Abstract

This article investigates the impact of heterogeneous foreign investment on home market stock price informativeness. Evidence from China’s nascent A-share market shows non-segmented foreign investment reduces firms’ stock return synchronicity, while segmented foreign investment does not. Using the Shanghai (Shenzhen)–Hong Kong Stock Connect program as a natural experiment that exogenously increases non-segmented foreign ownership, we find that synchronicity drops significantly for program stocks relative to the control stocks. Our results are most consistent with an “informed trading” explanation, rather than a “learning” or “governance” explanation. These results have policy implications for stock market liberalization programs.

Keywords

Introduction

Stock market liberalization is a central topic in international finance. Since the 1990s, many emerging markets have opened up their stock markets to foreign investors but there is ongoing debate about whether foreign investment is beneficial to local firms and markets. 1 A central question for governments is how to maximize the positive development benefits from foreign investment and how to minimize its negative impact.

An important impact of foreign investment is on the stock price informativeness of investee stocks. Stock markets in emerging economies are characterized by highly synchronous stock returns (Morck et al., 2000). 2 In these markets, an important policy objective is to facilitate more “informative” stock returns and thus efficient allocation of capital. This objective could be better achieved through the introduction of foreign (institutional) investors. For example, Li et al. (2004) show that firm-specific variations are positively associated with country-level capital market openness. Gul et al. (2010) find that firms in China with foreign investors have lower synchronicity than those without foreign investment.

Nevertheless, mechanism by which foreign investment improves stock price informativeness remains unclear. We compare two policy options to introduce foreign investment. First, the government could allow domestic publicly traded firms to dual-list their securities in foreign stock markets (“dual-listing”). Second, the government could allow foreign (institutional) investors to invest directly in domestic stock markets (“direct investment”). The key difference between the two types of foreign investment is the trading location of the firm’s foreign shares. In dual-listing, foreign investment is “segmented” from domestic stock market because foreign investors can only trade the company’s security on a foreign stock exchange. In direct trading, foreign investment is “non-segmented” because foreign investors can trade with domestic investors on a local stock market.

The contribution of this article is in our investigation of the impact of heterogeneous foreign investment on home stock price informativeness. For dual listed firms, the “learning” hypothesis argues that domestic investors react rationally to the firm-specific information produced in the foreign market, which allows for price discovery in the domestic market (Chakrabarti & Roll, 1999; Sjöö & Zhang, 2000). Compared with firms listed only in the domestic market, dual listed firms benefit in terms of price discovery from their investor base in the foreign market. More firm-specific information may also be available for dual listed firms because of enhanced media and analyst coverage, as well as because of disclosure requirements in both home and foreign markets. Through observational learning, domestic investors adjust their own expectations of the value of firms’ security in domestic market, making domestic stock prices more informative.

For non-segmented foreign investment, the “informed trading” hypothesis argues that foreign (institutional) investors who have access to domestic stock markets follow the “Wall Street rule” (Edmans, 2009) and trade aggressively on their private information (which is unavailable to domestic investors or even managers). Through their direct trading with domestic investors, non-public, firm-specific information is impounded into price, thereby increasing stock price informativeness (Edmans & Manso, 2011).

To disentangle the “learning” hypothesis from the “informed trading” hypothesis, we use China’s nascent A-share market as a natural laboratory. Established in 1991, the Chinese stock market shares many features of an emerging financial market (Chan et al., 2004; Morck et al., 2000; Y. Wang et al., 2009). To improve market quality, the government employed different liberalization programs, allowing us to differentiate segmented and non-segmented foreign investment and to make causal inferences.

Our empirical strategy compares the impact of two types of foreign investment—segmented and non-segmented—on stock return synchronicity of Chinese firms. Consistent with prior findings (Gul et al., 2010; He et al., 2013), we find a negative association between foreign investment and stock return synchronicity from 2004 through 2014. However, by partitioning the foreign invested firms (FIF) into segmented and non-segmented groups, we find stark differences: Non-segmented FIF exhibit a strong negative association with synchronicity, while segmented FIF do not. This pattern is remarkably consistent in the data and is robust to controlling for all observable variables in the synchronicity literature.

Our baseline result suggests that the trading location of the firm’s foreign shares matters: Foreign investment improves domestic stock market informativeness when foreign investors are allowed to access the domestic stock market, but not when they only trade in the foreign stock market. This evidence supports the “informed trading” hypothesis but not the “learning” hypothesis.

To make causal inferences on the impact of non-segmented foreign investment, we exploit novel, stock market connect programs that remove trading frictions of selected stocks in the Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE) for Hong Kong investors. Specifically, the Shanghai–Hong Kong Stock Connect program (SHHKSC), launched on November 17, 2014, allows Hong Kong investors to directly trade 568 (out of 985) stocks on the SSE through their own brokers. Two years later, on December 5, 2016, the Shenzhen–Hong Kong Stock Connect program (SZHKSC) removed trading frictions for Hong Kong investors for 881 (out of 1,828) stocks on the SZSE. These two programs provide an ideal laboratory for us to test the impact of exogenous increases in non-segmented foreign investment using a difference-in-differences (DiD) set up.

Consistent with the informed trading hypothesis, we find the removal of trading frictions between the two segmented markets has a large and significant impact on stock price informativeness: The synchronicity (R2) of program stocks drops significantly compared with non-program stocks. Moreover, we find in the cross-section, the effect of the SHHKSC program is more pronounced for firms without prior non-segmented foreign investment and for firms subject to more active northbound trading. 3 Taken together, our evidence confirms that non-segmented foreign investment has a causal effect on synchronicity, and the channel is through informed trading.

We also consider corporate governance as an alternative channel for foreign investment to influence firms’ stock price informativeness. For example, foreign block holders can prompt governance changes in their investees through board seats, proxy fights, securities lawsuits, and private communications (Cheng et al., 2010; Kahn & Winton, 1998; Maug, 1998), which increases firm-specific information. 4 Therefore, our finding that non-segmented FIF have more informative stock prices than segmented FIF can be confounded if non-segmented FIF have better “governance” than segmented FIF. However, this proposition is not supported by the data. We find that segmented FIF (dual-listed firms without B- or QFII-shares) are larger and appear to have better governance (larger board size and independence, more analyst coverage, less duality of chairman and the chief executive officer [CEO]), than non-segmented FIF. Additional tests using discretionary accruals to proxy for financial reporting transparency indicate no difference in transparency between segmented and non-segmented FIF. For robustness, we check the directors’ biographies and find no board seats occupied by foreign block holders and no proxy fights or securities actions brought by foreign institutions in China’s FIF (segmented or non-segmented). This evidence echoes findings of Fung et al. (2013) and Ke et al. (2012), who show that in a weak legal investor protection environment like China, the corporate governance role of foreign block holders is minimal.

This study relates to a large body of literature on the determinants of stock price informativeness (Durnev et al., 2003; Roll, 1988). Prior work finds that synchronicity is affected by country / region level institutional environments (Fernandes & Ferreira, 2009; Hasan et al., 2014; Jin & Myers, 2006; Morck et al., 2000), corporate governance indicators (D. Ferreira et al., 2011; Khanna & Thomas, 2009), institutional ownership (An & Zhang, 2013; Piotroski & Roulstone, 2004), and analyst coverage (Chan & Hameed, 2006). Regarding the role of foreign ownership, Gul et al. (2010) find that from 1996 through 2003, the R2 is lower for Chinese firms with foreign ownership than for peer firms. He et al. (2013) find a negative association between large foreign ownership (defined as foreign ownership greater than 5%) and synchronicity in markets with high investor protection. Unlike prior work, our focus is not whether FIF have lower synchronicity than non-FIF, but rather, which type of foreign investment (segmented or non-segmented) helps to improve stock price informativeness. The Chinese stock market setting allows us to identify the channel.

