Abstract

Using a sample of 22,442 firm-year observations for 3,721 U.S. listed firms, we show that family firms, on average, issue annual reports with higher readability than non-family firms. Higher readability could occur due to lower obfuscation or less information conveyance. By controlling complexity and choosing readability measures linked to obfuscation, we attribute the higher readability to lower obfuscation. Our investigation into the heterogeneity in family firms shows that the positive effect of family control on reporting readability exists for eponymous family firms but not for non-eponymous family firms. We also find that family firms managed by founders or heirs issue more readable 10-K reports than non-family firms, but family firms managed by outsiders do not exhibit such a difference. Cross-sectional analyses show that the difference in readability between family and non-family firms diminishes for firms with more earnings manipulation, weaker board governance, and dual-class shares. Further, we find that investors perceive family firms’ annual reports with higher readability to be more informative. Finally, we use state-level succession tax cuts as an exogenous shock to link the higher readability to family insiders’ incentives and preferences. Our findings are consistent with the view that family insiders’ incentive to maintain family reputation contributes to lower obfuscation in 10-K narrative disclosures.

Introduction

This study examines whether family firms’ annual report (10-K) readability differs from that of non-family firms. Family firms have a significant presence in the U.S. corporate landscape, constituting a third of the Standard & Poor’s 500 companies and more than 10% of the market capitalization of all listed firms (Ali et al., 2007; D. Wang, 2006). Several well-known and highly capitalized U.S. firms, such as Wal-Mart, GAP, CBS, Thomson Reuters, Marriott International, and Nordstrom, are family firms (Srinidhi et al., 2014).

The incentives for operating, strategic, and reporting decisions in family firms differ notably from those in non-family firms with diffused ownership. Prior studies show that family firms exhibit less separation between ownership and control than non-family firms (Demsetz & Lehn, 1985; Shleifer & Vishny, 1997), resulting in a greater alignment of interests and lower information asymmetry between investors and managers (i.e., lower Type 1 agency problem). However, family firms face an agency conflict between family insiders and non-family shareholders. 1 This inter-investor agency conflict, referred to as the Type 2 agency problem, is not typical in diffusely owned firms. Moreover, in a family firm, the controlling family is especially concerned about losing its socioemotional wealth (Gomez-Mejia, Cruz, & Imperatore, 2014; Prencipe et al., 2014). While the family insiders are keen to protect family influence and control from outside investors, they are also keen to protect their family reputation.

These distinguishing features have led several studies to investigate the differences in financial reporting quality and disclosure practices between family and non-family firms (Ali et al., 2007; Anderson et al., 2009; Chen et al., 2008; D. Wang, 2006). However, there is no consensus in the findings on whether family firms exhibit better or worse financial reporting quality, disclosure practices, or information environments than non-family firms. 2 The mixed evidence limits our ability to generalize prior results to other reporting attributes, such as textual quality.

We are interested in annual report readability for three reasons. First, textual narratives constitute 80% of annual reports (Lo et al., 2017). However, most current studies on family firms’ financial disclosures focus solely on the numerical component. Second, low 10-K readability could result from managers’ intentional obfuscation to hide unsavory information (F. Li, 2008; Lo et al., 2017). Textual obfuscation increases investors’ information extraction costs, reducing their likely negative responses to that information (Bloomfield, 2002). Under the obfuscation view, low readability is deliberate and meant to mislead investors, making it a matter of grave concern to investors and regulators. Third, despite regulators’ advocacy for “plain English” and simple disclosure (e.g., Cox, 2007; Securities & Exchange Commission [SEC], 1998), readability has been steadily decreasing in both the U.S. and other countries (e.g., Bonsall et al., 2017; Dyer et al., 2017; Lang & Stice-Lawrence, 2015).

Managers have vastly more discretion in obfuscating the narrative content of 10-Ks opportunistically than in managing the numerical values. They could write the report in a simple, precise, and understandable manner when conveying the news they want to communicate but write it in a confusing, ambiguous, and unintelligible way when they want to obfuscate unfavorable news that they are mandated to convey. Therefore, the preferences and incentives of managers are likely the main drivers of deliberate obfuscation leading to low readability of textual narratives. Given the different incentives and preferences facing the managers of family firms versus those of their non-family counterparts, we expect the readability of 10-K reports of family firms to differ from that of non-family firms. Ex-ante, the direction of this difference is not obvious. Family firms are less likely than non-family firms to obfuscate news because of a lower Type 1 agency problem and a higher incentive to protect family reputation. On the other hand, family firms face a more severe Type 2 agency problem and could use textual obfuscation to extract private control benefits. Therefore, it is an empirical question whether family firms have a higher or lower incentive to obfuscate 10-K reports.

Using an entropy-balanced sample of 22,442 10-K filings issued by 3,721 U.S. firms for fiscal years 2003–2013, we find that family firms produce 10-K reports that exhibit higher readability on average compared to 10-K reports issued by non-family firms. This result sustains after controlling for factors that reflect firms’ business complexity. Our main finding supports the view that family firms have lower agency conflicts and higher reputation concerns, both potentially contributing to more readable 10-K reports issued by family firms.

We seek to distinguish between the incentives due to agency conflicts and reputation concerns by considering the heterogeneity of family firms in two dimensions. First, we classify family firms into eponymous and non-eponymous (Minichilli et al., 2022). Agency theory does not predict any difference in the agency conflicts between eponymous and non-eponymous firms. However, socioemotional wealth theory predicts that eponymous family firms care more about the firm’s reputation than non-eponymous firms because the former carries the family name.

Second, we separate family firms into founder firms, heir firms, and outsider-managed firms according to whether a founder, an heir, or a hired outsider takes the position of the chief executive officer (CEO) or the chairperson of the board of directors (e.g., Villalonga & Amit, 2006). Under both the agency conflict argument and the reputation concern argument, we expect to observe a stronger effect on founder and heir firms than on outsider-managed firms. However, the different incentives between founders and heirs can help differentiate the two arguments. As founding family members, both founders and heirs care about family reputation. However, founders have stronger incentives to reduce agency conflicts than heirs because founders have significant undiversified investments of human capital in establishing the firm and sustaining it in its early stages. Under the agency theory explanation, we expect founder firms to exhibit a stronger effect than heir firms.

Our results show that eponymous family firms produce more readable 10-K reports than non-family firms, but there is no such difference for non-eponymous family firms. Further, founder and heir firms, but not outsider-managed firms, issue more readable 10-K reports than non-family firms. Among eponymous family firms, we observe that founder firms and heir firms issue more readable 10-K reports than outsider-managed firms, but there is no significant difference in 10-K readability between founder firms and heir firms. These findings are consistent with the reputation concern argument but inconsistent with the agency conflict argument.

To obtain a more comprehensive picture of the relationship between family control and 10-K readability, we identify three factors that may capture family insiders’ extraction of private control benefits. Our cross-sectional tests show that the positive association between family control and 10-K readability diminishes among firms with higher earnings management, weaker board governance, or dual-class share structures. These results suggest that the insiders’ tendency to exploit firm opacity and preserve family influence and control offsets the reputation effect of family control on improving 10-K readability.

We also examine the capital market effects of 10-K reports issued by family firms compared to that issued by non-family firms to separate the obfuscation view from the information conveyance view. Consistent with the obfuscation view, we show that family firms with higher 10-K readability experience a more significant stock market response and a greater increase in liquidity over the narrow window surrounding the 10-K filings than non-family firms or other family firms do.

To mitigate endogeneity concerns, we use state-level succession tax cuts to conduct a difference-in-difference-in-differences (DiDiD) analysis. The intergenerational control transfer is a crucial consideration for a family firm (e.g., Ellul et al., 2010; Kang & Kim, 2020; Tsoutsoura, 2015). A cut in succession taxes increases the net benefit of intergenerational control transfer for family firms but not for non-family firms. Thus, succession tax cuts widen the gaps in the reputation concerns and investment horizons between family and non-family firms. We find that the positive effect of family control on reporting readability becomes stronger for firms located in states that cut succession taxes than for other firms in the post-tax-cut period. These findings suggest that the distinct reputation concerns of family versus non-family firms constitute a determinant of readability.

We contribute to the literature in the following ways. First, we add to the debate on whether family firms provide better or poorer financial disclosure to investors than similar non-family firms. Prior studies, by and large, focus on numeric information in financial disclosures and document mixed evidence about how family control affects disclosure quality (Ali et al., 2007; Anderson et al., 2009; Chen et al., 2008; D. Wang, 2006). 3 These mixed results make it hard to infer how family control is associated with the readability of corporate narrative disclosures. We present clear evidence that family firms issue more readable 10-Ks.

Second, we identify family reputation as a driving force behind corporate disclosure practices by investigating the heterogeneity among family firms in eponymy and family influence. We show that the improving effect of family control on reporting readability is prevalent among eponymous family firms and family firms with a founder or heir serving as the CEO or chairperson. These findings support the argument that differences in the incentives and preferences of managers between family and non-family firms influence the relationship between family control and financial reporting readability.

Third, we demonstrate that ownership and control structures constitute essential determinants of disclosure readability. Prior studies are largely silent about the effect of a firm’s ownership structure on its readability. 4 Our paper is the first to show that disclosure readability can vary depending on family ownership and control, as well as related reputation concerns.

The remainder of our paper proceeds as follows. We develop our hypothesis in the next section. The third section presents our sample selection procedure, defines key variables, and specifies empirical models. The fourth section discusses our empirical results. The fifth section concludes the paper.

