Abstract

In 2010, there were more nuclear power units under construction worldwide than in any year since 1988. Even before Fukushima, however, status indicators for the international nuclear industry were showing a negative trend. Fewer countries are operating nuclear fission reactors for energy purposes than in previous years, and many countries are now past their nuclear peak. Worldwide nuclear production is generally declining, and many new projects are experiencing construction delays. Even if reactors can be operated for an average of 40 years, 74 new plants would have to come on line by 2015 to maintain the status quo, which is impossible given current constraints on fabricating reactor components. Developments in Asia, particularly in China, do not fundamentally change the global picture. The dramatic post-Fukushima decisions in two of the four largest economies, Japan and Germany, and in several other nuclear countries could accelerate the decline of a rapidly aging industry.

Keywords

Bushehr went critical. According to industry news outlets, the Iranian nuclear reactor project was finally completed on May 8, 2011—36 years after the first shovel hit the ground. The historic event closely followed the first grid connection, on May 3, of the second unit of the Chinese Ling Ao II nuclear plant. And on March 14, only three days after the Fukushima crisis began, and without any publicity, the Pakistani Chasnupp-2 reactor generated its first power.

These milestones suggest that it is business as usual in the nuclear world, despite the ongoing Japanese crisis. But are projects still lining up, investors eager to engage, politicians convinced, and public opinion in favor of continued nuclear energy development? Where does the industry stand today? And how does the current situation compare with life before Fukushima?

The first global analysis of the state of the industry before and after the Japanese drama began shows that the industry was having difficulties before Fukushima hit the news and that political reactions to Fukushima were surprisingly fast and deep in a number of countries (Schneider et al., 2011).

The accident came where few expected it to happen. On March 11, triggered by the largest earthquake in the nation’s history, a nuclear catastrophe of yet unknown proportions started unfolding in the world’s preeminent high-tech country: Japan. Analysts at Swiss-based investment bank UBS summarized the situation in early April 2011: “At Fukushima, four reactors have been out of control for weeks—casting doubt on whether even an advanced economy can master nuclear safety … . We believe the Fukushima accident was the most serious ever for the credibility of nuclear power” (Paton, 2011).

After months of uncertainty, the seemingly endless patience of the Japanese people is eroding. Tens of thousands of evacuees are waiting for clear information about when, if ever, they can return home. Dogs and cows that were left behind wander along empty roads. Measurements taken as far as 50 kilometers (30 miles) from the Fukushima plant show extremely high levels of radiation at schools outside the evacuation zone. People don’t know what they can safely eat or drink.

Prior to the events in Japan, it appeared that the international nuclear industry had successfully overcome the “Chernobyl syndrome.” The 1986 disaster and its horrific consequences were largely forgotten, downplayed, or ignored. In December 2010, the oldest Ukrainian reactor, Rovno-1, was granted a 20-year lifetime extension, and by 2030 the country projected a doubling of its installed nuclear capacity. Belarus plans to enter into an agreement with Russia to build its first nuclear power plant (The Voice of Russia, 2011). And Russia officially has 11 reactors under construction, second only to China.

According to the International Atomic Energy Agency (IAEA), “some 60 countries have turned to the IAEA for guidance” as they consider introducing nuclear power. One IAEA expert estimates that “probably 11 or 12 countries … are actively developing the infrastructure for a nuclear power program” (International Atomic Energy Agency, 2011). Today there are more units under construction worldwide than in any year since 1988 (except for 2010). Fifteen projects broke ground in 2010—more than in any year since the Chernobyl disaster. Is this, finally, the “nuclear renaissance” that the industry has been heralding for the past decade? 1

The answer is no. Construction starts aside, many industry status indicators are on a negative trend. As of 2010, a total of 30 countries were operating nuclear fission reactors for energy purposes—one fewer than in previous years. Lithuania became the third country ever to revert to “non-nuclear energy” status, following Italy, which abandoned nuclear power after Chernobyl, and Kazakhstan, which shut down its only reactor in 1999.

