Abstract

This study seeks to examine the influence of multi-layered gender diversity mechanisms on firms’ decision to engage in pro-sustainable performance in the context of Hospitality and Tourism (H&T) firms worldwide. Using Powell’s Panel Quantile Regression (PQR) model, this paper finds that females on boards and sub-boards tend to display a more communal, participative, and democratic leadership style, demonstrating greater responsibilities toward stakeholders’ concerns and engaging with sustainability strategies to make a positive contribution to society. Our findings also reaffirm that women on the boards of H&T firms are more community-oriented and philanthropically driven than women in senior management positions who can be perceived as being profit-oriented rather than stakeholder-oriented as managers. Our results offer implications for policymakers and practitioners, and we suggest several avenues for future studies that could build upon our research.

Keywords

Introduction

The hospitality and tourism (H&T) sector is known for its potential to engender both positive (Davidson and Sahli 2015; Pérez and Rodríguez del Bosque 2014; Scheyvens and Hughes 2019; Soteriou and Coccossis 2010), and negative socio-economic and environmental impacts (Buckley 1996, 2012; Holden 2005; Poudel, Nyaupane, and Budruk 2016; Rhou and Singal 2020). In relation to the latter, environmental harm created through disruption to wildlife, the over-extraction of water sources, deforestation and the draining of coastal wetlands (Holden 2005), to the propagation of social inequalities through sustained low wages has often been the subject of public criticism (Rhou and Singal 2020). The H&T sector has nevertheless been earmarked as a critical sector capable of contributing to the achievement of the sustainable development goals (SDGs) across developing and least-developed countries (Alarcón and Cole 2019; Kim, Bonn, and Hall 2021), with the United Nations World Tourism Organization, incorporating “sustainability” into their “2030 Agenda.”

Thus, increasing stakeholder pressure, together with widespread criticism of the H&T sector’s performance related to social and environmental sustainability, have compelled companies operating within the sector to adopt pro-sustainable corporate practices in recent times (Paramati, Alam, and Chen 2017; Uyar et al. 2020; Zhang et al. 2021).

The Covid-19 crisis, however, has setback the progress made in relation to the SDGs world over (Jones and Comfort 2020), with many countries compelled to adopt corrective actions to resolve major socio-economic challenges arising from job losses to increasing levels of poverty. As a sector which was impacted the most due to the pandemic, it is even more important now to understand “how” the H&T sector and companies operating within it upheld their commitments toward social and environmental sustainability by engaging in associated pro-sustainable corporate performance whilst addressing strategic priorities for financial solvency (Bramwell 2015; Corne and Peypoch 2020), during the pandemic.

The issue of gender diversity, specifically, has been seen as a core tenet in addressing pro-sustainable corporate practices in recent times. For example, in companies such as Schneider Electric, listed by Fortune as one of the World’s most admired companies and ranked third worldwide (within the sector) for its commitment to innovation and sustainability performance (Where Women Work 2021), the executive committee consists of 38% women and three out of five business markets are led by women (Workplace Intelligence 2021). As reiterated by Tina Mylon, a Female Senior Vice President of Schneider Electric, the company’s pro-sustainability practices are a balance between “gender diversity” and “sustainability,” with each complementing the other; “At Schneider, when it comes to measuring success, we are quite transparent about the importance of driving metrics around gender diversity & inclusion on the one hand and sustainability on the other hand. Nevertheless, these metrics should have a purpose and accountability scheme. The central pillar for Schneider, in this case, is what we call Schneider sustainability index, which is very much aligned with the UN’s SDGs” (Workplace Intelligence 2021, p 6).

Thus, the adoption of inclusive diversity management strategies, promoting the equal participation of women across different levels of governance in companies, can lead to more pro-sustainable corporate performance (Where Women Work 2021). Nevertheless, extant data and corporate trends contradict the manifestation of gender equality within corporate governance, with a substantive lack of women’s leadership in business. For example, based on their 2019 data set of over 1,000 large companies across 15 countries, McKinsey & Company (2020) observed that women made up just 15% of executive positions, and more than a third of firms surveyed had no women at all on their executive teams. The level of women’s representation also varied across countries, with companies in Norway having at least one female executive on their boards and countries such as Germany, India, Japan, and Brazil having 8% or fewer women representation on board (McKinsey & Company 2020). There are also significant differences in the rates of progress, in gender diversity on boards, across industries, with healthcare and finance industries having the highest level and the H&T sector being only slightly more gender diverse, with the percentage of female representation in top management positions made up by 29% in restaurants (McKinsey & Company 2021), 17% in hotels (Castell Project 2022), and 23% in tourism (UNWTO 2019). Overall, while women make up 51.9% of the hospitality workforce and 61% of the H&T tourism industry, women on the board of directors in these sectors are only 23% (Equality in Tourism International 2018; MBS Intelligence 2021; UNWTO 2019). Recent research has also suggested that women in the H&T sector still experience more barriers and disadvantages compared to their male counterparts (Ali, Grabarski, and Konrad 2022; Baum et al. 2020; Gebbels, Gao, and Cai 2020; Mooney 2020). As such, although significant progress in relation to gender diversity has been achieved since 2015, within the H&T sector, there is as yet substantial room for further improvement (Russen, Dawson, and Madera 2021).

Decision-making for pro-sustainable corporate performance is made by the board of directors of companies, and as such, corporate governance has been closely examined as one of the key determinants of firms’ sustainability performance. A variety of such governance factors, including board independence, board composition, CEO duality, directors’ ownership, etc., are often identified as key factors influencing pro-sustainability corporate performance (See Hussain, Rigoni, and Orij 2018; Naciti, Cesaroni, and Pulejo 2022). The presence of higher levels of risk, leverage, capital intensity and competitive rivalry (Singal 2015) within the H&T sector inherently accords greater decision-making power to corporate boards (Uyar et al. 2020). As such, these boards of directors are expected to protect the interests of all stakeholders’ (Pucheta-Martínez and Gallego-álvarez 2019) and fulfill their ethical, social and environmental responsibilities (García Martín and Herrero 2020) by making the right decisions related to corporate sustainability.

There have been many studies which have examined the manifestation of gender diversity at the board level of companies as a pre-cursor toward more pro-sustainable corporate performance. Empirical evidence substantiates the existence of a positive relationship between gender diversity in management and pro-sustainability corporate performance (Ben-Amar, Chang, and McIlkenny 2017; Shoham et al. 2020). Thus, the presence of female directors on corporate boards is deemed to be more supportive of stakeholder-focused and socially responsible initiatives (Amorelli and García-Sánchez 2021; Atif et al. 2021). From a broader perspective, gender diversity across various leadership positions has been found to have positive effects on various corporate practices, such as governance structures, managerial actions, innovation, risk management, and financial performance (See Almor, Bazel-Shoham, and Lee 2022; Arun, Almahrog, and Ali Aribi 2015; Baixauli-Soler, Belda-Ruiz, and Sanchez-Marin 2015; Carter et al. 2010; Chijoke-Mgbame, Boateng, and Mgbame 2020; Griffin, Li, and Xu 2021; Gul, Srinidhi, and Ng 2011; Gull et al. 2018; Tingbani et al. 2020; Triana, Miller, and Trzebiatowski 2014).

Thus, we argue that rather than exclusively focusing on the impact of gender diversity (or female representation) on boards of directors, we should examine the role of gender diversity at various managerial levels within the organization in engendering pro-sustainable performance. In this regard, we argue that even on corporate boards, women could hold different positions and responsibilities that may influence their decision-making. For instance, female directors could either hold executive or non-executive positions, therefore, influencing their independence, strategic priorities, and decision-making (Cullinan, Mahoney, and Roush 2019). As such, decisions undertaken by female executives regarding pro-sustainable corporate performance may differ (e.g., Branson 2006; Niederle and Vesterlund 2010) from those undertaken by female directors in specialist committees, such as sustainability committees.

However, our understanding of “how” can effective women’s representation in sustainability-related committees enhance firms’ sustainability performance is as yet absent, to the best of our knowledge, from extant literature, specifically with regard to the H&T sector (Kılıç et al. 2021; Ooi, Hooy, and Som 2015). Considering many major board decisions are taken at the sub-board (committee) level rather than the full corporate board level, we argue that a multi-level perspective on gender diversity would provide significant insights into how differences in female directors’ roles and responsibilities could alter our existing understanding of the relationship between gender diversity and pro-sustainability corporate performance. As such, we aim in this paper to examine the association between a multi-layered gender diversity criterion—including board gender diversity, female executives and women on sustainability committees—on firms’ sustainability performance in the H&T sector worldwide.

Using Powell’s (2022) panel quantile regression (PQR) model, our international empirical evidence suggests that board gender diversity is positively and significantly associated with pro-sustainability corporate performance as measured by ESG rating and its dimensions (i.e., environmental, social and governance scores) among a select sample of 1507 firm-year observations of 137 H&T firms over the period from 2010 to 2020. In contrast, executive women are negatively attributed to sustainability performance and its environmental and governance categories. However, this association is statistically positive in the case of social performance. Our additional analysis shows that women on sustainability/CSR committees as the third dimension of gender diversity positively influence the sustainability performance and its dimensions among a focused sample of 495 firm-year observations of 45 H&T companies worldwide. Our results are robust to alternative measures of gender diversity and sustainability performance, and endogeneity concerns.

Our study, therefore, contributes to the ongoing debate about the role of women (and gender diversity) within the boardroom. While calls for corporate board reforms, engendering greater gender diversity, have gained global momentum, questions still abound in relation to the “added value” of such a diverse board of directors (Adams and Ferreira 2009). The results of our study provide much-needed clarity on this matter by indicating that despite the general belief on the positive impact of board gender diversity on corporate sustainability performance, within the H&T sector, the effectiveness of female directors in propagating pro-sustainable corporate behaviors is very much dependent on their role and responsibilities. Thus, when female directors are given a role and associated responsibilities that are designed to protect stakeholder interests, they do encourage and support pro-sustainable corporate performance. On the other hand, the constraints of traditional management roles could limit the effectiveness of female directors due to the rigidity of their work self-schema and the expectation to focus on financial performance and shareholders’ demands in such positions.

From a narrower perspective, our study contributes to the H&T literature by examining pro-sustainability corporate performance at the sectoral level during the past 10 years. Despite the growing interest in corporate sustainability in the H&T sector, associated studies on the matter are largely theoretical, resulting in a growing need for both theory testing and theory elaboration (Rhou and Singal 2020). Prior research on pro-sustainability corporate performance, in particular, is scarce and mostly relies upon a single country context (mainly developed countries) or a specific sub-sector (mainly hotels) (See Alonso and Ogle 2010; Asadi et al. 2020; Martinez-Martinez et al. 2019). Limited attention has also been paid to the role of organizational capabilities in developing pro-sustainability performance in the H&T sector (Aragon-Correa, Martin-Tapia, and de la Torre-Ruiz 2015). Such an understanding, however, is particularly helpful for enabling appropriate decisions to be undertaken in order to improve the sector’s pro-sustainability performance. Our study reaffirms the effect of multi-level gender diversity upon engendering organizational capabilities (See Quintana-García and Benavides-Velasco 2016; Ruiz-Jiménez, Fuentes-Fuentes, and Ruiz-Arroyo 2016; Ruiz-Jiménez and del Mar Fuentes-Fuentes 2016), required for sustainability performance in numerous subsectors of H&T using a large international sample and providing industry-specific evidence.

Methodologically, our study is longitudinal and hinges upon both well-developed databases (i.e., Bloomberg and Eikon datasets) and manual content analysis of sustainability reports, which allowed us to identify the long-term impact of multi-level gender diversity on the various trends of corporate sustainability performance. Crucially, using the panel quantile regression (PQR) model of Powell (2022), our study uses the most appropriate estimation method to provide a more comprehensive analysis of the gender diversity-sustainability performance nexus than previous studies that were confined to the traditional regression models, including the least-squares methods (Elheddad et al. 2020; Gerged, Matthews, and Elheddad 2021). These traditional linear regressions summarize the average relationship between dependent and independent variables based on the traditional mean function E(yjx), which partially explains the examined relationships (Cobb-Clark, Kassenboehmer, and Sinning 2016). Thus, the conventional estimators are inefficient in examining the associations at various points in the conditional distribution of the outcome (dependent variable) (Koenker and Bassett 1978). Our study, therefore, methodologically contributes to extant gender diversity-to-sustainability literature by applying Powell’s (2022) PQR that overcomes traditional estimators’ limits. Specifically, Powell’s (2022) PQR predicts the conditional median (quantiles) of the dependent variable that is regarded as more robust to outliers than least squares regression. Also, the PQR model is semiparametric since it does not support parametric distribution assumptions of the error process (Cobb-Clark, Kassenboehmer, and Sinning 2016).

Together, our evidence supports the theoretical underpinnings of the upper echelon theory and gender socialization theory. While the upper-echelon theory provides a theoretical framework to explain the influence of the psychological and observable traits of directors on formulating and implementing strategies that affect corporate outcomes, such as sustainability performance (Nadeem et al. 2020), the gender socialization theory helps to distinguish the differences in values and traits between males and females due to their upbringing (Liu 2018) that could be brought to the management context and reflect in their approach to managing stakeholder interests and fostering sustainability practices (McGuinness, Vieito, and Wang 2017; Nadeem, Gyapong, and Ahmed 2020). Combining both theories in our study, therefore, is of theoretical value in explaining whether female directors, due to their caring and sensitive nature, may be vital for improving pro-sustainability corporate performance in modern corporations.

The remainder of this article is structured as follows. First, we discuss prior empirical literature, theoretical underpinning, and hypotheses development. Second, we explain the research design. Third, we discuss our empirical findings; finally, we conclude our implications, acknowledge the limitations, and open avenues for future studies.

Previous Studies

The issue of gender diversity at the management level has received some attention in both academic research and in practice. From a practice-based perspective, corporations have been pressured to increase female representation at the management level, primarily to fulfill their legitimacy seeking objectives (Hillman, Cannella, and Harris 2002). Although legitimacy has been the primary motivator for promoting greater gender diversity within corporate management, the detrimental results of its absence in sectors such as banking leading to numerous corporate scandals and crises (Kristof 2009; Majic 2014; Morris 2009) have reaffirmed the need to have more female representation at the top management levels of corporations (Huffington 2003). As a result, countries have pro-actively promoted minimum threshold requirements for female representation on boards through changes to corporate governance (CG) codes or listing requirements (Adams and Funk 2012).

