Abstract

Entrepreneurial finance varies as per the startup stage, such as bootstrapping, crowdfunding, angel investors, venture capital (VC), banks and initial public offer (IPO). Many times, entrepreneurial finance comes with knowledge, experience, innovation, value, etc., in addition to the fund brought in. Venture capitals are the most common such contributors. This study illustrates some significant value-added activities by venture capital firms operating in India. It explores some evidence from venture capitals such as Tiger Global, Accel Partners and DST Global who fund Flipkart, an Indian e-commerce firm.

Discussion Questions

What are the different forms of entrepreneurial finances at various stages of a startup firm?

What can be some of the non-financial or value addition roles of venture capital (VC) firms in a startup firm’s success?

Establish some examples of non-financial or value addition roles played by VC firms such as Accel Partner and Tiger Global for Flipkart?

Introduction

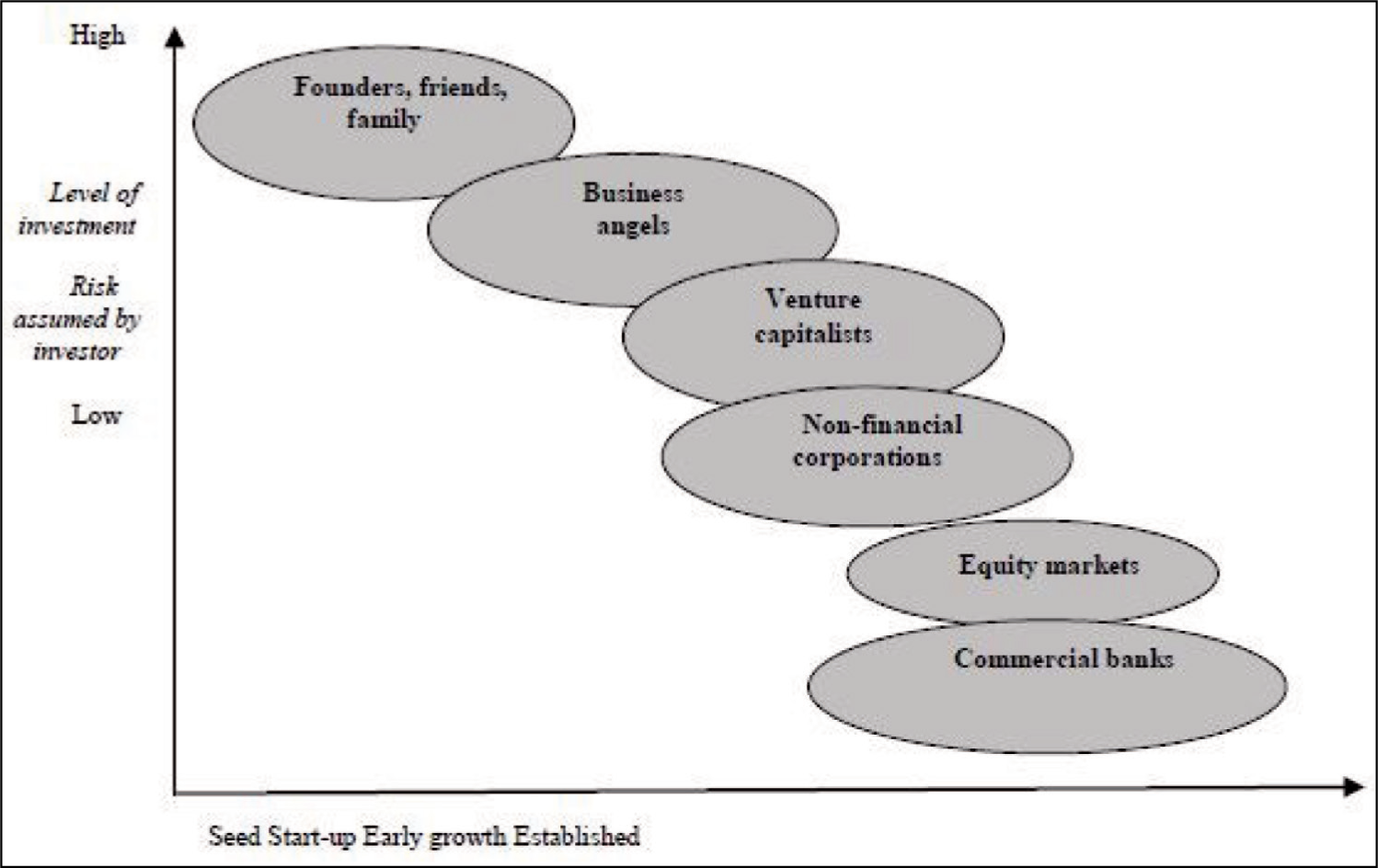

Venture capital, one of the many sources of entrepreneurial finance, played a vital role in economic growth, especially in emerging markets like India, by supporting new business creations or startups. The new business creation rate was enhanced by VC investments (Popov & Roosenboom, 2013). The contribution of VC to economic growth has been proven in many studies. There was a huge contribution by American VCs in economic and innovation growth in the USA (Gu et al., 2017). One such example of growth included a big increase in the number of employees in VC companies after receiving funding (Davilaa et al., 2003). In the last two decades in the US economy, VCs were significant, seeding major technological firms, which contributed to the national economy to a large extent, such as Microsoft, Compaq, Sun Microsystem and Oracle, thereby introducing innovation in the market, bringing in a lot of employment, economic growth, and scope for newer technological innovation and development (Jeng & Wells, 2000). According to Geronikolaou and Papachristou (2012), in Europe, an increase in innovation caused a rise in demand for VCs to fund them. There was no alternative, implying that the innovative ideas could not be introduced in the market for commercialization without venture capital. Also, venture capital and innovation were some drivers of the growth of long-run per capita income in selective European countries (Pradhan et al., 2017). When these startups were new and technology-intensive with little information, traditional finance channels were not eager to fund them, especially in not-so-matured markets like India. This is due to the high risk associated with startups, despite their high growth potential. Venture capitals only funded such high potential technology startups after evaluating, many