Literature and Hypotheses

Theoretical Frameworks for Family Firms

Extensive literature has examined the effect of family control within U.S. corporations. In their paper on the survey of corporate governance, Shleifer and Vishny (1997) argue that family ownership substitutes for board-based and other governance procedures through a greater alignment of managers’ and investors’ interests. Early studies on family firms in the finance literature show that family firms have a better return on assets and Tobin’s Q (Anderson & Reeb, 2003) and a lower cost of debt (Anderson et al., 2003). These studies attribute the better performance and lower risk in family-owned firms to less severe agency problems caused by the separation of ownership and control. However, these early studies also identify the Type 2 agency conflict—the entrenchment of insiders whose interests may differ from those of outside investors—as a potential adverse effect of family ownership.

While agency theory focuses on the economic benefits of family owners and managers, recent literature on family firms highlights the socioemotional wealth theory (Gomez-Mejia, Cruz, & Imperatore, 2014; Prencipe et al., 2014). This theory posits that owners and managers of family firms perceive the loss of socioemotional wealth as more salient than business risk. To safeguard socioemotional wealth, family insiders are protective of the firm reputation, which reflects the external image of the family. However, they are also reluctant to lose the influence and control over the firm to outside parties and may take actions to preserve family influence and control at the expense of financial outcomes. Gomez-Mejia, Campbell, et al. (2014) show that family firms are still likely to invest less in R&D than non-family firms, even in the high-technology industry, where such underinvestment in R&D could significantly increase business risk. The authors attribute the hesitation to invest in R&D among family firms to family owners’ aversion to loss of control rather than to business risk.

The traditional agency theory and the socioemotional wealth theory focus on different aspects of outcomes of corporate actions and make different assumptions about corporate managers’ utility functions. We do not distinguish between these two frameworks when developing our main hypothesis below.

Family Firm Studies in Accounting

Several accounting studies on family firms examine the effect of family control on information environments in the U.S. setting. Ali et al. (2007) and D. Wang (2006) find that family firms exhibit higher financial reporting quality. 5 Srinidhi et al. (2014) show that family firms with good governance choose higher-quality auditors, implying that these firms encourage greater transparency than similarly placed non-family firms. 6 Besides, Chen et al. (2010) find that family firms are less tax-aggressive and more transparent than non-family firms. Ali et al. (2007) show that family firms issue more management earnings forecasts than non-family firms.

In contrast, Chen et al. (2008) find that family firms, on average, are less likely to issue management earnings forecasts, although more likely to issue earnings warnings, which are bad news earnings forecasts of very short horizons. Using a sample of pharmaceutical firms, Jayamohan et al. (2017) show that family firms tend to attribute poor firm performance to external factors in their 10-K reports compared with non-family firms. Finally, Anderson et al. (2009) look at market-based measures of firm opacity without focusing on an individual disclosure outlet. They provide systematic evidence that family firms are more informationally opaque than non-family firms.

The findings in the literature do not present a clear consensus on whether family firms have a better or poorer information environment. In addition, research comparing family and non-family firms has focused almost exclusively on numeric information rather than textual disclosures. The study by Jayamohan et al. (2017) is an exception, but it focuses on the pharmaceutical industry over a two-year period.

Readability of Financial Disclosures

Bloomfield (2002) suggests that managers could strategically obfuscate the text to withhold negative news from investors. Consistent with this argument, F. Li (2008) shows that firms with lower current earnings and transient profits or persistent losses produce less readable 10-K reports. Y. Li and Zhang (2015) show that poorly performing firms issue less readable 10-K reports when facing greater short-selling pressure. Lo et al. (2017) find that firms with higher levels of earnings management also have lower readability scores, further supporting the obfuscation explanation. Given that prior studies consistently find prominent adverse market implications of lower readability of financial documents (C. F. Kim et al., 2019; Lawrence, 2013; Lee, 2012; Lehavy et al., 2011; B. P. Miller, 2010; You & Zhang, 2009), understanding the determinants of readability is an important area for investigation.

Hypothesis Development

A family firm experiences less agency conflict between its owners and managers, often because the senior managers are also family members (Srinidhi et al., 2014). The alignment of interests between owners and managers reduces moral hazard and improves the incentive for managerial effort. In addition, the family owners and managers are more familiar with the firm’s operations and the environment because they have been involved with the firm on a long-term basis, often since founding the firm. Their firm-specific operational and environmental knowledge reduces information asymmetry between managers and investors and limits the opportunity for managers’ self-serving actions. As a result, the managers in a family firm (both the family managers and professional managers who are answerable to the family insiders) have less incentive and opportunity to obfuscate the text to mask the true performance of the firm.

Moreover, family owners and managers view the reputation of the firm as their family reputation. A reputation loss to the firm is perceived as damage to the family’s reputation, a consequence that is often more salient than a temporary financial loss. Therefore, family firm managers are more likely than non-family firm managers to avoid getting a bad reputation for obfuscating news in narrative disclosure, even in the face of a temporary financial setback. These arguments suggest that family firms have less obfuscation, resulting in higher readability of their 10-K reports than those filed by non-family firms.

A counterargument is that family insiders prioritize maximizing the family value over the firm value. As a result, they might take actions that reduce the firm’s value but increase the family’s shares disproportionately. As insiders, they have the ability and incentive to take these actions. Leuz et al. (2003) show that insiders can use their accounting discretion to conceal their private control benefits from outsiders. Further, the entrenchment of family insiders shields them from the disciplining effect of outside investors’ takeover threats. 7 Family insiders are also averse to losing authority, power, or control over the firm because such a loss hurts their socioemotional wealth besides the financial benefits of control. For example, family insiders could forego investment projects with a positive net present value because such projects require capital infusion that dilutes the family’s control over the firm. These arguments suggest that, compared with non-family firms, family firms could resort to obfuscating textual disclosure to hide the expropriation activity and preserve family influence and control.

The readability difference between family and non-family firms could be confounded if the two have varying degrees of business or financial complexity. If family and non-family firms differ only in intrinsic business or financial complexity, we should not observe a difference in reporting readability after controlling for the intrinsic complexity.

The takeaway from the above discussions is that the issue of whether (and how) family firms differ in financial reporting readability compared with non-family firms is an empirical question. We thus state our hypothesis in the null form.

Research Methods

Measuring Family Control

In this paper, we classify a firm as a family firm in a particular year if it satisfies the following two criteria: (i) the family members, defined as the founder(s) or their descendants within two generations, have at least 20% voting rights; and (ii) at least one family member serves on the board. Our definition of family firms imposes significant threshold restrictions on voting rights held by family members and is more stringent than that of several prior studies on family firms’ earnings quality or disclosure choices (e.g., Ali et al., 2007; Chen et al., 2008; D. Wang, 2006). Our definition ensures that family members retain significant influence over the company (e.g., Barontini & Caprio, 2006; Barth et al., 2005; Srinidhi et al., 2014). 8

Measuring the Readability of 10-K Reports

A challenge to empirically studying management obfuscation in 10-K reports is that low readability could indicate information conveyance rather than obfuscation. Accounting standards require nuanced and finer reporting when dealing with complex operations. Bushee et al. (2018) show that the conveyance of such nuanced information through financial reports can result in low readability. To address this challenge, we identify simplicity and specificity as two aspects of readability and carefully select a set of empirical measures of readability that are mapped more to obfuscation than to information conveyance.

Our first measure is the Bog Index (BOG), a plain English-based measure that summarizes all the attributes listed by the SEC’s plain English advocate (Bonsall et al., 2017). The Bog Index has three components, computed as follows:

where Sentence Bog focuses on the average sentence length of a document; Word Bog identifies readability issues with word usage, exemplified by passive verbs, hidden verbs, legal terms, wordy phrases, overwriting, and clichés; and Pep accounts for good writing attributes such as names, interesting words, and sentence length variety. While the first two components of the Bog Index are related to the simplicity aspect of readability, the final component incorporates the specificity aspect. A higher value of the Bog Index suggests that the document is less readable. For expressional ease, we define the variable BOG as the negative value of the Bog Index.

Our second measure is the modified Fog Index (MODFOG). The Fog Index combines sentence length and the use of complex words, calculated as follows:

where complex words are words with three or more syllables. Higher values of the Fog Index indicate that the text is more difficult to understand. To address the misspecification issue stemming from the definition of complex words, C. F. Kim et al. (2019) adapt the Fog Index to the financial context by reclassifying a list of multi-syllable words as simple words. The modified Fog Index focuses on the simplicity aspect of readability. For ease of interpretation, MODFOG is the negative value of the modified Fog Index.

Our third measure is the proportion of numbers used in the narrative disclosure in a 10-K report (PCTNUM) (Campbell et al., 2021; Lundholm et al., 2014). Consistent with Lundholm et al. (2014), we count the number of substrings with numeric characters, excluding those denoting a year or a date. A higher value of PCTNUM suggests that the text is more specific and thus easier to digest. We multiply this measure by 1,000 for expressional convenience.

Our three measures of readability can be empirically or conceptually mapped to management obfuscation rather than information conveyance. Prior studies have conducted validity tests to show that the Bog Index and the modified Fog Index of 10-K reports are negatively related to firms’ information environments (Bonsall et al., 2017; C. F. Kim et al., 2019). In addition, the proportion of numbers is a relative measure that already controls, in its denominator, the effect of the total amount of information conveyed by managers. Firms may try to be more informative, but if they intend to facilitate investors’ understanding of the information, they can be more specific by using more numbers instead of writing long paragraphs without including any numbers. In this sense, a smaller proportion of numbers indicates management obfuscation rather than information conveyance. 9

In addition to separately using the above three readability measures, we construct a composite readability score. Consistent with De Franco et al. (2015), we compute percentile ranks of each measure and take the average rank as an aggregated readability measure (READ).