Using SHHKSC and SZHKSC as natural experiments, we offer causal evidence on the impact of stock market liberalization programs on emerging market efficiency. Under the “One Country, Two Systems” principle, SHHKSC and SZHKSC are novel pilot programs that connect one emerging with one developed financial market. Close to a laboratory setting, the stocks included in the program are clearly prescribed, the implementation date is precise and other major policies are not implemented in the surrounding dates. As a result, our results can inform policymakers in emerging markets about the conditions under which foreign investment can contribute to local market efficiency. On one hand, we show that due to institutional differences and market frictions, domestic investors do not easily learn about for firm-specific information from foreign market activities; if the two markets are segmented, foreign investors cannot trade with domestic investors on their private information. On the other hand, our results show that even in markets with weak investor protection and with institutions that are unfriendly to shareholder activism, foreign investment can improve local market quality through informed trading. This is our contribution to the international finance literature.

The remainder of the paper is organized as follows. Part 2 illustrates the institutional setting and the liberalization history of China’s stock market to foreign investors. Part 3 develops the hypotheses. Part 4 presents the data, variables, and the empirical model. Part 5 presents the results and robustness tests, and Part 6 concludes.

China’s Stock Market and Foreign Investors

China’s Stock Market Development

The inception of China’s stock market can be understood in the context of the partial privatization of state-owned enterprises (SOEs) in the 1990s. During this decade, selected SOEs were allowed to issue new and minority shares to private investors who could trade their shares freely on the newly established SSE and SZSE (in 1990 and 1991, respectively).

The empirical literature has documents efficiency gains after SOE privatization in the Chinese stock market. 5 Nevertheless, direct evidence showing that private investors play an active role in the governance of Chinese SOEs is scarce. 6 Although domestic institutional investors are significantly growing in number, their governance role relative to firm management is symbolic at best. 7 Bushee (1998) classifies institutional investors as either “owners” or “traders,” depending on the nature of their ownership and the horizon of their trading behavior. Given the poor legal protection for investors in China, most institutional investors choose “not to fight” and instead trade on their private information (Firth et al., 2010; Tong et al., 2013).

Foreign Investment in Listed Chinese Firms: B-, H-, and QFII-Shares

Since 1992, China has allowed select companies to issue Class A and Class B shares. Before 2001, the A- and B-share markets were segmented. Domestic investors could trade only Class A shares (denominated in CNY), and foreign investors could trade only Class B shares (denominated in USD on the SSE and HKD on the SZSE). Since 2001, domestic investors with foreign currency accounts are allowed to trade B shares, making firms with A+B shares non-segmented FIF.

Since the 1990s, Hong Kong has become an important fund-raising platform for Chinese firms (Sun et al., 2013). By 2015, 194 Chinese enterprises (mostly SOEs) had listed their H shares on the Hong Kong Stock Exchange (HKEx), and most of them are dual-listed in both the A (domestic) and H (Hong Kong) stock market. 8

Since 2003, China has allowed selected qualified foreign institutional investors (QFII) to invest in its A-share market. Under the QFII scheme, foreign financial institutions that satisfy prescribed size and profitability requirements are permitted to convert foreign currency into CNY to invest any stocks traded on the SSE and SZSE. Each QFII is given an investment quota and profits can be repatriated. The aggregate quota granted to all QFIIs increased from USD10 billion in 2003 to USD150 billion in 2015. CSRC statistics show that the top five QFII origin countries/regions are the United States, United Kingdom, Japan, Korea, and Hong Kong. Liu et al. (2014) compare the portfolio investees of QFII and domestic funds and find that QFII appears to favor sectors that do not require high levels of local knowledge.

The Shanghai–Hong Kong Stock Connect (SHHKSC)

The SHHKSC, launched on November 17, 2014, is a pilot trading and clearing linkage program between the SSE and HKEx. The SHHKSC enables investors in Hong Kong and the mainland to trade and settle stocks listed on the other market by their local securities brokers without requiring securities accounts in the other market. 9

Given that the two stock markets are historically segmented and regulated under a distinct legal–political regime, a prominent feature of the SHHKSC is that “home market” laws and rules apply. This rule is beneficial for our test because parallel changes in the regulatory environment may affect our variable of interest (i.e., synchronicity). In other words, the SHHKSC is a trading and clearing program that exogenously increases non-segmented foreign investment of selected stocks without changing any fundamentals of the firm or of the regulatory environment.

Another important feature of the SHHKSC program is the “investibility” of stocks on the other exchange. Although the long-term objective is to make all stocks on each stock market investible to investors on the other market, in the initial stage, Hong Kong investors were allowed to trade only “investible” stocks listed on the SSE market. 10 Investible stocks include all of the constituent stocks in the SSE 180 Index and SSE 380 Index, and all of the SSE-listed “A+H” stocks (“Northbound Trading”). In contrast, mainland investors could trade the constituent stocks of the Hang Seng Composite LargeCap Index and Hang Seng Composite MidCap Index and all H shares that had corresponding A shares (“Southbound Trading”). Finally, trading under the SHHKSC was subject to a maximum cross-boundary investment quota, together with a daily quota.

The Shenzhen–Hong Kong Stock Connect (SZHKSC)

Follow the success of SHHKSC, the SZHKSC was launched on December 5, 2016. This is a pilot trading and clearing linkage program between the SZSE and HKEx. The SZHKSC enables investors in Hong Kong and the mainland to trade and settle stocks listed on the other market using their local securities brokers. The SZHKSC follows the same rules and principles as SHHKSC. The SZHKSC program firms were drawn from three sources: the Shenzhen Component Index constituents, the SZSE SME Innovation Index constituents, and the A+H stocks. All SZHKSC program firms were required to have daily average market capitalization of more than RMB 6 billion in the past 6 months.

Development of Hypotheses and Empirical Design

Our objective is to assess the impact of (heterogeneous) foreign investment on stock return synchronicity (“synchronicity”). Depending on the trading locations, foreign investment in Chinese publicly traded firms can be segmented or non-segmented. Non-segmented FIF include those with B- or QFII-shares where foreign investors can trade directly with domestic investors. Segmented FIF include dual-listed firms without B- or QFII-shares.

For segmented FIF, the “learning” hypothesis argues that domestic investors react rationally to firm-specific information produced in foreign markets. This firm-specific information can be public or private, and explicit or implicit. Through active learning, domestic investors revise their beliefs about the firm’s value. In this way, information produced in the foreign market is transmitted to the home market, making domestic stock prices of segmented FIF more informative (Chakrabarti & Roll, 1999; Sjöö & Zhang, 2000). If this proposition is true, then we hypothesize:

For non-segmented FIF, the “informed trading” hypothesis posits that foreign (institutional) investors possess firm-specific, value relevant information that is not available to the public or even firm managers. Their private information can come, for example, from global market information about demand for the firm’s products or competition with other firms (Albuquerque et al., 2009; Bae et al., 2012). Alternatively, private information can come from their superior resources and skills in collecting and processing firm-specific information (Aslan et al., 2011; Chakravarty, 2001; M. A. Ferreira & Laux, 2007; Hartzell & Starks, 2003; O. Kim & Verrecchia, 1994; Piotroski & Roulstone, 2004). Because they have access to domestic stock markets, their private information is impounded into domestic stock prices through informed trading, making stock prices of their investees more informative. We therefore hypothesize:

Furthermore, if H2 is correct (i.e., informed trading is the crucial mechanism), then we should observe a reduction in synchronicity following exogenous increases in non-segmented foreign investment. The two stock connect programs, that is, the SHHKSC and the SZHKSC, provide an ideal setting for this test. The programs removed trading frictions of eligible stocks in the A-share markets for Hong Kong investors without other corresponding changes in the regulatory environment, leading to an exogenous increase in non-segmented foreign investment. We therefore hypothesize:

Sample and Variables

Much of our data come from the CSMAR database, which contains the daily trading, financial statement information, and ownership information for all Chinese listed companies. The CSMAR also contains quarterly ownership data on QFII. We also obtain the lists of SHHKSC and SZHKSC program stocks from CSMAR. Our baseline sample period is from 2004 through 2014. 11

