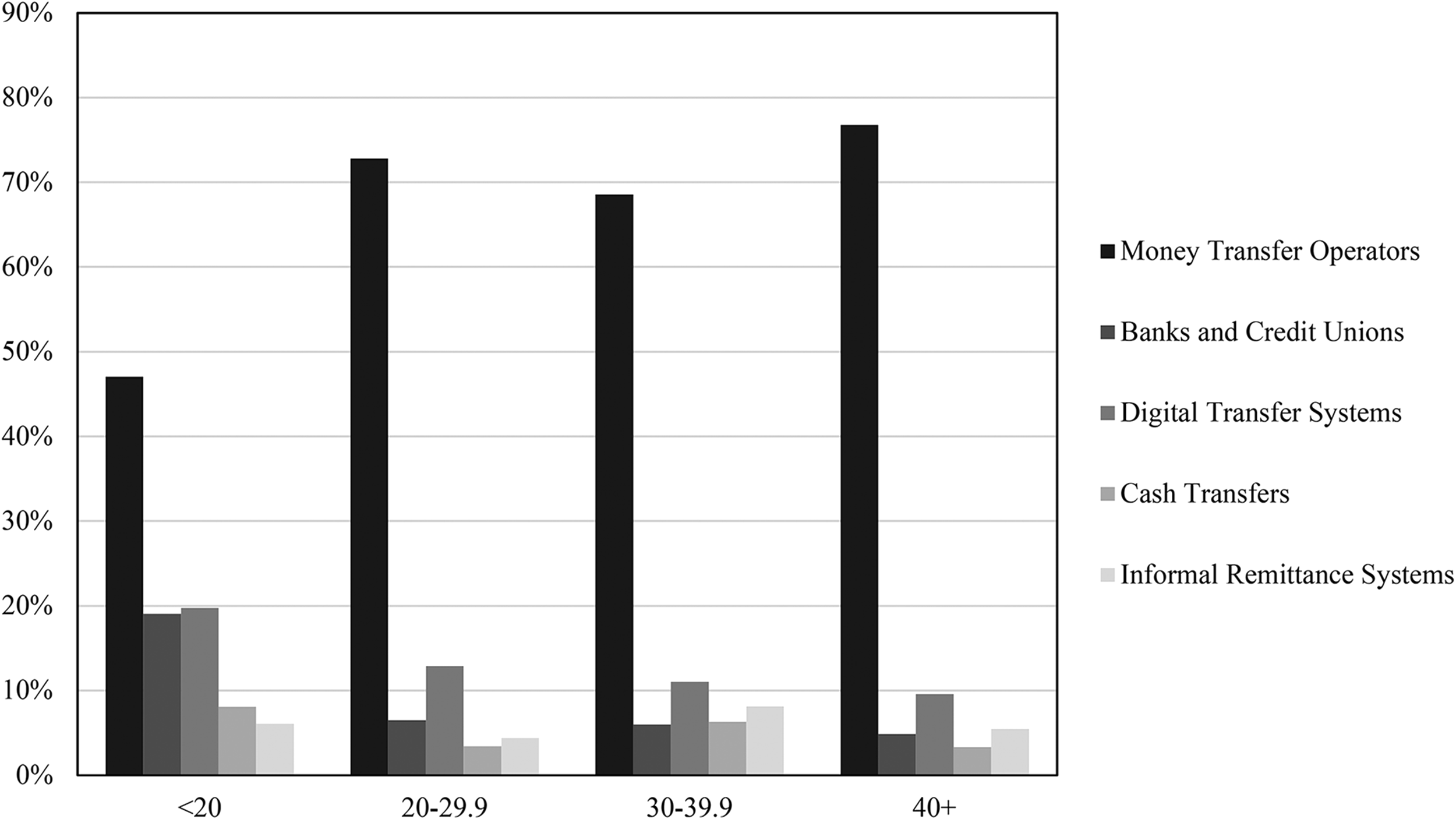

Regardless of the recipient country's informal sector size, remitters are most likely to use in-person MTOs. Moreover, MTO market share correlates positively with informal sector size. Canadian remittance outflows to informal regions (i.e., countries where the informal sector is estimated to represent 40 percent of GDP or more) gravitate towards MTOs first, followed by informal channels, digital transfer methods, and in-person banks and credit unions. Figure 4 depicts how informal channel usage is not exclusive to highly informal countries.