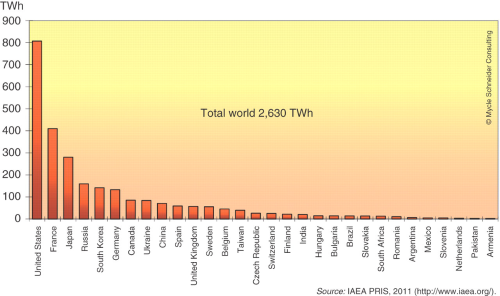

Nuclear production briefly increased to a worldwide total of 2,630 terawatt-hours (TWh or billion kilowatt-hours) of electricity in 2010 (see Figure 1), a gain of 2.8 percent over the preceding year. Before that, however, production had fallen for three years in a row, with nuclear power plants generating 103 TWh (or nearly 4 percent) less electricity in 2009 than in 2006. Production in 2010 was practically identical to production in 2005, and production in 2011 will undoubtedly be lower.

Generation of nuclear electricity in the world in 2010 (net TWh).

The main reasons for nuclear’s poor global performance are technical problems with the reactor fleets of some of the largest nuclear players; the small producers have remained more or less stable. Between 2008 and 2009, nuclear generation declined in four of the “big six” countries: France, Germany, South Korea, and the United States. In Japan, the industry had been slowly recovering from the 2007 Kashiwasaki earthquake, 2 and in Russia, production remained stable. These six countries generate nearly three-quarters (73 percent over the past two years) of the world’s nuclear electricity. In 2010, the nuclear share in four of the “big six” remained stable, while it declined in two countries (Germany and South Korea).

Many countries are now past their nuclear peak. The three phase-out countries (Italy, Kazakhstan, and Lithuania) and Armenia generated their historical maximum of nuclear electricity in the 1980s. Several other countries had their nuclear power generation peak in the 1990s, including Belgium, Canada, Japan, and the UK. And seven additional countries peaked between 2001 and 2005: Bulgaria, France, Germany, India, South Africa, Spain, and Sweden.

Among the countries with a remarkably steady increase in nuclear generation over the years are China, the Czech Republic, Romania, Russia, and the United States (except for 2009, when production dropped by almost 10 terawatt hours). Considering the size of the US program, the industry’s rather continuous improvement in load factor (which reached 88 percent in 2009, the latest year for which figures are available) is impressive. 3 Russia is also generally on an upward trend for load factor (at 78.3 percent in 2009), and South Korea is fluctuating at a very high level (90.3 percent). France (at a 70.6 percent load factor), Japan (66.2 percent), and Germany (69.5 percent), which are already on the lower end for this performance indicator, have exhibited a further downward trend over the past few years (Peachey, 2010).

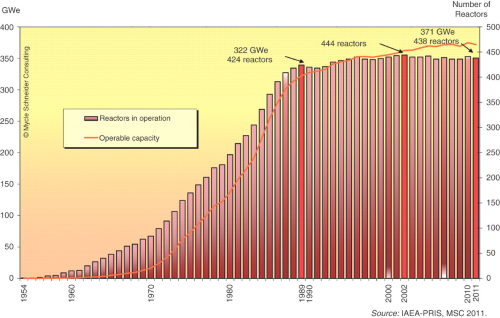

As of May 15, 2011, a total of 438 nuclear reactors were operating in 30 countries, six fewer than the historical maximum of 444 in 2002 (see Figure 2). Since 2002, utilities have started up 26 units and disconnected 32—including six units at the Fukushima Daiichi nuclear power plant in Japan.

Nuclear reactors and new operation capacity in the world in GWe, from 1954 to 15 May 2011.