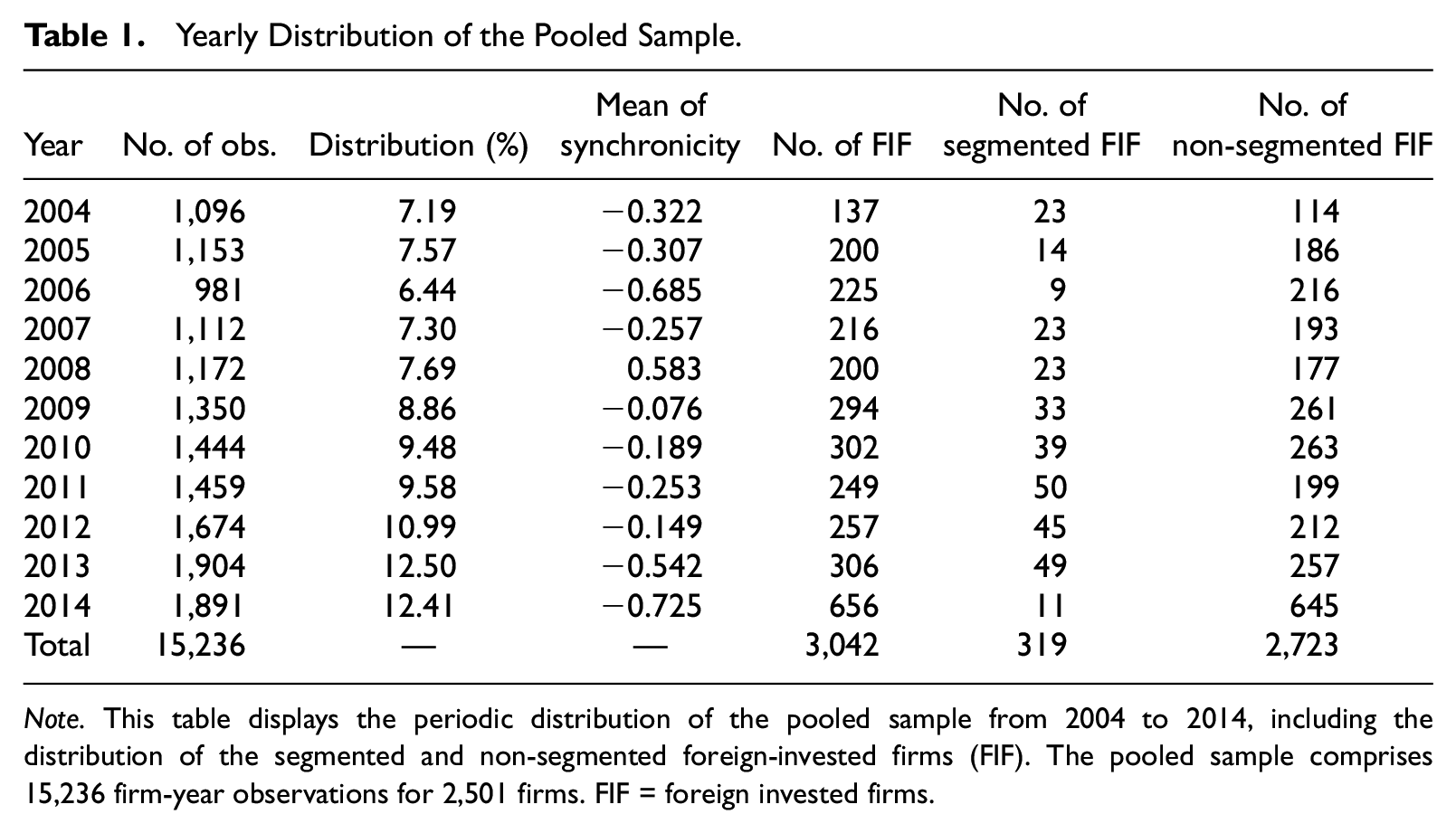

The annual measure of synchronicity for a stock (described next) is calculated annually using its daily trading data, with at least 200 trading days required. The final sample comprises 15,236 firm-year observations for 2,501 firms. Panel A of Table 1 shows the yearly distribution of the pooled sample, including the distribution of FIF. The number of observations increases steadily over the sample period, except for a slight decrease in 2014. This occurs because of many trading halts during the Chinese A-share market boom in 2014. 12 Regarding the industrial distribution, approximately 60.53% of the observations are from the manufacturing sector, followed by 7.00 % from wholesale and retail, and 6.36% from real estate.

Yearly Distribution of the Pooled Sample.

Note. This table displays the periodic distribution of the pooled sample from 2004 to 2014, including the distribution of the segmented and non-segmented foreign-invested firms (FIF). The pooled sample comprises 15,236 firm-year observations for 2,501 firms. FIF = foreign invested firms.

There are 3,042 FIF observations in our sample. The number of FIF increases over time, from 137 in 2004 to 656 in 2014, the majority are non-segmented FIF. In 2014, there is a large increase in the number of non-segmented FIF (from 257 to 645) and a drop in the number of segmented FIF (from 49 to 11). This is due to the SHHKSC program in November 2014. This program exogenously increased non-segmented foreign investment in publicly traded firms. The impact of SHHKSC is investigated separately in the next section.

Measuring Stock Return Synchronicity

Our dependent variable, synchronicity, is calculated in two steps following Durnev et al. (2003), Gul et al. (2010), and Chan and Chan (2014). First, we estimate the market model:

where

Baseline Model and Control Variables

Using the data described in the previous section, we estimate regressions of the following form:

where Synch is our synchronicity measure. It is the logarithmic transformation of

