Abstract

This study investigated the spillover effects of geopolitical risks on energy (crude oil, coal and natural gas) markets. The empirical evidence is based on the CoVaR index and the CAViaR-EGARCH model. Results demonstrate that the spillover effects of geopolitical risks on the global energy market are nonlinear, asymmetric and time-varying. With each 1% rise in global geopolitical risks, the left tail risks in the crude oil, coal, and natural gas markets decreased by 0.179%, 0.119% and 0.113%, while the right tail risks increased by 0.144%, 0.135% and 0.097%, respectively. In addition, the magnitude of energy crises triggered by different geopolitical events varies. Lastly, the spillover effects of GPR on energy markets vary considerably across nations, with more substantial effects observed on average in BRICS than in G7 countries. The primary implication is to provide references for government and energy investors to avoid energy market risks timely.

Introduction

Energy resources are the fundamental driving force behind modern economic development, which is pivotal in safeguarding national economic and social well-being. The smooth operation of economic and social systems throughout the globe is substantially impacted by the stability of the energy markets (Nyangarika et al., 2019; Sivaram and Saha, 2018; Wen et al., 2019). According to the International Energy Agency (IEA), ensuring energy security necessitates stabilizing energy supply and pricing. Nevertheless, as the global economy becomes more interconnected, the externalities resulting from fluctuations in national energy markets are experiencing an upward trend. Furthermore, the 21st century has witnessed heightened instances of regional conflicts, social upheaval, and geopolitical strains, encompassing notable occurrences such as the 9/11 incident, the U.S. invasion of Afghanistan, the war in Iraq, the London bombings, terrorist attacks in Paris, and the Russia–Ukraine conflict. These occurrences have frequently triggered violent conflicts and even economic downturns (Li et al., 2023). Within the present intricate and unpredictable global environment, reconfiguring the global energy supply–demand landscape has resulted in disorderly energy prices. Moreover, the above instability is exacerbated by the concentration of nations that produce energy in geopolitically unstable regions. The previously mentioned scenario has significantly jeopardized the interests of international investors and posed threats to the economic progress and public safety of nations worldwide. Consequently, these circumstances prompt us to reflect on and explore the intricate relationship between geopolitics and the energy market.

Many energy crises have occurred throughout history due to geopolitical conflicts involving the primary energy-producing nations. During the Iran–Iraq War in 1979, international oil prices rose from $14.50/barrel to over $40/barrel, causing stagflation in Europe and the United States. In August 1990, Iraq invaded Kuwait, and the UN subsequently imposed an oil embargo on Iraq, triggering a rise in international oil prices from $16/barrel in July to $26/barrel in September. In February 2022, Russia launched an extraordinary military action against Ukraine, after which the European countries and the United States imposed broad sanctions against Russia. This conflict led to massive shocks in global energy markets, with Brent crude oil futures jumping to nearly $140/barrel in March 2022, the highest level since 2008. As Europe's energy crisis deepened, Dutch TTF gas prices peaked in August 2022. E.U. countries were generally plagued by rising energy prices, leading to severe impacts on livelihoods and industry, causing widespread concern. The empirical evidence of energy crises has once again underscored the significant influence of geopolitical risks on the security of energy at both global and regional levels (Antonakakis et al., 2017; Bompard et al., 2017; Cunado et al., 2020). Given this perspective, it is paramount to analyze the ramifications of geopolitical risks on the energy market, as it plays a crucial role in safeguarding energy security and maintaining the stability of the global economy.

This paper uses crude oil, natural gas, and coal to represent energy (Stenvall et al., 2022; Zolfaghari et al., 2020) while utilizing the prices of Brent crude oil, South African coal, and Dutch TTF natural gas as representative indicators for energy prices. These are the primary reasons: In market significance, the types of these energies are different, which facilitates a comprehensive analysis of the spillover effect of geopolitical risk on the energy industry. Additionally, these energy types are extensively traded in the global energy market, thereby exerting a significant influence on the dynamics of the global energy market (Kuik et al., 2022; Wang et al., 2022) and the overall economic situation (Ma et al., 2021; Yao et al., 2020). In geographic diversity, this study selects energy commodities from various continents, enhancing the examination of the role of geopolitical risk in specific regional energy markets. For instance, Brent oil serves as the global price benchmark for crude oil, while the Dutch TTF gas has emerged as a significant European gas hub, playing a crucial role in the European energy landscape. Additionally, South African coal is the windsock for coal prices throughout Africa. On the sensitivity to geopolitical risks, the study shows that Brent oil, Dutch TTF gas, and South African coal are all vulnerable to geopolitical factors and are thus more persuasive in characterizing the response of energy markets to geopolitical risk spillovers (Abdel-Latif et al., 2020; Amineh and Crijns-Graus, 2018; Banya, 2022).

Specifically, the decent objectives of this paper can be stated as follows:

This article constructs a CAViaR-EGARCH model incorporating geopolitical risk to examine the transmission of tail risk spillover from geopolitics to the energy market to make a marginal contribution. Within the global landscape characterized by a rise in localized conflicts, social upheaval, and heightened tensions, clarifying the ramifications of geopolitical risks on the energy market becomes imperative. This study offers a pragmatic framework for protecting global energy security and the interests of international energy investors.

The rest of the paper is organized as follows. Section “Literature review” clarifies the underlying mechanisms of geopolitical risk spillovers to energy markets and reviews existing research on the relationship between geopolitical risk and energy market volatility. Section “Methodology and data” presents the model constructed in this paper and describes the sources and characteristics of the data. Section “Results and discussion” provides the results of our tests, encompassing four parts: parameter estimation, spillover effect assessment, spillover effect simulation, and risk spillovers from GPR in different countries. The last section reports the findings of this paper.

