Abstract

Extant research has yielded conflicting theoretical and empirical predictions about whether family firm acquirers perform better or worse in mergers and acquisitions (M&As) than their nonfamily firm counterparts. To help resolve this controversy, we take a socioemotional wealth (SEW) perspective to theorize that family members’ desire to preserve their SEW favors the pursuit of M&A strategies that are both beneficial (industry-related M&As) and detrimental (domestic M&As) to M&A performance. We further theorize that the desire to preserve SEW leads to family firm idiosyncratic SEW resources that help family firm acquirers, on average, achieve better M&A performance than nonfamily firm acquirers. Meta-analytic results based on 51 primary studies covering 242,123 M&A deals are in line with our predictions. Thus, our study contributes to the literature on family firms and M&A performance by explaining how the different M&A strategies chosen by family firms have positive and negative consequences for M&A performance. Our theory and findings have implications for future family business and M&A research.

Keywords

Introduction

Mergers and acquisitions (M&As) represent a promising source of firm growth and have become an essential pillar of firm strategies in recent decades (Bauer & Matzler, 2014; Graebner, Heimeriks, Huy, & Vaara, 2017; Haleblian, Devers, McNamara, Carpenter, & Davison, 2009). However, an abundant body of research suggests that the majority of M&As fail to create value (Datta, Pinches, & Narayanan, 1992; King, Dalton, Daily, & Covin, 2004; King, Wang, Samimi, & Cortes, 2021). Due to family firms’ nonfinancial goals and unique resources (Chrisman, Sharma, Steier, & Chua, 2013; De Massis, Kotlar, Chua, & Chrisman, 2014), an increasing number of scholars have examined the performance of M&As conducted by family firms (e.g., Bauguess & Stegemoller, 2008; Caprio, Croci, & Del Giudice, 2011; Feldman, Amit, & Villalonga, 2019).

This literature is characterized by several challenges. First, there is a controversial theoretical discussion on whether family firm acquirers are superior or inferior M&A performers as compared with their nonfamily firm counterparts. Due to family firms’ idiosyncrasies (Chrisman et al., 2013; De Massis et al., 2014), some researchers refer to the potential self-serving motives of family members engaging in M&As (e.g., Bauguess & Stegemoller, 2008), whereas others highlight their superior M&A decision-making processes (e.g., Feldman et al., 2019). Thus, coherent theorizing that accounts for family firms’ idiosyncrasies with regard to M&A performance is still lacking. The controversy in the literature is also reflected in conflicting empirical findings on the family firm acquirer–M&A performance relationship (Bauguess & Stegemoller, 2008; Feldman et al., 2019; Miller, Le Breton-Miller, & Lester, 2010). Second, prior research has typically focused on questions regarding the direct M&A performance effect of family firm acquirers (e.g., Ben-Amar & André, 2006; Caprio et al., 2011) and therefore neglected to examine the strategic mechanisms that explain the influence of family firm acquirers on M&A performance. This omission constitutes a relevant research gap because the general M&A literature emphasizes that specific M&A strategies,1 such as diversifying M&As, substantially influence M&A performance (e.g., Datta et al., 1992; King et al., 2021; Meckl & Röhrle, 2016). To help resolve these theoretical challenges and extend this stream of research, we examine the following research questions: Which strategic mechanisms help explain the contradictory findings in the literature on the M&A performance of family firm acquirers? Do family firm acquirers over- or underperform their nonfamily firm counterparts with regard to M&A performance?

To answer these questions, we build on theory about socioemotional wealth (SEW). SEW is a multidimensional umbrella term capturing all the affect-related value that family members derive from their firm ownership (Berrone, Cruz, & Gomez-Mejia, 2012; Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson, & Moyano-Fuentes, 2007). We propose that the theoretical and empirical inconsistencies of prior research on the M&A performance of family firm acquirers can be explained by theorizing that family members’ desire to protect their SEW influences the pursuit of specific M&A strategies, which in turn has diverging performance implications. We focus on two important M&A diversification strategies—industry related versus industry diversifying and country related (i.e., domestic) versus country diversifying (i.e., cross-border)—for two reasons. First, prior M&A literature has demonstrated their impact on M&A performance (Datta et al., 1992; King et al., 2021; Meckl & Röhrle, 2016). Second, these M&A strategies are likely to be influenced by family members’ SEW preservation concerns (Gomez-Mejia, Patel, & Zellweger, 2018). Building on prior family firm research (Gomez-Mejia et al., 2018; Gomez-Mejia, Makri, & Larraza-Kintana, 2010), we argue that due to their desire to protect their SEW, family firms engage more in industry-related and domestic M&A strategies than their nonfamily firm counterparts. By integrating insights from the M&A literature (e.g., Chakrabarti, Gupta-Mukherjee, & Jayaraman, 2009; Datta et al., 1992) that industry-related (vs. industry-diversifying) M&As are beneficial for M&A performance whereas domestic (vs. cross-border) M&As are detrimental to M&A performance, we suggest that family firm acquirers can influence M&A performance both positively and negatively.

We build on recent theoretical advancements suggesting that the desire to build and preserve SEW not only affects family firms’ strategic behaviors (as proposed) but also leads to the development of specific SEW resources (Combs, Jaskiewicz, Ravi, & Walls, 2022), which enable family firms “to do it better” (Combs et al., 2022: 2). Applied to our setting, we theorize that SEW resources support family firms in their M&A target selection and integration, leading to overall better M&A performance as compared with their nonfamily firm counterparts irrespective of the underlying M&A motives. To empirically examine our predictions, we conducted a meta-analysis based on 51 primary studies and 210 effect sizes, covering 242,123 M&A deals. Meta-analytic methods are particularly appropriate for our research purpose, given the existing body of primary studies. Specifically, we performed meta-analytical structural equation modeling (MASEM; Viswesvaran & Ones, 1995), which allowed us to examine our theoretically derived but previously unexplored mediation model (Bergh et al., 2016; Combs, Crook, & Rauch, 2019).

Building on empirical evidence from more than 20 years of research, our study contributes to the family firm and M&A literature in the following ways. First, we contribute by providing novel insights into the strategic mechanisms that help explain the relationship between family firm acquirers and M&A performance. We theorize and find that family firms engage in distinctive M&A strategies—industry-related and domestic M&As—with contrary effects on M&A performance. Our theory is that family members’ SEW preservation desires are associated with the pursuit of performance-enhancing and performance-destroying M&A strategies, which helps reconcile prior conflicting findings on family firm acquirers’ M&A performance (e.g., Bauguess & Stegemoller, 2008; Bouzgarrou & Navatte, 2013).

Second, our study helps advance the controversial theoretical discussion on the family firm acquirer–M&A performance relationship (e.g., Bauguess & Stegemoller, 2008; Feldman et al., 2019; Miller et al., 2010) by providing novel theorizing: Building on the perspective that the pursuit of SEW not only affects the strategic behaviors of family firms (Gomez-Mejia, Cruz, Berrone, & De Castro, 2011) but also generates important SEW resources (Combs et al., 2022), we theoretically explain why family firm acquirers—irrespective of their M&A motives—outperform their nonfamily firm counterparts in M&As due to better target selection and integration. Our meta-analytic evidence is in line with our theorizing.

Literature Review on Family Firms and M&A Performance

M&As have become a prominent strategy for firm growth (Bauer & Matzler, 2014; Cartwright & Schoenberg, 2006; Haleblian et al., 2009; Steigenberger, 2017). A substantial body of literature has thus focused on M&A performance (e.g., King et al., 2021), which is defined as “the amount of value, in cost efficiencies and revenue growth, generated by the complete transaction process” (Zollo & Meier, 2008: 56).2 The value potentially created by M&As can cover short-term effects (i.e., stock market reactions affecting firm value) and long-term effects, which typically cover the entire integration process (e.g., synergies through economies of scale and scope; Zollo & Meier, 2008).

Despite potential growth benefits, M&A research suggests that most M&A deals do not create and often destroy value (Datta et al., 1992; King et al., 2004; King et al., 2021).3 Researchers have mainly attributed acquirers’ lack of M&A value creation to managers’ pursuit of M&As to advance their self-interests, such as their personal job security (Amihud & Lev, 1981) or managerial compensation and prestige (Avery, Chevalier, & Schaefer, 1998), rather than to maximize shareholder returns (Hoskisson, Hill, & Kim, 1993; Jensen, 1986). Moreover, a growing body of research indicates that the integration phase, including the organizational integration and alignment of the target, is critical for M&A performance but challenging for acquirers (for a review, see Graebner et al., 2017; Steigenberger, 2017). In light of often unsatisfactory M&A performance consequences for acquirers, M&A research has turned to identifying the drivers of M&A performance (Haleblian et al., 2009), such as the relatedness of the acquirer and target and the method of payment (Bilgili, Calderon, Allen, & Kedia, 2016; King et al., 2004; King et al., 2021).

In recent years, scholars have increasingly investigated the effect of family firm acquirers on M&A propensity and M&A performance (for a review, see Worek, 2017). Family firms are typically defined as firms that are “governed and/or managed with the intention to shape and pursue the vision of the business held by a dominant coalition controlled by members of the same family or a small number of families in a manner that is potentially sustainable across generations of the family or families” (Chua, Chrisman, & Sharma, 1999: 25). They are not only the most prevalent type of organization around the world (La Porta, Lopez-De-Silanes, & Shleifer, 1999) but also differ in their behaviors from nonfamily firms. Prior research has shown that family firms have a lower propensity for M&As (Caprio et al., 2011; Gomez-Mejia et al., 2018; Miller et al., 2010; Requejo, Reyes-Reina, Sanchez-Bueno, & Suárez-González, 2018). These studies theorize that family members focus on building and protecting SEW and pursuing nonfinancial goals, the most important of which is maintaining control over the firm (Gomez-Mejia et al., 2007); this and their wealth concentration in the firm render them risk averse (Donckels & Fröhlich, 1991; Schulze, Lubatkin, & Dino, 2002) and thus less likely to engage in M&As (Caprio et al., 2011; Gomez-Mejia et al., 2018). When family firms decide to pursue M&As, they tend to engage in smaller M&A deals in terms of financial value as compared with nonfamily firms (Miller et al., 2010).

Research on the M&A performance of family firms has put forth conflicting theoretical arguments and yielded mixed empirical results regarding whether family firm acquirers perform better or worse in M&As (e.g., Bauguess & Stegemoller, 2008; Feldman et al., 2019; Miller et al., 2010). Several researchers contend that family members conduct M&As to advance their own interests at the expense of minority shareholders, which leads to principal-principal conflicts (Schulze, Lubatkin, & Dino, 2003; Schulze, Lubatkin, Dino, & Buchholtz, 2001) and therefore lower M&A performance among family firm acquirers (e.g., Bauguess & Stegemoller, 2008; Shim & Okamuro, 2011). By contrast, other researchers argue that family members can effectively monitor managers, which restrains principal-agent conflicts (Fama & Jensen, 1983; Jensen & Meckling, 1976) and leads to better M&A performance among family firm acquirers (André, Ben-Amar, & Saadi, 2014; Basu, Dimitrova, & Paeglis, 2009; Bouzgarrou & Navatte, 2013).

