Abstract

While firms compensate executives in many ways, severance pay is perhaps the most controversial yet least understood form of executive compensation. In this study, we outline a review and agenda for severance pay owed if an executive is dismissed without cause from their role. Following changes to the disclosure of executive compensation in 2006, researchers have taken a renewed interest in studying executive severance pay. The current literature on this topic, however, has evolved along loosely connected research streams across multiple disciplines. This lack of integration presents a challenge for management scholars seeking to advance our knowledge of this important form of compensation. To address this issue, we provide an interdisciplinary review, incorporating recent studies that have taken advantage of the increased transparency of severance pay. Our review clarifies key differences between severance and other forms of executive pay and organizes prior studies along three main areas of research to draw conclusions about the current literature on this form of compensation. We also outline an agenda for future research, drawing upon several literatures that are key to management research—agency theory, managerial power theory, upper echelons theory, stakeholder theory, impression management theory, and the executive labor market. By integrating perspectives that, while less common in related fields, are central to management research, we provide unique insights for future research. Finally, we discuss key methodological issues, including data accuracy, measurement consistency, and analytical approaches, and how these can be addressed moving forward.

Executives exit their roles for a wide array of reasons, such as declining health, poor performance, retirement, or to take other jobs (Gentry, Harrison, Quigley, & Boivie, 2021; Klein, McSweeney, Devers, McNamara, & Blosser, 2017; Ridge, Hill, & Aime, 2014). These departing executives often take with them large payments, negotiated ex-ante, that are commonly referred to as severance pay. Severance is a unique form of executive compensation in that, although the payment terms are negotiated and confirmed ex-ante, severance is only paid to executives if they exit their roles (a list of common forms of executive compensation and their key features is presented in Table 1). While firms compensate executives in many ways (Devers, Cannella, Reilly, & Yoder, 2007; Finkelstein, Hambrick, & Cannella, 2009), severance pay is perhaps the most controversial yet least understood form of executive compensation (Cadman, Campbell, & Klasa, 2016; Cowen, King, & Marcel, 2016).

Common Components of Executive Compensation Packages

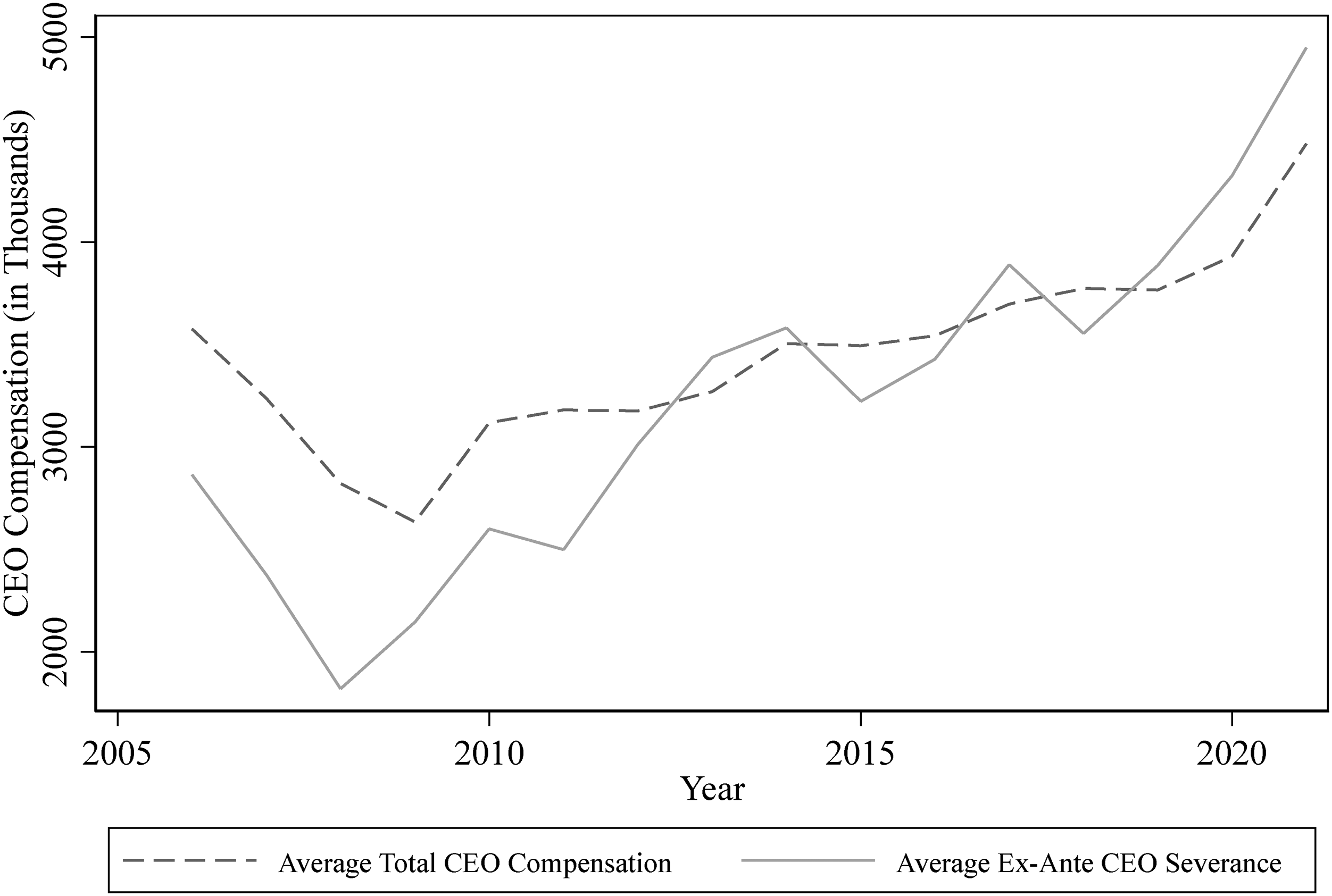

In this study, we focus on severance pay owed to executives if they are dismissed from their roles without legal cause, because of the controversy associated with these specific payouts (for ease of presentation we use the term “severance” to refer to pay owed to an executive in the event of a dismissal—that is not legally “for-cause”—for the remainder of the study). The terms of severance pay 1 have, for several decades, attracted considerable attention from stakeholders because such additional payments for dismissed executives seem to be the exact opposite of pay for performance (e.g., Bebchuk & Fried, 2006; Knight & Ward, 2022; Za, 2022). In response to such scrutiny, in 2006, the Securities and Exchange Commission (SEC) adopted new rules for the disclosure of executive compensation. These changes included mandates regarding the disclosure of severance agreements with executives. As shown in Figure 1, severance pay tied to “without cause” dismissal 2 has only grown in popularity, with the average ex-ante value of these agreements more than doubling since the rules were adopted.

The Growing Value Executive Severance Agreements

While linking severance payments to dismissal has remained controversial since the adoption of these amendments, scholars have also demonstrated that utilizing severance can provide potential advantages for firms. For instance, research has pointed to the role of severance in recruiting new executives and favorably influencing executive decision-making (e.g., Almazan & Suarez, 2003; Cowen et al., 2016; Klein, Chaigneau, & Devers, 2021; Rau & Xu, 2013). These contradicting views are consistent with a tension motivating much of the current discussion about severance, and highlight the need for additional studies on this increasingly important form of compensation. To date, however, management research on executive severance pay remains at a nascent stage of development. Our current understanding of compensation linked to dismissal relies heavily on studies outside the field of management. These studies have reached mixed conclusions and, aside from the perspective of agency theory, lack theoretical development. While these issues present considerable challenges, they also present abundant opportunities for management scholars to build upon existing findings.

