Abstract

Women founders frequently appear to encounter varied and often negatively biased decisions from investors. Our study builds on the theoretical and practical interest in understanding whether and how biases against women entrepreneurs are attributed to men investors’ cognitive and physiological (i.e., hormonal) responses to the women’s physical appearance. Using a cross-sectional research design, we recruited 106 experienced investors and randomly assigned them to one of two versions of a prerecorded pitch to test the effect of a woman entrepreneur’s physical attractiveness. The versions were identical in content and form but were delivered by different actresses, one of whom was considered highly attractive. We asked participants to observe the pitch and answer questions on related topics, including how likely they believed the business described would successfully progress through the screening stage of the investment process. In contrast to our hypothesis, we find that a woman entrepreneur’s attractiveness positively influences men investors’ assessments of her competence. These competence assessments lead to evaluations that the entrepreneur’s proposal would progress through the investment screening stage. We also theorize and find that men investors have a marked increase in cortisol levels when presented with an attractive woman entrepreneur. This increased cortisol leads to evaluations that the entrepreneur’s proposal would progress through the screening stage. Identifying the role physiological mechanisms play in investment evaluations underscores the importance of adopting proactive measures to ensure equitable and fair investment practices alongside fostering introspection within the investment community.

Keywords

Business investments result from a complex decision-making process in which investors carefully screen and evaluate business opportunities to determine the potential for financial returns (Ferrati & Muffato, 2021; Kollmann & Kuckertz, 2010; Petty, Gruber, & Harhoff, 2023; Skalicka, Zinecker, Balcerzak, & Pietrzak, 2023). As part of this activity, investors constantly evaluate entrepreneurs and their ventures based on predetermined criteria. Some entrepreneur factors commonly considered by investors include entrepreneurs’ prior experience, education level, and perceived competence (Berre & Pendeven, 2023; Lavi & Yaniv, 2023; Snellman & Solal, 2023), whereas some venture factors commonly considered by investors include a company’s revenue growth, the management team’s track record, profitability, business model, and current investors (Block, Fisch, Vismara, & Andres, 2019; Ferrati & Muffato, 2021; Kim & Lee, 2022). Investors must constantly refine and improve on these criteria and the weight they assign to them because high-quality investment decisions can lead to superior performance (Blohm, Antretter, Sirén, Grichnik, & Wincent, 2022; Guarana, Stevenson, Gish, Ryu, & Crawley, 2022; J. Zhang, Zhang, Li, & Caglayan, 2021). In contrast, poor-quality investment decisions often lead to substantial losses (Basoglu & Long, 2023; Escobar & Pedraza, 2023).

Despite the wealth of literature on the systematic and deliberate investment decision-making process, evidence suggests that investment decisions may also fall prey to biases that affect decision-making more generally. This evidence comes from studies investigating the investment decision-making process (e.g., Ahmad & Shah, 2022; Bigelow, Lundmark, Parks, & Wuebker, 2014; Weixiang, Qamruzzaman, Rui, & Kler, 2022) and the unequal distribution of funds across ventures (e.g., Hamdan, Calavia, & Aminu, 2023; Zhu, Qi, & Jin, 2023). Indeed, biases are a primary source of the gender funding gap (Balachandra, 2020; Snellman & Solal, 2023)—that is, the decreased likelihood of funding for women-led businesses (Guzman & Kacperczyk, 2019) and the smaller amounts they receive (Geiger, 2020) relative to men-led ventures. For example, investors tend to direct prevention-focused questions toward women entrepreneurs and promotion-focused questions toward men entrepreneurs (Malmström, Voitkane, Johansson, & Wincent, 2020), with the promotion-question condition resulting in twice as much investment in initiatives compared with the prevention-question condition (Kanze, Huang, Conley, & Higgins, 2018). In another demonstration of bias, Kanze, Conley, Okimoto, Phillips, and Merluzzi (2020) found that women-led ventures operating in men-dominated industries receive significantly less funding at lower valuations than women entrepreneurs operating in women-dominated industries. These findings show not only the disadvantages but also the diversity of experiences among women in attracting funding contingent upon the contexts in which they operate. The literature has often linked these outcomes of investors’ decision-making to the role of unconscious gender-role-incongruent expectations about entrepreneurs and their ventures (e.g., Balachandra, Briggs, Eddleston, & Brush, 2019).

While awareness of these investor biases is the first step toward minimizing or overcoming them, we must also understand their underlying mechanisms, which is key for proactively addressing and preventing unfair investment outcomes. Therefore, in this study, we move beyond the cognitive mechanisms responsible for investor biases that have been extensively studied (Abatecola, Cristofaro, Giannetti, & Kask, 2022) to a smaller but equally important stream of research on the physiological mechanisms underlying investors’ decision-making (e.g., Cueva et al., 2015). This nascent stream of research recognizes how cues (e.g., an individual’s first impression of a situation) are associated with biological processes in the human body that can influence an individual’s decision-making (Glimcher & Fehr, 2013; Hirshleifer, Lourie, Ruchti, & Truong, 2021). For instance, such physiological mechanisms may drive our desire for social interaction with other individuals (e.g., Aspesi, Bass, Kavaliers, & Choleris, 2023; Forbes & Dahl, 2010; Gordon, Martin, Feldman, & Leckman, 2011; McCall & Singer, 2012). Interestingly, research has also shown that increased physiological reactions positively affect investors’ financial risk-taking behavior (Coates & Herbert, 2008).

In our theoretical framework, we aim to elaborate on the existing knowledge about cognitive biases that account for the biases against women in funding by investigating these physiological aspects. In other words, while men investors may exhibit cognitive biases in their decision-making (e.g., due to gender-role-incongruent expectations), their physiological responses to a situation may trigger the release of hormones associated with the desire for social interaction and increased risk-taking tendencies in investment decisions. Consequently, when considering whether to invest in a woman-led venture, men investors may be influenced by interpersonal factors that affect decision-making across other contexts, including physical attractiveness.

Physical attractiveness has been shown to influence interpersonal decisions and assessments of personality traits across several contexts, ranging from customer service interactions (e.g., Choi, Huang, Choi, & Chang, 2020; Fang, Zhang, & Li, 2020) to the criminal justice system (Mazzella & Feingold, 1994) to moral decision-making (e.g., Cheng, Han, Liu, Kong, Weng, & Mo, 2022; Knox & TenEyck, 2023). Indeed, physical attractiveness is a critical attribute people use to form first impressions (Fultz, Stosic, & Bernieri, 2023), and it influences ongoing decision-making. However, an attractiveness bias is not necessarily universal. For example, men process attractive faces differently than women at the neural level (Tiedt, Weber, Pauls, Beier, & Lueschow, 2013). Importantly, compared with women, men are more easily distracted by attractive faces of the opposite sex (given heterosexuality; Van Hooff, Crawford, & Van Vugt, 2011). Similarly, men and women differ in their physiological mechanisms, and there is limited possibility of comparing, for instance, hormone levels between women and men (e.g., Apicella, Dreber, Campbell, Gray, Hoffman, & Little, 2008; Archer, 2006; Coates & Herbert, 2008; Kudielka & Kirschbaum, 2005; Santoro & Wierman, 2021).

Given that men investors still dominate the venture funding industry (Balachandra, 2020) and are still responsible for most venture evaluations and investment decisions, we are interested in understanding more about the variance in the gender funding gap—that is, the gap attributed to men investors’ biases against women entrepreneurs and how cognitive and physiological factors explain variance in these biases. Given the regrettable nature of such bias, we ask, How do men investors’ cognitive and physiological responses to a woman entrepreneur’s attractiveness impact their screening evaluations of that entrepreneur and her venture?

Building on cognitive-experiential self-theory (Baldacchino, Ucbasaran, & Cabantous, 2023; Denes-Raj & Epstein, 1994; Eunjin & Kim, 2023) and the gender literature (Henry, Foss, & Ahl, 2016; Kanze et al., 2018; Oh et al., 2022), we test our model on 106 men investors using an experimental design that manipulates the attractiveness of the woman entrepreneur and captures the investors’ evaluations of the likelihood that the woman entrepreneur’s venture would progress through the screening stage of the investment process. In doing so, we offer three primary contributions to the entrepreneurship and decision-making literatures.

First, prior research has highlighted a gender funding gap (Bringmann & Veer, 2021; Geiger, 2020; Guzman & Kacperczyk, 2019; Sud & Vohra, 2023). Investor biases contribute to this gap (Ewens & Townsend, 2020; Kanze et al., 2020). However, most previous studies have treated women entrepreneurs as a homogeneous group, as evidenced by these studies’ focus on men investors’ responses to women entrepreneurs in general regardless of substantive differences among the entrepreneurs. In this study, we look at this disadvantaged group (i.e., women entrepreneurs seeking funding) but focus on women entrepreneurs who may face greater biases than other women entrepreneurs. This especially disadvantaged subgroup merits additional study and interventions to level the entrepreneurial playing field.

Second, prior research on decision-making has highlighted physical attractiveness as an important consideration in consumer purchase decisions, monetary decisions, and justice outcomes (Knox & TenEyck, 2023; Onu, Nwaulune, Adegbola, & Nnorom, 2019; Pandey & Zyas, 2021). Although physical attractiveness is often beneficial (Cheng et al., 2022; Póvoa, Pech, Viacava, & Schwartz, 2020), it appears that in specific interpersonal contexts, a woman’s attractiveness can be a liability (Dilmaghani, 2020; C. Li, Lin, Lu, & Veenstra, 2020). While we theorize that physical attractiveness negatively affects investors’ perceived competence of entrepreneurs, our results are significant in the direction opposite to our hypotheses. Therefore, we provide an empirical counterweight to the gender incongruence of an attractiveness bias. We highlight how a woman entrepreneur’s attractiveness can lead men investors to assess her competence more positively, boosting the investors’ screening evaluations of the entrepreneur’s investment proposal. This finding highlights the need for more theoretical work to understand the mechanisms underlying this counterintuitive finding.