To extend this stream of research, we propose that prior research has overlooked two important aspects. First, the specific M&A strategies pursued by family firm acquirers might be different due to their SEW considerations. Second, building and protecting SEW can also yield family firm idiosyncratic “SEW resources” (Combs et al., 2022) that might help family firms cautiously select and integrate their M&A targets. In the following, we rely on theory about family firms’ desire to maintain SEW endowments to develop hypotheses about the family firm acquirer–M&A performance relationship.

SEW Preservation and M&A Strategies

Research suggests that family firms differ from nonfamily firms in their strategic behaviors (Arregle, Duran, Hitt, & van Essen, 2017; Duran, Kammerlander, van Essen, & Zellweger, 2016; Gomez-Mejia et al., 2010). The literature on family firms explains their distinctiveness predominantly through family members’ desire to build and preserve their SEW (Berrone et al., 2012; Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2011), which often takes precedence over their financial wealth considerations in their strategic decision making (e.g., Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2011). To preserve their SEW, family members typically maintain their personal wealth in the family firm because this safeguards their ability to exercise control over the firm (Duran et al., 2016; Gedajlovic & Carney, 2010). This wealth concentration in turn shapes the strategic decision making of family members (e.g., Donckels & Fröhlich, 1991), leading, for instance, to fewer innovation investments (Duran et al., 2016), lower use of leverage (Hansen & Block, 2021), and lower M&A propensity (Gomez-Mejia et al., 2018; Miller et al., 2010). Thus, family members typically adopt conservative strategies to preserve or even enhance their SEW, which serves as their main reference point for decision making at the cost of not maximizing financial returns (Combs et al., 2022; Gomez-Mejia et al., 2011).

In the following, we build on this theorizing to suggest that family members’ SEW preservation concerns influence the firms’ choice of specific M&A strategies, which according to the M&A literature, affects M&A performance (e.g., Datta et al., 1992; King et al., 2021). We propose that at least three SEW dimensions (Berrone et al., 2012) help explain how SEW affects M&A strategies: family members’ transgenerational control desires, their desire for enduring stakeholder relationships, and their strong identification with the family firm.4 We focus on these three dimensions because prior research suggests that family firms’ growth strategies are influenced by their transgenerational control intentions (Miller et al., 2010; Zahra, 2003), enduring stakeholder relationships (Arregle et al., 2017; Arregle, Hitt, Sirmon, & Very, 2007), and strong identification with the firm (Hussinger & Issah, 2019; Zahra, 2003). We examine two important M&A diversification strategies that are likely influenced by family members’ SEW preservation concerns: industry-related and domestic M&A strategies. Furthermore, we build on prior M&A research to propose that pursuing these two M&A strategies influences M&A performance.

Industry-Related M&As

We propose that family firm acquirers have a higher preference for industry-related as compared with industry-diversifying M&As than do nonfamily firm acquirers. From a portfolio perspective (Markowitz, 1952), industry-diversifying M&As offer acquirers the opportunity to reduce a firm's unsystematic risk by depending less on one industry (Miller et al., 2010). However, we propose that despite these benefits, family firms prefer industry-related M&As over industry-diversifying M&As. Our theory is that industry-related M&As better protect three dimensions of SEW: transgenerational control, strong stakeholder relationships, and the family's identification with the firm.

First, we argue that family members favor industry-related M&A deals because they allow them to maintain higher levels of transgenerational control over their firm (Berrone et al., 2012; Gomez-Mejia et al., 2007). The underlying reason is that industry-related M&A deals reduce the need to hire outside industry experts because the family firm already possesses the required industry expertise. Although industry-related M&As may lead to more power in the hands of the firm's existing nonfamily managers, prior research argues that nonfamily managers in family firms are typically loyal and trustworthy regarding the owning family and thus do not threaten the family's control (Aronoff & Ward, 2011). By contrast, industry-diversifying M&As require delegation of more decision-making power to newly hired managers who possess the necessary industry expertise to manage the newly acquired target (Gomez-Mejia et al., 2010; Muñoz-Bullón & Sánchez-Bueno, 2012). However, the trustworthiness and loyalty of these new executives are “yet to be tested” (Aronoff & Ward, 2011: 15). Because giving power to outside industry experts would, to some degree, erode the family's control over their firm (Gomez-Mejia et al., 2007; Schulze et al., 2003) and therefore threaten their transgenerational control (Berrone et al., 2012), family members might prefer M&A targets that operate in related industries.

Second, industry-related M&As typically allow acquirers to mostly rely on the same supplier and customer networks (Hitt, Harrison, & Ireland, 2001) as well as on their existing employees, thereby enabling family firms to preserve and strengthen their established stakeholder relationships (Berrone et al., 2012; Gomez-Mejia et al., 2007). By contrast, industry-diversifying M&As typically require the establishment of new relationships with unfamiliar stakeholders (e.g., new suppliers) in the new industry (Hitt et al., 2001). These efforts have the potential to break the tight-knitted social networks that characterize family firms (Gomez-Mejia et al., 2011). In anticipation of these threats to their existing stakeholder relationships in industry-diversifying M&As (Gomez-Mejia et al., 2010), family members will select industry-related M&A targets.

Third, industry-related M&As allow family members to retain a strong focus on their core industry (Hussinger & Issah, 2019). This is important because it helps them maintain their traditions and routines (e.g., decision-making processes, operational procedures; Dyer, 1988), which are typically deeply anchored in the firm's core industry (Berrone et al., 2012; Gomez-Mejia et al., 2010; Hussinger & Issah, 2019). Upholding these traditions and routines allows family members to preserve their strong identification with the firm (Hussinger & Issah, 2019; Pratt & Foreman, 2000). In contrast, industry-diversifying M&As typically require new routines and ways of operating (Barkema & Schijven, 2008; Gomez-Mejia et al., 2010). Family members likely perceive such changes to their traditions and routines as a potential threat to their identification with the family firm (Casson, 1999; Gomez-Mejia et al., 2007) and thus prefer industry-related M&A targets.

Together, these arguments suggest that family firm acquirers will engage more in industry-related M&As than their nonfamily firm counterparts:

Hypothesis 1a: Family firm acquirers are more likely to engage in industry-related M&A deals as compared with nonfamily firm acquirers.

Building on insights from the extant M&A literature (Datta et al., 1992; Martynova & Renneboog, 2011; Singh & Montgomery, 1987), we argue that the strategic preference for industry-related over industry-diversifying M&As is associated with higher M&A performance. Extant research argues that industry-related M&As allow firms to benefit from resource complementarities (Hussinger & Issah, 2019) and economies of scale and scope (Helfat & Eisenhardt, 2004; Singh & Montgomery, 1987), which lead to lower costs (e.g., through efficiency gains), higher revenues (e.g., through acquisition of competitors’ customers), and subsequently better M&A performance than unrelated M&A deals (Datta et al., 1992; Salter & Weinhold, 1979). The synergy gains in terms of economies of scale and scope are significantly higher in industry-related M&As than in industry-diversifying M&As because core resources (i.e., technologies) and skills (i.e., know-how on production, marketing, or distribution) can be transferred to or shared with the M&A target (e.g., Datta et al., 1992; Singh & Montgomery, 1987). In contrast, industry-diversifying M&As often require restructuring and building new skills and relationships that can be costly to the acquirer (Barkema & Schijven, 2008) and therefore reduce M&A performance. Finally, industry-related M&A deals can increase the acquirer's market power (Singh & Montgomery, 1987) and thus help shape product pricing and reduce supplier costs (i.e., quantity discounts; Bhattacharyya & Nain, 2011). Therefore, we argue that industry-related M&As are associated with better M&A performance.

Hypothesis 1b: Industry-related M&A deals are associated with a higher M&A performance than industry-diversifying M&A deals.

Combining research on family firms with the M&A literature, we further propose that industry-related M&A strategies represent a crucial mediating mechanism in the family firm acquirer–M&A performance relationship. Specifically, we argued in Hypothesis 1a that family firm acquirers, due to their desire to protect their SEW (e.g., Gomez-Mejia et al., 2007), engage more in industry-related M&As. As described in Hypothesis 1b, a substantial body of M&A research argues that industry-related M&A strategies are beneficial for M&A performance because they increase economies of scale and scope and market power (e.g., Datta et al., 1992).

Combining Hypotheses 1a and 1b, we propose that family firms are more likely to engage in industry-related M&A deals (vs. industry diversifying), which in turn relates positively to M&A performance:

Hypothesis 1c: Higher levels of industry-related M&A deals positively mediate the relationship between family firm acquirers and M&A performance.

Domestic M&As

We further argue that family firm acquirers have a higher preference for domestic over cross-border M&As. Although cross-border M&As offer diversification advantages similar to industry-diversifying M&As (Gomez-Mejia et al., 2010), we submit that the desire to preserve the same three SEW dimensions—transgenerational control, strong stakeholder relationships, and the family's identification with the firm—lead family firm acquirers to pursue more domestic M&As.

First, family members should prefer domestic M&As over cross-border M&As because they allow greater transgenerational control (Berrone et al., 2012). Cross-border M&As typically require more external upfront financing because of higher initial transaction costs and more complex integration relative to domestic M&As (Chen, Huang, & Chen, 2009; Graves & Thomas, 2008). The required financial resources may lead to a long-term dependency on financial capital providers from outside the family firm (i.e., banks and investors; Gomez-Mejia et al., 2010). Such external financing dilutes family ownership and power and thus threatens family members’ transgenerational control (Gallo, Tàpies, & Cappuyns, 2004). Moreover, in domestic M&As, family members can exert more direct control over the newly acquired firm due to closer proximity in terms of distance, thereby ensuring that it is run according to their preferences. For instance, family members or their trusted nonfamily managers can monitor acquired firms through unannounced irregular plant visits. Cross-border M&As, in contrast, typically require more reliance on new executives who have foreign country knowledge from outside the family firm (Gomez-Mejia et al., 2010). This reduces the autonomy of family members (Haider, Li, Wang, & Wu, 2021) because they have to delegate some decision-making authority to these new executives. Since cross-border M&As likely threaten family members’ ability to exercise control across generations, they are more likely to select M&A targets within their familiar domestic sphere than to pursue cross-border M&As.

Second, family members prefer domestic M&As because they allow the family to rely more on existing stakeholder relationships with people in relevant positions (e.g., politicians, bankers, and lawyers) that support their M&A endeavors, for instance, with regard to legal or financial issues (Bird & Wennberg, 2014; Gomez-Mejia et al., 2010). In contrast, cross-border M&As require family firms to establish new relationships with unfamiliar stakeholders (e.g., foreign banks, government bodies, and local suppliers) to close the deal and successfully integrate the target (Arregle et al., 2017; Hitt, Hoskisson, & Kim, 1997; Moeller & Schlingemann, 2005). Due to family members’ strong desire to preserve their established network of stakeholder relationships, we suggest that they will be more likely to pursue domestic rather than cross-border M&As.