Our study provides three primary contributions. First, we add clarity to the literature on executive severance pay. We do so by outlining key differences between severance pay and other types of executive compensation, as well as highlighting the importance of considering distinctions between severance pay linked to various executive exit scenarios. While studies have begun to advance our view of severance at a broad level (for a related review of severance payments triggered due to various forms of departures, see Klein et al., 2017), prior research has often lacked precision in discussions involving severance, a critical oversight since the exact terms of severance pay are contingent upon the mode of an executive's departure. This lack of precision is likely a factor in why the evolving research in this area has thus far often produced mixed or complicated conclusions. We believe that our work adds much needed clarity to these discussions and will ultimately play an important role in advancing our understanding of this form of executive compensation.

Second, we provide a focused and updated review of the literature on this form of compensation. We extend our current understanding of research on severance by engaging in a thorough discussion of the theoretical motivations underlying these studies, enabling a critique of their assumptions and conclusions. Furthermore, we incorporate recent findings from this rapidly evolving literature; over 75% of the papers in our review are additions to the book chapter by Klein et al. (2017), enabling us to extend and refine the review and model from their review. Our work synthesizes extant research streams to demonstrate the relevance of these findings to management studies and clarify the state of research on this form of compensation. This is an important contribution as we expect the rapid increase in research on severance to continue now that data on ex-ante executive severance pay agreements is publicly disclosed.

Finally, this study outlines a future research agenda for scholars interested in applying the conclusions we draw to novel research contexts in the field of management. Despite the increasing prevalence of severance, we have much to learn about pay to dismissed executives. The agenda outlined in this study extends prior research on this form of compensation by integrating this work into perspectives that, while less common in related fields, are central to management. This presents an opportunity for management researchers to build upon earlier studies and integrate central topics in management research with the literature on executive severance pay. We also introduce novel ideas from perspectives that have been previously linked to severance pay and expand on how researchers can enhance our understanding of severance, moving forward. To accomplish this, we next outline an introduction to severance pay before reviewing the extant literature and proceeding to our future research agenda.

An Introduction to Executive Severance Pay

Executive compensation agreements specify a variety of important terms, including the ex-ante severance arrangements for payouts that would be owed to an executive in the event of various departure scenarios. Given that executive departures are inherent to the payout terms of severance, these agreements have also been referred to as separation payments. Severance has also been discussed interchangeably with pay awarded in the event of a change in control of the firm, a form of pay commonly referred to as a “golden parachute.” Severance agreements, however, are only truly related to golden parachutes that are activated by a “double-trigger.” Unlike single-trigger golden parachutes, which vest immediately upon a change in control regardless of whether an executive is retained after an acquisition, double-trigger agreements are linked to severance payments because they are only activated if an executive is also dismissed after a change in control (Murphy & Jensen, 2018).

As noted earlier, the focus of this review is on severance pay due to a dismissal without legal cause. This form of severance pay is triggered if the classification for the executive departure is designated as “without cause” as opposed to instances where there is evidence of illegal or grossly negligent behavior (Cowen et al., 2016; Gentry et al., 2021). Thus, severance payouts are still owed to executives even when they are dismissed for poor performance. Due to the rarity of “for-cause” exits—Gentry et al. (2021) determine that this designation applies to less than three percent of CEO departures—most dismissed executives are owed severance payouts upon their departures (Album & Magas, 2020). Furthermore, Klein et al. (2017) found that while relatively few CEOs have contracts that specify payments in the event of for-cause terminations, most CEOs have severance agreements in place for dismissals occurring without legal cause. This is noteworthy given that the dismissals (and corresponding pay) we focus on in this review represent the third most common classification of executive departure (Gentry et al., 2021).

In 2006, the SEC altered the rules requiring the disclosure (SEC, 2006). These changes were intended to increase the transparency of reporting compensation arrangements for CEOs, boards of directors, and other top executives (SEC, 2006). Severance is further regulated by Section 280G of the Internal Revenue Code, which imposes an additional tax burden on both the company and the executive if payments to departing executives exceed 2.99 times the executive's annual salary. Despite these regulations, severance agreements and payouts remain both controversial and commonplace. 3 Researchers have consequently started to devote greater attention to this unique form of executive compensation. In the next section, we review the current literature on executive severance pay, aiming to integrate key insights from various fields and identify promising avenues for future research.

Literature Review: What We Know

Our method follows the recommendations for comprehensiveness outlined by Short (2009) and is modeled after recently published review papers in the Journal of Management. 4 As noted earlier, our work focuses on severance pay that is due to executives if they are dismissed from their roles. The review revealed that findings from the existing literature on executive severance pay are complex, offering mixed conclusions in some areas and leaving other areas considerably underexplored. Interestingly, within the past 10 years, over 70% (29 out of 40) of the empirical articles on executive severance pay use quantitative data. This current emphasis on quantitative analyses of severance pay likely results from the increased transparency of severance agreements after the passage of the SEC amendments in 2006. Indeed, it is evident from our review that the SEC's changes have enabled scholars to address a wider array of questions about executive severance pay, a trend we hope continues in the future.

