Abstract

This paper is concerned with the oil & gas assets portfolio. A multi-objective portfolio model of oil & gas assets is studied from two perspectives—scale and revenue. Considering the nonlinear and integer constraints in the model, a class of oil & gas assets portfolio model of nonlinear multi-objective mixed integer programming is established. The weight of the multi-objective is solved by the support vector machine model. A hybrid genetic algorithm, which uses the position displacement strategy of the particle swarm optimizer as a mutation operation, is applied to the optimization model. Finally, two examples are applied to verify the effectiveness of the model and algorithm.

Keywords

Introduction

One of the common questions in the oil & gas portfolio is how to allocate some amount of money to different assets. There are many different models and methodologies for the analysis of the oil and gas portfolio. The first approach for considering the optimal portfolio problem is the so-called mean-variance. It was pioneered by Markowitz (1952) and he played a critical role in the theory of Portfolio selection.

In the Markowitz portfolio model, the risk dispersion problem with the upstream field of the oil & gas industry is simulated and decided. The optimal portfolio is consistent with the minimum risk under the determined return or the maximum return under the determined risk (Guo et al., 2012; Markowitz, 1952). Conditional value at risk (CVaR) is the most frequently used risk measure in current risk management practice. It evaluates the average loss comprehensively when the potential decline of oil & gas assets are higher than the value at risk values under a given confidence level during a certain investment period. Then the portfolio can be re-adjusted asset ratios based on this loss (Li, 2013; Wu et al., 2018; Yang, 2017). The Boston Consulting Group (BCG) Matrix divides different strategic business units into four categories and presents them intuitively. It can help strategy makers analyze the market performance and cash flow of products of their portfolio through the matrix (Li et al., 2019; Zhang, 2007). The General Electric Matrix is a comprehensive portfolio planning tool jointly developed by McKinsey and General Electric in the early 1970s. It primarily uses the rate of return on investment as the norm for assessing investment opportunities. It adds more evaluation indicators to the BCG growth-share model, adopts comprehensive measurement standards of the classification of business units, and introduces the middle position to make the evaluation more accurate (Zhang , 2007). The Arthur D. Little (ADL) Matrix was proposed by Arthur D. International Management Consulting Company in the 1970s. The model relies on the industry life cycle for portfolio management. The structure of the autoregressive distributed lag model includes two main analysis indexes. One is an environmental indicator that represents the industry life cycle. Another is the competitive position indicator which reflects the strength of enterprises (Zhang , 2007). The Shell Directional Policy Matrix (DPM) is proposed by Royal Dutch Shell in the 1970s. It makes a qualitative analysis of the business based on the business prospect attraction and company competitiveness. Each dimension of the DPM is divided into three categories. Enterprises can evaluate the characteristics of nine types of businesses in the matrix and formulate the corresponding policies strategies and suggestions regarding the direction provided by the matrix (Tuncay, 2013; Zhang , 2007).

The above portfolio optimization methodologies have different purposes. They focus on the internal benefit evaluation under the consideration of the external market, the quality evaluation of assets themselves, and the income evaluation under the consideration of risk. Compared with the return of optimization purposes. The above portfolio optimization methodologies are more concentrated and the quantitative consideration of the multi-objective of the oil & gas portfolio is insufficient. There is a lack of multi-objective decision-making. In some assets, the decision variables are often limited to invest or not, which the mixed 0–1 integer decision should be considered in the portfolio (Bigerna et al, 2021; Gazijahani et al., 2017; Globocnik et al., 2020; Kiamehr et al, 2018; Ning et al., 2020; Yan, 2018).

In this paper, a class of nonlinear multi-objective mixed integer programming models for oil & gas portfolios is formulated. The outline of this paper is as follows. Then, we formulate a mathematical model to describe the oil & gas portfolio framework, including the nonlinear multi-objective and mixed integer decision-making. Nest, this paper devotes a support vector machine (SVM) model to obtain the weights of the multi-objective. Moreover, the hybrid genetic algorithm (GA) with particle swarm optimizer (PSO) is applied to the portfolio model. Two numerical experiments are studied. It concludes the whole paper at last.