a time, management expertise, which the entrepreneurs needed to prove (Baum & Silverman, 2004; Gompers, 1995). With a huge youth population and diversity, India was an emerging market with many technology students who were coming up with a lot of new ideas. One of the immediate requirements of every startup was capital; to survive and scale up the new venture. The startups also needed expert guidance in refining ideas, product designing, operations, marketing, etc., at every stage of the startup. Many entrepreneurial ventures die because of a lack of proper strategy and capable management to scale up, not from lack of capital. Entrepreneurial finance or funding a new startup was generally in the form of owner’s fund, bootstrapping, crowdfunding, angel investor, VC, initial public offer (IPO) and merger and acquisition, etc., as per the stage of development of the firm (Vasilescu, 2009) as in Figure 1. Entrepreneurial finance depended on startup age, business size, and ownership type (Fraser et al., 2015). Small businesses had a financial growth cycle and a startup growth cycle, in which funding sources and needs changed as they grew and matured (Berger & Udell, 1998). According to them, the stages of startup business had been named as an infant (0–2 years), adolescent (3–4 years), middle-aged (5–24 years), and old (above 25 years). There was no legitimate division of stages of growth and source of entrepreneurial finance. These were relative measures, not absolute criteria, which were observed in small business growth and practices (Gompers, 1995). According to Bain & Company (2016) report the government grants, internal funds, that is, own savings or crowdfunding, and angel investors were generally used while the concept or idea was converted to the startup stage. Other seed funds like a mix of angel and initial VC were used to convert startup to growth stage. The portion of VC increased as series A, B, etc., during the startup firm’s growth stages. Next came the expansion stage at which VCs existed and startup firms went for a public market like IPO. This financial escalation of a startup was discussed in four non-overlapping stages by Van Osnabrugge (2000) and Reitan and Sorheim (2000), namely first stage funds from founders, friends, and family, second stage funds from informal investors (angels), third stage funds from institutional VC and banks, and lastly fourth stage funds from the IPO. Similar studies of entrepreneurial finance like Murzacheva and Levie (2020) linked the four-stage of development of startup with different types of source of the finance-concept-proving period with own savings, family, and friends, and partially from grants, pre-trading period with business angels, public grants, and crowdfunding, commercialization period with VC and banks, and expansion period with the public (stock) market.

