Abstract

The executive labor market (ELM) is a topic of interest that spans several academic fields. The outcomes of the ELM, including executive selection, succession, and compensation, are important considerations as they influence executive decision making and other organizational outcomes. Yet, a comprehensive framework of ELM dynamics currently does not exist. To address this shortcoming, we reviewed the existing literature using five fundamental questions: (1) What executive jobs are available? (2) Who is available to fill executive jobs, and what is valued on the ELM? (3) Who signals interest in the executive jobs? (4) Who gets offered/accepts the executive job, and what is the agreed-upon compensation? (5) How do status and social capital influence ELM outcomes? By answering these questions, our review provides a framework for integrating existing research on the ELM while suggesting avenues for future research.

Keywords

Who advances to the top executive positions of organizations? What characteristics do these individuals possess that allow them to advance? How do these characteristics influence their subsequent decision making and other organizational outcomes? How are these individuals compensated? What is the process of executive turnover? These questions and many others reflect the general interests in the labor market surrounding the recruitment, selection, compensation, and turnover of executives (Boivie, Graffin, Oliver, & Withers, 2016; Gayle, Golan, & Miller, 2015). The executive labor market (ELM) is a critical topic within the broad study of strategic leadership (Finkelstein, Hambrick, & Cannella, 2009; Hambrick & Wowak, 2021). It has garnered this attention because of the recognition that executives help shape firm strategy (Hambrick & Mason, 1984) and influence a variety of organizational outcomes (Finkelstein et al., 2009).

The ELM also reflects the complex dynamics underlying the market, as well as the social and behavioral processes that occur within the corporate elite (Mills, 1956; Useem, 1979). As such, the study of the ELM spans a number of disciplinary fields, including management (e.g., Ference, Stoner, & Warren, 1977; Hitt & Barr, 1989; Pan, 2017), labor economics (e.g., Gayle, Golan, & Miller, 2012), sociology (e.g., Blair-Loy, 1999), accounting (e.g., Baginski, Campbell, Hinson, & Koo, 2018), finance (e.g., Li, Low, & Makhija, 2017), and marketing (e.g., Rui, Gupta, & Grewal, 2017). Research has leveraged multiple perspectives to examine the ELM, including agency theory (Fama, 1980), upper echelons theory (Hambrick, 1989), the resource-based theory of managerial capabilities (Datta & Iskandar-Datta, 2014), resource dependence theory (Pfeffer & Leblebici, 1973), and human and social capital theory (Bermiss & Murmann, 2015). This research has offered a number of insights into the aforementioned questions related to the ELM.

However, despite these critical insights, much of the research on the ELM remains siloed across the different disciplinary and theoretical areas. Consequently, little integration of the existing literature on the ELM exists, creating disparate research areas focused on general topics such as succession, compensation, and turnover. This lack of integration is problematic given the implications that the ELM may have for executive decision making and organizational outcomes (Engel, van Burg, Kleijn, & Khapova, 2017; Gunz & Jalland, 1996; Zhao, 2018). A comprehensive framework of ELM could offer a multifaceted perspective of these dynamics. Such a framework could also offer broader societal benefits by providing a foundation for the study of diversity at the top of organizations (Gayle et al., 2012), which in turn has important implications for diversity and social class dynamics more generally (Lee, Kish-Gephart, Mizruchi, Palmer, & Useem, 2021). As executives expand their traditional roles to focus on social problems and issues (Krause & Miller, 2020), the ELM could offer important insights into the individual and organizational drivers of such outcomes.

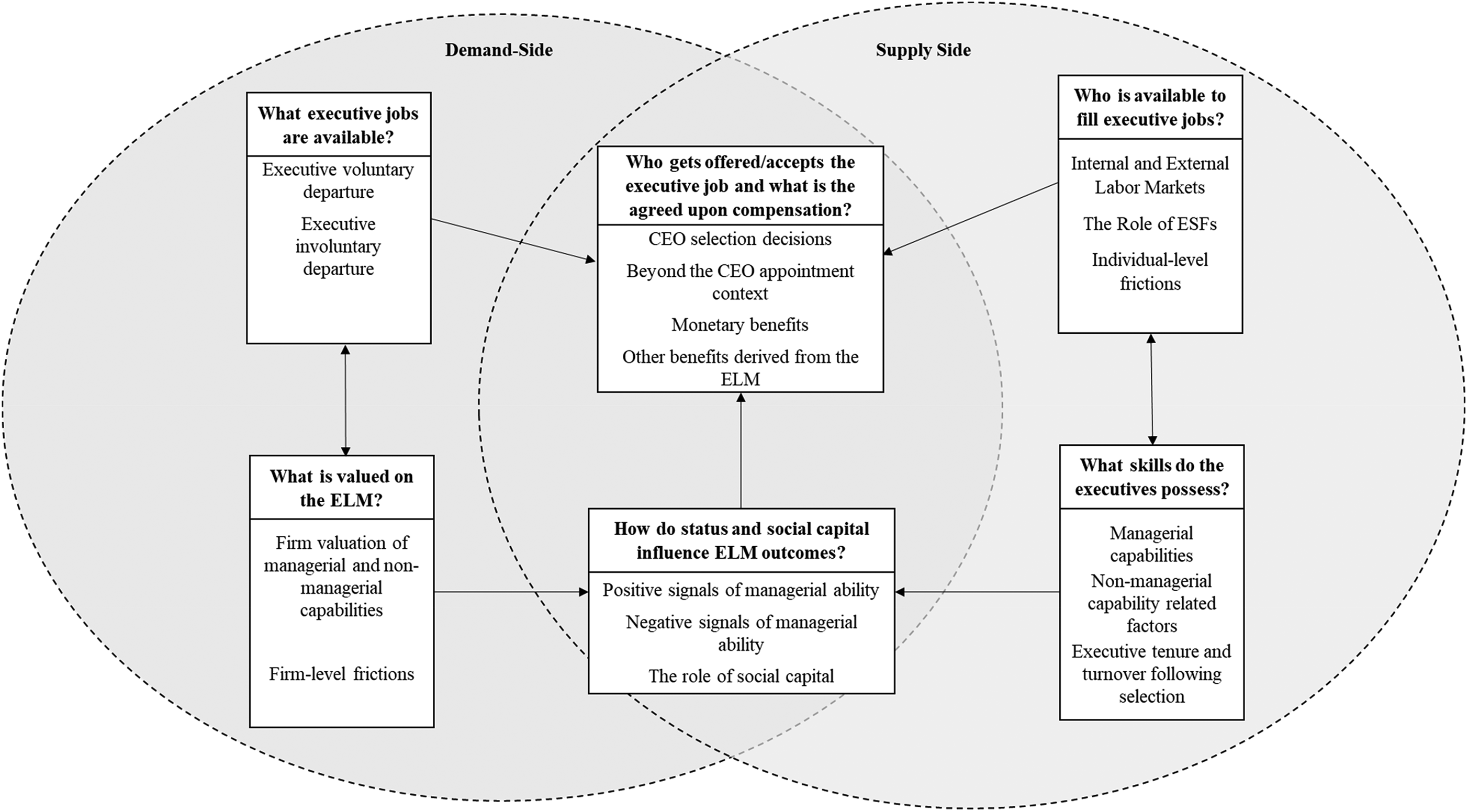

Consequently, in this article, we conduct a review of research on the ELM. In doing so, we seek to develop a framework of ELM dynamics and highlight future research opportunities so that scholars in different disciplines can explore the influence of the ELM from a unified perspective. To do so, we first define the ELM and describe the unique properties of this market as compared with other labor markets. We then organize our review around five fundamental questions: (1) What executive jobs are available? (2) Who is available to fill executive jobs, and what is valued on the ELM? (3) Who signals interest in executive jobs? (4) Who gets offered/accepts the executive job, and what is the agreed-upon compensation? (5) How do status and social capital influence ELM outcomes? By leveraging existing research to answer these questions, we offer a unified perspective of the ELM.