Literature review

The mechanisms by which geopolitical risks affect energy markets are multifaceted and intricate. First, the emergence of heightened geopolitical risks will force energy-exporting nations to modify their energy supply policies, resulting in a notable level of uncertainty regarding the quantity and price of global energy commodity supplies (Cunado et al., 2020; Liu et al., 2019, 2021; Sharma et al., 2021). For instance, when the fourth Middle East war broke out in 1973, the Arab nations within the Organization of Petroleum Exporting Countries (OPEC) initiated an oil embargo against select countries. This action resulted in a substantial escalation of the international oil price, surging from under $3/barrel in 1973 to over $13/barrel, triggering the 1973 oil crisis. Secondly, geopolitical risk can potentially induce volatility in global economic activities, affecting energy demand (Ersin and Bildirici, 2023; Song et al., 2022; Yatsenko et al., 2018). Li et al. (2021) found that the rise of geopolitical risk will lead to the lower prices of coal and crude oil and the higher price of natural gas, inhibiting the total amount of energy imports and exports. Furthermore, the stability of the energy market is also significantly influenced by expectations regarding the trend in the evolution of energy supply and demand. These expectations are projected onto the overall sentiment of global investors and their trading decisions, subsequently impacting the current levels of energy inventories and prices (Balcilar et al., 2018; Bouoiyour et al., 2019; Kilian and Murphy, 2014; Su et al., 2019; Wang and Liao, 2022). Among them, changes in supply and demand expectations exert a more immediate influence, whereas modifications in actual supply and demand exert a longer-term impact on energy prices. Finally, geopolitical uncertainty will disrupt energy markets through the indirect mechanism of financial linkage networks (Li and Umair, 2023; Ouyang et al., 2021; Shahzad et al., 2023). Based on the above theoretical analysis, it can be concluded that geopolitical risk exists objectively in the formation mechanism of energy supply demand and price. Therefore, this study considers evaluating the marginal explanatory power of geopolitical risk for volatility in energy markets.

The impact of geopolitical risk on the global economy is apparent. However, due to the inherent challenges in quantifying geopolitical risk, initial studies primarily focused on examining the consequences of particular geopolitical occurrences, such as the impact of terrorist events on commodity and stock markets (Ramiah et al., 2019), and the effects of geopolitical events on oil prices (Noguera-Santaella, 2016). In recent years, certain scholars have clearly defined and quantified geopolitical risk (Hu and Li, 2023; Liu and Tao, 2023; Neacşu, 2016). Among them, the GPR index proposed by Caldara and Iacoviello (2022) is quite notable. This index is derived from news reports about geopolitical circumstances and effectively portrays various geopolitical occurrences, including acts of terrorism, military provocations, and regional instabilities. Several studies have demonstrated the scientific validity of the GPR index (Aysan et al., 2019; Mei et al., 2020), which has thus been widely used in the empirical literature (Alam et al., 2023; Bossman et al., 2023; Bussy and Zheng, 2023; Zheng et al., 2023). This study employs the measure developed by Caldara and Iacoviello (2022) to investigate the influence of the time-series monthly GPR index on volatility within the energy market.

With the maturity of measurement methods, scholars have extensively discussed the correlation between geopolitical risks and energy market fluctuations. Qin et al. (2020) examined the asymmetric effects of geopolitical risk on energy returns and volatility using a quantile regression model. Aslam et al. (2022) employ the multifractal detrended cross-correlation analysis to investigate the nonlinear structure and multi-component behavior between geopolitical risks and energy markets. Shahbaz et al. (2023) analyzed to examine the causal association between oil price movements and geopolitical risks through the Granger causality within quantiles. Hence, further analysis from a time-varying perspective is necessary. Lau et al. (2023) employed the variational mode decomposition-based copula method to identify the dependency structure between crude oil prices and geopolitical risks, exhibiting both time-varying and frequency-varying characteristics. Additionally, Jin et al. (2023) investigated the dynamic relationship particularly pronounced at high frequencies among geopolitical risk, energy risk, and climate risk using the BEKK-GARCH and BK models.

Although the existing literature fills the research gap in examining the dynamic influence of geopolitical risk on energy markets, it falls short in identifying tail risk spillovers between the two. The global financial crisis in 2008 has underscored the necessity and urgency of capturing market tail risks and their correlations. Adrin and Brunnermeier constructed the conditional value-at-risk (CoVaR) model in 2008, which has gained widespread usage in empirical research as it better reflects the impact of extreme losses suffered by a particular institution (market) on other institutions (markets). For example, Keilbar and Wang (2022) calibrated the CoVaR of global systemically important financial institutions from the USA based on neural network quantile regression. The estimation results showed that their methodology accurately quantified the interbank risk spillover effect in the nonlinear and multivariable context. Tian and Ji (2022) proposed a CoVaR model based on GARCH copula quantile regression-based and proved it could capture nonlinear tail correlations at different risk levels and is more manageable than the time-varying copula model. However, the model has the drawback of being unable to calculate the upward risk spillover effect. Given the above, this paper uses CoVaR to quantify the tail risk of geopolitical and energy market.

In summary, the preceding research findings provide a substantial theoretical groundwork for this study and inspire research ideas, but aspects remain to be deepened. On the one hand, few literatures examine whether geopolitical risks trigger violent fluctuations in the energy market and the characteristics of such effects. On the other hand, studies testing the risk spillover effects of geopolitics on the energy market from a dynamic nonlinear, and asymmetric perspective are scarce, and the research needs to be improved.

The academic innovation of this paper lies in the following aspects: In terms of research perspectives, this paper focuses on the tail risk spillover of geopolitical to the energy market, and the findings will help the countries and investors to guard against extreme risks. In terms of research methodology, this paper uses CoVaR index to characterize tail risks and uses Cornish–Fisher method to calculate them, and constructs CAViaR-EGARCH model to test the tail risk spillover effect of geopolitical risks on energy markets, which can depict time-varying, asymmetric and nonlinear characteristics. In terms of research content, this paper selects three primary energy sources as the object and further explores the impact of different geopolitical events and geopolitical risks of different countries on the international energy market. This dramatically distinguishes this paper from the present research and is innovative.

Methodology and data

Methodology

VaR is the maximum loss faced by assets at a specific confidence level q. Specifically, VaR is defined in terms of the 1-q percentile of the yield distribution.

