Abstract

Firms are increasingly adopting pro-lesbian, -gay, -bisexual, -transgender, inclusivity and diversity (LGBT-ID) policies for workforce management. This study develops a parsimonious, albeit complex, moderated-mediated framework by employing a panel dataset combining data from archival sources and involving a sample of predominantly large and publicly held firms from the USA between 2002 and 2018. The number of observations varied across variables with a minimum of 414 observations (corporate brand equity) and a maximum of 3,566 observations (self-reported LGBT-ID policy). This treatise demonstrates that adopting LGBT-ID policies positively impacts firms’ profitability. Moreover, pro-LGBT-ID policies during this specific period have a positive effect on corporate brand equity, which in turn affects firm profitability, indicating that brand equity plays a mediating role in the nexus between pro-LGBT-ID policies and firms’ financial performance. Furthermore, innovation intensity strengthens the relationship between pro-LGBT-ID policies and brand equity during the sample period of the study.

Introduction

Americans’ positive perception of the LGBT community, support for same-sex marriage, and acceptance of homosexuality have grown dramatically in recent decades (Shan, Fu, and Zheng 2017). In response to this trend as well as to the United Nation's policy for the promotion of fair treatment of the LGBT community, businesses have been increasingly incorporating workplace diversity issues into their strategic stance. Many firms now proactively employ lesbian, gay, bisexual, and transgender (LGBT) individuals as a means of demonstrating their corporate social responsibility. Businesses are now adopting pro-LGBT policies (hereafter “LGBT-ID”) in response to implicit and explicit pressures from various stakeholder groups, including customers, suppliers, lenders, and others (Hossain et al. 2020; Patel and Feng 2021; Shan, Fu, and Zheng 2017).

In view of this burgeoning phenomenon, scholars have begun investigating this societally consequential topic. These studies, although very few in number, have evaluated whether adopting LGBT-ID policies engenders any strategic benefit. Two strands of literature examining the effect of LGBT-ID policies have developed. The first comprises investigations of the financial implications of such policies for the firms that adopt them: the findings of these studies have been mostly mixed and occasionally conflicting (Johnston and Malina 2008; Pichler et al. 2018; Shan, Fu, and Zheng 2017), indicating that the relationship between these two factors is more complex than has been conceptualized in prior studies. The second strand of research consists of studies examining whether firms gain any nonfinancial benefits from incorporating LGBT-ID policies. Hossain et al. (2020) reported that adopting LGBT-ID policies positively affects firms’ innovation capabilities, which in turn improves these firms’ value. Patel and Feng (2021) found that LGBT-ID policies positively impacted customer satisfaction. The current study falls within the purview of the first strand of the literature.

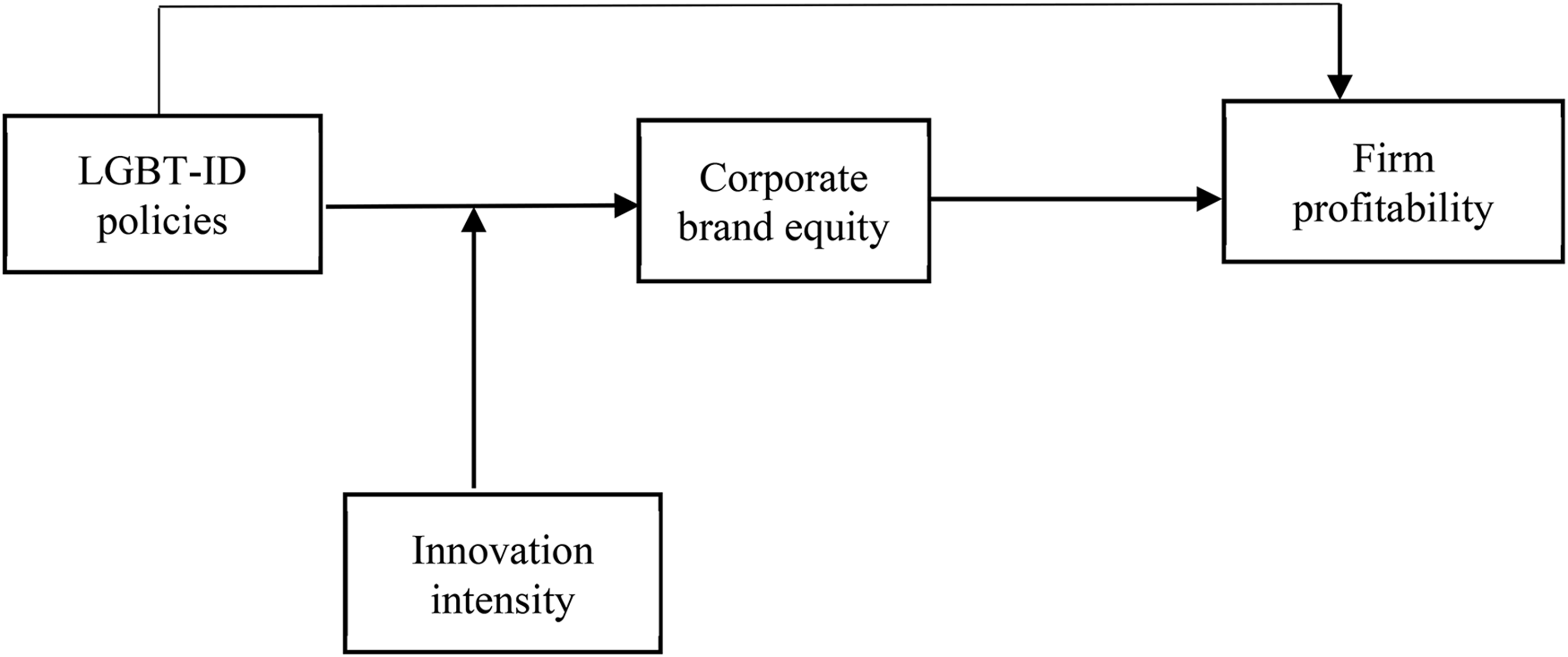

The mixed findings of prior studies have prompted scholars to underscore the need to develop a more complex theoretical model that incorporates mediating and moderating factors in exploring the link between LGBT-ID policies and firm performance (Patel and Feng 2021; Shan, Fu, and Zheng 2017). Indeed, very little is known about whether LGBT-ID policies directly and indirectly, in combination with innovation intensity and brand equity, enhance firm performance. Drawing on organizational justice theory (OJT) and instrumental stakeholder theory (IST), the current study develops a moderated mediational conceptual model (Fig. 1) and proposes that there are both direct and indirect links between LGBT-ID policies and firm profitability. To test the proposed conceptual model, this study employed a time-series, cross-sectional dataset involving a sample of large and publicly held firms from the USA during the period between 2002 and 2018. The number of observations across the variables studied in this research ranged between 414 (corporate brand equity) and 3,566 (self-reported LGBT-ID policy). This research empirically documents that during this time, LGBT-ID policies directly and positively affect firm profitability. Furthermore, this study demonstrates that the nexus between LGBT-ID policies and firm profitability is mediated by corporate brand equity, a market-based firm asset, in our sample firms during the specific time period. The relationship between LGBT-ID policies and corporate brand equity is further accentuated by the extent of a firm's innovation intensity during the sample period of the current study.