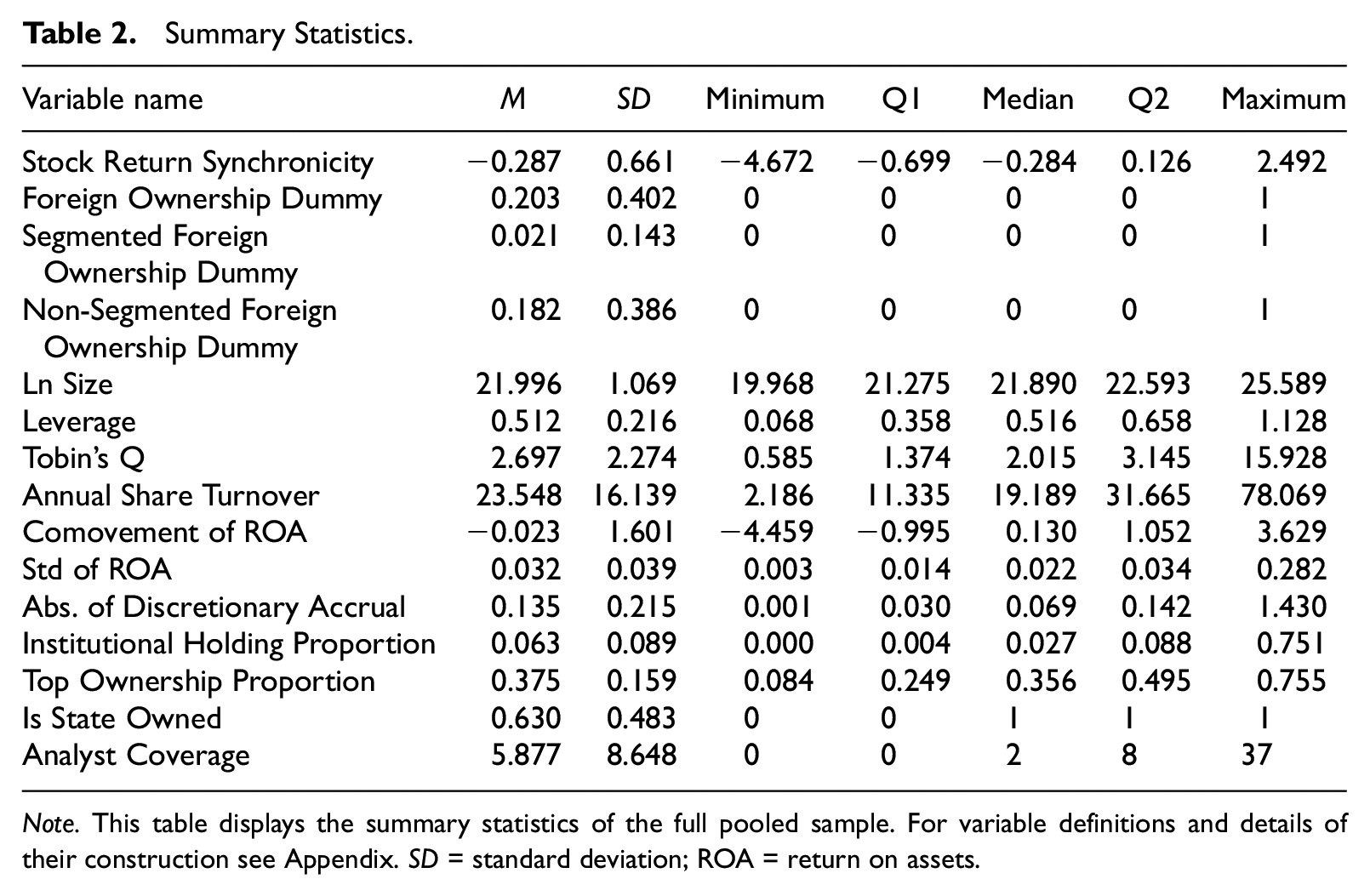

Table 2 reports summary statistics for the 15,236 firm-year observations. The mean and median of stock return synchronicity are −0.287 and −0.284, respectively. These statistics are lower than, but comparable to, the reported synchronicity for China in the samples in Morck et al. (2000) and Gul et al. (2010), which covered earlier periods. 13 Stock return synchronicity for our sample exhibits considerable cross-sectional variation, with a standard deviation of 0.661. Approximately 20.3% of our sample observations have foreign investment, with 2.1% of the observations being segmented foreign-invested firms and 18.2% being non-segmented foreign-invested firms. The logarithm size of our sample firms ranges from 19.968 to 25.589, inclusive, with a sample mean of 22. The book leverage ranges from 6.8% to 112.8%, with a sample mean of 51.2%, and 284 observations temporally have book liabilities greater than total assets. Tobin’s Q ranges from 0.585 to 15.928, with a sample mean of 2.697. The annual share turnover ranges from 2.186 to 78.069, with a sample mean of 23.548. The comovement of ROA is between −4.459 and 3.629, with a sample mean of −0.023. The standard deviation of ROA is between 0.3% and 28.2%, with a mean of 3.2%. The absolute value of discretionary accruals ranges from 0.001 to 1.430, with a sample mean of 0.135. The institutional holding proportion is between 0% and 75.1%, with a sample mean of 6.3%; this is consistent with claims that that Chinese A-share market is a dominated by retail investors. The top ownership proportion ranges from 8.4% to 75.5%, with a sample mean of 37.5%; this is consistent with claims that Chinese listed firms have concentrated top ownership. Approximately 63% of our sample observations are SOEs. Analyst coverage ranges from 0 to 37, with a sample mean of 5.877 but a median of 2; this indicates that most firms have limited analyst coverage and analysts mainly concentrate on a few popular firms.

Summary Statistics.

Note. This table displays the summary statistics of the full pooled sample. For variable definitions and details of their construction see Appendix. SD = standard deviation; ROA = return on assets.

Empirical Results

Baseline Model Results

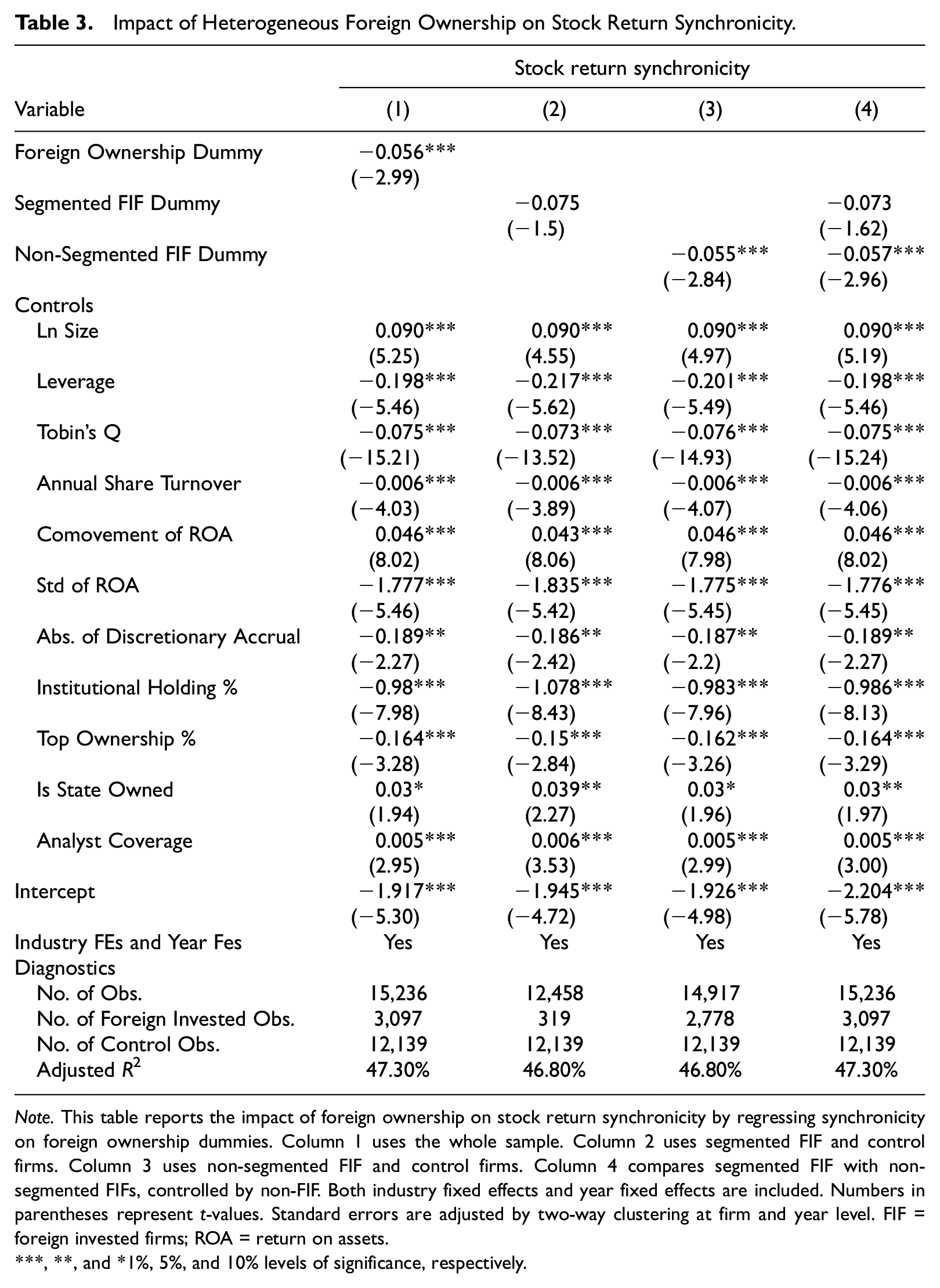

Table 3 presents our baseline model results from regressing synchronicity on the foreign ownership dummies. Column 1 uses the whole sample, Column 2 only uses segmented FIF and non-FIF, and Column 3 uses non-segmented FIF and non-FIF. Industry fixed effects and year fixed effects are included. Standard errors are adjusted using two-way clustering at the firm and year level.

Impact of Heterogeneous Foreign Ownership on Stock Return Synchronicity.

Note. This table reports the impact of foreign ownership on stock return synchronicity by regressing synchronicity on foreign ownership dummies. Column 1 uses the whole sample. Column 2 uses segmented FIF and control firms. Column 3 uses non-segmented FIF and control firms. Column 4 compares segmented FIF with non-segmented FIFs, controlled by non-FIF. Both industry fixed effects and year fixed effects are included. Numbers in parentheses represent t-values. Standard errors are adjusted by two-way clustering at firm and year level. FIF = foreign invested firms; ROA = return on assets.