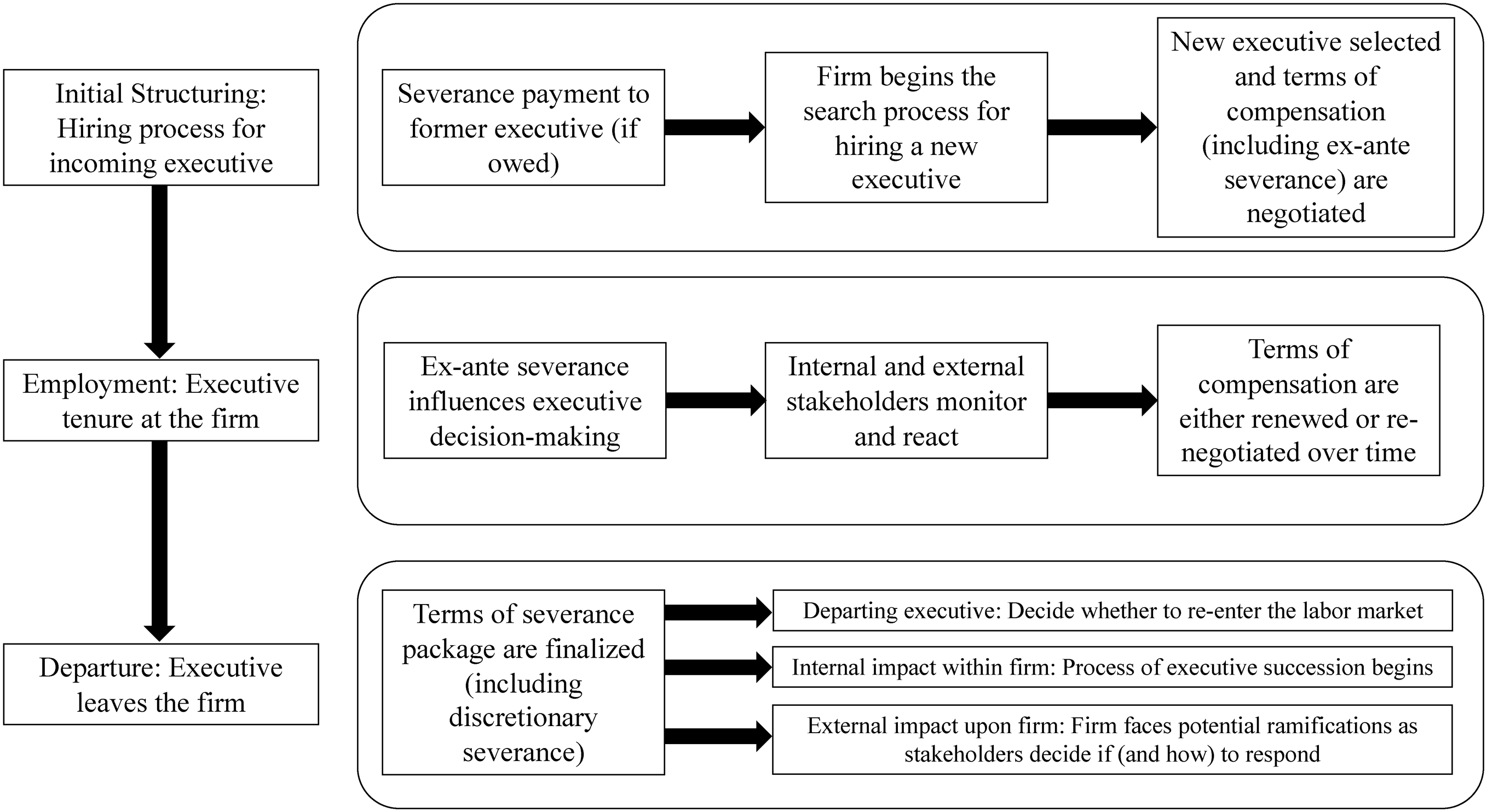

We use the model outlined in Figure 2 to guide our review and thus sort prior studies into three overarching categories: (1) Initial structuring: the antecedents, structure, and role of ex-ante severance in compensation; (2) Employment: the influence of ex-ante severance on decision-making and firm outcomes; and (3) Departure: the severance payout and ex-post consequences. While this model is an extension of the framework in Klein et al. (2017), we put forth two primary extensions to their model. First, we do not restrict the ex-ante influence of severance to incentive alignment (Stage 2 of our model). Additionally, we assert that the impact of severance payments extends well beyond facilitating firm exits and the immediate market reaction to the event (Stage 3 of our model) and may even have consequences beyond the focal firm. We also update their model to incorporate recent findings and extensions from studies in our review of the literature on executive severance pay. In sum, our work in Figure 2 extends and refines the review and model offered in their broader examination of various forms of severance.

Executive Severance Pay: A Brief Overview

Initial Structuring: Antecedents, Structure, and Role of Ex-Ante Severance Compensation

The first stage of our model considers the initial structuring of severance agreements. This area has produced a wide array of research into the antecedents to ex-ante severance and how the terms of these agreements should be structured. We begin our review with papers that discuss the role severance agreements can play in the recruitment and hiring of executives.

Based on this logic, scholars have suggested that severance agreements can be useful during the search for, and the recruitment of, incoming executives (Cowen et al., 2016). Empirical research into severance has confirmed that these agreements can counter the additional risk born by executives accepting roles in which they face a greater chance of dismissal or who would suffer greater costs should they be dismissed (Cadman et al., 2016; Gillan, Hartzell, & Parrino, 2009; He, 2012; Rau & Xu, 2013). For example, Klein et al. (2021) show that incoming female executives, who are perceived as more vulnerable than their male counterparts, are more likely to prioritize severance in their negotiation of the initial compensation contract. Chaigneau and Sahuguet (2018) build similar arguments, theorizing that severance agreements should be greater in firms with lesser blockholder ownership because the insurance executives associate with severance is more necessary. Severance agreements are also theorized to be most valuable for firms with greater opportunities to screen incoming executives because this enables firms to decrease information asymmetry when determining a candidate’s fit for the role (Van Wesep & Wang, 2014). Awarding severance agreements of greater value to incoming executives may indicate confidence in them, as firms may be willing to offer greater ex-ante terms of severance to those they view as less likely to ever receive the payment (Van Wesep, 2010).

The role of severance agreements in attracting candidates has likewise been confirmed by political science research, which has found that municipal city leaders are awarded greater severance agreements when they face greater political risk (i.e., when they accept a higher likelihood of losing their jobs) due to serving in a district with more competitive elections (Connolly, 2017) or a higher likelihood of holding recall elections (Compton, Gore, & Kulp, 2017). Severance agreements are especially impactful in assuaging incoming executives’ concerns when other contextual factors suggest an increased risk of future dismissals, such as when prior firm performance has been poor (Klein et al., 2021; Xu & Yang, 2016). From the perspective of stigma research, Wiesenfeld et al. (2008) theorize that executives at larger and more visible firms are also likely to secure greater severance agreements as these executives face a greater risk of stigmatization from dismissal.

Overall, there is robust evidence that executives prioritize ex-ante severance agreements when they face a greater potential for future dismissal or would suffer greater costs due to dismissal. The findings from prior research linked to this section of our model are perhaps the most consistent and straightforward. While the agency theory approach has produced convincing evidence that severance agreements are linked to risk and information asymmetry, less is known about when severance does not work in such recruitment efforts. As severance is a negotiation (Cowen et al., 2016), a better understanding of what causes severance to be ineffective in the recruitment process is desirable. For example, scholars could consider the factors linked to job offers being rebuffed despite including ex-ante severance agreements. We look forward to more research exploring related questions about the role of severance in the recruitment of executives, especially from perspectives outside of agency theory.

As we discuss further in our review of the second stage of Figure 2, studies have also focused on shareholder concerns about the initial structure of these ex-ante severance agreements after an executive's tenure is already underway (Ertimur, Ferri, & Oesch, 2013; Ertimur, Ferri, & Muslu, 2011; Ferri & Maber, 2013). Some of these concerns do not appear to be unique to the United States. Conyon, Core, and Guay (2011) adopt an agency theory lens to provide a rare look into severance policies outside the United States. Interestingly, they find that severance agreements are also used in the United Kingdom, noting that the terms of agreements in the British context seem to be as common and generous as they are in the United States. This study demonstrates that discussions about the value and terms of severance extend across international borders.

We encourage more work examining the terms of the clauses that are currently linked to severance (Cowen et al., 2016; Gillan & Nguyen, 2016) as well as a consideration of new clauses that could be adopted for future severance agreements. The lack of current research in this area is especially noteworthy given the widespread increase in the value of severance agreements. As discussed earlier, integrating new approaches into this research may prove helpful in examining this stage of our model. In addition to the theoretical perspectives discussed in our future research agenda, studies by legal scholars could help inform how management researchers should view the various clauses linked to severance agreements. Further attention to nuances in the structuring of these agreements will add important new insights into our understanding of the wider compensation packages awarded to incoming executives.

Employment: The Influence of Ex-Ante Severance on Decision-Making and Firm Outcomes

Previous research has sought to integrate ex-ante severance agreements into a discussion of whether severance can be a component in efficient contracting. Friebel and Raith (2004) point out that, unlike most other forms of compensation, increasing the value of ex-ante severance agreements does not raise the baseline annual total compensation that an executive takes home. They argue that increasing the value of severance agreements is consistent with efficient contracting because, hopefully, the executive will never be dismissed from their role. Others, however, have argued that ex-ante severance agreements are inconsistent with efficient contracting for firms. Ellingsen and Kristiansen (2022), for example, assert that the argument against severance pay as a component in efficient contracting is predicated on the ability of boards to avoid committing to ex-ante severance agreements. Instead of agreeing to severance payouts ex-ante, this model advises firms to rely exclusively on awarding discretionary bonus payments to executives if warranted at the time of dismissal. Anderson, Bustamante, Guibaud, and Zervos (2018) also argue against severance agreements as an efficient form of compensation. In their model, firms are always better off increasing the total compensation of the incumbent executive to spur growth.