Conceptual model of the study.

This research makes three significant contributions. First, by combining propositions from OJT and IST, this study shows that during the sample period of the current study, firms used LGBT-ID policies as an instrument to represent themselves as fair and equitable in their treatment of LGBT employees to their various internal and external business-critical stakeholder groups. In other words, the data of the present study reveal that incorporating LGBT-ID policies helps firms attain organizational legitimacy, which increases profitability. Second, this study shows that incorporating LGBT-ID policies during the sample period of this study also positively impacts a firm's corporate brand equity and, in turn, its performance. Corporate brand equity thus mediates the link between LGBT-ID policies and firm profitability. Third, this study demonstrates that firms that deploy other germane firm-specific capabilities, such as innovation intensity, reap greater rewards in the form of strengthening their corporate brand when they incorporate LGBT-ID policies in their strategic stance during this period of time.

Literature Review

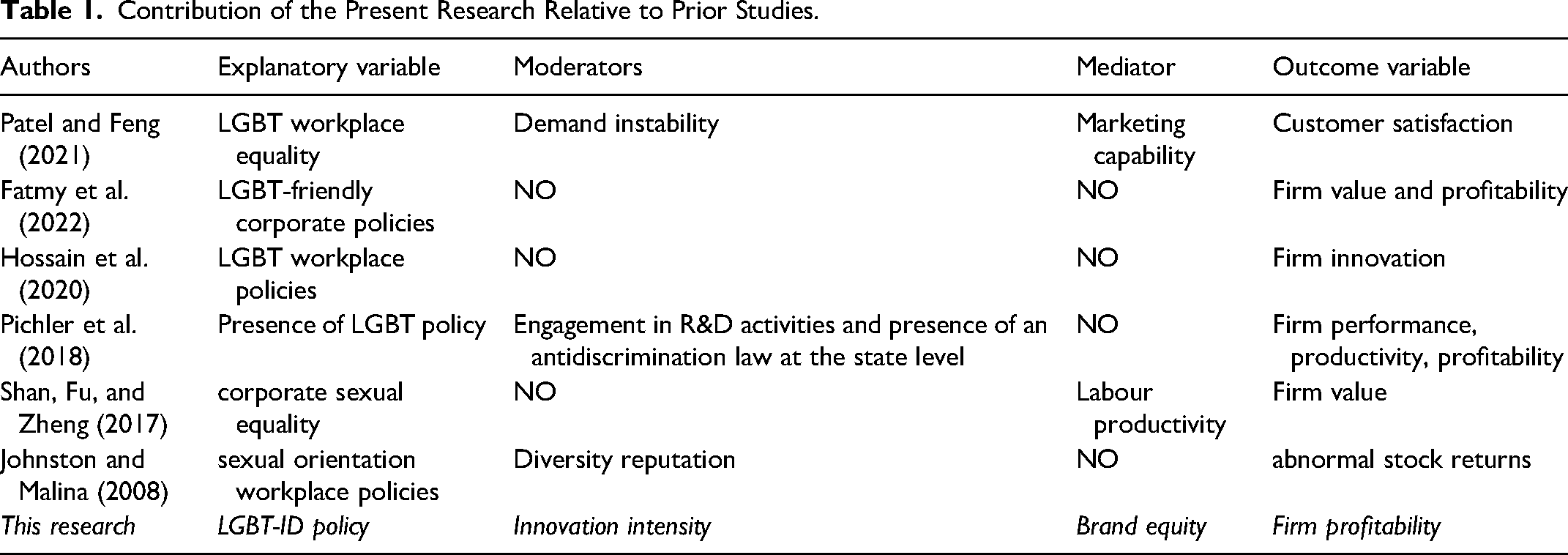

We searched extensively for relevant studies using pertinent keywords. All the pertinent studies are summarized in Table 1, which also shows how the current study adds to the existing body of knowledge. Only a handful of studies have examined the impact of pro-LGBT workforce policies on firms’ financial and nonfinancial performance (e.g., Hossain et al. 2020; Johnston and Malina 2008; Shan, Fu, and Zheng 2017). This meager body of literature has predominantly examined whether incorporating LGBT-ID policies into a firm's overall corporate strategy has any positive business implications.

Contribution of the Present Research Relative to Prior Studies.

As delineated in Table 1, prior relevant studies can be broadly classified into two categories. One strand of studies has explored the effect of adopting LGBT-ID policies on firms’ nonfinancial performance, i.e., firm innovation (Hossain et al. 2020; Patel and Feng 2021); the other has investigated the impact of such policies on a firm's financial performance, i.e., its value (Fatmy et al. 2022; Pichler et al. 2018; Shan, Fu, and Zheng 2017). While some studies examining the effect of LGBT-ID policies on financial performance have found it to be positive (Fatmy et al. 2022; Hossain et al. 2020; Shan, Fu, and Zheng 2017), others have reported that this effect is neutral, mixed, or insignificant (Johnston and Malina 2008; Pichler et al. 2018). These mixed findings, though produced by a small number of studies, imply that the impact of LGBT-ID policies on firm performance may be more complex than has yet been recognized.

In Section 3, we draw on OJT and IST to put forward a moderated-mediation conceptual model that encompasses corporate brand equity as a mediator and innovation intensity as a moderator in the relationship between LGBT-ID policies and firm profitability.

Theory and Hypotheses

Before we propose the hypotheses of this research (Figure 1), the fundamental tenets of OJT and IST are first briefly delineated below.

Organizational Justice Theory

Greenberg's (1987) OJT emphasizes employees’ perceived fairness within an organization. Perceptions of fairness are based on the processes (i.e., procedural and interactional justice) and outcomes (i.e., distributive justice) of the decisions implemented by an organization (Folger and Cropanzano 1998; Greenberg 1990). Organizational theorists extend interactional justice into two subcomponents: informational justice refers to providing candid explanations to employees, while interpersonal justice refers to treating employees with respect and dignity (Colquitt 2001; Colquitt and Shaw 2005). The notion of justice in an organization becomes evident in two phases. First, organizations must communicate and consult with the relevant employees when executing a decision; second, authorities must ensure that employees are fairly affected by the outcome of the decision (Greenberg 1987; Sheppard and Lewicki 1987). That is, organizations should (i) consider the viewpoints of others, (ii) have consistent decision-making criteria, (iii) be bias-free, (iv) provide timely feedback, and (v) effectively communicate the decision-making policies. Thus, the principles of organizational justice regulate the structure of organizations and distributive shares so that organizational procedures are both efficient and fair. Studies largely support the idea that perceived organizational justice influences employee satisfaction, commitment, and performance (e.g., Heffernan and Dundon 2016).