A mathematical model

An oil company will make a portfolio decision on

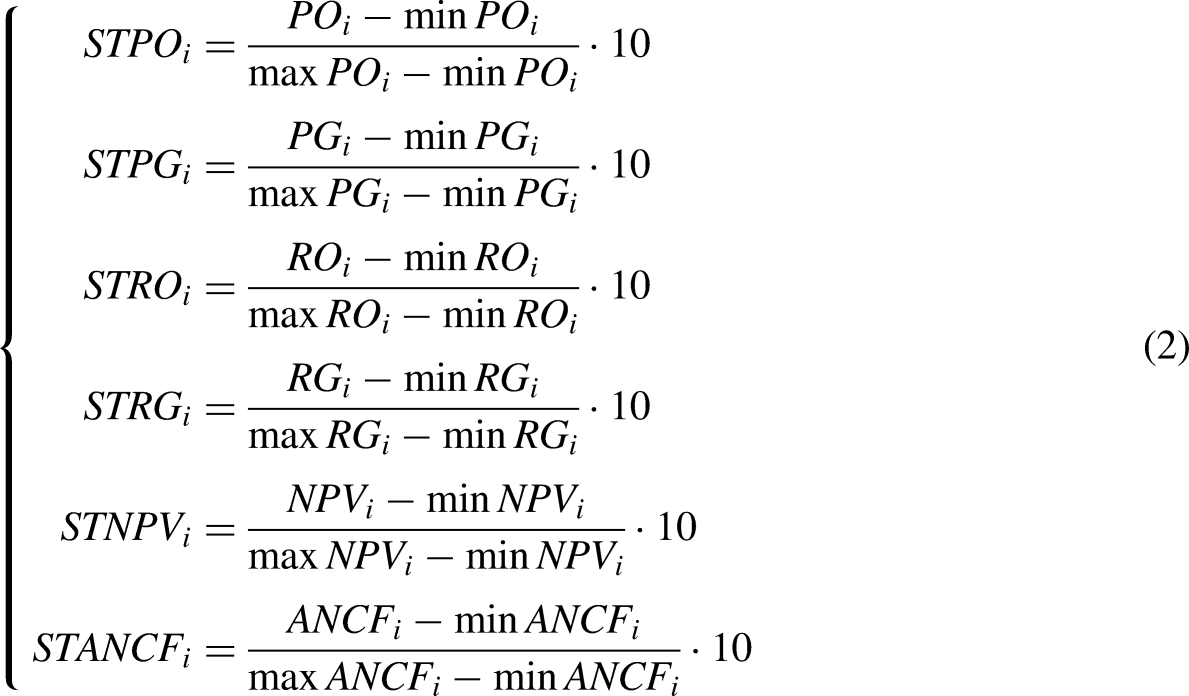

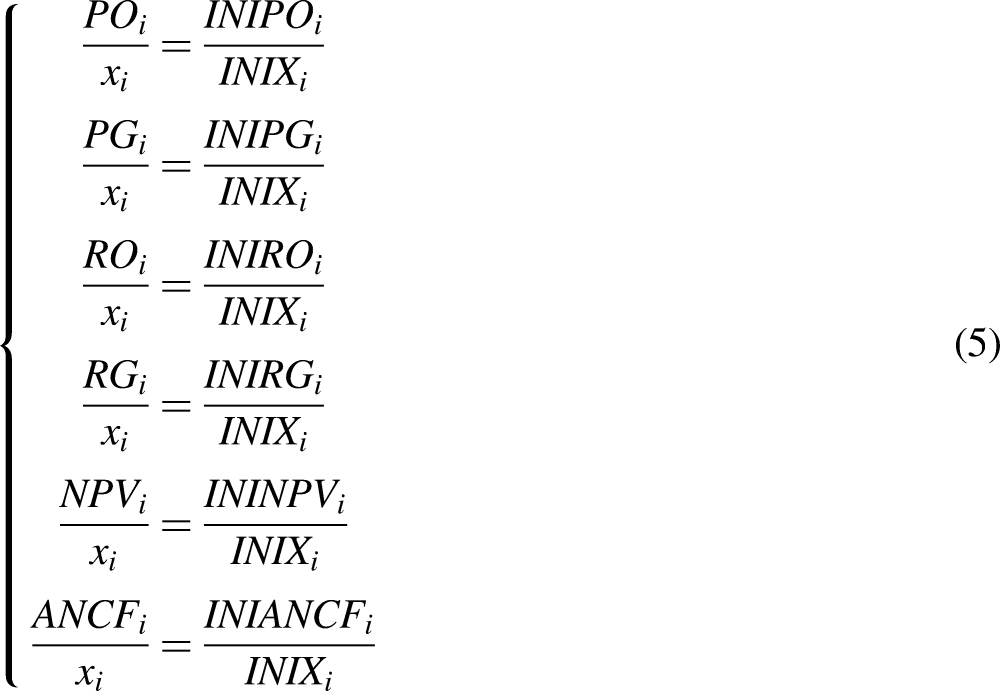

After normalization, oil production, natural gas production, oil reserves, natural gas reserves, NPV of the remaining contract period, and cumulative net cash flow of the remaining contract period are

The model sets some constraints, including the ratio of high-risk assets, the ratio of oil assets, the ratio of conventional assets, the ratio of exploration assets, the ratio of onshore assets, the scope of equity ratio after optimization, the scope of equity ratio change after optimization, and the scope of equity ratio change for some specific assets and so on.