The ELM as a Unique Labor Market

The ELM represents the interaction of supply-and-demand forces for executive positions (Gayle et al., 2012). The demand side reflects potential hiring firms, and the supply side is the pool of potential executive candidates. While it shares many overlapping characteristics with other labor markets, researchers studying the ELM have typically assumed that key differences exist between the ELM and other labor markets in terms of executive job demands, discretion, liability, stability, and visibility (Broschak, 2021; Busenbark, Krause, Boivie, & Graffin, 2016; Hambrick, Finkelstein, & Mooney, 2005). From serving as leaders, spokespeople, and figureheads to resource allocators, entrepreneurs, and negotiators (Mintzberg, 1973), executives perform unique roles that span boundaries between a firm and its environment (Thompson, 1967). These critical roles not only give them the autonomy and ability to shape firm actions but also make them highly visible to actors inside and outside their firms.

The ELM is more visible with executive appointments, departures, and compensation packages garnering significant media and, in turn, public attention (Bednar, Love, & Kraatz, 2015; Jensen & Zimmerman, 1985; Kang & Kim, 2017). Reflecting the growing influence of media within the CEO succession context, Khurana (2002: 78) explains, The rise of business media and analysts, with their fixation on the CEO, has, in turn, introduced a new set of informal ground rules to CEO succession: a critical consideration in evaluation a potential CEO today is his or her ability to command attention from the media and stock market analysts in a way that will establish credibility for the firm and inspire confidence in both investors and others.

Through their roles, executives set their firms’ vision and mission and make important decisions for the firms’ future directions (Cyert & March, 1963; Hambrick & Mason, 1984). They exert significant power and control throughout the organization, as reflected in the titles of their positions, such as president, (executive/senior) vice president (VP), and various C-suite titles (Flöthmann & Hoberg, 2017; Menz, 2012). While some studies focus on the divisional role of executives tied to a specific region or a business unit (e.g., Drazin & Rao, 1999), extant literature has paid greater attention to the functional roles of top managers (e.g., Cannella, Park, & Lee, 2008; Hambrick, Cho, & Chen, 1996; Ndofor, Sirmon, & He, 2015). Targeted functional groups include chief financial officers (CFOs; e.g., Khan, Kalelkar, Miller, & Gerard Sanders, 2018), chief operating officers (e.g., Marcel, 2009), chief accounting officers (e.g., Wu & Liu, 2022), chief information officers (e.g., Sobol & Klein, 2009), marketing and sales executives (e.g., Wang, Gupta, & Grewal, 2017), human resource executives (e.g., Lawson & Limbrick, 1996), and supply chain executives (e.g., Flöthmann & Hoberg, 2017).

The labor market for CEOs is the most comprehensively studied market by researchers focused on senior executives (Finkelstein et al., 2009; Hambrick, 2007; Schoar & Zuo, 2016). Indeed, even research positioned as studying the broader ELM has largely limited itself to the context of CEOs (DiPrete, Eirich, & Pittinsky, 2010; Nagel, 2010; Palia, 2000; Rajgopal, Taylor, & Venkatachalam, 2012). In contrast, significantly less research has focused on understanding the labor market for other top executives. This imbalance, however, more than likely reflects limitations in data availability on other non-CEO executives (Krause, Roh, & Whitler, 2022) than their importance, as upper echelons theory has historically considered the entire top management team (TMT) as central to understanding firm outcomes (Hambrick & Mason, 1984).

Review Methodology

To conduct our narrative review of the ELM literature, we worked to follow best practices for systematic literature reviews (Hiebl, 2021; Short, 2009). Our review was based on keyword searches using the Business Source Ultimate database. We used a combination of two sets of keywords and downloaded all citations in reference management software Endnote if those two keywords concurrently appeared in the abstract of the article. The first set of keywords included “CEO,” “executive,” “managerial,” and “top management team,” while the second set of keywords included “appointment,” “career, departures,” “dismissal,” “exit,” “interfirm mobility,” “labor market,” “migration,” “mobility,” “movement,” “promotion,” “raise,” “recruitment,” “selection,” and “succession.”

Our review is distinctive in several ways. First, we focus on the prior research that has explicitly examined labor market dynamics and considerations when examining executive appointments, departures, and compensation. In this regard, our review complements previous reviews of these different areas. Second, we limited our focus to executives and did not cover research related to corporate directors given the unique context of the market for corporate directors (Withers, Hillman, & Cannella, 2012). Last, we prioritized research focused on ELM dynamics and outcomes; yet, research on related areas—including CEO and executive succession (Berns & Klarner, 2017), executive compensation (Devers, Cannella, Reilly, & Yoder, 2007; Wowak, Gomez-Mejia, & Steinbach, 2017), and executives on the market for corporate directors (Withers et al., 2012)—also inform the broader work on the ELM.

As expected, the initial search resulted in a substantial number of empirical and conceptual articles (n = 3,404). We utilized the journal name and the article's title for our initial screening to remove articles that have no relationship to our topic and to select studies published in prestigious outlets in accounting, finance, economics, sociology, and management. 1 We then closely read through the abstract of >1,500 articles that were singled out from the initial screening to determine our final set for review. After this process, we were left with the final list of 307 articles. We then organized the existing literature to answer several critical questions and produce a general ELM framework. Table 1 provides a detailed overview of several studies considering the dynamics and outcomes of the ELM.

Exemplar Studies Examining the ELM

Note: CEO = chief executive officer; CFO = chief financial officer; CSR = corporate social responsibility; ELM = executive labor market; NA = not applicable; R&D = research and development; TMT = top management team.

An ELM Framework

What Executive Jobs Are Available?

A vacant executive position may be due in part to retirements, voluntary (or involuntary) exits, or expansion of the executive team (Finkelstein et al., 2009). Expanding the executive team may occur in response to a variety of organizational considerations, including changes in the organization’s scope, after an acquisition or merger (Hambrick & Cannella, 1993), or in the firm's external environment (Yamak, Nielsen, & Escribá-Esteve, 2013). Scholars studying ELM dynamics acknowledge the challenges in observing many of the available positions on the market. To address this shortcoming, the literature has instead focused on the voluntary or involuntary departures of executives; however, empirically, this distinction can often be challenging to determine (Gentry, Harrison, Quigley, & Boivie, 2021). Executive voluntary turnover derives primarily from individuals’ motivation or abilities, whereas involuntary turnover is more contingent on contextual factors, such as an organization's financial conditions. CEO and executive succession are extensively studied topics, representing a well-developed literature in and of itself (for reviews see Berns & Klarner, 2017; Berns, Gupta, Schnatterly, & Steele, 2021). Our intention is not to review the overall drivers of executive succession, but we leverage this literature to inform us regarding how positions become available on the ELM.

Executive Voluntary Departure

One of the primary motives for executives’ voluntary exit may be closely associated with their desire for career advancement or to be rewarded with higher compensation (for a review of the broader literature on exit turnover, see Hom, Lee, Shaw, & Hausknecht, 2017). In turn, executives’ probability of getting promoted into CEO positions may influence their turnover rates. Vancil (1987) states that firms are expected to lose some of the executives who are passed over during the CEO succession process. Shen and Cannella (2002) find that a large portion of heirs apparent leave their firms without promotion or never ascend to the CEO position. Friedman and Olk (1995) assert that wait time to promotion can be a frustrating experience for appointed successors, leading these executives to departures to other firms before experiencing promotion. In that sense, executives with the desire to become a CEO will be more likely to depart when the incumbent CEO has strong power and is unwilling to give up influence and control (Bickford, 2001; Cannella & Shen, 2001). Moreover, executives who are able to signal their managerial capabilities may be more likely to exit their firms. In particular, firms that voluntarily disclose positive information about their value creation and appropriation activities are also providing positive signals about their managers' abilities, which leads to an increase in executive voluntary turnover (Stern & James, 2016).

Another important driver of voluntary executive departures is the desire to increase compensation through interfirm mobility (Broschak, 2021; Hall, 1996; Reitman & Schneer, 2005). Scholars have primarily utilized the theoretical lens of tournament theory (Main, O'Reilly, & Wade, 1993) or social comparison theory (Festinger, 1954) to examine the relationship between compensation and executive turnover, suggesting that executives consider other top executives (i.e., horizontal comparison) or CEOs (i.e., vertical comparison) as frames of reference and compare their levels of compensation with them (Wowak et al., 2017). This research suggests an important role that social comparison performs in influencing TMT group-level turnover (Ridge, Aime, & White, 2015; Ridge, Hill, & Aime, 2014). For instance, Ridge et al. (2014) find that the level of pay dispersion among executives was positively related to their turnovers, while the pay disparity between CEO and executives was negatively related to their turnovers (pay disparity is also studied more broadly; e.g., Trevor, Reilly, & Gerhart, 2012). Ridge et al. (2014) also examine the moderating effect of firms’ pay level relative to the market finding that firms paying higher compensation as compared with other firms attenuate the relationship between CEO–TMT pay disparity and executive turnover. Finally, Pissaris, Heavey, and Golden (2017) find that executives with oversight responsibilities, such as chief operating officer or CFO, experience greater pay sensitivity than those with divisional responsibilities, such as a regional VP, with horizontal and vertical pay disparities in predicting their turnover.