Instrumental Stakeholder Theory

IST explains how firms can gain a competitive advantage through effective stakeholder management (Harrison, Felps, and Jones 2019; Jones 1995). The theory suggests that firms need to design and execute strategies that will satisfy the relational obligations of various stakeholders to achieve a competitive advantage. Jones, Harrison, and Felps (2018) noted that sharing information among stakeholders (e.g., employees) facilitates knowledge transfer and productivity, which also provides firms with a competitive advantage. When the employees realize that sharing information benefits them, they feel a sense of closeness and more trust in the firm (Albu and Flyverbom 2019; Laplume et al. 2021; Schnackenberg and Tomlinson 2016). Laplume et al. (2021) suggest that an efficient flow of information creates transparency in the firm's operational and strategic directions and enhances the firm's reputation among the stakeholders. In particular, the functional departments of business organizations are strongly embraced with task and outcome interdependence, whereas collaborative sharing relationships are vital for incremental value creation (Jones, Harrison, and Felps 2018). This further creates a better understanding among the firm's stakeholders in terms of tailoring the deals (e.g., between the firm and employees/customers) and achieving the objectives. Thereby, employees better understand the market and can deliver ideas for new products and services within the industry. The impacts of knowledge-sharing and innovation advantage are often reflected in the firm's reputation, fairness, competitive position, and financial performance (Laplume et al. 2021; Tantalo and Priem 2016). In essence, IST postulates that firms proactively formulate and execute specific strategies aimed at building and bolstering relationships with diverse stakeholders, with the eventual goal of attaining performance-related outcomes (Rahman, Aziz, and Hughes 2020).

Hypotheses Development

LGBT-ID Policies and Firm Performance

Combining propositions from OJT and IST, we argue that firms proactively adopt and encompass LGBT-ID policies in their overall corporate strategy, with a view to gaining legitimacy among various stakeholders. Specifically, we postulate that firms use LGBT-ID policies as an instrument to promote the notion among diverse stakeholders that they are fair and equitable in their operations (Jamali 2008; Jones 1995; Rahman, Aziz, and Hughes 2020). This strategic stance is expected to impact firms’ profitability in multiple ways.

LGBT-ID corporate policies refer to firms’ overall policies in regard to proactively welcoming and accommodating employees with diverse sexual orientations (Patel and Feng 2021). Because such socially responsible firms do not discriminate against any social groups based on sexual orientation, they have more opportunities to recruit employees from a larger pool of candidates (Richard 2000; Shan, Fu, and Zheng 2017; Wettstein and Baur 2016). A heterogeneous workforce creates a tolerable and hospitable work environment that promotes employees’ comfort and confidence (Hossain et al. 2020; Shan, Fu, and Zheng 2017). As a reflection of perceived procedural and interpersonal justice, employees feel less job-related anxiety, improved psychological well-being, confidence in skills, improved teamwork, and higher job satisfaction (Griffith and Hebl 2002; Ragins, Singh, and Cornwell 2007). A stronger market-focused innovation capability thus encourages employees to exert more discretionary efforts and generate novel ideas to enhance problem-solving, boost service quality, and improve customer satisfaction. (Patel and Feng 2021; Shan, Fu, and Zheng 2017) In essence, an inclusive work environment enhances employee productivity, which, in turn, positively affects firm profitability (Hossain et al. 2020; Shan, Fu, and Zheng 2017).

Previous studies have shown that external stakeholders recognize diversity-friendly policies as a social commitment on the part of the firm. For instance, customers tend to prefer firms that demonstrate social and ethical responsibility by committing to act fairly toward sexual and racial minority groups (Richard 2000; see Webster et al. 2018 for a review). As a consequence of such cognitive and emotional identification with firms, socially conscious customers demonstrate a positive attitude toward and (re)purchase products from these firms (Li and Nagar 2013; Patel and Feng 2021). Enhanced customer—firm identification, ideological congruence, and perceived satisfaction thus make a firm more profitable (Bhattacharya and Sen 2004; Morgan, Slotegraaf, and Vorhies 2009; Pichler et al. 2018).

The cumulative impact of inclusion and diversity in the workforce is reflected in the firm's performance. For example, when firms adopt LGBT-friendly policies (e.g., same-sex domestic partner benefits), their profitability is increased as well (Li and Nagar 2013; Wang and Schwarz 2010). The impact of socially responsible behavior is also often evident in a firm's stock price (Alexander and Buchholz 1978; Jia, Gao, and Julian 2020) and fund performance (El Ghoul and Karoui 2017). Moreover, socially responsible policies increase both internal and external stakeholder engagement, reducing agency costs and providing firms with better finance access (Cheng, Ioannou, and Serafeim 2014). The business reporting practices (e.g., decision-making and operations) of firms with proactive social agenda are relatively more transparent, which reduces information asymmetry between socially responsible firms and other business-critical stakeholders, such as financial institutions and suppliers (Cho, Lee, and Pfeiffer 2013; Cui, Jo, and Na 2018; Holod and Peek 2007; Patel and Feng 2021). This transparency ensures that the affected stakeholders have the information they need to make decisions about firms, such as interest rates charged by lending institutions and credit terms offered by suppliers (Cho, Lee, and Pfeiffer 2013; Cui, Jo, and Na 2018; Holod and Peek 2007; Patel and Feng 2021). Reducing information asymmetry between pro-social firms and other trade partners also assists socially responsible firms in gaining an edge with their trade partners because such firms have a lower risk of non-payment and thus attract more potential trade partners (Bae, Chang, and Yi 2018; Cho, Lee, and Pfeiffer 2013; Cui, Jo, and Na 2018; Goss and Roberts 2011).

In sum, socially responsible firms with an LGBT-ID corporate policy attain employee productivity, attract a strong customer base, and gain enhanced support from external business-critical stakeholders. Taken together, a satisfied customer-base engenders a revenue advantage, and satisfied trade partners assist firms in conducting business operations on more favorable terms, which in turn creates a cost advantage for firms with a proactive LGBT-ID agenda. In view of the foregoing, the following baseline hypothesis is proposed:

LGBT-ID Policies and Corporate Brand Equity

Brand equity is defined as the additional value conferred on a product by a brand name compared to the value of similar products (Aaker 1996; Rahman, Rodríguez-Serrano, and Lambkin 2019). Studies show that increased brand awareness and incremental preference due to enhanced (non-) attribute perceptions are the key sources of brand equity (Juntunen, Juntunen, and Juga 2010; Srinivasan, Park, and Chang 2005). For instance, greater brand awareness and positive brand associations affect customers’ purchase behavior (Keller 1993; Netemeyer et al. 2004). Customers’ brand trust, combined with their affective commitment to and satisfaction with the brand, is often considered a key driver of brand equity (Baalbaki and Guzmán 2016; Keller 2002).

Past studies have suggested that corporate policies supporting heterogeneous workforces reduce work stress, psychological threats, and switching intentions among employees. Such positive work cultures promote employee satisfaction, labor productivity, and excellent customer service (Patel and Feng 2021; Shan, Fu, and Zheng 2017). In turn, customers develop a positive attitude and strong brand knowledge (i.e., brand awareness and brand image), as well as psychological proximity toward firms that accommodate diversity and equality (Armstrong et al. 2010). Strong brand association from external stakeholders provides firms with a strategic and competitive position in the market. Enhanced consumer—firm identification increases consumers’ purchase intentions (i.e., brand loyalty), which positively influences brand equity (Johnston and Malina 2008; Shan, Fu, and Zheng 2017).