The owner’s fund was the founders’ or owners’ capital without charging any interest on it and without any security for the fund. Bootstrapping was similar to financing from its saving or internal sources. Crowdfunding was generally the process of raising funds for startup businesses from many sources or supporters, usually through internet platforms. It was a funding process by numerous individuals, and not professionals, unlike VC or angel investors. Crowdfunding did not need an intermediary, and so, entrepreneurs directly contacted individuals (Schwienbacher & Larralde, 2012). It was prevalent among entrepreneurial finance because of the liability of newness and efficiency to run a startup (Winborg, 2015). Other advantages of crowdfunding included public attention and validation of their idea (Schwienbacher & Larralde, 2012). Mediator websites provided links between waiting investors and idea generators. Examples of crowdfunding platforms in India were Ketto, Wishberry, Rangde.org, Faircent, etc. Angel investors were wealthy individuals who supported the idea financially at a very early stage without charging interest. Usually, angel investors were friends, family members, or persons who loved the idea without caring about the project’s risk of failure. They could ask for ownership equity or convertible debt. Sometimes, individual angels grouped together to make syndicate, transforming from a personal approach to portfolio management, enhancing efficiency, and mitigating risks (Mason et al., 2016; White & Dumay, 2017). The fast-growing phenomenon of crowdfunding, microfinance, and individual-to-individual lending filled some of the financial gaps of startup ventures (Bruton et al., 2015). However, the angel fund and crowdfunding were limited by individual investors’ wealth (Jeng & Wells, 2000).

The most common source of funding for startups was venture capital. Venture capital was a pool of professional investors who looked for innovative startups that had the long-term potential to grow. European Venture Capital Association’s (EVCA) terminology split VC into three stages: seed finance to support their initial concept and startup finance to develop its product and expansion finance. Similarly, Pradhan et al. (2017) categorized VC investment into early stage, later stage, and stage investments. But venture capitals invested their capital for a short term and left at high return by selling off their equity share in the form of public offers or mergers and acquisitions.

Interestingly, VC invested traditionally across geographical borders (Devigne et al., 2018). Venture capital had a say in the decision-making process too. Such value-added activities were crucial for the firm to scale up and survive. The past studies showed that companies backed by VC were comparatively more successful (Jeng & Wells, 2000). The knowledge of different entrepreneurial finance types along the various stages of a startup was very useful for all decision-makers and support systems. Irrespective of the above discussion, the source type of startup funding did not solely depend on the stage of growth. It also depended on different aspects, including business type, location, preparation, research, pitching abilities of an entrepreneur, and others (Jeffrey et al., 2016; Kotha & George, 2012). Many studies focused on a specific source of finance. This case study discussed the value additions of VC in detail. The later stage finance commonly approached by startup firms was a public offer or stock market. An IPO raised funds from the public by the firm through a secured and regularized exchange. The public purchased the ownership in the form of equity shares or debt. To expand or scale-up, smaller firms could also merge or be acquired by larger firms. As investors felt the risk to fund startups, the expected return on financing new enterprises was very high, that is, typically 25–45% p.a. for VCs (Halt et al., 2017). That was why the investors monitor, interfere and support the performance of the startup (Macmillan et al., 1989). Many times, founders or entrepreneurs found it valuable for the firm’s growth (Thillai, 2010). Here, this study tried to understand the extent of VC involvement in a startup’s growth.