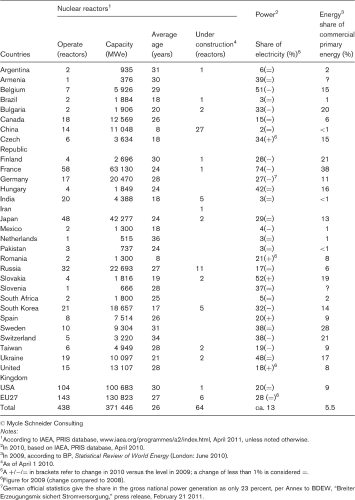

Status of nuclear power in the world (May 15 2011)

© Mycle Schneider Consulting

Notes:

According to IAEA, PRIS database, www.iaea.org/programmes/a2/index.html, April 2011, unless noted otherwise.

In 2010, based on IAEA, PRIS database, April 2010.

In 2009, according to BP, Statistical Review of World Energy (London: June 2010).

As of April 1 2010.

A +/−/= in brackets refer to change in 2010 versus the level in 2009; a change of less than 1% is considered =.

Figure for 2009 (change compared to 2008).

German official statistics give the share in the gross national power generation as only 23 percent, per Annex to BDEW, “Breiter Erzeugungsmix sichert Stromversorgung,” press release, February 21 2011.

Post-Fukushima decisions

In response to the Fukushima events, a number of countries have taken measures that are unprecedented in scope and speed and that will rapidly change the global outlook for the nuclear industry. In the European Union (EU), where nearly half of the world’s nuclear energy is produced, there will be EU-wide “stress tests” of nuclear facilities, under the auspices of the European Commission, implemented by national safety authorities. While the provisional outline of these tests has been criticized as being too superficial, Energy Commissioner Günther Oettinger declared that he wants to continue the discussion: “Content is more important than timing. The public expects credible stress tests covering a wide range of risks and safety issues. This is what we are working on” (European Parliament, 2011). What follows is a country-by-country look at where some of the most significant post-Fukushima changes are occurring.

Japan

It is obvious that the six Fukushima-I (Daiichi) units are condemned. The fate of the four Fukushima-II (Daini) reactors remains uncertain. However, they are only 15 kilometers (9 miles) away from Daiichi and therefore within the evacuation zone. Three more reactors at the Onagawa site, closest to the epicenter of the March 11 earthquake, might be down for years if not for good. In addition, Japanese Prime Minister Naoto Kan has requested that three units at the Hamaoka plant southwest of Tokyo be shut down because of the very high probability of a major earthquake in the region. By May 14, 2011, operator Chubu Electric had taken the remaining two units off the grid. The credit rating agency Standard & Poor’s immediately down-rated the utility. While a restart seems unlikely under any circumstances, it would take years to build seawalls and take other measures to protect the Hamaoka reactors from earthquakes and tsunamis. The Japan Times considers that “the decision on Hamaoka represents a major shift in the nation’s core energy policy” (Jiji Press, 2011; Takahara and Hongo, 2011). Reuters calculated that by the middle of May 2011 more than 62 percent of Japan’s nuclear capacity was off-line for one reason or another (Maeda, 2011). Some insiders confirm that the Hamaoka decision is to be considered only the beginning of a profound reorientation of Japan’s energy policy away from nuclear power and toward the massive expansion of renewables and efficiency.

France

Prime Minister François Fillon requested the Nuclear Safety Authority (ASN) to carry out a safety audit of all operating nuclear facilities in France until the end of 2011. The authority wishes to accelerate the process, and has asked the operators of major facilities, such as AREVA’s La Hague spent fuel reprocessing plant, to deliver their reports by September 15, 2011. 5 France alone generates close to half of the EU’s nuclear production.

During a visit to Europe’s largest nuclear power plant at Gravelines, President Nicolas Sarkozy stated, “As Chief of State I have confidence in the safety of the French nuclear fleet. I have not been elected to call it into question and it will not be called into question . … Because there was a tsunami in Japan we should call into question what represents the strength of France, the pride of France, the independence of France?” (Sarkozy, 2011).