Third, while domestic and cross-border M&As entail dealing with the different corporate cultures of the acquirer and the target, cross-border M&As bring a foreign national culture to the M&A deals, which prompts a “double-layered acculturation” process (Barkema, Bell, & Pennings, 1996: 151). However, family members are concerned about conserving the established values, traditions, and routines of their firm and its modus operandi (Eisenmann, 2002) to preserve their strong identification with the family firm (Berrone et al., 2012; Bird & Wennberg, 2014; Casson, 1999). In domestic M&As, family firms’ values, traditions, and routines (e.g., decision-making structures and failure cultures) can be better passed on to M&A targets because the acquirer and target share a mutual understanding based on the same national culture (Schneider & De Meyer, 1991). Thus, domestic M&As help family members preserve coherent family identification with their firm over time (Pratt & Foreman, 2000). In contrast, cross-border M&As and the associated national cultural foreignness (Arregle et al., 2017; Zaheer, 1995) make it more difficult to transfer the family firm's values and routines to the target, which might threaten family members’ identification with the firm (Berrone et al., 2012; Gomez-Mejia et al., 2007). In anticipation of such threats, family members likely prefer domestic M&A targets.

In summary, we propose that family firm acquirers, due to their desire to protect their SEW, conduct more domestic M&As than cross-border M&As relative to nonfamily firm acquirers:

Hypothesis 2a: Family firm acquirers are more likely to engage in domestic M&A deals than nonfamily firm acquirers.

While some researchers argue that domestic M&As have lower integration costs, for example, due to lower complexity and similar cultures (e.g., Moeller & Schlingemann, 2005), other researchers argue that the shortcomings of domestic M&As outweigh their benefits for M&A performance (Bertrand & Capron, 2015; Chakrabarti et al., 2009; Markides & Ittner, 1994; Morosini, Shane, & Singh, 1998). We follow this line of argumentation and propose that domestic, in contrast with cross-border, M&As are associated with lower M&A performance for the following reasons.

First, cross-border M&As provide the opportunity to access new international markets (Hitt et al., 1997; Shimizu, Hitt, Vaidyanath, & Pisano, 2004), whereas domestic M&As largely restrict acquirers’ operations to the current domestic market. Hence, due to access to new markets, cross-border M&As permit higher revenue growth as compared with domestic M&As (Hitt et al., 1997), thereby leading to better M&A performance.

Second, in addition to increased market access, cross-border M&As allow exploitation of favorable government policies and regulations in other countries to, for instance, optimize taxation (Markides & Ittner, 1994) or reduce factor costs (i.e., wages, material, capital costs; Bertrand & Capron, 2015; Kogut, 1985). Cross-border M&A deals allow for greater opportunities to benefit from efficiency gains resulting from economies of scale and scope on a global scale through, for instance, standardized products and production processes across countries (Bertrand & Capron, 2015; Doukas & Travlos, 1988; Kogut, 1985). Cross-border M&As can thus lead to increased bargaining power (i.e., over suppliers, distributors, or customers), which helps to reduce costs (Hitt et al., 1997; Kogut, 1985). In summary, we argue that based on fewer opportunities to increase revenues and reduce costs, domestic M&As underperform cross-border M&As:

Hypothesis 2b: Domestic M&A deals are associated with lower M&A performance than cross-border M&A deals.

Combining research on family firms with the literature on M&A performance, we further propose that domestic M&A strategies mediate the relationship between family firm acquirers and M&A performance. As we theorized in Hypothesis 2a, family firm acquirers, due to their desire to maintain transgenerational control, stakeholder relationships, and their identification with the firm, conduct more domestic M&As than their nonfamily firm counterparts. We propose in Hypothesis 2b, based on the M&A literature, that domestic M&As are less beneficial for M&A performance than cross-border M&A deals. Combining Hypotheses 2a and 2b, we propose that family firms are more likely to engage in domestic M&As, which in turn are associated with lower M&A performance:

Hypothesis 2c: Higher levels of domestic M&A deals negatively mediate the relationship between family firm acquirers and M&A performance.

SEW Resources and M&A Performance

While it is well established that family members’ desire to grow and preserve their SEW affects their strategic behavior (Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2011), more recent theorizing suggests that pursuing SEW generates SEW resources that can provide family firms with competitive advantages under certain conditions (Combs et al., 2022; Naldi, Cennamo, Corbetta, & Gomez-Mejia, 2013). Building on this perspective, we argue that aside from influencing the M&A strategies that family firms pursue, the family members’ SEW endowments create SEW resources that affect the selection and integration of M&A targets and thus, ultimately, M&A performance. Specifically, according to Combs et al. (2022), the three SEW dimensions used in our theorizing before (i.e., family members’ transgenerational control desires, their desire for enduring stakeholder relationships, and their strong identification with the family firm) lead to three specific SEW resources—long-term orientation (LTO), strong stakeholder relationships, and favorable firm reputation—which are disproportionately generated in family firms and help them to “reap more bang for their buck” (Combs et al., 2022: 3). Building on and extending the research by Combs et al. (2022) to the M&A context, we propose that these three specific SEW resources help family firms achieve better M&A performance. This theorizing is in line with the general M&A literature emphasizing the role of resources in target integration (Graebner et al., 2017).

First, family members’ desire for transgenerational control not only affects their strategic behaviors but also yields an LTO (Combs et al., 2022; Lumpkin & Brigham, 2011), which endows them with patient capital (König, Kammerlander, & Enders, 2013; Sirmon & Hitt, 2003). Family firms typically face less pressure to meet short-term results (i.e., quarterly earnings; Flammer & Bansal, 2017), which enables them to focus on transgenerational investment decisions with longer time horizons (Sirmon & Hitt, 2003; Strike, Berrone, Sapp, & Congiu, 2015). We therefore propose that family firms, because of their LTO resource, are particularly interested in and well equipped for pursuing only M&A deals with targets that provide them with clear long-term benefits (i.e., long-term fit, synergies, adequate price) and the prospect of enhancing the viability and family firm value across generations. To identify promising targets, we argue that LTO encourages family firms to evaluate M&A targets more carefully, including, for instance, the technological, product, or market complementarities that are crucial for M&A performance (Bauer & Matzler, 2014; Larsson & Finkelstein, 1999). Hence, due to their LTO, family firms should be, irrespective of their specific M&A motives, better able to conduct thorough assessments of potential targets, leading to more realistic synergy expectations and thus fewer failures in due diligence (e.g., overoptimistic expectations; Welch, Pavićević, Keil, & Laamanen, 2020). Moreover, the LTO resource provides family firms with more time to carefully integrate M&A targets, which is crucial because integration processes can last for years (Graebner et al., 2017). Their LTO, including patient capital and long-term commitment (Combs et al., 2022), constitute important resources required to integrate organizational structures, processes, employees, and cultures (Graebner et al., 2017). Family firms should therefore be, on average, better able to carefully integrate their targets, which helps them avoid disruptions in the firm's operations (Feldman et al., 2019), thereby decreasing long-term integration costs and improving the acquisition value (Birkinshaw, Bresman, & Håkanson, 2000).

Second, the resource of strong stakeholder relationships (Combs et al., 2022), which again stems from family firms pursuing SEW, improves stakeholder trust (Zellweger & Nason, 2008), collaboration, and knowledge sharing (Zahra, Neubaum, & Larrañeta, 2007). We propose that employees in family firms, due to this specific resource, better collaborate and exchange with one another in the M&A context. Such collaboration facilitates a more thorough exchange of relevant information (i.e., from different departments, such as finance, sales, production) and coordination of different M&A-related tasks, which improves the due diligence process (e.g., target identification). Employees in family firms are often more committed to the firm and tend to trust their managers (Kets de Vries, 1993; Zahra, Hayton, Neubaum, Dibrell, & Craig, 2008), which is particularly helpful for the integration of the target firm (Colman & Lunnan, 2011). Strong stakeholder relationships might help family firms reduce interorganizational frictions and potential feelings of frustration, which could reduce costly postacquisition voluntary turnover among target firm employees (Steigenberger, 2017). Strong personal relationships with external stakeholders, such as suppliers, should also help family firms better integrate the newly acquired target into their established networks (e.g., with suppliers). Better integration into the supply chain reduces friction and thus enables realization of synergies (e.g., reduced costs through realized economies of scale; Langabeer & Seifert, 2003), which increases M&A performance.

Finally, family members’ strong identification with their firm leads to the resource favorable firm reputation (Combs et al., 2022; Miller & Le Breton-Miller, 2014). We propose that possessing better corporate reputations (Deephouse & Jaskiewicz, 2013) can be strategically valuable when approaching and negotiating with M&A targets. Prior research suggests that the acquirer's reputation sends important signals about the firm's trustworthiness and its ability to stick to its commitments regarding the M&A deal and its future prospects (Chalençon, Colovic, Lamotte, & Mayrhofer, 2017). Because of their favorable reputation, which serves as an important intangible asset (Rindova, Williamson, & Petkova, 2010), we propose that family firms will be better able to attract and negotiate favorable M&A deals, resulting in better M&A prices (i.e., less likely to pay high acquisition premiums), thereby increasing M&A performance. Moreover, we argue that employees of the newly acquired M&A target are more likely to have a favorable attitude toward the M&A deal because of the family firm's good reputation. Hence, this resource motivates new employees from the target firm to become part of the family firm acquirer, leading to less voluntary employee turnover and thus better retention of relevant expertise. This positive attitude should reduce tension and friction and foster effective interactions, knowledge retention, and the creation of synergies that are important for successful integration (Graebner et al., 2017), thereby helping increase the value created from the M&A deal.

In summary, we propose that the three SEW resources that prior theory anticipates from family firms’ desire to preserve SEW—LTO, strong stakeholder relationships, and favorable firm reputation—help family firms in the selection, negotiation, and integration of M&A deals, which lead to better M&A performance:

Hypothesis 3: Family firm acquirers are associated with a higher M&A performance as compared with nonfamily firm acquirers.