**, and *1%, 5%, and 10% levels of significance, respectively.

Consistent with prior literature (Gul et al., 2010; Morck et al., 2000), the coefficient on the foreign ownership dummy in Column 1 is negative (coef = −0.0559) and significant (p = .0030), indicating that FIF exhibit significantly lower synchronicity than non-FIF. However, when we only include segmented FIF in our test, the coefficient on the foreign ownership dummy becomes insignificant (p = .134) although it remains negative. H1 is therefore not supported. In contrast, when we only include non-segmented FIF as treatment firms in our test, the coefficient on the foreign ownership dummy is negative and significant (p = .005), supporting H2. These findings indicate that the impact of foreign ownership on stock price informativeness is driven by non-segmented FIF. Also, when we include both segmented FIF and non-segmented FIF as treatment firms in our test, the coefficient on the segmented foreign ownership dummy remains negative and insignificant (p = .104), and the coefficient on the non-segmented foreign ownership dummy is negative and significant (p = .003). This result suggests that domestic investors do not easily impound price information from a firm dual-listed in a foreign market into the price of the firm in the domestic market. However, when foreign investors have the ability to trade the firm’s security in the domestic market, their private information is incorporated into price, making their investees’ stock prices more informative.

Most of the signs and significance on control variables are consistent with our expectations and the prior literature. The positive coefficients on firm size and synchronicity are consistent with large firms being influential constituents of the market index and industry indices, which in turn have synchronicity (Piotroski & Roulstone, 2004). The annual share turnover has a negative coefficient, suggesting that active trading enhances the incorporation of firm-specific information into stock prices. The coefficients on Tobin’s Q are negative, suggesting that firms with high growth potential tend to have more firm-specific information incorporated into their stock prices. The significantly positive coefficients on the comovement of ROA and negative coefficients on the standard deviation of ROA suggest that the comovement of fundamental performance is positively correlated with the comovement of stock prices and the noise in fundamental performance is also positively correlated with firm-specific risk. Finally, consistent with Chan and Hameed (2006), we find the coefficients on analyst coverage are positive and significant, indicating that securities which are covered by more analysts incorporate greater (lesser) market-wide (firm-specific) information.

Regarding the governance-related variables, the negative coefficients on institutional holding proportion are consistent with the expectation that better governance improves the information environment, and thus increases firm-specific information. The coefficients on the absolute value of discretionary accruals are marginally significant and negative, which is inconsistent with Hutton et al. (2009) who find that in the U.S. market, opacity is positively associated with stock return synchronicity. This inconsistency could be attributed to the difference of markets. In the U.S. market, firms with opaque financial reports tend to hide their bad news to resemble average firms, increasing synchronicity. However, in the Chinese market, firms use earnings management to present good news, which increases firm-specific stock price volatility, leading to lower stock return synchronicity.

Our result that dual listed firms’ foreign prices do not easily inform home stock prices is not inconsistent with prior empirical literature. Grammig et al. (2004) find that most foreign stocks traded simultaneously in New York and on their home markets have the largest fraction of price discovery occurring in the home markets, with New York playing a smaller role. Eun and Sabherwal (2003) examine the extent to which U.S. trading contributes to price discovery in Canadian firms cross-listed in the United States. They find that price adjustments occur in both Toronto and New York, with New York prices adjusting more to Toronto prices than vice versa. Using a sample of Hong Kong-listed stocks that are also traded on the London Exchange, Agarwal et al. (2007) demonstrate that home market is the primary location for price discovery, even when the bulk of trading activity in the foreign market is conducted by institutional investors.

We offer several possible explanations for why the “learning” hypothesis does not work: First, institutional differences between the firm’s home and foreign market translate into arbitrage costs that hamper the transmission of price information. Explicit arbitrage costs include transaction costs, taxes, regulatory restrictions, currency controls, and foreign ownership limits. Implicit costs are related to the quality of the information environment. For example, the number of analysts following the stocks, the fraction of shares held by institutional investors, and market liquidity (Gagnon & Karolyi, 2010). Second, it is possible what domestic investors infer from foreign prices is market information rather than firm-specific information, because securities traded in a foreign market are often synchronized with the market index of the host market (S. S. Wang & Jiang, 2004). Third, even when domestic traders react rationally to foreign market price movements, they cannot easily arrive at a common posterior assessment of value.

Stock Connect Events DiD Analysis

Stock connect event sample

Our key finding—that non-segmented foreign investment improves stock price informativeness—requires validation. A strong test is to observe what happens to firms’ synchronicity when there is an exogenous increase in non-segmented foreign investment. Fortunately, the SHHKSC program, launched on November 17, 2014, allows Hong Kong investors to directly trade 568 (out of 985) stocks on the SSE through their own brokers. Similarly, on December 5, 2016, the SZHKSC program removed the trading frictions for 881 (out of 1,828) stocks on the SZSE. These two programs provide the ideal setting to test the impact of non-segmented foreign investment in a DiD set up.

Our SHHKSC event sample covers the 2-year period from November 2013 through November 2015. The pre-SHHKSC period is from November 1, 2013 through October 31, 2014 with 245 trading days, and the post-SHHKSC period is from December 1, 2014 through November 30, 2015 with 245 trading days. Similarly, our SZHKSC event sample covers the 2-year period from December 2015 through December 2017. The pre-SZHKSC period is from December 1, 2015 through November 30, 2016 with 245 trading days, and the post-SZHKSC period is from January 1, 2017 through December 31, 2017 with 245 trading days. For both events, we exclude the event month to avoid potential noise around the launch days.

It is important to note that investible stocks in the programs are clearly not randomly selected. Nor, however, is it a choice variable. Take SHHKSC as an example, eligible stocks include all the constituent stocks included in the SSE 180 Index and SSE 380 Index and all SSE-listed “A+H” stocks. The SSE180 index was established in 2002 and the SSE 380 index was established in 2010. According to China Securities Index Co. Ltd. (the producer of SSE180 and SSE380), the inclusion criteria for SSE180 and SSE380 consider the overall rank for stocks, based on market capitalization and trading volume. 14 Chan and Kwok (2017) analyze the determinants of being included in the SHSC program and find that firm size explains 26% of the variation in investibility.

Given that SHHKSC investible stocks are not a choice, the main identification challenge is not self-selection but systematic differences between SHHKSC and non-SHHKSC stocks. To overcome this challenge, we take the advantage of the SZHKSC program, which was launched two years later. Because the two stock connect programs are different in terms of exchange market but the selection criteria for the program firms are quite similar, we can consider the SZHKSC investible firms in 2016 as a counterfactual group for the SHHKSC investible firms in 2014. Therefore, our focused DiD test studies the SHHKSC program, and use the SZHKSC program firms as the control group. As a robustness check, we also conduct a DiD test on both the SHHKSC and SZHKSC programs, using non-program firms as the control group.