There has been increasing interest in the scholar community pertaining to the impact of gender diversity (at the management level) and its impact on organizational practices. In this regard, previous studies have shown that female directors provide better oversight of managerial actions (Tingbani et al. 2020) improve governance structure and financial performance (Arun, Almahrog, and Ali Aribi 2015; Carter et al. 2010; Chijoke-Mgbame, Boateng, and Mgbame 2020; Gul, Srinidhi, and Ng 2011; Gull et al. 2018; Triana, Miller, and Trzebiatowski 2014), are more innovative (Almor, Bazel-Shoham, and Lee 2022; Griffin, Li, and Xu 2021), and less risk-taking (Baixauli-Soler, Belda-Ruiz, and Sanchez-Marin 2015) and are collectively more responsive to diverse stakeholder interests (Amorelli and García-Sánchez 2021). Most of these studies argue that differences associated with the “female gender,” such as unique female characteristics, are the key factor influencing these results. For instance, female attributes such as being sensitive, nurturing, kind, helpful, and sympathetic (Eagly, Johannesen-Schmidt, and van Engen 2003), and being concerned about others’ welfare, could collectively propagate more socially responsible behaviors and decisions pertaining to stakeholder issues, by female directors, than their male counterparts (Amorelli and García-Sánchez 2021; Atif et al. 2021; Jaffee and Hyde 2000).

The positive impact of gender diversity upon corporate sustainability and financial performance has also been substantiated with real-life corporate examples. In the “Diversity wins: how inclusion matters” report, for instance, McKinsey collected data from more than 1,000 large companies in 15 countries to provide new insights into how inclusion matters (McKinsey & Company 2020). The findings showed that companies with more women on their executive teams are significantly more likely to outperform companies with fewer or no women executives. The substantial performance differential is 48% between the most and least gender-diverse firms (McKinsey & Company 2020). The effect of gender diversity on outperformance is also different between advanced economies and emerging economies. The likelihood of financial outperformance reaches as high as 47% in advanced economies with high gender parity, such as the UK, US, Sweden and Finland, whilst it is limited to an average of 17% in lower-parity economies, such as Nigeria, India and Brazil. These findings echo previous results of a Credit Suisse (2016) analysis, where companies with more than 15% of women in senior management positions had 18% higher profitability compared to those with less than 10% representation. On average, the study found that firms with at least one woman on board had generated a 3.5% higher return per year for investors since 2005 than companies with all-male boards.

While evidence of the positive effect of gender diversity in management on pro-sustainable corporate performance has been substantial (Ben-Amar, Chang, and McIlkenny 2017; Shoham et al. 2020), questions remain as to whether a similar effect occurs when women act in key leadership positions (e.g., Branson 2006; Niederle and Vesterlund 2010), with some arguing that in a predominantly male environment, gender differences may disappear due to females adapting their behavior (Furlotti et al. 2019). Besides these inconclusive findings of women leaders’ impact on pro-sustainable corporate performance, most of the existing literature also focuses exclusively on examining gender diversity only at the board level (e.g., Almor, Bazel-Shoham, and Lee 2022; Amorelli and García-Sánchez 2021; Arun, Almahrog, and Ali Aribi 2015; Baixauli-Soler, Belda-Ruiz, and Sanchez-Marin 2015; Chijoke-Mgbame, Boateng, and Mgbame 2020; Griffin, Li, and Xu 2021; Gull et al. 2018; Tingbani et al. 2020). However, women do not just act as token board members but hold different positions and responsibilities, including acting as members of board committees (Bilimoria and Piderit 1994; Kesner 1988). As such, focusing only on gender diversity at the board level does not sufficiently capture the role of women in the top leadership in companies and their contributions toward achieving organizational outcomes, such as corporate sustainability performance. Aiming to capture the dynamic nature of female leadership and associated decision-making, our study adopts a multi-level perspective—that is, board-level, management level and sustainability committee level, and thereby examines whether gender diversity across these three levels influences pro-sustainable corporate performance within the H&T industry.

Theoretical Framework

Several theories have been utilized to explain the relationship between gender diversity at the management level and pro-sustainability performance, such as gender socialization (Chijoke-Mgbame, Boateng, and Mgbame 2020; Furlotti et al. 2019; Liu 2018), resource dependence theory (Tingbani et al. 2020), upper echelon theory (Li et al. 2017; Nadeem et al. 2020; Pan et al. 2020), and agency theory (Bravo and Reguera-Alvarado 2018). In this study, we adopt theoretical arguments from gender socialization and upper echelon theories to examine the impact of gender diversity at the top levels, including board, management, and sustainability committee, upon pro- sustainability corporate performance.

The upper echelon theory takes into consideration the links between the top management team’s behaviors and its performance (Li et al. 2017). The theory views the consentaneous values and recognitions of the top management members as important sources to explain the differences in corporate performance as top executives interpret situations through their personalized lenses and individual factors that undoubtedly influence corporate strategic choices (Li et al. 2017; Pan et al. 2020). With regard to corporate sustainability, for instance, if the board members and management teams share a stakeholder value perception, the more likely the firm’s management will develop an effective and coherent pro-sustainability strategy.

While the upper echelon theory emphasizes the essential role of top managers and their values in defining a firm’s strategic choices, the gender socialization theory provides a complementary perspective on how gender may affect top management’s decision-making approach. The primary argument under gender socialization theory is that the way different genders interact socially shapes their diverse interests and qualities, which leads to manifested differences in their actions and behaviors (Liu 2018; Nadeem et al. 2020; Rahman, Ibrahim, and Che Ahmad 2017). The theory postulates that through socialization, women have focused more on developing interpersonal skills, becoming more cooperative, compassionate, and nurturing (Liu 2018; Skogen 1999; Zelezny, Chua, and Aldrich 2000), therefore, exhibiting agentic, and communal attributes. Specifically, while men are mainly associated with being confident, independent, ambitious, aggressive, assertive and competitive, women are primarily referred to as being sympathetic, helpful, kind, nurturing, and sensitive (Nielsen and Huse 2010). Such differences could influence business decision-making related to pro-sustainability strategies in the business context. For example, when entering business careers, women may pay more attention to the ethical aspects of companies as compared to men (See Chijoke-Mgbame, Boateng, and Mgbame 2020; Chonko and Hunt 1985; Ferrell and Skinner 1988) due to their distinctive female values. At the management level, female leaders rely more on collaboration and cooperation with and amongst subordinates instead of asserting their control and outcompeting each other, and hence, are more likely to employ an interactive, democratic and inclusive leadership style (Adams and Funk 2012; Eagly, Johannesen-Schmidt, and van Engen 2003; Rudman and Glick 2001; Singh, Vinnicombe, and Johnson 2001). With these characteristics and their ability to facilitate more informed decisions, gender diversity at this level might help to improve the quality and effectiveness of board-level decision-making (Ben-Amar, Chang, and McIlkenny 2017), thereby increasing its attention and commitment toward managing stakeholder interests and engaging with pro-sustainability corporate performance (Nadeem et al. 2020).

Drawing collectively from both the upper echelon theory and gender socialization theory arguments, we assert that companies’ strategic decision choices related to pro-sustainable behavior are influenced by their top managers’ (and leaders) personal interpretations (Hambrick 2007), and due to the unique nature of female personality, values and experiences, greater female representation at the top management level in companies, would have a substantial influence upon the firm’s strategic sustainability trajectory.

Hypotheses Development

Gender Diversity on Board and Pro-Sustainability Corporate Performance

In public corporations, the board of directors is responsible for every significant operational or strategic decision, including sustainability policies and strategy (Dixon-Fowler, Ellstrand, and Johnson 2017). Due to the important role that the boards of directors play in formulating and implementing strategies, from the upper echelon theory perspective, the demographic traits, characteristics, and unique values of these directors are expected to influence their decision-making process (Nadeem, Zaman, and Saleem 2017), consequently influencing the company’s strategic direction. As a result of increased public scrutiny, the development of corporate governance codes and associated regulatory changes, collectively promoting gender diversity, the issue of gender diversity on boards has received major attention in recent years (Ben-Amar, Chang, and McIlkenny 2017). These changes, together with an increasing focus on upholding stakeholder interests rather than protecting shareholder interests, have presented an interesting context to examine the relationship between gender diversity and pro-sustainability corporate performance (See Bear, Rahman, and Post 2010; Nadeem, Zaman, and Saleem 2017; Nadeem et al. 2020). While there has been overwhelming empirical evidence supporting the positive impact of board gender diversity on corporate sustainability decisions and performance (See Bear, Rahman, and Post 2010; Ben-Amar, Chang, and McIlkenny 2017; Glass, Cook, and Ingersoll 2016; Hollindale et al. 2019; Liao, Luo, and Tang 2015; Mallin and Michelon 2011), some studies have argued that board gender diversity might not have any real impact, upon pro-sustainability decisions, as the appointment of female directors can be carried out for purely symbolic reasons, driven by ethical and social pressures, thus becoming a mechanism to counter social injustice and mitigate discrimination at corporate top management level (Chijoke-Mgbame, Boateng, and Mgbame 2020). Female directors’ ability to create a positive impact and perform successfully is also constrained by both tokenism and stereotype threats (Low, Roberts, and Whiting 2015), limiting the demonstration of typical gender traits at the director level. For instance, in their study on gender differences in the boardroom, Adams and Funk (2012) observe that, unlike women’s characteristics in the general population, female directors pay less attention to conformity, security and tradition and more to stimulation. On boards where women are under-represented below a critical mass, they might feel pressured to fit into a typical role by exhibiting extreme values (Adams and Funk 2012) and therefore failing to exert any influence on a board’s strategic decision-making process (Ben-Amar, Chang, and McIlkenny 2017).

Despite the contradictory findings, drawing from upper echelon and gender socialization theories, we argue that increasing female board representation may positively impact sustainability performance. As high-skilled individuals, directors bring to the boardroom their distinctive leadership styles. With traits that are closely linked to their genders, such as cooperation, risk-averseness and high standards of ethical judgment, female directors tend to display and adopt a more communal, participative, and democratic leadership style (Akaah 1989; Chijoke-Mgbame, Boateng, and Mgbame 2020; Dawson 1997; Eagly, Johannesen-Schmidt, and van Engen 2003; Gilligan 1993; Rudman and Glick 2001; Tingbani et al. 2020). From the gender socialization perspective, these characteristics, together with a greater sense of moral responsibility and awareness, may motivate female directors to demonstrate greater sensitivity toward stakeholders’ concerns and engage with sustainability strategies which make a positive contribution to the environment and society (Bear, Rahman, and Post 2010; Ben-Amar, Chang, and McIlkenny 2017; Glass, Cook, and Ingersoll 2016; Haque and Jones 2020; Liao, Luo, and Tang 2015; Mallin and Michelon 2011; Nielsen and Huse 2010). Additionally, the presence of female board members has been argued to contribute to the improvement of Corporate Governance (CG) practices by enhancing high-quality board decisions and effectiveness (Bear, Rahman, and Post 2010; Coffey and Wang 1998; Nielsen and Huse 2010). Therefore, our hypothesis on the impact of board gender diversity on pro-sustainability corporate performance is presented as follows:

H1: Ceteris paribus, there is a statistically positive and significant relationship between women on boards and sustainability performance in H&T sectors.

This hypothesis can be divided into the following sub-hypothesis:

H1-a: Ceteris paribus, there is a statistically positive and significant relationship between women on boards and environmental performance in H&T sectors.

H1-b: Ceteris paribus, there is a statistically positive and significant relationship between women on boards and social performance in H&T sectors.

H1-c: Ceteris paribus, there is a statistically positive and significant relationship between women on boards and governance performance in H&T sectors.

Gender Diversity in Management and Pro-Sustainability Corporate Performance

The majority of existing organizational studies on gender diversity at the board level have taken a simplistic approach with a strong assumption that all female directors behave in the same way due to their inherent female nature. However, such an approach ignores the type of roles that female directors assume as board members (Cullinan, Mahoney, and Roush 2019) and the subsequent influence their role would have upon their decision-making. For instance, CG literature argues that directors appointed from outside of the company are more likely to fulfill their corporate oversight responsibilities than those appointed from inside the company (Alkalbani, Cuomo, and Mallin 2019). Furthermore, independent (or non-executive) directors usually tend to be more aware of stakeholder demands and, therefore, tend to consider broader stakeholder interests when making decisions (See Boulouta 2013; Dunn and Sainty 2009; Kassinis and Vafeas 2002). On the other hand, executive directors and CEOs, exuding entrepreneurial values, such as power, higher achievement, lower universalism values and self-direction values (Adams, Licht, and Sagiv 2011), tend to be more pro-shareholder. A question arises as to whether female directors or those in senior management positions would exhibit the same role-specific behaviors and, if so, whether their impact upon pro-sustainable behavior would be similar to those of their male counterparts.

From the upper-echelon theory perspective, the focus on the role and influence of female executives have long been an important aspect of studies on executive teams and corporate strategic decision-making. The extent to which female executives demonstrate gendered attributes in their positions has been a subject of debate in this body of literature (Adams and Funk 2012; Glass, Cook, and Ingersoll 2016; Ibrahim, Angelidis, and Tomic 2009; Lim and Chung 2021; Martin, Nishikawa, and Williams 2009; Matsa and Miller 2013; Oakley 2000; Oumlil and Balloun 2009).

On the one hand, scholars expect differences in gender would lead to individual differences in beliefs, attitudes, norms, and other cognitive factors (Pan et al. 2020). Supporting this view, several studies on female executives confirm that as leaders, women are more ethical, risk-averse, long-term oriented, and stakeholder focused than men due to the nature of their socialization and career path that place a stronger emphasis on community focus and relationship building (Adams and Funk 2012; Glass, Cook, and Ingersoll 2016; Ibrahim, Angelidis, and Tomic 2009; Martin, Nishikawa, and Williams 2009; Matsa and Miller 2013; Oumlil and Balloun 2009). As female managers often experience difficulties and prejudice upon their journey to the upper echelons of the firm (Oakley 2000), they will be more supportive and inclined toward helping minorities and communities through corporate social responsibility actions (Lim and Chung 2021).

On the other hand, some studies report a lack of strong evidence to argue that gendered differences in managerial decision-making influence a company’s ethical attitudes and support for sustainability-related issues (Chijoke-Mgbame, Boateng, and Mgbame 2020; Cullinan, Mahoney, and Roush 2019; Glass, Cook, and Ingersoll 2016). Furlotti et al. (2019), for instance, argue that as the position of managers is usually associated with males, the job self-schema could prevail over any influence exerted by the gender self-schema. Nevertheless, we argue that while the gender gap could decrease for those who have entered the upper echelons of a company due to workplace socialization, the fundamental differences attributable to trait differences between genders do remain (Adams and Funk 2012). Therefore, drawing upon the theoretical views of the upper echelon and gender socialization theories, female managers adopting a more stakeholder-oriented leadership is hypothesized to play a crucial role in adopting and improving pro-sustainability corporate performance (Dyllick and Hockerts 2002).