Methods

Meta-Analytic Database and Coding

To empirically examine our hypothesized model, we built a meta-analytic database to perform MASEM (Bergh et al., 2016; Viswesvaran & Ones, 1995). The advantage of MASEM is that it enables testing of the hypothesized mediation model based on the cumulative statistical evidence of existing studies, while controlling for other variables (Bergh et al., 2016; Combs et al., 2019; Tihanyi et al., 2019). Following previous meta-analyses (e.g., Arregle et al., 2017; Duran et al., 2016; Tihanyi et al., 2019), we used five complementary search strategies to identify studies that investigated the relationship between family firms and M&A performance. First, we searched three major electronic databases (EBSCO, ABI/INFORM Global, and Google Scholar) using the following family firm search terms (e.g., Duran et al., 2016): family firm*, family business*, family compan*, family own*, family control*, family enterprise, family led, founding family, family manag*, privately held firm*, privately held compan*, and founder*. We combined these family firm keywords with M&A-related keywords (e.g., King et al., 2021; Meckl & Röhrle, 2016): mergers and acquisitions, M&A*, merger*, acquisition*, takeover*, industry-related, industry-divers*, industry related, industry divers*, related, domestic, cross-border, international*, foreign, divers*. Second, we consulted extant literature reviews on M&As in family firms (e.g., Worek, 2017) and searched their reference lists for relevant studies. Third, we conducted a targeted manual search of 17 selected academic journals to ensure that key studies were not omitted.5 Fourth, to reduce the threat of publication bias (Rosenthal, 1979), we searched for dissertations in the ProQuest database, examined conference proceedings (and contacted authors), and posted on the Listservs of the Academy of Management and Family Enterprise Research Conference to identify relevant unpublished papers. Fifth, we applied the two-way snowball sampling technique (Von Hippel, Franke, & Prügl, 2009), which entails backward tracing of all references in the identified studies and forward tracing of all articles that referenced these studies.

The studies obtained through this sampling process had to meet two inclusion criteria to be retained. First, studies needed to empirically examine the relationship between family firm acquirers and the specific M&A strategies (i.e., industry related and domestic), between family firm acquirers and M&A performance, or between the specific M&A strategies and M&A performance using a sample of family and nonfamily firms. Second, studies had to report Pearson's correlation coefficients or other appropriate statistics (e.g., t statistics from independent group tests) that could be converted into correlation coefficients.6 We corresponded with 61 authors on missing correlation coefficients or omitted information that would allow conversion to correlation coefficients, which enabled us to include seven additional studies.

To enhance the robustness of our study (Landis, 2013), we included (in addition to the findings from the primary studies) the meta-analytic effect size estimates from the most recently published meta-analyses on the relationship between industry-related M&As and M&A performance (King et al., 2021) as well as between domestic M&As and M&A performance (Meckl & Röhrle, 2016) in our database.7 We included only these two meta-analyses to avoid sample overlap. By December 2021, this search process had led to a final sample of 51 primary studies (38 published and 13 unpublished, including 5 working/conference papers and 8 dissertations) and 210 effect sizes, capturing 242,123 M&A deals between 1950 and 2017.8

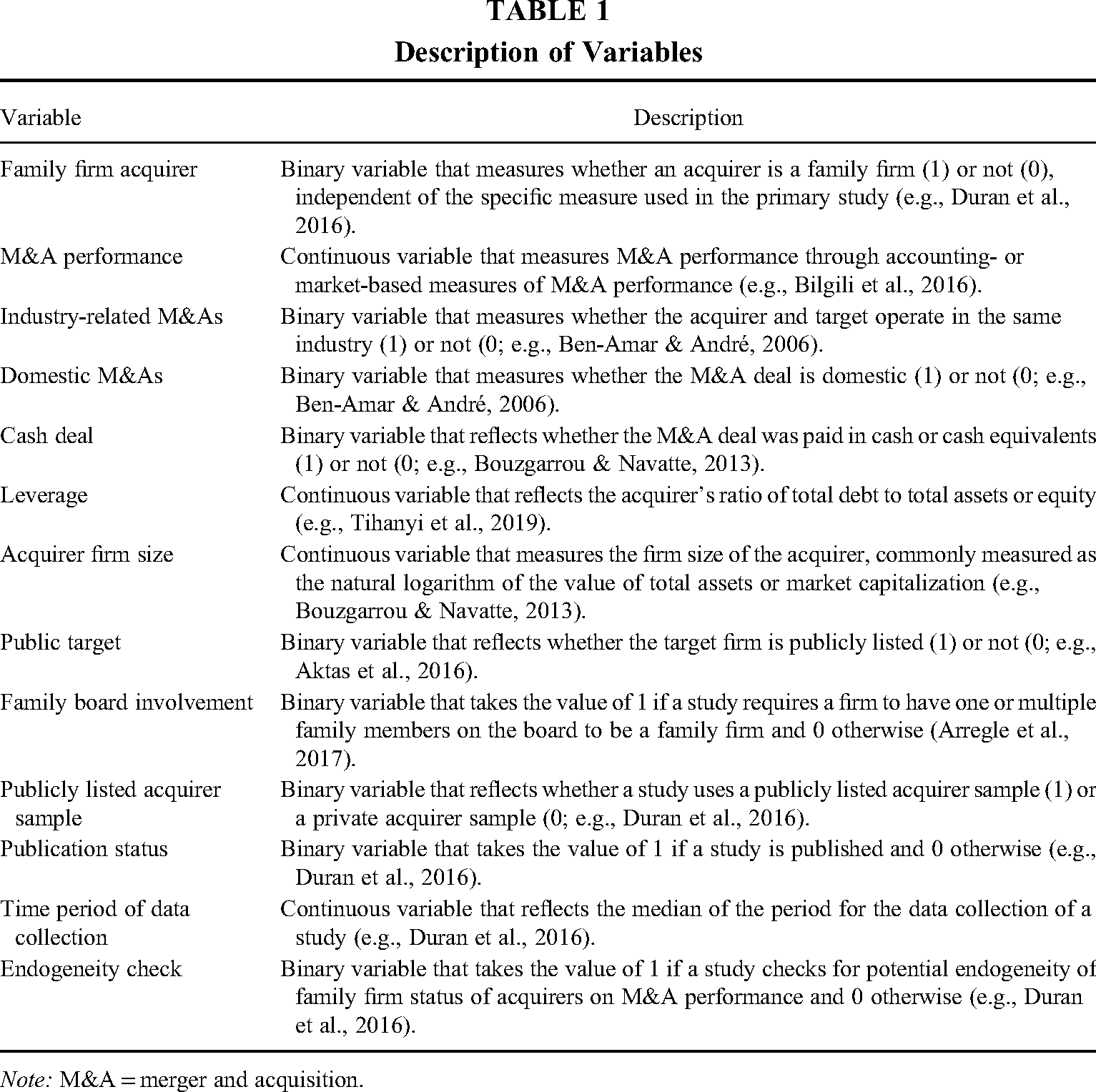

Following our search process, we read all primary studies and developed a coding protocol outlining all information to be extracted from the studies (e.g., effect sizes and control variables) to reduce coding error (Lipsey & Wilson, 2001). All the studies were manually coded according to the coding protocol by the first author. The second author independently coded all studies with high interrater reliability (Cohen's kappa coefficient = 0.97; Cohen, 1960). Disagreements were resolved by discussion. Table 1 provides a description of the variables collected from the primary studies; details about the primary studies can be found in Supplement 1 online.

Description of Variables

Note: M&A = merger and acquisition.

Variables

Independent variable—family firm acquirers

We considered all variables from the primary studies that measured whether an acquirer is a family firm (1) or not (0) for the variable family firm acquirers, independent of the specific operationalization employed by primary studies. The extant literature has used various definitions to extract the influence of family firm acquirers (e.g., Ben-Amar & André, 2006; Caprio et al., 2011), such as (1) family ownership through substantial voting or cash flow rights, presented as a dummy variable with a defined percentage of voting or cash flow rights or as a continuous variable (e.g., André et al., 2014); (2) family presence via one or multiple family members on the executive or nonexecutive board (e.g., Li & Srinivasan, 2011); and (3) combinations thereof (e.g., Defrancq, Huyghebaert, & Luypaert, 2016). In a post hoc test, we controlled for different operationalizations used in primary studies. For this purpose, we created a dummy variable, family board involvement, which takes the value of 1 if all the family firms in the primary study had one or more family members involved in management and/or the board to be considered a family firm and 0 otherwise.

Dependent variable—M&A performance

In line with prior M&A meta-analyses (e.g., Bilgili et al., 2016; King et al., 2021), we considered all M&A performance variables used in primary studies. While some studies relied on market-based measures of M&A performance, such as cumulative abnormal returns around the M&A deal announcement (André et al., 2014; Bauguess & Stegemoller, 2008), buy-and-hold abnormal returns (Ottolenghi, 2017), or Tobin's Q (Miller et al., 2010), others relied on accounting-based measures of M&A performance, such as EBITDA (earnings before interest, taxes, depreciation and amortization)/total assets (Bouzgarrou & Navatte, 2013), industry-adjusted sales growth (Shim & Okamuro, 2011), or ROA (return on assets; Hussinger & Issah, 2019).9 We controlled for differences between accounting- and market-based measures in a post hoc analysis.

Mediation variable—industry-related M&As

Industry-related M&As is a binary variable that measures whether acquirer and target operate in the same industry (1) or not (0; e.g., Ben-Amar & André, 2006). The underlying studies measure industry-related M&As through different operationalizations of related industries, using two-digit (e.g., Ben-Amar & André, 2006; Lahlou, 2018), three-digit (e.g., Defrancq et al., 2016; Feldman et al., 2019), or four-digit SIC codes (Standard Industrial Classification; e.g., André et al., 2014; Patel & King, 2015). In line with other meta-analyses (King et al., 2021), we followed the definitions of the primary studies and included all of them in our variable industry-related M&As. When studies measured industry diversification, we reversed the sign of the effect size. None of the underlying studies used entropy or Herfindahl indices. To control for the different operationalizations used by the underlying studies, we ran a series of post hoc MASEM analyses in which we differentiated effect sizes stemming from studies that employed two-, three-, or four-digit SIC codes to measure industry-related M&As.

Mediation variable—domestic M&As

Domestic M&As is a binary variable that measures whether the M&A deal is domestic (1) or not (0; i.e., cross-border) (e.g., Ben-Amar & André, 2006; Feito-Ruiz & Menéndez-Requejo, 2012; Gonenc, Hermes, & van Sinderen, 2013). An M&A deal is considered domestic when the acquirer and the target are located in the same country. We reversed the sign of the effect size when studies measured cross-border M&As.

Control variables

In line with prior M&A meta-analyses (e.g., King et al., 2004; King et al., 2021), we controlled for whether the M&A deal was paid in cash or cash equivalents (i.e., cash deal) (1) or otherwise (0). The payment method in M&A deals has been shown to significantly influence M&A performance (King et al., 2021), which could be a result of cash payments signaling acquirer confidence in an M&A deal (Blackburn, Dark, & Hanson, 1997) and public firms’ stock payments signaling that the acquirer's share price is overvalued, thereby prompting a negative market reaction (Welch et al., 2020). We controlled for the acquirer's leverage, typically measured as the ratio of total debt to the total value of assets or equity. High leverage can signal, as well as act as a financial constraint to, the integration of the M&A target (King et al., 2021), but it can also represent a form of beneficial external governance, usually in the form of banks or other creditors (Jensen, 1986). Next, we controlled for the acquirer's firm size because larger acquirers are more likely to have the capacity to integrate the target's operations and thus to realize synergies (King et al., 2021). Primary studies typically measured the acquirer's firm size as the natural logarithm of the value of total assets (e.g., Bouzgarrou & Navatte, 2013) or as the market capitalization (e.g., Gonenc et al., 2013). Last, we controlled for whether the target firm was publicly listed, which was measured as a binary variable in primary studies (1 = publicly listed target; 0 = private target), because prior research shows that M&A deals with publicly listed targets are associated with higher acquisition costs due to greater competition in the stock market (Aktas, Centineo, & Croci, 2016).