A stream of research in the efficient contracting literature has focused more specifically on the tradeoff between severance agreements and alternative forms of compensation. This research has produced mixed findings. In support of severance agreements being consistent with efficient contracting, Cziraki and Groen-Xu (2020) claim that firms can offer severance to executives to secure other, more favorable terms of compensation because ex-ante severance is more valuable to a risk-averse employee than to a risk-neutral firm. Peters and Wagner (2014) confirm that the premium paid for an increased risk of dismissal is lower for executives who received additional compensation that was not tied to severance, consistent with their argument that severance agreements attenuate the need for an additional turnover risk premium.

In contrast, other studies have argued that there is not a tradeoff between severance agreements and other compensation. An empirical investigation by Carter, Franco, and Tuna (2019) found that severance agreements are an additional, rather than a substitute, form of protection for the dismissal risk borne by executives when switching firms. Rau and Xu (2013) similarly concluded that firms do not trade severance for other compensation benefits. Xu and Yang (2016) also found a correlation between severance agreements and signing bonuses for incoming executives. In a study of Canadian firms, Bodolica and Spraggon (2009) concluded that compensation protection devices, such as ex-ante severance provisions, are asymmetric with long-term incentive plans, but both can play important roles in protecting executives’ interests.

Many studies have explored how severance may be consistent with efficient contracting by focusing on the relationship between these agreements and executive risk-taking. These studies typically assert that ex-ante severance agreements can be consistent with efficient contracting by offsetting managerial risk aversion, as executives otherwise tend to be more risk-averse than shareholders would like due to the employment risk they face from the threat of dismissal (Eisenhardt, 1989). Scholars have used this logic to argue that severance agreements discourage firms from replacing executives with marginally better candidates, such that these agreements shape executives’ incentives (Berkovitch, Israel, & Spiegel, 2000). Ex-ante severance can, therefore, benefit both executives and shareholders by attenuating managerial risk aversion and curbing the impact of executive short-termism in decision-making (Almazan & Suarez, 2003). The reduction in agency costs that severance imposes has been theorized to combat excessive conservativism and encourage the exploration of innovative ideas (Laux, 2015). Ju, Leland, and Senbet (2014) argue that these properties of severance agreements make them analogous to put options in how they should be interpreted as mitigating executive risk aversion. Thus, many scholars have asserted that severance agreements are consistent with efficient contracting because they aim to incentivize executives to pursue risks that investors find desirable (Ju et al., 2014; Laux, 2012), and avoid shirking or strategies that deviate from desirable risks (He, 2012; Van Wesep & Wang, 2014).

This view has shown that severance agreements effectively mitigate executives’ risk aversion in a wide variety of contexts. Scholars have found a positive association between ex-ante severance and increased investments in various proxies for risk-taking, such as stock return volatility (Cadman et al., 2016), a decreased delay in the disclosure of bad news (Baginski, Campbell, Hinson, & Koo, 2018; Ling, 2012), and more efficient tax planning (Campbell, Guan, Li, & Zheng, 2020). Likewise, severance agreements can induce executives to invest in more research and development (R&D) expenditures by mitigating managerial career concerns (Chen, Cheng, Lo, & Wang, 2015; Lai, Li, & Yang, 2020). However, in a sample of European companies, Honoré, Munari, and de la Potterie (2015) do not find support for their prediction that limitations on severance agreements are negatively related to R&D spending. This finding highlights the importance of considering international contexts, a point we return to in our future research agenda.

Brown (2015) suggests that while executives may be tempted to engage in earnings management to increase the value of their ex-ante severance agreements, the potential cost of dismissal curbs such manipulation. Chen et al. (2015), who found that this effect is particularly pronounced for severance agreements of greater value or duration, affirm this conclusion. Studies have also identified other relevant contextual factors that can amplify the positive relationship between severance agreements and risk-taking, such as executives having a high-variable pay structure (Ling, 2012) or more promising career prospects outside of the firm (Akamah, Brockbank, & Shu, 2022).

An interesting outlier in the literature on how ex-ante severance shapes executive decision-making was conducted by Brown, Jha, and Pacharn (2015). These authors aimed to determine whether the risk-mitigation associated with severance agreements could over-incentivize executives to pursue risk-taking. Their study found that severance agreements lead to excessive risk-taking by executives, such that risk mitigation does indeed occur but in a way that is inconsistent with efficient contracting.

Consistent with the argument that severance must be structured appropriately to create joint value for executives and shareholders (Cowen et al., 2016), the various terms and components of severance agreements have also spurred research motivated to understand the efficiency of ex-ante severance. Severance pay primarily combines three components: cash compensation, equity awards, and benefits that extend past the departure date. Of these three, equity is theorized to be the only necessary component for efficient contracting (Ferreira, Ornelas, & Turner, 2015). Laux (2012) further argues that only equity can be included in an efficient severance contract because, unlike severance tied to cash or benefits, retaining equity upon dismissal links an executive's wealth to the firm's future performance. Focusing on how the terms of severance agreements are structured, Zhao (2013) found that accelerated vesting provisions for restricted stocks and options in severance agreements are associated with greater acquirer value creation from merger and acquisition (M&A) announcements. This is consistent with the theoretical argument that equity incentives linked to ex-ante severance can align the risk preferences of executives to encourage the pursuit of value-increasing risk.

As outlined above, studies have begun to develop our understanding of whether severance can be a component in an efficient compensation contract; however, the conclusions from this line of research are currently mixed. The current literature demonstrates that severance agreements are clearly effective at attenuating executive risk aversion; however, it is less evident that ex-ante severance agreements lead to desirable risk-taking. While research has shown that severance agreements generally mitigate risk aversion effectively, much less is known about the ex-ante influence of severance on executive decision-making beyond incentive alignment. This narrow focus has left us with an incomplete understanding of this stage in our model, an issue we return to in our future research agenda. Such complex findings suggest that further research is still needed to clarify when these agreements are consistent with efficient contracting.

Ferri and Maber (2013) similarly focus on how shareholder activists shape severance policies in the United Kingdom. Their work highlights a government-led initiative launched in 2003 that was overtly critical of severance agreements and produced the Rewards for Failure report. This report, coupled with shareholder demands for reform, prompted many firms in the United Kingdom to adjust their severance agreements (Ferri & Maber, 2013). Studies on shareholders and severance have, thus, presented evidence that shareholders in both the United States and the United Kingdom monitor and react to the terms of ex-ante severance agreements. However, research on severance has thus far devoted surprisingly little attention to the role of stakeholders other than shareholders.

Similarly, little attention has been paid to the final point in the employment stage of our model, which considers how ex-ante severance agreements evolve over time. Research has shown that the value of severance agreements tends to fluctuate along with changes to other forms of executive compensation (Gillan et al., 2009). This occurs because severance agreements are often structured to be partially based on other components of executives’ compensation packages. By separating new and incumbent executives, Rau and Xu (2013) uncovered important differences in how these two groups’ risk preferences motivate a divergence in their prioritization of ex-ante severance pay. Specifically, they found that incumbent executives who face a greater risk of dismissal are more likely to enter new or revised severance contracts. These findings confirm the need for additional research into the renegotiation and evolution of ex-ante severance agreements throughout executives’ tenure (Klein et al., 2017; 2021). An existing example of such research is provided by Cronqvist and Fahlenbrach (2013), who examined contractual changes to executive compensation in the context of firms’ transitions from public to private ownership. Consistent with the logic that private equity firms are owned by strong principals, they found that changes to severance pay agreements were negatively related to the strength of firm governance. These authors also note that changes to ex-ante severance contracts are stricter for the terms of unvested equity than changes to cash severance agreements.