Channel choice by destination country shadow economy size. Sources: SIMT and Medina and Schneider (2018) Note: Informality as a proportion of GDP estimates (in percentages) on the horizontal axis are obtained using Medina and Schneider's (2018) estimates of the shadow economy based on countries' fiscal burden, institutional quality, economic openness, unemployment, and other control variables.

Data Limitations and Potential Biases

Remittance outflows from Canada predominantly travel via formal channels. While not entirely surprising given the higher levels of financial access in Canada, questions remain regarding measurement bias and the possibility of undercounting informality. Informal channels are certainly subject to additional measurement challenges, seeing that they are innately more obscure by virtue of their unofficial and unregulated status (IMF 2009). Two main potential sources of respondent biases stand out: desirability bias and selection bias.

Desirability Bias

In this study, desirability bias refers to migrants’ fear of government reprisal or immigration consequences based on migrant status or how they remit abroad. A type of response bias, desirability bias corresponds to respondents’ predisposition to appear as only remitting through formal means. This is particularly notable in the case of government officials interviewing migrants.

Although such a bias may exist, informal remittance channels are not inherently illegal. Moreover, none of the survey respondents in the sample are undocumented since undocumented migrants to Canada are not part of the sampling frame.

Selection Bias

Selection bias limitations stem from the SIMT data's non-observation of undocumented migrants, who are typically more likely to use informal means (Siegel and Lücke 2013). Given that the SIMT excludes undocumented migrants from the sample, this bias could lead this study to overstate findings regarding the low usage of informal methods in Canada.

Despite this limitation, two main arguments justify the validity of the findings. First, including undocumented migrants would impair the study's ability to have a weighted random sample broadly generalizable to the Canadian immigrant population born in ODA-eligible countries. A random sample of undocumented migrants is not feasible given the unavailability of a suitable survey frame.

Second, Canada's undocumented population is relatively small, limiting this potential bias's overall effect. Albeit dated, the 2003 Report of the Auditor General of Canada states that “the gap between removal orders issued and confirmed removals has grown by about 36,000 in the past six years” (Office of the Auditor General of Canada 2003).

Methodology

The analytical methods used in this study resemble those of previously cited empirical studies (Amuedo-Dorantes and Pozo 2005; Karafolas and Konteos 2010; Siegel and Lücke 2013; Kosse and Vermeulen 2014). Using multinomial logistic regressions, the model studies respondents’ most frequently used channel in 2017. Individual remitters (i) have the choice between five aggregate channels (j): in-person banks or credit unions (j = 1), in-person MTOs and stores (j = 2), digital mechanisms including all apps, websites, or cryptocurrencies (j = 3), cash carried by oneself or visiting relatives (j = 4), and cash carried by others, informal methods, and other methods (j = 5).

Individual i has the choice between five channels where

Amuedo-Dorantes and Pozo (2005) discuss the possibility of a simultaneity bias. In addition to the amount sent influencing remittance channel choices, the cost structure of individual channels also influences the amount sent. For instance, a remitter may want to remit more at a time, albeit less frequently, if considerable economies of scale exist within a discrete step structure (refer to Section 3 for details). Such a bias would violate the validity of the proposed model.

Although there is little to no evidence of discrete pricing structures across modern Canadian remittance channels, additional checks were conducted replicating Amuedo-Dorantes and Pozo's (2005) simultaneity correction estimation. The results show minimal changes across models, suggesting dual causation is improbable. This finding also aligns with Kosse and Vermeulen's (2014) suggestion that such simultaneity biases are less problematic when studying annual remittance amounts as in this study.