MASEM Procedure

To examine our hypothesized model, we performed MASEM following established methodological guidelines (Bergh et al., 2016; Combs et al., 2019; Viswesvaran & Ones, 1995). Specifically, MASEM was conducted in two steps. In the first step, a meta-analytic correlation matrix was developed wherein the meta-analytic effect size was calculated for each relationship in the correlation matrix. We used Pearson’s product-moment correlation coefficients (r) from primary studies to empirically synthesize prior research findings. If studies reported multiple effect sizes for the relationships of interest, we included all of them (Bijmolt & Pieters, 2001; Tihanyi et al., 2019).10 However, using multiple effect sizes that stem from the same study violates the assumption of independence (Cheung, 2019; Hunter & Schmidt, 2004) and thus might bias the results (i.e., due to the underestimation of standard errors; Cheung, 2019; López-López, Van den Noortgate, Tanner-Smith, Wilson, & Lipsey, 2017).11 Therefore, we followed recent recommendations (e.g., Cheung, 2014, 2019; Fernández-Castilla et al., 2020) and used multilevel meta-analysis, which accounts for the fact that multiple effect sizes can be nested within studies while preventing the loss of information that inevitably comes with averaging dependent effect sizes within studies. We conducted a multilevel approach with restricted maximum likelihood estimation procedures (Cheung, 2019; Fernández-Castilla et al., 2020) using the metafor package by Viechtbauer (2010) in R. In the second step, we used the meta-analytic correlation matrix as input to apply structural equation modeling using maximum likelihood estimation procedures (Bergh et al., 2016; Viswesvaran & Ones, 1995). Given that the meta-analytic relationships in the correlation matrix were based on different sample sizes, we followed current conventions (Bergh et al., 2016; Combs et al., 2019) and used the harmonic mean of the sample sizes across all cells for the path analysis (N = 9,117) (Viswesvaran & Ones, 1995). The harmonic mean is less sensitive to large values when compared with the arithmetic mean and therefore provides more conservative values (Landis, 2013).

Results

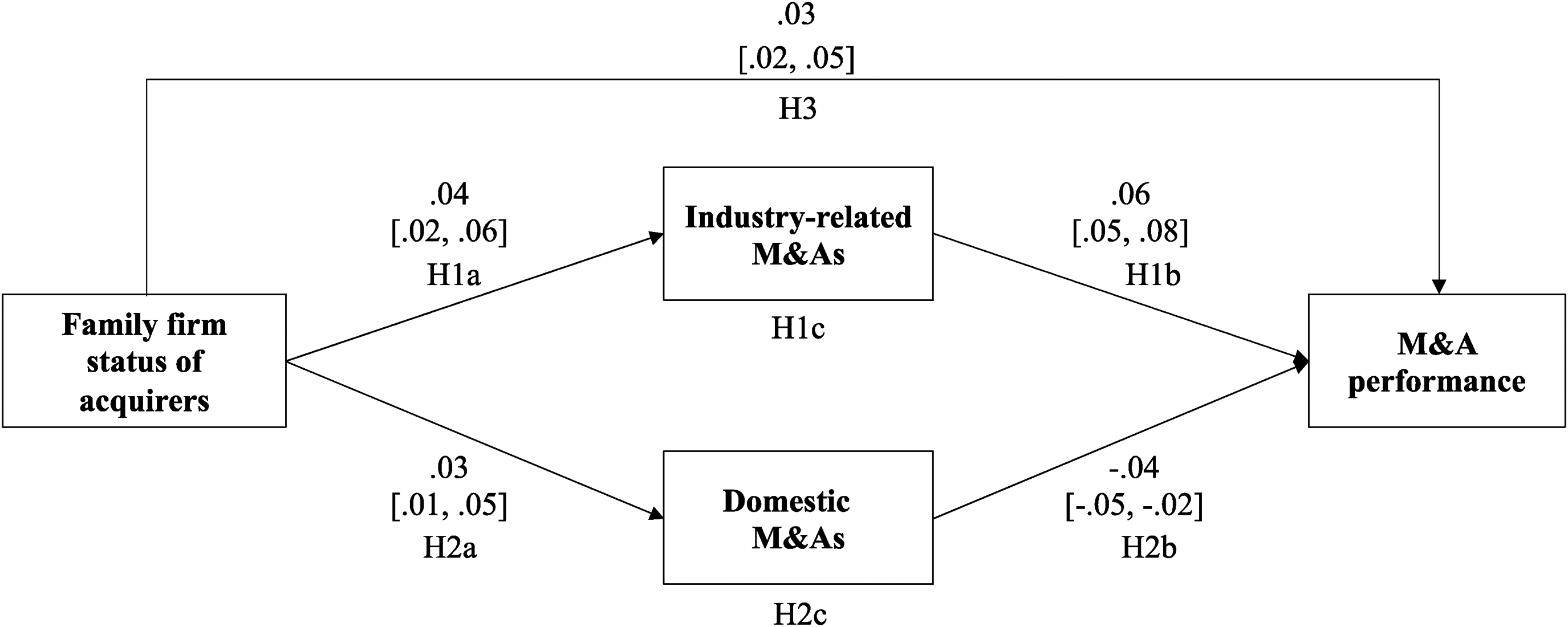

MASEM Results

Table 2 presents the meta-analytic correlation matrix, which was used as input for structural equation modeling. Table 3 and Figure 1 present the detailed MASEM path results. The fit indices indicate that the proposed model fits the data well (root mean square error of approximation = .01, goodness-of-fit index = 1.00, normative fit index = .98, standardized root mean square residual = .01). We followed Hayes (2013) and tested different nested models, including direct, partial, and full mediation models.12 A comparison of the different models indicates that the partial model exhibits a significantly better fit than the direct effects (Δχ2 [10] = 128.98, p = .000) and the full mediation model (Δχ2 [1] = 10.27, p = .001). To further examine the mediation hypotheses, we calculated the direct, indirect, and total effects of family firm acquirers on M&A performance using bootstrapping procedures to assess the level of significance of the mediation effects (Hayes, 2013).13 In addition, we conducted a series of Sobel, Aroian, and Goodman tests to assess the level of significance of the different mediator effects between family firm acquirers and M&A performance (Preacher & Hayes, 2008; Tihanyi et al., 2019).

MASEM Results

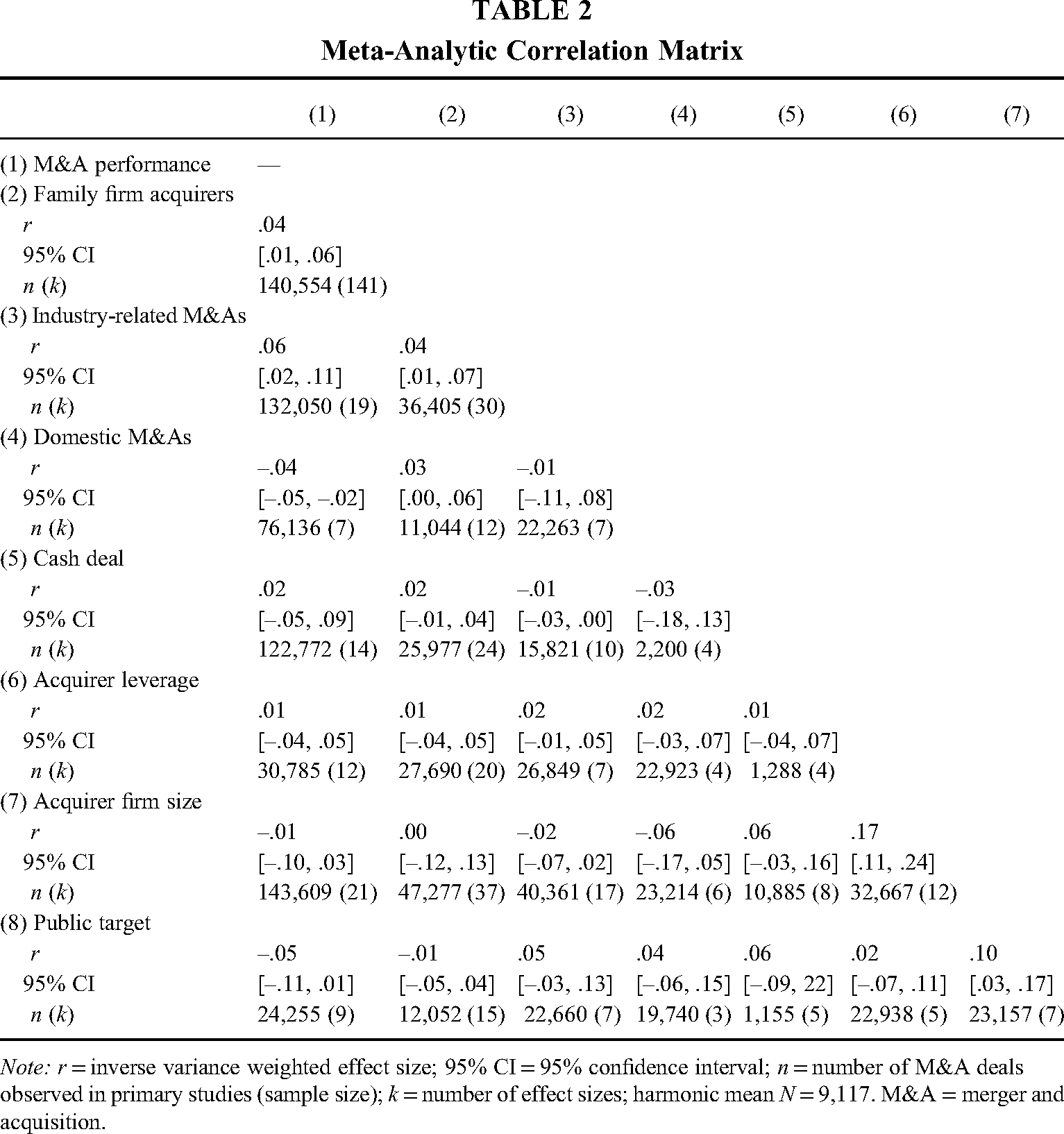

Meta-Analytic Correlation Matrix

Note: r = inverse variance weighted effect size; 95% CI = 95% confidence interval; n = number of M&A deals observed in primary studies (sample size); k = number of effect sizes; harmonic mean N = 9,117. M&A = merger and acquisition.

