Abstract

It is tempting to attribute variations in support for nuclear power to prominent accidents such as Three Mile Island in the United States or Fukushima in Japan. To illuminate how such attribution can be problematic, the authors discuss the historical context of the Three Mile Island accident in the United States. They point out that the US nuclear industry faced major challenges even before the 1979 accident: Forty percent of all US reactor cancellations between 1960 and 2010, they write, occurred before the accident in Pennsylvania. While safety concerns were undoubtedly a driver of public aversion to new nuclear construction in the United States, the nuclear industry already faced substantial economic and competitiveness obstacles, much like the nuclear industry worldwide before Fukushima.

Keywords

After the earthquake, tsunami, and nuclear disaster that struck Japan’s Fukushima Prefecture two years ago, debates about nuclear power flared in a number of countries. The entire Japanese nuclear reactor fleet was shut down over a period of months, and several countries—including Germany, Switzerland, and Japan—took political steps (some of which may prove to be temporary) toward phasing out nuclear in their long-term energy mixes. Before Fukushima, advocates of nuclear power had argued that a new period of nuclear expansion was close at hand, enabled by advances in design, manufacturing, safety, and regulatory processes. Fukushima threw much of that argument into question, with the results now percolating through national debates and regulatory processes.

During this period of heightened discussion about the future of nuclear power, it has been tempting to draw parallels with the 1979 Three Mile Island accident in the United States. As with Fukushima, Three Mile Island instigated a major public conversation about nuclear safety. At the time, it halted nuclear construction and permitting in the United States. The accident also correlates roughly with the time that nuclear power ceased to be a major source of new electricity supply, and is often viewed as the catalyst for nuclear power’s downturn in the United States. For example, a 2006 New York Times Magazine article (Gertner, 2006) stated: The received wisdom about the United States nuclear industry is that it began a long and inexorable decline immediately after the near meltdown, in 1979, at Three Mile Island in central Pennsylvania, an accident that—in one of those rare alignments of Hollywood fantasy and real-world events—was preceded by the release of the film The China Syndrome two weeks earlier. In the 1970s it looked as if nuclear power was going to play a much bigger role than eventually turned out to be the case. What happened was Three Mile Island, and the birth of an antinuclear movement that stopped dozens of half-built or proposed reactors.

There can be little doubt that Three Mile Island affected the US nuclear industry, public opinion, and regulatory regime. It was, after all, the worst nuclear accident in the history of the United States, and even 34 years later remains the third worst nuclear accident globally. As such it very well ought to have affected, at a minimum, the domestic energy debate in the United States. Nevertheless, laying the entire blame for the decline of US nuclear power on the incident is not justified. The argument for doing so is superficially plausible, but it is incomplete—and, if taken as the basis for future policies, dangerously misleading. The nation’s nuclear industry was in fact facing substantial structural obstacles and economic challenges even before the accident, obstacles that reflect the challenging nature of nuclear technology in a world of fast-changing competition and fickle demand growth.