Results

The Determinants of Remittance Modality

Table 4 outlines the multinomial logistic regression results with respondents’ most frequently used channel as the dependent variable. This maximum entropy model is ideal when comparing the relative likelihood of selecting any given channel over any other, holding all other explanatory variables constant. As previously noted, the coefficients of multinomial logistic regressions are relative risk ratios.

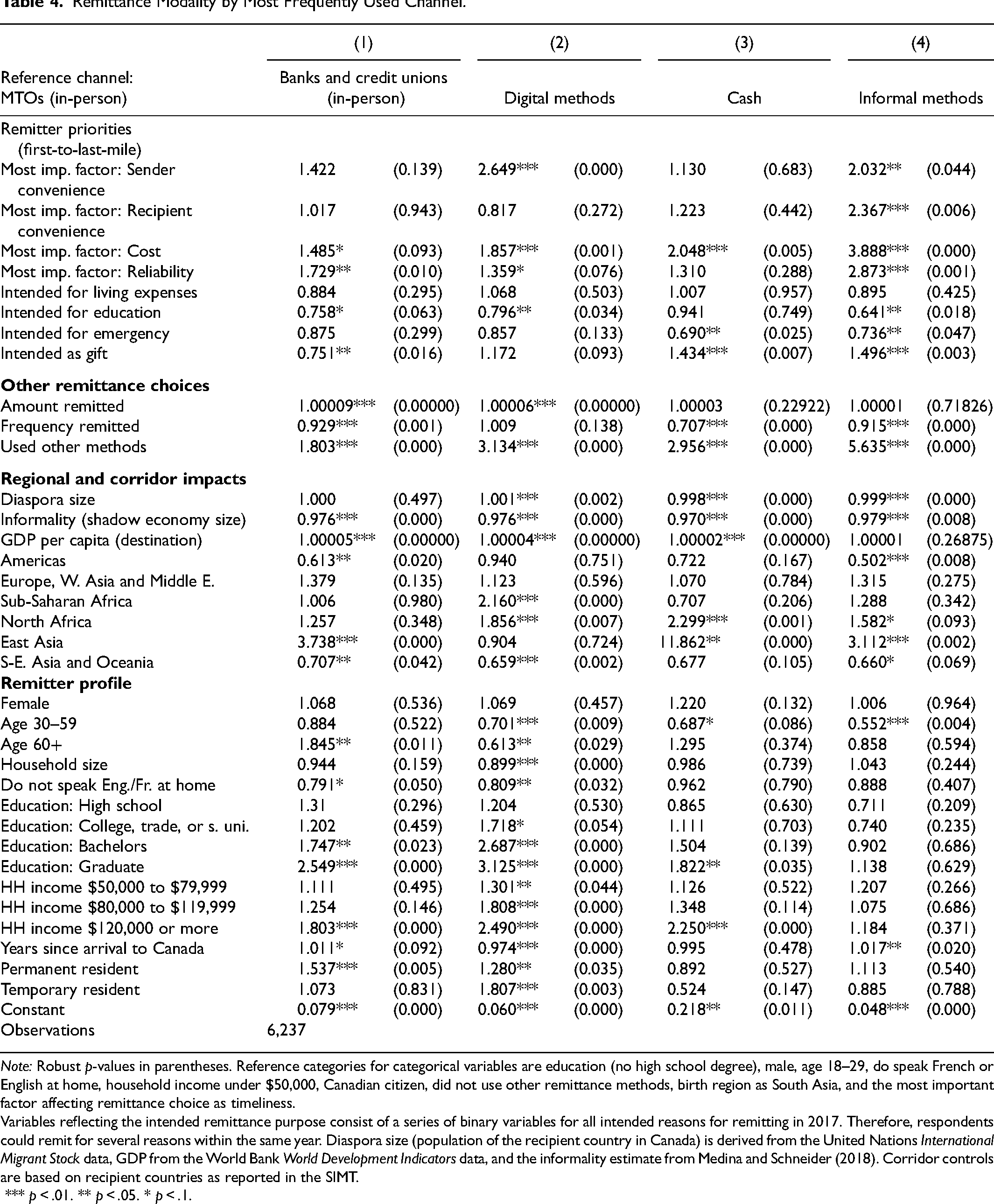

Remittance Modality by Most Frequently Used Channel.