The spillover effect of geopolitical risks on the energy market in this study is expressed by the conditional value at risk (CoVaR).

C(q) is the q percentile of the standard normal distribution. μ, σ, s and k are the return series’ mean, variance, skewness and kurtosis, respectively.

We construct the CAViaR-EGARCH model and add the geopolitical risk index to it to measure the VaR value. The model is stated as follows:

Where rt denotes energy returns; xt denotes global geopolitical risks; ht is the conditional variance of energy revenue series; ε1t and ε2t are residual series. c0, ci, b, ω, αi, βj, γk,

Data source and descriptive statistics

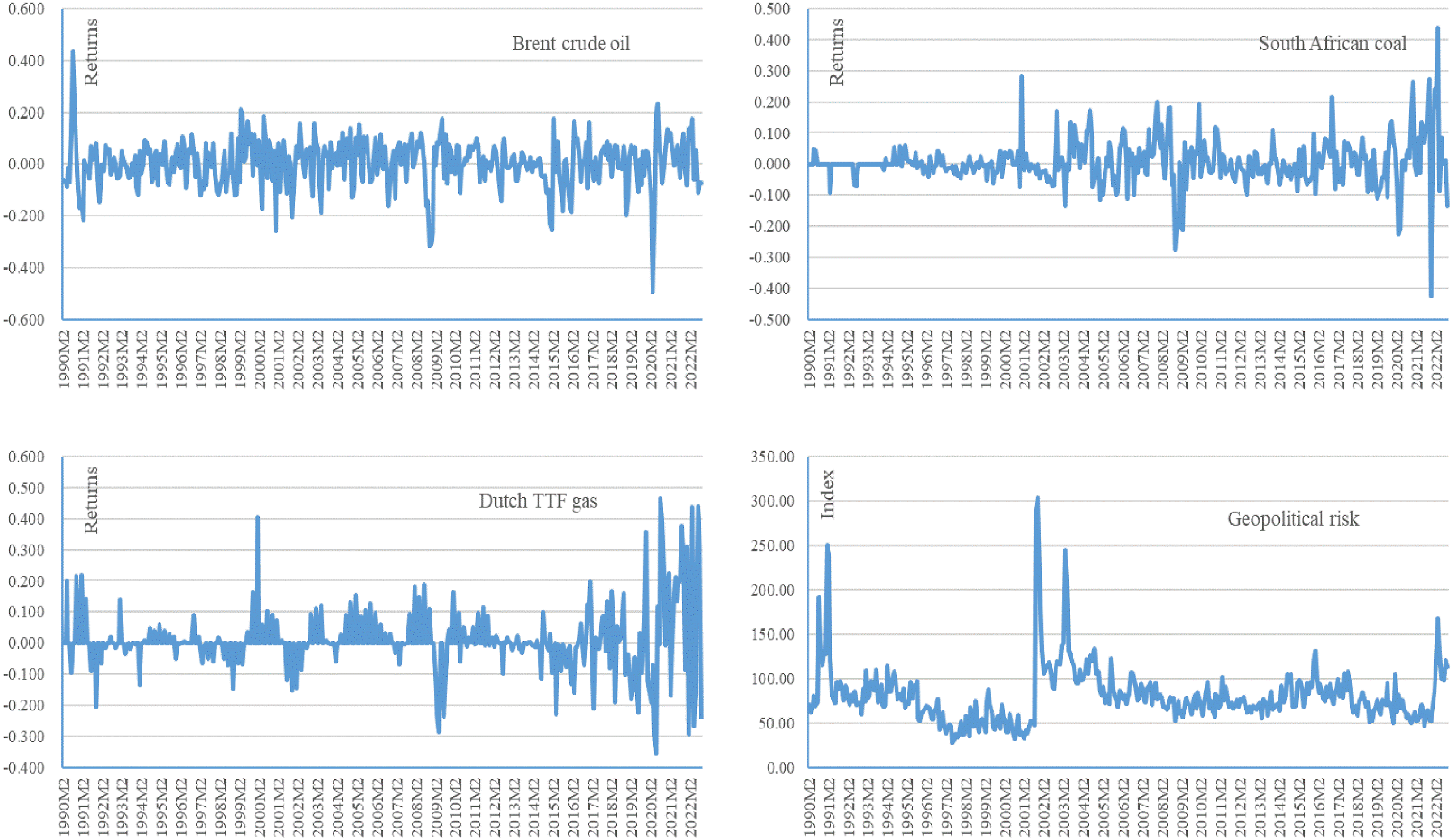

The International Geopolitical Risk Index (GPR) was published by Caldara and Iacoviello (2022). 1 Brent crude oil, South African coal and Netherlands TTF natural gas prices are obtained from the IMF's commodity price database. 2 The data were sampled by monthly frequency from January 1990 to September 2022, with 393 sets of data. Figure 1 reports the variation characteristics of energy market returns and the geopolitical risk index. The trend chart of the geopolitical risk index shows that the global geopolitical risks and threats increased after 9-11 compared to before 9-11. In addition, Figure 1 shows that after the events of the U.S. invasion of Afghanistan, the Iraq War, and the Russia–Ukraine conflict, major energy markets such as crude oil, coal, and natural gas all experienced significant volatility. Especially after the outbreak of the Russian–Ukrainian conflict, the coal and gas market has experienced historic shocks.

Energy market returns and geopolitical risk index.

Table 1 reports the descriptive statistical results of each variable. The statistical characteristics of the energy return data show that the average rates of returns of the three energy sources are all positive, but the fluctuation range of the crude oil and natural gas market is greater than that of the coal market; the skewness of crude oil yield is negative, while the skewness of natural gas and coal yield is positive. These indicate a greater probability of negative returns in the crude oil market, i.e. companies are more exposed to the depreciation of crude oil assets than to asset appreciation after purchasing crude oil. The natural gas and coal markets have a higher probability of positive returns, i.e. companies are less exposed to asset depreciation after purchasing natural gas and coal. The kurtosis of the return series is greater than 3, indicating more extreme values in the data compared to the normal distribution. From the perspective of skewness and kurtosis, the minimum value of crude oil price appears more than the maximum value, while coal and natural gas prices have fewer minima than maxima. In addition, the ADF unit root test indicates that all four series are stationary sequences.