In the context of the current research, we argue that adopting LGBT-ID policies strengthens brand equity. In particular, brand equity increases consistently following interactions between a firm and its stakeholders (Merz, He, and Vargo 2009; Wang and Sengupta 2016). This aligns with the combined notion of OJT and IST: maintaining a diverse workforce creates a talented pool of human capital, which contributes to enhancing both attribute and non-attribute perceptions of a firm's brand. Consequently, customers become more aware of the brand, feel a strong attraction to the brand's imagery, evaluate the brand positively and develop an emotional attachment to the brand (Keller 1993). Adopting LGBT-ID policies thus improves reciprocal coordination, knowledge sharing, and employee morale (Jones, Harrison, and Felps 2018). Combined with a higher customer—firm identification, delivery of the exceptional brand experience, customer information exchange, customer acquisition, and customer satisfaction, implementing LGBT-ID policies can directly and indirectly strengthen a firm's brand equity (Hossain et al. 2020; Jayachandran et al. 2005; Wang and Sengupta 2016). Therefore, the following hypothesis is proposed:

LGBT-ID Policies, Innovation Intensity, and Brand Equity

Innovation intensity refers to a firm's commitment, initiative, and activities designed to implement new ideas, products, processes, and services (Horbach, Rammer, and Rennings 2011; Liao and Tsai 2019). Strategic investment in innovation provides firms with competitive advantages within the context of cost efficiency and differentiations (Ambec and Lanoie 2008; Russo and Fouts 1997). Firms with a greater innovation intensity gain the dynamic capability of responding to changes in the business environment (McAlister, Srinivasan, and Kim 2007). Extant research provides empirical evidence that R&D expenditures aiming at innovation enhance a firm's sales, profitability, and market value (Choi and Williams 2014; Hall and Oriani 2006). Thompson and Heron (2006) argued that a firm's innovation capacity is influenced by its relational capital, which can be infused with pro-social activities. For instance, a diverse and talented workforce may fuel creativity, productivity, and innovative activities by integrating the internal and external information necessary to generate new ideas (Hossain et al. 2020; Tsai 2001). This argument aligns with the findings of Badgett, Waaldijk, and van der Meulen Rodgers (2019), who noted that LGBT inclusion encourages economic growth and development.

Referring to OJT and IST and their relevance to LGBT-ID policies, we contend that strong human capital is necessary to carry out innovation within a firm. A diverse workforce attracts more talent, enhances creativity, and increases productivity, which subsequently contributes to the operational and strategic decisions of the firm (Hossain et al. 2020; Laplume et al. 2021). Past studies have reported that employees who feel welcome within a diverse workforce feel a stronger connection and commitment to their employers; thus, workforce diversity enhances employee involvement and maximizes innovation (Shan, Fu, and Zheng 2017; Yang and Konrad 2011). Therefore, we also argue that firms that adopt LGBT-ID policies share relevant information with their stakeholders, and thus their employees better understand their strategic goals. This further encourages employees to take on challenges and put forward new ideas related to the firm's R&D and core competencies. Moreover, continuous innovations result in novel offerings in the market that create value for customers (Linder, Jarvenpaa, and Davenport 2003). Innovation intensity thus supports firms in gaining the trust and confidence of both internal and external stakeholders, which in turn augments their brand equity.

While diversity and inclusion in the workforce may strengthen a firm's resources and capacity, thereby reinforcing customers’ incremental preference and enhancing corporate brand equity (Wang and Sengupta 2016), some desired performance outcomes (e.g., price premium, market share) may not be evident due to poor technological capability, obsolete product design, and lack of differentiation. Efficient integration of LGBT-ID policies and innovation intensity is therefore essential. Thus, we argue that a firm with both stronger human capital and higher innovation intensity will have stronger corporate brand equity. Therefore, the following hypothesis is proposed:

LGBT-ID Policies, Brand Equity, and Firm Performance

Whereas the OJT emphasizes equity and fairness, the IST indicates that diversity and inclusion in the workplace strengthen firm performance. However, one can argue that establishing social and economic justice in an organization by implementing LGBT-ID policies and diversity alone may not warrant economic benefits for the firm (Chih, Chih, and Chen 2010; Jiraporn, Potosky, and Lee 2019; McWilliams and Siegel 2000). It is necessary to ensure that LGBT-ID policies are effectively operationalized to improve internal marketing resources, productivity, and competitiveness. Workplace diversity facilitates building a positive corporate image that has implications from the perspective of other stakeholders. For instance, customers develop a positive attitude toward firms that accommodate diversity and equality (e.g., Armstrong et al. 2010). The enhanced consumer-firm identification increases the consumers’ patronization intention, which positively influences the brand value of the firm (Johnston and Malina 2008; Shan, Fu, and Zheng 2017). Therefore, we posit brand equity as the transformational component through which LGBT-ID policies are strategically utilized and converted into quantifiable financial output. As discussed in relation to the development of H2, we reiterate that LGBT-ID policies are a strong source of brand equity. Furthermore, brand equity is a key driver of firm performance (Morgan, Slotegraaf, and Vorhies 2009; Wang and Schwarz 2010), as it reflects a brand's distinct position in the competitive market, as well as customers’ strong brand familiarity, brand association, and purchase behavior (Keller 1993). Strong brand equity can increase revenue and simultaneously decrease a firm's costs (Keller and Lehmann 2006). Firms with strong brand equity can maintain a committed customer base that not only ensures a consistent flow of revenue into business but also promotes the brand to others (through, for example, positive word-of-mouth, which may subsequently reduce the brand's advertising and promotional expenditures). Firms can capitalize on brand equity to leverage components such as brand commitment and loyalty to achieve marketing objectives at a lower cost (Simon and Sullivan 1993). Therefore, we postulate that utilizing and deploying LGBT-ID policies in combination with brand equity improves firm performance. In view of the foregoing, the following hypothesis is proposed:

Methodology

Model Specification

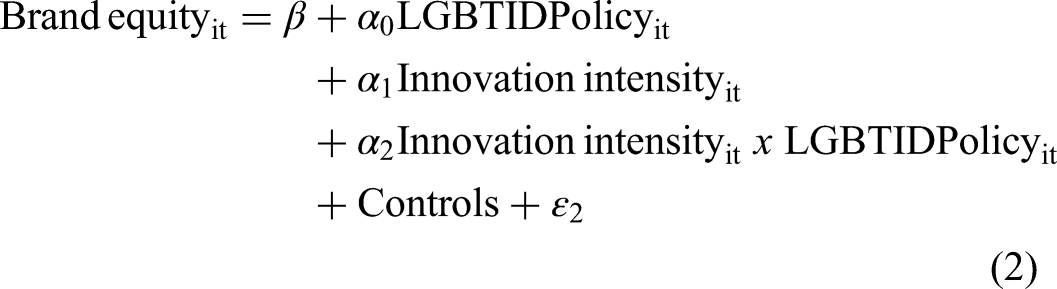

Investigating the mediational effect requires a system of equations, so we simultaneously developed a system of equations to examine the nexus between LGBT-ID policies, brand equity, innovation intensity, and firm profitability. Specifically, we followed the commonly recommended approach in similar research (Baron and Kenny 1986; Luo et al. 2015; Shaver 2005). This system of simultaneous equations (see Models 1–3 below) offers one salient advantage over separate equations. Because the variable ‘brand equity’ acts as both an independent and a dependent variable in different equations, endogeneity problems may arise, and the error terms in Models 2 and 3 are likely to be correlated. Such thorny issues can be ameliorated by estimating all the models simultaneously, as this can account for correlated errors and produce more efficient estimates with greater statistical efficiency.