Third, unsurprisingly, prior research on investors’ biased decision-making has focused on cognitive mechanisms (e.g., Abatecola et al., 2022; Atasoy, Trudel, Noseworthy, & Kaufmann, 2022; L. Zhang & Guler, 2020), especially regarding investors’ evaluations of women entrepreneurs (Brenner, Solal, & Wernicke, 2023; Snellman & Solal, 2020; Sud & Vohra, 2023). Recent research has complemented the cognitive approach with an experiential approach exploring the role of hormones in investment decisions (Nofsinger, Patterson, & Shank, 2018). We highlight these physiological mechanisms to link mixed-gender dynamics to explain heterogeneity in women entrepreneurs’ experiences of investor biases. We highlight how the hormone levels of men investors lead to less attractive women facing greater biases in the fundraising process than more attractive women. This physiological link provides new insights into how investor biases outside the cognitive domain may affect women entrepreneurs and their ventures—it reveals an additional source of bias beyond expectations or norms.

Finally, we discuss the practical implications of our study and explicitly highlight that our findings do not justify perpetuating an attractiveness bias in investment decisions involving men investors and women entrepreneurs given its partial physiological basis. Our findings warn of its existence, making it imperative to take proactive measures and implement strategies to combat cognitive and physiological biases.

Literature Review and Hypothesis Development

Physical Attractiveness and Investment Decisions

Theories of emotions involving physiological and cognitive determinants (Schachter & Singer, 1962) and somatic marker theory (Bechara, Damasio, Tranel, & Damasio, 1997) have helped shape the field of cognitive neuroscience in investigating decision-making. In particular, cognitive-experiential self-theory suggests that two parallel systems are involved in decision-making: cognitive and experiential systems (Baldacchino et al., 2023; Denes-Raj & Epstein, 1994; Eunjin & Kim, 2023). According to this theory, people make biased decisions about others through the cognitive and/or experiential system(s). Biases are often driven by an individual’s first impressions of a situation (Hirshleifer et al., 2021) or the people involved in a decision-making scenario (Buijsrogge, Duyck, & Derous, 2021).

In interpersonal decisions, a target’s physical attractiveness is a major determinant of first impressions and judgments (Hall, Ruben, & Swatantra, 2020; Menegatti, Pireddu, Crocetti, Moscatelli, & Rubini, 2021; Papio, Fields, Beck, Firestone, & Rosenstiel, 2019). Decision-makers can be biased in favor of attractive individuals (vis-à-vis those who are less attractive), attributing to these attractive individuals the positive attributes of intelligence, friendliness, and kindness (C. Murphy, Hussey, Barnes-Holmes, & Kelly, 2015). In the context of employability, attractive individuals are typically viewed as more compatible with descriptors like “confident,” “ambitious,” and “skilled” than their less attractive counterparts (R. Murphy, Murphy, Kelly, & Roche, 2021). Although an attractiveness bias can occur in most social decision-making settings, this bias is most evident in mixed-gender conditions (Maestripieri, Henry, & Nickels, 2017).

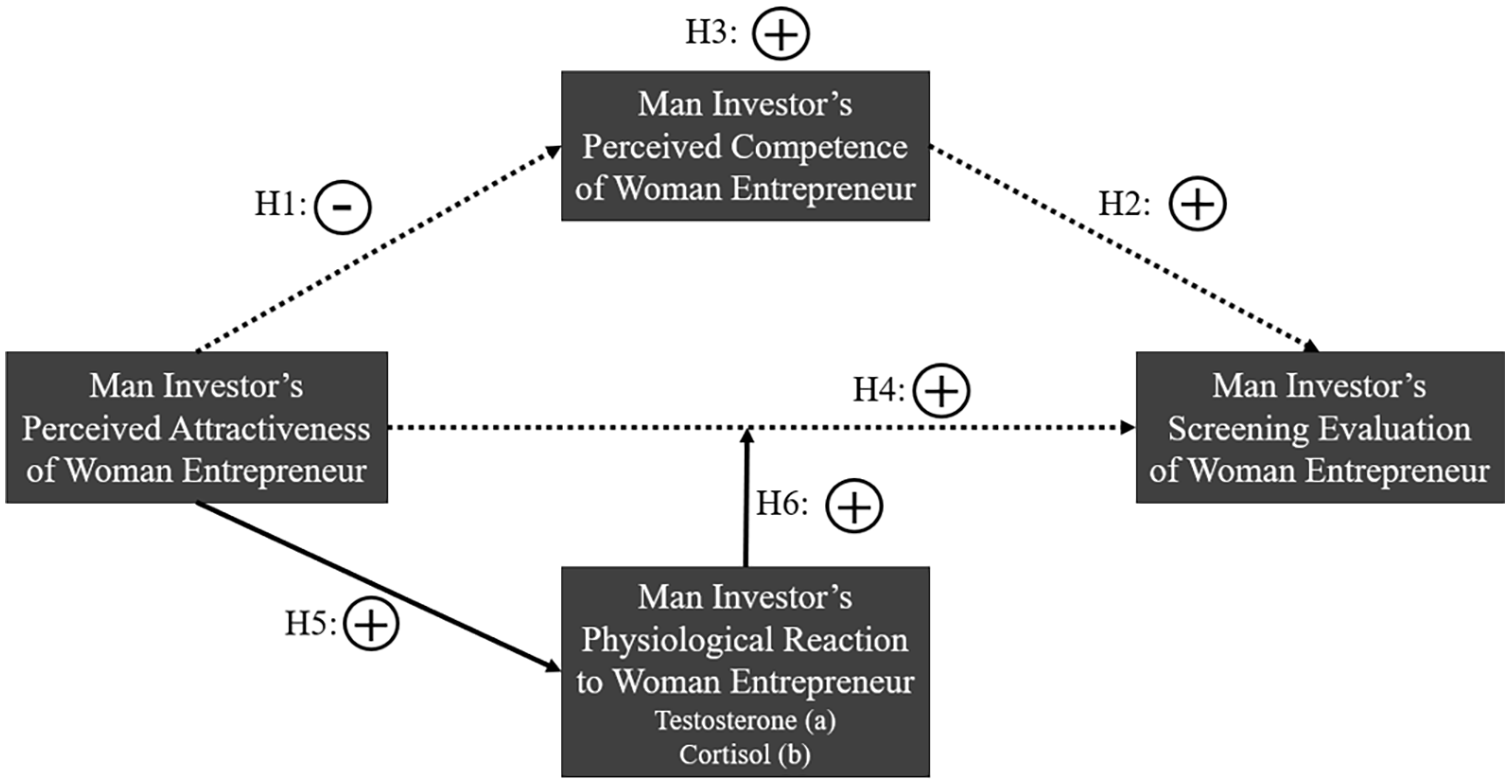

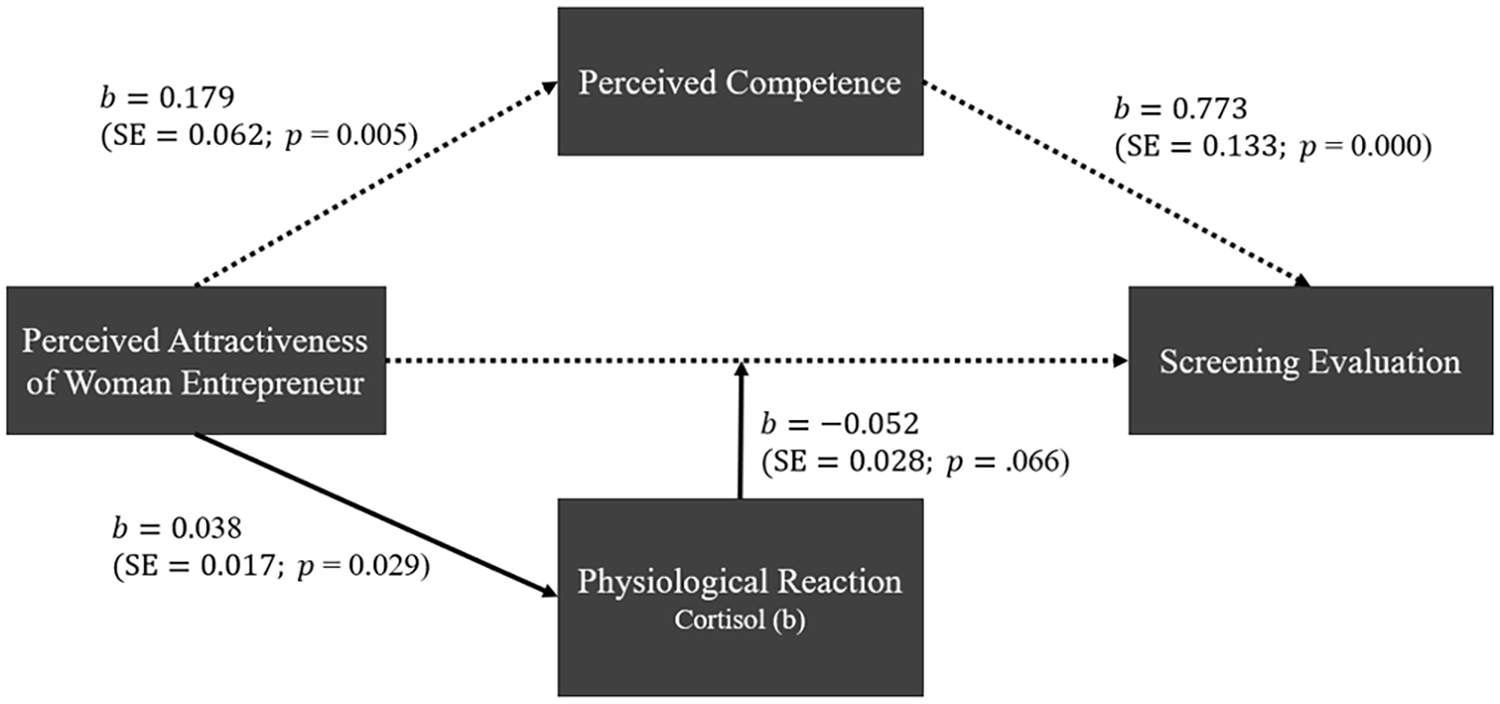

We build on cognitive-experiential self-theory to theorize how women entrepreneurs’ physical attractiveness influences men investors’ screening evaluations of the entrepreneurs’ proposals through cognitive and/or physiological pathways. Figure 1 illustrates how the attractiveness of women entrepreneurs may impact men investors’ decision-making at the earliest stage of the funding process. Through a cognitive pathway—illustrated as the upper path in Figure 1—we theorize that a woman entrepreneur’s attractiveness impacts a man investor’s assessment of the entrepreneur’s competence and that this assessment impacts the likelihood that the entrepreneur’s venture will successfully progress through the screening stage of the investment process. Through a physiological pathway—the lower path in Figure 1—we theorize that a woman entrepreneur’s attractiveness generates a physiological response in a man investor. This physiological response impacts the likelihood that the investor will successfully progress the entrepreneur’s venture through the screening stage of the investment process.

