Abstract

Renewable energy installations are rapidly gaining market share due to falling technology costs and supportive policies. Meanwhile, the energy price crisis in 2022 shifted the energy policy debate toward the question of how consumers can better benefit from the low and stable generation costs of renewable electricity. Long-term contracts for renewable energy to link producers and consumers are an option to address these concerns. Various market failures limit the potential for bilateral contract structures between power producers and consumers. Hence, we assess the option of a government-backed Renewable Energy Pool which tenders long-term contracts with new renewable projects and passes the pooled contracts on to consumers who thereby benefit from reliably lower-cost electricity supply. We assess the effect of the measure on producers and consumers of clean electricity, as well as the incentives for investing in flexibility options.

Keywords

1. Introduction

The European energy crisis in 2022 has sparked a debate about how the European electricity market design can support the accelerated expansion of renewable energy and contribute to affordable energy expenditures for consumers. While short-term electricity markets should provide price signals to market participants (e.g., by raising prices in times of scarce gas supply), 1 the existing markets have proven insufficient to hedge consumers against such price spikes and to minimize investment risks and financing costs for producers. (Battle et al. 2023; European Commission 2023; Fabra 2023).

These developments raise the question of how long-term contracting arrangements can be developed to provide the necessary hedge for producers and consumers, such that the level and volatility of consumers’ electricity expenditures are reduced. Long-term contracts should provide an attractive investment framework to realize the renewable deployment targets while enhancing the effectiveness of the power market in supporting investment and the use of clean flexibility options (e.g., demand side response or storage). Two basic options that connect the producer with the consumer side are being discussed in this context. First, bilaterally agreed long-term contracts between wind- and solar projects on the one side and energy companies or large electricity users on the other side, typically structured as so-called “power purchasing agreements” (PPAs). Second, what we refer to as a “Renewable Energy Pool” (from here on: “RE-Pool”), which tenders long-term contracts with and passes the pooled provisions to consumers.

The RE-Pool comprises three elements: The tender of long-term contracts for new wind- and solar projects, the pooling of these contracts, and the passing on of these provisions to consumers. First, for producers of renewable energy, the RE-Pool provides long-term contracts to remunerate new wind and solar power projects. Usually, this is based on financial contracts as hedging instruments, referred to as contracts for differences (from here on: “CfD”), for each installation that is tendered by a government agency. In a second step, the agency then combines all individual government-backed long-term contracts into a contract with the aggregate profile of the total renewable production in a region, the so-called “Renewable Pool.” In a third step, consumers are awarded a share of the pool that is allocated to final electricity consumers (e.g., industry, private households). For these consumers, the RE-Pool provides a hedge against fluctuating power prices for the generation volume according to the generation profile of the RE-pool, without diluting energy price signals on short-term markets. There are different ways of allocating access to the pool, including pro-rata among all consumers, auctions, and administrative decision for preferred groups (e.g., vulnerable consumers or companies engaged in transition activities). For governments, the pool is budget-neutral, except in situations of correlated contract defaults.

The suggestion of an RE-Pool builds on several policy instruments that have emerged in recent years. First, it relates to the literature on the design of contracts for differences that provides a two-sided derisking for renewable energy projects (Fabra 2023; Kröger, Neuhoff and Richstein 2022; Newbery 2023; Schlecht, Hirth and Maurer 2023) and the wider discussion on the efficient design and allocation of renewable energy policies (Abrell, Rausch and Streitberger 2019; Grubb and Newbery 2018; Haufe and Ehrhart 2018; Lehmann and Söderholm 2018; Petitet, Finon and Janssen 2016). Second, concerning the pooling of renewable energy generation, it relates to a proposal by Grubb, Drummond and Maximov (2022) of a so-called “Green Power Pool.” It differs from this proposal by structuring the hedging payments as a financial hedge rather than as a physical delivery. Finally, it relates to the debates about how to allow consumers to benefit from stable generation costs of renewable energy in light of the energy price crisis triggered by the Ukrainian-Russian war (Battle, Schittekatte and Knittel 2022; Fabra 2022; Polo et al. 2023; von der Fehr et al. 2022; Zachmann and Heusaff 2023) and on how renewable energy policies affect the welfare of electricity consumers (Neuhoff et al. 2013; Newbery 2023; Pahle et al. 2017).

The RE-Pool offers several benefits over both bilateral private agreements and one-sided derisking policies (e.g., the German sliding premium). First, it supports the deployment of renewable installations at the speed required to reach policy targets. In contrast, the capacity of utilities and energy-intensive consumers to underwrite purely bilateral long-term contracts without endangering their credit ratings is limited even though it would provide a hedge for electricity prices of companies investing in electrification. Hence, a policy design focused on bilateral private contracts will not be able to back the renewables expansion at a sufficient speed. Second, an RE-Pool has the potential to reduce renewable energy costs by keeping financing costs low as compared to the counterfactual of a PPA-driven deployment or maintaining the historic approach of sliding market premia in some European markets into the future (Neuhoff, May and Richstein 2022). Third, based on recent data including the energy crisis era, we illustrate that an RE-Pool is effective at considerably reducing energy expenditure volatility and providing green power delivery for off-takers. Finally, since the RE-Pool is a partial hedge against price fluctuations, it sets incentives to acquire additional flexibility contracts (or realize the flexibility potential of off-takers) that complement the renewable profile, to fully hedge price risk and by doing so unlocking flexibility investments. Overall, the RE-Pool solves the market failure arising from the mismatch between the contract lengths required by renewable energy investors and the ability of consumers to sign such bilateral long-term contracts, as well as reducing the costs of the energy transition through reduced generation costs.

The remainder of the paper is organized as follows. In the second section, we motivate the need for an RE-Pool. In the third section, the key design elements of contracts for differences for renewable energy are discussed and their aggregation into a pool is presented. The fourth section discusses the benefits that the RE-Pool would have for consumers and producers. The fifth section presents a numerical analysis of the compatibility of the policy with common flexibility options. The sixth section concludes.

2. Motivation

2.1. The Need for Long-term Contracts

Project developers require long-term contracts to finance wind- and solar projects. This is because the power prices expected over the next twenty years are highly uncertain and, hence, the revenue from wind- and solar-power plants is equally uncertain over this time horizon. 2 Consequently, it is not possible to access low-cost debt finance with such uncertain revenues (Gohdes, Simshauser and Wilson 2022). Relying largely on equity to fund projects would strongly increase renewable costs because financing costs and, hence, costs of delivering energy might double. Thus, project developers require long-term contracts that secure the price at which the project can sell electricity to secure financing (Neuhoff, May and Richstein 2022). At the same time, industrial companies are increasingly interested in reducing the volatility of their power purchases, especially when investing in transformative projects that often involve electrification and increase the relevance of electricity costs for profitability (Richstein and Neuhoff 2023).