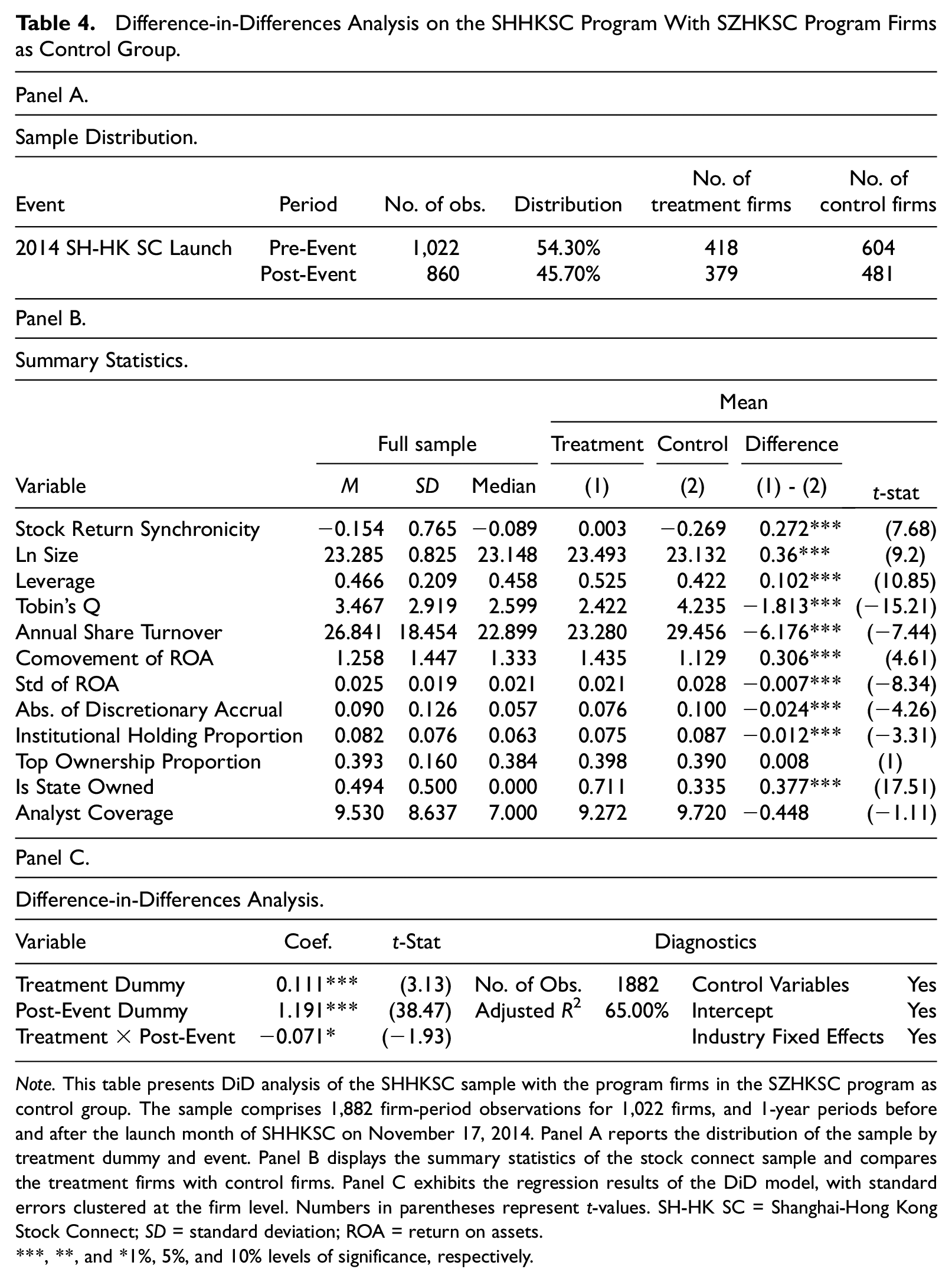

Panel A of Table 4 reports the distribution of our matched sample firms across periods and based on treatment group (SHHKSC firms) versus control group (SZHKSC firms). We take the program firms selected for the event day as our treatment group and exclude those firms that are removed from the program within 1 year from our sample. We also exclude a small number of program firms which are not included in the program on the event date, but are later added to the program. The final sample is comprised of 445 treatment firms and 694 control firms.

Difference-in-Differences Analysis on the SHHKSC Program With SZHKSC Program Firms as Control Group.

Note. This table presents DiD analysis of the SHHKSC sample with the program firms in the SZHKSC program as control group. The sample comprises 1,882 firm-period observations for 1,022 firms, and 1-year periods before and after the launch month of SHHKSC on November 17, 2014. Panel A reports the distribution of the sample by treatment dummy and event. Panel B displays the summary statistics of the stock connect sample and compares the treatment firms with control firms. Panel C exhibits the regression results of the DiD model, with standard errors clustered at the firm level. Numbers in parentheses represent t-values. SH-HK SC = Shanghai-Hong Kong Stock Connect; SD = standard deviation; ROA = return on assets.

**, and *1%, 5%, and 10% levels of significance, respectively.

Panel B of Table 4 displays summary statistics for the matched sample and compares the treatment and control firms. Although the two groups exhibit significant differences in many characters, we note that using the SZHKSC program firms as a control group helps to reduce systematic differences between the program and non-program firms. Specifically, the difference in firm size and share turnover, which are two explicitly stated selection criteria in selecting SHHKSC stocks, become both economically and statistically smaller. 15 Moreover, differences in the top ownership proportion and analyst coverage between the two groups become insignificant.

We apply the DiD design in the following form to test for an impact of non-segmented foreign ownership on synchronicity:

where

Panel C of Table 4 reports the results from our DiD analysis. Consistent with our hypothesis, the coefficient of the interaction of the treatment dummy and the post-event dummy is negative (coef = −0.071) and statistically significant (p = .0540), indicating that the stock return synchronicity for domestic securities of the treatment firms indeed falls after the launch of the programs when compared to the control firms.

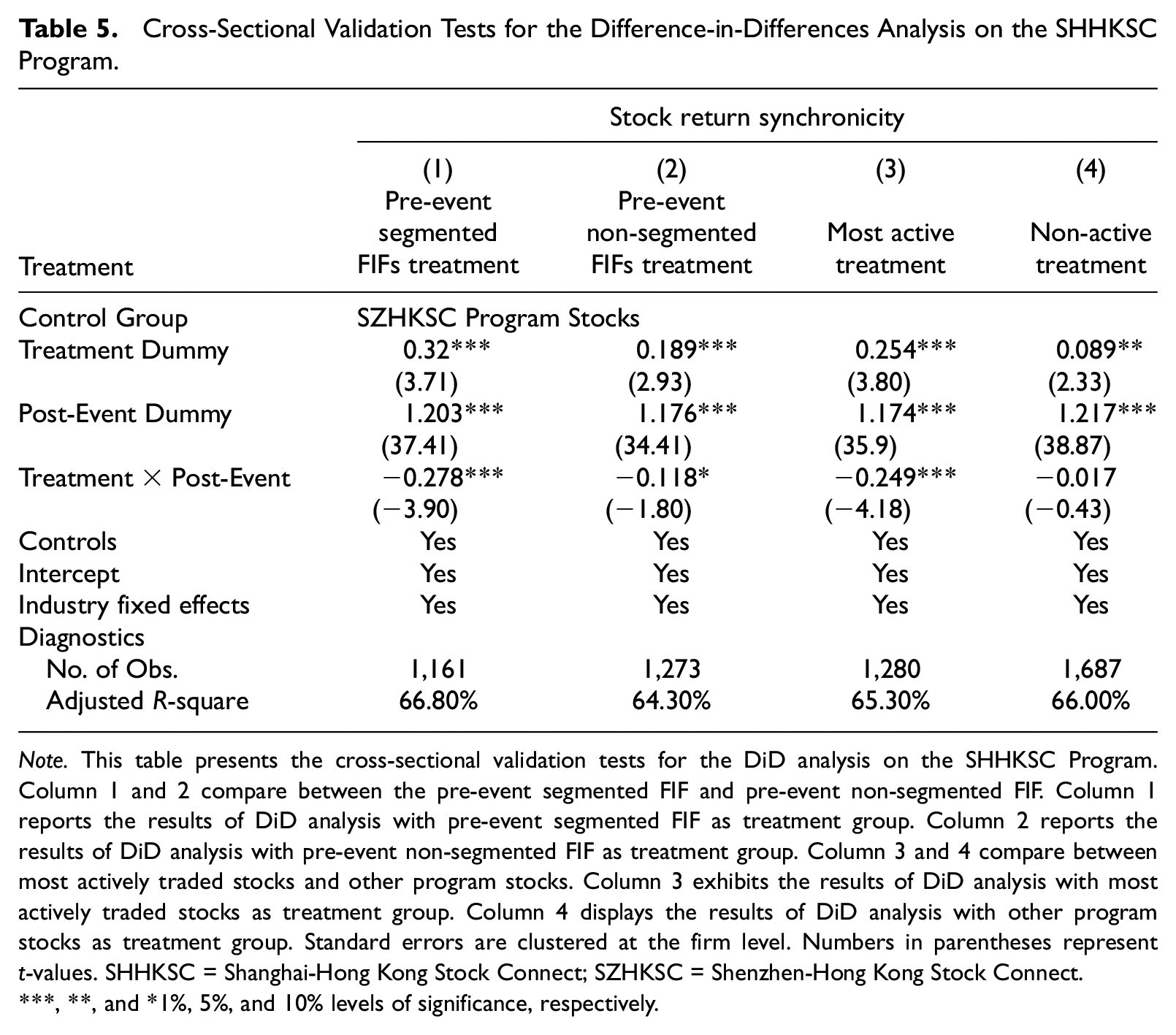

Pre-event segmented FIF vs. pre-event non-segmented FIF

If non-segmented foreign investment lowers the return synchronicity for domestic securities, in the cross-section, we should observe a greater impact of the stock connect events on the pre-event segmented FIF than on the pre-event non-segmented FIF, because the latter has already been accessed by foreign investors. Hence, in this section, we compare the pre-event segmented FIF as the treatment group and the pre-event non-segmented FIF as the treatment group. Pre-event segmented FIF are defined as segmented FIF at the end of 2013. The control group is still SZHKSC stocks.