Hypothesis Framework

As a preview of our results, while our findings are consistent with our theorizing for the physiological pathway, our findings for the cognitive pathway are significant but opposite to what we theorize.

Cognitive Pathway

Cognitive studies have shown that a first impression about a person is powerful and enduring, continuing to predict an individual’s assessment of another’s character and qualities even after a relationship has been formed (Fultz et al., 2023; Swider, Harris, & Gong, 2022). In interpersonal situations, this first impression is highly influenced by a target’s physical attractiveness (Menegatti et al., 2021; Peng, Teoh, Wang, & Yan, 2022). Although there is considerable scholarly interest in the impact of attractiveness on decision-making, the underlying effects are disputed—namely, whether “beauty is good” or “beauty is beastly” (Dion, Berscheid, & Walster, 1972; Heilman & Saruwatari, 1979; Morrow, 1990; Straus, Miles, & Levesque, 2001).

The notion that beauty is good describes how decision-makers assign more positive qualities to attractive people across various domains, including trustworthiness (R. K. Wilson & Eckel, 2006), interpersonal ease (Dion et al., 1972), and interpersonal skills (Eagly, Ashmore, Makhijani, & Longo, 1991). Importantly, it appears that attractiveness influences audiences’ assessments of competence such that more attractive people are perceived to be more competent than less attractive people (Eagly et al., 1991; Todorov, Mandisodza, Goren, & Hall, 2005). For instance, Verhulst, Lodge, and Lavine (2010) showed that political candidates rated as more attractive are perceived as more competent, thus increasing their likelihood of being elected (vis-à-vis their less attractive opponents; Feingold, 1992; Hosoda, Stone-Romero, & Coats, 2003).

In contrast, the notion that beauty is beastly indicates the negative consequences of attractiveness. For example, in a study of financial analysts competing to be nominated as an all-star, C. Li et al. (2020) observed that attractive women were less likely to win a vote than their less attractive counterparts. In other professions, such as sales, customers view more attractive professionals as less trustworthy (Wongkitrungrueng, Hildebrand, Sen, & Nuttavuthisit, 2020). Furthermore, among retail business owners, attractiveness appears to place individuals at a disadvantage as they are more likely to be offered higher average wholesale prices (Starostyuk, Chen, & Prater, 2023). Even after controlling for potential confounds, such findings reflect negative perceptions of attractive individuals based on their appearance, including preconceived notions about their character. These societal stereotypes about attractiveness and women also apply to clothing such that more attractive women tend to be judged more harshly when they wear “provocative” styles (Goodin, Van Denburg, Murnen, & Smolak, 2011; Graff, Murnen, & Smolak, 2012).

However, this notion that beauty is beastly appears to be context specific. For example, attractiveness seems more of a liability for women in high-status positions than for those in low-status positions (Heilman & Saruwatari, 1979; Heilman & Stopeck, 1985). Furthermore, while attractiveness is an advantage for women in jobs that are gender-role congruent (e.g., Y. Li, Zhang, & Fang, 2022), attractiveness is a disadvantage for women in jobs and industries that are characterized as more masculine (Eagly & Karau, 2002; Tartaglia & Rollero, 2015). For example, women appear to be assessed as gender-role incongruent in management jobs and, as a result, are perceived to be less competent and intelligent by individuals asked to rate the suitability of potential applicants for these positions (Johnson, Podratz, Dipboye, & Gibbons, 2010). Therefore, in some contexts, beauty and competence are perceived as incompatible attributes for women (Holahan & Stephan, 1981).

Gender stereotypes also exist in the entrepreneurial funding context, in which gender-role expectations tend to affect how peers evaluate women and their performance. For instance, studies have found that women are often perceived to be incongruent with the entrepreneurial role (Balachandra, 2020; Eagly & Karau, 2002; McAdam, Harrison, & Leitch, 2019) because the attributes associated with successful entrepreneurship—boldness, risk-taking, and assertiveness—are viewed as masculine rather than feminine (Ahl, 2006; Oliver, Krause, Busenbark, & Kalm, 2018). These beliefs become reinforced in the investment community as investors share their knowledge about what represents a promising investment prospect (Berre & Pendeven, 2023; Kanze et al., 2018; L. Zhang & Guler, 2020). However, this shared understanding of what constitutes a successful entrepreneur is produced (and perpetuated) by male-centric stereotypes of entrepreneurs in masculine jobs and industries by investors who are mostly men (see Malmström, Voitkane, Johansson, & Wincent, 2018; L. Zhang & Guler, 2020). When judged against these criteria, women may be perceived as inadequate because they differ from the general image of a prototypical successful entrepreneur.

The reported findings suggest that social norms may reinforce the masculinity of entrepreneurship such that women are perceived as incongruent with the entrepreneurial role. This incongruence is likely associated with the degree of femininity, or stereotypically feminine traits, displayed by an entrepreneur. Studies conducted on heterosexual men across several cultures have suggested that these populations view women perceived as more feminine as more attractive (Fiala et al., 2021; Kleisner et al., 2021). Given the association between attractiveness and femininity, gender incongruence with entrepreneurial tasks is likely more salient for more attractive women than for less attractive women. This view would penalize attractive women, who would be perceived as lacking the (stereotypically masculine) qualities required to run and competently lead a venture. Based on the preceding reasoning, we offer the following hypotheses:

Hypothesis 1: Men investors assess more attractive women entrepreneurs as less competent than less attractive women entrepreneurs.

Hypothesis 2: Women entrepreneurs assessed as more competent receive more positive screening evaluations than those assessed as less competent.

Hypothesis 3: Men investors’ assessments of women entrepreneurs’ competence negatively mediate the relationship between women entrepreneurs’ attractiveness and men investors’ screening evaluations of these entrepreneurs’ ventures.

Physiological Pathway

We theorize that over and above women’s beauty penalty of reduced perceived competence from performing the gender-incongruent tasks of founding a venture, there may be an underlying beauty benefit. For example, people evaluate more attractive individuals of a different gender more positively in selection tasks because these decision-makers desire increased engagement and communication with them compared with less attractive targets (Agthe, Spörrle, & Maner, 2011; Lemay, Clark, & Greenberg, 2010; Voit, Weiß, & Hewig, 2023; for a meta-analysis, see Eagly et al., 1991). This desire for social interaction may occur even when an attractive person is perceived as incompetent for the job at hand. For example, men executive managers tend to evaluate attractive women executives as less professionally competent but more socially engaging (i.e., stronger social skills) than less attractive women executives (M. Wilson, Crocker, Brown, Johnson, Liotta, & Konat, 1985). Furthermore, attractiveness can capture a decision-maker’s attention for reasons unrelated to perceived work-related competence (Becker, 2017; Maner et al., 2003). Therefore, along with men investors’ competence discount for attractive women entrepreneurs (indirect path; Hypothesis 3), men investors may also desire greater social interaction with and pay more attention to more attractive women entrepreneurs relative to less attractive women entrepreneurs—a positive direct path between women entrepreneurs’ attractiveness and men investors’ screening evaluations of these entrepreneurs’ ventures. We theorize that a physiological pathway moderates this direct relationship.

A physiological perspective recognizes how biological processes in the human body can influence an individual’s decision-making (Glimcher & Fehr, 2013). While neurons process, transmit, and encode information through electrical impulses, chemical processes modulate and transfer information between neurons, impacting decision-making (Hyman, 2005). Chemical signals involve the release of neurotransmitters and hormones, such as cortisol and testosterone, which can influence behavior without interfering with cognition (Allan, 2014; Janowsky, Chavez, & Orwoll, 2000; Schiller, Johnson, Abate, Schmidt, & Rubinow, 2016). Various stimuli trigger the release of hormones, such as changes in lighting (e.g., Rahman, Wright, Lockley, Czeisler, & Gronfier, 2019) or frightening images, like those of a spider (e.g., Abad-Tortosa, Costa, Alacreu-Crespo, Hidalgo, Salvador, & Serrano, 2019; Hamm, 2020). Cognitive processes do not control these physiological responses (Bechara et al., 1997).

We theorize that the release of hormones in reaction to a woman’s physical attractiveness (Frankenhuis, Dotsch, Karremans, & Wigboldus, 2010; Ronay & von Hippel, 2010; van der Meij, Buunk, & Salvador, 2010) can influence the strength of the positive direct relationship between women entrepreneurs’ attractiveness and men investors’ screening evaluations of these entrepreneurs’ ventures. Indeed, a woman’s attractiveness influences men’s decision-making through the biological mechanism of elevated hormone levels (Goldey & van Anders, 2012). This hormonal response is related to activating the body’s hypothalamus-pituitary-adrenal axis, which is involved in human courtship. An evolutionary thesis for an attractiveness bias proposes that more attractive individuals are favored because they are (unconsciously) viewed as preferred sexual partners (Maestripieri et al., 2017). This idea is supported by multiple findings suggesting that attractiveness effects are stronger in mixed-sex scenarios than in situations in which both participants are of the same sex. For example, testosterone levels in men rise after exposure to pictures of women but not of other men, and men’s cognitive performance worsens after interacting with women but not with other men (Karremans, Verwijmeren, Pronk, & Reitsma, 2009; Zilioli, Caldbick, & Watson, 2014).