Note: Robust p-values in parentheses. Reference categories for categorical variables are education (no high school degree), male, age 18–29, do speak French or English at home, household income under $50,000, Canadian citizen, did not use other remittance methods, birth region as South Asia, and the most important factor affecting remittance choice as timeliness.

Variables reflecting the intended remittance purpose consist of a series of binary variables for all intended reasons for remitting in 2017. Therefore, respondents could remit for several reasons within the same year. Diaspora size (population of the recipient country in Canada) is derived from the United Nations International Migrant Stock data, GDP from the World Bank World Development Indicators data, and the informality estimate from Medina and Schneider (2018). Corridor controls are based on recipient countries as reported in the SIMT.

*** p < .01. ** p < .05. * p < .1.

Most Important Factor Identified by the Remitter

In line with the first-to-last mile theoretical framework, modality choices vary following six main factors.

First, respondents reporting sender convenience as the most important factor affecting their remittance decisions are more than twice as likely to opt for digital or informal methods than other channels. In contrast, sender convenience is not statistically significant given the choice between in-person bank (or credit unions), cash, and in-person MTO transfers.

Second, selecting recipient convenience as one's preferred factor indicates respondents are 2.37 times as likely to select informal methods compared to in-person MTOs (reference category). Meanwhile, other channels are not significantly different from the reference channel for recipient convenience. This result aligns with other findings that informal remittances can carry advantages in terms of accessibility and anonymity that may favor recipient convenience (Kapur 2005; Pieke, Van Hear and Lindley 2007).

Third, reliability is the favored factor for those remitting using in-person bank (or credit union) transfers, digital methods, and especially informal methods. As the most common factor selected by survey respondents, one can interpret reliability as analogous to perceptions of trust in a specific channel. Remitters identifying reliability as the most important consideration when remitting are nearly three times as likely to select an informal channel over in-person MTOs.

Fourth, the intended purpose of remitting captures remitters’ perspective on recipient needs and how this impacts remitters’ modality choices. As shown in Table 4, respondents who report the intention of covering recipients’ emergency expenses are less likely to select cash and informal methods (31 and 26.4 percent, respectively) than in-person MTOs.

Fifth, although timeliness acts as the reference category, those that select timeliness as the most important remittance decision factor tend to gravitate towards in-person MTOs (refer to Table 3).

Finally, the cost factor is essential. Respondents claiming to be sensitive to costs are the least likely to use in-person MTOs. Remitters indicating transfer cost is the most important factor when remitting are almost four times as likely to choose informal methods, twice as likely to choose cash transfers, and respectively 85.7 percent and 48.5 percent more likely to select digital methods or in-person banks (or credit unions) compared to in-person MTOs.

Recipient Region Characteristics and Informality

The size of a recipient country's informal sector matters for remittance modality choices. Surprisingly, in-person MTOs are the most likely channel used by those remitting to more informal countries. Remitters are 2 percent less likely to use informal methods for every percentage point increase in the recipient country's informal economy as a proportion of GDP compared to in-person MTOs. Moreover, the size of the recipient economy's informal sector is only marginally less likely to impact digital channel and in-person bank (or credit union) use.