Therefore, long-term contractual arrangements should be designed symmetrically to simultaneously secure power producers against the risk of low prices and energy consumers against the risk of high prices. As introduced before, bilateral private contracts (PPAs) between power producers and consumers as well as government-backed long-term contracts, are the two main options for such symmetric contracts. Given that both types of contracts can be structured in various forms, their main difference lies in their counterparty, which can be either the government or a private company, and the government’s ability to pass on the conditions to consumers. In theory, if bilateral private contracts and the publicly backed pool would deliver the required investment for reaching climate neutrality at the same speed and costs to consumers, constrained administrative capacities and risks of lock-ins would argue for purely bilateral contracts. However, a set of concerns relate to private bilateral contracts that justify, and would be solved through the public policy instrument of an RE-Pool.

2.2. Can Bilateral Private Contracting Address Current Energy Policy Objectives?

Historically, bilateral private contracts were primarily used to back investments that were small relative to overall demand, but now a far larger scale of funding is supposed to be backed by private PPAs. However, earlier analysis shows that the demand for PPAs from commercial consumers and energy companies will be insufficient to back the scale of wind- and solar investments required to reach the European renewable targets (May and Neuhoff 2019). Even when including short-term and post-subsidy 3 PPAs, which do not finance additional installations, the volume of the total corporate PPA market in Europe in 2022 was only 9 percent of the yearly additional capacity needed to reach the EU 2030 renewable energy targets (Pexapark 2023). This is because energy companies and commercial users take a large risk if they underwrite a PPA with a long contract duration, like twenty years. If the basis of customers of a retail company shrinks or the product price of a firm is set by competitors without long-term contracts, this leaves companies underwriting large volumes of PPAs with an open position whose value fluctuates with electricity prices in shorter-term markets (May and Neuhoff 2021). Therefore, a long-term contract for electricity poses a risk for these companies. Consequently, rating agencies in principle treat PPAs as imputed debt in their credit rating by adding a share of the value of the long-term contract to a company’s liabilities raising the debt-equity ratio (Baringa LLP 2013; Standard & Poor’s 2017). However, these long-term contracts are precisely what is needed for renewable energy investors to finance the development of new installations. Additional issues restricting the volume of private contracts are the counterparty risk that is present in bilateral agreements and the risk of price developments that leave firms exposed to overpriced contracts.

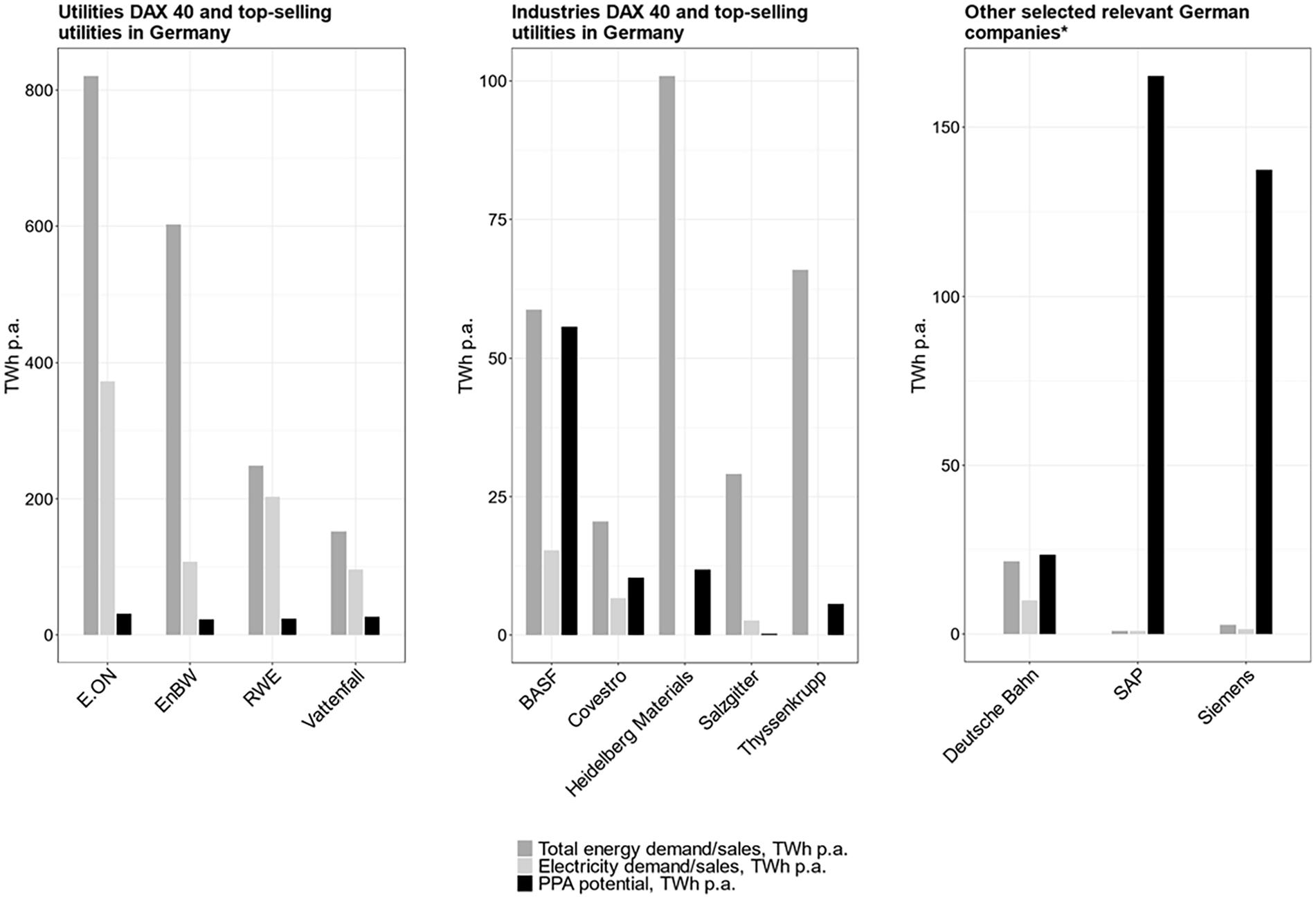

Figure 1 applies the methodology of rating agencies to assess the maximum scale of PPAs companies may be able to underwrite. 4

Estimated PPA volumes of major German companies.