Therefore, we propose that observing a physically attractive woman entrepreneur present a venture proposal triggers chemical messengers (the release of testosterone and cortisol) in men investors. Those who experience elevated testosterone and cortisol make decisions based on more focused attention, greater risk-taking, and a more optimistic view of the future, magnifying the direct evaluation benefit of attractiveness (i.e., over and above the indirect pathway involving perceived competence). On the basis of the above reasoning, we offer the following hypotheses:

Hypothesis 4: Over and above perceived competence, men investors provide more positive screening evaluations of the ventures of more attractive women entrepreneurs than less attractive women entrepreneurs.

Hypothesis 5: Men investors experience higher hormone levels ([a] testosterone and [b] cortisol) when observing more attractive women entrepreneurs than less attractive women entrepreneurs.

Hypothesis 6: Over and above perceived competence, the positive relationship between women entrepreneurs’ attractiveness and men investors’ positive screening evaluations of these entrepreneurs’ ventures is more positive for men investors experiencing higher hormone levels ([a] testosterone and [b] cortisol) than for those experiencing lower hormone levels.

The Experiment

Ethical Considerations

The internal research ethics committee of a public university in Switzerland approved this study. Participants gave informed written consent before participation. For the study, we collected saliva samples to measure hormone levels. The test tubes were labeled with random numbers and sent in envelopes to participants. No record was kept of this number assignment to ensure participant confidentiality. We used the numbers as unique identifiers for the decision-making task. We provided participants with a plain, unmarked envelope for sample collection. For the main study, we chose the recordings of two actresses with the largest difference in their attractiveness scores from a pool of 11. To protect their self-images, we did not publish any personal details about their attractiveness scores. We informed the actresses that they would be rated on their attractiveness in the study, and they provided us with their written consent.

Sample and Participant Recruitment

Our sample constitutes men who are experienced business angels and venture capital investors between the ages of 23 and 57. Our study’s statistical power and sample size considerations were rigorously defined through a comprehensive power analysis conducted before data collection. This analysis, aiming for 80% power and an alpha level of .05, indicated that at least 50 participants would be necessary to achieve statistical significance for the expected effect sizes. To further substantiate our sample size adequacy, we reviewed previous research in hormone level studies, finding support for our target; for instance, Ronay and von Hippel (2010) suggest that a sample of approximately 96 participants is deemed sufficient. In our study, we initially recruited 111 participants, although five were excluded during the analysis phase due to specific criteria not being met. This process resulted in a final sample of 106 participants, comfortably surpassing the minimum required for robust statistical analysis.

We recruited the sample through LinkedIn, university incubator investor networks, and different online platforms: Business Angels Switzerland, Start Angels, the Swiss Private Equity and Corporate Finance Association (SECA), and Angel.co. We embarked on strategic outreach on LinkedIn via the accounts of two professors and a PhD student in entrepreneurship. Using their profiles as guides, we identified and engaged with professional business angels and venture capital investors. For investors who expressed interest in the study, we asked them to share their e-mail addresses to receive an in-depth study description.

In recognition of their contribution, we offered participants several potential rewards. First, we randomly chose one participant from the pool of all participants to receive a monetary award of CHF 200 (approximately US$225). Second, we offered participants early access to the contact information of a nascent yet promising start-up, positioning them at the forefront of potential investment opportunities. Upholding fairness and ethical standards, we ensured that all participants had equal access to this start-up opportunity after participating. Our study’s design precluded the linkage of individual investors with their respective screening evaluations, preserving anonymity and averting potential researcher biases. Finally, we granted participants access to the study’s findings, empowering them with a deeper comprehension of their investment decision-making geared toward fostering more informed and sound investment choices in subsequent ventures.

We focused on recruiting investors in the major start-up hubs in Germany and Switzerland because these countries are close to the first author’s work location. Proximity was important because saliva samples—used to measure the investors’ testosterone and cortisol levels—had to be collected in person by an individual on the research team. Specifically, we needed to transport the saliva samples in a frozen state from the investors’ locations to the laboratory for analysis to avoid degradation of the hormones (see Measures). Hence, we focused on investors in Berlin, Cologne, Munich, Bonn, Frankfurt, Zurich, Geneva, Lausanne, and St. Gallen. Another reason for our focus on Germany and Switzerland was the prevalence of English speakers in these locations, especially in these investment communities. All our study materials, such as the different versions of the elevator pitch provided to investors for evaluation, were in English. Using a single language throughout the study helped eliminate any confounding effects introduced by linguistic variations resulting from translating our material.

All investors answered a set of screening questions, and we included only investors who had made investment decisions and had made at least one start-up investment. Consistent with Hair, Black, Babin, and Anderson’ (2014) criterion for an invalid response, we excluded two investors because they answered fewer than half of the survey questions. Additionally, we excluded one participant due to recent eye surgery that could have influenced the physiological measures. Finally, we excluded two participants due to missing cortisol and testosterone values to ensure consistency of the sample between the models for all analyses.

The final sample included 106 men investors (N = 106). The participants in the study were between 23 and 57 years old, with an average age of 37.871 (SD = 8.51). On average, each participant had invested in 10.02 start-ups (SD = 12.42). The median number of previous investments was 5.5, with the lower quartile (25th percentile) at 2.25 investments and the upper quartile (75th percentile) at 12 investments. Their experience as investors was quantified by how many years they had worked as venture investors. They had an average of 6.36 years (SD = 5.51) of experience. The experience distribution showed the first quartile at 2 years, the median at 5 years, and the third quartile at 9.75 years.

Experimental Setting and Design

The present study used a between-subjects design with the attractiveness of the woman entrepreneur as the treatment, which we used to capture the men investors’ perceptions of attractiveness (detailed later). Before the main study, we conducted a pilot study with 67 men investors who rated the physical attractiveness of 11 women actresses on a scale created by Brooks, Huang, Kearney, and Murray (2014) ranging from 0 (very unattractive) to 100 (very attractive). The individuals involved in the pilot study came from the same population as those in the subsequent procedures. However, the samples were distinct: Individuals who participated in the pilot study were not involved in the final study.

In the pilot study, the investors evaluated the 11 women entrepreneurs (actresses playing the role of entrepreneurs) based on prerecorded versions of an elevator pitch, which were read from a teleprompter to ensure the versions differed only in the attractiveness of the woman presenting. We used a professional start-up pitch deck from an early-stage company as a template. We chose the most promising start-up case from our university’s accelerator program, which selects eight start-ups from more than 40 applications twice a year. The founders later achieved notable success, with one launching a start-up securing US$44 million in funding and the other organizing a major European start-up conference and earning Forbes 30 Under 30 recognition. To maintain confidentiality, we used a fictional start-up name and obtained written consent from the founders.

We selected two actresses for the experimental task manipulation for the main study based on their attractiveness scores. Specifically, we chose the woman with the highest average score (M = 77.95, SD = 17.99) and the woman with the lowest average score (M = 36.30, SD = 20.05). A two-tailed t test indicated a significant difference between these women’s scores (t = −12.66, p < .001). To protect the self-images of the actual actresses chosen for the main study, we did not publish any personal details, and we blinded the actresses to our hypotheses. Finally, we confirmed that the content of the 10-min investor pitch was consistent across the presentations. Specifically, we played the audio recordings of the presentations (with no video) to 27 men investors (different sample). We asked them to rate the similarity of the content of the two versions on a scale from 1 (completely different) to 7 (identical). Overall, 26 of the 27 investors (96%) rated the content of the two versions of the investor pitch as identical.

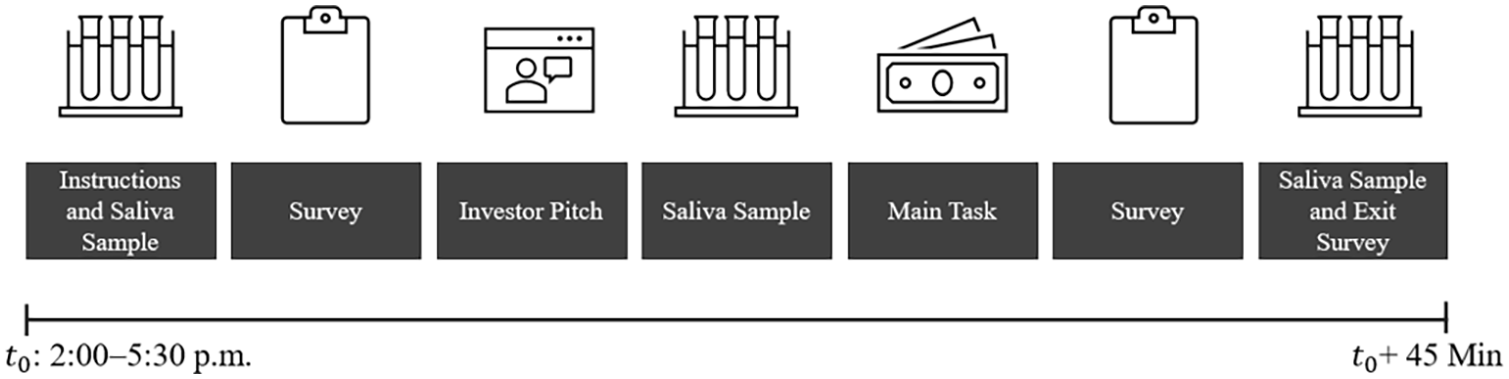

After developing the experimental task, we started recruiting men investors. We informed study candidates via mail that we were investigating the effect of physiological reactions on early-stage venture investment decision-making and that they would receive an envelope within the next 2 weeks containing initial instructions for the experimental task and tubes for saliva sample collection using passive drool (Salicaps, Tecan). All participants provided written informed consent before engaging in the experimental task. We asked the investors to complete the task between 2:00 p.m. and 5:30 p.m. and to avoid starting the experiment within 1 hr of eating food or brushing their teeth, 24 hr after chewing gum, 18 hr after smoking or drinking caffeinated beverages, 24 hr after engaging in physical exercise, and 10 min after drinking water. These instructions reduced the risk of confounding the hormone level measurements.