Empirical Model

To test our hypothesis, we estimate a regression of readability on family control as well as the known determinants of readability (F. Li, 2008; Lo et al., 2017):

In Equation 3, Readability represents one of our readability measures: BOG, MODFOG, PCTNUM, and READ. Our key variable, FAMILY, is a dummy variable that indicates the existence of family control as defined above. F. Li (2008) finds that firms with poor current earnings performance tend to issue difficult-to-read 10-K reports, and we thus expect a positive coefficient of EARN. Besides, we control for firm size (SIZE), market-to-book (MTB), firm age (AGE), special items (SI), earnings volatility (EARN_VOL), returns volatility (RET_VOL), business complexity (NBSEG and NGSEG), financial complexity (NITEM), unusual events (SEO and MA), and Delaware incorporation (DLW). We also control for earnings management, proxied by firms’ behavior of meeting or just beating earnings targets (MBE), to ensure that any result for readability in our paper is not simply a manifestation of earnings management. Finally, we include year dummies (δt) and industry dummies (φi) in all regressions to control for time trends and industry heterogeneity, respectively, of financial reporting readability. 10

Data Sources and Sample Selection

We download the Bog Index data from Professor Brian Miller’s webpage. 11 To construct the modified Fog Index and the proportion of numbers, we acquire 10-K filings from the SEC online EDGAR system and parse the filings following the procedure presented in the online appendix of C. F. Kim et al. (2019). Besides, we obtain family control and board characteristics data from GMI Ratings (formerly Corporate Library); equity offerings data from the SDC Global New Issues database; mergers and acquisition data from the SDC Platinum M&A database; stock returns data from CRSP; and financial data from Compustat.

Our initial sample includes all observations with information on family control from GMI Ratings for 2004–2014. We choose this period because GMI Ratings started providing information on family control in 2004, and our version has complete data up to 2014. As the year variable in GMI Ratings indicates the year of proxy statements, our sample covers the fiscal years 2003–2013. 12 The final sample for our main tests consists of 22,442 firm-year observations for 3,721 firms. See Appendix B for our sample selection procedure.

Entropy Balancing

To mitigate the potential confounding caused by the differences in firm characteristics, especially business complexity, between family and non-family firms, we use an entropy balancing technique, which has recently gained popularity in accounting literature (e.g., Chapman et al., 2019; Gallemore et al., 2019; McMullin & Schonberger, 2020). Entropy balancing is a quasi-matching approach that assigns a weight to each observation to balance the treatment and control sample distribution properties.

Results

Descriptive Statistics

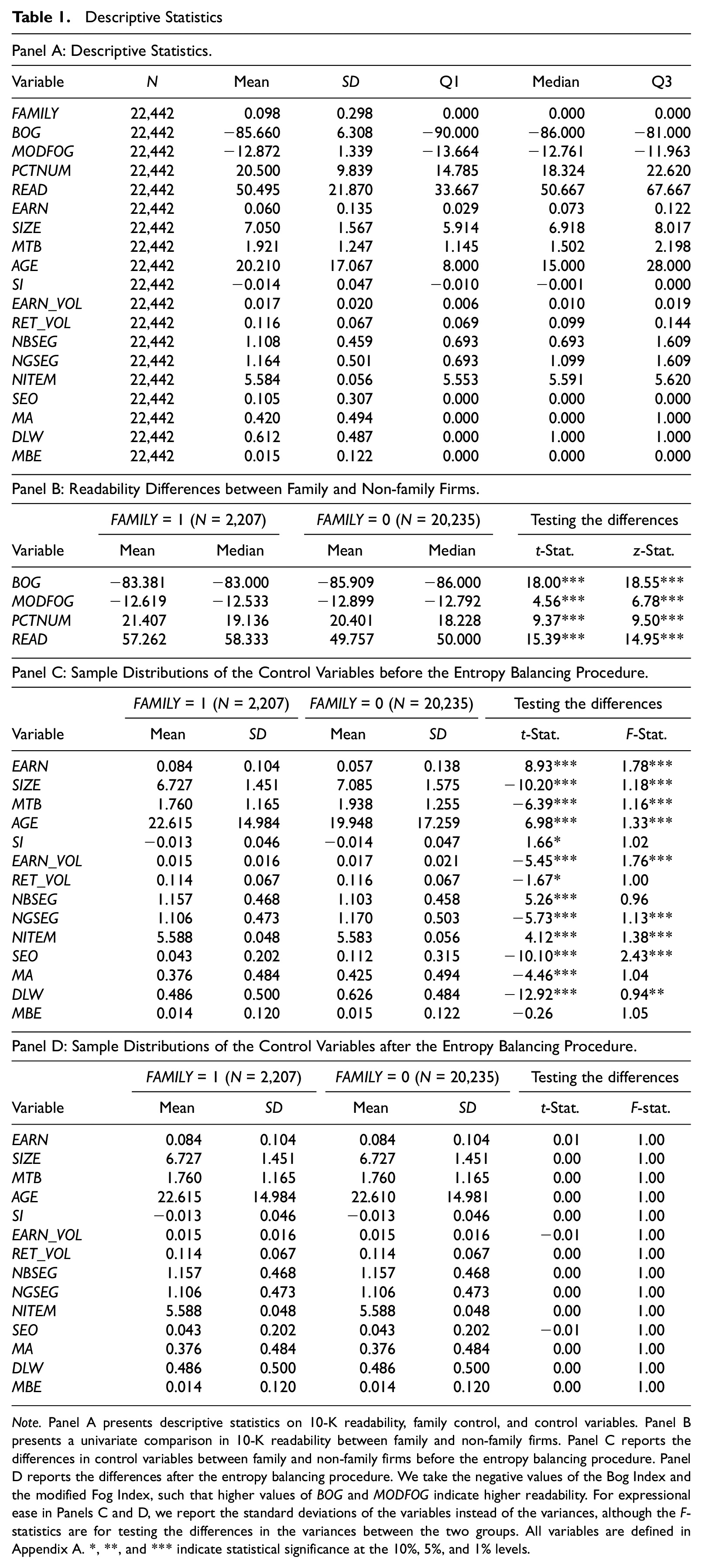

Panel A in Table 1 presents the descriptive statistics for the variables used in Equation 3. Of our 22,442 firm-year observations, 2,207 belong to family firms, representing 9.8% of our sample. This figure is comparable with Srinidhi et al. (2014), who adopt the same approach to define family firms. We notice that the proportion of family firms in our sample is smaller than in prior related studies (e.g., Ali et al., 2007; Chen et al., 2008; D. Wang, 2006). The smaller proportion is consistent with our expectations, given that we employ a more stringent definition of family firms. The sample means of the Bog Index and the modified Fog Index are 85.660 and 12.872, respectively, similar to the statistics reported by Bonsall et al. (2017) and C. F. Kim et al. (2019). 13 On average, the 10-K reports in our sample contain 20.5 numbers per 1,000 words.

Descriptive Statistics

Note. Panel A presents descriptive statistics on 10-K readability, family control, and control variables. Panel B presents a univariate comparison in 10-K readability between family and non-family firms. Panel C reports the differences in control variables between family and non-family firms before the entropy balancing procedure. Panel D reports the differences after the entropy balancing procedure. We take the negative values of the Bog Index and the modified Fog Index, such that higher values of BOG and MODFOG indicate higher readability. For expressional ease in Panels C and D, we report the standard deviations of the variables instead of the variances, although the F-statistics are for testing the differences in the variances between the two groups. All variables are defined in Appendix A. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels.

In Panel B of Table 1, we separately report the mean and median values of the readability measures for family and non-family firms and make a univariate comparison. The results indicate that family firms produce more readable 10-K reports than non-family firms, and the differences in readability are significant at the 1% level.

Panel C of Table 1 reports the means and standard deviations of the control variables before the entropy balancing procedure, while Panel D reports these statistics after entropy balancing. The results indicate that family and non-family firms have significantly different characteristics, but the entropy balancing procedure eliminates such differences. 14