The preservation of reputation is another significant driver of voluntary executive departure (Jiang, Cannella, Xia, & Semadeni, 2017). Research suggests that executives from firms that experience bankruptcy (Eckbo, Thorburn, & Wang, 2016) or organizational scandals may experience negative repercussions on the market for managerial talent (Cannella, Fraser, & Lee, 1995; Sutton & Callahan, 1987). Therefore, executives may “jump ship” from an offending firm and obtain employment in other firms to avoid reputational penalties (Semadeni, Cannella, Fraser, & Lee, 2008). For instance, organizational shocks, such as relational changes from other executive turnover or reputational threats from bankruptcies or lawsuits, may increase the likelihood of executives’ exit in an effort to preserve their future career opportunities (Andrus, Withers, Courtright, & Boivie, 2019).

Executives may also voluntarily depart if they perceive that their relative standing in their firm is reduced—for example, due to the firm being acquired by another firm (Hambrick & Cannella, 1993). Executives in critical roles experience higher turnover after their firms are acquired (Ng & Stuart, 2022). Other motives that executives express for voluntary departures include health reasons and personal reasons, such as the desire to spend more time with family (e.g., Nelson & Burke, 2000). Executives also may leave to fulfill their personal values, such as by engaging in meaningful work or becoming a founding member of a new company (Agarwal, Campbell, Franco, & Ganco, 2016).

Executive Involuntary Departure

Involuntary turnover occurs when an executive is replaced because of ineffective or incompetent management (Berns et al., 2021). Research in this area generally finds that negative organizational performance is the strongest predictor of CEO and executive openings (Finkelstein et al., 2009). Similarly, firms engaging in turnaround or strategic change exhibit greater levels of executive turnover (Barron, Chulkov, & Waddell, 2011; Mueller & Barker, 1997). More recently, other measures of performance, such as poor social performance, have been found to be associated with executive turnover (Dai, Gao, Lisic, & Zhang, 2023; Hubbard, Christensen, & Graffin, 2017). Relatedly, shareholder unrest regarding wealth creation and corporate social responsibility is related to CEO turnover (Lee, Gupta, & Hambrick, 2022).

Prior research also suggests that incumbent CEOs may seek to dismiss other executives as a form of scapegoating to reduce their own employment risks following poor firm performance and other events such as bankruptcies or other corporate failings. In these cases, CEOs dismiss executives who directly report to them in an attempt to appease shareholders and stakeholders (Boeker, 1992). Under the scapegoating scenario, executives who have less relationship capital with the current CEO (e.g., executives who were appointed by the previous CEO) or have less power (e.g., executives who do not hold board positions) are more likely to be dismissed (Boeker, 1992; Mizruchi, 1983).

CEOs may also change executives based on their personal values or beliefs. For example, Crossland, Zyung, Hiller, and Hambrick (2014) find that CEOs with high career variety are associated with higher turnover in their TMTs, because they prefer to have their teams equipped with divergent perspectives and capabilities. CEOs can also replace executives for instrumental reasons, such as to better match the composition of the TMT to its external task environment (Keck & Tushman, 1993). For instance, unstable industry environments were related to higher executive replacement because firms have a greater need to continuously adapt to the quickly changing environment (Wiersema & Bantel, 1993).

Research suggests that while the rate of non-CEO dismissal is similar to that of CEOs, the direct effect of firm performance on executive turnover is weaker for non-CEOs (Fee & Hadlock, 2004). Cannella et al. (1995) similarly find that the chance of reemployment is significantly reduced for CEOs when they are associated with failed organizations, yet lower-level managers (e.g., executive VPs) are less likely to experience negative labor market consequences. These results indicate that non-CEO executives may not experience the same market settling up from poor performance as CEOs do; however, other factors may influence the relationship between firm performance and executive involuntary turnover. The broader literature contends that non-CEO executive turnover is more likely following CEO dismissal, especially when the new incoming CEO is selected from outside the organization (Friedman & Saul, 1991; Helmich & Brown, 1972; Shen & Cannella, 2002; Yan & Rajagopalan, 2004). This increased likelihood of turnover is partly because firms hire outside CEOs often to facilitate strategic change and divert strategic directions from the previous regime (Kesner & Dalton, 1994; Wiersema, 1995). Outside CEOs may thus dismiss incumbent TMT members to select new executives for their own management team (Fee & Hadlock, 2004; Friedman & Saul, 1991).

Various organizational- and environmental-level factors may also affect the likelihood of executives being dismissed. For example, corporate governance events, such as earnings restatements, are associated with increased levels of turnover in the TMT and especially for CFOs (Agrawal & Cooper, 2017; Arthaud-Day, Certo, Dalton, & Dalton, 2006; Collins, Masli, Reitenga, & Sanchez, 2009). Similarly, executives at firms being targeted by corporate lawsuits and those at firms with poor tax strategies may experience increased rates of turnover (Aharony, Liu, & Yawson, 2015; Andrus et al., 2019; Chyz & Gaertner, 2018). Moreover, firms that experience takeover bids are more likely to experience executive turnover, as such events signal information about managerial performance (Agrawal & Walkling, 1994), while the level of takeover intensity within the industry accentuates the relationship between poor firm performance and executive turnover (Denis & Denis, 1995). Finally, larger firms are more likely than smaller firms to be associated with a higher level of executive exit, in part, because executives at larger firms have increased employment opportunities (James & Soref, 1981; Pfeffer & Moore, 1980).

Market Dynamics Driving Turnover

Characteristics of the focal ELM may influence whether new executive jobs become available. For example, Fredrickson, Hambrick, and Baumrin (1988) contend that CEOs are more likely to be dismissed in industries in which there is a larger number of firms, as the number of firms signifies the volume of the executive pool from which firms can hire. Empirically, firms are more aggressive in replacing CEOs when the variance in CEO talent is low, suggesting a number of viable replacements (Aghamolla & Hashimoto, 2021). The presence of potential replacement candidates on the board of directors also may lead to an increase in the likelihood of executive turnover, especially for CEOs (Mobbs, 2013). Changes in labor market frictions can also lead to an increase in openings on the ELM. For example, using a sample from the National Football League, Allen, Schepker, and Chadwick (2022) find that the institution of a salary cap and free agency for players led to a decrease in coaching tenures and significantly increased dismissal rates. These authors suggest that these changes led to different types of human capital being valued on the coaching market.

Summary

Our understanding of what executive jobs are available on the ELM mainly derives from studies examining executive departures, either voluntary or involuntary. In this way, much of the existing research has been more concerned with what leads to executive openings (e.g., poor performance, better career opportunities) than connecting the outcome of job openings with a broader perspective on labor market dynamics. This suggest an opportunity for future research to more directly assess the implications of the circumstances surrounding how executive positions become available. In addition, the role of executive team expansion is less well studied given some of the unique challenges with capturing these dynamics. However, opportunities exist to continue to assess how firms respond to opportunities and threats in the external environment as well as changes in corporate scope through executive team expansion.

Who Is Available to Fill Executive Jobs, and What Is Valued on the ELM?

Executive selection and turnover decisions are influenced by the availability of potential candidates inside and outside the hiring firm who represent the available labor pool (Borokhovich, Parrino, & Trapani, 1996; Davis, 2005). Recent trends show that outside hiring for executives has surged, as the ELM is becoming more flexible and fluid (Crossland et al., 2014; Hollenbeck, 2009). This trend is partly explained by insights from the boundaryless career theory (Arthur & Rousseau, 2001; Baruch, Altman, & Tung, 2016; DeFillippi & Arthur, 1994), which was developed to explain the phenomenon of employees’ vigorous movement across firms, industries, and countries (Cheramie, Sturman, & Walsh, 2007; Sullivan, 1999). This perspective may be particularly relevant for the study of the ELM given changing dynamics in this interfirm mobility, reflecting the fact that executive skills and knowledge are often less firm specific and hence more easily transferable among firms (Frydman, 2019). Accordingly, executives may be less focused on developing firm-specific managerial capital and more focused on transferable skills that are highly rewarded on the ELM.

