Abstract

This study investigates whether capital account liberalization, a leading characteristic of globalization, is associated with firms’ future innovation output. Employing a novel firm-level panel data set covering 41 countries over two decades, we show that capital account liberalization is significantly associated with higher corporate patenting activities, particularly for firms from innovation-intensive industries. Further analyses show that the effect is stronger among firms from economies in a better legal environment, signifying the important role of good institutional quality in facilitating the positive impact of liberalization. The effect is also stronger among firms with higher initial productivity, consistent with the “productivity” hypothesis, according to which bigger and more productive firms generate more innovation after liberalization. Our findings are robust to the use of various measurements, subsamples, and estimation models. This study provides global firm-level evidence of the real economic impact of financial globalization.

Keywords

Introduction

Globalization and innovation are defining themes of this historical moment. On the one hand, innovation is at the heart of sustainable long-term growth and development; on the other hand, despite recent setbacks, globalization has “flattened” our world by lifting barriers to cross-border trade flows (trade liberalization) and capital flows (capital account liberalization) (Friedman, 2007). But how does the advance of globalization impact firm innovation? Does globalization spur more firm innovation? A substantial body of literature, both theoretical and empirical, examines the impact of trade liberalization—one aspect of globalization—on innovation by domestic firms (see Arkolakis et al., 2018; Bustos, 2011; Coelli et al., 2020, among others). Yet, less is known about the impact of capital account liberalization, another important aspect of globalization, on firm innovation. 1 Based on a comprehensive firm-level patent and financial characteristic data set that covers more than 40 countries over two decades, this article fills this gap by examining the impact of lifting barriers to cross-border capital flows on firm innovation.

Following a novel internet-based matching approach in Autor et al. (2020), we construct an international, wide-ranging firm-level data set by combining global patents and financial data. This method corrects for many false negatives that occur when matching by company name only. After matching global patents to financial data by firm name and web URL, our comprehensive firm-level data set includes both detailed financial information and patent data. This data set enables us to investigate the relation between capital account liberalization and firm innovation by controlling for a group of firm-, industry-, and country-level characteristics that might contribute to firms’ innovation investment and output.

According to extant studies, capital account liberalization influences firm innovation through several different channels. The first channel is a reduction in the cost of capital. As the neoclassical model (Solow, 1956) predicts, a temporary decrease in the cost of capital follows advances in globalization, and firms are expected to borrow more from the international market and increase their investment during the transition period (Henry, 2007, 2003) The second channel is risk sharing (or resource reallocation). Financial integration such as equity market liberalization enables risk sharing between domestic and foreign firms through cross-border portfolio holdings (Bekaert et al., 2005; Moshirian et al., 2021). The third channel is increased competition. Reduced capital controls can spur increased competition because some originally constrained firms become able to conduct innovation projects and foreign competitors are permitted to enter the market (Aghion et al., 2005; Deng, 2009; Walz, 1997). Combined, these major channels result in a positive impact of capital account liberalization on firm innovation.

In our baseline regression, we find that the removal of capital controls is significantly and positively associated with firms’ patenting activity. This result holds not only for patent counts but also for patent family size and citations, which suggests that the increase in patenting activity is not simply a “lawyer effect” (i.e., patenting more to protect intellectual property). Rather, real innovation takes place after liberalization.

Most importantly, we identify the impact of capital account liberalization on innovation, following Acharya and Subramanian (2009). Our identification comes from differential responses across firms in sectors with varying innovation intensity in the same treatment group (i.e., countries that liberalize their capital accounts). Specifically, under a generalized difference-in-differences (DiD) framework, we introduce an interaction term between the capital account liberalization variable and a time-varying, sectoral innovation intensity variable. 2 We find that the positive effect of capital account liberalization on firm innovation is more pronounced in more innovation-intensive sectors.

In additional analyses, we find that firms from economies with better legal environments are more innovative after liberalization, emphasizing the importance of good institutional environment for innovation performance. Furthermore, we find that the effect is stronger among firms with higher initial productivity, consistent with the “productivity channel,” whereby bigger, more productive firms are better positioned to take advantage of liberalization and generate more innovation afterward.

To capture major events in the liberalization process and document the timing of the impact, we follow Larrain (2015) and identify an opening date for each country as the year in which a 1 SD increase happened in the continuous capital account liberalization index. We trace the year-by-year effect of capital opening on firm innovation and find that the positive impact on innovation is enduring. Moreover, we find that firms spend more on research and development (R&D), generate patents with high originality and generality, and cite more foreign patents after liberalization, suggesting that capital account liberalization increases knowledge-expanding innovation. Finally, we show that our results are robust to various specifications including alternative measures, estimation models, and subsamples.

A large body of prior research focuses on the impact of liberalization on business performance, such as total factor productivity or investment (Aghion et al., 2010; Varela, 2018), but little evidence exists regarding observable firm-level innovation inputs and outputs (e.g., R&D spending and patenting activities). We provide comprehensive and consistent evidence of the influence of capital account liberalization on firm innovation for a large group of countries over several decades. The scope of our analyses provides external validity to extant literature, which has largely concentrated on relatively limited policy reforms (e.g., Bustos, 2011).

Second, by combining our cross-country staggered capital account liberalization events with firm-level panel data, we are able to compare cross-sector variation within the group of countries that relaxed restrictions on capital accounts. Therefore, our methodology does not rely on the usual assumptions for controlling for a common trend between the treatment group (countries that liberalize their capital accounts) and the control group (countries that did not liberalize their capital accounts), as in conventional DiD estimation. Instead, our identification comes from within-country variations in innovation levels across sectors that are more (or less) dependent on new technologies. In addition, we exploit a novel, large, and inclusive firm-level patent data set that is infrequently used in the global financial openness setting. Our study, therefore, provides a deeper understanding of the economic mechanisms that help generate industrial innovations.

This study most closely resembles Moshirian et al. (2021), but it differs in important ways. First, Moshirian et al. (2021) focused on equity market liberalization, which is only one of 10 categories of capital account opening. However, it is difficult to separately identify the effect of reform in one category from the effect of reform in the other categories, which could have confounding impacts on firms’ innovation activity. Second, our estimation uses a firm-level panel data from multiple countries, whereas Moshirian et al. (2021) looked at aggregate industry-level innovation activity. Our cross-country firm-level sample allows us to (a) use more powerful tools to mitigate endogeneity concerns, (b) look deeper into firms’ heterogeneous responses to globalization, and (c) control for firm characteristics that influence firms’ innovation output. This isolates the component of firm innovation driven by a country’s removal of capital controls rather than by firm-specific or industry characteristics. As such, our article provides the first large-scale, cross-country, firm-level evidence on the impact of capital market integration on firm-level innovation.

The article proceeds as follows. Section “Development of Hypotheses” provides the theoretical background and develops the hypotheses. Section “Data” describes the data and sample selection. Section “Capital Account Liberalization and Firm Innovation” presents the main empirical results. Section “Additional Analyses” explores cross-sectional variations. Section “Robustness Check” describes various robustness tests. Section “Concluding Remarks” concludes.

Development of Hypotheses

Capital account liberalization can influence firm innovation through three possible channels. The first channel is a reduced cost of capital. Theoretically, the neoclassical model predicts that liberalization, by allowing free movement of financial resources from capital-rich economies (where expected returns are low) to capital-constrained economies (where expected returns are high), will reduce the cost of capital (Henry, 2007; Solow, 1956). 3 On a more practical level, liberalization allows investors to repatriate profits so that they are willing to risk their money in these developing economies (Desai et al., 2006; Laban & Larrain, 1997; Levine, 1997). In practice, research finds that when countries liberalize their capital account, they experience increases in the gross domestic product (GDP) per worker and average investment rates of all firms because of the reduced cost of capital (Henry, 2007, 2003) In addition, there is a natural feedback mechanism in this context: firms’ engagement in patenting activity can lower the cost of financing, which generates further innovation (Mann, 2018).