Descriptive statistics and results of the ADF test.

Note: ***, ** and * indicate significance at the 1%, 5% and 10% levels, respectively.

Results and discussion

Parameter estimation results

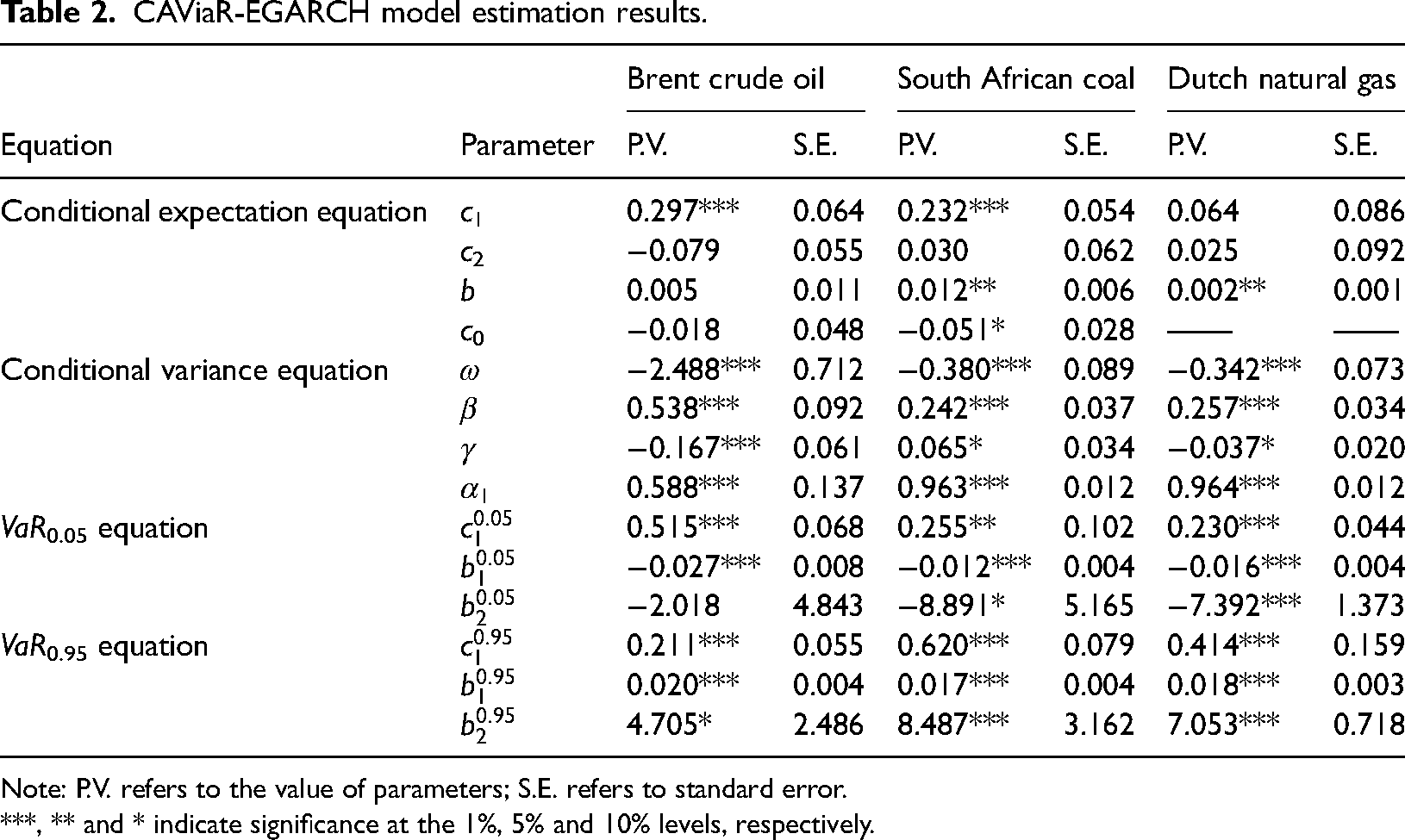

MATLAB was used to estimate the parameters of the CAViaR-EGARCH model. Table 2 reports the results of parameter estimation for equations (7)–(9). The estimation results of the conditional expectation equation indicate that the return series of Brent crude oil and South African coal have first-order positive correlation characteristics, while geopolitical risks have a positive effect on the average return. For each 1% increase in global geopolitical risk, South African coal's average rate of returns increases by 0.012 units, and the average rate of returns of Dutch natural gas increases by 0.002 units. Moreover, the estimation results of the conditional variance equation indicate a first-order positive correlation in return volatility. The “leverage effect” exists in all three energy markets. In the Brent crude oil market, good news will bring 0.371 times the impact, while bad news will bring 0.705 times the impact; in the South African coal market, good news will bring 0.307 times the impact, while bad news will bring 0.177 times the impact; in the Dutch natural gas market, good news will bring 0.220 times the impact, while bad news will bring 0.294 times the impact. Meanwhile, the estimation results of the VaR0.05 and VaR0.95 equation suggest that the impacts of global geopolitical risk on the energy market's left and right tail risks are asymmetric. When the global geopolitical risk increases by 1%, the Brent crude oil market's left tail risk VaR0.05 decreases by 0.179%, while the right tail risk VaR0.95 increases by 0.144%; the South African coal market's left tail risk VaR0.05 decreases by 0.119%, while the right tail risk VaR0.95 increases by 0.135%; the Dutch natural gas market's left tail risk VaR0.05 decreased by 0.113%, while right tail risk VaR0.95 increased by 0.097%.

CAViaR-EGARCH model estimation results.

Note: P.V. refers to the value of parameters; S.E. refers to standard error.