We find that energy utilities can only underwrite PPAs at the scale of 4 to 18 percent of their energy demand. They could, in principle, get the PPAs “off their books” again, thus increasing the total scale of PPAs they can take on, if they were to sign corresponding long-term contracts with their consumers. Yet, only large industrial consumers can underwrite such long-term contracts with utilities or directly underwrite long-term PPAs. We find that large technology companies, like SAP or Siemens, can potentially underwrite long-term PPAs at the scale of their energy demand because their energy costs and, therefore, risk exposures are very small compared to their market capitalization. This is in accordance with international findings showing that six out of the seven largest off-takers of PPAs in the world between 2010 and 2020 were US-American technology companies (International Energy Agency 2022) which is similar to numbers from Europe where only a small number of industrial firms were among the largest off-takers of PPAs (Enervis 2023; Pexapark 2023). For energy-intensive industries, energy costs are high compared to margins, profits, and market capitalization (Wesseling et al. 2017). Hence, they are constrained in their ability to underwrite PPAs. In fact, they can only underwrite PPAs at the scale of 5 to 51 percent of their total energy need. 5 This leaves them exposed to electricity price fluctuations.

If all analyzed utilities as well as industrial and commercial consumers were to realize the maximum value of PPAs they could underwrite, this would still only allow for covering 30 percent of their energy needs (consumption weighted), far below the envisaged additional renewable investments for the coming years.

Additionally, in light of the experiences during the energy crisis, a prevailing expectation emerged that governments are tempted to intervene to protect firms against extremely high power prices (Brown, Eckert and Eckert 2017; Sirin et al. 2023). Such interventions are subject to constrained public budgets and hence inherently uncertain. When governments provide such insurance against high power prices for actors without long-term coverage, it reduces the incentives for commercial and industrial firms to engage in private long-term contracts. In this scenario, long-term contracts imply that companies expose themselves to the risk that their individual contracts are too expensive if prices fall in the future, but they may not benefit relative to their competitors if prices rise.

2.3. Scaling Renewable Investments: The Need for an Alternative Policy Framework

A renewable deployment strategy focusing on private bilateral contracts implies that many energy-intensive companies will be excluded from the potential benefits renewables can offer for price levels and hedging. They will thereby be limited in accessing green electricity that may be necessary to reach net-zero targets. Public guarantees for private bilateral contracts are being discussed but will not address this shortcoming, because a contract guarantee will only help the counterparty to the contract, for example, the renewable project, to deal with the limited creditworthiness of the industrial consumers. However, it will not address the financing implications of resulting misaligned timelines of price hedges for production inputs and products for the industrial consumer itself. Furthermore, public guarantees for private bilateral contracts would provide a safety net that could encourage irresponsible risk-taking behavior or even gaming by energy utilities and industrial companies (Polo et al. 2023). For instance, entrant energy retailers might underwrite a large quantity of government-secured PPAs and bet on rising electricity prices that allow them to undercut incumbents. Meanwhile, if wholesale prices turn out to be low, the company can dissolve, leaving the tax-payer with the difference between PPA and wholesale costs. Vice versa, a lack of sufficient demand for PPAs with long contract tenures would result in a delay of the renewable energy expansion, as well as higher financing and generation costs. This motivates the exploration of alternative market design options to address the hedging needs of producers and consumers.

3. A Renewable Pool of Long-term Contracts

Supporting the energy transition via government-backed long-term contracts would avoid the drawbacks of private bilateral long-term contracts. An RE-Pool allocating the contracts to consumers would provide a set of benefits for industrial and household consumers and the speed of RE deployment.

3.1. Designing the Underlying Long-term Contract

Government-backed long-term contracts and bilateral private contracts are established instruments for derisking investment into renewable energy installations. Public tenders have typically focused on the financial hedge, with ample experience in implementation of CfDs in countries such as France, Spain, Poland, and the United Kingdom. However, there remains a debate about the detailed design of the tender and contract. To allow for a consistent discussion of the combination with an RE-Pool for consumers, we assume the following design elements for contracts for differences and their tender: A government-mandated and secured agency tenders CfDs. Renewable projects offer a bid that reflects the strike price they desire in a CfD contract. The projects offering the lowest strike prices are granted CfDs. In the auction clearance, a bonus is applied to bids from installations that are system-friendly, for example, PV panels facing east or west (May, Neuhoff and Borggrefe 2015). Thus, the plant can win a contract even if it requires a somewhat higher strike price.

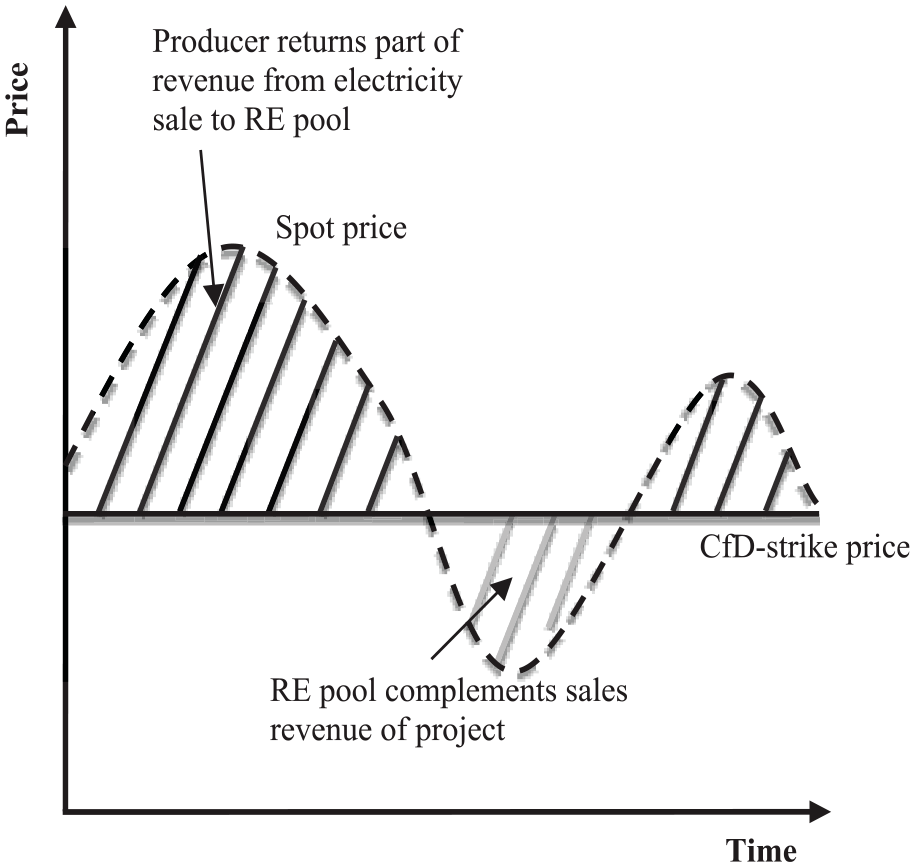

The CfD awarded to a wind- or solar-project hedges the project against power price volatility as shown in Figure 2. 6 When the actual power price for the reference period (fifteen-minute or hourly) interval is below the strike price, then the renewable project will obtain a payment for the difference corresponding to the price difference between the strike price and the reference price multiplied by its uncurtailed power production. The reference market is the day-ahead market in the bidding zone. 7 Symmetrically, if the power price exceeds the strike price, the renewable project pays back the difference to the government agency. Thus, the revenue level for the project is stabilized. To ensure the renewable project retains full incentives to respond to spot and balancing market prices, the payments under the CfD are not linked to the produced volume of energy in any fifteen-minute or hourly time interval where production is curtailed. Instead, in the case that production is curtailed due to zero power prices or balancing needs, the production used for remuneration is equal to the available active power that wind, and solar projects already calculate as the basis for remuneration in balancing mechanisms by several European transmission system operators (Elia 2021). The contract is tied to the operation so that, if the project changes ownership or the producer declares bankruptcy, the new owners of the plant would become party to the contract for difference.