Before and after Three Mile Island

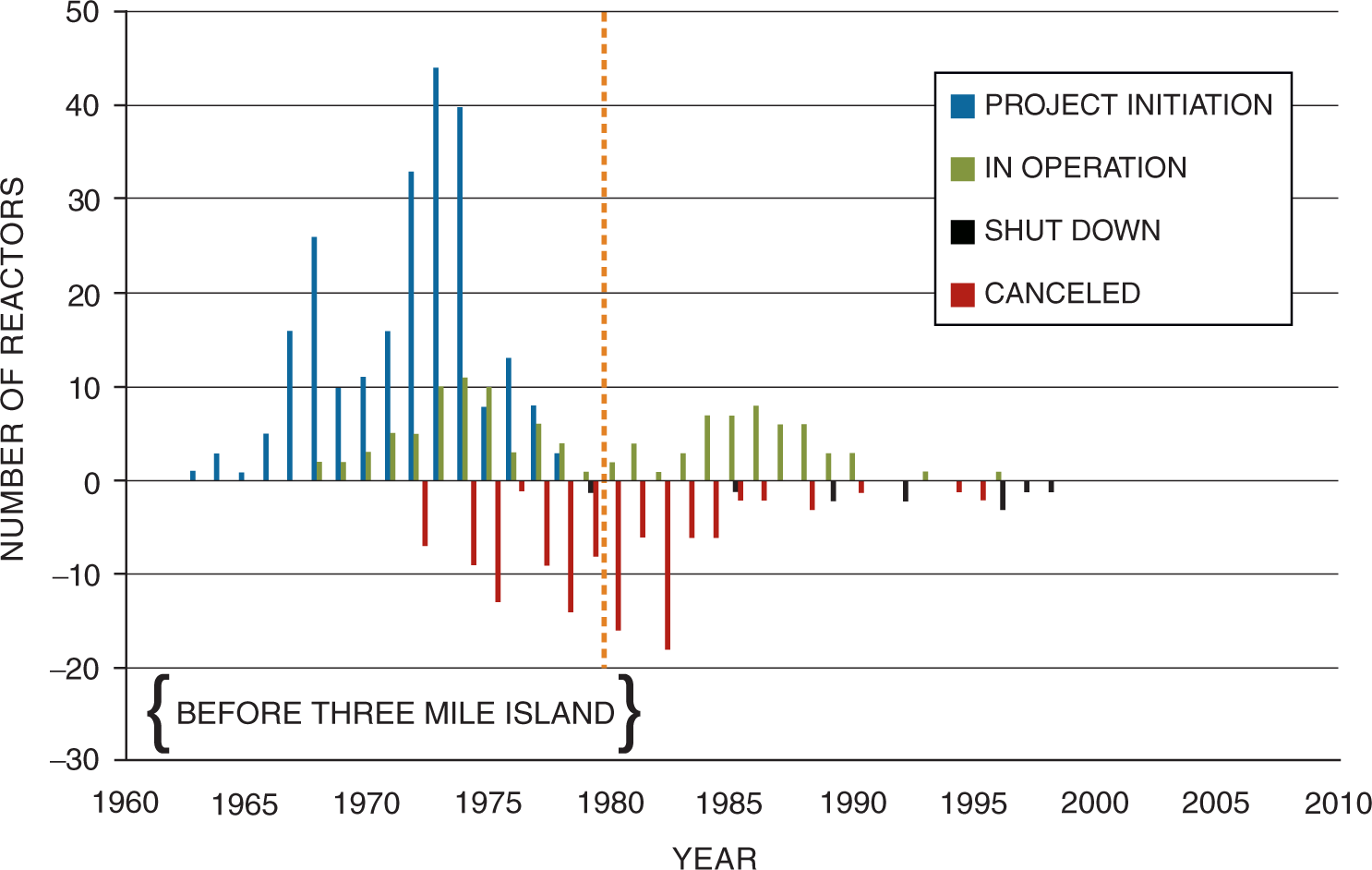

A careful assessment of historical data illustrates the rise and fall of the nuclear industry in the United States (Hultman and Koomey, 2007; Hultman et al., 2007; Koomey and Hultman, 2007, 2009). Every reactor has a well-documented history that includes project initiation (approximated by the approval date of a construction permit), the year of project completion or cancellation, and, in a few cases, the year of reactor shutdown. Data on nuclear power plant costs show that some plants experienced cost increases after Three Mile Island, and some plants already under construction experienced delayed construction times. But these trends were already in progress before the accident, with plant costs rising and completion rates slowing in the second half of the 1970s (Bupp and Derian, 1981; Komanoff, 1981; Koomey and Hultman, 2007). The most that can be claimed is that the partial meltdown at the nuclear plant may have exacerbated these existing trends.

For example, the overall reactor “order book” had deteriorated dramatically even before 1979. The history of reactor starts, completions, cancellations, and shutdowns is shown in Figure 1.

1

While there was a rapid expansion of reactor orders in the first half of the 1970s, the additions to the order book had clearly peaked by about 1974—five years before the accident in Pennsylvania—which was also the time when American utilities, in aggregate, were not only cutting back on orders but also cancelling orders they had already made. These two trends indicate that utilities were reconsidering their earlier rapid expansion plans for nuclear—though they don’t publicize the reasoning behind those decisions. Perhaps nuclear power was becoming a liability, or, more benignly, expectations for rapidly expanding demand were simply not materializing. The pattern of reactor completions in Figure 1 shows a slowdown before 1979 and then a slow but temporary increase thereafter—consistent with a delay incurred for some late-stage construction while designs were re-evaluated.