Executive search firms (ESFs) also play an important role in determining who is potentially considered to fill executive positions (Bonet, Cappelli, & Hamori, 2013; Dreher, Lee, & Clerkin, 2010; Manfredi, Clayton-Hathway, & Cousens, 2019). The increasing role of ESFs has fueled executives’ greater mobility, with these firms acting as an important labor market intermediary for filling executive positions (Cappelli & Hamori, 2014; Hollenbeck, 2009). ESFs thus serve as a gatekeeper regarding who is considered for executive openings (Bidwell, Choi, & Fernandez-Mateo, 2023), and for executives, being identified as a candidate by an ESF serves as a signal to the market (Steuer, Abell, & Wynn, 2015). Interestingly, prior managerial performance seems to play less of role in determining whom a search firm identifies, and the matches created between firms and executives through ESFs are not necessarily better than those matches created without the assistance of ESFs (Bidwell et al., 2023; Steuer et al., 2015).

Despite the prevalence of interfirm mobility, the value of firm-specific knowledge is still important when considering executive selection decisions (Shen & Cannella, 2002; Wang, Zhao, & Chen, 2017a). As such, internal labor market dynamics remain an important topic in the study of the ELM (Frederiksen & Kato, 2018; Frederiksen, Halliday, & Koch, 2016). Internal candidates for executive positions often possess existing relationships with other executives and information regarding the internal workings of the firm, which can lead to strategy stability (Brady & Helmich, 1984). Extensive CEO selection and succession literature thus advocates that it is the organizational context that determines the relative value of insiders versus outsiders, rather than one type of succession being universally better than the other (Finkelstein et al., 2009). One example can be employing outside CEOs when a firm is surrounded by an unstable environment. This combination can be detrimental for the organization since the new yet unfamiliar perspective that outside CEOs bring to the organization may be too abrupt and hence destructive under a quickly changing environment (Virany, Tushman, & Romanelli, 1992; Zhang & Rajagopalan, 2004). In general, the risk of mismatch between the executive and the organization is likely to be higher in the case of outside hiring (Zajac, 1990).

Managerial Capabilities

The research on executive selection and compensation emphasizes the role of managerial capabilities (Quigley, Wowak, & Crossland, 2020; Salvato, Minichilli, & Piccarreta, 2012) and generally finds that managerial capabilities are strongly associated with objective career success, such as compensation and promotions (Fitzsimmons & Callan, 2016; Kirchmeyer, 1998). For instance, Brookman and Thistle (2013) find that about 40% of the variation in executive compensation is explained by executives’ general skills. Furthermore, Salvato et al. (2012) identify that even in family firms, accumulated human capital is the most salient factor (more than other family-related considerations) that enabled individuals to obtain top executive and CEO positions. Managerial capabilities in this context indicate executives’ overall knowledge, skills, and abilities (KSAs) to effectively manage firms and influence firm performance (Carpenter, Sanders, & Gregersen, 2001; Datta & Iskandar-Datta, 2014). Given that managerial ability is generally unobservable, scholars have commonly used indicators such as tenure, experience, career background, and quantity and quality of education as proxies for executive human capital (Conyon, Haß, Vergauwe, & Zhang, 2019; Falato, Li, & Milbourn, 2015; Finkelstein et al., 2009).

Among many types of human capital, studies have largely paid attention to the value of executive experience (Crossland et al., 2014). Experience may include firm-specific, industry-specific, functional, board, and international experience. For example, Pan (2017) suggests that executive experience in conglomerates is especially valuable in highly diversified firms. Phan and Lee (1995) find that industry experience lowers the chance of a CEO's dismissal, while firm-specific skills had no such effects. Sobol and Klein (2009) show that chief information officers with information technology backgrounds provide greater benefits to the company than those with a general management background. Boivie et al. (2016) find that board service serves as an important signal of managerial capabilities and provides executives with greater mobility ability on the ELM. Finally, Carpenter et al. (2001) find that executives with international experience have an advantage on the ELM, leading to an increase in the likelihood of being promoted to a CEO position. In terms of other indicators of managerial capabilities, research finds that the amount and quality of education are associated with faster career success and advancement for executives (Flöthmann & Hoberg, 2017; Myers, Griffith, Daugherty, & Lusch, 2004). Judge, Cable, Boudreau, and Bretz (1995) similarly find that educational content mattered such that executives with business or law degrees had greater objective success than those with other degrees.

Following existing research on labor market consequences of general versus firm-specific human capital (Campbell, Saxton, & Banerjee, 2014; Coff, 1997; Raffiee & Byun, 2020; Raffiee & Coff, 2016), research finds that general managerial capabilities are rewarded with an increase in internal promotions and interfirm mobility (Frederiksen & Kato, 2018). Similarly, signals of general managerial capabilities, such as acquisition experience, lead to positive labor market outcomes, including promotion to the CEO position (Greene & Smith, 2021). Frydman (2019) contends that as general managerial capabilities gained in importance on the ELM, compensation within and between firms increased, as did interfirm mobility. In other words, the modern ELM emerged as managerial capabilities became more professionalized and less firm specific (Murphy & Zábojník, 2007). In contrast, executives with specialized support functions are generally less likely to receive favorable labor market outcomes (Olson, 2021).

Regarding the specific skill requirements for a firm, firms often seek executives who can provide knowledge that firms do not currently possess. For example, at the TMT level, Angwin, Paroutis, and Mitson (2009) claim that executives who supplement KSAs of CEOs are particularly valuable. Kor and Misangyi (2008) similarly find that there is an inverse relationship between board members’ and TMTs’ collective level of industry experience, suggesting that executives may be appointed to complement existing managerial capabilities of the TMT and board. At the organizational level, firms with higher research and development intensity may value executives with technical expertise (Pan, 2017), while complex firms may seek executives who seem capable to manage a challenging organizational context (Berry, Bizjak, Lemmon, & Naveen, 2006). Similarly, executives’ international experience is valuable when firms have a high level of international diversification, yet it may be less useful when firms are focused more on domestic markets (Daily, Certo, & Dalton, 2000). In the context of international experience, firms selecting a new CEO will attempt to match their global strategic context to the CEO's characteristics (Thams, Chacar, & Wiersema, 2020). Other specialized skills, such as tax savviness, may be sought by firms as well (Kubick, Li, & Robinson, 2020). At the environmental level, firms in a munificent environment tend to hire executives possessing similar industry experience to existing TMT members, while firms in more dynamic industries tend to hire executives possessing less similar industry experience (Nielsen, 2009).

Nonmanagerial Capability-Related Factors

While a rational economic perspective suggests that firms should select executives who possess the optimal level of managerial capital that meets their needs, executive selection decisions are complex and often go beyond simple considerations of managerial capabilities (Hitt & Barr, 1989). This occurs because the individuals involved in the selection decisions will be limited in their decision-making capability and may weigh benefits and costs differently (Sebora & Kesner, 1996). Nontask-related factors thus sometimes heavily affect executive selection decisions and, in turn, executive career outcomes.

For instance, scholars have focused on the role of gender in who is considered for executive positions. Consistent with self-categorization theory (Tajfel, 1978), one line of research suggests that female executives are more likely to be hired by firms with female CEOs (Bell, 2005) and a greater number of female board members (Terjesen & Singh, 2008). In contrast, the “queen bee syndrome” proposes that a token woman in the TMT may rather deter the promotion of other female employees into the TMT, positing a more competitive instead of supportive environment (Blalock, 1967; Staines, Tavris, & Jayaratne, 1974). Similarly, Dezső, Ross, and Uribe (2016) find that most firms have only one female executive on their TMTs, and the presence of a female executives lowers the likelihood of hiring additional female executives by 51%. In terms of work-family factors, being married and having children are reported to provide advantages to males in attaining executive positions in comparison with females (Schneer & Reitman, 2002; Smith, Smith, & Verner, 2013). In addition, male executives experience compensation and promotion benefits when their spouses are not working (Judge et al., 1995; Pfeffer & Ross, 1982; Stroh & Brett, 1996).