Overall, studies linked to the employment stage of our model have demonstrated the importance of ex-ante severance agreements throughout an executive’s tenure. However, we have much to learn about when the terms of severance are actively supported by shareholders. Likewise, it is vital that future research expands beyond a focus on shareholders and develops research linking severance to a wider array of stakeholders, a point we return to in our research agenda. Concerns regarding the lack of research in this stage of the model parallel a critique by Cowen et al. (2016: 165), who suggested that “Future work could likewise benefit from more explicit treatment of external audiences’ reactions to severance.” Taken together, it is our hope that there will soon be greater development of the current conclusions drawn from this stage.

Departure: The Severance Payout and Subsequent Consequences

The final stage of Figure 2 focuses on the severance payment triggered by a departure event and extends to the ex-post consequences of these payouts. Early discussions of severance pay often criticized these payouts, arguing that they represented an extreme example of managers using their power to decouple executive compensation from performance and reduced the alignment of executive and shareholder interests (Bebchuk & Fried, 2003, 2006). Interestingly, papers corresponding to this stage of our model have drawn on a more diverse set of management perspectives to develop their theoretical arguments.

An alternate view holds that these agreements are consistent with efficient contracting because they increase the incentive for certain executives to exit firms. Inderst and Mueller (2010) propose that ex-ante severance incentivizes an expedited departure for executives who do not fit well in their roles. This may occur in part because ex-ante severance fosters more honest communication about the performance of the firm (Laux, 2008). Expanding on the risk-aversion logic discussed earlier, severance agreements have also been linked to an increase in executive turnover due to increased risk-taking (Mansi, Wald, & Zhang, 2016).

These contradictory findings suggest that more research into the link between the second stage of our model (Figure 2) and executive turnover is needed. While severance payments are inherently linked to executive exits, exploring heterogeneity in the causes of such departures may add new insights into this relationship. For example, it is possible that severance is more likely to facilitate entrenchment for executives with certain characteristics. Whether severance serves as an antecedent to dismissal may also be contingent on previously uncovered contextual factors. Given the costs firms face from replacing executives (Finkelstein et al., 2009), especially for cases in which severance payouts are due, future work should clarify this relationship.

Other studies on the payment of severance are more closely aligned with research examining the role of external stakeholders—the last point we identify in Figure 2. These studies on the final payout terms of severance are directly relevant to the stream of research focused on investigating the role that external stakeholders play in shaping ex-ante severance agreements. The agreement of special terms, such as bonus discretionary severance pay contingent upon the completion of a deal, was found by Jiang, Li, and Mei (2018) to cause increased targeting from shareholder activists concerned that such agreements indicate poor governance and executive rent extraction from investors. The odds of activist targeting in such cases increase by over 60% (Jiang et al., 2018). A study by Qiu, Trapkov, and Yakoub (2014) suggests that such agency concerns are warranted. They affirm that as firms near the completion of M&A deals, the executives at target firms may leverage severance agreements to negotiate more favorable severance payout terms. Viewed as a whole, these findings indicate that stakeholder activism aimed at challenging severance is not limited to ex-ante severance agreements but can also persist—and may well be warranted—for severance payouts.

A final set of papers on severance payouts seeks to understand the conditions under which dismissed individuals re-enter the executive labor market. In contrast to the studies which found that severance is consistent with efficient contracting, this set of studies also provides convincing evidence that many executives receive severance payouts beyond what firms are legally obligated to pay under the ex-ante terms of these agreements. In a sample of firms filing for bankruptcy, Eckbo, Thorburn, and Wang (2016) found that 28% of departing executives received a median total payment of $1.6 million in severance, with discretionary severance accounting for almost 25% of the total awarded. Fee and Hadlock (2004) provide insight into how receiving severance payments influences an executive's future career. In their sample, only 33% of dismissed executives who received severance payouts found comparable positions, providing clear evidence that the labor market considers the circumstances surrounding an executive's departure. These findings warn against assumptions that severance payouts reflect the ex-ante terms of these agreements and highlight the importance of considering perspectives beyond the efficient contracting perspective when researching executive severance pay.

While these studies have contributed to our knowledge of severance payouts, we assert that many unstudied ex-post consequences exist and that these outcomes are relevant to various key perspectives in management research. Indeed, we wish to highlight that there is currently a need for this literature to move beyond a focus on the antecedents of severance payouts and develop research on the consequences of these payouts. In fact, the review of exit payments by Klein et al. (2017) ends with investors’ reactions as the sole consequence identified after the payment of severance. The future research directions that Cowen et al. (2016) suggest likewise include insightful ideas that primarily focus on ex-ante severance agreements. Perhaps this is to be expected as severance is only invoked if an executive is no longer employed by the firm; however, the dearth of research on these ex-post ramifications renders our understanding of severance incomplete. It is critical that scholars further explore these moving forward.