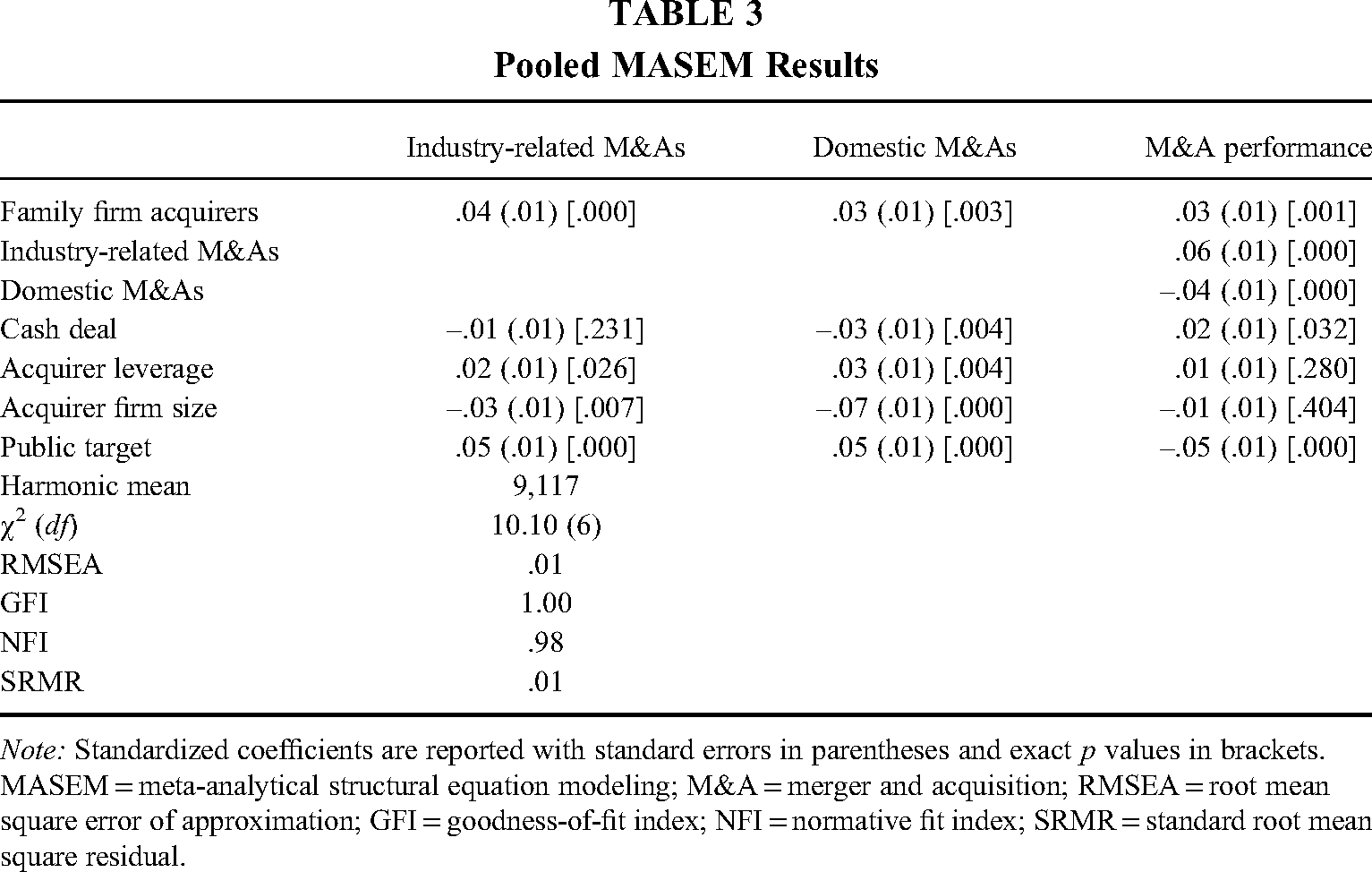

Pooled MASEM Results

Note: Standardized coefficients are reported with standard errors in parentheses and exact p values in brackets. MASEM = meta-analytical structural equation modeling; M&A = merger and acquisition; RMSEA = root mean square error of approximation; GFI = goodness-of-fit index; NFI = normative fit index; SRMR = standard root mean square residual.

H1a predicts that family firm acquirers are more likely to engage in industry-related M&A deals than nonfamily firm acquirers. In line with this prediction, the results in Table 3 show that family firm acquirers are positively associated with industry-related M&As (β = .04, p = .000). To illustrate the practical relevance, we applied the binomial effect size display (BESD; Rosenthal & Rubin, 1982). According to this approach, the meta-analytic effect size of r = .04 (Table 2) between family firm acquirers and industry-related M&As means that family firm acquirers are 4% more likely to pursue industry-related M&A deals than nonfamily firm acquirers. Applied to the worldwide M&A activities in 2022 (Institute for Mergers, Acquisitons, and Alliances [IMAA], 2022), this effect relates to 1,985 more industry-related M&A deals (4% of 49,622 deals) conducted by family firm acquirers, reflecting a deal value of US $136 billion (4% of worldwide M&A deal value of US $3.39 trillion).14

In support of H1b, which predicts that industry-related M&A deals are associated with higher M&A performance than industry-diversifying M&A deals, the results in Table 3 show that industry-related M&A deals are positively associated with M&A performance (β = .06, p = .000). While the BESD was initially developed to display the change in success rates (e.g., survival rates; Rosenthal & Rubin, 1982), we follow prior research (e.g., Han, Harold, Oh, Kim, & Agolli, 2022; Wang, Holmes Jr, Oh, & Zhu, 2016) and apply this approach for interpreting our findings on M&A performance through assuming successful versus unsuccessful dichotomies. Based on the assumption of such dichotomies, the correlation of r = .06 (Table 2) between industry-related M&As and M&A performance means that industry-related M&As have 6% higher success rates than industry-diversifying M&A deals, which relates to 2,977 industry-related M&A deals with higher success rates, reflecting a deal value of US $203 billion if applied to the worldwide M&A activities in 2022 (IMAA, 2022).

Consistent with H1c, which predicts that the relationship between family firm acquirers and M&A performance is mediated by higher levels of industry-related M&As, we find a significant positive indirect effect of family firm acquirers on M&A performance through industry-related M&As (β = .002, p = .002; Sobel test, z = 3.33, p = .000; Aroian test, z = 3.30, p = .001; Goodman test, z = 3.36, p = .001).

H2a predicts that family firm acquirers are more likely to engage in domestic M&A deals than nonfamily firm acquirers. In support of this, the results in Table 3 show that family firm acquirers are positively associated with domestic M&A deals (β = .03, p = .003). The BESD suggests that family firm acquirers are 3% more likely to pursue domestic M&A deals than nonfamily firm acquirers.15 Applied to the worldwide M&A activities in 2022 (IMAA, 2022), this relates to 1,489 more domestic M&A deals conducted by family firm acquirers, reflecting a deal value of US $102 billion.

H2b predicts that domestic M&As are associated with a lower M&A performance than cross-border M&A deals. The results show that domestic M&A deals are negatively associated with M&A performance (β = –.04, p = .000), thus supporting H2b. The BESD illustrates that domestic M&As have 4% lower success rates than cross-border M&As, which, again applied to the worldwide M&A activities in 2022, relates to 1,985 domestic M&A deals with lower success rates, reflecting a deal value of US $136 billion.

H2c predicts that higher levels of domestic M&As negatively mediate the relationship between family firm acquirers and M&A performance. In line with this prediction, we find a significant negative indirect effect of family firm acquirers on M&A performance through domestic M&As (β = –.001, p = .005; Sobel test, z = –2.32, p = .020; Aroian test, z = –2.27, p = .023; Goodman test, z = –2.38, p = .018), which supports H2c.

Finally, H3 predicts that family firm acquirers are associated with higher M&A performance than nonfamily firm acquirers. In line with H3, the MASEM results in Table 3 show a positive and significant direct effect of family firm acquirers on M&A performance (β = .034, p = .001), resulting in a positive and significant total effect (β = .035, p = .001). The BESD illustrates that family firm acquirers have 4% higher success rates in M&As than nonfamily firm acquirers. Applied to the worldwide M&A activities in 2022 (IMAA, 2022), this relates to 1,985 M&A deals with higher success rates conducted by family firm acquirers, reflecting a deal value of US $136 billion.