The second channel is risk sharing (or resource allocation). Financial integration such as equity market liberalization enables risk sharing between domestic and foreign firms through cross-border portfolio holdings (Bekaert et al., 2005; Moshirian et al., 2021). Moreover, given that the fundamental purpose of financial liberalization is to allow free movement of various financial resources, liberalization permits resources to flow from places where they are abundant to where they are scarce (Henry, 2003). Reinhardt et al. (2013) show that among financially liberalized economies, capital flows from developed countries into less developed ones. If credit constraints depress investment in long-term projects (Aghion et al., 2010), then it is rational to expect that the increase in credit brought by liberalization will benefit long-term investment. 4 In addition, recent studies show that previously constrained firms react to better financing terms following the liberalization by investing more in technology, which corresponds to the resource reallocation effect (Varela, 2018; Wang, 2021). 5

The third channel is increased competition. This competition comes from two sources. The first is from initially constrained domestic firms because reduced capital constraints enable these firms to invest in innovative projects that could not be undertaken in the absence of liberalization (Aghion et al., 2005; Varela, 2018). The second is from the entrance of foreign firms, for example, through direct investment or merger and acquisitions (Deng, 2009; Walz, 1997). Through this pro-competitive channel, firms are likely to have higher innovation quality following liberalization. For example, research shows that the arrival of foreign entrants boosts domestic firms’ innovation quality (Aghion et al., 2009; Coelli et al., 2020). However, the innovation quantity effect remains ambiguous because competition is productivity destructive and the relation between competition and firm-level innovation is an inverted-U (Bento, 2014; Hashmi, 2013). 6

Taking the three above channels together, we expect a positive impact on firm patenting activities following capital account liberalization. Hence, our main hypothesis, stated in the alternative, is as follows:

External finance is one of the most important sources of firms’ R&D financing, and firms in R&D-intensive sectors are more likely to benefit from regulatory changes that bring financing and growth opportunities (Brown et al., 2013). Capital account liberalization provides opportunities that attract foreign capital to the domestic market and enable firms to directly invest in other countries as they search for new growth opportunities (Henry, 2007). Under fierce competition from both domestic and foreign entrants, firms in innovation-intensive sectors tend to respond rapidly to market liberalization (Moshirian et al., 2021). Therefore, we predict that capital account liberalization benefits firm innovation more for firms in high innovation-intensive industries. Hence, our next hypothesis, stated in the alternative, is as follows:

Studies also document that the impact of capital account liberalization depends on a given country’s legal environment, which in turn affects the composition of foreign portfolios (Benhabib & Spiegel, 2000; Mendoza et al., 2009). Lane (2013) found that financial globalization amplified the crisis for some countries but provided a buffer against the crisis for others. As such, Lane (2013) concluded that financial openness can positively affect risk sharing and efficient capital allocation if institutional support exists. Moreover, as documented in Desai et al. (2004), multinational firms are financed with less external debt in countries with underdeveloped capital markets or weaker creditor protection because of higher local borrowing costs. Overall, external shocks to capital flows will have a larger impact on innovation in countries with better legal environments (i.e., ones that encourage firm innovation activities). This leads to our second alternative hypothesis:

According to Melitz (2003), firms with better initial productivity are better prepared to take advantage of financial globalization. With better productive ability, these firms can benefit from liberalization by expanding their domestic and overseas businesses in response to lower capital barriers. Other firms are less likely to improve their operations during periods of liberalization. According to Aghion et al. (2005), firms with lower productivity are less motivated to innovate when they are faced with tighter competition within the industry. Therefore, our third alternative hypothesis is as follows:

Data

We measure a firm’s innovation output using patent data obtained from European Patent Office World Patent Statistical Database (hereafter, EPO PATSTAT). 7 This database contains information on patent assignees, patent family links, and patent citations, which facilitates the computation of different measures of innovation (see section “Firm-Level Innovation Variables” for a discussion of these measures). We collect firm-level financial data from Capital IQ Global and North America. One of the biggest obstacles faced by cross-country innovation studies is matching across different data sources because there are no common IDs. We address this challenge by employing the refined matching procedure proposed by Autor et al. (2020). Specifically, we match patent data from EPO PATSTAT to financial data from Capital IQ by both firm name and firm web URLs. 8

We then calculate sectoral indexes from publicly listed firms in the United States. Finally, we match several country-level measures that are used as control variables and partition measures from World Bank World Development Indicators (WDI), Global Financial Development database (GFD), UNCTAD World Investment Report, and several other data sources. We exclude firms from financial sectors (SIC 2-digit: 60-69) and restrict our study to firms that have the necessary data to compute the firm-level control variables. 9 Our final sample relies on the joint availability of innovation measures, financial variables, and the capital account liberalization index. It consists of 170,375 firm-year observations representing 17,331 nonfinancial firms from 41 countries from 1995 through 2013.

Firm-Level Innovation Variables

Following Balsmeier et al. (2017) and Bena et al. (2017), we use patent counts to measure firm innovation quantity. PATit represents the count of patent applications made by firm i in year t. Fortunately, EPO PATSTAT organizes patents in “patent families,” wherein each unique patent corresponds to a unique family identifier. Hence, in our estimation, each patent represents a unique invention. To measure patent quality, we follow Harhoff et al. (2003) and use two measures that are positively correlated with the value of patent rights: patent “family size” and patent citations. Patent “family size” is computed as the number of jurisdictions in which patent protection was sought for the same invention. 10 Patent citation is the total number of forward citations received by patent applications filed by the firm.

Similar to Balsmeier et al. (2017), Bena et al. (2017), and Luong et al. (2017), we address several concerns related to the innovation measures calculated using data from PATSTAT. First, we avoid truncation problems by using published patents and we calculate citations over the full post-publication sample period. Second, we avoid the double-counting problem by retrieving patents with a unique family ID. Third, we address the right skewness of patent count and citation distributions by winsorizing these variables at 1% and then using the natural logarithm of 1 plus the actual values to avoid losing firm-year observations with 0 patents or citations.

Capital Account Liberalization

We use an integrated capital account restrictions index—KA. This index is constructed by Fernández et al. (2016) based on the information from International Monetary Fund’s Annual Report on Exchange Arrangements and Exchange Restrictions. This is a de jure indicator of capital account restrictions in that it is based on officially designated policy reforms, so it is less susceptible to reverse causality issues common in panel regressions (Collins, 2007). 11 The index measures a country’s degree of financial openness based upon binary dummy variables that classify restrictions on cross-border financial transactions for 10 asset categories: equities, bonds, collective investments (also referred to as funds), derivatives, financial credits, commercial credits, real estate, direct investments, money market instruments, and guarantees, sureties, and financial backup facilities. We rescale the variable by using 1 minus the original index so that a value of 0 indicates full capital controls and a value of 1 indicates no restrictions on the overall capital account. 12 This index is available for an unbalanced panel of 100 economies from 1995 through 2013.

Control Variables

Following prior literature, we control for observable firm-level variables that are commonly found to effect innovation. Specifically, we control for firm age (ln(AGE)), firm size (ln(SALE)), capital expenditures (CAPEX), R&D expense (R&D), total property, plant, and equipment (PPE), book leverage (LEV), asset growth (GROWTH), return on assets (ROA), growth opportunities (TOBINS_Q), and financial constraints (WW). We also control for industry concentration (HHI and HHI2) to alleviate the concern that product market competition might have a nonlinear effect on firm innovation.

To control for the impact of lifting trade barriers on innovation, our regression includes a measure of a country’s trade openness (TradeOpen). We further control for country time-varying factors such as the country’s economic growth (GDPGrowth), government expenditures (GovExpense), and financial development (CreditGDP). Finally, we add country and industry (firm) fixed effects. Detailed variable definitions are provided in Online Table OA1.