Green Party leaders in France, encouraged by a poll that found 70 percent of people in favor of abandoning nuclear power, have requested a referendum on a progressive phase-out that would start with the immediate closure of France’s oldest reactors—at Fessenheim, sitting right on a seismic fault line next to the border with Germany. The city council has already voted in favor of a shutdown. On the other side of the border, a Green state prime minister took office on May 12, 2011. Recently, nuclear opponents got unexpected support from the leaders of the French Socialist Party (PS). Party president Martine Aubry and number two Harlem Désir have both declared support for a nuclear phase-out—a situation without precedent in France. Presidential elections are coming up in April 2012. According to current opinion surveys, President Sarkozy does not have the slightest chance of re-election. The most likely alternative is a PS–Green coalition government.

Germany

Germany was the sixth-largest nuclear generator in the world in 2010, but since the March 11 disaster seven units with operating ages of 30 years or more have been “provisionally” shut down (plus one that was already down) and will likely never start up again. A paper by the government-appointed Ethics Commission that is looking into Germany’s new energy policy orientation states that the reactor closures will not affect the security of the country’s power supply (Ethikkommission Sichere Energieversorgung, 2011). The Ethics Commission clearly states that the final shutdown of the last operating unit can be done within 10 years and adds that “in the best case the phase-out corridor can be shortened in such a way that the last nuclear power plant will be taken off the grid much earlier.” Furthermore, the commission calls the nuclear phase-out an “economic growth accelerator” and “the chance for a high-performance economy.” This is a document prepared under the auspices of former environment minister, Klaus Töpfer, a member of Chancellor Merkel’s Christian Democratic party. Two of the shuttered units, as well as two operating ones, are located in Baden-Württemberg—a state now governed by Germany’s first Green prime minister. Possibly a Green–Red coalition federal government will come in after the 2013 elections. The Social Democrats favor a rapid nuclear phase-out and might go along with the Green Party position, which will likely be the shutdown of the last German reactor within the next legislative period—that is, before 2018.

Italy

All of Italy’s nuclear power plants were closed following a post-Chernobyl referendum in 1987. More than two decades later, in May 2008, the government introduced a package of nuclear legislation that included measures to set up a national nuclear research and development entity to expedite licensing of new reactors at existing nuclear power plant sites and to facilitate licensing of new reactor sites. The Italian utility ENEL and its French counterpart EDF have subsequently stated that they intend to build four EPR reactors (previously known as European Pressurized Water Reactors) by 2020. A new referendum is scheduled for June 2011. On March 23, 2011, the Italian cabinet approved a one-year moratorium on the attempt to relaunch a nuclear program. Energy Minister Paolo Romani stated: “The government won’t proceed with the realization [of a nuclear program] if the initiatives at the European Union level don’t provide full guarantees on safety” (Moloney, 2011). While the referendum could have derailed any potential further plans, the Italian government decided to pull the plug even earlier, on April 20, 2011. The cabinet went a step further and tabled a bill repealing previous legislation that would have set the scene for a restart of the nuclear program (Dinmore, 2011). The latest opinion polls show that three-quarters of Italians surveyed favor dropping the country’s nuclear plans.

Sweden

Only six countries rely more heavily on nuclear plants as a share of their total power mix, but Sweden now wants to reduce its dependence on nuclear power. The Minister for Enterprise and Energy, Maud Olofsson, said in an April 12, 2011 parliamentary debate: “We are not prolonging the use of nuclear power. We have said that we will cut our reliance on nuclear power and that is exactly what we are doing” (Nucleonics Week, 2011). Three days after the Fukushima accidents started, Swedish Prime Minister Fredrik Reinfeldt said the decision “still holds” to allow for replacement of any of the country’s ten operating units that will be shut down in the future, and that safety reviews are not foreseen (Kinnunen and Johnson, 2011). But on March 30, 2011, the Swedish Radiation Authority agreed with the nuclear operators to review nuclear safety and to carry out “stress tests,” following the EU line (Radio Sweden, 2011). Public opinion has been shifting. A poll in the leading Swedish daily Dagens Nyheter showed that 36 percent of Swedes now support a phase-out of nuclear power, up from 15 percent in 2008 and up sharply since the Japanese crisis started. The poll also showed that only 21 percent of Swedes now favor further development of the country’s nuclear power capacity, a spectacular drop from 47 percent in 2008 (Agence France-Presse, 2011b).