Venture Capital Definition and Its Importance

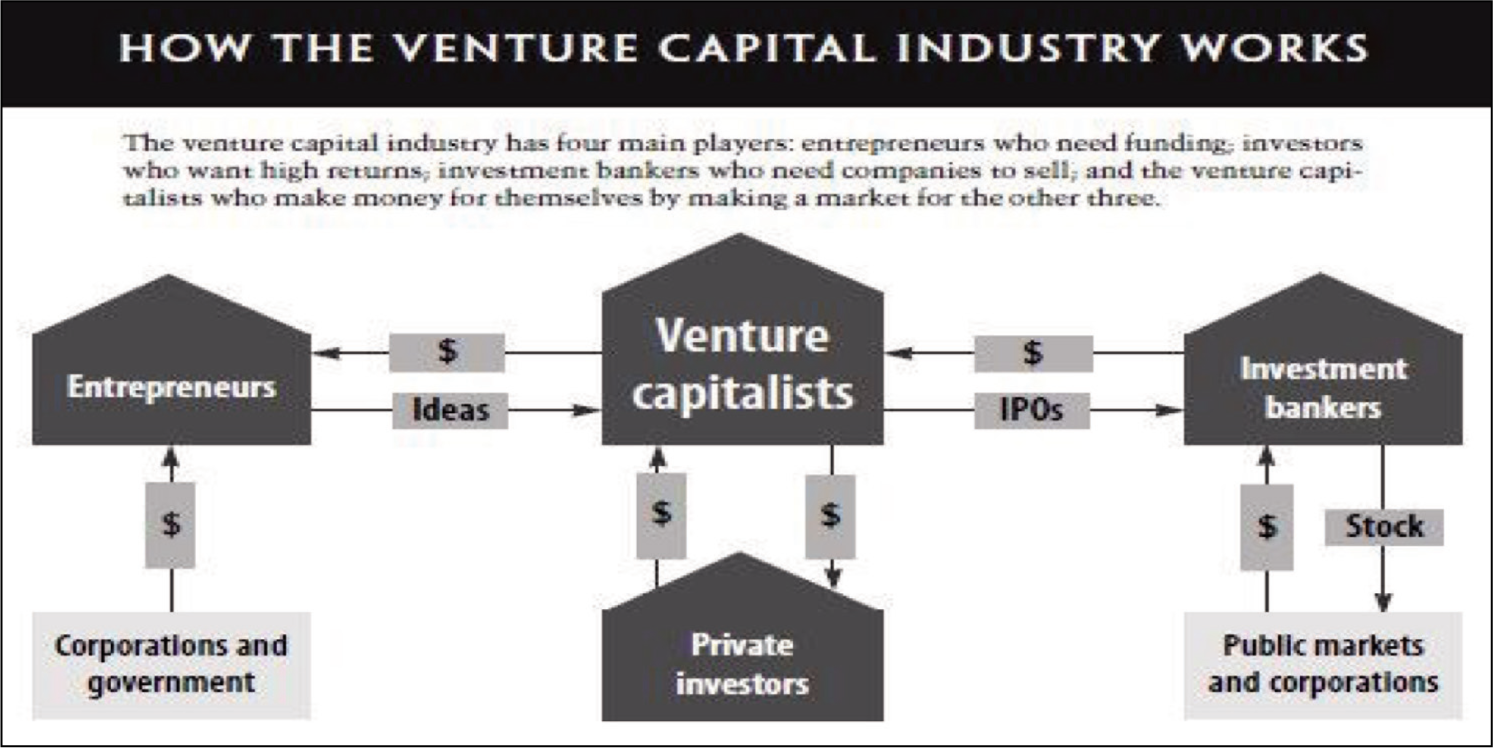

Venture capital was a type of professional financial intermediary in which institution or wealthy investors brought the money and invested in newly started firms which seemed to have a high potential for future growth. It was also a private equity investment in publicly and privately held companies (Jeng & Wells, 2000). As other sources of capital were not easily approachable, in maximum cases, entrepreneurs got their initial funds from VC, as shown in Figure 2.

For example, banks demanded collateral security and high-interest charges. Strict regulations blocked newly formed firms to go for public equities. Venture capital filled this gap between capital requirements by the startups and seed funds available. At present, investors in many VCs were of large financial institutions such as pension funds, insurance funds and university endowments (Zider, 1998). For example, VC firm Accel Partners had Delaware Public Employees’ Retirement System as one of the investors. As per Bloomberg, Helion Ventures had Mayo Clinic Master Retirement Plan, and Sequoia Capital India had Duke University Pension Plan as one of the fund holders. These VC firms were all active in India. India was one of the leading destinations for VCs (Thillai & Deshmukh, 2009).

As VCs invested in risky startups or ventures, their expected return was higher than other alternative sources of funds. That was why VCs monitored the performance of the firm they invested in, and their target was to exit at a higher valuation point at the shortest by IPO or merger and acquisition, even before the breakeven of the startup. VCs were not only infusing capital to the enterprises, but they were also helping them with non-financial value additions. The investors in the VC –institutions or individuals had a lot of experience in their domains. The network of VC was also one of the sources of knowledge. It could be in the form of planning, strategy, market opportunities for expansion, operation, and legal aspects (Berglund et al., 2007; Elfring & Hulsink, 2003; Hsu 2004; Panda & Dash, 2016). These were vital for successful growth and expansion of the startups. As a result of continuous monitoring and interference of VC with entrepreneurs’ functions, sometimes, conflict arose between the venture capitalist and the entrepreneur (Higashide & Birley, 2002; Jensen & Meckling, 1976; Panda & Dash, 2016). But there was evidence of success and a lot of research supported the significant role of venture capitalists and found that there was a cooperative synergy between the entrepreneur and investors.