Descriptive Statistics

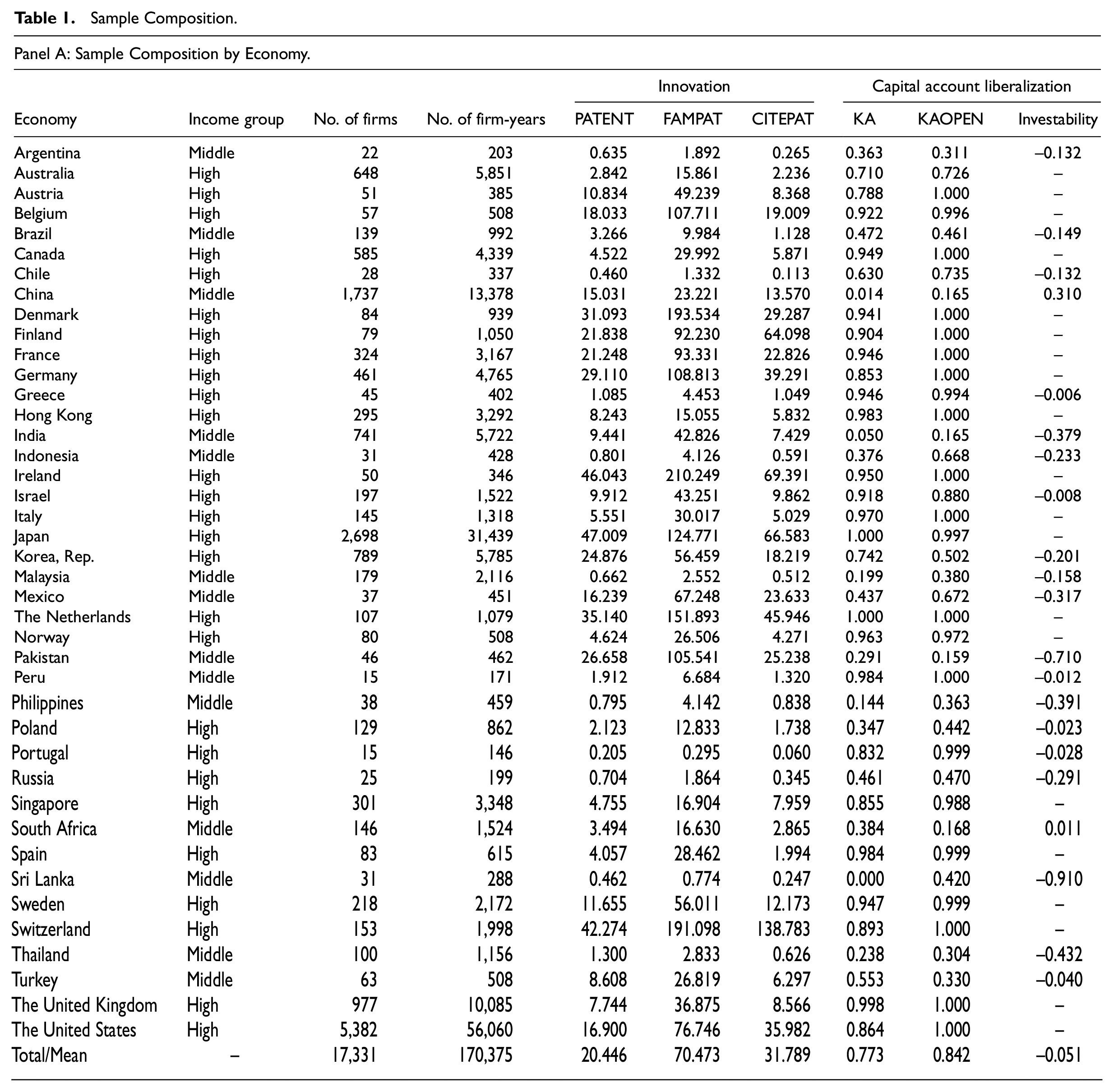

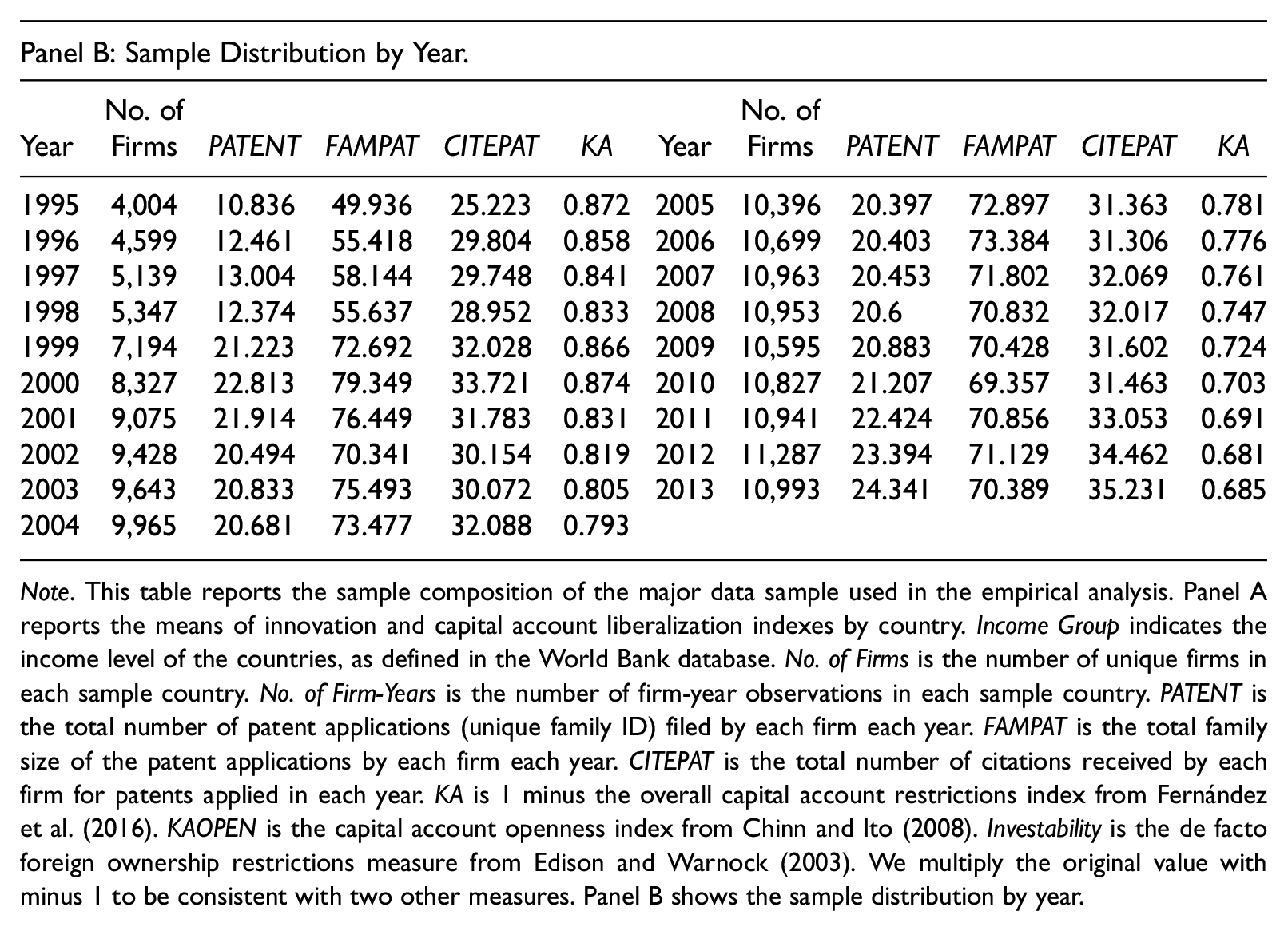

Panel A of Table 1 shows the means of innovation and capital account liberalization data by country. In total, the sample covers 41 different jurisdictions, with the United States having the largest number of firms (5,382), followed by Japan (2,698), China (1,737), and the United Kingdom (977). Only two economies, Peru and Portugal, provide fewer than 20 sample firms. Firms in Japan have the largest number of patents per year (47), followed by firms in Ireland (46), Switzerland (42), and the Netherlands (35). The pattern is mostly similar for patent family size and citations. On average, a firm in a high-income economy has more patents and citations than a firm in an emerging economy. Regarding capital account liberalization, high-income economies have higher values on average. As shown in Panel B, firms in the sample register more patents over time, from an average of 11 patents per firm in 1995 to an average of 24 patents per firm in 2013. Year and technology class adjusted citations (CITEPAT) also exhibit a slight increase over the sample period. 13

Sample Composition.

Note. This table reports the sample composition of the major data sample used in the empirical analysis. Panel A reports the means of innovation and capital account liberalization indexes by country. Income Group indicates the income level of the countries, as defined in the World Bank database. No. of Firms is the number of unique firms in each sample country. No. of Firm-Years is the number of firm-year observations in each sample country. PATENT is the total number of patent applications (unique family ID) filed by each firm each year. FAMPAT is the total family size of the patent applications by each firm each year. CITEPAT is the total number of citations received by each firm for patents applied in each year. KA is 1 minus the overall capital account restrictions index from Fernández et al. (2016). KAOPEN is the capital account openness index from Chinn and Ito (2008). Investability is the de facto foreign ownership restrictions measure from Edison and Warnock (2003). We multiply the original value with minus 1 to be consistent with two other measures. Panel B shows the sample distribution by year.

Table 2 presents the sample means and medians of the innovation measures, capital account liberalization indexes, and firm- and country-level characteristics. On average, each firm files 20 patents each year and receives 31 citations (adjusted) after publication of the application. The mean of the capital account liberalization index (KA) is 0.773, suggesting that, on average, countries in the sample have a high degree of openness in capital accounts. Regarding the firm-level variables, the mean and median of firm size (ln(SALE)) are 5.414 and 5.487, respectively; average R&D spending (R&D) is about 5.8% of total assets; the mean value of asset growth (GROWTH) is 19.6%; the average profitability measured by return on assets (ROA) is about 5.8%; and the average Tobin’s Q ratio (TOBINS_Q) is 1.907.

Descriptive Statistics.