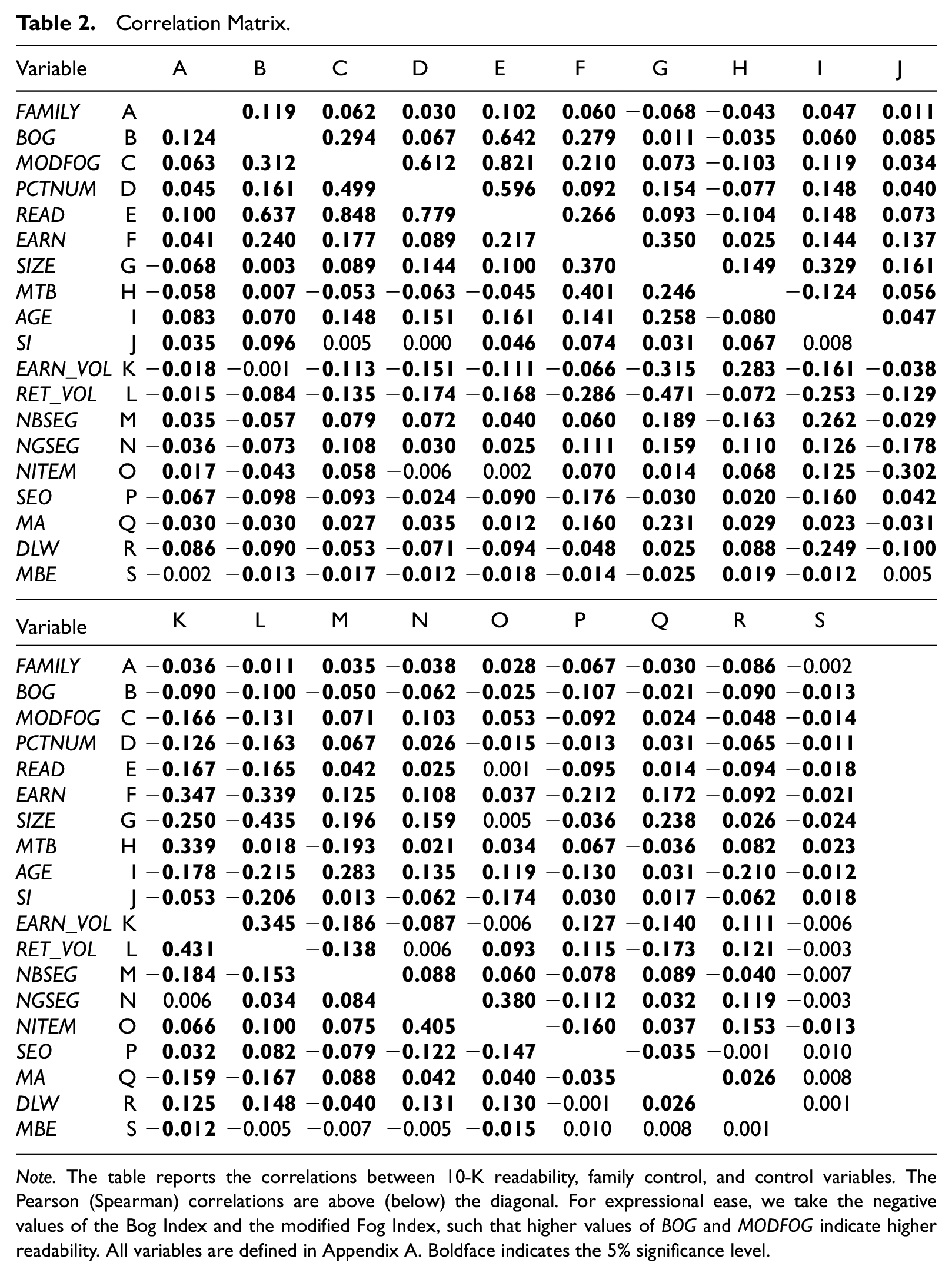

Table 2 presents the correlations among readability, family control, and control variables. We find that each of the three measures of readability and the aggregated readability score exhibits significant positive correlations with family control, consistent with the notion that the 10-K reports filed by family firms are more readable than those filed by non-family firms.

Correlation Matrix.

Note. The table reports the correlations between 10-K readability, family control, and control variables. The Pearson (Spearman) correlations are above (below) the diagonal. For expressional ease, we take the negative values of the Bog Index and the modified Fog Index, such that higher values of BOG and MODFOG indicate higher readability. All variables are defined in Appendix A. Boldface indicates the 5% significance level.

Family Control and 10-K Readability

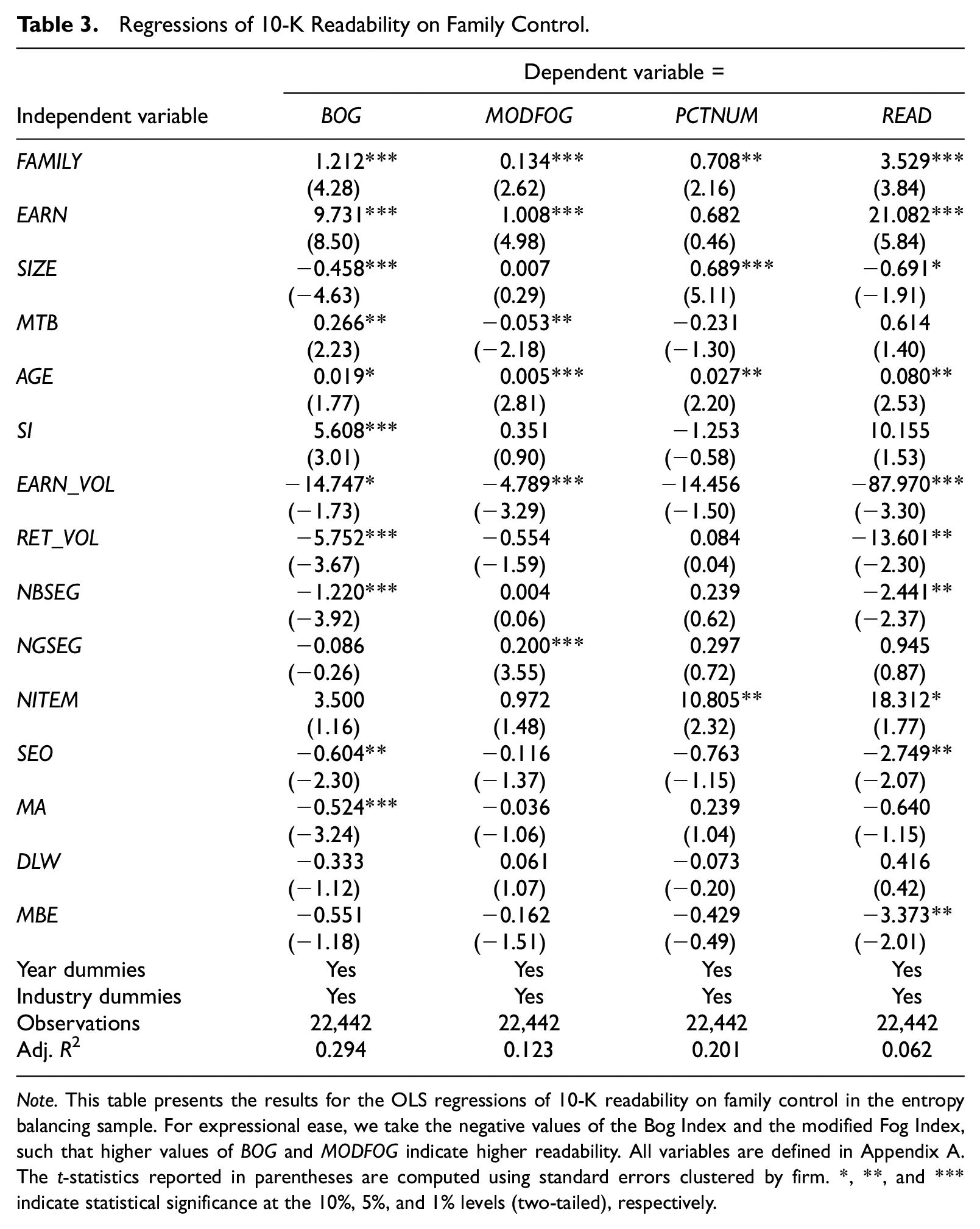

Table 3 presents the results of the regressions of our readability measures on the status of family control and the control variables. While columns 1–3 report the results for BOG, MODFOG, and PCTNUM, respectively, column 4 reports the result for the aggregated readability score, READ. The coefficients of FAMILY are significantly positive, at least at the 5% level across the readability measures, indicating that family firms issue more readable 10-K reports than non-family firms do. The results further suggest that family firms produce 10-K reports that are simpler and more specific than non-family firms. Taking BOG as an example, the difference in BOG between family and non-family firms is 1.212, or 19.2% of the standard deviation of this readability measure in our sample. Thus, the association between family control and 10-K readability is statistically and economically significant. In the remainder of the paper, we focus on the aggregated readability score (READ) because it incorporates all the readability aspects we are concerned about.

Regressions of 10-K Readability on Family Control.

Note. This table presents the results for the OLS regressions of 10-K readability on family control in the entropy balancing sample. For expressional ease, we take the negative values of the Bog Index and the modified Fog Index, such that higher values of BOG and MODFOG indicate higher readability. All variables are defined in Appendix A. The t-statistics reported in parentheses are computed using standard errors clustered by firm. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels (two-tailed), respectively.

The estimated coefficients of control variables are generally consistent with our predictions and those reported in prior studies (e.g., F. Li, 2008; Lo et al., 2017). First, the readability of 10-K reports is positively related to current earnings in three out of the four columns, suggesting that firms with poorer performance issue less readable 10-K reports. Second, we show that 10-K reports are generally more readable among older firms, firms with lower earnings or return volatility, firms with lower business complexity, and firms without seasoned equity offering activity. Third, we find that firms’ MBE targets tend to issue less readable 10-K reports when using the aggregated readability score, whereas the results for the three individual readability measures are somewhat weaker. More importantly, even after these control variables and industry/year fixed effects are included in the model, the difference in 10-K readability between family and non-family firms remains significant. 15

Our main finding suggests that family firms tend to obfuscate disclosure text less than non-family firms in their annual reports. This finding is attributable to two features of family firms. First, family firms experience a lower agency conflict. Second, family firms are more concerned about potential reputation loss. The main test does not allow us to isolate these two arguments because it operationalizes the family firm concept through one dummy variable. To understand the nature of the relation between family control and reporting readability, we next examine the heterogeneity among family firms.

Heterogeneity Among Family Firms

Significant within-sample variations exist among family firms. Prior studies consider the heterogeneity in management and control structures of family firms when examining the firm value of family versus non-family firms (D. Miller et al., 2013; Villalonga & Amit, 2006). Following the suggestions from recent literature (e.g., Salvato & Moores, 2010), we examine the role of family-related characteristics that reflect different incentives and preferences between founding family members and outsiders in shaping the readability of 10-K reports. Such an investigation can help us distinguish between agency conflict and reputation arguments.

First, we examine eponymy as a feature that shapes reputation concerns among founding family members. Prior studies argue that eponymous firms have higher reputation costs because a damaged firm reputation would directly affect the founders and their family members (Belenzon et al., 2017; Deephouse & Jaskiewicz, 2013). Under this premise, Minichilli et al. (2022) show that eponymous firms exhibit higher financial reporting quality than non-eponymous firms. Similarly, we expect our main finding to be concentrated among eponymous family firms if it is mainly attributable to the reputation argument under the socioemotional wealth theory. On the other hand, eponymy is not relevant under the traditional agency theory. Agency theory does not predict any difference between eponymous and non-eponymous family firms in the improving effect of family control on 10-K readability.