The Scenario of Venture Capital Investment in India

The emergence of VC in India was a recent phenomenon compared to the USA and Europe. Earlier, individual investors and financial institutions were the main formal sources of capital. The institutional financiers such as IDBI, ICICI and IFCI were pioneers in small technology startup funding during the mid-80s. In the private sector, regional players such as Gujarat Venture Finance Ltd., ICICI Ventures and Actis Capital emerged during the 1990s (Dave & Banerjee, 2014). For the first time, in 1973, a committee on ‘Development of Small and Medium Enterprises’ pointed out the significant role of VC as a source of capital for startups. In 1988, based on the World Bank report on the possibility of developing VC in India, the Government of India showed its initiative publishing guidelines for VC funds (Kohli, 2009). SEBI looked after VC and private equity investment regulations in India. In terms of investment, the value of deals with VC in Q1-2016 was reported to be $1.59 billion as per the online magazine Inc42 report, and it was, till September 2015, $1.44 billion as per Business Standard report. As per the report of Bain & Company Ltd. published by Indian VC and Private Equity Association, the total private equity investment in India in 2015 came to be approximately $22.9 billion, which included a top deal of $700 million of Flipkart; raised from one of its existing VCs, Tiger Global. Though VC and private equity investment in India were growing, most of them were foreign investors (Dave & Banerjee, 2014). The Indian VC was very encouraging, with the capital deployment of $10 billion in 2019, which was 55% higher than that of 2018 as per Bain & Company-Indian Venture Capital Report 2020. During 2019, the share of Indian VC investment in the global VC market stood approximately 4%, and this was approximately 16% of total private-market investment (Mustafa, 2019).

Value-Added Activities of Venture Capitals

The value-added activities of VC had been widely studied and acknowledged. While investing, they took a keen interest in profitable exit from the firm within 2–3 years. And so, VCs took an active role in monitoring, strategic advice, recruitment of top management, marketing, operation, product design, network building, additional fundraising, technology, team building, etc. The entrepreneurs lacked experience and skills, while VC investors gained experience and knowledge about various emerging market technologies. Their presence in the startup also boosted the valuation of the startup in the market (Denis, 2004). The monitoring role of VCs showed frequent visits to the firm and a higher number of presentations on the firm’s board of directors. In the Indian context also, a study on value-added services (other than financing) by Indian VC firms showed that 19 out of 32 firms responded positively (Kumar, 2013). The study also indicated that the other value-added services such as marketing, customer network and monitoring tended to increase with the increased financing. It enabled the control of the governance of the firm. There were occasions of replacement of CEOs and top management of the firms by the VC in serious issues. A study by Kaplan and Stromberg (2004) showed that VCs determined the area in which monitoring was required. Hellmann and Puri (2002) found that firms backed by VCs offered more professionalism in human resource policies, recruitment, and stock options than those without VC’s backing. The study also found VCs helped firms with their innovative level and enabled the firms to bring their product to the market at the earliest. During exit valuation, VC acted as a genuine certification of the firm. Megginson and Weiss (1991) showed that firms backed by VC, which was a repeat player with a lot of success stories, lowered underpricing in IPOs than non-VC-backed firms.

In short, some of the value-added activities of VCs brought new ideas, monitoring financial performance, monitoring non-financial performance, development of new strategies, crisis management, helping merger and acquisition, seeking additional finance, introduction to new customers and suppliers, recruitment of staff and top management, technology platform, marketing and networking, operations planning, etc. (Kumar, 2013). In Mason (2005), they were also called ‘capital and consulting’ for the same reason. Informed entrepreneurs looked for VC with high managerial input capability, while their productivity was low (Bettignies & Brander, 2007). Informal involvement with entrepreneurs enabled VCs to monitor continuously; creating personal connections with stakeholders was another major value-added activity (Ahlstrom & Bruton, 2006). These were practices that were essential in emerging markets like India. The VC firm involvement, including business model change and bringing outside Chief Executive Officer, improved the firm (Gerasymenko et al., 2014). Kortum and Lerner (2000) studied the enhancement of R&D spend and patent activity due to VC support. VC-backed companies transferred the know-how to employees, thereby enabling spin-offs, and many employees dared to venture their ideas (Samila & Sorenson, 2011). India was witnessing many technology startups with uncertain and unproven tracks such as Flipkart, Ola, Tesla, Paytm, Bookmyshow, Oyo and Zomato giving varied services or products employing a large number of recruits every year, each trying to contribute to this emerging Indian economy. And given the above roles of VCs, this study takes up the case of Flipkart, an e-commerce startup, and its VCs.