Note. This table reports the summary statistics of main variables used in the empirical analysis. N is the total number of firm-year observations. Mean is the average value of each variable. Median is the median value of each variable. SD is the standard deviation of each variable. P25 is the lower quartile of each variable. P25 is the upper quartile of each variable. The sample period is from 1995 to 2013. Following the literature, all firm-level continuous variables are winsorized at 1% tails.

Capital Account Liberalization and Firm Innovation

Baseline Regression Results

To assess the impact of capital account liberalization on firm innovation, we estimate various forms of the following ordinary least squares (OLS) model at the firm level:

where i, j, c, and t refer to firm, industry, country, and year, respectively.

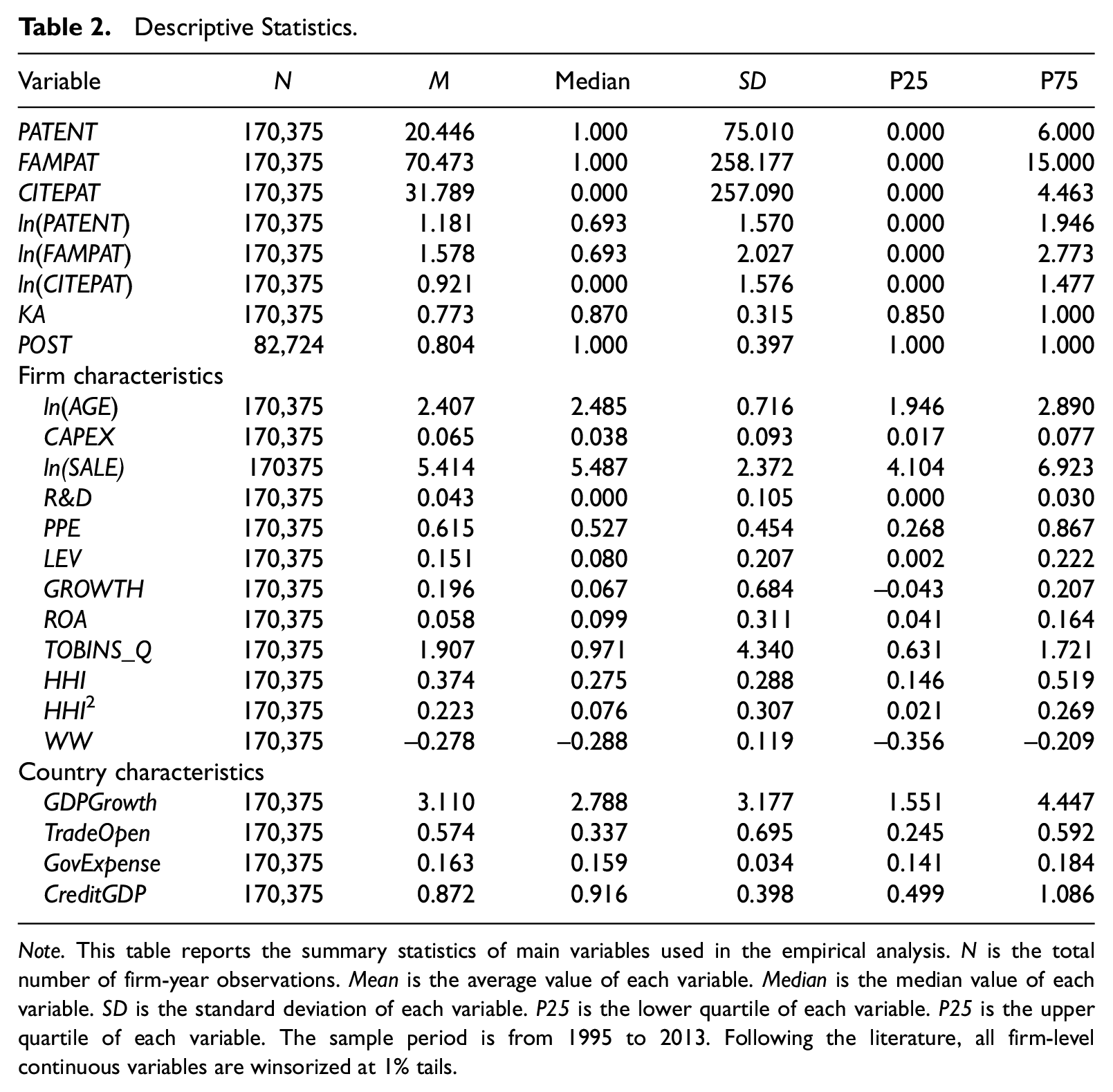

Table 3 presents the results from the baseline regression. Columns 1 through 3 report the results using three measures of innovation. The regression of firm innovation on KA in Column 1 yields a positive coefficient of 0.54, which is statistically significant at the 1% level. This positive association is consistent with H1a. The magnitude of impact is economically meaningful. Quantitatively, a 0.1-unit increase in the capital account openness index KA, from its mean of 0.77 to 0.87, is associated with a 5.4% increase in the number of patents registered by domestic firms, from the mean of 20 to 21 patents per year. We also present results for the impact of capital account liberalization on patent quality, as proxied by patent family size and patent citations, in Columns 2 and 3. As reported, the estimated coefficients on KA are all positive and statistically significant at the 1% level using either of the patent quality measures. 15

Baseline Regressions.

Note. This table reports the overall impacts of capital account liberalization on firm innovation. The main independent variable is the capital account liberalization (KA) index from Fernández et al. (2016). The higher the index, the more open a country’s capital account is. Columns 1 to 3 show the pooled ordinary least squares (OLS) (country, industry, and year FE) regression results on total number of patents ln(PATENT), patent family size ln(FAMPAT), and patent citations ln(CITEPAT). Following the prior literature, all explanatory variables are lagged by 1 year. For brevity, all variables are defined in Online Table OA1. Standard errors in parentheses are robust to heterogeneity and clustered by country and year. FE = fixed effect.

**, and * indicate significance at 1%, 5%, and 10% levels, respectively.

For firm-level control variables, the estimated coefficients on firm size are positive and significant, suggesting that larger firms tend to innovate more and receive more patent citations. Firms that spend more on R&D also tend to innovate more. In addition, firms that have higher leverage are associated with lower innovation output, whereas firms that have a higher return on assets are associated with less innovation. Financially constrained firms are associated with less innovation output. All of these results are generally consistent with previous studies (e.g., Bena et al., 2017; Luong et al., 2017).

For country-level control variables, the coefficient on GDPGrowth is negative and significant, consistent with the observation that high-income countries (with low GDP growth) exhibit a higher level of innovation output. Government expenditure is negatively related to firm innovation. Financial development is positively associated with innovation. However, there is no clear relation between trade openness and innovation because the coefficients on trade openness are insignificant. Overall, our results support H1a—that there is indeed a real impact on firm innovation from the removal of capital controls.