Evidence also exists on the role of other noncognitive characteristics that affect executive selection decisions. For instance, personality traits such as proactiveness, extraversion, and level of ambition are closely aligned with leadership roles and positively related to successful managerial career outcomes (Boudreau, Boswell, & Judge, 2001; Cannings & Montmarquette, 1991; Green, Jame, & Lock, 2019; Seibert, Crant, & Kraimer, 1999). In an early study of these dynamics, Howard and Bray (1988) follow managers from a specific firm (i.e., AT&T) and find that career ambition is among the highest explanatory variables in predicting career progress. Furthermore, relatively recent research has started to focus on the function of physical appearance in predicting the leadership position. By leveraging implicit leadership theories, numerous characteristics have been examined, such as weight (Roehling, Roehling, Vandlen, Blazek, & Guy, 2009), height (Lindqvist, 2012), hair color (Takeda, Helms, Klintworth, & Sompayrac, 2005), baby faceness (Livingston & Pearce, 2009), vocal pitch (Mayew, Parsons, & Venkatachalam, 2013; Nair, Haque, & Sauerwald, 2022), and look of competence (Graham, Harvey, & Puri, 2017). This research generally suggests that decisions regarding executive selection can be biased by extraneous considerations and even limit the candidates who are considered for such positions (Khurana, 2002).

Summary

The research on who is available to fill executive openings has offered critical insights into the role of information intermediaries and what is valued on the ELM. As interfirm executive mobility has increased substantially, research has offered a nuanced perspective of the role that ESFs and other intermediaries perform in helping firms determine who might be a viable candidate for open positions. Research also suggests that general managerial capabilities remain a critical determinant of who is perceived as viable for executive positions, while some specialized managerial capabilities can be valued on the ELM. A number of nonmanagerial characteristics have also been shown to have a significant impact on this labor market.

Who Signals Interest in the Executive Jobs?

An executive job represents a prestigious position with power and influence at a firm, and some have argued at a societal level as well (Mills, 1956; Useem, 1984). The attainment of executive positions and promotions is recognized as a particularly motivating force for most individuals (Holmström, 1982). This interest in executive positions is reflected in the research on executive career concerns (Miner & Crane, 1981) or the apprehension about the impact of current performance on current and future career outcomes (Gibbons & Murphy, 1992).

Several factors may determine whether an executive signals interest in an executive position. Consistent with employee mobility research, early research on executive mobility suggests that job satisfaction, compensation, and perceptions of organizational success reduce job search (Bretz, Boudreau, & Judge, 1994). While job satisfaction has been less of a focus for recent research given the need to collect primary data to assess it, more recent research underscores some factors that influence job satisfaction. For example, Aime, Hill, and Ridge (2020) find that executives who experience larger relative pay disparity in the previous positions subsequently join TMTs with less pay disparity. Similarly, in the context of the institutional transition within China, CEOs who are underpaid are more likely to voluntarily exit their firms (He, Shaw, & Fang, 2017).

Executives also may have geographic preferences that influence their likelihood of pursuing executive positions in other firms (Yonker, 2016). For example, Ma, Jing, and Stubben (2020) find that hired executives are more likely to be from local firms than nonlocal firms. The presence of noncompete clauses may also limit labor market opportunities and reduce interfirm mobility for executives (Aydinliyim, 2022; Garmaise, 2011). Beyond these considerations, executives often possess idiosyncratic preferences that influence whether an executive pursues certain labor market opportunities (Betzer, Lee, Limbach, & Salas, 2020; Schoar & Zuo, 2016).

Research on the ELM has offered critical insights into the challenges and opportunities that females and minorities face in pursuing executive positions (Fernandez-Mateo & Fernandez, 2016; Gupta, Mortal, Silveri, Sun, & Turban, 2018). For example, research suggests that female executives may experience different careers paths and unique challenges as compared with their male counterparts (Blair-Loy, 1999; Dencker, 2008; Eagly & Carli, 2007). Brands and Fernandez-Mateo (2017) find that gender differences in response to recruitment rejections contribute to women's underrepresentation in top management. Similarly, female managers are more likely to rely on formal processes for promotion, whereas men rely more on informal networks (Cannings & Montmarquette, 1991) or are more likely to use different tactics when negotiating for promotions (Bowles, Thomason, & Bear, 2019). Dreher et al. (2010) also find that ESFs are more likely to contact White male executives, and these individuals are more likely to reap the most benefit from opportunities in the external labor market. Gender difference may even start earlier, with childhood experiences potentially influencing gender disparity at the executive level (Fitzsimmons, Callan, & Paulsen, 2014).

Female and minority executives may experience obstacles, as suggested by research on the “glass ceiling” that leads them to be less likely to signify interest in executive positions (Becker-Blease, Elkinawy, & Stater, 2010). Smith et al. (2013) find that women have a significantly lower likelihood of getting promoted into a CEO position from a VP position than their male counterparts. Gayle et al. (2012) came to a similar conclusion finding that women's probability of attaining the CEO position was less than half that of male executives at the ages of 39 and 49. These results may at least partially explain the general pattern of female executives exhibiting much greater departure than male executives (Stroh, Brett, & Reilly, 1996).

Summary

In most cases, for an executive to be considered for a position, the individual must explicitly express interest. The determinants of who self-selects into consideration reflects a complex set of individual-level factors that reflect motivation for career success on the ELM as well as idiosyncratic considerations, such as locational preferences. While progress has been made for ensuring that executive openings are available to a wide group of potential candidates, female and minority executive candidates may still face systematic barriers that impede their advancement into these positions.

Who Gets Offered/Accepts the Executive Job, and What Is the Agreed-Upon Compensation?

Decisions makers on both sides of the ELM experience bounded rationality (Aguinis, Gomez-Mejia, Martin, & Joo, 2018; Hitt & Barr, 1989; Sebora & Kesner, 1996), influencing the aspirations, judgments, and justification of those involved in the selection process (Haleblian & Rajagopalan, 2006; Sebora & Kesner, 1996). Similar to the bounded rationality view of director selection decisions (Bazerman & Schoorman, 1983), executive search processes are incomplete, as such decisions are often limited and biased by existing executives’ social contacts. With these decisions, factors such as geographic preferences can influence decisions (Blair-Loy, 1999; Yonker, 2016).

From the firm perspective, a firm is likely to select an executive when the potential executive's resources match with the resources that firms are seeking, while weighing the potential benefits against the costs of appointing the executive. From the executive perspective, an individual will be willing to accept an executive position when the job resources offered by the firm match with those job resources that the individual desires. A potential executive will weigh the opportunity to develop transferable capital (e.g., learning, prestige, power, links to other social elite) and other personal benefits (e.g., remuneration) against the costs (e.g., time, resource commitments) that come with serving as an executive. In performing these considerations, the potential benefits and costs are weighted by the individuals’ personal preferences, and the overall decision is limited by their bounded rationality (Sebora & Kesner, 1996). For example, individuals later in their executive careers may weigh the benefits and costs differently than executives just beginning their careers (Gibbons & Murphy, 1992). For the early-career executive, perhaps the benefits of developing transferable managerial capabilities are weighted more heavily relative to the personal costs.

Research often turns to tournament theory to explain who is selected and accepts executive positions and what the agreed-upon compensation is for these positions (Eriksson, 1999; Main, Jackson, Pymm, & Wright, 2008). While it was originally developed to examine compensation schemes for optimum labor contracts (Lazear & Rosen, 1981), tournament theory has been applied in management to examine a variety of outcomes associated with relative “rank-order prizes” (for a review, see Connelly, Tihanyi, Crook, & Gangloff, 2014). From this perspective, individuals may be promoted to an executive position because of their ordinal ranking among the candidates rather than absolute performance-related factors (Cichello, Fee, Hadlock, & Sonti, 2009). This perspective offers critical insights into executive compensation and how those who win the “tournament” for the executive position are compensated (Messersmith, Guthrie, Ji, & Lee, 2011). The compensation gap between CEOs and other executives also offers insights into why individuals seek to ascend to the top of organizations (Ridge et al., 2014; Ridge et al., 2015). The tournament dynamics at the executive level may incentivize executives to engage in unethical behaviors given the competition to become the CEO (Shi, Connelly, & Sanders, 2016).