The destination country's diaspora size in Canada and its GDP per capita also influence remittance modality. Though larger diaspora in Canada is more likely to use digital remittance channels, it also correlates with a decrease in cash and informal channel use. Filipino, Chinese, and Indian immigrant remitters are the primary drivers of this result, among other significant corridors. One possible explanation is that all three countries retain exclusivity arrangements (i.e., contract clauses for MTOs and local partners), which could prevent numerous remitters in Canada from sending funds via other channels (IOM 2019). Migrants remitting to countries with a higher GDP per capita tend to favor in-person bank and credit union transfers, digital channels, and cash over in-person MTOs or informal channels.

Results in Table 4 show several corridor-specific trends. Most notably, migrants born in East Asia are almost 12 times as likely to remit using cash and more than three times as likely to remit using in-person bank (or credit union) transfers or informal methods than in-person MTOs or digital channels. Other groups with proclivities for channels other than in-person MTOs include North African-born migrants (who are more likely to choose digital, cash, or informal channels) and Sub-Saharan African-born migrants (who are more likely to choose digital channels).

Remitter Demographic and Socioeconomic Profile

Linking remitter profiles to channel preferences is important for more targeted policies. Highly educated and higher-income households favor in-person banks and credit unions, digital methods, and cash to remit. The use of cash by more educated remitters is possibly attributable to frequent trips to, or visits from, the “home” country like in other comparable studies (Karafolas and Konteos 2010; Siegel and Lücke 2013). Regrettably, the absence of data on return trips means this cannot be confirmed.

Age, duration of stay in Canada, and immigration status also matter for channel choice. Prime working-age (30–59 years) remitters are more likely to opt for transfers via in-person banks (and credit unions) and MTOs. In contrast, younger remitters are more likely to resort to digital mechanisms. Interestingly, those having spent the most years in Canada are more likely to use in-person banks (and credit unions) and informal methods to remit, and temporary residents favor digital channels over all other remittance methods. Those reporting to speak English or French at home are most likely to use in-person bank (or credit union) or digital channels to remit.