Column 1 of Table 5 reports the results from our DiD analysis with the pre-event segmented FIF as the treatment group. Column 2 uses pre-event non-segmented FIF as the treatment group. Consistent with expectations, the coefficient on the interaction of the treatment dummy and the post-event dummy in Column 1 is economically large and statistically significant (coef = −0.278 and p < .0001), while the coefficient on the interaction in Column 2 is barely significant (coef = −0.118 and p = .0720). These results provide some evidence that the impact of the stock connect event on the pre-event segmented FIF is greater than that on the pre-event non-segmented FIF. This indicates that non-segmented foreign ownership indeed lowers the synchronicity for the domestic securities.

Cross-Sectional Validation Tests for the Difference-in-Differences Analysis on the SHHKSC Program.

Note. This table presents the cross-sectional validation tests for the DiD analysis on the SHHKSC Program. Column 1 and 2 compare between the pre-event segmented FIF and pre-event non-segmented FIF. Column 1 reports the results of DiD analysis with pre-event segmented FIF as treatment group. Column 2 reports the results of DiD analysis with pre-event non-segmented FIF as treatment group. Column 3 and 4 compare between most actively traded stocks and other program stocks. Column 3 exhibits the results of DiD analysis with most actively traded stocks as treatment group. Column 4 displays the results of DiD analysis with other program stocks as treatment group. Standard errors are clustered at the firm level. Numbers in parentheses represent t-values. SHHKSC = Shanghai-Hong Kong Stock Connect; SZHKSC = Shenzhen-Hong Kong Stock Connect.

**, and *1%, 5%, and 10% levels of significance, respectively.

Most actively traded stocks vs. other program stocks

If “informed trading” is the mechanism that incorporates foreign investors’ private information into domestic prices, then we expect to observe a greater impact of the stock connect events on the most actively traded program stocks relative to other program stocks. Since January 2015, the HKEx publishes the monthly top 10 active SHHKSC stocks through northbound trading. 16 We define the most actively traded stocks as the stocks that are listed in the monthly top 10 at least once during the post-event period, and from this, we obtain the 101 most active SHHKSC stocks. The rest are defined as other program stocks.

Column 3 of Table 5 reports the results from our DiD analysis using the matched sample with the most actively traded SHHKSC stocks as the treatment group. Column 4 uses the other SHHKSC stocks as the treatment group. Consistent with expectations, the coefficient on the interaction of the treatment dummy and the post-event dummy in Column 3 (coef = −0.249 and p < .0001) is larger in economic magnitude and more significant in statistical magnitude than that in Column 4 (coef = −0.017 and p = .6660). The coefficient on the interaction term is even insignificant using the other SHHKSC stocks as the treatment group. These results support our argument that the impact of the stock connect events on the most actively traded program stocks is greater than that on the other SHHKSC stocks. This again indicates that trading activities of foreign investors lower the return synchronicity for domestic securities.

Robustness check with the SZHKSC event

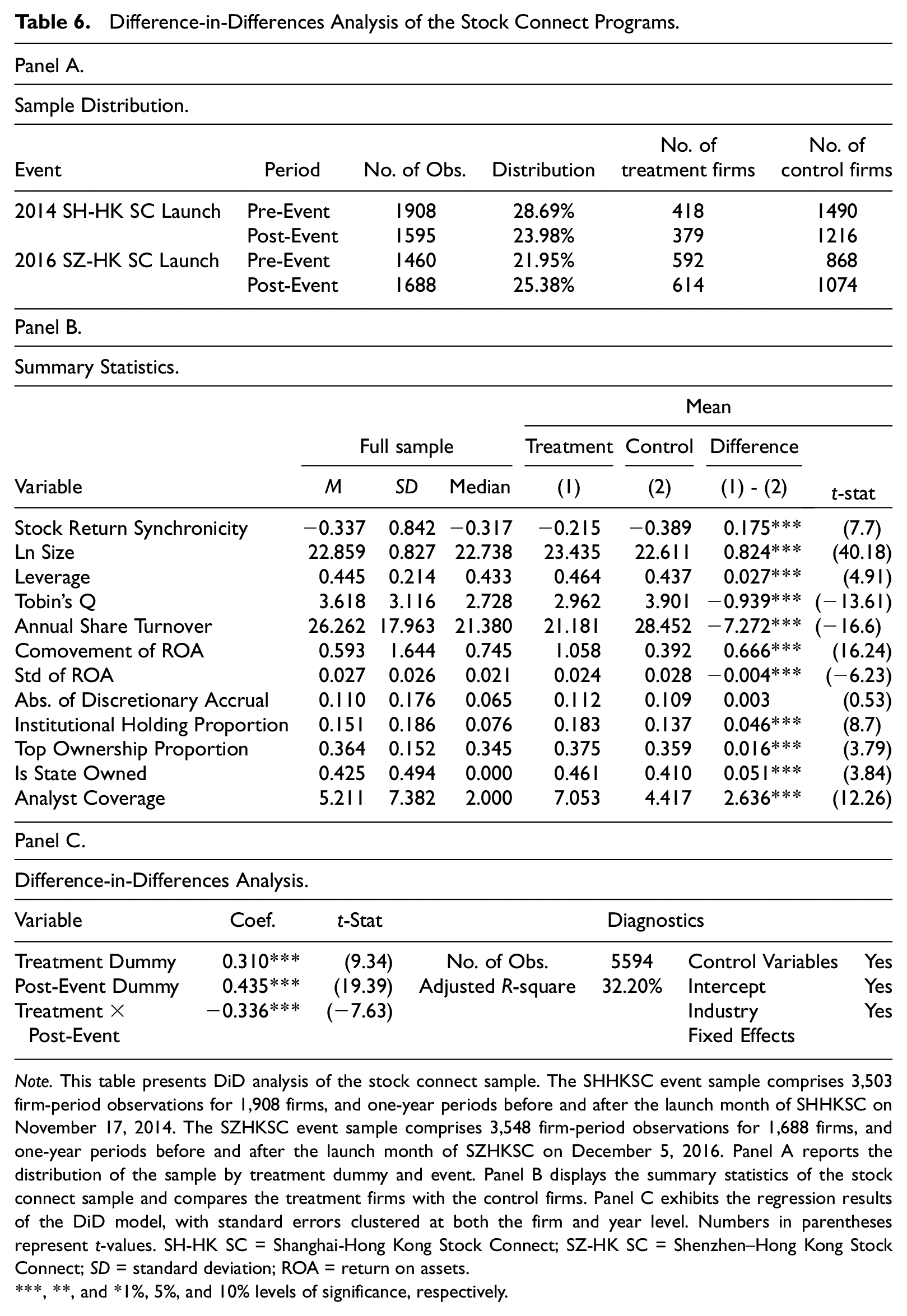

In this sub-section, we conduct a robustness check using the SZHKSC event. In contrast to the previous test, we use the SHHKSC and SZHKSC program stocks as the treatment group and use the remaining A share firms as the control group. For the SZHKSC event, we exclude the SHHKSC program stocks from our sample because they are neither affected by the SZHKSC event nor can be used as the control group.

We construct a periodic measure of synchronicity for a stock using daily trading data and Equation 1, requiring at least 200 trading days for each period. The final sample is comprised of 6,651 firm-period observations for 2,501 firms listed on the SSE and SZSE.

Panel A of Table 6 shows the distribution of our sample firms across periods for the treatment and control groups. The number of firms in the post-event period for the SHHKSC event (1,595) is less than in the pre-event period (1,908). This is due to many trading halts during the Chinese A-share market boom in the last quarter 2014 and the first half of 2015.

Difference-in-Differences Analysis of the Stock Connect Programs.