H2: Ceteris paribus, there is a statistically positive and significant relationship between executive women and sustainability performance in H&T sectors.

This hypothesis can be divided into the following sub-hypothesis:

H2-a: Ceteris paribus, there is a statistically positive and significant relationship between executive women and environmental performance in H&T sectors.

H2-b: Ceteris paribus, there is a statistically positive and significant relationship between executive women and social performance in H&T sectors.

H2-c: Ceteris paribus, there is a statistically positive and significant relationship between executive women and governance performance in H&T sectors.

Gender Diversity in Sustainability Committee and Pro-Sustainability Corporate Performance

In response to the complexity and enormous responsibility of the board oversight role, following good CG codes and practice, boards of listed firms are required to establish standing committees to help with decision-making and improve the board’s effectiveness (Chijoke-Mgbame, Boateng, and Mgbame 2020; Huang et al. 2011). These committees, composed of directors with more specialized responsibilities, focus on addressing specific corporate concerns and the performance of key tasks (Adams and Ferreira 2004; Dixon-Fowler, Ellstrand, and Johnson 2017). Indeed, many critical corporate decisions are initiated at the committee level (Jiraporn, Singh, and Lee 2009; Kesner 1988). Hence, the limited empirical work on board committees has raised the need for CG research to move away from a focus on the board of directors to board committees for more meaningful results (Dixon-Fowler, Ellstrand, and Johnson 2017).

Aligned with the extension of a board’s role and responsibility to encompass the interests of wider stakeholders (Rao and Tilt 2016), increasingly, companies have established a separate committee to take care of corporate sustainability matters and satisfy stakeholder concerns for increased accountability (Amran, Lee, and Devi 2014; Kassinis and Vafeas 2002; Liao, Luo, and Tang 2015). The existence of such committees signals the firm’s concern for sustainability (Neu, Warsame, and Pedwell 1998) and its willingness to engage with relevant issues (Liao, Luo, and Tang 2015; Peters and Romi 2014), thereby undoubtedly influencing companies’ sustainability policies, strategies, and performance. While certain committees, such as audit and compensation, are mandated by regulations and the stock exchange’s listing requirements, sustainability committees are primarily regarded as voluntary mechanisms of board governance, which raises interesting questions on the decision to form such committees, the structure of the committees, and the specific role they play.

Existing literature has discussed at length the presence and impact of sustainability committees on corporate social and environmental performance (Biswas, Mansi, and Pandey 2018), the effectiveness of CSR strategies (Orazalin 2020) and corporate transparency (Hussain, Rigoni, and Orij 2018; Kılıç et al. 2021). Nevertheless, consistent with the lack of CG research on board committees (Berrone and Gomez-Mejia 2009), current literature has provided relatively little insight into the composition of such committees and their impact on pro-sustainable corporate performance. Emphasizing the importance of a board committee’s composition, Klein (1998) postulates that membership of board committees is a more accurate reflection of the relationship between board composition and board effectiveness as it indicates the specific role each director plays on the board. Since most of the board work is carried out at the committee level, the composition of board committees, such as its gender diversity, may affect the functioning of such committees and the firm as a whole (Green and Homroy 2018; Guo and Masulis 2015). Nevertheless, the effect of female participation in such committees, while being interesting, has largely been ignored in extent research (Chijoke-Mgbame, Boateng, and Mgbame 2020). Therefore, in this study, we argue that as sustainability committees are set up for a specific purpose, female directors appointed to these committees should have the requisite expertise and be actively involved in carrying out the mandate of the committee. As previously argued by gender socialization theory, women on sustainability committees, due to their associated gendered traits and qualities, should be more actively interested in propagating sustainability and, as such, would positively influence the firm’s pro-sustainability performance. Thus, we formulate the third hypothesis as follows:

H3: Ceteris paribus, there is a statistically positive and significant relationship between sustainability committee gender diversity and sustainability performance in H&T sectors.

This hypothesis can be divided into the following sub-hypothesis:

H3-a: Ceteris paribus, there is a statistically positive and significant relationship between sustainability committee gender diversity and the environmental performance in H&T sectors.

H3-b: Ceteris paribus, there is a statistically positive and significant relationship between sustainability committee gender diversity and the social performance in H&T sectors.

H3-c: Ceteris paribus, there is a statistically positive and significant relationship between sustainability committee gender diversity and the governance performance in H&T sectors.

Research Design

Data and Sampling Criteria

This study employs the Bloomberg index and Refinitiv Eikon (aka Thomson Reuters Eikon; Eikon thereafter) databases to measure our research variables. We use the Eikon dataset for environmental, social, and governance (ESG) scores to measure firms’ sustainability performance (Flammer 2021). ESG ratings are primarily based on information available in firms’ annual reports, CSR/sustainability reports, and websites. Specifically, ESG scores are associated with quantitative and policy-related ESG activities (Huber and Comstock 2017). Also, ESG data comprises 120 indicators, including 10 categories divided into three individual dimensions (i.e., environmental score, social score and governance score) to measure pro-sustainability corporate performance. Arguably, ESG scores are expected to directly track sustainability performance (Zumente and Lāce 2021) and thus, are employed as proxies for sustainability performance in the current study.

Each ESG pillar is associated with industry-specific scores, whose specifications establish exclusive information that Eikon and Bloomberg do not share in full detail. These weights are normalized from 0 to 100 and available either as a total ESG score or as single-category or dimension scores. Crucially, according to Refinitiv Eikon (2021), the Environment score (ENV) represents three main categories of environmental performance, including emissions, innovation, and resource use. Likewise, the social score (SOCIAL) reflects four social categories, which are human rights, product responsibility, workforce, and community. Besides, the governance score (GOVER) measures three broad categories: management, shareholders, and CSR strategy. Although prior studies used ESG data from different sources, such as KLD Research and Analytics, these datasets are binary; thus, they are less affluent in terms of variations in ESG data than Eikon and Bloomberg scores (Eliwa, Aboud, and Saleh 2021; Zumente and Lāce 2021).

Our study seeks to assess whether a multi-layered gender diversity criterion can work efficiently in H&T firms seeking to eliminate harmful global warming and other sustainability effects in order to develop well-functioning societies and protect the environment around the world. We collected data to develop a multi-layered gender diversity criterion and then examine its impact on the sustainability performance of H&T institutions around the world. The dataset required for the study has been collected from Bloomberg and Eikon, including board gender diversity and female executives. However, data related to women on sustainability/CSR committees (i.e., corporate-level management committees, other than the board of directors) was manually collected from other sources, such as annual reports, sustainability/CSR reports, and firms’ websites. We have done an initial screening on both Refinitiv Eikon and Bloomberg databases to figure out the extent to which ESG-related data (i.e., to measure the sustainability performance of companies) is available, and we conclude the following. First, based on Bloomberg classification and in line with prior studies of a similar nature (e.g., Frechtling 2004; Pechlaner et al. 2004), the H&T sector in our study consists of the following industries: Casino & Gaming, Cruise lines, Entertainment facilities, Lodging, Restaurants and Travel and Tourism services. In this regard, Zabel (2003) stated that H&T sectors are umbrella terms for a wide range of commercial activities. For instance, the hospitality sectors include lodging, food services in restaurants, planes and cruise ships, clubs, cafeterias, hospitals, etc., while the tourism sectors support a traveler requirements for transportation, food, amusement, lodging, and entertainment. Zabel (2003) added that while the tourism sectors serve people away from home, the hospitality industry serves not only travelers but also people in their local area. Therefore, our focus on examining the gender diversity-sustainability nexus has been extended to cover the wider umbrella of tourism and travel industries, namely the H&T sector. Second, our initial sample comprises approximately 1,713 H&T companies globally, resulting possibly in 18,843 firm-year observations worldwide.

Our sampling criteria are based on two main pillars. First, to be included in our sample, every firm should offer data relating to gender diversity and ESG scores from 2010 to 2020. Applying this criterion has only led to considering a final sample of 137 H&T companies worldwide, resulting in 1,507 firm-year observations. Second, we collected additional data for a more focused sample of firms that have established sustainability/CSR committees in order to examine the impact of women on the sustainability committee, as the third dimension of gender diversity, on ESG proxies. Specifically, this data has been collected manually from annual reports, sustainability/CSR reports, and corporate websites about women’s representation (percentage) on sustainability/CSR committees of H&T firms and from Bloomberg and Eikon datasets for the remaining variables. This process has resulted in 45 firms with multi-leveled gender diversity data from 2010 to 2020, considering 495 firm-year observations. This means that we conduct our statistical analysis using two sets of samples. The first is a comprehensive sample that consists of 1,507 firm-year observations to examine the effect of two-layered gender diversity (i.e., board gender diversity and management gender diversity) on sustainability performance. The second is a focused sample that includes 495 firm-year observations to examine the influence of three-leveled gender diversity (i.e., board gender diversity, top management gender diversity, sustainability/CSR committee gender diversity) on the sustainability performance of H&T firms worldwide.

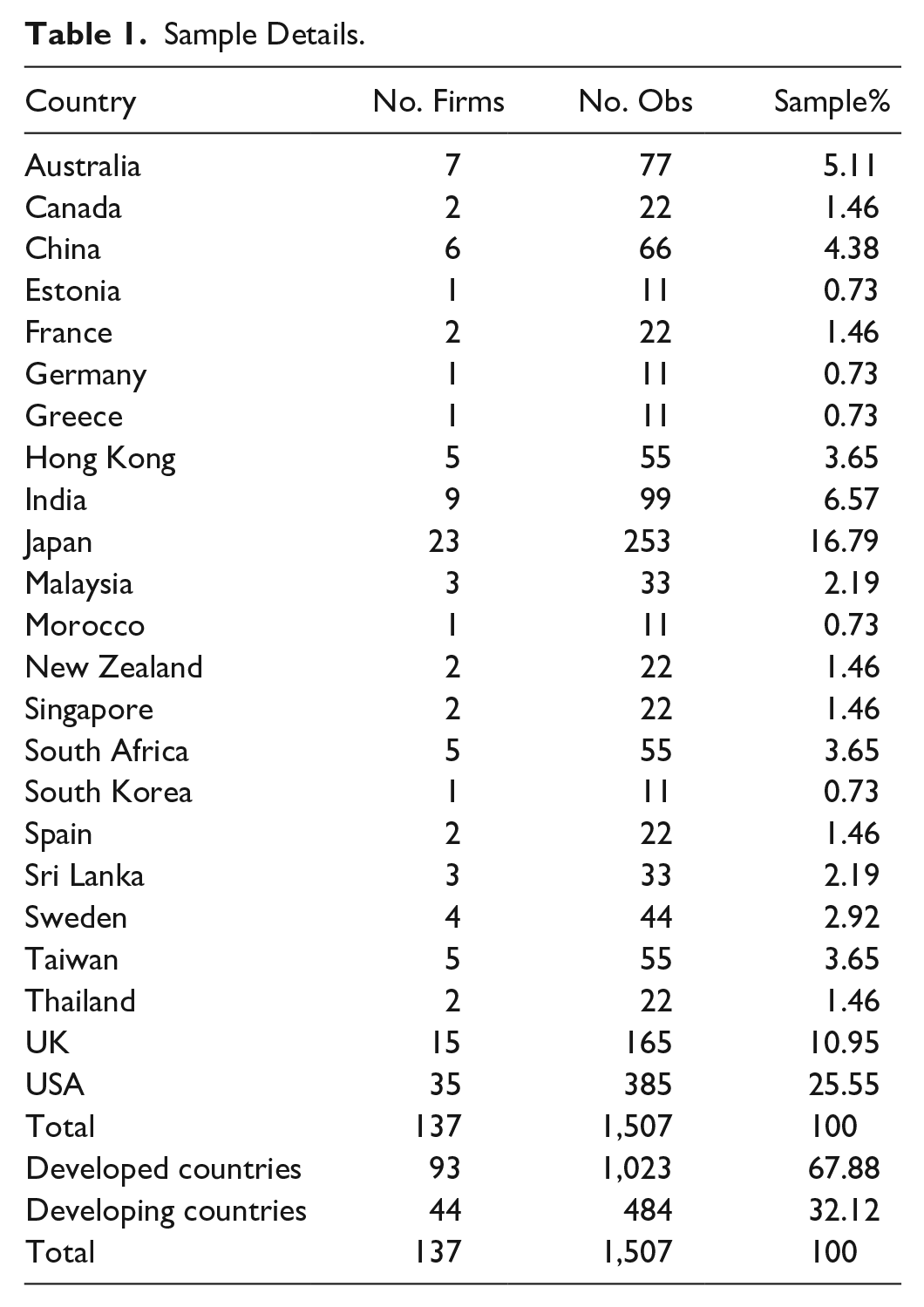

Table 1 shows the details of the sample of our study. Specifically, Table 1 suggests that about 67.9% of our sampled firms are related to developed economies, while only 32.1% belong to their developing counterparts. The United States has the largest share of this sample with 35 firms (25.55% of the sample), followed by Japan and the United Kingdom with 16.79% and 10.95%, respectively. On the other hand, the lowest representation in our sample was associated with Germany, Morocco, Estonia, Greece, and South Korea with 0.73%, only.

Sample Details.