Switzerland

The country was one of the first to take domestic action in response to the Fukushima crisis. On March 14, 2011, Energy Minister Doris Leuthard suspended the approval process for three new nuclear power stations so that safety standards could be revisited (Reid and Thomasson, 2011). Support for nuclear plants fell sharply in Switzerland following the crisis, with a poll published on March 20 showing that 87 percent of the population wants the country’s four reactors phased out (Agence France-Presse, 2011a).

United States

The American political system seems stunningly impervious to the concerns expressed in other countries after Fukushima. Energy Secretary Steven Chu stated on April 22, 2011: “President Obama and I believe that safe nuclear power has an important role to play in our energy mix as we move to a clean energy future” (Chu, 2011). By the end of April 2011, the Nuclear Regulatory Commission had not “identified anything that requires immediate action” (Nuclear Regulatory Commission, 2011a), even though current rules for station blackout (four hours autonomy) had been recognized as a serious potential safety problem.

Deputy Energy Secretary Daniel Poneman said nuclear power must be considered as part of any energy strategy, stating “we do see nuclear power as continuing to play an important role in building a low-carbon future. But be assured that we will take the safety aspect of that as our paramount concern” (Memoli, 2011). Senator Joe Lieberman of Connecticut stated on CBS’s Face the Nation: “I don’t want to stop the building of nuclear power plants, but I think we’ve got to kind of quietly, quickly put the brakes on until we can absorb what has happened in Japan … and then see what more, if anything, we can demand of the new power plants that are coming on line” (Mason and Dunham, 2011).

US Republican lawmakers who back nuclear power do not appear ready to give up the struggle because of events in Japan. Even though his state is a known earthquake-prone region, Congressman Devin Nunes of California has proposed a comprehensive energy bill that calls for 200 new nuclear power plants nationwide by 2040 and thinks the events at Fukushima will “make the case for nuclear power in the long run” (Acosta and Glass, 2011; The Guardian, 2011). Christine Tezak, an energy analyst with Robert W. Baird and Co., is skeptical, noting that there will be “further re-examination of future nuclear construction plans in the United States” and that “inexpensive natural gas in the United States has made it difficult to move forward with nuclear projects” (Behr, 2011).

Utilities and their investors, not politicians, ultimately decide whether to order new nuclear plants. John Rowe, CEO of Exelon, the largest US nuclear plant operator, agrees that “new nuclear plants are not economic investments with today’s natural gas forecasts” (Stelzer, 2011). Nuclear utility NRG, the majority shareholder of the South Texas Project (STP), announced in April 2011 that it is withdrawing from the project, writing off its $481 million investment and ruling out any further investment. The utility’s CEO David Crane said: “The tragic nuclear incident in Japan has introduced multiple uncertainties around new nuclear development in the United States which have had the effect of dramatically reducing the probability that STP 3 and 4 can be successfully developed in a timely fashion” (World Nuclear News, 2011b).

London-based bank HSBC concludes: “With Three Mile Island and Fukushima as a backdrop, the US public may find it difficult to support major nuclear new build and we expect that no new plant extensions will be granted either. Thus we expect the ‘clean energy’ standard under discussion in US legislative chambers will see a far greater emphasis on gas and renewables plus efficiency” (HSBC, 2011).