US nuclear construction starts, completions, cancellations, and shutdowns by year

Including the period before and after Three Mile Island, more than half of all reactors ordered were subsequently canceled. Tellingly, fully 40 percent of these cancellations happened before the accident—that is, the headwinds for the nuclear industry had already been blowing hard.

One of the key factors affecting reactor costs is the duration of construction. Our own earlier work (Koomey and Hultman, 2007) shows that reactors begun between 1966 and 1972 took, at a minimum, about four years to complete. After 1973, the minimum duration for completion began to rise rapidly, to a minimum of more than eight years for reactors started from 1974 to 1976. Moreover, construction times varied more during this period, with about three-fourths of reactors taking 10 to 15 years to complete (Koomey and Hultman, 2007). These reactors were well under construction before Three Mile Island. Reactors started immediately before and after the accident may have had some advantages over reactors whose construction was further along, in that design modifications necessitated by the accident were easier to implement.

The broader economic landscape

The overall picture that emerges from reactor construction history is that the industry was in the midst of a major retrenchment even before the alarm bells sounded in Pennsylvania. New orders had dropped precipitously starting in 1975, existing orders were being canceled at a rapid pace, and costs and construction times were starting to increase. The advent of new scrutiny, public opposition, and regulations no doubt added additional weight to the existing burden. Precisely quantifying this added burden is impossible, but it is clear that multiple factors created an extremely unfavorable environment for new reactor construction (Komanoff, 2005). Many factors have been proposed and discussed at length in the literature, and they can be combined into five broad categories.

Declining growth in electricity demand

Projected electricity demand was a clear factor in both the initial enthusiasm to continue nuclear expansion in the early 1970s and in the bust after 1975. Demand growth was very high (though erratic) during the early 1950s and remained near 7 percent annually through the 1960s. It was not unreasonable to imagine that this growth rate would continue through the 1970s, but the economic contraction caused by the oil price shock in 1973 brought with it a contraction in electricity demand growth, and this contraction continued apace through the 1970s. Whereas five-year average demand growth was about 7 percent in 1970, it had fallen steadily, to near 2 percent, by 1980 (Energy Information Administration, 2012).

National average reserve margins also began to increase substantially during this period, indicating excess electricity supply. At the time, utilities typically aimed for a reserve margin of 15 to 20 percent. From 1966 to 1973, reserve margins fell within the desired range. But this began to change in 1974, when the margin rose to 27 percent and then to 35 percent in 1975. Margins stayed between 30 percent and 41 percent through 1984 (Edison Electric Institute, 1963–1988). These numbers indicate a large national aggregate oversupply; pitching an expensive new power plant in this environment would have been reckless unless there was an obvious source of new demand. A contemporaneous account quoted a member of the Atomic Industrial Forum making this very point: “Utilities suddenly found that they were overcommitted, and their load growth projections had to be tossed in the wastebasket” (Lambrecht, 1980).

Such an environment—with declining demand growth, rising oversupply, and increased volatility—is particularly antithetical to large, long-lead-time, capital-intensive projects such as nuclear power plants; even a commissioner with the Nuclear Regulatory Commission acknowledged this right after Three Mile Island (Gilinsky, 1980). Our own work in this area leads us to believe that this factor was significant in driving longer lead times and higher construction costs.

High interest rates and construction costs

High financing costs hindered new construction of all kinds in the mid- to late 1970s. Peaking at an unprecedented level of 20 percent in 1980, and combined with the risk of longer construction times, interest rates weighed on the cash flows of an industry focused on large, capital-intensive projects. These factors were completely separate from the public and regulatory response to Three Mile Island. Construction costs were already increasing before the accident (Koomey and Hultman, 2007). Even outside the United States, other countries (such as France, Germany, and the United Kingdom) faced cost escalation and plant delays without having comparable reactor accidents (Grubler, 2010; Krause et al., 1994; Romm, 2011).