Note. This table presents DiD analysis of the stock connect sample. The SHHKSC event sample comprises 3,503 firm-period observations for 1,908 firms, and one-year periods before and after the launch month of SHHKSC on November 17, 2014. The SZHKSC event sample comprises 3,548 firm-period observations for 1,688 firms, and one-year periods before and after the launch month of SZHKSC on December 5, 2016. Panel A reports the distribution of the sample by treatment dummy and event. Panel B displays the summary statistics of the stock connect sample and compares the treatment firms with the control firms. Panel C exhibits the regression results of the DiD model, with standard errors clustered at both the firm and year level. Numbers in parentheses represent t-values. SH-HK SC = Shanghai-Hong Kong Stock Connect; SZ-HK SC = Shenzhen–Hong Kong Stock Connect; SD = standard deviation; ROA = return on assets.

**, and *1%, 5%, and 10% levels of significance, respectively.

Panel B of Table 6 shows summary statistics for the stock connect sample and compares the treatment firms and the control firms. The mean and median stock return synchronicity are −0.337 and −0.317, respectively, which are slightly lower than for the pooled sample.

Panel C of Table 6 reports the results from our vanilla DiD analysis using the full stock connect sample. Consistent with our prediction, the coefficient on the interaction of the treatment dummy and the post-event dummy is negative (coef = −0.242) and statistically significant (p < .0001), indicating that the two events reduce the stock return synchronicity of the program firms relative to the non-program firms.

The Governance Hypothesis

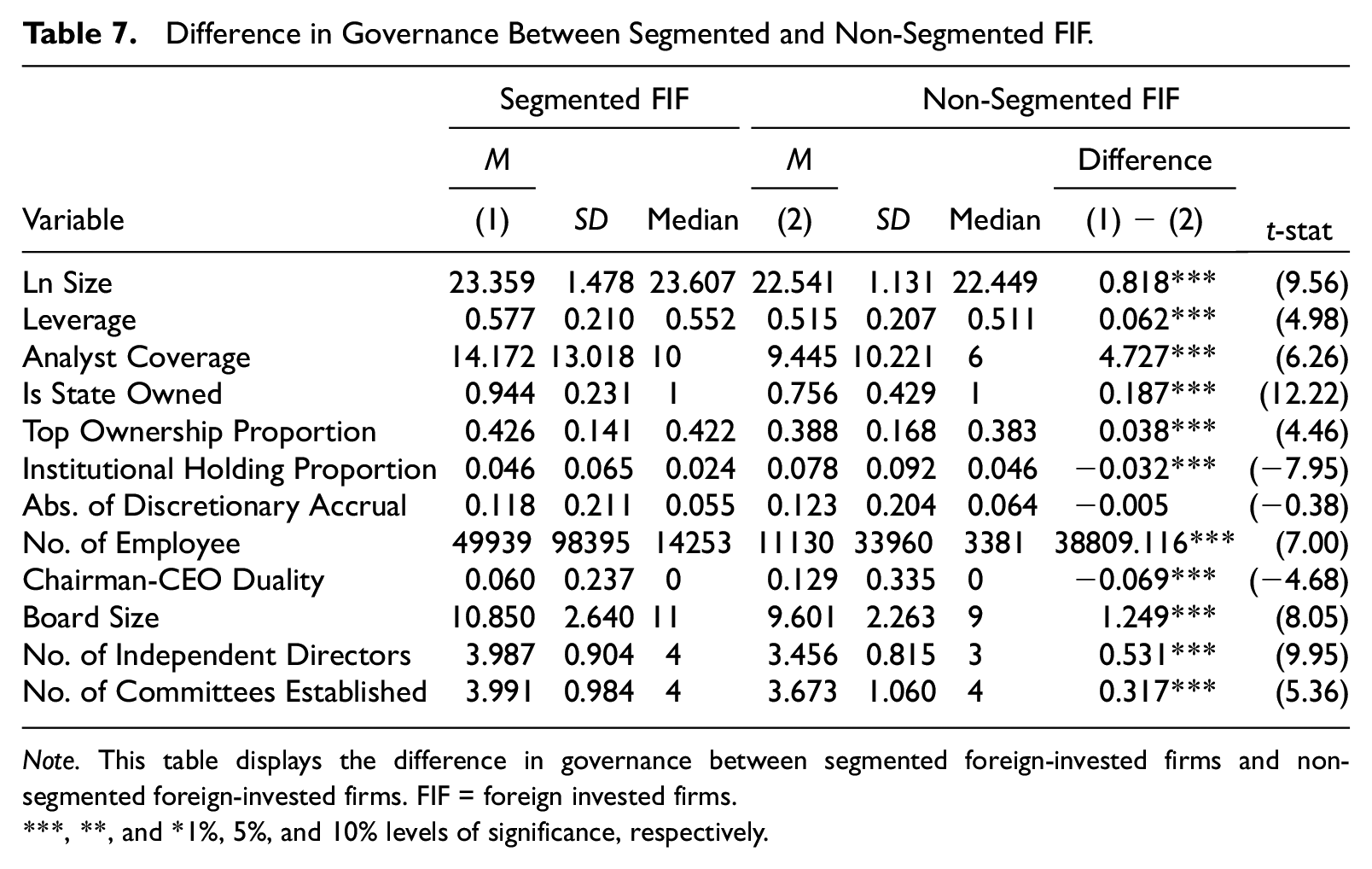

Prior empirical literature shows that foreign block holders can prompt positive governance changes in their investee firms, which increases the revelation of firm-specific information (Cheng et al., 2010; Kahn & Winton, 1998; Maug, 1998). We note, however, that if this argument is true, it should apply to all FIF. To the extent that our study focuses on the heterogeneous impact of segmented versus non-segmented foreign ownership, the governance hypothesis will contaminate our result if non-segmented FIF have better governance than segmented FIF. However, we find the opposite. In Table 7, we compare a battery of corporate governance indicators for the segmented versus non-segmented FIF. We find that segmented FIF are significantly larger than non-segmented FIF. Segmented FIF also excel in many corporate governance metrics, including larger board size, larger number of independent directors and board committees, higher analyst coverage, and lower chairman-CEO duality. Supplemental Table IA of the internet Appendix formally tests the impact of heterogeneous foreign investment on the firm’s disclosure quality and finds no difference in disclosure quality between segmented and non-segmented FIF.

Difference in Governance Between Segmented and Non-Segmented FIF.

Note. This table displays the difference in governance between segmented foreign-invested firms and non-segmented foreign-invested firms. FIF = foreign invested firms.

**, and *1%, 5%, and 10% levels of significance, respectively.

As a robustness check, we access the directors’ biographies for all FIF. We find no board seats occupied by foreign block holders and no proxy fights or securities actions brought by foreign institutions. This evidence is consistent with findings in Becht et al. (2009), that for U.S.-style corporate governance to be effective, a domestic institutional environment that is friendly to activist shareholders is important, and with findings in Fung et al. (2013) and Ke et al. (2012), which shows that in a weak legal investor protection environment like China, the corporate governance role of foreign block holders is minimal.

Conclusion

This study investigates the impact of heterogeneous foreign investment on the stock price informativeness in China’s nascent A-share market. Exploiting the distinction between segmented and non-segmented foreign investment, as well as the unique institutional settings of China, we find that non-segmented foreign investment reduces firms’ stock return synchronicity, while segmented foreign investment does not. Further evidence from the stock connect programs validates this proposition: we find that an exogenous increase in non-segmented foreign ownership reduces the synchronicity of program firms relative to the control firms.

Our results are more consistent with the “informed trading” explanation than with the “learning” or “governance” explanation of the impact of foreign investment on stock price informativeness. This evidence can inform governments in emerging markets who wish to utilize foreign investment to improve the quality of their domestic stock markets. This article shows that from a policy objective of stock price informativeness, allowing foreign investors to access domestic markets is more effective than allowing domestic firms’ securities to be traded only in foreign markets.

Supplemental Material

sj-docx-1-jaf-10.1177_0148558X211042953 – Supplemental material for Foreign Investment and Stock Price Informativeness: Evidence From the Shanghai (Shenzhen)–Hong Kong Stock Connect

Supplemental material, sj-docx-1-jaf-10.1177_0148558X211042953 for Foreign Investment and Stock Price Informativeness: Evidence From the Shanghai (Shenzhen)–Hong Kong Stock Connect by Zhen Lei and Haitian Lu in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Acknowledgements

The authors wish to thank the editor, associate editor, and anonymous reviewers for the diligent review and excellent comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study received funding support from Hong Kong Government RGC-GRF PolyU 156057/15H.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.