Value-added Activities of Leading Venture Capitals Who Fund Flipkart

Flipkart was founded in 2007 by Binny Bansal and Sachin Bansal, both were from IIT Delhi, after a short stint at Amazon. Flipkart was started with seed funding of ₹400,000 only from founders’ savings (Rajan, 2020; The Economic Times, 2010). In January and February 2009, it received an angel investment of $40,000 and $100,000, respectively. Its early supporters were Julia Popowitze, David Popowitze, Lee Fixel, and Allan Kaplan, according to a website named angel.co. The first VC to step in the e-commerce firm was Accel Partners, which invested $1 million in October 2009. Since then, there were many rounds of funding from VCs, such as Accel Partners, Tiger Global, DIG, DST and Iconiaq Capital.

It raised $10 million and $20 million during 2010 and 2011 consecutively from a New York-based VC, Tiger Global, which held a major portion of the equity after a series of funding. The fourth round raised further $150 million from Naspers Group and Iconiq Capital on 24 August 2012 (Gutka, 2012). On 10 July 2013, Flipkart collected an infusion of $200 million from existing venture capitalists, namely Tiger Global, Accel Partner, Naspers Group, and Iconiq Capital (Dutta & Bhat, 2014). A group of new VCs, including Dragoneer Investment Group, Morgan Stanley Wealth Management, etc., funded a new capital of $160 million on 8 October 2013. In May 2014, it raised an additional $210 million from Hong Kong-based investor DST and from the existing investors, which included Tiger Global. In July 2014, Flipkart raised a historical amount for startups in India with $1 billion from investors like Tiger Global, Accel Partner, Morgan Stanley, and Singapore-based GIC (Thoppil, 2014). In December 2014, it again raised additional capital of $700 million from the existing investors. It raised $3 billion during 2015 with the help of some additional finances collected from various investors.

Simultaneously, Flipkart also gained value-additions from its associated VC from time to time in the form of company board members, help in manufacturer and supplier negotiation, selection of top management, recruitment of lower-level staff, etc. (Cumming et al., 2005; Davilaa et al., 2003; Hellmann & Puri, 2002). Such positive support from the right VCs at the right time encouraged many technology startups in the Indian startup ecosystem. In emerging economies like India, where the market was not matured in terms of VC laws, regulations, and protections, the success of Flipkart, funded by many VCs, was a learning curve and a motivating force for other startups in India. Some evidence on how leading venture capitals who funded Flipkart and provided value-added activities to this e-commerce startup has been observed, studied and discussed in this study.

VCs Helping Startups Monitor Operational Performance

Illustration from Flipkart: For Flipkart, which was an e-commerce startup, the major problem was not only the markdown of its valuation by many agencies, but it was also the increased operational expenses. From some sources (

In many cases, startups fail as they lack experience and skill. Krishnamurthy was expected to look after the firm’s profit and loss and worked directly with heads of marketing, categories, operations, and engineering. This also enabled Tiger Global to control Flipkart’s operation to anticipate a profitable exit sooner. Under Krishnamurthy, Flipkart had aggressively formed strategies to keep the sales and growth sustained and defeat Amazon (Thomas & Tom, 2017). Krishnamurthy started with sales strategies like the Big Billion Day (BBD) sale in October 2014 and made it successful. He had broad targets like increasing sales and month-wise focus on prime sectors such as smartphone and expensive appliances, cutting expenses including logistics, for example, shutting down hyperlocal delivery, and improving net promoter score (NPS), an index for customer loyalty and satisfaction. The score went up to 65 from previous year score of 55. There were contradictions with the founder’s idea and long-term vision. But every stakeholder wanted a profitable exit at the desired timing.

VCs Providing Network and Support to the Recruitment Process of Startups

Illustration from Flipkart: Accel Partners, one of the first VCs who funded Flipkart, wanted to recruit employees for its investee companies (Gulati, 2014). Through their job portal, Accel Partners provided value addition to the startup by recruiting competent candidates on their behalf, as the startups did not have much of a network and knowledge about the recruitment processes. Accel Partners had more than 40 companies in its portfolio, whose domain includes internet, mobile, healthcare, education, etc. Many middle and senior executives looking for startups did not know how to contact these startups. This portal or service was a good platform. Like any other portfolio company, Flipkart asked to recruit suitable candidates through Accel partners.