Research Agenda for Executive Severance Pay

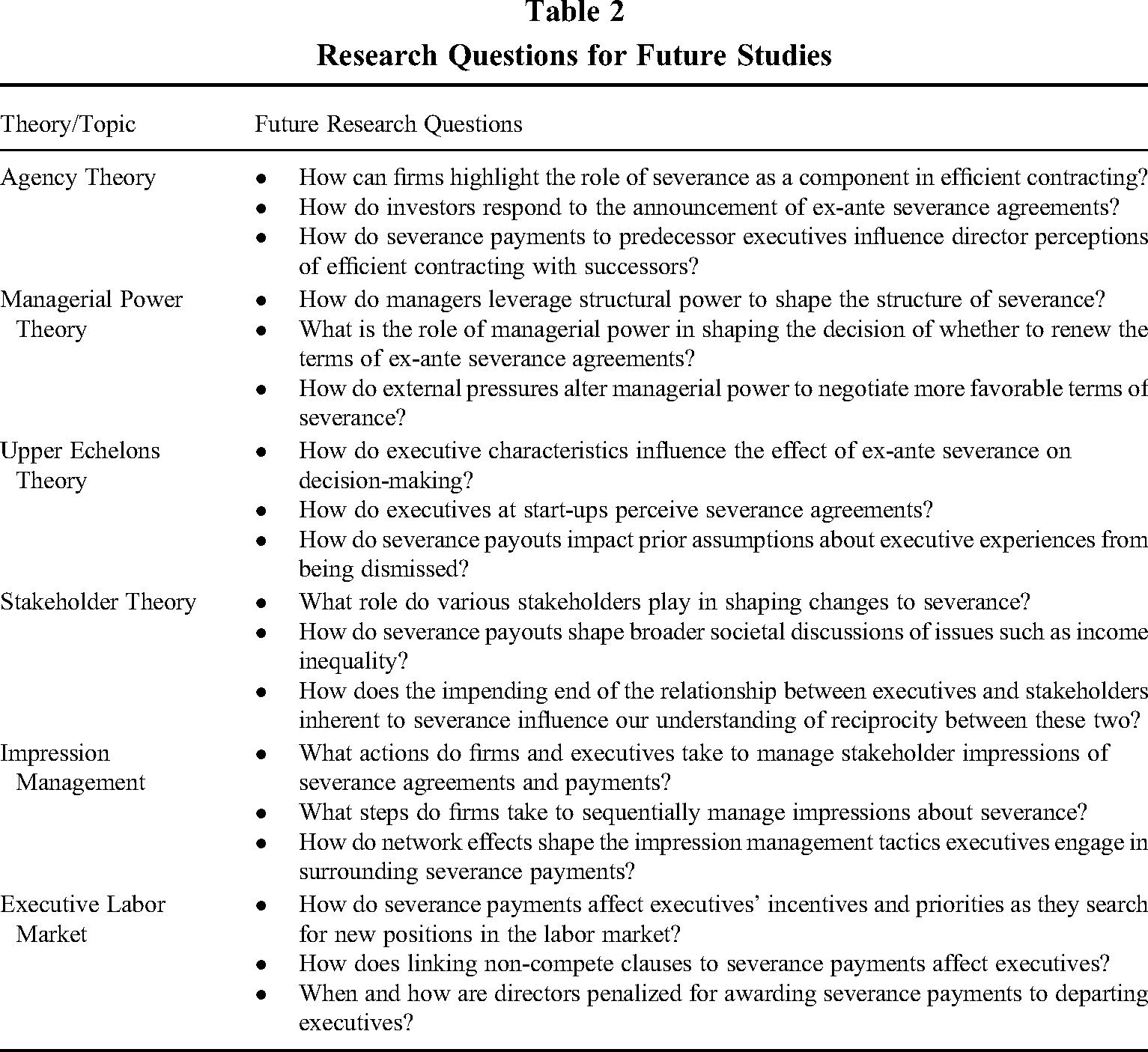

Our review demonstrates that research has widely established the importance of executive severance pay. As noted earlier, while the previous research in this area has produced complex and occasionally conflicting findings; this points to many opportunities for future research on this topic. Our agenda aims to develop such paths forward by integrating conclusions from our review with research opportunities for management scholars as well as developing nuances specific to the payout terms of severance that can be leveraged to advance research on the three stages of Figure 2. Much of the extant research involving executive severance pay draws upon agency theory; we begin with this topic due to severance's relevance to key questions from this theoretical perspective. We then progress to other theories and areas that are commonly the focus of management research. The potential future research questions we outline are summarized in Table 2. We end our agenda with critical observations of current empirical studies and advice on how to best address relevant issues in the future.

Research Questions for Future Studies

Theoretical and Phenomenological Extensions

Another research topic that warrants further attention is investors’ responses to the announcement of ex-ante severance agreements. Agency theory highlights the potential for goal incongruence between principals and agents such that executives may subordinate organizational interests to personal objectives (Fama, 1980; Jensen & Meckling, 1976). Research from the perspective of shareholder activism has demonstrated that investors often attempt to change the terms of ex-ante severance to account for this potential issue (Ertimur et al., 2013; Ferri & Maber, 2013). However, our review indicates that little empirical research into investors’ immediate reactions to the announcement of the terms of severance agreements exists. Studies aiming to assess investors’ perceptions of severance as a component of efficient contracting may even be more informative when focused on the ex-ante terms of severance (rather than severance payouts) because valuable ex-ante information about severance is typically already public when the final terms of severance payouts are announced. Additional research in this area will add to our understanding of investors’ perceptions of severance as a component of efficient contracting.

The board of directors sets top managers’ compensation and is empowered to replace executives (Hillman & Dalziel, 2003). As such, agency theory highlights directors’ duty to monitor and control executives on investors’ behalf. Given the controversial nature of severance, shareholders may perceive greater severance payments as failures on the part of directors. Despite this, our review suggests that there is ample room for advancing research on the role the board of directors plays in executive severance pay. This point is especially salient as it pertains to the departure stage of our model. For example, examining how severance payouts to departed predecessors influence the negotiation of severance agreements with successors could shed light on how directors approach efficient contracting with incoming executives. Additionally, examining whether directors are compelled to adjust their monitoring after awarding severance payouts can add to our understanding of the principal-agent relationship. While agency theory has, thus far, been the dominant theoretical lens for studies on severance, we believe that this perspective still presents exciting opportunities for future management research.

Managerial power theory focuses on the potential importance that structural positions held by executives play in influencing compensation agreements, as these positions facilitate entrenchment (Finkelstein, 1992). It has been argued that the power managers derive from such positions affects severance (Bebchuk & Fried, 2003), yet we know little about this connection. As such, further research into how executives leverage these positions could prove useful in resolving the discrepancy we uncovered in our review about whether the value of severance payouts is consistent with the total owed according to the terms of ex-ante severance agreements. A lack of alignment between ex-ante agreements and severance payouts could indeed arise if managers are able to leverage structural power to negotiate more favorable terms of departure. Interestingly, however, Goldman and Huang (2015) found that executive tenure is not associated with discretionary severance payouts in their sample of CEOs dismissed from firms. Further investigation into this topic can resolve such tensions and add to our understanding of the third stage of our model. The literature on executive severance pay would also benefit from research into how various manifestations of power (e.g., Boeker, 1992; Seo, Gamache, Devers, & Carpenter, 2015; Westphal & Zajac, 2001) may alter our understanding of how managerial power shapes severance pay.

Managerial power theory is also relevant to determining whether the terms of ex-ante severance are renegotiated over time (a key focus of the second stage in Figure 2). As noted by prior studies, many executives have their initial severance agreement continually renewed over time (Cowen et al., 2016). It is possible that this tendency to renew severance is the result of managerial influence over the board, as executives may prefer to keep the terms of their initial agreements rather than renegotiate with the board. However, this could also be the result of negligence. Directors have many obligations (Boivie, Bednar, Aguilera, & Andrus, 2016) and thus may opt not to prioritize the renegotiation of these ex-ante agreements. We believe that severance pay provides an interesting context for future research using this theory, given that the ex-ante terms of severance can be challenging to navigate from a social perspective. As Cowen et al. (2016) point out, understanding the social pressures surrounding severance negotiations is crucial to optimizing the efficiency of severance. Further exploring the reasoning behind this renewal will help determine whether this decision about compensation is linked to manager power or a lack of oversight from boards.

Determining how external pressures may alter managerial power to negotiate favorable terms of ex-ante severance is another promising area for future research. In addition to managerial power, executive compensation is also shaped by external forces such as industry membership and geographic location (Harris & Helfat, 1997). While various pressures have decreased the differences in severance agreements across firms (Cowen et al., 2016; Klein et al., 2017), variations in the exact terms of these agreements persist. It would thus be worthwhile for scholars to examine whether the terms of severance pay are better predicted by managerial power or external factors such as the industry or location in which a firm operates. For example, researchers could explore whether firms operating in certain industries are less likely to have severance agreements for their executives, or whether such factors influence the structure of these agreements (Cowen et al., 2016). As many forces may shape these agreements, it would also be useful to understand how external pressures and managerial power interact and jointly impact the terms of severance agreements.

Taken together, we believe that drawing on this theoretical perspective in the context of severance can add to our understanding of both executive severance pay and managerial power theory. The lack of studies currently drawing on this theory is especially surprising given the inherent contrast between the logic of efficient contracting and managerial power theory. We strongly encourage future research that draws on managerial power theory and other key management theories beyond agency theory.

An important research stream in upper echelons theory has focused on how an individual's background shapes their information-processing and strategic choices (Hambrick & Mason, 1984; Hambrick, 2007). Relatedly, much literature exists on the unique preferences of executives at entrepreneurial firms (e.g., Baron, 2007; Lee, Yoon, & Boivie, 2020; Wasserman, 2006). While many new ventures begin each year, few ultimately succeed and most fail within a few years (Cooper, Woo, & Dunkelberg, 1988); however, there is robust support for the notion that executives at these firms overestimate their likelihood of success (Koellinger, Minniti, & Schade, 2007; Lee, Hwang, & Chen, 2017). We believe that such biases are likely relevant to executive requests when negotiating the terms of severance agreements at start-ups. The lack of studies at the intersection of severance and entrepreneurship presents many exciting opportunities for future research. Data on severance agreements at private companies, while potentially difficult to obtain, could be captured through surveys or interviews. The insights resulting from such data could answer a host of crucial research questions. Research by entrepreneurship scholars into the severance agreements that executives sign would also advance our understanding of how this form of compensation evolves over time. Moving forward, we hope that scholars will explicitly focus on how severance agreements and payouts for executives at start-ups differ from those for other executives.