We also provided participants a link with login details to access the internet-based investment task via Qualtrics. After logging into the experiment, the investors answered questions about recent activities that may have distorted their hormone levels (e.g., eating or brushing their teeth) and confirmed that all instructions were followed. If all answers indicated adherence to the study instructions, the investors received video instructions on how to take a baseline saliva sample (Figure 2) and collect the first saliva sample. After that, the investors answered several questions about their demographic characteristics and start-up experience.

Experimental Design

Finally, the investors received information about the main task, which required them to pay attention to a 10-min investor pitch for a start-up and answer several questions regarding the start-up, including whether they would progress the venture through the screening stage to the next stage of the investment process. We asked participants to view this material on their own to prevent any bystanders from influencing their reactions or hormone levels. We randomly assigned the investors to one of the two prerecorded pitch versions, which differed in the woman entrepreneur’s attractiveness (experimental stimulus). We informed the investors that they should carefully listen to the pitch as they would have to answer several questions about the start-up and make investment decisions.

We directed the investors to the iMotions biometric research platform to watch the entrepreneur’s pitch. We showed each investor one pitch to ensure sufficient experimental power, reduce order effects, and reduce the likelihood of hypothesis guessing. Upon viewing the woman entrepreneur’s venture pitch, we directed the investors to the Qualtrics survey. We asked them to provide a second saliva sample by again displaying the instructions for the baseline saliva sample. After saliva collection, we asked them to indicate their likelihood of proceeding with a personal discussion and due diligence of the company—representing successfully passing the screening stage of the investment process. We used a single item as we were interested in measuring a concrete decision. Previous research has shown that single-item measures can be equally valid as multiple-item measures (Allen, Iliescu, & Greiff, 2022), and they have been used in previous studies on decision-making and evaluations (Brooks et al., 2014; Tinkler, Whittington, Ku, & Davies, 2015).

After the main investment task, we collected a variety of potential covariates. Of particular interest, the investors reported their assessments of the woman entrepreneur’s competence level. We used an open question to allow the investors to elaborate on their assessments of the entrepreneur’s competence. We included a standard question to ensure they could not guess our hypotheses as well as questions about their relationship status and the attractiveness of the entrepreneur (Brooks et al., 2014). We intentionally asked these questions at the end of the instrument to avoid informing them about our hypotheses. Finally, we asked the investors to report their perceived stress and how much they trusted the woman entrepreneur based on adaptations of established questionnaires in the management literature (i.e., Hunter & Thatcher, 2007; Schoorman, Mayer, & Davis, 2007, respectively). An open-feedback section concluded the experiment. The comments in the open-feedback section primarily reflected the reality of the video pitch and its alignment with pitches the investors often see in their work.

Measures

Dependent variable: Screening evaluation

In the typical venture capital investment process, the first step is the initial screening of a start-up. This step usually consists of a 10-min investor pitch and a round of questions and answers. If the investor believes the entrepreneur has presented a potential investment opportunity, the entrepreneur’s proposal passes the screening stage and progresses to an in-depth discussion and due-diligence process (Klonowski, 2010). We asked, “How likely would you proceed with a personal discussion and due diligence of the company?” The investors responded to the question using a continuous scale ranging from 0 (very unlikely to proceed) to 100 (very likely to proceed). Six experienced investors from different funds independently confirmed that the question we asked reflects their screening evaluations after seeing a pitch and that a larger number represents a more positive screening evaluation.

Independent variable: Physical attractiveness

Although we manipulated the experiment to present a highly attractive versus a less attractive woman entrepreneur (based on a pilot study), we had to capture the men investors’ perceptions of attractiveness as the independent variable. While some attributes of attractiveness are primarily recognized and agreed upon across individuals, our focus is on individual-level cognitions and physiological responses, so it was essential to capture the investors’ perceptions rather than rely on the manipulation (Berscheid & Walster, 1974). We used the pilot study’s results to increase the likelihood of obtaining sufficient variance in perceived attractiveness (consistent with Carney, Cuddy, & Yap, 2010; Thorndike, 1920). At the end of the experiment, the investors rated the perceived attractiveness of the woman entrepreneur they observed pitching a venture. Following Brooks et al. (2014), we asked the investors to rate their impressions of the appearance and attractiveness of the founder they saw (0 = very unattractive, 100 = very attractive)—namely, “To what degree were you physically attracted to the founder?”

Mediator: Assessed competence

Immediately after the decision-making task, the investors rated the perceived competence of the woman entrepreneur they saw via a five-item competency questionnaire used in previous research (Fiske, Cuddy, Glick, & Xu, 2002; Glick, Larsen, Johnson, & Branstiter, 2005) that we adapted to the entrepreneurial context. Specifically, we adapted the scale to measure the competence of the founder of the start-up: (a) “How capable is the founder of this start-up?” (b) “How efficient is the founder of this start-up?” (c) “How intelligent is the founder of this start-up?” (d) “How skillful is the founder of this start-up?” and (e) “How responsible is the founder of this start-up?” (α = .88). The investors responded to the questions using a continuous scale ranging from 0 (very negative) to 100 (very positive).

Mediator: Hormone levels

We collected saliva samples through passive drool (Salicaps from IBL-International) at three time points during the experiment to capture hormonal changes over time and determine the area under the curve (AUC; Figure 2). Researchers calculate the AUC from repeated physiological measurements to reflect the overall secretion of a hormone over a specific period (Pruessner, Kirschbaum, Meinlschmid, & Hellhammer, 2003). We included all three testosterone and cortisol collection periods to calculate the AUC for analyses.

We instructed the investors to store their saliva samples in their kitchen freezers at −20 °C within 60 min of collection. A research team member collected the samples within 2 weeks of the experiment, checked that the samples had been stored as instructed, and transported the saliva samples to the laboratory in a dry-ice box. Laboratory technicians analyzed the saliva samples within 28 days to prevent significant degradation of testosterone or cortisol levels (Toone et al., 2013). We contracted Dresden Labservice GmbH to conduct the tests using tandem mass spectrometry (LC-MS/MS). The intra- and interassay coefficients of variation (CVs) were below 9%, indicating that the saliva samples were consistent and precise across multiple times (intraassay CV) and that the test would produce similar results between different series of tests (interassay CV; Gao, Stalder, & Kirschbaum, 2015).

Controls

As controls, we included the investors’ age and experience because age appears to be associated with declining biological mechanisms, such as testosterone, and risk-taking (Feldman et al., 2002), and investors’ decision-making can change with age (Bali, Demirtas, Levy, & Wolf, 2009; Mishra, 2014), which may impact how they assess attractiveness. For age, we simply asked the investors how old they were. For experience, we asked them how many years they had invested in start-ups.