CEO Selection Decisions

Much of the ELM considerations on CEO selection have focused on the choice to select an inside versus outside successor (Berns & Klarner, 2017). The two major competing theoretical perspectives to explain this matter are the adaptive view and the inertial view (Cannella & Lubatkin, 1993). The adaptive view posits a positive relationship between poor performance and the selection of an outside successor because outsiders are expected to bring in fresh perspectives and be more willing to change the status quo relative to insiders (Friedman & Singh, 1989; Virany et al., 1992; Walsh & Seward, 1990). From this view, outside succession following poor performance may be more desirable to the board and other stakeholders because outside succession is more likely to lead to the requisite changes to improve performance. Conversely, the inertial view posits that because established organizations tend to resist change, they may be unlikely to select an outsider to replace the CEO, even when confronted with poor performance and other events (Goodstein & Boeker, 1991; Miller, 1991). Overall, competing forces are often at work within organizations that complicate the choice of successor (Cannella & Lubatkin, 1993; Ocasio, 1999; Ocasio & Kim, 1999).

Reflecting these competing forces, empirical work examining the effect of firm performance on the selection of an outside successor has been largely inconclusive (Finkelstein et al., 2009). Although some studies find a positive relationship between poor performance and outside succession (e.g., Datta & Guthrie, 1994; Schwartz & Menon, 1985), most find no support for the positive relationship (e.g., Dalton & Kesner, 1985; Friedman & Singh, 1989; Furtado & Karan, 1990). While some studies have argued that the selection of an outside successor may be a way to signal change to investors (Friedman & Singh, 1989; Worrell, Davidson, & Glascock, 1993), research finds that CEO succession announcements are often intentionally obscured by the simultaneous release of confounding information as a way to manage stakeholder impressions (Graffin, Carpenter, & Boivie, 2011).

While prior CEOs are potentially strong candidates for CEO positions on the ELM, their attachment to their prior employers limits their ability to obtain these new positions (Fee, Hadlock, & Pierce, 2018). Interfirm mobility also may have some negative implications, as executives who spent less time in a current organization take longer to obtain the CEO position (Hamori & Kakarika, 2009). For example, Koch, Forgues, and Monties (2017) find that executives obtaining CEO positions often experienced little interfirm or interindustry mobility, as they were more likely to follow traditional career paths with a steady progress of responsibilities and general management experience.

Beyond the CEO Appointment Context

When compared with the research on CEOs, researchers have paid less attention on trying to understand the labor market for top executives. One of few exceptions that has explored this question is Nielsen's (2009) study examining why TMTs look the way that they do, by considering previous team, organizational, and environmental factors that influence TMT composition. Similarly, corporate spinoffs represent an opportunity to examine TMT composition dynamics (Wruck & Wruck, 2002). In his assessment of opportunities to further upper echelons theory, Hambrick (2007: 338) explains, There is a need to turn upper echelons theory on its head by considering executive characteristics as consequences rather than as causes. Can we improve our predictions of who will win CEO succession contests? Why do top management teams look the way they do? What are the factors that cause the profiles of TMTs to change? By treating executive characteristics as dependent variables, we will not only open up new avenues for thinking about organizational adaptation and intraorganizational power struggles but will almost certainly gain insights that will eventually help sharpen our predictions of how and why executives’ characteristics become manifested in organizational outcomes.

Monetary Benefits

As executive compensation has increased over time, so has the debate for why executive pay continues to rise as well (Bebchuk & Fried, 2003; Murphy, 2013). One explanation for this is that shifts in the managerial labor market, such as higher executive mobility, may have led to the increase in managerial compensation (Carter, Franco, & Tuna, 2019). Research finds that losing executives may increase compensation for other executives who remain at the firm (Gao, Luo, & Tang, 2015). At the same time, managers with certain characteristics may be more valued on the ELM (Conyon et al., 2019). For example, Falato et al. (2015) find that pay premiums are provided to the most accomplished CEOs at the largest firms, suggesting a competitive sorting process on the ELM (Norburn, 1989; Pan, 2017). This sorting-out process may reflect industry-level and corporate tournament processes (Bognanno, 2001; Coles, Zhichuan, & Wang, 2018). Inefficiencies or frictions in the ELM that make managerial talent relatively scarce also partially explain the overall rise in executive compensation (Fahlenbrach, 2009). As competition for managerial talent increases, so does executive compensation as executives have greater bargaining power (Bolton, Mehran, & Shapiro, 2015; Dencker, 2009). Similarly, whether firms focus on the external ELM or only on their internal labor markets may influence executive compensation, as firms that consider the broader ELM will typically pay higher levels of compensation (Martijn Cremers & Grinstein, 2014).

More generally, though, the labor market dynamics greatly influence executive compensation (Acharya & Volpin, 2010; Fulmer, 2009). In particular, Fulmer (2009) finds that for CEO compensation, external market factors and individual characteristics that increase a CEO's marketability on the labor market increase CEO compensation. Similarly, research finds that CEOs who possess labor market opportunities often receive increases in compensation. For example, executives in metropolitan areas with greater job opportunities may receive higher compensation (Francis, Hasan, John, & Waisman, 2016). Research also suggests that exogenous changes in the market may increase compensation. Following staggered rejection of the inevitable disclosure doctrine by US courts, Na (2020) suggests that CEOs experienced an increase in external employment opportunities and, in turn, firms increased their compensation as an executive retention mechanism. As firms have shifted their compensation practices to focus on retention with the possibility of increased interfirm mobility (O’Byrne, 2014; O’Byrne & Gressle, 2013), the ELM provides insights beyond the traditional focus on the link between firm performance and CEO compensation. As Ezzamel and Watson (1998: 221) explain, in an informationally efficient executive labor market, it is unrealistic to expect changes in executive pay to be closely related to firm performance measures. This is because, irrespective of firm performance, for motivational, recruitment, and retention reasons, a firm's compensation committee has to ensure that its senior executives are paid at least the going rate, or the compensation level typically paid by similar firms.

These market dynamics also have a direct influence on compensation in public firms, as the usage of compensation consultants and relative performance compensation packages have become more institutionalized (Bizjak, Lemmon, & Nguyen, 2011). The use of consultants is to obtain information about the pay practices of peer firms (Murphy & Sandino, 2020), while the ELM is used as a means to select peer groups and set relative performance evaluation targets (Balsam, Fan, Mawani, & Zhang, 2022). Research suggests that peer firms may be chosen to purposefully increase executive compensation (Bizjak et al., 2011), and switching compensation consultants may be used to similarly increase executive compensation (Gao et al., 2015). As a result, ambiguity emerges regarding which firms should be used as peers for a particular firm, which can lead to these types of manipulations of the compensation consultant and peer firms (Cadman & Carter, 2014).

In terms of managerial capabilities, research finds that generalist executives with highly transferable managerial capabilities tend to receive higher pay on the ELM (Betzer et al., 2020; Brookman & Thistle, 2013; De Angelis & Grinstein, 2020). Similarly, prior CEO experience is found to lead to higher levels of initial compensation as a CEO (Bragaw & Misangyi, 2017). Executives who receive some form of certification, such as executive awards, board seats, and media attention, also may experience increases in compensation (Boivie et al., 2016; Kang & Kim, 2017; Malmendier & Tate, 2009; Wade, O'Reilly, & Pollock, 2006). Interestingly, research suggests that factors unrelated to managerial capability, such as CEO attractiveness, may influence executive compensation (Graham et al., 2017; Halford & Hsu, 2020; Lindqvist, 2012).

Overall, Devers et al. (2007: 1020) in their review of executive compensation suggest that “the extant literature is fairly silent on labor market influences.” The recognition of the role that the ELM performs in setting compensation is a critical insight, and research has suggested that prior work not considering the endogenous labor market process may be biased (Armstrong, Jagolinzer, & Larcker, 2010).

Other Benefits Derived From the ELM

Individuals often aspire to executive positions for the prestige (D’Aveni, 1990) and career outcomes (Brickley, Linck, & Coles, 1999; Cannella & Shen, 2001) that accompany them. Executives also benefit from the connection to other social elite who may provide future career advancement opportunities (Useem, 1984; Westphal & Stern, 2006, 2007). Previous research recognizes that executive mobility and promotions are primary means of rewarding executives who perform well in managerial positions (Fama, 1980; Gayle et al., 2015; Jensen & Zimmerman, 1985), where they gain further experience from their promotions and mobility (Broschak, 2021; Crossland et al., 2014). Finally, ELM considerations may drive executive perks. For example, CEOs may use perks to compensate for underpaid executives as they make the compensation more competitive (Adithipyangkul, Alon, & Zhang, 2011).