Below, we delineate the equations developed to examine the relationships between the key variables of theoretical interest in this study. The first equation was used to explore the direct relationship between LGBT-ID policies and firm profitability:

Data Sources and Sample

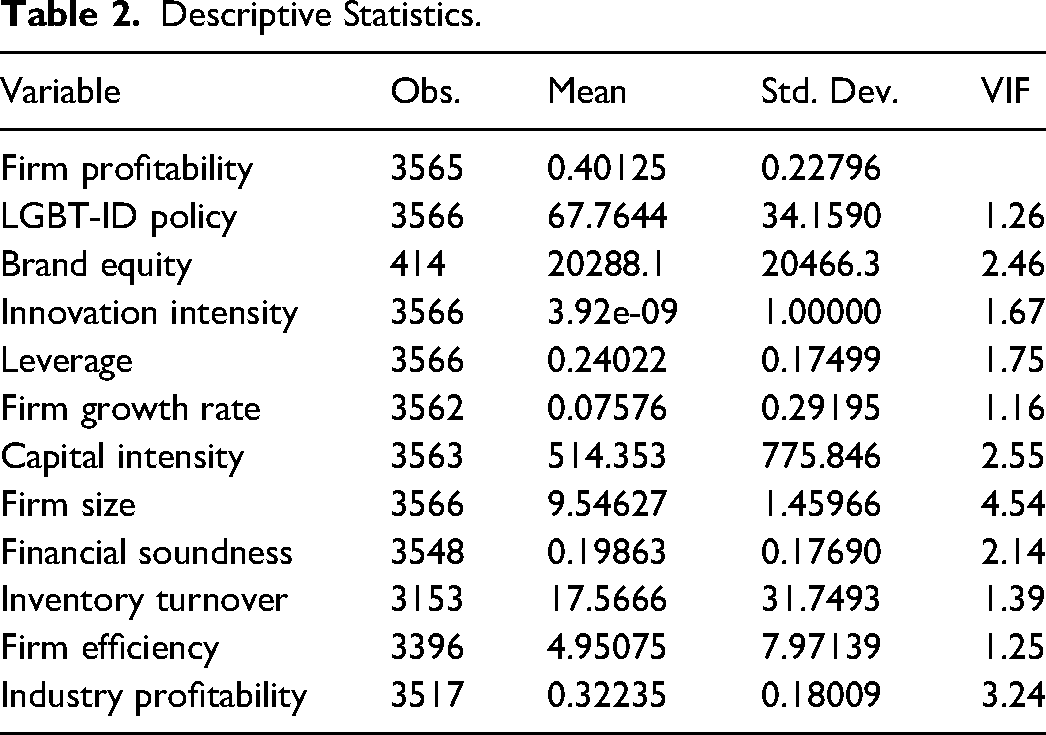

The sample period of this study was from 2002 to 2018. Data for this study were collected from multiple archival sources, which enabled this study to avoid common method bias. Data were collected in a series of steps. In the first step, data for the key explanatory variable, LGBT-ID policies, were collected from the Human Rights Campaign Foundation (www.hrc.org), which has been used as a reliable source of such data by numerous studies (Hossain et al. 2020; Patel and Feng 2021; Shan, Fu, and Zheng 2017). The HRC, which is the largest LGBT civil rights organization in the United States, rates large U.S.-based companies on a scale (from 0–100) according to how these firms treat their LGBT employees and consumers. HRC conducts survey on a yearly basis among the large USA-based companies and rates the firms based on the information provided by the participating firms (self-reported data shared by the firms). However, non-participating Fortune 500 companies are independently evaluated and rated by HRC. These scores are published annually in the Corporate Equality Index (CEI). The number of firms rated by the HRC varied from year to year: for example, in 2002, 2010, and 2017, a total of 319, 590, and 887 companies were rated, respectively. We hand-collected the names and scores for all the firms that appeared in the CEI from 2002 to 2018, but we retained only the data for the publicly held firms; the private firms were removed from the dataset because other pertinent data, such as firm performance data, were not available. The final number of observations for the LGBT-ID policy variable studied in this research was 3,566. We then manually collected the relevant company identifiers (ticker symbols) from the Compustat database to facilitate the collection of other required data (i.e., firm profitability). Any firms appearing in the HRC dataset but not in Compustat were also discarded. In the second step, we collected the requisite data from Compustat to calculate the outcome (firm profitability) and control variables. In the third step, we collected data pertaining to the mediating variable brand equity from Interbrand, a consultancy firm based in New York. We collected brand equity data for all US-based public firms listed in the Interbrand dataset. Private firms were again excluded for the reason explained above. We retained only the corporate brands; the product brands were discarded to achieve alignment among the explanatory, outcome, and moderating variables. The total number of observations for the corporate brand equity variable was 414. In the fourth step, the data necessary to measure the moderating variable, i.e., innovation intensity, were collected from Compustat. We merged the data based on company identifier and year to create the final dataset for this research. The number of observations for each variable is presented in Table 2.

Descriptive Statistics.

Measurement of Variables

LGBT-ID policies. We measured LGBT-ID policies based on data on the CEI gathered from the HRC database. Prior studies have used HRC data as a reliable and valid measure for LGBT-ID policies (Hossain et al. 2020; Patel and Feng 2021; Shan, Fu, and Zheng 2017). HRC considers a range of criteria to compute and assign an overall score for each firm. Factors such as equitable benefits for LGBTQ workers, non-discrimination with regard to sexual orientation and gender identity, partner health insurance, etc., are considered in this scoring (details are available at www.hrc.org). The scores range from 0 to 100, and higher scores denote better LGBT-ID policies.

Brand Equity. The brand equity of each of the companies in our sample was measured using the brand valuation estimates reported by Interbrand. These values have been used by numerous earlier studies as valid and reliable measures of brand equity (Kirk, Ray, and Wilson 2013; Raggio and Leone 2009; Wang and Sengupta 2016).

Innovation Intensity. Innovation intensity, which is defined as a firm's effort to create innovative products, services, and processes that will enhance customers’ overall brand experience, is reflected in a firm's resource allocation strategy (Rahman, Aziz, and Hughes 2020). Previous studies have measured innovation intensity as a firm's resource allocation strategy compared to its overall resource base (Fu, Boehe, and Orlitzky 2020; Rahman, Rodríguez-Serrano, and Lambkin 2019). Consequently, in line with earlier research, innovation intensity was measured as yearly R&D expenditure divided by total assets. The missing R&D values were replaced with zero (Koh, Reeb, and Zhao 2018).

Firm Profitability. The dependent variable, firm profitability, was measured as gross profit divided by sales revenue.