Results

Main Results

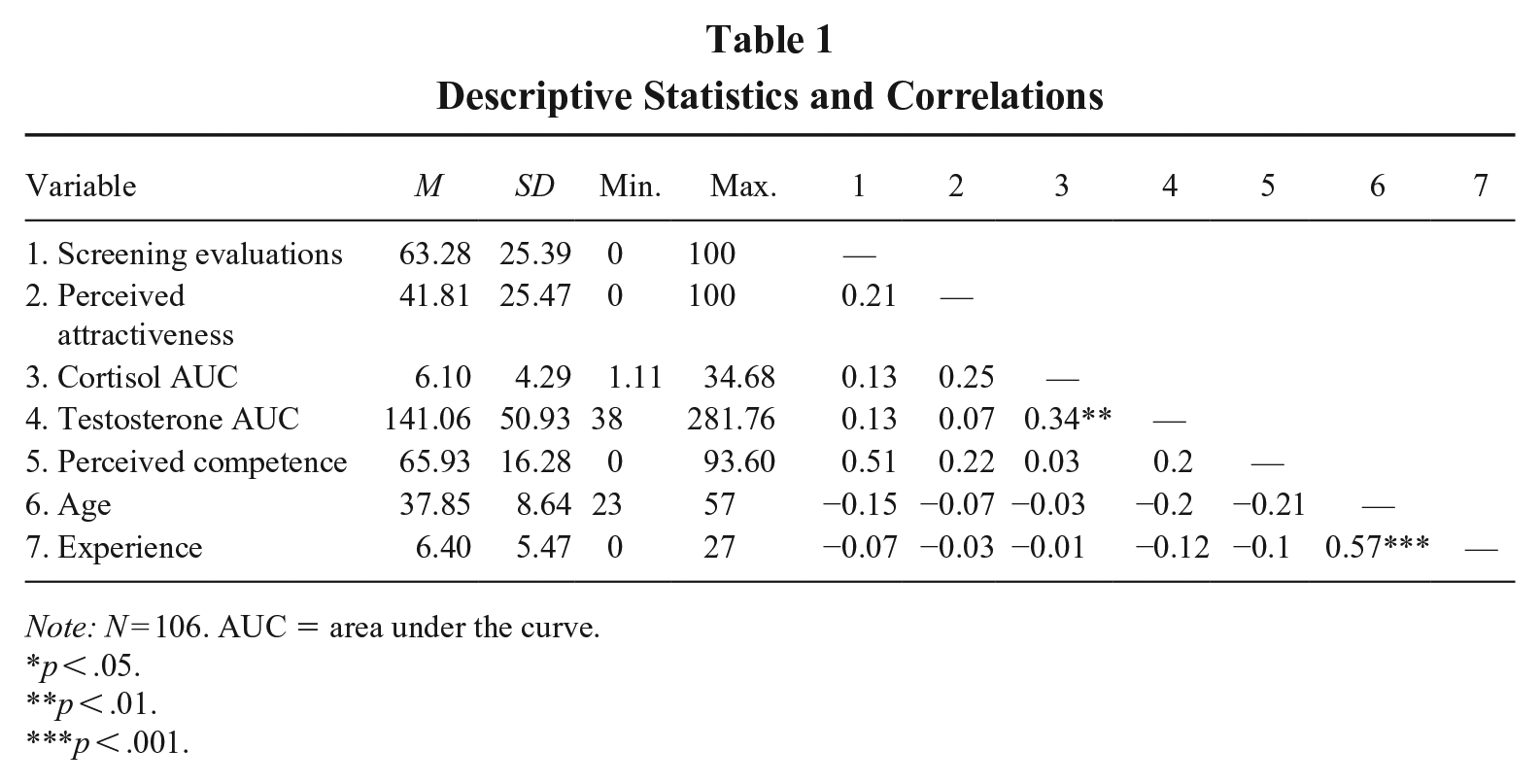

Table 1 summarizes the descriptive statistics. We used Spearman correlation coefficients because the dependent variable did not have a normal probability distribution (Shapiro-Wilk normality test W = 0.93245, p = .000). To detect multicollinearity issues, we computed the generalized variance inflation factors. As all values were below 1.5, multicollinearity is unlikely to be an issue. To assess the risk of omitted-variable bias, we calculated the impact threshold of confounding variable (ITCV) for each model. We compared the ITCV against the square root of the product of those same partial correlations with each control variable (consistent with Busenbark, Yoon, Gamache, & Withers, 2022). In every model except Model 5, which investigates the effect of perceived attractiveness on cortisol levels, the partial correlations with the controls were below the ITCV. For Model 5, the partial correlation with the strongest control was 0.34, which exceeds the ITCV of 0.027. Therefore, we computed the robustness of interference, indicating that 12 observations would have to be replaced with cases for which the effect is zero (Frank, Maroulis, Duong, & Kelcey, 2013). This slight deviation points to a significant, yet nuanced, link between perceived attractiveness and cortisol, paving the way for future investigations into the complex dynamics of attractiveness and physiological reactions within rigorously controlled study conditions. We also checked the treatment condition’s robustness by conducting a two-sample t test between the women entrepreneurs. On average, the woman entrepreneur deemed more attractive received a significantly higher rating by the men investors (M = 56.64) than the less attractive counterpart (M = 28.00). A two-tailed t test confirmed this significant difference, t(101) = −7.03, p = .000.

Descriptive Statistics and Correlations

Note: N = 106. AUC = area under the curve.

p < .05.

p < .01.

p < .001.

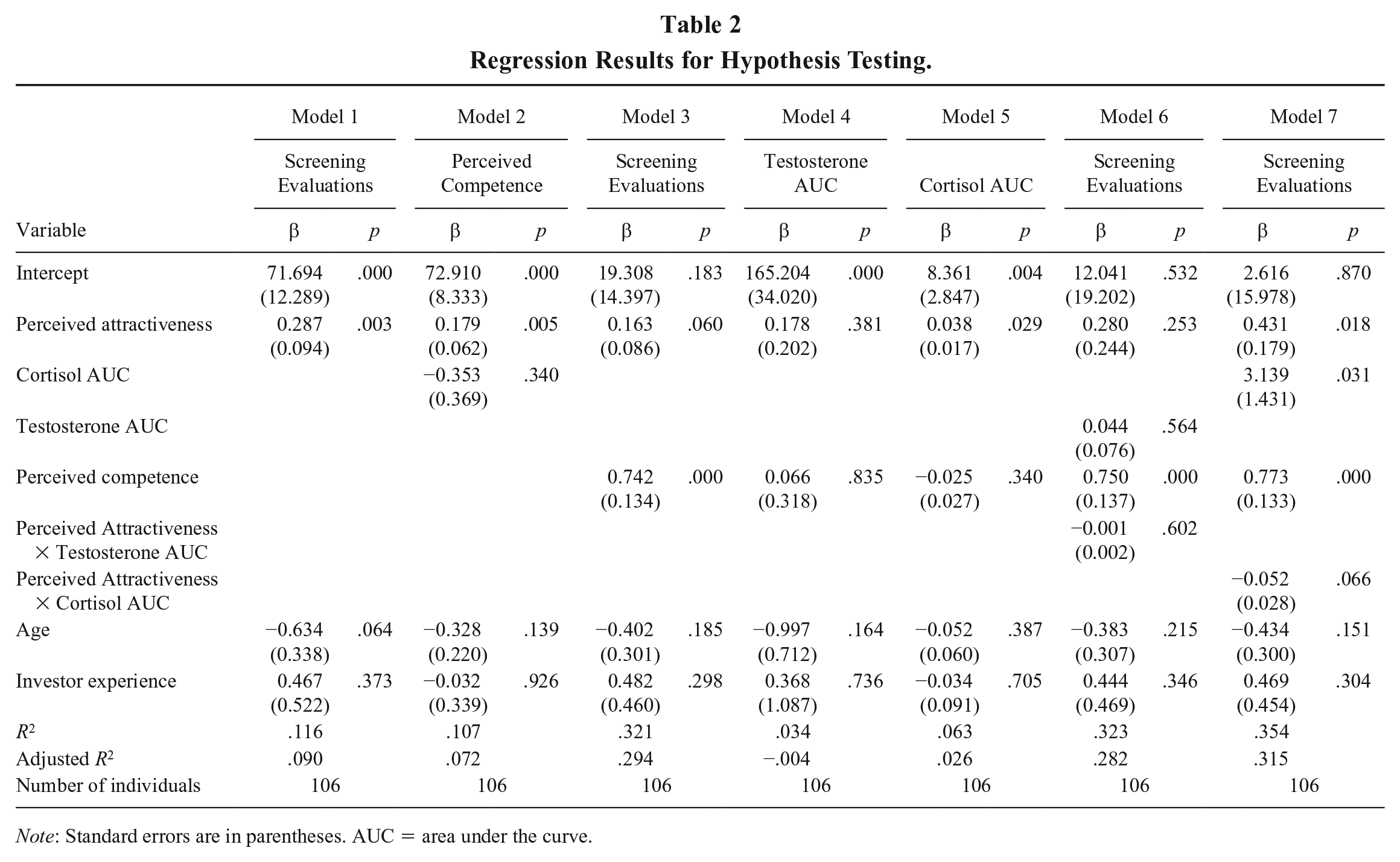

To test the hypothesized model in Figure 1, we used linear regression and tested the mediation effect by bootstrapping 10,000 random resamples (with replacement) of the data (Revelle, 2018). We constructed a model that would demonstrate the direct, indirect, and conditional indirect effects of our variables of interest on the investors’ screening evaluations. We report the results in Table 2.

Regression Results for Hypothesis Testing.

Note: Standard errors are in parentheses. AUC = area under the curve.

The initial model testing the total effect of the women entrepreneurs’ attractiveness on the men investors’ screening evaluations showed a significant positive effect (p = .003; Model 1 in Table 2). Next, we tested the hypothesized mediation of the cognitive pathway. We found a positive relationship between the women entrepreneurs’ perceived attractiveness and the men investors’ perceptions of the entrepreneurs’ competence (p = .005; Model 2 in Table 2). The positive coefficient demonstrated that the woman entrepreneur the men investors perceived as more attractive was considered more competent overall. This finding is significant in the opposite direction proposed in Hypothesis 1; thus, Hypothesis 1 is not supported. However, Hypothesis 2 is supported by these results. The full model demonstrated that the woman entrepreneur the men investors perceived as more competent received more positive screening evaluations for the venture (p = .000; Model 7 in Table 2).

The mediation analysis further showed that the men investors’ attributions of the women entrepreneurs’ competence partially mediated the relationship between the women entrepreneurs’ attractiveness and the men investors’ positive screening evaluations of the venture. The indirect effect of competence was significant based on a bootstrapped confidence interval (indirect effect [ab] = 0.129; SE = 0.072; 95% confidence interval

For the physiological pathway, we first tested whether the men investors provided more positive screening evaluations of the venture for the more attractive woman entrepreneur than for the less attractive woman entrepreneur while controlling for perceived competence. We found marginal significance for Hypothesis 4 (p < .060; Model 3 in Table 2). When competence was included as a mediator, the coefficient of perceived attractiveness decreased from 0.287 in Model 1 to 0.163 in Model 3.

Next, we tested whether the men investors experienced higher hormone levels (testosterone and cortisol) when observing the more attractive woman entrepreneur compared with the less attractive woman entrepreneur. Perceived attractiveness did not significantly affect testosterone (p = .381; Model 4 in Table 2). Thus, Hypothesis 5a was not supported. However, in support of Hypothesis 5b, we did find a positive relationship between perceived attractiveness and cortisol levels (p = .029; Model 5 in Table 2).