For the ratio of high-risk assets, it is satisfied as follows by setting an interval For the ratio of oil assets, it is satisfied as follows by setting an interval For the ratio of conventional assets, it is satisfied as follows by setting an interval For the ratio of exploration assets, it is satisfied as follows by setting an interval For the ratio of onshore assets, it is satisfied as follows by setting an interval For the scope of equity ratio after optimization, it is satisfied as follows by setting an interval For the equity ratio change after optimization, it is satisfied as follows by setting an interval For the scope of equity ratio change about some specific assets, the decision variable is limited to investment or not. Therefore, the equity ratio is considered to be

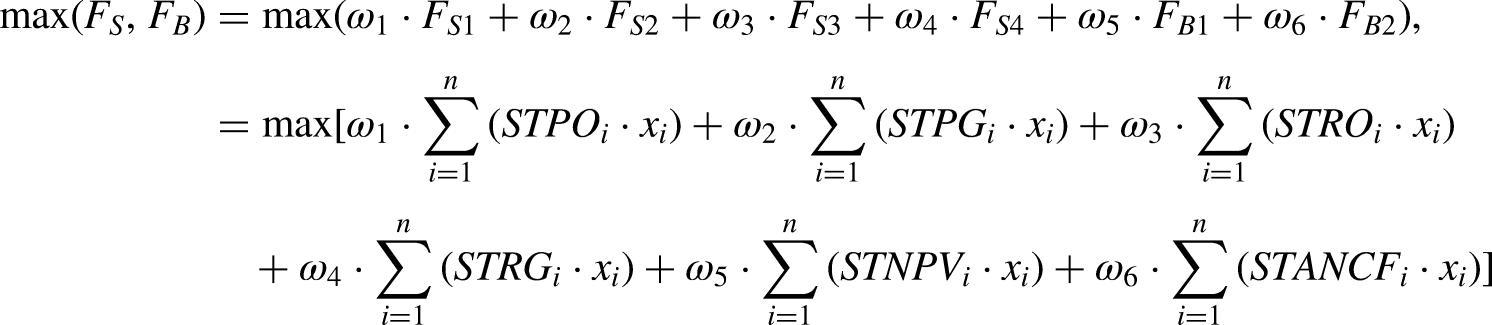

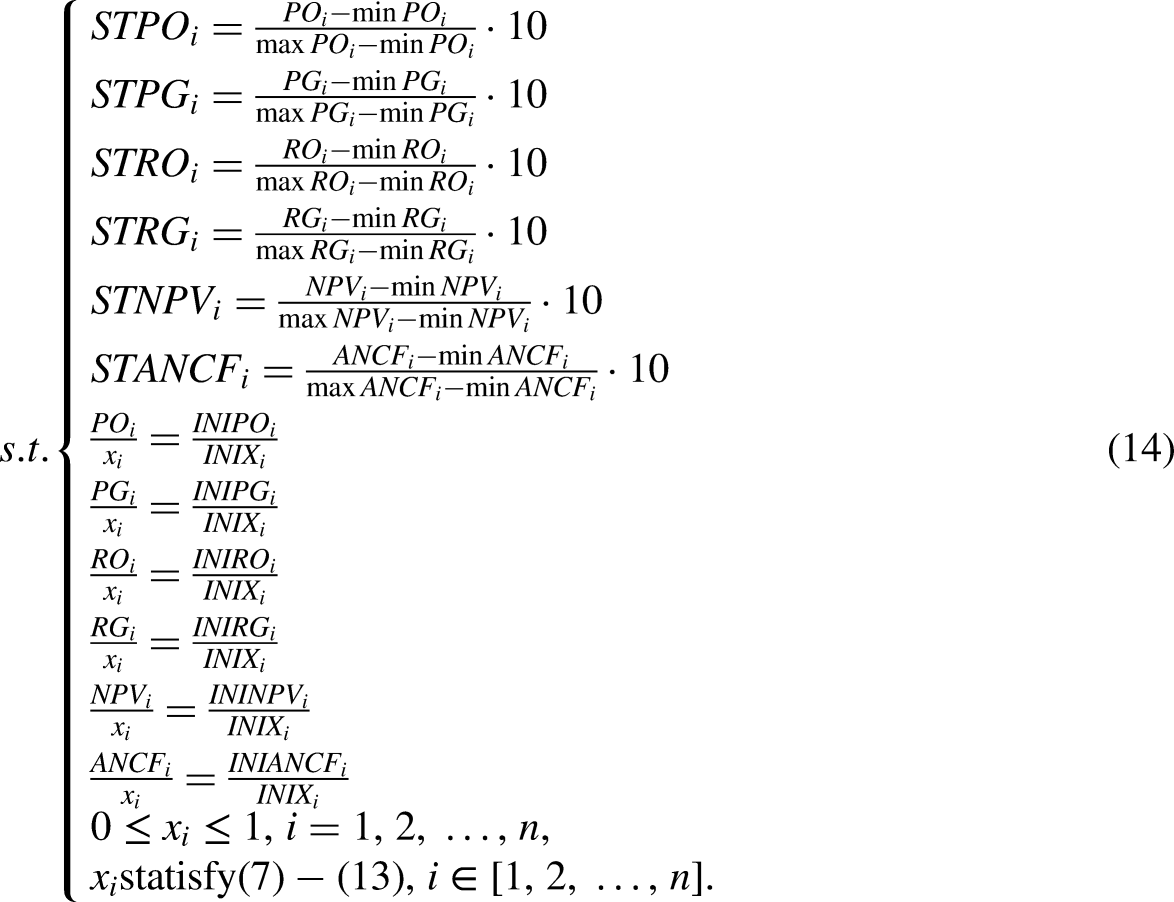

In summary, we can establish an optimization model of the portfolio as follows:

A calculation methodology

It is found that model (14) is a highly nonlinear optimization model, which can not be solved by a gradient algorithm. In addition, it is found that the weight proportion

A solution of the objective function weight

There are two ways to obtain the weight of the objective function

First, we suppose that H-asset is the asset with both high scale value and high return, L-asset is the asset with both low scale value and low return. For