Price hedging function of a CfD for renewable energy producers.

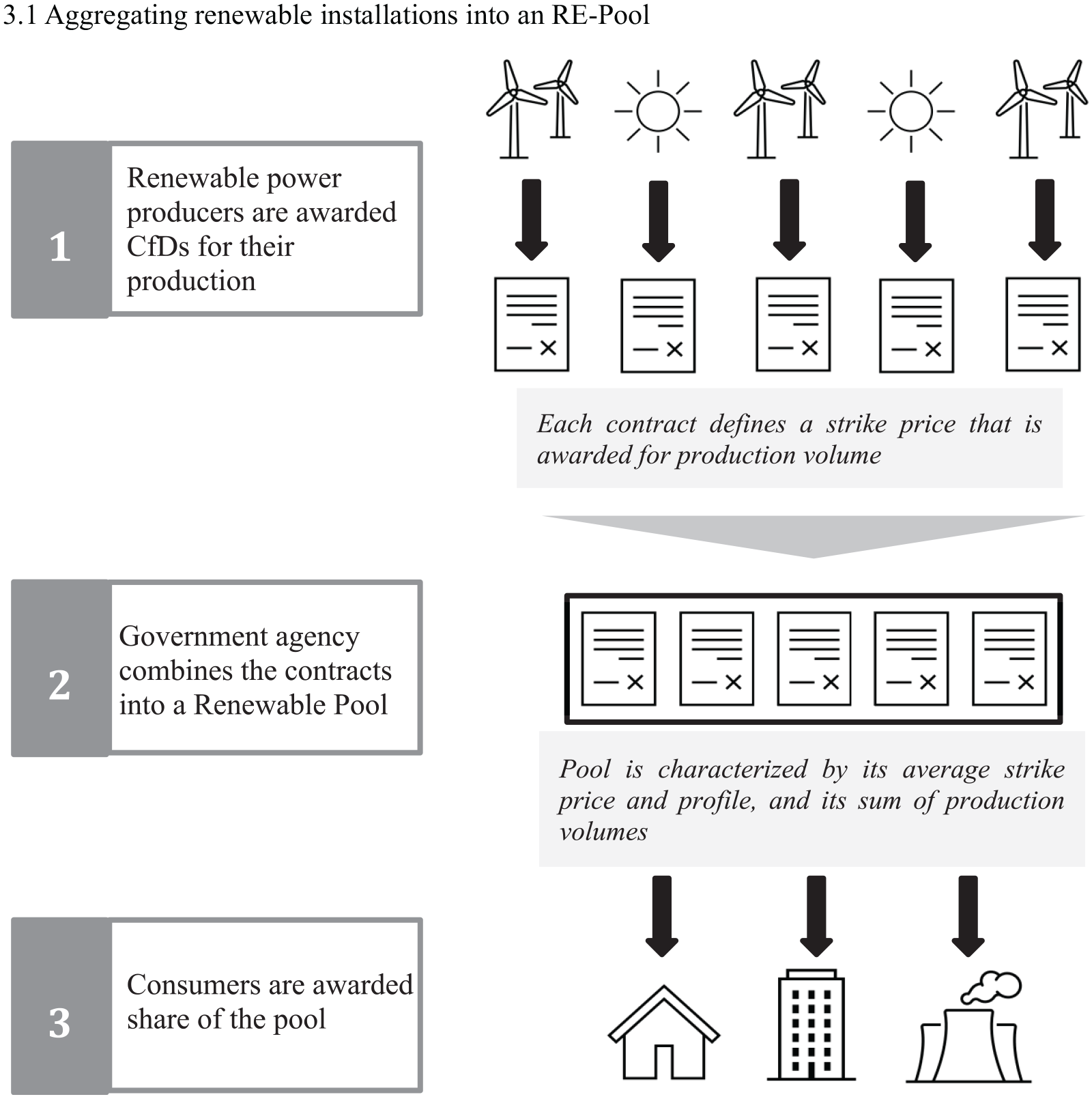

3.1. Aggregating Renewable Installations into an RE-Pool

The standardized structure of renewable energy support through CfDs allows the aggregation of contracts into a “Renewable Energy Pool” as is illustrated in Figure 3. The pool is defined by the sum of production capacities, the aggregated production profile, as well as the strike prices for producers and consumers. As more contracts from diverse wind and solar projects are combined, the production profile that is hedged will be more stable, and the more attractive the RE-Pool will be for electricity consumers.

Functioning of the RE-Pool.

The volume of the RE-Pool is defined by the aggregated generation potential of all installations in the pool. Based on statistics for wind- and solar generation for an average weather year, the expected annual power production volume for the pooled CfD is calculated. A consumer would obtain, for example, 1 MWh of the pooled contract for the average weather year. If the total contracts covered by the pool constitute 100 MWh, then the consumer effectively is hedged with 1 percent of each of the projects that are part of the RE-Pool.

The share of the RE-Pool that is granted to a firm or a retail company determines the revenue stream the electricity consumer will obtain or be liable for to hedge electricity costs. As the payments are independent from the realized demand of the consumer, they will not distort consumption choices, but preserve incentives that may result from, for example, real-time pricing. If, for example, electricity prices are high in a period, then the consumer is incentivized to reduce or shift electricity demand. The CfD payment for the period is not dependent on this consumption choice and, thus, should not result in distortions. Payments to consumers will coincide with times of higher power prices, subsequently reducing the level and volatility of electricity costs to consumers.

To realize the full benefit of a diversified portfolio and provide a standardized reference product for complementary investments into flexibility, all projects should be included in one RE-Pool, and projects in future years should also be added to the pool. Thus, the production profile gradually evolves with the type and location of additional renewables connected to the system. Further, the average strike price for renewable projects in the pool will evolve over time. The cost of new renewables will likely be lower as technology costs fall but might also rise, if less attractive sites must be used. This results in two different design options for consumer pricing. Consumer contracts with the RE-Pool could be set at the average strike price set by the renewables added to the pool in the specific year (so-called vintage prices). This would lock in precise hedging prices for consumers. Alternatively, consumer contracts with the RE-Pool could be set at the average price level of all renewables connected to the pool and might as a result be slightly adjusted over time. Importantly, in both approaches, the contracts for difference with the consumer is based on the production profile of all renewables in the pool. This standardized reference product will help catalyze the development of complementary forward products to unlock flexibility and hedge profile risks for consumers.