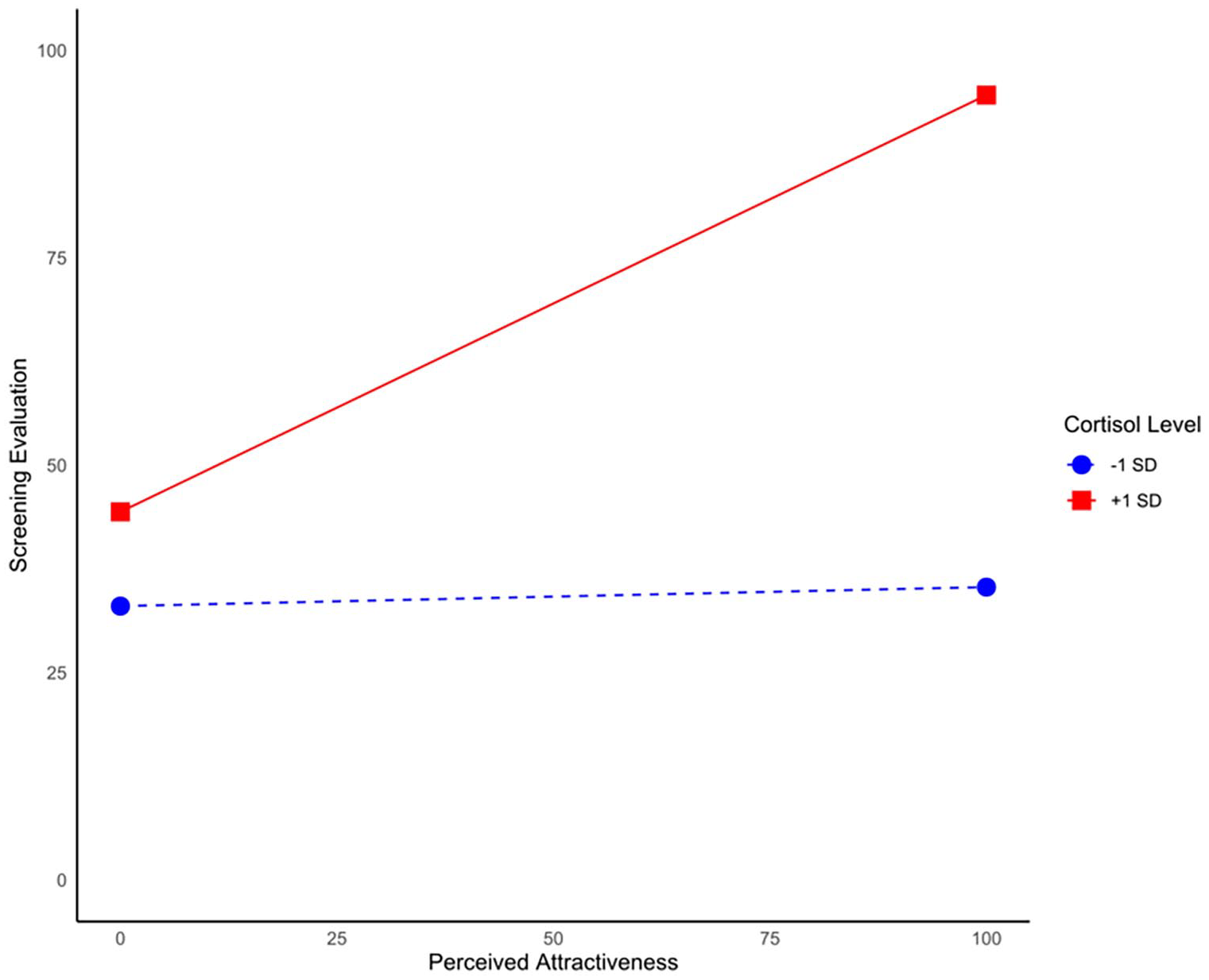

In the last step, we tested if the positive relationship between the women entrepreneurs’ attractiveness and the men investors’ positive screening evaluations of the venture was more positive for the men investors who experienced higher hormone levels than for those who experienced lower hormone levels. After including testosterone as a moderator, we did not find support for Hypothesis 6a (p = .602; Model 6 in Table 2), and the overall model fit slightly decreased (

Interaction Effect of Cortisol Levels and the Perceived Attractiveness of Women Entrepreneurs on Screening Evaluations Among Men Investors

Final Model Showing the Effects of Perceived Competence as a Mediator and Cortisol as a Moderator of Perceived Attractiveness on Screening Evaluations

Effect Sizes

We found that the attractive woman entrepreneur had, on average, a 68.94% chance of advancing to the next step of the investment process versus 56.64% for the less attractive woman entrepreneur. A two-tailed t test confirmed this difference in the men investors’ screening evaluations, t(104) = −2.50, p = .014. Therefore, the attractive woman entrepreneur was 21.72% more likely to pass the screening stage to progress to the next stage of the investment process. We also found that the men investors perceived the attractive woman entrepreneur as more competent, with a mean rating of 68.45, compared with the less attractive woman entrepreneur, with a mean rating of 63.06 (the highly attractive woman entrepreneur was perceived as 8.55% more competent than the less attractive woman entrepreneur). We found that the men investors evaluating the attractive woman entrepreneur had a mean cortisol AUC level of 6.76. In contrast, the men investors assigned to the less attractive woman entrepreneur had a mean cortisol AUC level of 5.44 (the average cortisol level of the men investors evaluating the more attractive woman entrepreneur was 24.26% higher). Notably, in Model 7, we observed an increase in the outcome linked to the main effect of cortisol (coefficient of 3.139) and perceived attractiveness (coefficient of 0.431), accompanied by improved model fit (

Discussion and Implications

Researchers have long argued that physical attractiveness is one of the most powerful characteristics in biasing decisions (Agthe, Spörrle, & Försterling, 2008; Baker & Maner, 2008; Hamermesh & Biddle, 1993; Ruffle & Shtudiner, 2015). However, during our interactions with early-stage start-up investors while collecting saliva samples, we frequently encountered the belief that an entrepreneur’s physical attractiveness does not significantly influence their investment decisions. Instead, they believe their decisions are determined by a variety of factors, including the quality of the product or service being offered, the strength of the business model, the experience and expertise of the founding team, and the overall market conditions (Gompers, Gornall, Kaplan, & Strebulaev, 2020; Zacharakis & Meyer, 1998). However, we expand the existing theory that attractiveness triggers investors’ cognitive and physiological responses. In turn, these responses affect investors’ decisions. In particular, investors’ physiological responses represent a subconscious pathway through which women entrepreneurs’ attractiveness influences men investors’ decision-making, positively impacting these investors’ screening evaluations such that attractive women entrepreneurs’ ventures are more likely to progress to the next stage of the investment process.

These results have several implications for the entrepreneurship and decision-making literatures. In the literature studying pitching events and entrepreneurs’ presentations, scholars have tested the effects of language patterns, gestures, and passion in entrepreneurs’ pitches to investors—one of the most critical situations during fundraising (Anglin, Short, Drover, Stevenson, McKenny, & Allison, 2018; Clarke, Cornelissen, & Healey, 2019; Shane, Drover, Clingingsmith, & Cerf, 2020). However, researchers have paid little attention to the relevance of presenting founders’ attractiveness, as done in this study. Attractiveness strongly influences investors’ impressions of founders’ capabilities and investors’ gut feelings about an early-stage investment, which can trump deliberate reasoning (Eagly et al., 1991; Huang & Pearce, 2015). Indeed, our findings indicate the relevance of physical appearance triggering investors’ physiological responses when considering women entrepreneurs, which has gone unnoticed in prior entrepreneurial finance research.

Considering the literature on gender biases in entrepreneurial finance, our results contribute to a deeper understanding of why some women are assessed differently than other women. By now, it is well understood that women entrepreneurs receive significantly less funding than men entrepreneurs (Balachandra, 2020; Bird & Brush, 2002) and that several biases lead to this situation, including unconscious biases, stereotypes, and a lack of diversity among investors (Kanze et al., 2018; Snellman & Solal, 2023). Although studying these biases between women and men is of major importance, focusing on biases within one gender can provide a deeper understanding of the specific issues faced by individuals within that gender, which can be particularly useful for identifying and addressing areas of inequality. We focused exclusively on women entrepreneurs to contribute to such an in-depth understanding. We found evidence that some women face greater biases than other women—namely, women entrepreneurs perceived by men investors as less attractive are biased against more than women entrepreneurs perceived as more attractive.

Specifically, our study shows a positive mediation effect of appraised entrepreneurial competence on the relationship between men investors’ perceptions of women entrepreneurs’ attractiveness and their screening evaluations of start-ups led by women entrepreneurs. This finding of a beauty premium is contrary to studies in management showing that physical attractiveness disadvantages women in managerial positions due to perceptions that attractive women lack competence (Glick et al., 2005; Johnson et al., 2010). This difference between our findings and previous research may be due to the nature of the intentions of the raters of perceived competence. Indeed, managers in organizations might compete with colleagues in their career advancement and hence be inclined to discriminate against them based on physical appearance (Charney & Gulati, 1998). Research has shown that women in management positions face resistance not only from men colleagues (Cotter, Hermsen, Ovadia, & Vanneman, 2001; Riger & Galligan, 1980) but also from their women peers (Derks, Van Laar, & Ellemers, 2016; Staines, Tavris, & Jayaratne, 1974) as they may be viewed as competition, which can lead to negative perceptions and evaluations of their competence (Glick et al., 2005; Heilman & Saruwatari, 1979).

However, our findings regarding a positive relationship between attractiveness and competence that increases men’s screening evaluations of women entrepreneurs’ ventures are supported by some studies in the literature. Previous studies have shown a stronger correlation between attractiveness and perceived competence in judgments of women compared with judgments of men (Menegatti et al., 2021). As for the direction of these effects, studies in the context of electoral research have demonstrated that judgments of attractiveness occur before judgments of competence, so the former are likely to exert a downstream effect on the latter (Verhulst et al., 2010). These findings uphold the beauty-is-good theory, demonstrating a positive effect of attractiveness on individuals’ perceptions. They also align with evolutionary hypotheses, supporting an attractiveness bias presumably tied to underlying reproductive motivations (Maestripieri et al., 2017). Ultimately, our finding that attractiveness leads to more positive screening evaluations for women entrepreneurs mirrors a finding that more attractive men entrepreneurs are more persuasive vis-à-vis their less attractive peers (Brooks et al., 2014).

For the literature on decision-making, our findings evidence irrational decision-making. We drew on two themes from the psychological literature to investigate whether rational and unconscious factors influence investors’ decisions. These themes explain how conscious and unconscious mechanisms align or misalign and lead to biased assessments. For instance, research has revealed that people show preferential and nonpreferential treatment toward those they consider attractive depending on the focal individual’s gender and the overall context (Nisbett & Wilson, 1977). Despite growing calls to incorporate biological explanations for many aspects of entrepreneurship, scholars have conducted only a few studies that do so (Nicolaou, Phan, & Stephan, 2021). With this study, we contribute to this recent nascent stream of research by exploring the link between physiological reactions to and conscious cognitive assessments of women entrepreneurs and how these pathways impact men investors’ screening evaluations (Day, Boardman, & Krueger, 2017). Opening the black box of investors’ implicit biases can help clarify their decision-making, which may help investors develop effective strategies and interventions to improve their decision-making—for example, by reducing or eliminating the bias based on women entrepreneurs’ attractiveness when assessing their competence and deciding whether to fund their ventures. Furthermore, physiological measures, such as those captured through saliva samples, provide objective data. These measures are generally considered more reliable than commonly used self-reported measures from investors because they are less influenced by subjective factors, such as presenting oneself in a particular way (Eatough, Shockley, & Yu, 2016).