Post Hoc Analyses

Family board involvement

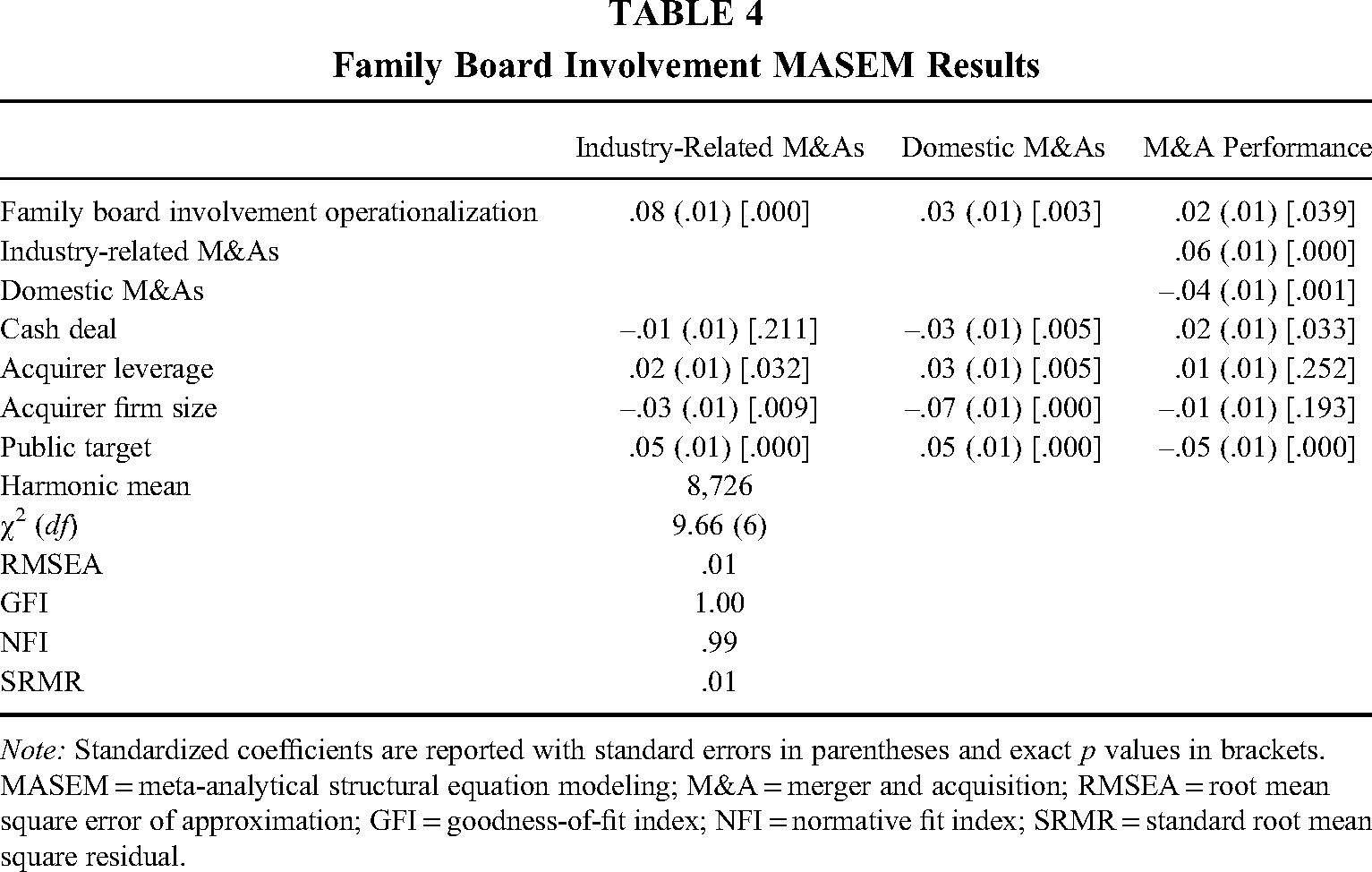

We examined whether the influence of family firm acquirers on industry-related and domestic M&As depends on the operationalization of family firm. For this purpose, we created a subsample of primary studies that used family board involvement to differentiate family and nonfamily firms. Given this, we created another meta-analytic correlation matrix and reran the MASEM. The results presented in Table 4 show that the influence of family firm acquirers on industry-related M&As is significantly (p = .031) more positive for studies using the family board involvement operationalization (β = .08, p = .000) as compared with ownership-based operationalizations (β = .02, p = .024). The mediation analysis shows that the indirect effect of family firm acquirers on M&A performance through industry-related M&As is substantially higher for family board involvement operationalization (β = .01, p = .001; Sobel test, z = 4.88, p = .000; Aroian test, z = 4.85, p = .000; Goodman test, z = 4.90, p = .000) than otherwise (β = .001, p = .019; Sobel test, z = 2.23, p = .026; Aroian test, z = 2.21, p = .027; Goodman test, z = 2.26, p = .024).

Family Board Involvement MASEM Results

Note: Standardized coefficients are reported with standard errors in parentheses and exact p values in brackets. MASEM = meta-analytical structural equation modeling; M&A = merger and acquisition; RMSEA = root mean square error of approximation; GFI = goodness-of-fit index; NFI = normative fit index; SRMR = standard root mean square residual.

The results in Table 4 show that the influence of family firm acquirers on domestic M&As according to family board involvement operationalization (β = .03, p = .003) did not significantly differ (p = .851) from studies using other ownership-based operationalizations (β = .04, p = .000). The mediation analysis shows that the negative indirect effect of family firm acquirers on M&A performance through domestic M&As does not differ for studies using the family board involvement operationalization (β = –.001, p = .006; Sobel test, z = –2.36, p = .018; Aroian test, z = –2.31, p = .020; Goodman test, z = –2.42, p = .016) than otherwise (β = –.001, p = .003; Sobel test, z = –2.58, p = .010; Aroian test, z = –2.53, p = .011; Goodman test, z = –2.63, p = .009). In summary, our post hoc analysis suggests that the indirect effect of family firm acquirers on M&A performance through industry-related M&As is stronger for studies applying a narrow definition of family firms that requires board involvement rather than mere ownership.

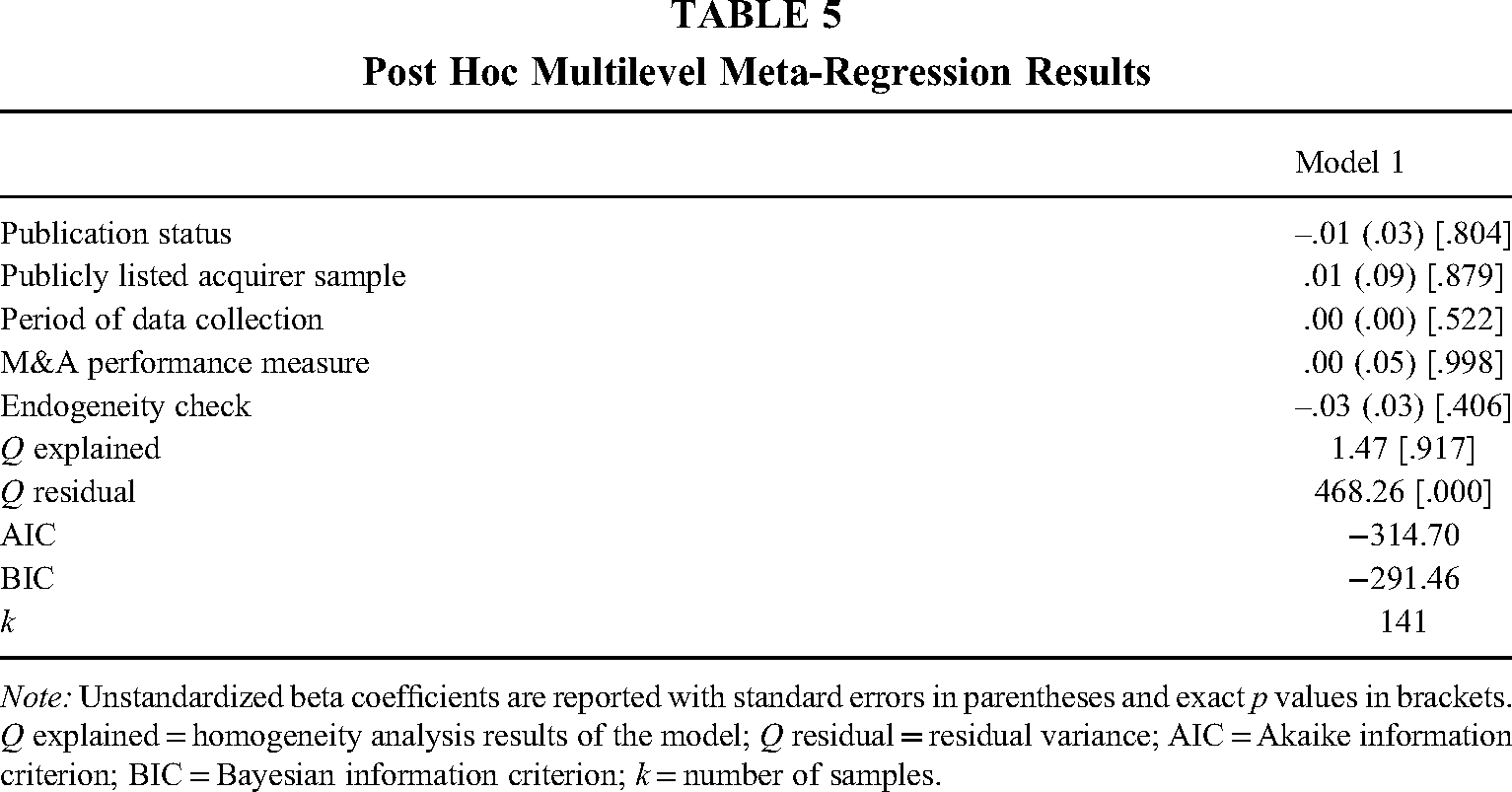

Post hoc meta-regression

Our meta-analytic results may have been affected by the research design and characteristics of the underlying studies. To check the robustness of our results, we conducted a post hoc multilevel meta-analytic regression analysis. Specifically, meta-regressions use the effect size of the underlying study as the dependent variable and potential moderator variables as independent variables (Gonzalez-Mulé & Aguinis, 2018; Lipsey & Wilson, 2001). Again, we followed recent recommendations (Cheung, 2019; Fernández-Castilla et al., 2020) and employed a multilevel approach to account for the fact that multiple effect sizes are nested within studies through a three-level random effects meta-regression using the metaphor package in R (Viechtbauer, 2010). In our multilevel meta-regression, we first controlled for publication bias (Rosenthal, 1979) by including a dummy variable denoting whether a study is published (1) or not (0). Second, extant literature has stressed that publicly listed firms are exposed to the pressures for greater risk taking and higher returns (Carney, van Essen, Gedajlovic, & Heugens, 2015). Hence, we controlled for whether a study based its sample on publicly listed (1) or private (0) acquirers.16 Third, the analysis of M&A performance in specific periods, such as during M&A waves, may have a significant effect on M&A performance (Wang & Shailer, 2017). We thus controlled for primary study samples that analyzed M&A deals in different periods by including the median of the period of the data collection for each study (Bilgili et al., 2016). Fourth, we controlled for different M&A performance measures used in primary studies by differentiating market-based (1) and accounting-based (0) measures of M&A performance. Finally, we included a dummy variable coded as (1) when effect sizes were taken from primary studies that conducted an endogeneity check and (0) otherwise (Duran et al., 2016). Results from our post hoc multilevel meta-analytic regression analysis reported in Table 5 revealed no evidence that different characteristics of the underlying studies significantly affect the relationship between family firm acquirers and M&A performance.

Post Hoc Multilevel Meta-Regression Results

Note: Unstandardized beta coefficients are reported with standard errors in parentheses and exact p values in brackets. Q explained = homogeneity analysis results of the model; Q residual = residual variance; AIC = Akaike information criterion; BIC = Bayesian information criterion; k = number of samples.

Publication bias

We calculated the number of samples reporting insignificant results that would be needed to reduce our meta-analytic effect sizes to the point of nonsignificance (fail-safe n; Rosenthal, 1979). The fail-safe n values indicate that publication bias is not a concern in this study: family firm acquirers–M&A performance, n = 10,814; family firm acquirers–industry-related M&As, n = 764; family firm acquirers–domestic M&As, n = 61; industry-related M&As–M&A performance, n = 717; domestic M&As–M&A performance, n = 122. Finally, we performed a MASEM with published studies only (see Supplement 2A online). Our results remain robust.

Different operationalizations of industry-related M&As

We conducted post hoc MASEM analyses to control for different operationalizations of industry-related M&As (see Supplements 2B–D online). This shows that the influence of family firm acquirers on industry-related M&As and the effect of industry-related M&As on M&A performance are strongest in studies using four-digit SIC codes (i.e., horizontal M&As) and weakest yet still significant in studies using two-digit SIC codes. The mediation path from family firm acquirers to M&A performance through industry-related M&As increases when the underlying studies measure industry-related M&As using two-digit SIC codes (β = .001, p = .016) to three-digit SIC codes (β = .002, p = .025) to four-digit SIC codes (β = .006, p = .001). These results indicate that horizontal M&As have the strongest M&A performance. Finally, we controlled for the extent of prior industry diversification of acquirers in our MASEM, which shows that our results remain robust (see Supplement 2E online).

Discussion

Prior research has sparked a controversial discussion about M&A performance differences between family and nonfamily firm acquirers (e.g., Bauguess & Stegemoller, 2008; Caprio et al., 2011; Feldman et al., 2019). Although research agrees that family influence matters for M&A performance, the underlying mechanisms and direction of this effect remain unclear.