Factor Preferences by Demographic and Socioeconomic Status

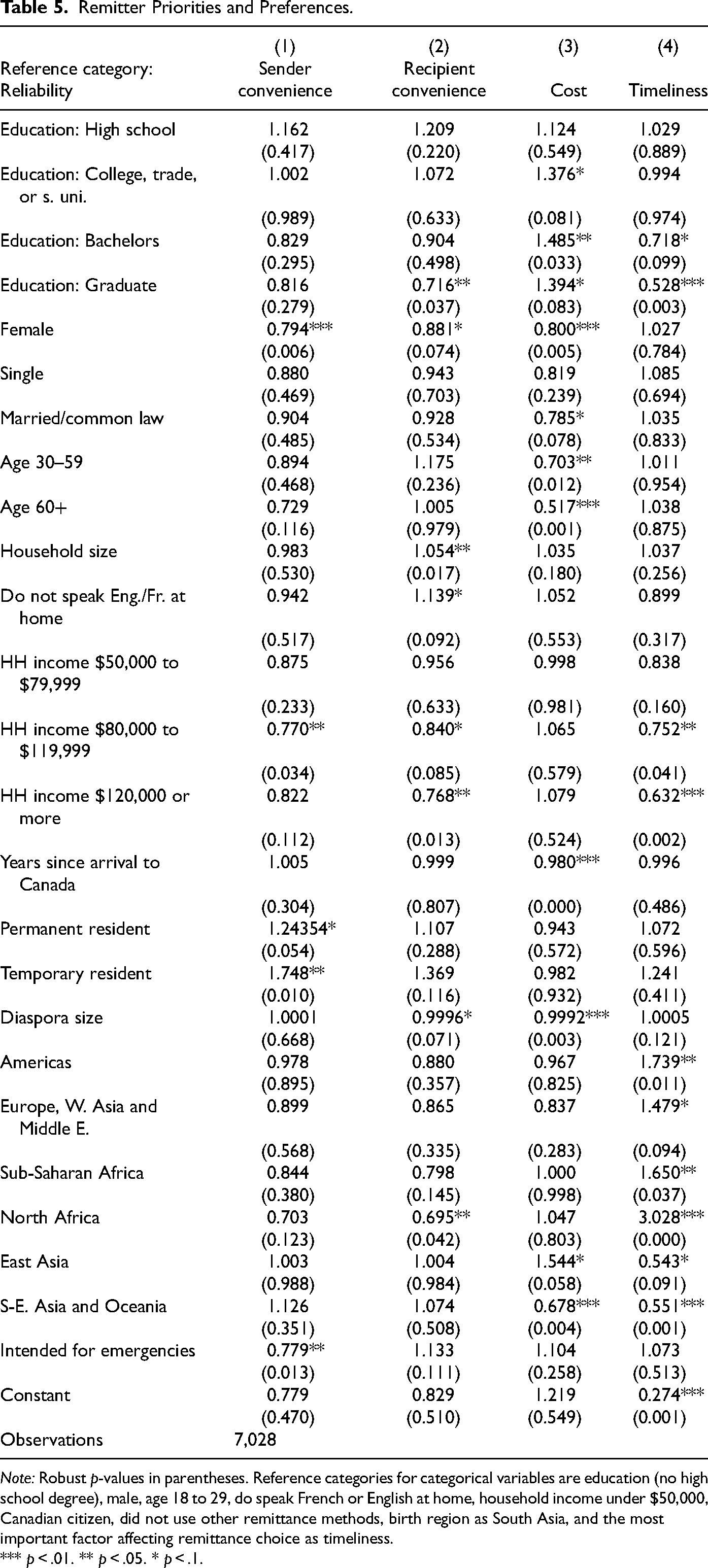

Factor preferences are critical to better understanding remittance modality choices. Table 5 links important factors influencing remittance decisions to respondent demographic and socioeconomic characteristics using a multinomial logit model (with reliability as the reference category). Differences in the number of observations between Tables 4 and 5 are attributable to varying response rates across variables in each model.

Remitter Priorities and Preferences.

Note: Robust p-values in parentheses. Reference categories for categorical variables are education (no high school degree), male, age 18 to 29, do speak French or English at home, household income under $50,000, Canadian citizen, did not use other remittance methods, birth region as South Asia, and the most important factor affecting remittance choice as timeliness.

*** p < .01. ** p < .05. * p < .1.

Sender Characteristics Impacting the Importance Allocated to Each Priority

Table 5 shows that higher degree attainment and household incomes correlate with a higher sensitivity to cost and reliability relative to other factors. Education is assumed to act as a proxy for financial literacy, meaning more educated individuals are likely more aware of alternate remittance methods and cost differences across channels. As for income, remitters from higher-income households remit more on average and are more likely to identify reliability and cost, and to a lesser extent sender convenience, as their most important remittance considerations.

Other important remitter characteristics include gender, age, immigration status, and language skills. Female respondents are 20 percent less likely to select cost or sender convenience as their most important remittance decision considerations. Instead, the average female remitter favors recipient convenience, reliability, and timeliness. Regarding age, younger remitters are likelier to list cost as the most important factor influencing their decision. At the same time, those aged over 60 are less likely to choose sender convenience as a determining factor. The longer migrants spent time in Canada, the lower their propensity to favor cost and timeliness factors. In contrast, temporary residents are more likely to select sender convenience, timeliness of transfer, or recipient convenience as their most important factor when remitting. Lastly, those who do not speak English or French at home tend to favor recipient convenience.

The Impact of Urgent Needs on Factor Importance

Another important consideration is the impact of urgent needs and emergencies on remitter priorities. When migrants remit funds (or a portion of the total funds) to help during crises, remitters are less likely to select sender convenience as the most important factor impacting remittance decisions (22 percent lower likelihood than other factors). Despite weak statistical significance (p-value of 0.11), results suggest that those sending remittances intended to aid recipients in emergencies are 13 percent more likely to identify recipient convenience as the most important decision factor.