3.3. Allocation the RE-Pool to Consumers

Access to the RE-Pool will be attractive for consumers as it ensures reliably low electricity prices and a climate-neutral electricity supply. It can be expected that demand for such a product would be larger than the supply in situations where the additional supply of renewable energy is constrained by supply chain, land, and planning constraints. This raises the question of how access to the RE-Pool should be organized. In general, the RE-Pool could be allocated through a pro-rata approach, a prioritization for certain customer groups, or auctions.

First, the EU Commission has suggested allocating the revenues and costs from contracts for differences equally among all consumers based on their share of total electricity consumption (European Commission 2023). According to this principle, the allocation could be based on the consumers’ past consumption volumes (e.g., the average electricity purchased over the past three years). The RE-Pool would then reflect a growing share of electricity in each consumer’s hedging portfolio or in the portfolio of the retailer serving the consumer. This approach would have the benefits of being equitable and proof against lobbying and political capture.

Second, the RE-Pool could be allocated to prioritized consumer groups during the initial years, when the pool is still small. This would allow the government to address the needs of consumer groups that are more affected by higher energy price levels and volatility. Groups that could be considered for such a prioritization are vulnerable electricity consumers (i.e., low-income households with limited ability to invest in energy efficiency), energy-intensive companies and investors in transformative processes. Also, direct neighbors of renewable energy plants could be considered, to increase public acceptance of the energy transition. In the case of energy intensive companies and transformative investments the renewable profile ensures strong incentives for realizing flexibility options in the projects to contribute toward matching the demand profile with the renewable generation profile. This approach would, however, have to cope with the challenge of lobbying by interest groups for qualification as prioritized groups.

Third, the RE-Pool could be allocated to consumers through an auction on the supply side. Consumers would bid their willingness to pay for the electricity from the RE-Pool mirroring the auction on the supply side. In this case, a separate strike price on the demand side would be decided in the auction. While avoiding potential controversies in defining priority groups, it might raise the price of electricity for these—potentially vulnerable—consumers if demand exceeds supply, thereby increasing the costs of the energy transition. Additionally, it is unclear if consumers with the highest willingness to pay for reliable and affordable electricity are the same that would benefit most from the long-term electricity price hedge provided by the RE-Pool.

In addition to the decision of how the grant access to the RE-Pool, there are a number of further important design options on the consumer side. An exit option will determine under which conditions firms can opt out of their obligation to purchase electricity from the RE-Pool. Access to the RE-Pool offers a hedge against potentially high electricity prices but also entails a liability for payments at times of low electricity prices. Therefore, the assumed value of this hedge will vary over time. It is important to ensure that consumers will not opportunistically abandon or interrupt their participation in the RE-pool when expected electricity prices are low. Hence, contract termination options have to be very restrictive—for example, comprising a five-year notice period. Commodity price cycles tend to be shorter, and price expectations are highly uncertain beyond this time horizon, hence it would ensure that the benefit of longer-term price stability will guarantee continued participation. Thus, the design of the termination option can limit the financial liability of pool participation for consumers while avoiding the risk of opportunistic or strategic behavior.

The government agency backing the contracts for differences would serve as the counterparty for all producers and consumers for contracts and payments under the contract. Large consumers would be the direct contractual and commercial counterparty of the RE-Pool, based on a fixed amount of energy, much like how financial hedges are concluded. For households and smaller industrial and commercial consumers, the retailer they select would facilitate the commercial transactions with the RE-Pool where the allocated volume is based on the historical consumption of the consumer (thus preserving incentives from short-term price signals). The payments would be made through the retail firms that include the RE-Pool contracts in their risk management according to the share of the RE-Pool granted to consumers. If consumers change their retailer, the RE-Pool access will change accordingly.

4. Potential Benefits and Challenges of an RE-Pool

By providing a hedge against fluctuating power prices for both consumers and producers of clean electricity, the RE-Pool could offer benefits over private PPAs and public one-sided derisking policies. It would, however, also induce a risk regarding the long-term development of electricity prices that needs to be addressed in the contract design.

For producers of clean electricity, long-term contracts with the publicly backed RE-Pool would lead to lower financing costs than private contracts and one-sided derisking policies for a number of several reasons. First, contract duration matters because it determines the duration for which debt can be raised to replace equity. Although, in principle all contracts could be signed for a length matching the minimum expected operation of twenty to twenty-five years, in practice private PPAs are often signed for shorter periods (Mendicino et al. 2019), thus inherently resulting in higher financing costs. Second, a government-backed long-term contract is significantly more credible for investors than privately backed PPAs. An earlier analysis of the impacts of financing costs comparing the situation across EU member states with different support mechanisms found that increased risks will result in an increase of financing costs and, thus, average renewable generation costs of about 10 percent on the side of renewable producers and excluding impacts on the side of PPA buyers (May and Neuhoff 2021).

The award of a CfD for the expansion of renewable energy provides the reliable speed that is required for the successful energy transition by providing a predictable stream of revenues along the entire renewable energy value chain (Neuhoff, Richstein and Kröger 2023). By providing a secure stream of revenues, the risk is reduced that firms speculate on rising electricity prices and abandon a project when the price increases fail to materialize. Thereby, the CfD should increase the realization rates of awarded projects.

For consumers of electricity, the RE-Pool could likewise lead to a reduction in their financing costs since they typically have to put the long-term PPAs on their books, which reduces their creditworthiness. This increase in financing costs translates in an overall cost increase of about 20 percent of long-term private PPAs in comparison to participation in an RE-pool with suitable termination closes on the side of the buyers. In total this results in cost differences of up to 30 percent if producer and buyer side effects are combined (May and Neuhoff 2021). Compared to bilateral projects, the RE-Pool also reduces the counterparty risk for consumers emerging from default or failure to complete a renewable energy project since each individual project only constitutes a small share of the overall RE-Pool.