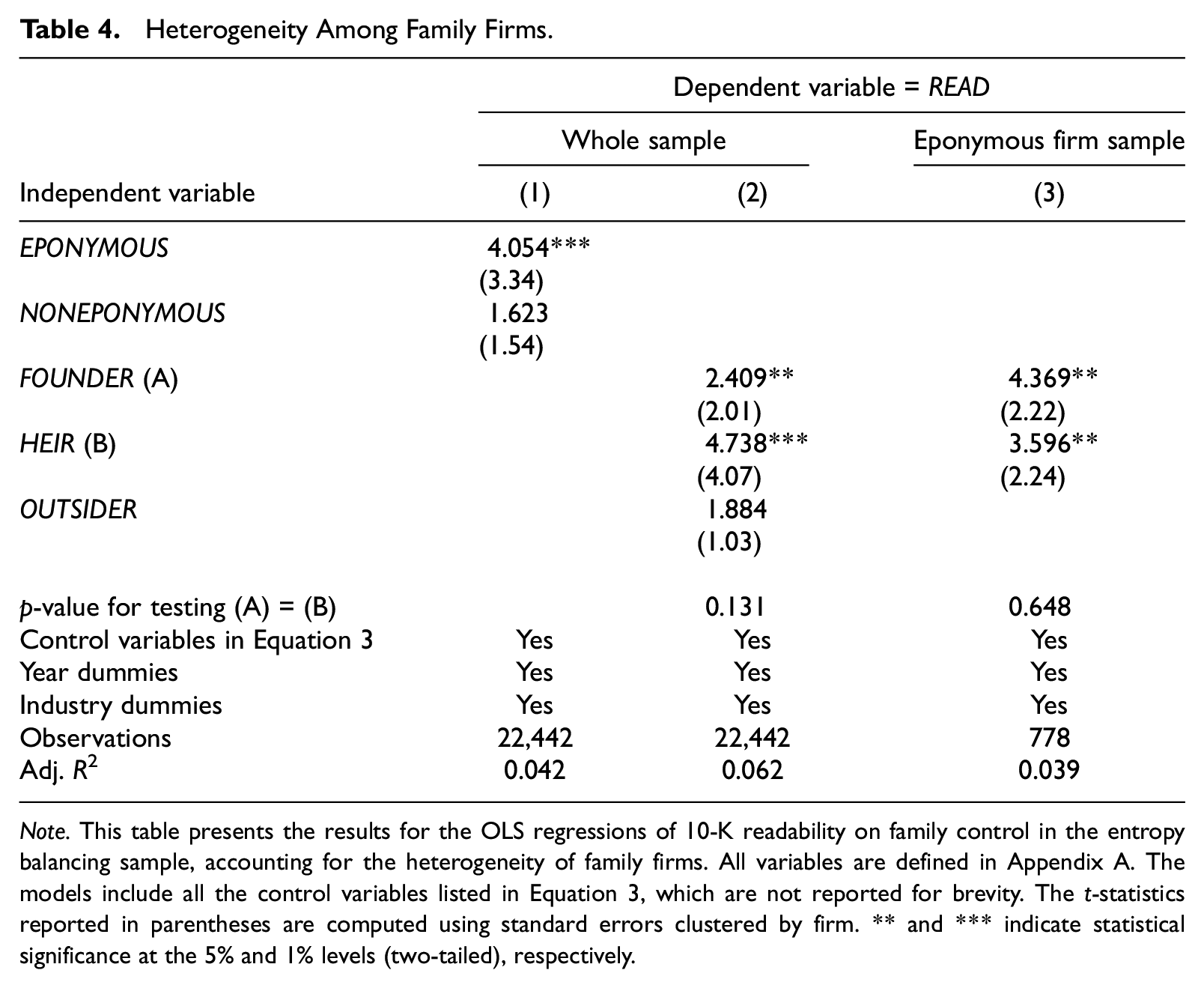

For each of the 2,207 family firm-year observations in our sample, we check the firm name to determine the eponymy of the family firm. Specifically, we define EPONYMOUS as an indicator variable that equals one if the family firm’s name includes the entire last name or the standalone initials of the first and last names of the founders or their family members and zero otherwise. In contrast, NONEPONYMOUS equals one if the firm is a family firm but not eponymous and zero otherwise. This definition results in 778 eponymous and 1,429 non-eponymous family firm-year observations. To test the predictions regarding eponymy, we replace the key variable in Equation 3, FAMILY, with EPONYMOUS and NONEPONYMOUS.

Column 1 of Table 4 shows that the coefficient of EPONYMOUS is significantly positive, whereas the coefficient of NONEPONYMOUS is positive but not significant. In other words, the 10-K reports issued by eponymous family firms are more readable than those issued by non-family firms, but this distinction does not extend to non-eponymous family firms. This result supports the reputation argument under the socioemotional wealth theory rather than the agency conflict argument under the traditional agency theory.

Heterogeneity Among Family Firms.

Note. This table presents the results for the OLS regressions of 10-K readability on family control in the entropy balancing sample, accounting for the heterogeneity of family firms. All variables are defined in Appendix A. The models include all the control variables listed in Equation 3, which are not reported for brevity. The t-statistics reported in parentheses are computed using standard errors clustered by firm. ** and *** indicate statistical significance at the 5% and 1% levels (two-tailed), respectively.

Second, we study the influence of founding family members in managing and monitoring the firm by classifying family firms into founder, heir, and outsider-managed firms. Under the traditional agency theory, founder and heir firms are subject to different levels of agency conflicts. As founders heavily invest their non-diversifiable human capital in establishing the firm and are fully committed to its survival and growth, the agency conflict between owners and managers is minimized when founders play an influential role in the firm. On the other hand, heirs inherit control from founders and thus are often less devoted to the firm and more likely to exploit their entrenched position to expropriate outside investors. Consistent with such differences between founders and heirs, Villalonga and Amit (2006) show that family firm premiums are prevalent only in cases where the founder is the CEO or the chairperson of the board of directors. Prior studies also show that heirs serving as the CEO are generally perceived to be value-destroying (e.g., Pérez-González, 2006; Villalonga & Amit, 2006). As a result, we expect the positive effect of family control on reporting readability to be concentrated among founder firms if the traditional agency theory dominates in explaining our main finding.

Under the socioemotional wealth theory, we expect the founders and heirs to have similar incentives to protect the firm reputation because the firm’s reputation is closely tied to the family’s reputation. Both founders and heirs would be concerned about potential damage to their family’s reputation. Consistent with this view, Minichilli et al. (2022) show that the reputation effect of eponymy on financial reporting quality equally applies to the first and later generations of founding families. In a similar vein, we expect our main finding to be strong for both founder and heir firms if it is primarily driven by the reputation argument.

To test these predictions, we manually search proxy statements, company websites, Capital IQ, and D&B Hoovers to identify the founders of each family firm in our sample. For each family firm-year observation, we determine whether the CEO and the chairperson is the founder or a family member that inherits control from the founder(s). We then categorize family firms into founder firms, heir firms, and outsider-managed firms. If the CEO or the chairperson is a founder, we classify the firm as a founder firm. If the founder holds neither of the two positions, but at least one is taken by a family member of the founder(s), we classify the firm as an heir firm. If neither the founders nor their family members serve as the CEO or the chairperson, we classify the firm as managed by hired outsiders. Among the 2,207 family firm-year observations, our data collection procedure yields 884 founder, 993 heir, and 330 outsider firm-years. We next replace the key variable in Equation 3, FAMILY, with three variables: (i) FOUNDER, an indicator variable that equals one for founder-managed family firms and zero otherwise; (ii) HEIR, an indicator variable that equals one for heir-managed family firms, and zero otherwise; and (iii) OUTSIDER, an indicator variable that equals one for family firms managed by hired outsiders, and zero otherwise.

As shown in column 2 of Table 4, the coefficients of FOUNDER and HEIR are significantly positive, while the coefficient of OUTSIDER is not significant. In addition, we do not observe a significant difference between the coefficients of FOUNDER and HEIR. This result means that both founder and heir firms issue more readable 10-K reports than non-family firms, but outsider-managed family firms do not. 16

To pin down the difference among founder, heir, and outsider-managed family firms, we further examine such differences within the sample of eponymous family firms. In column 3 of Table 4, we estimate the effect of FOUNDER and HEIR on 10-K readability, using outsider-managed eponymous firms as the benchmark. We find that both FOUNDER and HEIR load positively, but their coefficients are not significantly different. This result shows that the reputational effect of eponymy applies similarly to founder and heir firms.

Taken together, the results from investigating the heterogeneity among family firms suggest that the positive effect of family control on 10-K readability is linked to the influence of family members in managing and monitoring the firm and, more importantly, attributable to the reputation, not the agency conflict argument.

Cross-Sectional Variations

Thus far, we have established that family firms (versus non-family firms) tend to issue more readable 10-K reports and attribute this finding to greater reputation concerns among founding family members. To further link our findings to the socioemotional wealth theory, we next investigate whether the improving effect of family control on reporting readability is offset when family insiders are more likely to exploit opacity to extract private control benefits. We identify three factors that capture family insiders’ incentive and opportunity to expropriate outsides: earnings management, weak board governance, and dual-class share structures.

Earnings Management

We expect the improving effect of family control on 10-K readability to be smaller among firms that manage earnings more for two reasons. First, earnings management by a family firm may reflect the family insiders’ intention to expropriate outside minority investors and protect family control by hiding the true firm performance. We expect the positive effect of the reputational concern of the family to be offset by the expropriation motive reflected in earnings management. Second, Lo et al. (2017) find that firms may obfuscate disclosure text to mask their earnings management behavior. Along this line, earnings management per se provides more incentive to obfuscate textual information for any firm, thus diminishing the difference between family and non-family firms in their obfuscation incentives.

Weak Board Governance

We expect that weaker board governance provides family insiders with more opportunities to entrench themselves and extract private benefits of control. Consistent with Srinidhi et al. (2014), we construct a board governance index (BOARD_INDEX) that incorporates five characteristics of board composition: board independence, board diversity, board diligence, audit committee size, and board expertise. A lower board governance index indicates less effective board monitoring and, in turn, a higher likelihood of entrenchment or minority shareholder expropriation. See Appendix B for the detailed definition of the index.