VCs Helping Firm’s Initiative for Mergers and Acquisitions or IPOs

Illustration from Flipkart: In 2012, Flipkart acquired Letsbuy, whose domain was in electronics retails. The acquisition was made easy due to common investors, namely Accel Partners and Tiger Global. These experienced VCs helped in the completion of the acquisition and merger successfully. This helped customers of Letsbuy reach a wider selection platform from Flipkart, and it helped Flipkart face the Amazon expansion. Similarly, Flipkart acquired Myntra in 2014. Both had some common VCs such as Tiger Global, Accel Partners, and Sofina Capital. It was reported that the investors proposed the consolidation. Myntra kept its separate website, and its founder joined Flipkart Board. By the acquisition, Flipkart gained the fashion and apparel category while Myntra used the technology platform of Flipkart. Myntra’s acquisition helped Flipkart consolidate its position against competitors such as Amazon, Snapdeal and eBay (Prasad & Rao, 2015). The deal was key to cost efficiency, revenue enhancement, and increased shareholder value (Malik, 2014).

On the one hand, many analysts speculated that the investors, including Tiger Global, looked forward to obtaining an IPO within 2–3 years as soon as they saw a profitable exit. Tiger Global successfully exited 7 IPOs and 19 acquisitions. Accel Partners had 30 IPOs, including Facebook, and 200 acquisitions in its profile. So, the valuation of the stock of Flipkart post-IPO was expected to be less underpriced, considering Tiger Global’s and Accel’s network and reputation.

VCs Connecting Startups with Manufacturers or Suppliers

Illustration from Flipkart: VCs did have a network and relationships with different manufacturers and suppliers. They helped startups connect to manufacturers and suppliers with profitable deals. For example, Mr Shou Zi Chew, CFO of Xiaomi, was also one of the partners at DST Global, which was one of the VCs of Flipkart. This empowered Flipkart and CEO Krishnamurthy to make a better deal with Xiaomi. The relation with DST Global also made negotiations for offering deals with top manufacturers like Motorola successful. Motorola and Xiaomi came back to Flipkart after Krishnamurthy led the deal, personally (Mihir & Sen 2017).

VCs Sharing Innovation and Technology

Illustration from Flipkart: As Flipkart raised $1.4 billion from VCs such as Tencent, eBay and Microsoft in April 2017, it had the opportunity to share the innovation platform and technology from these investors. Microsoft allowed it to work on its cloud computing platform Azure. Tencent shared its social messaging and payment platform WeChat. The relationship with eBay enabled Flipkart local customers to access global inventories and vice versa.

Conclusions and Research Suggestions

There had been much research that indicated the value additions of VC to startups. As VCs looked for a profitable exit, they were bound to safeguard the growth of the firm. With their network and experience, VC seemed to play a significant role in providing funds to startups. This study looks at Flipkart, an Indian e-commerce firm, which had been monitored and supported from time to time by its VC to face the rivals and emerge as a profitable firm in the long run. Flipkart had to face the challenges of consolidating its position in the presence of a global e-commerce giant like Amazon.

The case study analyses how VCs were associated with a firm, infusing their value-added activities. The entrepreneurs should also positively and effectively take those initiatives from the VCs to enable the firm’s overall growth. It also indicates that the founders sometimes need to compromise their self-aspirations in all stakeholders’ interests, including investors. And external support and value additions were antecedents for the firm’s growth. From this case analysis, it is observed that VCs brought in many non-financial resources, which were significantly important for the survival, growth, and expansion of new technology startups in India. This phenomenon encouraged local Indian entrepreneurs to new business creation and spillover effect, and the outcome was an innovation culture contributing to the national economy.

The discussion above does not cover analysis of funding and utilization of VC money in the growth of the startup. Many value-added activities were discussed in this study. These gaps can be treated as the scope of research. It would also be interesting to explore if startups could approach VC for reasons other than funding. This can lead to deviation from the mission and vision of these young companies. However, from Flipkart and its survival in the face of fierce competition, it did indicate a very important role that VC could potentially play. Exploration of common reasons for failure among VC-backed startups will be useful to potential entrepreneurs. Does it pertain to micro- and macroeconomic conditions or firm-specific characteristics or VC-entrepreneur relationship or others?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.