Structural problems in the nuclear industry

Amid the rush of new orders in the late 1960s and early 1970s, new plant designs were sold, even though there was little experience in engineering, constructing, and operating those designs. This practice was based, in part, on an assumption that costs would drop with additional experience, though it turned out that they did not (Bupp and Derian, 1981; Hirsh, 1989). Unlike today, construction of some reactors began with as little as 10 percent of their designs completed, creating the conditions for potential future cost escalation (Koomey and Hultman, 2007).

The rise of nonutility generators

The Public Utility Regulatory Policies Act of 1978 (PURPA) triggered a restructuring of the previously monolithic utility sector, stipulating in particular that electricity produced by independent power producers must be purchased by utilities at “avoided cost.” The new power from independent producers, combined with lack of demand for electricity, further eroded utilities’ need for new nuclear plants. In large part owing to the provisions of PURPA, nonutility generation rose steadily from 71 billion kilowatt-hours per year in 1979 to almost 400 billion kilowatt-hours per year by 1995—this new, nonutility generation was the equivalent of adding more than 50 typical 1,000-megawatt nuclear plants (Energy Information Administration, 1996). As Peter Bradford (2011), a former member of the Nuclear Regulatory Commission, argued in the Wall Street Journal: Nuclear-plant construction in this country came to a halt because a law passed in 1978 [PURPA] created competitive markets for power. These markets required investors rather than utility customers to assume the risk of cost overruns, plant cancellations, and poor operation. Today, private investors still shun the risks of building new reactors in all nations that employ power markets.

Changing perceptions of the nuclear industry

Three Mile Island was a pivotal event that fit into a developing public narrative of questionable nuclear safety. Earlier events had a similar effect (Komanoff, 2005), including a 1975 fire at Browns Ferry in Alabama and the 1976 testimonials of three former GE nuclear engineers who joined antinuclear organizations because of their concerns about nuclear safety. In 1981, workers inadvertently reversed pipe restraints at the Diablo Canyon reactors in California, “virtually disabling their seismic protection systems,” which further undermined public confidence in nuclear safety (Komanoff, 2005). These events, combined with Three Mile Island, undermined public support for the nuclear industry.

The post-Fukushima era

The Three Mile Island accident likely had some effect on reactors that were, at that time, ordered or under construction, but even without a nuclear disaster, it is not clear that the industry would have overcome the other big challenges it faced. It is our view that these other factors may, in the aggregate, have been the most important in determining the likelihood of new nuclear orders after 1979.

Framing nuclear power’s woes as a Three Mile Island postmortem of social pressure and regulatory overreach suggests a much narrower remedy than would be the case if multiple vulnerabilities were viewed in aggregate. Regulatory streamlining, better permitting procedures, and improved reactor designs are appropriate responses to the former framing. Such improvements are welcome to the extent that they improve efficiency without sacrificing safety or public participation, but are only partial remedies to the broader set of challenges—foremost among them a greater emphasis on energy efficiency and alternative supply options.

It is tempting to attribute weakness in the global nuclear industry after Fukushima to public fears about nuclear energy. And it may be accurate to do so, in some places and with some constituencies. But the nuclear industry before Fukushima was already facing substantial challenges in many areas. While costs of new nuclear installations had escalated, the costs of natural gas and other sources of supply were dropping. With global demand slackening because of the recession, most power companies were already hard pressed to justify new investments in nuclear. While there are exceptions—in cases where demand continues to grow quickly and governments are able to share the financial and political risks—the picture for nuclear remains challenging in the near to medium term.

Outside the several countries with robust national support for nuclear expansion, the best hope for the global nuclear industry probably lies in policy interventions that put a price on carbon, which would bring the costs of nuclear energy closer to parity with coal and natural gas. Competing resources—such as wind, solar, and energy efficiency— would also benefit from a carbon charge; it would not be a panacea for the nuclear industry, but would certainly improve its prospects.

Footnotes

Acknowledgements

We are grateful for discussions with Peter Bradford, Ralph Cavanagh, Mark Cooper, Victor Gilinsky, Jim Harding, Charles Komanoff, Amory Lovins, and Joe Romm. Gregory Carlock helped us with some data collection and analysis. Any mistakes or misinterpretations are our own.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.