Dual-Class Share Structures

Villalonga and Amit (2006) argue that, through issuing dual-class shares, families obtain control of a firm with a disproportionately low cash flow ownership, thus intensifying the agency conflict between family insiders and minority investors. Along this line, Ali et al. (2007) show that the improving effect of family ownership on earnings quality and voluntary disclosure practices is lower in firms that choose a dual-class share structure. Likewise, we expect the positive relation between family control and 10-K readability to diminish in firms with dual share classes.

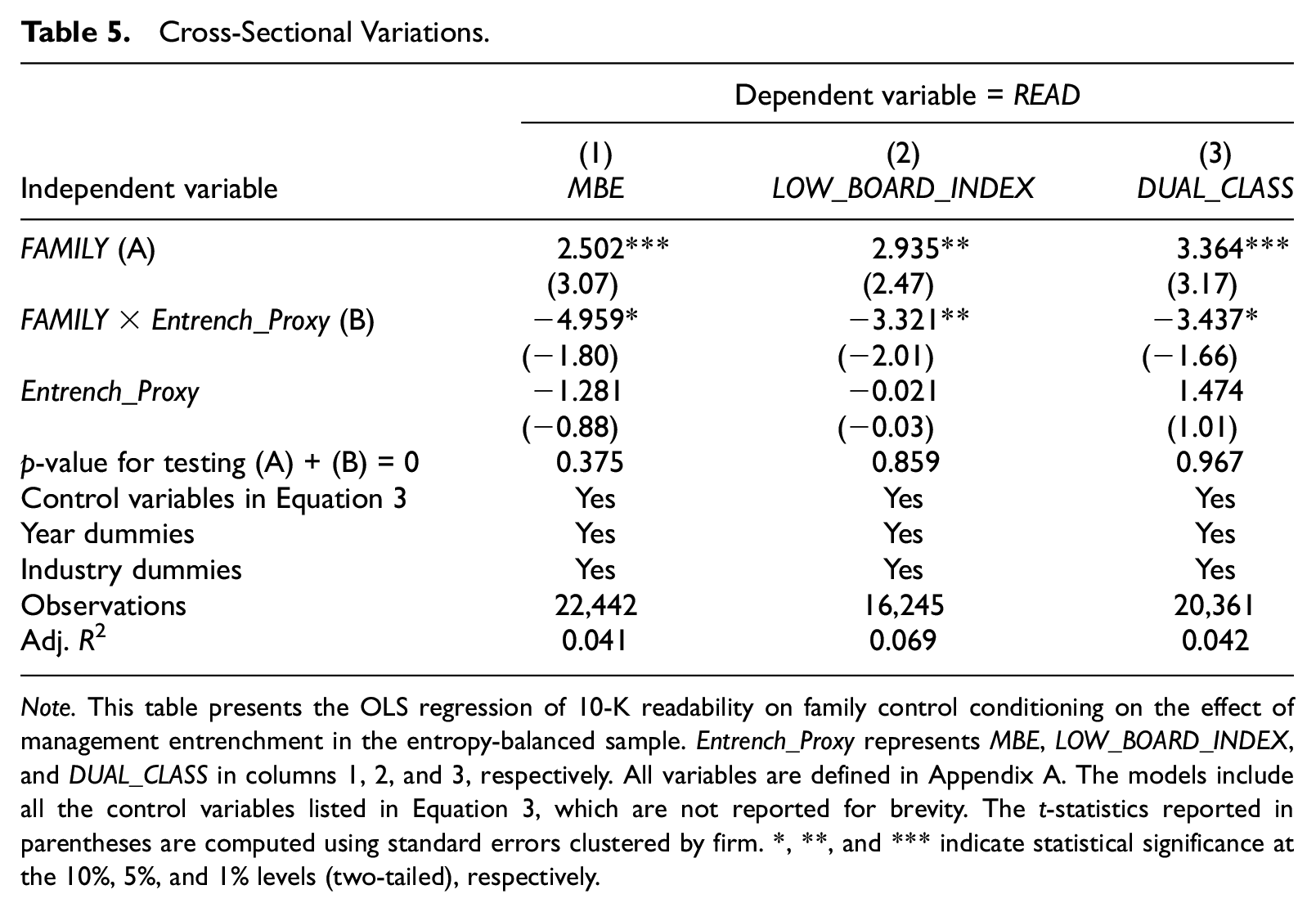

Column 1 of Table 5 reports the result for estimating Equation 3 augmented by the interaction term of FAMILY×MBE. We find that FAMILY loads positively in the model. At the same time, the interaction term FAMILY×MBE loads negatively, and the sum of the coefficients of FAMILY and FAMILY×MBE is not significantly different from zero. Columns 2 and 3 show that the interaction terms FAMILY×LOW_BOARD_INDEX and FAMILY×DUAL_CLASS load negatively. Also, we find that the overall effect of FAMILY, captured by the sum of the coefficients of FAMILY and the interaction terms, is not significantly different from zero across the two columns. These results indicate that consistent with our predictions, the positive relationship between family control and 10-K readability (i) exists only in cases where the firm is less likely to manipulate earnings, (ii) exists only when the board governance is strong, and (iii) the firm does not have dual-class share structures.

Cross-Sectional Variations.

Note. This table presents the OLS regression of 10-K readability on family control conditioning on the effect of management entrenchment in the entropy-balanced sample. Entrench_Proxy represents MBE, LOW_BOARD_INDEX, and DUAL_CLASS in columns 1, 2, and 3, respectively. All variables are defined in Appendix A. The models include all the control variables listed in Equation 3, which are not reported for brevity. The t-statistics reported in parentheses are computed using standard errors clustered by firm. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels (two-tailed), respectively.

Obfuscation Versus Information: Testing Market Response to 10-K Filings

We argue that our main result is consistent with family firms being less likely to obfuscate textual information. However, Bushee et al. (2018) show that low readability can also reflect the conveyance of complex information. In this sense, an alternative explanation for our main result is that family firms (versus non-family firms) are less responsive to investors’ information needs. Therefore, they provide less information, thus increasing 10-K readability.

To disentangle the obfuscation argument, we test whether investors perceive the 10-K reports with higher readability issued by family firms to be more informative. Specifically, we estimate the following regression of 10-K informativeness on family control and its interaction with an indicator variable that captures the high readability of 10-K reports:

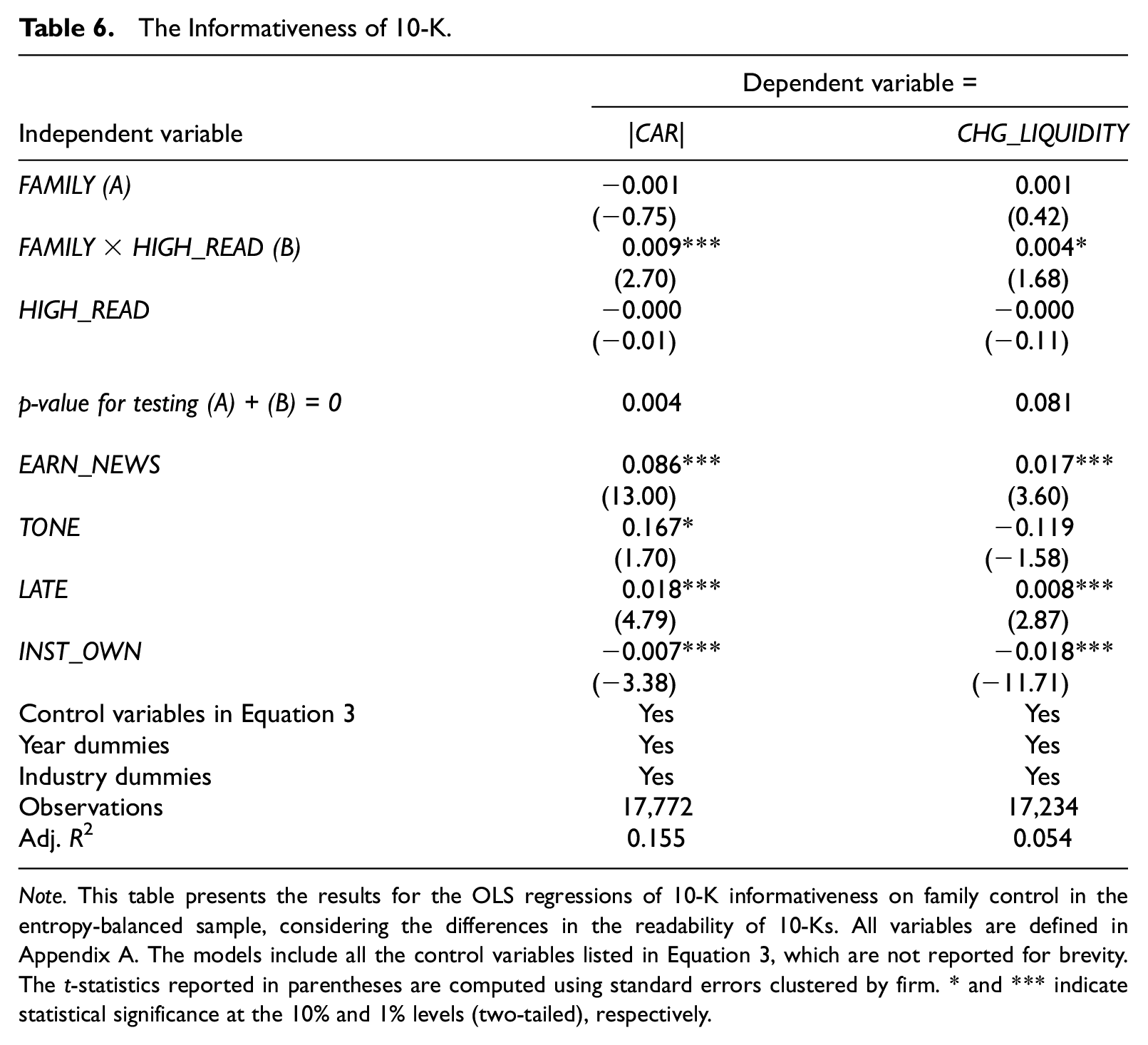

In Equation 4, the dependent variable, Informativeness, represents one of the two measures of 10-K informativeness. Our first measure is |CAR|, the absolute value of cumulative abnormal returns over the [0,+1] window relative to the 10-K filing date. A more informative 10-K filing should generate greater abnormal returns over the filing period (Brown & Tucker, 2011). Our second measure is CHG_LIQUIDITY, the negative value of Amihud’s (2002) measure of illiquidity estimated over the [0,+1] window relative to the 10-K filing date adjusted by illiquidity in the pre-filing periods. If a 10-K filing is informative, the information asymmetry should decrease, and liquidity should thus increase around the filing date (Guay et al., 2016).