Identification: Innovation Intensity

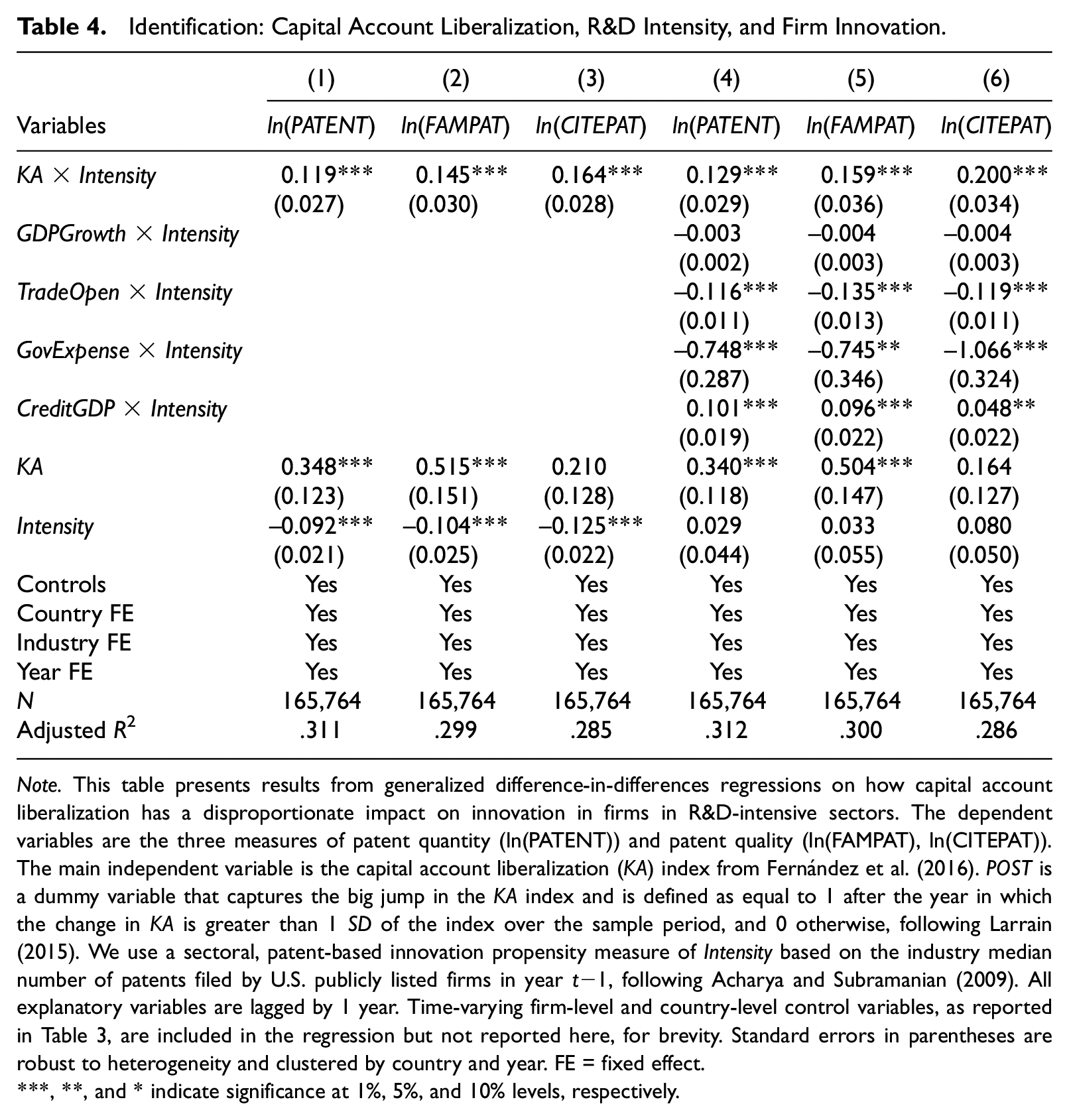

Prior empirical studies document that firms in innovation-intensive sectors are more likely to be influenced by macroeconomic changes in external capital because external equity and debt are major sources for financing innovation (Acharya & Subramanian, 2009; Moshirian et al., 2021). To examine whether the positive effect of capital account liberalization on firm innovation differs in sectors with different levels of innovation intensity, we add an interaction between the innovation intensity measure and capital account liberalization.

Table 4 presents the results. Columns 1 through 3 report the results with only one interaction term

Identification: Capital Account Liberalization, R&D Intensity, and Firm Innovation.

Note. This table presents results from generalized difference-in-differences regressions on how capital account liberalization has a disproportionate impact on innovation in firms in R&D-intensive sectors. The dependent variables are the three measures of patent quantity (ln(PATENT)) and patent quality (ln(FAMPAT), ln(CITEPAT)). The main independent variable is the capital account liberalization (KA) index from Fernández et al. (2016). POST is a dummy variable that captures the big jump in the KA index and is defined as equal to 1 after the year in which the change in KA is greater than 1 SD of the index over the sample period, and 0 otherwise, following Larrain (2015). We use a sectoral, patent-based innovation propensity measure of Intensity based on the industry median number of patents filed by U.S. publicly listed firms in year t−1, following Acharya and Subramanian (2009). All explanatory variables are lagged by 1 year. Time-varying firm-level and country-level control variables, as reported in Table 3, are included in the regression but not reported here, for brevity. Standard errors in parentheses are robust to heterogeneity and clustered by country and year. FE = fixed effect.

**, and * indicate significance at 1%, 5%, and 10% levels, respectively.

Overall, industry-level innovation intensity plays a role in explaining how capital account liberalization influences firm innovation. According to Acharya and Subramanian (2009), the country-level analysis looks at the aggregate effect, whereas the sectoral analysis identifies the underlying mechanism. Consequently, this evidence reveals that innovation-intensive sectors respond more to capital account liberalizations in terms of firm innovation output.

Additional Analyses

In this section, we explore how capital account liberalization promotes firm innovation by testing possible underlying economic mechanisms: legal protection and productivity.

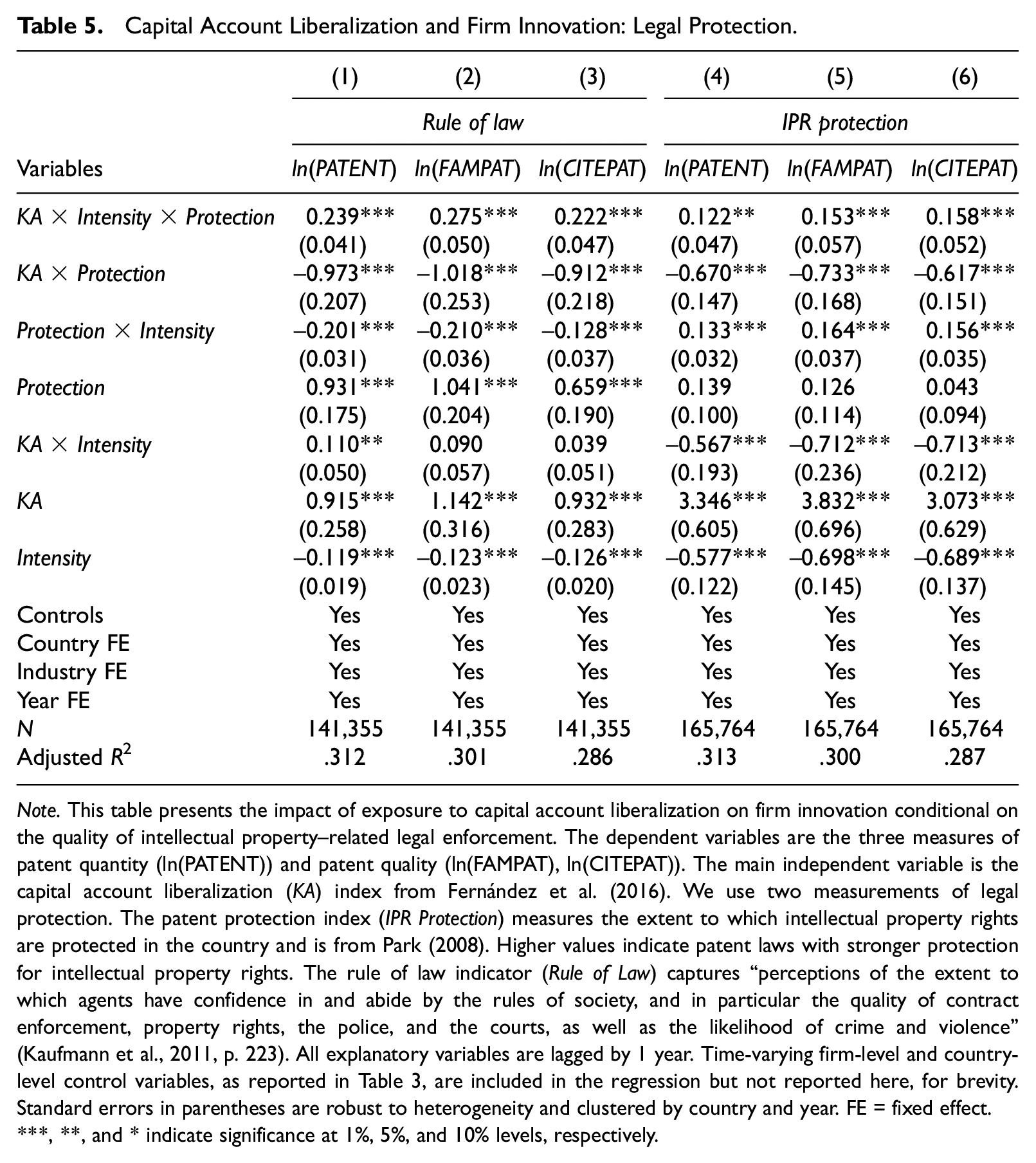

Legal Enforcement

Prior literature indicates that institutional environments are important for innovation (Guellec & Van Pottelsberghe, 2004; Levine et al., 2017). To investigate whether the impact of capital account liberalization on firms’ innovation varies in the quality of institutional environments, we consider two commonly used measures of a country’s legal environment that are closely related to patenting activity. Taken from Park (2008), the patent protection index (IPR Protection) measures the extent to which intellectual property rights are protected in a country. Higher values indicate patent laws with stronger intellectual property rights. The rule of law indicator (Rule of Law) captures perceptions of the extent to which agents have confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence. (Kaufmann et al., 2011, p. 223)

We introduce three-way interactions among KA, patent intensity, and legal protection proxies in the regression. The estimation results are shown in Table 5. Across all specifications, the coefficient estimates on the triple interactions are positive and significant. This indicates that capital account liberalization benefits firms’ innovation output, especially for firms from countries with higher property rights protection or countries with better rule of law.