Under construction

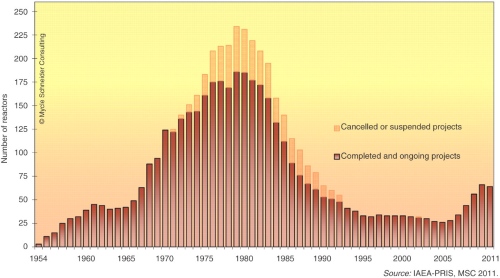

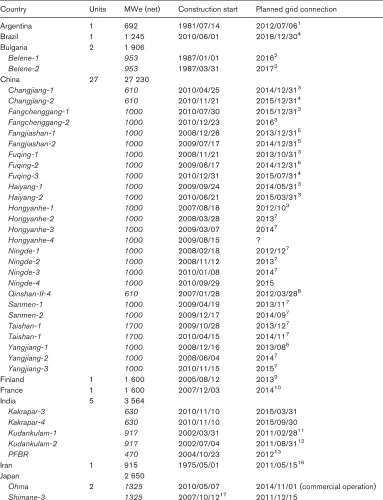

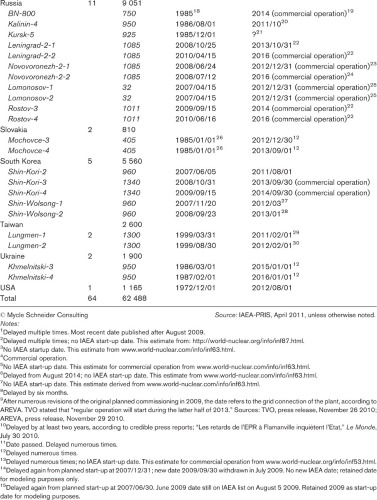

Currently, 14 countries are building nuclear power plants, and most of the sites are accumulating substantial and costly delays. As of May 15, 2011, the IAEA listed 64 reactors as “under construction,” nine more than at the end of 2009. This compares with 120 units under construction at the end of 1987 and a peak of 233 such units—totaling more than 200 gigawatts—in 1979 (HSBC, 2011: Fig. 4). (See Figure 3.) The year 2004, with 26 units under construction, marked a record low for construction since the beginning of the nuclear age in the 1950s.

Number of nuclear reactors listed as “under construction” by year, 1954 to 15 May 2011.

The total capacity of units now under construction is about 62.5 gigawatts, with an average unit size of around 980 megawatts. (See Annex 2 for details.) A closer look at currently listed projects illustrates the level of uncertainty associated with reactor building:

Twelve reactors have been listed as “under construction” for more than 20 years. The US Watts Bar-2 project in Tennessee holds the record, with an original construction start in December 1972 (subsequently frozen). Second place goes to the Iranian Bushehr plant, which went critical in May 2011 but is still not connected to the grid. It was originally started by the German company Siemens in May 1975 and has been completed by the Russian nuclear industry. Other long-term construction projects include three Russian units, two Belene units in Bulgaria, two Mochovce units in Slovakia, and two Khmelnitski units in Ukraine. The construction of the Argentinian Atucha-2 reactor started 30 years ago. In addition, two Taiwanese units at Lungmen have been listed for 12 years. Thirty-five projects do not have an official (IAEA) planned start-up date, including six of the 11 Russian projects, the two Bulgarian reactors, and 25 of the 27 Chinese units under construction. Two units officially under construction in Japan are likely to be abandoned. Many of the units listed by the IAEA as “under construction” have encountered construction delays, most of them significant. Construction of the remaining units started within the past five years, and expected start-up dates have not been reached yet. This makes it difficult or impossible to assess whether they are running on schedule. Nearly three-quarters (47) of the units under construction are located in just four countries: China, India, Russia, and South Korea. None of these countries has historically been very transparent or reliable about information on the status of their construction work. Nuclear reactors in the world listed as “under construction” (May 15 2011) © Mycle Schneider ConsultingSource: IAEA-PRIS, April 2011, unless otherwise noted.