Research Variables

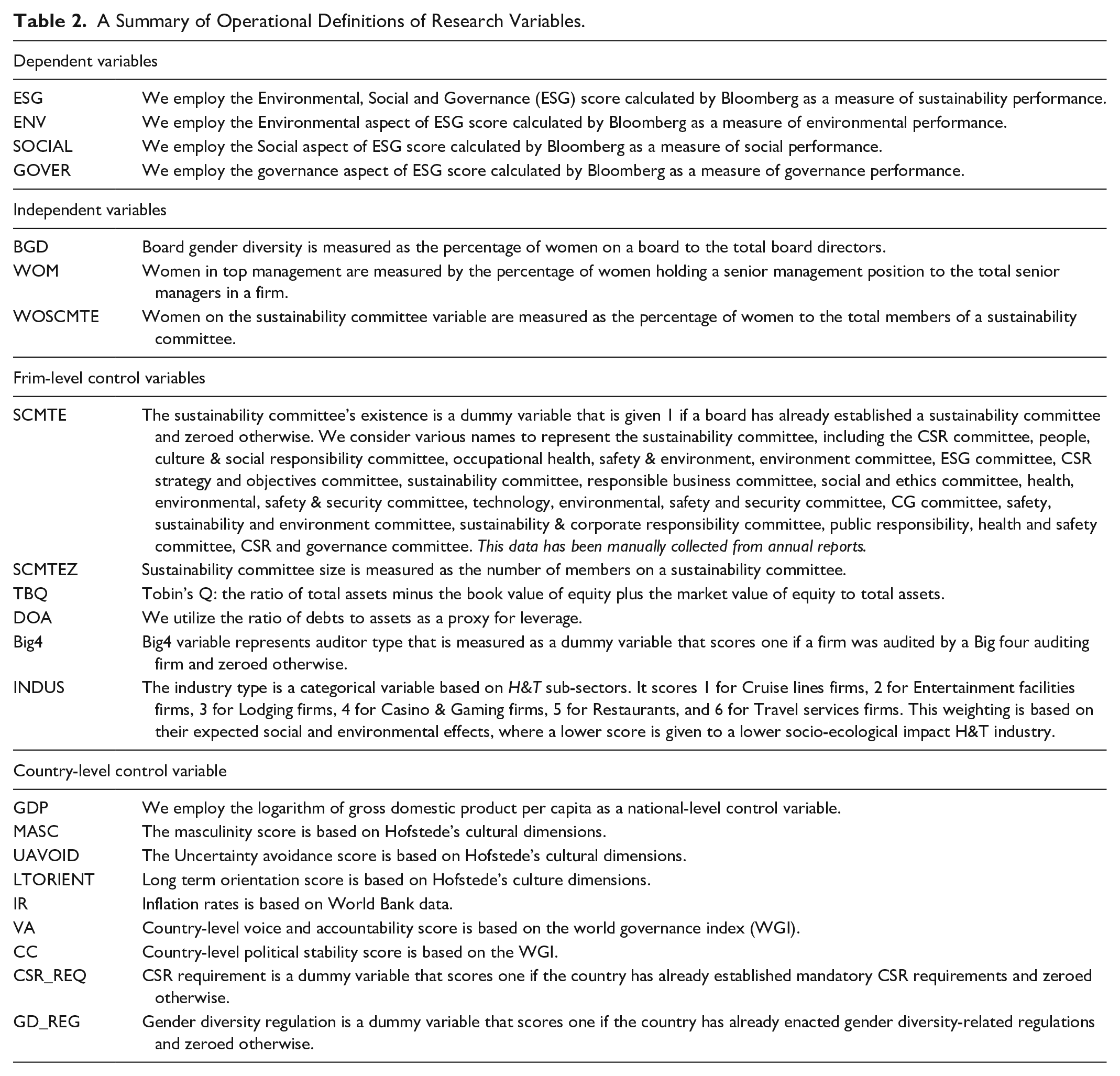

Table 2 defines our research variables operationally. In examining the research hypotheses, we divide the variables’ measurement into four stages. First, as a dependent variable, sustainability performance is measured using the scores of ESG variables, including the total ESG score, the environmental score (ENV), the social score (SOCIAL), and the governance score (GOVER). According to Refinitiv’s methodology, calculating the overall (total) ESG score is the relative sum of the weights of 10 categories, including emissions, innovation, resource use, human rights, product responsibility, workforce, community, management, shareholders, and CSR strategy (Refinitiv 2021). These categories are divided into the three main dimensions of the total ESG score as follows: environmental score (i.e., emissions, innovation, and resource use), social score (i.e., human rights, product responsibility, workforce, and community) and governance score (i.e., management, shareholders, and CSR strategy), which are calculated based on the Refinitiv magnitude matrix. Second, board gender diversity (BGD) and women in management (WOM), as independent variables and proxies for the multi-layered gender diversity measurement, are also measured using the Bloomberg dataset from 2010 to 2020. In contrast, the percentage of women on sustainability committees (WOSCMTE) has been collected manually from annual reports, CSR/sustainability reports and firms’ websites. Third, in line with prior studies (see Baldini et al. 2018; Crifo and Forget 2015; Fifka 2013; Hassan, Roberts, and Atkins 2020; Ntim 2016), we employ a set of firm-level and country-level variables to control for gender diversity-ESG nexuses in an effort to overcome any omitted variables-related concerns (Wooldridge 2016). The selected firm-level control variables are sustainability committee size (SCMTE), the firm market value represented by Tobins’ Q (TBQ), leverage, as measured by debt to assets ratio (DOA), firm size proxied by the logarithm of market capitalization (MKTCAP), auditor type as measured by big four auditors (Big4), and a dummy variable, represents the sub-industry type. The selected country-level control variables are culture dimensions as measured by masculinity (MASC), uncertainty avoidance (UAVOID), and long term orientation (LTORIEN), national-level governance as proxied by voice and accountability (VA) and control of corruption (CC), the gross domestic product (GDP), inflation rate (IR), CSR requirements (CSR_REQ), and the gender diversity regulations (GD_REQ) (See Table 2 for further details).

A Summary of Operational Definitions of Research Variables.

Fourth, to explore the multi-gender diversity-ESG nexuses, we use a panel quantile regression (PQR) model (Cobb-Clark, Kassenboehmer, and Sinning 2016; Powell 2022). This technique is also supplemented with conducting a two-step generalized method of moment (GMM) model to address any possible endogeneity concerns.

Econometric Models

Following Powell (2022), we examine the possible impact of multi-layered gender diversity criteria on sustainability performance using a PQR model. Unlike the conventional least squares regression models, which estimate the conditional mean of targets across different values of variables, a PQR model computes the target’s conditional median (Baum 2013). By doing this, we intend to offer a more comprehensive understanding of the gender diversity-ESG nexuses than previous work that was limited to traditional least squares models, such as fixed-effects and OLS regressions, for two reasons (Fernandes, Bornia, and Nakamura 2018; Giannarakis, Andronikidis, and Sariannidis 2020; Jizi 2017; Tauringana and Chithambo 2015; Wang 2017). Firstly, a PQR model is relatively more robust to outliers than other least-squares methods. Secondly, a PQR model is semiparametric, avoiding assumptions related to the parametric distribution of the error process (Baum 2013; Cobb-Clark, Kassenboehmer, and Sinning 2016; Powell 2022).

Thus, the specification of the main model is as follows.

Where ESG is the total environmental, social and governance score as a proxy for sustainability performance, BGD is board gender diversity, WOM is women in top management positions, and WOSCMTE is the percentage of women on sustainability committees. SCMTE is sustainability committee size, TBQ is Tobin’s Q as a measure for firm market value, DOA is debt to assets ratio as a proxy for leverage, MKTCAP is the logarithm of market capitalization as a proxy for firm size, Big4 is auditor type, INDUS is the sub-H&T industry, MASC is masculinity, UAVOID is uncertainty avoidance, LTORIEN is long term orientation, VA is voice and accountability, CC is control of corruption, GDP is the gross domestic product, IR is the inflation rate, CSR_REQ is CSR requirements, and GD_REQ is gender diversity regulations.

Empirical Findings

Univariate Analysis

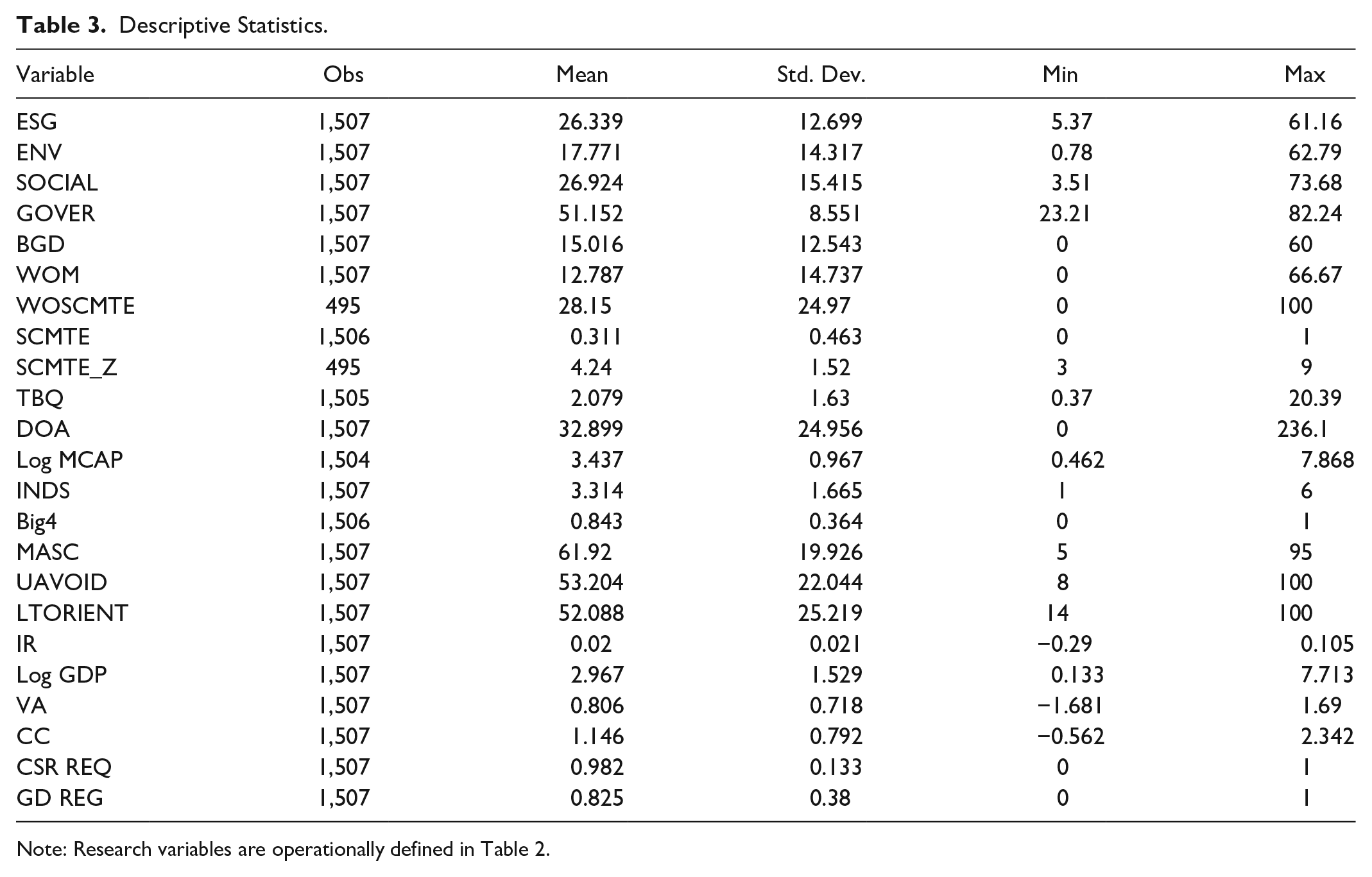

Table 3 presents a summary of the descriptive statistics of the study variables. Remarkably, it shows that the mean value of ESG is 26.34%, with a standard deviation of 12.7% that varies from a minimum value of 5.37% and a maximum value of 61.16%. Using fewer H&T firms across fewer countries, Koseoglu et al. (2021) and Uyar et al. (2020) report a mean value of ESG scores of 49.74% and 49.66%, respectively. When it comes to the environmental category (ENV), Table 3 shows that the mean value of ENV is 17.11%, with a standard deviation of 14.31%, ranging from 3.51% minimum value and 73.86% maximum value. This, however, is much lower than the mean value of the ENV score (50.71%) that has been reported by Uyar et al. (2020) for a smaller international sample of H&T firms. Specifically, Uyar et al. (2020) was confined to a smaller sample (920 firm-year observations) and shorter period of time (from 2011 to 2018) compared with 1,507 firm-year observations in our study that also covers a longer period from 2010 to 2020.

Descriptive Statistics.

Note: Research variables are operationally defined in Table 2.

Regarding the social score, Table 3 reports a mean value of 26.92% with a 15.42% standard deviation, ranging between a minimum value of 5.51% and a maximum value of 73.68%. Again, this is lower than what has been reported by prior studies of a similar nature (Ionescu et al. 2019; Koseoglu et al. 2021; Uyar et al. 2020). For example, Ionescu et al. (2019) indicated a mean value of 41.29% for the social pillar of ESG of H&T firms worldwide. However, it was limited to 434 firm-year observations from 2010 to 2015 only. Also, Ionescu et al. (2019) has adopted a different methodology to measure ESG scores, namely the RobecoSAM database. In relation to the governance dimension of ESG performance, our results report a mean value of 51.15% with a standard deviation of 8.55%, which ranges from a minimum value of 23.21% and a maximum value of 82.24%. This result is in line with those of prior studies (e.g., 46.29% in Uyar et al. (2020) and 47.84% in Ionescu et al. (2019). This implies that the different ESG methodologies have consistently measured the governance score, tracking issues related to board structures, its functionality, ownership structure, a firm’s participation in policy development, and executive compensation.

For gender diversity proxies, Table 3 shows that the mean value of the board gender diversity (BGD) variable is 15.02%. This means that women represent about 15% of directors on the boards of the sampled H&T firms. This is consistent with Koseoglu et al. (2021), that reported a mean value of 16.63% for board gender diversity among a sample of H&T firms internationally. Also, Table 3 presents a mean value of 12.8% for female executives among the sampled firms. This indicates an increasing trend in appointing women in senior management roles compared with Lim and Chung (2021), which reported only a 3% mean value of female managers among a sample of US firms from 1999 to 2013. With respect to women on CSR/sustainability committees (WOSCMTE), Table 3 shows a mean value of 28.15% with a standard deviation of 24.97%, ranging from 0% to 100%. This means that women’s representation on CSR/sustainability committees is greater than their representation on boards and senior management teams. This result is tied to the gender socialization perspective that suggests that female directors tend to demonstrate greater responsibility and sensitivity toward stakeholders’ concerns and engage with sustainability strategies to make a positive contribution to the environment and society (Ben-Amar, Chang, and McIlkenny 2017; Haque and Jones 2020; Liao, Luo, and Tang 2015). In this study, we add to the ongoing debate on the role of gender diversity in enhancing sustainability practices of firms by manually collecting data about the WOSCMTE variable to examine its impact on ESG score as a proxy for sustainability performance for the first time in the literature to the best of our knowledge. This means no single study has included women’s representation on CSR/sustainability committees in a multi-dimensional measurement of the influence of gender diversity in the workplace on sustainability performance.