***, ** and * indicate significance at the 1%, 5% and 10% levels, respectively.

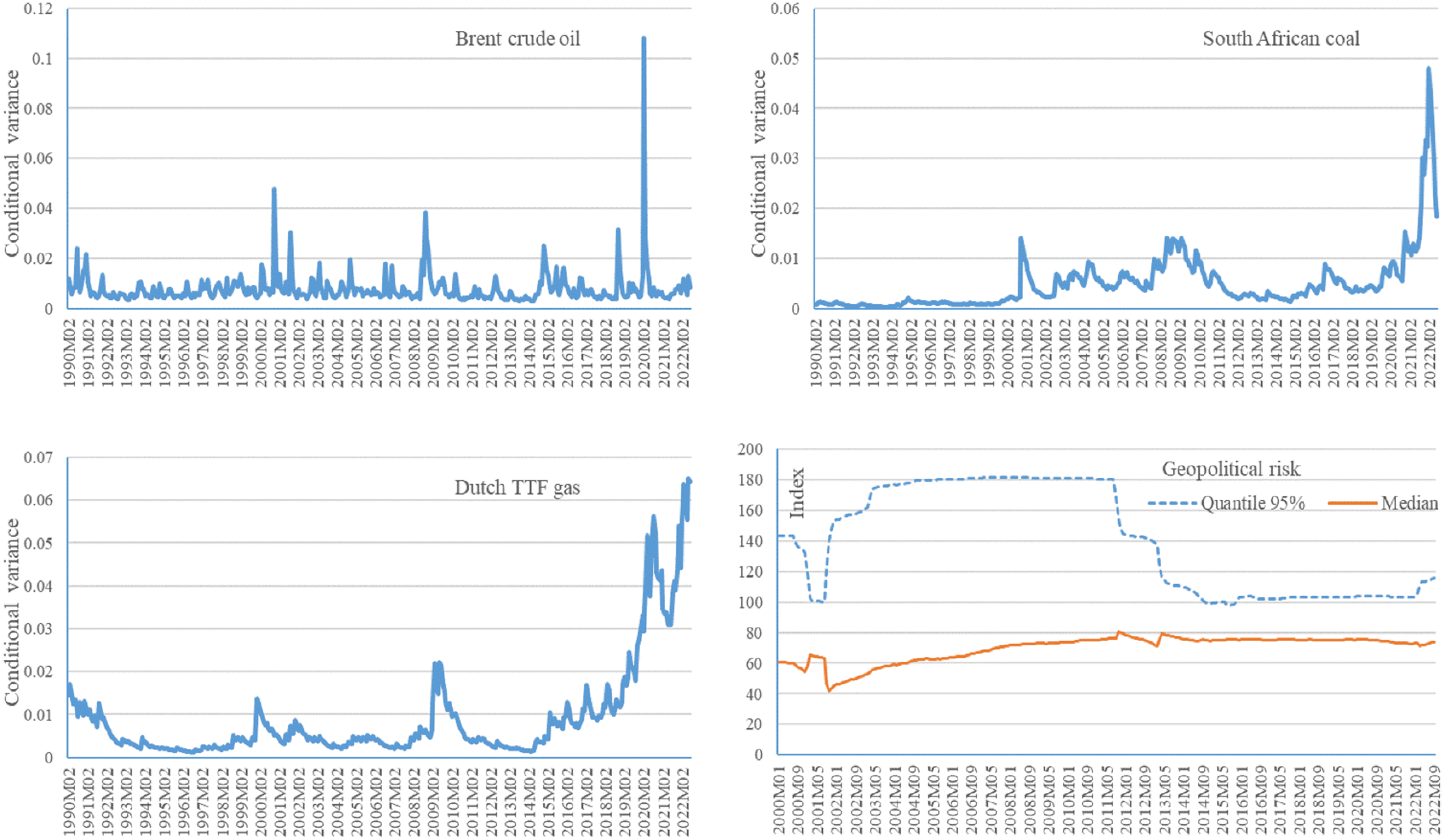

Further, the estimation results of the VaR0.05 equation and the VaR0.95 equation also indicate that the tail risk of the energy markets is significantly influenced by the volatility and the tail risk of the previous period, in addition to the geopolitical risk. Figure 2 reports the energy market volatility and geopolitical risk quantile. The results show that global geopolitical risks have increased significantly in recent years. At the same time, the energy market has fluctuated violently and has reached the highest level in history.

Energy market volatility and geopolitical risk quantiles.

Assessment of global GPR spillover effects

According to the three methods of historical simulation, Monte Carlo simulation and Cornish–Fisher, the tail risk value of the three energy markets is calculated, respectively. The results are as follows: the 0.95 quantiles of the geopolitical risk index are 127.546, 135.293, and 148.143, respectively, and the 0.5 quantiles are 75.005, 80.821 and 65.032, respectively. As measured by equation (8), the mean values of conditional variance for the three markets are 0.008, 0.005, and 0.009, respectively. CoVaR0.95, CoVaR0.05, ΔCoVaR0.95, ΔCoVaR0.05, % ΔCoVaR0.95, and % ΔCoVaR0.05 of the three energy markets from January 1990 to September 2022 can be calculated according to equation (9). Tables 3 and 4 report the relevant calculation results.

Right tail risk assessment values for energy markets.

Left tail risk assessment values for energy markets.

The results in Tables 3 and 4 show that when geopolitical risk changes from the median to the 0.95 quantiles, the Brent crude oil market increases right tail risk by approximately 11.515% and left tail risk by approximately 22.805%; the South African coal market increases right tail risk by approximately 22.225% and left tail risk by approximately 10.095%; and the Dutch natural gas market increases right tail risk by approximately 10.336% and left tail risk by approximately 9.518%. The above results support the view that geopolitical risks have asymmetric spillover effects on energy markets.