Notes:

Delayed multiple times. Most recent date published after August 2009. Delayed multiple times; no IAEA start-up date. This estimate from: http://world-nuclear.org/info/inf87.html. No IAEA startup date. This estimate from www.world-nuclear.com/info/inf63.html. Commercial operation. No IAEA start-up date. This estimate for commercial operation from www.world-nuclear.com/info/inf63.html. Delayed from August 2014; no IAEA start-up date. This estimate from www.world-nuclear.com/info/inf63.html. No IAEA start-up date. This estimate derived from www.world-nuclear.com/info/inf63.html. Delayed by six months. After numerous revisions of the original planned commissioning in 2009, the date refers to the grid connection of the plant, according to AREVA. TVO stated that “regular operation will start during the latter half of 2013.” Sources: TVO, press release, November 26 2010; AREVA, press release, November 29 2010. Delayed by at least two years, according to credible press reports; “Les retards de l’EPR à Flamanville inquiètent l’Etat,” Le Monde, July 30 2010. Date passed. Delayed numerous times. Delayed numerous times. Delayed numerous times; no IAEA start-up date. This estimate for commercial operation from www.world-nuclear.org/info/inf53.html. Delayed again from planned start-up at 2007/12/31; new date 2009/09/30 withdrawn in July 2009. No new IAEA date; retained date for modeling purposes only. Delayed again from planned start-up at 2007/06/30. June 2009 date still on IAEA list on August 5 2009. Retained 2009 as start-up date for modeling purposes. Delayed countless times. This unit was added to the IAEA list only in October 2008. The IAEA Power Reactor Information System (PRIS) database curiously provides a new construction start date as 2006/07/18. Until 2003, the French Atomic Energy Commission (CEA) listed the BN-800 as “under construction,” with a construction start-up date of “1985.” In subsequent editions of the CEA’s annual publication ELECNUC, Nuclear Power Plants in the World, the BN-800 had disappeared. Delayed numerous times; no IAEA start-up date. This estimate from www.world-nuclear.com/info/inf29.html. Delayed from planned start-up at 2010/12/31 as of end of 2007; no new IAEA date. This estimate from www.world-nuclear.org/info/inf45.html. Delayed from planned start-up at 2010/12/31 as of end of 2007; no new IAEA date and deleted from WNA construction list. Kursk-5 is based on an upgraded RBMK design and its completion seems highly uncertain. We have arbitrarily envisaged, for modeling purposes only, that it starts in 2018. No IAEA start-up date; this estimate for commercial operation from www.world-nuclear.org/info/inf45.html. Commercial operation date introduced in early 2009. Delayed by two years; no IAEA start-up date. This estimate for commercial operation from www.world-nuclear.org/info/inf45.html. Commercial operation originally planned for 2010 at Severod. Since moved to Lomonosov and delayed by two years. On June 11 2009 construction officially resumed. Delayed. Start-up date of 2011/05/28 withdrawn from IAEA-PRIS. This date from www.world-nuclear.org/info/inf81.html. Delayed. Start-up date of 2012/05/28 withdrawn from IAEA-PRIS. This date from www.world-nuclear.org/info/inf81.html. Delayed many times from original start-up date of mid-2006. IAEA startup date passed. Delayed many times from original start-up date of mid-2007.

The geographical distribution of nuclear power plant projects is concentrated in Asia and Eastern Europe, extending a trend from earlier years. Between 2009 and May 15, 2011, a total of 10 units were started up, all in these two regions.

An aging population

In the absence of any significant new construction and grid connection over many years, the average age (since grid connection) of operating nuclear power plants has been increasing steadily and now stands at about 26 years. 6 Some nuclear utilities envisage average reactor lifetimes of beyond 40 years and even up to 60 years. The Organisation for Economic Co-operation and Development (OECD) World Energy Outlook 2010 recently gave a timeframe of 45 to 55 years, up five years from the 2008 edition of the report. It is obvious that the main incentive for lifetime extensions is their considerable economic advantage over new construction.