We advance the discussion on the underlying mechanisms by theorizing that family members’ desire to preserve SEW influences their choice of specific M&A strategies toward industry-related and domestic M&As, which have contrary effects on M&A performance. Thus, we contribute to prior research on the family firm–M&A performance relationship by providing a more nuanced understanding of the underlying mechanisms explaining these relationships. Specifically, we argue, based on family firm research, that family firms favor the pursuit of industry-related and domestic M&As because they foster transgenerational control, strengthen stakeholder relationships, and maintain the family's identification with the firm (Berrone et al., 2012). By integrating prior M&A research, we further suggest that their preference for industry-related M&As leads to increased M&A performance (Datta et al., 1992), but their preference for domestic M&As lowers M&A performance (Meckl & Röhrle, 2016). Mediation hypotheses are supported through meta-analytic techniques based on 51 primary studies, 210 effect sizes, and 242,123 M&A deals. By uncovering these diverging effects of family firm acquirers, our study helps explain the previously inconsistent findings on family firm acquirers’ M&A performance.

Our study contributes to the controversial discussion about the overall effect of family firm acquirers on M&A performance by building on the concept of SEW resources (Combs et al., 2022). While prior research shows that family members’ pursuit of SEW creates specific resources in family firms (e.g., Deephouse & Jaskiewicz, 2013) that can change firm outcomes (Combs et al., 2022), we extend this idea to the M&A context. We argue that family firms, due to at least three SEW resources—LTO, strong stakeholder relationships, and a favorable firm reputation—are particularly well suited to diligently select and thoroughly integrate target firms, leading to overall better M&A performance when compared with their nonfamily firm counterparts. The meta-analytical results are in line with our predictions: we find a positive direct effect in addition to the previously described mediated effects of M&A strategies, resulting in an overall positive relationship between family firm acquirers and M&A performance. As such, our study provides important implications for future family firm research and the M&A literature in general.

Implications for Family Firm Research

Our study identified two important M&A diversification strategies that help explain how family firm acquirers affect M&A performance. The finding that family firms prefer certain M&A strategies might also inform family firm research on other firm outcomes, such as innovation (e.g., Duran et al., 2016), encouraging researchers to identify specific strategies that are preferred by family firms. Our study suggests that family firms engage in beneficial and detrimental M&A strategies, indicating that family owners can be a double-edged sword for M&A performance. This insight might inform other “black box” discussions in the family firm literature, such as the general family firm–performance discussion (e.g., Davila, Duran, Gómez-Mejía, & Sanchez-Bueno, 2022; Lohwasser, Hoch, & Kellermanns, 2022).

In our theorizing, we highlighted the role of SEW preservation concerns in pursuing specific M&A strategies. Prior work by Gomez-Mejia et al. (2018) suggests that M&A decisions may pose dilemmas for family firms regarding whether to maintain SEW or pursue future financial wealth. These researchers argue that under certain conditions—specifically, unsatisfactory firm performance—family firms are willing to forgo their SEW preservation concerns and engage in unrelated M&As to diversify the family firm's portfolio. Our findings show that unrelated M&A strategies do not lead to better, but worse, M&A performance (on average). In other words, the atypical M&A strategies chosen by family firms in difficult financial situations might destroy rather than create financial wealth. As suggested by Gomez-Mejia et al. (2018), one reason for this behavior is that family owners might look at M&As from a portfolio risk diversification perspective rather than a strategic fit perspective (Larsson & Finkelstein, 1999), thereby overlooking the enormous challenges of diversifying M&As (i.e., increased complexity; Gomez-Mejia et al., 2010). Hence, more in-depth research is needed to investigate why family firms engage in these detrimental M&A strategies under conditions of financial pressure and how specific situations, such as financial duress, alter strategic preferences (i.e., domestic vs. cross-border M&As).

Our theorizing builds on and extends the concept of SEW resources (Combs et al., 2022) to the M&A context. Prior theory suggests that SEW resources help family firms better implement strategies, such as corporate social responsibility, and thus enhance firm performance (Combs et al., 2022). We apply and adapt this idea by arguing that because of their SEW resources, family firms are better able to integrate their M&A targets. We theorize that SEW resources, such as LTO, strong stakeholder relationships, and favorable reputations (Combs et al., 2022), enable family firms to also make better decisions in the target selection process. One implication of this theorizing is that future research could investigate how SEW resources influence other strategic decisions, such as international entry mode decisions (Arregle et al., 2017), innovation decisions (Calabrò et al., 2019), and corporate entrepreneurship decisions (Kellermanns & Eddleston, 2006), and their performance consequences.

Implications for M&A Research

Our study emphasizes that the M&A strategies pursued by family firms differ from those of their nonfamily firm counterparts, leading to a variance in M&A performance. This finding implies that different firm owners favor different M&A strategies, which can lead to different performance outcomes. We focused on the idiosyncrasies of family firm acquirers in this study; however, the preferred M&A strategies of other firm owners, such as institutional investors or blockholders, warrant further investigation because they may have different strategic goals that might contribute to performance differences among M&As (Connelly, Hoskisson, Tihanyi, & Certo, 2010; King et al., 2021). Such future research might differentiate between owners focused on operational levers, such as family firms, and those focusing on financial levers, such as family offices. Future research may also examine whether firms owned by specific owners use M&As primarily to achieve efficiency gains (i.e., economies of scale and scope) or if they use them as a catalyst for strategic change and corporate renewal. Prior research suggests that M&As can be particularly helpful for gaining access to new knowledge (i.e., about technologies; Ahuja & Katila, 2001) or to “recombine knowledge in novel ways” (Graebner et al., 2017: 8). Hence, an important implication of our study is that future research should move beyond efforts to analyze whether firms owned by a specific ownership type have better or worse M&A performance (i.e., the direct effect) toward how their strategic M&A decisions differ and thus help explain different M&A performance effects.

Our study shows that family firms, irrespective of their motives for pursuing M&As (e.g., self-serving motives; Bauguess & Stegemoller, 2008), have better M&A performance. We theorize that this is a result of their unique SEW resources. This finding might also inform the general M&A literature, which shows that resources such as knowledge, experience, and capital (social, human, and financial) are important for M&A performance (for an overview, see Graebner et al., 2017; King et al., 2021). Our theorizing suggests that other resources might be important for the selection and integration of M&A targets, such as “patient capital” (i.e., long-term vs. short-term), the personal networks inside and outside the acquiring firm (e.g., of the top management, the corporate board, or institutional investors), and the motivation of the acquirers’ employees. While certainly not all such resources will be found to be important to the same extent as in nonfamily firms, our research suggests merit in future studies that investigate whether similar resources matter for other firms (and, if so, under which conditions) and how such resources affect M&A performance.

Practical Implications

Our study has practical implications for family and nonfamily firms pursuing M&A deals. First, we present further evidence that industry-related M&As lead to superior M&A performance, encouraging family and nonfamily firms to pursue this M&A strategy. Moreover, our study cautions family firms against the pursuit of often-preferred domestic (vs. cross-border) M&A deals. Finally, given our findings, decision makers in family and nonfamily firms should be encouraged to critically assess the resources available in the firm for selecting and integrating M&A targets, given their critical relevance for M&A performance.

Limitations

Our study has several limitations that provide fruitful additional opportunities for future research. First, as in any meta-analysis, our study was constrained by the characteristics of the underlying primary studies. In a post hoc meta-regression, we controlled for whether the primary studies accounted for endogeneity issues, but meta-analytic methods are unable to empirically address causality concerns with the methodological approaches available in primary empirical studies (e.g., instrumental variables; Bergh et al., 2016). To validate the causal nature of the proposed mechanisms, we encourage future studies to employ alternative empirical designs, such as matched-pair or single-industry studies, to study the relationships of interest.

Second, our findings primarily stem from samples of publicly listed acquirers. However, privately held family firms are spared from the pressures of the stock market (Carney et al., 2015) and thus might place even greater emphasis on preserving family members’ SEW in M&A deals, thereby strengthening the proposed relationships. Although we controlled for public versus private acquirer status in a post hoc meta-regression, we encourage future studies to investigate the M&A strategies of privately held family firm acquirers. The relationship between family firm acquirers and M&A performance might also be influenced by acquirers’ prior M&A experience; research has shown that acquirers are more successful in M&As when they have conducted M&As in the past, especially when the target is similar to prior M&As (e.g., prior cross-border M&A activities; Basuil & Datta, 2015; Hitt et al., 2001). Yet, we were unable to account for this because of the lack of information provided by primary studies. We therefore encourage future studies to examine whether the performance implications and the M&A strategies chosen of family versus nonfamily firms are affected by prior M&A experiences. In addition, we could test only for linear effects of prior industry diversification (see supplemental analyses online), and we encourage future research on this topic.

Third, our study is unable to capture the full spectrum of family firm heterogeneity (Chua, Chrisman, Steier, & Rau, 2012) because we are constrained to variables investigated sufficiently in primary studies. Future research might investigate the effects of additional sources of family firm heterogeneity, such as generational stage (Villalonga & Amit, 2006) or different SEW goals (Kotlar & De Massis, 2013), on family firms’ M&A strategies and M&A performance.

Fourth, our study builds on only 51 primary studies, and some of our meta-analytic estimates are based on few effects and sample sizes, thereby covering a fraction of all M&A deals. Although the synthesis of effect sizes from primary studies reduces sampling error, our findings, particularly those based on a few effect sizes, should still be interpreted with caution because they may suffer from second-order sampling error (Schmidt & Hunter, 2015).

Conclusion

We theorized that family members’ desire to preserve their SEW favors the pursuit of distinctive M&A strategies that are beneficial (industry-related M&As) and detrimental (domestic M&As) to M&A performance. We therefore shed light on the different strategic mechanisms that help reconcile prior inconclusive findings on the family firm acquirer–M&A performance relationship. Given recent family firm theorizing, we further argue that the desire to preserve their SEW also leads to idiosyncratic SEW resources that help family firm acquirers in better selecting and integrating M&A targets. Consistent with this logic, family firm acquirers are, on average, associated with better M&A performance than nonfamily firm acquirers. Our meta-analytic results, based on 51 primary studies covering 242,123 M&A deals, are consistent with our predictions. We hope that our study encourages scholars to go beyond examining the direct (M&A) performance consequence of family influence and thus to provide more insights into the mechanisms that help explain these relationships. For practitioners, we hope that our study provides valuable guidance regarding which M&A strategies are more promising than others to enhance M&A performance.

Supplemental Material

sj-docx-1-jom-10.1177_01492063231178027 - Supplemental material for Family Firms, M&A Strategies, and M&A Performance: A Meta-Analysis

Supplemental material, sj-docx-1-jom-10.1177_01492063231178027 for Family Firms, M&A Strategies, and M&A Performance: A Meta-Analysis by Marina Palm, Priscilla S. Kraft, and Nadine Kammerlander in Journal of Management

Footnotes

Acknowledgments

We thank the associate editor Jim Combs and the anonymous reviewers for their extremely helpful guidance in the revision process. We also thank Martin Eisend, Marc van Essen, and Michael Withers for their very helpful comments on the manuscript.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.