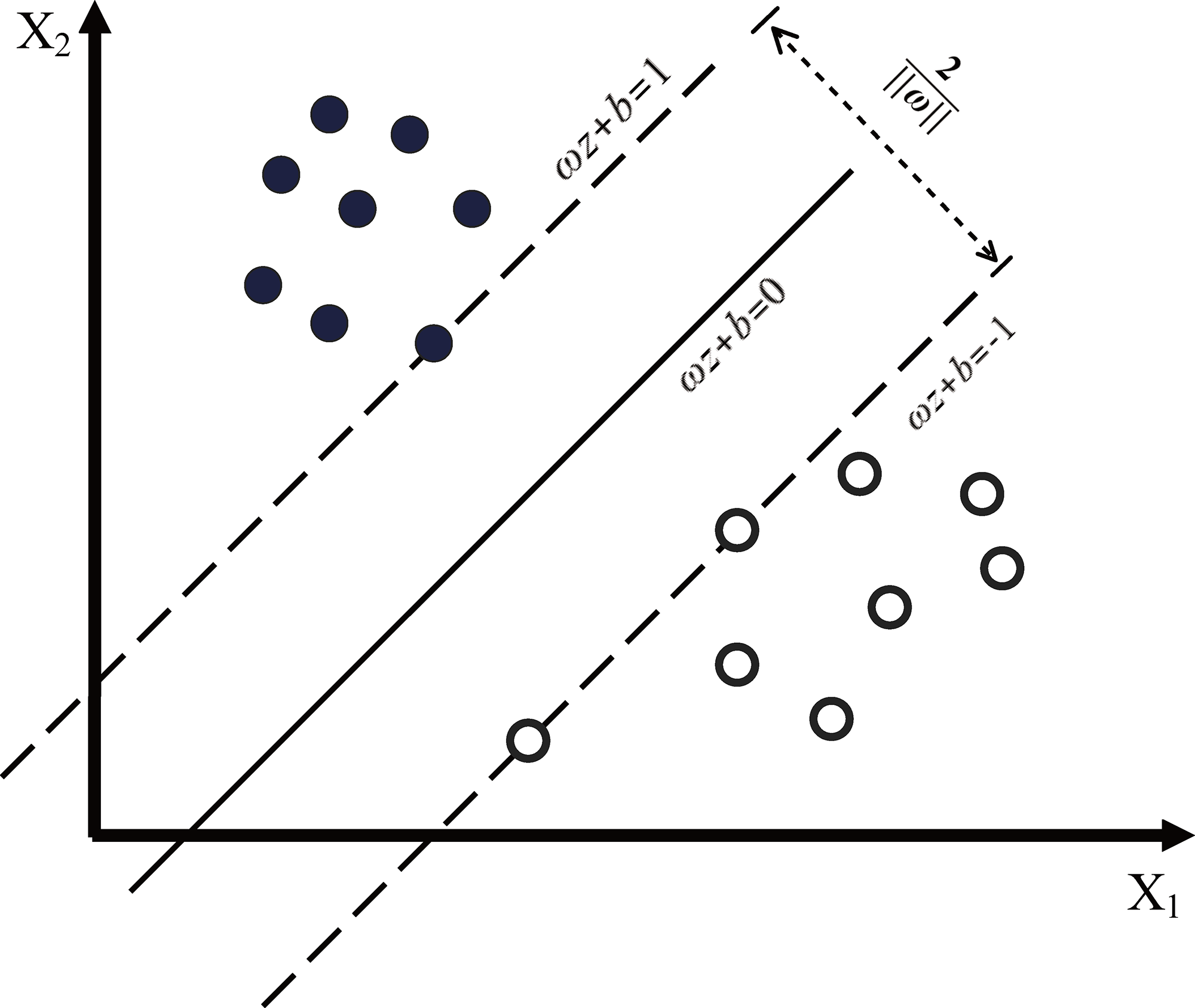

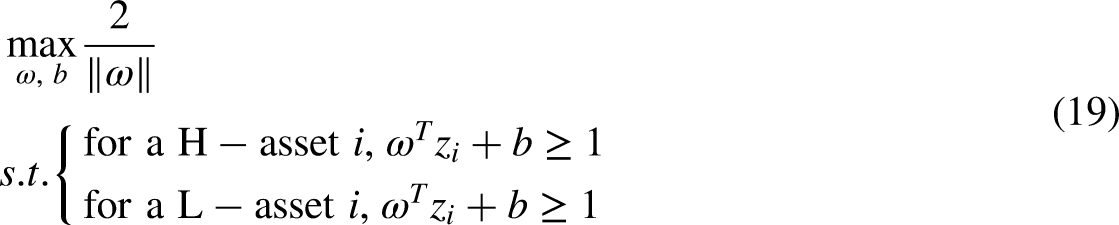

Schematic diagram of the risk assessment using the support vector machine model.

We can prove the following Theorems 1 to 4 easily. Theorem 1 shows that the countries that belong to the same scale and return category are on the same side of the critical plane. Moreover, the assets that belong to different scale and return categories are on different sides of the critical plane. Theorems 2 to 4 provide the theoretical foundation of the SVM.

For an H-asset

As mentioned earlier, for both H- and L-assets, the farther from the plane

For two H-assets A and B, the scale and return vector are

For two L-assets A and B, the scale and return vector are

It is not difficult to prove Theorems 2 and 3, based on the distance between the H-/L-assets and the critical plane