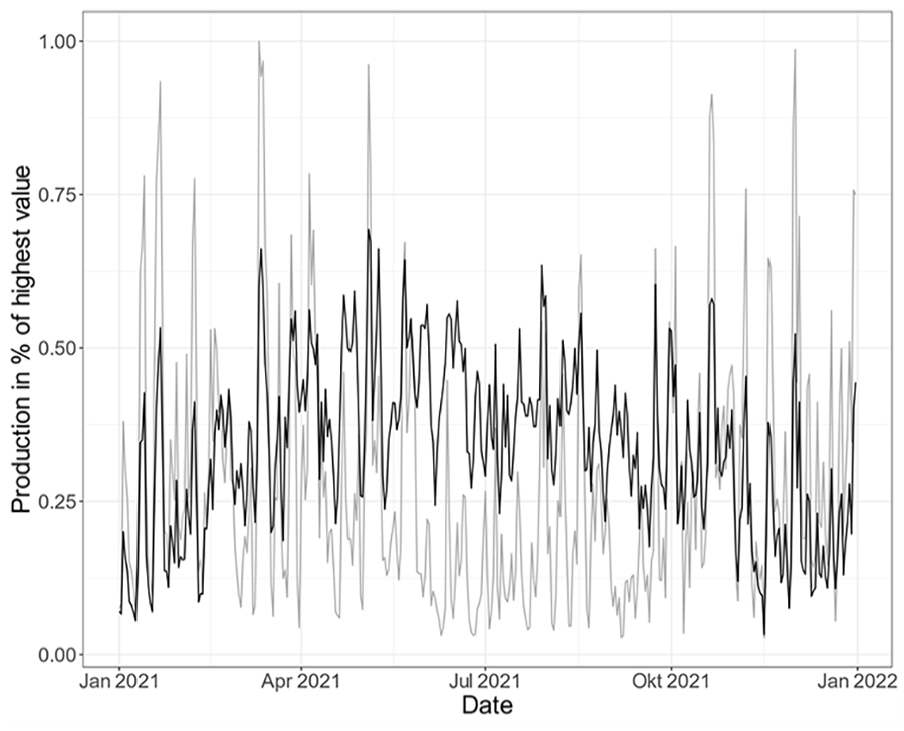

An additional benefit of the RE-Pool emerges when producers can obtain the green attribute of the electricity production hedged by the pool. This is valuable for industrial consumers who often need to be able to demonstrate the usage of green electricity to investors or their clients in order to charge a “green premium” (Köveker et al. 2023). Additionally, the RE-Pool would provide a more regular stream of electricity than a single contract or a small number of PPAs since the power production is diversified both technologically and geographically. Figure 4 shows how a stronger diversification leads to a lower volatility in the electricity supplied, especially when multiple technologies are combined in the pool. 8 This is especially important for cases in which producers have to certify that they purchased clean electricity at the time of production such as electrolyzers under the EU hydrogen directive. Thus, the benefit of a diversified production portfolio and the certification of the purchasing of clean electricity would become available to a wider array of companies than just those able to sign a large number of PPAs.

Smoother production of the RE-Pool (black) versus onshore wind (gray) due to technological diversification.

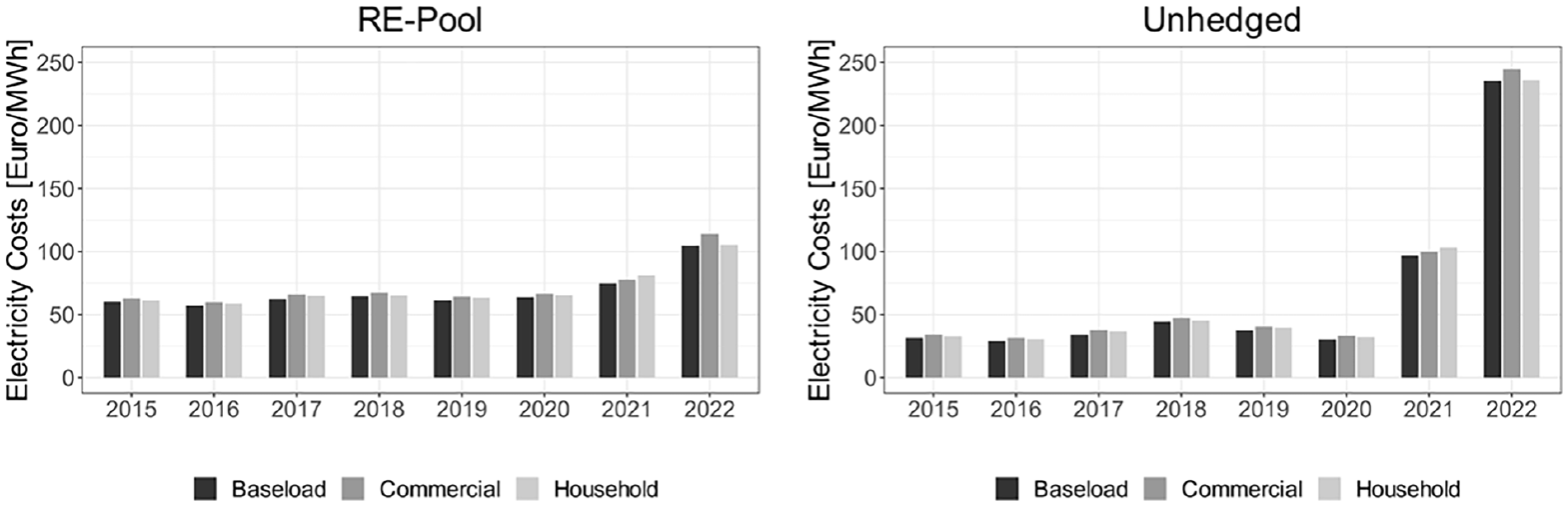

Most importantly, however, the RE-Pool would significantly reduce the volatility of energy expenditures for both households and industrial consumers of clean electricity. Figure 5 quantifies the stabilizing effect that the RE-Pool would have had on the electricity expenditures of different consumer types (baseload, commercial, and private households), based on historical data from 2015 to 2022. For comparability of results, we assume that all contract types are concluded at their fair market price over the entire period. We further assume that the RE-Pool covers 100 percent of the consumers’ energy demand in an average year and that the pool’s profile is equal to the aggregated renewable profile across all onshore wind, offshore wind, and photovoltaic installations in Germany. More information on how the data is calculated can be found in Appendix C.

Comparison of unhedged wholesale electricity costs (right panel), with costs hedged through full RE-Pool coverage (left panel).