Also, Table 3 shows the descriptive statistics of firm-level control variables, indicating that the mean value of establishing a CSR/sustainability committee (SCMTE) is 0.311 ± 0.46, the CSR/sustainability committee size is 4.24 ± 1.52, Tobin’s Q (TBQ) is 2.079 ± 1.63, the leverage as measured by the debt to assets (DOA) ratio is 32.899 ± 24.956, the logarithm of market capitalization (Log MCAP) is 3.437 ± 0.967, the sub- H&T industry type (INDUS) is 3.314 ± 1.665, the auditor type (Big4) is 0.843 ± 0.364. For the country-level control variables, Table 3 also presents that the average masculinity (MASC) is 61.92 ± 19.926, the uncertainty avoidance (UAVOID) is 53.204 ± 22.044, the long-term orientation (LTORIENT) is 52.088 ± 25.219, the inflation rate (IR) is 0.02 ± 0.021, the logarithm of gross domestic product (GDP) is 2.967 ± 1.529, the voice and accountability (VA) are 0.806 ± 0.718, the control of corruption (CC) is 1.146 ± 0.792, the CSR requirements (CSR REQ) is 0.982 ± 0.133, the gender diversity regulations (GD REG) is 0.825 ± 0.38. It is worth mentioning that the mean values of CSR_REQ and GD_REG (i.e., 0.982 and 0.825, respectively) imply that the vast majority of our sampled countries have already enacted CSR and gender diversity regulations. Additionally, about 31% of the sampled firms have already established CSR/sustainability-related committees. This gives us the potential to examine the influence of women’s representation in sustainability committees on sustainability performance among a sample of H&T firms worldwide.

Bivariate Analysis

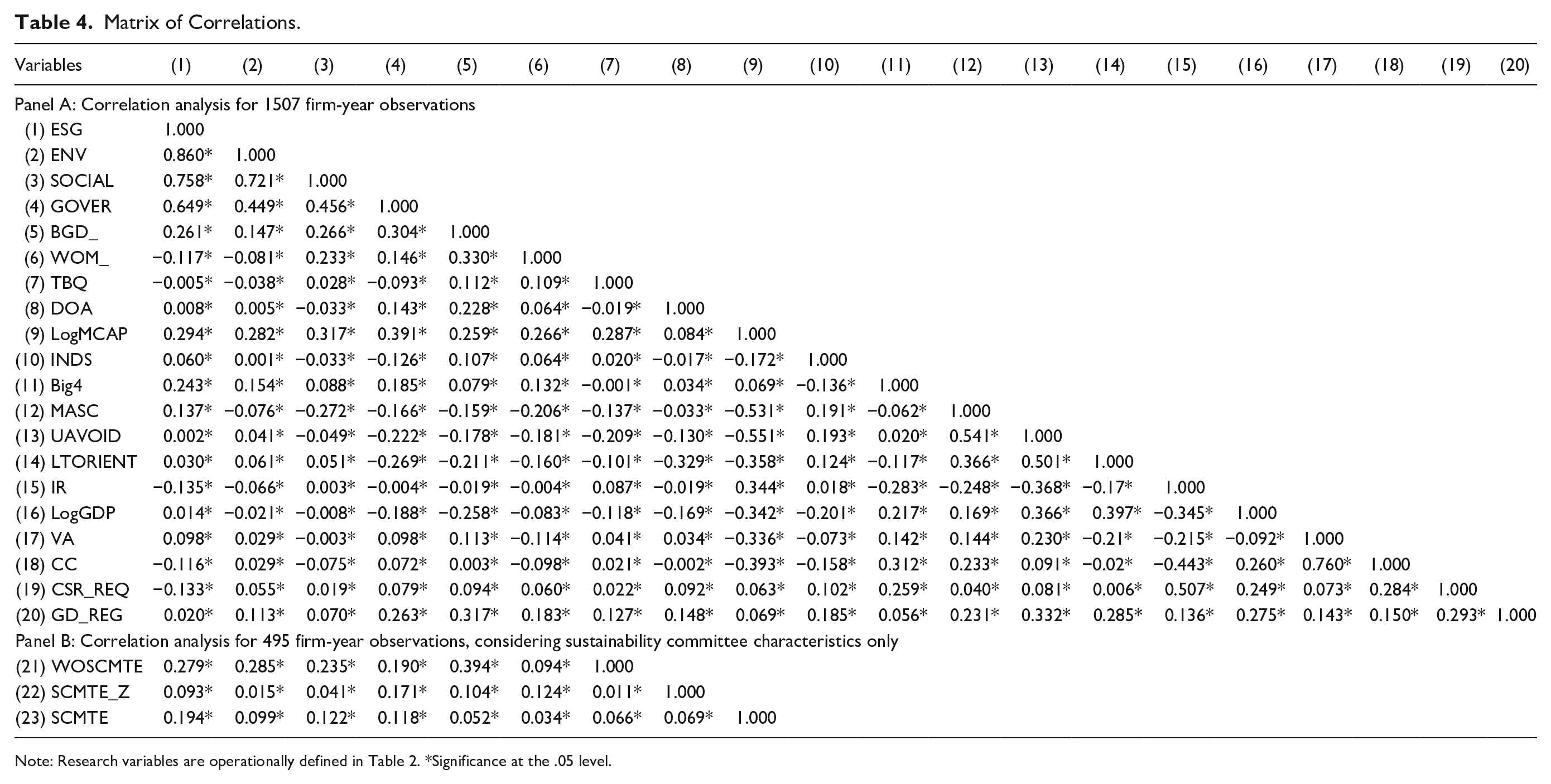

Table 4 shows the correlations matrix for the main variables of the study. It reports the Pearson correlation coefficients for the entire sample (1507 firm-year observations) in Panel A and for the sub-sample (495 firm-year observations) in Panel B. The nature of coefficients designates that any residual non-normality in the distribution of variables appeared to be mild and is in line with those presented by prior studies (e.g., Haque and Jones 2020; Koseoglu et al. 2021; Uyar et al. 2020). According to the correlation analysis findings, ESG, ENV, SOCIAL, and GOVER variables have significant and positive associations with board gender diversity, supporting H1 and its sub-hypotheses (i.e., H1-a, H1-b, and H1-c). In contrast, Panel A of Table 4 shows that sustainability proxies (i.e., ESG, ENV, and GOVER) are negatively attributed to female executives, whereas the social pillar of sustainability performance (SOCIAL) is positively related to women in senior management roles. This statistically challenges H2 and its sub-hypotheses H2-a and H2-c, although it gives empirical credibility to H2-b. Considering CSR/sustainability committee characteristics for only 495 firm-year observations, Panel B of Table 4 shows that ESG performance and its sub-dimensions are positively and significantly linked to women on sustainability committees (WOSCMTE) variable, which supports H3 and its sub-hypotheses. Besides, the positive and significant correlation coefficients reveal that the existence of a CSR/sustainability committee (SCMTE) and its size (SCMTE_Z), mandatory CSR requirements and gender diversity regulations are positively attributable to sustainability performance proxies. Additionally, the other firm-level and country-level controls are heterogeneously associated with sustainability proxies.

Matrix of Correlations.

Note: Research variables are operationally defined in Table 2. *Significance at the .05 level.

Panel Quantile Regression Analysis

Women on boards and sustainability performance

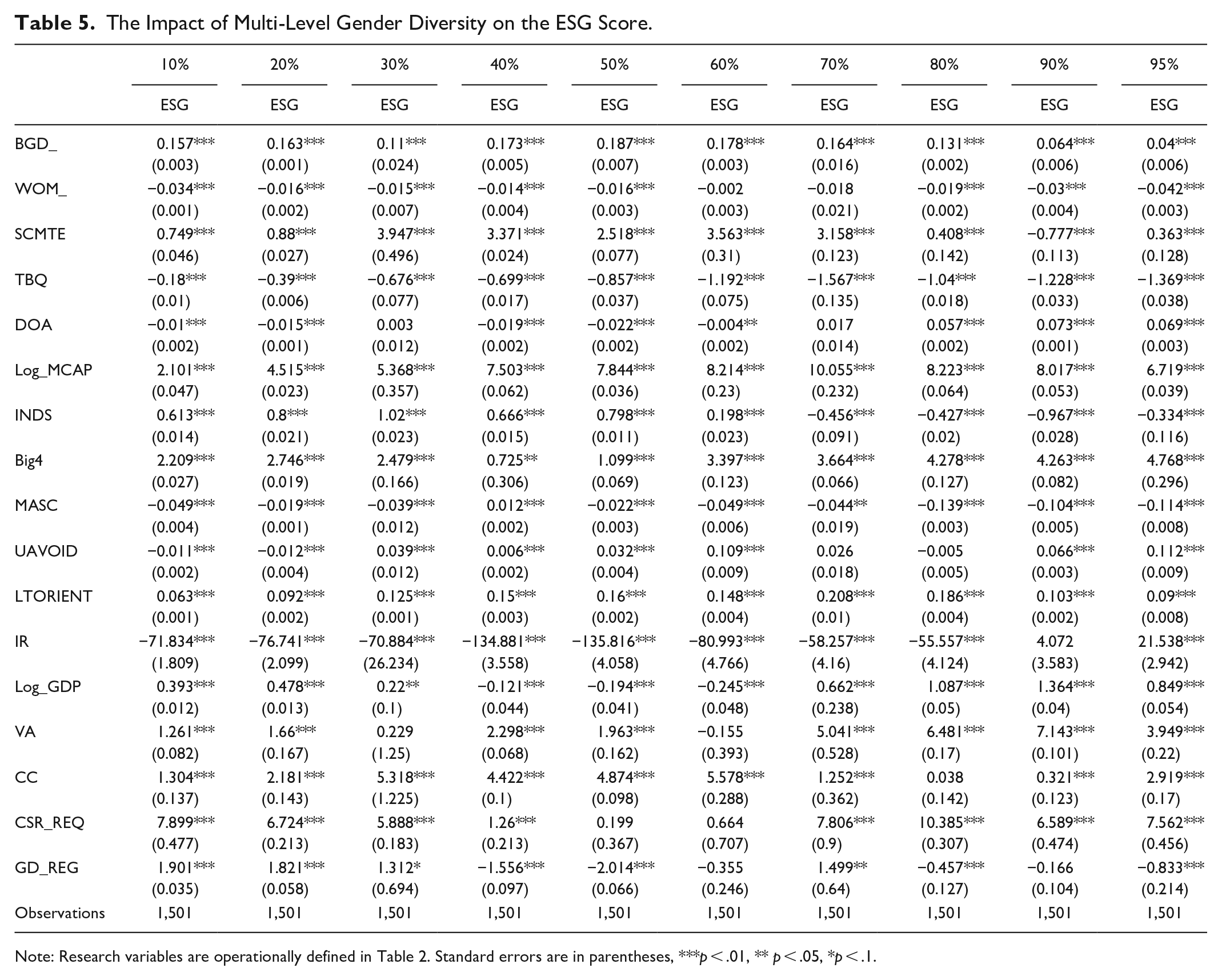

To achieve the first objective of this study, and consistent with Powell (2022), we innovatively apply a PQR model to examine the potential influence of multi-dimensional measures of gender diversity, mainly female directors, female executives and female members of sustainability committees, on sustainability performance as proxied by ESG scores and its main pillars among a sample of H&T firms worldwide. Overall, the 10 quantiles of Table 5 indicate that BGD has a significant and positive impact on H&T firms’ decision to engage in sustainability (ESG) performance at a 1% level of significance. This implies that H1 has been supported. Recall that women account only for 15.02% of directors (See Table 3); thus, the boards are skewed male in our sample. This point poses the question: Do female directors play a symbolic role on boards in the H&T sector? Previous literature suggests that female representation on boards appears to have a negligible impact unless a critical mass of at least 30% of women directors exists on a firm’s board (Liao, Luo, and Tang 2015; Post, Rahman, and Rubow 2011; Torchia, Calabrò, and Huse 2011). However, our evidence suggests that the small representation of female directors on the boards of H&T firms seemed to make a change in relation to sustainability engagements. This finding is consistent with those of previous studies of a similar nature that support the role of female directors in strengthening their firms’ sustainability decisions (e.g., Ben-Amar, Chang, and McIlkenny 2017; Chijoke-Mgbame, Boateng, and Mgbame 2020; Glass, Cook, and Ingersoll 2016; Haque and Jones 2020; Liao, Luo, and Tang 2015; Tingbani et al. 2020).

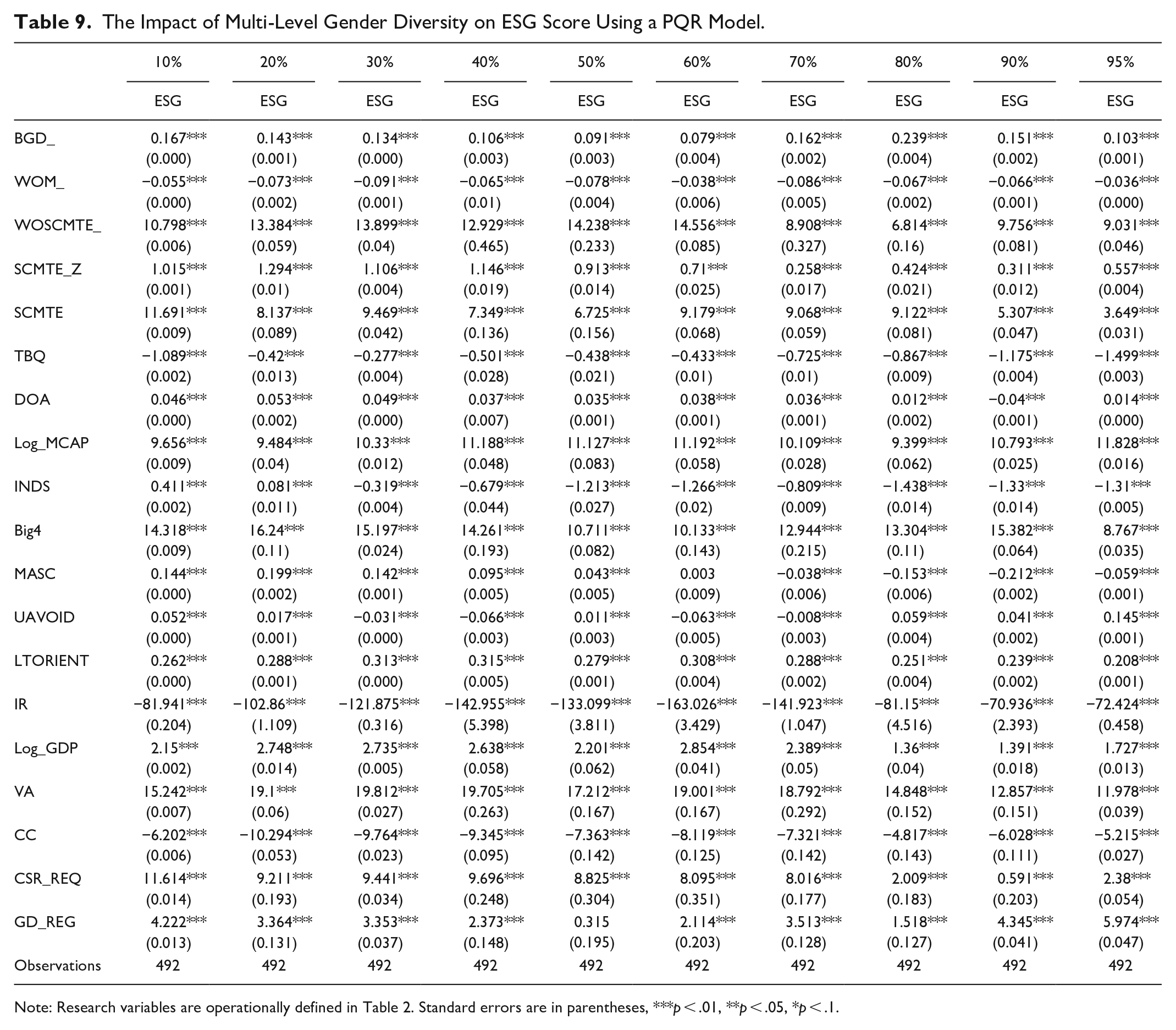

The Impact of Multi-Level Gender Diversity on the ESG Score.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, ** p < .05, *p < .1.