Severance may also provide new insights into how executives’ career experiences influence their decision-making following dismissal. For example, previous research has typically assumed that executives are negatively impacted by dismissal (Mehran, Nogler, & Schwartz, 1998; Ward, Sonnenfeld, & Kimberly, 1995; Wiesenfeld et al., 2008). Given the salience associated with dismissal, the logic of upper echelons theory suggests that the experience of being dismissed could affect an executive and their future decision-making. However, relaxing this assumption is critical in the context of severance because these payouts may alter how executives experience dismissal, with larger severance payouts likely offsetting some of the negative repercussions. Indeed, it is possible that the potential for behavioral changes stemming from a prior dismissal could be contingent on the terms of severance packages. We encourage researchers to employ the context of severance payments to advance our understanding of how managers in the upper echelons experience dismissal and how this may impact our assumptions about executives’ acceptance of roles at new organizations.

The actions taken by activist groups in attempts to influence company policy and practices are a core component of research on stakeholder management (Goranova & Ryan, 2014). Building on this, we believe that stakeholder activists’ role in compelling firms to enforce the terms of severance agreements is a critical area for future research, addressing the final stage of our model. In some cases, executives who depart due to indiscretions are still awarded portions of their severance payments (Cline, Walkling, & Yore, 2018). For example, when Steve Easterbrook was dismissed as the CEO of McDonald's, the board initially agreed to award him a severance payout and allow him to resign (as opposed to firing him for-cause), despite his departure resulting from allegations of having an inappropriate relationship with a subordinate. Eventually, however, Easterbrook was forced to return this payment due to a clawback clause in his compensation contract. Clawbacks and related holdback clauses legally compel dismissed executives to forfeit or return severance pay if evidence emerges that they engaged in inappropriate conduct while employed by the firm (Gillan & Nguyen, 2016). While activists were successful in forcing Easterbrook to repay (Channick, 2021; Gray, 2020), why such clauses might not be pursued remains an open question. Future research should explore the actions taken by activist stakeholders who target severance policies or payments.

Notably, key outcomes linked to severance may be contingent on media coverage. While media outlets primarily function as an information intermediary, they play an important role in mitigating the information asymmetry between firms and the public, and determining how issues are framed to key stakeholders (Graf-Vlachy, Oliver, Banfield, König, & Bundy, 2020). Despite the frequent media criticism of severance payouts (e.g., Brown & Farrell, 2021; Jenkins, 2018), there is ample room for integrating this “infomediary” into research on executive severance pay. For instance, perceptions of severance may be contingent upon stakeholder attention. As the media coverage of such agreements is often negative, greater media coverage of severance may be a liability; in the absence of negative coverage, however, this effect could be muted.

Our review also indicates that management research would benefit from a wider view of the distributional consequences from severance payouts. While severance terms may be viewed by some as rent-seeking by executives, we currently have little understanding of what determines when stakeholders view terms as excessive. This line of research can offer novel insights into the role severance plays in shaping broader outcomes, such as societal perceptions of income inequality or public debates over whether firm leaders are over-compensated relative to other workers. Relatedly, while prior research has generally focused on severance pay for firm leaders (Klein et al., 2017), future studies should consider how severance influences lower-level employees. Severance has often been linked to concerns about wealth transfer from shareholders, yet larger payouts may also impact employees. Such studies could provide valuable insights into the internal consequences of severance payouts, a topic that has thus far received minimal discussion from scholars. Research should consider how severance payouts to departing executives, as well as the consistency of severance policies across organizational levels, influence various employee- and firm-level outcomes.

Studying severance payments may also prove to be a useful context for stakeholder theory because these payments are tied to the conclusion of a relationship between a manager and stakeholders. This end of a relationship contrasts with the emphasis on norms inherent to the continued reciprocity between these parties, which characterizes stakeholder theory. While the interdependent nature of these relationships is key to understanding interactions between firm leaders and stakeholders (Shani & Westphal, 2016), these dynamics may be altered in the context of severance. We encourage researchers to consider relaxing assumptions about reciprocity in the context of severance payouts, given the impending end of the reciprocal relationship between executives and certain stakeholders, to add nuance to our understanding of their interactions.

Future work should examine the actions taken to manage impressions surrounding severance payments (corresponding to the third stage in our model), as well as the varying effectiveness of these tactics. For example, firms may engage in impression offsetting to mitigate external stakeholders’ potentially negative reactions (Gamache, McNamara, Graffin, Kiley, Haleblian, & Devers, 2019) before announcing the terms of severance payouts. Management research would also benefit from further exploration into whether severance payments prompt internal changes to the corporate governance of firms to manage stakeholders’ impressions of severance. While Bodolica and Spraggon (2009) argue that firms are cognizant of how implementing changes to severance can reduce stakeholders’ scrutiny, management research would benefit from more thoroughly outlining firms’ responses to such potential criticism.

Scholars could address calls from the impression management literature for more research into the sequential steps actors take to manage impressions (Bolino et al., 2008; Gamache et al., 2019) by focusing on the unique payout structure of severance, which lends itself well to this topic because announcements related to severance unfold over time. The points at which firm leaders might seek to engage in impression management tactics surrounding the release of severance information include, but are not necessarily limited to, the initial disclosure of ex-ante severance agreement terms, voting on proposals related to severance agreements at shareholder meetings, and the announcement of discretionary severance payouts. Therefore, this topic is relevant to every stage of our model. We encourage researchers to leverage the sequential timing of severance pay to track how actors utilize such tactics over time.

The context of severance is also promising for researchers seeking to understand the network effects of organizational impression management tactics. While the importance of network effects has been established for individuals who engage in impression management (Bolino, Long, & Turnley, 2016), our knowledge of how these tactics interact is limited because scholars have typically focused on how an organization's tactics affect focal firms. This is a potentially important oversight because firm leaders’ decision-making can be influenced by network effects (McDonald & Westphal, 2003). Future studies should consider the external effect that a focal firm's severance payouts may have on other firms’ leaders, such as prompting executives at peer firms to engage in impression management to mitigate any negative ripple effects of these payments on their own severance agreements. Individual executives are also likely to engage in tactics to mitigate external perceptions of certain connections following severance payments. In sum, there is substantial scope for future research to integrate impression management theory across several stages of executive severance pay.

Ex-ante severance agreements often contain various post-termination clauses. Non-compete clauses are especially relevant to the executive labor market literature and the dismissed executive in our model. These clauses prohibit an employee from competing with the firm either directly or indirectly for a specified period after their employment ends (Kini, Williams, & Yin, 2021). Previous research has shown that many severance agreements make payouts conditional on the departing executive signing a non-compete agreement (Cadman et al., 2016; Goldman & Huang, 2015; Zhao, 2013). These clauses have become commonplace because, without them, an executive can retain severance benefits while receiving income from a new role at a competing firm (Cowen et al., 2016). Studying how executives navigate clauses such as non-competes is critical to understanding their motivations in the labor market. Variations in the terms of severance agreements may also help clarify the conclusions from previous studies about whether severance increases the likelihood of an executive being dismissed.

A final topic we wish to call greater attention to is the potential repercussions for directors still serving on the board when firms award severance payouts. As noted earlier, the board of directors is empowered to determine top managers’ compensation and dismiss these executives. The absence of studies focusing on what happens to these directors following severance payments to dismissed executives is a notable omission, given the controversial nature of such payouts. Scholars could examine whether directors who award greater severance payouts to departing executives are punished in the executive labor market, such as through decreases in their compensation or the loss of their board seats. Ironically, however, directors who award more generous severance payments could also be more attractive candidates from the perspective of CEOs, as CEOs may desire to appoint directors who are more likely to provide generous terms of severance. Given the unique nature of severance, the impact of such payments on board decision-making and directorships in the executive labor market remains unclear. We await future research delving further into these apparent contradictions.