Capital Account Liberalization and Firm Innovation: Legal Protection.

Note. This table presents the impact of exposure to capital account liberalization on firm innovation conditional on the quality of intellectual property–related legal enforcement. The dependent variables are the three measures of patent quantity (ln(PATENT)) and patent quality (ln(FAMPAT), ln(CITEPAT)). The main independent variable is the capital account liberalization (KA) index from Fernández et al. (2016). We use two measurements of legal protection. The patent protection index (IPR Protection) measures the extent to which intellectual property rights are protected in the country and is from Park (2008). Higher values indicate patent laws with stronger protection for intellectual property rights. The rule of law indicator (Rule of Law) captures “perceptions of the extent to which agents have confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence” (Kaufmann et al., 2011, p. 223). All explanatory variables are lagged by 1 year. Time-varying firm-level and country-level control variables, as reported in Table 3, are included in the regression but not reported here, for brevity. Standard errors in parentheses are robust to heterogeneity and clustered by country and year. FE = fixed effect.

**, and * indicate significance at 1%, 5%, and 10% levels, respectively.

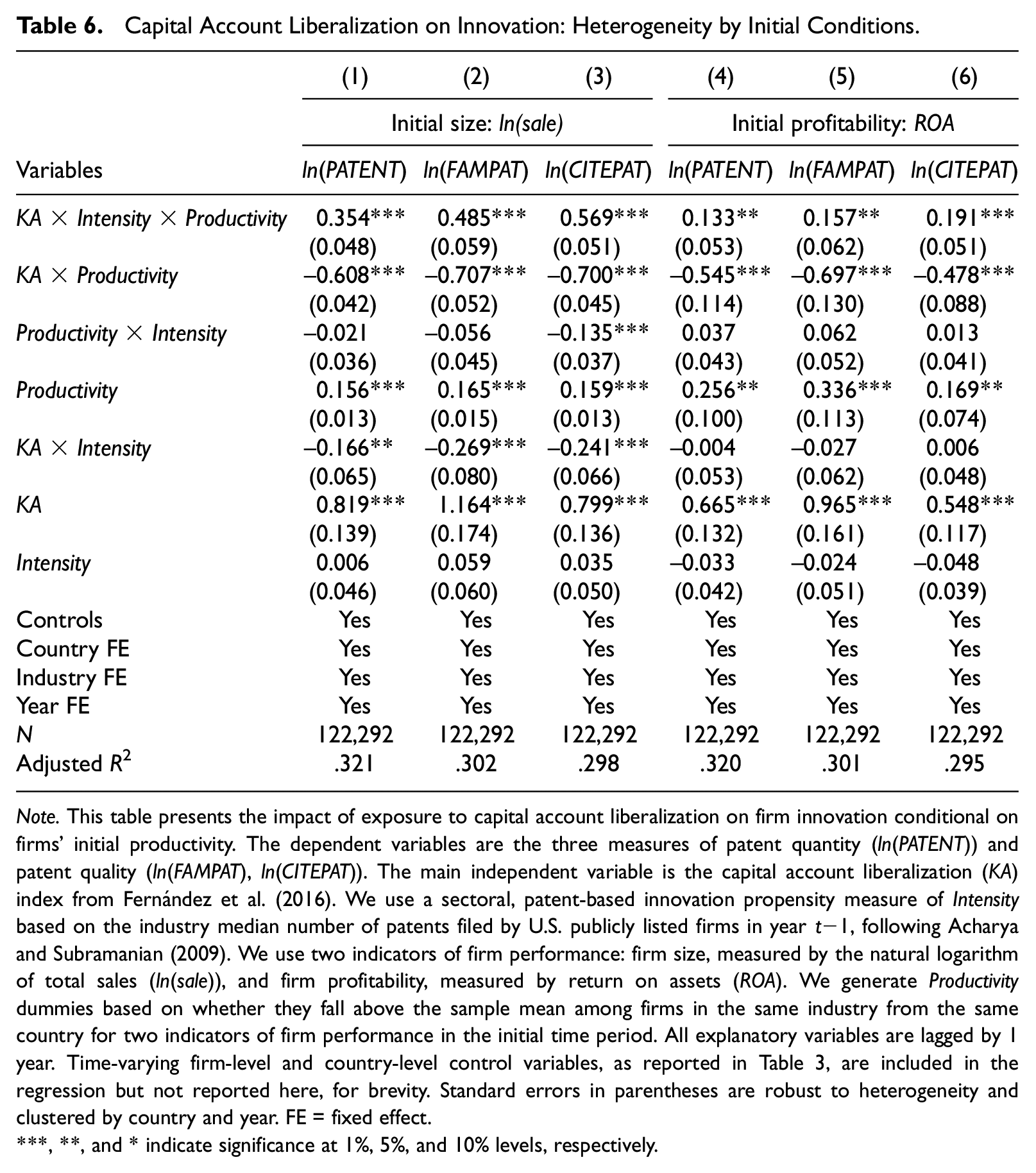

Initial Productivity

We next explore whether the impact of capital account liberalization on firm innovation is more positive for firms that are already more productive prior to liberalization. 17 In Table 6, we examine the impact of capital account liberalization on firm patenting when we separate firms into subsamples based on their initial productivity. We use two indicators of initial firm performance: firm size, proxied by the natural logarithm of total sales (ln(sale)), 18 and firm profitability, proxied by return on assets (ROA). We then introduce three-way interactions among liberalization, patent intensity, and initial productivity in the regression. All regression results convey that firms from innovation-intensive sectors with a higher initial firm size (Columns 1–3) and higher initial profitability (Columns 4 and 5) experience a larger increase in patenting activities for a comparable increase in exposure to capital account liberalization, relative to their less productive counterparts.

Capital Account Liberalization on Innovation: Heterogeneity by Initial Conditions.

Note. This table presents the impact of exposure to capital account liberalization on firm innovation conditional on firms’ initial productivity. The dependent variables are the three measures of patent quantity (ln(PATENT)) and patent quality (ln(FAMPAT), ln(CITEPAT)). The main independent variable is the capital account liberalization (KA) index from Fernández et al. (2016). We use a sectoral, patent-based innovation propensity measure of Intensity based on the industry median number of patents filed by U.S. publicly listed firms in year t−1, following Acharya and Subramanian (2009). We use two indicators of firm performance: firm size, measured by the natural logarithm of total sales (ln(sale)), and firm profitability, measured by return on assets (ROA). We generate Productivity dummies based on whether they fall above the sample mean among firms in the same industry from the same country for two indicators of firm performance in the initial time period. All explanatory variables are lagged by 1 year. Time-varying firm-level and country-level control variables, as reported in Table 3, are included in the regression but not reported here, for brevity. Standard errors in parentheses are robust to heterogeneity and clustered by country and year. FE = fixed effect.

**, and * indicate significance at 1%, 5%, and 10% levels, respectively.

Finding more positive innovation shocks from capital account liberalization for more productive firms is broadly consistent with extant studies (e.g., Aghion et al., 2005; Autor et al., 2020; Melitz, 2003). In a recent study using data from French firms, Aghion et al. (2018) showed that, in terms of manufacturing firms’ patenting activity, more productive corporations respond more positively to export-demand shocks. This outcome is consistent with our findings that firms with higher initial productivity seem to be more responsive to capital shocks and are more likely to take advantage of the innovation opportunities brought about by liberalization.