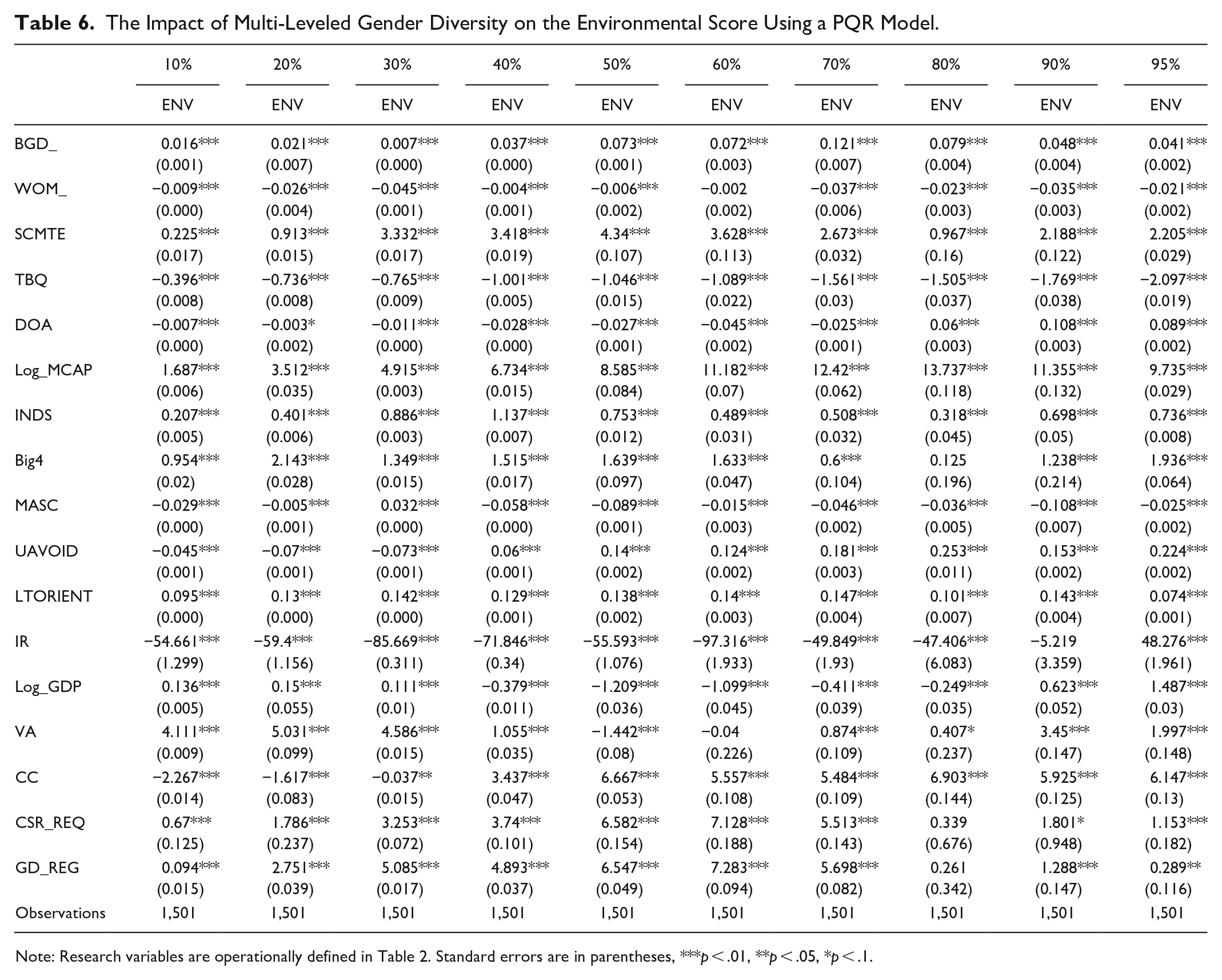

To examine the impact of board gender diversity on the main pillars of ESG score as proxies for pro-sustainable corporate performance, we run PQR models to examine the possible influence of BGD on ENV, SOCIAL, and GOVERN dimensions. Table 6 shows that BGD is positively and significantly associated with environmental performance (ENV) of H&T firms globally at a 1% level across all the quantiles. This supports H1-a statistically. This is also consistent with the results of prior studies (e.g., Atif et al. 2021; Chijoke-Mgbame, Boateng, and Mgbame 2020; Cordeiro, Profumo, and Tutore 2020; Haque and Jones 2020; Lu and Herremans 2019; Pucheta-Martínez and Gallego-álvarez 2019; Tingbani et al. 2020). This means that women on boards of H&T firms have a tendency to push their firms toward more engagement in environmentally responsible behaviors (Hillman, Withers, and Collins 2009). Relatedly, Uyar et al. (2020) indicate that BGD is positively and significantly attributable to the ENV pillar of ESG score among a smaller sample of H&T firms over a shorter period compared with our empirical evidence. Theoretically, female directors tend to display a more communal, participative, and democratic leadership style (Akaah 1989; Chijoke-Mgbame, Boateng, and Mgbame 2020; Dawson 1997; Eagly, Johannesen-Schmidt, and van Engen 2003; Gilligan 1993; Rudman and Glick 2001; Tingbani et al. 2020), which may motivate them to demonstrate greater sensitivity toward stakeholders concerns and engage with sustainability strategies to make a positive contribution to the environment and society (Ben-Amar, Chang, and McIlkenny 2017; Glass, Cook, and Ingersoll 2016; Haque and Jones 2020; Liao, Luo, and Tang 2015; Mallin and Michelon 2011; Nielsen and Huse 2010).

The Impact of Multi-Leveled Gender Diversity on the Environmental Score Using a PQR Model.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

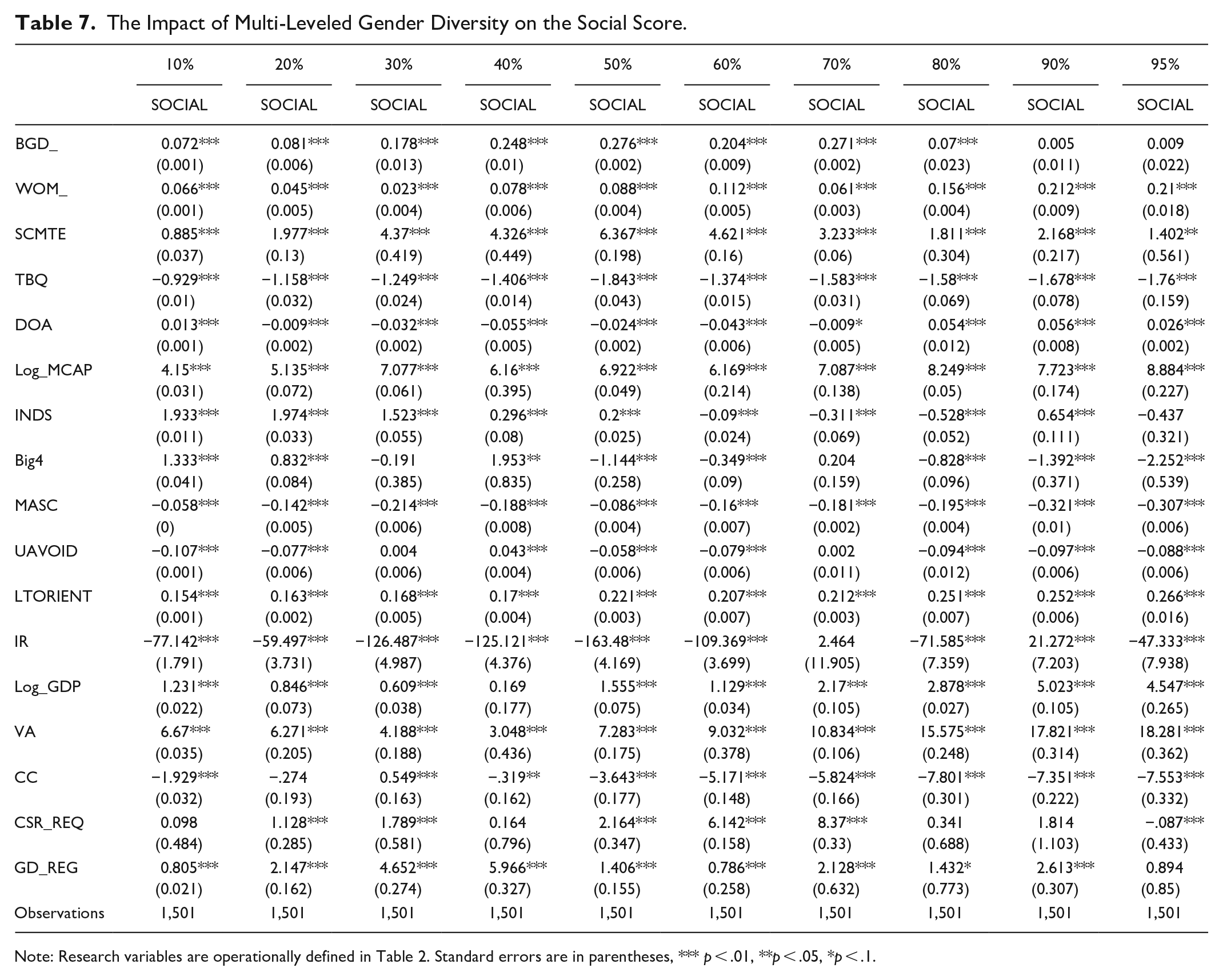

Likewise, Table 7 shows that quantiles 10%–80% support a positive and significant relationship between BGD and SOCIAL at a 1% significance level. This means that H1-b has been empirically approved. Based on this, we argue that due to their characteristics, including being nurturing, helpful and sympathetic in their organizational decision-making approach (Eagly, Johannesen-Schmidt, and van Engen 2003), women directors are more likely to be stakeholder-oriented and sympathetic to socially responsible initiatives (Amorelli and García-Sánchez 2021; Atif et al. 2021).

The Impact of Multi-Leveled Gender Diversity on the Social Score.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, *** p < .01, **p < .05, *p < .1.

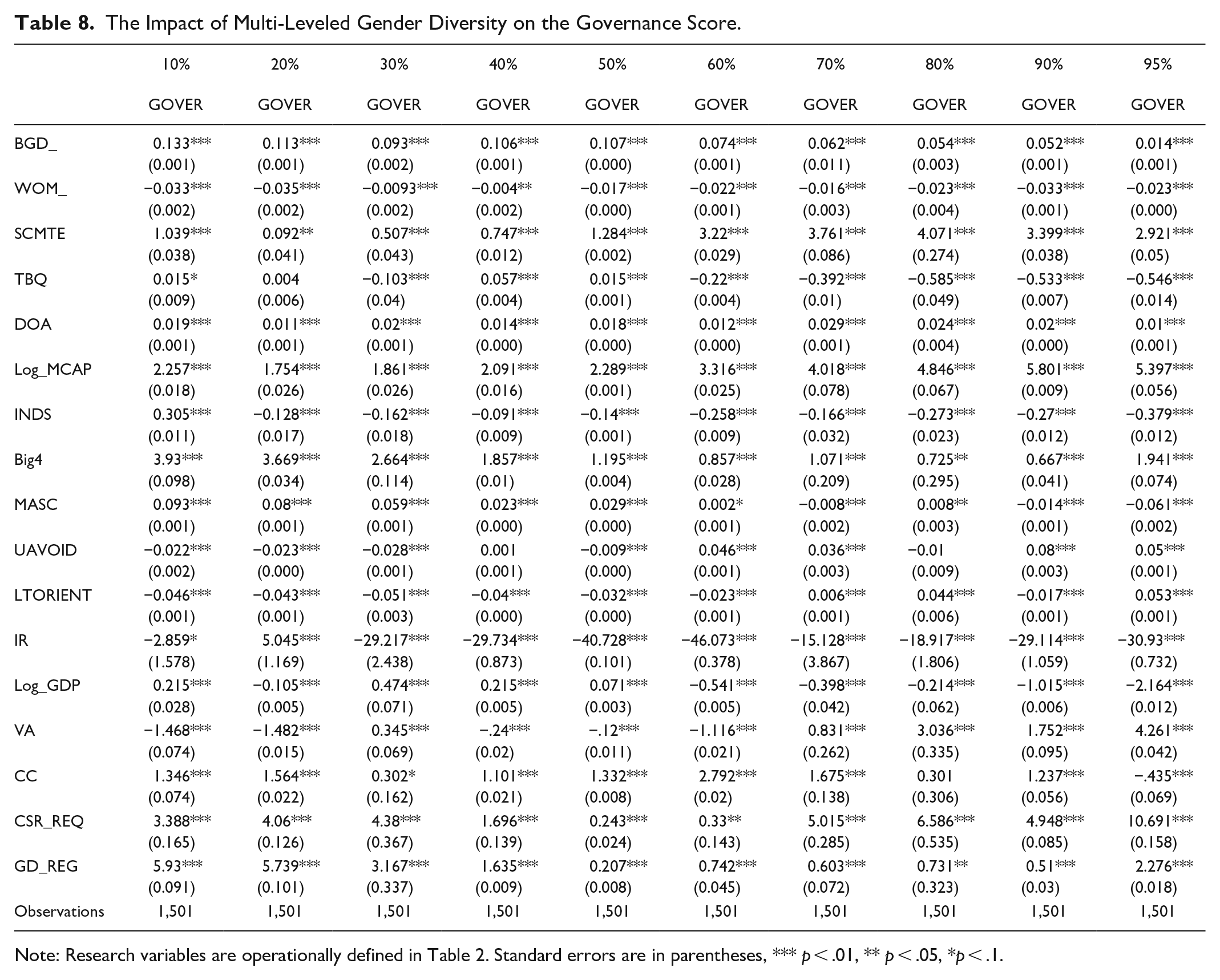

With respect to CG, Table 8 shows that all quantiles (10%–95%) support a positive association between BGD and the governance pillar (GOVER) at a 1% level of significance. This means that H1-c has been statistically accepted. This result is aligned with prior studies that argue that female directors tend to improve CG practices by enhancing high-quality board decisions and effectiveness (e.g., Bear, Rahman, and Post 2010; Coffey and Wang 1998; Nielsen and Huse 2010). Also, our empirical evidence gives more credibility to Uyar et al. (2020) that indicates a positive and significant relationship between BGD and the governance score among a smaller sample of H&T firms.