Control Variables. This study incorporated a set of pertinent covariates that were selected based on theory and earlier studies (Hossain et al. 2020; Rahman, Aziz, and Hughes 2020; Shan, Fu, and Zheng 2017). Prior studies have shown that a firm's performance depends on its size (Shan, Fu, and Zheng 2017). Therefore, we controlled for firm size by measuring it as the log of total assets. Firm leverage is another variable that has been documented to impact financial performance (Hossain et al. 2020). Leverage was measured as long-term debt divided by total assets and incorporated as a covariate. Firm growth rate was also controlled for, as it can affect performance (Rahman, Aziz, and Hughes 2020). Firm growth rate was measured as the yearly growth rate of a firm's assets. Capital intensity was measured as invested capital divided by the number of employees and was controlled for because earlier studies have documented its effect on financial performance (Rahman, Aziz, and Hughes 2020). The overall financial soundness of a firm is expected to influence its performance because financially sound firms have access to more resources and are, therefore, able to undertake gainful investment projects. Financial soundness was measured as cash flow divided by total debt. Firm efficiency is likely to impact firm performance because firms with greater efficiency are better able to manage available firm resources, which improves financial performance. Firm efficiency was measured as sales revenue divided by stockholders’ equity. Inventory turnover was also controlled for, as it can affect firm performance (Park and Kim 2021); it was measured as the cost of goods sold (COGS) as a fraction of inventories. Finally, firm profitability can vary depending on industry affiliation (Beard and Dess 1981). Hence, this study also incorporated industry profitability as a covariate, which was measured as the industry median ratio of gross profit to total assets. As firm profitability can vary owing to unobserved heterogeneities across industries and time periods, we also included year and industry dummies to control for the time effect and unobserved industry heterogeneity.

Model Estimation Technique

The system of equations developed in the preceding section might potentially suffer from endogeneity bias (Malshe and Agarwal 2015). Endogeneity bias might arise from omitted variable bias, simultaneity bias and measurement error (Abdallah, Goergen, and O'Sullivan 2015; Rahman, Aziz, and Hughes 2020; Rutz and Watson 2019). Although we incorporated a set of relevant firm and industry-level control variables guided by theory and prior studies, collecting data for other pertinent control variables was not practically feasible. For instance, other relevant variables, such as organizational culture, could not be incorporated into the model due to the non-availability of organizational culture data. Hence, the omission of such variables may engender omitted variable bias. There may also be a simultaneity bias between the dependent variable and the key explanatory variables of the study. For example, even though we argue that LGBT-ID policies influence firm profitability, the reverse might also be true—that is, firm profitability can influence a firm's decision to engage in corporate social responsibility initiatives (such as LGBT-ID policies). Furthermore, the mediating variable, brand equity, appears as both an explanatory and an outcome variable, so we used the instrumental variable estimation method to ameliorate the effect of endogeneity bias. Specifically, we estimated the system of equations using the three-stage least squares (3SLS) estimation method. Furthermore, if the error terms (

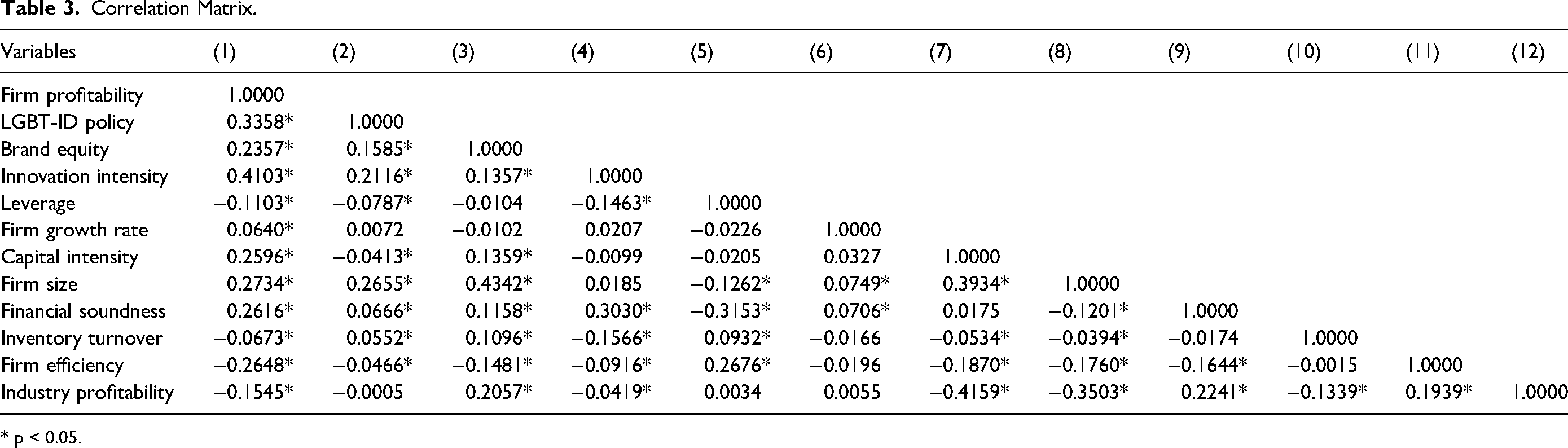

Descriptive Statistics and the Correlation Matrix

Our descriptive statistics and correlation matrix are presented in Tables 2 and 3, respectively. We calculated the variance inflation factors (VIF) to examine the presence of multicollinearity among the explanatory variables. The VIF ranged from 1.16 to 4.54 (see Table 2), which was substantially lower than the cut-off value of 10 for multiple regression models (Rahman, Aziz, and Hughes 2020). These VIF values indicate that multicollinearity is not an issue. To deal with the potential presence of outliers in the dataset, we winsorized all variables at the 1st and 99th percentiles.

Correlation Matrix.

* p < 0.05.