Simulation of global GPR spillover effects

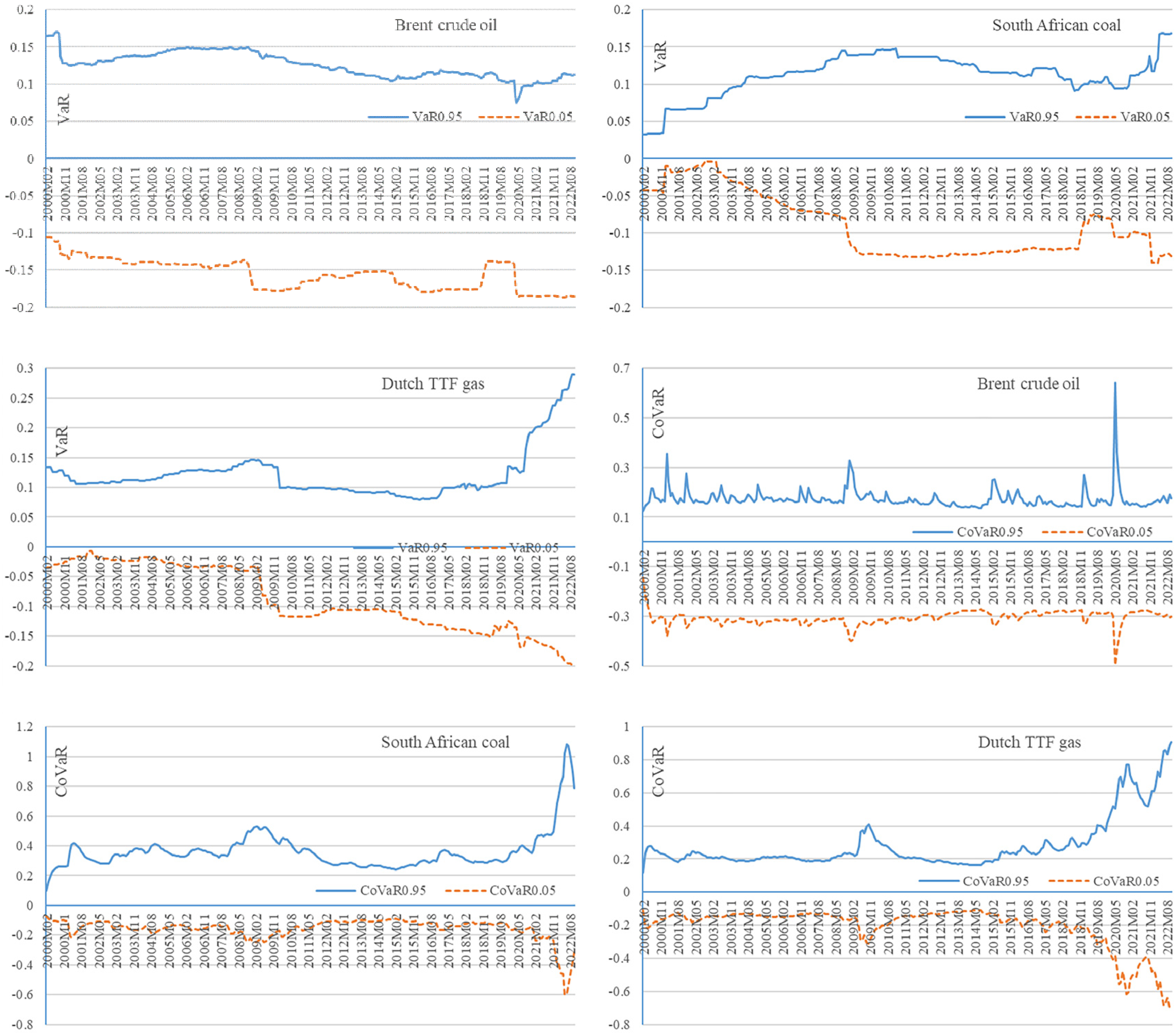

Figure 3 reports VaR and CoVaR simulation results in the energy market based on equations (6) and (9). According to the simulation results, the CoVaR values of the three energy markets are significantly higher than the VaR values. Over the period January 2000 to September 2022, the mean CoVaR0.95 values of the Brent crude oil, South African coal, and Dutch natural gas markets are 0.173, 0.362, and 0.283, respectively; the mean VaR0.95 values are 0.125, 0.112 and 0.121, respectively; the mean CoVaR0.05 values are −0.306, −0.157 and −0.208; the mean VaR0.05 values are −0.156, −0.090 and −0.088, respectively. Figure 3 shows the nonlinear, asymmetric, and time-varying characteristics of the spillover effects of geopolitical risk on energy markets. The left tail risk of the crude oil market is higher than the right tail risk, while the right tail risk of coal and natural gas markets is higher than the left tail risk. Since the Russia–Ukraine conflict, the risk exposure of the crude oil market has not changed much; the risk exposure of the coal market increased first and then decreased; the risk exposure of the natural gas market has continued to expand.

VaR and CoVaR of energy market simulation results.