The Impact of Multi-Leveled Gender Diversity on the Governance Score.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, *** p < .01, ** p < .05, *p < .1.

In brief, we argue that with female characteristics, such as cooperation, risk-averseness, and high standards of ethical judgment, diverse boards tend to display a more communal, participative, and democratic leadership style (Chijoke-Mgbame, Boateng, and Mgbame 2020; Tingbani et al. 2020), which is, in turn, positively linked to the sustainability performance of H&T firms worldwide (Uyar et al. 2020).

Female executives and sustainability performance

In our attempt to examine the association between multi-layered gender diversity criteria and sustainability performance, we use a PQR model to examine the link between female executives and ESG scores among a sample of H&T firms worldwide, achieving the second objective of this study. Table 5 shows that quantiles 10%–50% and 80%–95% indicate that female managers are negatively attributable to the total ESG performance at a 1% significance level. This means that H2 has been statistically rejected. This finding is consistent with a shred of previous literature (e.g., Chijoke-Mgbame, Boateng, and Mgbame 2020; Cullinan, Mahoney, and Roush 2019; Furlotti et al. 2019; Glass, Cook, and Ingersoll 2016) that indicated no evidence of variations in ethical attitudes toward ESG-related issues between male and female managers from a managerial decision-making perspective. Therefore, we argue that as the position of managers is usually associated with males, the job self-schema prevails over the gender self-schema, suggesting a negative association between female directors and ESG engagements. This implies that female managers might be perceived as profit-driven instead of stakeholder-focused managers (Chijoke-Mgbame, Boateng, and Mgbame 2020).

Similarly, Tables 6 and 8 indicate that women in senior management positions are associated with fewer engagements in environmental (ENV) and governance (GOVER) categories of ESG scores, rejecting both H2-a and H2-c empirically. Nevertheless, Table 7 suggests that female managers are more engaged in socially responsible activities (SOCIAL). This result supports H2-b statistically. Drawing on Adams and Funk (2012), we argue that while the gender gap could decrease for those who have entered the upper echelons of a firm owing to workplace socialization, the essential difference is remained because of the general trait differences between genders. Theoretically speaking, the upper echelon and gender socialization indicate that female executives with a stakeholder-oriented leadership approach are expected to play a significant role in adopting and improving firms’ social performance, focusing on satisfying the requirements of diverse stakeholders (Dyllick and Hockerts 2002).

Sustainability committees’ gender diversity and sustainability performance

To achieve the third objective, we examine the impact of gender diversity within the sustainability committee (WOSCMTE) on ESG proxies. Crucially, only 31% of the sampled H&T firms had already established a CSR/sustainability-related committee. Therefore, we have limited our focus to a smaller sample of 495-firm year observations. By doing this, we extend the ongoing debate about the association of gender diversity aspects with sustainability performance by innovatively considering the impact of WOSCMTE on ESG proxies for the first time in the literature to our best knowledge.

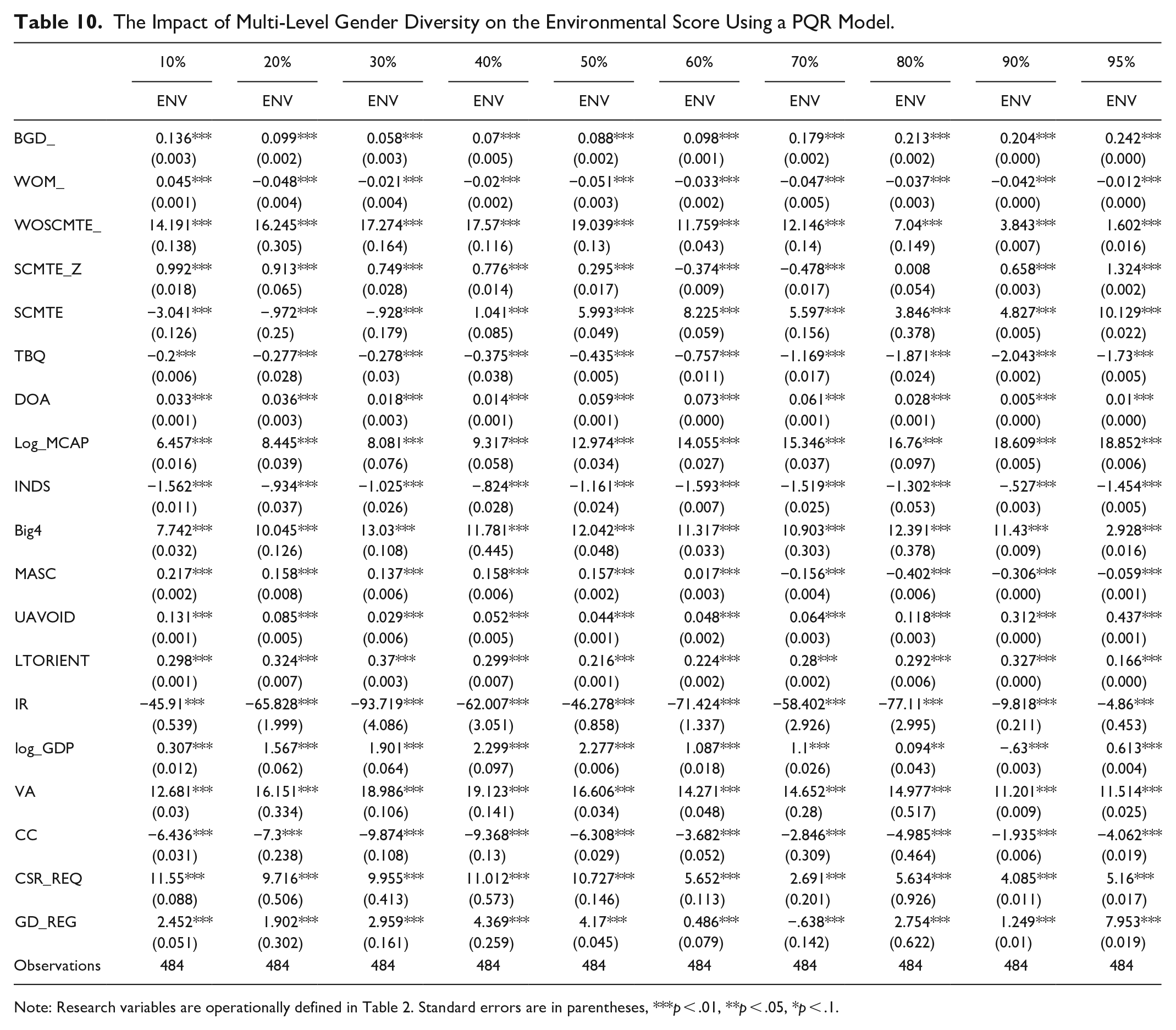

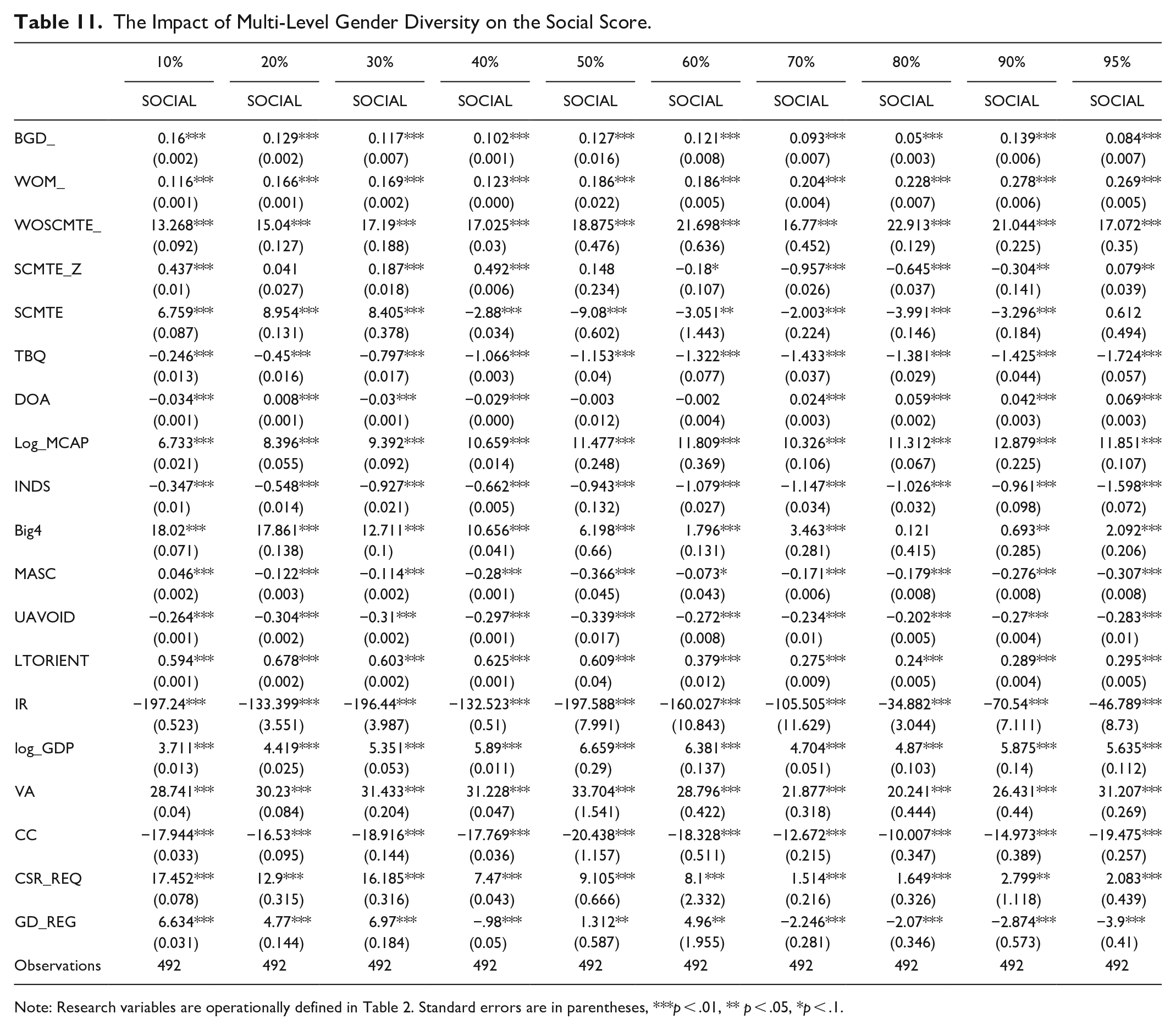

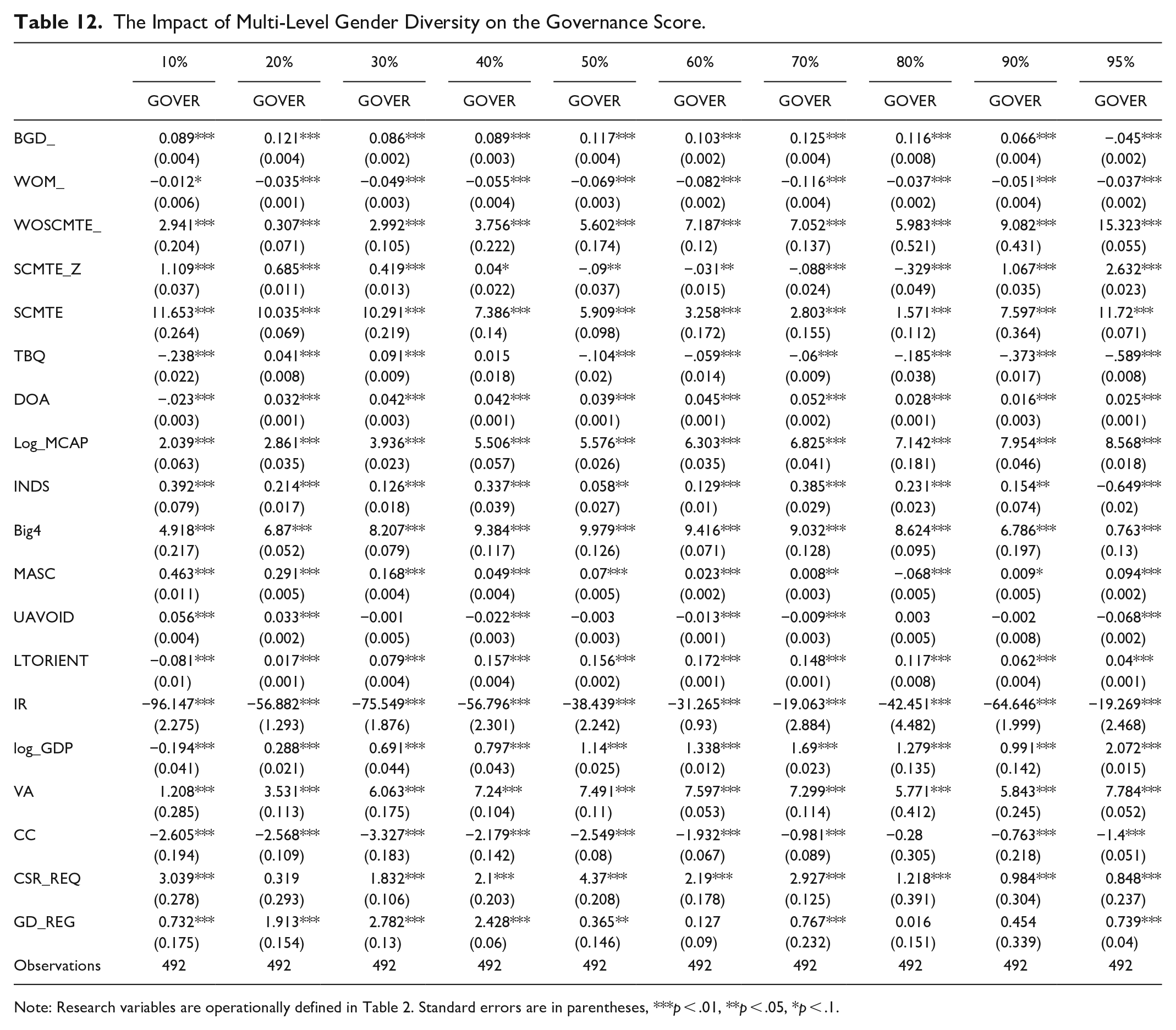

Table 9 indicates that female members of sustainability committees are positively related to the total ESG score at all quantiles at a 1% significance level. This gives empirical credibility to H3. Similarly, Tables 10 to 12 show that women on sustainability committees of H&T firms tend to enhance their firms’ engagement in each individual ESG practice, including environmental (ENV), social (SOCIAL), and good CG (GOVER) practices at a 1% level of significance at all quantiles. This implies that H3-a, H3-b, and H3-c have been statistically approved. Crucially, we argue that as sustainability committees are established for a specific purpose, female members appointed to these committees should have the necessary expertise and be actively involved in carrying out the committee’s mandate. Therefore, our empirical evidence gives further credibility to this theoretical argument and suggests that female members of sustainability committees, with endearing qualities and abilities, should be more interested in supporting their firms’ involvement in pro-sustainable practices and positively influence the firm’s ESG issues rather than for the sake of its image.