Conclusion

The main objectives at the onset of the article were to unpack the frequent remittance dichotomization between formal and informal channels and to explore the key determinants of channel choice. Four main points summarize the bottom-line findings. First, remittance channels operate distinctly, including within broad formal and informal categories of channels. Second, lack of recipient financial access and convenience are important factors underlying informal channel use. Third, cash operates quite distinctly from other informal channels in Canada, unlike in several other jurisdictions. Fourth, a larger informal sector in the recipient country favors informal channel use and specific formal channels such as MTOs.

This study demonstrates that convenience, knowledge and financial literacy, transfer costs, channel reliability, transfer timeliness, and recipient needs influence remittance modality choices. The first hypothesis linking these factors to the first-to-last mile model is fundamental in distinguishing channel use. Like Kosse and Vermeulen (2014), this article demonstrates that remitters gravitate towards informal channels and MTOs based on lower transfer costs.

These modality-determining factors also help understand the selection process between competing formal channels. Although differences between banks and MTOs matter little when using their respective digital service variants, the differences between digital, in-person banks (and credit unions), and in-person MTO transfers matter. Existing research and data scantly address the rise in digital transfer mechanism choices and their evolving characteristics (Dimbuene and Turcotte 2020).

One key contribution of this article is the disaggregation of cash from informal methods, and how this relates to Canada's geographic isolation from recipient countries. Canada's isolation from the developing world means its hand-carried remittances must travel longer distances and incur higher travel costs. From a policy perspective, cash hardly appears to take on the same role as viajeros crossing the US–Mexico border or other informal methods reliant on proximate border crossings. Consequently, cash transfers operate quite distinctly from informal methods. Unlike in several other jurisdictions, cash is primarily an opportunistic option for remitters in Canada. SIMT data suggest that highly educated individuals and high-income earners often resort to cash out of convenience when visiting abroad or receiving visitors. This finding aligns with Siegel and Lücke (2013) and Kosse and Vermeulen (2014), who find that cash has distinct properties. This is especially true when remitters travel back to their home country (or receiving relatives) and use cash out of convenience given that travel costs are already covered (i.e., a sunk cost), substantially reducing transfer costs.

Another contribution includes clarifying the potential influence of the recipient country's informal sector size on remittance mode selection. The findings nuance the notion that a larger informal sector in the recipient country favors informal channel use. Destination countries with larger informal sectors are more likely to resort to MTOs than informal methods in the case of Canadian remittance outflows. The prevalence of MTO use is likely due to their cash pickup or delivery options. Such options make remitted funds readily available to recipients regardless of their access to banking and other forms of formal finance.

From an international development standpoint, evidence in this article suggests that more vulnerable migrants often use informal channels to remit. Furthermore, in the destination country, numerous remittance recipients lack access to formal financial intermediaries that act as alternatives to informal channels. Given international efforts to discourage informal channel use (MacIsaac 2021), the reliance of vulnerable remitters and remittance recipients on informal channels casts doubts on the benefits of such remittance formalization policies. Moving forward, there should be a greater emphasis on the equitable impacts of remittance formalization goals.

Footnotes

Acknowledgements

This research benefited from the valuable comments and suggestions of Dane Rowlands, Meredith Lilly, David Carment, Ravi Pendakur and Krishna Pendakur. I also wish to thank the two anonymous reviewers and the Editor for their helpful comments. Any remaining errors are my own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by funds to the Canadian Research Data Centre Network (CRDCN) from the Social Sciences and Humanities Research Council (SSHRC), the Canadian Institute for Health Research (CIHR), the Canadian Foundation for Innovation (CFI), and Statistics Canada. Although the research and analysis are based on data from Statistics Canada, the opinions expressed do not represent the views of Statistics Canada. Social Sciences and Humanities Research Council of Canada, (grant number 767-2017-1776).