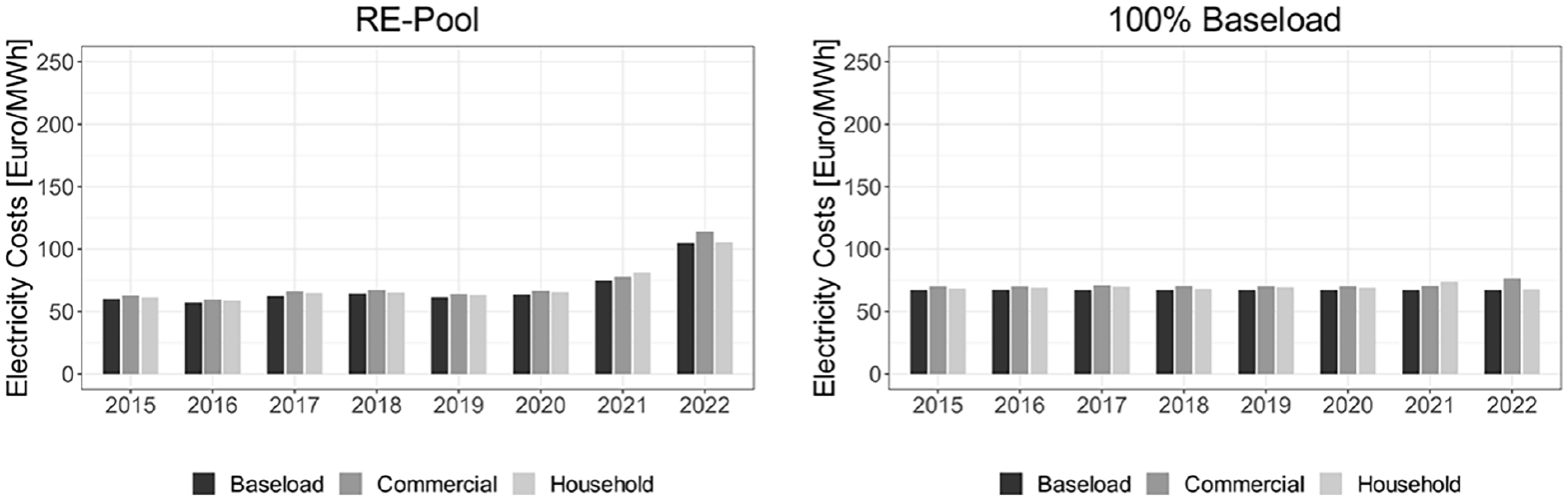

The RE-Pool by itself already reduces the electricity cost risk by reducing the volatility of expenditure from around 344 percent of the average expenditures for the high price year 2022 in the unhedged case to 153 percent in the RE-Pool case. While the RE-Pool reduces risks, it does not completely eliminate them since a basis risk (i.e., the difference between their own profile and the RE-Pool profile) remains. Figure 6 compares the RE-Pool to a hedge via a baseload contract. The volatility of electricity via the RE-Pool hedge is higher, as the baseload contract secures expenditures in 2022 to 106 percent for private households and 108 percent for commercial profiles, while it perfectly hedges baseload consumption.

Comparison of hedge via a baseload contract (right panel) and via the RE-Pool (left panel).

An inherent concern for consumers underwriting long-term commodity contracts is that the spot market prices will fall below the contract price. To a certain degree, this is the nature of a hedge. However, the risk that the price difference persists for a sustained period could reduce the attractiveness of the RE-Pool. The long-term cost of the RE-Pool will be determined by the levelized cost of electricity of the included technology. In the current situation, where the high price of electricity at the spot market is, in most hours, determined by the marginal fossil electricity producer, the RE-Pool is likely to reduce electricity costs below the spot market.

In the longer term, RE-Pool prices could result above average spot-market prices for RE generation from two possible developments: An overly fast deployment of renewable energy or a rapid decline of renewable energy costs. However, if renewable energy is deployed faster than flexibility and storage of renewable energy it would increase the number of hours of near-zero prices. This would increase the value of and the incentives for flexibility and storage, and thus government and private responses that result in an alignment of pool price and average RE spot price. If, instead, costs for new renewable projects will decline steeply in the future, then the envisaged pool will also include these projects. Thus, its contract price will fall with decreasing renewable energy costs. Only in the case of a rapid drop in renewable energy costs, would the pool price significantly deviate from the marginal cost of the cheapest new installations that may be accessible by competitors for a sustained period. Such a scenario would be for many reasons highly welcome but is at today’s already rather low RE costs not highly likely. It would raise managebale question of how to then allocate the sunk costs of historic investments irrespective of the RE-Pool.

5. How the Re-Pool Could Assist the Development of Flexibility Options

The energy transition requires the rapid build-up of flexibility options in order to balance the variability of renewable energy production which otherwise induces an inefficiency in the electricity system (Haar and Haar 2017). However, despite many efforts to introduce new products, liquid trade in forward and future markets only exists for base and peak load contracts. 9 This inhibits the realization of flexibility potentials required in a power system with increasing shares of renewables and rapidly declining availability of gas power generation as a traditional flexibility provider: Without forward products reflecting the characteristics of flexibility (load shifting or storage), providers of complementary flexibility have no market to hedge the value they can offer to the system. Without reliable revenue streams and forward markets to align demand and supply, investments to unlock flexibility potentials are difficult to realize.

Furthermore, as electricity prices are so far hedged with base- and peak-load contracts, a consumer that fails to unlock flexibility potential does not bear price risks. Thus, in the current system, for the consumer, realizing flexibility potentials is not a risk-reducing activity, but merely an uncertain revenue potential that is additional to their core business and, hence, not pursued with priority.

This one of several reasons, why the current market design fails to unlock the large flexibility potential of large energy users and to realize the benefits of pooling demand side flexibility across the integrated European power system.

It is therefore necessary that electricity users are aware of the profile risk and opportunities, if their electricity demand profile is not aligned with the power generation profile of wind- and solar power. Gradually increasing exposure of consumers to this profile risk incentivizes them to realize flexibility potentials. They will to the extent economically viable physically hedge the profile risk and purchase hedges for the remaining profile risks. This demand for hedges creates stable revenue streams and allows third parties to realize flexibility potentials.

The allocation of the RE-Pool exposes consumers (and retailers on their behalf) to profile risks and opportunitiese. The Pooled contracts provide a hedge for power prices with a profile of the wind- and solar power generation. By being independent of the actual consumption, but instead depending on the production of renewables, the RE-Pool at the same time ensures efficient short-term incentives to respond to electricity prices.