Robustness Check

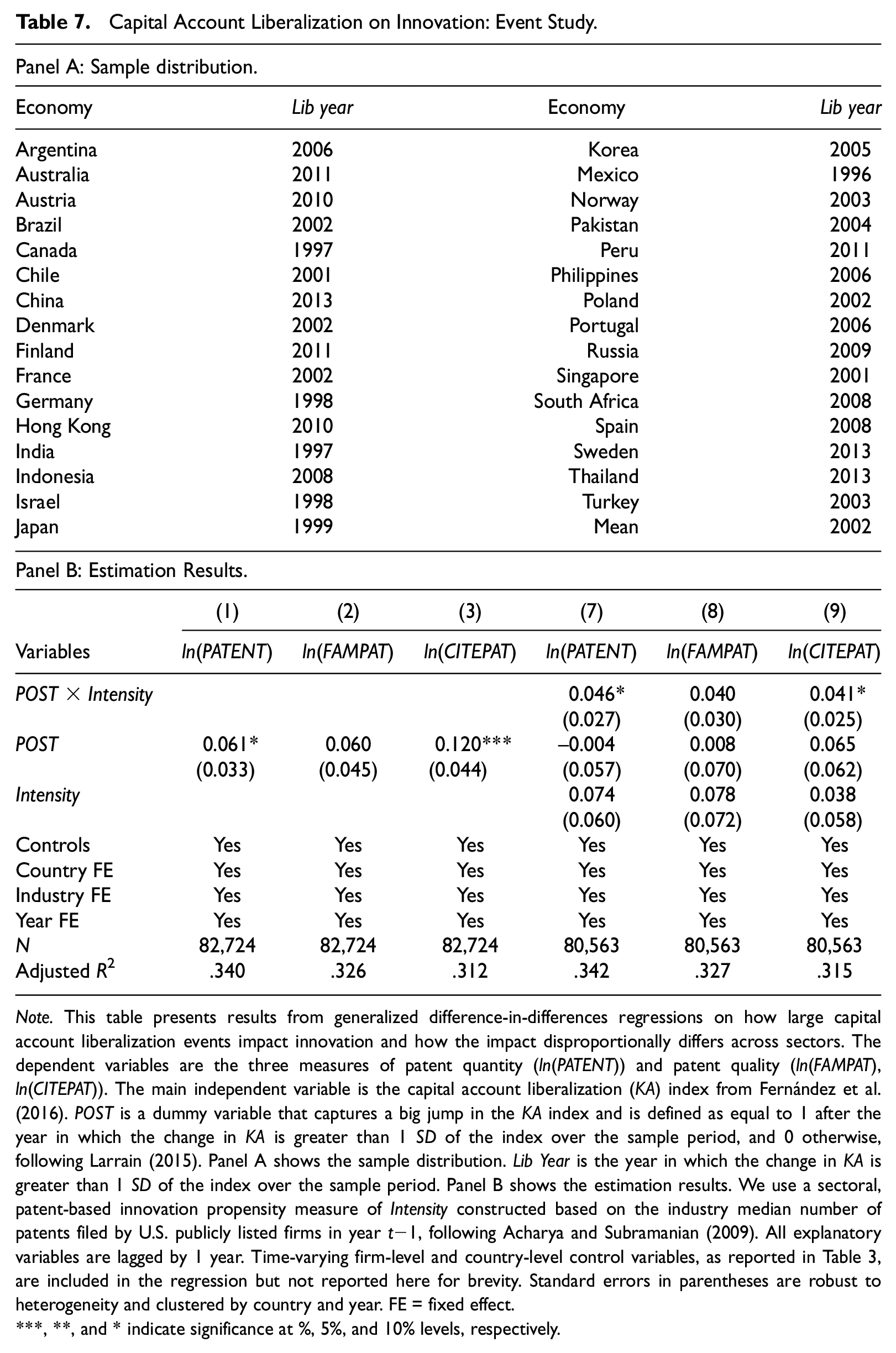

Event Study

As we mentioned previously, our continuous measure of capital account liberalization index does not provide a timeline of the impact on innovation. Therefore, we replace the continuous KA index with an alternative measure, POST, in the baseline regression. This captures large jumps and major events in the liberalization process. Following Larrain (2015), we identify the opening date as the year in which a 1 SD increase happened in the continuous KA index (presented in Panel A of Table 7). The POST dummy equals 1 if an observation is at or after the liberalization year, and 0 otherwise. The mean of POST dummy is 0.804, indicating that about 20% of the sample observation is in the pre-opening period. 19 The results in Panel B reveal that the effect of liberalization on patent counts and citations is positive and significant at the 10% level. For example, patent counts increase about 6.1% after the capital account opening year. We also observe positive and significant coefficients on the POST×Intensity interaction.

Capital Account Liberalization on Innovation: Event Study.

Note. This table presents results from generalized difference-in-differences regressions on how large capital account liberalization events impact innovation and how the impact disproportionally differs across sectors. The dependent variables are the three measures of patent quantity (ln(PATENT)) and patent quality (ln(FAMPAT), ln(CITEPAT)). The main independent variable is the capital account liberalization (KA) index from Fernández et al. (2016). POST is a dummy variable that captures a big jump in the KA index and is defined as equal to 1 after the year in which the change in KA is greater than 1 SD of the index over the sample period, and 0 otherwise, following Larrain (2015). Panel A shows the sample distribution. Lib Year is the year in which the change in KA is greater than 1 SD of the index over the sample period. Panel B shows the estimation results. We use a sectoral, patent-based innovation propensity measure of Intensity constructed based on the industry median number of patents filed by U.S. publicly listed firms in year t−1, following Acharya and Subramanian (2009). All explanatory variables are lagged by 1 year. Time-varying firm-level and country-level control variables, as reported in Table 3, are included in the regression but not reported here for brevity. Standard errors in parentheses are robust to heterogeneity and clustered by country and year. FE = fixed effect.

**, and * indicate significance at %, 5%, and 10% levels, respectively.

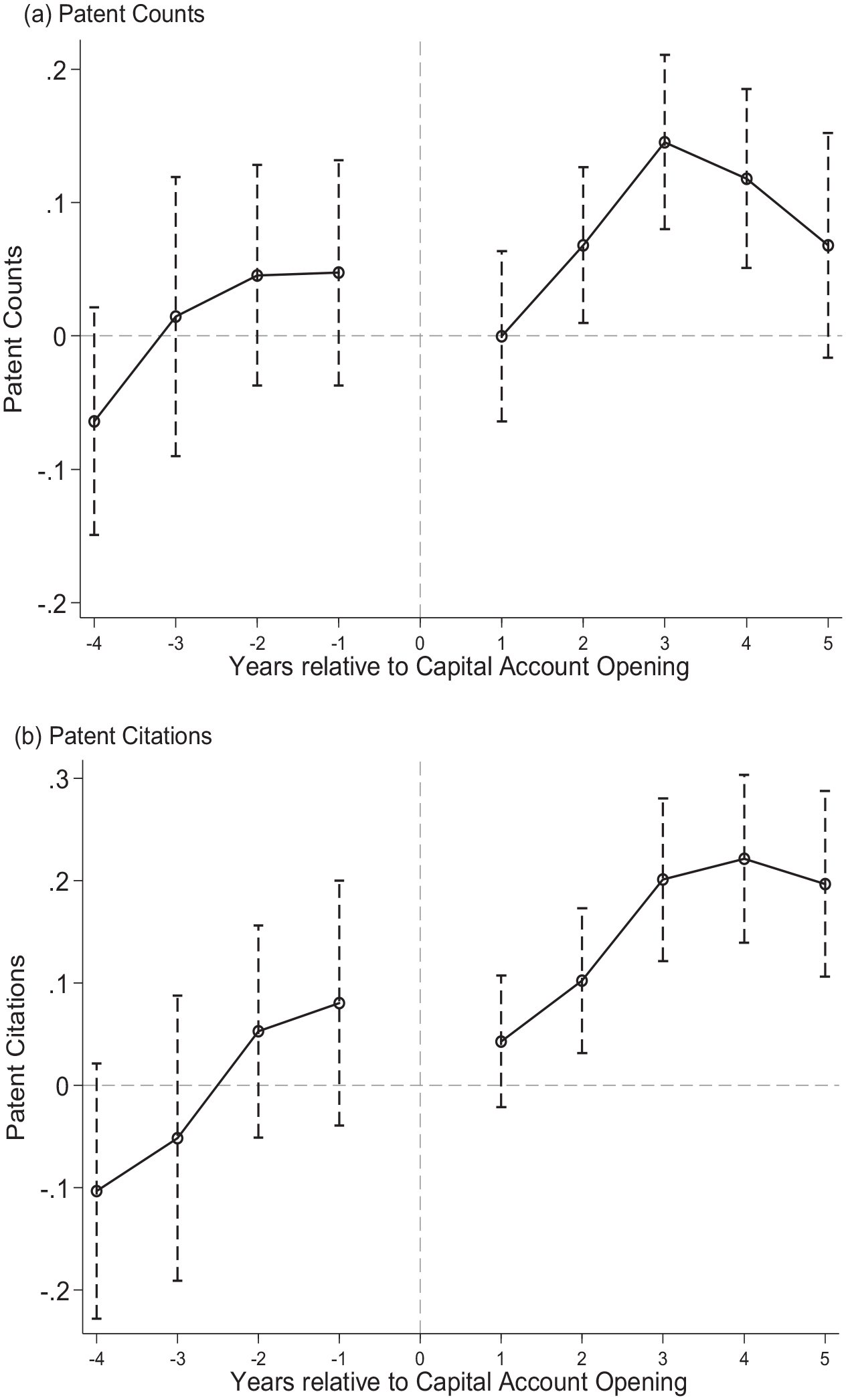

Next, we trace the year-by-year dynamics of the impact of capital account liberalization on firm innovation. We follow Larrain (2015) and include a series of dummy variables in Equation 1, such that each dummy variable captures the pre- and post-year effect of opening on innovation in a different year:

where

Figure 1 plots the coefficient estimates and the corresponding 95% confidence intervals, adjusted for country and year clustering, for (a) patent counts and (b) patent citations. The coefficients on all pre-event dummies are not significant, but the coefficients on the post-opening dummies become significant and positive 2 years after opening. In addition, the effect lasts for at least 5 years. Overall, these results trace the dynamic effect of opening over the years.