Summary

Beyond the broader considerations of internal versus external market dynamic, research has often not considered the overall market dynamics for CEOs and other executives, including supply-and-demand considerations influencing turnover and selection. Similarly, this work has not often considered the behavioral and psychological drivers of these market considerations from either the firm's or executive's perspective. As such, a more fully developed labor market perspective is needed to enrich executive turnover and selection research. For executive compensation and other benefits, the research examining ELM suggests that labor market dynamics provide critical insights into what has driven the increase in CEO compensation, how peer firms are selected in compensation decisions, and how the market generally rewards interfirm mobility while remaining at the same firm may provide some benefits. However, we still lack insight into how these factors affect non-CEO executives.

How Do Status and Social Capital Influence ELM Outcomes?

Much of the research on the ELM is predicated on the fact that executives can provide signals about their managerial capabilities, and they are motivated by reputational concerns on the ELM (Berck & Lipow, 2000). In describing the role of the ELM as a mechanism addressing agency concerns, Fama (1980: 292) suggests that “the previous associations of a manager with success and failure are information about his talents.” In this regard, being associated with a successful firm serves as a signal of managerial ability (Spence, 1973, 1974), affecting an executive's value on the ELM in the form of increased future compensation (Andreou, Louca, & Petrou, 2017) and future employment prospects (Casamatta & Guembel, 2010), including board seats (Brickley et al., 1999). Such an association with other successful firms carries status, and executives may provide prestige to hiring firms through their previous affiliation with successful firms (Chen, Hambrick, & Pollock, 2008). Executives with strong reputation and greater social capital should thus have more opportunities for intra- and interfirm mobility.

Research also considers the opportunity for prestigious board appointments as a key motivating factor for executives (Lorsch & MacIver, 1989; Mace, 1971; Zajac, 1988). In early research in this area, Mace (1971: 109) found that “directors accept board memberships, not for income, but for the opportunity to learn how other companies operate and for the prestige value derived from an identification with other impressive names.” From this perspective, executives seek board appointments to continually develop their own strategic expertise and garner prestige and social status. For executives, firm status and prestige may be particularly important in their decisions to serve on a board or not (Withers et al., 2012).

Positive and Negative Signals of Managerial Ability

Those CEOs whose firms have “enjoyed sustained levels of high performance” often obtain star status on the ELM (Graffin, Boivie, & Carpenter, 2013: 387), which affords them great visibility on the ELM (Asgari et al., 2021). Furthermore, Boivie et al. (2016) find that non-CEO executives have a higher likelihood of being promoted to CEO positions at outside firms when they attained either an inside or outside board position. They theorize that board membership helps executives build relationships with executives from other firms, increasing their social status and leading to new opportunities in the ELM. Conversely, executive dismissal serves as a strong signal regarding managerial ability and negatively influences managerial reputation. The general findings on the subsequent labor market outcomes suggest that dismissed CEOs are less valued and disadvantaged on the ELM (for a review, see Berns et al., 2021).

Different audiences may impose different reputational penalties, and these penalties for questionable behaviors are contingent on a number of factors. For example, Bednar et al. (2015) find that stock analysts and peer executives applied different penalties to executives adopting poison pills and that the relationship between the adoption and reputational penalties depended on media coverage of the adoption, prior performance, and extent to which the practice had already been adopted. Similarly, country-level differences may influence the efficiency of the ELM in rewarding high-reputation managers and punishing reputationally compromised mangers. Bloom, Genakos, Sadun, and Van Reenen (2012), for example, suggest that in the US ELM, which is relatively less regulated than other countries’ markets, is better able to remove managers associated with poor firm performance and reward those who are higher performing.

Firms with great reputations also may be able to more easily recruit and hire executives, and these executives may be willing to take less compensation, given the desire to be associated with high-status firms, which provide other career benefits (Focke, Maug, & Niessen-Ruenzi, 2017). In contrast, reputationally compromised firms may experience executive departures (Jiang et al., 2017) and challenges in attracting and hiring executives. For example, firms that disclose material internal control weakness, which is associated with an increase in the likelihood of material accounting misstatements, are less likely to appoint CEOs with higher managerial ability (Khurana & Kyung, 2021).

The Role of Social Capital

Executives’ social capital—reflecting the “assets embedded in relationships” (Shaw, Duffy, Johnson, & Lockhart, 2005: 594)—may signify their levels of access to new and nonredundant information and knowledge; therefore, it is likely to be highly valuable for employing firm (Wang, Gupta, & Grewal, 2017). For instance, incoming executives with high social capital may be able to more effectively bring implicit knowledge of the previous firm that they worked for, such as valuable customer or supplier relationships (Boeker, 1997). By securing executives with high social capital, firms have better access to critical external resources, such as communication channels to legal or political authorities, which can in turn confer status and signal legitimacy (Adler & Kwon, 2002; Davis, Yoo, & Baker, 2003). From this perspective, an individual's network of relationships represents a key resource for the actors, which may be valued by organizations but also may allow executives to maximize their employment opportunities by benefiting from the informational advantage leading to several labor market benefits (Engelberg, Gao, & Parsons, 2013; Liu, 2014).

Executives with greater social capital may have a stronger ability to engage in interfirm mobility (Jiang et al., 2017; Wiersema, Nishimura, & Suzuki, 2018). For instance, Jiang et al. (2017) observe that executives’ greater social capital helped them to exit failing firms while preserving their overall reputation. They find that executive departures were highest when executives had medium levels of social capital, suggesting that low social capital deterred executives’ ability to migrate to other firms while high social capital dissuaded them from leaving the focal firm, as they have the ability to minimize their stigmatization from the prospective failure of their firms (Wiesenfeld, Wurthmann, & Hambrick, 2008). Harrison, Boivie, and Withers (2022) find that non-CEO executives with ties to their home firms’ board members are more likely to experience interfirm mobility because of this social capital.

In high-friction labor markets, social capital may play an important role in obtaining information about CEO candidates. For example, on the ELM in India, for which class status is particularly salient, those individuals with higher social class proximity as reflected by caste and with religions similar to the owners and chairpersons of the hiring firms are more likely to receive CEO appointments, given the informational advantages that occur from the homophilic overlap (Damaraju & Makhija, 2018). Similarly, in institutional transitions, social capital derived from political capital may affect who receives benefits on the ELM (Conyon, He, & Zhou, 2015).

Summary

The ELM reflects reputational considerations for hiring firms and potential executives. On each side of the market, signals are provided to suggest the value that may arise when entering an employment relationship. These signaling dynamics may be more intense than other labor markets, given the social status that accompanies the appointment to an executive position at a corporation and the vetting process that can often accompany executive selection decisions on both sides of the decision (i.e., the hiring firm and the potential executive). As research continues within the broader area of the study of ELM, examining status, signaling, social capital, and other social dynamics will remain critical.

A Research Agenda for the ELM

While research on strategic leadership has continued to increase across different disciplines, research on this topic rarely considers broader issues of ELM dynamics in its theorizing or empirical modeling. To offer a more comprehensive framework for the study of the ELM and its implications for organizations, we have organized the literature around several research questions. Figure 1 provides an overview of several exemplar studies that specifically consider ELM dynamics and outcomes organized by the fundamental questions that we address in our review. From our review, we believe that several critical research opportunities exist to move the study of the ELM forward.

Executive Labor Market Framework

The Implications of Studying Gender and Minority Executive Experiences on the ELM

As we note in our review, the research broadly on gender and minority experiences on the ELM remains understudied, in part, because of data availability. However, such research has the potential to have an important societal impact regarding diversity, equity, and inclusion within the upper echelons of the organization. In particular, future research should continue to explore the unique dynamics that female and minority executives face in the upper echelons. Given that they are often in a minority position within their executive teams and on the broader ELM, female and minority executives may have different labor market experiences. Taking this line of inquiry further, future research is needed to understand how discrimination may operate within the ELM, particularly in regard to how the critical stakeholders react to the appointment of CEOs from underrepresented demographic groups (Jeong, Mooney, Zhang, & Quigley, 2022; Lee & James, 2007). An extensive body of research has supported the differences between female and male employees on dimensions such as diversity belief systems, experience in organizations, and expected roles (Eagly & Johnson, 1990; Hoffman, 1977; Homan, Greer, Jehn, & Koning, 2010). Our review suggests that focusing on other key factors that may influence career outcomes for female and minority executives may enrich our understanding of diversity within the upper echelons.