In the United States, reactors are usually licensed to operate for a period of 40 years. Nuclear operators can request a license renewal for an additional 20 years from the Nuclear Regulatory Commission. More than half of operating US units have received this extension. Many other countries, however, have no time limitations on reactor licenses.

At present, 12 of the world’s operating reactors have exceeded the 40-year mark. That number will rapidly increase over the next few years, with nine more units reaching age 40 in 2011. A total of 165 units have reached age 30 or more.

After the Fukushima disaster, it is obvious that operating age will get a second look. The troubled Fukushima-I units (1 to 4) were initially connected to the grid between 1971 and 1974. The license for unit 1 was extended for another 10 years only in February 2011. Four days after the beginning of the drama in Japan, the German government ordered the shutdown (for a three-month period) of seven reactors that had started up before 1981. It is now clear that the political climate in Germany makes a restart of these reactors practically impossible. Other countries might follow in a less dramatic manner, but there is no question that recent events are having an impact on previous assumptions about extended lifetimes.

Even if reactors can be operated for an average of 40 years, many new plants would have to come on line by 2015 to maintain the current number of operating reactors worldwide. Besides the 56 units that are under construction and expected to become operational by 2015, 7 18 additional reactors would have to be finished and started up within the next four years. This corresponds to one new grid connection every three months. An additional 191 units (175 GW) would have to come on line over the following 10-year period—one every 19 days—just to maintain the status quo. This situation has hardly changed from previous years.

Aside from any post-Fukushima effect, achievement of the short-term targets is simply impossible given the existing constraints on the fabrication of key reactor components. As a result, the number of reactors in operation will decline over the years to come (even if the installed capacity level could be maintained) unless lifetime extensions beyond 40 years become a widespread standard. The scenario of generalized lifetime extensions has grown less likely after Fukushima, as questions regarding safety upgrades, maintenance costs, and other issues would need to be much more carefully addressed.

Developments in Asia, and particularly in China, do not fundamentally change the global picture. Reported “official” figures for China’s 2020 target for installed nuclear capacity have fluctuated between 40 gigawatts and 120 gigawatts. 8 However, the average construction time for China’s first 10 operating units was 6.3 years. At present, about 27 gigawatts are under construction. While the acceleration of construction starts has been very impressive—with a total of 20 new building sites initiated in 2009 and 2010—the prospects for significantly exceeding the original 2008 target of 40 gigawatts for 2020 now seem dim. 9 China has reacted surprisingly rapidly and strongly to the Fukushima events by temporarily suspending approval of nuclear power projects. But even doubling the current capacity under construction would represent only half of the worldwide capacity of 145 units that reach age 40 by 2020.

Deutsche Bank analysts conclude that the global impact of the Fukushima accident is “a fundamental shift in public perception with regard to how a nation prioritizes and values its population’s health, safety, security, and natural environment when determining its current and future energy pathways.” As a consequence, “renewable energy will be a clear long-term winner in most energy systems, a conclusion supported by many voter surveys conducted over the past few weeks. At the same time, we consider natural gas to be, at the very least, an important transition fuel, especially in those regions where it is considered secure” (Deutsche Bank Group, 2011).

With utilities and the public doubtful about new nuclear investment in the United States, the largest economy in the world (by GDP), political leadership and society seriously warming up to a nuclear phase-out in the third- and fourth-largest economies, and financial institutions becoming increasingly hostile to nuclear projects, there seems to be little chance that the international nuclear industry will be able to keep selling lifetime extension of an aging technology as a nuclear renaissance.

Editor’s note

This article is based on the 85-page World Nuclear Industry Status Report 2010–2011: Nuclear Power in a Post-Fukushima World, published by Worldwatch Institute, Washington in April 2011 (see http://www.worldwatch.org/end-nuclear). The article includes updated statistics and policy measures that were current as of June 13, 2011.

Footnotes

Notes

Author biographies