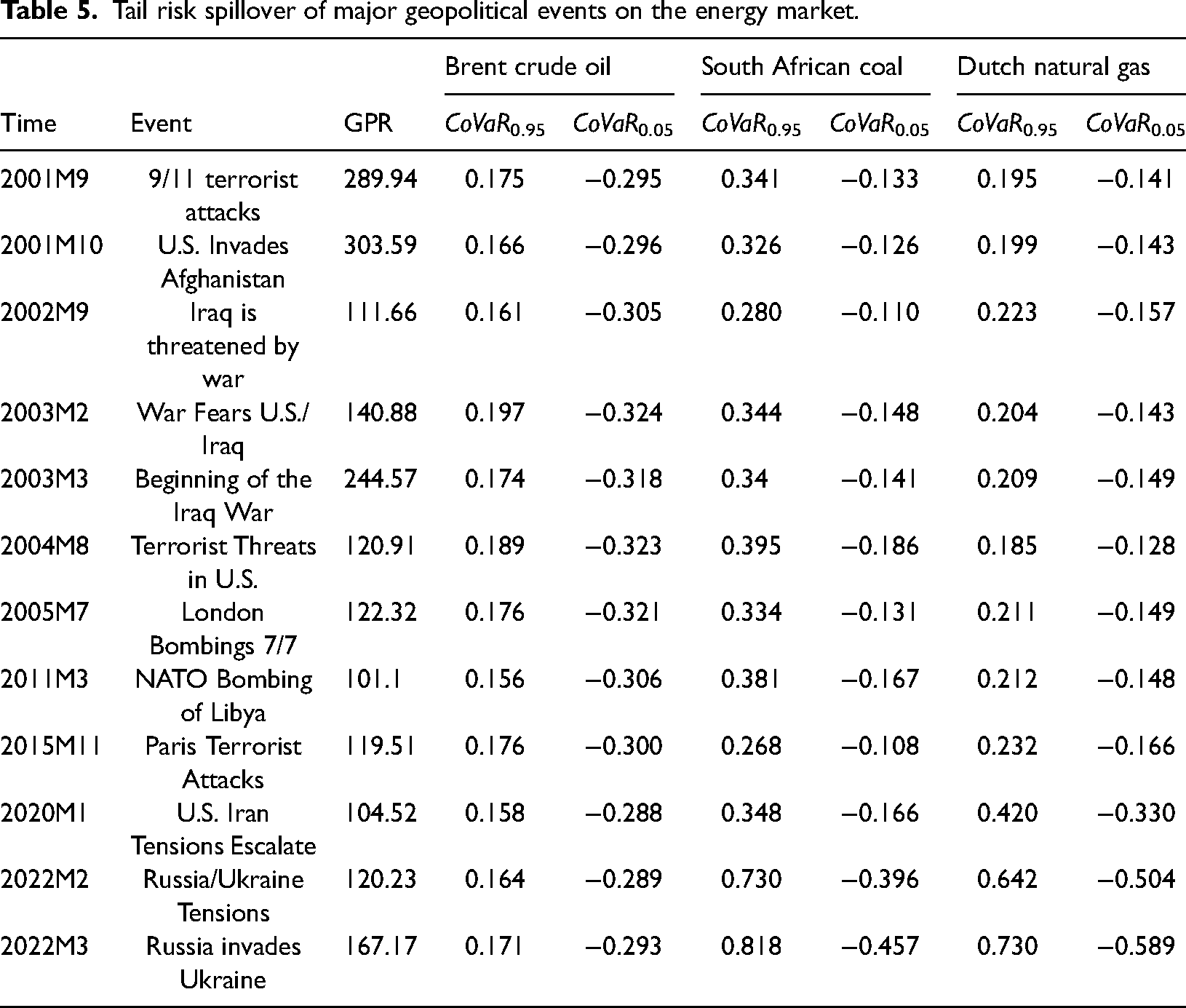

Table 5 reports the main events corresponding to the local peaks of the geopolitical risk index since the beginning of the 21st century, as well as the CoVaR values of energy markets after being affected by geopolitical risks. The results show that the impact of major geopolitical events on the tail risk of the Brent crude oil market differs little over time, while the natural gas market has seen a significant increase in condition risk since the deterioration of USA–Iran relations in 2020, and then the Russia–Ukraine conflict in 2022 has further pushed upmarket risks. Moreover, we find that major geopolitical events induce significantly more upside than downside risk in coal and natural gas markets, while in crude oil markets they induce significantly less upside than downside risk.

Tail risk spillover of major geopolitical events on the energy market.