Results

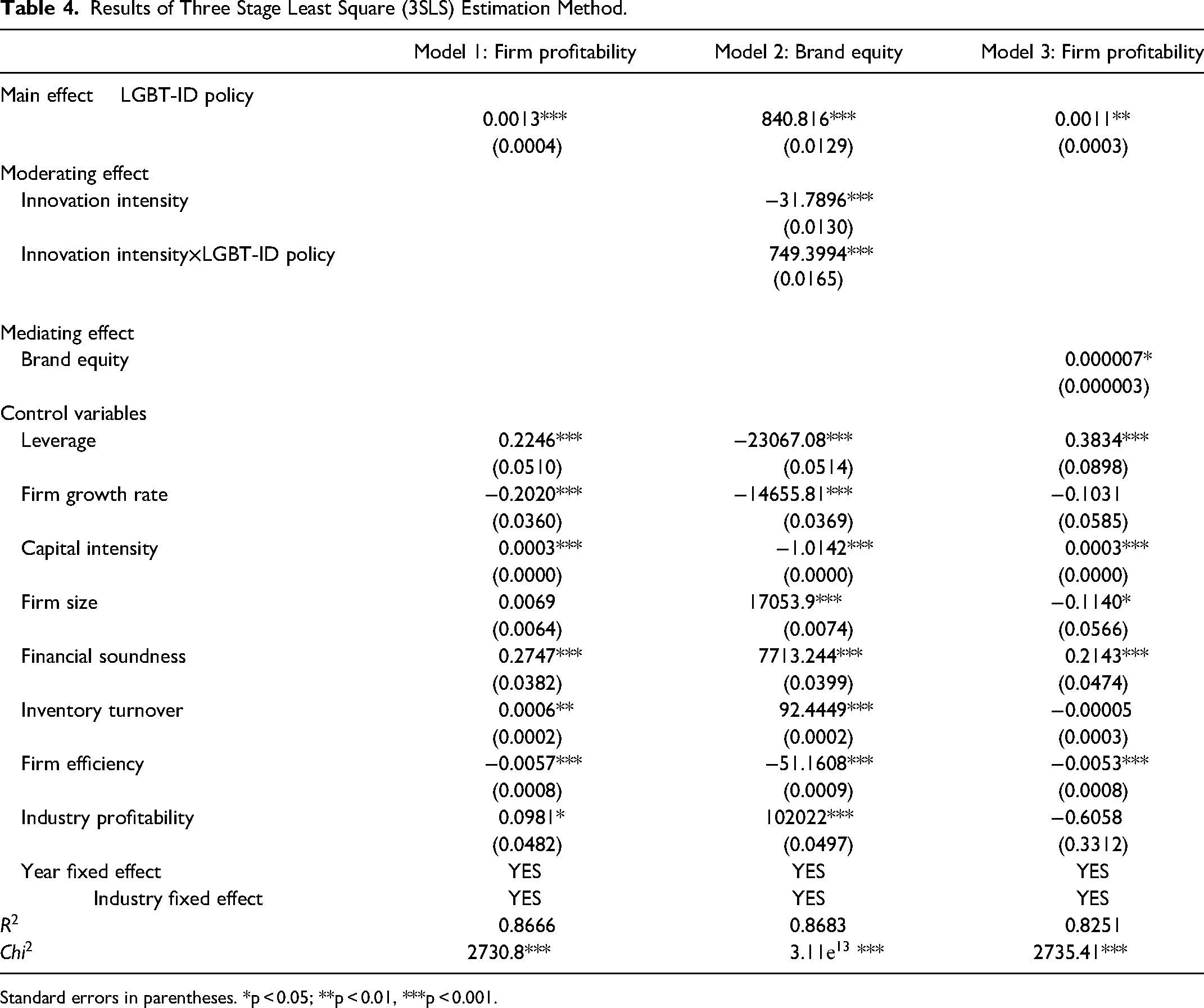

The results of simultaneous equation modelling using the 3SLS estimation method are reported in Table 4. The first column presents the results of equation 1; the third column reports the results of equation 3, wherein firm profitability was the dependent variable. The second column reports the results of equation 2, wherein the dependent variable was brand equity. In all models, the key explanatory variable was LGBT-ID policies. The findings demonstrate that the coefficient estimate of LGBT-ID policies is positive and significant (Model 1), thus supporting our first hypothesis (H1), which predicted a positive relationship between LGBT-ID policies and firm profitability. This finding demonstrates that firms that adopt LGBT-ID policies during the sample period of the current study reap financial rewards in the form of higher profitability.

Results of Three Stage Least Square (3SLS) Estimation Method.

Standard errors in parentheses. *p < 0.05; **p < 0.01, ***p < 0.001.

The second hypothesis (H2) assumed that firms with LGBT-ID policies would increase their corporate brand equity, which was also supported by our results. As shown in the results for Model 2, the coefficient of LGBT-ID policies was positive and strongly significant, confirming the predicted positive impact of LGBT-ID policies on corporate brand equity. Specifically, the present study's data reveal that adopting LGBT-ID policies enhances corporate brand equity. The third hypothesis (H3) assumed that the positive relationship between LGBT-ID policies and corporate brand equity is accentuated by a firm's level of innovation intensity. As shown by the results for Model 2, the estimated coefficient of the interaction term between innovation intensity and LGBT-ID policies was positive and strongly significant, demonstrating that when companies bolster their innovation efforts, LGBT-ID policies have a greater impact on brand equity, thus supporting H3. In essence, the data of the current study reveals the positive moderating effect of innovation intensity in the association between LGBT-ID policies and corporate brand equity.

In the fourth hypothesis (H4), it was assumed that brand equity plays a mediating role in the nexus between LGBT-ID policies and firm profitability. In order to establish mediation in the LGBT-ID policies → corporate brand equity → firm profitability relationship, LGBT-ID policies must affect brand equity, and brand equity must affect firm profitability. The results presented in Table 4 indicate that LGBT-ID policies positively affect brand equity (Model 2) during the present study's sample period. Entering the intervening variable brand equity reduces the strength of the effects of LGBT-ID policies on firm profitability during this period (from P < 0.001 to P < 0.01), thus supporting the mediational role of corporate brand equity in the effects of LGBT-ID policies on firm profitability. Furthermore, the coefficient for the direct impact of LGBT-ID policies on firm profitability drops from 0.0013 (Model 1) to 0.0011 (Model 3) when the effect of brand equity is controlled for, indicating that brand equity plays a mediating role in the nexus between LGBT-ID policies and firm profitability during the present study's sample period.

To gauge whether the indirect mediation effects were statistically significant (Sobel 1982), we also conducted an extended Sobel test with the bootstrapping meditation approach (Zhao, Lynch Jr., and Chen 2010). The results were significant (zvalue = 2.99, P < 0.01), thus confirming H4: firm's brand equity during this period intervenes in the effects of LGBT-ID policies on firm profitability. The Wald Chi-square statistic was used as a complementary measure of model fit (Table 4) and confirmed that at least one coefficient was statistically different from zero in all models.

Discussion and Conclusion

While a handful of prior studies demonstrated that adopting LGBT-ID policies positively affects a firm's forward-looking stock-market-based measures of firm performance, such as stock return and firm value (Hossain et al. 2020; Shan, Fu, and Zheng 2017), little is known about the effect of LGBT-ID policies on a firm's contemporaneous accounting-based financial performance (i.e., profitability). The current research adds to the existing literature by showing that during the sample period of the study (2002 to 2018) LGBT-ID policies have a positive effect on a firm's profitability. Specifically, the data of this study reveal that the more equitably a firm treats people with different sexual orientations and gender-based identities, the higher its profitability. Furthermore, responding to the call to identify the mediating mechanism (Patel and Feng 2021; Shan, Fu, and Zheng 2017), this study sheds light on the novel intervening mechanism in the link between LGBT-ID policies and firm performance. This research demonstrates that the adoption of LGBT-ID policies during the sample period of this study strongly and significantly impacts one of the most consequential market-based assets, i.e., corporate brand equity, which in turn positively affects a firm's profitability. In essence, the results confirm that corporate brand equity serves as a conduit in the relationship between LGBT-ID policies and profitability during this time. The data of the present study also reveal that innovation intensity further bolsters the nexus between LGBT-ID policies and profitability. That is to say, the positive impact of LGBT-ID policies on brand equity is accentuated when the focal firm invests more in innovation efforts.

Theoretical Implications

From a theoretical perspective, this study has several implications for researchers. First, this study shows that during this time incorporating LGBT-ID policies increases the financial viabilities (e.g., profitability) of firms. Combining propositions from OJT and IST, we argued that by adopting such policies in terms of fair and equitable treatment of LGBT employees, firms attain organizational legitimacy as well as gain enhanced support from external business-critical stakeholders. A revenue advantage is engendered due to the satisfaction of customers who become not only repeat customers but also strong advocates of the brand. Satisfied trade partners also support these firms with more favorable business terms, which results in a cost advantage for firms with a proactive LGBT-ID agenda. Thus, this study confirms the findings of similar yet very few studies in this stream of research (Hossain et al. 2020; Johnston and Malina 2008; Shan, Fu, and Zheng 2017) that LGBT-ID policies bring strong financial benefits.