The Impact of Multi-Level Gender Diversity on ESG Score Using a PQR Model.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

The Impact of Multi-Level Gender Diversity on the Environmental Score Using a PQR Model.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

The Impact of Multi-Level Gender Diversity on the Social Score.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, ** p < .05, *p < .1.

The Impact of Multi-Level Gender Diversity on the Governance Score.

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

Endogeneity Checks

In line with Blundell and Bond (1998), we use a two-step dynamic GMM model as an endogeneity check to ensure that our main findings are not relentlessly affected by the potential incidence of endogeneity problems. The application of the GMM process in this paper is as follows. First, we use both the Wu–Hausman test and the Durbin test to identify the possible occurrence of individual regressors’ endogeneity issues. Hypothetically, the independent variables (i.e., BGD, WOM, and WOSCMTE) should not be associated with the residuals. In this regard, the Wu–Hausman test and the Durbin test decide whether these residuals are linked with the proxies of the independent variables or not (Ullah, Akhtar, and Zaefarian 2018). The outcomes of running these tests suggest that the BGD, WOM, and WOSCMTE are endogenously, and not exogenously, associated with sustainability performance proxies (i.e., total ESG, ENV, SOCIAL, GOVER). This implies that our main findings shown in Tables 5 to 12 might be biased. Thus, this paper uses a two-step dynamic GMM regression model to address the probable existence of the endogeneity problem.

Consistent with previous sustainability studies (e.g., Moumen, Ben Othman, and Hussainey 2015; Ullah, Akhtar, and Zaefarian 2018, among others), we use a two-step dynamic GMM regression model to tackle the possibility of endogeneity issues that might occur from both omitted variables and reverse causality association between gender diversity measures and sustainability performance proxies. Fundamentally, we incorporate the lagged values of ESG proxies into the GMM system. Therefore, the two-step GMM models can be specified in the following equations as follows:

Definitions of this research’s variables are detailed in Table 2. In equation (2), for example, ESGit-1 embodies the one-year lag of the total score of ESG (last year’s ESG), and ESGit-2 refers to the second lagged value of ESG, representing ESG two years earlier. The same process is implemented on ESG pillars (i.e., ENV, SOCIAL, GOVER) in questions 3, 4, and 5. The lags of ESG and its dimensions are considered explanatory variables in the two-stage GMM system. According to Roodman (2009), incorporating these lagged values of the dependent variables is believed to address the expected endogeneity issue by internally transforming the data where a variable’s value of the previous year is subtracted from its present value. Wooldridge (2016) consistently indicates that internal transformation in the two-stage GMM system can improve its function statistically.

Furthermore, we use a set of post-estimation tests, such as the Arellano-Bond test and the Hansen test, to evaluate the validity and reliability of the two-staged dynamic GMM estimator and whether the instruments (i.e., lags of ESG and its pillars in equations (2)–(5)) are appropriately specified. A fundamental hypothesis of the validity of the two-stage GMM method is that the used instruments should be exogenous (Ullah, Akhtar, and Zaefarian 2018). The findings of the pre-estimation and post-estimation tests seemed to be non-significant, indicating that our instruments are exogenous; thus, they are valid. This means that a two-stage GMM model is an appropriate method to check and overcome the possible presence of endogeneity concerns.

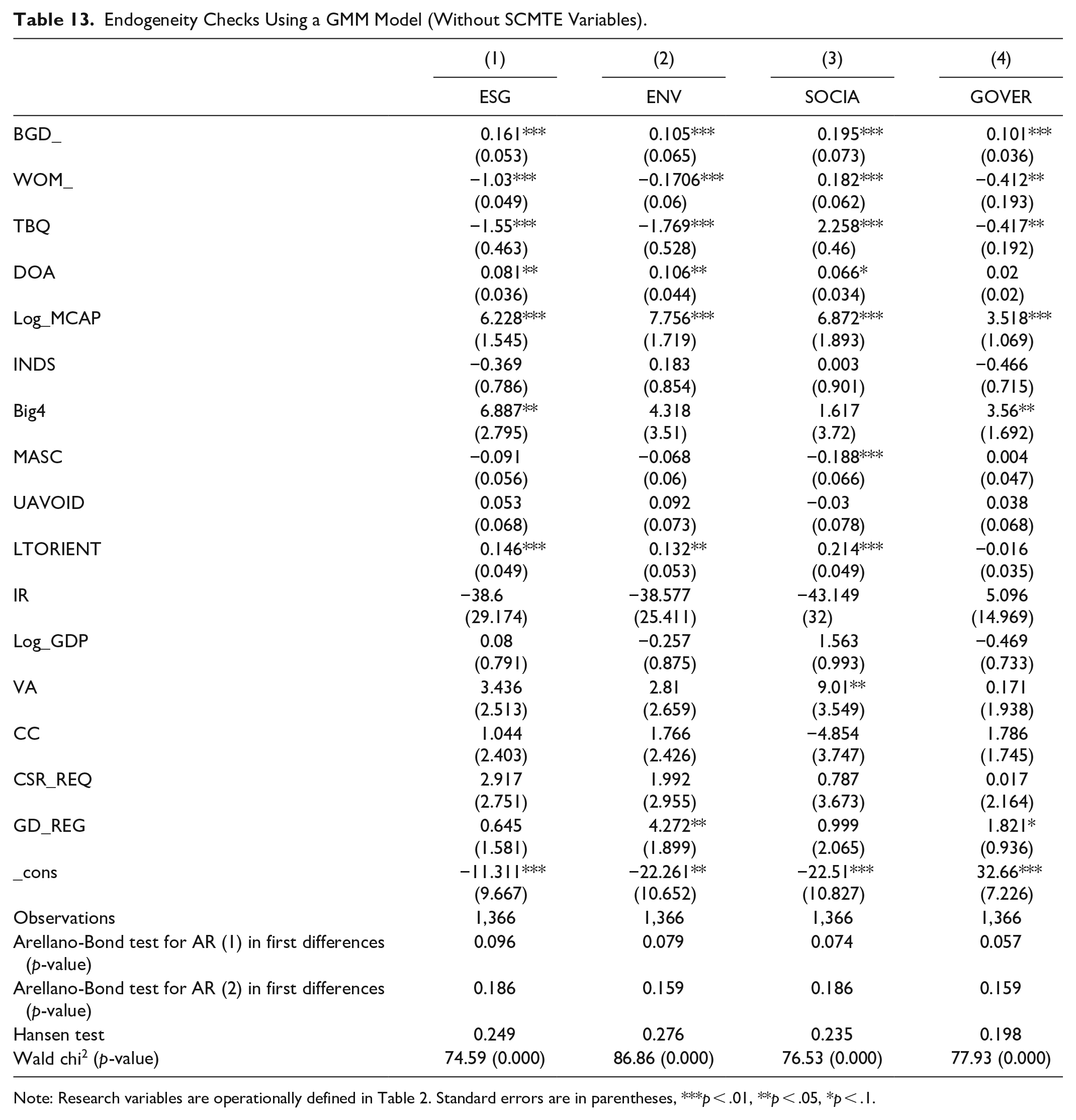

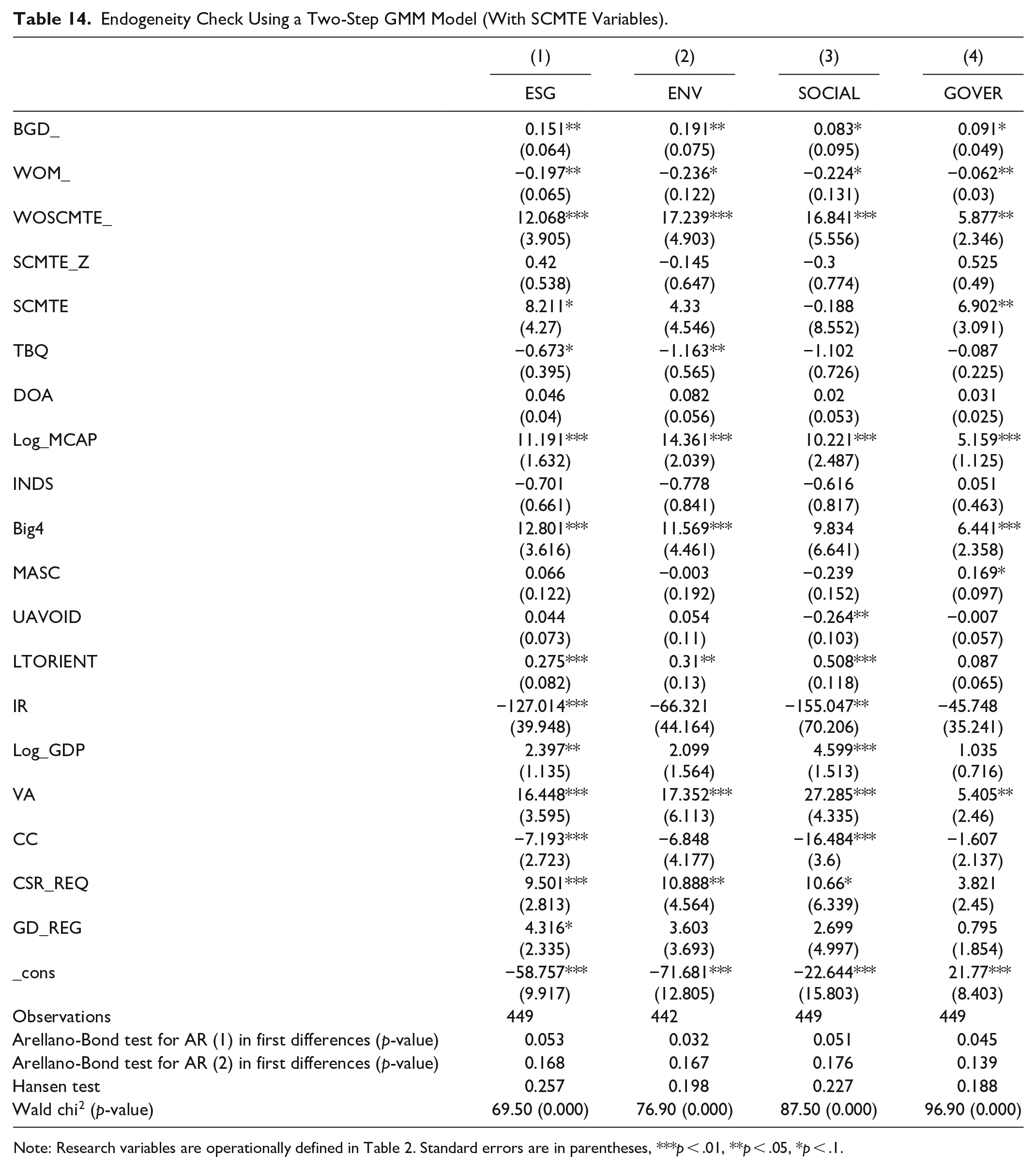

Models 1–4 of Tables 13 and 14 show the findings of conducting the two-step GMM models. Crucially, the results indicate that female directors (BGD) and women members of CSR/sustainability committees (WOSCMTE) significantly and positively influence ESG and its pillar, including environmental performance (ENV), social performance (SOCIAL), and CG (GOVER). In contrast, female executive (WOM) is negatively associated with ESG, ENV, and GOVER, whereas it is positively attributable to SOCIAL. To the extent that the main findings of the endogeneity checks are statistically comparable to those of the basic models (i.e., the PQR model of Powell (2022)), we are relatively confident that these results are robust and not sensitive to the potential existence of endogeneity problems. This implies that the existence of endogeneity matters does not severely affect our main results.

Endogeneity Checks Using a GMM Model (Without SCMTE Variables).

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

Endogeneity Check Using a Two-Step GMM Model (With SCMTE Variables).

Note: Research variables are operationally defined in Table 2. Standard errors are in parentheses, ***p < .01, **p < .05, *p < .1.

Conclusion

The involvement of women in the H&T sector has been found to result in more sustainable socio-economic and environmental developments. However, what is less known, is whether the presence of gender diversity within multiple corporate-level management committees (e.g., board of directors, top management, sustainability committee) will result in the adoption and implementation of corporate sustainability strategies, ultimately leading to pro-sustainable performance outcomes of corporations operating within the global H&T sector.

Our paper, therefore, addresses this extent shortage in the current literature by investigating “how” and “why” a multi-layered gender diversity structure (e.g., female directors, female senior managers and female members of sustainability committees) could influence corporate decisions to engage in corporate sustainability activities in the global H&T sector.

Using Powell’s (2022) PQR, our empirical evidence supports the positive association between boards’ female directors and the sustainability performance of H&T firms worldwide as measured by the total ESG score. In contrast, female executives were negatively attributable to the total ESG engagement (see Table 5). Similarly, in line with Table 5, the noted influence of female directors (positive) and female executives (negative) are consistent across all ESG dimensions, including the environmental score (see Table 6) and the governance score (see Table 8) except for the social score where a positive nexus exists between female executives and social engagement of H&T firms (see Table 7). As an additional analysis, and focusing on a smaller sample of 495 firm-year observations, our PQR findings indicate that women members on sustainability committees of H&T firms are attributed to enhanced sustainability performance as proxied by total ESG score (see Table 9), the environmental score (see Table 10), the social score (see Table 11), and the governance score (see Table 12). Our GMM analysis shows that the PQR’s findings are robust to endogeneity problems (see Tables 13 and 14)