We contribute two primary insights to the discussion on dualistic decision models and how explicitly rational, deliberate, and more intuitive processes relate to decision-making (Grayot, 2020). First, we show that attractiveness (of women presenters) stimulates chemical messengers (in the audience of men investors). Therefore, despite professional investors’ claims that they solely rely on rational factors in the screening evaluation process, we provide insights into how and when (or, more precisely, against whom) those decisions are biased and how unconscious intuitive factors reinforce this bias in their decision-making. Second, we did not find interference between the conscious and unconscious pathways, as is often suggested in dualistic decision models (Abelson & Rosenberg, 1958; Denes-Raj & Epstein, 1994; Grayot, 2020). Instead, our study provides evidence of a decision-making situation in which the conscious and unconscious paths align in their effects, with physical attractiveness being a stimulus triggering this alignment (Archer, 2006; Goldey & van Anders, 2012; van der Meij, Demetriou, Tulin, Méndez, Dekker, & Pronk, 2019).

Practical Implications

Finally, we highlight some of our study’s practical implications, focusing on fostering change within the investor community. Raising awareness among men investors about the unconscious biases elucidated in this study that influence their screening evaluations is paramount as recognizing and addressing these implicit mechanisms can lead to more informed and equitable investment decisions. Investors must recognize the economic benefits of diversity and actively seek investment opportunities in women-led ventures (or, at a minimum, not discriminate against them). Indeed, research has indicated that gender diversity contributes to economic gains by enriching the workplace, increasing the creative capacity within firms, improving innovation performance, and leading to a pay premium for high-potential women. Studies have also shown that gender diversity enhances productivity and wages by widening employee perspectives, providing greater resources for problem resolution, and strengthening teams (Becker-Blease & Sohl, 2011; Dai, Byun, & Fang-sheng, 2018; Leslie, Manchester, & Dahm, 2017). Additionally, gender diversity has been linked to increased innovation performance in new venture teams as it influences investment behavior and contributes to the success of venture capital investments (Becker-Blease & Sohl, 2011; Dai et al., 2018; Leslie et al., 2017). Furthermore, research has highlighted the benefits of a climate of inclusion for gender-diverse groups, emphasizing the positive impact of gender diversity on overall group functioning and performance (Nishii, 2013).

Therefore, we encourage (investor) networks, institutional stakeholders, and coaches to consider how to best manage biases against women based on their physical appearance. Awareness training could include discussing how superficial physical features influence investors’ assessments of women entrepreneurs. Informed investors may challenge their unconscious reasoning to judge women’s investment proposals more effectively. Awareness of gender biases is known to decrease their effect on subsequent behavior (Kalra & Boukes, 2021; Mengel, 2021). As such, disseminating our findings might decrease biased decision-making regarding screening evaluations. For example, in a recent investigation of scientific evaluation committees, groups with strong implicit biases promoted more women when they were informed of an ongoing study on gender biases (Régner, Thinus-Blanc, Netter, Schmader, & Huguet, 2019). The authors observed that presenting evidence of the existence and impact of systemic biases decreased the influence of implicit gender biases on the committees’ decision-making process.

Women entrepreneurs seeking funding can also benefit from our findings by raising awareness of the systemic biases they face in the investment arena. Once investors are aware of these issues, they may be less likely to be guided by gender-biased decisions when determining whether to fund a specific initiative. In light of the challenges women entrepreneurs face in accessing venture capital and being exposed to biases caused by factors like attractiveness, they should consider proactively improving factors they can influence. For example, it has been shown that building strong networks, joining accelerators, and strategically navigating investor interactions significantly improve the likelihood of raising funding and can diminish the effect of biases based on superficial features. Academic research has underscored the pivotal role of networks in facilitating deal sourcing, syndication, and decision-making process in the venture capital landscape (e.g., Jääskeläinen & Maula, 2014). Thus, efforts to build a strong network can foster supportive relationships and mentorship opportunities, empowering women to navigate the funding landscape effectively. Moreover, education initiatives to enhance women’s understanding of the funding process and strategies to counter biases, such as answering prevention-focused questions with a promotion-focused answer (Kanze et al., 2018), can be instrumental in closing the gender funding gap. Accelerators also play a vital role in providing mentorship, capital, and connections, especially for women-led startups (Dams, Allende, Cornejo, Pasquini, & Robiolo, 2021).

Limitations and Directions for Future Research

As with all studies, the current study has limitations that provide avenues for future research. First, the physiological system is complex, so further research on different hormones (other than cortisol and testosterone) is necessary to understand the complexity of unconscious chemical messengers and their effects on decision-making and biases. For example, dual-hormone theory suggests that certain physiological effects of testosterone on status-seeking behavior depend on cortisol levels (Mehta & Josephs, 2010; Mehta & Prasad, 2015)—an interaction effect of different hormones. We explored this possible relationship (post hoc) but did not find a statistically significant relationship. Still, future research may focus on the role of other hormones and neurotransmitters, such as estradiol, oxytocin, dopamine, and serotonin, in early-stage venture investment decisions that may reveal a more complex role of testosterone (and offer an alternative explanation for the nonsignificant findings for the mediation effects involving testosterone).

Second, our study advances knowledge on gender biases by taking a fine-grained approach to investigate the mixed-gender effect of women presenters’ attractiveness on men’s decisions in the context of what is typically considered the masculine domain of entrepreneurship. We intentionally chose an experimental design to focus on the key relationships and to draw clear conclusions about causality. Furthermore, we focused exclusively on men investors and women entrepreneurs, which reflects the dominance of men in this source of funding—80% to 93% of investors are men (EBAN Statistics Compendium, 2017; Lerner & Nada, 2020; Sohl, 2018)—and the situation of women receiving significantly less funding than men (Brush & Greene, 2020; Joint EIF–Invest Europe, 2023; McCarthy, 2018; PitchBook & All Raise, 2019; PitchBook & National Venture Capital Association, 2016; Skonieczna & Castellano, 2020). It would be interesting to determine if the findings also hold for women investors evaluating women and/or men entrepreneurs who vary in attractiveness.

While we would have ideally included women investors in our study, several factors influenced our decision to focus exclusively on men investors. First, we aimed to shed light on the challenges faced by a marginalized group in entrepreneurship—namely, women entrepreneurs seeking funding—who may encounter heightened biases due to their physical attractiveness, which are known to influence first impressions (Fultz et al., 2023). Furthermore, logistical constraints posed significant challenges, including difficulties in recruiting a sufficient number of experienced women investors to find significant effects. Last, the complexities of comparing hormonal effects across genders, such as the significant differences in testosterone and cortisol levels, further complicates gender comparisons (e.g., Apicella et al., 2008; Archer, 2006; Coates & Herbert, 2008; Kudielka & Kirschbaum, 2005; Santoro & Wierman, 2021). Despite these limitations, we acknowledge the importance of including women investors in future research endeavors to provide a more comprehensive understanding of gender-specific influences on decision-making in the venture capital context. With this study, we present initial findings on how physiological responses can impact the decision-making of the early-stage venture investment decision-making of men investors. We hope to stimulate further inquiry and establish a foundational framework for future research.

Similarly, while our sample mainly consisted of heterosexual investors, it is essential to extend this investigation into nonheterosexual populations. These individuals are known to exhibit more intense stress responses than their heterosexual peers (Juster et al., 2015). As such, our findings cannot necessarily be generalized to nonheterosexual individuals or to different gender-combination pairs. Given the growing literature on the participation of lesbian, gay, bisexual, transgender, and queer people in the corporate world (Brahma, Gavriilidis, Kallinterakis, Verousis, & Zhang, 2023), it may be relevant to study their investment practices. While the representation of diverse populations in the corporate world and the entrepreneurial literature is growing, such studies are still nascent, and dedicated investigations of these populations are lacking.

Third, we are aware that venture capital investors typically include their partners in decisions and, likewise, that business angels often have rigorous exchanges within their networks about potential investments (Huang & Pearce, 2015; Petty & Gruber, 2011; Skalicka et al., 2023). Indeed, decision-making can be influenced by various social factors, including group dynamics, social pressure, and the need to conform to group norms and expectations (Butticè, Croce, & Ughetto, 2021; Mason, Botelho, & Harrison, 2019). Given the significance of group dynamics in investment decisions, future research holds immense potential in exploring how these dynamics interact with unconscious chemical mechanisms involved in investors’ decision-making. Investigating such interactions could offer invaluable insights into how group composition, including predominantly male or more gender-balanced teams, influences decision outcomes. Moreover, future studies could explore how initial reactions during the screening process differ from decisions made over time as investors have more opportunities to deliberate and assess the potential of investment opportunities.

Finally, since our focus was on the results of physical attractiveness ratings rather than other features of the entrepreneurs’ presentations, we did not evaluate variables like vocal pitch, tone, and other voice characteristics. We did control for the content of the start-up pitch, but certain variations in how the material was delivered may have occurred due to individual differences. Indeed, vocal tone can affect the persuasiveness of a pitch (Wang, Lu, Li, Khamitov, & Bendle, 2021), and certain speech melodies are associated with traits like charisma, confidence, and likeability (Carlson, 2017; Niebuhr & Neitsch, 2020). Since these factors can also affect funding outcomes, they may have influenced our findings. We cannot exclude a joint or overlapping influence of these features on the investors’ screening evaluations, in addition to the physical attractiveness of the entrepreneurs.

Conclusion

There has been an increase in the desire to understand how investors make decisions. However, only a few behavioral studies have investigated biases in early-stage venture investments, for which limited financial data or other information is available and for which investors tend to rely on their gut feelings. Our study combines cognitive and physiological data to investigate such biases, examining the impact of women entrepreneurs’ physical attractiveness on men investors’ decisions to progress the entrepreneurs’ ventures through the screening stage. Our results suggest that “hot,” unconscious factors—rather than just “cold,” rational factors—play a role in early-stage venture investment decisions. While this study is specific to men investors and women entrepreneurs, it contributes to the ongoing discussions on dualistic decision models, the impact of unconscious biases on screening evaluations, and the understanding of the gender funding gap by looking at differences within women entrepreneurs in their interactions with men investors. However, this study’s emphasis on the partial physiological basis of the attractiveness bias in investment decisions does not justify its continuation. Instead, it highlights the need for proactive measures and strategies to counteract cognitive and physiological biases.