Second, this study shows that incorporating LGBT-ID policies during the studied period of this research also positively impacts a firm's performance through corporate brand equity, thus shedding light on the novel mediating mechanism in the link between LGBT-ID policies and firm performance. Past studies that primarily investigated the financial implications of such policies adopted by the firms reported very mixed and conflicting results (Johnston and Malina 2008; Pichler et al. 2018; Shan, Fu, and Zheng 2017). This indicates that the relationship between them is rather complex, and therefore scholars called for identifying the possibility of the existence of other variables in the relationship between these two factors (Patel and Feng 2021; Shan, Fu, and Zheng 2017).

Third, in addition to uncovering the mediating mechanism that exists in the relationship between LGBT-ID policies and firm performance, this study also demonstrates that during the sample period of this study higher innovation intensity helps firms in securing greater reward in terms of a stronger corporate brand when they incorporate LGBT-ID policies. In accordance with OJT and IST and their relevance to LGBT-ID policies, this study shows that in an environment with a diverse workforce, employees feel more welcome and sense a stronger connection and commitment to their employers, which also helps in retaining and attracting more talent, enhancing creativity, and improving productivity (Hossain et al. 2020; Laplume et al. 2021). Firms with LGBT-ID policies share relevant information with their stakeholders, including their employees, which endows them with a better understanding of the firms’ strategic goals, and further encourages employees to embrace more challenges and bring more innovative ideas. This results in novel products and services that create more value for customers (Linder, Jarvenpaa, and Davenport 2003), gain the trust and confidence of both internal and external stakeholders and build brand equity. Efficient integration of LGBT-ID policies and innovation intensity is therefore essential because it compensates for the poor technological capability, obsolete product design, and lack of differentiation which may act as impediments to some desired performance outcomes (e.g., price premium, market share).

Managerial Implications

This study elucidates that LGBT-ID corporate policies enhance firm profitability during the study's sample period, which suggests that managers should consider implementing LGBT-ID corporate policies if they want to improve their firms’ profits. The data of this study also indicate that LGBT-ID corporate policies increase profits through the mediational effect of corporate brand equity. Therefore, brand managers could think of more plausible ways to implement innovative LGBT-ID corporate policies and publicize them so that the outcomes of the policies are reflected in their companies’ brand equity, which ultimately increases profitability. Finally, The results suggest that to shore up this link between LGBT-ID corporate policies and brand equity, R&D managers must have an informed knowledge of the relationship between LGBT-ID corporate policies and brand equity and come up with innovative products and services that can strengthen this link.

Policy Implications

At a macro-level, innovations from the private sector are core drivers of increased productivity (Gentimir 2013). Therefore, governments in most countries have innovation policies in place to promote a level playing field that allows local companies to thrive in global markets (https://www.state.gov/innovation-policy/). Given that companies that are more diverse and inclusive are better able to compete and have higher levels of innovation and creativity (Hossain et al. 2020), policymakers should have policy incentives to encourage companies to build a diversified workforce to maintain and thrive on innovation.

Limitations

Like any other study, this study has some limitations. The current study's sample was drawn solely from US corporations, which may have limited the generalizability of the results to this region. Perceptions toward LGBT people might vary considerably across countries. Future research should consider both US and non-US samples to enhance the generalizability of the findings. The preponderance of the firms assessed in this study was large, so further research on small and family-owned firms is warranted. Furthermore, this study uncovered the effect of one mediating and one moderating variable. Moderators other than innovation intensity and mediators other than brand equity could also be investigated in future research. Specifically, future studies should endeavor to unearth other mediating and moderating variables. For example, future studies could explore whether the psychological safety of the employees mediates the association between pro-LGBT policy and firm performance. Also, future studies could examine whether the commitment of the employees and employees’ satisfaction moderate the relationship between pro-LGBT policy and firm financial performance.

Future Research

While most studies in this area (including this one) have reported positive outcomes of LGBT-ID corporate policies, future research should develop and empirically test more complex research models in relation to this topic. However, this is only one side of the coin—there has been heated debate on the rights of LGBT people, and prejudice against them remains across the globe. Until 1973, the American Psychiatric Association defined homosexuality as a mental illness. States and societies are increasingly more accepting of LGBT people, but at present, there remains little research into how and why this transformation took place and how this has benefitted companies and their brands. Nevertheless, people in the USA with different sexual orientations (Lesbian, gay, bisexual, transgender and queer) are not treated in the same manner across different states. Some recent events indicate that in some states in the USA, transgenders and queers are not receiving the same level of treatment as people with other types of sexual orientations, such as gays and lesbians (Parker, Horowitz, and Brown 2022). That is, transgenders and queers seem to be encountering some discrimination in some states. Consequently, future studies should adopt a more nuanced approach and explore how the treatment of people with various types of sexual orientations by ordinary Americans as well as other relevant stakeholders affect firms’ overall strategic stance toward those who are not treated in an equal manner. More studies are needed incorporating the recent developments in some states in the USA to uncover how the association between the focal variables dynamically evolve due to state-level legal development against some LGBT people (e.g., transgender) in some states, such as the bathroom bill in Kansas. In sum, while the data of the current study revealed a positive association between LGBT-ID policy and profitability, future studies should incorporate the recent developments to examine how these affect the firms’ orientation as well as how these changes in firms’ stances affect firm outcomes.

This issue is particularly closely related to religion, and prejudice based on faith is very hard to revise or change. Therefore, future cross-border and cross-cultural research is needed to determine whether LGBT-ID policies are harming brands from the perspectives of a broad spectrum of religious views about LGBT people around the globe, especially with regard to Christianity, Islam, and Hinduism, the three most prevalent religions in the world. Another potential topic of research in this area would be to investigate whether global brands are losing their “global” image by being inclusive of LGBT people and ignoring the views of the people who remain critical of this group. This is a real challenge for global brands, and future research could investigate whether and how these brands are managing this paradox and handling this issue through their ambidextrous focus on LGBT, pro-LGBT, and anti-LGBT customers. Furthermore, while the inclusion of LGBT people in diverse workforces is expected to strengthen the resources and capacity of the companies, a similar paradox arises in managing such a diverse and multicultural workforce with differing attitudes, religious views, and beliefs.

In their study of a sample of US companies, Maks-Solomon and Drewry (2021) reported that LGBT employee groups have convinced employers to promote LGBT rights publicly, suggesting that internal pressures, rather than social, political, or market forces, encourage companies to take a public stance on LGBT issues. Future research should take a 360° approach to incorporate all internal and external forces, their differing views and influences, and determine how all of these factors impact brand equity and firm performance in a holistic manner. Another potential topic of research in LGBT-ID policies would be to investigate the real motives of companies and brands in promoting such policies. Many companies have been heavily criticized for perpetuating “pinkwashing”, a term used to describe when companies pretend to adopt a positive attitude toward LGBT people in order to promote their brand or product for marketing purposes rather than making concrete contributions to pursuing LGBT equality. Also, some people think that society has gone too far to act in favor of LGBT people (Parker, Horowitz, and Brown 2022) and therefore, research should also address the concerns of this group, and companies should come up with appropriate strategic options to balance their policies and practices toward LGBT people.

Footnotes

Associate Editor

Teresa Pavia

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.