For two assets A and B, the scale and return vector are

From Theorem 4, we initially obtained the critical plane

As shown in Figure 1, two support planes

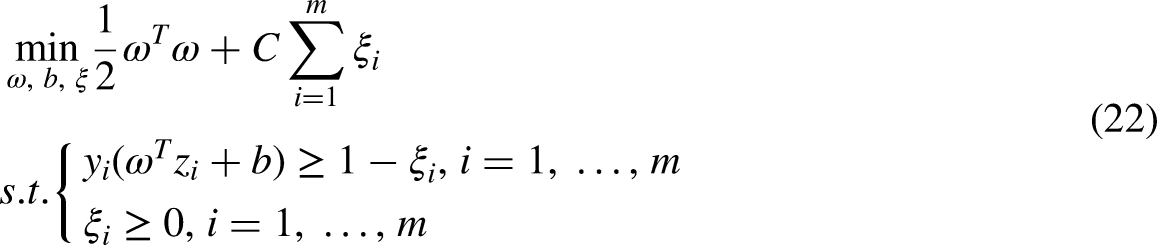

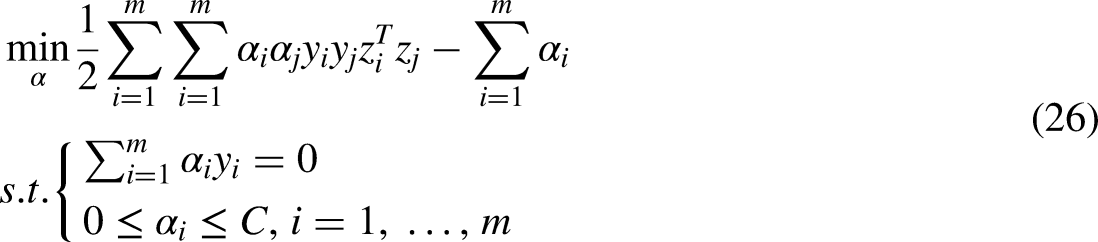

Model (20) uses convex quadratic programming. However, we selected a hyperplane to divide the training set accurately and completely. However, in practical applications, there may not be such a perfect situation, which means it could be a linear non-separable problem. In other words, some hollow circles might be in the solid-circle region and vice versa. In that case, some training points that do not satisfy the constraints are allowed to exist. Therefore, we introduced slack variables to identify the weakening constraint condition (Platt, 1998; Xu et al., 2021; Zhang, 2021).