Dynamics effect of capital account opening on firm innovation: (a) patent counts and (b) patent citations.

Decomposing the Capital Account Liberalization Index

Because firms generate new patents in different ways (e.g., internal resource allocation, external knowledge spillover), capital inflows and outflows could have different effects on firm innovation. We therefore decompose the capital account liberalization index into inflows and outflows as well as sub-indices. For brevity, we report the findings in Online Table OA3. We observe significant coefficients on both Capital Inflow and Capital Outflow, as well as on their interactions with Intensity. This suggest that both capital inflows and outflows give rise to firm innovation. However, the coefficients on Capital Inflow are generally larger than those on Capital Outflow (e.g., 0.532 vs. 0.365 when regressing on patent counts), indicating that the positive impact of capital inflows on innovation is greater than the positive impact of capital outflows. In fact, if we introduce these two indices at one time into the regression, we observe that our baseline results are mainly driven by liberalization of capital inflows. This supports prior literature that finds that by allowing free movement of capital and repatriation of profits, capital flows contribute to domestic long-run economic growth (Albuquerque, 2003; Igan et al., 2020; Levine, 1997; Zeev, 2017).

Moving to the asset subcategories, we find some evidence that liberalization of money market, collective investments (funds), derivatives, and commercial and financial credit inflows have a positive impact on innovation. This finding is consistent with evidence of the increasing importance of fund investment, derivatives, and credit investment in alleviating financing frictions in international capital markets (Bena et al., 2017; Caballero et al., 2019; Coppola et al., 2021). We do not detect a significant, positive impact of equity inflow or other asset categories on innovation. 20 However, we do observe positive and significant coefficients when we interact innovation intensity with all asset subcategories, suggesting that compared with other sectors, firms from innovation-intensive industries respond more to these investments. In general, these findings are consistent with our cross-sectional results because investments in funds, credits, and money markets are normally made by sophisticated foreign investors who are likely to be very selective about the investment environment (Benhabib & Spiegel, 2000; Mendoza et al., 2009), have a high demand for good corporate governance (Bae & Goyal, 2010; Luong et al., 2017), and prefer large firms with stable productivity (Dahlquist & Robertsson, 2001).

Other Robustness Tests

We conduct a series of robustness checks which show that our findings are robust to various specifications. For brevity, we present the results in Online Table OA4. We first attempt to address the omitted correlated variable issue by controlling for possible confounding factors: the level of economic development (Luong et al., 2017), stock market development (Hsu et al., 2014), change in creditor rights protection (Acharya & Subramanian, 2009), stock market liberalization (Bekaert et al., 2005), inflows and outflows of foreign direct investment (Walz, 1997), the patent rights protection index (Aghion et al., 2015), and insider trading law enforcement (Levine et al., 2017). Our main inferences are robust to controlling for these variables. 21 We then show that our baseline regression results are robust to different combinations of firm, country-year, and industry-year fixed effects. The robust estimates help to alleviate the concern that firm-specific, country-level, or industry-level time-varying characteristics are driving our results.

We also find that our inferences are robust when we use (a) several alternative innovation measures, including patent generality, originality, citations per patent, cited foreign patents, and R&D spending; (b) two alternative measures of capital account liberalization to estimate the baseline regression—KAOPEN, the financial openness index from Chinn and Ito (2008), and Investability, liberalization of foreign ownership restrictions from Edison and Warnock (2003); and (c) two alternative measures of innovation intensity from Levine et al. (2017)—R&D Intensity, the average two-digit SIC industry level of annual growth in R&D expenses of U.S. publicly listed firms, and Innovate Propensity, the innovation propensity measured as the two-digit SIC industry-level average number of patents filed by U.S. publicly listed firms. Taken together, our main conclusion that capital account liberalization promotes firm innovation is robust to various estimation models, alternative measures, and specifications.

Subsample Analyses

We further look at subsets of countries with particular capital market constraints to refine our analyses and generate additional results. For brevity, we report the estimated results in Online Table OA5. In these subsample analyses, we find that the coefficients on capital account liberalization are slightly larger for firms from emerging markets compared with those from developed economies, but the differences are not statistically significant. We also observe that the effect of liberalization on innovation is statistically significant for firms from Europe (including countries from the former Soviet Union) and East Asia Pacific, but not significant in America (North and Latin America) or other regions. These results suggest that capital account liberalization benefits innovation in relatively less economically developed but rapidly growing markets. We also show that the main effects remain robust when we exclude specific countries including the United States, China, and countries that do not experience variations in liberalization, suggesting that our findings are not driven by these countries or country groups.

We next present results based on subsamples comprised of either pure domestic firms or firms with foreign exposure. Desai et al. (2008) showed that multinational affiliates tend to have a superior ability to overcome financial constraints compared with local firms. This finding implies that capital controls—especially on inflows—could be less important for multinational firms that have been exposed to foreign investment shocks prior to liberalization (Luo, 2003). Consequently, we predict that firms less exposed to foreign investment shocks tend to benefit more from the liberalization of capital account inflows. Consistent with our conjecture, for pure domestic firms, the coefficient estimates on the liberalization of capital inflows are positive and significant, and are stronger than those on outflows, whereas the results are insignificant for firms that are either cross-listed abroad or have foreign segments. 22

Finally, we conduct a subsample analysis focusing on firms with high innovation efficiency in highly innovative sectors. This test helps us to verify one assumption in the hypothesis. As argued, liberalization brings new financing opportunities to innovative firms. However, patenting activity creates better access to financing at the firm level, such that financing availability feeds further innovation. Thus, we expect that highly innovative firms patent and finance more after liberalization. We observe significant and positive coefficients on the interaction between KA and high innovation efficiency, whereas the coefficients on KA alone are significantly negative. This outcome suggests that firms with high innovation efficiency from innovative sectors contribute to our main finding.

Concluding Remarks

This article empirically investigates the impact of capital account liberalization on firm innovation. We construct a novel international firm-patent panel data and find that capital account liberalization is associated with higher patenting activity. More importantly, by employing a generalized DiD estimation framework and exploiting within-country variation in innovation intensity at the industry level, we show that the effects are more pronounced for firms in more innovation-intensive sectors. Furthermore, in more innovation-intensive industries, firms with better legal protections and greater productivity respond more to the opening up of capital accounts by filing more patents. The observed innovation effect is not merely a “lawyer effect,” because the impact exists for various patent quality measures as well. Our results are robust to a battery of tests, including alternative measures of capital account liberalization, the inclusion of firm-level and country-level characteristics, and other specifications of the estimation model. Overall, our article provides robust firm-level evidence of the real economic effect of capital account liberalization globally.

These findings have meaningful implications for corporate investment and policy reform. As Henry (2007) pointed out, financial globalization leads to only transitory growth in a country’s economy, even in the fundamental neoclassical model setting. In contrast to most empirical studies, this article sheds light on the temporary effects of macro-level financial reforms that are ultimately reflected in the behavior of micro-level entities. Overall, financial integration can serve as a driving force that gives rise to domestic firms’ innovation growth, at least temporarily.

Supplemental Material

sj-docx-1-jaf-10.1177_0148558X211059401 – Supplemental material for Capital Account Liberalization and Firm Innovation

Supplemental material, sj-docx-1-jaf-10.1177_0148558X211059401 for Capital Account Liberalization and Firm Innovation by Fangfang Hou and Xinpeng Xu in Journal of Accounting, Auditing & Finance

Footnotes

Acknowledgements

We are grateful to two anonymous reviewers, Linda Myers (JAAF conference editor) and Bharat Sarath (the editor), Louis Cheng, Nan Yang, Jeffery Ng, Lan Yang, Ji-Chai Lin, Cheng Jiang (discussant), Zhiwei Wang (discussant), seminar participants at the Hong Kong Polytechnic University and Xiamen University, and conference participants at 2018 Summer Boot Camp of Corporate Finance and Financial Markets, 2018 World Finance & Banking Symposium, 2020 JAAF meetings, and 2020 China Accounting and Finance Review conference for helpful comments and useful suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Fundamental Research Funds for the Central Universities of China (20720201024). The views expressed herein are those of the authors and all errors are our own.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.