The variable of interest is the interaction between FAMILY and HIGH_READ. In this test, we focus on variations of readability that cannot be explained by the control variables or industry/year fixed effects in Equation 3. Specifically, we estimate Equation 3 by excluding FAMILY, obtain the residual value, and define HIGH_READ as an indicator variable that equals one if the residual value falls in the top quintile, and zero otherwise. Consistent with prior studies (Brown & Tucker, 2011; Feldman et al., 2010; Griffin, 2003; Loughran & McDonald, 2011; K. Wang, 2021), we include four additional variables in Equation 4 to control for other factors that potentially affect stock market reactions to 10-K filings: investors’ response to earnings announcements (EARN_NEWS), optimistic/pessimistic language in 10-K filings (TONE), late filings (LATE), and institutional ownership (INST_OWN).

As reported in Table 6, the interaction term FAMILY×HIGH_READ loads positively in both columns. In addition, the sum of FAMILY and FAMILY×HIGH_READ is positive and statistically significant. These findings indicate that the market perceives a 10-K report issued by family firms as more informative only when the reporting readability is high. Overall, our test of stock market effects of 10-K filings shows that the higher 10-K readability exhibited by family firms than non-family firms is more likely attributable to the obfuscation explanation than the information conveyance explanation.

The Informativeness of 10-K.

Note. This table presents the results for the OLS regressions of 10-K informativeness on family control in the entropy-balanced sample, considering the differences in the readability of 10-Ks. All variables are defined in Appendix A. The models include all the control variables listed in Equation 3, which are not reported for brevity. The t-statistics reported in parentheses are computed using standard errors clustered by firm. * and *** indicate statistical significance at the 10% and 1% levels (two-tailed), respectively.

State-Level Succession Tax Cuts: An Exogenous Shock on Family Control

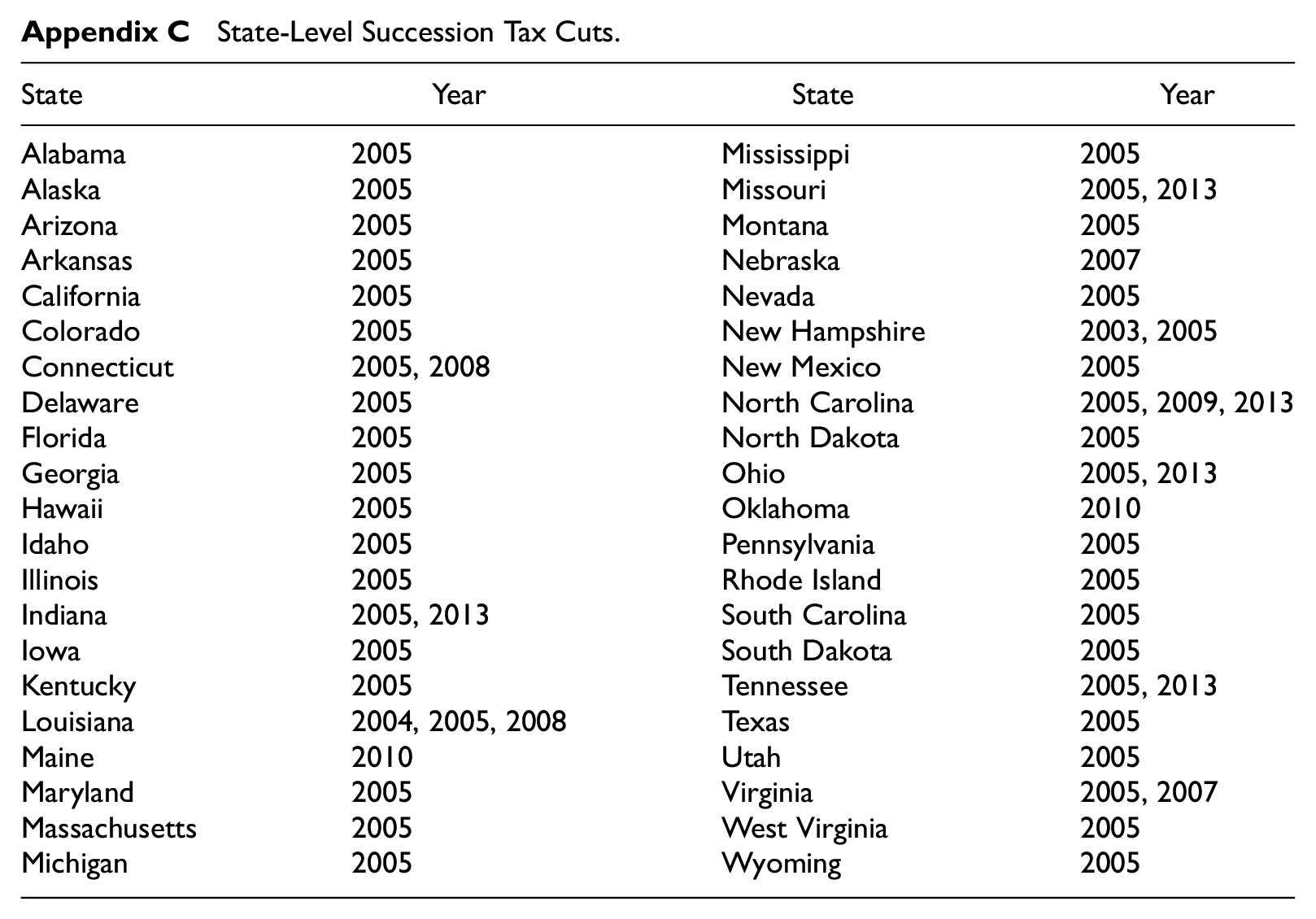

To mitigate potential endogeneity concerns, we use state-level succession tax cuts as an exogenous shock on the incentives of a family firm to pass control to later generations. We obtain state-level changes in inheritance, gift, generation-skipping, and estate taxes for 2003–2010 from Massa and Zaldokas (2016). For years after 2010, we manually collect information on succession tax cuts from Thomson Reuters RIA Checkpoint State Tax Reporters, supplemented by intensive Google searches. 17 Over our sample period, we identify 42 states that repealed at least one type of succession tax. 18

The staggered succession tax cuts that apply to a family firm’s state of headquarters location increase the financial advantage of retaining the family control and passing it on to future generations. Therefore, it enhances the family owners’ incentive to preserve family control, maintain the family’s reputation, and engage in long-term investments. In contrast, we do not expect a reduction in succession taxes to affect non-family firms significantly. Differently stated, the staggered succession tax cuts provide an exogenous shock on the differences between family and non-family firms in their incentives and preferences. If the difference in 10-K readability between family and non-family firms is driven by family insiders caring about the firm reputation, one should expect the difference to widen after a state cuts its succession taxes.

We test this prediction by applying the generalized difference-in-differences approach (Bertrand & Mullainathan, 2003) to the coefficient of FAMILY in Equation 3:

where s and t denote states and years, respectively. POST_TAXCUTs,t is a dummy variable that equals one if state s has cut succession taxes by year t, and zero otherwise. By substituting Equation 5 into Equation 3, we obtain the following model

The coefficient of this interaction term, FAMILY × POST_TAXCUT, is a DiDiD estimator that captures the effect of state-level succession tax cuts on the relation between family control and 10-K readability. The variable FAMLY also interacts with state and year dummies to capture the cross-state and temporal variations, respectively, of the improving effect of family control on 10-K readability. Since we do not have information on the exact dates of the succession tax cuts, we exclude the years of the tax cuts from our sample in this analysis to avoid misclassifying a firm-year observation as pre-treatment or post-treatment.