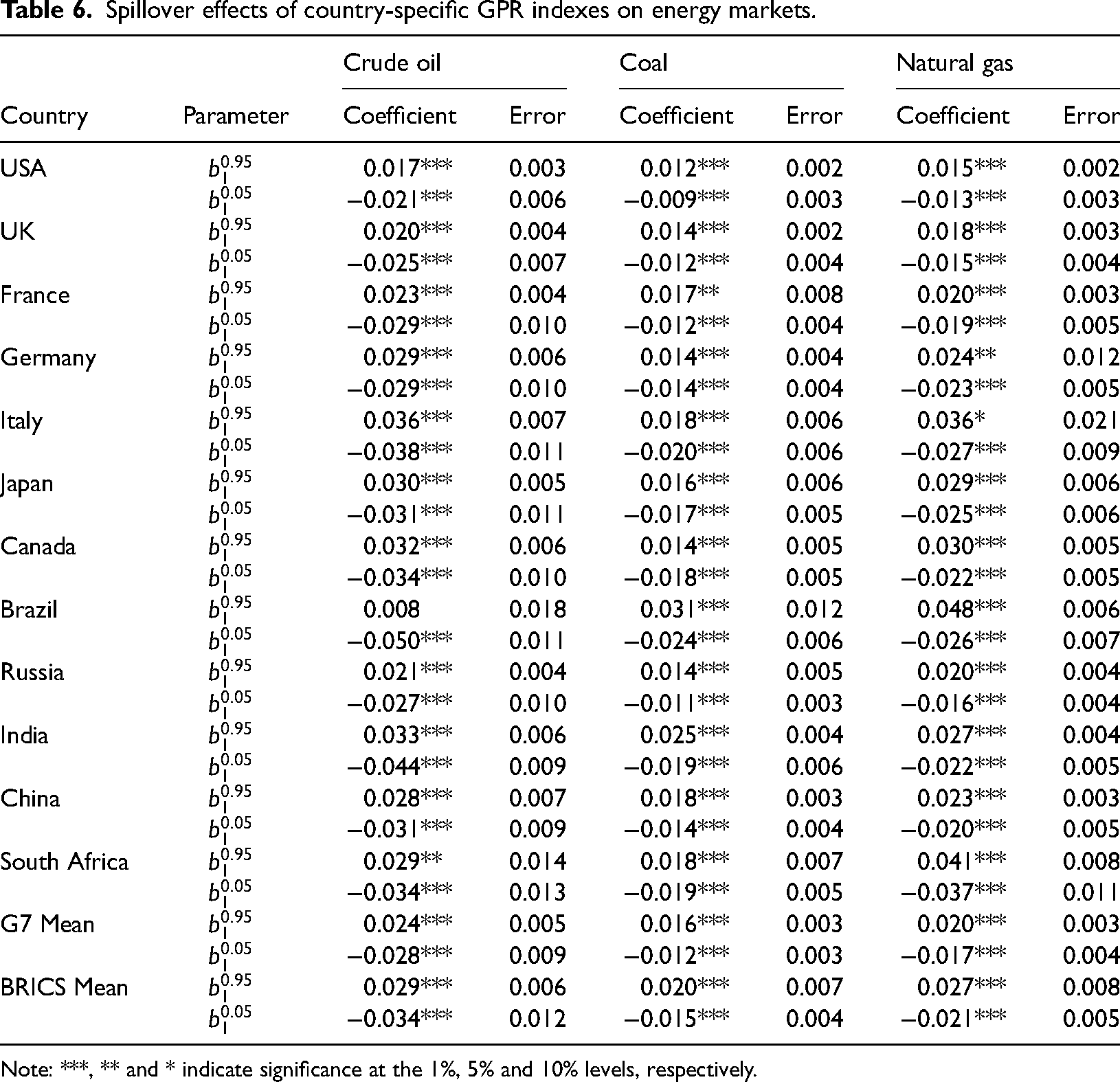

Spillover effects of GPR on energy markets in major countries

The spillover effects of Country-specific GPR indexes on energy markets are further measured and compared using equation (9) for a sample of Group of Seven, BRICS countries. 3 As shown in Table 6, the Country-specific GPR indexes have a significant spillover effect on the energy market. Except for a few countries such as Germany, the geopolitical risk indexes for most of the Group of Seven and BRICS countries have greater left-tail spillover effects on the crude oil market than the right-tail spillover effects, and more minor left-tail spillover effects on the coal and natural gas markets than the right tail spillover effects. It reaffirms that after 2000, the downside risk is greater than the upside risk in crude oil prices when hit by geopolitical risks, while the upside risk is greater than the downside risk in coal and natural gas markets. Taking the USA as an example, for every 1% increase in the GPR indexes, CoVaR0.95 in the crude oil market increases by 0.122%, and CoVaR0.05 decreases by 0.139%; the coal market CoVaR0.95 increases by 0.095% and CoVaR0.05 decreases by 0.089%; the natural gas market CoVaR0.95 increases by 0.081%, CoVaR0.05 decreased by 0.092%. On average, the spillover effect of BRICS countries ‘ geopolitical risks on the energy market is higher than that of Group of Seven countries.

Spillover effects of country-specific GPR indexes on energy markets.

Note: ***, ** and * indicate significance at the 1%, 5% and 10% levels, respectively.

Antonakakis et al. (2017) and Plakandaras et al. (2019) found that geopolitical risk negatively affected crude oil returns. Qin et al. (2020) suggested that geopolitical risk significantly negatively affected oil market returns at the lower quantiles but had no impact on gas returns in any quantile. These findings corroborate the argument of this paper to some extent. However, they do not consider whether geopolitical risk affects the return of energy commodities at the extreme (0.05 and 0.95 quantiles) situations. Additionally, Gong et al. (2023) showed a significant risk spillover effect between crude oil spot prices and geopolitical risk. Li et al. (2023) found that GPR had time-varying and heterogeneous characteristics on the volatility of crude oil and natural gas prices. The results of these studies are similar to this paper. Furthermore, the results of this paper show that geopolitical risk has time-lag characteristics in the energy market.

Conclusion

This paper employs the CoVaR and the CAViaR-EGARCH models to examine the dynamic spillover effects and tail characteristics of geopolitical risks on major global energy markets from 1990 to 2022. The empirical analysis results show that: First, the spillover effect of geopolitical risk on energy markets is nonlinear, asymmetric, and time-varying. In the crude oil market, geopolitical risk spillovers generate higher left tail risk than right tail risk, while the opposite is true for coal and natural gas markets. Second, major geopolitical risk events will lead to greater tail risk. Since 2020, the deteriorating relationship between the USA and Iran and the Russia–Ukraine conflict have pushed up energy market risk, with the upside risk induced by the two events being significantly greater than the downside risk in the coal and natural gas markets, but the opposite being true in the crude oil market. Third, the spillover effects of national GPRs on energy markets are comparable to those of global GPRs, but the spillover effects of GPR on energy markets vary significantly across nations. On average, the spillover effects of geopolitical risks on energy markets are generally higher in BRICS countries than in Group of Seven countries.

The findings of this paper provide valuable insights for countries to solidify their energy security and for energy investors to avoid market tail risks. On the one hand, given the heterogeneity of the spillover effects of geopolitical risks on various energy sources, energy market participants, including investors, enterprises, and governments, should formulate corresponding risk management strategies, such as diversified energy investment or reserve portfolios, to control geopolitical risk exposures and mitigate the risk of losses that specific energy commodities may bring about. On the other hand, tail geopolitical risks can induce tail risks in energy markets. Policymakers should establish early warning systems to monitor tail risk spillovers between geopolitical and energy markets in real-time and prepare crisis coping measures, such as promoting the diversification of energy sources, to minimize energy security risks and prevent and control imported financial risks.

The main highlights of this paper are as follows. First, a CAViaR-EGARCH model is constructed, and GPR is added to enhance energy market risk prediction accuracy. Second, the spillover effects of global and major country geopolitical risk indices and major risk events on the three major energy markets of crude oil, coal, and natural gas are evaluated. Third, the principal features and change patterns of the spillover effects of geopolitical risks on the three major energy markets are identified. The limitations are as follows. First, the GPR is derived from the frequency of geopolitical risk phrases in the U.S. media and does not reflect the media coverage in other nations, which may lead to the neglect of some critical geopolitical events. Second, the EGARCH model presupposes a priori that residual terms adhere to a particular distribution, which may result in an incomplete depiction of the return features of the energy market. Third, the work solely examined the impact of geopolitical risk events on energy market risk and did not assess the cumulative excess returns from geopolitical risk events, which is also a topic for future research.

Footnotes

Availability of data and materials

Authors do not have the right to share the data. However, it will be made available to the reader upon reasonable request.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (grant number: 72063001) and Bidding project of key research base of humanities and social sciences in colleges and universities in Jiangxi province (grant number: JD20005).