Sample and Methods

We identified several key points through our review of quantitative studies on executive severance pay that warrant further attention. First, we wish to highlight the potential difficulty in obtaining accurate severance data. Following the passage of the 2006 SEC amendments, ExecuComp began to provide ex-ante severance values for executives. Unfortunately, however, a recent study by Cadman et al. (2016) found only a 0.76 correlation between what ExecuComp reports for severance agreements and their manual coding of the “true value” for each executive. They suggest that this issue reflects errors made by ExecuComp in coding payments, such as conflating severance agreements with other potential exit scenarios. This discrepancy highlights the need to carefully consider the nuances of severance agreements and how these nuances may influence data accuracy when incorporating severance pay into quantitative analyses. Relatedly, it is critical that future researchers consider how the conclusions drawn from wider discussions of severance pay may be contingent upon the motivation driving executive turnover. While the focus of this study is on severance owed due to dismissal, executives exit their roles for a wide array of different reasons (Gentry et al., 2021). Research into such differences can help develop a more holistic view of how executives perceive severance, as well as parse out divergences between various forms of severance pay.

Another key question for future empirical research on severance is how best to capture the value of ex-ante severance agreements. One approach has been to capture the influence of severance agreements by using a ratio, typically relative to proxies for executive wealth such as total compensation (Eckbo et al., 2016; Qiu et al., 2014) or the market value of the firm equity shares that the executive holds (Cadman et al., 2016; Campbell et al., 2020). However, scholars have recently identified issues with the usage of ratios in statistical analyses (Certo, Busenbark, Kalm, & LePine, 2020). These authors find that utilizing ratios as variables of interest can reduce statistical power (Certo et al., 2020), posing a barrier to interpreting results. An alternative approach to proxying for severance agreements is taking the log of severance values (Klein et al., 2021). This method enables researchers to control for factors used as denominators in scaling, while avoiding the issues with ratio variables. Other studies have simply utilized the total value of severance agreements as reported by firms (Cronqvist & Fahlenbrach, 2013; Xu & Yang, 2016; Yermack, 2006). Regardless of the approach taken, we advise scholars to ensure the robustness of their findings when analyzing the influence of severance pay.

Scholars should also consider novel ways of capturing the influence of this form of compensation. As we noted in our review, severance payments worth over 2.99 times the recipient's annual salary and bonus result in extra tax penalties. Currently, this stipulation has led to the 2.99 multiplier serving as a cap for the ex-ante valuation of most severance agreements. We propose that agreements for more than this value could be fundamentally different and encourage researchers to explore these agreements, which we label “excessive severance.” Firms (executives) that offer (receive) excessive severance may be fundamentally different from their counterparts. Examining the circumstances surrounding these instances would be informative, especially if undertaken through the lens of stakeholder management theory.

In addition to these issues, two matters related to analytical approaches in studies that utilize data on ex-ante severance also merit further discussion. First, we wish to stress that the structure of these agreements often lends itself to substantial annual variations in the total amount of severance promised to executives. This may occur because executives exercise outstanding stock options that would have been accelerated if the cash component of ex-ante severance was linked to a bonus contingent upon performance. Given this issue, it is critical that researchers analyzing severance with panel datasets consider using a Hausman test (Hausman, 1978) to determine whether their models are best suited to either fixed or random effects. Future research on this topic could provide insights into how such changes during an executive's tenure impact their decision-making processes.

We also found that most empirical studies in our review rely upon annual panel data. We echo the call by other researchers (Cowen et al., 2016; Klein et al., 2017) to consider more diverse analytical techniques when designing studies that involve severance pay. For example, many questions related to more micro-level constructs could be addressed via experiments. Researchers could alter the value of severance payments to assess how these manipulations affect critical outcomes, including employee satisfaction, organizational identification, and organizational justice. Utilizing configurational models (Fiss, 2007) would allow researchers to take a more holistic view of how severance is structured relative to other components of compensation. Additionally, researchers could employ textual and sentiment analyses to answer questions related to how managers communicate with various stakeholders. As noted earlier, organizational leaders engage in impression management to influence the social perceptions of their firms. Understanding the messaging managers use to communicate about severance to various stakeholders, as well as how stakeholders respond, presents a fascinating opportunity for future research. The burgeoning literature on social media (Etter, Ravasi, & Colleoni, 2019) may also be a useful source of data for scholars aiming to advance our understanding of the responses to severance payments by various stakeholder groups.

Finally, as quantitative research on this topic continues to increase, international samples must be considered. Our review uncovered that there is scant discussion about how severance may differ in international contexts, although Bodolica and Spraggon (2009), Ferri and Maber (2013), and Conyon et al. (2011) provide notable exceptions. This is an important omission as the legislation governing severance disclosure and payment varies across countries. As noted earlier, Honoré et al. (2015) found divergent results when testing the relationship between severance agreements and R&D expenditures, highlighting the potential importance of such differences. We hope this distinction demonstrates the need to advance our knowledge of executive severance pay in settings outside of the United States.

Practical Implications

Our review of the research on executive severance pay suggests that this form of compensation can create value for firms through various avenues, such as aiding in the recruitment of talented candidates, exerting an influence on executive decision-making, or making it easier to remove an executive (Klein et al., 2017). However, there is also ample evidence that many stakeholders have concerns regarding severance. To address this divergence, firms must foster an environment in which compensation agreements for executives are thoroughly negotiated, transparently disclosed, and tailored to fit the firm's strategic goals. We also urge firms to regularly review severance agreements for all employees. This should be done specifically to ensure that ex-ante severance agreements are structured to create value for the firm (Cowen et al., 2016) and reduce any possible negative impact. We believe that this exercise will be beneficial for firms, regardless of whether it is a proactive or reactive action.

Additionally, during our review we found very few recent examples of executives discussing severance firsthand. An updated series of interviews, similar to an earlier set of special commentaries on severance published in 1993 (Guthman, 1993; Hansen, 1993; McDowell, 1993; Meehan, 1993), would be very useful given the changes in legislation about executive severance pay. We encourage sitting executives to openly discuss the role of severance and how they view it as a component of the overall compensation package. It would also be useful to hear more directly about dismissed executives’ own perceptions of severance. Due to how consequential severance pay is for executives, considering the effect of this form of executive compensation is critical for practitioners. Additional insights from executives would help researchers and policymakers to gain a more complete understanding of the role of severance pay and better inform future policy decisions, as the legislation governing executive severance pay, and executive compensation more broadly, continues to evolve.

Conclusion

Our interdisciplinary review integrates the extant research on executive severance pay to offer a holistic overview of the current state of research on this form of compensation. Expanding on the complicated findings in prior studies on severance, we outline how the current literature can inform future management research involving severance pay. Given the widespread interest in severance and the disclosure amendments adopted by the SEC, we believe that management research on severance pay is poised to expand in the coming years. We hope that our review makes research on executive severance more salient and accessible to management scholars and prompts future study of executive severance pay in an even wider range of contexts.

Supplemental Material

sj-docx-1-jom-10.1177_01492063231172181 - Supplemental material for Arranging Golden Goodbyes for Executive Exits: A Review and Agenda for Severance Pay

Supplemental material, sj-docx-1-jom-10.1177_01492063231172181 for Arranging Golden Goodbyes for Executive Exits: A Review and Agenda for Severance Pay by Conor Callahan in Journal of Management

Footnotes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.