Thus, the original problem is transformed into a relatively simple quadratic programming model. Therefore, we initially solved a programming model (27) to obtain

The GA with PSO

The GA originated in the 1960s and is a global random search heuristic algorithm, which draws on the idea of evolution. It is a search technique used in computing to find exact or approximate solutions to optimization and search problems. GAs are categorized as global search heuristics. GAs are a particular class of evolutionary algorithms that use techniques inspired by evolutionary biology such as inheritance, mutation, selection, and crossover. The GA is implemented in a computer simulation in which a population of abstract representations of candidate solutions to an optimization problem evolves toward better solutions. However, the GA has some inherent flaws, such as slow convergence. We draw the displacement of the particle swarm algorithm to improve the GA to modify the thinking of mutation.

The PSO is a population-based algorithm. It was studied by Kennedy et al. (1995). PSO algorithm relies on a group of particles to modify the displacement continuously in the solution space according to the group experience and the individual optimization process, to realize the search for the optimal solution in multi-dimensional space. The swarm is initialized firstly in a set of randomly generated potential solutions and each particle in the population is a feasible solution to the optimization problem. Then a fitness function is used to calibrate the fitness value of the particle to judge whether the particle is optimal. Each particle will move in the solution space and correct its displacement constantly until the optimal solution is found. The modification of displacement depends on a velocity vector, which is determined by the optimal solution found so far by the particle itself and the optimal solution found so far by the whole population. The former represents the cognitive level of individual particles and the latter represents the cognitive ability of groups.

Suppose that the population size is

Krohling (2004) proposed a new position displacement principle. He suggested that the updating of the velocity vector is independent of the history velocity vector. According to his work, the particles are manipulated as follows:

It can be seen that the optimization of particles depends on position transfer from the standard PSO algorithm. Angeline (1998a,b) pointed out that the position displacement of particles was a kind of mutation operation. We make use of the position displacement as a mutation operator to modify the GA. During the mutation operation, the position of those individuals selected for mutation is modified via a vector that depends on the personal best position and the current global best position. If GA adopts the new mutation operator, it can use the history information of the chromosomes and share information among the population. The mutation will no longer be stochastic and the local search will be more efficient. At the same time, it keeps the GA’s good property in global search. So the hybrid GA can provide more efficient exploration and exploitation ability (Ding, 2018; Wei et al., 2022).

However, the velocity vector has to be treated specially during the mutation operation. After selection and crossover, the chromosomes are different from their parents. The history velocity vectors present the parents’ information and will not make sense anymore. So during the mutation, equation (29) is not suitable. But equation (30) is available for the operation. The hybrid GA with PSO is described as follows:

Step 1. Initialize the population in the search space. Step 2. Record every individual’s best solution Step 3. Perform selection operation. Step 4. According to the crossover probability pc, perform crossover operation. Step 5. Select individuals for mutation and employ the results coming from Step 2 to perform the mutation operation according to equation (30). Step 6. If the optimum is found, quit the iterative operation; if not, return to Step 2.

Numerical experiments

To verify the effectiveness of the nonlinear multi-objective mixed integer programming model for oil & gas portfolio, the algorithm for objective function weight with support vector machine (SVM) and the hybrid GA with PSO discussed in the previous section, two numerical experiments applied carried out in this section. All the computations are performed in Matlab on a Pentium PC under the Windows 10 environment.

S company oil & gas portfolio

Firstly, we take the international oil company-S as an example to optimize 170 assets from 25 countries in the oil & gas upstream. The data of 170 assets are obtained from IHS Markit, World Bank, and Wood Mackenzie. For these 170 assets, we select 10 extremely H-assets and L-assets and substitute them into the model (27) to solve the corresponding problems

Then, we solve model (14) and set the constraint interval for the ratio of high-risk assets as