To this point, future research may examine how specific diversity-supporting actions by organizations (e.g., hiring diverse TMT or board members, distributing rewards among TMT members), market intermediaries, and other executives on the ELM can lead to more opportunities for female and minority executives to pursue executive positions and experience career advancement (Dwivedi, Gee, Withers, & Boivie, 2022). Relatedly, future research may expand earlier work on executive job attitudes (Finkelstein et al., 2009) to consider the difference between female and minority executives in terms of their unique experiences on the ELM, where executive job satisfaction critically influences several career outcomes, such as executive exit decisions from the ELM.

Research also may look to explore some of the related dynamics that occur within the boardroom and on the market for corporate directors in the context of ELM. For example, female and minority executives may experience a recategorization process in different ways on the ELM (Zhu, Shen, & Hillman, 2014). In the board context, Hillman (2015: 106) explains that because female directors typically are more educated, come from nonbusiness backgrounds, and are appointed to other boards more quickly, it may be “harder for them to be seen as ‘similar’ by their male director counter-parts.” However, female and minority executives who experience some recategorization on the ELM may be seen as more similar (rather than different), while this may reduce the likelihood that these individuals bring their unique perspectives to their hiring firms. Future research may look to the board literature on female and minority diversity to consider whether such dynamics are similar on the ELM.

Opportunities for Research Integration on the ELM

One of the broad challenges with research in the ELM is that, even though supply-and-demand considerations are essential components influencing a variety of outcomes, most studies typically focus on one side of the market at a time. Often this happens for reasons both theoretical and empirical. In the ELM, we often see only the outcome of market activities (e.g., we see who got promoted to a position), but we do not see the counterfactuals (e.g., the pool of people who applied or were considered for the promotion). Consequently, as our review around five fundamental questions suggests, this challenge contributes to fragmentation across subdomains, limiting the ways in which scholars consider the dynamic interplay among various factors in the ELM process. To enrich the ELM literature, it is thus critical for researchers to work toward synthesizing the literature and developing a more holistic perspective of ELM dynamics.

While there is no surefire way to bridge the gap between subdomains or to consider supply-and-demand elements simultaneously, introducing some recent work may help researchers on how to approach this task. For instance, Pan (2017) develops a model of executive-firm matching and finds that the assignment of managers to firms and the distribution of executive pay are endogenously determined in the ELM. In other words, higher marginal productivity is expected in specific matches between a firm and a manager due to their complementary attributes. As a result, firms with certain characteristics are able to attract executives who can provide the resources they need by offering higher pay. Another exemplar work is by Busenbark, Marshall, Miller, and Pfarrer (2019). In the context of collegiate sports, they show how internal and external stakeholders may react differently to violations by head coaches, affecting the head coaches’ chances of dismissal and their labor market prospects. They find that internal stakeholders tend to protect high-performing coaches when they are associated with negative social perceptions following violations, while the external stakeholders become more skeptical and distance themselves from hiring these coaches. Finally, ELM researchers may gain insights by referring to studies at the employee level. As one great example, Bidwell and Keller (2014) show how organizations balance their decisions to fill jobs between hiring and internal mobility depending on job characteristics. They find that firms are more likely to fill jobs from the external labor market rather than through internal mobility when the job has lower performance variability. Interestingly, this effect is weakened when there is a higher supply of internal candidates waiting for the promotion to the job. In other words, organizational selection decisions are influenced by not only the considerations on the best ex ante fit between the worker and job but also the size of the candidate supply pool.

Modeling a Counterfactual Slate of Candidates

Despite a significant amount of research on the ELM, we still know little about the pool of labor below the C-suite that is available to fill these positions. While previous research has studied the pathway that leads to an executive being promoted to CEO, substantially less research has explored how middle managers get promoted into upper management and how upper management ascends into the C-suite. One of the factors that likely drives the scarcity of this research is the difficulty of viewing the labor pool below the C-suite, as public firms are required to report only their top five highest-paid executives. This results in archival databases such as Execucomp, for which some biographical information and compensation of these executives are visible, and this readily available data have driven much of the empirical work in this area.

To gain a deeper understanding of who is available to fill executive jobs and who meets the skill requirements for such jobs, there may be several ways to build a counterfactual pool of candidates. For instance, researchers may leverage sociodemographic information of employees by getting access to the Federal Statistical Research Data Center governed by the US Census. Data sets such as the Decennial Census, American Community Survey, and Longitudinal Employer-Household Dynamics provide detailed information about employee demographics, education, income, occupation, and more (e.g., Bailey, Hoynes, Rossin-Slater, & Walker, 2020; Barth, Bryson, Davis, & Freeman, 2016). Another method for identifying a counterfactual slate of executive candidates would be to create a list of employees who are paid at a similar level (e.g., top 5% paid employees of each firm who are observed in the same industry and year) or hold similar positions (e.g., middle/high-level marketing managers among the S&P 1500). This list can then be refined by using network properties that point to logical nodes of candidates who are more likely to be considered. For example, researchers may consider only those employees who have a social tie with a focal firm, such as employees from current and former alliance partners, employees from firms where board members are affiliated, or employees who graduated from the same school as the executives in the focal firm.

Moreover, data regarding the broader pool of managerial talent is becoming more publicly available. For instance, researchers have been able to get access to data from prominent ESFs, and that has driven thought-provoking research on gender effects in the ELM (Brands & Fernandez-Mateo, 2017; Fernandez-Mateo, 2009; Fernandez-Mateo & Fernandez, 2016). Similarly, researchers may benefit from opportunities from publicly accessible labor market platforms (e.g., LinkedIn) where individuals post their names, career histories, and other information that is related to the ELM. Online labor market platforms have grown tremendously in size and influence such that executives are compelled to have a public account. Tools such as web scrapers may make it easier to study who the labor pool is below the C-suite so that we can more accurately measure their work histories and what it takes to ascend into the upper levels of public firms. Furthermore, since it is possible to view social connections on labor market platforms, building the narrowest counterfactuals who are considered for the future executive position is attainable. One research question that looks especially fruitful may be examining what factors lead firms to fill vacancies using external searches as opposed to internal labor markets, given that there is a high level of information asymmetry about external candidates relative to internal candidates (Bidwell, 2017).

Labor Market Intermediaries

The ELM is characterized by significant levels of information asymmetry between supply and demand–side actors. For firms, an executive hire can thus be considered an experience good, an asset whose quality can only be accurately measured once it has been purchased. We find that firms continue to allocate significant resources attempting to overcome this asymmetry by utilizing labor market intermediaries to help them identify high-quality executive candidates. The dynamics between ESFs and the ELM largely remain a black box within current ELM theorizing. For example, while firms are hiring ESFs to find high-quality candidates, it is not clear what evaluative assessments are used to develop this applicant pool nor what signals are utilized to investigate the executive labor supply. These insights would inform the research on executive appointments as well as the research on the consequences of executive career variety (Crossland et al., 2014; Mueller, Georgakakis, Greve, Peck, & Ruigrok, 2020; Semadeni et al., 2008).

More research is also needed to understand how ESFs control and shape the ELM. Qualitative research suggests that professionals in this space have successfully established legitimate jurisdiction on this domain by becoming the default normative option for the executive recruiting process and determining what constitutes an ideal executive candidate (Faulconbridge, Beaverstock, Hall, & Hewitson, 2009). As a result, current theorizing about executive mobility, recruitment, and hiring is largely underspecified. The field of ELM research would greatly benefit from future research that explicitly accounts for search firms, including questions about how the incentives for search firms may align or misalign with the incentives of the supply and demand–side actors. In addition, future research might seek to better understand the interorganizational dynamics between corporations and ESFs, similar to research on other professional advisory industries, such as law (Somaya, Williamson, & Lorinkova, 2008; Uzzi & Lancaster, 2004), accounting (Levinthal & Fichman, 1988; Seabright, Levinthal, & Fichman, 1992), and advertising (Broschak, 2004; Rogan, 2013).

Market Frictions