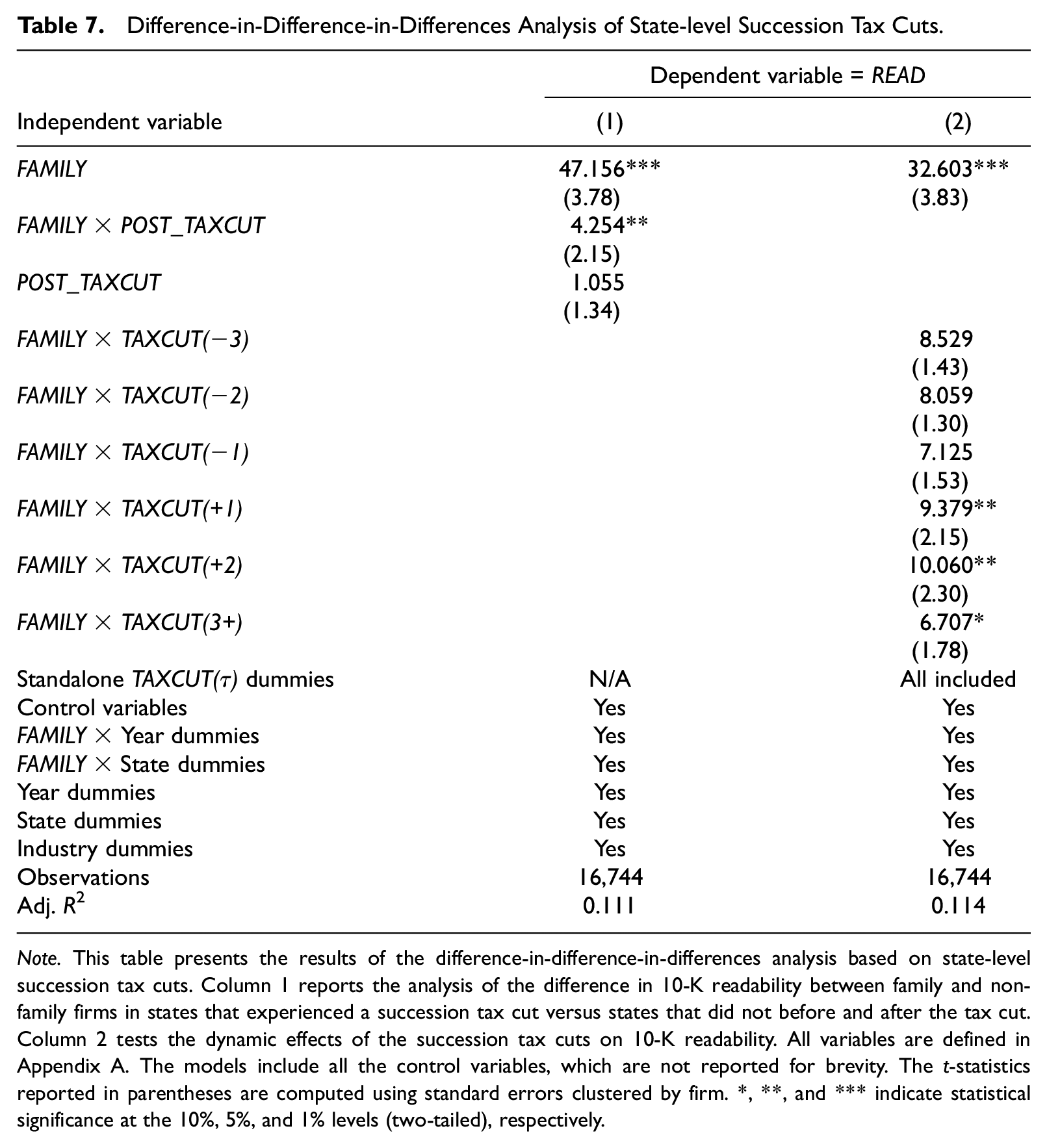

As shown in column 1 of Table 7, the coefficient of FAMILY × POST_TAXCUT is significantly positive at the 5% level, indicating that state-level succession tax cuts strengthen the positive relationship between family control and 10-K readability. Using the difference in 10-K readability between family and non-family firms in the benchmark state-year (represented by the coefficient of FAMILY) as a reference point, such difference widens by 9.0% due to a reduction in state succession taxes. Overall, the results link the readability difference between family and non-family firms to family owners’ incentive to preserve the family’s reputation to ease the transfer to future generations. 19

Difference-in-Difference-in-Differences Analysis of State-level Succession Tax Cuts.

Note. This table presents the results of the difference-in-difference-in-differences analysis based on state-level succession tax cuts. Column 1 reports the analysis of the difference in 10-K readability between family and non-family firms in states that experienced a succession tax cut versus states that did not before and after the tax cut. Column 2 tests the dynamic effects of the succession tax cuts on 10-K readability. All variables are defined in Appendix A. The models include all the control variables, which are not reported for brevity. The t-statistics reported in parentheses are computed using standard errors clustered by firm. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels (two-tailed), respectively.

To check the parallel trends assumption, we expand Equation 6 by replacing the dummy variable POST_TAXCUT with the following six variables: TAXCUT(−3), TAXCUT(−2), TAXCUT(−1), TAXCUT(+1), TAXCUT(+2), and TAXCUT(3+). These variables represent the years relative to the year of the succession tax cut, leaving the earliest years to the benchmark group. For example, TAXCUT(−3) indicates 3 years before the succession tax cut, while TAXCUT(3+) indicates 3 or more years after the succession tax cut. Column 2 of Table 7 shows that the interactions of FAMILY with TAXCUT(+1), TAXCUT(+2), and TAXCUT(3+) load positively, while those with TAXCUT(−3), TAXCUT(−2), and TAXCUT(−1) do not load. We conclude that the effects of succession tax cuts on 10-K readability do not exist before the tax cuts, appear in the first year after the tax cuts, and sustain in subsequent years.

Obfuscation Versus Ontological Complexity

Although we have carefully designed our empirical analyses to attribute the higher readability of family firms’ 10-K reports to lower obfuscation, one may still be concerned about the ontological complexity explanation that family firms are inherently more complex than non-family firms (see Bloomfield, 2008). Ideally, such a concern can be mitigated by focusing on the discretionary components of 10-K disclosures. However, it is notoriously challenging to disentangle discretionary disclosures from nondiscretionary or boilerplate components of 10-K reports. We argue that most nondiscretionary or boilerplate components should arise from industry or market dynamics, which can be reasonably eliminated by adjusting for industry norms of readability. The rationale is that if a sentence or block of text in the 10-K is commonly used by firms in the same industry, it should affect (either increase or decrease) the readability of all 10-Ks in this industry in the same manner.

We thus conduct the following two robustness checks. First, we include the industry–year joint fixed effects in Equation 3 and find that the coefficients of FAMILY are highly comparable with those reported in Table 3, both economically and statistically. Second, our results hold when we re-estimate Equation 3 using industry-adjusted readability measures as the dependent variables. These untabulated results reduce the concern that our results are driven by nondiscretionary disclosures that is common among industry peers. In this sense, the chance is low that our results are mainly driven by ontological complexity instead of obfuscation. 20

Conclusion

In this paper, we find that family firms issue more readable 10-K reports than non-family firms. This result holds in an entropy-balanced sample that largely eliminates the differences in other determinants of readability, including inherent firm complexity between family and non-family firms. In examining the effect of heterogeneity among family firms, we find that eponymous family firms issue more readable 10-K reports than non-family firms, but this result does not extend to non-eponymous family firms. In addition, the positive effect on 10-K readability exists for family firms managed by founders or their family members but not for those managed by outsiders. Our cross-sectional tests show that the positive effect of family control on 10-K readability is reduced in firms with higher earnings management, weaker board governance, and dual-class share structures. Further, family firms’ 10-K reports with higher readability are perceived by investors to be more informative than those issued by non-family firms. Finally, using state-level succession tax cuts as an exogenous shock on family owners’ incentive to continue the business under family control, we show that the positive relation between family control and 10-K readability strengthens after a succession tax cut.

Overall, our results suggest that family firms exhibit lower obfuscation of textual information in financial reports than non-family firms. This positive effect on readability is attributable to the family insiders’ incentives to maintain the firm’s reputation, consistent with the socioemotional wealth theory of family firms.

Our paper is among the few that study narrative disclosure in the family firm context. We contribute to the debate on disclosure practices of family versus non-family firms, where the existing literature provides mixed results. By investigating the heterogeneity among family firms, we identify the reputation costs of family insiders as an important factor shaping corporate disclosure practices. This paper is also the first to link disclosure practices to family insiders’ incentives and preferences through the exogenous variations of family owners’ succession incentives brought by a reduction in succession taxes at the state level. Finally, we contribute to the readability literature by showing that financial reporting readability varies with family control in particular and corporate ownership and control structure in general.

Footnotes

Appendix

State-Level Succession Tax Cuts.

| State | Year | State | Year |

|---|---|---|---|

| Alabama | 2005 | Mississippi | 2005 |

| Alaska | 2005 | Missouri | 2005, 2013 |

| Arizona | 2005 | Montana | 2005 |

| Arkansas | 2005 | Nebraska | 2007 |

| California | 2005 | Nevada | 2005 |

| Colorado | 2005 | New Hampshire | 2003, 2005 |

| Connecticut | 2005, 2008 | New Mexico | 2005 |

| Delaware | 2005 | North Carolina | 2005, 2009, 2013 |

| Florida | 2005 | North Dakota | 2005 |

| Georgia | 2005 | Ohio | 2005, 2013 |

| Hawaii | 2005 | Oklahoma | 2010 |

| Idaho | 2005 | Pennsylvania | 2005 |

| Illinois | 2005 | Rhode Island | 2005 |

| Indiana | 2005, 2013 | South Carolina | 2005 |

| Iowa | 2005 | South Dakota | 2005 |

| Kentucky | 2005 | Tennessee | 2005, 2013 |

| Louisiana | 2004, 2005, 2008 | Texas | 2005 |

| Maine | 2010 | Utah | 2005 |

| Maryland | 2005 | Virginia | 2005, 2007 |

| Massachusetts | 2005 | West Virginia | 2005 |

| Michigan | 2005 | Wyoming | 2005 |

Acknowledgements

We are grateful to Xiao-Jun Zhang (Editor in Chief), Bharat Sarath (Associate Editor), Annalisa Prencipe (Associate Editor), and an anonymous reviewer for their insightful comments and suggestions. We appreciate helpful comments from workshop participants at Deakin University (Melbourne), University of Michigan-Flint, and University of Texas at Arlington. We also thank Cassandra Harms, Alessandra Tranchida, Alex Ye, and Yi Zhang for their excellent research assistance. All errors are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Qunfeng Liao gratefully acknowledges the financial support from the School of Business Administration Spring/Summer Research Fellowship at Oakland University.