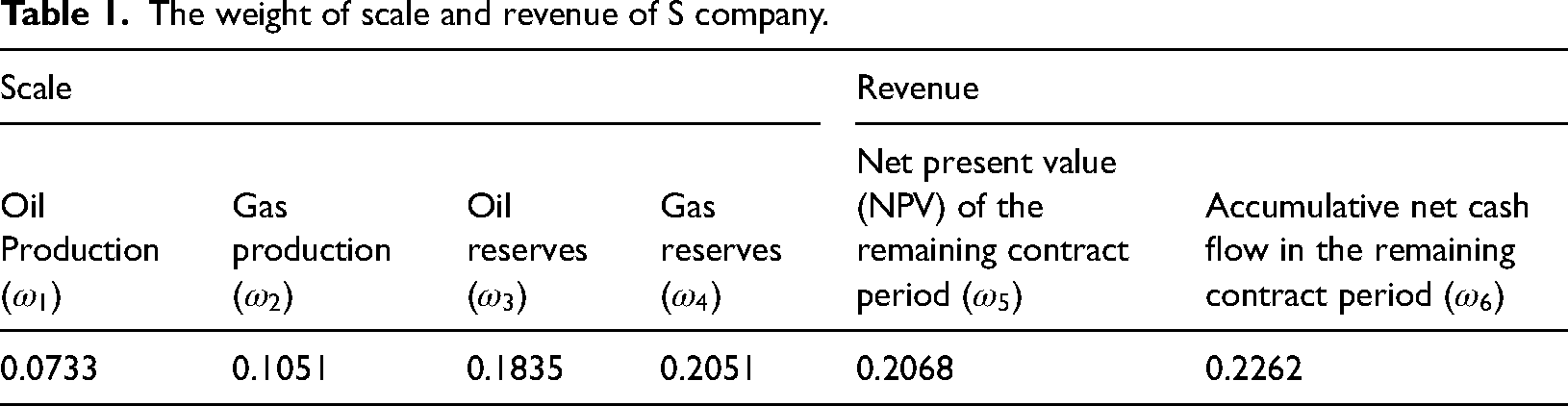

The weight of scale and revenue of S company.

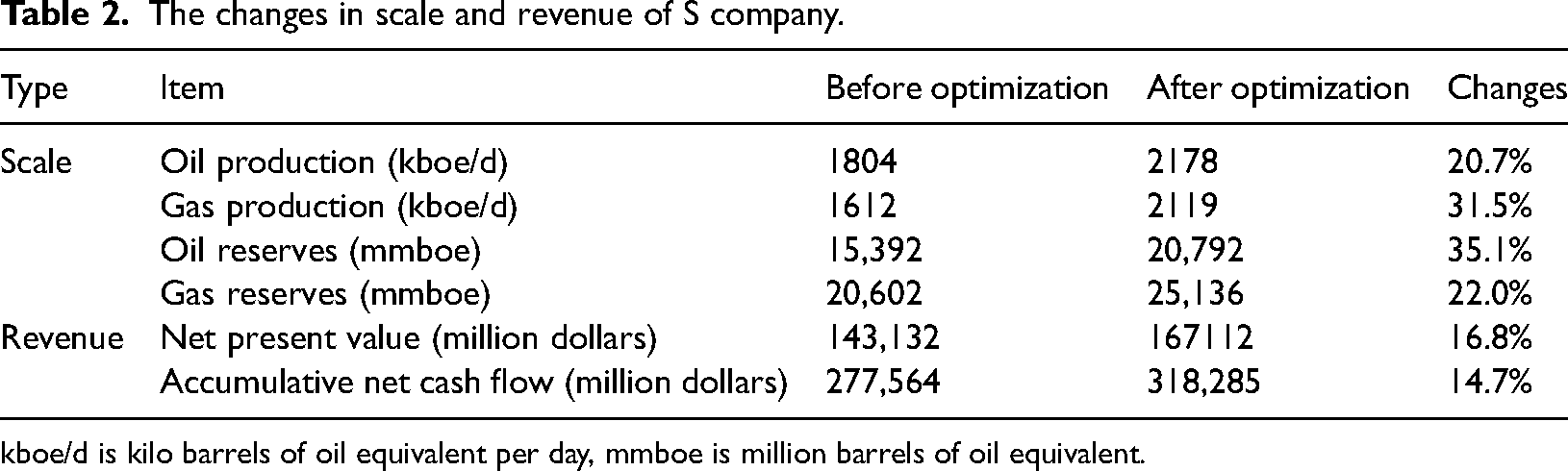

The changes in scale and revenue of S company.

kboe/d is kilo barrels of oil equivalent per day, mmboe is million barrels of oil equivalent.

C company oil & gas portfolio

Next, we take a national oil company-C as another example to optimize 42 assets from 20 countries in the oil & gas upstream. The data of 42 assets are also obtained from IHS Markit, World Bank, and Wood Mackenzie. For these 42 assets, we select 6 extremely H-assets and L-assets and substitute them into model (27) to solve the corresponding problems