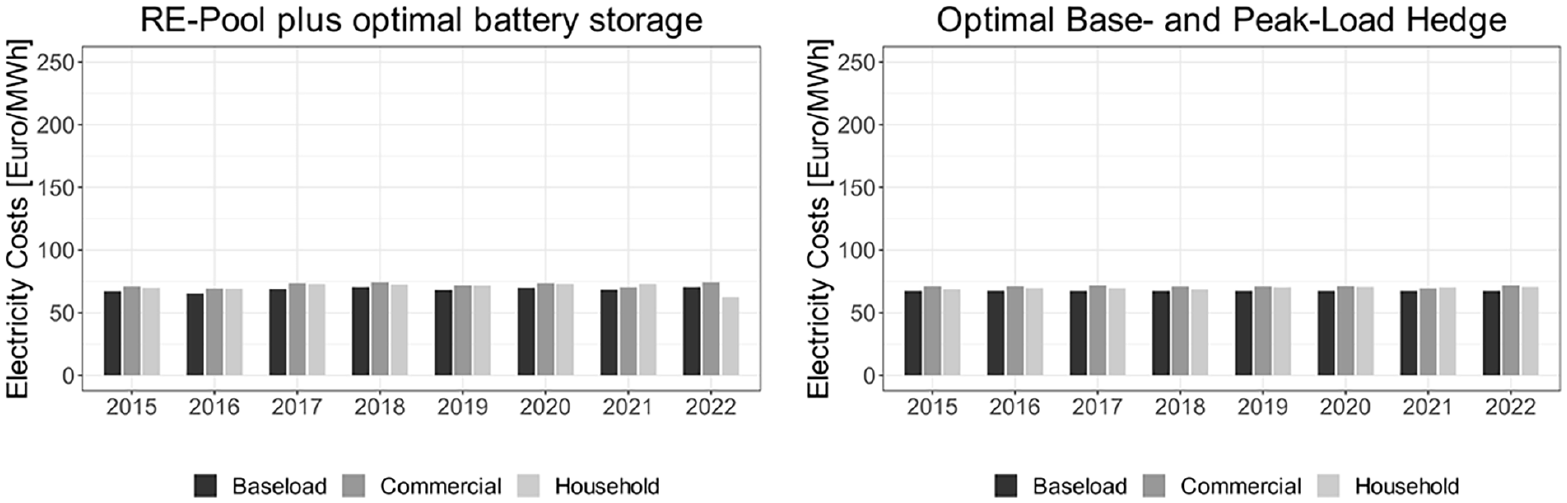

A typical hedge contract, which might evolve in the future, could be based on the price difference between the four hours of a day with the highest power prices and four hours of the day with the lowest prices (Renewable Energy Hub 2020), or more sophisticated storage contracts (Billimoria and Simshauser 2023). This would match the characteristics of a typical physical underlying process (i.e., battery storage or load shifting demand response), thus minimizing risk for flexibilty providers and facilitating the financing of their investments.

As shown in Figure 7 (left panel), even such a simple hedging combination of an RE-Pool with a fairly priced “4-hour product” (concluded for around 33 percent of yearly energy consumption) strongly reduces volatility. Even in the crisis year, power costs only incrase by 3 percent above the average electricity consumption costs. This nearly matches the stabilty achieved with a optimal combination of base- and peak-load contracts (right panel, with a 1 percent electricity cost increase).

RE-Pool hedge plus optimal battery hedge (left panel), optimal base- and peak-load hedge (right panel).

It warrants further analysis whether established approaches to adjust the remuneration to the realized wind patterns, as currently part of, for example, the tenders for the sliding market premium, should also be adapted. This can reduce risks resulting from imprecise wind forecasts during the planning stage or from new neighboring wind parks reducing the wind speed.

6. Conclusion

Long-term contracting arrangements are required to ensure continued renewable deployment after public support mechanisms are phased out that used to secure revenue streams. At the same time, recent energy price crises demonstrate the economic, inflationary and distributional costs of exposing consumers to price risk in the current market framework. While private bilateral contracts can provide a hedge for some companies, their negative impact on firms’ credit rating prevents many energy-intensive industries from signing such contracts. Hence bilateral contracts are insufficient to provide the required reliable speed and scale of the energy transition.

Instead, this paper proposes the introduction of an RE-Pool illustrating its potential for the support of renewable energy that passes on the conditions of publicly backed long-term contracts to the consumers of clean electricity. For producers, the pool offers a long-term contract for their production with a reliable counterparty, thus reducing financing costs and contributing to a stable production pipeline for investments along the value chain. For consumers, the RE-Pool reduces their exposure to power price volatility and offers a larger group of consumers access to certified clean electricity production. The pooling reduces counterparty risks and reduces exposure to the cost structure and production profile of a single project. The pool approach does, however, leave consumers exposed to the renewable energy production profile. This has a desired effect to incentivize consumers to hedge their remaining profile risk through investment in own flexibilty and purchase of flexibility products. This would help unlock the desired flexibilty investments and catalyze the financial markets for such products. While our proposal here is limited to wind and solar to simplify the operation of the pool, it needs to be investigated how such a pool could accommodate long-term contracts for dispatchable clean energy technologies.

A set of elements warrants particular attention and needs to be addressed in the design of the RE-pool. First, in order to avoid the negative effects of long-term contracts on capital costs and credit ratings of off-takers, the exit option for participating firms must be well designed while at the same time not offering any incentives to game the systems (e.g., firms should not be able to opportunistically terminate their obligations during times of low energy prices). Second, in the initial years, the volume of new long-term contracts underwritten in tenders may not meet the demand of industry and household consumers. The allocation of the RE-Pool to consumers will raise debates regarding those groups that are granted access to the attractive instrument, and it will be important to agree on objective and fair criteria. To reduce any such tensions, opportunities to broaden the available renewables in the pool should be explored. A rapid implementation, broad coverage of all wind- and solar projects, and cooperation with neighboring member states will be critical.

Supplemental Material

sj-docx-1-enj-10.1177_01956574251325486 – Supplemental material for Contracting Matters: Hedging Producers and Consumers With a Renewable Energy Pool

Supplemental material, sj-docx-1-enj-10.1177_01956574251325486 for Contracting Matters: Hedging Producers and Consumers With a Renewable Energy Pool by Karsten Neuhoff, Fernanda Ballesteros, Mats Kröger and Jörn C. Richstein in The Energy Journal

Footnotes

Appendix A

Appendix B

Appendix C

Acknowledgements

We would like to thank the two anonymous referees for their insightful comments and suggestions. We thank Jonas Schumacher for his excellent research assistance with this project.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received gratefully acknowledge the financial support received as part of the Kopernikus project SynErgie by the Federal Ministry of Education and Research (BMBF) [03SFK30-3].

Data Availability

All data used in this article can be made available upon request.

Supplemental Material

Supplemental material for this article is available online.

1

If anything, the marginal pricing system in electricity needs to become more fine grained both in time and in terms of providing locational price signals including for all demand side flexibility and load.

3

At times PPAs are signed after the support scheme awarded for the construction of a renewable energy plant has run out in order to extend its lifetime.

4

For this we assume that half of the PPA’s financial volume is considered as additional debt and that companies are prepared to underwrite PPAs with an undiscounted payment liability at the scale of half their market capitalization. This equals an increase in their debt-equity-ratio of 0.5, if long-term-debt and market capitalization are considered for this ratio. For detailed assumptions, please refer to ![]() .

.

5

BASF is a special case in this respect, as high value chemicals such as coatings or catalyst reflect a larger share of its activity than energy-intensive basic chemicals. This explains, why it could, in principle, underwrite PPAs for a larger share of its energy needs than firms more narrowly focused on energy intensive activities.

6

In theory, the pool could also be based on physical contracts rather than a financial contract. For simplicity we will assume a financial contract in the remainder of the article.

7

In a power market design with multiple bidding zones or even nodal prices, the reference market would be the local bidding zone or the local power price, thus ensuring that potential changes to bidding zones or a shift to nodal pricing will not impact viability of projects.

8

See Appendix B for a description of how the data in ![]() was computed.

was computed.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.