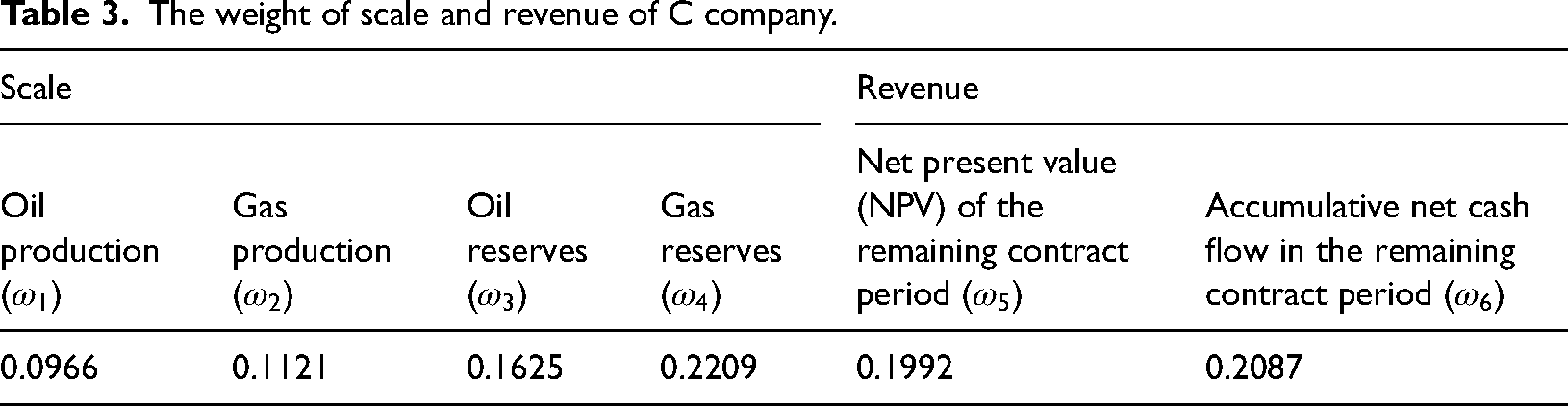

The weight of scale and revenue of C company.

By setting the constraint interval for the ratio of high-risk assets as

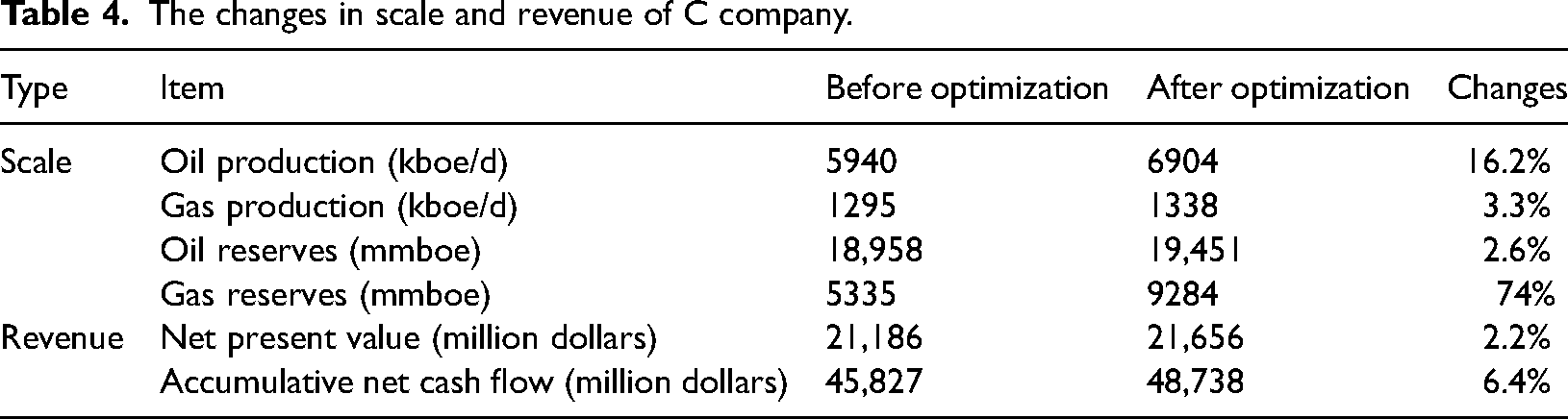

The changes in scale and revenue of C company.

It can be seen from the above table that the scale and revenue of S company and C company have been optimized after applying the models and algorithms in this paper. In the case of S company, the oil & gas production has been improved greatly. However, in the case of C company, the oil production has a significant increase after optimization while the increase in gas production is not significant. The increase in oil reserves is not significant while there has been a significant increase in gas reserves.

Conclusion

This paper establishes an optimization model based on project level for the investment decision of upstream oil & gas of international oil companies. A nonlinear multi-objective mixed integer programming model with scale and revenue as objectives and structure as constraints are established. The method of SVM is used for the weight of the target, and the hybrid GA based on the idea of particle swarm displacement transfer is used for the planning model to construct the calculation system. The case of an oil company is verified. From the results, our method is effective and feasible.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.